Embed Size (px)

Citation preview

1

Emotions and Your Money

5 potentially costly mistakes and how to avoid them

2

SunAmerica is a sponsor of this seminar. As a sponsor, it has

contributed a fee or services to help defer seminar costs. During the

course of this seminar, your financial advisor may recommend

products from SunAmerica Mutual Funds. Neither SunAmerica nor its

representatives may provide individual investment recommendations

or advice. SunAmerica and the Broker Dealer that employs your

financial advisor may or may not be affiliated. Please see your

financial advisor for details.

3

Agenda

1. Understanding Emotions

2. Emotions and Investing—5 potentially costly mistakes and how to avoid them

3. Managing Emotions—the keys to staying calm in a turbulent market

4

Understanding Emotions

5

Many psychologists believe that people are “hard-wired” to make irrational, emotional decisions

7

One of the most common biases is

Loss Aversion

A psychological trait that makes losses seem twice as painful as the pleasure of gains.

It’s known as a Psychological Bias.

A tendency for the human brain to respond emotionally and make errors in judgment

when faced with uncertainty.

9

Let’s put this bias to the test Investment A

Offers a sure gain of $500Which investment would you choose in each of the following scenarios?

If you had $1,000 to invest, would you select:

Investment BOffers a 50% chance of either gaining $1,000 or gaining nothing

OR

Scenario 1

Investment A Offers a sure loss of $500

If you had $2,000 to invest, would you select:

Investment BOffers a 50% chance of either losing $1,000 or losing nothing

OR

Scenario 2

11

Investment A Offers a sure gain of $500

Investment BOffers a 50% chance of either gaining $1,000 or gaining nothing

OR

Investment A Offers a sure loss of $500

Investment BOffers a 50% chance of either losing $1,000 or losing nothing

OR

Surprising results

69% chose this answer, even though it’s the riskier choice

If you’re like most people, you chose:Scenario 1: Scenario 2:

84% chose this answer

Why did most people make this choice? Because Loss Aversion causes you to take

on more risk to avoid a sure loss!

12

Psychological biases combined with the emotions of investing can lead to costly mistakes

13

14

Emotions and Investing

5 potentially costly mistakes and how to avoid them

15

1. Impatience

• Investment Trap: Trading more frequently to try to quickly enhance returns

• Unintended Consequence: Potential for higher trading costs, more taxes and lower returns

• How to Avoid the Trap: Build and follow an investment plan that can help you stay invested

16

Many investors don’t have the patience to stay invested

How long do you think most equity fund investors have remained in their investment over the last 20 years?

Source: 2014 Quantitative Analysis of Investment Behavior, DALBAR.

Only 3.33 years!

17

Source: 2014 Quantitative Analysis of Investment Behavior, DALBAR. This study utilizes data from the Investment Company Institute and Standard & Poor ’s to compare investor behavior with the returns of the overall equity market. The Average Equity Fund Investor represents the aggregate action of all investors in equity mutual funds. Investor returns are determined using the change in total equity fund assets after excluding sales, redemptions and exchanges. This method of calculation captures realized and unrealized capital gains, dividends, interest, trading costs, sales charges, fees, expenses and any other costs. The S&P 500 Index is an unmanaged index of large-cap U.S. stocks that is considered to be representative of the U.S. equity market.

Moving in and out of the market can lead to lower returns

Investor behavior contributed to a performance gap of almost 7.5% per year over 30 years!

18

• Stay focused on strategy, not emotions

• Don’t get distracted by the short-term movement of the market

• Remain on track with your long-term goals

Following a plan can help control emotions

19

2. Overconfidence

• Investment Trap: Relying on “hot” investments to help boost your portfolio’s performance

• Unintended Consequence: Lower performance and increased risk of loss

• How to Avoid the Trap: Diversify and select investments based on research, not emotions or hot tips

20

Momentum can turn at any time

For example, the 2 best years in terms

of new money invested into the financial markets were followed by

the 2 worst years in terms of investment

returns!

Follow the crowd and you may end up buying at the top of the market, right before a significant decline!

Source: Investment Company Institute Fact Book 2014

21

What a difference a year makes—Last year’s winner may be this year’s loser!

Source: Callan Associates, 2014. International stocks are represented by the MSCI EAFE Index. Emerging Markets stocks are represented by the MSCI Emerging Markets Index. Asset class rankings are based on eight indices representing different asset classes from bonds to international stocks. Investments in non-US stocks are subject to additional risks including political and social instability, differing securities regulations and accounting standards and limited public information.

22

Diversification can help you generate more consistent returns in any market

Annual returns for select asset classes (1994-2013)

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS. The historical performance data for each index is provided to illustrate market trends. Indices are unmanaged and do not represent the performance of any specific fund or investment product. You cannot invest directly in the indices. Indices do not include expenses, fees, or sales charges that are typically associated with investments and would lower performance results. Equity investments are subject to market risk. Stocks with lower market capitalization generally involve greater risks. An investment in foreign securities may be subject to different and additional risks associated with, but not limited to: foreign currencies, securities regulation, investment disclosure, commissions, accounting, taxes, political or social instability, war, or expropriation. Bonds and bond funds are subject to interest rate risks. If held to maturity, bonds can provide a fixed rate of return and a fixed principal value, while bond funds will fluctuate in value and may be worth more or less than your original investment when redeemed. High yield bonds are subject to greater price swings than higher-rated bonds and payment of interest and principal is not assured. Source: Wilshire Compass, 2014.

24

3. Fear

• Investment Trap: Waiting too long to get back into the equity market

• Unintended Consequence: Inability to capitalize fully on a potential market rebound

• How to Avoid the Trap Consider easing back into equities with an automatic investing strategy like dollar cost averaging (DCA)

25

Fear may result in lost incomeResearch has shown that bull markets are front-loaded. Miss the first year of a rebound and you could lose out on NEARLY HALF of the average bull

market’s total gains!

Returns of the Dow Jones Industrial Average for every bull market since 1900

Note: Past performance is not a guarantee of future results. The Dow Jones Industrial Average is an index that consists of 30 of the largest and most widely held public companies in the U.S. Indices are unmanaged and cannot be invested in directly. Source: The Leuthold Group, 2014.

26

Take the guesswork out of timing the market

NOTE: Dollar cost averaging does not guarantee a profit or protect against a loss in declining markets. Dollar cost averaging involves continuous investment in securities regardless of fluctuating price levels. Before starting such a program, you should consider your ability to make purchases through periods of fluctuating price levels. This hypothetical illustration is for illustrative purposes only. It is only intended to show how dollar cost averaging works, not to reflect the performance of an actual investment.

Dollar cost averaging (DCA) allows you to increase your exposure to the growth potential of equities, while potentially reducing the average cost of your investment

In this example, more units at lower cost equals greater potential for future growth!

27

4. Panic

• Investment Trap: Selling equities in down markets and moving to cash for short-term safety

• Unintended Consequence: Potential shortfall in retirement income

• How to Avoid the Trap: Stay calm and use history as a guide to maintaining your long-term focus

28

The cost of selling stocks can be highStocks have historically outperformed bonds and cash over time.

In fact, stocks generated nearly $2 million more over the last 30 years!

Note: Past performance is not a guarantee of future results. Stocks are represented by the S&P 500 Index; bonds by the Barclays U.S. Aggregate Bond Index; and cash by the BofA Merrill Lynch US Treasury Bill 3-Month Index. Stocks are subject to significant price fluctuations and therefore an investor may have a gain or loss in principal when shares are sold. Government Bonds and Treasury Bills are subject to interest rate risk but are backed by the full faith and credit of the U.S. government if held to maturity. Indices are unmanaged and cannot be invested in directly. Source: Morningstar, 2014

29

Source: Wellington Management Company, 2014. This chart is for illustrative purposes only. It is based on the S&P 500 Index and is not intended to be indicative of the performance of any specific investment. Indices are unmanaged. An investment cannot be made directly in an index. Past performance is not a guarantee of future results.

The price of missing the best days of the equity market from 1993-2013

It can pay to stay invested in the market

30

History has been on your side Since 1926, stocks have consistently provided long-term growth through

wars, recessions, financial crises, natural disasters and more

Source: Ibbotson, 2014. Large company stocks are represented by the S&P 500 Index, an unmanaged index of large-cap stocks in the U.S. stock market. Stocks are often subject to significant price fluctuations and therefore an investor may have a gain or loss in principal when shares are sold. Higher volatility and greater risk may be associated with investing in stocks of small or emerging companies. This chart is for illustrative purposes only and is not representative of any specific investment. Performance for any specific investment is available from your investment representative. Past performance is not a guarantee of future results. Indices are unmanaged; you cannot invest directly in these indices.

31

5. Indecision

• Investor Behavior: Staying in cash to help protect your assets from market volatility

• Unintended Consequence: Loss of purchasing power over time

• How to Avoid the Trap Review your asset allocation mix

32

Don’t let indecision reduce your returnsCash alone is unlikely to generate the returns necessary to

achieve your retirement goals

Source: Ibbotson Associates, 2014. Stocks are represented by the S&P 500 Index; bonds by 20-Year U.S. Government Bonds; cash by 30-day U.S. Treasury Bills; and inflation by the Consumer Price Index. Stocks are often subject to significant price fluctuations and therefore an investor may have a gain or loss in principal when shares are sold. Government bonds and Treasury Bills are subject to interest rate risk but are backed by the full faith and credit of the U.S. government if held to maturity. The data assumes reinvestment of income and does not account for transaction costs. Federal income tax is calculated using the historical marginal and capital gains tax rates for a single taxpayer earning $110,000. No state income taxes are included. Indices are unmanaged and cannot be invested in directly. Past performance is not a guarantee of future results.

2013

-0.8%

0.4%

5.5%5.1%

10.1%

33

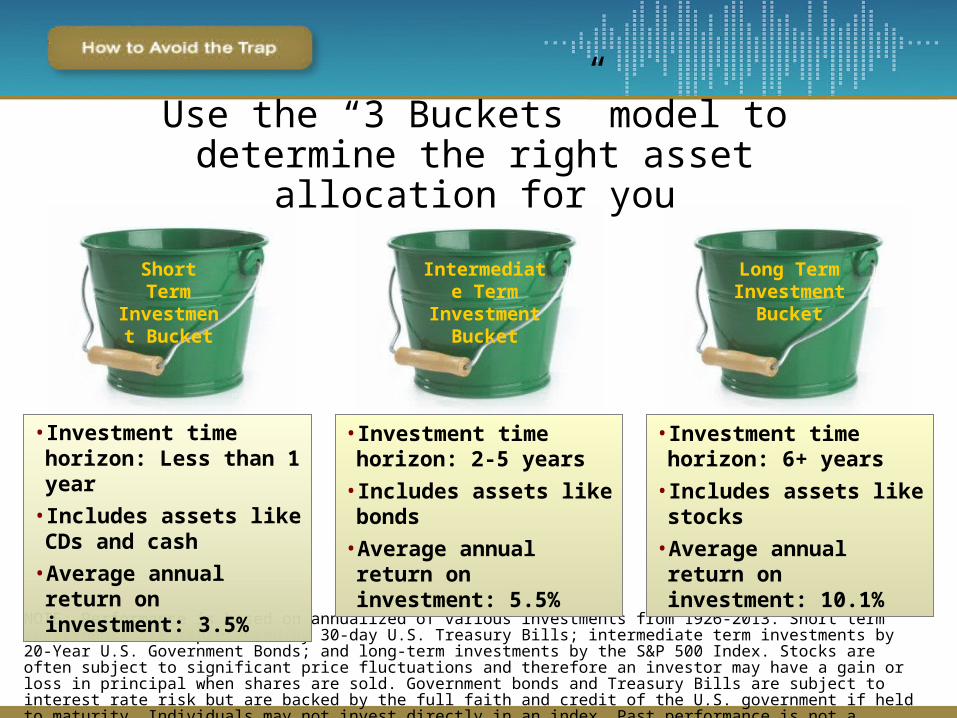

Short Term Investment

Bucket

Intermediate Term

Investment Bucket

Long Term Investment

Bucket

Use the “3 Buckets” model to determine the right asset allocation for you

NOTE: Performance is based on annualized of various investments from 1926-2013. Short term investments are represented by 30-day U.S. Treasury Bills; intermediate term investments by 20-Year U.S. Government Bonds; and long-term investments by the S&P 500 Index. Stocks are often subject to significant price fluctuations and therefore an investor may have a gain or loss in principal when shares are sold. Government bonds and Treasury Bills are subject to interest rate risk but are backed by the full faith and credit of the U.S. government if held to maturity. Individuals may not invest directly in an index. Past performance is not a guarantee of future results. Source: Ibbotson Associates, 2014.

• Investment time horizon: Less than 1 year

• Includes assets like CDs and cash

• Average annual return on investment: 3.5%

• Investment time horizon: 2-5 years

• Includes assets like bonds

• Average annual return on investment: 5.5%

• Investment time horizon: 6+ years

• Includes assets like stocks

• Average annual return on investment: 10.1%

34

Managing Emotions

35

The keys to staying calm in a turbulent market

• Knowledge: Understand how your investments will react to different market conditions.

• Strategy: Build a broadly diversified portfolio that may help you generate more consistent returns.

• Perspective: Work with a trusted financial advisor who has the expertise, experience and third-party objectivity to guide you through difficult times.

36

Understanding your investments

• Volatility and income • Key benefits• Potential pitfalls

Focus on three areas:

Remember, the more volatile your investment, the greater the range of emotions you may feel and the more likely it may be that you’ll make costly emotional mistakes

37

Stocks

Key Benefits• Growth potential• Diversification

opportunities• Possibility of

dividend income

Potential Pitfalls• No protection against

market uncertainty• No income

guarantees

Monthly returns of the S&P 500 Index (2003-2013)

Volatility and Income

When you invest in equities, your emotions and income may go up or

down with the market.

38

Bonds

Key Benefits• Fixed rate• Government bonds

backed by the U.S. government

• Certain types of bonds offer tax advantages

Potential Pitfalls• No potential for market

growth• No lifetime income

options

Monthly returns of the Barclays U.S. Aggregate Bond Index (2003-2013)

Volatility and Income

Bonds tend to be less volatile than stocks, so your emotions and income

may not fluctuate as much.

39

Cash

Key Benefits• Fixed rate• Returns guaranteed

by the FDIC (CDs) or the U.S. government (T-bills)

• Good for short-term investing

Potential Pitfall• No potential for

market growth• No lifetime income

options

Volatility and Income

Monthly returns of 91-day Treasury Bills (2003-2013)

Treasury Bills and other cash investments can help you stay calm, but they offer little income

and no potential for market growth.

40

Build a broadly diversified portfolio of traditional and alternative assets

Traditional• Stocks• Bonds• Cash• International • Small Cap

Traditional• Stocks• Bonds• Cash• International • Small Cap

Alternative• Commodities• Hedge funds• Managed futures• Currencies• Metals

Alternative• Commodities• Hedge funds• Managed futures• Currencies• Metals

Help control emotions and earn potentially higher, more consistent returns by combining asset classes, such as:

41

Six ways to manage emotions while diversifying your portfolio

Consider adding:

•Global allocation strategies that use a rules-based approach to get in and out of changing markets

•Dividend-yielding stocks for income and capital appreciation potential

•Managed portfolios that rely on the stock-picking expertise of premier money managers to deliver potential results

•Senior floating rate bank loans to help provide consistent income in any interest rate environment

•Multi-sector bond investments to seek total returns

•Alternative Investments that can help enhance returns and lower overall portfolio volatility.

Global Trends Fund: Futures and forward contracts are contractual agreements that involve the right to receive, or obligation to deliver, assets or money depending on the performance of one or more underlying assets, currencies or a market or economic index. The risks associated with the Fund’s use of futures contracts include the risk that: (i) changes in the price of a futures contract may not always track the changes in market value of the underlying reference asset; (ii) trading restrictions or limitations may be imposed by an exchange, and government regulations may restrict trading in futures contracts; and (iii) if the Fund has insufficient cash to meet margin requirements, the Fund may need to sell other investments, including at disadvantageous times. Forwards are not exchange-traded and therefore no clearinghouse or exchange stands ready to meet the obligations ofthe contracts. Thus, the Fund faces the risk that its counterparties may not perform their obligations. Forward contracts are also not regulated by the Commodity Futures Trading Commission (“CFTC”) and therefore the Fund will not receive any benefit of CFTC regulation when trading forwards. The Fund’s investment in futures may provide leveraged exposure which may cause the Fund to lose more than the amount it invested in those instruments. The Fund also has exposure to the commodities markets, which may subject the Fund to greater volatility than investments in traditional securities. The value of commodity futures instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or events affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investments that provide exposure to foreign markets involve special risks, such as currency fluctuations, differing financial reporting and regulatory standards, and economic and political instability. These risks are highlighted when the issuer is in an emerging market. Fixed income securities and currency and fixed income futures are subject to changes in their value when prevailing interest rates change. Adverse changes in currency exchange rates (relative to the U.S. dollar) may erode or reverse any potential gains from futures instruments that are tied to foreign instruments or currencies. Emerging market exposure generally has a higher level of currency risk. Credit risk (i.e., the risk that an issuer might not pay interest when due or repay principal at maturity of the obligation) could affect the value of the investments in the Fund’s portfolio exposed to fixed income securities. The Fund’s investments in repurchase agreements involve certain risks involving the default or insolvency of the seller and counterparty risk (i.e. the risk that the counterparty will not perform its obligations). Active trading of the Fund’s portfolio may result in high portfolio turnover and correspondingly greater brokerage commissions and other transaction costs, which will be borne directly by the Fund and which will affect the Fund’s performance. Active trading may also result in increased tax liability for Fund shareholders. Investors should note that the ability of the sub-adviser to successfully implement the Fund’s strategies, including the proprietary investment process used by the sub-adviser, will influence the performance of the Fund significantly.

Focused Dividend Strategy Portfolio and the International Dividend Strategy Fund: Investments in stocks are subject to risk, including the possible loss of principal. Stocks of small-cap and mid-cap companies are generally more volatile than, and not as readily marketable as those of larger companies, and may have less resources and a greater risk of business failure than do large companies. The Focused Dividend Strategy Portfolio and the International Dividend Strategy Fund each employ a disciplined strategy and will not deviate from their respective strategies (except to the extent necessary to comply with federal tax laws or other applicable laws). If either Fund is committed to a strategy that is unsuccessful, that Fund will not meet its investment goals. Because the Funds will not use certain techniques available to other mutual funds to reduce stock market exposure, the Funds may be more susceptible to general market declines than other mutual funds.

International Dividend Strategy Fund: Effective July 2, 2012, the name of the Fund was changed to the SunAmerica International Dividend Strategy Fund and certain changes were made to the Fund’s investment strategy and techniques. Prior to this date, the Fund was managed as an international equity fund employing a different strategy. Stocks of international companies are subject to additional risks including currency fluctuations, economic and political instability, greater market volatility, and limited liquidity. These risks can be greater in the case of emerging country securities. Preferred stock is subject to interest rate fluctuations as well as credit risk, which is the possibility that an issuer of preferred stock will fail to make its dividend payments. The market may fail to recognize the intrinsic value of particular dividend-paying stocks the Fund may hold.

Senior Floating Rate Fund and Strategic Bond Fund: Senior floating rate funds are not money market funds; their NAVs will fluctuate and may lose value. Investment in these loans involves certain risks, including, among others, risks of nonpayment of principal and interest; collateral impairment; non-diversification and borrower industry concentration; and lack of full liquidity. High yield debt instruments carry a greater default risk, and may be more volatile, less liquid, more difficult to value and more susceptible to adverse economic conditions or investor perceptions than other debt instruments.

Alternative Strategies Fund: The commodity and hedge fund-linked derivative instruments in which the Fund invests have substantial risks, including risk of loss of a significant portion of their principal value. Commodity and hedge fund-linked derivative instruments may be more volatile and less liquid than the underlying instruments and their value will be affected by the performance of the commodity markets or underlying hedge funds, as well as overall market movements and other factors. Commodity and hedge fund exposure may also subject the Fund to greater volatility than investing in traditional securities. The value of commodity-linked derivative instruments may be affected by commodity index volatility, changes in interest rates, or sectors affecting a particular industry or commodity, drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. The hedge funds comprising a hedge fund index invest in and may actively trade securities and other financial instruments using a variety of strategies and investment techniques that may involve significant risks. Managed futures involve going long or short in futures contracts and futures-related instruments. If the Fund’s investment advisor uses a future or other derivative instrument at the wrong time or judges market conditions incorrectly, use of such instruments may result in a significant loss to the Fund. The Fund could also experience losses if the prices of its futures or other derivative instruments were not properly correlated with other investments. Managed futures instruments and some other derivatives the Fund buys involve a degree of leverage. The Fund’s use of certain economically leveraged futures and other derivatives can result in a loss substantially greater than the amount invested in the futures or other derivatives. Certain futures and other derivatives have the potential for unlimited loss, regardless of the size of the initial investment. When the Fund uses futures and other derivatives for leverage, a shareholder’s investment in the Fund will tend to be more volatile, resulting in larger gains or losses in response to the fluctuating prices of the Fund’s investments. The Fund is not a complete investment program and should not be an investor’s sole investment because its performance is linked to the performance of highly volatile commodities and hedge funds. Investors should consider buying shares of the Fund only as part of an overall portfolio strategy that includes other asset classes, such as fixed income and equity investments. Investors in the Fund should be willing to assume greater risks of potentially significant short-term share price fluctuation because of the Fund’s investments in commodity-linked and hedge fund-linked instruments.

44

Knowledge Experience Responsiveness Availability Trust

Gain a new perspective on retirement income planning

Checklist for finding the right financial advisor

45

A good financial advisor can help you navigate the ups and downs of investing

46

Let’s work together to create a customized investment strategy that can

smooth out the emotional volatility of investing in today’s market!

Schedule a free investment review today!

47

Thank you for attending!

Funds distributed by AIG Capital Services, Inc., Harborside Financial Center, 3200 Plaza 5, Jersey City, NJ 07311-4992, 800-858-8850.

Investors should carefully consider a Fund’s investment objectives, risks, charges and expenses before investing. The

prospectus, containing this and other important information, can be obtained at the end of this presentation, by calling the

SunAmerica Sales Desk at 800-858-8850, ext. 6003, or by visiting our website at www.safunds.com. Read the prospectus

carefully before investing.

S5187PPT (6/14)