Embed Size (px)

Citation preview

1

Chapter 7 – Bond Concepts

• What are they?• Types and issuers

– Junk– Convertibles– Callables– Asset-backed

• Credit ratings

• Calculations– YTM– Price– Current yield– Tax impacts

• Relationships– Price– Term– Type

2

Types of Bonds

• Bond – a long-term promissory note– Pays a fixed amount of interest each period– At maturity, principal is repaid

• Types– Secured and Asset-backed securities– Debentures – unsecured– Subordinated debentures – “junior”– Junk or High-yield bonds– Municipals – non taxable interest

3

Bonds- Issuer Types

Mortgage-related $7.9T 40.6%

Corporations 4.4 22.6

US Treasuries 3.6 18.5

State & Local Gov’t 1.9 9.8

Other-asset backed 1.7 8.5

Total $19.5 100.0%

4

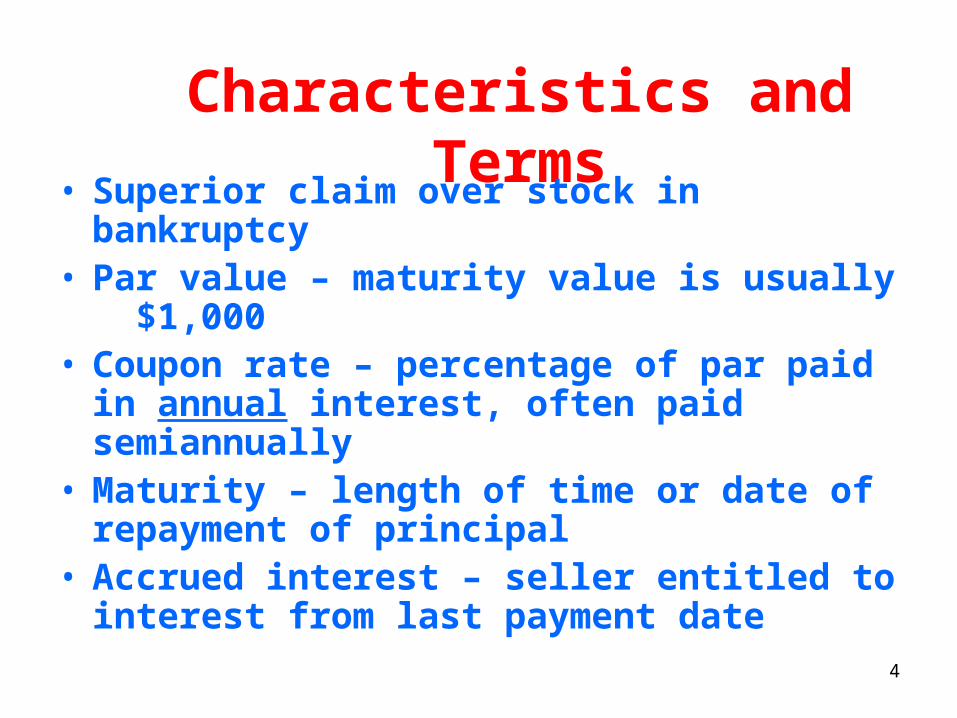

Characteristics and Terms• Superior claim over stock in bankruptcy• Par value – maturity value is usually $1,000• Coupon rate – percentage of par paid in

annual interest, often paid semiannually• Maturity – length of time or date of

repayment of principal• Accrued interest – seller entitled to interest

from last payment date

5

Capital Food Chain

• Secured creditors (OK if < assets)• General creditors:

– Debenture holders & unsecured creditors– Subordinated debenture holders

• Preferred stockholders• Common stockholders

6

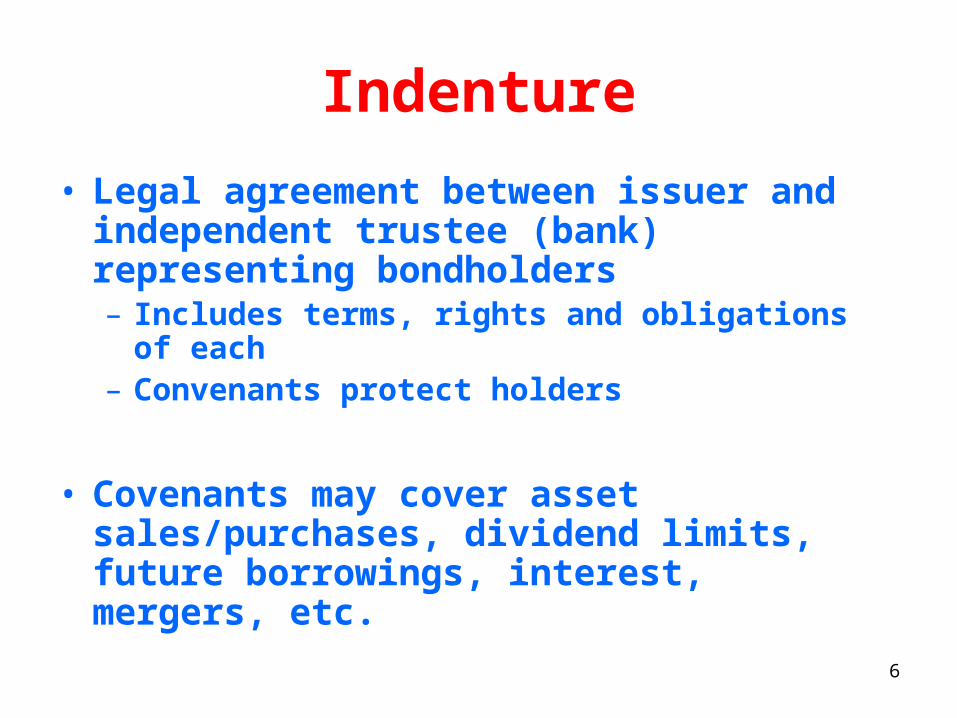

Indenture

• Legal agreement between issuer and independent trustee (bank) representing bondholders– Includes terms, rights and obligations of each– Convenants protect holders

• Covenants may cover asset sales/purchases, dividend limits, future borrowings, interest, mergers, etc.

7

Other Provisions

• Callability – issuer may redeem before maturity

• Tax shield – interest expense is tax deductible.

• At 34% tax, 8% becomes 5.28%

• Current yield (not YTM) = annual interest divided by market price

8

Convertible Securities

• Convertible into common stock at a fixed rate at bondholder’s option

• $1,000 bond convertible into 20 shares– Equal to $50/share (1,000/20)– Stock rises to $60, bond worth $1,200 (60 * 20)

• Offers upside potential but lower rate than on comparable nonconvertible securities

• Look at coupon and conversion ratio

9

Callable Bonds

• Redeemable at issuer’s option– Rates drop, bond called, new bonds issued– Investor forced to reinvest at lower rate

• Deferred calls and call premiums– Some not callable for say first five years– Premiums: say 105% of par in year 6, 104%

year 7 … par in year 11.

• Effect: callables pay a higher rate

10

Zero Coupon Bonds

• No interest paid until maturity• Sold at steep discount, say 60¢ on the $

– Discount represents unpaid interest

• Disadvantages: huge outflow at maturity; not callable; tax issues for holder

• Advantages: interest deferred; deductible by issuer; no reinvestment problem for holder

11

Asset-Backed Securities

• Bonds or notes owning pool of financial assets; outright asset sale– Credit cards, car loans, other assets

• Credit ratings: 90% rated AAA– Based on quality of assets, not issuer’s

credit

• Process called “securitization”• More details on my web page

12

Municipal Bonds

11

13

Credit Ratings

• Judgment of risk potential by rating firm– Standard & Poors, Moody’s, Fitch

• Factors: leverage, coverage, liquidity, profitability ratios; cash to debt, size, etc

• Range from AAA to D (in default)– BB and below called junk or speculative bonds– Did they predict Enron? No!

14

S & P Ratings

15

Junk Bonds

• AKA “high risk”, “non-investment grade”, “high yield” or “speculative”

• Low credit rating – rated BB and below– Higher risk, higher rates

• Fallen angels (crisis) or new, unproven firms

16

Quality SpreadsTen Year Maturity

Yield Spread Example

USTN 4.40

AAA 4.71% +31 GE & UPS

AA 4.91 51 Abbott Labs

A 5.25 85 McDonalds

BBB 5.70 145 GM

BB 7.90 350 Goodyear

17

Bond Valuation

• Value of any asset: present value of expected cash flows discounted to PV at market’s rate– Considering amount, timing, riskiness

• Market rate – the collective rate of return required by investors in that security– Rate based on risk; different rates for different

bonds

18

Valuation Steps

1. Estimate amount and timing of each cash flow– Most US bonds pay interest semiannually

2. Determine required rate of return – what’s available on similar bonds?

3. Calculate PV of each cash flow discounted at required or market rate

19

Yield to Maturity

• Rate holder earns if bond held to maturity• Price may be more or less than par value• One year bond pays 6%, market rate is 10%• Market price in very round numbers to get

10% ($100) is $960 • Holder receives $40 cap gain + $ 60 interest

20

6% bond,due 2 years;market rate = 10%. Semiannual pmts

Time CF 5% PVIF PV

6 mo $30 .9524 $28.57

12 mo 30 .9070 27.21

18 30 .8638 25.92

24 30 .8227 24.68

1,000 .8227 822.70

Market value is 92.908% of par or $929.08

21

Hitting the Right Keys

Market Price Yield to Maturity

N 4 N 4

PMT 30 PMT 30

FV 1000 * FV 1000

I/Y 5 PV 929.08 +/- *

CPT PV - 929.08 CPT I/Y = 5

5 * 2 = 10

* No +/- sign * Needs +/- sign

22

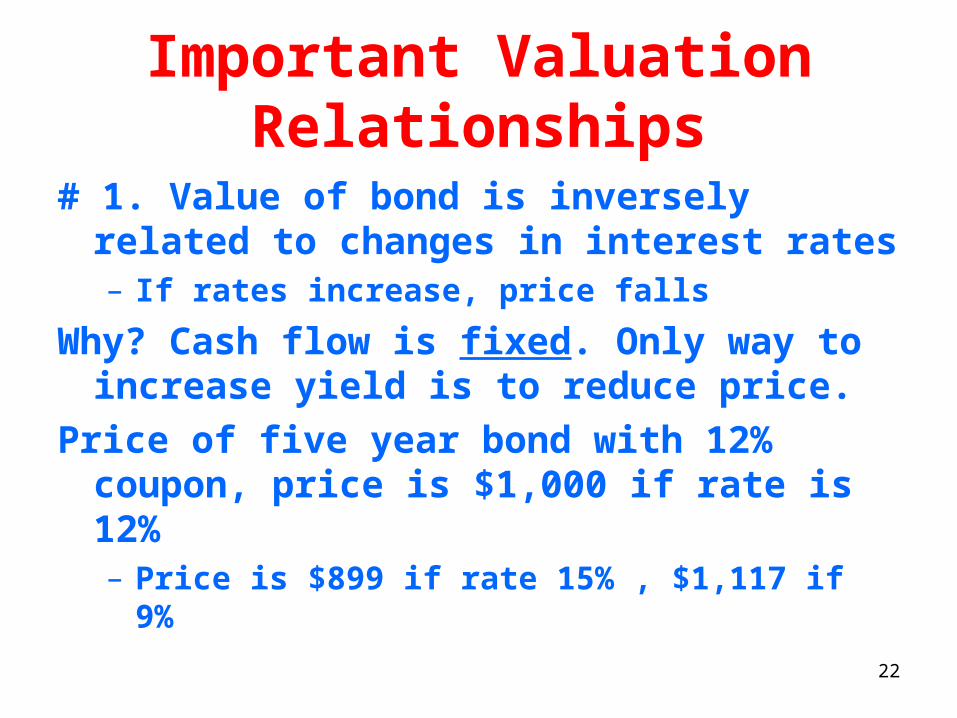

Important Valuation Relationships

# 1. Value of bond is inversely related to changes in interest rates– If rates increase, price falls

Why? Cash flow is fixed. Only way to increase yield is to reduce price.

Price of five year bond with 12% coupon, price is $1,000 if rate is 12%– Price is $899 if rate 15% , $1,117 if 9%

23

Relation #2

• If market rate equals coupon rate, bond sells at par

• If market rate exceeds coupon, bond sells for less than par (discount pond)

• If rate less than coupon sells above par (premium bond)

24

#2 Example

• The market value will be less than par if the investors’ required rate of return is above the coupon rate; converse is true

• Five Year, 12% Bond

Required Coupon Price

12% 12% $1,000

15 12 899

9 12 1,117

25

Interest Rate and Price Changes

26

Relationship #3

• Long-term bond subject to greater price risk than short-term bond

•

Price of 12% 5 and 10 year Bonds

Rate 5 year 10 year

9% $1,117 $1,192

12% 1,000 1,000

15% 899 849

27

5 and 10 Year Price Sensitivity

28

29

FinCoach Tips

• Be able to calculate market price and yield to maturity– (The return the investor would earn if he

bought the bond at the market price and held it to maturity = I/Y)

• Read questions carefully - look for– Coupon dollars, coupon rates, payment

frequency