Embed Size (px)

Citation preview

Axia Economicswww.axiaecon.com

Comparing pension systems

MethodologySelected results for OECD countries, Eastern Europe/Central Asia, Latin America/Caribbean

Edward Whitehouse

Comparing pension systems

Fiscal approach: projections of pension expenditure

Institutional approach: describing pension systems’ parameters

Income-distribution analysis: comparing incomes of older people and the

population as a whole

A microeconomic approach

Model of pension entitlements at the individual level Goal: quantitative indicators of pension-system parameters

for cross-country monitoring of retirement-income systems Consistent across a broad range of countries Covers all mandatory pensions

resource-tested schemes (including social assistance) basic schemes minimum pensions earnings-related public and mandatory private schemes mandatory defined-contribution plans

Includes effect of personal income tax and social security contributions

A microeconomic approach

Full-career workers contribute every year from age 20 (or standard entry age) to

normal pension eligibility age Across the earnings distribution: (0.3 to 5 times average

pay) All currently legislated reforms fully in place

‘steady-state’ assumption new labour-market entrants

Macroeconomic assumptions earnings growth (individual and economy): 2% real rate of return (on funded pensions): 3.5% discount rate (for actuarial calculations): 2% mortality rates: latest data for individual countries and

regional averages

Results

Relative pension value pension entitlement as a proportion of

economy-wide average earnings

Indicators of redistributive power of pension systems overall generosity of schemes: average

pension value potential resource transfer to pensioners:

average pension wealth

Pension values0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsio

n va

lue

0 .5 1 1.5 2 2.5Earnings

Pension values: OECD0

.25

.5.7

51

1.25

1.5

1.75

2G

ross

pen

sion

val

ue

0 .5 1 1.5 2 2.5Earnings

Ireland

Canada

UK

NZ

Czech R

Pension values: OECD0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsio

n v

alu

e

0 .5 1 1.5 2 2.5Earnings

Finland

Spain

Austria

Hungary

Netherlands

Italy

Sweden

Poland

Pension values: OECD0

.25

.5.7

51

1.25

1.5

1.75

2G

ross

pen

sion

val

ue

0 .5 1 1.5 2 2.5Earnings

Switzerland

Norway

Belgium

Pension values: OECD0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsio

n va

lue

0 .5 1 1.5 2 2.5Earnings

Luxembourg

Mexico

Iceland

Australia

Pension values: OECD0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsio

n v

alue

0 .5 1 1.5 2 2.5Earnings

France

Korea

Germany

Slovak RUS

Japan

Pension values: OECD0

.25

.5.7

51

1.25

1.5

1.75

2G

ross

pen

sion

val

ue

0 .5 1 1.5 2 2.5Earnings

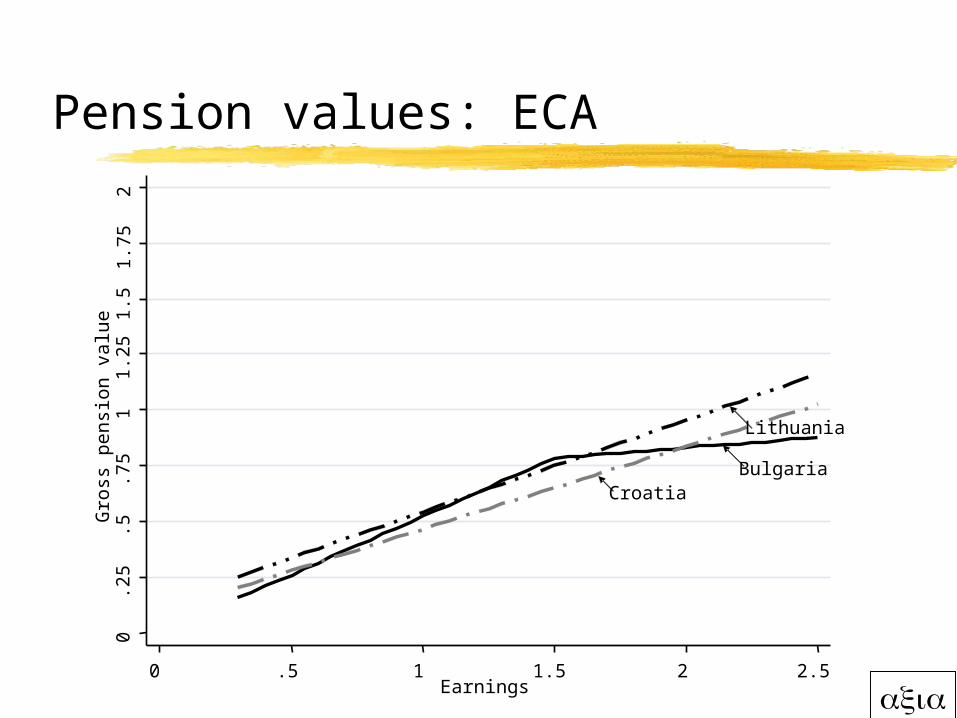

Pension values: ECA0

.25

.5.7

51

1.25

1.5

1.75

2G

ross

pen

sion

val

ue

0 .5 1 1.5 2 2.5Earnings

Bulgaria

Lithuania

Croatia

Pension values: ECA0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsio

n v

alu

e

0 .5 1 1.5 2 2.5Earnings

Hungary

Bulgaria

Macedonia

Latvia Poland

EstoniaKazakhstan

Lithuania

Croatia

Pension values: LAC0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsi

on

va

lue

0 .5 1 1.5 2 2.5Earnings

Costa Rica

Dominican R

Pension values: LAC0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsi

on

va

lue

0 .5 1 1.5 2 2.5Earnings

Costa Rica

Peru

Colombia

Dominican R

Mexico

El Salvador

Chile

Pension values: LAC0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsi

on

va

lue

0 .5 1 1.5 2 2.5Earnings

Costa Rica

Peru

Colombia

Argentina

Dominican R

Mexico

El Salvador

Chile

Pension values: LAC0

.25

.5.7

51

1.2

51

.51

.75

2G

ross

pe

nsi

on

va

lue

0 .5 1 1.5 2 2.5Earnings

Costa Rica

Uruguay

Peru

Colombia

Argentina

Dominican R

Mexico

El Salvador

Chile

Redistributive power

All pension systems redistribute income in many complex ways both between and within generations

Focus on one aspect: pension benefits of workers at different earnings levels

An ‘index of redistributive power’ of pension systems that is zero if rich and poor workers get the same replacement rate

(e.g., most funded plans, some public, defined-benefit schemes) is one if rich and poor workers get the same pension amount

(e.g., a universal, flat-rate ‘citizens pension’)

)(, xy

y

y

x

PV

PVI

y

xyx

Role of the tax system

Personal income tax systems are progressive so average effective tax rates are lower for people when

they are retired than when they were working (if replacement rates are less than 100 per cent)

Most countries have concessions for older people in their personal income taxes favourable treatment of pensioners (e.g., extra allowances) favourable treatment of pension income

Pensioners usually not liable for social security contributions (or pay at a much reduced rate)

Therefore, net replacement rates are higher than gross the personal tax system plays an important role in old-age

support

Difference in taxes paid by workers and pensioners

0 .5 1 1.5 2 2.5

-.05

0

.05

.1

.15

.2

.25

.3 Difference in average effective tax rate, percentage points

earnings/income, proportion of average

Germany

Canada

Australia

Finland

France

Difference in taxes paid by workers and pensioners

0 .5 1 1.5 2 2.5

-.05

0

.05

.1

.15

.2

.25

.3 Difference in average effective tax rate, percentage points

Norway

Japan

Netherlands

Italy

Korea

earnings/income, proportion of average

Difference in taxes paid by workers and pensioners

0 .5 1 1.5 2 2.5

-.05

0

.05

.1

.15

.2

.25

.3 Difference in average effective tax rate, percentage points

earnings/income, proportion of average

Sweden

United States

United KingdomSwitzerland

Spain

Gross and net replacement rates: Germany

0

0.25

0.5

0.75

1

1.25

0 0.5 1 1.5 2 2.5 3

Replacement rate,per cent of individual earnings

Individual earnings, proportion of average

Net

Gross

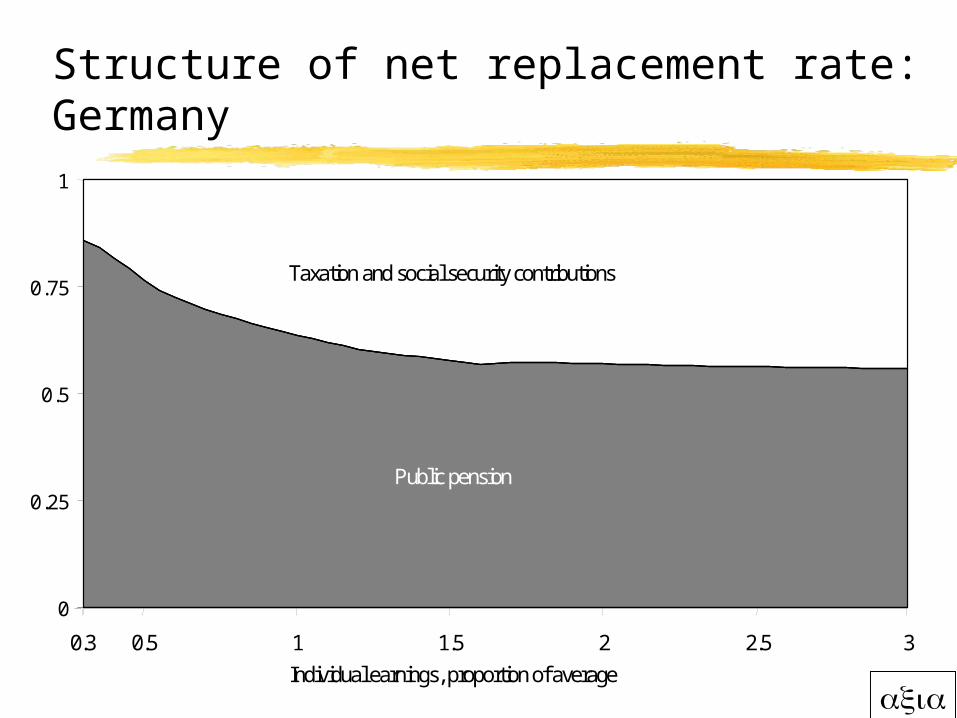

Structure of net replacement rate: Germany

0

0.25

0.5

0.75

1

0.3 0.5 1 1.5 2 2.5 3Individual earnings, proportion of average

Public pension

Taxation and social security contributions

System generosity

Calculate average pension value relative to economy-wide average earnings

Use same synthetic earnings distribution for all countries

System generosity

Calculate average pension value relative to economy-wide average earnings

Use same synthetic earnings distribution for all countries

0 1 2 3 4 5Earnings, multiple of average

Proportion of contributors

Potential resource transfer

Convert weighted average of relative pension value into pension wealth

Relationship between pension value at retirement and pension wealth depends on: indexation of pensions in payment pension eligibility age country-specific mortality

Calculating pension wealth

Pension eligibility age

Age 57 60 63 64 65 67 Value +27.0% +15.4% +3.8% 0 -3.8% -11.3%

Calculating pension wealth

Indexation

Indexing Prices Earnings 50:50 80:20 Value 0 +19.0% +8.9% +3.4%

Calculating pension wealth

Country-specific mortality e.g., life expectancy of Hungarian men is six

years below OECD average this reduces value of pension wealth by 19 per

cent in Australia, France, Japan, New Zealand and

Switzerland, life expectancy is two years above OECD average

this increases value of pension wealth by 7-8 per cent

Structure of pension systems: role of basic schemes

0 25 50 75 100

Estonia

Czech Republic

Lithuania

Canada

Norway

Japan

Netherlands

United Kingdom

Argentina

Ireland

New Zealand

Basic Means-tested DB DC

Per cent of weighted average of total pension wealth by source

Structure of pension systems: role of targeted schemes

0 25 50 75 100

Colombia

Iceland

Australia

Canada

Dominican R

Per cent of weighted average of total pension wealth by source

Structure of pension systems: role of DC schemes

0 25 50 75 100

Costa RicaUruguay

Argentina

Dominican R

ColombiaEl Salvador

ChileMexico

Peru

Per cent of weighted average of total pension wealth from DC scheme

Structure of pension systems: role of DC schemes

0 25 50 75 100

SwedenBulgaria

Costa RicaUruguayHungary

ArgentinaLithuania

EstoniaMacedonia

PolandLatvia

Dominican RCroatia

AustraliaColombia

El SalvadorChile

MexicoKazakhstan

Peru

Per cent of weighted average of total pension wealth from DC scheme

Conclusions

Microeconomic modelling of individual pension entitlements is a useful tool consistent approach across countries with very different

retirement-income systems forward-looking comprehensive: covering all mandatory sources of

retirement income incorporates effect of tax system can isolate the impact of pension policy choices from

the effects of earnings distribution, macroeconomic performance and demographics on the retirement-income system

Future

Gender Disability and survivors’ benefits Pension entitlements and age of retirement Sensitivity analysis Partial careers Special schemes (e.g., public-sector workers) Voluntary schemes (e.g., occupational plans) Incorporate financing of benefits Extend to other regions Regular updates