Embed Size (px)

Citation preview

© Henley Business School 2008 www.henley.reading.ac.uk

School of Real Estate & Planning

Optimal Portfolio Allocation using TLI

Tommaso Gabrieli University of Reading

Davide Manstretta IPD

School of Real Estate & Planning

Introduction• Motivation

– Property market returns (IPD) are based on Valuers’ appraisal

– Vast literature argues that data underestimates true volatility

(smoothing)

– New IPD series Transaction-Linked Index (TLI) should

represent true returns and correct for the problem

• Devaney and Martinez Diaz JPR 2011

• Research Questions:– Is TLI series different form de-smoothed Valuers’ Based

Index (VBI) series?

– Implications for portfolio allocation?

2

School of Real Estate & Planning

Agenda

• Introduction and Results Overview

• A little bit of theory:– Problem definition

• Empirical Results:– Differences between TLI and de-smoothed VBI

– Portfolio Allocation analysis

• Conclusions• Main Result

– TLI and de-smoothed VBI are very different; strong implications for portfolio allocation

3

School of Real Estate & Planning

TLI vs. VBI capital growth, QTLY 2002-2010

4

Sep-

02

Jan-

03

May-0

3

Sep-

03

Jan-

04

May-0

4

Sep-

04

Jan-

05

May-0

5

Sep-

05

Jan-

06

May-0

6

Sep-

06

Jan-

07

May-0

7

Sep-

07

Jan-

08

May-0

8

Sep-

08

Jan-

09

May-0

9

Sep-

09

Jan-

10

May-1

0

Sep-

10

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

TLI q410IPD VBI CG

Quarter

Returns

School of Real Estate & Planning

Smoothing • Assumptions:

– Property Market Returns are Valuation Based• May Lag Market Movements – Distorts Correlation• May Be “Smoothed” – Understates the Volatility

– “De-smoothing” Procedures• Remove the Impact of Valuations in Data

– Reported return is a blend of “true” and previous return

• De-smoothing:– Rv

t = a Rvt-1 + (1-a)Rt

Therefore Rt = {Rvt - a Rv

t-1 } / (1-a)

where a is the “smoothing parameter”

• Vast literature: – Blundell and Ward (1987), Quan and Quigley (1991), Brown

and Matysiak (2000), Geltner et al. (2002) and many others…

5

School of Real Estate & Planning

TLI vs. De-smoothedTLI Des

0.8Des 0.65

Des 0.5

Des 0.25

Des 0.1

VBI

St Dev

6.4 15.2 8.8 6.5 5.1 4.7 4.5

AR1 0.2 0.1 0.3 0.4 0.6 0.7 0.76

Corr with TLI

1 0.38 0.52 0.62 0.72 0.74 0.74

6

School of Real Estate & Planning

TLI vs. De-smoothed

7

Sep-02

Dec-02

Mar-03

Jun-03

Sep-03

Dec-03

Mar-04

Jun-04

Sep-04

Dec-04

Mar-05

Jun-05

Sep-05

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Mar-07

Jun-07

Sep-07

Dec-07

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

TLI q410

VBI des 65%

VBI des 10%

Quarters

Returns

School of Real Estate & Planning

TLI vs. De-smoothed (Q3 2002 – Q1 2007)

TLI Des 0.8

Des 0.65

Des 0.5

Des 0.25

Des 0.1

VBI

St Dev

4.80 5.1 2.8 2.0 1.4 1.3 1.2

AR1 -0.34 -0.4 -0.3 -0.1 0.3 0.5 0.6

Corr with TLI

1.00 0.33 0.34 0.35 0.32 0.30 0.29

8

School of Real Estate & Planning

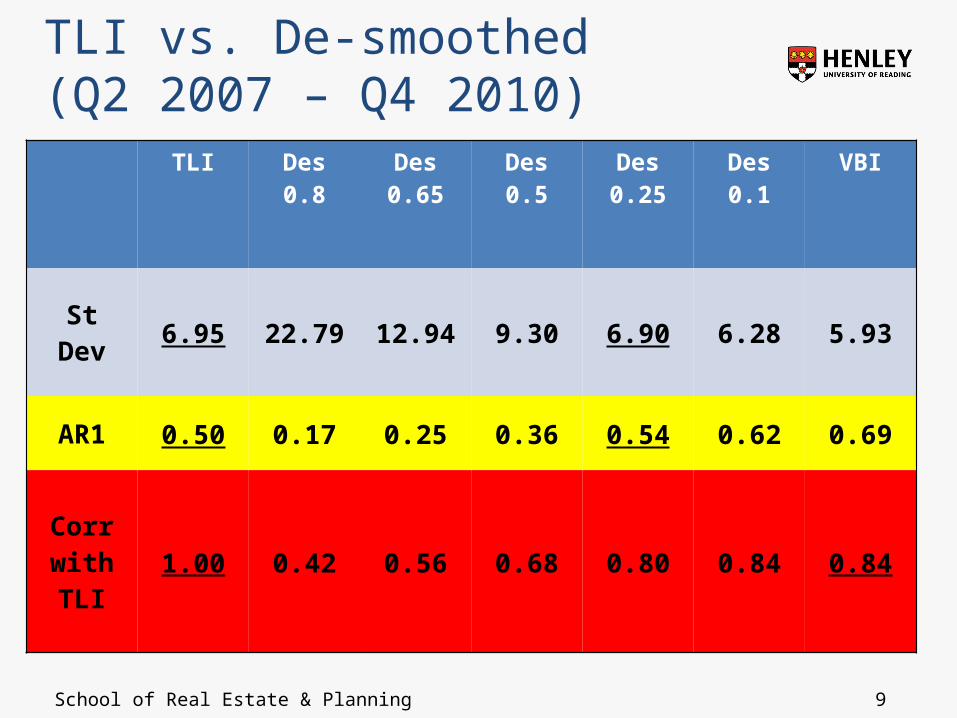

TLI vs. De-smoothed (Q2 2007 – Q4 2010)

TLI Des 0.8

Des 0.65

Des 0.5

Des 0.25

Des 0.1

VBI

St Dev

6.95 22.79 12.94 9.30 6.90 6.28 5.93

AR1 0.50 0.17 0.25 0.36 0.54 0.62 0.69

Corr with TLI

1.00 0.42 0.56 0.68 0.80 0.84 0.84

9

School of Real Estate & Planning

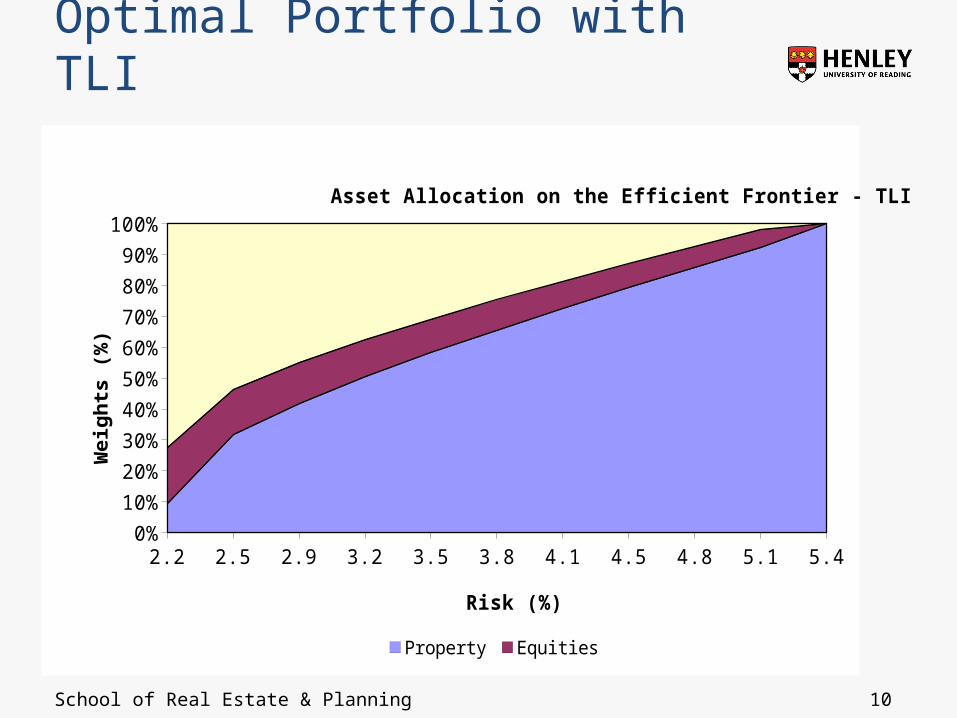

Optimal Portfolio with TLI

10

2.2 2.5 2.9 3.2 3.5 3.8 4.1 4.5 4.8 5.1 5.4 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Asset Allocation on the Efficient Frontier - TLI

Property Equities Gilts

Risk (%)

We

igh

ts (

%)

School of Real Estate & Planning

Optimal Portfolio, TLI vs. VBI

11

2.2

2.5

2.9

3.2

3.5

3.8

4.1

4.5

4.8

5.1

5.4

0%20%40%60%80%

100%Asset Allocation on the Efficient Frontier - TLI

Risk (%)

Wei

gh

ts (

%)

1.8

2.5

3.2

3.9

4.5

5.2

5.9

6.6

7.2

7.9

8.6

0%20%40%60%80%

100%

Asset Allocation on the Efficient FrontierUnsmoothed Property Data

Risk (%)

Wei

gh

ts (

%)

1.8

2.5

3.1

3.8

4.5

5.2

5.9

6.5

7.2

7.9

7.8

0%20%40%60%80%

100%

Asset Allocation on the Efficient FrontierDe-Smoothed (0.65) Property Data

Risk (%)Wei

gh

ts (

%)

1.8

2.5

3.1

3.8

4.5

5.2

5.9

6.5

7.2

7.9

7.8

0%20%40%60%80%

100%

Asset Allocation on the Efficient FrontierDe-Smoothed (0.25) Property Data

Risk (%)Wei

gh

ts (

%)

School of Real Estate & Planning

Optimal Portfolio, TLI vs. VBI (Q3 2002 – Q1 2007)

12

2.2

2.5

2.9

3.2

3.5

3.8

4.1

4.5

4.8

5.1

5.4

0%20%40%60%80%

100%Asset Allocation on the Efficient Frontier - TLI

Risk (%)

We

igh

ts (

%)

1.8

2.5

3.2

3.9

4.5

5.2

5.9

6.6

7.2

7.9

8.6

0%

50%

100%

Asset Allocation on the Efficient FrontierUnsmoothed Property Data

Risk (%)

Wei

gh

ts (

%)

1.8

2.5

3.1

3.8

4.5

5.2

5.9

6.5

7.2

7.9

7.8

0%

50%

100%

Asset Allocation on the Efficient FrontierDe-Smoothed (0.65) Property Data

Risk (%)

We

igh

ts (

%)

1.8

2.5

3.1

3.8

4.5

5.2

5.9

6.5

7.2

7.9

7.8

0%

50%

100%

Asset Allocation on the Efficient FrontierDe-Smoothed (0.25) Property Data

Risk (%)

Wei

gh

ts (

%)

School of Real Estate & Planning

Efficient Frontier

13

1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 -

0.5

1.0

1.5

2.0

2.5

3.0

3.5

VBI

VBI des 025

TLI

VBI des 065

St Dev

Retu

rns

School of Real Estate & Planning

Conclusion• Findings

– According to TLI, property is a very attractive asset class– TLI and De-smoothed VBI are very different, which is

theoretically worrying...

• Extensions– Annual Data– Implied smoothing parameter

14

School of Real Estate & Planning

Thank you for your attention

Questions?

Comments?

15