Embed Size (px)

Citation preview

© 2009 The Conference Board, Inc.1 www.conference-board.org

Ken GoldsteinThe Conference Board

Trusted Insights for Business Worldwide

LONG SLOW SLOG

© 2009 The Conference Board, Inc.2 www.conference-board.org

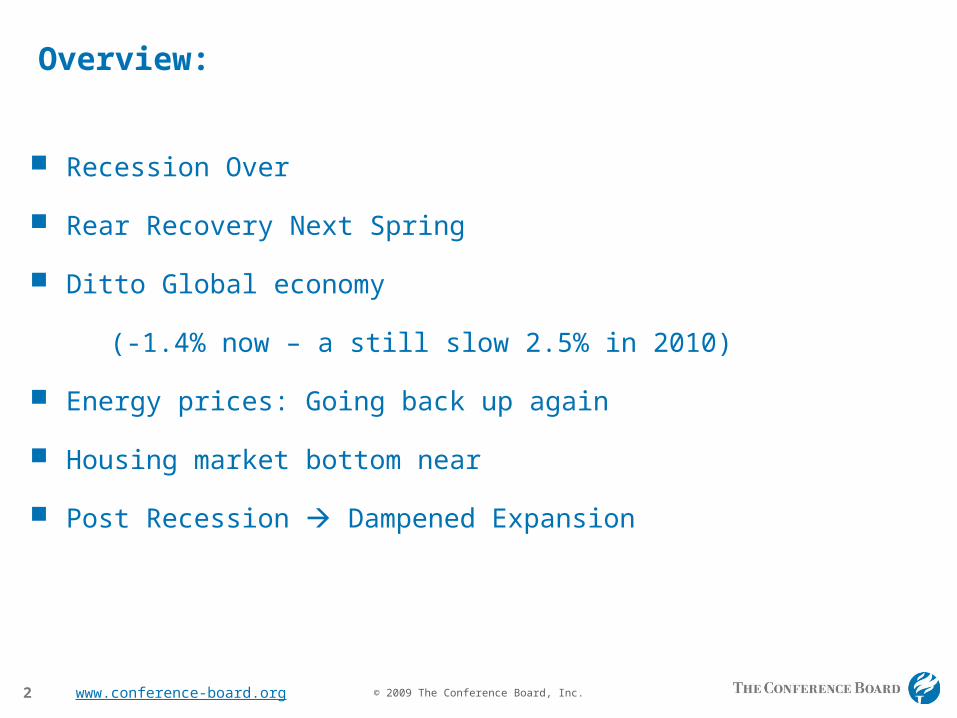

Overview:

Recession Over

Rear Recovery Next Spring

Ditto Global economy

(-1.4% now – a still slow 2.5% in 2010)

Energy prices: Going back up again

Housing market bottom near

Post Recession Dampened Expansion

© 2009 The Conference Board, Inc.3 www.conference-board.org

WHAT IS NOT CHANGING

1) DEMOGRAPHICS

2) PRODUCTIVITY

3) PRICE/COST

4) INTERNATIONALIZATION

© 2009 The Conference Board, Inc.4 www.conference-board.org

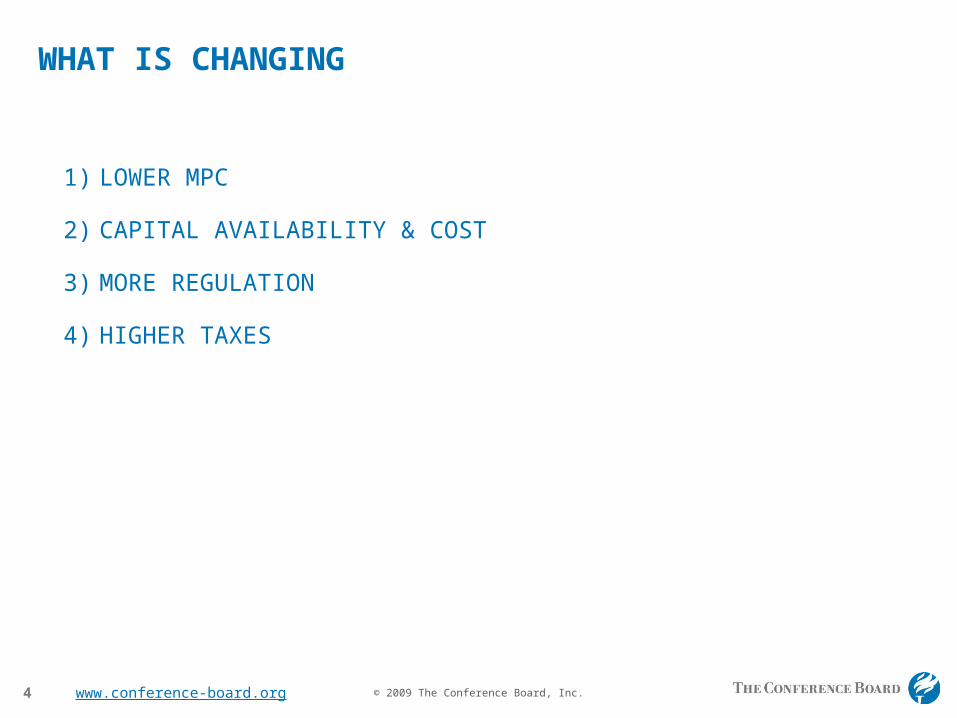

WHAT IS CHANGING

1) LOWER MPC

2) CAPITAL AVAILABILITY & COST

3) MORE REGULATION

4) HIGHER TAXES

© 2009 The Conference Board, Inc.5 www.conference-board.org

All Regions Are Slowly Turning

Notes: Shaded areas represent U.S. recessionsSource: The Conference Board

-30

-25

-20

-15

-10

-5

0

5

10

15

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

U.S. LEI (Jul '09)

Euro Area LEI (Jul '09)

Asia LEI (Jun '09)

6-month annualized percent change

© 2009 The Conference Board, Inc.6 www.conference-board.org

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1999 2000 '01 '02 '03 '04 '05 '06 '07 '08

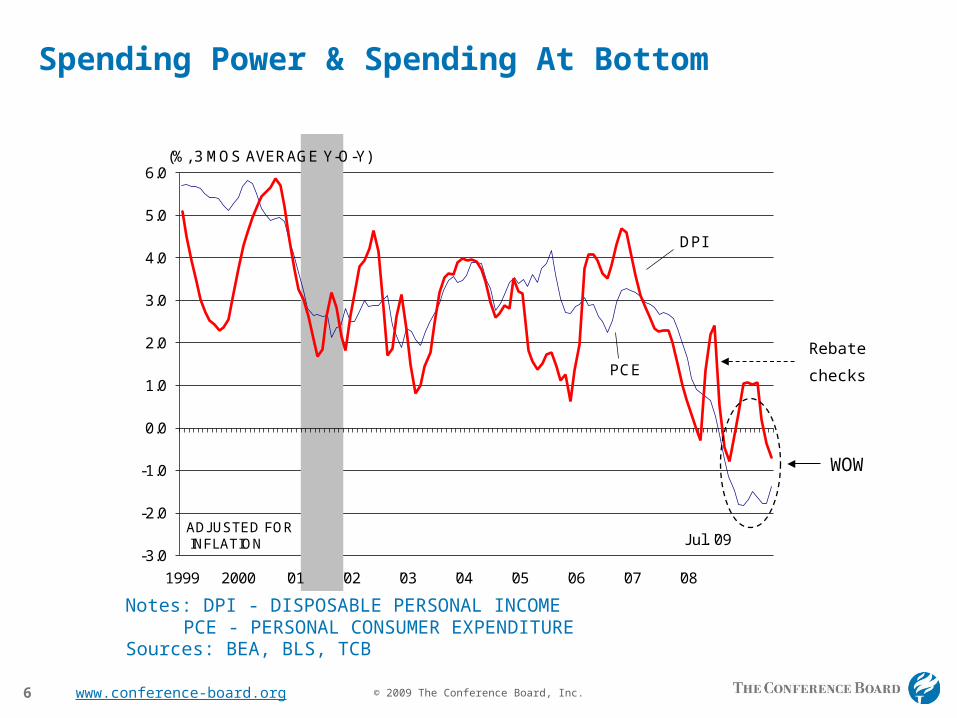

(%, 3 MOS AVERAGE Y-O-Y)

DPI

PCE

ADJUSTED FORINFLATION Jul. '09

Spending Power & Spending At Bottom

Sources: BEA, BLS, TCBPCE - PERSONAL CONSUMER EXPENDITURE

Notes: DPI - DISPOSABLE PERSONAL INCOME

Rebate

checks

WOW

© 2009 The Conference Board, Inc.7 www.conference-board.org

SPENDING POWER WILL CONSISTENTLY RISE FASTER THAN SPENDING

1.1 1.2 0.5 1.8

2.2 2.1 2.1

1.8 2.6 2.8

2.4

2.3 2.1

-2.2

0.6

-1.2

2.1

1.9 1.2

-2.0

1.9

2.7 3.0

1.0

3.7 3.1

-4

-2

0

2

4

6

3Q-09 4Q-09 1Q-10 2Q-10 3Q-10 4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12

Sources:TCB

(% Change, Seasonally Adjusted Annual Rates) FORECAST

DISPOSABLE PERS INCOME

PERS CONSUMPTION EXP.

© 2009 The Conference Board, Inc.8 www.conference-board.org

HIGHER GAS PRICES DRIVE DEMAND FOR FUEL EFFICIENCY

1.1 1.2

0.5

1.8

2.2 2.1 2.1 1.8

2.6 2.8

2.4 2.3 2.1

11.9

10.4 10.0

10.3 11.2

12.0 12.8 13.4 14.0

14.5 15.1 15.3 15.6

0

4

8

12

16

20

0

1

2

3

4

5

3Q-09 4Q-09 1Q-10 2Q-10 3Q-10 4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12

Sources:TCB

(% Change, Seasonally Adjusted Annual Rates) FORECAST

LIGHT VEHICLE SALES ()

PERS CONSUMPTION EXP. ()

(Mil. Units)

© 2009 The Conference Board, Inc.9 www.conference-board.org

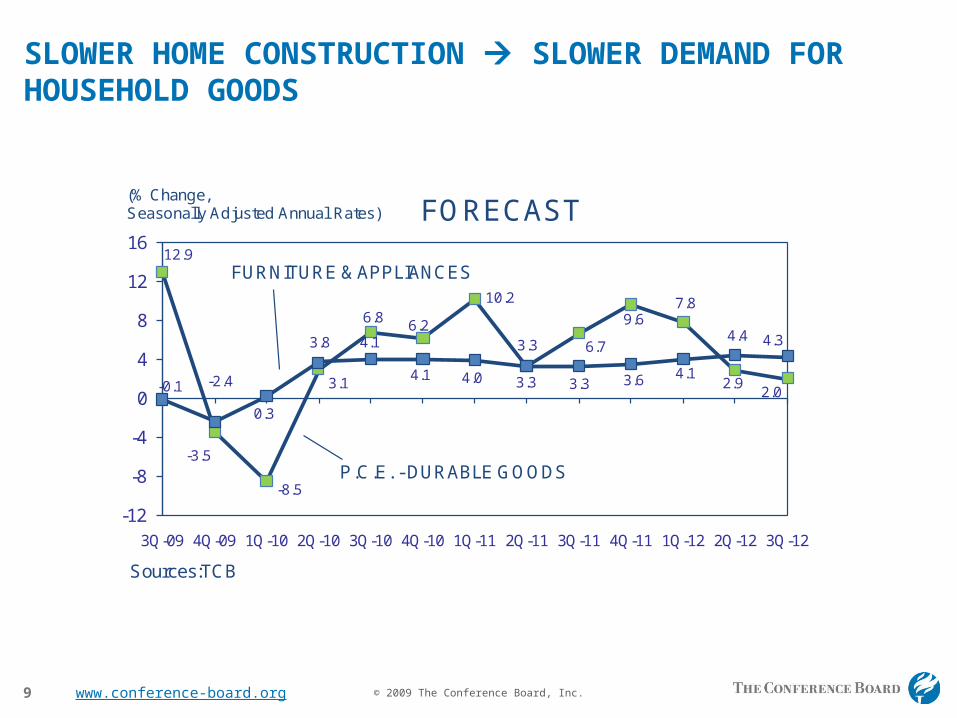

SLOWER HOME CONSTRUCTION SLOWER DEMAND FOR HOUSEHOLD GOODS

12.9

-3.5

-8.5

3.1

6.8 6.2

10.2

3.3 6.7

9.6 7.8

2.9 2.0 -0.1 -2.4

0.3

3.8 4.1

4.1 4.0 3.3 3.3 3.6 4.1

4.4 4.3

-12

-8

-4

0

4

8

12

16

3Q-09 4Q-09 1Q-10 2Q-10 3Q-10 4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12

Sources:TCB

(% Change, Seasonally Adjusted Annual Rates) FORECAST

P.C.E. - DURABLE GOODS

FURNITURE & APPLIANCES

© 2009 The Conference Board, Inc.10 www.conference-board.org

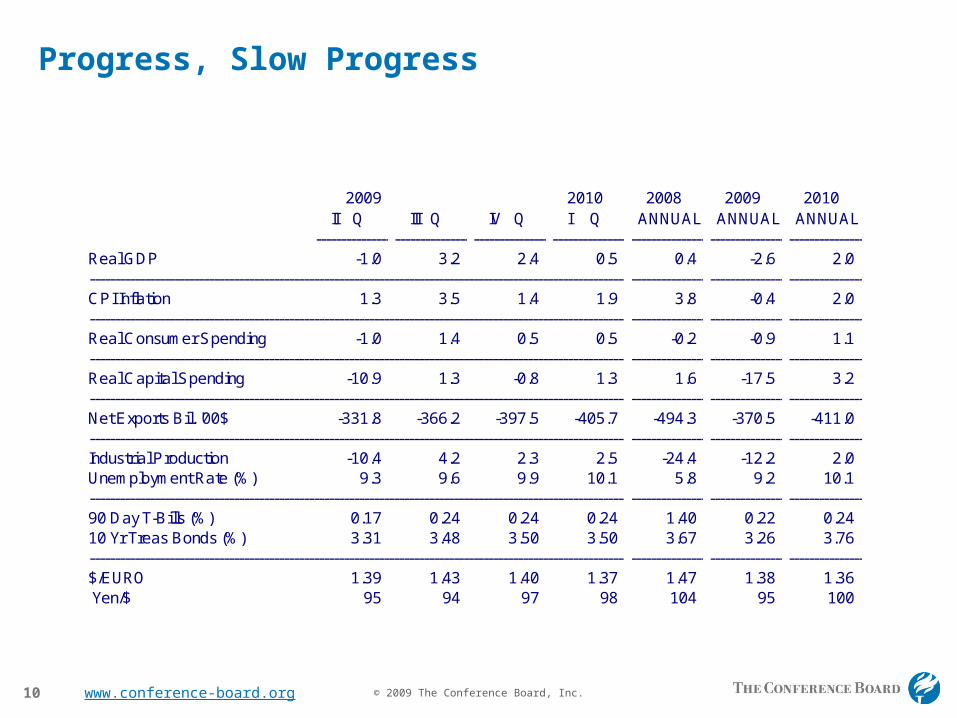

Progress, Slow Progress

2009 2010 2008 2009 2010 II Q III Q IV Q I Q ANNUAL ANNUAL ANNUAL---------------------------------------------------------------------------------------------------------------------------------------------------

Real GDP -1.0 3.2 2.4 0.5 0.4 -2.6 2.0--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------CPI Inflation 1.3 3.5 1.4 1.9 3.8 -0.4 2.0--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------Real Consumer Spending -1.0 1.4 0.5 0.5 -0.2 -0.9 1.1--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------Real Capital Spending -10.9 1.3 -0.8 1.3 1.6 -17.5 3.2--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------Net Exports Bil. '00$ -331.8 -366.2 -397.5 -405.7 -494.3 -370.5 -411.0--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------Industrial Production -10.4 4.2 2.3 2.5 -24.4 -12.2 2.0Unemployment Rate (%) 9.3 9.6 9.9 10.1 5.8 9.2 10.1--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------90 Day T-Bills (%) 0.17 0.24 0.24 0.24 1.40 0.22 0.2410 Yr Treas Bonds (%) 3.31 3.48 3.50 3.50 3.67 3.26 3.76--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------$/EURO 1.39 1.43 1.40 1.37 1.47 1.38 1.36 Yen/$ 95 94 97 98 104 95 100

© 2009 The Conference Board, Inc.11 www.conference-board.org

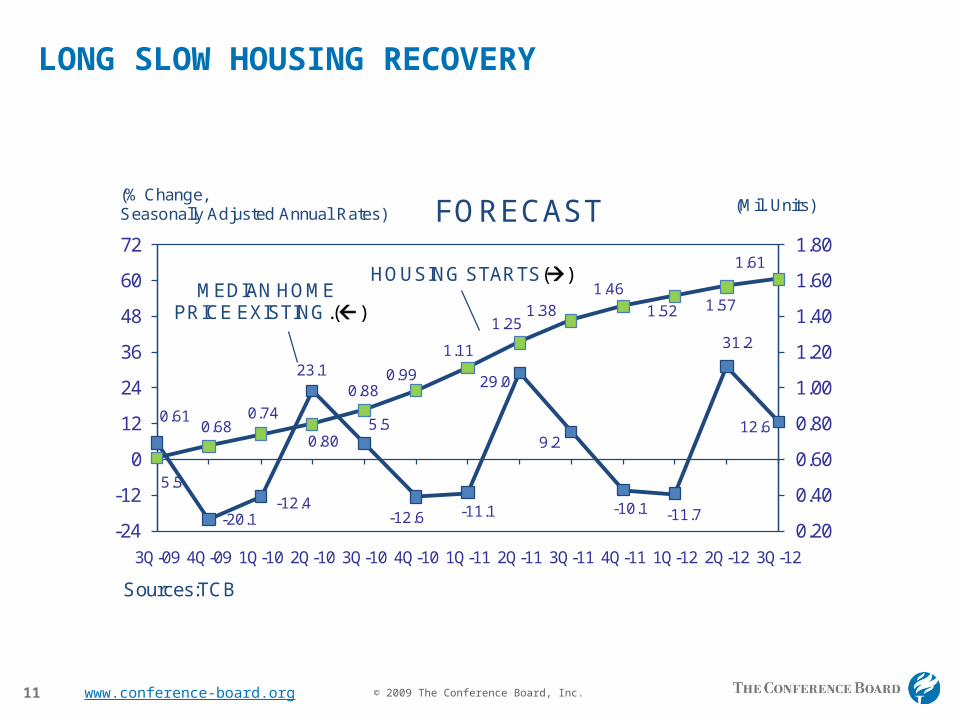

LONG SLOW HOUSING RECOVERY

5.5

-20.1 -12.4

23.1

5.5

-12.6 -11.1

29.0

9.2

-10.1 -11.7

31.2

12.6 0.61

0.68 0.74

0.80

0.88 0.99

1.11

1.25 1.38

1.46

1.52 1.57

1.61

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

-24

-12

0

12

24

36

48

60

72

3Q-09 4Q-09 1Q-10 2Q-10 3Q-10 4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12

Sources:TCB

(% Change, Seasonally Adjusted Annual Rates) FORECAST

MEDIAN HOMEPRICE EXISTING.()

HOUSING STARTS()

(Mil. Units)

© 2009 The Conference Board, Inc.12 www.conference-board.org

MATERIAL COST NOT A PROBLEM POST-RECESSION

-6

-4

-2

0

2

4

6

8

3Q-09 4Q-09 1Q-10 2Q-10 3Q-10 4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12

Sources:TCB

MATERIAL COST NOT A PROBLEM POST-RECESSION

CORE CPI

PPI finished goods

FORECAST(% Change, Seasonally Adjusted Annual Rates)

© 2009 The Conference Board, Inc.13 www.conference-board.org

Source: TCB, Freddie Mac “Conventional Mortgage Home Price Index”

South Atlantic

POST HURRICANE CONTRACTION

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

%(% change y-o-y) (monthly)Employment Trends Index

Rest of U.S.

South Atlantic

-40

-30

-20

-10

0

10

20

30

40

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

Jul-

09

% (% change y-o-y) (monthly)HWI Online

Rest of U.S.

South Atlantic

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

Jul-

09

% (% change y-o-y) (monthly)Consumer Confidence Index

Rest of U.S.

South Atlantic

-10

-5

0

5

10

15

2Q-0

6

3Q-0

6

4Q-0

6

1Q-0

7

2Q-0

7

3Q-0

7

4Q-0

7

1Q-0

8

2Q-0

8

3Q-0

8

4Q-0

8

1Q-0

9

2Q-0

9

% (% change y-o-y) Home Price (quarterly)

Rest of U.S.

South Atlantic

© 2009 The Conference Board, Inc.14 www.conference-board.org

Source: TCB, Freddie Mac “Conventional Mortgage Home Price Index”

Mountain

SOFTENED CONFIDENCE / JOB DECLINE

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

%(% change y-o-y) (monthly)Employment Trends IndexRest of U.S.

Mountain

-50

-40

-30

-20

-10

0

10

20

30

40

50

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

Jul-

09

% (% change y-o-y) (monthly)HWI Online

Rest of U.S.

Mountain

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

May

-06

Jul-

06

Sep

-06

No

v-06

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-07

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-08

Jan

-09

Mar

-09

May

-09

Jul-

09

% (% change y-o-y) (monthly)Consumer Confidence Index

Rest of U.S.

Mountain

-10

-5

0

5

10

15

2Q-0

6

3Q-0

6

4Q-0

6

1Q-0

7

2Q-0

7

3Q-0

7

4Q-0

7

1Q-0

8

2Q-0

8

3Q-0

8

4Q-0

8

1Q-0

9

2Q-0

9

% (% change y-o-y) Home Price (quarterly)

Rest of U.S.

Mountain

© 2009 The Conference Board, Inc.15 www.conference-board.org

Losers and winners in manufacturing and services often the same

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

GoodsCore services excludes health, education and government

Growth in jobs (2008-2015)

PercentD

etro

itLo

s A

ngel

esA

tlant

aB

irmin

gham

Min

neap

olis

Bos

ton

Phi

lade

lphi

aB

altim

ore

Chi

cago

Nas

hvill

eP

hoen

ixK

ansa

s C

ityS

t. Lo

uis

San

Die

goM

iam

iD

enve

rS

eattl

eS

an F

ranc

isco

New

Yor

k C

ityD

alla

sH

oust

on

Sources:

BLS, The Conference Board

© 2009 The Conference Board, Inc.16 www.conference-board.org

Service jobs decline less percentage-wise, but recovery may take longer

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1980-20082008-2015

Average annual change

Employment by industry

Adm

inis

trativ

e

ser

vice

sR

ecre

atio

nP

rofe

ssio

nal

serv

ices

Con

stru

ctio

nA

ccom

mo-

datio

nsO

ther

ser

vice

sM

anag

emen

t se

rvic

esFi

nanc

ial

serv

ices

Min

ing

Ret

ail t

rade

Who

lesa

le tr

ade

Util

ities

Man

ufac

turin

g

Sources:

BLS, The Conference Board

© 2009 The Conference Board, Inc.17 www.conference-board.org

-1

0

1

2

3

4

5

88 90 92 94 96 98 00 02 04 06 08

October1987Crash

JunkBondCrashandFridaythe 13thmini crash

AsianCrisis

Long TermCapital

CorporateAccountingScandals

Burstingof EquityBubble

Credit CrunchFinancial Instability Index

8/3/2009

Bear SternsCollapse

Lehman BrothersCollapse

Wealth destruction phase Cresting?

Note: Shaded areas represent U.S. recessions.

Sources: FRB, The Conference Board

© 2009 The Conference Board, Inc.18 www.conference-board.org

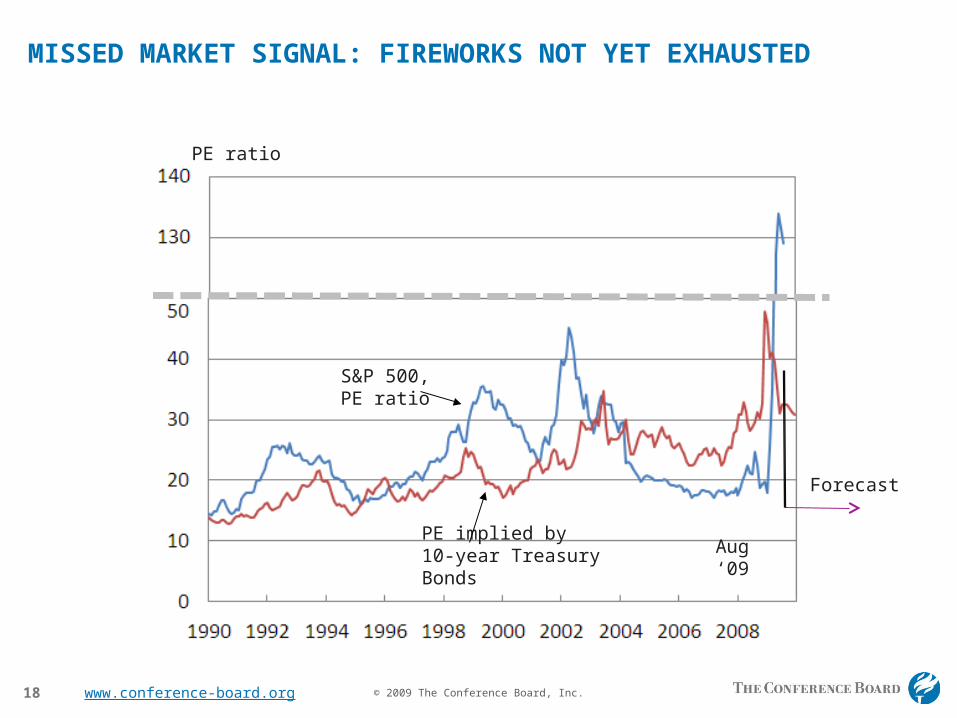

MISSED MARKET SIGNAL: FIREWORKS NOT YET EXHAUSTED

Aug ‘09

Forecast

S&P 500,PE ratio

PE implied by10-year Treasury Bonds

PE ratio

© 2009 The Conference Board, Inc.19 www.conference-board.org

Financing Gap: Danger Signal

-400

-300

-200

-100

0

100

200

300

400

80 85 90 95 00 05

(Bil $)

4Q '08

Note: Proxy for external funding of investmentSource: FRB, The Conference Board

www.conference-board.org

The US Consumer

Lynn Franco

Director, Consumer Research Center

September 2009

© 2009 The Conference Board, Inc.21 www.conference-board.org

Rapid consumer recovery remains an unlikely scenario as demand constraints persist

Supply constraints are improving as inventories, production, trade and employment numbers are coming in better

… but demand side remains constrained as discrepancy between willingness and ability to spend persists

Most channels for rapid recovery of consumer demand are clogged as rise in compensation and income and access to credit remain weak

Holiday season likely to be a challenging one for retailers

© 2009 The Conference Board, Inc.22 www.conference-board.org

Present Situation and Expectations Indexes suggest the worst is behind us

0

20

40

60

80

100

120

140

160

180

200

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Index, 1985 = 100

Present Situation Expectations

Sources: NBER; TNS; The Conference Board

© 2009 The Conference Board, Inc.23 www.conference-board.org

Income expectations remain quite negative

0

5

10

15

20

25

30

35

40

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Percent Expectations for Six Months Hence: Income

Income Increase Income Decrease

Sources: NBER; TNS; The Conference Board

© 2009 The Conference Board, Inc.24 www.conference-board.org

Household net worth has declined dramatically

30

40

50

60

70

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Trillions of U.S. dollars, NSA

Sources: FRB; The Conference Board

Households and non profit organizationsNet worth = assets (tangible plus financial) minus liabilities

Q3 2007$65.3 trillion

Q1 2009$51.1 trillion

© 2009 The Conference Board, Inc.25 www.conference-board.org

Consumers saving more, but for how long?

0%

2%

4%

6%

8%

10%

12%

14%

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Percent

Sources: BEA; The Conference Board

Personal saving as a percentage of disposable personal income - quarterly

© 2009 The Conference Board, Inc.26 www.conference-board.org

The era of rapid home equity extraction has ended

-800

-600

-400

-200

0

200

400

600

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Billions of US dollars

Sources: FRB; The Conference Board

Net equity extraction: Flow of home mortgages minus residential investment

© 2009 The Conference Board, Inc.27 www.conference-board.org

-20

-10

0

10

20

30

40

50

60

70

80

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

*Selected domestic banks in the United States

Sources: FRB; The Conference Board

Net percentage (tightened minus eased)

Percent

"Over the past three months, how have your bank's* credit standards for approving applications changed?"

Credit conditions have eased, but remain tight

Credit Cards

OtherConsumer

Loans

© 2009 The Conference Board, Inc.28 www.conference-board.org

The Conference Board Employment Trends Index™ signals end of massive job cuts

104

108

112

116

120

124

128

132

136

140

72

76

80

84

88

92

96

100

104

108

112

116

120

124

128MillionsIndex, 1996 = 100 Employment Trends Index (ETI) Total Employed

Sources: BLS; The Conference Board

© 2009 The Conference Board, Inc.29 www.conference-board.org

Compensation is expected to grow very slowly

0

4

8

12

16

20

24

28

32

Percent

Sources: NFIB; The Conference Board

Net percent (“increase” minus “decrease”) of firms planning to raise worker compensation

© 2009 The Conference Board, Inc.30 www.conference-board.org

Recovery in consumer spending is slow compared to previous recoveries

-10

-8

-6

-4

-2

0

2

4

6

8

10

Q1 '80

Q3 '80

Q1 '81

Q3 '81

Q1 '82

Q3 '82

Q1 '83

Q3 '83

Q1 '90

Q3 '90

Q1 '91

Q3 '91

Q1 '92

Q3 '92

Q1 '00

Q3 '00

Q1 '01

Q3 '01

Q1 '02

Q3 '02

Q1 '08

Q3 '08

Q1 '09

Q3 '09

Q1 '10

Q3 '10

1980-1983 1990-1992 2000-2002 2008-2010

ForecastReal personal consumption expenditures

Quarter to quarter annual percentage change

© 2009 The Conference Board, Inc.31 www.conference-board.org

No clear leaders in pickup on consumer spending

Volatility of spending will remain with consumers' low ability to spend

Bargain-hunting mode will prevail for remainder of 2009, and especially for holiday season

As economy improves, spending on “affordable” discretionary items will likely lead the way

But large ticket items will remain slow as long as personal balance sheets remain weak – exception “cash for clunkers”

Rise in gas and commodity prices can hold consumers back further