Embed Size (px)

Citation preview

BUSINESS APPRAISAL

of

Sample Paving & Excavation, Inc.

as of

March 31, 2006

Prepared for

Mr. James G. Sample

Prepared by

George D. AbrahamBCBA,CMEA,FCBI,SBA,BCB,AAR

Houston Corporate OfficeP.O. Box 1262

Dickinson, Texas 77539_____________________________

Research and Production1120 Nasa Parkway, Suite 440

Houston, Texas 77058

TABLE OF CONTENTS_______________________________________________________________________________________________

Page

1. Table of Contents 12. What is Valued in this Report 23. Contingent and Limiting Conditions/Departure Provisions 34. Opinion Letter 55. Stock Sale Analysis 66. Statistical Summary 77. Graphic Display 88. Valuation Methods 99. Comparable Sales Analysis 1110. Critical Factors Discount/Premium Analysis 1211. Risk Factor Method 1312. Weighted Value Formulas 1513. Correlation of Methods 1714. Clarification of Value 1815. Comments on Appraisals 2016. Comments on Fair Market Value 2117. Comments on Certification 2418. Confidentiality Agreement 2519. Introduction 2620. Appraiser's Certification 2821. Required Rates of Return - Forming a Capitalization Rate 2922. Principles of Evaluation 3323. Evaluation Model 3424. Supporting Data Section 4125. Interview Questionnaire and General Assumption by the Appraiser 4226. Discretionary Net Profit Analysis 4727. Historical and Projected Overview 4828. Normalized Discretionary Earnings 4929. Justification For Purchase Tests 5030. Sources of Information 5331. Evaluators Qualifications 5632. Appendices 64

a) Robert Morris Associates Ratios and definitions b) BES Required Rates of Return c) Comparable Sales d) Industry Report e) Trade Area Outlook f) International Glossary

1

WHAT IS VALUED IN THIS REPORT This Business Evaluation Report and analysis of value assumes a "Corporate Sale" and reflects the"Stock Value" of the company. It does include "Current Assets" such as cash, accounts receivable,prepaid expenses and other liquid assets that would normally show up on the accountants balance sheetfor the company. It also includes all of the company's liabilities. This report values the tangible assets of the company and the intangible business value and assumes that the seller would transfer to apurchaser all current assets and liabilities of the company at the time of sale. For further clarification,please see page six of this report.

The report does not take into consideration the real estate that the company may own and considers this tobe an "Investment Asset". However, when the company does own real estate, a comparative market rentis deducted from the earnings to reflect the true earning power of the company, since the ownership ofreal property is discretionary to a business. If the company being value owns the real estate it should beconsidered an investment asset that would be added to the value opinion in this report. Also, BusinessEvaluation Systems has not valued the real estate nor the hard assets of this business and has relied onsources deemed reliable.

WRITTEN VALUATION REPORTS

The Uniform Standards of Professional Appraisal Practice (USPAP) outlines the minimum requirements for afull, formal written report. USPAP also allows for departure from some, but not all, of its requirements for more limited forms of reports. The more limited reports are designed for situations like client decision making, butthe complete report is suited for many litigation purposes. The full valuation report will typically include thefollowing sections:

1. A valuation opinion letter summarizing the appraisal procedures and the valuation conclusions.

2. Several sections summarizing the relevant valuation theory, methodology, procedures, analyses, and conclusions.

3. A Valuation synthesis and conclusion.

4. An exhibit section presenting a summary of the quantitative and qualitative appraisal analysis.

5. A listing of the data and documents the appraiser relied on.

6. A statement of the contingent and limiting conditions of the appraisal.

7. An appraisal certification.

8. The professional qualifications of the principal analysts.

2

DISCLAIMER_______________________________________________________________________________________________

PLEASE TAKE NOTICE that in this Business Appraisal report we have utilized the "DepartureProvision" as allowed by the Appraisal Foundation. This provision allows the appraiser to eliminate certain parts of the report that the client would be totally familiar with and thus provide an appraisal reportthat is cost efficient for the client. Utilizing the Departure Provision should not and does not lessen thestatus of an appraisal report. The parts of the report we may have eliminated, but did research are:A write-up on the history of the company, the local and national economy, industry forecasts and a step-by-step display of all formulas and calculations.

A Business Appraisal, as defined by current certification rules, may be performed without liability, if theuser is aware that the appraisal is a departure from the standards for formal appraisals as outlined by theAppraisal Foundation. Also, the user of this report should be aware that Business Evaluation Systems, norany of its representatives, have verified any information as to accuracy and any conclusion is only supported by the quality of the data provided.

CONTINGENT AND LIMITING CONDITIONS/DEPARTURE PROVISIONS

1. The appraiser, by reason of performing this Business Evaluation and preparing this report, is notto be required to give testimony nor be in attendance in court or any other governmental hearingwith reference to matters herein, unless prior arrangements have been made with the evaluatorrelative to such additional employment.

2. The appraiser assumes no responsibility for matters of a legal nature affecting the propertyvalued or the title thereto, nor does the Evaluator render any opinion as to the title, which isassumed to be good and marketable. The property is valued as though under responsibleownership.

3. Business Evaluation Systems assumes no responsibility for any environmental problems and hasnot inspected the property.

4. This appraisal was based on a specific period of time. Data for this period of time has beencollected from several sources. The particular market environment may not be exhibited again inthe future. A Business Appraisal is based on market data and research of factors surrounding thesubject at a particular time. The appraiser assumes no responsibility for errors in data availablefrom sources external to Business Evaluation Systems.

5. The selection of the use of Fair Market Value was made by the client. The appraiser assumes noresponsibility for the type of value selected as opposed to other types of value.

6. Business Evaluation Systems was retained by its client, who is thoroughly familiar with thebusiness and all past and future performance information used in this report has been based oninformation provided by the client and other sources deemed to be reliable. Business EvaluationSystems disclaims any ability of any potential purchaser to generate any future income, cost andexpense potential or expectations as may be stated in this report.

3

CONTINGENT AND LIMITING CONDITIONS/DEPARTURE PROVISIONS_______________________________________________________________________________________________(Continued)

7. All information in this report has been provided by our client, most of which is contained in the

questionnaire section of this report and is assumed to be reliable. No verification of the informationhas been done by Business Evaluation Systems, nor has the appraiser made an inspection or onsite visit of the business premises or facilities.

8. Any sketch that may be presented in this report may show approximate dimensions and is includedto assist the reader in visualizing the property. The appraiser has made no survey of theproperty.

9. Information, estimates, and opinions furnished to the appraiser and contained in this report wereobtained from sources considered reliable and believed to be true and correct. However, noresponsibility for accuracy of such items furnished the appraiser can be assumed by the appraiser.

10. Disclosure of the contents of this report is governed by the bylaws and regulations of theprofessional organizations with which the appraiser is affiliated.

11. Possession of this report or a copy thereof does not carry with it the right of publication. It may notbe used for any other purpose, in whole or in part, by anyone except the client, his advisors, or taxing agencies and for whom the appraisal was prepared without the previous written consent of the appraiser.

12. It is assumed that the reader of this report has at least a basic understanding of the subject'sindustry, terminology, and operations.

13. Other assumptions and limiting conditions are, as may be stated, in various other contents of thisreport.

14. Should new information be discovered that would alter the value of this report or an error in the report found, the appraiser reserves the right to change the report.

4

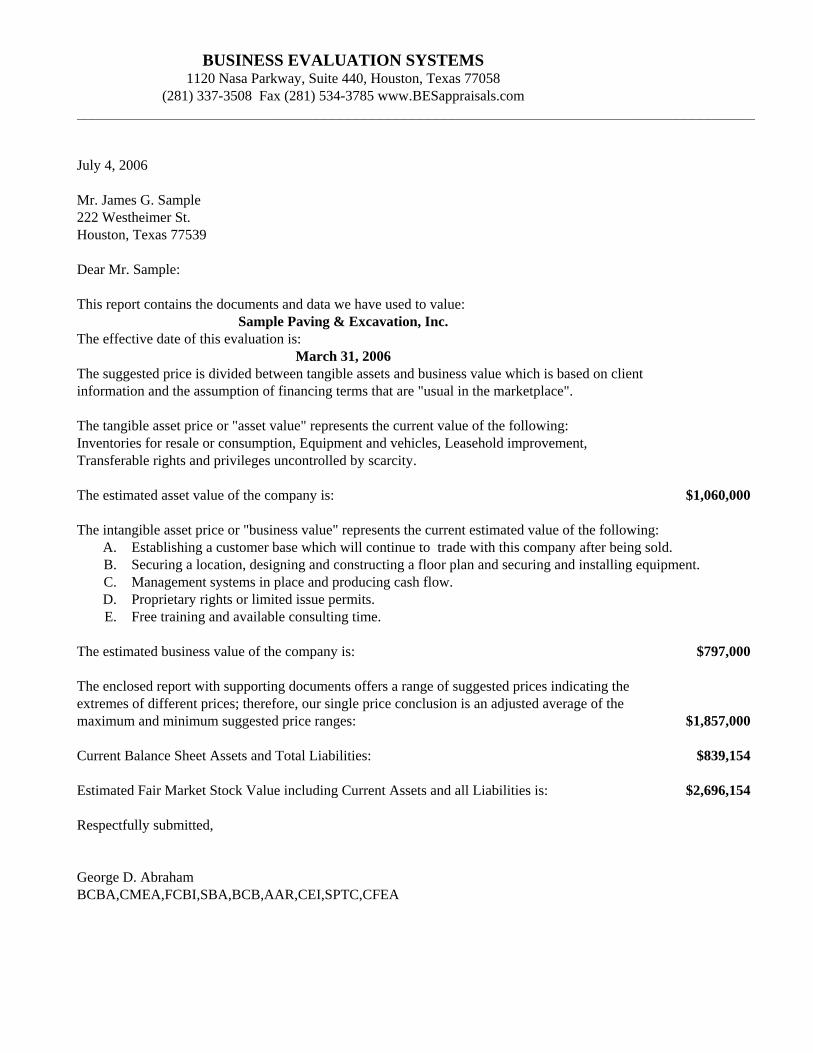

BUSINESS EVALUATION SYSTEMS 1120 Nasa Parkway, Suite 440, Houston, Texas 77058

(281) 337-3508 Fax (281) 534-3785 www.BESappraisals.com______________________________________________________________________________________

July 4, 2006

Mr. James G. Sample222 Westheimer St.Houston, Texas 77539

Dear Mr. Sample:

This report contains the documents and data we have used to value:Sample Paving & Excavation, Inc.

The effective date of this evaluation is:March 31, 2006

The suggested price is divided between tangible assets and business value which is based on clientinformation and the assumption of financing terms that are "usual in the marketplace".

The tangible asset price or "asset value" represents the current value of the following:Inventories for resale or consumption, Equipment and vehicles, Leasehold improvement,Transferable rights and privileges uncontrolled by scarcity.

The estimated asset value of the company is: $1,060,000

The intangible asset price or "business value" represents the current estimated value of the following:A. Establishing a customer base which will continue to trade with this company after being sold.B. Securing a location, designing and constructing a floor plan and securing and installing equipment.C. Management systems in place and producing cash flow.D. Proprietary rights or limited issue permits.E. Free training and available consulting time.

The estimated business value of the company is: $797,000

The enclosed report with supporting documents offers a range of suggested prices indicating theextremes of different prices; therefore, our single price conclusion is an adjusted average of themaximum and minimum suggested price ranges: $1,857,000

Current Balance Sheet Assets and Total Liabilities: $839,154

Estimated Fair Market Stock Value including Current Assets and all Liabilities is: $2,696,154

Respectfully submitted,

George D. AbrahamBCBA,CMEA,FCBI,SBA,BCB,AAR,CEI,SPTC,CFEA

STOCK SALE ANALYSIS Sample Paving & Excavation, Inc.

This evaluation has been performed under the assumption of an Asset Sale. To convert our analysisof value to a stock sale as of the effective date of the evaluation, the calculations would be as follows:

Sample Paving & Excavation, Inc. As of: March 31, 2006

Total Asset Value, including both tangible and intangible values as stated on page five: $1,857,000

ADD all of the Current Assets as shown on the Accountant's Balance Sheetfor : Sample Paving & Excavation, Inc. $2,289,140

SUBTRACT all of the Corporation's Liabilities as shown on the Accountant's Balance Sheet. ($1,449,986)

____________Current Assets minus Total Liabilities Sub Total: $839,154

Estimated Business Value, Current Balance Sheet Assets and Total Liabilities: $2,696,154

6

STATISTICAL SUMMARY Sample Paving & Excavation, Inc.________________________________________________________________________________________

For summary purposes we have included a specific value for "ASSETS" and "BUSINESSVALUE" and a conclusive "SELLING PRICE".________________________________________________________________________________________

We estimate the Tangible Asset Value of this company to be: $1,060,000

We estimate the Intangible Asset Value of this company at: $797,000

We estimate the Fair Market Value of this company to be: $1,857,000_______________________________________________________________________________________________

Our analysis generates a price range representing the highest price a seller could expect andthe lowest price a seller should accept.

The "SUGGESTED PRICE" is calculated based on the information generated by the variousformulas, but does not account for special situations and discount deviations.

_____________________________________________________________________________________________

Suggested Pricing Upper Range Value Weight Lower Range Value

_______________________________________________________________________________________________Going Concern Asset Method $1,150,000 $940,000

Basic Method $3,070,000 $1,330,000 ASTCapitalization $1,790,000 80% $1,670,000 BASCritical Factor $4,300,000 $1,856,000 CAPDebt Capacity $2,150,000 20% $1,520,000 CRT

Comparable Sales $2,700,000 $1,380,000 DBTRisk Analysis Table $1,310,000 $1,310,000 CMP

Required Rates of Return $1,790,000 $1,670,000 RATIndustry Risk Factor $1,790,000 $1,580,000 RRR

Weighted Factors $1,250,000 $750,000 IRFMultiple Average $2,880,000 $1,630,000 WGTSuggested Range $1,860,000 $1,640,000 MLTSuggested Price $1,857,000 100% $1,857,000 RNG

PRCNOTES ABOUT SPECIAL CONDITIONS: If a particular range value is extremely high or extremelylow, do not be alarmed. Extreme deviations are the product of formulas which consider only one or twobusiness factors and are not representative of the total business.

This report will make adjustments and allowances for these extremes in the suggested range value.

If potential buyers used only one method for evaluation and that formula produced one extreme valuethere would be reason for concern. However, very few buyers consider only one formula, rather mostbuyers base their decision on the debt capacity and assets of a business and become generous orconservative based on their beliefs for all the other factors.

7

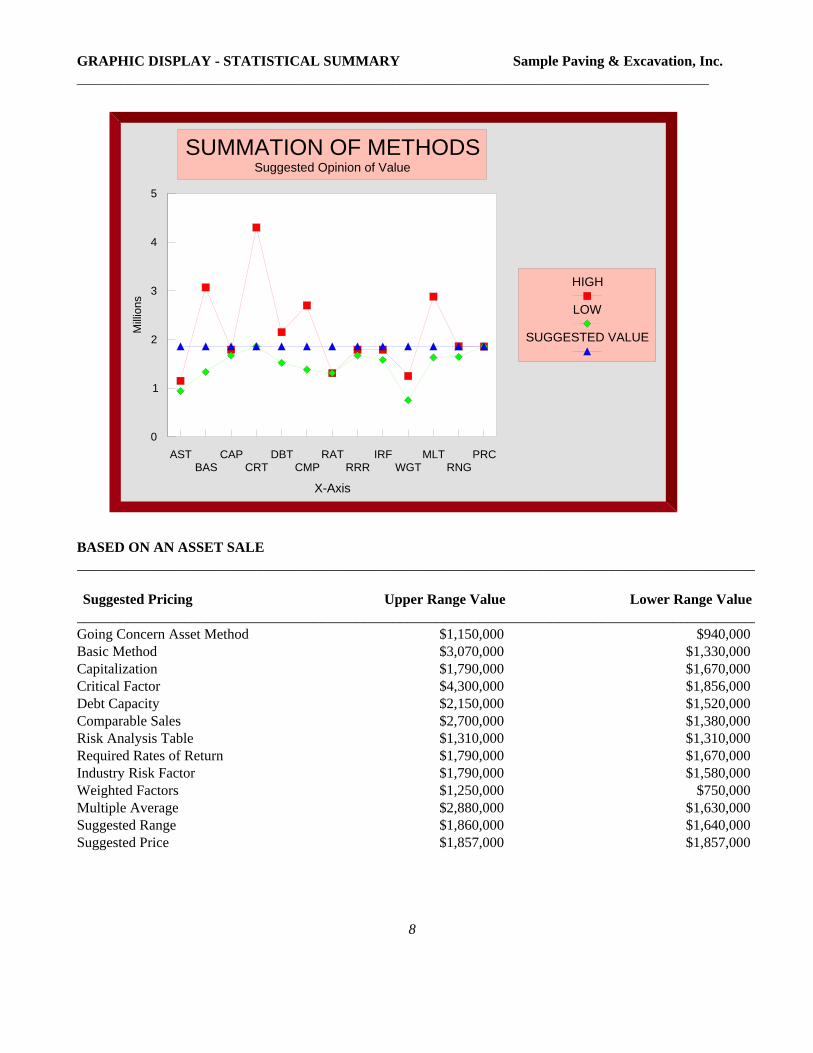

GRAPHIC DISPLAY - STATISTICAL SUMMARY Sample Paving & Excavation, Inc.________________________________________________________________________________________

BASED ON AN ASSET SALE_______________________________________________________________________________________________

Suggested Pricing Upper Range Value Lower Range Value

_______________________________________________________________________________________________Going Concern Asset Method $1,150,000 $940,000Basic Method $3,070,000 $1,330,000Capitalization $1,790,000 $1,670,000Critical Factor $4,300,000 $1,856,000Debt Capacity $2,150,000 $1,520,000Comparable Sales $2,700,000 $1,380,000Risk Analysis Table $1,310,000 $1,310,000Required Rates of Return $1,790,000 $1,670,000Industry Risk Factor $1,790,000 $1,580,000Weighted Factors $1,250,000 $750,000Multiple Average $2,880,000 $1,630,000Suggested Range $1,860,000 $1,640,000Suggested Price $1,857,000 $1,857,000

8

ASTBAS

CAPCRT

DBTCMP

RATRRR

IRFWGT

MLTRNG

PRC

X-Axis

0

1

2

3

4

5

Milli

ons

HIGH

LOW

SUGGESTED VALUE

SUMMATION OF METHODSSuggested Opinion of Value

VALUATION METHODS Sample Paving & Excavation, Inc. ____________________________________________________________________________________________

INDUSTRY RISK FACTOR BASIC VALUE Base Value $2,969,292 Adjusted Normalized Earnings $383,982 Asset Value $1,049,382 Competition $267,236 Management Type $801,709 Basic High $3,074,230 Turnover $623,551 Basic Low $1,328,426 Type Of Business $504,780 ______________________________________________ Owner Finance Yrs $296,929 CAPITALIZATION Owner Finance Rate $1,098,638 High Return % 23% Owner Finance % $148,465 Low Return % 22% Bank Finance Years $296,929 Bank Finance Rate $742,323 Capital Rate High $1,785,963 Bank Finance % $564,166 Capital Rate Low $1,669,487 Number of Employees $207,850 ______________________________________________ Age of Industry $801,709 WEIGHTED Industry Market $712,630 Target $2,201,328 Years Of Operation $1,425,260 Consulting Time $623,551 Labor 114% Net Cash - Salary $1,306,489 Predictability -264% Local Economy $801,709 Management 57% Labor Market $0 Competition 84% Skills Required ($267,236) Revenue 100% Union Strength ($1,098,638) Longevity 101% Location $3,830,387 Location 214% National Economy $356,315 Loanability 38% Clientele 61% National High $1,792,718 Liability 63% National Low $1,582,842 ___________________________________________ Weighted High $1,248,765 CRITICAL FACTOR Weighted Low $753,587 Financing 38% ______________________________________________ Desirability 93% DEBT CAPACITY METHOD Lease 188% Normalized Discretionary Earnings $512,132 Economy 240% Less: Managment Compensation $80,000 Less: Economic Depreciation $48,150 Critical High $4,295,455 Adjusted Normalized Earnings $383,982 Critical Low $1,856,137 ___________________________________________ Interest Rate 9.50% ASSET METHOD Equipment and Equity $435,000 Fast Payout Years 5 Improvements $0 Slow Payout Years 8 Vehicles $46,500 Stock/Supplies $567,882 Debt High $2,145,983 Licenses/Patents $0 Debt Low $1,523,603 Asset High $1,154,320 Asset Low $944,444 9

VALUATION METHODS______________________________________________________________________________________________

Risk Analysis Table______________________________________________________________________________________________

Adjusted Normalized Discretionary Earnings (page 49): $383,982 $383,982Multiples representing general industry: 4.35 4.65 Questions 17 and 18 divided by 100 (1.00/Q17) __________ __________

Target values $1,669,487 $1,785,963________________________________________________________ __________ ______________ ___________

Discount/PremiumTopics Reported for Importance Factored________________________________________________________ __________ ______________ ___________

Labor 3.0 100% 3.00 See question 53Financial Strength 3.0 100% 3.00 See question 57Facilities and Location 4.0 110% 4.40 See question 66Diversity of Accounts 3.0 140% 4.20 See questions 39 and 40Competition 3.0 100% 3.00 See question 51Predictability 3.8 120% 4.50 See questions 40, 50, 60 and 62Marketability 3.4 110% 3.71 See questions 45, 54, 59 and 68Future Outlook 4.0 140% 5.60 See questions 60 and 62Owner Importance 3.5 100% 3.50 See questions 52, 56 and 58 --------------- --------------------- -----------------

Totals (9 topics): 30.6 1020.0% 34.9

Divided by number of topics (Reported Multiples): 3.4 113.3% 3.9

Total Ratings used for this method (Adjusted Multiple): 3.4 3.9________________________________________________________ __________ ______________ ___________

Conclusion Risk Analysis Table________________________________________________________ __________ ______________ ___________

High Range Low Range

Reported (Adjusted Normalized Discretionary Earnings x Reported Multiple): $1,306,606

Adjusted Ratings (Adjusted Normalized Discretionary Earnings x Adjusted Multiple): $1,306,606

10

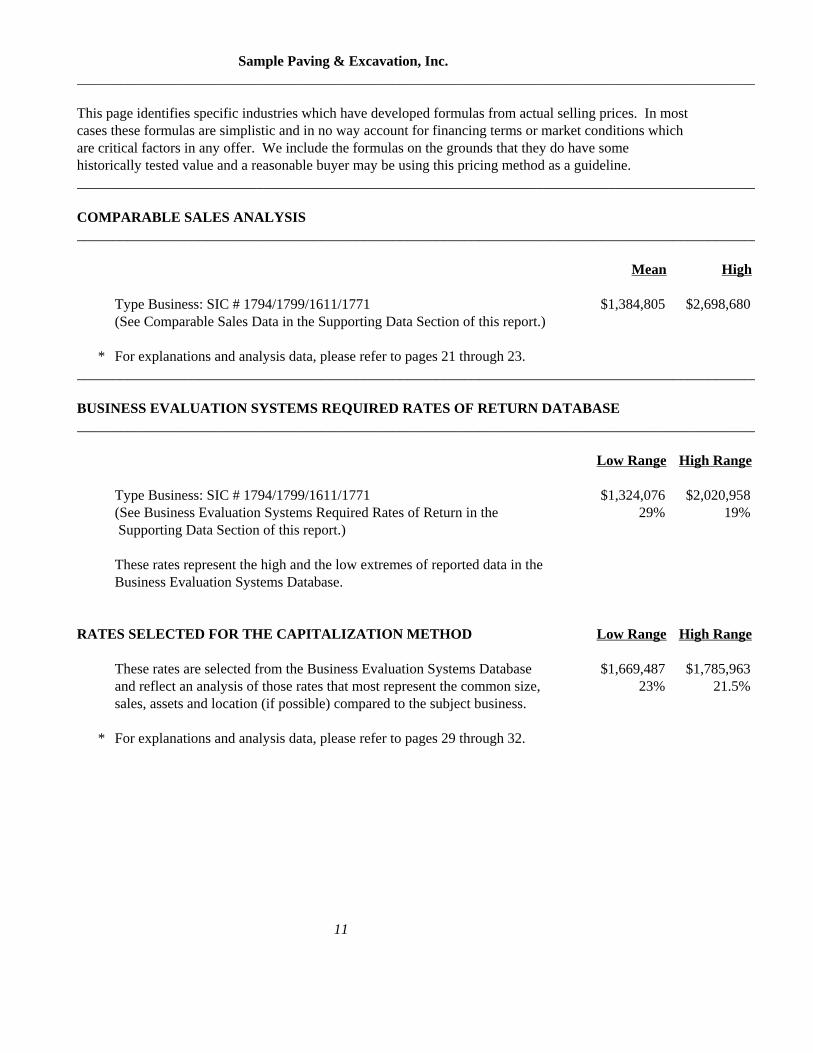

Sample Paving & Excavation, Inc._______________________________________________________________________________________________

This page identifies specific industries which have developed formulas from actual selling prices. In mostcases these formulas are simplistic and in no way account for financing terms or market conditions whichare critical factors in any offer. We include the formulas on the grounds that they do have somehistorically tested value and a reasonable buyer may be using this pricing method as a guideline._______________________________________________________________________________________________

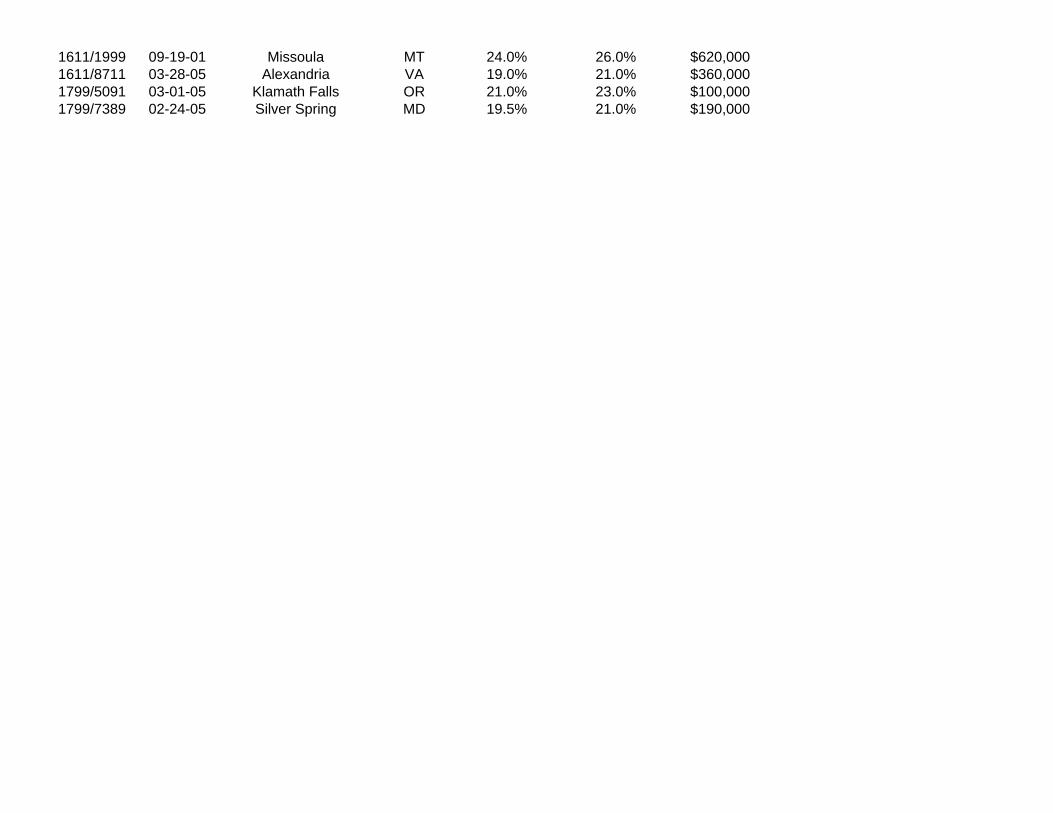

COMPARABLE SALES ANALYSIS_______________________________________________________________________________________________

Mean High

Type Business: SIC # 1794/1799/1611/1771 $1,384,805 $2,698,680(See Comparable Sales Data in the Supporting Data Section of this report.)

* For explanations and analysis data, please refer to pages 21 through 23. _______________________________________________________________________________________________

BUSINESS EVALUATION SYSTEMS REQUIRED RATES OF RETURN DATABASE_______________________________________________________________________________________________

Low Range High Range

Type Business: SIC # 1794/1799/1611/1771 $1,324,076 $2,020,958(See Business Evaluation Systems Required Rates of Return in the 29% 19% Supporting Data Section of this report.)

These rates represent the high and the low extremes of reported data in theBusiness Evaluation Systems Database.

RATES SELECTED FOR THE CAPITALIZATION METHOD Low Range High Range

These rates are selected from the Business Evaluation Systems Database $1,669,487 $1,785,963and reflect an analysis of those rates that most represent the common size, 23% 21.5%sales, assets and location (if possible) compared to the subject business.

* For explanations and analysis data, please refer to pages 29 through 32.

11

CRITICAL FACTORS DISCOUNT/PREMIUM ANALYSIS_________________________________________ __________________________________________________

Down Down Int Bank Owner Bank OwnerPmt Pmt Rate Fixed Fixed Vary Vary

% % $ % % % % % %________________ __________ _________ ___________________ __________ __________ __________

0% 150% 38398 296% 6.0% 126% 138% 113% 116%5% 135% 76796 204% 6.5% 101% 114% 90% 95%

10% 122% 115195 163% 7.0% 80% 94% 71% 77%15% 110% 153593 138% 7.5% 62% 78% 55% 62%20% 103% 191991 121% 8.0% 48% 64% 41% 50%25% 96% 230389 109% 8.5% 35% 52% 29% 38%30% 92% 268787 100% 9.0% 24% 42% 18% 28%35% 90% 307186 92% 9.5% 15% 34% 8% 19%40% 87% 345584 85% 10.0% 6% 26% -0% 11%45% 85% 383982 80% 10.5% -1% 20% -8% 4%50% 84% 422380 75% 11.0% -9% 13% -16% -3%55% 83% 460778 71% 11.5% -15% 8% -23% -9%60% 82% 499177 68% 12.0% -21% 3% -29% -15%65% 81% 537575 65% 12.5% -27% -2% -35% -21%70% 80% 575973 62% 13.0% -32% -6% -41% -26%75% 79% 575973 62% 13.5% -37% -10% -46% -31%80% 78% 652770 57% 14.0% -41% -13% -51% -35%85% 77% 691168 55% 14.5% -46% -17% -56% -40%90% 76% 729566 53% 15.0% -50% -20% -61% -44%95% 75% 767964 51% 15.5% -54% -23% -66% -48%

100% 75% 806362 49% 19.0% -79% -41% -95% -74%______ __________ __________ _________ ___________________ __________ __________ __________Industry Value Desire Selection Value

% Levels Number %______ __________ __________ _________ ___________________ __________ __________ __________

Individual 0 0% Minimal 1 38%Service 1 50% Workable 2 71%Retail 2 71% Interesting 3 100%Wholesale 3 87% Excellent 4 141%Industrial 4 100% Perfect 5 224%Monopoly 5 112%

12

INDUSTRY RISK FACTOR___________ ___________ ___________ ___________ ___________ ___________ ___________ ___________

Owner Finance % Competition Management Type

0% 0.02 0 -0.93 0 -1.1220% 0.05 1 -0.37 1 -0.8740% 0.12 2 0.00 2 -0.5260% 0.19 3 0.09 3 -0.0380% 0.41 4 0.36 4 0.27

100% 0.58 5 0.52 5 0.41___________ ___________ ___________ ___________ ___________ ___________Location Turnover Type Of Business

0 -0.63 0% -0.37 0 -0.221 0.00 10% -0.23 1 -0.142 0.47 25% 0.00 2 0.003 0.98 45% 0.16 3 0.17

4-5 1.29 65% 0.21 4 0.26___________ ___________ ___________ ___________ ___________ ___________Finance Years Owner Interest % Bank Interest %

0 -0.46 5% 0.66 0% 2.503 -0.20 8% 0.37 3% 1.605 0.10 10% 0.24 5% 0.708 0.20 12% 0.00 7% 0.25

10 0.35 15% -0.22 10% 0.0015 0.46 16% -0.50 12% -0.1420 0.63 17% -1.00 15% -0.2230 0.81 18% -3.20 17% -0.31

100 1.10 19% -3.70 19% -0.45___________ ___________ ___________ ___________ ___________ ___________Consulting Time Number of Employees Net Cash - Salary

0 0.03 0 0.23 $0 0.011 0.09 5 0.17 $30,000 0.082 0.13 11 0.11 $49,000 0.173 0.14 20 0.07 $99,000 0.314 0.16 50 -0.05 $250,000 0.445 0.21 100 -0.12 $999,999 0.49

___________ ___________ ___________ ___________ ___________ ___________Local Economy Labor Market Skills Required

1 -0.38 1 -0.17 1 0.272 0.00 2 0.00 3 -0.093 0.27 3 0.11 5 -0.31

4 0.235 0.31

13

INDUSTRY RISK FACTOR (Continued)___________ ___________ ___________ ___________ ___________ ___________ ___________ ___________

___________ ___________ ___________ ___________ ___________ ___________Union Strength Bank Finance % Years Operating

1 0.00 0% 0.00 0 0.002 -0.37 20% 0.05 1 0.023 -0.43 40% 0.12 2 0.134 -0.45 60% 0.19 5 0.285 -1.31 80% 0.41 10 0.41

100% 0.58 15 0.4620 0.48

100 0.51___________ ___________ ___________ ___________ ___________ ___________Age of Industry National Economy Industry Market

1 -0.71 1 -0.09 1 -0.292 -0.12 2 0.00 2 0.003 0.27 3 0.12 3 0.24

14

WEIGHTED VALUE FORMULAS______________________________________________ _______________________ _____________________

Labor and Workforce Predictability______________________________________________ _______________________ _____________________

Longevity 95% Revenue Growth -1703%Quantity 280% Survival 90%

Recruiting 100% Lease Time 154%Skill 60% Trends 60%

Market 67% Budgeting 80%Union 80%

Average 114% Average -264%______________________________________________ _______________________ _____________________Management Structure Financing______________________________________________ _______________________ _____________________

Family/Partners 50% Percent of Banks 80%Family Percent 91% Collateral Value 60%

Influence 1% Bank Interest 42%Skill 80% Owner Interest 18%

Autonomy 60% Owner Finance 20%

Average 57% Average 38%______________________________________________ _______________________ _____________________Revenue Security Longevity______________________________________________ _______________________ _____________________

Percentage of Cash 0% Desirability 70%Local Trends 150% Trends 133%

National Trends 150% Age 100%

Average 100% Average 101%______________________________________________ _______________________ _____________________Location Competition______________________________________________ _______________________ _____________________

Lease Cost 122% Start Up Time 17%Establishment 570% Knowledge 80%

Location -50% Training 200%Competitors 40%

Average 214% Average 84%______________________________________________ _______________________ _____________________Clientele Stability Liability Exposure______________________________________________ _______________________ _____________________

Accounts 33% Exposure 50%Influence 90% Rates 75%

Trade 60%

Average 61% Average 63%

15

WEIGHTED VALUE FORMULAS (Continued)______________________________________________ _______________________ _____________________

______________________________________________ _______________________ _____________________Market Demand $2,567,500 Economic Demand $2,880,000______________________________________________ _______________________ _____________________

2 $1,630,000 3 $1,630,0004 $1,942,500 5 $1,942,5006 $2,255,000 7 $2,255,0007 $2,567,500 8 $2,567,5008 $2,880,000 9 $2,880,000

16

CORRELATION OF METHODS_______________________________________________________________________________________________

Discussion of Weighting

It is important to note that under guidelines set by "The Uniform Standards of Professional AppraisalPractice" (Standards Rule 9-5), The Internal Revenue Service (Revenue Ruling 59-60), as well as mostappraisal societies, require the appraiser to use all approaches for which reliable data is available andapplicable. The use of as many approaches and methods within these approaches is useful to the extentthat it will establish a range of values for the entity being appraised.

Revenue Ruling 59-60, in Section 3, Approach To Valuation, recognizes that appraising is not an exactscience in the statement that "A sound valuation will be based upon all the relevant facts, but the elementof common sense, informed judgment and reasonableness must enter into the process of weighing thosefacts and determining their aggregate significance".

Sometimes it will be obvious that the analyst should rely on a single approach, such as methods under theCost Approach whereby earnings are insignificant to the value of the assets. An example of this would bea new enterprise with little or no longevity or profits, and projections would be meaningless. Anotherexample would be a company that has longevity, but insignificant profits and would be a candidate forliquidation. In other cases it may be apparent that several methods would be appropriate for the finalvalue conclusion. When this is the case, the appraiser must look to the real world to determine whichmethod or methods should receive the most weighting.

Service companies can represent a significant problem to the appraiser in that there are few assets thatwould give a buyer confidence should the business someday fail. In any case, risk is the most importantfactor to consider in an appraisal. As stated earlier, and acknowledged in Revenue Ruling 59-60, value isbased on anticipated expectations of the buyer as to the performance of the future. In other words, whata company did in the past has no significance to its value if that trend is not anticipated in the future.

Although assets play an important role in risk calculations, one must remember that earnings and theanticipation of an increasing income stream are the overriding factor in the purchase of a business. Notonly through the process of elimination, but an analysis of the methods suggests that methods under theincome approach are clearly the most representative of the current market.

17

Sample Paving & Excavation, Inc.

CLARIFICATION OF VALUE ______________________________________________________________________________________________

The value of the subject company has been stated on the Opinion Letter on page five. This value does notinclude real estate or improvements which are considered Investment Assets. The following additionsshould clarify to the reader of this report the final Opinion of Value for the entity:

Asset Value of Business: Furniture, Fixtures, Equipment and Equipment Equity $435,000 Leasehold Improvements $0 rolling Stock 46,500 Inventory 567,882 License/Patents $0

Adjusted to Percentage of Error, Less adjustment for Fair Market Value of Furniture, Fixtures and Equipment and obsolete or dead inventory $10,618

Total Asset Value of Business $1,060,000

Value of Business: $797,000

TOTAL FAIR MARKET VALUE OF THE BUSINESS: $1,857,000_______________________________________________________________________________

As of March 31, 2006CURRENT ASSETS: As Listed on Recast

Balance Sheet Adjustments Balance SheetPetty Cash $83,561 $83,561Cash - ABC Bank 287,304 287,304Accounts Receivable Employees 17,001 17,001Accounts Receivable Trade 1,539,020 1,539,020Unbilled Work in Progress 362,255 362,255

Total Current Assets $2,289,140 $0 $2,289,140

PROPERTY & EQUIPMENTInventory Material $567,882 $567,882Office Equipment 57,916 57,916Less: Accumulated Depreciation (1) (56,262) 23,479 (32,783)Rolling Stock 205,188 205,188Less: Accumulated Depreciation (1) (145,927) 32,918 (113,009)Shop Equipment 374,529 374,529Less: Accumulated Depreciation (1) (372,842) 303,245 (69,597)Computer Equipment 93,485 93,485Less: Accumulated Depreciation (1) (87,189) 12,000 (75,189)Computer Software 39,424 39,424

18

Sample Paving & Excavation, Inc. As Listed on Recast Balance Sheet Adjustments Balance Sheet

Amortization - Computer Software ($33,071) ($33,071)Leasehold Improvements - Building (2) 221,599 (221,599) 0Less: Accumulated Depreciation (2) (165,581) 165,581 (0)Shop and Repair Facility 63,482 63,482Less: Accumulated Depreciation (1) (63,482) 45,226 (18,256)

Total Property & Equipment $699,150 $360,850 $1,060,000

OTHER ASSETSPrepaid Insurance $16,587 $16,587Prepaid Interest 1,960 1,960Loan Fee Costs 286 286Cash-Surrender Value of Life Insurance (3) 349,526 (349,526) 0Deposits 1,618 1,618

Total Property & Equipment $369,977 ($349,526) $20,452

TOTAL ASSETS $3,358,268 $11,325 $3,369,592

LIABILITIES & EQUITY

CURRENT LIABILITIESAccounts Payable $622,259 $622,259Deposits $379,953 379,953Accrued Salaries 41,344 41,344Notes Payable - Line of Credit 370,940 370,940A/B Notes Payable 21,855 21,855Texas Unemployment Tax 102 102Texas Withholding Tax 5,393 5,393

Total Current Liabilities $1,441,845 $0 $1,441,845

LONG-TERM LIABILITIES:Long Term Notes Payable - Bank $8,141 $8,141Long Term Notes Payable - Insurance Companies (3) 142,848 ($142,848) 0

Total Long-Term Liabilities: $150,989 ($142,848) $8,141

TOTAL LIABILITIES $1,592,834 ($142,848) $1,449,986

EQUITY $1,765,433 $1,919,606

LIABILITIES AND STOCKHOLDERS' EQUITY $3,358,268 $3,369,592

NOTES TO THE BALANCE SHEET(1) Amount needed to bring Equipment, Furniture and Fixtures, Office Equipment and Inventory and Rolling Stock to "Fair Market Value".(2) Buildings and Real Estate are not part of this appraisal.(3) The owner is going to keep the insurance and the notes associated with it, as it is his personal insurance.

19

COMMENTS ON APPRAISALS_______________________________________________________________________________________________

A Business Appraisal is a type of investigation into the law of probabilities with respect to valuation. Through the appraiser's experience, training, and integrity, we are able to project the activities of buyersand sellers in the marketplace into an estimation of value. In reaching a conclusion, comparison ofbusinesses usually involves adjustments due to the individuality and uniqueness of each business. Transactions are often influenced by sentiment, bias, specific needs, politics, familiarity, lack ofunderstanding, and other conditions not considered by the impartial appraiser. The appraiser cannot lendcredence to these possible factors lest he misrepresent the very reason for his profession.

A Business Appraisal is an Opinion of Value that cannot be guaranteed, nor can it be proven. The opinion ofvalue can, however, be substantiated and the final opinion is the result of a thorough professional analysis ofa vast quantity of data. An appraisal must not be considered absolute but should be used as a basis ofnegotiations between concerned parties, whatever their interests.

The appraisal process as followed in the preparation of this report is an orderly procedure for arriving atan estimate of value. By following this procedure the appraiser begins with a preliminary study of theproblem involved and defines the basis from which the Opinion of Value is to be made. A program is theninitiated for the accumulation, analysis, and observation of data. The data called for in the preliminary studyis then gathered, classified and analyzed.

In assignments to estimate Fair Market Value, the ultimate goal of the valuation process is a supportedconclusion that reflects the appraiser's study of all influences on the value of the company being appraised.Therefore, the appraiser studies the business from various applicable viewpoints. Various questions areraised and answered through research of the industry and financial capabilities of the subject business. Some of the questions researched may be found in the supporting data section of this report.

Various approaches are interrelated, and each involves the gathering and analysis of sales, activity, andvalue data in relation to the company being analyzed. From the analysis, the appraiser derives separateindications of value for the company being valued. One or more approaches may be used, depending ontheir applicability to the particular assignment.

To complete the valuation process, the appraiser integrates the information drawn from the marketresearch and analysis of data and from the application of valuation techniques to form a conclusion. Thisconclusion may be an estimate of value or a range in which the value may fall. An effective integrationdepends on an appraiser's skill, experience, and judgment.

With the preceding in mind, the reader's attention is invited to the appraisal report and various exhibitswhich point out the facts and reasoning leading to the final Opinion of Value.

20

COMMENTS ON FAIR MARKET VALUE_______________________________________________________________________________________________

The single most important market factor to impact the value of a business is the supply and demand of anequally desirable substitute that is available in the marketplace. According to the Principle of Substitution,the value of a thing (business) tends to be determined by the cost of acquiring an equally desirablesubstitute. The concept of valuation considering an equally desirable substitute dictates that a buyer willpay no more for a business than what he or she can currently purchase the same or another business oflike kind. This concept is the basis of Fair Market Value and is the overriding methodology in thisevaluation report.

There are only three approaches to determining the value of any asset: the Cost Approach, which basicallyconsiders the cost of purchasing or producing the business, the Market Data Approach which values thebusiness based on current sales in the market place for the same or similar business, and the IncomeApproach which is a mathematical analysis of capitalizing an income stream by a return that best representsthe activity of the current market.

In other types of valuations, mainly real estate, the Market Data Approach indisputably will always yield themost accurate results. It is a true representation of the current market place because it is what the market ispaying for the same or similar asset. However, in the case of a business, using public or private comparablesales price-to-earnings or income-to-sales ratios may be the least reliable for several reasons: no twobusinesses are alike, business sales are not recorded and, therefore, information gathered is usuallysketchy, accounting records are not always standard between the same companies, there is no standarddefinition of "Net Profit" or "Income, Revenue", "Cost of Sales" and many others. Some comparable salesinclude assets that the subject business does not have and these assets are not valued separately, therefore,the appraiser can not make proper adjustments. The Market Data Approach can be very useful whenanalyzing data drawn from the market as to what types of return on investment or data based on multiplesof annual earnings that buyers are willing to pay in order to purchase a certain type of business.

It can be argued that the use of stock prices of publicly-owned companies to estimate the market value ofprivately-held companies is a source of comparable data. However, most business appraisers realize thatto estimate the market value of a privately-held business using this data is seriously flawed in severalrespects:

1. Publicly-held companies whose stock is listed on the major exchanges are usually much larger than closely-held businesses that are being appraised. This difference in size raises serious questions as to whether the two are, in fact, comparable.

2. Prices of publicly-traded stock always reflect the sale of a very small fractional ownership interests. On the other hand, the appraiser's objective is usually to estimate the market value of a major ownership interest, frequently, one hundred percent ownership of the closely-held business.

3. The above must be selected by the appraiser through a process that amounts to little more than guess work, and thus cannot be relied upon.

4. The price-to-earnings ratio represents the ratio of a current stock to an earnings-per-share figure that can be from a few weeks to several months old.

21

5. Probably the greatest fallacy of attempting to use publicly-traded stock prices to estimate the value of a closely-held business lies in the psychology of the investor. The potential buyer for a closely-held business is almost always concerned with the anticipated performance of the business itself. Of course, it is sometimes argued that the trend of stock prices of a publicly-held company is strongly influenced by the company's performance. However, it is demonstrable that, whereas this does tend to be true in the long run, there are many influences on stock that tend to be of short-term nature,

and that strongly influence stock prices while bearing relatively little long-term relationship to thecompany's fortunes. This is not recommended as a means of estimating the value of closely-heldbusinesses.

Still another source of Market Data is, of course, information on actual sales of companies, such as thesubject, in the appraiser's local community. It is unlikely, however, that there will be enough informationavailable on sales similar to the subject to provide statistically sound basis for estimating market value. However, as mentioned above, when analysis based on research on potential buyers for this kind ofinvestment is made, important insight into what a buyer is willing to pay for a particular business can assistthe appraiser in determining an accurate opinion of value. Please keep in mind that this analysis mustinclude such factors as industry risk, the local and national economy, competition, ease of entry into theindustry and the company's portrayal of future performance and the length of time it will last that thebuyer can reasonably expect to receive after acquisition.

In conclusion, on the subject of the Market Data Approach for closely-held businesses, while we mayinclude information or make comments on similar business sales that might have reciprocity in valuationtechniques, the lack of enough market data from public or private sales based solely on price-to-earningsand income to selling price may make this technique unsound and may eliminate the use of the MarketData Approach in this valuation.

In the Cost Approach, the cost of an item is rarely what its selling price or value may be and in many casespriceis not the value. This is especially true in a rapidly changing market which is highly affected by technological changes or variances in supply and demand or especially a company that is very youngand has not yet established enough longevity to make a confident analysis of the future performance.

Also, in the case of a business, all serious practitioners of business valuation agree that book value is notnecessarily an adequate proxy for representing the underlying net asset of a business for valuationpurposes, much less for representing the value of the business itself. However, book value is a figurethat is available for almost all businesses. Furthermore, it is a value that different businesses have arrivedat by some more or less common set of rules, usually some variation within the scope of generallyaccepted accounting principles (GAAP). Also, each asset or liability number that is a component of bookvalue as shown in the financial statements represents a specific set of obligations that can be identified indetail by referring to the company's records, assuming that the bookkeeping is complete and accurate.Therefore, book value usually provides the most convenient starting point for an asset valueapproach to the valuation of a business interest.

The nature and extent of adjustments that should be made to book value for the business valuationdepend on many factors. One, of course, is the valuation's purpose, another which is frequently alimiting factor, is the availability of reliable data on which to base the adjustments both for the subjectcompany and for other companies which might be compared in the course of the valuation.

Another concept for fixed assets is "Value in Use". The value of the operating assets to the owner/useror buyer who will use them in a similar manner is the value that includes consideration for the uniquerelationship of the item to a particular business such as the subject.

22

There is a value for an item which is already in place and is ready to use. The value might be the item'sretail price, plus applicable taxes, freight, and installation charges. The summation of these costs, afterproper deductions for depreciation and obsolescence is the "Value in Use" of that item. This value maybe different from its Fair Market Value to a buyer who will not use the equipment at its presentlocation. A definition for "Value in Use" is as follows:

"The value of an economic good to its owner/user is based on the production (privacies in income, utility oramenity form) of the economic good to a specific individual. This is a subjective value, however, and maynot necessarily represent the market value."

We, therefore, have to subjectively estimate the "Value in Use" of the subject's assets based on pastexperience with assets of a similar nature.

The Income Approach is especially meaningful if the assets are used to produce income, such as in thevaluation of a business. However, it still takes root from the Market Data Approach because it is an analysisof what the current market is paying by determining a comparable return that can be capitalized into acomparable purchase price.

In this report you will find as many methods, under each approach, as is reasonably applicable to valuingthe subject business. In order to arrive at a supportable value, we have chosen those methods that wouldbest apply to the purchase of the subject business as reflected by the marketplace.

The Internal Revenue Service established Revenue Ruling 59-60 as the standard for the valuation ofclosely-held companies. The following summarize the key factors to consider:

A. History and Nature of the Business

B. Economic Outlook

C. Book Value

D. Earning Capacity of the Enterprise

E. Dividend Paying Capacity of the Enterprise

F. Goodwill and Intangible Assets

G. Recent Sales of Stocks

H. Market Value of Comparable Companies

23

COMMENTS ON CERTIFICATION_______________________________________________________________________________________________

Although stated earlier with clarification, this report is a departure from the appraisal guidelines and in ouropinion must be recognized and clarified further for the reader of this report.

The term certified appraiser or certified appraisal used in this report refers to the certifications held by theappraiser who has completed this appraisal report. The appraiser has earned the various designationsfrom recognized appraisal and consulting societies, organizations and instructional institutions. Certifications are granted based on meeting strict guidelines for education, experience, examinations anddemonstrating high levels of expertise. Each certification carries with it high levels of professional ethicsand standards.

As a result of various new state and federal legislation, appraisal practice has become a regulated industryrequiring certain appraisers to become state certified by 12/31/92. This appraisal is for business valuationand does not require a state certification, nor is there one available at this time. The state of Texas and theFederal Appraisal Foundation have not developed a state certified or licensing application or examinationto meet the new laws at this time. HB270 specifies the new standards required for certified appraisals, andthe standards in this report meet federal guidelines.

Although neither the state nor federal government has required the new appraisal standards to becomeeffective for business valuation, we have completed this appraisal consistent with the state and federalguidelines for state certified or licensed appraisals. Business Evaluation Systems appraisals have met orexceeded the standards as set forth by the state and federal governments.

Further, comments concerning appraiser certifications or licensing are not required as part of appraisals. We have chosen to include these brief comments in our appraisal to assure the reader of this report that weunderstand and are in compliance with existing state and federal laws concerning appraisals.

It should be further noted that Business Evaluation Systems appraisers have exceeded therequired experience and education requirements and await the development and approval of thestate examination.

Please refer to the appraiser's qualifications exhibit to this report for additional information.

Business Evaluation Systems appraisers have earned the following professional designations:

* BCBA - Board Certified in Business Appraisal (National Society of Appraiser Specialists)* CBC - Certified Business Counselor (Institute of Certified Business Counselors)* SBA - Senior Business Analyst (Society of Business Analysts)* AAR - Accredited in Appraisal Review ( Accredited Review Appraisers Council)* CEI - Certified Environmental Inspector (Environmental Assessment Association)* BCB - Board Certified Broker (Texas Association of Business Brokers)* FCBI - "Fellow" Certified Business Intermediary (International Business Brokers Association) * SPTC - State Property Tax Consultant (Texas Department of Licensing and Regulations)* CFEA - Certified Farm Equipment Appraiser (American Society of Farm Equipment Appraisers)* CREA - Certified Real Estate Appraiser (National Association of Real Estate Appraisers)* LREB - Licensed Real Estate Broker (Texas and Nevada)* CMEA - Certified Machinery and Equipment Appraiser (Institute of National Equipment and Business Brokers)

24

CONFIDENTIALITY AGREEMENT_______________________________________________________________________________________________

Agreement and acknowledgment between the client ordering this document and Business EvaluationSystems (undersigned).

Whereas, the client agrees to furnish the undersigned certain confidential information relating to theaffairs of the client for purposes of evaluation, consulting, or related analysis:

Whereas, the undersigned agrees to review, examine, inspect, or obtain such information only for thepurposes intended and to otherwise hold such information confidential pursuant to the terms of thisagreement:

Be it known that the client has or shall furnish to the undersigned certain confidential information asrequired and may further allow the undersigned or his field representative to inspect the business of theclient and interview representatives of the clients on the following conditions:

1. The undersigned agrees to hold all confidential or proprietary information to trade secrets("information") in trust and confidence and agrees that it shall be used only for the contemplatedpurpose, shall not be used for any other purpose or disclosed to any third party.

2. At the conclusion of our discussions and upon demand by the client, all information, includingphotographs, memoranda, or written notes shall be returned to the client.

3. This information shall not be disclosed to any employee or consultant unless they agree to executeand be bound by the terms of this agreement.

4. It is understood that the undersigned shall have no obligation with respect to any informationknown by the undersigned or generally known within the industry prior to the date of thisagreement, or becomes common knowledge within the industry thereafter.

Dated:July 4, 2006

George D. AbrahamBCBA,CMEA,FCBI,SBA,BCB,AAR,CEI,SPTC,CFEA

P.O. Box 1262Dickinson, Texas 77539

(281) 337-3508FAX: (281) 534-3785

25

INTRODUCTION

I. CLIENT DATA

Mr. James G. SampleSample Paving & Excavation, Inc.222 Westheimer St.Houston, Texas 77539

II. AUTHORIZATION

Client verification and authority given to our field technician, ordering this report.

III. NATURE OF ASSIGNMENT

Determine the estimated Fair Market Value of Sample Paving & Excavation, Inc., based on a stock sale (hereinafter sometimes referred to as the "business") located in Houston, Texas.

Utilize Business Evaluation Systems national data information, exclusive to Business EvaluationSystems, and market research to prepare an opinion of value report based on resulting data andknowledge. Assumptions and limiting conditions are stated in the exhibits to the evaluation report.

IV. PURPOSE OF EVALUATION

The purpose of this report is to provide the client with an opinion of Fair Market Value for thepurpose of contemplation of sale.

V. DEFINITION OF VALUE

Fair Market Value is the price, in cash or equivalent, that a buyer could reasonably be expectedto pay, and a seller could reasonably be expected to accept, if the property were exposed for saleon the open market for a reasonable period of time, both buyer and seller being in possession ofthe pertinent facts and neither being under compulsion to act.

VI. OWNERSHIP

Ownership or title to the business and equipment appraised was not a consideration of thisassignment; it was assumed that the business appraised was the property of Sample Paving & Excavation, Inc., free and clear.

VII. ADDITIONAL INFORMATION CONTACT

For additional information, contact Mr. James G. Sample, the client. Do not contact the appraiserwithout written authorization from the client. All information contained in this report is confidential.

VIII. LOCATION OF THE BUSINESS

At the time of the evaluation, the business was located at 222 Westheimer St., Houston, TX 77539

26

IX. DOCUMENTS REVIEWED BY FIELD TECHNICIAN Financial Statements for the years 2002, 2003, 2004, and 2005 Internal Financials for the period ending March 31, 2006 Balance Sheet as of March 31, 2006 Equipment and Inventory lists X. INTERVIEWS Interviews were conducted by the field technician and furnished to Business Evaluation Systems using our forms and questionnaires. XI. ENVIRONMENTAL CONCERNS Business Evaluation Systems has made no inspections of the premises, expresses no opinions and has received no information that an environmental concern exists. XII. EVALUATION EFFECTIVE DATE

Values state are effective as of March 31, 2006. Any difference between the date this report ispresented and the effective date could have a bearing on the value opinion stated.

XIII. WHAT IS VALUED IN THIS REPORT

Business Evaluation Systems was asked to value the subject company, including all assets of thebusiness, both tangible and intangible.

1. Sample Paving & Excavation, Inc., is the valued entity and owned by its shareholders.Please refer to the Questionnaire Section of this report for a more detailed analysis ofassets, included in the valuation.

2. Rolling Stock has not been valued but is INCLUDED in this valuation.

3. Liabilities have NOT been valued and are INCLUDED in this valuation.

4. Tangible assets have NOT been valued but are INCLUDED in this valuation.

5. Intangible assets are valued and INCLUDED even though they may not be shown on thecompany's balance sheet.

6. Accounts Receivable have NOT been valued but are INCLUDED in the valuation report.

7. Real Estate and Improvements have NOT been valued by Business Evaluation Systems andare NOT INCLUDED in this report.

8. Documents listed as reviewed above have NOT been reviewed or analyzed by BusinessEvaluation Systems and any values derived from such documents or reports may be includedin this report. We have relied on the expertise of the company's financial advisors supplyingthis information to the field technician for any values used.

27

APPRAISER'S CERTIFICATION_______________________________________________________________________________________________

I HEREBY CERTIFY TO THE BEST OF MY KNOWLEDGE AND BELIEF:

1. That the statements of fact contained in this report are believed to be true and correct.

2. That the reported analysis, opinions, and conclusions are limited only by the reportedassumptions and limiting conditions, and are my personal, unbiased professional analysis,opinions, and conclusions.

3. That I have no present or prospective interest in the property that is the subject of thisreport, and I have no personal interest or bias with respect to the parties involved.

4. That my compensation is not contingent upon the reporting of a predetermined value ordirection in value that favors the cause of the client, the amount of the value estimate, theattainment of a stipulated result, or the occurrence of a subsequent event.

5. That my analysis, opinions, and conclusions were developed, and this report has beenprepared in conformity with the Uniform Standards of Professional Appraisal Practice. Departure provisions are stated in another section of this report.

6. That I have not made a personal inspection of the property that is the subject of thisreport and am relying on information provided by the field technician and the client.

7. That no one provided significant professional assistance to the person(s) signing this reportother than the field representative gathering the information for our questionnaire.

8. That this opinion of value has been performed in accordance with the code of ethics ofthe associations of which I am a member.

9. That it is my opinion that the value of the property valued is as stated in this report.

10. That the fair market value of the subject business, including all assets and reflectingmarket conditions as stated in the report on the effective date is:

$2,696,154

Date:July 4, 2006

George D. AbrahamBCBA,CMEA,FCBI,SBA,BCB,AAR,CEI,SPTC,CFEA

28

REQUIRED RATES OF RETURN - FORMING A CAPITALIZATION RATE_______________________________________________________________________________________________

To an investor, when we speak of return and rate of return, we are referring to the totalyield to the investor, reflecting all dividends, interest, or cash equivalents received, plusor minus any realized or unrealized appreciation or depreciation in the investment'svalue. Capitalizing, for which a capitalization rate is used, is a process applied to anamount representing some measure of economic income for some single period toconvert that economic income amount to an estimate of present value.

Capitalizing procedures can be used with expected, current, historical, or "normalized"(or "stabilized") measures of economic income. If growth is expected from the baselevel of economic income being capitalized, then that expected growth is reflected inthe capitalization rate.

Business Evaluation Systems has, since 1983, monitored these rates of return andcapitalization rates for almost every type of business imaginable from hundreds ofcompanies involved in the business transfer industry all across America. These are ratesthat the business transfer industry reports are required to stimulate the purchase of abusiness. Business Evaluation Systems has the largest database of theserequired rates of return in the country. Also, there are probably more theories oncapitalization rates than any other subject in valuation. With this in mind, pleaseunderstand that this discussion will leave many methods unmentioned.

The first thing to remember is that we are going to keep this brief and fairly simple. A capitalization rate (Cap Rate) can be looked at in three different ways: (1) a multiple ofearnings, (2) a percent rate of return or (3) the time by which a buyer would demand topay off the business or get his or her money back. With this in mind there are twomethods that I think most of us would agree on. The high and the low capitalizationrates for a business. The low range for a normal and profitable business is usually oneyear net profit plus the value of the assets. Most owners will make it clear that they willjust run the company for another year and then sell the assets.

The highest price is a multiple of earnings that after management compensation and debtservice is less than a money market fund. This is also logical because the buyer couldjust go to work for that company or another company and keep his or her money in asafe fund and not take the risk.

With this is mind, let's look at multiples, keeping in mind the three ways to view them. The following diagram should help:

The following diagram can be used to extrapolate a Cap Rate by years to pay off thebusiness or a multiples of earnings:

1______2______3______4______5Cap Rates or Risk Factors100% 50% 33.3% 25% 20%

29

REQUIRED RATES OF RETURN - FORMING A CAPITALIZATION RATE_______________________________________________________________________________________________

It can also be used to rate the company by looking at several areas within the companyas well as outside factors which could affect the company's future performance.

These multiples can usually mean the following:

1=100% = Drastic Outlook2=50% = Unstable Future3=33.3% = Normal4=25% = Better than normal5 =20% = Excellent, hardly any risk

Of course this is an extremely simple model but should be one of the basis of the appraiser'sassumptions. Also, realize that some industries are tempered with highly advantageoustechnological future changes. Also, some are much more desirable and have morestatus to own than others (i.e. a bank). The following risk topics (there are many more)should be researched and assigned a quantitative level of importance to the overallmodel for the above multiples:

LaborThere are many key factors to look at as far as labor is concerned. Are employees hardto find? Will key employees stay? Are they due a significant salary increase? Whateducational skills or level is required and is the labor pool such that they could be replaced?

ManagementWill management stay? What is the average age of key management? Hasmanagement been efficient?

Financial StrengthIs the company financially solid or do they have cash flow problems?

Facilities and LocationWhat is the length of the lease? Is it likely to increase? Are the facilities sufficient forthe business and possible expansion? What about the company's location? Are anymajor roadways or changes in the area likely to affect the company?

Diversity of AccountsIf the company loses one or two accounts will they be out of business? Will theaccounts stay with a new owner?

CompetitionHow strong is competition? What is the level of ease of entry into this industry? Aretechnological changes going to give a major competitor with more cash a significantadvantage?

30

REQUIRED RATES OF RETURN - FORMING A CAPITALIZATION RATE_______________________________________________________________________________________________

PredictabilityWhat has the historical financial picture shown? What would it tell a buyer as to what heor she can expect in the future?

MarketabilityHow hard would it be to sell this company? How many buyers would be interested inthis type of business?

Future OutlookAlways remember that a business is bought on the assumption of its economic benefit toits new owner. The more stable the financial future as well as other factors like technologicalchanges, environmental regulations, and public attitude affect a buyer emotionally. Thisrelates to how long the buyer is willing to risk his or her money and, therefore, how fast he or shewould expect it back and thus affecting the multiple of earnings they are willing to pay.

An illustration of this method, using a hypothetical company and assigning the multiplesabove would be as follows:

Topics: Rating:Labor 2Management 4Financial Strength 4Facilities and Location 2Diversity of Accounts 2Competition 3Predictability 4Marketability 2Future Outlook 4

____Total 27Divided by 9 topics = 3This would equal a 33.3% Cap Rate (i.e. Discretionary Cash Flow divided by 33.3% = Value of Company).

Several of the Interview Questions will also give us the data to form a Cap Rate.For instance, questions 17 and 18 ask:"What would be the minimum and maximum rates of return a buyer would expect toassume this risk?" When the Field Representative answers these questions, he is telling us hisviews on the Cap Rate. For example, if the Field Representative reports that the rates of return forQuestions 17 and 18 are 25% to 33%, we can then begin to formulate a Cap Rate. Byusing the example on page 20, a 25% rate would, of course, be a Cap Rate, but would also mean that abuyer in his (the Field Representative) area would not pay more than a multiple of four times earnings.

Therefore, we would know that a buyer, for this kind of business, in this part of thecountry, would not pay more than three to four times earnings and the Cap Rates would be25% to 33%.

31

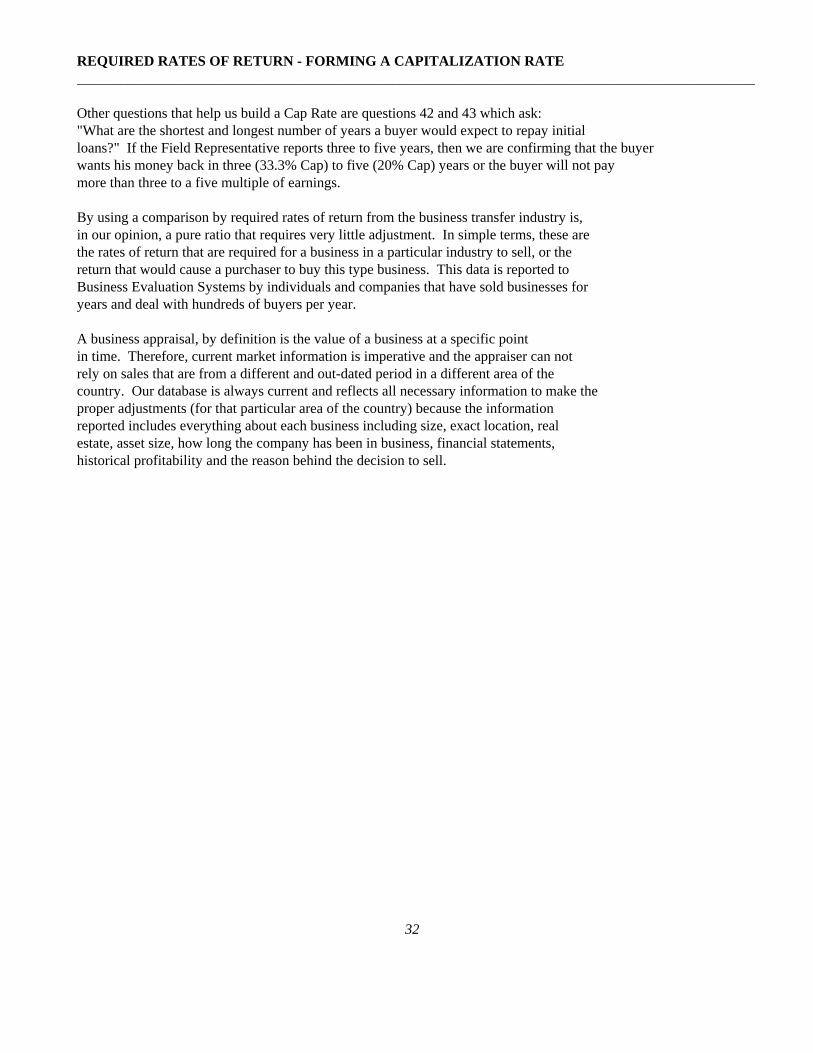

REQUIRED RATES OF RETURN - FORMING A CAPITALIZATION RATE_______________________________________________________________________________________________

Other questions that help us build a Cap Rate are questions 42 and 43 which ask:"What are the shortest and longest number of years a buyer would expect to repay initialloans?" If the Field Representative reports three to five years, then we are confirming that the buyerwants his money back in three (33.3% Cap) to five (20% Cap) years or the buyer will not paymore than three to a five multiple of earnings.

By using a comparison by required rates of return from the business transfer industry is,in our opinion, a pure ratio that requires very little adjustment. In simple terms, these arethe rates of return that are required for a business in a particular industry to sell, or thereturn that would cause a purchaser to buy this type business. This data is reported toBusiness Evaluation Systems by individuals and companies that have sold businesses foryears and deal with hundreds of buyers per year.

A business appraisal, by definition is the value of a business at a specific pointin time. Therefore, current market information is imperative and the appraiser can notrely on sales that are from a different and out-dated period in a different area of thecountry. Our database is always current and reflects all necessary information to make theproper adjustments (for that particular area of the country) because the informationreported includes everything about each business including size, exact location, realestate, asset size, how long the company has been in business, financial statements,historical profitability and the reason behind the decision to sell.

32

PRINCIPLES OF EVALUATION_______________________________________________________________________________________________

In theory, all formula calculations are simple.

Actually calculating logical financial formulas is generally simple because most of the input valuesoriginate as dollar amounts or other numerical data and can be graphically displayed as a linear curve.

However, formulas based on the emotional factors which influence a buyer are more difficult to calculatebecause feelings and desires must translate into numerical values. These values can only be manipulatedby extremely complicated mathematical functions. The graphic display of these functional relationshipsgenerally resembles standard distribution, parabolic curves.

This evaluation report has overcome the two most difficult factors: gathering the emotional data andquantifying the emotional data.

1. The first difficulty encountered when using emotionally based formulas is the gathering ofdata. The report model requires numerical data. Unfortunately, feelings and desires aregenerally expressed by actions and words.

2. To convert the qualitative emotions into quantitative data, a series of questions were designedto set up an emotional environment with a finite number of choices. Each choice is numberedand has a specific set of criteria which must be met.

3. The second major difficulty encountered was quantifying emotions through a series offormulas. Most formulas are not clearly defined with standard levels of criteria; therebyallowing the evaluator latitude in responding, based on current market conditions and theeffect they have on values. The questions and explanations in this report are rigidly wordedrequiring fewer judgments by the appraiser.

The emotional choices which might elude the evaluator can be narrowed, because bydefinition they fall into two categories: environmental and situational.

For example, consider an interest rate. An interest rate of 12% is desirable when otheravailable rates are higher but undesirable when other available rates are less. Additionally,interest rates have an absolute demand ceiling and an absolute floor. The ceiling is based onthe history and duration of high rates and the floor is dictated by the IRS.

33

EVALUATION MODELS_______________________________________________________________________________________________

A businesses value can actually be divided into five parts:A. Market value of assetsB. Historical trends of revenues, expenses and cash flowsC. The value of rights, privileges, and knowledgeD. Estimated stability in the futureE. Esthetic appeal

This evaluation report addresses all five parts of a business' value through a series of questionswhich define each of these aspects numerically. The computer manipulates the statistics and calculates asuggested price based on the most widely accepted mathematical models.

Not every method will necessarily be used in the appraisal report. The methods used in this report aredescribed below:

ASSET VALUE_______________________________________________________________________________________________

The Asset Value Method is used to determine a minimum value range for a business. That valuerepresents the estimated worth of all tangible and intangible assets.

Asset value must not be determined solely on the basis of book value or an asset's worth in itscurrent application but rather replacement value including all installation and testing costs.

Upper $1,150,000Lower $940,000

BASIC VALUE METHOD_______________________________________________________________________________________________

This method is based on two pricing formulas.

The first formula is a "rule of thumb" multiplier; one year's net cash flow plus assets at currentmarket value. The second formula begins with the current market value of assets and to this adds amultiple of the monthly discretionary income based on the number of months required to start asimilar business and bring it to a break even cash flow position.

Upper $3,070,000Lower $1,330,000

CAPITALIZATION METHOD (RETURN ON INVESTMENT)_______________________________________________________________________________________________

This method is based on a simple mathematical model which calculates a total investment based ondiscretionary cash flow divided by a rate of return associated with the level of risk.

Upper $1,790,000Lower $1,670,000

34

EVALUATION MODELS_______________________________________________________________________________________________

CRITICAL FACTORS METHOD_______________________________________________________________________________________________ This method takes into account the critical factors which will encourage or discourage a potential buyerprior to any in-depth investigation into this business. The various factors comprising this method are: 1. Percent of Down Payment This factor is based on the common belief that lending institutions generally require 20% of the total purchase price as a down payment. This factor also considers the relativity of dollars in down payment to profits. 2. Dollars of Down Payment This factor relates the absolute dollars required as a down payment to the potential number of qualified buyers with that volume of cash or other liquid assets. The larger the cash down payment the fewer qualified buyers will be available, thereby, limiting the demand and, consequently, reducing the emotional dollar value of a suggested price. 3. Interest Rate, Interest Type and Term of Years This factor relates the various loan types, loan terms and interest rates as offered to a potential buyer by the owner and any other available lending institution to the propensity of a buyer to purchase this business. 4. Industry This factor weighs the possibility of market saturation, currently predicted survival for an established business and the future stability of profits. 5. Desire This factor quantifies the emotional motivation to buy based on status, visual appeal, profitability, risk and skills required. 6. Lease This factor determines sufficient time available to repay loans and earn a reasonable return, a rate comparable to similar available spaces. 7. Utility This factor examines the alternative use of the land and buildings for sale. 8. Accounts This factor places value on the collectability of accounts receivable and the security of the clientele base. Upper $4,300,000 Lower $1,856,000

35

EVALUATION MODELS_______________________________________________________________________________________________

DEBT CAPACITY METHOD_______________________________________________________________________________________________

This method of evaluation is purely a mathematical financial model. Direct business cash expensesare deducted from direct business cash revenues to determine discretionary cash flow.Deductions are then made for an operator's salary and the real depreciation cost of assets. Theresult is discretionary cash for debt service.

A present value table will calculate the future value of a series of payments. The figure generatedis the debt service this business could handle given the current level of discretionary cash.

Most evaluators agree that any future increases in revenues while under the management of anew owner belong to that new owner. If the previous owner had generated more revenue thesuggested price would reflect this.

Upper $2,150,000Lower $1,520,000

COMPARABLE SALES METHOD_______________________________________________________________________________________________

This method is based on ratios generated by actual sales found in the specific industry.

The ratios used for the subject company are usually a price to earnings ratio or can be arevenue to selling price ratio. In determining the most meaningfull ratio, the appraiser must takeinto consideration the date of sale, location, comparable size of the sales researched.

Upper $2,700,000Lower $1,380,000

INDUSTRY RISK FACTOR METHOD_______________________________________________________________________________________________

This method is based on a series of weighted factors which resemble many of the functionspreviously used in the weighted and critical factors methods. However, in spite of oversimplification and the inability of the functions to shift with changing economic conditions, theseformulas have been included because they are routinely used as part of a curriculum for thepotential buyers.

These formulas are generally of a hyperbolic or parabolic nature but in actual use are staticbecause the mathematics required to adjust these curves for the dynamics of an economy wouldbe impossible to complete manually.

36

EVALUATION MODELS_______________________________________________________________________________________________

INDUSTRY RISK FACTOR METHOD (continued)_______________________________________________________________________________________________

The following are actual computed categories:

Finance YearsThis factor assumes the greater the loan period, the more a buyer will pay.

Financing RateThis factor considers interest rates and types. It decreases the amount payable to a selleras the cost of doing business, interest cost, etc., increases.

Years OperatingThis factor assumes each year of survival indicates a greater chance of future survival andpays for years survived to date.

Consulting TimeThis factor pays for education time from a seller.

Employees This factor pays less for more employees assuming a larger work force creates labor problems.

Net CashThe greater a businesses discretionary cash, the more a buyer should be willing to pay.

Local EconomyThe better the economy the greater the security of future revenues and demand so theprice will be higher.

Labor Market This factor assumes labor is a major cost and if the labor market is soft for this business, labor cost will not rise as quickly and profitability is more likely. The converse is also

assumed true.

This factor also assumes if a business requires a high level of skills it is a higher risk andworth less to a potential buyer.

Union StrengthThis factor analyzes how an outside organization can control your business. The lesscontrol the owner has the less a person should pay.

Age of IndustryThis factor pays for stability and longevity in proportion to an industry's age.

37

EVALUATION MODELS_______________________________________________________________________________________________

INDUSTRY RISK FACTOR METHOD (continued)_______________________________________________________________________________________________

National EconomyThis factor assumes a growing economy increases demand and prices. Conversely, adeclining economy decreases demand for a particular business and its price.

Industry MarketThis factor looks at the future markets for the products or services of this company andindustry. The security or risk assigned to the future will directly raise or lower anysuggested price.

Upper $1,790,000Lower $1,580,000

WEIGHTED FACTORS OR EMOTIONAL FACTORING_______________________________________________________________________________________________

Emotionally motivated choices can be displayed mathematically through the use of parabolic andhyperbolic functions. These functions seem to simulate how emotions relate current conditions toabsolute conditions.

The following factors comprise the key factors which will be functionalized: