Embed Size (px)

Citation preview

1

Chapter 14

Insurance

Chapter 14.1How Insurance Works

ObjectivesDescribe the role of insurance in managing risk;Explain basic insurance concepts; andGive guidelines for choosing insurance.

2

3

Managing Financial Risks

Categories of Risk:

1. Property Risk – property damaged, destroyed, or stolen

2. Personal Risks – Illness, injury, disability, or death3. Liability Risk – legal responsibility to pay someone

who has suffered an injury or loss caused by you

4

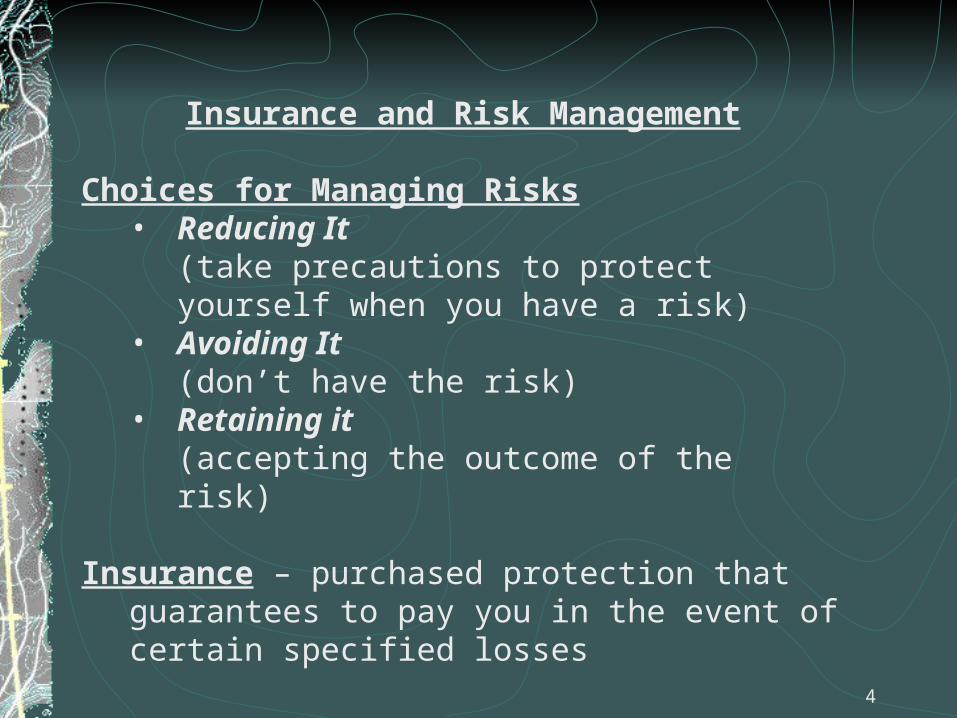

Insurance and Risk Management Choices for Managing Risks

• Reducing It (take precautions to protect yourself when you have a risk)

• Avoiding It (don’t have the risk)

• Retaining it (accepting the outcome of the risk)

Insurance – purchased protection that guarantees to pay

you in the event of certain specified losses

5

Transferring Risk – limiting any one person’s financial risk by sharing the risk among a large group of people.

• Many people pay into a common fund, few who actually do have losses draw on

that money

Two Basic Insurance Principles• Indemnity – restoring the insured person to the

financial position he or she was in before the loss occurred

• Insurable Interest – have a financial stake in the life or property being insured

Prioritizing Risk

• Consumers must decide which risks they can afford to retain and which they

cannot

6

Understanding Insurance Terms:

• Policy – written agreement between the policyholder – the consumer who purchases insurance – and the insurance company

o Rights and obligations stated is a legal contract

• Exclusions – specific risks not covered by a policy, such as normal wear and tear or

damage caused intentionally

• Endorsements (Riders) – attachments to a standard insurance policy that add or take

away coverage

7

Understanding Insurance Terms: Continued…

• Premiums – payments insured people make to the insurance company in exchange for coverage

• Claim – request for payment of a loss

• Deductible – a set amount the insured person must pay per loss before the insurer will

pay benefits

• Co-insurance – arrangement in which the insurance company and the insured person share the costs of claims after the deductible is met

8

Understanding Insurance Costs:

• Premiums provide money for operating expenses and payment of losses

• If losses are , then premiums or if losses are , then premiums are

• Rates are divided into rating territories:o cityo part of a cityo suburbo rural area

• Rates are also based on groups of people (example - males under age 25)

9

Choosing Insurance Four Basic Types of Insurance1. Auto Insurance – can provide payment for damage to

vehicles and other property and injuries to you and others

2. Home Insurance – protects you in case your possessions are stolen or damaged, even if the loss occurs away from home

3. Health Insurance – minimal coverage = medical emergencies / extensive coverage = everything from routine doctor visits to elective surgeries

• Can be individual policies• Group policies usually offered by employers

(lower costs)

10

Choosing Insurance Continued…

4. Life Insurance – pays benefits to designated people if the insured person dies

• Can be individual policies• Group policies usually offered by employers

(lower cost)

11

Sources of Insurance • Employers• Insurance Agent• Over the Phone• Through the Mail• Internet (low personal service but, lower costs)

Applying for Insurance

• Detailed questions.• Auto – need to know citations/accidents.• May have waiting periods for pre-existing medical

conditions

Chapter 14.2Auto Insurance

ObjectivesAnalyze the need for various types of auto insurance coverage;Compare the pros and cons of no-fault insurance;Describe factors that affect auto insurance rates; andExplain what to do in case of a traffic accident.

12

13

The Need for Auto Insurance:

• Due to high risks and statistics most states require that drivers carry certain minimum

auto insurance coverage

System of Auto Insurance: • Traditional Fault System – pays claims according to

each person’s degree of fault, or responsibility for causing the accidentso Expensive and lengthy court cases are often

required to determine fault

14

System of Auto Insurance: Continued…

• No-fault Insurance – no fault or blame is assigned in

the event of an accident o All parties involved collect from their own

insurance companieso Avoids lawsuits unless permanent damages.o May have higher rateso Medical conditions may not always be covered.o Strict monetary limit above which no payments are

madeo No incentive for bad drivers

15

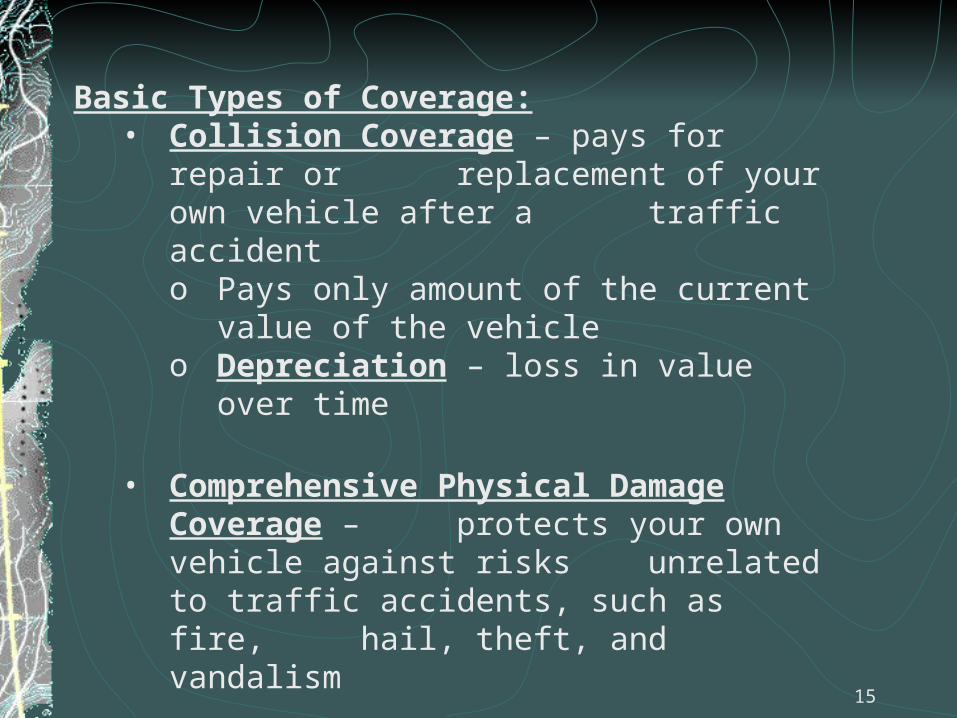

Basic Types of Coverage:• Collision Coverage – pays for repair or

replacement of your own vehicle after a traffic accidento Pays only amount of the current value of the

vehicleo Depreciation – loss in value over time

• Comprehensive Physical Damage Coverage – protects your own vehicle against

risks unrelated to traffic accidents, such as fire, hail, theft, and vandalism

16

Basic Types of Coverage: Continued…

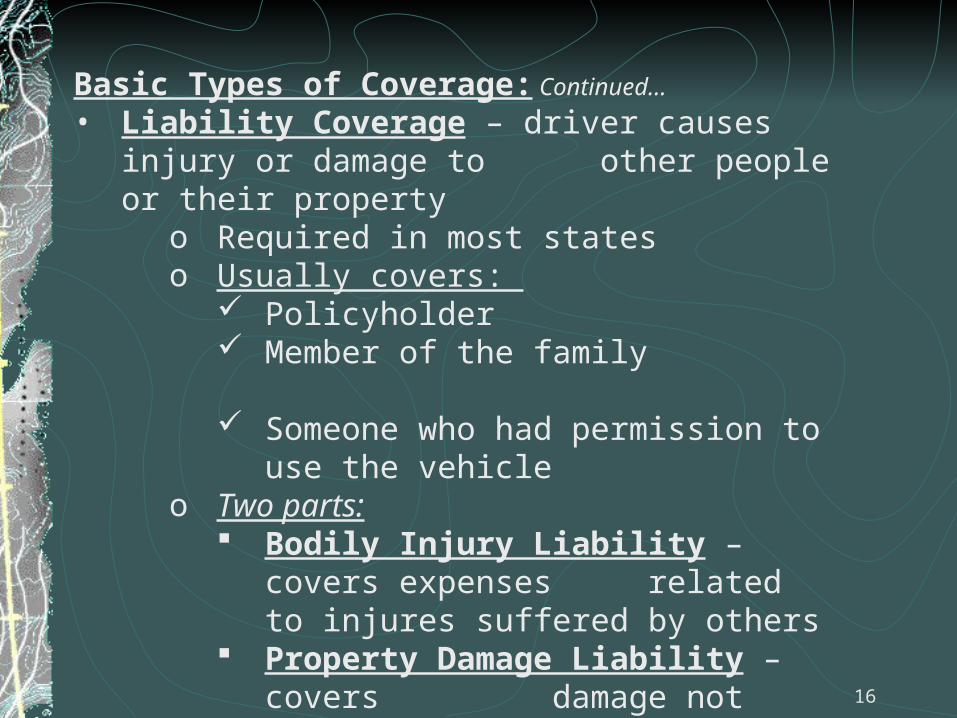

• Liability Coverage – driver causes injury or damage to other people or their property

o Required in most stateso Usually covers:

Policyholder Member of the family Someone who had permission to use the

vehicleo Two parts:

Bodily Injury Liability – covers expenses related to injures

suffered by others Property Damage Liability – covers

damage not only to vehicles, but also to buildings, trees, lawns, telephone poles, and so on (court cost, legal fees)

17

Basic Types of Coverage: Continued…

• Medical Payments Coverage – coverage would pay for immediate, short-term medical treatment

costs.o Immediate family o Relatives living with youo Passengers

• Personal Injury Protection (PIP) – covers medical

expenses for the policyholder and other passengers in the policyholder’s vehicle

o Some states provide at least partial coverage of injury related expenses such as

lost wages, rehabilitation, and home nursing care

18

Basic Types of Coverage: Continued…

• Uninsured / Underinsured Motorists Coverage – provides protection in situations such as:

o Hit-and-runo Uninsured driver at faulto Someone who doesn’t have enough insurance at

fault

• Other Types of Coverageo Emergency Road Serviceo Rental Caro New-car Coverageo Motorcycle Insurance

19

Assessing Your Coverage Needs:

1. How much liability coverage is needed?• 50/100/25• $50,000 for the injuries of any one person• $100,000 for all injured parties (two or more)• $25,000 for property damage

2. What is the minimum required coverage by state?• 100/300/50

3. Should you have collision and comprehensive coverage?• Some new cars require it• Could drop it later after car has depreciated

4. Consider the size deductible• $250 or $500

20

Auto Insurance Rates Factors:

• Age• Gender• Marital Status• Driving Record• Type and Age of Vehicle• Vehicle Use• Place of Residence• Number of Drivers on the Policy

21

Discounts:

• Good Grades• Good Driving Record• Seat Belts• Antitheft Devices• More Vehicles• More that One Type of Policy with the Company• Long-time Customers

Options for Problem DriversAssigned-risk pool – a person with a poor driving record who has been turned down 3 times for insurance is eligible.High-risk and can not find insurance on their own.Randomly assigned to an insurance company.Company must insure for at least 3 years, offer minimum liability, rates are 25-50% than other drivers.Pay premiums promptly and improve record.

22

In case of an AccidentSafety firstPull off side of road if possible, if serious leave vehicles where they areTurn on your flashersCall 911 for police and/or medicalStay on sceneDon’t discuss details of accidentExchange driver informationPolice report if needed

23

Filing a ClaimCall insurance company ASAPAdjuster will handle claimSubmit paperwork if needed

Choose your own repair facilitySeek appropriate medial careGet legal help if needed

24

Chapter 14.3Home Insurance

ObjectivesAnalyze the need for various types of home insurance coverage; Describe factors affecting home insurance rates; andExplain the purpose of a household inventory.

25

26

Home Insurance Needs

Two Types of Coverage:1. Property Coverage – insures against risks such as fire

and theft.• Personal Property – is property that can be

moved, such as furniture, appliances, clothing, and jewelry.

2. Liability Coverage – provides financial protection against certain losses caused to others.

Home Insurance is sometimes referred to as Homeowner’s

Policy, but also very important to renters.

27

Common Property Coverage:

• Basic Form (HO-1 = Home Owners-1) – covers the home and personal property against damage

from 11 perils. (see chart on pg. 370)

• Broad Form (HO-2) – covers more perils than HO-1. (see chart on pg. 370)

• Special Form (HO-3) – most common form, homeowners who want extensive protection.o Covers home, additional structures, and personal

property against almost any peril except earthquake, flood, war, and nuclear

accident.

28

Common Property Coverage: Continued…

• Tenants Form (HO-4) – contents form, covers the renters’ personal property only, perils are same as HO-2.

• Condominium Owners Form (HO-6) – developed for people who own an apartment or other housing

unit through the condominium form of ownership.o Covers only the parts of a structure that are the

individual owner’s responsibility.

29

Replacement versus Actual Cash Value:

• Actual Cash Value Coverage – only paying money for the current value of the

item, not what you paid for it or to get a new one

• Replacement Coverage – has higher premiums, owner will receive money for

replacing the item with comparable new ones.

30

Amount of Coverage:

• Insurers are recommended to insure their home for 100% of full replacement value

• Appraisal – is an estimate of value made by a qualified person

• Some insurance policies cover other structures such as a tool shed, guest house, or detached garage

• Personal property does not cover vehicles

• Check the value of your home and personal property every 3 years

31

Additional Coverage:

•Endorsements – attachments to the policy – can add coverage for specific hazards not normally

included in a standard home insurance package

•Flood insurance must be purchased as a separate insurance policy, not through an endorsement

32

Additional Coverage: Continued…

•You can only purchase flood insurance only if you live in a community that participates in the National Flood Insurance Program, which is a

partnership with insurance companies and Federal Emergency Management Agency (FEMA)

•Rates are based on the level of flood risk

•Earthquake insurance also requires a separate policy

•Premium rates are generally based on risk

33

Liability Coverage Claims:

1. Personal Liability Coverage – protects you from lawsuit arising from property damage or bodily injury.

2. Medical Payment Coverage – protects you, your family, and your guest from accident-related medical bills.

3. Physical Damage Coverage – minor damage that you or someone in your family causes to another property is paid for by physical damage coverage.

34

Umbrella Policy:

• Personal Liability Umbrella Policy – is a separate insurance policy that supplements the liability coverage provided by your home and auto insurance.

35

Home Insurance Rates:• Deductible – standard is $250 increasing to $500,

$1000 or more, this will lower premiums.• Local Firefighting Capability – insurance

companies look at factors such as the distance to the nearest fire station and hydrants, whether the local fire department is professional or volunteer, and the amount of equipment it has.

• Construction Materials – rates are lower for homes built of concrete or brick.

• Preventive Measures – Insurance companies offer discounts to homeowners who have alarm systems, smoke detectors, fire extinguishers, and deadbolt locks.

36

Filing a Claim:

1. Contact insurance company ASAP

2. Fill out claims form

3. Adjuster will inspect the damage and submit a report to the company

4. Insurance company will receive an estimate for the claim

5. Claim will be paid if covered by insurance company

37

Household Inventory:

• List all of the items and values that are damaged or stolen

• Household Inventory – detailed list of personal belongings (should be done prior to accident)

• Be Specific!

• Videotape or pictures

• Put in safe place outside the home

• Update periodically (6 months)

Chapter 14.4Health Insurance

ObjectivesAnalyze the need for various types of health insurance;Identify sources of health care benefits;Compare managed care and traditional health plans; andDescribe government-sponsored health care programs.

38

The Need for Health and InsuranceCan’t predict the future medical expenses.

39

Kinds of CoverageMedical Benefits – pays a large share of hospital and surgical expenses. (Routine doctor visits and prescription drugs)Major Medical Coverage – is for catastrophic illnesses such as a heart attack or cancer. (Long hospital stays and multiple surgeries)Dental Benefits – may cover services such as routine examinations, cleanings, x-rays, fillings and other repairs and oral surgery.

40

Kinds of Coverage ContinuedVision Benefits – May pay part of all of the cost of eye exams, glasses, and contact lenses.Disability Insurance – provides weekly or monthly payments to people who can’t work because of illness or accident. (Replaces part or all income)Long-term Care Insurance – designed to cover costs of an extended nursing home stay. (May include home health care and other forms of assistance.)

41

Exclusions from Coverage

Exclusions – are specific conditions not covered or services not paid for by health insurance. (Cosmetic Surgeries)If covered by more than one insurance, usually insurance companies will work together to coordinate their benefits, instead of pay twice on benefits.

42

Sources of CoverageGroup Policies – most people with health insurance are covered under group plans through their employers or other organizations.COBRA (Consolidated Omnibus Budget Reconciliation Act) – if you leave your employer and you are not covered for several months, you might be eligible

Keep previous groups coverage at own expense for 18 monthsIndividual policies – more expensive, enrolled separately, you choose benefitsGovernment programs – Medicare and Medicaid

43

Types of Health Care Plans

Fee-for-Service Plans – plan you’re charged a fee for each medical service you receive, and your insurance plan pays a portion of the fee

Widest range of choices for doctors and hospitalsResponsible for paperwork80/20 (insurance company pays 80% and you pay 20% of cost) after deductible is metOut-of-Pocket Maximum – upper limit you pay for deductibles during the year

44

Types of Health Care Plans Cont.

Managed Care Plans – designed to lower costs for both parties

Common Characteristics Network of providers Encourage wellness and preventive care Primary care physician must be chosen in some plans Yearly or monthly fee Co-payment – flat fee to visit the provider

HMO (Health Maintenance Organization) – least cost, most restrictions

45

Types of Health Care Plans Cont.POS (Point-Of-Service) – More freedom of choice than HMOPPO (Preferred Provider Organization) – group that work together to provide a discount

Like POS, but does not require a primary physician

46

Government Health Care Programs

Medicare – federal program, coverage for people over 65 and some under usually if they have a disability

Hospital insurance (Part A) – pays for hospitals and other expenses-home health care Medical insurance (Part B) – services not covered in Part A, such as doctor’s visit, lab tests, therapy care; pay monthly premiumMedigap policies – used to supplement Medicare; plan is same from state to state and company to company, but different premiums

Medicaid – federal and state program to help low-income familiesPrograms and benefits very from state to stateSome items are required

Social Security Disability BenefitsBegins after 6 months of being disabled and continues as long as the disability lasts

47

Workers’ Compensation

Insured against injury that occur on the job Plans vary depending on employer

Can not sue employer for injury

48

Chapter 14.5Life Insurance

ObjectivesAnalyze the need for various types of life insurance coverage;Distinguish between insurance and investment features of life insurance policies; and Explain factors to consider when purchasing life insurance.

49

Reasons for life insuranceLife insurance is insurance coverage that pays benefits to a designated person in the event of the insured’s deathCan pay for lost salary, funeral expenses, medical bills, other servicesCan guarantee a loanInvestment

50

Types of life insurance• 1. Term insurance-specific period of time

Level term-most common; premiums and death benefits remain sameDecreasing term- premiums fixed; death benefit gradually reducesRenewable term- guarantees the right to renew policy w/o physical-expertConvertible term- allows change from term to permanent- higher premiums

51

1. 2. Permanent insurance-coverage for lifetime (Cash Value Life Insurance)

Premium covers insurance and allows for a small investment (CASH VALUE)

If cancelled, you may be able to get some of the investment $ back

Can borrow from the funds without canceling the policy

Face value- amount paid if the insured dies

TYPES OF PERMANENT LIFE INSURANCE1. Whole life-coverage for entire life as long as policy is in

effect-premiums stay the same2. Limited payment life- Pay premiums to a certain age but

you are covered until death- higher premiums3. Universal life- guaranteed minimum rate of return for

investment and is flexible4. Variable life- you control how the cash value is invested-

no guaranteed cash value but usually a minimum face value; payment schedule varies

53

Deciding which type of insurance you need:

Term costs less than permanent ($200 vs. $2,000)Permanent builds cash value but rate of return might be hard to calculate

54

Policy Features and ProvisionsCan buy insurance from: employer, association, agent (read before signing)Premiums: annual, semi-annually, quarterly, monthlyGrace period: amount of time to pay the premium before the policy expires (consequences)Dividends: share of the company’s surplus; Policy is called participating policy and is issued by a mutual life insurance company (not guaranteed)Beneficiaries: person or group to whom death benefits will be paid To get benefits the beneficiary must make a claim and decide how they want the benefits to be paid

55

How much life insurance do you need?

It changes over your lifetimeTalk to insurance agent or use computer software

Social Security survivor benefits

Check your annual social security statement

After worker dies, benefits go to spouse or children

56

Factors affecting cost

Compare rates between several companies

Insured’s health: poor health = higher rate; Smokers= higher rate

Family health history: poor = higher rate

Occupation or hobbies: hazards affect premiums

Gender: life expectancy of women is longer = lower premiums

Age of insured: older you get, more expensive it is