Embed Size (px)

Citation preview

1

Karlsruhe -Liverpool Exchange

November 2003

Investment Portfolio Management

2

The Hope Sessions

The project sessions led by Liverpool Hope Staff will be concerned with shares, share investment and the management of share portfolios.• Part A consists of devising a share portfolio to match

a given description on a simulated Stock Exchange.• Part B consists of managing a £100,000 share

portfolio over a three month period• Part C consists of devising an investment decision

tool to help in managing portfolios

3

Purpose of the Session

This session provides an introduction to the project, discussing some of the background, and ensuring that you have a broad understanding of the topic, and a specific understanding of some of the terms used in the activity sheets which follow.

It also lays down some of the framework for the later stages of the project.

4

Session Content

In this session we will cover:

1. The main types of UK business organisation.

2. The stakeholders in companies and their financial and other interests.

3. The methods of financing a limited company.

4. Inspecting a company’s finances.

5. Shares and Shareholdings.

6. The Stock Exchange.

5

Discussions

Every so often, a ‘Discussion’ slide will appear. This is to cause you to take stock, and to review what has been said.

You should do this as a group, and each discussion period will be no more than 5 minutes.

Before we continue, a spokesperson from one of the groups will be asked to report on the result of their group’s discussions, and other groups will be asked to comment.

6

Part 1

The Main types of Business Organisation in the UK

7

The Main Types of Business Organisation in the UK

Sole Trader Partnership Limited Company (Ltd) Public Limited Company (PLC) Voluntary organisations Central and local government Quasi-governmental bodies

8

Limited Companies

In this session, we will concentrate on two of these: Limited Company (Ltd) Public Limited Company (PLC)

These organisations are similar, in that A limited company is an artificial legal person They are normally owned by at least two people

called shareholders A shareholder’s investment (their shares in the

company) is called the share capital The shares may be sold or given to another person.

9

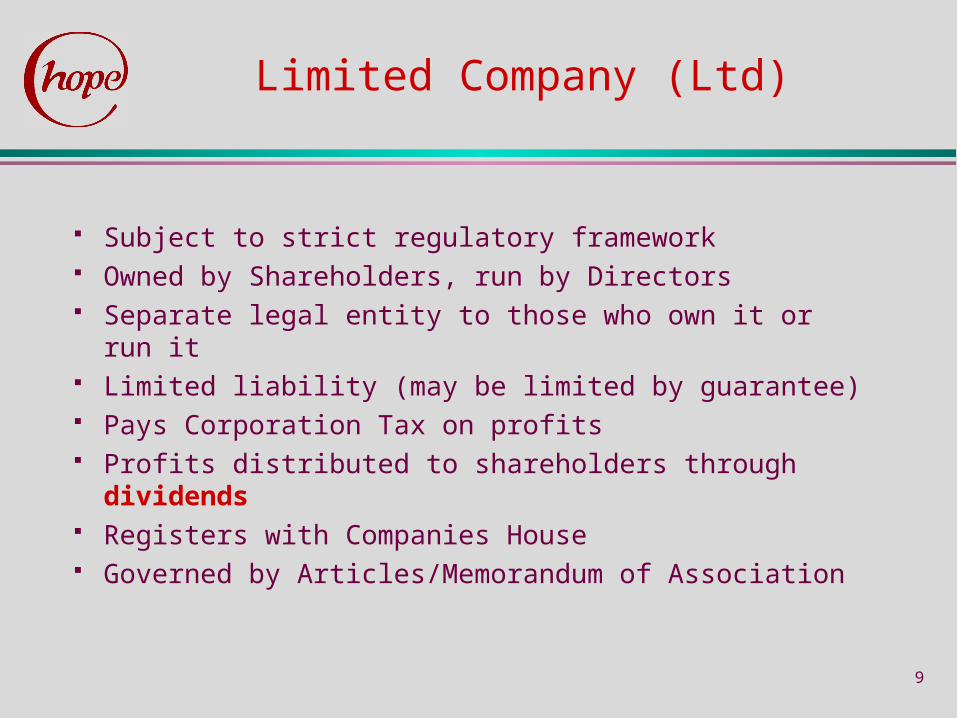

Limited Company (Ltd)

Subject to strict regulatory framework Owned by Shareholders, run by Directors Separate legal entity to those who own it or run it Limited liability (may be limited by guarantee) Pays Corporation Tax on profits Profits distributed to shareholders through dividends Registers with Companies House Governed by Articles/Memorandum of Association

10

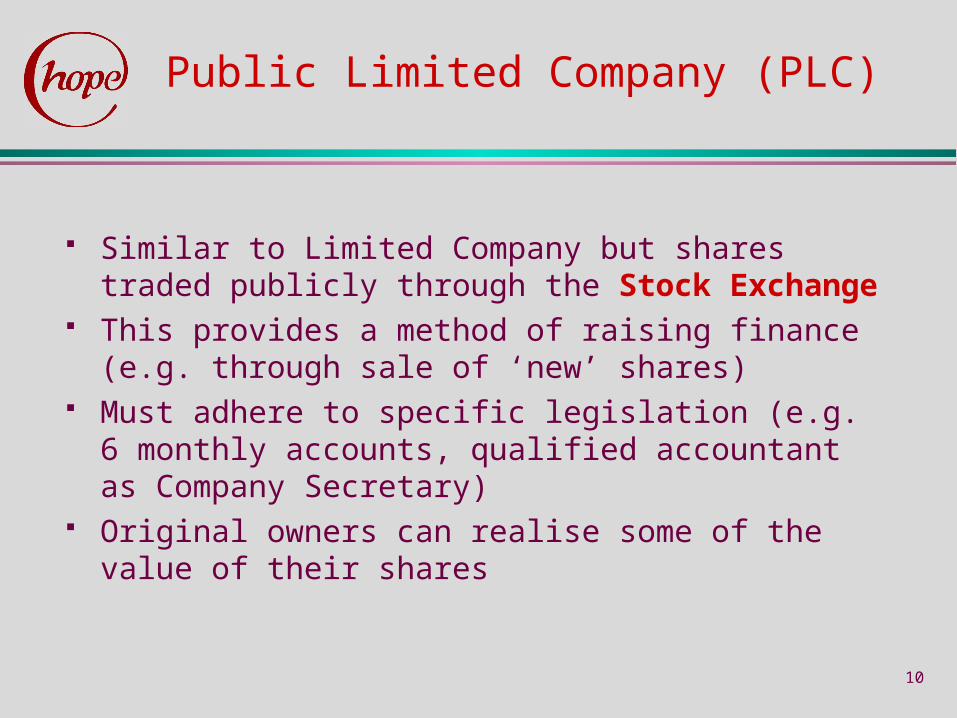

Public Limited Company (PLC)

Similar to Limited Company but shares traded publicly through the Stock Exchange

This provides a method of raising finance (e.g. through sale of ‘new’ shares)

Must adhere to specific legislation (e.g. 6 monthly accounts, qualified accountant as Company Secretary)

Original owners can realise some of the value of their shares

11

Statutory Requirements for Limited Companies

Annual report including:

Annual return

Profit and Loss Account, Balance Sheet &

Cash-flow Statement

Notes to Accounts

Directors report

Auditors’ report (if appropriate) Information required is dependent on size of the

Company (small, medium, or large)

12

Discussion 1

What are the different types of German business organisation?

Is there a similar division between private and public limited liability companies?

What rules apply to them?

13

Part 2

The Stakeholders in a Company

14

Business organisation

Competitors

Lenders

Managers

Shareholders Customers

Suppliers Investment analysis

Community representatives

Government

Employees and their

representatives

The main stakeholders in a company

15

Discussion 2

What sorts of things do you think these stakeholders might be interested in?

16

The interests of StakeholdersSocial, Legal & Ethical

EMPLOYEES Job security

Remuneration comparison

COMMUNITY Environmental Impact

Social Contribution

Jobs

GOVERNMENT Statutory legislation

Social responsibility

PAYE, Corporation Tax, VAT

17

The interests of stakeholders:Business

CUSTOMERS Continuity of supply

SUPPLIERS Credit risk

MANAGERS Company Performance

Strategic Plans

Corporate Objectives

COMPETITORS Threats

18

The interests of Stakeholders:Financial

LENDERS SecurityCredit riskFinancial structure

SHAREHOLDERS Organisational performanceValue of sharesManagement performanceReturn v. risk

INVESTMENT Performance of SharesANALYSTS Share Value v. Company Finances

19

Part 3

Financing a Limited Company

20

How Does a Company Finance its Operations?

Company Finance has 2 elements:• Long term Finance (Investment Capital)

• Money needed to set up an run the company over a period of years, used to buy plant, machinery etc. This finance purchases the Fixed Assets

• Short Term Finance (Working Capital)• Money needed to run the company on a day-to-day

basis, used to pay wages, buy stock etc. This finance is part of our Current Assets

21

Sources of Finance

Bank overdraft

Debt factoring

Ordinary shares

Preference shares

Total finance

Long-term

Short-term

Loans/ debentures

Leases

Invoice discounting

22

The major internal sources of finance for a company

Total internal finance

Tighter credit control

Delayed payment to creditors

Reduced stock levels

Long-termShort-term

Retained profits

These are the elements that the company can control to a certain extent; managers and directors can use these methods to increase or decrease available finance

23

The major external sources of finance for a company

Total external finance

Leasing

Loans &

Debentures

Share Issues

Short-termLong-term

Bank Overdraft

Although managers and directors can decide whether and how much to rely on these sources, each source represents an obligation on the company.

24

Capital Structure

Capital Structure is a term used to describe the mix of share capital, reserves and long-term loans etc. used to finance the company

The long term elements of Capital Structure are invested in Fixed Assets, with some left over for working capital

The short term elements come from items such as trade creditors and bank overdraft. They are normally used to cover seasonal or cyclical fluctuations

Long term finance incurs costs even when not needed Short term finance is flexible but may be more

expensive

25

Short-term finance

Long-term finance

Total funds

Time

Fixed assets

Permanent current assets

Fluctuating current assets

Short-term and long-term financial requirements

26

Discussion 3

Why does a company need long term finance anyway? Why, for example could the company not just work on overdrafts and credit?

27

Part 4

Inspecting a Company’s Finances

28

How can we find out where a company’s money comes from?

If we look at a company’s Balance Sheet, we can detect how a company’s finances are deployed, and what is the source of their financing. The headings for a limited company are:

Fixed Assets Current Assets Creditors: amounts falling due within 1 yr

(i.e. current liabilities) Creditors: amounts falling due after more than 1 yr

(i.e. long-term liabilities)

Capital & Reserves

29

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

30

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The figure above the line is what the company is worth when all debts have been paid off.

The figure above the line is what the company is worth when all debts have been paid off.

31

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The figure below the line is the total capital invested by or on behalf of the shareholders.

The figure below the line is the total capital invested by or on behalf of the shareholders.

32

Balance Sheet: Sheer Fiction PLC – In Summary

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The company is worth £1MThe company is worth £1M

The company OWES £1M to its shareholders

The company OWES £1M to its shareholders

33

Balance Sheet: Sheer Fiction PLC – In Summary

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The company is worth £1MThe company is worth £1M

The company OWES £1M to its shareholders

The company OWES £1M to its shareholders

Net value:

ZERO

Net value:

ZERO

34

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The total value of buildings, machinery, transport, fixtures and fittings.

The total value of buildings, machinery, transport, fixtures and fittings.

35

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

Money we could lay our hands on in a short space of time

Money we could lay our hands on in a short space of time

36

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

Money we have to pay out before the end of the year

Money we have to pay out before the end of the year

37

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

Money we will have to pay out eventually, but not in the near future.

Money we will have to pay out eventually, but not in the near future.

38

Balance Sheet: Sheer Fiction PLC

Fixed Assets £800,000Current Assets

Stock £500,000Debtors £50,000

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

Money the company owes to its shareholders.

Money the company owes to its shareholders.

39

Financing a Limited Company 1

If we take these in turn,

Fixed Assets £800,000

Current Assets

Stock £500,000

Debtors £50,000

This section shows what the company owns. There are several important ways a company can use

to raise finance through its assets, apart form simply selling them.

40

Financing a Limited Company 2

In the middle section of the balance sheet we have:

Creditors: Amounts falling due within 1 yr.Trade Creditors -£100,000Tax -£50,000

Creditors: Amounts falling due after 1 yr.Long Term Loan -£200,000

£1,000,000

This is what the company owes, and each item can be viewed directly as a source of finance.

They are items that we have either borrowed, or not yet paid. Therefore in some sense they represent money which is not ours, but we currently have in our possession and can deploy to our benefit.

41

Financing a Limited Company 3

On the final section of the Balance Sheet is:

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

This section again can be viewed as what the company owes, and so it is a source of finance.

In this case, the money is owed to its shareholders, the investors who have chosen to lend money to the company in return for a ‘share’ in the profits.

42

The Shareholder’s Claim on a Company

Share Capital

The amount of money invested in the company represented by the ‘face value’ of the shares.

Capital Reserves

The additional amount of money generated by the share capital from special transactions: e.g. upwards valuation of fixed assets, selling new shares for a price above their face value.

Retained Profits

The total amount of profit made prior to this year, but which has not been distributed to shareholders.

Profit for the Year

The amount of profit generated this year.

43

Discussion 4

As explained above, the profit after tax is the property of the shareholders.Sometimes this is retained by the company.

For what reason would a company retain profits and not distribute them to shareholders?

Why would shareholders stand for this - after all the company is keeping hold of their earnings!

44

Part 5

Shares and Shareholdings

45

Shares and Shareholdings

We will examine the following issues: Types of Share The Value of Shares Dividends

46

Shares

Shares are the basic units of ownership of a business. The number of shares that are issued and their nominal

value (sometimes called ‘face’ value) are at the discretion of the people who start up the company.

For example, a company may have an initial capital requirement of £10,000. This could be obtained by issuing: 10 shares at £1,000 each, 10,000 shares at £1 each 1 million shares at 1p each.

All shares must have the same value

47

Shares and the Stock Exchange

Shares in a PLC may be traded at the Stock Exchange. This is simply a marketplace for the buying and selling of

shares. Prices on the stock exchange are subject to the law of

supply and demand. The market value of a share is simply the price that

another investor is prepared to pay for it. This may be well above (or below) the face value of the share.

No money from this buying or selling of shares goes to the company.

48

The Value of Shares

There are three different values that can be attached to a share. We have seen two of these already:

The nominal value is the amount that the share was issued for in the first place.

The market value is its current price on the Stock Exchange

There is a third value: The actual value of a share is the total current value of a

share, if the company’s assets were all sold at their current value, all debts paid off and the proceeds distributed to each shareholder.

49

The Actual Value of Shares

On the final section of the Balance Sheet is:

Capital & ReservesShare Capital ( 500,000 shares, £1 each) £500,000Capital Reserves £250,000Retained Profits £200,000Profit for the Year £50,000

£1,000,000

The total worth of the company is £1,000,000; all of this is owed to its 500,000 shareholders.

If the £1,000,000 were shared out, each share would be £2.00 This is the actual value of the share.

50

Dividends

A Dividend is the amount earned by the shareholder’s investment over a period of time.

The term comes form the ‘dividing up’ of the profits so that each person get their ‘share’.

Companies will declare ‘dividends’ on each share. For example a dividend of 6.8% on a share with face value of 50p means that each share will earn 3.4p.

51

Rights of Shareholders

An ordinary shareholder in a company has the right to: Share in any profits Share in any funds remaining if business is wound up

(after all other liabilities paid off) (Usually) Vote at shareholders’ meetings over electing

directors & auditors, and accepting corporate report Vote to accept or reject takeover bids

52

Types of Shares

There are two different types of share that we need to consider:

Ordinary Shares All companies issue these type of shares. The total of the amount invested in these is normally

referred to as the equity of the company.

Preference Shares These shares guarantee that if a dividend is paid,

preference shareholders get the first part of it.

53

Discussion 5

In the main, the long-term capital to finance a company is derived from two sources: the money from shareholders, and money from loans.

Can you suggest some of the advantages and disadvantages of each type?

54

£m

2000

4000

6000

8000

10000

12000

14000

1986 199219901988 198919871985 19911984

16000

0

Ordinary shares

Preference shares

Loan capital

Capital issues of UK listed companies, 1984-92 Source: Annual Abstract of Statistics 1996

55

Changing the number and value of shares

Companies may Issue new shares Offer ‘rights issues’ Issue bonus shares Revalue shares

Each of these may have implications for current shareholders and may require changes to be made to the ‘Capital & Reserves’ section of the Balance Sheet.

We will consider this in a later session.

56

Part 6

The Stock Exchange

57

Trading Shares on the Stock Exchange

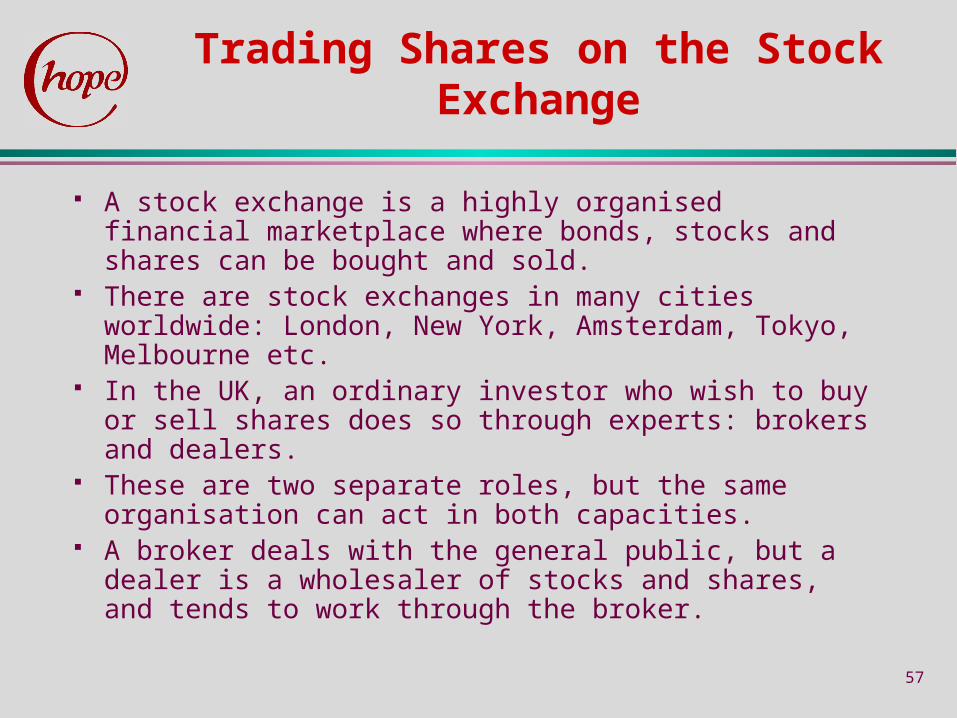

A stock exchange is a highly organised financial marketplace where bonds, stocks and shares can be bought and sold.

There are stock exchanges in many cities worldwide: London, New York, Amsterdam, Tokyo, Melbourne etc.

In the UK, an ordinary investor who wish to buy or sell shares does so through experts: brokers and dealers.

These are two separate roles, but the same organisation can act in both capacities.

A broker deals with the general public, but a dealer is a wholesaler of stocks and shares, and tends to work through the broker.

58

Fluctuations in Share Prices

Share prices are subject to the law of supply & demand. The prices quoted on the stock exchange will fluctuate constantly throughout the day. This graph shows end-of-day prices, and is typical of the variability to be expected.

Share prices are subject to the law of supply & demand. The prices quoted on the stock exchange will fluctuate constantly throughout the day. This graph shows end-of-day prices, and is typical of the variability to be expected.

59

Why do share prices Change?

Main reasons for changes in the market value of shares:• Changes in the overall market conditions, for example

external events such as 9/11. (A “Bull” market is when the market is generally optimistic, and shares are expected to rise; a “Bear” market is one where the mood is pessimistic, and shares are falling in value.)

• General nervousness & uncertainty in the political climate, for example general elections.

• Day-to-day trading: supply & demand - profit-taking on high-valued stock, bulk purchase of low-valued stock.

• Specific circumstances: takeovers, good/poor end-of-year result, seasonal variation etc.

60

The Problem of Risk

• All share investment involves risk; shares can lose much of their value as well as increase in value.(Foe example, in 1999 Marconi shares were over £11 each; in 2002 they were worth about 1.5 pence.)

• New companies tend to involve more risk than established companies.

• Smaller Companies tend to involve more risk than larger companies.

• Companies involved in peripheral services such as advertising, publishing tend to involve more risk than those involved in essential services such as fuel, transport and food.

61

Coping with Risk

There are several methods that investors use to cope with this uncertainty:• Trying to read market trends; spotting a bargain; buying

cheap and selling at a profit when the price has risen.• Keeping abreast of events; takeovers, profitability

forecasts; social changes.• Create a portfolio of shares of different types to balance

risk (Unit Trusts)• Balance different types of investment: shares, bonds,

property• Using statistics to attempt to predict trends and movements• Using automated share dealing software to respond

immediately to sudden share movements.

62

The FTSE Index

• The Financial Time Stock Exchange (FTSE) Index is a measure of the current confidence of investors in the Stock Market as a whole.

• It is based on an average of the current value of 100 of the the most popular and important shares

• In 2000 the FTSE stood at around 7000; at the beginning of 2002 it had dropped to around 3500; currently it is about 4300

63

Discussion 6

Can you suggest some of the companies listed on the FTSE 100?

What were the reasons that the FTSE lost about half its value between 2000 and 2002?

What implications do you think that this had for the companies listed?

64

Summary

• During this session we have looked at the background to shares, share investment and the stock market.

• The information presented here is sufficient to get you started on Task A, which will be explained shortly.