Embed Size (px)

Citation preview

AUDIT FRAMEWORK FOR VERIFICATION ENGAGEMENTS UNDER THE NATIONAL CARBON OFFSET STANDARD FOR PRODUCTS & SERVICESVersion 1.0

(Published March 2018)

1

ContentsAUDIT FRAMEWORK FOR VERIFICATION ENGAGEMENTS UNDER THE NATIONAL CARBON OFFSET STANDARD FOR PRODUCTS & SERVICES.......1

1 OVERVIEW............................................................................................................3

1.1 Purpose and use of this document................................................................3

1.2 Audit framework and requirements................................................................4

1.2.1 Further guidance.....................................................................................5

1.3 Responsibilities..............................................................................................6

1.3.1 Responsibility of auditor..........................................................................6

1.3.2 Responsibility of audited body................................................................6

1.4 Changes to audit requirements from National Carbon Offset Standard version 3.0.................................................................................................................7

1.4.1 Use of the term ‘product greenhouse gas inventory’..............................7

1.4.2 Recognition of Environmental Product Declarations..............................7

1.4.3 Two options for audit engagement type..................................................8

2 Agreed-upon procedures for product greenhouse gas inventories only................9

3 Agreed-upon procedures for environmental product declarations only...............16

4 Agreed-upon procedures for all carbon neutral products and services...............19

5 Verification report template..................................................................................24

Report on verification type audit of a carbon neutral claim against the National Carbon Offset Standard for Products and Services................................................24

Appendix 1 Choosing an assurance or verification engagement.........................32

2

1 OVERVIEW

1.1 Purpose and use of this documentThe National Carbon Offset Standard for Products & Services (Product and Service Standard) allows a choice between two types of audit engagements for carbon neutral claims: assurance engagements or verification engagements. This document is for verification type audits. It is to be used by suitably qualified auditors as defined in section 2.7 of the Product and Service Standard. (The exception is Appendix 1, which provides information for audited bodies who need to choose whether to commission a verification engagement or an assurance engagement.)

Auditors carrying out assurance audits against the Product and Service Standard must not use this document. They will need to refer to the ‘Audit Guidance for Assurance Engagements under the National carbon offset standard’ and ‘National Carbon Offset Standard Assurance Audit Report’ template available at www.environment.gov.au/carbon-neutral.

Sections 2 to 4 of this document set out the agreed-upon procedures that must be carried out during a verification engagement for a carbon neutral claim under the Product and Service Standard. Such claims may be based on either a product greenhouse gas inventory (product GHG inventory, previously referred to as a Lifecycle Analysis) or an Environmental Product Declaration (EPD). Table 2 shows which procedures must be carried out for verifications of Product GHG Inventories, which for EPDs, and which for both.

It is important to note that only EPDs that have been verified against the EN 15804 Standard can use the agreed-upon procedures for EPDs. All other EPDs are treated as product GHG inventories, and must be verified against the agreed-upon procedures for Product GHG inventories.

Table 1 Agreed-upon Procedures for Product GHG Inventories and Environmental Product Declarations

Section of this document

Agreed- upon Procedures

Must be applied to

2 1, 2, 3, 4, 5 Product GHG inventories only

3 6, 7 EPDs only

4 8, 9, 10, 11, 12 Both EPDs and Product GHG Inventories

3

If for a particular verification engagement, the auditor and/or audited body have reason to amend the agreed-upon procedures provided in sections 2 to 4, the amendments must:

• Be discussed between the auditor and the Department of the Environment and

Energy (the Department), contacted via [email protected]

• Be mutually agreed in writing between the auditor and the Department

Section 5 of this document is the template for the report of factual findings. The auditor must complete this report at the conclusion of the verification engagement. The audit team leader must provide their factual findings to the audited body in draft form prior to completing the verification engagement to give the audited body the opportunity to address any corrective action requests before the closure of the audit. Where the carbon neutral claim is certified by the Department, the audited body must submit the completed report of factual findings to the Department within four months of the end of the relevant reporting period.

For full requirements on the conduct of verification engagements for carbon neutral claims under the Product and Service Standard, auditors will need to refer to:

1. The National Carbon Offset Standard for Products & Services section 2.72. The National Greenhouse and Energy Reporting (Audit) Determination 2009,

parts 1, 2 and 4, with the exceptions set out in section 1.2 below3. The Clean Energy Regulator’s Audit Determination Handbook chapters 2, 3, 4

and in particular 6, with exceptions set out in section 1.2.1 below (www.cleanenergyregulator.gov.au).

All auditors are required to be familiar with the requirements set out in the above documents. These requirements are not replicated in this document.

1.2 Audit framework and requirements The key elements of verification type audits under the Product and Service Standard are set out in Table 2 below.

Table 1 Elements of verification type audits against the National Carbon Offset Standard for Products and Services

Element Description

Audit framework: National Greenhouse and Energy Reporting (Audit) Determination 2009 (NGER (Audit) Determination)

Audit type: Verification

4

Audit standards (as referenced through NGER Audit Determination):

• ASRS 4400; or

• ISO 14064

Audit criteria: National Carbon Offset Standard for Products and Services

Subject matter: Carbon neutral claim under the National Carbon Offset Standard for Products and Services

Audited body: The Responsible Entity for the carbon neutral claim, as defined in the National Carbon Offset Standard for Products and Services

Agreed-upon procedures: See Sections 2 to 4 of this document

High level audit requirements under the Product and Service Standard are set out in section 2.7 of the Product and Service Standard.

Verification engagements under the Product and Service Standard must be carried out in accordance with the provisions of parts 1, 2 and 4 of the National Greenhouse and Energy Reporting (Audit) Determination 2009 (NGER (Audit) Determination), with the following exceptions:

• The definition of ‘Part 6 audit’ in section 1.4 of the NGER (Audit) Determination

is expanded to include audits that assess compliance with the Product and

Service Standard.

• The audit team leader is not required to be a registered greenhouse and energy

auditor, but must instead be a suitably qualified auditor as defined in Section

2.7.1 of the Product and Service Standard.

1.2.1 Further guidance

Auditors carrying out verification engagements under the Product and Service Standard should refer to chapters 2, 3, 4 and in particular chapter 6 of the Clean Energy Regulator’s Audit Determination Handbook (www.cleanenergyregulator.gov.au) for detailed guidance. Auditors will need to apply the following exceptions to the Audit Determination Handbook guidance:

• References to the Clean Energy Regulator are to be read as references to the

Department of the Environment and Energy

• References to the schemes administered by the Clean Energy Regulator are to

5

be read as references to the Product and Service Standard and to the

Australian Government’s Carbon Neutral Program

• References to the legislation underpinning or governing the schemes

administered by the Clean Energy Regulator are to be read as references to the

Product and Service Standard

• References to Part 6 audits are to be read as references to audits that assess

compliance with the Product and Service Standard

• If the auditor and/or audited body believe it is necessary to amend the agreed-

upon procedures, the amendments must be discussed and agreed in writing

between the auditor and the Department of the Environment and Energy

1.3 Responsibilities1.3.1 Responsibility of auditor

The auditor’s responsibility is to report factual findings obtained from conducting the agreed-upon procedures set out in Sections 2 to 4 below. The verification engagement must be undertaken in accordance with the National Carbon Offset Standard for Products and Services, the National Greenhouse and Energy Reporting (Audit) Determination 2009, parts 1, 2 and 4 and the Clean Energy Regulator’s Audit Determination Handbook chapters 2, 3, 4 and 6, with the exceptions set out in section 1.2 above. The auditor must comply with the relevant ethical requirements relating to verification engagements, which include independence and other requirements founded on fundamental principles of integrity, objectivity, professional competence, due care, confidentiality and professional behaviour. Because the agreed-upon procedures do not constitute an assurance engagement the auditor does not express any conclusion and provides no assurance on the carbon neutral claim. The auditor must report if the documentation prepared by the audited body for verification is not complete or if the data is incorrect.

1.3.2 Responsibility of audited body

The audited body is responsible for preparing the carbon neutral claim in accordance with the requirements of the Product and Service Standard, maintaining appropriate records for auditing, and paying for the audit.

The audited body acknowledges is also responsible for providing the auditors with reasonable access to:

• All information that management is aware is necessary for the performance of

the agreed-upon procedures;

6

• Additional information that may be requested for the purpose of the

engagement; and

• Persons within the entity from whom the auditors require co-operation in order

to perform the agreed-upon procedures.

1.4 Changes to audit requirements from National Carbon Offset Standard version 3.0

The Product and Service Standard was published in October 2017. It is one of five standards that replaced the National carbon offset standard version 3.0. Changes in the Product and Service Standard that are relevant to audit requirements are:

The term “product GHG inventory” is now used instead of lifecycle assessment or greenhouse gas inventory.

The Department has recognised EPDs created in the Australasian EPD program as meeting many of the requirements of the Product and Service Standard. In most cases this includes meeting part of the audit requirements.

There are now two options for auditing a carbon neutral claim under the Product and Service Standard: either through an assurance engagement or a verification engagement.

Further detail on each change is below.

1.4.1 Use of the term ‘product greenhouse gas inventory’

In the Product and Service Standard, the distinction between a GHG inventory and life cycle assessment (LCA) has been removed. In practice, entities making carbon neutral claims, consultants and the broader professional community used these terms interchangeably. The term “product GHG inventory” is now used, aligning the National carbon offset standard terminology with the Greenhouse Gas Protocol. A product GHG inventory is defined as ‘compilation and evaluation of the inputs, outputs, and the potential GHG impacts of a product system throughout its life cycle’. The accounting methodologies and requirements of a product GHG inventory follow the life cycle approach established by ISO LCA standards 14040 and 14044.

1.4.2 Recognition of Environmental Product Declarations

The Department has recognised the synergy between the Australasian Environmental Product Declaration Program and the Product & Service Standard. Environmental Product Declarations (EPDs) present relevant and verified environmental information about products and services from a life cycle perspective. Because EPDs are created using LCA methodology and the LCA and EPD have undergone independent verification based on ISO LCA standards, the carbon footprint presented on an EPD can be used to fulfil most of the National carbon offset standard carbon accounting and verification requirements, with the following caveats:

7

• When using an EPD to meet the requirements of the Product and Service

Standard only EPDs verified against the EN 15804 standard can use the

agreed-upon procedures for EPDs be used to meet the auditing requirements of

the Product & Service Standard.

• If an EPD used to make a carbon neutral claim under the Product and Service

Standard has not been verified against the EN 15804 standard, then the carbon

neutral claim (including the EPD) must be audited either through an assurance

engagement, or a verification engagement using the agreed-upon procedures

for Product GHG inventories.

1.4.3 Two options for audit engagement type

There are now two options for auditing a carbon neutral claim under the Product and Service Standard. Previously auditors were required to conduct assurance type audits over a carbon neutral claim. This is still an option, but the alternative option of a verification engagement has been introduced to better align with the approach used in the EPD Program. The option of assurance engagements has been retained to maintain alignment with the National Carbon Offset Standard for Organisations, National Carbon Offset Standard for Events and National Carbon Offset Standard for Precincts. This will allow entities making multiple carbon neutral claims across different National carbon offset standard categories to commission a single audit for all of the claims. Each entity that makes a carbon neutral claim under the Product and Service Standard can choose to commission either a verification type audit or assurance type audit of the claim based on their particular circumstances.

A further change is that the required frequency of audits has been reduced. See section 2.7 of the Product and Service Standard for details.

8

2 Agreed-upon procedures for product greenhouse gas inventories only

AUP1 Preparation of the product greenhouse gas inventory

Introduction: This procedure verifies that the product greenhouse gas inventory has been prepared in accordance with current international standards and for the correct reporting period.

Specific tests

1. Verify that the product GHG inventory has been prepared in accordance with current international standards.

Has the product GHG inventory been prepared in accordance with current international standards?

For example: ISO 14040:2006, ISO14044:2006, or other international standards based on the ISO 14040 series such as PAS 2050 and the GHG Protocol Product Life Cycle Accounting and Reporting Standard.

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that the time period for the product GHG inventory has been clearly stated and is for the correct reporting period.

Has the time period for the product GHG inventory been clearly stated and does it match the reporting period under audit?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

AUP2 Product or service scope and emissions boundary

Introduction: This procedure verifies that the scope and emissions boundary of the product or service have been clearly and adequately described.

Specific tests

1. Verify that the product or service has been fully described.

Has the product or service been fully described, including its

• If the answer is Yes, proceed to the next

9

function and purpose and in accordance with section 2.3.1 of the Product and Service Standard?

test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that the functional unit or declared unit has been described.

Has the functional unit or declared unit of the product or service been described?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

3. Verify that all material uncertainties are clearly documented and valid.

Are all material uncertainties (choices, assumptions and scenarios) within the product GHG inventory clearly documented and valid?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

4. Verify that the emissions boundary has been clearly defined.

Has the emissions boundary been clearly defined in accordance with section 2.3.1 of the Product and Service Standard?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

5. Verify that any exclusions from the emissions boundary have been clearly stated and justified.

Have all exclusions from the emissions boundary been clearly stated and justified?

Are all exclusions and justifications in line with the allowable reasons for exclusion set out in section 2.3.1 of the Product and Service Standard?

• If the answer to both questions is Yes or Not Applicable, proceed to the next test.

• If the answer to either question is No, mark this as a CAR that must be closed out prior to finalising verification.

10

AUP3 Calculation of emissions

Introduction: This procedure verifies that the appropriate emission sources have been included, clearly identified and calculated correctly in accordance with the Product and Service Standard. All testing must include checks of source data (e.g. invoices, meter records, receipts etc.).

Emissions should include the seven GHGs included under the Kyoto Protocol, i.e. carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFC), perfluorocarbons (PFC), sulphur hexafluoride (SF6) and nitrogen trifluoride (NF3).

Specific tests

1. Verify that all emissions sources have been clearly identified and catalogued.

Have all sources of emissions from within the emissions boundary been clearly identified and catalogued in accordance with the instructions in section 2.3.2 of the Product and Service Standard?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that all exclusions of emissions from within the emissions boundary have been clearly stated and justified.

If any emissions sources from attributable processes, or from non-attributable processes within the emissions boundary, have been excluded, have the exclusions been clearly stated and justified in accordance with section 2.3.2 of the Product and Service Standard?

• If the answer is Yes or not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

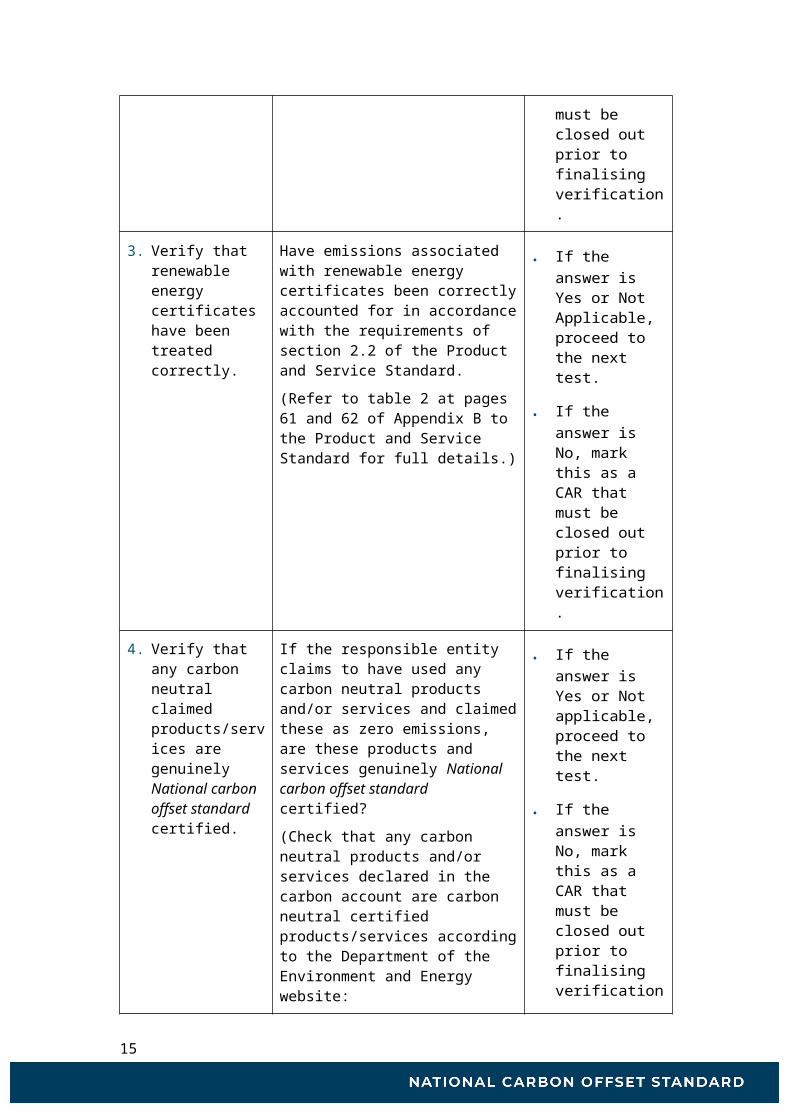

3. Verify that renewable energy certificates have been treated correctly.

Have emissions associated with renewable energy certificates been correctly accounted for in accordance with the requirements of section 2.2 of the Product and Service Standard.

(Refer to table 2 at pages 61 and 62 of Appendix B to the Product and Service Standard for full details.)

• If the answer is Yes or Not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

11

4. Verify that any carbon neutral claimed products/services are genuinely National carbon offset standard certified.

If the responsible entity claims to have used any carbon neutral products and/or services and claimed these as zero emissions, are these products and services genuinely National carbon offset standard certified?

(Check that any carbon neutral products and/or services declared in the carbon account are carbon neutral certified products/services according to the Department of the Environment and Energy website:

www.environment.gov.au/carbon-neutra l )

If you require further clarification on the carbon neutral certification status of the product or service, contact the Department of the Environment and Energy via [email protected].

• If the answer is Yes or Not applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

5. Verify that Scope 1 and Scope 2 emission factors have been sourced from approved sources.

Have approved Scope 1 and 2 emission factors been used in accordance with the requirements set out in section 2.3.5 of the Product and Service Standard?

(Note that the Product and Service Standard requires that National Greenhouse Account (NGA) Factors be used unless more accurate emission factors or calculation methodologies are publicly available. Factors available in AusLCI and GaBi databases align with the NGA factors and can be used.)

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

6. Verify that Scope 3 emission factors have been sourced from appropriate sources.

Have all Scope 3 emission factors been sourced from appropriate sources in accordance with section 2.3.5 of the Product and Service Standard?

(For guidance on the recommended hierarchy of emission factors, see Appendix B of the Product and Service Standard).

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

7. Verify activity data for all material emission

Do all source data values for material sources of emissions match the values inputted into the product

• If the answer is Yes, proceed to

12

sources identified in the product GHG assessment.

GHG inventory?

(The definition of a material emission source is provided in section 2.3.1 of the Product and Service Standard.)

the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

8. Verify that emissions have been calculated correctly for each emission source.

Have the emissions attributable to each emission source been calculated correctly?

Check that the calculations are accurate and in accordance with section 2.3.5 and Appendix B of the Product and Service Standard.

• If the answer is Yes or not applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

9. Verify that total emissions have been correctly calculated.

Have all individual emission sources been accurately summed to give the total attributable emissions for the full life cycle of the product?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

AUP4 Product GHG inventory analysis

Introduction: This procedure verifies that the product greenhouse gas inventory has been correctly prepared.

Specific tests

1. Verify that the data collection procedures and calculation methodologies have been clearly stated.

Have all data collection procedures and calculation methodologies been clearly stated?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

13

2. Verify that the sources of information and activity data have been clearly identified.

Have the sources of all information and activity data been clearly identified?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

3. Verify that regional variations in emission factors have been accounted for.

Have the correct national, jurisdictional or regional emissions factors been applied when calculating emissions that occur in particular locations?

• If the answer is Yes or not applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

4. Verify that data periods and database and software versions used have been disclosed.

Has the data period and/or software version been clearly stated for each database used to source emissions factors?

• If the answer is Yes or Not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

5. Verify that assumptions and constraints have been clearly described and justified.

To the best of the auditor’s knowledge, have all assumptions and constraints been clearly described and justified?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

14

AUP5 Base year identification

Introduction: This procedure verifies that the base year has been correctly identified and that reasons for differences in emissions since the base year have been disclosed.

Specific tests

1. Verify that the Product GHG inventory base year has been correctly identified.

If applicable to the product or service, has the product GHG inventory base year been correctly identified in accordance with section 2.3.3 of the Product and Service Standard?

If a base year calculation is not applicable to the product or service, have alternative arrangements stipulated by the Department of the Environment and Energy been followed in accordance with section 3.1.1 of the Product and Service Standard?

• If the answer to one of these questions is Yes, proceed to the next test.

• If the answer to both questions is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that significant changes in the carbon account since base year have been disclosed.

Have significant changes (> ±5%) in the carbon account between the base year and the current reporting year that are not attributed to emissions reduction actions or changes in the volume of product or service produced by the responsible entity been disclosed in accordance with section 2.3.3 of the Product and Service Standard?

• If the answer is Yes, proceed to Section 4, AUP 8.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

15

3 Agreed-upon procedures for environmental product declarations only1

AUP6 Environmental Product Declaration (EPD) verification

Introduction: This procedure confirms that the EPD was verified in accordance with the requirements of the Australasian Environmental Product Declaration Programme as well as confirming that the verifier meets the qualification requirements of section 2.7 of the Product and Service Standard.

Specific tests

1. Confirm that the EPD has been verified in line with the requirements of the Australasian EPD Programme.

Has the audited body provided a completed, signed and valid EPD verification report including the verification statement, checklist parts A, B and C and dialogue that verifies that the product or service seeking carbon neutral certification has met the requirements of the Australasian Environmental Product Declaration Program?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Confirm that the EPD verifier is a qualified auditor under the Product and Service Standard.

Is the verifier who undertook the EPD verification an Australian Life Cycle Assessment Society (ALCAS) certified practitioner, (and therefore qualified to undertake an audit under the Product and Service Standard)?

ALCAS certified practitioners meet the auditor qualification criteria set out in section 2.7 of the Product and Service Standard as they are accredited to a recognised international standard based on ISO 14040.

• If the answer is Yes, proceed to the next test.

• If the answer is No, the remaining agreed upon procedures for environmental product declarations cannot be used for this verification engagement. The audited body must choose to either:

1 Only EPDs that have been verified against the EN 15804 Standard can use the agreed-upon procedures for EPDs. EPDs that have not been verified against that standard are treated as product GHG inventories, and must be verified against the agreed-upon procedures for Product GHG inventories, or undergo an assurance audit.

16

1. Continue with the verification engagement using the agreed-upon procedures for product GHG inventories;

2. Commission an assurance engagement instead of the verification engagement; or

3. Have the EPD verified by an ALCAS certified practitioner.

AUP7 Calculation of emissions

Introduction: This procedure verifies that emissions have been correctly calculated in accordance with the Product and Service Standard, where the standard has additional requirements not covered by the EPD.

Specific tests

1. Verify that renewable energy certificates have been treated correctly.

Have emissions associated with renewable energy certificates been correctly accounted for in accordance with the requirements of section 2.2 of the Product and Service Standard.

(Refer to table 2 at pages 61 and 62 of Appendix B to the Product and Service Standard for full details.)

• If the answer is Yes or Not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that any carbon neutral claimed products/services are genuinely National carbon offset standard certified.

If the responsible entity claims to have used any carbon neutral products and/or services and claimed these as zero emissions, are these products and services genuinely National carbon offset standard certified?

Check that any carbon neutral products and/or services declared in the carbon account are carbon neutral certified products/services according to the Department of the

• If the answer is Yes or Not Applicable, proceed to the next test.

17

Environment and Energy website:

www.environment.gov.au/carbon-neutral.

If you require further clarification on the carbon neutral certification status of the product or service, contact the Department of the Environment and Energy via [email protected].

3. Verify that Scope 1 and Scope 2 emission factors have been sourced from approved sources.

Have the correct Scope 1 and 2 emission factors been used in accordance with the requirements set out in section 2.3.5 of the Product and Service Standard?

(Note that the Product and Service Standard requires that National Greenhouse Account (NGA) Factors be used unless more accurate emission factors or calculation methodologies are publicly available. Factors available in AusLCI and GaBi databases align with the NGA factors and can be used.)

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

18

4 Agreed-upon procedures for all carbon neutral products and services

AUP8 Emissions reductions

Introduction: This procedure verifies that an emissions reduction strategy has been developed and documented in accordance with the requirements of the Product and Service Standard.

Specific tests

1. Verify that the emissions reduction strategy has been adequately described.

Has the emissions reduction strategy been adequately described in accordance with sections 2.4.1 and 2.6 of the Product and Service Standard?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that emissions reduction measures have been considered and documented.

Have reduction measures been considered and documented in accordance with sections 2.4.1 and 2.6 of the Product and Service Standard?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

3. Verify that quantities of planned emissions reductions have been estimated where practicable.

Has the estimated quantity of emissions reductions from each emission reduction measure been stated where practicable in accordance with section 2.4.1 of the Product and Service Standard?

• If the answer is Yes or Not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR. However, the verification can still be finalised if the audited body is not able to address this

19

request.

AUP9 Carbon offsetting

Introduction: This procedure verifies that the audited body has taken the correct approach to offsetting the carbon account and documenting the offsets.

Specific tests

1. Assess the offset units.

Review the following:

• Have the details (including quantity, type, serial numbers, registry and date of cancellation) of the cancelled offsets been provided by the audited body?

• Has the responsible entity provided evidence or can the verifier locate evidence that the offsets were retired in the name of the responsible entity for the correct year (e.g. screenshot of registry account, confirmation email from registry, verifier search for serial numbers on online registry and view associated entity)?

• Are the total offsets cancelled equal to (or greater than) the total carbon account calculated by the audited body (as verified by the auditor)?

• Is/are the offset units eligible under the National carbon offset standard (see Appendix A of the Product and Service Standard)?

• If the answer to all four questions is Yes, proceed to the next test.

• If the answer to any of the questions is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Assess reporting of offsets banked for future years.

Has the quantity of offsets banked for future years been clearly stated?

Have details of banked offsets been provided, including the offset type, serial numbers, and evidence to support the transaction?

• If the answer to both questions is Yes or Not Applicable proceed to the next test.

• If the answer to either of the

20

questions is No, mark this as a CAR that must be closed out prior to finalising verification.

3. Assess reporting of previously banked offsets used this reporting period.

If offsets are used from earlier periods, have these been adequately described and proof of cancellation provided?

Review the type and vintage of previously banked offsets that have been used to offset emissions in the reporting period under audit. Refer to Appendix A of the Product and Service Standard for eligibility and vintage requirements. Are the banked offsets that have been used eligible for use in this reporting period?

• If the answer to both questions is Yes or Not Applicable proceed to the next test.

• If the answer to either of the questions is No, mark this as a CAR that must be closed out prior to finalising verification.

AUP10 Record keeping, data management and quality control

Introduction: This procedure verifies that record keeping, data management and quality control practices are in accordance with the requirements of the Product and Service Standard.

Specific tests

1. Verify the adequacy of record keeping and data management practices.

Are record keeping and data management practices carried out in accordance with the requirements set out in section 2.3.4 of the Product and Service Standard?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that records of reporting documents have been kept.

Are details of the required annual inventories, product disclosure summaries and audit reports for the duration of the carbon neutral claim included in records management systems?

• If the answer is Yes proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising

21

verification.

3. Verify that responsibility for record keeping is clearly stated.

Has the person responsible for establishing and maintaining the records, and their position title, been identified?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

4. Verify that quality control practices have been described.

Has a description been provided of the quality control practices that are in place to ensure that data quality is maintained?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

AUP11 Trade mark use and marketing

Introduction: This procedure verifies that the audited body has kept adequate records of its use of the Carbon Neutral Certification Trade Mark and has sought approval for use of the Trade Mark as required by the User Guide for the Carbon Neutral Certification Trade Mark v.5.

Specific tests

1. Verify that adequate records have been kept of use of the Carbon Neutral Certification Trade Mark.

Have adequate records of use of the Carbon Neutral Certification Trade Mark been kept in accordance with section 1.4 of the User Guide for the Carbon Neutral Certification Trade Mark v.5?

(This requirement is applicable only to entities that are licenced to use and have used the Carbon Neutral Certification Trade Mark.)

• If the answer is Yes or Not Applicable, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify that approval has been sought for Trade Mark use in accordance

Has proposed marketing material bearing the certification Trade Mark been provided to the Department for approval in accordance with Section 3 of the User Guide for the

• If the answer is Yes or Not Applicable, proceed to the

22

with the User Guide.

Carbon Neutral Certification Trade Mark v.5?

(This requirement is applicable only to entities that are licenced to use and have used the Carbon Neutral Certification Trade Mark.)

next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

AUP12 Reporting documents

Introduction: This procedure verifies that information contained in the product GHG inventory or EPD is consistent with the information contained in the Product Disclosure Summary, and that the Public Disclosure Summary has been declared true and correct and in accordance with the National carbon offset standard by the audited body’s representative.

Specific tests

1. Verify that the reporting documents are consistent.

Is the information contained in the Public Disclosure Summary consistent with the product GHG inventory or EPD?

(Consider emissions, emission sources, description of boundary and excluded emissions, reporting year, reduction and offsetting activities).

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

2. Verify the signed declaration in the Public Disclosure Summary.

Does the Public Disclosure Summary include a signed, dated declaration by an authorised representative of the audited body that the information provided in the Public Disclosure Summary is true and correct and meets the requirements of the Product and Service Standard?

Has the signatory provided their name and position title?

• If the answer is Yes, proceed to the next test.

• If the answer is No, mark this as a CAR that must be closed out prior to finalising verification.

23

5 Verification report template This template has been adapted from the Clean Energy Regulator’s Audit Determination Handbook template for a National Greenhouse and Energy Reporting audit report (verification engagement). The auditor must complete their report using the MS Word version of this template available at www.environment.gov.au//carbon-neutral, including by replacing text in square brackets as prompted. Text in blue italics is for guidance and should be deleted.

Report on verification type audit of a carbon neutral claim against the National Carbon Offset Standard for Products and Services

Audited body

Name and address of audited body

Name of contact person for audited body

Position title

Contact person phone number

Contact person email address

Audited body’s street address

Audit description

Kind of audit engagement Verification

Product(s) or service(s) covered by engagement

Reporting period covered by engagement

Date terms of engagement signed

Date audit report signed

Audited emissions inventory [insert year e.g. 2017–18]

Audited Scope 1 emissions (tonnes CO2-e)Audited Scope 2 emissions (tonnes

24

CO2-e)Audited Scope 3 emissions (tonnes CO2-e)Emissions reduced through LGCs (tonnes CO2-e)Total retired offsets (tonnes CO2-e)

Auditor detailsThe auditor must confirm that they are a suitably qualified auditor in accordance with the National Carbon Offset Standard for Products and Services. Rotation of auditors is required where five consecutive audits have been carried out by an individual auditor for the audited body.

Name of audit team leader

Organisation

Phone number

Address

Names and contact details of other audit team members if applicable

Lead auditor’s relevant qualifications, registrations and credentials

These must include:

NGER registration number;

Accreditation against ISO 14065:2013; or

Accreditation against recognised international standard based on ISO 14040.

[Insert name of audit organisation] confirms that we are not aware of any actual or perceived conflict of interest in having completed this engagement.

[Insert name of lead auditor] confirms that he/she has not carried out more than four previous consecutive audits for [insert audited body name].

25

Report of factual findings [Insert name of auditor or auditor’s organisation] was engaged to undertake a verification engagement of [insert name of audited body]’s carbon neutral claim for [insert name of product(s) or service(s)] in accordance with the requirements set out in the National carbon offset standard for Products and Services (the standard). The procedures set out below have been applied to the documentation that forms and supports the carbon neutral claim. Where the carbon neutral claim is used as a basis for certification against the standard, the Australian Government Department of the Environment and Energy determines whether the factual findings provide a reasonable basis for certification. We do not express any conclusion, nor do we provide any assurance regarding the carbon neutral claim or certification.

Factual findingsThe procedures were performed to ensure the carbon neutral claim was in accordance with the requirements set out in the National Carbon Offset Standard for Products and Services.

The procedures performed and the factual findings obtained are as follows:

Auditor to delete rows that are not applicable to an Environmental Product Declaration or product greenhouse gas inventory as relevant.

Test performed Factual findings Errors, exceptions or contraventions identified

AUP1: Preparation of the product greenhouse gas inventory

Verify that the product GHG inventory has been prepared in accordance with current international standards.

[Insert findings] [None/detail the exceptions]

Verify that the time period for the product GHG inventory has been clearly stated and is for the correct reporting period.

[Insert findings] [None/detail the exceptions]

AUP2: Product or service scope and emissions boundary

Verify that the product or service has been fully described.

[Insert findings] [None/detail the exceptions]

Verify that the functional unit or declared unit has been described.

[Insert findings] [None/detail the exceptions]

26

Verify that all material uncertainties are clearly documented and valid.

[Insert findings] [None/detail the exceptions]

Verify that the emissions boundary has been clearly defined.

[Insert findings] [None/detail the exceptions]

Verify that any exclusions from the emissions boundary have been clearly stated and justified.

[Insert findings] [None/detail the exceptions]

AUP3: Calculation of emissions

Verify that all emissions sources have been clearly identified and catalogued.

[Insert findings] [None/detail the exceptions]

Verify that all exclusions of emissions from within the emissions boundary have been clearly stated and justified.

[Insert findings] [None/detail the exceptions]

Verify that renewable energy certificates have been treated correctly.

[Insert findings] [None/detail the exceptions]

Verify that any carbon neutral claimed products/services are genuinely National carbon offset standard certified.

[Insert findings] [None/detail the exceptions]

Verify that Scope 1 and Scope 2 emission factors have been sourced from approved sources.

[Insert findings] [None/detail the exceptions]

Verify that Scope 3 emission factors have been sourced from appropriate sources.

[Insert findings] [None/detail the exceptions]

Verify activity data for all material emission sources identified in the product GHG assessment.

[Insert findings] [None/detail the exceptions]

Verify that emissions have been calculated correctly for each emissions source.

[Insert findings] [None/detail the exceptions]

Verify that total emissions have been correctly calculated.

[Insert findings] [None/detail the exceptions]

AUP4: Product GHG inventory analysis

27

Verify that the data collection procedures and calculation methodologies have been clearly stated.

[Insert findings] [None/detail the exceptions]

Verify that the sources of information and activity data have been clearly identified.

[Insert findings] [None/detail the exceptions]

Verify that regional variations in emission factors have been accounted for.

[Insert findings] [None/detail the exceptions]

Verify that data periods and database and software versions used have been disclosed.

[Insert findings] [None/detail the exceptions]

Verify that assumptions and constraints have been clearly described and justified.

[Insert findings] [None/detail the exceptions]

AUP5: Base year identification

Verify that the Product GHG inventory base year has been correctly identified.

[Insert findings] [None/detail the exceptions]

Verify that significant changes in the carbon account since base year have been disclosed.

[Insert findings] [None/detail the exceptions]

AUP6: Environmental Product Declaration verification

Confirm that the EPD has been verified in line with the requirements of the Australasian EPD Programme.

[Insert findings] [None/detail the exceptions]

Confirm that the EPD verifier is a qualified auditor under the Product and Service Standard.

[Insert findings] [None/detail the exceptions]

AUP7: Calculation of emissions

Verify that renewable energy certificates have been treated correctly.

[Insert findings] [None/detail the exceptions]

Verify that any carbon neutral claimed products/services are genuinely National carbon offset standard certified.

[Insert findings] [None/detail the exceptions]

28

Verify that Scope 1 and Scope 2 emission factors have been sourced from approved sources.

[Insert findings] [None/detail the exceptions]

AUP8: Emissions reductions

Verify that the emissions reduction strategy has been adequately described.

[Insert findings] [None/detail the exceptions]

Verify that emissions reduction measures have been considered and documented.

[Insert findings] [None/detail the exceptions]

Verify that quantities of planned emissions reductions have been estimated where practicable.

[Insert findings] [None/detail the exceptions]

Verify that total estimated emissions reductions have been calculated where practicable.

[Insert findings] [None/detail the exceptions]

AUP9: Carbon offsetting

Assess the offset units. [Insert findings] [None/detail the exceptions]

Assess reporting of offsets banked for future years.

[Insert findings] [None/detail the exceptions]

Assess reporting of previously banked offsets used this reporting period.

[Insert findings] [None/detail the exceptions]

AUP10: Record keeping, data management and quality control

Verify the adequacy of record keeping and data management practices.

[Insert findings] [None/detail the exceptions]

Verify that records of reporting documents have been kept.

[Insert findings] [None/detail the exceptions]

Verify that responsibility for record keeping is clearly stated.

[Insert findings] [None/detail the exceptions]

Verify that quality control practices have been described.

[Insert findings] [None/detail the exceptions]

29

AUP11: Trade mark use and marketing

Verify that adequate records have been kept of use of the Carbon Neutral Certification Trade Mark.

[Insert findings] [None/detail the exceptions]

Verify that approval has been sought for Trade Mark use in accordance with the User Guide.

[Insert findings] [None/detail the exceptions]

AUP12: Reporting documents

Verify that the reporting documents are consistent.

[Insert findings] [None/detail the exceptions]

Verify the signed declaration in the Public Disclosure Summary.

[Insert findings] [None/detail the exceptions]

Documents reviewedThis section provides details of all documents reviewed by the Auditor during the audit. Auditor to add rows as necessary.

Name or description of document Document title / filename

Author and date prepared, and version if applicable

Other matters to be reportedAspects impacting on the verification engagement [Insert any details of aspects of the matter being audited that particularly impacted on the carrying out of the verification engagement.]

Other matters[Insert any details of any matter related to the matter being audited that the audit team leader has found during the carrying out of the verification engagement that he or she believes amount to a contravention of the National Carbon Offset Standard for Products and Services.]

30

Restriction on use of reportThis report is intended for solely for the use of the audited body and the Department of the Environment and Energy, solely for use to verify carbon neutral claims under the National Carbon Offset Standard for Products and Services. Accordingly, we expressly disclaim and do not accept any responsibility or liability to any party other than these intended users for any consequences of reliance on this report for any purpose.

Yours faithfully[Signature—of audit team leader]

[Name—of audit team leader][Organisation][Date]

31

Appendix 1 Choosing an assurance or verification engagement

The National Carbon Offset Standard for Products & Services (Product & Service Standard) allows the entity responsible for the carbon neutral claim to choose an assurance type audit or a verification engagement.

Table 2 Definitions of assurance engagement and verification engagement

Assurance engagement definition Verification engagement definition

The audit team leader uses professional judgment in preparing for and carrying out the audit and provides an independent opinion about the matter being audited.

The audit team leader carries out specified procedures to verify the matter being audited but does not provide any assurance or an audit opinion.

Source: National Greenhouse and Energy (Audit) Determination 2009

Reasons for choosing one audit engagement type over the other may include:

• Using an EPD as the basis of the carbon neutral claim. A verification

engagement under the Product and Service Standard recognises the

verification already undertaken for an EPD, provided that the EPD was verified

against the EN 15804 Standard by an Australian Life Cycle Assessment Society

certified practitioner. (Products and services that do not have an EPD, or have

an EPD that was not verified in this way, can also undergo a verification type

audit but there are more procedures that the auditor must perform in these

cases).

• Having responsibility for a second carbon neutral claim under a different

category of the Standard. In these cases it may be simpler and more cost

effective to commission a single assurance audit for both claims because the

other categories of the standard do not allow verification engagements.

• Other reasons identified by the auditor or audited body.

32