Embed Size (px)

Citation preview

1

BSE and the Alberta Beef IndustryPresentation to

Canada/US Transportation Border Working Group

Calgary, AlbertaOctober 20, 2004

Nithi Govindasamy, P.Ag.

Policy Secretariat

Alberta Agriculture, Food and Rural Development

2

Outline

Size and Economic Importance of Cattle and Beef Industries

Impacts of BSE and border closures Contingency Planning Policy Responses The Future

3

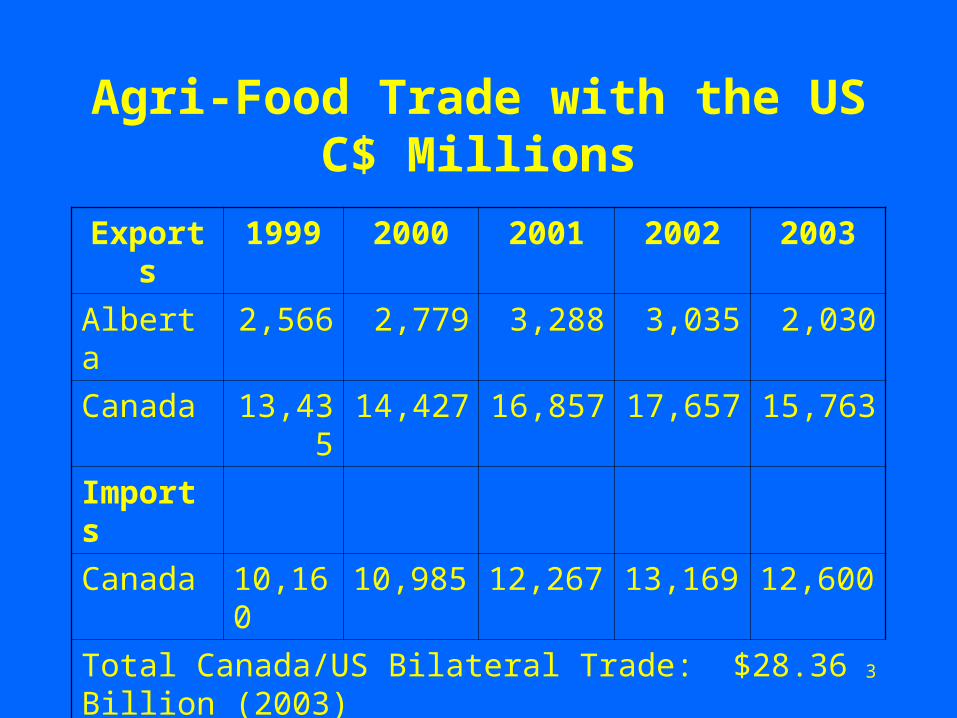

Agri-Food Trade with the USC$ Millions

Exports 1999 2000 2001 2002 2003

Alberta 2,566 2,779 3,288 3,035 2,030

Canada 13,435 14,427 16,857 17,657 15,763

Imports

Canada 10,160 10,985 12,267 13,169 12,600

Total Canada/US Bilateral Trade: $28.36 Billion (2003)

(Largest Bilateral Agricultural Trade Relationship in the world)

4

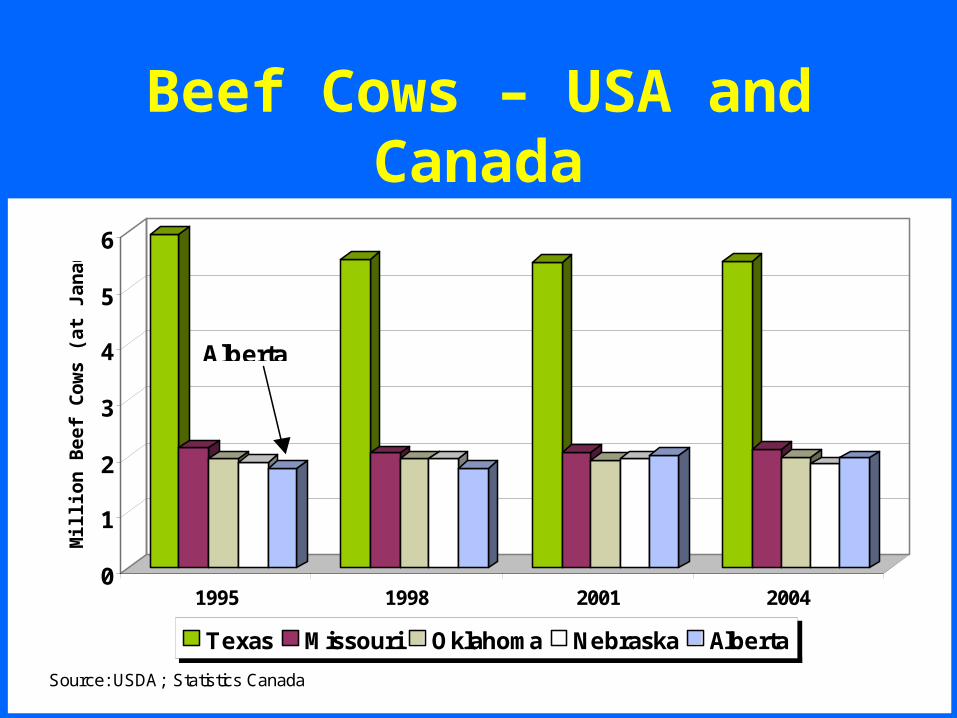

Beef Cows – USA and Canada

0

1

2

3

4

5

6

Mill

ion

Be

ef

Co

ws

(a

t J

an

au

ry 1

)

1995 1998 2001 2004

Texas Missouri Oklahoma Nebraska Alberta

Source: USDA; Statistics Canada

Alberta

5

North American Cattle Numbers

Jan 2004 Jan 2003 change

Canada – total

14.7 mil 13.5 mil +1.2 mil

US - total 94.9 mil 96.1 mil -1.2 mil

NA total 109.6 mil 109.6 mil No change

6

CanadaWhat is the 2004 imbalance?

Supply – 3.6 million fed cattle– 820,000 non fed animals– 4.42 million total marketings

2004 kill projections– 3.31 million fed cattle

• 290,000 head carryover (8%)– 500,000 non-fed cattle

• 320,000 head surplus (40%)

For cull animals, capacity has been reduced because of inability to kill OTM and UTM in the same plant. Has helped fed capacity.

7

SIZE OF INDUSTRY (2002) Cattle and calves in Alberta: 5.2 million

head (Canada: 13.4 million head) (39%). Cattle slaughtered in Alberta: 2.34

million head. Federally inspected: 2.34 million head. In 2003 cattle slaughter in Alberta was

about 2.08 million head – down 11% from 2002.

8

Size of Industry (cont’d)

Provincially inspected: 30,724 head (less than 1.5% of total).

Alberta feeds over 2.4 million cattle with total beef production of over 800,000 tonnes.

9

Size of Industry (cont’d)

Alberta’s beef production: – 13% sold in Alberta; – 15% to Quebec; – 30% to other Provinces; – 32% to US;– 9% to other countries.

71% of all Canadian cattle fed 68% of total Canadian slaughter

10

Size of Industry (cont’d)

Farm cash receipts (FCR) in Alberta: $8.23 billion (includes program payments).

Cattle and calves accounted for $3.89 billion or 47.3% of total FCR. Largest single agricultural sector.

Meat packing is Alberta’s second largest manufacturing industry.

11

Size of Industry (cont’d)

Value of Alberta’s cattle and beef exports to all countries: $2.27 billion.

Value of Alberta’s cattle and beef exports to US: $1.93 billion (85%).

Alberta shipped over half a million cattle to the US.

12

Canada/USC$ Millions

Cattle 1999 2000 2001 2002 2003

Exports 1,068 1,127 1,655 1,821 596

Imports 158 265 238 77 38

Beef

Exports 1,454 1,512 1,770 1,809 1,241

Imports 335 336 347 350 352

Total Exports 2,522 2,639 3,425 3,630 1,835

Total Imports 493 631 585 427 390

13

Alberta Trade in Cattle and BeefC$ Millions (Exports to the US)

Exports 1999 2000 2001 2002 2003

Cattle 461 510 712 634 196

Beef 1,074 1,115 1,218 1,298 909

Total 1,535 1,625 2,030 1,932 1,105

14

US Beef Exports in 2002Top 5 Markets (C$ Millions)

Japan 1,531 (34%)

Mexico 1,038

South Korea 999

Canada 361

Russia 90

% of Total 90%

Total All Countries 4,466

15

Canada Beef Exports in 2002Top 5 Markets (C$ Million)

United States 1,809 (82.5%)

Mexico 199

Japan 81

South Korea 50

Taiwan 20

% of Total 98.5%

Total All Countries 2,192

16

Economic Impacts BSE incident reduced 2003 cattle and beef

export revenue by about $1 billion for Alberta and $2 billion for Canada.

Declines in farm cash receipts estimated at $1.38 billion in Alberta ($2.1 billion for Canada).

Receipts for cattle alone declined by $1.32 billion in Alberta and $2.52 billion in Canada.

Average income loss estimated at $20,000 per farm family.

17

Economic Impacts (cont’d)

Estimated loss in equity to the cow calf sector: $3 billion

Estimated decline of $ 5.7 billion in total output for Canadian economy,$ 1 billion decline in labour income and loss of 75,000 jobs.

Normal 7 to 8 cent per lb. spread for fed cattle has averaged 34 cents per lb. under the US price since January, 2004

18

Source: Alberta Agriculture, Food and Rural Development, Strategic Information Services

19

20

Contingency and IndustryAdjustment Strategies (CCA)

Increased slaughter of Canadian cattle with a high priority to increase Canadian processing capacity.

Development of a delayed marketing strategy.

Alternative tax strategies. Cash advances, loan guarantees and debt

restructuring.

21

Contingency and Industry (cont’d)

Increased Canadian beef usage and export market diversification.

Increased surveillance and slaughter of cattle born prior to the 1997 feed ban.

Continued pursuit of all avenues to restore live cattle export trade.

22

Surveillance

6,400 cattle tested up to early October, 2004 (all negative).

Target: 8,000 (2004)

30,000 (2005 and beyond)

23

Access to the US

August 8th, 2003 US – announcement of partial re-opening of border: boneless beef UTM; liver; tallow.

August 15th, 2003 – product list amended to include trimmings; plant segregations allowed (UTM/OTM).

Sept. 4th, 2003 – first shipments begin. Nov 4th, 2003 – rulemaking process begins.

24

Access to the US (cont’d)

December 23rd, 2003 – discovery of US BSE. Jan. 5th, 2004 – first comment period for Rule

ends. Jan. 5th to March 6th, 2004 – Rule making

suspended. March 7th, 2004 – comment period re-opened

for one month. Includes consideration for OTM meat.

April 7th, 2004 – comment period ends.

25

Access to the US (cont’d)

April 19th, 2004 – USDA amends product entry list to include bone-in beef, ground beef, processed beef products.

April 21st, 2004 – RCALF court challenge.

May 6th, 2004 – injunction granted. Product list amended (August 15th list now in operation).

26

Canadian Policy Responses

Ruminant to ruminant feed ban in effect since 1997.

Removal of SRMs from food chain. Enhanced surveillance. Changes to feed ban (removal of SRMs

from feed) -- scope and implementation to be determined.

27

Canadian Policy Responses (cont’d)

Measured, consistent with known available science.

Need to be in harmony with US policy changes.

Trade considerations have been the main driver.

Not necessarily irrational.

28

Canadian Policy Responses (cont’d)

Somewhat haphazard due to uncertainty of US actions.

Support programs exceed $1.5 billion. Supplementary import permits

restricted.

29

International Panel Recommendations to US

Recognized integrated nature of NA industry.

Case of BSE in US cannot be considered in isolation.

North American BSE Task Force – consistent and scientifically valid policy development and implementation.

30

International Panel (cont’d)

Limitations of NA cattle Identification System.

Recommended SRM removal from food and feed chain.

Significant enhancement of surveillance.

Testing of all cattle for human consumption unjustified in terms of protecting human and animal health.

31

International Panel (cont’d)

US should demonstrate leadership in trade matters by adopting trade policies in accordance with international standards and discontinuing irrational trade barriers.

32

Conclusions

One incident of BSE in Canada was sufficient to close all borders and create havoc in the industry.

Importance of maintaining and enhancing close relationship with the US highlighted.

Close integration and interdependence of NA cattle and beef industries.

33

Conclusions (cont’d)

Export dependency of Canadian industry.

Urgent need to review, revise OIE guidelines to make them more practical and take into account trade realities while adequately safeguarding human and animal health.

34

Conclusions (cont’d)

Guidelines need to become rules with compliance mechanisms.

NA harmonization of policies and regulations.

Strong public and government support for industry.

35

Conclusions (cont’d)

Canada and US should move quickly to complete and implement remaining policy measures necessary to eradicate disease and reassure consumers and trading partners.

Additional policy measures, however, must be guided by sound science and should not be an overreaction to closed markets.

36

Conclusions (cont’d)

Need for coherent, coordinated science-based policy undertakings.

Canada needs to continue applying pressure to re-open US market and other offshore markets.

To the extent possible, issue needs to be depoliticized.

37

Conclusions (cont’d)

Rational trade policies, based on science, not on politics or protectionism.

Need for multilaterally accepted international rules of management and trade so as to avert problems experienced with BSE.