Embed Size (px)

Citation preview

1

Hantie van HeerdenElash Mistry14 Nov 2007

Overview of Experience for Long-term Insurers in SA

2006

2

Why are we here?

To provide information to practicing life actuaries on representative SA Statutory

Valuation Method bases reported in 2006

3

What will we show you?

• Brief overview of the LT insurance market in 2006

• Review the representative:– Reported AOS results (C7),– Reported valuation assumptions (G10.x) and– Reported actual experience (B - statements) for

certain key elements in a valuation basis

4

Overview of the LT Insurance Market in 2006

5

Overview: rankings

InsurerIndustr

y

% of Marke

t Assets

Rank on Assets

2006 2005 2004

Old Mutual Typical 28.3% 1 1 1

Sanlam Typical 17.1% 2 2 2

Liberty Typical 12.1% 3 3 3

Momentum Typical 11.3% 4 4 4

Investment Solutions Linked 8.0% 5 5 5

Metropolitan Life Typical 4.6% 6 6 6

Investec Assurance Linked 2.1% 7 7 8

Allan Gray Life Linked 1.9% 8 10 13

Capital Alliance Life Typical 1.5% 9 8 9

Investec Employee Benefits Typical 1.3% 10 9 7

6

Overview: by year-end

9 10

16

35

1

32

0

100

200

300

400

500

600

700

800

900

Feb Mar Jun Aug Sep Nov Dec

Month of year-end

As

se

ts in

R'b

n

0

5

10

15

20

25

30

35

Nu

mb

er

of

ins

ure

rs

Total assets Number of insurers

7

Overview: by license

R235 bn premiums | R220 bn benefits | 94% retention

3 4 2

100

52 3 1

88

8

119 118

0

50

100

150

Assistance Disability Fund Health Life SinkingFund

R'b

n

Gross premiums Gross benefits

8

Overview: per business class

R235 bn premiums | R220 bn benefits | R1,146 bn assets

291

68 82

438

201

66

0

50

100

150

With-profitbusiness

With-profitannuities

Without-profitannuities

Linked Marketrelated

OtherPre

miu

ms

an

d b

en

efi

tsR

'bn

050100150200250300350400450500

As

se

ts R

'bn

Gross premiums Gross benefits Total Assets

9

Overview: growth by license

Growth from 2005 to 2006 by type of licence

18%12%

16% 14%11%

32%

19%14%

4%

14%

21%

31%

57%

49%

0%

10%

20%

30%

40%

50%

60%

Assistance Disability Fund Health Life SinkingFund

TotalGross

Gross premiums Gross benefits

10

Overview: growth per business class

Growth from 2005 to 2006 per type of business

2%

24%

54%

10%

31%

3%

13%

53%

23%

29%

17%15%

4%8%

46%

5%

27%26%

0%

10%

20%

30%

40%

50%

60%

With-profitbusiness

With-profitannuities

Without-profitannuities

Linked Market related Total

Gross premiums Gross benefits Total Assets

11

Overview: over time

Amounts in R‘bn 2006 2005 2004 2003

Total assets 1,281 1,069 906 817

Total liabilities 1,170 975 817 736

Excess assets 111 94 89 81

CAR before management action

69 65 63 73

CAR after management action

29 27 27 32

Funding factor (Excl CAR)

1.10 1.10 1.11 1.11

CAR Cover 3.89 3.48 3.28 2.55

CAR after / CAR before 42% 41% 43% 44%

12

Overview: key indicators

IndustryTotal R'bn 2006

Total R'bn 2005

Total R'bn 2004t l r a n c

Number of active insurers

31 11 6 9 12 4 73 71 70

Net premiums received

69% 29% 1.3% 0.3% 0.5% 0.6% 220 166 151

Net benefits paid

68% 29% 1.0% 0.2% 0.4% 1.0% 210 160 162

Acquisition expenses

94% 0.4% 1.7% 0.7% 1.0% 2.1% 16 15 12

Operational expenses

94% 2.5% 1.3% 0.7% 0.7% 0.8% 13 10 8t = typical; l = linked; r = reinsurer; a = assistance; n = niche; c = captive

13

Overview: asset composition per industry

Asset classes t l r a n c All

Equities 45% 44% 0% 7% 59% 21% 45%

Fixed interest 20% 13% 62% 5% 29% 32% 19%

CIS 12% 21% 2% 51% 3% 13% 14%

Cash 9% 14% 24% 22% 7% 25% 10%

Property 4% 0% 0% 1% 0% 0% 3%

Other 10% 7% 12% 12% 2% 9% 9%

Investment Yield 22.1% 31.3% 6.2% 14.6% 24.8% 13.8% 23.1%

Total Assets (R'bn)

1,060 200 8 1 9 3 1,281

14

Capital Adequacy Requirement (CAR)

15

Distribution of CAR

80%

2%

18%

0%

20%

40%

60%

80%

MCAR TCAR OCAR

% of Active Insurers % of Total CAR

16

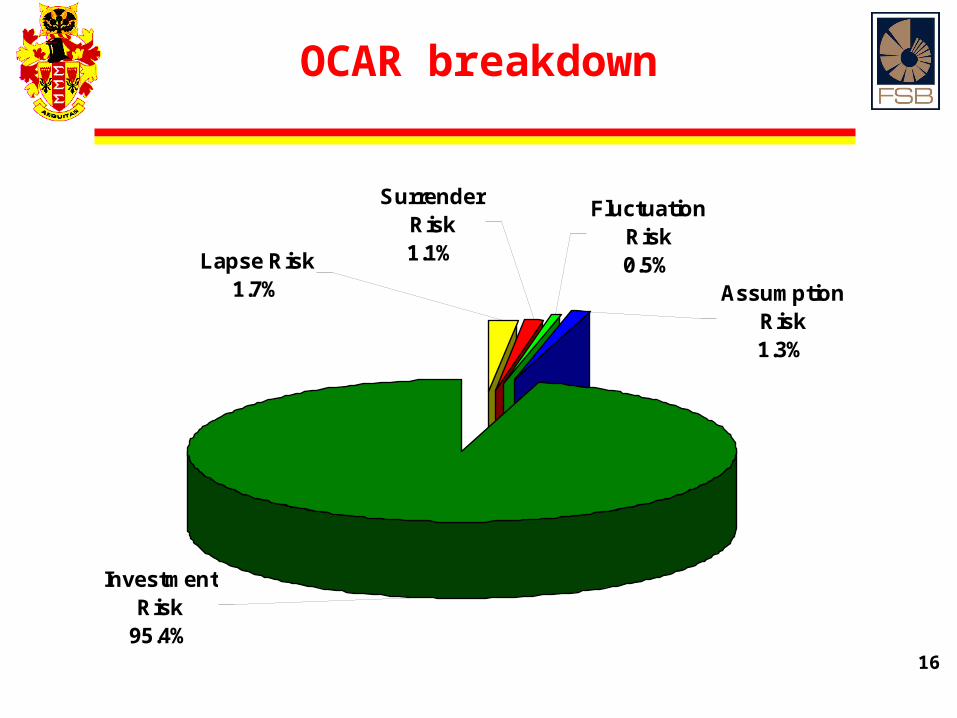

OCAR breakdown

Investment Risk

95.4%

Fluctuation Risk0.5%

Surrender Risk1.1%Lapse Risk

1.7% Assumption Risk1.3%

17

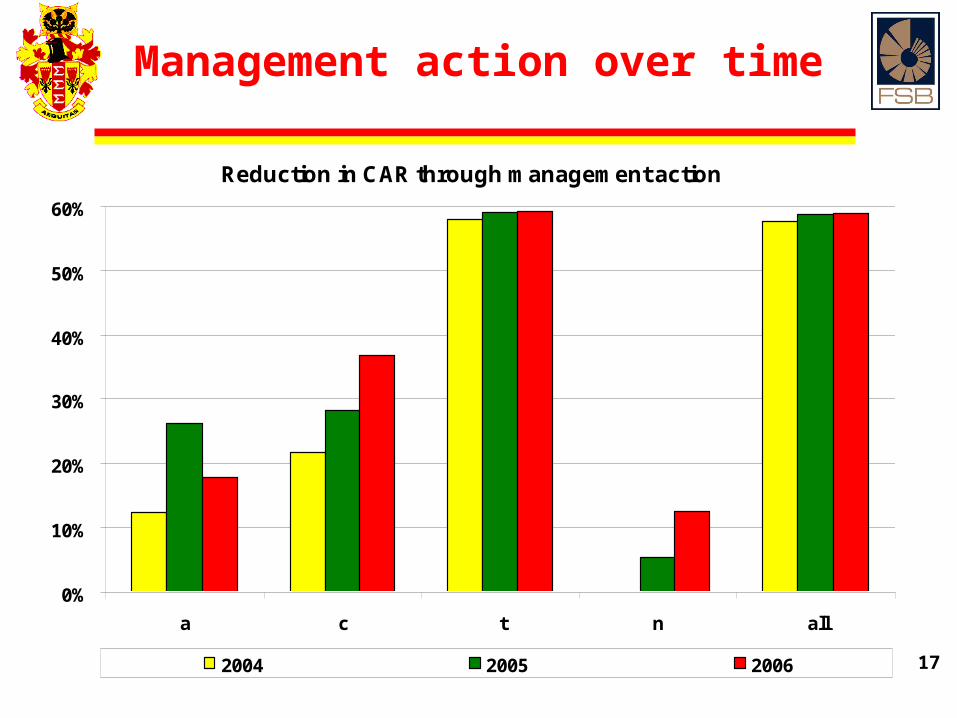

Management action over time

Reduction in CAR through management action

0%

10%

20%

30%

40%

50%

60%

a c t n all

2004 2005 2006

18

Proportion of insurers that applymanagement action

Industry

Number ofinsurers usingmanagement

action

Total numberof insurers

Proportion

Assistance 1 9 11%

Captives 1 4 25%

Niche 3 12 25%

Typical 11 31 35%

Total 16 73 22%

19

Management action

• Examples of management actions used:– Reduce future bonuses– Reduce/Remove non-vested bonuses– Reduce bonus smoothing reserve– Implement additional surrender charge

20

Analysis of Surplus (AOS)

21

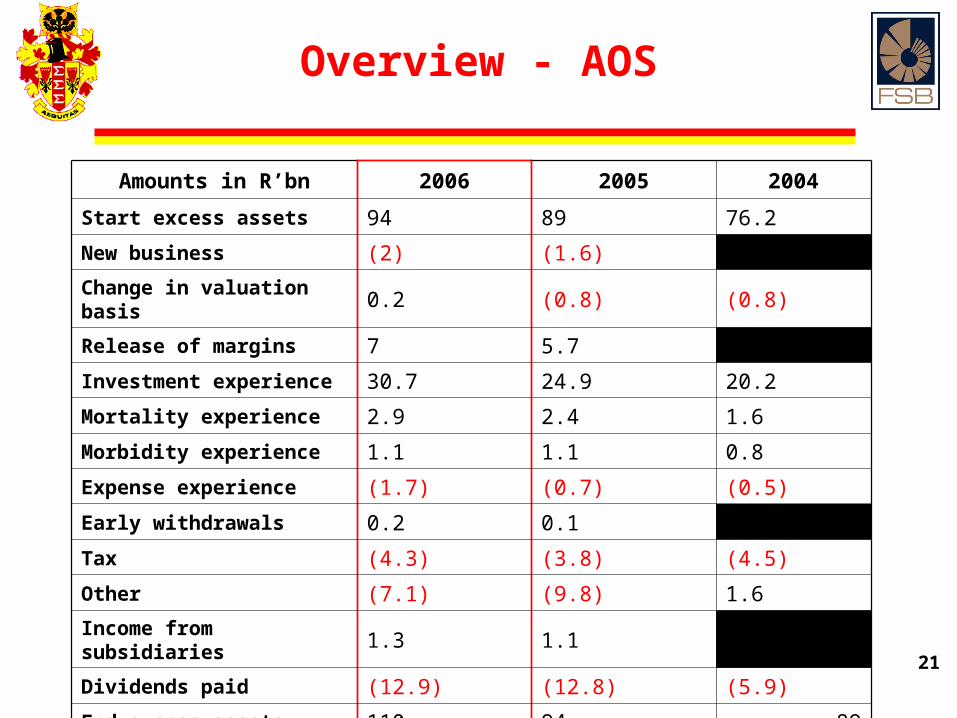

Overview - AOS

Amounts in R’bn 2006 2005 2004

Start excess assets 94 89 76.2

New business (2) (1.6)

Change in valuation basis 0.2 (0.8) (0.8)

Release of margins 7 5.7

Investment experience 30.7 24.9 20.2

Mortality experience 2.9 2.4 1.6

Morbidity experience 1.1 1.1 0.8

Expense experience (1.7) (0.7) (0.5)

Early withdrawals 0.2 0.1

Tax (4.3) (3.8) (4.5)

Other (7.1) (9.8) 1.6

Income from subsidiaries 1.3 1.1

Dividends paid (12.9) (12.8) (5.9)

End excess assets 110 94 89

22

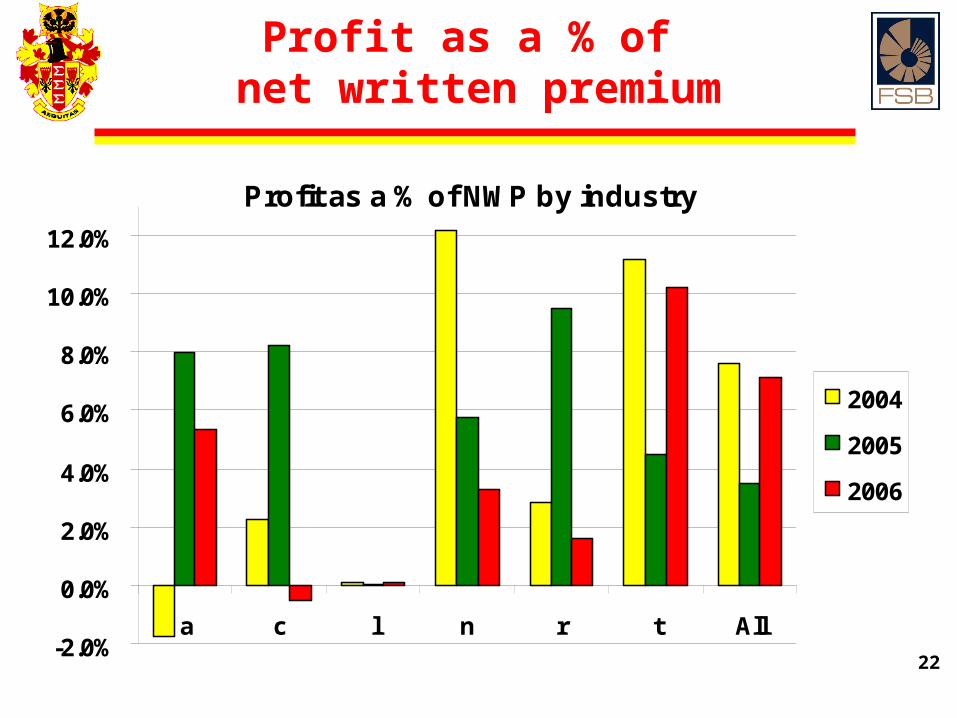

Profit as a % of net written premium

Profit as a % of NWP by industry

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

a c l n r t All

2004

2005

2006

23

Expenses

24

Split of expense losses

Split of expense losses between individual business, group business and shareholders

15% 13% 14%

5% 13% 3%

82%74%79%

0%

20%

40%

60%

80%

100%

2004 2005 2006

YearIndividual Business Group Business Shareholders

25

Expense inflation assumption

Individual Business

9.0% 9.5%

7.0% 7.0%

2.0%

5.0%

3.4% 3.9%

9.6%

7.2%

5.0%5.5% 5.1%

11.0%

4.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2002 2003 2004 2005 2006

Year

Ex

pe

ns

e In

fla

tio

n

Maximum Minimum Weighted Average

26

Actual expense inflation

Individual Business

9.9

2.8

10.7

5.1

12.9

5.2

13.5

6.3

0

2

4

6

8

10

12

14

16

Total Acquisition Expenses Total Operating Expenses

R'b

n

2003 2004 2005 2006

8%

21%

4%

79%3%

21%

27

Initial per policy expense assumption

Initial Expenses for Recurring Premium Policies (Individual Business)

With-profit annuities

With-profits

Without-profit annuities

Other

Market-related

Linked

R 600

R 900

R 1,200

R 1,500

R 1,800

R 2,100

R 2,400

R 2,700

R 3,000

2004 2005 2006

28

Actual initial expense(individual business)

Industry

Average Initial Expense

per new policy

Average Premium per new policy

2006Change

from 20052006

Change from 2005

Assistance business

R 309 101% R 837 -35%

Cell captives R 586 -25% R 263 -8%

Linked insurers R 7,736 -11% R 561,622 5%

Niche insurers R 105 49% R 441 75%

Typical insurers R 2,382 -7% R 9,358 -1%

All R 1,831 4% R 7,530 8%

29

Actual initial expense(individual business)

Industry

Initial expense as a % of new business net premium

2006 2005 2004

Assistance business 37% 12% 49%

Cell captives 223% 270% 54%

Linked insurers 1% 2% 1%

Niche insurers 24% 28% 9%

Typical insurers 25% 27% 27%

Total 24% 25% 25%

30

Actual initial expense(individual business)

Business Class

Initial expense as % of net premium

2006 2005

New Business Premium

s

Total Premium

s

New Business Premium

s

Total Premium

s

With-profit business

108% 12% 104% 11%

With-profit annuities

2% 2% 2% 2%

Without-profit annuities

2% 2% 2% 2%

Linked 5% 4% 5% 5%

Market-related 17% 9% 23% 14%

Other 74% 36% 68% 36%

All 24% 14% 24% 15%

31

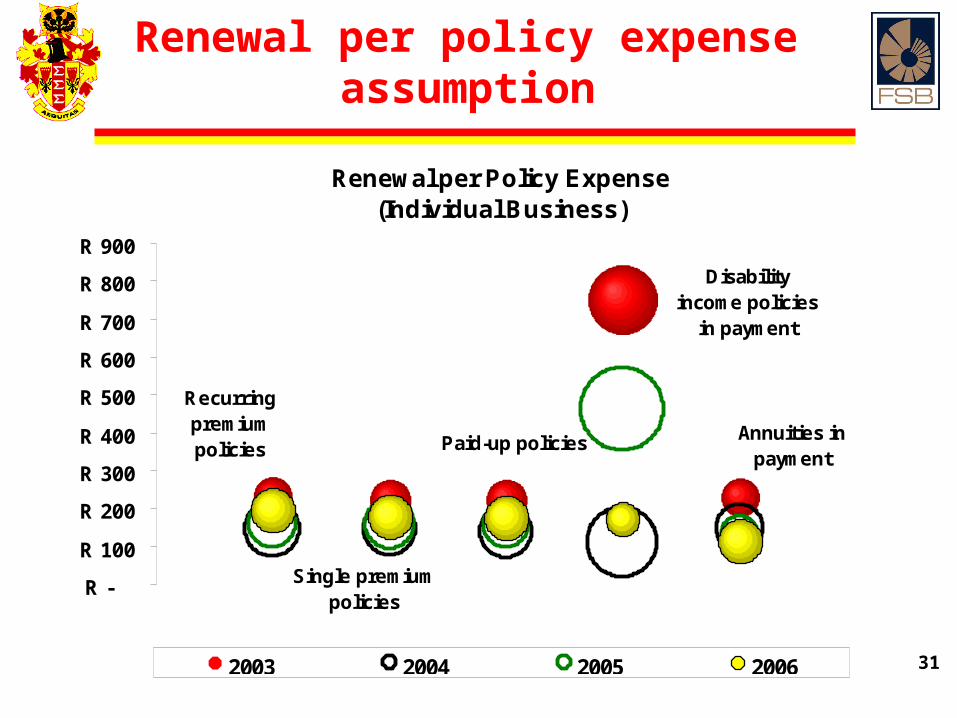

Renewal per policy expense assumption

Renewal per Policy Expense (Individual Business)

Recurring premium policies

Single premium policies

Paid-up policies

Disability income policies

in payment

Annuities in payment

R -

R 100

R 200

R 300

R 400

R 500

R 600

R 700

R 800

R 900

2003 2004 2005 2006

32

Actual operating expense(individual business)

IndustryAverage OperatingExpense per policy

Operating Expenses as % of

Total Net Premium

2006 2005 2006 2005

Assistance business

R 42 R 50 17% 16%

Cell captives R 40 R 31 5% 4%

Linked business R 303 R 302 0% 0%

Niche insurers R 22 R 20 7% 8%

Typical insurers R 255 R 220 7% 6%

Total R 226 R 199 6% 6%

33

Central Discount Rates

34

Assumed central discount rate

Individual Business

Linked MarketOther

Without-profit

annuities

With-profit annuities

With-profit business

5%

6%

7%

8%

9%

10%

11%

Ce

ntr

al D

isc

ou

nt

Ra

te

2006 2005

35

Observed investment yield

Individual BusinessWith-profit business Market

Without-profit annuities

Linked

With-profit annuities Other

0%

5%

10%

15%

20%

25%

30%

35%

Inv

es

tme

nt

Yie

ld

2006 2005

36

Cumulative distribution of assumed real returns

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

<0.5

%

<1.0

%

<1.5

%

<2.0

%

<2.5

%

<3.0

%

<3.5

%

<4.0

%

<4.5

%

<5.0

%

<5.5

%

<6.0

%

<6.5

%

<7.0

%

<7.5

%

<8.0

%

2006 2005

37

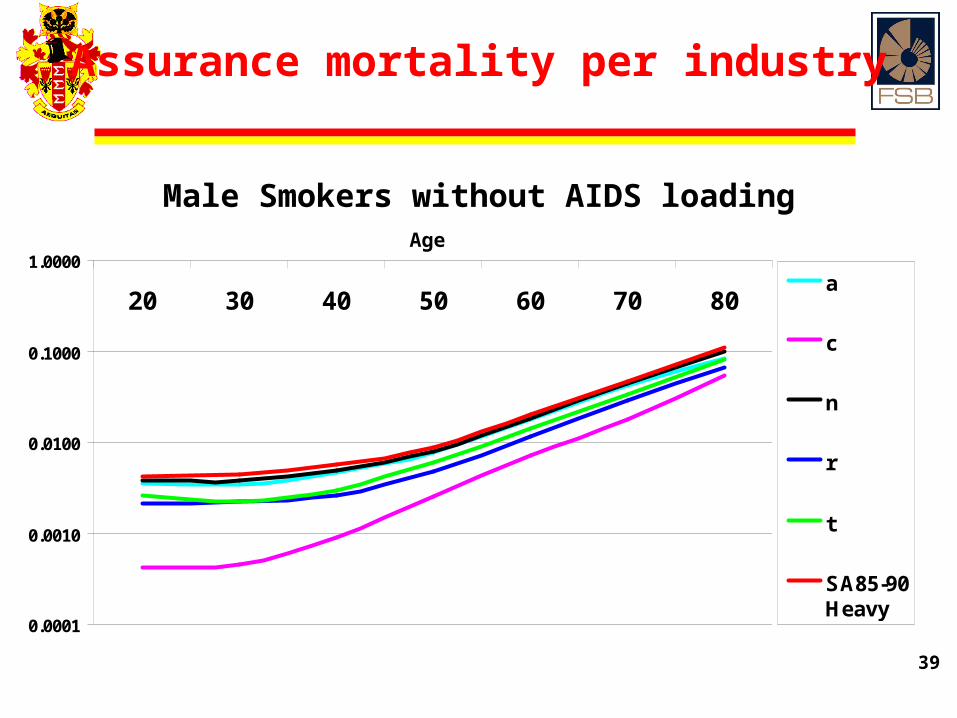

Mortality

38

Mortality

• In the graphed rates, we tried to determine representative mortality rates

• For assured lives we used SA85/90 ultimate 100% heavy to place weighted rates in perspective.

• For annuitants we used a(55) to put weighted average rates in perspective.

39

Assurance mortality per industry

Male Smokers without AIDS loading

0.0001

0.0010

0.0100

0.1000

1.0000

20 30 40 50 60 70 80

Age

a

c

n

r

t

SA85-90Heavy

40

Change in mortality for assured lives from 2005 to 2006

Smoker without AIDS loading

99%

100%

101%

102%

103%

104%

105%

106%

20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

Age

Male Female

41

AIDS loading comparison for 2005 and 2006

Mortality for Assured Lives Male Smoker

100%

110%

120%

130%

140%

150%

160%

25 30 35 40 45 50

Age

2005

2006

42

AIDS loading by industry

Mortality for Assured Lives Male Smoker

100%

120%

140%

160%

180%

200%

220%

240%

260%

280%

25 30 35 40 45 50

Age

Assistance

Niche

Reinsurers

Typical

43

Annuitant mortality by industry

Male Smoker

0.001

0.010

0.100

1.000

50 60 70 80Age a

c

r

t

a(55)

44

Change in mortality for annuitants from 2005 to 2006

93%

94%

95%

96%

97%

98%

99%

20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

Age

Male Female

45

Mortality: actual vs. expected

• For assurance products:

– Individual: 79% (79%) actual vs. expected

– Group: 90% (93%) actual vs. expected

• For annuity products:

– Individual: 114% (114%) actual

– Group: 87% (93%) actual vs. expected

* Figures in brackets represent 2005 assumptions

46

Morbidity: actual vs. expected

• For lump sum disability:– Individual: 59% (73%)

– Group: 80% (80%)

• For income disability:– Individual: 71% (43%)

– Group: 49% (81%)

* Figures in brackets represent 2005 assumptions

47

Withdrawal Rates

48

Assumed lapses per business class

Individual Business

0%

5%

10%

15%

20%

25%

30%

1st 2nd 3rd 1st 2nd 3rd 1st 2nd 3rd 1st 2nd 3rd

With-Profit business Linked Market related Other

As

su

me

d L

ap

se

Ra

te

2004 2005 2006

49

Assumed surrenders per business class

Individual Recurring Premium Policies

Min

Max

Weighted Avarage

0%

5%

10%

15%

20%

25%

2005 2006 2005 2006 2005 2006 2005 2006

With-Profitbusiness

Linked Market related Other

As

su

me

d S

urr

en

de

r R

ate

50

Assumed lapses per industry

Other Individual Business

0%5%

10%15%20%

25%30%

35%40%

a c n t

As

su

me

d L

ap

se

Ra

te

1st year 2nd year 3rd year

51

Observed withdrawals per industry

Individual Business

4%

9%

0%

10%

20%

30%

a c g l n All a c g l n All

Lapse rates Surrender rate

Ob

se

rve

d R

ate

s

2004 2005 2006

52

Thank you

Hantie van HeerdenHantie van Heerden(012) 422 2801(012) 422 2801

Elash MistryElash Mistry(012) 428 8164(012) 428 8164

www.fsb.co.za