Embed Size (px)

Citation preview

1-1

Dr. Hisham Madi

1-2

Main references Supporting the Course

Reeve, J. M., Warren, C. S. & Duchac, J. E. (2007). Principles of Accounting. (22nd ed.). Canada: Thomson South-Western.

Horngren, HT., Datar, S.M. and Rajan, M (2012). Cost Accounting A Managerial Emphasis (14th) Prentic Hall.

1-3

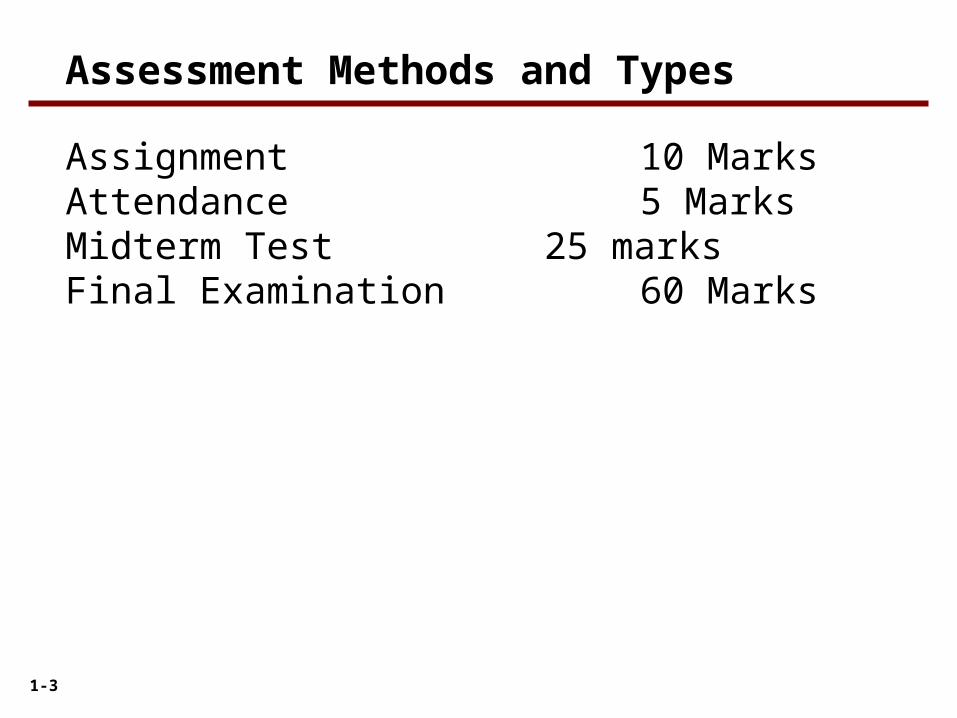

Assessment Methods and Types

Assignment 10 MarksAttendance 5 Marks Midterm Test 25 marksFinal Examination 60 Marks

1-4

Cost Accounting

Classification of cost

Costs control

Manufactured cost

Job Orders Cost

Activity Based Costing

Cost Volume Process

Content

1-5

What is A Cost

Accountants define cost as a resource sacrificed or forgone to achieve a specific objective.

A cost is a payment of cash or the commitment to pay cash in the future for the purpose of generating revenues.

A cost is usually measured as the monetary amount that must be paid to acquire goods or services.

Cash (or credit) used to purchase equipment is the cost of the equipment.

1-6

What is A Cost

Costs are often classified by their relationship to a segment of operations, called a cost object

A cost object may be a product, a sales territory, a department, or an activity, such as research and development

1-7

Direct Costs and Indirect Costs

Direct costs are identified with and can be traced to a cost object.The cost of wood (materials) used by Legend Guitars in manufacturing a guitar is a direct cost of the guitar.

1-8

Direct Costs and Indirect Costs

Indirect costs Cannot be identified with or traced to a cost object.The salaries of the Legend Guitars production supervisors are indirect costs of producing a guitarWhile the production supervisors contribute to the production of a guitar, their salaries cannot be identified with or traced to any individual guitar.

1-9

Business Sectors and Cost

Manufacturing-sector companies Purchase materials and components and convert them into various finished goods.

Merchandising-sector companies Purchase and then sell tangible products without changing their basic form. This sector includes companies engaged in retailing (Amazon)

Service-sector companies Provide services (intangible products)—for example, legal advice or audits—to their customers (accounting firms)

1-10

FactoryFactoryOverheadOverheadFactoryFactory

OverheadOverhead

DirectMaterials

DirectMaterials

DirectDirectLaborLaborDirectDirectLaborLabor

ProductProductCostsCosts

ProductProductCostsCosts

Materials that

are converted into finished products

The cost of labor directly involved in converting material

into the product.

Manufacturing costs other than direct materials and direct labor.

Manufacturing Costs

1-11

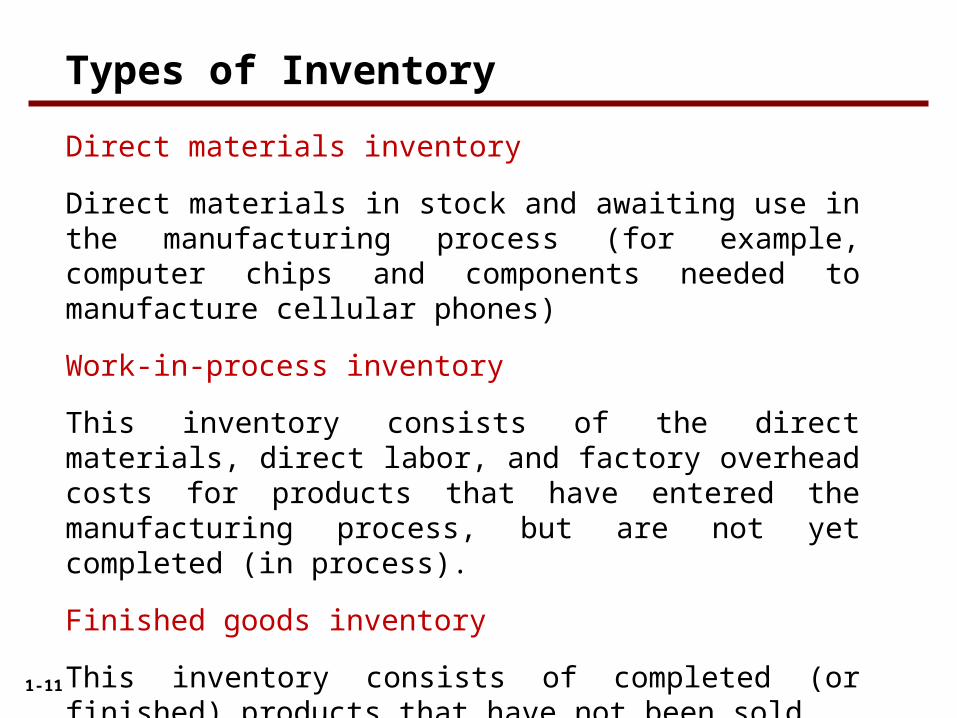

Direct materials inventory

Direct materials in stock and awaiting use in the manufacturing process (for example, computer chips and components needed to manufacture cellular phones)

Work-in-process inventory

This inventory consists of the direct materials, direct labor, and factory overhead costs for products that have entered the manufacturing process, but are not yet completed (in process).

Finished goods inventory

This inventory consists of completed (or finished) products that have not been sold.

Types of Inventory

1-12

are all costs of a product that are considered as assets in the balance sheet when they are incurred and that become cost of goods sold only when the product is sold.

Costs of direct materials, such as computer chips, issued to production (from direct material inventory),direct manufacturing labor costs, and manufacturing overhead costs create new assets, starting as work in process and becoming finished goods

Manufacturing costs are included in work-in-process inventory and in finished goods inventory (they are “inventoried”) to accumulate the costs of creating these assets

Inventoriable Costs

1-13

Product Costs and Period Costs

Product costs Consist of manufacturing costs: direct materials, direct labor, and factory overhead.

Period costs Consist of selling and administrative expenses. Period costs, such as marketing, distribution and customer service costs, are treated as expenses of the accounting period in which they are incurred because they are expected to benefit revenues in that period and are not expected to benefit revenues in future periods

1-14

Examples of Product Costs and Period Costs—Legend Guitars

1-15

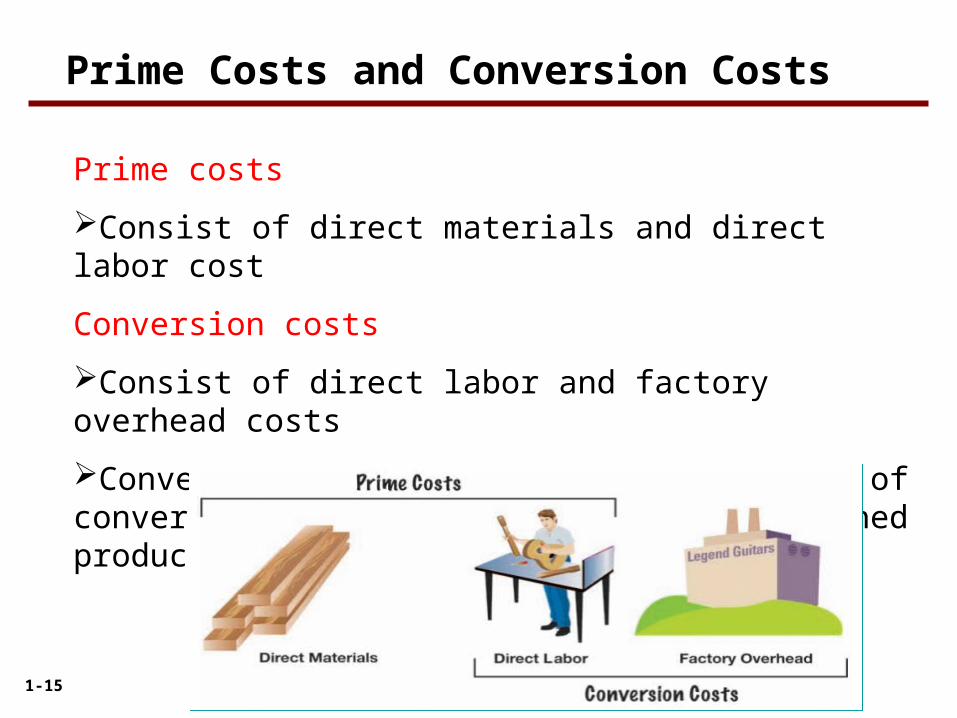

Prime Costs and Conversion Costs

Prime costs

Consist of direct materials and direct labor cost

Conversion costs

Consist of direct labor and factory overhead costs

Conversion costs are the costs of converting the materials into a finished product.

1-16

Financial Statements for a Manufacturing Business

Income Statement for a Manufacturing Company

1-17

Cost of Goods Manufactured

1-18

To illustrate, the following data for Legend Guitars are used:

Financial Statements for a Manufacturing Business

1-19

Financial Statements for a Manufacturing Business

Determine the cost of materials used. Determine the total manufacturing costs incurred Determine the cost of goods manufactured.

The cost of materials used in production is determined as follows:

Step 1

Step 2

1-20

Financial Statements for a Manufacturing Business

Determine the cost of materials used. Determine the total manufacturing costs incurred Determine the cost of goods manufactured.

The cost of materials used in production is determined as follows:

Step 3

1-21

Flow of Manufacturing Costs

1-22