Embed Size (px)

Citation preview

07 January 2009 An Introduction to Customs

1

An Introduction toIndian Customs(Laws and Procedures)

07 January 2009Essar House, Mahalaxmi

By K. R. Choudhary

07 January 2009 An Introduction to Customs 2

An Introduction to Customs

The purpose, objective and design of the presentation

Background and History

Direct and Indirect Taxation in independent India

Growth path of Customs Duty in Independent India

07 January 2009 An Introduction to Customs 3

The Beginning

As per ancient customs, a merchant entering a kingdom

with his goods ,had to make a suitable gift to king. In the

course of time, this ‘custom’ was formalized into Customs

Duty. This is collected on goods on imports (occasionally

on export goods too)

07 January 2009 An Introduction to Customs 4

Index

Customs Act Territorial Waters of India Indian Customs Water High Sea Import Customs House Agent Import Procedure Documents for Imports Advance Bill of Entry Classification Valuation of Imported goods for the purpose of Customs Act Date of determination of Rate of Duty Exchange Rate

07 January 2009 An Introduction to Customs 5

Index (continued)

Types of Customs Duty leviable Anti Dumping Duty Demurrage Calculation of Customs Duty Provisional Assessment Interest on delayed payment Exemptions Remission Relinquishing Title Transshipment of Goods (TP) Warehousing Procedure for warehousing Details of Licenses High Sea Sales Procedure at Custom House (Flow of Documents) Re-import of goods

07 January 2009 An Introduction to Customs 6

Customs Act

1. Customs Act 1962 – Is the main Act, which provides for levy and collection of Duty, Import / Export procedure, Prohibition, Penalties, Offences etc.

2. Customs Tariff Act 1975 – Is for the classification and rates of Duty for Import and Export

3. Rules under Customs Act – Under section 156 of Customs Act, 1962, Central Government has been empowered to make rules, consistent with Provisions of the Act

4. Notification under Customs Act – Various sections authorize Central Government to issue notifications

5. Board Circulars – Are instructions and directions to Customs officials

6. Public Notice – Issued by Commissioner of Customs. Can be issued for local requirement too.

07 January 2009 An Introduction to Customs 7

Territorial Waters of India

Territorial waters pertain to that portion of sea which is adjacent to the shores of a country

The territorial waters extend up to 12 nautical miles from the base line on the coast of India. (Any bay, gulf, harbor, creek, tidal water constitute Territorial Waters)

1 Nautical Mile = 1.1515 miles = 1.853 kms

07 January 2009 An Introduction to Customs 8

Indian Customs Waters

1. Indian Customs Water extends up to 12 nautical miles beyond territorial waters i.e. 24 nautical miles from the nearest point of base line

2. Significance of Indian Customs Water A Customs Officer has the powers to arrest a person

in India or within Indian Customs Water A Customs Officer can stop or search any vessel

within Indian Customs Water

07 January 2009 An Introduction to Customs 9

High Sea

The open sea of the

world outside the Territorial

Waters of any nation

Beyond 200 nautical miles

from the base line

of any country

07 January 2009 An Introduction to Customs 10

Imports

Import with its grammatical variation and cognate expression, means bringing into India from a place outside India

Import is completed only when goods cross the Customs barrier

The taxable event is the day of crossing of Customs barrier and not on the date when goods landed in India or had entered Territorial Waters

In the case of goods which are in the warehouse the customs barrier would be crossed when they are sought to be taken out of the Customs and brought to the mass of goods in the country

07 January 2009 An Introduction to Customs 11

Customs House Agent (CHA)

In order to assist importer and exporter, the services of CHA or Clearing Agents are available at international ports and airports

They are a body of professional experts duly licensed by Commissioner of Customs

07 January 2009 An Introduction to Customs 12

Import Procedure

Import General Manifest (IGM): A person in-charge of Vessel (i.e. Shipping Agent / Freight Forwarders etc.) should submit IGM – i.e. details of cargo to be unloaded, goods to be transshipped etc.

Bill of Entry: Importer should file Bill of Entry giving details of goods to be cleared from customs. Date of filing of Bill of entry is relevant for deciding Duty liability

OR

Warehousing – Keeping in warehouse without payment of Duty and later clearing on payment of Duty when required

07 January 2009 An Introduction to Customs 13

Documents for Imports

1. Bill of Entry – Its types are: (for Manual Clearance) White Bill of Entry for Home Consumption Yellow Bill of Entry for Warehousing Green Bill of Entry for Ex Bond

2. Invoice & Packing list

3. Import License (wherever necessary)

4. Certificate of country of origin, where preferential rate is claimed

5. Insurance Memo / Policy

6. Bill of Lading / Airway bill OR Delivery Order

07 January 2009 An Introduction to Customs 14

Advance Bill Of Entry

It is permissible to file the Import Bill of Entry 30 days in advance of the expected date of arrival of the concerned ship or aircraft. The intention is that this period may be utilized for sorting out tariff classification, valuation and ITC formalities

If the ship / aircraft does not arrive within 30 days , the advance cleared Bill of Entry would cease to be a legal document and a fresh Bill of Entry would have to be filed

Here Rate of Exchange and Rate of Duty etc. would have to be regulated by the date of presentation of the new Bill of Entry

07 January 2009 An Introduction to Customs 15

Classification

1. Import and export goods are to be classified according to the tariff item number mentioned against them in the customs tariff. This is an unique 8 digit code for all items based largely on the international system viz., Harmonized System of Nomenclature (HSN) adopted by almost all countries

2. Onus to establish tariff classification of goods is on the Department 3. Parameters for determination of classifications of goods are:

HSN along with Explanatory Notes provide a safe guide for interpretation of an entry

Equal importance to be given to Rules of Interpretation of Tariff Functional utility, design, shape and predominant usage have

also got to be taken into account Aforesaid aids are more important than names used in trade or

common parlance Classification determined on bond bill of entry at the time of

warehousing shall remain undisturbed except in case of a misdeclaration

07 January 2009 An Introduction to Customs 16

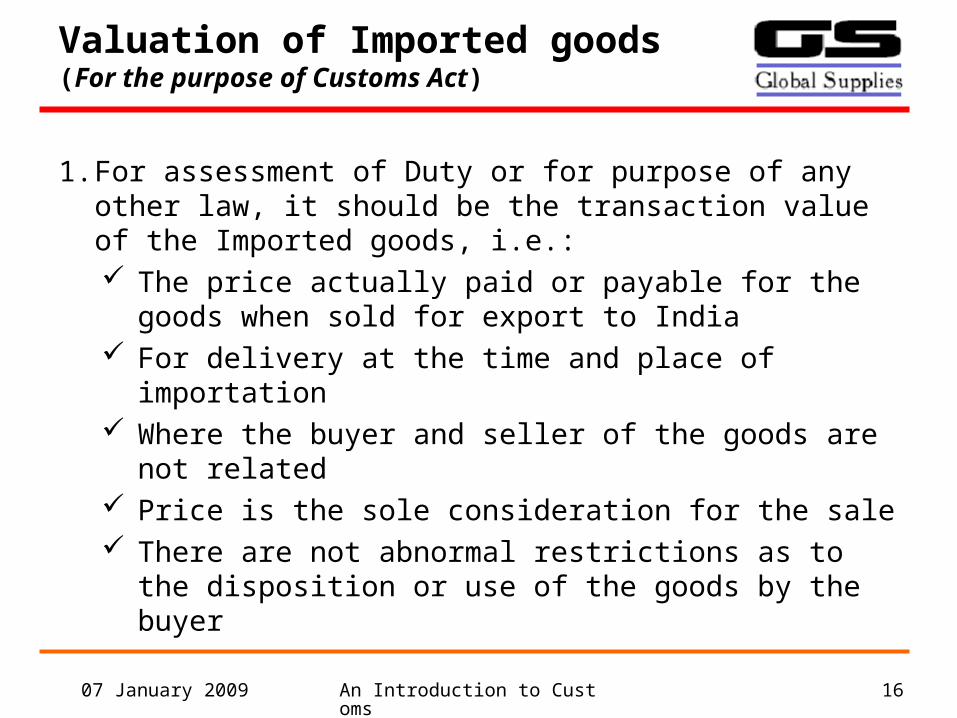

Valuation of Imported goods(For the purpose of Customs Act)

1. For assessment of Duty or for purpose of any other law, it should be the transaction value of the Imported goods, i.e.: The price actually paid or payable for the goods

when sold for export to India For delivery at the time and place of importation Where the buyer and seller of the goods are not

related Price is the sole consideration for the sale There are not abnormal restrictions as to the

disposition or use of the goods by the buyer

07 January 2009 An Introduction to Customs 17

Valuation of Imported goods(For the purpose of Customs Act) - continued

The transaction value includes the amount paid or payable for costsand service including: Commission and brokerage, except buying commissions Engineering Design work Royalties and license fees related to the imported goods Cost of transportation to the place of importation including shift

Demurrage charges Insurance Loading Unloading Handling charges Cost of containers and Cost packing (labor / materials)

07 January 2009 An Introduction to Customs 18

Date for Determination of Rate Of Duty

The rate which is in force on the date of presentation of Bill

of Entry for home consumption will be the rate applicable.

However there are two exemptions to it: In case the Bill of Entry has been filed in advance of

entry inwards of the vessel or the arrival of the aircraft, the crucial date will be date of entry inwards of the vessel or the date of arrival of the aircraft

Secondly, in the case of clearance of goods from a

bonded warehouse, the date of presentation of the ex bond bill of entry for home consumption is the crucial date.

07 January 2009 An Introduction to Customs 19

Exchange Rate

Exchange Rate is notified by the Central Board of Excise and Customs (CBEC) and is the one in force on the date of presentation of the Bill of Entry (for home consumption or for warehousing)

CBEC is the apex Administrative Body for Indirect Taxation in India

07 January 2009 An Introduction to Customs 20

Types of Customs Duty Leviable

1. Basic Duty: It may be at the standard rate or in the case of Import from some countries, at the preferential rate

2. Additional Customs Duty: Additional Customs Duty, equal to central excise Duty, is leviable

on like goods produced or manufactured in India. The MRP based valuation prevailing under Central excise is extended to Customs too

Is also referred to as Countervailing Duty (CVD). It is payable only if the imported article is such , if produced in India, its process of production would amount to ‘manufacture’ as per the definition in Central Excise Act 1944

Additional customs Duty is calculated on a value base of aggregate of value of the goods including landing charges and basic Customs Duty. In order to counter balance the burden of input Excise Duty

07 January 2009 An Introduction to Customs 21

Types of Customs Duty Leviable (continued)

3. Special Additional Duty of Customs : In order to counter balance various internal taxes like Sales Tax and VAT and to provide a level playing field to indigenous goods which have to bear these taxes.

4. Cess: A Duty levied for specified purpose. Presently HE Cess and SHE Cess

5. If goods are fully exempted from Duty or are chargeable to nil Duty or are cleared without payment of Duty under prescribed procedure such as clearance under bond, no Cess would be leviable

07 January 2009 An Introduction to Customs 22

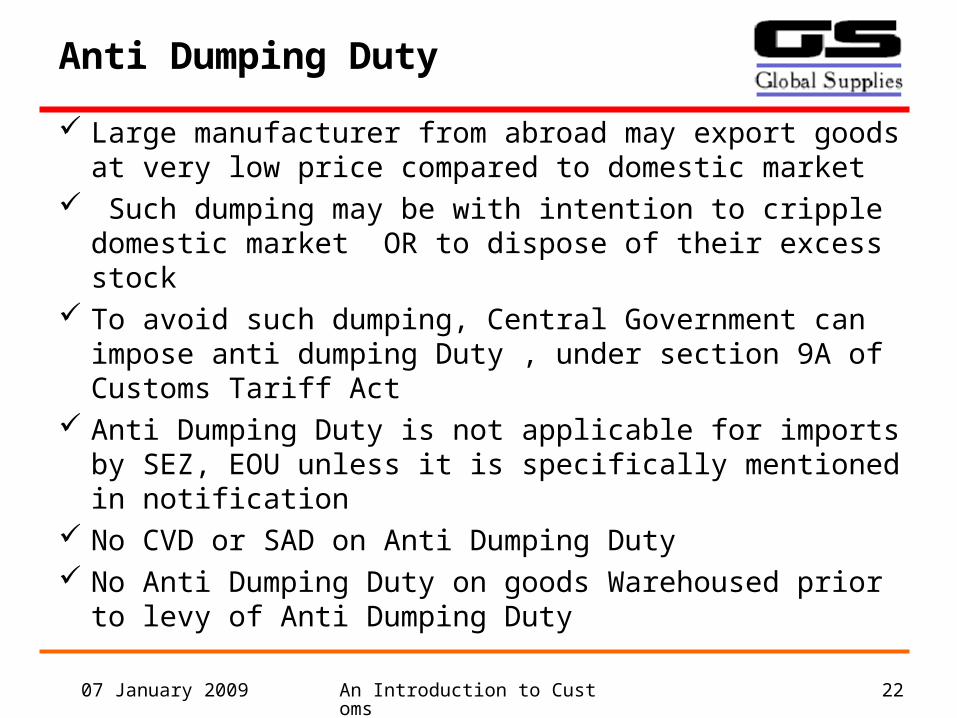

Anti Dumping Duty

Large manufacturer from abroad may export goods at very low price compared to domestic market

Such dumping may be with intention to cripple domestic market OR to dispose of their excess stock

To avoid such dumping, Central Government can impose anti dumping Duty , under section 9A of Customs Tariff Act

Anti Dumping Duty is not applicable for imports by SEZ, EOU unless it is specifically mentioned in notification

No CVD or SAD on Anti Dumping Duty No Anti Dumping Duty on goods Warehoused prior to

levy of Anti Dumping Duty

07 January 2009 An Introduction to Customs 23

Demurrage

Demurrage is a penal amount ,payable to the Port Trust Authorities, if the goods are not cleared from port within 3 working days after assessment

Option available to the importer for avoiding heavy demurrage on the goods pending resolution on the point of doubt or dispute, is to put the goods in bond under Section 49 or clear the goods on provisional assessment basis

If assessment is delayed due to Customs formalities, such demurrages may be remitted by Port Trust Authorities on the basis of a detention certificate issued by Customs

07 January 2009 An Introduction to Customs 24

Calculation of Customs Duty

Duty Rate% Amount Total Duty

a) Assessable Value Rs.10000 10000

b) Basic Custom Duty 7.5% 750 750

c) Sub Total for Calculating CVD (a+b) 10750

d) CVD @ 10% ‘ c ‘ 10% 1075 1075

e) Higher Education Cess of Excise – 2% of ‘d’ 2% 21.50 21.50

f) SHE Cess of excise – 1% of ‘d’ 1% 10.75 10.75

g) Sub total for Education Cess on Customs ‘B+D+E+F’

1857.25

h) Education Cess of Customs 2% of ‘g’ 2% 37.15 37.15

i) SHE Cess of Customs – 1% of ‘G’ 1% 18.57 18.57

j) Sub total for SAD a+c+d+e+f+h+i 11912.97

k) Special CVD – 4% of ‘j’ 4 % 476.52 476.52

l) Total Duty 2389.49

07 January 2009 An Introduction to Customs 25

Provisional Assessment

If the goods are required to be tested or there is a dispute regarding valuation, classification or there is a requirement of import license, there is provision to make a provisional assessment / clearance

It is subject to execution of bond with security (usually with Bank Guarantee) by the importer for the Duty difference after taking Assistant Commissioner’s Order

Penalty is not imposed when an Assessment is Provisional

07 January 2009 An Introduction to Customs 26

Interest on Delayed Payment

Under Section 47 of Customs Act, 1962 interest is payable when import Duty is not deposited within five days (excluding holidays) after assessment of the goods

Interest is payable at the rate of 15% per annum

07 January 2009 An Introduction to Customs 27

Exemptions

The Central Government has the power under Section 25 of Customs

Act, 1962 to exempt, in public interest, specified goods from levy of

Customs Duty by issue of notifications: Where there are two exemption notifications, one general and the other specific,

which cover the goods in question, the Assessee is entitled to the benefit of that one which gives him greater relief

Strict construction of the exemption notification cannot be at expense of object and purpose of the notification and ignoring words used therein to unjustifiably deny the exemption

Exemption from Customs Duty means exemption only from basic Customs Duty. Exemption from Excise Duty has the effect of exempting additional Duty of customs. Onus to establish eligibility to the exemption notification is on the Assessee

Accessory when imported with the machines is not eligible to exemption unless that accessory has expressly been included in the exemption notification

07 January 2009 An Introduction to Customs 28

Remission

Remission of Duty is available if imported goods are lost, pilfered or destroyed at any time before clearance for home consumption

The same principle applies also to goods deposited in a bonded warehouse

07 January 2009 An Introduction to Customs 29

Relinquishing Of The Title

The owner has also the right to relinquish his title to the goods (if they are not involved in an offence) at any time before an order for clearance of goods for home consumption has been made

Thereupon his liability to Duty or redemption fine ends

07 January 2009 An Introduction to Customs 30

Transshipment of Goods (TP)

Goods imported at any Customs station, can be transshipped without payment of Duty

Goods to be transshipped must be specified in IGM (Import General Manifest)

A Mother Bond (like a Running Bond) with security of 15%of bond value, is taken from the carriers. Security is taken separately for each trip and released on safe landing of the container in that trip at destination ICDs / CFSs

07 January 2009 An Introduction to Customs 31

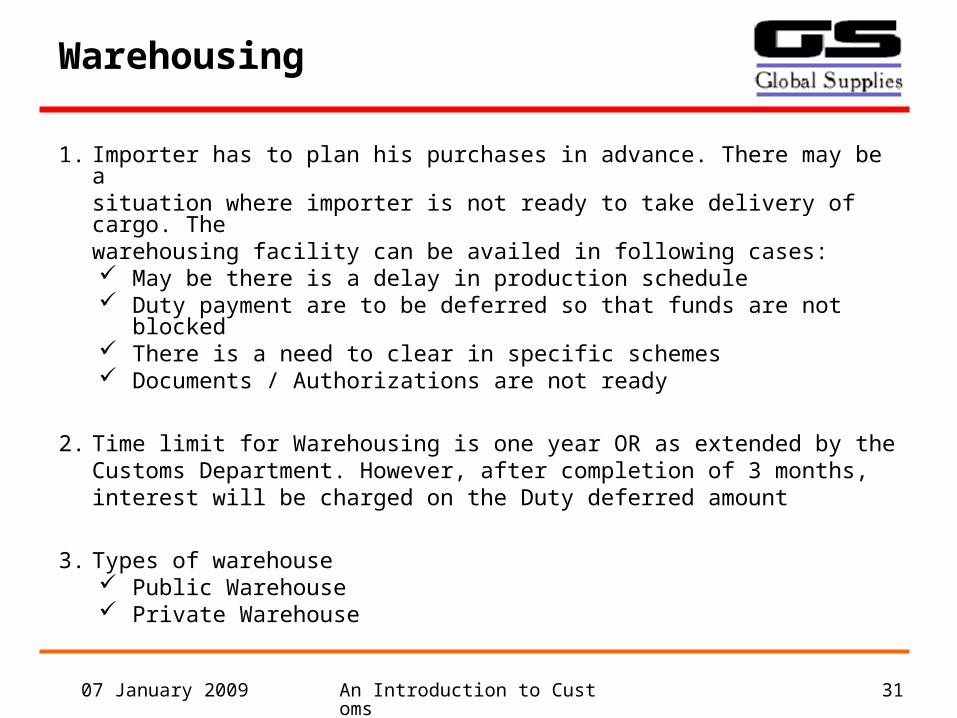

Warehousing

1. Importer has to plan his purchases in advance. There may be a situation where importer is not ready to take delivery of cargo. The warehousing facility can be availed in following cases: May be there is a delay in production schedule Duty payment are to be deferred so that funds are not blocked There is a need to clear in specific schemes Documents / Authorizations are not ready

2. Time limit for Warehousing is one year OR as extended by the Customs Department. However, after completion of 3 months, interest will be charged on the Duty deferred amount

3. Types of warehouse Public Warehouse Private Warehouse

07 January 2009 An Introduction to Customs 32

Procedure for Warehousing

1. All goods imported through Seaport / Airport can be warehoused, on submission of Bill of Entry for warehousing

2. Documents required for filing the Bill of Entry with Customs for Normal clearance or for warehousing: Signed Commercial Invoice Packing list Bill of lading or Airway Bill Purchase Order copy or Letter Of Credit copy Catalogue, Technical write-up in case of machineries Separate split up value of spares and components

07 January 2009 An Introduction to Customs 33

Details of Licenses

Export Promotion Capital Goods scheme (EPCG) Under this scheme a license holder can import capital

goods (i.e. plant, machinery, equipment, components, spare parts)

Customs Duty of 3% without CVD and SAD EPCG Authorization is valid for 36 months Obligation: Importer has to fulfill export obligation equal

to 8 times of Duty saved over the period of 8 years Non-fulfillment of Obligation: If goods are not exported

then differential customs Duty plus 15% interest is payable

07 January 2009 An Introduction to Customs 34

Details of Licenses

1. Duty Entitlement Pass Book (DEPB) This scheme is on post exportation basis DEPB holder is entitled to import all raw material,

components etc (Duty free) Capital Goods cannot be imported under DEPB

2. Advance Authorization: Inputs required to manufacture export products can be imported without payment of Duty Validity of license is 24 months The material imported under Advance Authorization is

not transferable even after completion of export obligation

07 January 2009 An Introduction to Customs 35

High Sea Sales (HSS)

High Sea sales (HSS) is a sale carried out by the original consignee to another buyer while the goods are yet on high seas

HSS Contract / Agreement should be signed after dispatch of goods from origin & prior to their arrival at destination. The agreement should be on stamp paper. On concluding the HSS agreement, the B/L should be endorsed in favor of the new buyer

The IGM should be filed by the carrier in the name of the HSS buyer

Sometimes, HSS buyers buy goods after their arrival. Such sale are not HSSs.

HSS goods are entitled to classification, rates of Duty and all notification benefits as would be applicable to similar import goods on normal sale

07 January 2009 An Introduction to Customs 36

Procedure at Customs House (Flow of documents)

Noting of Bill of Entry Filing of Bill of Entry Assessment Pre Audit Duty Payment / Bond (warehousing) Examination of Cargo Out of charge permission Delivery

07 January 2009 An Introduction to Customs 37

Re-import of Goods

If the same goods which were exported are re-imported within 3 years by the same person, Customs Duty is payable which will be equal to the Duty drawback claimed plus excise duties which were not paid. Basic principle being export incentives obtained at the time of export will be recovered

No Customs Duty will be payable if goods are re-imported for repairs/reconditioning (within 3 years from export)

If imported goods are sent abroad for repairs, then, Duty will be payable on fair charges of repairs including cost of materials

In case of goods exported under the EPCG scheme, re-importation should take place within one year (extendable by another year by the Commissioner) provided the period of full export performance under the EPCG Scheme should not have expired