Embed Size (px)

Citation preview

A New Perspective: The Consumer Electronics Buying Process

February 26, 2008

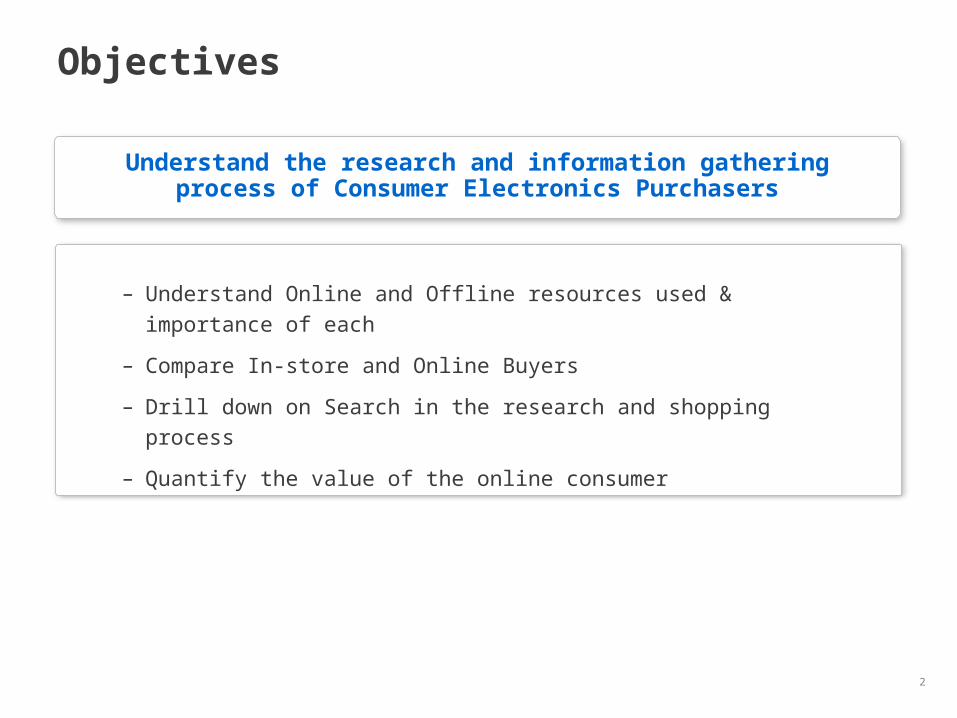

– Understand Online and Offline resources used & importance of each

– Compare In-store and Online Buyers

– Drill down on Search in the research and shopping process

– Quantify the value of the online consumer

Understand the research and information gathering process of Consumer Electronics Purchasers

Objectives

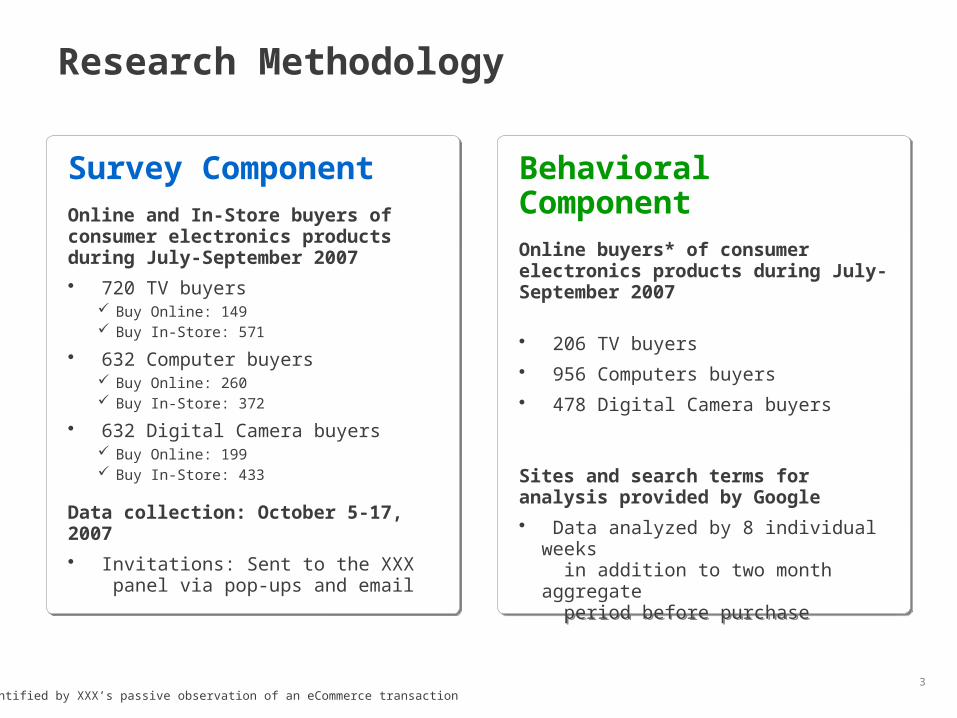

Survey ComponentOnline and In-Store buyers of consumer electronics products during July-September 2007

• 720 TV buyers Buy Online: 149 Buy In-Store: 571

• 632 Computer buyers Buy Online: 260 Buy In-Store: 372

• 632 Digital Camera buyers Buy Online: 199 Buy In-Store: 433

Data collection: October 5-17, 2007

• Invitations: Sent to the XXX panel via pop-ups and email

Survey ComponentOnline and In-Store buyers of consumer electronics products during July-September 2007

• 720 TV buyers Buy Online: 149 Buy In-Store: 571

• 632 Computer buyers Buy Online: 260 Buy In-Store: 372

• 632 Digital Camera buyers Buy Online: 199 Buy In-Store: 433

Data collection: October 5-17, 2007

• Invitations: Sent to the XXX panel via pop-ups and email

Behavioral ComponentOnline buyers* of consumer electronics products during July-September 2007

• 206 TV buyers

• 956 Computers buyers

• 478 Digital Camera buyers

Sites and search terms for analysis provided by Google

• Data analyzed by 8 individual weeks in addition to two month aggregate period before purchase

Behavioral ComponentOnline buyers* of consumer electronics products during July-September 2007

• 206 TV buyers

• 956 Computers buyers

• 478 Digital Camera buyers

Sites and search terms for analysis provided by Google

• Data analyzed by 8 individual weeks in addition to two month aggregate period before purchase

Research Methodology

* Identified by XXX’s passive observation of an eCommerce transaction

1 Online resources are critically important to the CE buyer

2 Buyers rely on Search throughout the shopping funnel

3 Online consumers are more valuable customers

Key Findings

Online Research is Criticalto the Consumer Electronics

Buying Process

Q11. How familiar were you with the brand before you bought it or before you started researching?. Base: Buy Online – 597, Buy In-Store – 1,344.

Q5a. Which statement below best describes your mindset when you first considered a purchase? Base: Buy Online – 572, Buy In-Store – 1,200.

Before purchase, shoppers are familiar with the major Consumer Electronics brands, but unsure of what to buy

Source: CE Purchasing Process Study November 2007

65% 68%

0%

20%

40%

60%

80%

Uncertain About What to BuyFamiliar with the Brand that I Ended Up Buying

In-Store buyers

Online buyers

61% 58%

0%

20%

40%

60%

80%

Before purchasing...

86%Online purchasers

60%In-Store purchasers

Q1. Which of the following sources did you use in your shopping and information gathering process to get info about your purchase Please check all that apply. Base: Buy Online - 608 ; Buy In-Store – 1,376. Online purchasers (86%), significantly > than In-Store purchasers (60%) @ 95% confidence,

Both In-Store and Online CE shoppers rely on online research

Research Their Purchase Online

“Online Research is Important to My

Purchase Decision”

Online Buyer89%

In-Store Buyer81%

Source: CE Purchasing Process Study November 2007

* For the 8 week period before purchase. Includes Retail sites (Consumer Electronic and Mass Merchandiser retailers), Manufacturer sites, and technology information, review, and discussion sites.

CE buyers invest hours in online research before purchase

3.7 hrs 1.9 hrs 2.3 hrs

Average 2.6 hours*of Online Research

Time spent on CE research was slightly less than IM’ing and more than reading online news and visiting auction and gaming sites

Source: CE Purchasing Process Study November 2007

3.7 hrs

* For the 8 week period before purchase. Retailers includes Consumer Electronic and Mass Merchandiser sites Other includes technology information, review, and discussion sites.

Focus of research varies by product

1.9 hrs 2.3 hrs

Manufacturer Sites 1.8hrs 0.2hrs 0.1hrs

Retailer Sites 1.1 1.6 1.9

Other Sites 0.8 0.1 0.3

Source: CE Purchasing Process Study November 2007

“Helped Me Learn More about a Brand/Product”

48% 49%46%

43%46%47%

0%

10%

20%

30%

40%

50%

60%

70%

SearchEngines

ManufacturerWebsites

RetailWebsites

Online Buyer In-Store Buyer

Q3. Now we would like to know how each of the following information sources helped you in your shopping and information gathering process for your “TV”, “computer” or “digital camera” purchase. Please indicate the statements you feel apply to each source of information. (You may choose more than one statement for each source of information if you feel it applies.) Base: Base: Buy Online – 240-300 ; Buy In-Store – 345-450. Online Buyer Manufacturer Websites (60%), significantly > @ 90% confidence for “Helped Me Decide What to Buy”.

In-Store Buyer Search (24%), significantly > than Print (18%) at 90% confidence.

Source: CE Purchasing Process Study, November 2007

“Helped Me Decide What to Buy”

45%

60%

50% 50%53%

50%

0%

10%

20%

30%

40%

50%

60%

70%

SearchEngines

ManufacturerWebsites

RetailWebsites

Online Buyer In-Store Buyer

Search engines, manufacturer sites and retail sites lead to the final purchase decision

“Introduced Me to a Brand/Product I Didn’t Know About”

Online Ads are at least as effective as traditional ads…At the top of the funnel…

25%24%

21%

24%

20%

23%

18%

21%21%

24%

0%

5%

10%

15%

20%

25%

30%

Search Online Ad TV Ad Radio Ad Print Ad

Online Buyer In-Store Buyer

Q3c. Please indicate how each of the following was helpful to you, if at all, in your shopping and information gathering process. (You may choose more than one of the ways shown in the top row for each if you feel it applies.). Base: Prompted by ad

to get more information, n = 57 – 349. In-Store Buyer Search (24%), significantly > than Print (18%) @ 90% confidence.

In-Store Buyer Search (24%), significantly > than Print (18%) at 90% confidence.

Source: CE Purchasing Process Study, November 2007

…and even more helpful through to the final CE purchase

Q3c. Please indicate how each of the following was helpful to you, if at all, in your shopping and information gathering process. (You may choose more than one of the ways shown in the top row for each if you feel it applies.)

Base: Prompted by ad to get more information, n = 57 – 349. Online Buyer Search (49%), significantly > than TV (29%) and Radio (31%) at 95%

confidence and Online Ad (40%) and Print Ad (38%) @ 90% confidence. In-Store Buyer Search (45%), significantly > than TV (33%) and Print (33%) @ 95% confidence. Online Buyer Online Ad (40%), significantly > than TV (29%) @ 90% confidence. Online Research, significantly more important to Online buyer (89%) than In-Store buyer (81%) @ 95% confidence.

“Helped Me Decide What to Buy”

49%

40%

29%31%

38%

33% 33%34%

39%

45%

0%

10%

20%

30%

40%

50%

60%

Search Online Ad TV Ad Radio Ad Print Ad

Online Buyer In-Store Buyer

Source: CE Purchasing Process Study, November 2007

69%

49%

Seeing the Product In-PersonIs Very Important in Influencing My Purchase*

Buy In-Store

Buy Online

Still, seeing the product in-person is very important before a purchase

Q6. Please think about your last experience in a retail store (e.g. Best Buy, Circuit City or Wal-Mart) before you purchased your “TV”, “computer” or “digital camera”. Using a scale from 1 to 5, where 1 is “strongly agree” and 5 is “strongly disagree”, indicate the extent to which you agree or disagree which each of the following statements regarding your last visit.Base: Respondents who checked Seeing the product in retail stores (e.g. Best Buy, Circuit City, or Wal-Mart); Buy Online – 244, Buy In-Store - 881.Buy In-Store (69%) significant > than Buy Online (49%) @ 95% confidence.

* “Strongly agree” with this statement

Source: CE Purchasing Process Study, November 2007

20% 30% 40% 50% 60% 70%

In-Store Buyer Online Buyer

Any online resource: 25%Any offline resource: 22%

Any online resource: 22%Any offline resource: 22%

Online resources are as effective as offline resources at driving CE customers into the store

Prompted Me To Visit A Retail Store

Q3. Now we would like to know how each of the following information sources helped you in your shopping and information gathering process for your < “TV”, “computer” or “digital camera” > purchase. Please indicate the statements you feel apply to each source of information. (You may choose more than one statement for each source of information if you feel it applies.) Base: Used any online or offline source: Buy Online – 519/395 respectively, Buy In-Store – 799/1,074 respectively.

Source: CE Purchasing Process Study, November 2007

Search is Pervasive ThroughoutThe Buying Process

16

Your customers use Search throughout theshopping funnel

Awareness

Consideration

Purchase

When did you use Search during your shopping and information gathering process?

Online Buyers 29%

In-Store Buyers 30%

Online Buyers 9%

In-Store Buyers 11%

Online Buyers 17%

In-Store Buyers 17%

Throughout the Shopping Process

Online Buyers 46%

In-Store Buyers 43%

Q2. And when did you use search during your shopping and information gathering process to get information about your “TV”, “computer” or “digital camera” purchase? Please select the one response that best applies. Base: Respondents who used search to get information about their purchase; Purchased online – 240, Purchased offline - 345Source: CE Purchasing Process Study, November 2007

69%

70%

Search is Important to My Purchase Decision

Buy In-Store

Buy Online

20% 30% 40% 50% 60% 70%

Search is important to the purchase decision, as much to In-Store as to Online CE buyers

Q3a. How important were each of the following information resources in deciding what “TV”, “computer” or “digital camera” to buy? % “extremely/very” importantBase: Used Search Engine, Buy Online – 240; Buy In-Store– 345.

Source: CE Purchasing Process Study, November 2007

Search is a critical piece of the online research process

Percent of Buyers Who Searched

6.2 4.9 6.44.7

42%

55%

35%

59%

All Buyers Computer Digital Camera TV

6.2Searches

4.9Searches

6.4Searches5.3

Searches

Source: CE Purchasing Process Study, November 2007

Searchers: all products n= 925; computer n= 397; digital camera= 139; television n= 114

All searchers: all terms n= 397 ; branded n= 232 ; generic n= 254; 2-month period before purchase

Total Searches Used For All Purchases

53%Generic

47%Branded

Branded and Generic searches are used equally by buyers

Source: CE Purchasing Process Study, November 2007

But Branded and Generic search terms are used differently by category

Source: CE Purchasing Process Study, November 2007.

Generic

33%

Computer Searchers

Branded

57% 10% 35%

TV Searchers

47% 18%

37%

Digital Camera Searchers

38% 25%

Generic Branded

Generic Branded

Searchers: all products n= 925; computer n= 397; digital camera= 139; television n= 114

Buyers use generic search in the weeks leading up to purchase

6% 5%8% 9%1% 3%

2%

3% 5%4%

8%

3%3%

17%

2%

21%

0%

8%

16%

24%

32%

40%

7 6 5 4 3 2 1 0

Weeks Prior to Purchase

Generic Searches Branded Searches

% of Total Searches During Research Process

Searchers: all products n= 397; computer n= 148; digital camera= 115; television n= 45

Source: CE Purchasing Process Study, November 2007.

Online Consumers AreMore Valuable Customers

Research Online

Research Offline

BuyOnline

BuyIn-Store

CE Average $744 $704 $751 $708

TV’s $1,084 $954 $1,135 $970

Computers $883 $808 $910 $833

Digital Cameras $289 $254 $258 $254

Q9. Approximately how much did you pay for your “TV”, “computer” or “digital camera”? Base: Respondents who know which brand of product they purchased: Researched Online – 638, Researched Offline – 766. Buy Online – 587 , Buy In-Store – 1,317 Research Online/buy Digital Cameras ($289), significantly > than Research Offline ($254) @ 90% confidence. Buy Online/buy TV’s or Computers ($1,135 or $910), significantly > than Buy In-Store ($910 and $833) @ 95% confidence.

Online consumers tend to spend more on CE purchases

Source: CE Purchasing Process Study, November 2007

Online consumers offer a more attractive demographic profile

Research Online

Research Offline

BuyOnline

BuyIn-Store

Average Age 40.8 41.6 40.4 41.7

Male 64% 57% 61% 58%

Female 36% 43% 39% 42%

Average Income $64.1k $63.0k $65.0k $60.8k

College Degree or Higher 43% 35% 42% 35%

Heavy Internet Usage (15+ hours/week) 60% 51% 56% 55%

Source: CE Purchasing Process Study, November 2007

Q’s S1-2 and D1-3: Internet usage and demographic questions Base: Total: Researched online - 656; Researched offline – 791. Buy Online - 608 ; Buy In-Store – 1,376.Research Online, significantly > Male (64%), College Degree or Higher (43%), and Heavy Internet Usage (60%) @ 95% confidence. Research Offline, significantly > Female (43%) @ 95% confidence. Buy Online, significantly > Income ($65.0) @ 90% confidence, College Degree or Higher (42%) @ 95% confidence, Buy In-Store, significantly > Age (41.7) @ 90% confidence.

…and online researchers are stronger brand advocates

46% Buyers who

Research Offline

54%

Buyers who Research Online

How likely are you to recommend your CE brand…?

Q12. How likely are you to recommend your purchase to a friend, family member, or colleague? % “definitely would recommend”Base: Respondents who know which brand of product they purchased; Researched online - 646; Researched offline – 782. Buyers who Research Online (54%), significant > than Buyers who Research Offline (46%) @ 95% confidence

Source: CE Purchasing Process Study, November 2007

Searchers are the most valuable customers

Searchers 4.7

Non-Searchers 2.9

# Photos or Videos Uploaded About

Purchase

Searchers 2.9

Non-Searchers 1.6

# Reviews or Blogs Written about

Purchase

# People Talked to About Purchase

Searchers 7.2

Non-Searchers 5.1 Spend 17% More onCE Purchase

Searchers $803

Non-Searchers $685

Q13. Thinking about “TV”, “computer” or “digital camera” you bought, how many times have you done the following since you bought it? Please give us your best estimate. Base: Respondents who know which brand of product they purchased; Searchers – 573-578 ; Non-Searchers – 1,345-1,359. Q9. Approximately how much did you pay for your “TV”, “computer” or “digital camera”? Base: Respondents who know which brand of product they purchased; Searchers – 567, Non-Searchers – 1,337. Searchers, significantly > # People (7.2), # Photos/Videos (4.7), # Reviews/Blogs (2.9), $ Spend ($803) @ 95% confidence.

Source: CE Purchasing Process Study, November 2007

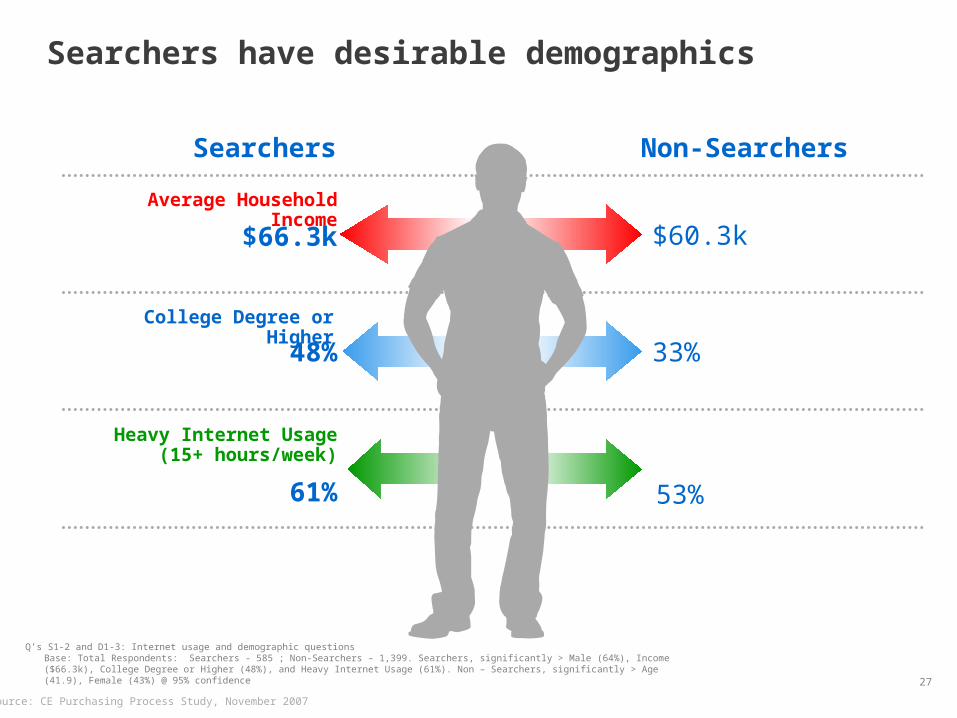

Searchers have desirable demographics

Source: CE Purchasing Process Study, November 2007

Q’s S1-2 and D1-3: Internet usage and demographic questions Base: Total Respondents: Searchers - 585 ; Non-Searchers – 1,399. Searchers, significantly > Male (64%), Income ($66.3k), College Degree or Higher (48%), and Heavy Internet Usage (61%). Non – Searchers, significantly > Age (41.9), Female (43%) @ 95% confidence

Average Household Income

53%

College Degree or Higher

48%

Heavy Internet Usage(15+ hours/week)

61%

$60.3k

33%

$66.3k

Searchers Non-Searchers

Key Findings

CE Buyers rely on Search throughout the shopping process• Search is used throughout the purchase funnel, not just at point of purchase

• Activity is split about equally between branded and generic terms

• Branded and generic term usage varies by category

Online CE consumers, particularly Searchers, are more valuable customers• Searchers spend more, are stronger brand advocates, are more affluent and highly

educated

• Shoppers who research online spend more, are more likely to recommend their product and have more attractive demographics

Online resources are critically important to the CE buyer• Equally important for in-store buyers and online buyers

• More useful than offline sources in building knowledge about brands/products andhelping with the final purchase decision

Implications For CE Advertisers

Use Online Advertising to Reach the In-store Buyer• All Consumer Electronics shoppers

have exposure to online advertising

• Online research plays a pivotal role to decision making process of in-store buyer

Measure Brand Impact as well as ROI of Search• Buy generic search terms – branded

terms only reach half of all purchasers

• Search is important at the top of the funnel, introducing brands and products

Leverage Online Marketing In Integrated Strategy• Use online channels to drive

customers to the store and reinforce messaging

• Opportunity for manufacturers to partner with retailers

• Use strength of online channels to compliment offline campaigns

Appendix

Computer buyers use generic search in the weeks leading up to purchase

1% 2%5% 4%

7%

19%

8%5% 7%

11%

2%

1%4%1%

22%

0.0%

8.0%

16.0%

24.0%

32.0%

40.0%

7 6 5 4 3 2 1 0

Weeks Prior to Purchase

Branded Searches Generic Searches

% of Total Searches During Research Process

Searchers: all products n= 397; computer n= 148; digital camera= 115; television n= 45Source: CE Purchasing Process Study, November 2007. Behavioral analysis of online buyers.

Digital camera buyers use generic search in the weeks leading up to purchase

2% 4% 4%8%

26%

2%3%

7%

12%

2%1% 2%3%3%

19%

3%

0%

8%

16%

24%

32%

40%

7 6 5 4 3 2 1 0

Weeks Prior to Purchase

Branded Searches Generic Searches

% of Total Searches During Research Process

Searchers: all products n= 397; computer n= 148; digital camera= 115; television n= 45Source: CE Purchasing Process Study, November 2007. Behavioral analysis of online buyers.

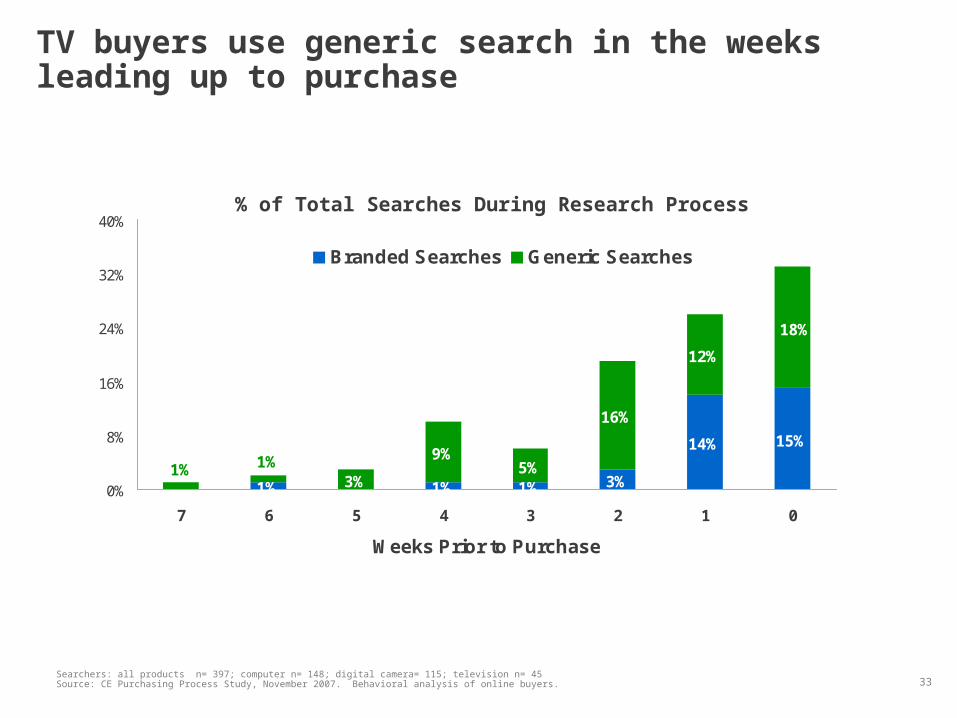

TV buyers use generic search in the weeks leading up to purchase

1% 1% 3%

14% 15%9%

5%

16%

12%

1%

1%1%

18%

3%0%

8%

16%

24%

32%

40%

7 6 5 4 3 2 1 0

Weeks Prior to Purchase

Branded Searches Generic Searches

% of Total Searches During Research Process

Searchers: all products n= 397; computer n= 148; digital camera= 115; television n= 45Source: CE Purchasing Process Study, November 2007. Behavioral analysis of online buyers.