Embed Size (px)

Citation preview

1

Paying For College

Brad Barnett, MS, AFC®, CPFMAccredited Financial Counselor

Certified Personal Financial ManagerSenior Associate Director

James Madison University Office of Financial Aid & Scholarships

2

Consult with Appropriate Stakeholders

Talk to Those Involved in This Decision

• If parents are assisting students with paying for

college it is important students take the time to sit and discuss details with them

• Financial aid is a long-term processHow much debt are students willing to accumulate How much debt can parents afford

3

Learn More About Schools

• Understand the costs of schools• Examine the types of schools• Learn about individual deadlines of schools• Try not to let cost be a large deterrent initially

MANY colleges are willing to work with students If during the process you find a college is too

expensive, then be realistic about what you can afford

4

Options• Personal savings• Investments (e.g., 529 plans, ESA’s, Mutual

Funds, etc.)• Payment plans • Part-time employment• Grants (federal and state)• Scholarships (institutional and private)• Federal Loans (student and parent)• Home Equity (risky!)• Private Loans (student and parent)

Caution!Loan Repayment Example

• Dependent student beginning in 2014-15 and eligible for maximum Direct Loans for 4 years (assume student accepts the loans):– 1st year - $5,500 - no more than $3,500 subsidized (4.66%)*– 2nd year - $6,500 - no more than $4,500 subsidized (4.66%)*– 3rd year - $7,500 - no more than $5,500 subsidized (4.66%)*– 4th year - $7,500 - no more than $5,500 subsidized (4.66%)*– Total debt - $27,000 (aggregate maximum $31,000, no more than $23,000 subsidized)

• Standard Repayment Plan is 10 year– $282/month in loan payments– $33,829 repaid over the 10 year period– $6,829 paid in interest– This does not include any capitalized interest, which will increase the cost– Note: This is based on the 2014-15 rate of 4.66% (rates will differ each

year)

5

Debt Consequences

• Lost Opportunity Cost:– Loan payments will total $33,829 in 10 years, and

$6,829 of this is interest!– $282/month invested with an average rate of return of

8% over 10 years is $51,591– $282/month stuffed under your mattress for 10 years

is $33,840

• What could you do now to minimize your need for loans with the goal of freeing up your income in the future?

6

7

Budget!

• Often overlooked…its not always about making more money

• If you begin using a zero-based budget, you may find you are spending money on things you do not need now

• Can incorporate college savings into your budget

• Get control of your money!• Generally, will spend less if you budget

8

Zero-Based Budget

• Income minus expenses each month equals zero

• This means you have told every dollar of income you have to do something very specific

• If you stick with this for each category, you will not overspend and will likely avoid unnecessary debt and expenditures

9

Budget Busters

• According to the Department of Agriculture the average family of four spent between $X and $X per month on groceries – $893 and $1,064 (moderate plan)– $568 and $650 (thrifty plan)

• The average car payment in North America is $X– $460. The average cost of insuring a passenger vehicle

is$85.75 per month.– Total payment and insurance = $545.75– The median U.S. household income per month is $4,277– That makes the car/insurance payment 12.8% of income– The average length of a new car loan is 5.5 years!

Cost of Living Adjustments

• Sample adjustments:– Cell phone: If your plan costs $200/month, eliminate some options to

perhaps $100– Dining out: If you spend $200/month dining out, cut back to $50– Car payment: If you have a $400/month car payment, sell the car and

pay cash for something less expensive– Total savings recouped in this scenario is $650/month that can be used

towards college savings• This is merely one example and may not apply directly to you• Looking at where you spend money and reducing some of the

“wants” can help make college more affordable• Track your spending (every dollar) for one month…it might surprise

you

10

Opportunity Cost(food or ?)

• Average family of four:– $979 per month– $11,748 per year

• My family of four:– $320 per month– $3,840 per year

• Annually, we spend $7,908 less than the average family

• What else can we do with $8k besides “eat it”

11

Payment PlanJMU Example

• Average semester cost of full-time in-state tuition/fees and room/board at JMU in 2014-15 is about $9,305

• Payment Plans (generally 5 month option each semester)• $9,305 / 5 months = $1,861 / month• Are there items you can reduce in your budget or debt you can

eliminate before college to help “cash flow” some of this?– Car payments– Improve food budgets– Credit card or other consumer debt– Other sacrifices to make for next 4 years to avoid long term college

loan debt (Opportunity Cost of debt)– Community college to 4 year option

12

13

FAFSA

• Free Application for Federal Student Aid• Required to apply for federal financial aid• May be required to apply for state or

institutional financial aid• Required, at times, by private entities to

determine a student’s “need” level

14

Cost of Attendance• Tuition & fees• Room & board• Books, supplies, transportation, & miscellaneous

personal expenses, including documented costs for personal computer

• Loan fees• Study abroad costs• Dependent care expenses• Disability-related expenses

15

EFC = Expected Family Contribution

• The federal government determines a family’s ability to pay for post-secondary expenses (including living expenses)

• The figure schools use to determine a student’s eligibility for need-based aid

16

Definition of Need

Cost of attendance (COA)

– Expected family contribution (EFC)

= Financial need

Professional Judgment

• Unexpected issues not reflected on the FAFSA– Tuition expenses at an elementary or secondary school– Medical or dental expenses not covered by insurance– Unusually high child care costs– Job loss or unemployment– Parents enrolled at least half-time in a degree or certificate program– Roth IRA rollovers– Dependency overrides

• Contact the financial aid administrator to discuss if these items can be considered in a Professional Judgment review

• Issues such as credit card expenses, car payments, standard living expenses, and other “normal” daily items cannot be considered under Professional Judgment for federal and state aid purposes

17

18

Financial Aid SourcesFour primary sources of financial aid are:• Federal• State• Institutional• Private

19

Major Federal Programs

• Pell Grant• Supplemental Educational Opportunity Grant (SEOG)• Teach Grant• Federal Work Study (FWS)• Perkins Loan• Direct Loans (subsidized/unsubsidized)• Parent PLUS Loans

20

Federal Perkins Loan

• Eligible students Undergraduate and graduate students Priority to students who show “exceptional

need,” as defined by school

• Loan amount varies • Maximum annual loan

$5,500 - undergraduate students $8,000 - graduate & professional students

21

Federal Perkins Loan

• Interest rate: 5%

• 9-month grace period

• Repayment period may be up to 10 years

• Deferment & cancellation provisions available

22

Direct Loans• Federal Direct Student Loan (Direct Loan)

Program with funds provided directly by federal government via participating schools

• Subsidized and unsubsidized loans carry a fixed 4.66%* interest rate for 2014-15

• 6-month grace period• Repayment period is 10 years (more in some

cases)

*Note: Rates will differ each year

23

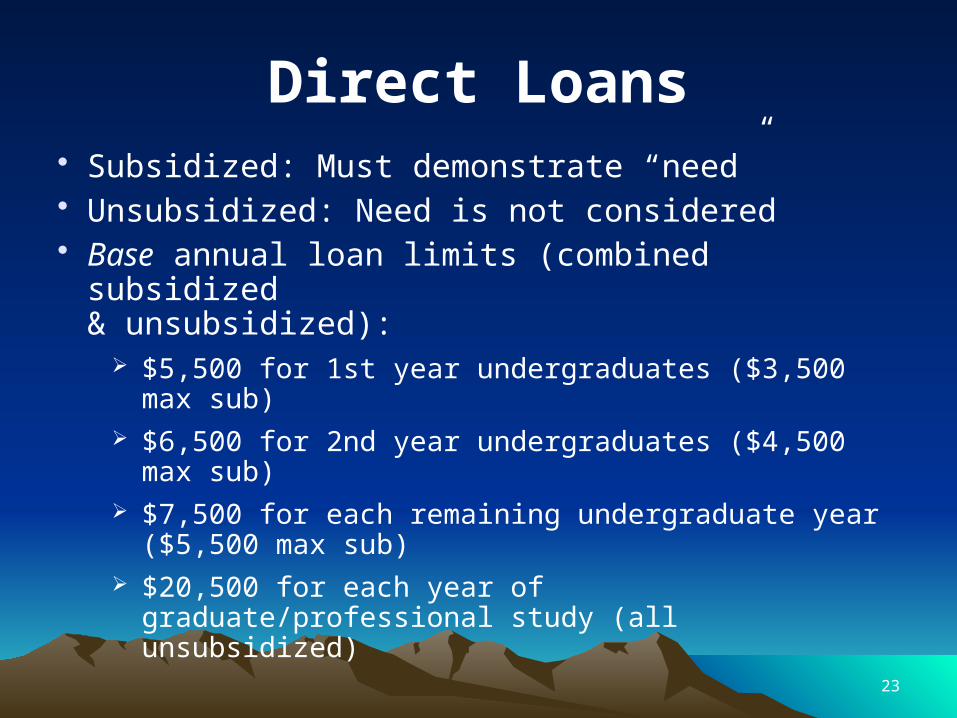

Direct Loans• Subsidized: Must demonstrate “need”• Unsubsidized: Need is not considered• Base annual loan limits (combined subsidized

& unsubsidized): $5,500 for 1st year undergraduates ($3,500 max sub) $6,500 for 2nd year undergraduates ($4,500 max sub) $7,500 for each remaining undergraduate year ($5,500 max

sub) $20,500 for each year of graduate/professional study (all

unsubsidized)

24

Parent PLUS

• Parent loan program for parents of dependent undergraduate students

• Annual loan limit: COA minus other aid• Fixed interest rate of 7.21%* in 2014-15

*Note: Rates will differ each year

25

Direct LoansAdditional unsubsidized loan eligibility for independent undergraduates, and dependent undergraduate students whose parents are unable to borrow Parent PLUS:

• $4,000 per year for first & second years of undergraduate study

• $5,000 per year for remaining years of undergraduate study

26

Parent PLUS• Repayment begins

after loan is fully disbursed; or

• Parents can request postponement of payment until 6 months after a student ceases to be enrolled at least half-time; interest may be capitalized

Private Educational Loans

• Generally variable interest rates• No federal protections

– Deferment– Forbearance– Forgiveness– Mandated repayment plans

• Co-signer requirements

27

Home Equity

• Possible tax benefits• Generally variable interest rate• Eligibility could be for more than federal

loan programs allow• RISK!

– Making an unsecured debt secured– Upside-down in house

29

Major State Programs

• Commonwealth Award• Virginia Guaranteed Assistance Program• Tuition Assistance Grant Program (private only)• Two Year College Transfer Grant

30

Public College & Universities

• Programs– VGAP– Commonwealth Award– Transfer Grant (Community College to 4 Year)

• Amounts vary at each institution based on funding

• Generally have FAFSA Priority Filing dates

31

Private Colleges & Universities

• Program - Tuition Assistance Grant Program• Award amounts are based on the number of

eligible students and the amount of funds appropriated by the General Assembly

• Maximum 2014-15 Annual Award to be determined and is generally in the $2,000 - $3,000 range

• Application deadline is July 31st! Talk to a private college or university for more details.

32

Community College to Four Year College

• Two Year College Transfer Grant• Be a first-time entering freshman no earlier than summer 2007 • Be a full-time undergraduate in-state student meeting selective service

requirements • Have received an Associate’s degree at a Virginia two-year public institution

with a cumulative GPA of 3.0 on a scale of 4.0 for the Associate’s degree • Enroll into a Virginia four-year public or Virginia four-year private nonprofit

college or university by the fall following completion of Associate’s degree • Have financial need: defined as a federally calculated EFC of 8,000, or less • Maximum annual standard award is $1,000 ($500 per term), with an

additional $1,000 ($500 per term) for students enrolled into a degree program in: engineering, mathematics, nursing, teaching, or science

• Limited to three years or 70 credit hours • Maintain college GPA of 3.0 on a 4.0 scale and continue to demonstrate

financial need according to a prescribed needs analysis

33

Institutional Aid

Types of Institutional Aid• Need-based or merit-based grants• Scholarships• Loans: Student and Parent loans • Work-study

Application Process:• The Financial Aid Office at each institution can

explain what type of aid is available and the application procedures

34

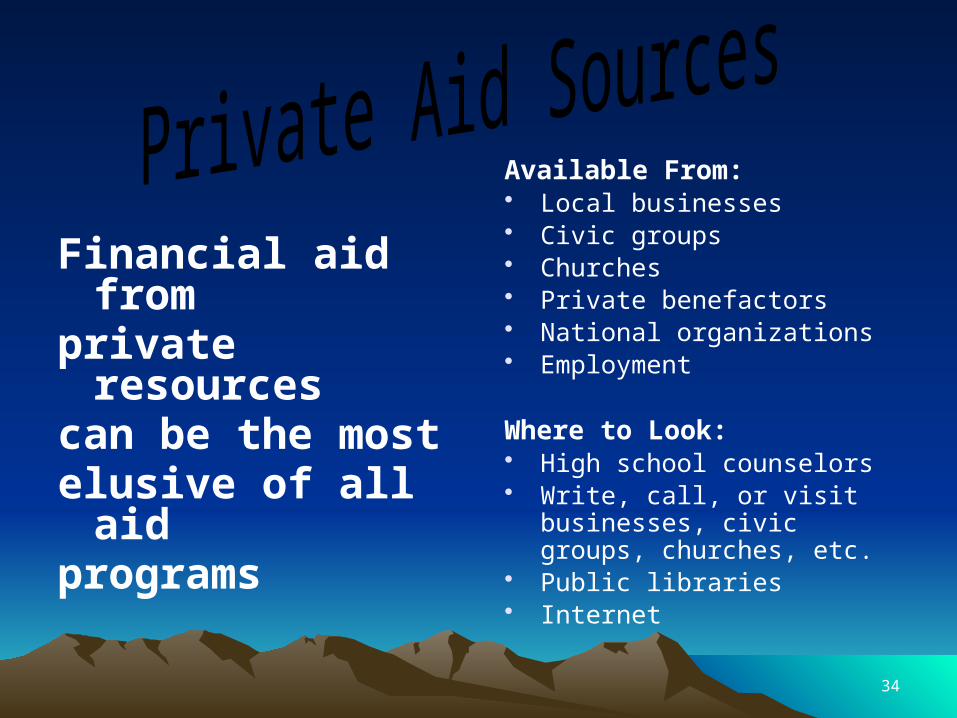

Financial aid fromprivate resourcescan be the mostelusive of all aidprograms

Available From:• Local businesses• Civic groups• Churches• Private benefactors • National organizations• Employment

Where to Look:• High school counselors• Write, call, or visit businesses,

civic groups, churches, etc.• Public libraries • Internet

35

Avoid Being Scammed

To check legitimacy of scholarship search services or individuals, for information about financial aid scams, & tips to avoid being scammed visit these Web sites:• Better Business Bureau: http://www.bbb.com • U.S. Department of Education:

http://studentaid.ed.gov/students/publications/lsa/index.html

36

Two Types of Financial Aid Award Notices

• Preliminary• Tentative• Estimated

• Official• Final (not an

accurate description)

• Non-preliminary• Actual

Timely responses are critical!

37

Net Price Calculators• All schools are required to have a “net price

calculator”• They all will NOT look or function identically• Example:

– Go to www.jmu.edu/finaid – Select “JMU Net Price Calculators” on the top bar– Answer the applicable questions– Receive an estimated award immediately

38

Finally

• Read each document• Keep copies of

EVERYTHING• Be aware of deadlines• File taxes early• Watch out for verification• Respond to all

correspondence• START LOOKING NOW!

39

Questions

Brad Barnett, MS, AFC®, CPFM

Senior Associate Director

James Madison University

Office of Financial Aid & Scholarships

MSC 3519

Harrisonburg, Virginia 22807

(540) 568-2894

www.jmu.edu/finaid