Embed Size (px)

Citation preview

1

MGT 821/ECON 873Martingales and Martingales and

MeasuresMeasures

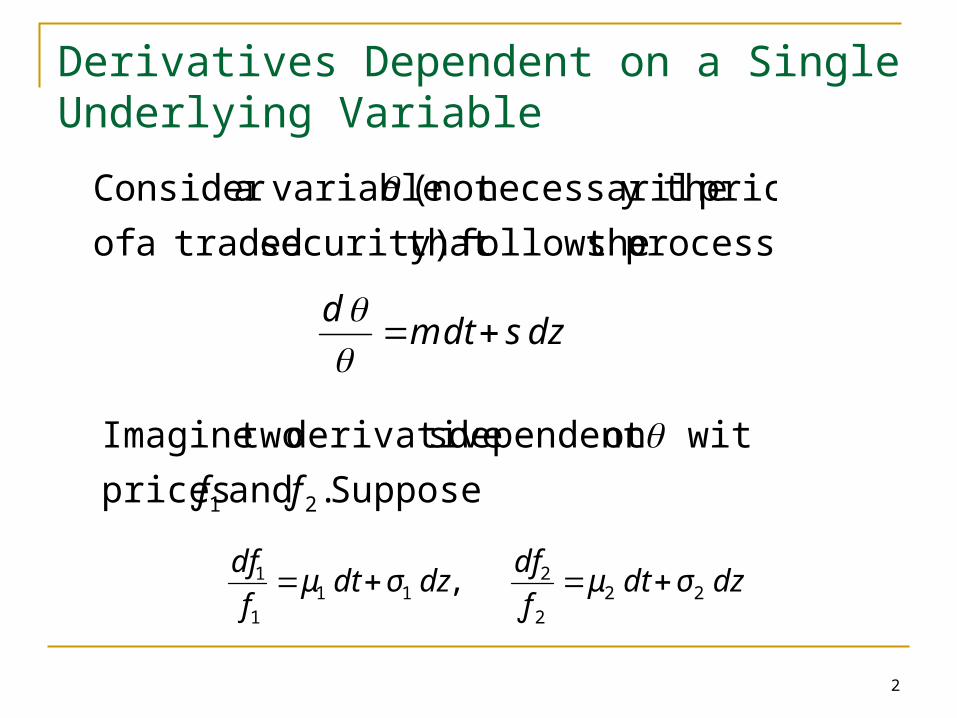

Derivatives Dependent on a Single Underlying Variable

2

process thefollows that security) tradeda of

price y thenecessaril(not variableaConsider

dzsdtmd

Suppose . and prices

with on dependent sderivative twoImagine

21 ƒƒ

dzσ dtμƒ

df dzσ dtμ

f

df22

2

211

1

1 ,

3

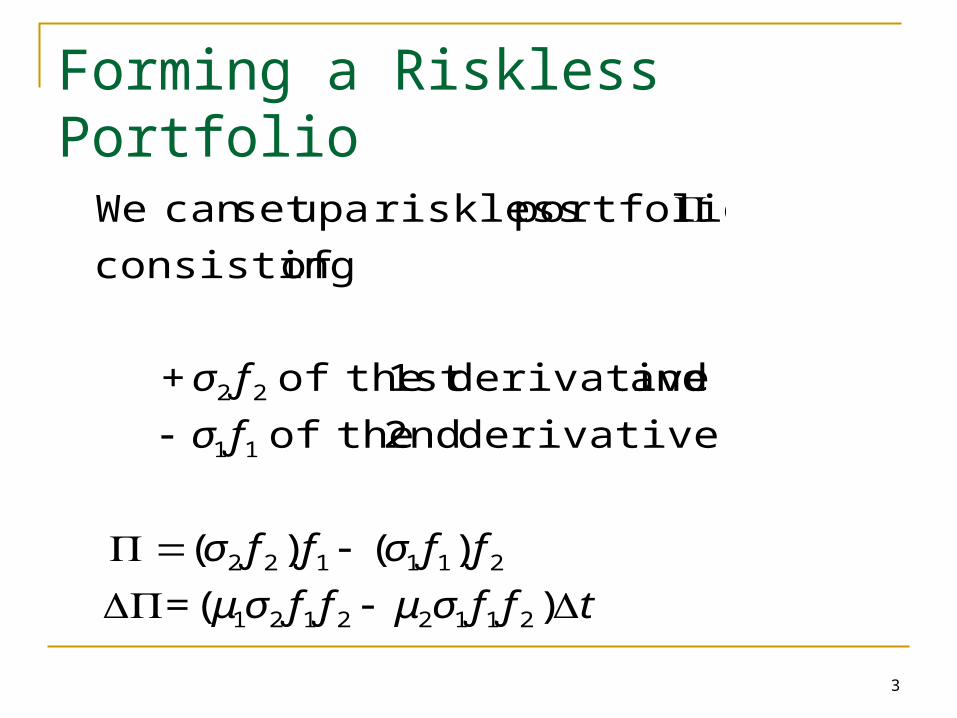

Forming a Riskless Portfolio

tƒƒσ샃σμ=

ƒƒσƒƒσ

ƒσ

ƒσ

)(

)()(

derivative 2nd theof

and derivative1st theof +

of consisting

portfolio riskless a upset can We

21122121

211122

11

22

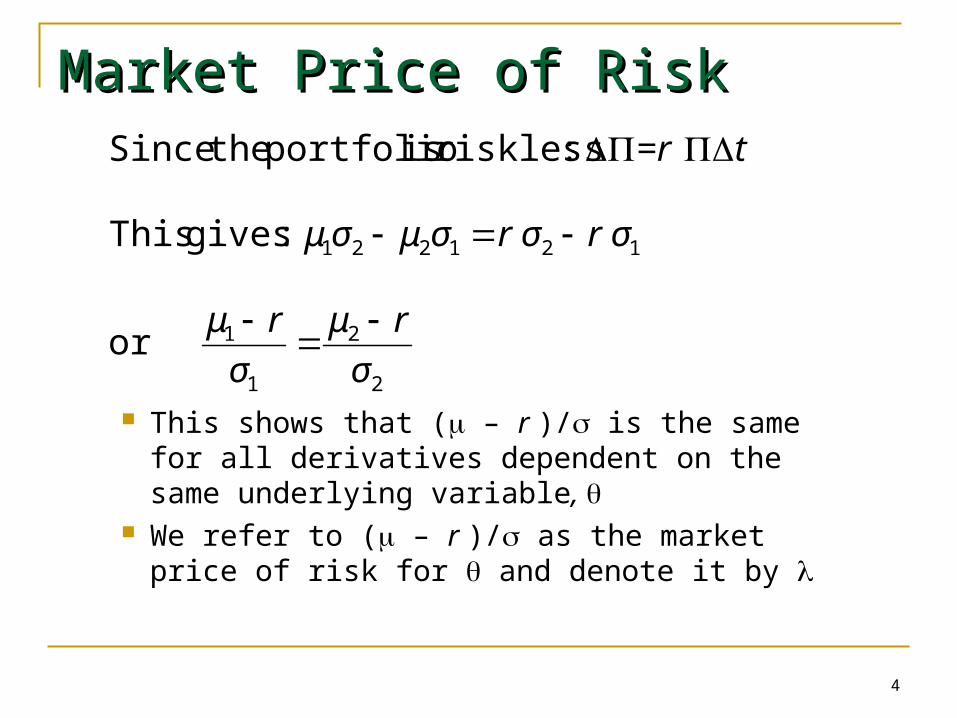

4

or

:gives This

:riskless is portfolio the Since

2

2

1

1

121221

σ

rμ

σ

rμ

r σr σσμσμ

t=r

Market Price of RiskMarket Price of Risk

This shows that ( – r )/ is the same for all derivatives dependent on the same underlying variable,

We refer to ( – r )/ as the market price of risk for and denote it by

5

Extension of the AnalysisExtension of the Analysisto Several Underlying Variablesto Several Underlying Variables

then

with

variablesunderlying severalon depends If

1

12

1

σλrμ

dzσμ dtf

df

f

n

iii

n

iii

6

MartingalesMartingales

A martingale is a stochastic process with zero drift

A variable following a martingale has the property that its expected future value equals its value today

7

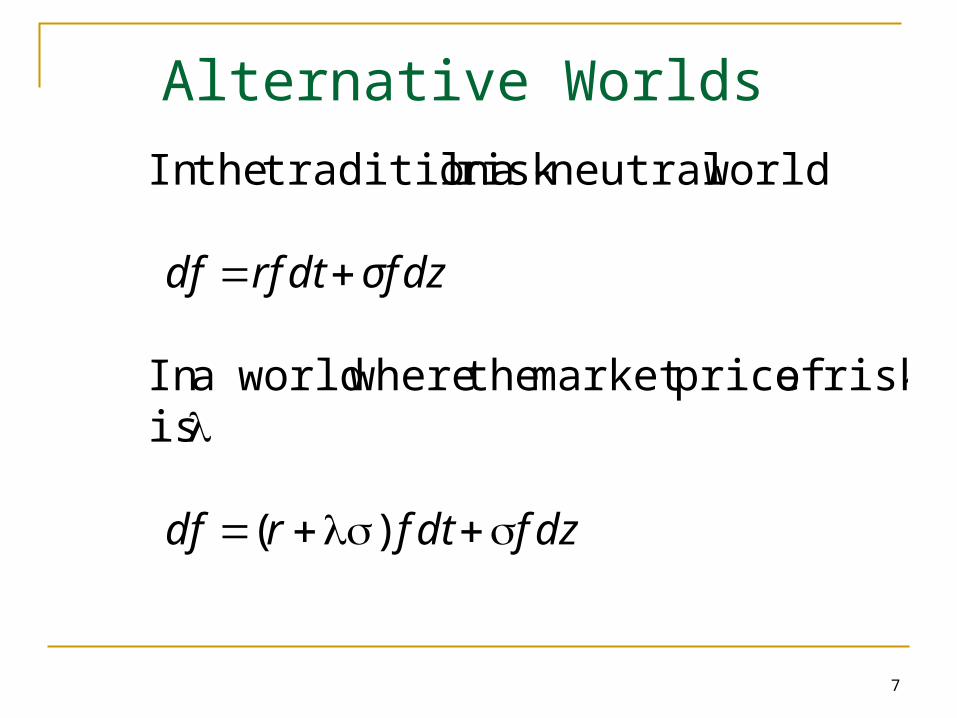

Alternative Worlds

dzfdtfrdf

dzσfdtrfdf

)(

is risk of price market the where worlda In

worldneutral-risk ltraditiona the In

8

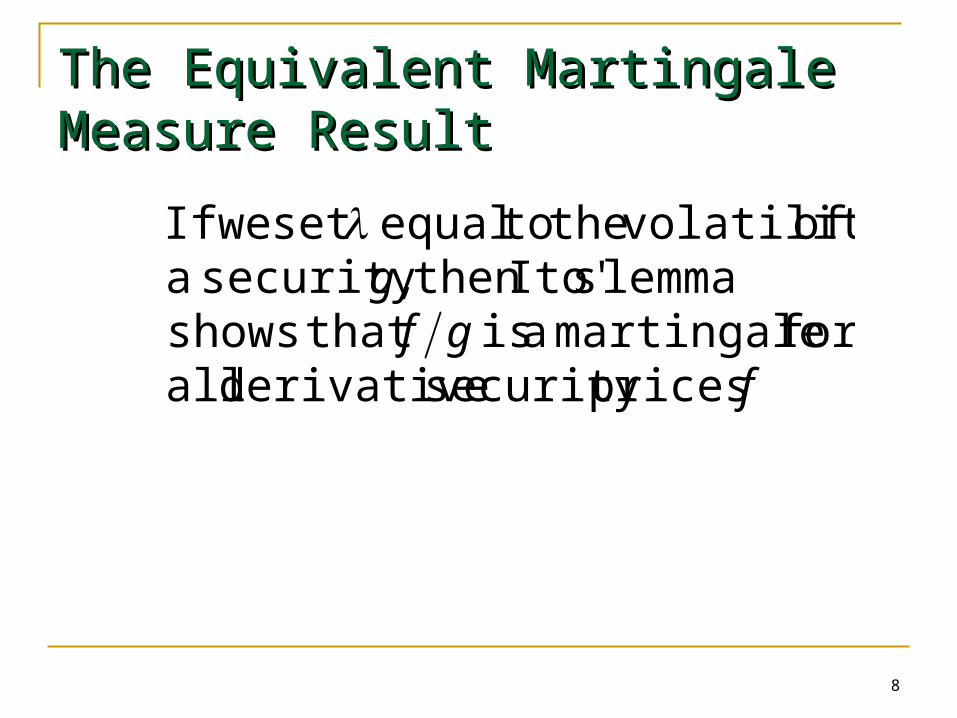

The Equivalent Martingale The Equivalent Martingale Measure ResultMeasure Result

fgf

g

pricessecurity derivative allfor martingale a is that shows

lemma sIto' then ,security a of volatility the to equal set weIf

9

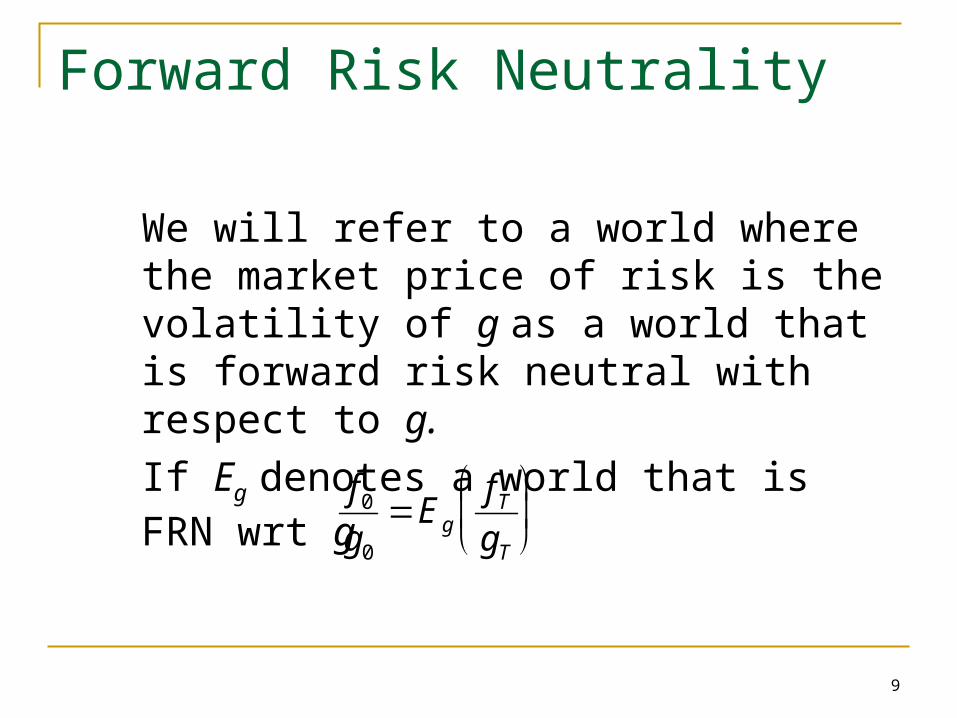

Forward Risk Neutrality

We will refer to a world where the market price of risk is the volatility of g as a world that is forward risk neutral with respect to g.

If Eg denotes a world that is FRN wrt g

f

gE

f

ggT

T

0

0

10

Alternative Choices for the Numeraire Security g

Money Market Account Zero-coupon bond price Annuity factor

11

Money Market Accountas the Numeraire

The money market account is an account that starts at $1 and is always invested at the short-term risk-free interest rate

The process for the value of the account is

dg=rg dt This has zero volatility. Using the money

market account as the numeraire leads to the traditional risk-neutral world where =0

12

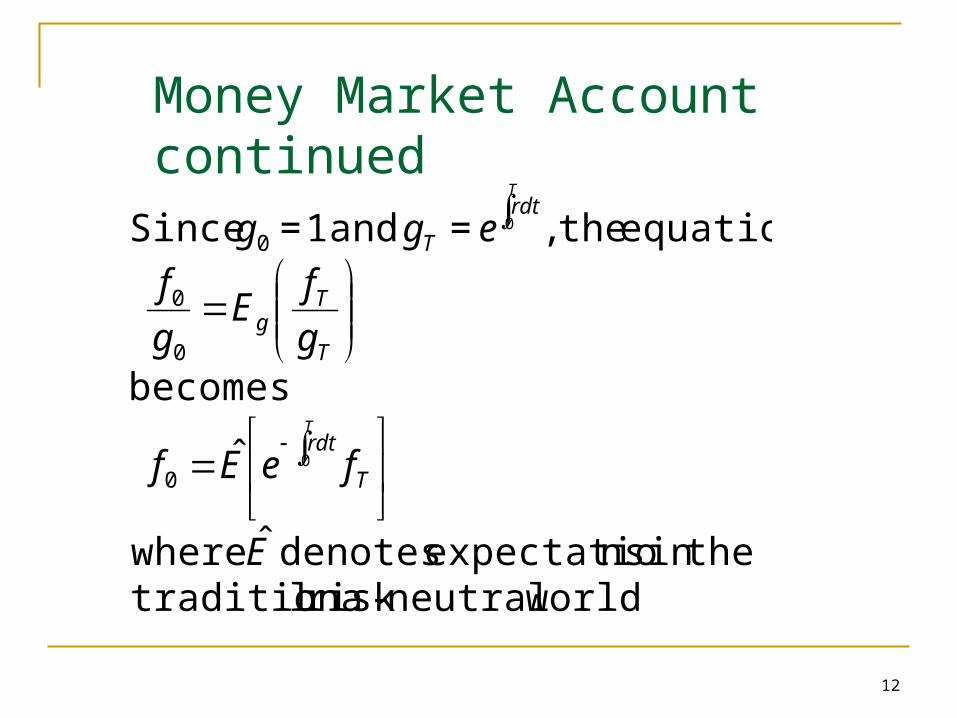

Money Market Accountcontinued

worldneutral-risk ltraditiona the in nsexpectatio denotes where

becomes

equation the ,= and 1= Since

E

feEf

g

fE

g

f

egg

T

rdt

T

Tg

rdt

T

T

T

ˆ

ˆ 0

0

0

0

0

0

13

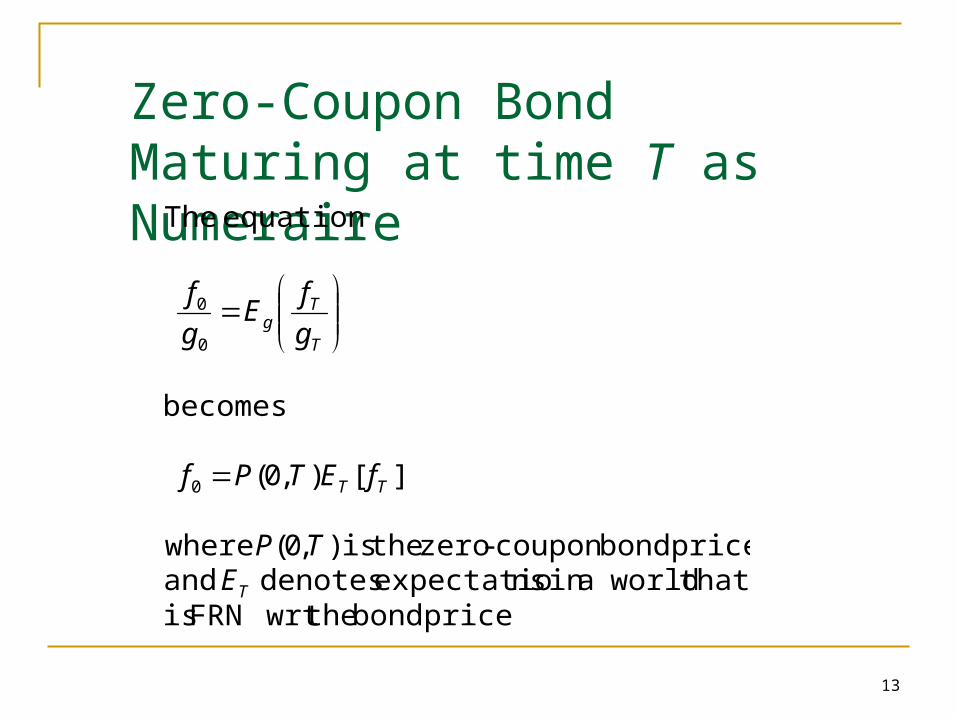

Zero-Coupon Bond Maturing at time T as Numeraire

price bond the wrtFRN is that worlda in nsexpectatio denotes and price bond coupon-zero the is ),( where

becomes

equation The

T

TT

T

Tg

ETP

fETPf

g

fE

g

f

0

][),0(0

0

0

14

Forward Prices

In a world that is FRN wrt P(0,T), the expected value of a security at time T is its forward price

15

Interest Rates

In a world that is FRN wrt P(0,T2) the expected value of an interest rate lasting between times T1 and T2 is the forward interest rate

16

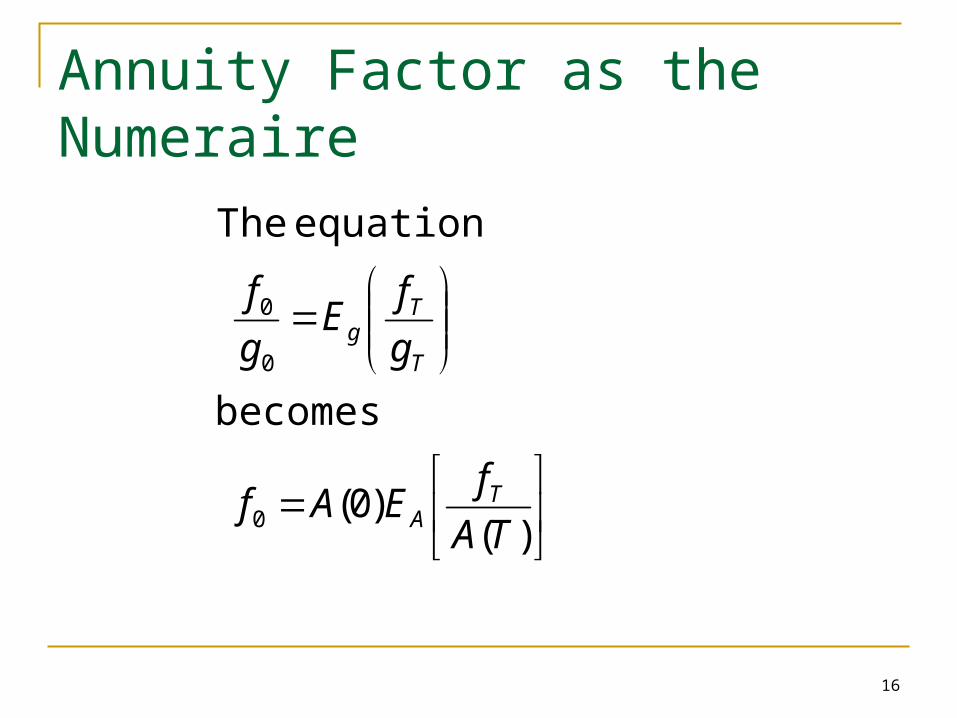

Annuity Factor as the Numeraire

)()0(0

0

0

TA

fEAf

g

fE

g

f

TA

T

Tg

becomes

equation The

17

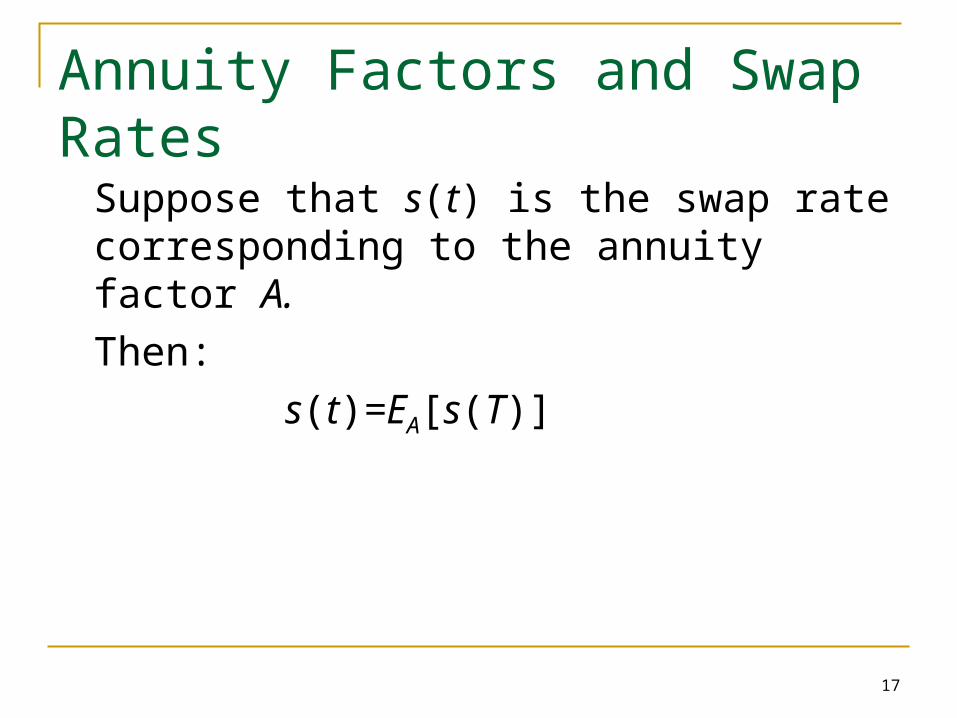

Annuity Factors and Swap Rates

Suppose that s(t) is the swap rate corresponding to the annuity factor A.

Then:

s(t)=EA[s(T)]

18

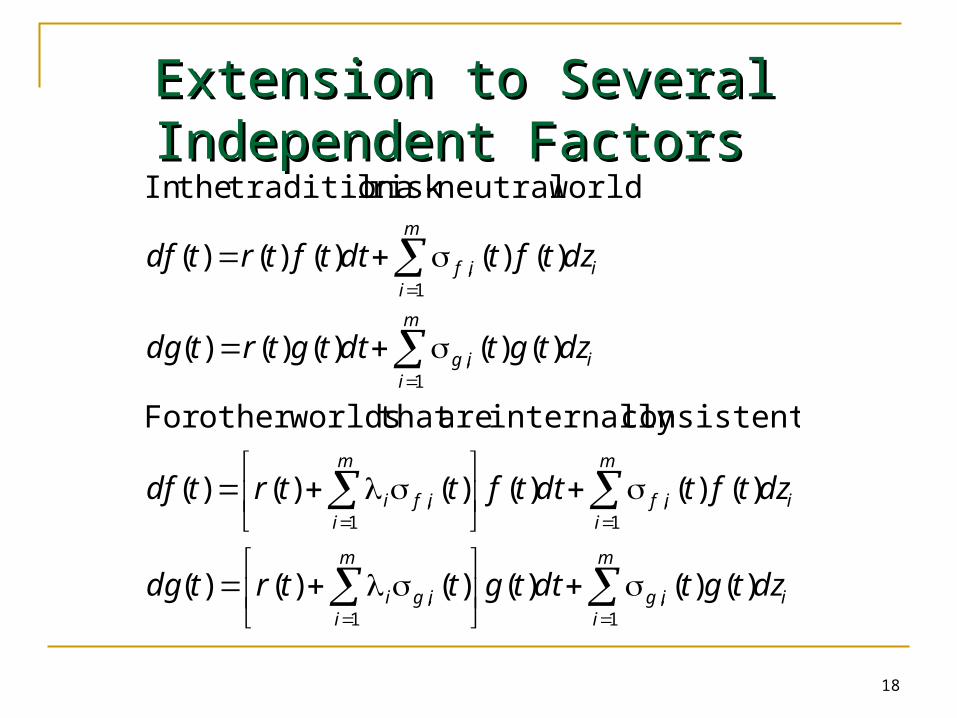

Extension to Several Extension to Several Independent FactorsIndependent Factors

m

iiig

m

iigi

m

iiif

m

iifi

m

iiig

m

iiif

dztgtdttgttrtdg

dztftdttfttrtdf

dztgtdttgtrtdg

dztftdttftrtdf

1,

1,

1,

1,

1,

1,

)()()()()()(

)()()()()()(

)()()()()(

)()()()()(

consistent internally are that worldsother For

worldneutral-risk ltraditiona the In

19

Extension to Several Independent Factors

hold. results the of rest the and martingalea is case, factor-one the in As

where worldas wrtFRN is that worlda define We

gf

σλg

igi ,

20

Applications

Extension of Black’s model to case where inbterest rates are stochastic

Valuation of an option to exchange one asset for another

Black’s ModelBlack’s Model

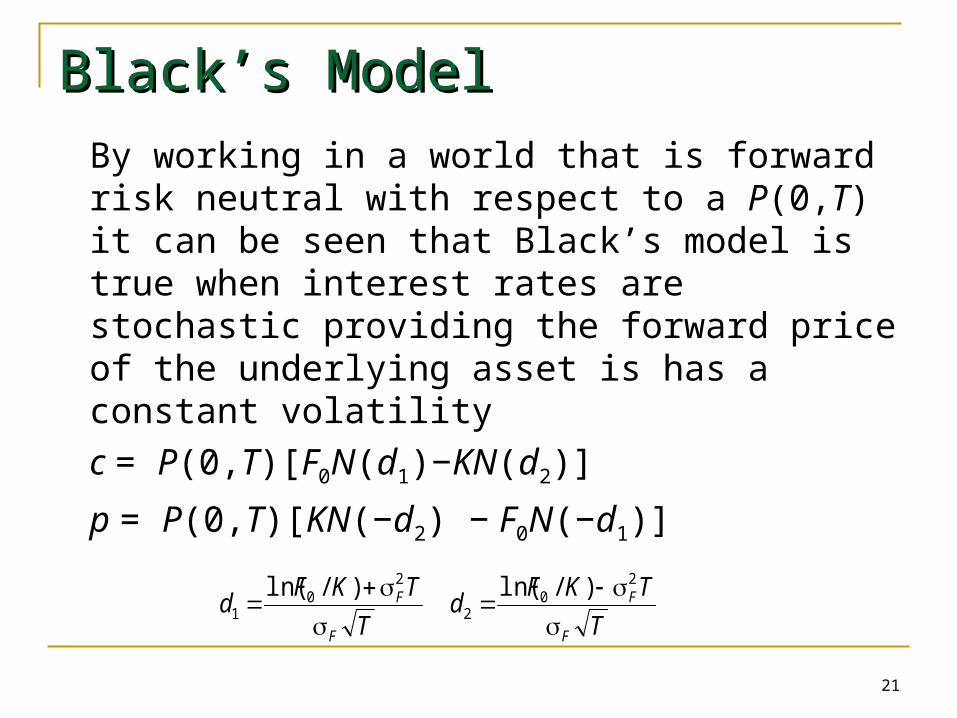

By working in a world that is forward risk neutral with respect to a P(0,T) it can be seen that Black’s model is true when interest rates are stochastic providing the forward price of the underlying asset is has a constant volatility

c = P(0,T)[F0N(d1)−KN(d2)]

p = P(0,T)[KN(−d2) − F0N(−d1)]

21

T

TKFd

T

TKFd

F

F

F

F

20

2

20

1

)/ln()/ln(

Option to exchange an asset Option to exchange an asset worth U for one worth Vworth U for one worth V This can be valued by working in a world that

is forward risk neutral with respect to U

22

23

Change of NumeraireChange of Numeraire

wvwghwv

vhg

w

vwv

and between ncorrelatio the is and of volatility the is of

volatility the is whereby increases variable a of drift the , to from

security numeraire the change weWhen

,,,

![Histoire de Martingales - [Mansuy]](https://img.dokumen.tips/doc/110x75/56d6bfa61a28ab30169713cc/histoire-de-martingales-mansuy.jpg)

![Quasi-Martingales - [Rao] - 1969](https://img.dokumen.tips/doc/110x75/577c80111a28abe054a72a6a/quasi-martingales-rao-1969.jpg)