Embed Size (px)

Citation preview

SAMPLE C

ONTENT

SAMPLE C

ONTENT

© Target Publications Pvt. Ltd. No part of this book may be reproduced or transmitted in any form or by any means, C.D. ROM/Audio Video Cassettes or electronic, mechanical

including photocopying; recording or by any information storage and retrieval system without permission in writing from the Publisher.

STD. XI Commerce

Book-Keeping & Accountancy

Printed at: Print Vision, Navi Mumbai

Written as per the revised syllabus prescribed by the Maharashtra State Board of Secondary and Higher Secondary Education, Pune.

Salient Features • Precise Theory for every topic including Specimen Journal Entries and

Formats for Ledger Accounts.

• Comprehensive Illustrations to cover the different types of problems.

• Practice Problems important from examination point of view.

• Answers and Working Notes to simplify the Textual Problems.

• Simple and Lucid language.

• Self evaluative in nature.

TEID: 12493_JUP

P.O. No. 124298

SAMPLE C

ONTENTPreface

“Std. XI Commerce: Book-Keeping and Accountancy” has been designed with a revolutionary fresh approach towards content, to facilitate thorough preparation of the subject for the student. This book has been written according to the revised syllabus and guidelines prescribed by the State Board. The book includes Precise Theory with Specimen Journal Entries and Formats for Ledger Accounts. The comprehensive illustrations included in this book cover different types of problems. A separate section of Practice Problems has also been provided which includes a variety of problems, important from examination point of view. Additionally, we have provided answers along with working notes to simplify the Textual Problems. We are sure, this study material will turn out to be a powerful resource for the students and facilitate them in understanding the concepts of this subject in the most lucid way. The journey to create a complete book is strewn with triumphs, failures and near misses. If you think we've nearly missed something or want to applaud us for our triumphs, we'd love to hear from you. Please write to us at: [email protected]

Best of luck to all the aspirants! Yours faithfully, Publisher Edition: Second

Disclaimer This reference book is transformative work based on textual contents published by Bureau of Textbook. We the publishers are making this reference book which constitutes as fair use of textual contents which are transformed by adding and elaborating, with a view to simplify the same to enable the students to understand, memorize and reproduce the same in examinations. This work is purely inspired upon the course work as prescribed by the Maharashtra State Board of Secondary and Higher Secondary Education, Pune. Every care has been taken in the publication of this reference book by the Authors while creating the contents. The Authors and the Publishers shall not be responsible for any loss or damages caused to any person on account of errors or omissions which might have crept in or disagreement of any third party on the point of view expressed in the reference book. © reserved with the Publisher for all the contents created by our Authors. No copyright is claimed in the textual contents which are presented as part of fair dealing with a view to provide best supplementary study material for the benefit of students.

Sr. No. Chapter Page No. 1 Introduction of Book-Keeping and Accountancy 1 2 Meaning and Fundamentals of Double Entry Book-Keeping 16 3 Source Documents Required for Accounting 35 4 Journal 57 5 Subsidiary Books 86 6 Ledger 135 7 Bank Reconciliation Statement 166 8 Trial Balance 197 9 Errors and their Rectification 217

10 Depreciation, Provisions & Reserves 245 11 Financial Statements of Proprietary Concern 273 12 Computer in Accounting 333

Note: All the Textual questions are represented by * mark.

SAMPLE C

ONTENT

16

Std. XI: Commerce

In 1494, Luca D Bargo Pacioli, an Italian merchant, a great philosopher and mathematician, evolved the present Double Entry Book Keeping System. This system was based on the fact that in every business transaction, two persons / parties / accounts are involved. Out of the two parties involved, one is considered as a receiver of the benefit while the other as provider of the benefit. There will be always two aspects to a transaction i.e. if something comes in the business it has to go out from other business. Recording such dual aspects of business transactions in the books of accounts in the form of Debit and Credit is known as “Double Entry System of Book Keeping”. As per the modern approach, each and every business transaction is related individually or jointly with assets, liabilities, capital, expenses or revenue. Here, every transaction either increases or decreases one of them or increases one and decreases the other. Hence, increase in assets and expenses are “Debited” whereas decrease in assets and expenses are duly “Credited”. There are various methods of recording accounting information, which can be explained as follows:

i. Indian System: This system of accounting is also known as Mahajani, Marwadi, Deshi Nama System, etc. It is the most traditional and conventional system of accounting. Records are kept or maintained in different languages such as Marathi, Hindi, Marwadi, Urdu etc. Here the business transactions are maintained in long books known as Kird and Bahi Khata. This system is still followed in India where the business is carried on small scale. However, such system is not scientific in nature as it is not based on Double Entry Book Keeping System.

ii. English Entry System: Under English Entry System, there are two systems of recording accounting information explained as follows:

a. Single Entry System: This system is limited in maintaining only Cash Book and Personal Accounts. This system changes with the suitability of businessmen for recording transactions due to which, it is known as an incomplete system of accounting. This system has several defects and faults and it is also unscientific in nature. It does not provide a true picture or accurate information about the financial position of business. It is suitable to small scale businesses only.

b. Double Entry System: This system is regarded as the most accurate, scientific and complete system of recording business transactions. It has established due to the evolution of various accounting methods and techniques. It assumes that every transaction have two aspects which affect two accounts.

The main principles of Double Entry Book Keeping System can be stated as follows:

i. Minimum two aspects are there for every business transaction.

ii. These two aspects involve two accounts.

iii. Out of the two accounts involved, one is the receiver of the benefit and the other is the giver of benefit.

iv. If one account is debited then the other must be credited with equal amount. i.e. every debit has corresponding credit and every credit has corresponding debit of an equal amount.

Introduction

Methods of Recording Accounting Information

Principles of Double Entry System

Meaning and Fundamentals of Double Entry Book‐Keeping 02

SAMPLE C

ONTENT

17

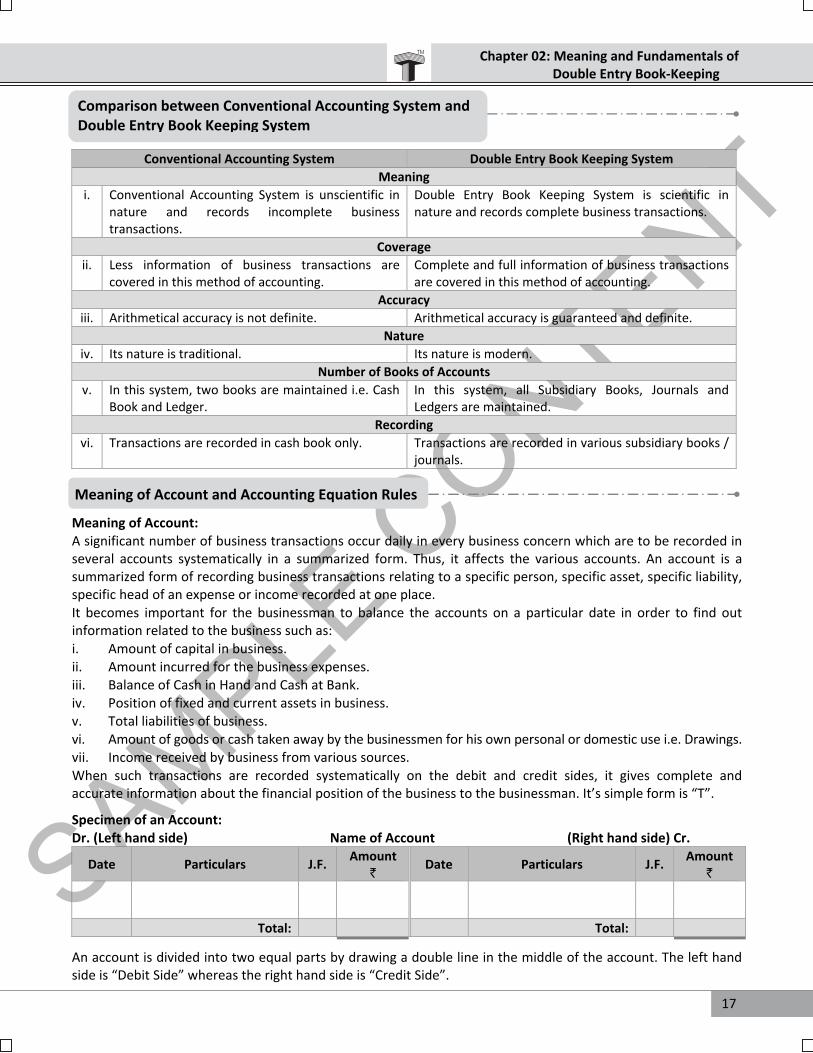

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

Conventional Accounting System Double Entry Book Keeping System

Meaning

i. Conventional Accounting System is unscientific in nature and records incomplete business transactions.

Double Entry Book Keeping System is scientific in nature and records complete business transactions.

Coverage

ii. Less information of business transactions are covered in this method of accounting.

Complete and full information of business transactions are covered in this method of accounting.

Accuracy

iii. Arithmetical accuracy is not definite. Arithmetical accuracy is guaranteed and definite.

Nature

iv. Its nature is traditional. Its nature is modern.

Number of Books of Accounts

v. In this system, two books are maintained i.e. Cash Book and Ledger.

In this system, all Subsidiary Books, Journals and Ledgers are maintained.

Recording

vi. Transactions are recorded in cash book only. Transactions are recorded in various subsidiary books / journals.

Meaning of Account: A significant number of business transactions occur daily in every business concern which are to be recorded in several accounts systematically in a summarized form. Thus, it affects the various accounts. An account is a summarized form of recording business transactions relating to a specific person, specific asset, specific liability, specific head of an expense or income recorded at one place. It becomes important for the businessman to balance the accounts on a particular date in order to find out information related to the business such as: i. Amount of capital in business. ii. Amount incurred for the business expenses. iii. Balance of Cash in Hand and Cash at Bank. iv. Position of fixed and current assets in business. v. Total liabilities of business. vi. Amount of goods or cash taken away by the businessmen for his own personal or domestic use i.e. Drawings. vii. Income received by business from various sources. When such transactions are recorded systematically on the debit and credit sides, it gives complete and accurate information about the financial position of the business to the businessman. It’s simple form is “T”. Specimen of an Account: Dr. (Left hand side) Name of Account (Right hand side) Cr.

Date Particulars J.F. Amount

`Date Particulars J.F.

Amount `

Total: Total:

An account is divided into two equal parts by drawing a double line in the middle of the account. The left hand side is “Debit Side” whereas the right hand side is “Credit Side”.

Comparison between Conventional Accounting System and Double Entry Book Keeping System

Meaning of Account and Accounting Equation Rules

SAMPLE C

ONTENT

18

Std. XI: Commerce

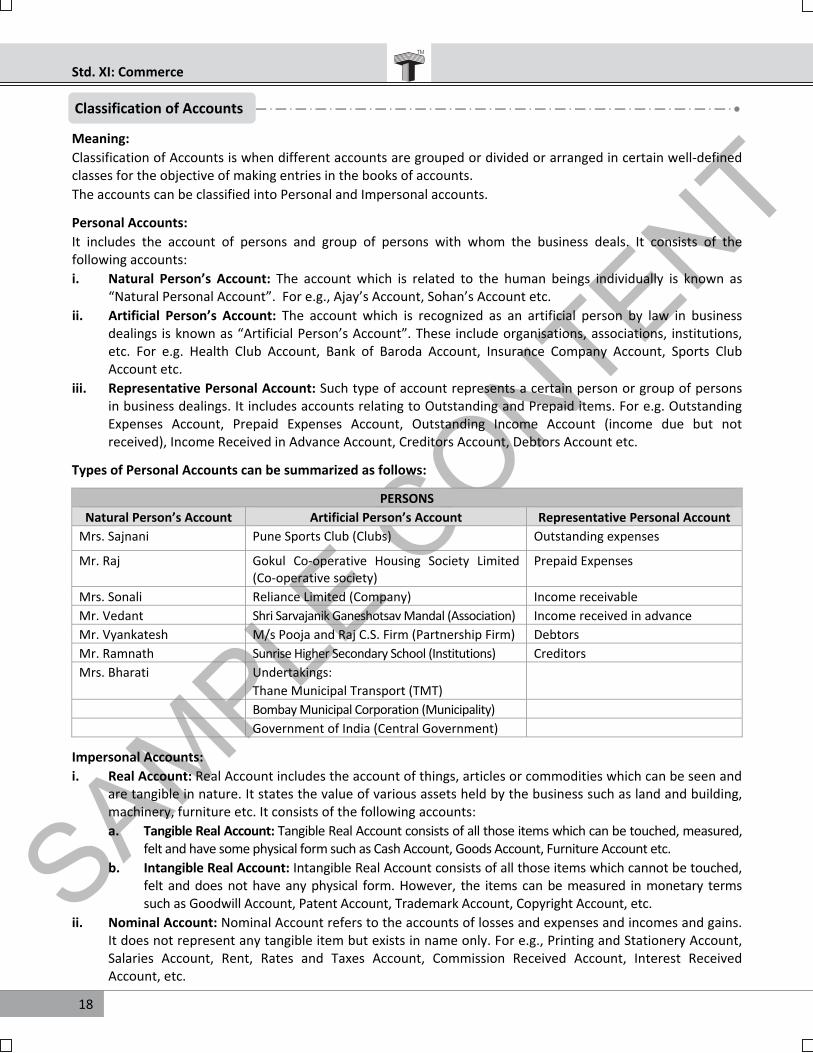

Meaning:

Classification of Accounts is when different accounts are grouped or divided or arranged in certain well‐defined classes for the objective of making entries in the books of accounts.

The accounts can be classified into Personal and Impersonal accounts. Personal Accounts:

It includes the account of persons and group of persons with whom the business deals. It consists of the following accounts:

i. Natural Person’s Account: The account which is related to the human beings individually is known as “Natural Personal Account”. For e.g., Ajay’s Account, Sohan’s Account etc.

ii. Artificial Person’s Account: The account which is recognized as an artificial person by law in business dealings is known as “Artificial Person’s Account”. These include organisations, associations, institutions, etc. For e.g. Health Club Account, Bank of Baroda Account, Insurance Company Account, Sports Club Account etc.

iii. Representative Personal Account: Such type of account represents a certain person or group of persons in business dealings. It includes accounts relating to Outstanding and Prepaid items. For e.g. Outstanding Expenses Account, Prepaid Expenses Account, Outstanding Income Account (income due but not received), Income Received in Advance Account, Creditors Account, Debtors Account etc.

Types of Personal Accounts can be summarized as follows:

PERSONS

Natural Person’s Account Artificial Person’s Account Representative Personal Account

Mrs. Sajnani Pune Sports Club (Clubs) Outstanding expenses

Mr. Raj Gokul Co‐operative Housing Society Limited (Co‐operative society)

Prepaid Expenses

Mrs. Sonali Reliance Limited (Company) Income receivable

Mr. Vedant Shri Sarvajanik Ganeshotsav Mandal (Association) Income received in advance

Mr. Vyankatesh M/s Pooja and Raj C.S. Firm (Partnership Firm) Debtors

Mr. Ramnath Sunrise Higher Secondary School (Institutions) Creditors

Mrs. Bharati Undertakings:

Thane Municipal Transport (TMT)

Bombay Municipal Corporation (Municipality)

Government of India (Central Government) Impersonal Accounts:

i. Real Account: Real Account includes the account of things, articles or commodities which can be seen and are tangible in nature. It states the value of various assets held by the business such as land and building, machinery, furniture etc. It consists of the following accounts:

a. Tangible Real Account: Tangible Real Account consists of all those items which can be touched, measured, felt and have some physical form such as Cash Account, Goods Account, Furniture Account etc.

b. Intangible Real Account: Intangible Real Account consists of all those items which cannot be touched, felt and does not have any physical form. However, the items can be measured in monetary terms such as Goodwill Account, Patent Account, Trademark Account, Copyright Account, etc.

ii. Nominal Account: Nominal Account refers to the accounts of losses and expenses and incomes and gains. It does not represent any tangible item but exists in name only. For e.g., Printing and Stationery Account, Salaries Account, Rent, Rates and Taxes Account, Commission Received Account, Interest Received Account, etc.

Classification of Accounts

SAMPLE C

ONTENT

19

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

Types of Impersonal Accounts can be summarized as follows: Impersonal Accounts

Real Accounts Nominal Accounts

Tangible Real Accounts Intangible Real Accounts Accounts of Expenses and Losses Account of Incomes and Gains

Loose Tools Goodwill Salaries paid Discount earned

Investments Copyrights Wages paid Interest received

Premises Patents Advertisement expenses paid Sundry income

Plant and Machinery Trademarks Commission paid Commission received

Furniture and Fixtures – Interest paid Dividend on shares received

Building – Office expenses Rent received

Stock of Goods – Rent paid –

Shares – Discount allowed / given –

Cash – Bad debts –

– – Loss on sale of assets – A brief review of Real Accounts, Nominal Accounts and Personal Accounts is as below:

Real Accounts Nominal Accounts Personal Accounts

Leasehold Building A/c Printing and Stationery A/c Mr. Raman’s A/c

Building A/c Salaries A/c Lifeline Hospital’s A/c

Plant and Machinery A/c Royalties A/c Bank A/c

Furniture and Fixtures A/c Wages A/c Bank of Baroda’s A/c

Land A/c Freight A/c Loan from Sairaj’s A/c

Premises A/c Trade Expenses A/c Drawings A/c

Copyright A/c Advertising A/c Capital A/c

Goodwill A/c Loss by Fire A/c Advance Received A/c

Office Equipments A/c Import Duty A/c Outstanding Commission A/c

Computer A/c Electricity Charges A/c Outstanding Interest A/c

Electrical Fittings A/c Audit Fees A/c Outstanding Salaries A/c

Investments A/c Repairs and Maintainence A/c Outstanding Interest A/c

Shares in XYZ Ltd.’s A/c Rent A/c Prepaid Salaries A/c

Freehold Premises A/c Interest A/c Prepaid Insurance A/c

Patents A/c Commission A/c Pre‐received Interest A/c

Motor Van A/c Bank Charges A/c Subscription Accured A/c

Debentures A/c Travelling Expenses A/c Interest Receivable A/c

Stock of Goods A/c Conveyance Expenses A/c Zilla Parishad’s A/c

Livestock A/c Clearing Charges A/c Government of India’s A/c

Stock of Stationery A/c Insurance Premium A/c Sports Club of Pune’s A/c

Cash A/c Brokerage A/c Commission Received in Advance A/c

Loose Tools A/c Dividend A/c –

Bills Receivable A/c Bad Debts A/c –

– Sundry Expenses A/c –

– Discount A/c – Debit refers to the benefit or gain received by a certain account. All debit items are to be recorded to the left hand side of the account. ‘Debiting an Account’ refers to making a record of a transaction after the proper and relevant rule is applied. Credit means the benefit or gain given by a certain account. All credit items are recorded to the right hand side of the account. ‘Crediting an Account’ refers to making a record of a transaction after the proper and relevant rule is applied.

Meaning of Debit and Credit

SAMPLE C

ONTENT

20

Std. XI: Commerce

Basic rules of Debit and Credit for different Accounts:

i. Personal Account: “Debit the Receiver” and “Credit the Giver”.

ii. Real Account: “Debit what Comes In” and “Credit what Goes Out”.

iii. Nominal Account: “Debit all Expenses and Losses” and “Credit all Incomes and Gains”.

To record changes in these accounts two fundamental rules are followed which are stated as below:

i. For recording changes in Assets and Expenses:

a. “Decrease in Assets is Credited” whereas “Increase in Assets is Debited.”

b. “Decrease in Expenses or Losses is Credited” whereas “Increase in expenses or losses is Debited.”

ii. For recording changes in Liabilities and Capital:

a. “Decrease in Liabilities is Debited” whereas “Increase in Liability is Credited.”

b. “Decrease in Capital is Debited” whereas “Increase in Capital is Credited.”

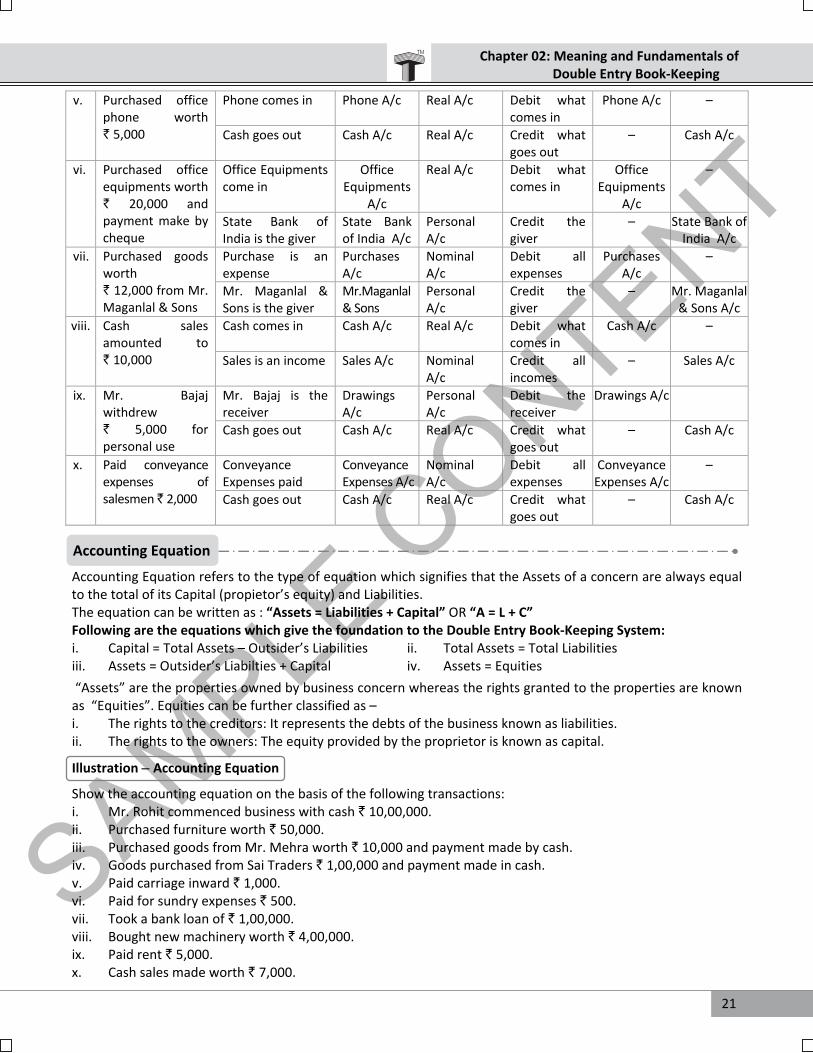

c. “Decrease in Revenue / Gain is Debited” whereas “Increase in Revenue / Gain is Credited.” Illustration – Analysis of Business Transactions Prepare chart showing Analysis of the following transactions in a Tabular form:

i. Mr. Bajaj started Pioneer Communication and introduced ` 15,00,000 into business. ii. Opened a Bank A/c with State Bank of India and deposited ` 12,00,000. iii. Purchased machinery worth ` 2,00,000 and payment made by cheque.

iv. Paid office Rent ` 12,000 by cheque. v. Purchased office phone worth ` 5,000. vi. Purchased office equipments worth ` 20,000 and payment make by cheque.

vii. Purchased goods worth ` 12,000 from Mr. Maganlal & Sons.

viii. Cash sales amounted to ` 10,000. ix. Mr. Bajaj withdrew ` 5,000 for personal use. x. Paid conveyance expenses of salesmen ` 2,000. Solution:

Chart showing the analysis of business transactions:

Sr.

No. Transactions

Two aspects/

Effects

Accounts

Involved Classification of Accounts

Rules applied

Account to be debited

Account

to be credited

i. Mr. Bajaj started Pioneer Communication and introduced ` 15,00,000 into business

Cash comes in the business

Cash A/c Real A/c Debit what comes in

Cash A/c –

Proprietor is giver of the capital

Capital A/c Personal A/c

Credit the giver

– Capital A/c

ii. Opened a Bank A/c with State Bank of India and deposited ` 12,00,000

State Bank of India is the receiver

State Bank of India A/c

Personal A/c

Debit the Receiver

State Bank of India A/c

–

Cash goes out from business

Cash A/c Real A/c Credit what goes out

– Cash A/c

iii. Purchased machinery worth ` 2,00,000 and payment made by cheque

Machinery Comes in

Machinery A/c

Real A/c Debit what comes in

Machinery A/c

–

State Bank of India is the giver

State Bank of India A/c

Personal A/c

Credit the giver

– State Bank of India A/c

iv. Paid office Rent ` 12,000 by cheque

Rent is an expense

Rent A/c Nominal A/c Debit all expenses

Rent A/c –

State Bank of India is the giver

State Bank of India A/c

Personal A/c

Credit the giver

– State Bank of India A/c

SAMPLE C

ONTENT

21

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

v. Purchased office phone worth ` 5,000

Phone comes in Phone A/c Real A/c Debit what comes in

Phone A/c –

Cash goes out Cash A/c Real A/c Credit what goes out

– Cash A/c

vi. Purchased office equipments worth ` 20,000 and payment make by cheque

Office Equipments come in

Office Equipments

A/c

Real A/c Debit what comes in

Office Equipments

A/c

–

State Bank of India is the giver

State Bank of India A/c

Personal A/c

Credit the giver

– State Bank of India A/c

vii. Purchased goods worth ` 12,000 from Mr. Maganlal & Sons

Purchase is an expense

Purchases A/c

Nominal A/c

Debit all expenses

Purchases A/c

–

Mr. Maganlal & Sons is the giver

Mr.Maganlal & Sons

Personal A/c

Credit the giver

– Mr. Maganlal & Sons A/c

viii. Cash sales amounted to ` 10,000

Cash comes in Cash A/c Real A/c Debit what comes in

Cash A/c –

Sales is an income Sales A/c Nominal A/c

Credit all incomes

– Sales A/c

ix. Mr. Bajaj withdrew ` 5,000 for personal use

Mr. Bajaj is the receiver

Drawings A/c

Personal A/c

Debit the receiver

Drawings A/c

Cash goes out Cash A/c Real A/c Credit what goes out

– Cash A/c

x. Paid conveyance expenses of salesmen ` 2,000

Conveyance Expenses paid

Conveyance Expenses A/c

Nominal A/c

Debit all expenses

Conveyance Expenses A/c

–

Cash goes out Cash A/c Real A/c Credit what goes out

– Cash A/c

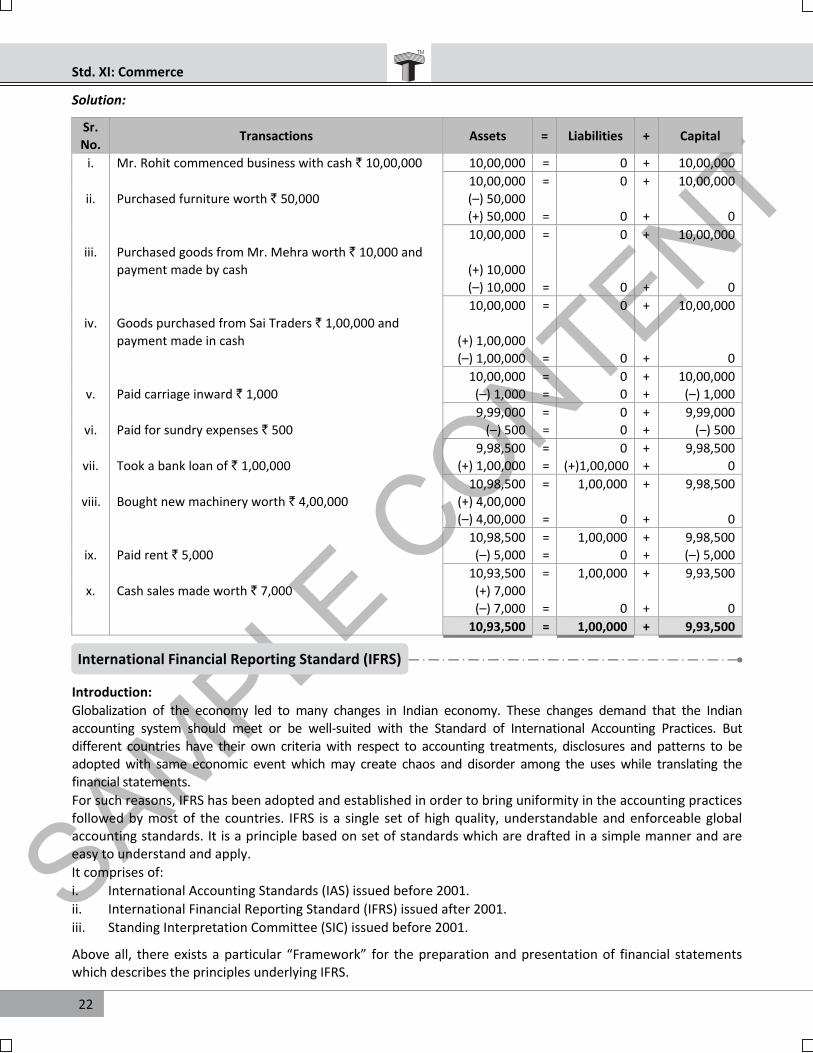

Accounting Equation refers to the type of equation which signifies that the Assets of a concern are always equal to the total of its Capital (propietor’s equity) and Liabilities. The equation can be written as : “Assets = Liabilities + Capital” OR “A = L + C” Following are the equations which give the foundation to the Double Entry Book‐Keeping System: i. Capital = Total Assets – Outsider’s Liabilities ii. Total Assets = Total Liabilities iii. Assets = Outsider’s Liabilties + Capital iv. Assets = Equities “Assets” are the properties owned by business concern whereas the rights granted to the properties are known as “Equities”. Equities can be further classified as – i. The rights to the creditors: It represents the debts of the business known as liabilities. ii. The rights to the owners: The equity provided by the proprietor is known as capital. Illustration Accounting Equation Show the accounting equation on the basis of the following transactions: i. Mr. Rohit commenced business with cash ` 10,00,000. ii. Purchased furniture worth ` 50,000. iii. Purchased goods from Mr. Mehra worth ` 10,000 and payment made by cash. iv. Goods purchased from Sai Traders ` 1,00,000 and payment made in cash. v. Paid carriage inward ` 1,000. vi. Paid for sundry expenses ` 500. vii. Took a bank loan of ` 1,00,000. viii. Bought new machinery worth ` 4,00,000. ix. Paid rent ` 5,000. x. Cash sales made worth ` 7,000.

Accounting Equation

SAMPLE C

ONTENT

22

Std. XI: Commerce

Solution: Sr.

No. Transactions Assets = Liabilities + Capital

i. Mr. Rohit commenced business with cash ` 10,00,000 10,00,000 = 0 + 10,00,000

10,00,000 = 0 + 10,00,000

ii. Purchased furniture worth ` 50,000 (–) 50,000

(+) 50,000 = 0 + 0

10,00,000 = 0 + 10,00,000

iii. Purchased goods from Mr. Mehra worth ` 10,000 and

payment made by cash (+) 10,000

(–) 10,000 = 0 + 0

10,00,000 = 0 + 10,00,000

iv. Goods purchased from Sai Traders ` 1,00,000 and

payment made in cash (+) 1,00,000

(–) 1,00,000 = 0 + 0

10,00,000 = 0 + 10,00,000

v. Paid carriage inward ` 1,000 (–) 1,000 = 0 + (–) 1,000

9,99,000 = 0 + 9,99,000

vi. Paid for sundry expenses ` 500 (–) 500 = 0 + (–) 500

9,98,500 = 0 + 9,98,500

vii. Took a bank loan of ` 1,00,000 (+) 1,00,000 = (+)1,00,000 + 0

10,98,500 = 1,00,000 + 9,98,500

viii. Bought new machinery worth ` 4,00,000 (+) 4,00,000

(–) 4,00,000 = 0 + 0

10,98,500 = 1,00,000 + 9,98,500

ix. Paid rent ` 5,000 (–) 5,000 = 0 + (–) 5,000

10,93,500 = 1,00,000 + 9,93,500

x. Cash sales made worth ` 7,000 (+) 7,000

(–) 7,000 = 0 + 0

10,93,500 = 1,00,000 + 9,93,500

Introduction:

Globalization of the economy led to many changes in Indian economy. These changes demand that the Indian accounting system should meet or be well‐suited with the Standard of International Accounting Practices. But different countries have their own criteria with respect to accounting treatments, disclosures and patterns to be adopted with same economic event which may create chaos and disorder among the uses while translating the financial statements.

For such reasons, IFRS has been adopted and established in order to bring uniformity in the accounting practices followed by most of the countries. IFRS is a single set of high quality, understandable and enforceable global accounting standards. It is a principle based on set of standards which are drafted in a simple manner and are easy to understand and apply.

It comprises of:

i. International Accounting Standards (IAS) issued before 2001.

ii. International Financial Reporting Standard (IFRS) issued after 2001.

iii. Standing Interpretation Committee (SIC) issued before 2001. Above all, there exists a particular “Framework” for the preparation and presentation of financial statements which describes the principles underlying IFRS.

International Financial Reporting Standard (IFRS)

SAMPLE C

ONTENT

23

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

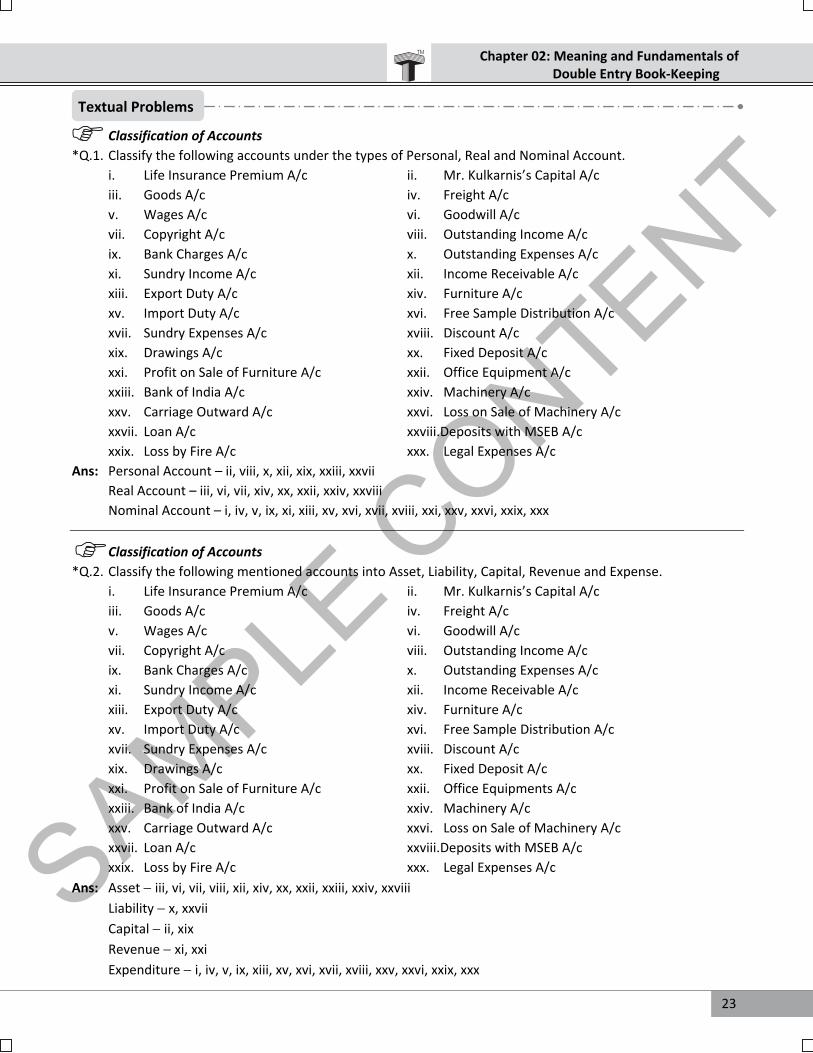

Classification of Accounts

*Q.1. Classify the following accounts under the types of Personal, Real and Nominal Account. i. Life Insurance Premium A/c ii. Mr. Kulkarnis’s Capital A/c iii. Goods A/c iv. Freight A/c v. Wages A/c vi. Goodwill A/c

vii. Copyright A/c viii. Outstanding Income A/c ix. Bank Charges A/c x. Outstanding Expenses A/c xi. Sundry Income A/c xii. Income Receivable A/c xiii. Export Duty A/c xiv. Furniture A/c xv. Import Duty A/c xvi. Free Sample Distribution A/c xvii. Sundry Expenses A/c xviii. Discount A/c xix. Drawings A/c xx. Fixed Deposit A/c xxi. Profit on Sale of Furniture A/c xxii. Office Equipment A/c xxiii. Bank of India A/c xxiv. Machinery A/c xxv. Carriage Outward A/c xxvi. Loss on Sale of Machinery A/c xxvii. Loan A/c xxviii.Deposits with MSEB A/c xxix. Loss by Fire A/c xxx. Legal Expenses A/c

Ans: Personal Account – ii, viii, x, xii, xix, xxiii, xxvii

Real Account – iii, vi, vii, xiv, xx, xxii, xxiv, xxviii

Nominal Account – i, iv, v, ix, xi, xiii, xv, xvi, xvii, xviii, xxi, xxv, xxvi, xxix, xxx Classification of Accounts

*Q.2. Classify the following mentioned accounts into Asset, Liability, Capital, Revenue and Expense.

i. Life Insurance Premium A/c ii. Mr. Kulkarnis’s Capital A/c iii. Goods A/c iv. Freight A/c v. Wages A/c vi. Goodwill A/c

vii. Copyright A/c viii. Outstanding Income A/c ix. Bank Charges A/c x. Outstanding Expenses A/c xi. Sundry Income A/c xii. Income Receivable A/c xiii. Export Duty A/c xiv. Furniture A/c xv. Import Duty A/c xvi. Free Sample Distribution A/c xvii. Sundry Expenses A/c xviii. Discount A/c xix. Drawings A/c xx. Fixed Deposit A/c xxi. Profit on Sale of Furniture A/c xxii. Office Equipments A/c xxiii. Bank of India A/c xxiv. Machinery A/c xxv. Carriage Outward A/c xxvi. Loss on Sale of Machinery A/c xxvii. Loan A/c xxviii.Deposits with MSEB A/c xxix. Loss by Fire A/c xxx. Legal Expenses A/c

Ans: Asset iii, vi, vii, viii, xii, xiv, xx, xxii, xxiii, xxiv, xxviii

Liability x, xxvii Capital ii, xix

Revenue xi, xxi Expenditure i, iv, v, ix, xiii, xv, xvi, xvii, xviii, xxv, xxvi, xxix, xxx

Textual Problems

SAMPLE C

ONTENT

24

Std. XI: Commerce

Problem based on Accounting Equations *Q.3. Show the accounting equation on the basis of the following transactions. i. Mr. Kumar commenced business with cash ` 50,000. ii. Paid salary ` 1,200. iii. Purchased furniture ` 5,000. iv. Purchased goods from Rakesh for cash ` 7,500. v. Sold goods to Shyam costing ` 13,000. vi. Paid Rent ` 500. Ans: Accounting Equation: Assets = Liabilities + Capital 48,300 = 0 + 48,300 Problem based on Accounting Equations *Q.4. Show the accounting equation on the basis of the following transactions. i. Mr. Rohit Kulkarni started business with cash ` 70,000. ii. Bought goods from Sanjay ` 10,000. iii. Sold goods to Shyam for ` 50,000 (costing ` 30,000). iv. Goods destroyed by fire (cost ` 500, sale price ` 600). v. Purchased Furniture from J.K. Furniture on credit ` 5,000. Ans: Accounting Equation: Assets = Liabilities + Capital 1,04,500 = 15,000 + 89,500 Problem based on Accounting Equations *Q.5. Show the accounting equation on the basis of the following transactions. i. Rajkumar started business with cash ` 30,000. ii. Purchased goods for cash ` 1,000. iii. Paid salary ` 400. iv. Paid rent in advance ` 2,000. v. Charged depreciation ` 300 on Furniture and ` 500 on Machinery. Ans: Accounting Equation: Assets = Liabilities + Capital 28,800 = 0 + 28,800 Problem based on Accounting Equations *Q.6. Show the accounting equation on the basis of the following transactions. i. Mr. Ketan Shah started business with cash ` 50,000. ii. Purchased goods from Ramesh ` 30,000. iii. Withdrew goods for personal use ` 2,000. iv. Purchased household goods for ` 15,000 giving ` 5,000 in cash and balance through loan. v. Paid cash ` 300 for interest. Ans: Accounting Equation: Assets = Liabilities + Capital 72,700 = 40,000 + 32,700 Analysis of Business Transactions *Q.7. Prepare chart showing Analysis of the following transactions in a Tabular form. i. Raghav started business with cash ` 50,000. ii. Sold goods for ` 1,500. iii. Purchased goods for ` 1,000 from Amit. iv. Deposited into Bank of India ` 5,000. v. Paid salary of ` 1,200. vi. Received commission ` 250 from Ram. vii. Purchased goods for cash worth ` 750 from Jay. viii. Withdrew ` 500 for personal use. ix. Sold goods to Roshan worth ` 1,500. x. Withdrew money for office use ` 1,300. xi. Paid for transportation ` 430. xii. Loan taken from Mr. Mehta ` 5,000.

SAMPLE C

ONTENT

25

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

xiii. Paid for advertisement ` 320. xiv. Additional capital introduced ` 5,000. xv. Received interest on investment ` 1,500. Ans:

Sr.

No. Accounts Involved

Nature of

Effect

Sr.

No. Accounts Involved

Nature of

Effect

i. Cash A/c Debit ix. Roshan’s A/c Debit

Capital A/c Credit Sales A/c Credit

ii. Cash A/c Debit x. Cash A/c Debit

Sales A/c Credit Bank A/c Credit

iii. Purchases A/c Debit xi. Transportation A/c Debit

Amit’s A/c Credit Cash A/c Credit

iv. Bank A/c Debit xii. Cash A/c Debit

Cash A/c Credit Loan from Mr. Mehta’s A/c Credit

v. Salary A/c Debit xiii. Advertisement A/c Debit

Cash A/c Credit Cash A/c Credit

vi. Cash A/c Debit xiv. Cash A/c Debit

Commission A/c Credit Capital A/c Credit

vii. Purchases A/c Debit xv. Cash A/c Debit

Cash A/c Credit Interest A/c Credit

viii. Drawings A/c Debit

Cash A/c Credit Analysis of Business Transactions

*Q.8. Prepare chart showing Analysis of the following transactions in a Tabular Form. i. Mr. Rohit Shah started business with cash ` 10,000. ii. Purchased goods for cash ` 1,500. iii. Deposited into Bank of Maharashtra ` 1,000. iv. Sold goods to Rakesh ` 500. v. Paid Rent of ` 200. vi. Received dividend of ` 550. vii. Loan taken from SBI ` 2,000. viii. Withdrew for office use ` 2,000. ix. Paid for repairs ` 150. x. Paid wages to Rane ` 200. Ans:

Sr.

No. Accounts Involved

Nature of

Effect

Sr.

No. Accounts Involved

Nature of

Effect

i. Cash A/c Debit vi. Cash A/c Debit

Capital A/c Credit Dividend A/c Credit

ii. Purchases A/c Debit vii. Cash A/c Debit

Cash A/c Credit Loan from SBI’s A/c Credit

iii. Bank A/c Debit viii. Cash A/c Debit

Cash A/c Credit Bank A/c Credit

iv. Rakesh’s A/c Debit ix. Repairs A/c Debit

Sales A/c Credit Cash A/c Credit

v. Rent A/c Debit x. Wages A/c Debit

Cash A/c Credit Cash A/c Credit

SAMPLE C

ONTENT

26

Std. XI: Commerce

Classification of Accounts Q.1. Classify the following accounts under the types of Personal, Real and Nominal Account: i. Octroi A/c ii. Loan A/c iii. Insurance Company’s A/c iv. Prepaid Insurance A/c v. Goodwill A/c vi. Commission A/c vii. Furniture A/c viii. Bank A/c ix. Archana’s A/c x. Goods stolen by theft A/c xi. Conveyance A/c Ans: Personal Account – ii, iii, iv, viii, ix Real Account – v, vii Nominal Account – i, vi, x, xi Classification of Accounts Q.2. Classify the below mentioned accounts into Asset, Liability, Income and Expenditure: i. Octroi A/c ii. Loan A/c iii. Copyright A/c iv. Prepaid Insurance A/c v. Goodwill A/c vi. Commission paid A/c vii. Furniture and Fixtures A/c viii. Land A/c ix. Patents A/c x. Livestock A/c xi. Rent received A/c

Ans: Asset iii, iv, v, vii, viii, ix, x Liability ii Income xi Expenditure i, vi

Classification of Accounts Q.3. Carefully analyse the following Accounts and classify into Asset, Liability, Capital, Revenue and Expenditure: i. Bank A/c ii. Octroi A/c iii. Printing & Stationery A/c iv. Depreciation A/c v. Ram’s Capital A/c vi. Interest on Loan Taken A/c vii. Live stock A/c viii. Investment A/c ix. Dividend Received A/c x. Rent Received A/c xi. Patents A/c xii. Bills Payable A/c xiii. Advance From Customer A/c xiv. Interest on Drawings A/c Ans: Asset – i, vii, viii, xi Liability – xii, xiii Capital – v Revenue – ix, x, xiv Expenditure – ii, iii, iv, vi Classification of Accounts Q.4. Classify the following accounts into Natural Personal Account, Artificial Personal Account and

Representative Personal Account: i. Kumar and Co.’s A/c ii. Ramakant’s Sports Club A/c iii. Sunny’s A/c iv. Akshay’s A/c v. Commission received in advance A/c vi. Outstanding salary A/c vii. Surveen’s A/c viii Outstanding Rent A/c ix. Jay’s A/c x. Nashik Corporation A/c

Ans: Natural Personal Account iii, iv, vii, ix Artificial Personal Account i, ii, x Representative Personal Account v, vi, viii Problem based on Accounting Equations Q.5. Mr. Shyam Ghosh submits the following information for the month ended 31st March, 2014. You are

required to show the accounting equation for the same. i. Opening Balances: Cash ` 1,00,000, Balance in Bank of Baroda A/c ` 3,50,000.

Practice Problems

SAMPLE C

ONTENT

27

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

ii. Ghosh paid salaries to staff ` 30,000 by cheque. iii. Paid ` 1,000 by cash towards office maintenance expenses. iv. Purchased on credit from Sinha & Co. goods worth ` 79,000. v. Paid ` 1,325 to Marketing Executive towards conveyance expenses. vi. Paid ` 975 by cheque towards electricity expenses. vii. Paid ` 12,000 by cheque towards office rent. viii. Issued a cheque to Sinha & Co. of ` 78,000 towards full and final settlement and received a discount

of ` 2,000 against purchase made. Ans: Accounting Equation: Assets = Liabilities + Capital 4,05,700 = 0 + 4,05,700 Problem based on Accounting Equations Q.6. Given below are some of the transactions from the books of Sunrise Ltd. Show how the accounting

equations tallies for each of them. i. Brought in ` 15,00,000 as capital into the business. ii. Opened account with SBI bank and deposited full amount therein. iii. Leased a premise for office and paid rent of ` 20,000 by cheque. iv. Purchased a second hand computer for office use on credit from Mr. Aniket ` 12,000. v. Withdrew from bank for business use ` 5,000. vi. Took a personal loan from Sudha ` 50,000. vii. Brought into business, additional capital in the form of Cash ` 25,000 and Furniture ` 40,000. viii. Bought Machinery worth ` 15,00,000 after paying 50% amount by cheque. Ans: Accounting Equation: Assets = Liabilities + Capital 23,57,000 = 8,12,000 + 15,45,000 Problem based on Accounting Equations Q.7. Following are the transactions for the month of April extracted from the books of Jugnu Enterprises. You

are required to prepare chart showing accounting equation of each of them. i. Opening Balance: Cash ` 50,000, HDFC Bank A/c ` 1,50,000, Stock ` 45,000. ii. Paid ` 4,500 by cheque towards stationery expenses. iii. Purchased goods from Mr. Bharat worth ` 12,500 on 15 days credit. iv. Purchased a computer from Global Computers on credit at ` 25,000. v. Cash sales made ` 19,500. vi. Depreciation charged on Computer ` 600. vii. Purchased a Motor Car worth ` 2,25,000 by issuing cheque. viii. Sold goods to Sharma Traders and received ` 11,600 by cheque. Ans: Accounting Equation: Assets = Liabilities + Capital 2,77,400 = 37,500 + 2,39,900 Problem based on Accounting Equations Q.8. Show the accounting equation on the basis of the following transactions: i. Rajesh started business with cash ` 40,000. ii. Purchased goods on credit ` 4,000. iii. Paid rent in advance ` 2,500. iv. Paid cash ` 500 for loan and ` 200 for interest. v. Sold goods to Rupal costing ` 25,000 for ` 30,000. vi. Paid salary ` 5,000. vii. Purchased chair for ` 500 in cash. viii. Paid rent ` 600. Ans: Accounting Equation: Assets = Liabilities + Capital 42,700 = 3,500 + 39,200

SAMPLE C

ONTENT

28

Std. XI: Commerce

Problem based on Accounting Equations

Q.9. Show the accounting equation on the basis of the following transactions:

i. Siddhi started business with cash ` 15,000. ii. Purchased goods on credit ` 5,000. iii. Paid salary ` 3,000. iv. Withdrew for personal use ` 3,000.

v. Received dividend of ` 2,000. vi. Purchased machinery for business ` 7,000.

vii. Paid to creditor ` 1,500. viii. Additional capital introduced in business ` 5,000.

Ans: Accounting Equation: Assets = Liabilities + Capital

19,500 = 3,500 + 16,000 Problem based on Accounting Equations

Q.10. Show the accounting equation on the basis of the following transactions:

i. Morari started business with cash ` 35,000.

ii. Borrowed from Palak ` 10,000.

iii. Goods destroyed by fire [cost price ` 400, sale price ` 500]. iv. Paid salary ` 2,500.

v. Purchased goods on credit ` 5,000.

vi. Withdrew for personal use ` 500.

vii. Received interest of ` 1,500. viii. Charged depreciation on Machinery ` 400.

Ans: Accounting Equation: Assets = Liabilities + Capital

47,700 = 15,000 + 32,700 Problem based on Accounting Equations

Q.11. Show the accounting equation on the basis of the following transactions:

i. Mr. Maulik started business with cash ` 25,000.

ii. Sold goods to Suhani costing ` 20,000 for ` 30,000.

iii. Paid rent ` 2,000.

iv. Purchased goods on credit ` 10,000.

v. Withdrew for personal use ` 500. vi. Received commission ` 1,500.

vii. Goods worth ` 5,000 were distributed as free samples.

viii. Purchased furniture for business ` 6,000.

Ans: Accounting Equation: Assets = Liabilities + Capital

39,000 = 10,000 + 29,000 Problem based on Accounting Equations

Q.12. Show the accounting equation on the basis of the following transactions:

i. Ronit commenced business with ` 60,000.

ii. Bought Machinery from Sumaria ` 4,000 on credit.

iii. Sold goods to Rajan costing ` 20,000 for ` 30,000. iv. Paid rent ` 5,000.

v. Received dividend of ` 3,500.

vi. Charged depreciation ` 600 on furniture.

vii. Goods destroyed by fire [cost price ` 600, sale price ` 700].

viii. Paid salary ` 2,500. Ans: Accounting Equation: Assets = Liabilities + Capital

68,800 = 4,000 + 64,800

SAMPLE C

ONTENT

29

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

Problem based on Accounting Equations Q.13. Show the accounting equation on the basis of the following transactions: i. Jackie started business with cash ` 30,000. ii. Cash Sales ` 8,000. iii. Received commission ` 1,500. iv. Cash purchases ` 7,000. v. Purchased machinery from Thacker and Sons ` 11,000 on credit. vi. Purchased goods for ` 4,500 on credit. vii. Paid salary ` 6,000. viii. Received interest ` 1,000. Ans: Accounting Equation: Assets = Liabilities + Capital 42,000 = 15,500 + 26,500 Problem based on Accounting Equations Q.14. Show the accounting equation on the basis of the following transactions: i. Cash introduced in business ` 5,00,000. ii. Opened an Account with Bank of Baroda and deposited ` 4,00,000. iii. Bought Machinery by issuing a cheque from Bank of Baroda A/c ` 50,000. iv. Goods purchased from Mr. Sarang on credit worth ` 50,000. v. Paid to Mr. Sarang in full by issuing a cheque. vi. Paid wages ` 5,000. vii. Royalty received in cash ` 7,000. viii. Paid salary by cheque ` 12,000. ix. Legal expenses paid in cash ` 2,500. x. Paid conveyance expenses ` 250. Ans: Accounting Equation: Assets = Liabilities + Capital 4,87,250 = 0 + 4,87,250 Problem based on Accounting Equations Q.15. Show the accounting equation on the basis of the following transactions: i. Mr. Rahul had an opening balance of ` 25,000 Cash, ` 30,000 Machinery, ` 3,70,000 Bank Balance

and ` 30,000 Furniture. ii. Bought computer from Ahmed on credit ` 20,000. iii. Advance from customer received in cash ` 10,000. iv. Sold machinery costing ` 20,000 at ` 25,000. v. Withdrew from Bank for business use ` 5,000. vi. Introduced additional capital of ` 50,000. vii. Charged depreciation on Machinery ` 500. viii. Carriage inward paid in cash ` 500. Ans: Accounting Equation: Assets = Liabilities + Capital 5,39,000 = 30,000 + 5,09,000 Classification of Accounts as per the accounts affected Q.16. Carefully examine the following transactions and advice as to which of the accounts will be affected and

accordingly classify the same. i. Commenced business with cash ` 7,000. ii. Purchased goods for cash ` 5,000. iii. Received commission ` 2,000. iv. Withdrew cash ` 3,000 for personal use. v. Sold goods to Chintan ` 20,000 on credit. vi. Cash purchases ` 10,000. vii. Purchased chair for business ` 800. viii. Paid rent ` 800. ix. Received interest of ` 1,000. x. Sold goods to Suraj for cash ` 3,000.

SAMPLE C

ONTENT

30

Std. XI: Commerce

Ans:

Sr.

No. Accounts Affected Classification

Sr.

No. Accounts Affected Classification

i. Cash A/c Real A/c vi.

Purchases A/c Nominal A/c

Capital A/c Personal A/c Cash A/c Real A/c

ii. Purchases A/c Nominal A/c vii.

Chair A/c Real A/c

Cash A/c Real A/c Cash A/c Real A/c

iii. Cash A/c Real A/c viii.

Rent A/c Nominal A/c

Commission A/c Nominal A/c Cash A/c Real A/c

iv. Drawings A/c Personal A/c ix.

Cash A/c Real A/c

Cash A/c Real A/c Interest A/c Nominal A/c

v. Chintan’s A/c Personal A/c x.

Cash A/c Real A/c

Sales A/c Nominal A/c Sales A/c Nominal A/c Classification of Accounts as per the accounts affected

Q.17. Carefully examine the following transactions and advice as to which of the accounts will be affected and accordingly classify the same.

i. Started business with cash ` 21,000. ii. Deposited into the bank ` 5,500. iii. Purchased goods for cash ` 7,000. iv. Paid salaries ` 7,700. v. Received rent ` 1,000. vi. Cash sales amounted to ` 5,000. vii. Bought goods from Viral ` 8,000. viii. Purchased furniture for cash ` 6,000. ix. Withdrew cash from business for personal use ` 1,500. x. Paid advertisement ` 7,000. Ans:

Sr.

No. Accounts Affected Classification

Sr.

No. Accounts Affected Classification

i. Cash A/c Real A/c vi.

Cash A/c Real A/c

Capital A/c Personal A/c Sales A/c Nominal A/c

ii. Bank A/c Personal A/c vii.

Purchases A/c Nominal A/c

Cash A/c Real A/c Viral’s A/c Personal A/c

iii. Purchases A/c Nominal Ac viii.

Furniture A/c Real A/c

Cash A/c Real A/c Cash A/c Real A/c

iv. Salaries A/c Nominal A/c ix.

Drawings A/c Personal A/c

Cash A/c Real A/c Cash A/c Real A/c

v. Cash A/c Real A/c x.

Advertisement A/c Nominal A/c

Rent A/c Nominal A/c Cash A/c Real A/c Analysis of Business Transactions

Q.18. Following are the balances extracted from the books of Mr. Mahesh. You are required prepare a chart showing analysis of the following transactions in a Tabular form:

i. Mahesh commenced business with a capital of ` 2,00,000. ii. Purchased goods from Mr. Raj ` 6,000 and payment made in cash.

iii. Paid telephone bill by cash ` 3,000. iv. Paid for electrical fittings for his business premises ` 5,000. v. Paid conveyance expenses in cash ` 2,000.

SAMPLE C

ONTENT

31

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

vi. Paid for advertisement ` 6,000. vii. Took loan from bank ` 5,00,000. viii. Salary paid ` 9,000. ix. Mahesh bought a Laptop for his personal use by withdrawing ` 30,000 from business.

x. Sold goods to Mr. Sunil on credit ` 7,000 Ans:

Sr.

No. Accounts Involved

Nature of

Effect

Sr.

No. Accounts Involved

Nature of

Effect

i. Cash A/c Debit vi. Advertisement A/c Debit

Capital A/c Credit Cash A/c Credit

ii. Purchases A/c Debit vii. Cash A/c Debit

Cash A/c Credit Bank Loan A/c Credit

iii. Telephone Expenses A/c Debit viii. Salaries A/c Debit

Cash A/c Credit Cash A/c Credit

iv. Electrical Fittings A/c Debit ix. Drawings A/c Debit

Cash A/c Credit Cash A/c Credit

v. Conveyance A/c Debit x. Sunil’s A/c Debit

Cash A/c Credit Sales A/c Credit Analysis of Business Transactions

Q.19. Following are the balances extracted from the books of Mr. Rahul. You are required prepare chart showing analysis of the following transactions in a Tabular form:

i. Mr. Rahul commenced business by introducing machinery worth ` 30,00,000. ii. Bought computer from Ahmed on credit ` 20,000. iii. Mr. Rahul paid LIC premium ` 5,000. iv. Advance from customer received in cash ` 10,000. v. Sold machinery costing ` 20,000 at ` 25,000. vi. Deposited into HDFC Bank amount of ` 20,000. vii. Introduced additional capital in the form of Furniture worth ` 50,000. viii. Interest on investments ` 2,500 received in cash. ix. Carriage Inward paid in cash ` 500. Ans:

Sr.

No. Accounts Involved

Nature of

Effect

Sr.

No. Accounts Involved

Nature of

Effect

i. Machinery A/c Debit vi.

HDFC Bank A/c Debit

Capital A/c Credit Cash A/c Credit

ii. Computer A/c Debit vii.

Furniture A/c Debit

Ahmed’s A/c Credit Capital A/c Credit

iii. Drawings A/c Debit viii.

Cash A/c Debit

Cash A/c Credit Interest on Investments A/c Credit

iv. Cash A/c Debit ix.

Carriage Inward A/c Debit

Advance from Customer A/c Credit Cash A/c Credit

v. Cash A/c Debit

Machinery A/c Credit

Profit on Sale of Machinery A/c Credit

SAMPLE C

ONTENT

32

Std. XI: Commerce

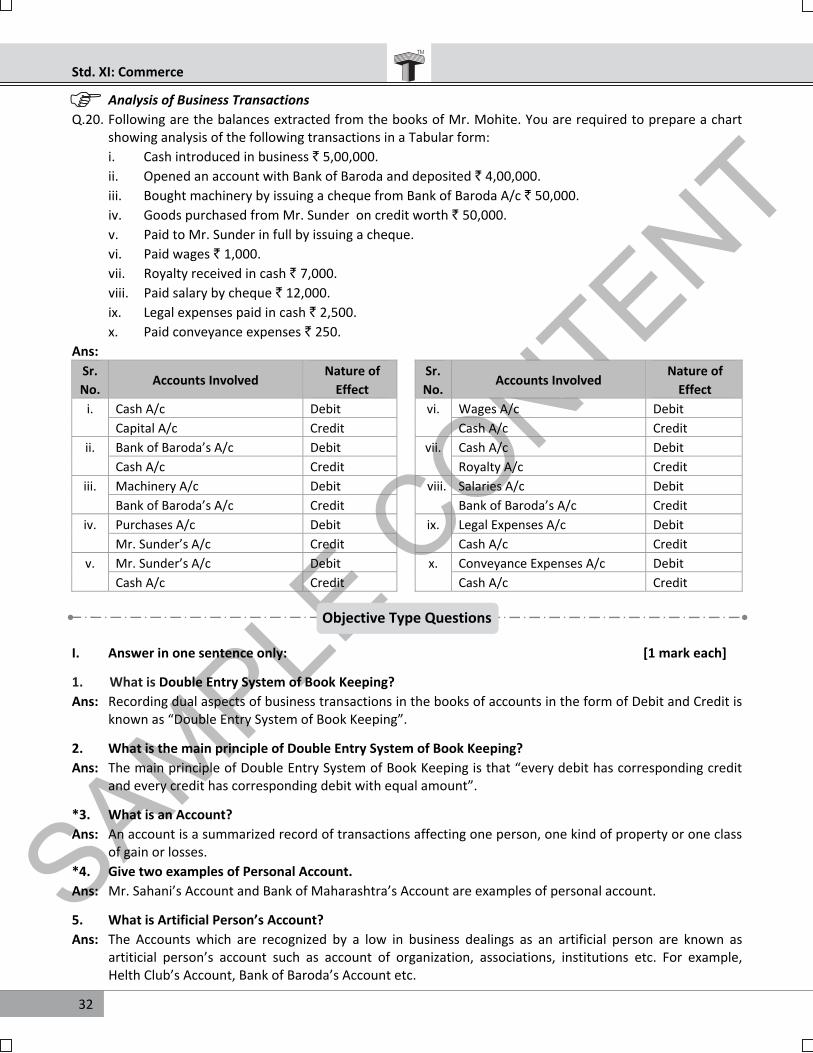

Analysis of Business Transactions

Q.20. Following are the balances extracted from the books of Mr. Mohite. You are required to prepare a chart showing analysis of the following transactions in a Tabular form:

i. Cash introduced in business ` 5,00,000.

ii. Opened an account with Bank of Baroda and deposited ` 4,00,000.

iii. Bought machinery by issuing a cheque from Bank of Baroda A/c ` 50,000.

iv. Goods purchased from Mr. Sunder on credit worth ` 50,000.

v. Paid to Mr. Sunder in full by issuing a cheque.

vi. Paid wages ` 1,000.

vii. Royalty received in cash ` 7,000.

viii. Paid salary by cheque ` 12,000.

ix. Legal expenses paid in cash ` 2,500.

x. Paid conveyance expenses ` 250.

Ans:

Sr.

No. Accounts Involved

Nature of

Effect

Sr.

No. Accounts Involved

Nature of

Effect

i. Cash A/c Debit vi. Wages A/c Debit

Capital A/c Credit Cash A/c Credit

ii. Bank of Baroda’s A/c Debit vii. Cash A/c Debit

Cash A/c Credit Royalty A/c Credit

iii. Machinery A/c Debit viii. Salaries A/c Debit

Bank of Baroda’s A/c Credit Bank of Baroda’s A/c Credit

iv. Purchases A/c Debit ix. Legal Expenses A/c Debit

Mr. Sunder’s A/c Credit Cash A/c Credit

v. Mr. Sunder’s A/c Debit x. Conveyance Expenses A/c Debit

Cash A/c Credit Cash A/c Credit

I. Answer in one sentence only: [1 mark each] 1. What is Double Entry System of Book Keeping?

Ans: Recording dual aspects of business transactions in the books of accounts in the form of Debit and Credit is known as “Double Entry System of Book Keeping”.

2. What is the main principle of Double Entry System of Book Keeping?

Ans: The main principle of Double Entry System of Book Keeping is that “every debit has corresponding credit and every credit has corresponding debit with equal amount”.

*3. What is an Account?

Ans: An account is a summarized record of transactions affecting one person, one kind of property or one class of gain or losses.

*4. Give two examples of Personal Account.

Ans: Mr. Sahani’s Account and Bank of Maharashtra’s Account are examples of personal account. 5. What is Artificial Person’s Account?

Ans: The Accounts which are recognized by a low in business dealings as an artificial person are known as artiticial person’s account such as account of organization, associations, institutions etc. For example, Helth Club’s Account, Bank of Baroda’s Account etc.

Objective Type Questions

SAMPLE C

ONTENT

33

Chapter 02: Meaning and Fundamentals of Double Entry Book‐Keeping

*6. What is Real Account? Ans: Real Account refers to an account of things, articles or commodities in the business which can be seen and

are tangible in nature. *7. Give two examples of Real Account. Ans: Building Account and Stock of Goods Account are the examples of real account. *8. What is Nominal Account? Ans: Nominal Account refers to an account of expenses, losses, incomes, gains. *9. What do you mean by debit? Ans: Debiting an account refers to recording a transaction on the left hand side of an account. *10. State the meaning of Accounting Equation. Ans: Accounting Equation refers to the equation which signifies that the assets of a business are always equal

to the total of its liabilities and capital. *11. State whether drawings increases or decreases owner’s equity. Ans: Drawings decreases the owner’s equity. *12. State the rule for Personal Account. Ans: The general rule applied for debiting and crediting the Personal account is “Debit the Receiver” and

“Credit the Giver”. *13. What is rule of debit and credit for Nominal Account? Ans: The rule of nominal account states that “Debit all Expenses or Losses” and “Credit all Incomes, Gains”. 14. Define IFRS. Ans: IFRS is a single set of high quality, understandable and enforceable global accounting standards which is

based on set of standards which are drafted in a simple manner and are easy to understand and apply. II. Write the word/ term/ phrase which can substitute each of the following statements: [1 mark each] 1. The system of accounting which is regarded as the most accurate, scientific and complete system of

recording business transactions. 2. The person who has evolved the present double entry book keeping system. 3. The system of accounting which is also known as Mahajani, Marwadi, Deshi Nama system. *4. Business Assets which cannot be seen, touched but can be sold for cash. *5. Accounts other than the impersonal account. 6. The account which includes accounts related to outstanding and prepaid items. *7. Accounts of properties. *8. Left hand side of an account. *9. Right hand side of an account. *10. Name the account which is debited when the proprietor uses business money for domestic use. *11. Proprietor’s personal account. *12. The amount paid to owner / author of book copyright for the use of book. *13. Name the account which is debited when dog is purchased for business security. *14. Name the account which is debited for payment of import duty. Ans: 1. Double Entry System of Book Keeping 2. Luca D Bargo Pacioli 3. Indian System 4. Intangible Assets 5. Personal Account 6. Representative Account 7. Real Account 8. Debit side A/c 9. Credit Side 10. Drawings 11. Capital Account 12. Royalty 13. Livestock A/c 14. Import duty

SAMPLE C

ONTENT

34

Std. XI: Commerce

III. Select the most appropriate alternative from those given below and rewrite the statements: [1 mark each]

1. Indian system is most _______ system of accounting. (A) traditional (B) accurate (C) scientific (D) complete 2. _______ system is known as incomplete system. (A) Indian system (B) Single entry system (C) Double entry system (D) None of these 3. Under Conventional accounting system, _______ book is maintained. (A) cash book (B) subsidiary books (C) journals (D) none of these 4. Copyright Account is an example of _______. (A) Tangible Real Account (B) Intangible Real Account (C) Nominal Account (D) None of these 5. Debit all _______. (A) expenses and losses (B) incomes and gains (C) expenses and revenue (D) losses and gains IV. State whether the following statements are TRUE or FALSE: [1 mark each] 1. Under Double Entry System, one is the receiver of the benefit and the other is the giver of benefit.

2. Arithmetical accuracy is not guaranteed and definite under double entry book keeping system.

*3. Every transaction has only one effect.

4. Single Entry System is suitable to small scale business.

*5. Every debit has an equal and corresponding credit.

6. The law gives recognition to Conventional Accounting System.

7. Debit the Receiver and Credit the Giver; is the rule applicable to Personal Account.

*8. Personal transactions of proprietor are recorded in the books of account of business.

*9. An order placed for the goods, entry is passed / recorded in the books of accounts.

10. Accounting Equation signifies that the capital and liabilities of the business are always equal.

*11. Prepaid insurance is a Nominal Account.

*12. Loan Account is Personal Account.

*13. Drawings Account is a Real Account.

*14. Commission received is a Nominal Account.

*15. Outstanding wages is a Nominal Account.

*16. Bank of India is an example of Real Account.

17. IFRS stands for Indian Financial Recording Standard.

Ans: 1. True 2. False 3. False 4. True

5. True 6. False 7. True 8. False

9. False 10. False 11. False 12. True

13. False 14. True 15. False 16. False

17. False