Embed Size (px)

Citation preview

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 1/18

Pakistan Power Sector Structureand Regulations

Presentedby

Mr. Zafar Ali Khan, MemberNational Electric Power Regulatory Authority, Pakistan

March 20, 2007

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 2/18

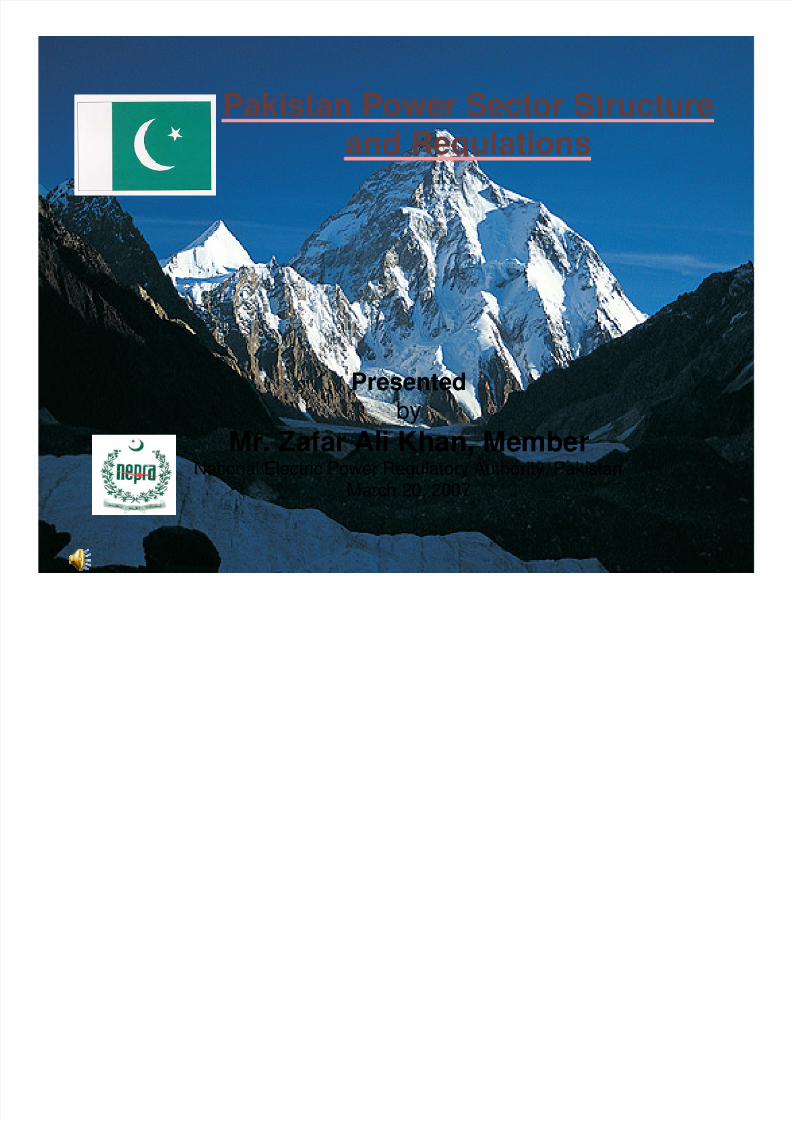

MARDANWARSAK

BANNU

DAUDKHEL

BURHANNEW RAWAT

I.S.P.R

MANGLA

TARBELA

GAKHAR

SAHOWALA

K.S.KAKU

RAVI

JAPAN

KEL

N.ABAD

SABA

YOUSAF WALA

VEHARI

KAPCO

ROUSCH

UCH

AES

N.G.P.SM.GARH

GUDDU

LIBERTY

DADU

HALARD

LAKHRA

JAMSHORO

KOTRI

HUBCO

KDA-33(KESC)

500 kV Grid Station

220 kV Grid Station500/220 kV Grid Station

Hydel Power Station

Thermal Power Station

IPPs at 220, 500 kV

IPPs at 132 kV

500 kV T/LINE

220 kV T/LINE

(240)

(3408)

(1000)

(107)

(120)

(195)

(1350)

(310)

CHEP

(184)

(355)

(1348)

(695)

HCPC(126)

(548)

(1655)

(212)

(150)

(850)

(174)(1200)

GAZI BAROTHA

(1450)

CHASNUPP

GATTI

BUND RD:

M.GARHGUDDU

JAMSHORO

PAKISTANPAKISTAN

TAPAL

G.AHMAD

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 3/18

Pakistan Power Structureand Regulations

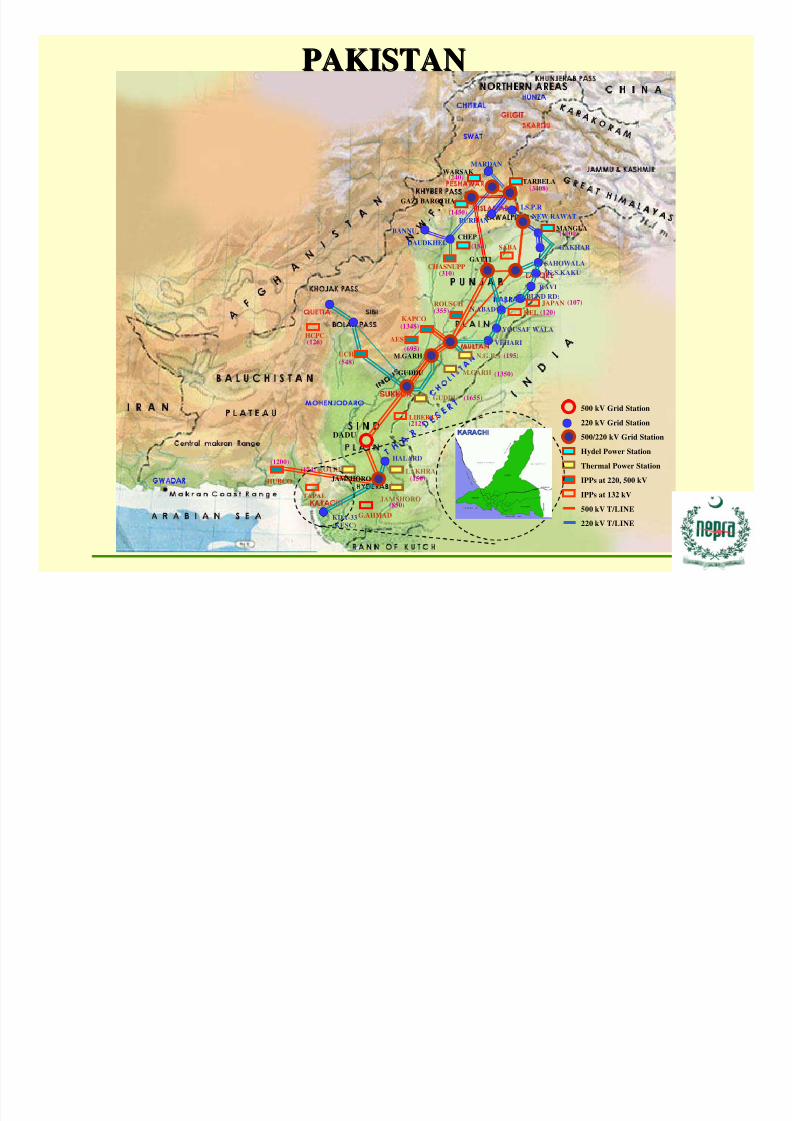

Why Reform?

Low electricity access-approx.60% population High system losses, transmission constraints, unreliable

service loaded with irrational tariff

Poor financial position of power utility companies

Power shortages from 2006-07 Uncoordinated efforts by the stakeholders with

conflicting goals

Heavy investments required for additional generationand improvements in Transmission and DistributionSystems

Public Sector resources insufficient for investment needs

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 4/18

Thermal Power

Stations

Thermal Power

Stations

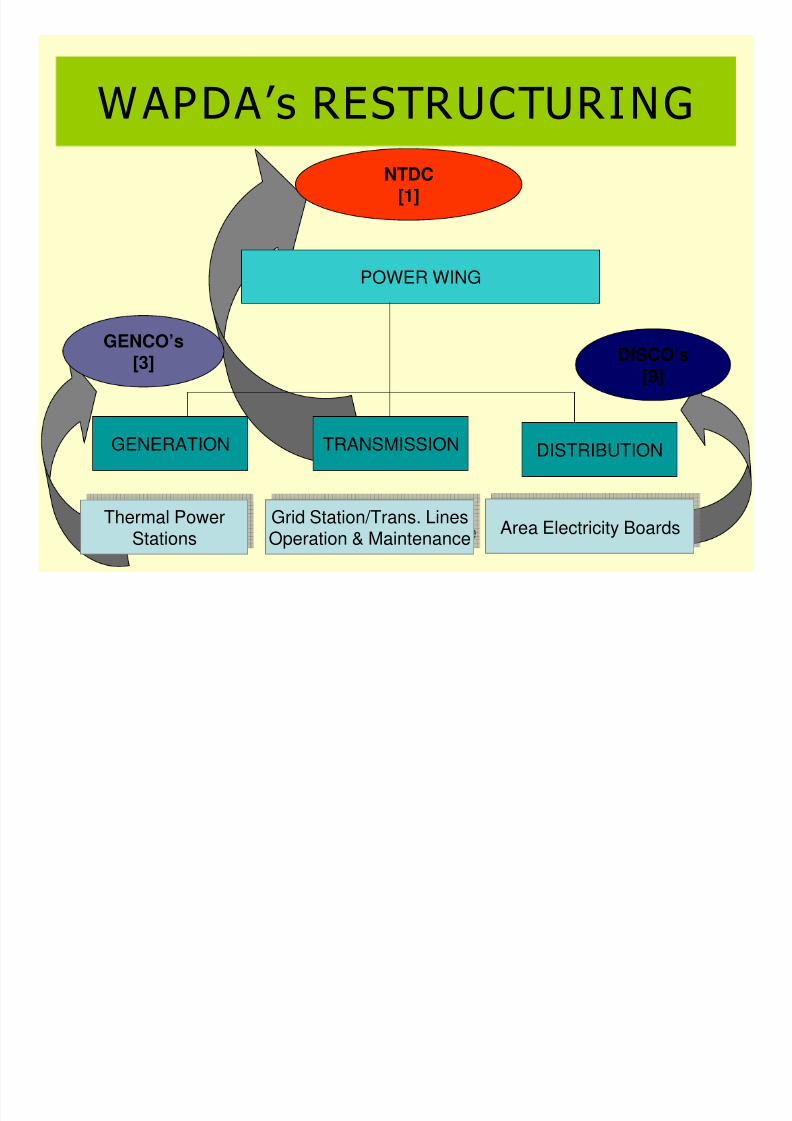

WAPDA’s RESTRUCTURINGNTDC

[1]

DISCO’s[9]

GENCO’s[3]

POWER WING

GENERATION DISTRIBUTIONTRANSMISSION

Grid Station/Trans. Lines

Operation & Maintenance

Grid Station/Trans. Lines

Operation & MaintenanceArea Electricity Boards

Area Electricity Boards

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 5/18

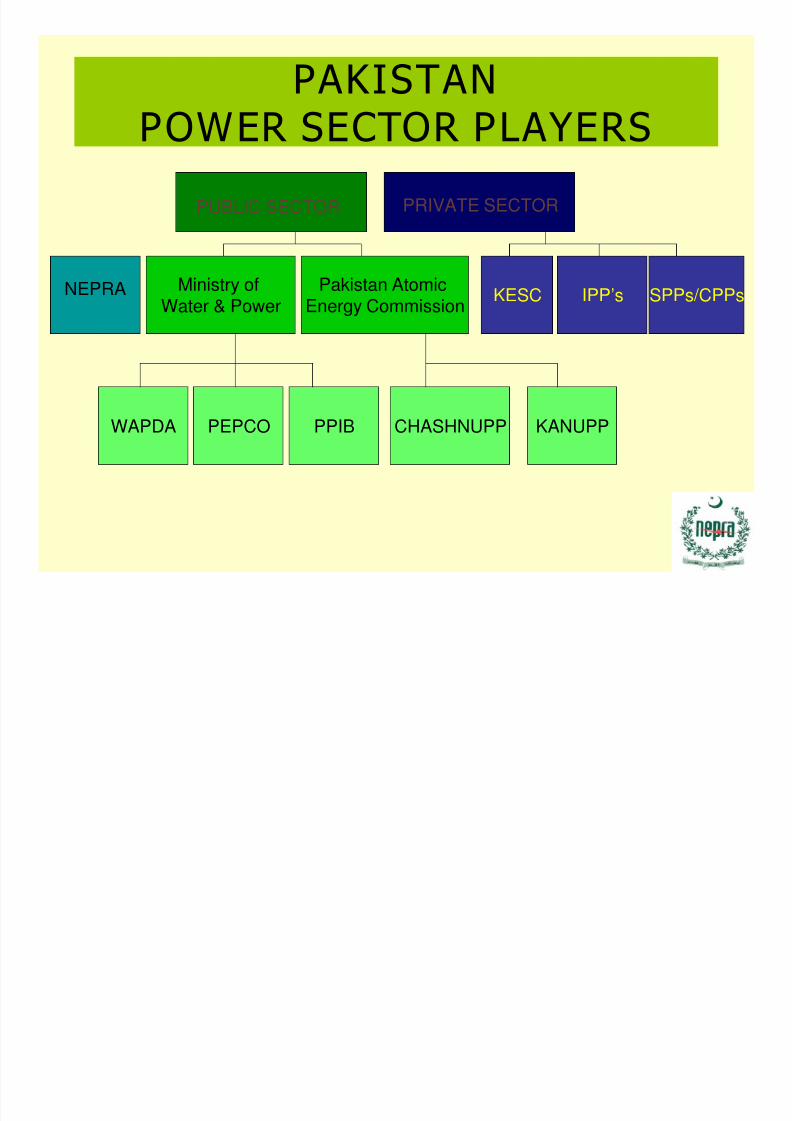

PAKISTANPOWER SECTOR PLAYERS

PUBLIC SECTOR PRIVATE SECTOR

NEPRA Ministry ofWater & Power

Pakistan AtomicEnergy Commission

KESC IPP’s SPPs/CPPs

CHASHNUPPPPIBPEPCOWAPDA KANUPP

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 6/18

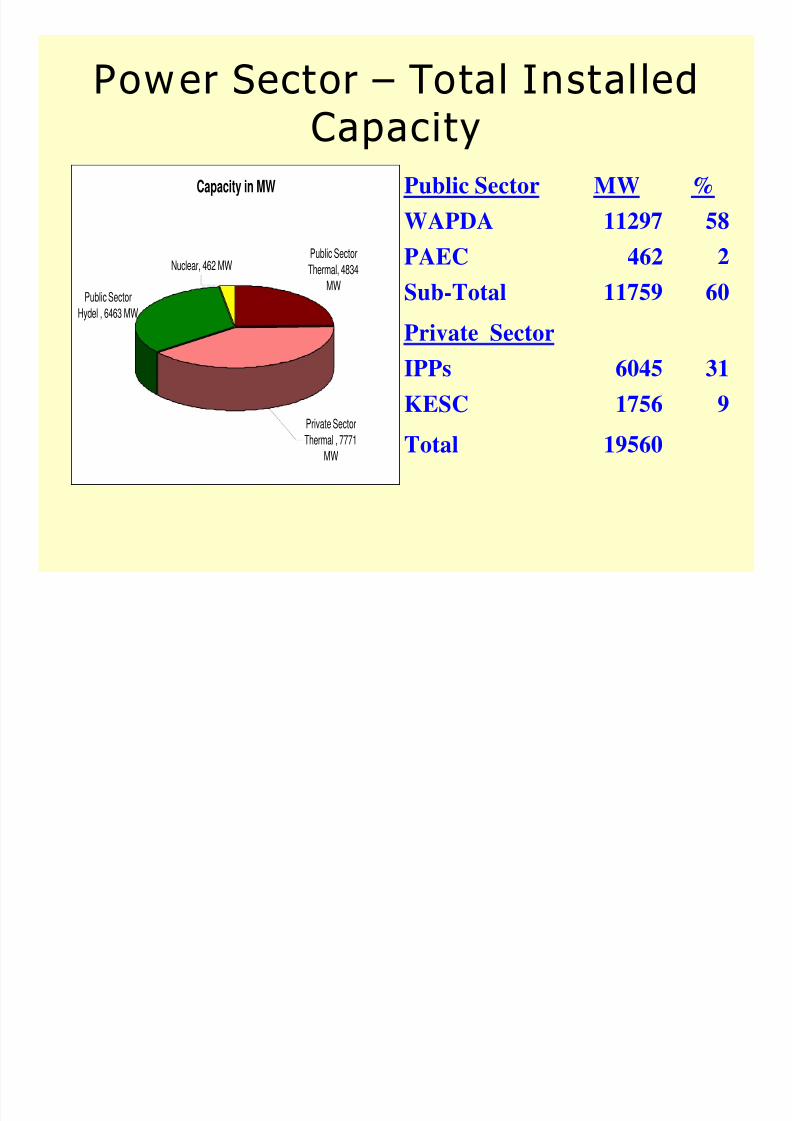

Power Sector – Total Instal ledCapacity

Capacity in MW

Nuclear, 462 MW

Private SectorThermal , 7771

MW

Public Sector

Hydel , 6463 MW

Public Sector

Thermal, 4834

MW

19560Total

91756KESC

316045IPPs

Private Sector

6011759Sub-Total

2462PAEC

5811297WAPDA

%MWPublic Sector

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 7/18

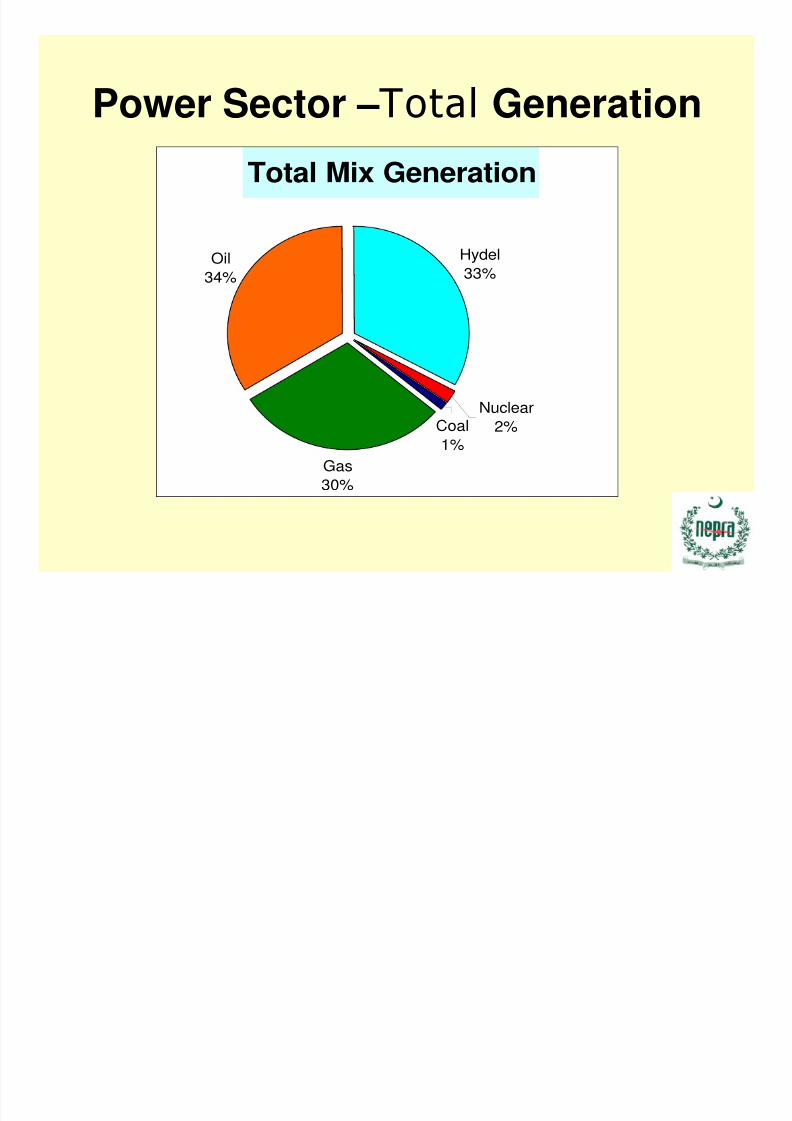

Power Sector –Total GenerationTotal Mix Generation

Hydel

33%

Gas

30%

Oil

34%

Coal1%

Nuclear

2%

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 8/18

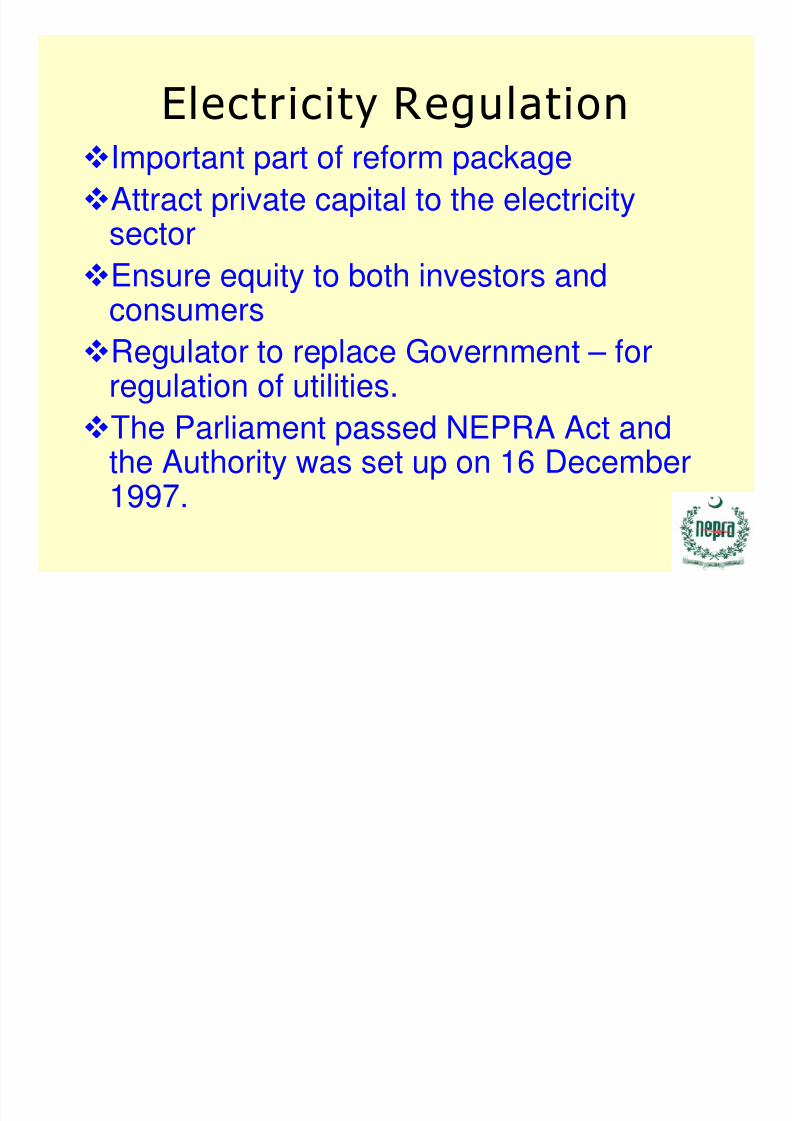

Electricity RegulationImportant part of reform package

Attract private capital to the electricitysector

Ensure equity to both investors and

consumersRegulator to replace Government – for

regulation of utilities.

The Parliament passed NEPRA Act andthe Authority was set up on 16 December1997.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 9/18

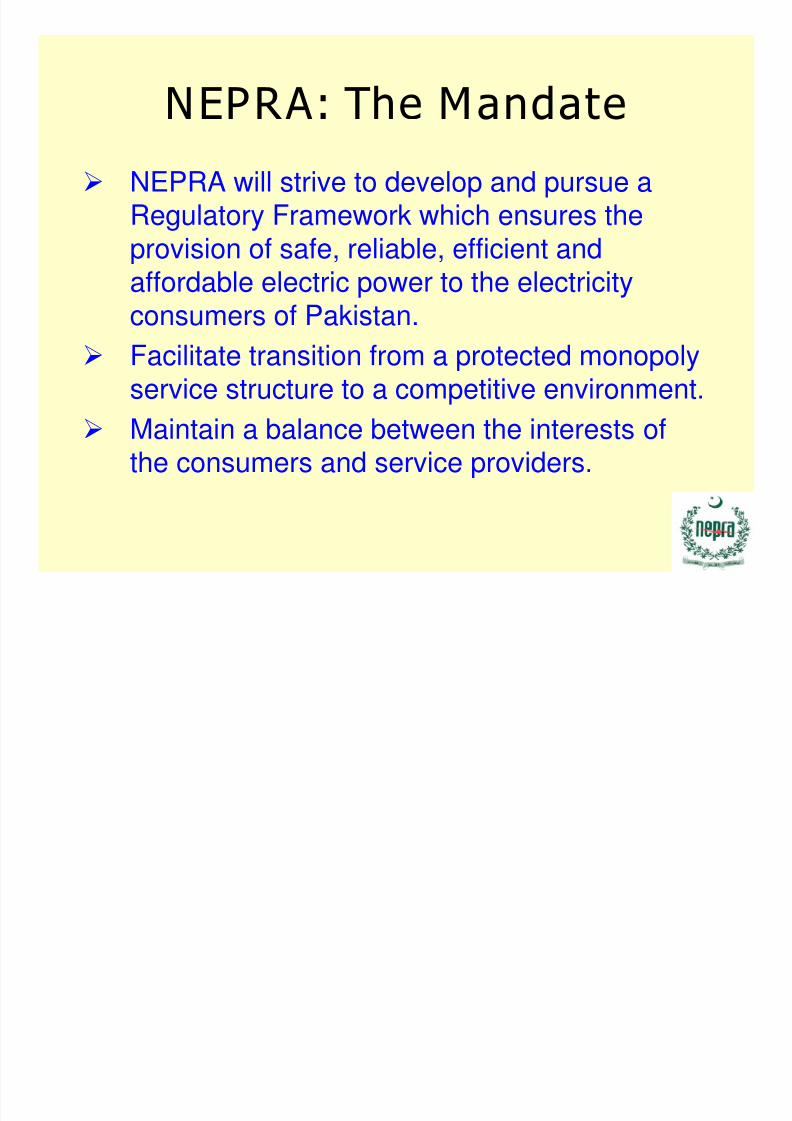

NEPRA: The Mandate NEPRA will strive to develop and pursue a

Regulatory Framework which ensures theprovision of safe, reliable, efficient andaffordable electric power to the electricity

consumers of Pakistan. Facilitate transition from a protected monopoly

service structure to a competitive environment.

Maintain a balance between the interests ofthe consumers and service providers.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 10/18

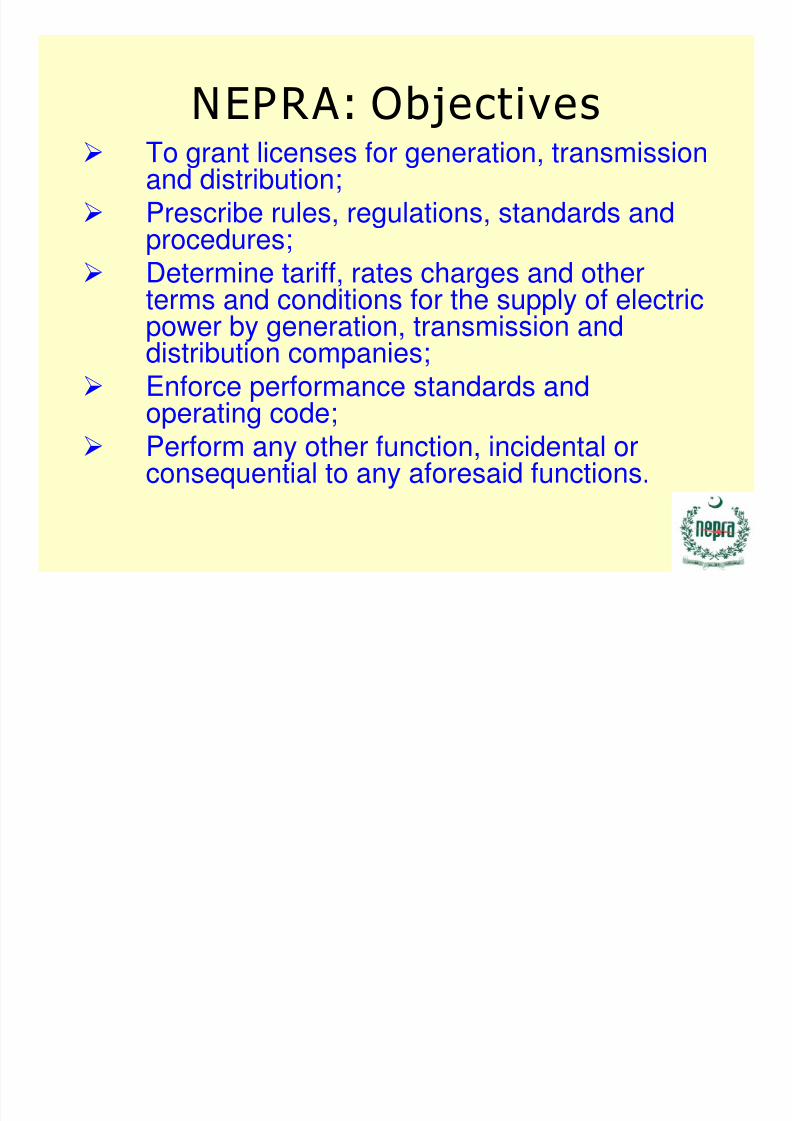

NEPRA: Objectives To grant licenses for generation, transmission

and distribution;

Prescribe rules, regulations, standards andprocedures; Determine tariff, rates charges and other

terms and conditions for the supply of electric

power by generation, transmission anddistribution companies;

Enforce performance standards andoperating code;

Perform any other function, incidental orconsequential to any aforesaid functions.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 11/18

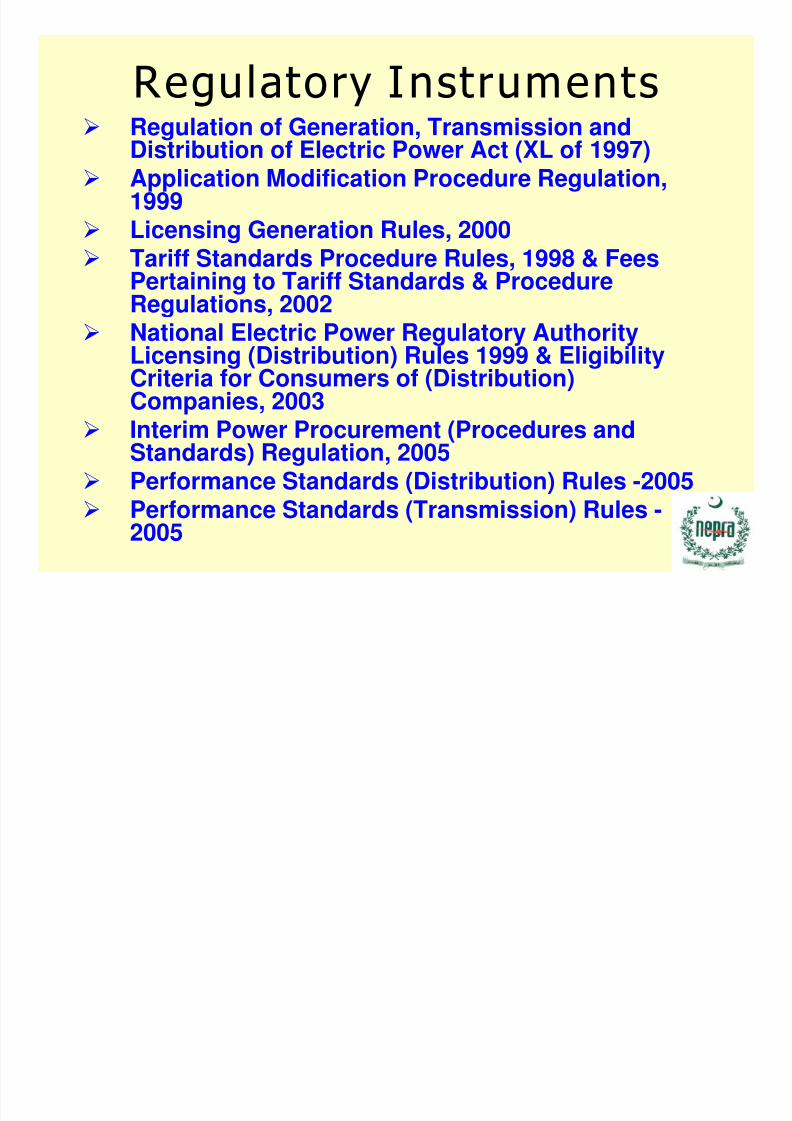

Regulatory Instruments Regulation of Generation, Transmission and

Distribution of Electric Power Act (XL of 1997) Application Modification Procedure Regulation,

1999 Licensing Generation Rules, 2000 Tariff Standards Procedure Rules, 1998 & Fees

Pertaining to Tariff Standards & ProcedureRegulations, 2002

National Electric Power Regulatory AuthorityLicensing (Distribution) Rules 1999 & EligibilityCriteria for Consumers of (Distribution)Companies, 2003

Interim Power Procurement (Procedures andStandards) Regulation, 2005

Performance Standards (Distribution) Rules -2005 Performance Standards (Transmission) Rules -

2005

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 12/18

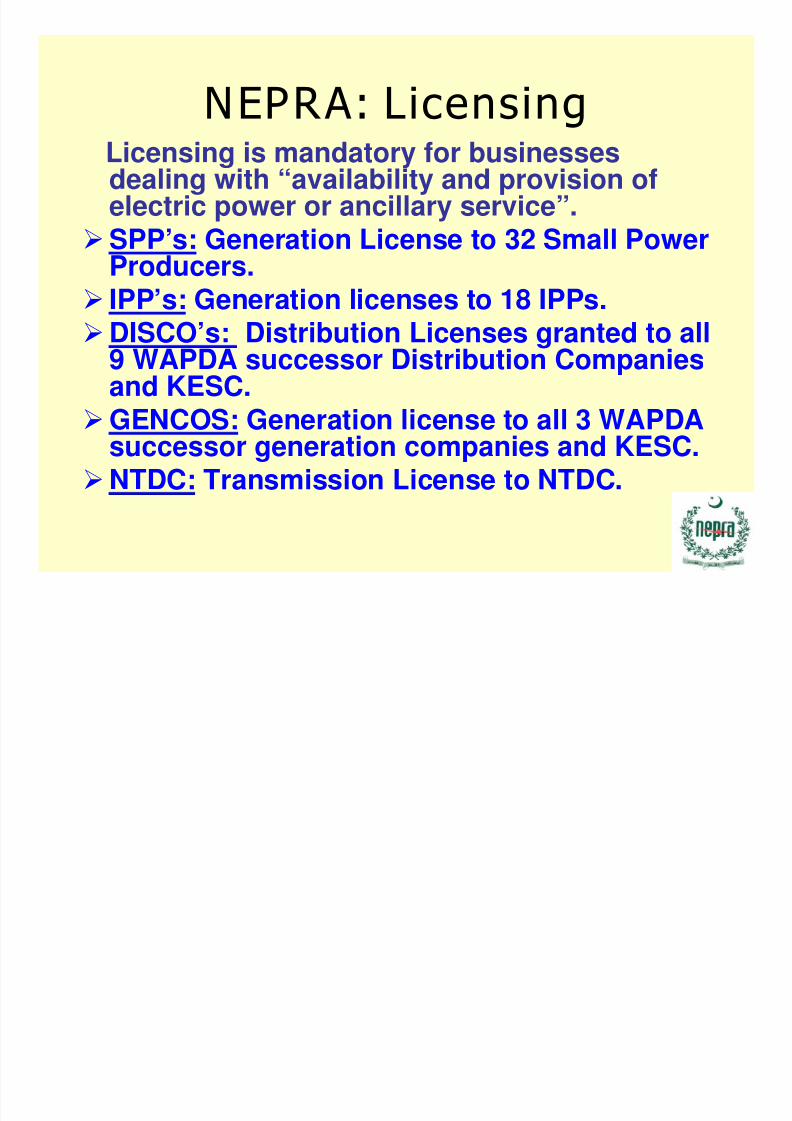

NEPRA: LicensingLicensing is mandatory for businessesdealing with “availability and provision of

electric power or ancillary service”.SPP’s: Generation License to 32 Small Power

Producers. IPP’s: Generation licenses to 18 IPPs.

DISCO’s: Distribution Licenses granted to all9 WAPDA successor Distribution Companiesand KESC.

GENCOS: Generation license to all 3 WAPDAsuccessor generation companies and KESC.

NTDC: Transmission License to NTDC.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 13/18

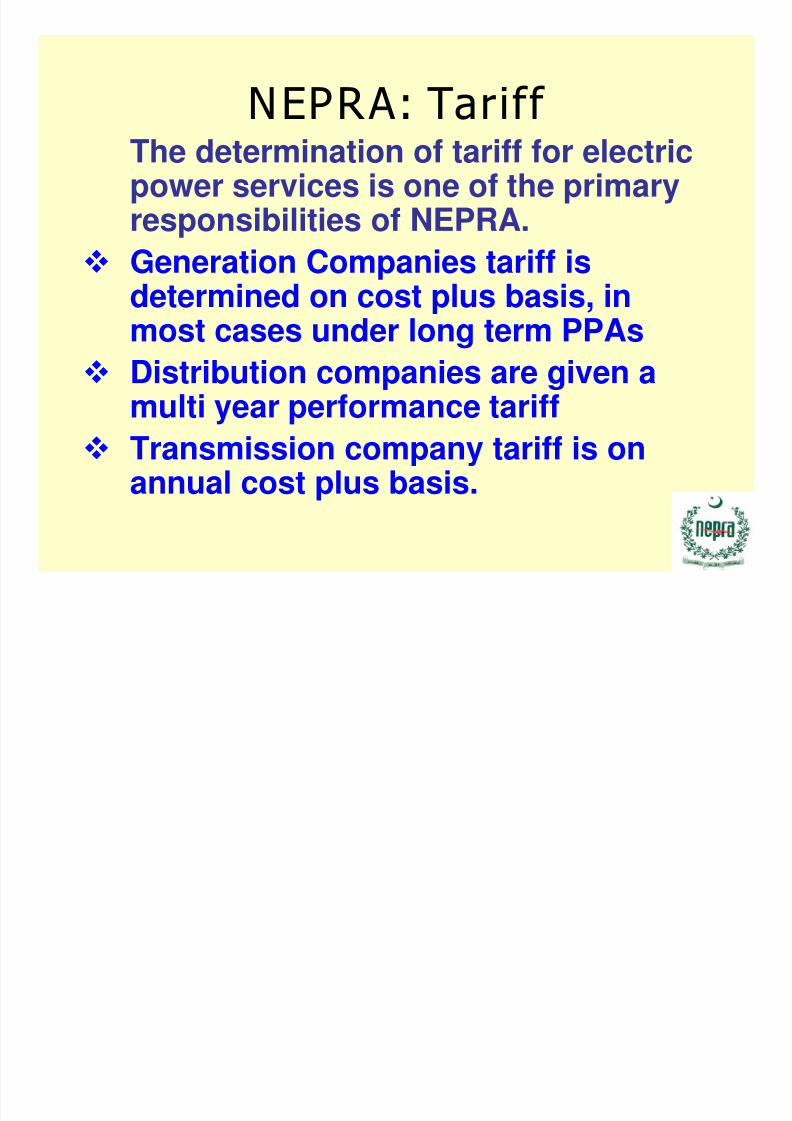

NEPRA: Tariff The determination of tariff for electricpower services is one of the primary

responsibilities of NEPRA. Generation Companies tariff is

determined on cost plus basis, in

most cases under long term PPAs Distribution companies are given a

multi year performance tariff

Transmission company tariff is onannual cost plus basis.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 14/18

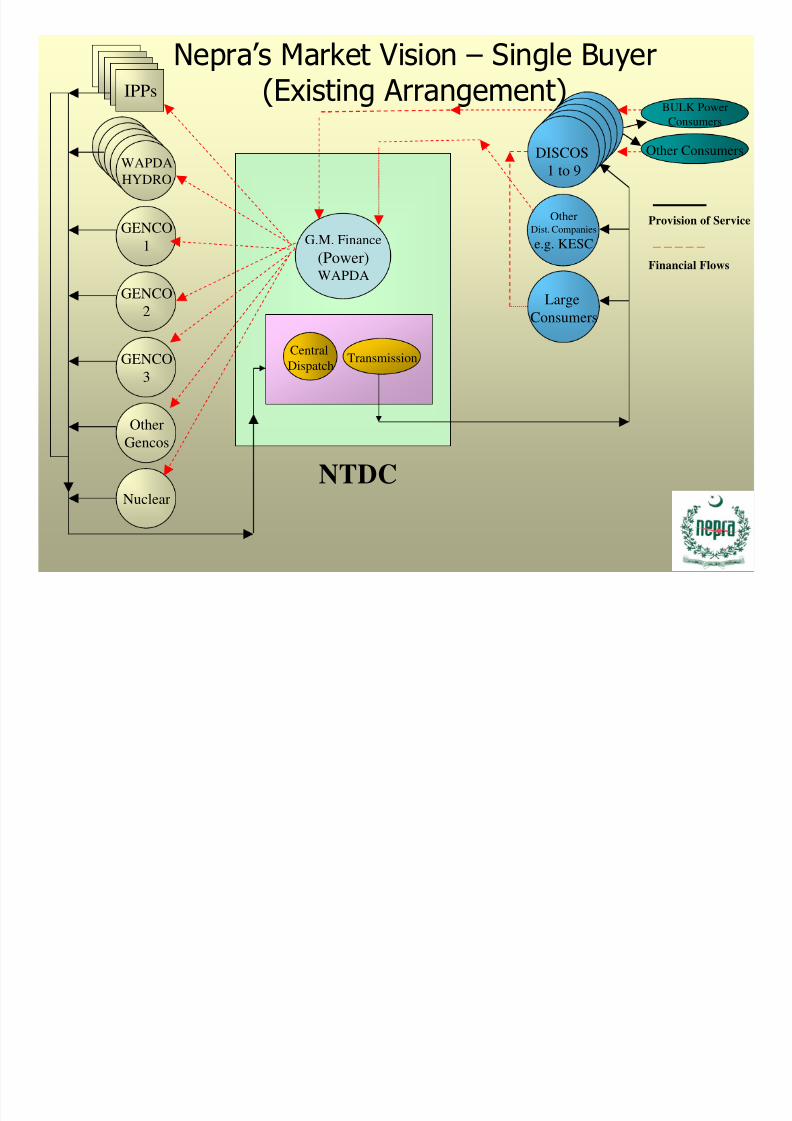

Nepra’s Market Vision – Single Buyer(Existing Arrangement)IPPs

WAPDA

HYDRO

GENCO

1

GENCO

2

GENCO

3

OtherGencos

Nuclear

OtherDist. Companies

e.g. KESC

DISCOS

1 to 9

Large

Consumers

BULK PowerConsumers

Other Consumers

G.M. Finance

(Power)WAPDA

TransmissionCentral

Dispatch

NTDC

Provision of Service

Financial Flows

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 15/18

Nepra’s Market Vision-Single Buyer Plus Arrangement (Phase-I)

IPPs

WAPDA

HYDRO

Other

Gencos

OtherDist. Companies

new demand

DISCOS

1 to 9

Large

Consumers

BULK Power

Consumers

Other

Consumers

System Operator

NTDC

Financial Flows

Provision of Service

Bilateral Contracts

New BPCs

New

Gencos

GENCO

3

GENCO

2

GENCO

1

Nuclear

Contracts Information

Other Gencos

May cater for 8May cater for 8

DiscosDiscos

Contract RegistrarContract Registrar

CPPACPPA

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 16/18

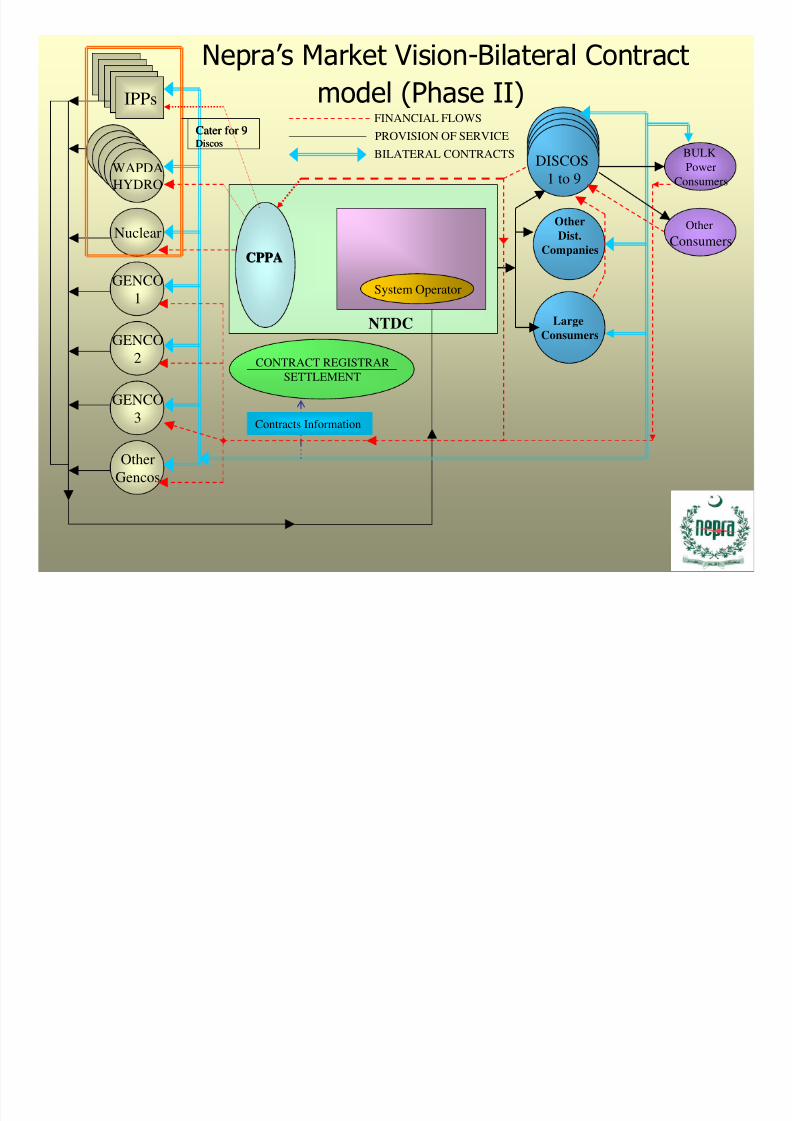

Nepra’s Market Vision-Bilateral Contract

model (Phase II)IPPs

WAPDA

HYDRO

Other

Gencos

Other

Dist.

Companies

DISCOS

1 to 9

LargeConsumers

BULK

Power

Consumers

Other

Consumers

CONTRACT REGISTRAR

SETTLEMENT

System Operator

NTDC

FINANCIAL FLOWS

PROVISION OF SERVICE

BILATERAL CONTRACTS

GENCO

3

GENCO

2

GENCO

1

Nuclear

Cater for 9Cater for 9DiscosDiscos

CPPACPPA

Contracts Information

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 17/18

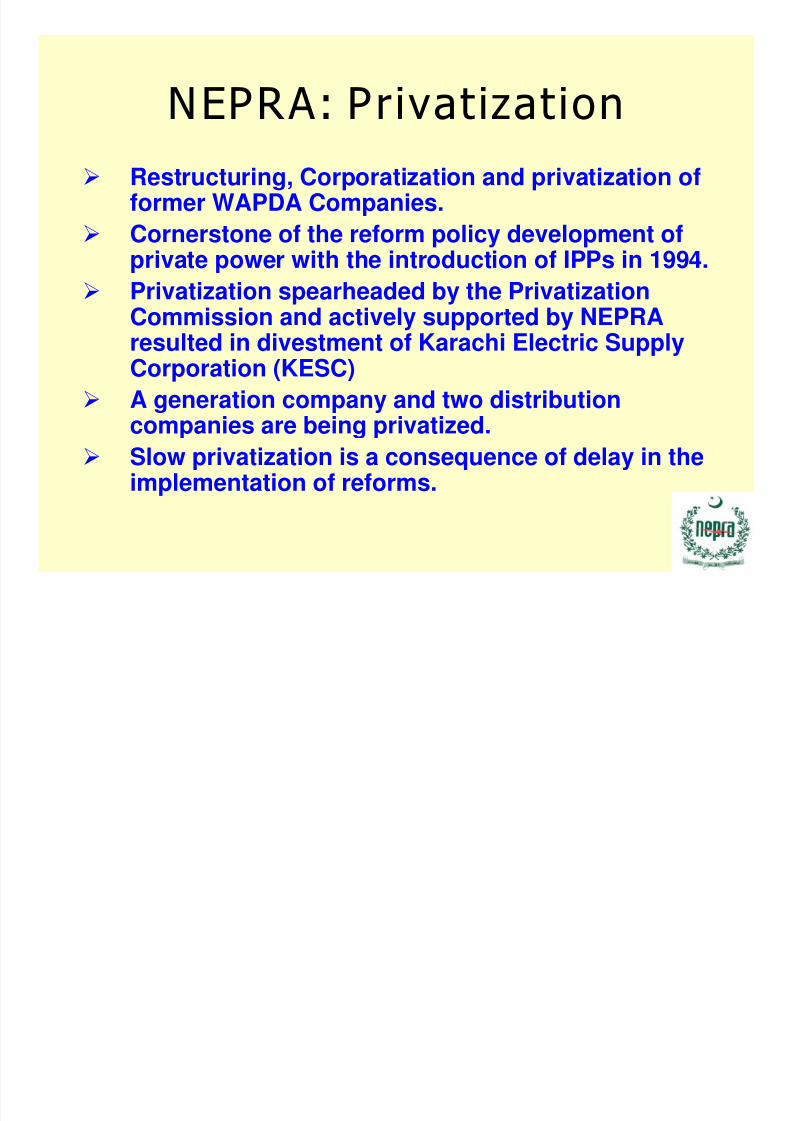

NEPRA: Privatization Restructuring, Corporatization and privatization of

former WAPDA Companies.

Cornerstone of the reform policy development ofprivate power with the introduction of IPPs in 1994.

Privatization spearheaded by the Privatization

Commission and actively supported by NEPRAresulted in divestment of Karachi Electric SupplyCorporation (KESC)

A generation company and two distribution

companies are being privatized. Slow privatization is a consequence of delay in the

implementation of reforms.

8/8/2019 04 Zafar Ali Khan, Pakistan

http://slidepdf.com/reader/full/04-zafar-ali-khan-pakistan 18/18

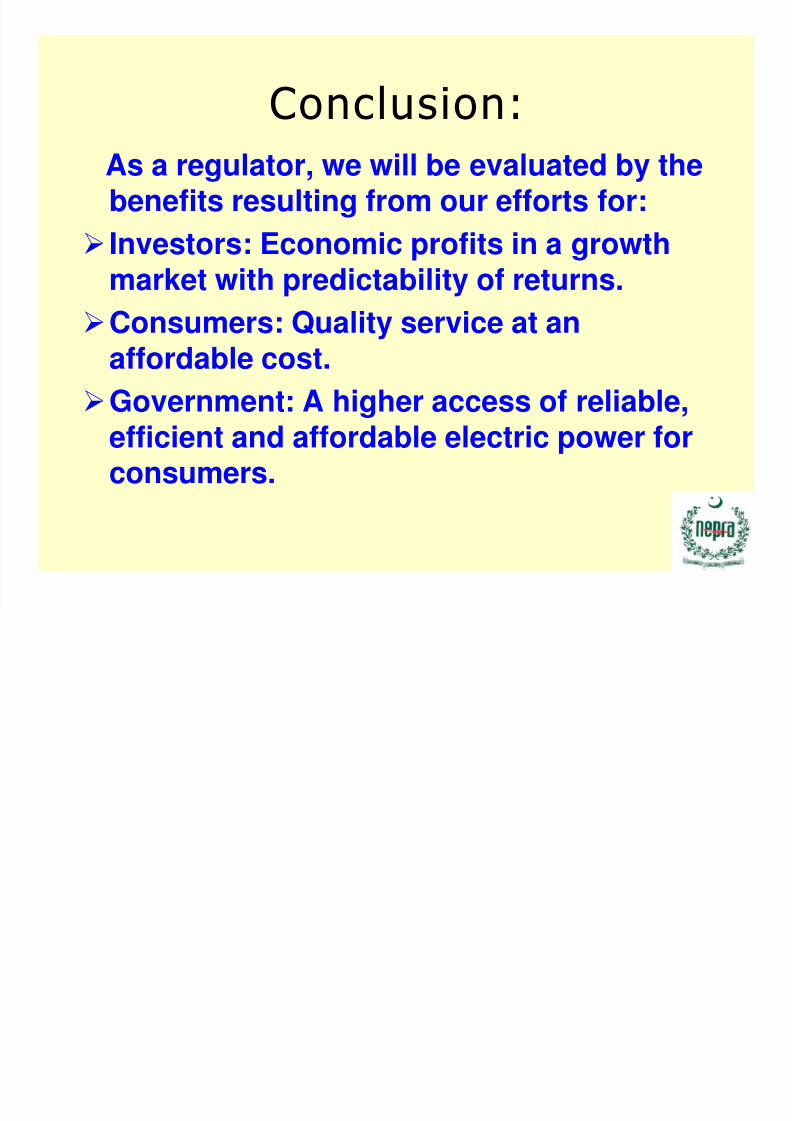

Conclusion:As a regulator, we will be evaluated by thebenefits resulting from our efforts for:

Investors: Economic profits in a growthmarket with predictability of returns.

Consumers: Quality service at anaffordable cost.

Government: A higher access of reliable,

efficient and affordable electric power forconsumers.