Embed Size (px)

Citation preview

Basic ConceptsPart 1

Economics

Study of scarcity and choice. People, firms, and governments make

choices because of scarcity.

Micro v Macro

Microeconomics Macroeconomics

•Focuses on the choices of individuals, households, and firms•“Bottom-up”

•Questions like:• Should a

business hire another worker

• Should I got to college or get a job?

VIDEO CLIP!

•Focuses on the economy as a whole and aggregate data (GDP, Unemployment, Inflation) and how it can be manipulated•“Top-down”

•Questions like:• How many

people are employed in the US Right now?

• What policies could the government adopt to increase economic growth?

Positive v Normative

Positive Normative

Focuses on concepts that have definitive answers.

Right answer everyone can agree on

Focuses on how the world should work.

“What if” questions or questions where there can be disagreement over the final outcome.

Scarcity: The Fundamental Problem

Rule one of Economics: Resources are scarce Resource = anything used to produce

something else

Productive Resources

A.K.A. Factors of Production Can be divided into four areas

LAND▪ Water, minerals, oil, and other natural resources

LABOR▪ The effort of workers

CAPITOL▪ Machinery, buildings, and tools used in production

of goods and services ENTREPRENUERSHIP

▪ Risk taking, innovation, and orginizational skills

Opportunity Cost

The economic “cost” of the decision is the benefit or alternative you give up to do something.

Example:

Production Possibilities Curves

Before we begin…

Just about every graph we do in this class is in Quadrant I of a x y plane X = Horizontal Y = Vertical O = origin (0,0)

Now that we have reviewed basic math…

I

Production Possibilities Curves

Graphical representation of the trade-off an economy must face when allocating resources between two goods

The frontier of the curve shows the maximum quantity of one good that can be produced for each quantity of the other

Production Possibilities Curve

0 10 20 30 40 50 600

10

20

30

40

50

60

Production Possibilities

Planes

Cars

Cars Planes

50 0

40 10

30 20

20 30

10 40

0 50

Frontier

PPCs and Efficiency

Points that are on the curve (or frontier) itself represent the use of all resources for production Maximum utilization of resources = efficiency

Points falling under the curve are feasible, but not efficient. This is called underutilization. An economy

producing below what it is capable is not efficient.▪ This can be caused by inefficiencies such as high

unemployment,

PPCs and Efficiency

In this graph: Points “H” and “D” (and

all other points on the curve itself) represent efficiency. ▪ more output can be

achieved from the given inputs

Point “B” represents underutilization. ▪ Producing this combination

of goods would be inefficient.

What can we determine about point “A”?

Points outside the PPC Frontier

Points beyond the PPC Frontier are considered to be unattainable due to scarcity of resources.

PPCs and Growth

A change in the amount of resources will change the frontier.

The curve will shift right when: More productive

resources become available

Better technology allows you to use your resources more efficiently.

PPCs and Opportunity Cost

Since resources are scarce, increasing production of a first good entails decreasing production of a second Scarce resources must be transferred to

the first and away from the second. The loss of production of one good to

increase production of the other is the opportunity cost.

Constant Opportunity Cost PPCs If the opportunity cost

to change production remains the same at all production points, the PPC will be straight.

The more similar the resources needed to produce each good, the straighter the PPC will be.

Constant Opportunity Cost PPCs

The slope of a straight line PPC = Opportunity Cost

Slope for a straight line PPC should always be negative

Increasing Opportunity Cost PPCs

The PPC is "bowed outward" (concave) from the origin. This represents INCREASING OPPORTUNITY COST. As more scarce resources are

used to increase production of one good or service, production of another good or service falls by larger and larger amounts.

The less similar the resources needed to produce each good, the further the PPC will be bowed out from the origin.

Economic Systems

System that coordinates production and distribution of goods and services.

Must answer the THREE BASIC questions of: What to produce? How to produce it? Who will consume it?

3 Basic types

Traditional Market Command

3 questions are answered by tradition and custom

3 questions are answered by individuals

3 questions are answered by the government.

• The way these questions are answered (and by whom) determines what type of economy

Centrally Planned Economies

The government…1.owns all the resources. 2.decides what to produce, how

much to produce, and who will receive it.

Examples:Cuba, North Korea, former Soviet

Union, and China

Two Types

COMMUNISM

Communism is a political system characterized by a centrally planned economy with all economic and political power resting in the hands of the government. Communist governments are authoritarian in nature.

SOCIALISM

Socialism is a social and political philosophy based on the belief that democratic means should be used to distribute wealth evenly throughout a society.

Advantages and Disadvantages

ADVANTAGES

1. Low unemployment-everyone has a job

2. Great Job Security-the government doesn’t go out of business

3. Equal incomes means no extremely poor people

DISADVANTAGES

1. No incentive to work harder

2. No incentive to innovate or come up with good ideas

3. No Competition keeps quality of goods poor.

4. Corrupt leaders5. Few individual

freedoms

Free Market System(aka Capitalism)

1. Little government involvement in the economy. (“Laissez Faire” = Let it be)

2. Individuals OWN resources and answer the three economic questions.

3. The opportunity to make PROFIT gives people INCENTIVE to produce quality items efficiently.

4. Wide variety of goods available to consumers.

5. Competition and Self-Interest work together to regulate the economy (keep prices down and quality up).

The “Invisible Hand”

The concept that society’s goals will be met as individuals seek their own self-interest.

Example: Society wants fuel efficient cars…• Profit seeking producers will

make more.• Competition between firms

results in low prices, high quality, and greater efficiency.

• The government doesn’t need to get involved since the needs of society are automatically met.

• Competition and self-interest act as an invisible hand that regulates the free market.

Advantages and Disadvantages

ADVANTAGES

Economic Efficiency As a self-regulating system,

a free market economy is efficient.

Economic Growth Because competition

encourages innovation, free markets encourage growth.

Economic Freedom Free markets offer a wider

variety of goods and services than any other economic system

DISADVANTAGES

Lack of Economic Equity

With freedom comes a degree of instability

The reality

All modern economies are a mix of market and command “Mixed” economies

Continuum of Mixed Economies

Centrally planned Free market

Source: 1999 Index of Economic Freedom, Bryan T. Johnson, Kim R. Holmes, and Melanie Kirkpatrick

Hong KongThe United

States

North Korea

Cuba

China

France

Canada

Greece

SingaporeThe United Kingdom

Mixed Economy

Government takes of people’s needs Marketplace takes care of people’s

wants.

Circular Flow model

Simplified view of how money and resources move through an economy.

In the circular flow model, the inter-dependent entities of producer and consumer are referred to as "firms" and "households" respectively and provide each other with factors in order to facilitate the flow of income.

Firms provide consumers with goods and services in exchange for consumer expenditure and "factors of production" from households.

Circular Flow of Economic Activity

Product Market (Goods & Services)

Goods & ServicesGoods & Services

Households/Individuals Businesses/Firms

$$$$$$ $$$$$$$$

Factor/Resource Market

(Factors of Production)

Factors of Production FOP

Circular Flow model

Product Market

Product Market - any setting where goods and services are bought and sold by producers and consumers Kroger, target, Taco Bell, ebay

▪ This type of market is where goods and services are bought by you

▪ Basically any purchase you make is in this market

▪ Bought by Households, sold by firms (businesses)

Factor Market

Factor Market – any setting where land, labor, capital, and entrepreneurship are bought and sold by producers and consumers This market is where Factors of

Production are sold by you (households) and bought by firms (businesses)▪ The best example – wages earned for

your labor▪ This market is where households earn

money to spend in the Product market

http://www.reffonomics.com/TRB/Chapter3/circularflow5.swf

International Trade

The process of buying goods and services from the rest of the world (importing) and that of selling goods and services to the rest of the world (exporting) is referred to as international trade

Why Trade?

Differences in Factor endowments Variety and quality of goods Gains from specialization Political reasons

Absolute Advantage

Adam Smith

1723-1790 “Father of Modern

Economics” Wrote “The Wealth of

Nations” Smith argued that it was

impossible for all nations to become rich simultaneously by following mercantilism and instead stated that all nations would gain simultaneously if they practiced free trade and specialized in accordance with their absolute advantage

Absolute Advantage

A country has an absolute advantage in the production of a good when it can produce more of that good than another country with the same resources.

Wine ComputersFrance 70 2

US 50 3

Suppose that by using x units of resources…

The French have an absolute advantage in the production of wine

Another Example

One of your friends, Gina, can print 5 t-shirts or build 3 birdhouses an hour.

Your other friend, Mike, can print 3 t-shirts an hour or build 2 birdhouses an hour.

Because your friend Gina is more productive at printing t-shirts and building birdhouses compared to Mike, she has an absolute advantage in both printing t-shirts and building birdhouses.

Comparative Advantage

David Ricardo

Came up with the law of comparative advantage.

According to this law, specialization and free trade benefits all trading partners. Countries should

specialize in those goods they can produce at the lowest opportunity cost

Comparative Advantage

The ability of a firm or individual to produce goods and/or services at a lower opportunity cost than other firms or individuals. A comparative advantage gives a company the

ability to sell goods and services at a lower price than its competitors and realize stronger sales margins.

This is not the same as being the best at something.

Comparative advantage is the basis for all trade between individuals, regions, and nations.

Production Possibilities without Trade

India can produce 4,000 yards of textile per day or 1 ton of chocolate per day.

Nepal can produce 1,000 yards of textile a day or 4 tons of chocolate per day.

Production Possibilities without Trade

India has a comparative advantage in producing textiles.

Nepal has a comparative advantage in chocolate.

Production Possibilities without Trade

1 2 3 4 5

4

3

2

1

5

Chocolate (in tons)

Text

iles

(in

thou

san

ds

of y

ards

)

Nepal

India

McGraw-Hill/Irwin

Production Possibilities without Trade

India has chosen to produce 2,000 yards of textiles and 0.5 tons of chocolate.

Nepal has chosen to produce 500 yards of textile and 2 tons of chocolate.

Production Possibilities without Trade

India’s and Nepal’s Individual Possibilities

Textile per day Chocolate per day

India 2,000 yards 0.5 ton

Nepal 500 yards 2 tons

Total 2,500 yards 2.5 tons

Production Possibilities without Trade

Point A: The combination of textile and chocolate chosen by India.

Point B: The combination of textile and chocolate chosen by Nepal.

Point C: The joint combination without trade.

Production Possibilities without Trade

1 2 3 4 5

4

3

2

1

5

Chocolate (in tons)

Text

iles

(in

thou

san

ds

of y

ards

)

Nepal

India

A

B

C

McGraw-Hill/Irwin © 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Production Possibilities without Trade

The two extreme combinations are: both countries producing only textile

(point D) both producing only chocolate (point E).

The combined production possibilities curve with no trade is drawn by connecting these two points.

Production Possibilities without Trade

1 2 3 4 5

4

3

2

1

5

Chocolate (in tons)

Text

iles

(in

thou

san

ds

of y

ards

)

Nepal

India

A

B

C

D

E

Joint ( trade)

McGraw-Hill/Irwin © 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

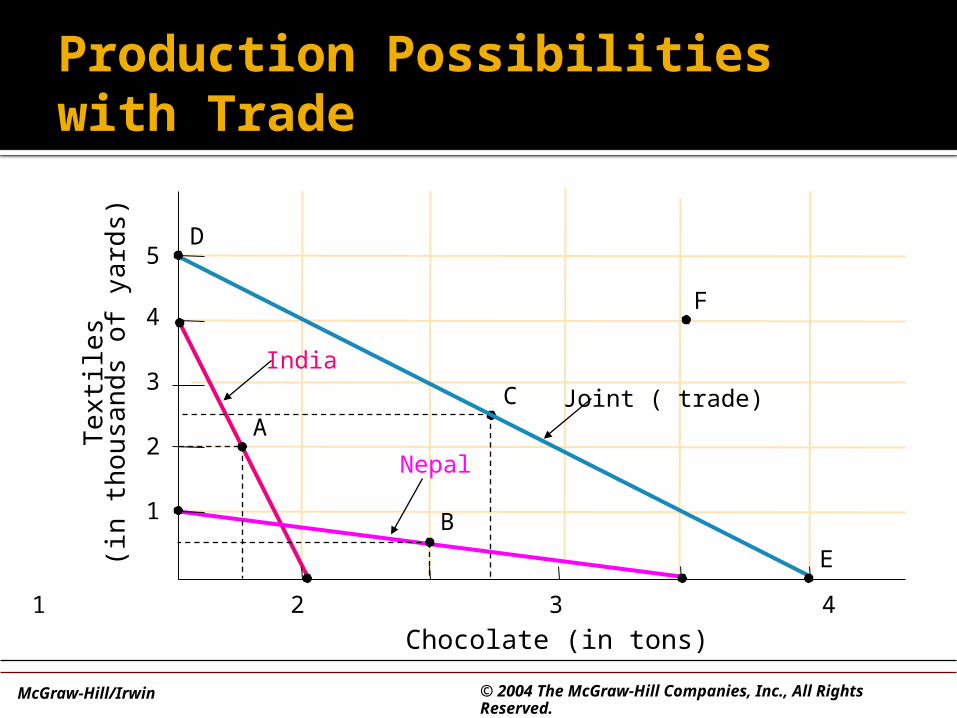

Production Possibilities with Trade

Point F: This is where each nation is focusing on that activity for which it has a comparative advantage. India produces 4,000 yards of textile. Nepal produces 4 tons of chocolate.

Production Possibilities with Trade

1 2 3 4 5

4

3

2

1

5

Chocolate (in tons)

Text

iles

(in

thou

san

ds

of y

ards

)

Nepal

India

A

B

C

D

E

Joint ( trade)

McGraw-Hill/Irwin © 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

F

Output Questions:

OOO=Output: Other goes Over

58

Input Questions:

IOU= Input: Other goes Under

59

Practice FRQ

A. Which country has an absolute advantage in the production of tractors? Explain how you determined your answer.

B. Which country has an absolute advantage in the production of cars? Explain how you determined your answer.

C. Which country has a comparative advantage in the production of cars? Use the concept of opportunity cost to explain how you determined your answer.

D. For Xanadu, what is the opportunity cost of producing one car?

E. If the two countries specialize and trade with each other, which country will import cars? Explain why?

10 Points Possible (2 Points For EACH: 1 point answer, 1 point

explanation)A. Answer-XanaduExplanation- Because they can produce more total tractors than Atlantis.

B. Answer-AtlantisExplanation- Because they can produce more total cars than Xanadu.

(2 Points For EACH: 1 point answer, 1 point explanation)C. Answer- Atlantis

Explanation- Because the opportunity cost for Atlantis to make one car is 1/3 a tractor which is less than then the opportunity cost for Xanadu (1 car =2 tractors).

D. Answer- Opportunity Costs is 2 Tractors.No explanation required

(2 Points For EACH: 1 point answer, 1 point explanation)E. Answer- Xanadu will import cars

Explanation- Xanadu should not make cars. They should specialize in making tractors and import cars from Atlantis since they have a lower opportunity cost.

Introduction to Macroeconomics

Business Cycle

Simplified view of the upturns and downturns in the macroeconomy

The increases and decreases in output consisting of four phases: Peak: highest point of

output Recession: output declining

for 6 months Trough: lowest point of

output Recovery: output increasing

(trough to peak)

Business Cycle

People generally prefer steady, stable growth to large “ups” and “downs.” Therefore, government policies, both fiscal and monetary (see later sections), are aimed at flattening the business cycle.

The government wants not only to stimulate the economy when it’s slow, but also to slow it down when it’s growing too quickly.

Employment & Unemployment

EMPLOYMENT

Total number of people working for pay

UNEMPLOYMENT

Total number of people looking for work that are not currently employed

LABOR FORCE

• Sum of employment and unemployment.

Unemployment Rate

Percentage of labor force that is unemployed

# UnemployedUnemployment Rate

Labor Force• Increases during

recession• Decreases during a

recovery

Aggregate output

Total production of all goods and services in the economy Measured by real GDP

Decreasing output leads to a recession

Increasing output leads to a recover/expansion

Inflation & Deflation

Inflation Rise in the general level of prices Reduces the purchasing power of money Measured with the Consumer Price Index

(CPI) Increases during periods of expansion

Deflation The opposite of inflation Prices go down Purchasing power of money increases

Activity

1. Draw and label the business cycle2. Explain what happens to output,

unemployment, and inflation in each stage.

![[PPT]Chapter 1: What is Economics? - Mr. Charles | … · Web viewSection 1: Scarcity and Factors of Production What is Economics? What is Economics? The study of scarcity and choices](https://img.dokumen.tips/doc/110x75/5ae393c17f8b9ad47c8e7988/pptchapter-1-what-is-economics-mr-charles-viewsection-1-scarcity-and.jpg)