Embed Size (px)

Citation preview

1

October 29, 2010

California Tourism Outlook 2010-2011

Dan MishellDirector, Research

California Travel & Tourism Commission

2

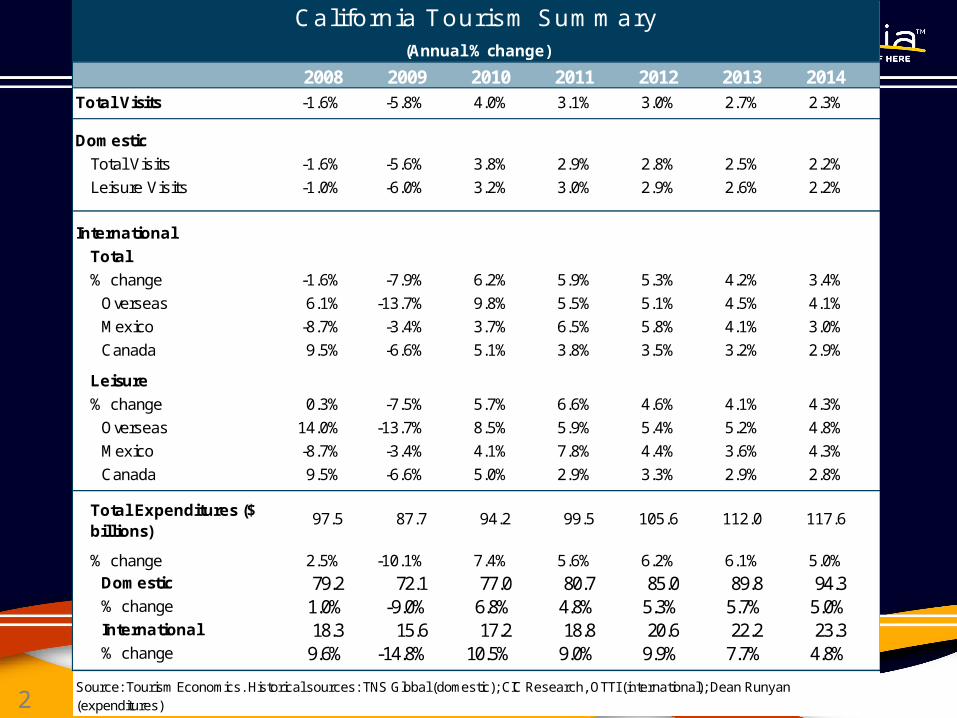

2008 2009 2010 2011 2012 2013 2014Total Visits -1.6% -5.8% 4.0% 3.1% 3.0% 2.7% 2.3%

Domestic

Total Visits -1.6% -5.6% 3.8% 2.9% 2.8% 2.5% 2.2%

Leisure Visits -1.0% -6.0% 3.2% 3.0% 2.9% 2.6% 2.2%

International

Total

% change -1.6% -7.9% 6.2% 5.9% 5.3% 4.2% 3.4%

Overseas 6.1% -13.7% 9.8% 5.5% 5.1% 4.5% 4.1%

Mexico -8.7% -3.4% 3.7% 6.5% 5.8% 4.1% 3.0%

Canada 9.5% -6.6% 5.1% 3.8% 3.5% 3.2% 2.9%

Leisure

% change 0.3% -7.5% 5.7% 6.6% 4.6% 4.1% 4.3%

Overseas 14.0% -13.7% 8.5% 5.9% 5.4% 5.2% 4.8%

Mexico -8.7% -3.4% 4.1% 7.8% 4.4% 3.6% 4.3%

Canada 9.5% -6.6% 5.0% 2.9% 3.3% 2.9% 2.8%

97.5 87.7 94.2 99.5 105.6 112.0 117.6

% change 2.5% -10.1% 7.4% 5.6% 6.2% 6.1% 5.0%Domestic 79.2 72.1 77.0 80.7 85.0 89.8 94.3% change 1.0% -9.0% 6.8% 4.8% 5.3% 5.7% 5.0%International 18.3 15.6 17.2 18.8 20.6 22.2 23.3% change 9.6% -14.8% 10.5% 9.0% 9.9% 7.7% 4.8%

California Tourism Summary(Annual % change)

Total Expenditures ($ billions)

Source: Tourism Economics. Historical sources: TNS Global (domestic); CIC Research, OTTI (international); Dean Runyan (expenditures)

3

California Tourism Mission

California has over 100 destination marketing organizations, and over 50 tourism business districts. (CTTC, Civitas)

CTTC provides a statewide platform for promoting the California brand to leisure travelers.

MISSION: To develop and maintain marketing programs in partnership with the state’s travel industry that keep California top-of-mind as a premier travel destination.

4

California’s Leisure Visitors

58%

42%

Spending

73%

27%

Person-Trips

DomesticInternational

36 million non-resident leisure person-trips in 2009

$24 billion in spending by non-resident leisure travelers

Sources: DK Shifflet & Assoc.; US Dept. of Commerce; CIC Research, Inc., Stats Canada

5

Domestic Leisure Overview

Six primary states account for nearly half of non-resident visits and 1/3 of non-resident spending in California.

Sources: DK Shifflet & Assoc.; TNS TravelsAmerica

6

International Market Overview, 2009

Canada UKJapan

Australia

Germany

Mexico (a

ir)

S. Korea

China India

France

Scandinavia

S. Americ

a0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

$0$200,000$400,000$600,000$800,000$1,000,000$1,200,000$1,400,000$1,600,000$1,800,000

Visit

ors

Spen

ding

in M

illio

ns

Lead

Mature

Emerging

Secondary

2009

Mexico Total • 6.3million visitors• $760 million spending

Sources: US Dept. of Commerce; CIC Research; Stats Canada; CTTC

7

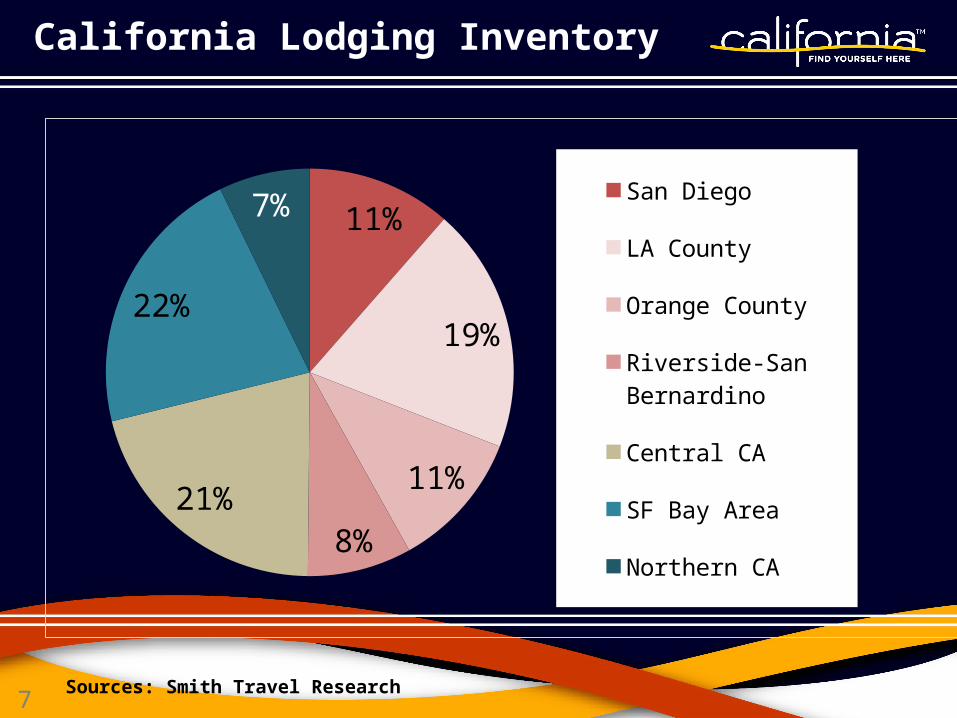

California Lodging Inventory

11%

19%

11%

8%21%

22%

7% San Diego

LA County

Orange County

Riverside-San Bernardino

Central CA

SF Bay Area

Northern CA

Sources: Smith Travel Research

8

04 05 06 07 08 09 10-60

-50

-40

-30

-20

-10

0

10

West region U.S.

Confidence Has Stabilized, but at a Low Level

Sources: ABC News, Washington Post

Consumer confidence index

The New Normal

9

2009 2010E 2011F 2012F

Unemployment rate 9.3 9.7 9.8 8.2

CPI -0.3 1.5 1.9 3.1Real personal disp. income 0.6 1.5 2.5 3.3

Real consumer spending -1.2 1.3 2.9 4.5

Real GDP -2.6 2.8 3.4 4.9Total after-tax profits 2.6 26.0 2.0 10.8

% change yr ago except unemployment rate

The New Normal

Recovery Will Proceed at a Tepid Pace

Sources: Moody’s Analytics, BLS, BEA

10

JapanFrance

U.K.Germany

CanadaAustralia

MexicoSouth Korea

IndiaChina

-10 0 10 20 30 40 50 60

2009-2014 2009

• China and India will remain growth leaders• Economies in Japan and Western Europe will be slower to recover• Australia shows no signs of slowing

New Normal – GDP

11

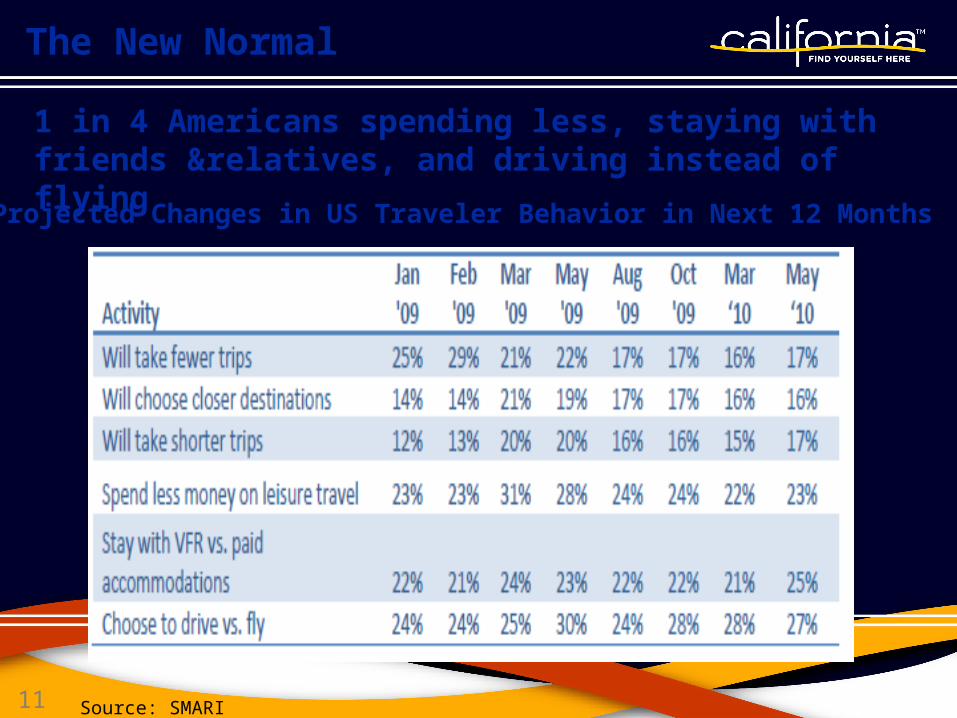

Projected Changes in US Traveler Behavior in Next 12 Months

1 in 4 Americans spending less, staying with friends &relatives, and driving instead of flying

Source: SMARI

The New Normal

12

Consumer Trends

• Recovery consumers are redefining value in a new era of consequences

• Consumers want transparency, trustworthiness and authenticity.

• The definition of “luxury” is morphing and now consumers want meaning along with material goods

The New Normal

Compiled from: The New Experience of Luxury Synovate 06/10, : PwC The New Consumer Paradigm: Permanent or Fleeting 10/09, Brand Keys 02/10, A Darwinian Tale The Futures Co 11/09

13

Forecast Overview

• Stronger than expected recovery in 2010 to date

• Visits will moderate in the second half of the year against headwinds from the economy and comparisons to late 2009

• The economic outlook is marred by uncertainty

14

CA Hotel Regional Occupancy

Source: Smith Travel Research

•Business and international travel are up

•Leisure travelers trading up from day to overnight

United St

ates

California

Anaheim LA SD SF

Oaklan

d

Riversi

de/SB

Sacra

mento

San Jo

se

CA South/C

entra

l

CA North

CA North

Centra

l

CA Centra

l Coast

0.0

5.0

10.0

15.0

20.0

Room Demand % Change by Region YTD August

GatewayRuralOther

15

Strong start to 2010…

-10%

0%

10%

20%

30%

40%

50%

60%To

tal

Chi

na

Indi

a

Japa

n

S. K

orea

Aus

tral

ia

U.K

.

Ger

man

y

Fra

nce

S. A

mer

ica

Mex

ico

(Air)

International Arrivals in California% change year ago, 2010H1

Source : CIC Research, OTTI

• International arrivals up 14% through June

16

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2007 2008 2009 2010 2011 2012 2013

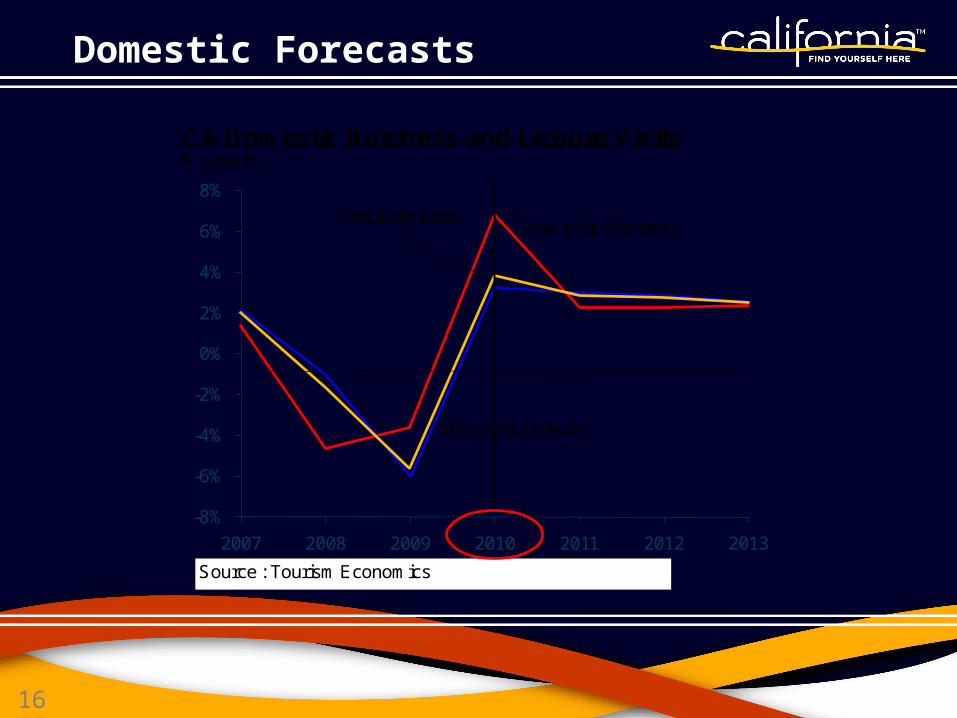

CA Domestic Business and Leisure Visits% growth

Source : Tourism Economics

Domestic Leisure

Domestic BusinessTotal Domestic

Domestic Forecasts

17

Domestic Forecasts

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2008 2009 2010 2011 2012 2013

Domestic Leisure Visits% growth

Source : Tourism Economics

Previous Forecast

Current Forecast

-6%

-4%

-2%

0%

2%

4%

6%

8%

2008 2009 2010 2011 2012 2013

Domestic Business Visits% growth

Source : Tourism Economics

Previous Forecast

Current Forecast

18

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2006 2007 2008 2009 2010 2011 2012 2013

CA International Inbound Travelannual % growth

Source : Tourism Economics

US inbound travel

CA inbound travel

International Forecast

19

-2

-1

0

1

2

3

4

5

6

7

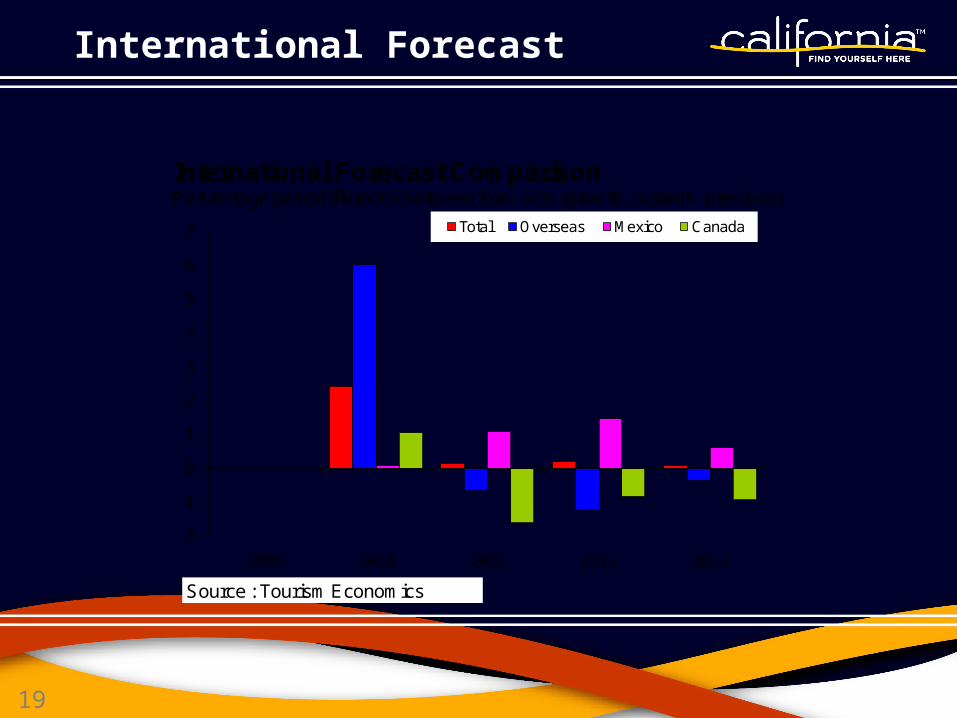

2009 2010 2011 2012 2013

Total Overseas Mexico Canada

International Forecast ComparisonPercentage point difference between forecasts (growth, current - previous)

Source : Tourism Economics

International Forecast

20

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2008 2009 2010 2011 2012 2013 2014

CA Visitor Expenditures% growth

Source : Dean Runyan, Tourism Economics

Total

Domestic

International

Spending Forecast

21

Spending Forecast

-15%

-10%

-5%

0%

5%

10%

15%

2008 2009 2010 2011 2012 2013

Visitor Spending% growth

Source : Tourism Economics

Previous ForecastCurrent Forecast

22

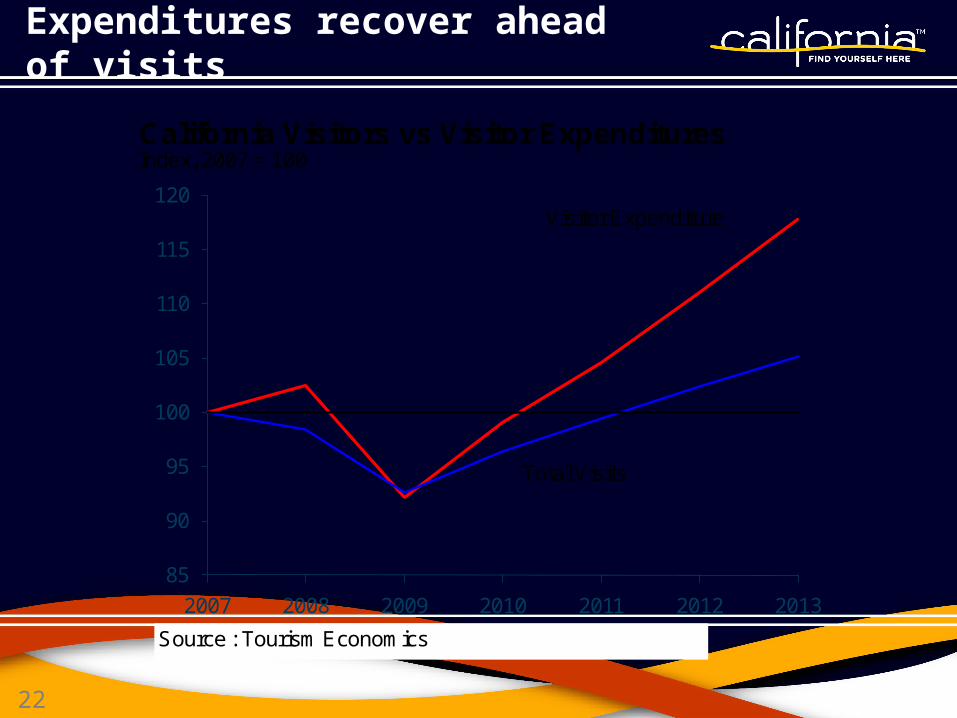

Expenditures recover ahead of visits

85

90

95

100

105

110

115

120

2007 2008 2009 2010 2011 2012 2013

California Visitors vs Visitor ExpendituresIndex, 2007 = 100

Source : Tourism Economics

Visitor Expenditure

Total Visits

23

2010 2011

Total Visits 4.0% 3.1%

Domestic Visits 3.8% 2.9%

International Visits 6.2% 5.9%

Total Spending 7.4% 5.6%

Domestic Spending 6.8% 4.8%

International Spending 10.5% 9.0%

California Travel Forecast Summary

Source: Tourism Economics

24

2008 2009 2010 2011 2012 2013 2014Total Visits -1.6% -5.8% 4.0% 3.1% 3.0% 2.7% 2.3%

Domestic

Total Visits -1.6% -5.6% 3.8% 2.9% 2.8% 2.5% 2.2%

Leisure Visits -1.0% -6.0% 3.2% 3.0% 2.9% 2.6% 2.2%

International

Total

% change -1.6% -7.9% 6.2% 5.9% 5.3% 4.2% 3.4%

Overseas 6.1% -13.7% 9.8% 5.5% 5.1% 4.5% 4.1%

Mexico -8.7% -3.4% 3.7% 6.5% 5.8% 4.1% 3.0%

Canada 9.5% -6.6% 5.1% 3.8% 3.5% 3.2% 2.9%

Leisure

% change 0.3% -7.5% 5.7% 6.6% 4.6% 4.1% 4.3%

Overseas 14.0% -13.7% 8.5% 5.9% 5.4% 5.2% 4.8%

Mexico -8.7% -3.4% 4.1% 7.8% 4.4% 3.6% 4.3%

Canada 9.5% -6.6% 5.0% 2.9% 3.3% 2.9% 2.8%

97.5 87.7 94.2 99.5 105.6 112.0 117.6

% change 2.5% -10.1% 7.4% 5.6% 6.2% 6.1% 5.0%Domestic 79.2 72.1 77.0 80.7 85.0 89.8 94.3% change 1.0% -9.0% 6.8% 4.8% 5.3% 5.7% 5.0%International 18.3 15.6 17.2 18.8 20.6 22.2 23.3% change 9.6% -14.8% 10.5% 9.0% 9.9% 7.7% 4.8%

California Tourism Summary(Annual % change)

Total Expenditures ($ billions)

Source: Tourism Economics. Historical sources: TNS Global (domestic); CIC Research, OTTI (international); Dean Runyan (expenditures)

tourism.visitcalifornia.com/research

Full Forecast Available Online