Embed Size (px)

Citation preview

1. One Seller 2. One Product

4. Non-Price competition

6. Price Maker (to maximize profits)

3. Blocked Entry (and exit?)

5. LR profits/losses

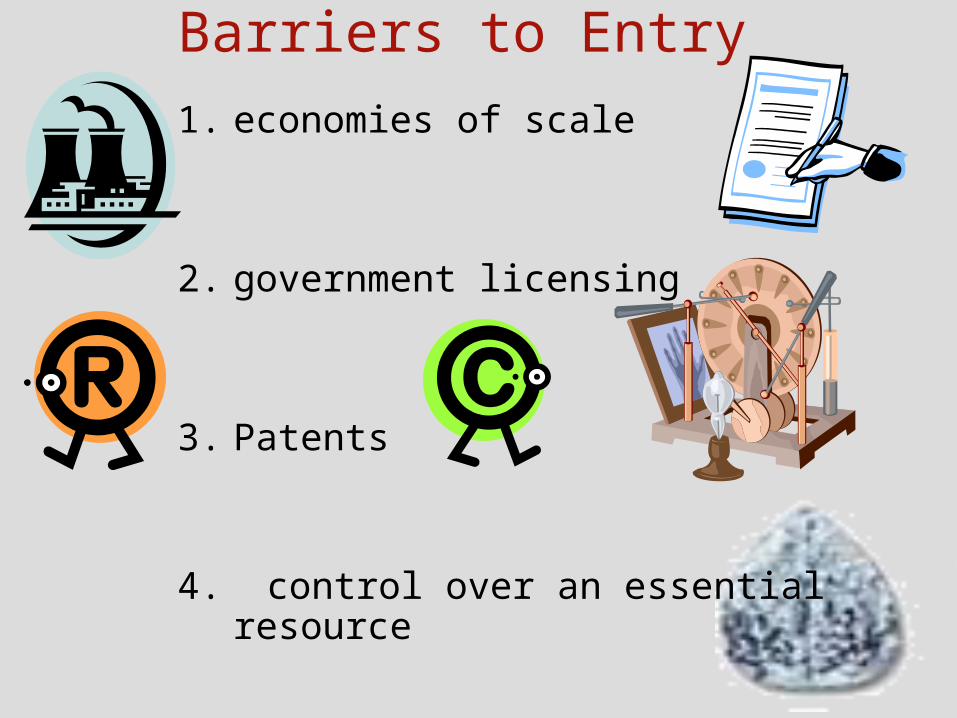

Barriers to Entry1. economies of scale

2. government licensing

3. Patents

4. control over an essential resource

Price and Output• A profit-maximizing firm will expand output

as long as marginal revenue exceeds marginal cost.• Price will be lowered and output expanded

until MR = MC

• The price charged will be greater than its marginal cost.

A Natural Monopoly Graph

Q

Average Cost

Q0.5

C1

Q1Q0.33

C0.5

C0.33

ATC

• One firm producing Q1 has average cost C1

• If two firms share the market, each produces Q0.5 and has average cost C0.5• If three firms share the market, each produces Q0.33 has average cost C0.33

d

Price

Quantity/time

P2

P1

MRq1 q2

Increase inTotal Revenue

Reduction inTotal Revenue

Marginal Revenue of a Monopolist• Initial price P1 & output q1.

Total revenue (TR) = P1 * q1.1. As price falls from P1 to P2,

output increases from q1 to q2,

two conflicting influences on TR.1. TR will rise because of an increase in the number of units sold (q2 - q1) * P2.

2. TR will decline [(P1 - P2) * q1] as q1 units once sold at the higher price (P1) are now sold at the lower price (P2). • Depending on the size of the shaded regions, total revenue may increase or decrease.

______

___

___

___

___

____________

0

1

2

3

4

5

6

7

8

9

10

OutputTotal Cost

Marginal Cost

Price (AR)Quantity Marginal

Revenue

50

80

90

110

140

180

230

290

360

440

530

0

1

2

3

4

5

6

7

8

9

10

120

110

100

90

80

70

60

50

40

30

20___

______

___

___

___

___

_________

0

110

200

270

320

350

360

350

320

270

200

30

10

20

30

40

50

60

70

80

90

Total Revenue

110

90

70

50

30

10

-10

-30

-50

-70___

______

___

___

___

___

_________

___

80

45

37

35

36

38

41

45

49

53

ATC

___

___

___

___

___

_________

___

Marginal Cost

Price (AR)Quantity Marginal

Revenue0

1

2

3

4

5

6

7

8

9

10

120

110

100

90

80

70

60

50

40

30

20

30

10

20

30

40

50

60

70

80

90

110

90

70

50

30

10

-10

-30

-50

-70

80

45

37

35

36

38

41

45

49

53

ATC

Cost

Output

60

50

40

30

20

10

1 2 3 4 5 60 7 8 9 10

70

80

90

100

110

120

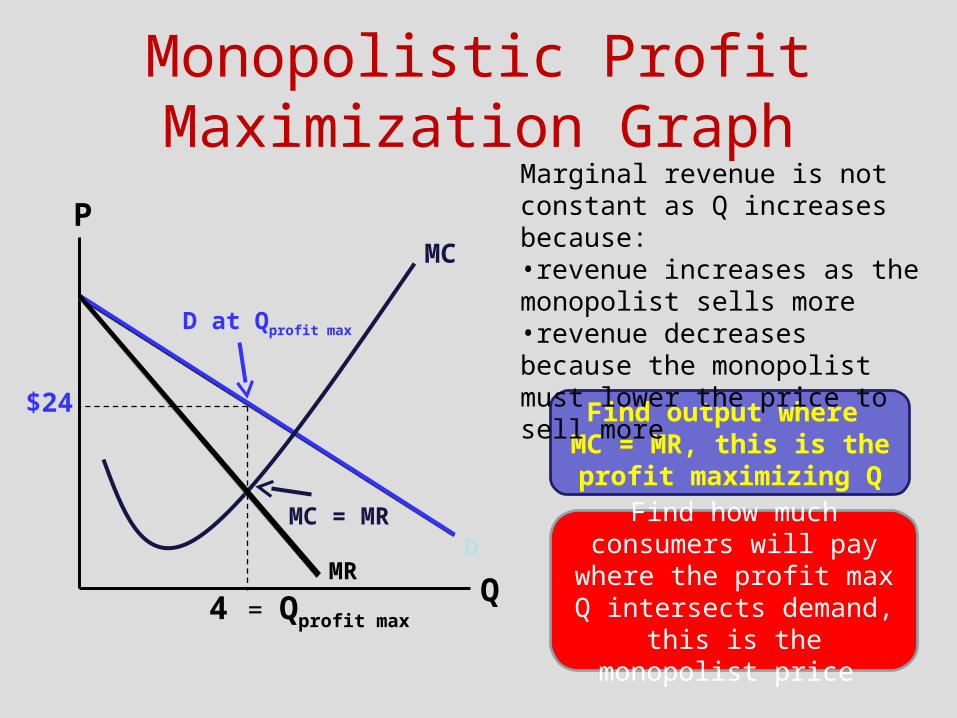

Monopolistic Profit Maximization Graph

MC

Q

P

Find output where MC = MR, this is the profit maximizing Q

DMC = MR

4 = Qprofit max

D at Qprofit max

$24

Marginal revenue is not constant as Q increases because:•revenue increases as the monopolist sells more•revenue decreases because the monopolist must lower the price to sell more

Find how much consumers will pay

where the profit max Q intersects demand, this is the monopolist price

MR

Monopoly Compared to Perfect Competition Graph

MC

Q

P

DM

QM

PM

Outcome: Monopoly output is lower and price

is higher than perfect competition

MRM

• In a monopoly, P>MR, • In perfect competition,

P=MR=D• MR=MC is the profit max

rule for both

PPC

QPC

First find the monopoly Q and P

Then find the perfectly

competitive Q and P

DPC= MRPC

The Welfare Loss from a Monopoly

MC

Q

P

D

QM

PM

• The welfare loss from a monopoly is represented by the triangles B and D

• The rectangle C is a transfer of surplus from the consumer to the monopolist

• The area A represents the opportunity cost of diverted resources, which is not a loss to society MR

PPC

QPC

A

BDC

dMR

MC

LRATC

Price

Quantity/time

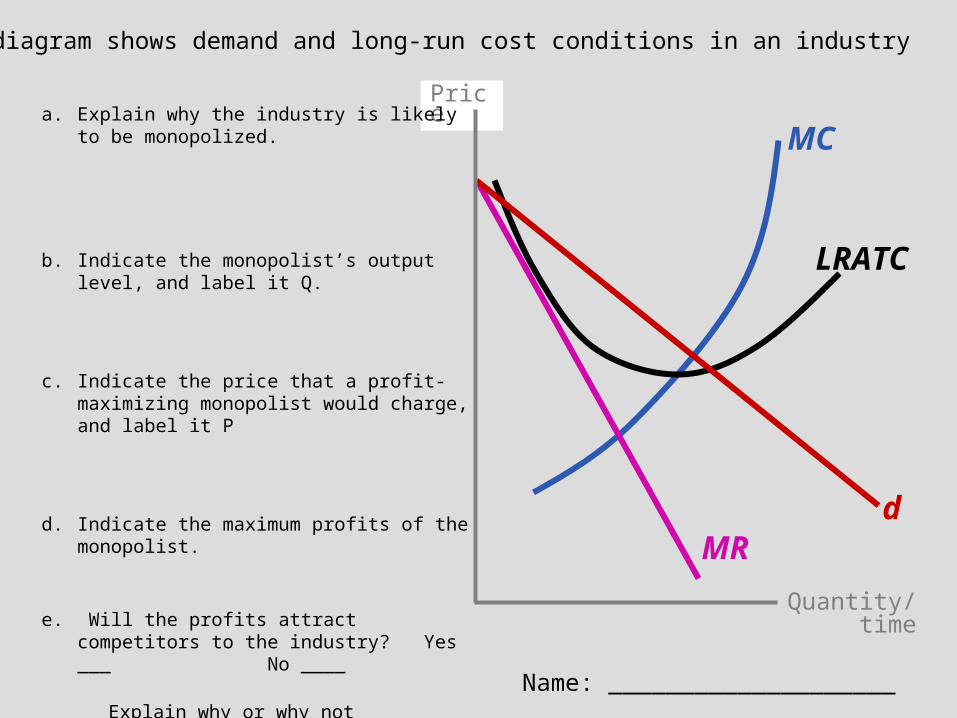

The diagram shows demand and long-run cost conditions in an industry

a. Explain why the industry is likely to be monopolized.

b. Indicate the monopolist’s output level, and label it Q.

c. Indicate the price that a profit-maximizing monopolist would charge, and label it P

d. Indicate the maximum profits of the monopolist.

e. Will the profits attract competitors to the industry? Yes ___ No ____

Explain why or why not

Name: ____________________

Price

Quantity/time

d

P

MR

q

MC

ATC

C B

A

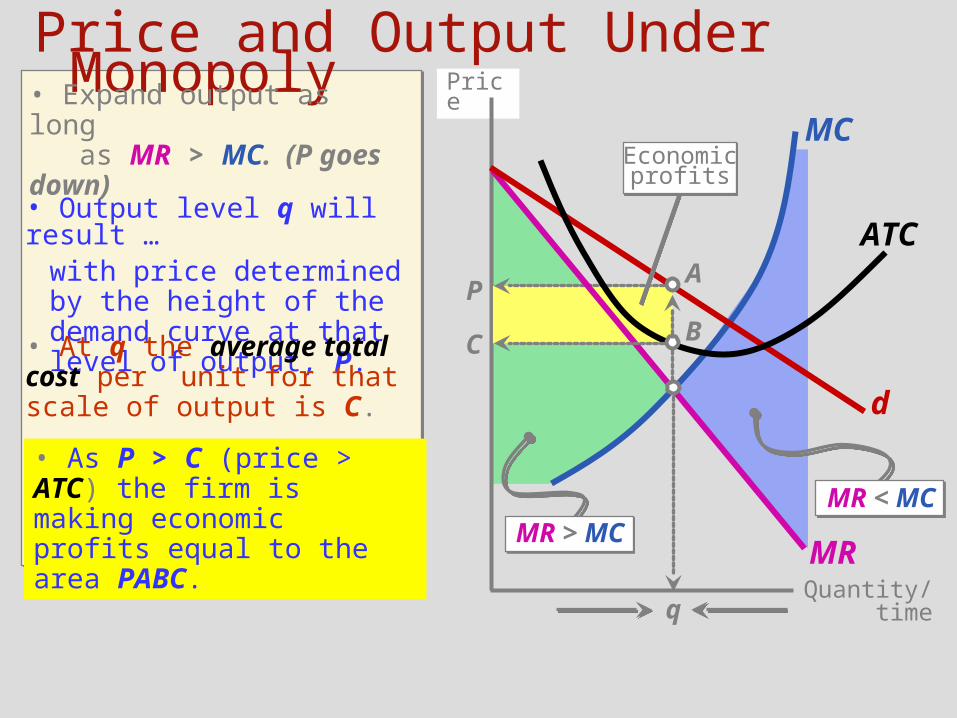

with price determined by the height of the demand curve at that level of output, P.

Price and Output Under Monopoly• Expand output as long

as MR > MC. (P goes down)

MR > MCMR < MC

• Output level q will result …

• At q the average total cost per unit for that scale of output is C.

• As P > C (price > ATC) the firm is making economic profits equal to the area PABC.

Economicprofits

0 ----

Totalrevenue

= (1)*(2) (3)

Price(per unit)

(2)

Output(per day)

(1)

1 $25.00 2 3 4 5 6 7 8 9

10

----- $50.00

Totalcosts

(per day) (4)

Profit

= (3) - (4) (5)

Marginal

cost(6)

Marginalrevenue

(7)

$24.00$23.00$22.00$21.00$19.75$18.50$17.25$16.00$14.75

$25.00$48.00$69.00$88.00

$105.00$118.50$129.50$138.00$144.00$147.50

$60.00$69.00$77.00$84.00$90.50$96.75

$102.75$108.50$114.75$121.25

-$35.00-$21.00-$8.00$4.00

$14.50$21.75$26.75$29.50$29.25$26.25

-$50.00 ----

$10.00 $25.00$9.00 $23.00$8.00 $21.00$7.00 $19.00$6.50 $17.00$6.25 $13.50$6.00 $11.00$5.75 $8.50$6.25 $6.00$6.50 $3.50

----

<<<<<<<<

Maximumprofits

• A monopolist will reduce price and expand output as long as MR > MC.

Price and Output Under Monopoly

• As the monopolist reduces price and expands output, profits increase … until the point where MC >

MR.• Here an output of 8 a day will maximize profits.

Profits Under Monopoly• High entry barriers protect

monopolists from competitive pressures.– Monopolists can earn long-run profits.

• However even a monopolist will not always be able to earn profit.– When ATC is always above the demand

curve, the monopolist will be unable to cover costs (unable to earn a profit).

• A monopolist will set output equal to q, where MR = MC

When a Monopolist Incurs Losses

d

P

MR

q

MC

ATC

C A

B

Price

Quantity/time

Short-runlosses

• At this level of output, the price that the monopolist charges does not cover the average total cost of producing the output ( P < C ).

• Whenever the ATC curve lies always above the demand curve, the monopolist will incur short-run losses.• In this diagram the firm is making economic losses equal to the shaded area, CABP.

D

P0

MRQ0

LRATC

MCP1

P2

Q1 Q2

Regulation of a MonopolistPrice

Quantity/time

• An unregulated monopolist produces where MR = MC (Q0) and charge price P0.• From an efficiency viewpoint, this output is too small and the price is too high. 1. average cost pricing

The monopolist is forced to reduce its price to P1 the expand output to Q1.

2. marginal cost pricing

-Force output to be expanded to Q2 where P = MC

- P = cost to produce

-Forces LR losses.

Average costpricing

Marginal costpricing

Allocative Efficiency• Allocative efficiency is achieved when the most

desired goods are produced at the lowest possible cost.

• The Minimum point on the ATC curve:• ATC > marginal cost at the minimum point• No allocative efficiency in a Monopoly.

Price Discrimination• Sellers may gain from price discrimination

by charging:• higher prices to groups of customers with

more inelastic demand • lower prices to groups of customers with

more elastic demand

• Price discrimination generally leads to more output and additional gains from trade.

The Economics of Price Discrimination

• If the airline charges all customers the same price, profits will be maximized where MC = MR. Here the airline charges everyone $400 and sells 100 seats.

Price

Quantity/timeSingle price

$400

$200

$300

$100

$500

$600

$700

MC

D100

MR

Net operating revenue($300*100) = $30,000

• Consider a hypothetical market for airline travel where the Marginal Cost per traveler is $100.

• This generates Net Operating Revenue of $30,000 or (total revenues) $40,000 – (operating costs) $10,000.

Price

Quantity/timeSingle price

$400

$200

$300

$100

$500

$600

$700

MC

D100

MR

Net operating revenue($300*100) = $30,000

The Economics of Price Discrimination• By charging higher prices to consumers with less

elastic demand and lower prices to those with more elastic demand it will increase net operating revenue.

• If the airline charges $600 to business travelers (who have a highly inelastic demand) and $300 to other travelers (who have a more elastic demand), it can increase its Net Operating Revenue to $42,000.

Price

Quantity/timePrice Discrim.

$400

$200

$300

$100

$500

$600

$700

MC

D

Net operating revenuefrom business travelers($500*60) = $30,000

Net operating revenuefrom all others($200*60) = $12,000

60 120

When economies of scale are important and an industry tends toward natural monopoly, splitting the industry into small, rival firms will a. lead to lower prices in the short run. b. cause prices to rise when demand is inelastic but fall when it is elastic. c. cause prices to fall because of the decline in producer profits.d. increase per-unit costs of production.

Which of the following is the most accurate description of a monopolist?

a. a firm that produces a single product b. a firm that is the sole producer of a narrowly defined product

class, such as yellow, grade-A butter produced in Jackson County, Wisconsin

c. a firm that is the sole producer of a product for which there are no good substitutes in a market with high barriers to entry

d. a firm that is large relative to its competitors

A monopolist will maximize profits bya. setting his price as high as possible. b. setting his price at the level that will maximize per-unit profit. c. producing the output where marginal revenue equals marginal cost

and charging the price on the demand curve at that quantity. d. producing the output where price equals marginal cost.

The incentive for the managers of a government-operated firm (for example, a state university) to promote internal efficiency and keep costs low will be

a. weak because it will be difficult for voters and their representatives to monitor and eliminate the inefficiency of such firms.

b. strong because public officials will have little concern for personal gain. c. strong because voters can easily recognize inefficiency and penalize the

public-sector managers who are responsible. d. weak because government employees are less competent than those who

work in the private sector.

Oligopolistic agreements on price tend to be unstable because a. although the monopoly price is the best price for all firms, oligopolists are

unaware of this.b. although the monopoly price maximizes the joint profits of the firms, a

secret price cut by any individual firm will increase the profits of that firm; hence, collusive agreements tend to break down.

c. the demand for the products of oligopolistic industries is inherently unstable relative to the demand for the products of non-oligopolistic industries.

d. firms in oligopolistic industries have more concern for consumers than do firms in competitive industries.

When firms use resources in an attempt to secure and maintain grants of market protection from the government, it is called a. rent seeking b. franchising.c. collusion. d. resource investment

What price and output in the graph would an unregulated profit-maximizing monopolist choose?

a. price C and output Rb. price B and output R c. price B and output S d. price A and output T

If a regulatory agency were using the “normal return” (zero economic profit) criteria to impose a price on a monopolist with the cost and demand conditions depicted, what price would the regulators set, and what output would the monopolist produce?

a. price A and output Tb. price C and output R c. price B and output R d. price B and output S

Would they be making a profit?a. yesb. no c. normal but not economic d. can’t tell

![[Christmas profits review] get $26,000 in one day!](https://img.dokumen.tips/doc/110x75/55a201a51a28ab42268b463a/christmas-profits-review-get-26000-in-one-day.jpg)