Embed Size (px)

Citation preview

1

THE PERSISTENCE OF FLORIDA’S SMALL ORGANIC FARMS IN THE FACE OF GROWING DEMAND FOR ORGANIC PRODUCTS

By

LINDSAY FERNANDEZ-SALVADOR

A THESIS PRESENTED TO THE GRADUATE SCHOOL OF THE UNIVERSITY OF FLORIDA IN PARTIAL FULFILLMENT

OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE

UNIVERSITY OF FLORIDA

2009

2

© 2009 Lindsay Fernandez-Salvador

3

To my husband and baby boy who kept me motivated

4

ACKNOWLEDGMENTS

I thank my advisor and chair, Dr. Eric Keys. I also thank my committee members, Dr.

Youliang Qui and Brian Childs. Thank you to the Geography Department Faculty and Staff,

who made it so easy for me to get my research done on time. I would also like to acknowledge

the Organic Farming Research Foundation for their generous financial support.

5

TABLE OF CONTENTS page

ACKNOWLEDGMENTS .................................................................................................................... 4

LIST OF TABLES ................................................................................................................................ 8

LIST OF FIGURES .............................................................................................................................. 9

ABSTRACT ........................................................................................................................................ 10

CHAPTER

1 INTRODUCTION....................................................................................................................... 12

The Organic Market and Small Farms ....................................................................................... 12Current Market Trends in Organics ........................................................................................... 14Florida in the Organic Marketplace ........................................................................................... 15Implications of Study .................................................................................................................. 16

2 LITERATURE REVIEW ........................................................................................................... 18

The Agrarian Question ................................................................................................................ 19Thomas Jefferson’s Agrarian Society and Agro-Industrialization ........................................... 20The Beginnings of Agro-Industrialization ................................................................................. 22Evolution of Organics ................................................................................................................. 24Organic Industrialization ............................................................................................................ 27

Concentrated Corporate Ownership ................................................................................... 27Vertically Integrated Distribution Networks ...................................................................... 28Capital- and Technology- Heavy Production Methods ..................................................... 30Implementation of Formula Standards ............................................................................... 31

3 RESEARCH QUESTIONS, METHODS, AND RESULTS .................................................... 33

Research Questions ..................................................................................................................... 33Methodological Framework ....................................................................................................... 34

Risk Analysis and Organic Farm Decision-Making .......................................................... 34Success on the Farm: What Does it Mean? ........................................................................ 35Agriculture Market Chains .................................................................................................. 37

Methods ....................................................................................................................................... 37Collection and Analysis of Organic Market Data, Surveys, and Reports ........................ 37Farmer Interviews ................................................................................................................ 38

Population and sampling design .................................................................................. 38Execution of interviews ............................................................................................... 39

Market Chain Analysis ........................................................................................................ 42Population and sampling design .................................................................................. 42Execution of interviews ............................................................................................... 43

6

Results .......................................................................................................................................... 44Farm Profiles ........................................................................................................................ 44

Aggregate profile .......................................................................................................... 44Small farm profile ........................................................................................................ 46Large farm profile ........................................................................................................ 47

Farm Success Scores ........................................................................................................... 47Direct-Retail and Wholesale Marketing Chains ................................................................ 52Market Factors and Perceptions of Risk ............................................................................ 53Attitudes and Futures in Organic Farming ......................................................................... 53Rapid Market Chain Analysis ............................................................................................. 55

4 DISCUSSION.............................................................................................................................. 57

Characteristics of Successful Farms .......................................................................................... 57Classic Case: Small Farm Success ..................................................................................... 58Classic Case: Large Farm Success ..................................................................................... 60

Characteristics of Struggling Farms ........................................................................................... 62Threats and Securities to Persistence ......................................................................................... 65

Threats to Farm Persistence ................................................................................................ 65Off-farm input cost and availability ............................................................................ 65Regional and international competition ...................................................................... 66Certification standards and requirements ................................................................... 69

Factors Associated With Farm Persistence ........................................................................ 70Increasing consumer demand for organic products ................................................... 70Price premiums for certified organic produce ............................................................ 72

Evidence of Organic Industrialization in Florida ...................................................................... 74Concentrated Corporate Ownership ................................................................................... 74Capital- and Technology-Intensive Production Methods .................................................. 75Vertically Integrated Distribution Networks ...................................................................... 77

Organic Market Chain Analysis: What Does it Mean for Small Farmers? ............................. 78Tracing a Product from Farmgate to Retailer: Chain Strucutre and Price Inflation ........ 78

Buyer/seller preferences .............................................................................................. 81

5 CONCLUSION ........................................................................................................................... 83

Implications for Small Organic Farms ....................................................................................... 84Implications for the Organic Industry ........................................................................................ 86

APPENDIX

A FARMER INTERVIEW QUESTIONS..................................................................................... 88

PART 1: Farm Profile ................................................................................................................. 88PART 2: Market Chain Description ........................................................................................... 89

B MARKET CHAIN ANALYIS INTERVIEW QUESTIONS................................................... 95

Introduction ................................................................................................................................. 95

7

REFERENCES ................................................................................................................................... 97

BIOGRAPHICAL SKETCH ........................................................................................................... 104

8

LIST OF TABLES

Table

page

3-1 Farm profile topics ................................................................................................................. 40

3-2 Farm risks and assessment values ......................................................................................... 41

3-3 Attitudes and future for organic farming topics ................................................................... 42

3-4 Farm profile results for all participating farms .................................................................... 45

3-5 Comparison of farm characteristics for small and large farms ........................................... 46

3-6 Percentage of farmers who used direct-retail and wholesale market outlets ...................... 52

3-7 Results from market chain interviews ................................................................................... 55

4-1 Generalized characteristics of successful and struggling farms .......................................... 64

4-2 Most important threats and securities to farm persistence ................................................... 74

9

LIST OF FIGURES

Figure

page

1-1 Share of organic sales by venue ............................................................................................ 14

3-1 Research sites and administrative areas ................................................................................ 39

3-2 Generalized rapid market sampling design .......................................................................... 43

3-3 Comparing success score and size of farm. .......................................................................... 48

3-4 Comparing success score and time certified organic. .......................................................... 49

3-5 Comparing success score and time farming non-certified organic. ................................... 49

3-6 Success scores for direct-retail marketers and average direct-retail success score ............ 50

3-7 Success scores for wholesale marketers and average wholesale market success score ..... 51

3-8 Average success scores for lifestyle vs. business decision farmers. ................................... 52

4-1 “Very successful” direct-retail market chain ........................................................................ 59

4-2 "Very successful" wholesale market chain ........................................................................... 61

4-3 Countries and states that compete directly with Florida organic growers and their certified acreage. .................................................................................................................... 67

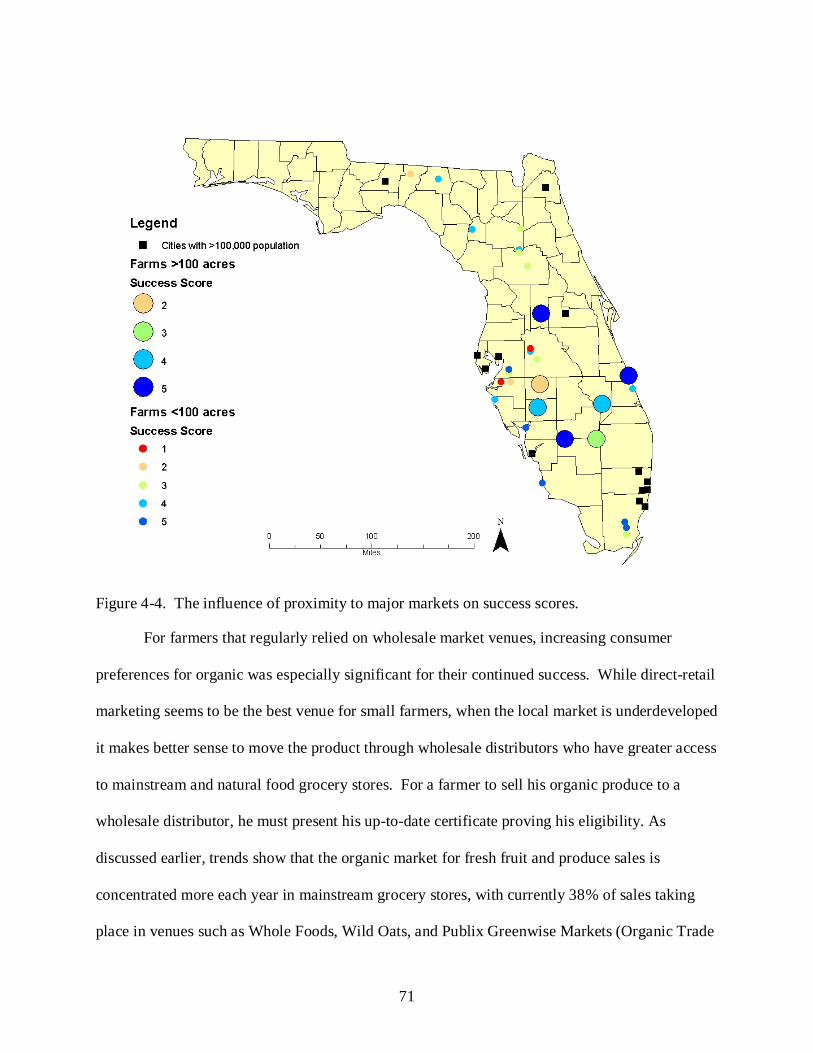

4-4 The influence of proximity to major markets on success scores. ........................................ 71

4-5 Typical wholesale market chain from farm to retailer. ........................................................ 79

4-6 Typical price mark-up as product travels the market chain ................................................. 80

10

Abstract of Thesis Presented to the Graduate School of the University of Florida in Partial Fulfillment of the

Requirements for the Degree of Master of Science

THE PERSISTENCE OF FLORIDA’S SMALL ORGANIC FARMS IN THE FACE OF GROWING DEMAND FOR ORGANIC PRODUCTS

By

Lindsay Fernandez-Salvador

May 2009 Chair: Eric Keys Major: Geography

With the expanding demand for organically grown produce, opportunities for both small-

scale and industrial farms continue to emerge and grow. Consumers of organic products are

found in every market outlet; both conventional and alternatives (natural food stores, farmer’s

markets, subscription boxes). Florida follows only California and Arizona as a top producer of

organic fresh fruits and vegetables, and holds an advantage as the only major producer east of the

Mississippi on the national fresh produce chain. In addition to the locational advantage that

Florida producers possess, they also enjoy a growing season that overlaps with what is largely a

limited fresh produce market in other parts of the country. This situation can create both security

for small farms, but also can provide the conditions in which the organic market becomes

industrialized to meet growing demand. This study uses a multi-method approach including

semi-structured interviews, rapid market chain analysis, and geospatial analysis to explore two

main research objectives: 1) Identify and analyze the most important market conditions that

enable small-scale organic farms in Florida to persist in their current livelihood, 2) Identify and

analyze market conditions in which the organic market may become industrialized. Of those

small farms that were found to be successful, the formation of a social-business contract was the

most important contribution to their success. Farms that adopted industrial methods of

11

production and marketing such as input substitution and vertical market chain integration

struggled the most.

12

CHAPTER 1 INTRODUCTION

The Organic Market and Small Farms

"Our nation's economic foundation is built on the backs of America's small farmers. Their survival and success is not only important to their families, but to consumers, rural communities, the environment, and the global economy." -- Former US Congressman Harold Volkmer

Organic farming has evolved from a grass-roots movement of a few “hippie” farmers in

California to a multi-billion dollar, international food network backed by government

certification standards (Guthman , 2004). Although still considered to be in its youth, the

organic retail market has grown by 16-20% every year since 1990 (Dimitri and Greene , 2002)

and shows no real sign of slowing. Initially, organic farming seemed to be a perfect solution to

the industrial agriculture problem: price premiums that provided income and opportunity to small

family farms, reduction of harsh and dangerous agro-chemicals, and maintenance of the rural

, Chairman, USDA National Commission on Small Farms ( USDA National Commission on Small Farms, 1998)

The development of industrial agriculture over the history of the United States has led to

many different debates, issues, and problems for small farms nationwide. Between Thomas

Jefferson’s agrarian vision of a small-holder agricultural landscape (Griswold, 1946) and today’s

modern agro-industrial food networks, the market space for small farmers has shrunk

significantly. Growing barriers to traditional markets, price indices, technology, and research

leave small farmers even further from the cusp of economic and social survival (Hazell, Poulton

and Wiggins 2007). Industrial agriculture also contributes to the degradation of our water and

soil resources through intensive chemical pest management (FAO, 2002). This combination of

social, economical and environmental threats posed by industrial agriculture led to an

agricultural reinvention, with one solution recognized today as “organic” production (Baker,

2002).

13

economy (Allen and Kovach, 2000; FAO, 2002). However, as the market grows, the same

pattern of large scale economies and agribusiness consolidation that occurred in conventional

agriculture is now occurring in organic agriculture (Goodman, 2000).

While a growing market is mostly a positive trend for small farmers, it is also a threat, as

more organic agriculture is being sold through mainstream outlets and global distribution food

networks (Dimitri and Greene, 2002). To meet the supply that these venues require, farms must

become bigger and adhere to conventionalized packing and safety standards; standards which are

next to impossible for small farmers to economically match (Raynolds, 2004; Weiss, 1999). This

is an urgent matter, as small farms are some of the most important players in rural economies.

Ashley and Maxwell (2001) contend rural populations are in a state of poverty, neglect, and

overall lack appropriate funding to maintain livelihoods. The poverty problem is often the

reason small farms go under; a working farm requires at least one person dedicated full-time

(Hazell, Poulton and Wiggins, 2007). Most farming families cannot forego even one wage-

earning member. While Brookfield (2008) claims that small family farms are not struggling as

much as suggested, and are in fact successfully competing against corporate farms, the question

of how they continue to do so is at the forefront of community development policy.

Pluriactivity-the adoption of diversified on- and off-farm activities-is the most common

mechanism in which otherwise “uneconomic” farms continue to survive (Brookfield, 2008:106).

Although Brookfield (2008:121) argues that the pluriactive farm can “allocate its resources in an

efficient manner, and nothing has diminished this competitive advantage”, he does not address

the flip side of the coin—why does the farming profession not produce a living family wage?

This study addresses the dual problem of small organic farm persistence in an expanding

market, and the industrialization of organic production such that the benefits are sacrificed for

14

continued market expansion. These two problems go hand-in-hand; organic industrialization

creates barriers to small farm success, and the loss of small farms from the agricultural landscape

decreases the barriers of entrance by agribusiness firms.

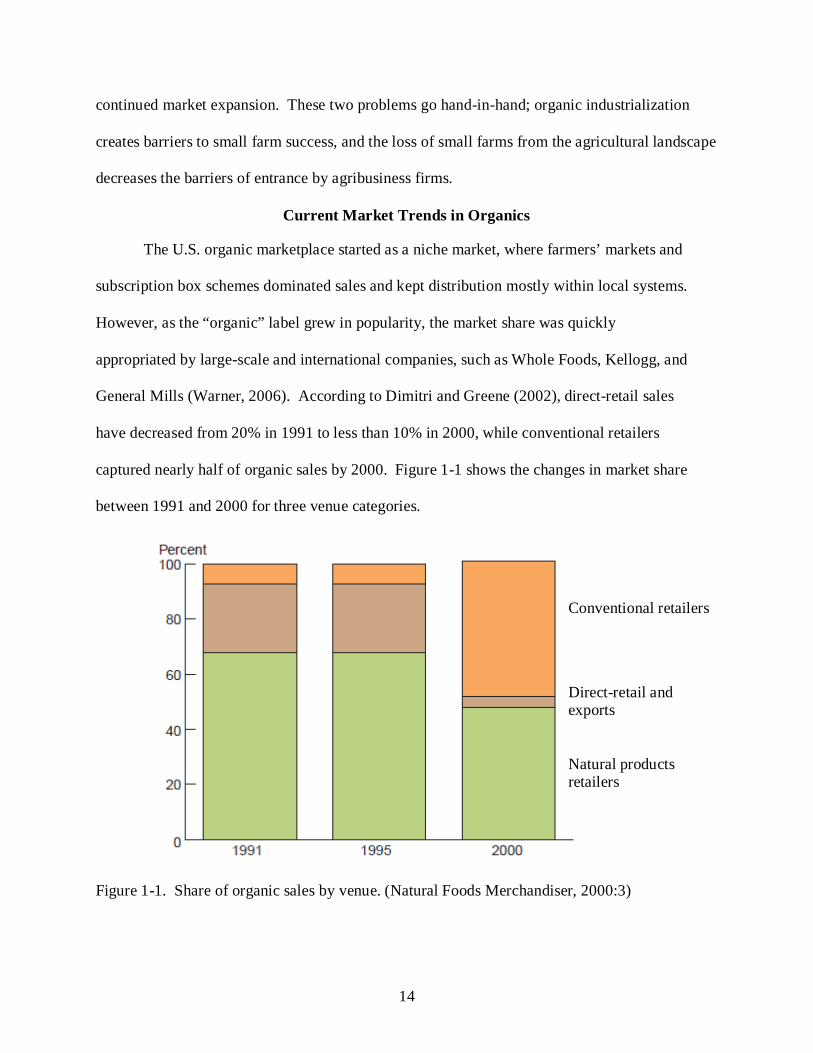

Current Market Trends in Organics

The U.S. organic marketplace started as a niche market, where farmers’ markets and

subscription box schemes dominated sales and kept distribution mostly within local systems.

However, as the “organic” label grew in popularity, the market share was quickly

appropriated by large-scale and international companies, such as Whole Foods, Kellogg, and

General Mills (Warner, 2006). According to Dimitri and Greene (2002), direct-retail sales

have decreased from 20% in 1991 to less than 10% in 2000, while conventional retailers

captured nearly half of organic sales by 2000. Figure 1-1 shows the changes in market share

between 1991 and 2000 for three venue categories.

Figure 1-1. Share of organic sales by venue. (Natural Foods Merchandiser, 2000:3)

Direct-retail and exports

Conventional retailers

Natural products retailers

15

These trends can signify two different possibilities: either more people are

purchasing organic products overall, thus boosting overall sales, or people who originally

bought exclusively at direct-retail outlets now have many more convenient options at which

to purchase their organic foods. Either way, this research finds that small organic farms that

rely heavily on direct-retail marketing are not seeing a significant increase in sales; rather

their sales are decreasing as conventional grocery stores lure current and new customers

away.

Not only are changes in market outlets affecting small organic farms, but increases in

demand and popularity of organic products have led to agribusiness and international

participation in the market. For example, organic production has increased in Mexico from

23,265 hectares in 1996 to 215,843 hectares in 2002. Currently 98% of this production is for

export (Landry Consulting, 2004). Furthermore, according to the USDA, preliminary reports

indicate that the value of imports into the U.S. now far exceeds the value of U.S. organic

exports. Imports accounted for 12-18 percent of the $8.6 billion in U.S. organic retail sales in

2002. Among the major categories of imports are fresh fruits and vegetables, coffee, and

tropical products (Economic Research Service, 2007). Because many small farms focus on

fresh fruit and vegetable production, these emerging trends pose a strong risk to their already

tiny market share.

Florida in the Organic Marketplace

Florida follows only California and Arizona as a top producer of organic fresh fruits

and vegetables (Dimitri and Greene, 2002), and holds an advantage as the only major

producer east of the Mississippi on the national fresh produce chain. In addition to the

locational advantage that Florida producers possess, they also enjoy a growing season that

overlaps with what is largely a limited fresh produce market in other parts of the country.

16

According to Austin and Chase (2002), fresh organic fruit and vegetable production in

Florida constituted over 80% of sales for surveyed organic growers. This unique combination

of factors can foster or inhibit the organic fruits and vegetable producer in Florida, as it either

provides security of livelihood or generates strong pressure to convert to industrial organic

agriculture and thereby forego the very livelihood that the organic market helped create.

Implications of Study

According to the ERS/USDA, a farm is ‘small’ when its sales are under $250,000 per

year. The great majority of farms fall under this category, although many of them are what

the USDA considers ‘lifestyle farms’ (principal operator is retired or has other off-farm

employment) (USDA Economic Research Service, 2005). The United States has a rich

agricultural history to which small farms have contributed significant knowledge, rural

employment, and cultural diversity and symbolism. While more acreage was concentrated

into fewer hands, industrial agriculture upset the balance that small farms offered in terms of

social, economic and ecological benefits. The development of organic production presented

a niche opportunity for small farmers again by utilizing certain marketing and production

methods difficult to recreate on large scales, although efforts exist to fit small economies of

scale production into a large-scale framework. For example, gourmet baby salad mix started

in California among a few chefs that desired fresh local salad mixes. Today, organic salad

mix is one of the top organic products on the national market (Fromartz, 2006). As the

organic market continues to expand at 16-20% annually (Dimitri and Greene, 2002), it is

important to concentrate on from where and who organic produce comes. Because many

small farms saw their livelihoods revitalized by the emergence of organics, their continued

persistence is directly influenced by the changing organic market trends.

17

The results from this study can help both the organic farmer and the community in

which the farm operates. Organic farmers can use this study to determine future management

strategies to plan for changing trends in the local, national, and international organic

marketplace. Community leaders and policy makers will better understand the needs of small

organic producers and become more prepared to implement policies and incentives to booster

organic market share for small organic producers. An informed community of organic

producers, consumers, and leaders will help to guide the market such that both small and

large producers can meet their own needs and the needs of society. The academic community

too can contribute to the advancement of small farm resources and organic agriculture

through further research in these topics.

18

CHAPTER 2 LITERATURE REVIEW

According to Thomas Jefferson, America was slated to be an agrarian society, made up of

many land owners each with a small portion of land on which to farm. In a letter to James

Madison in 1795, Jefferson states, "it is not too soon to provide by every possible means that as

few as possible shall be without a little portion of land. The small landholders are the most

precious part of a state” (Stanton, 1994). Jefferson’s belief in an agrarian society translated to

his political life (Griswold, 1946), and helped to shaped our agricultural ideals as we know it

today. As America’s democracy developed, so did the agrarian society change and adapt to the

rising demand for agricultural products. Although Jefferson promoted a mosaic of “family-sized

farms” (Ezekiel, 1942), the next 300 years of American history oversaw the radical change from

an agrarian society made up primarily of small landowners to a capitalism driven global

commodity chain, of which most of the major players are industrial agribusinesses. In this

historical process, a disconnection between consumer and farmer widened to the point where

most people today are unaware of the energy and resources needed to bring food to the table

(Allen, et al., 2003).

This research takes place at the theoretical nexus of several bodies of literature. It is

important to examine how the agrarian question influenced the agricultural history of the United

States and the modern organic marketplace (Guthman, 2004). Through the evolution of

agribusiness and depletion of small farm resources in conventional agriculture, we can begin to

understand how and why the organic label advanced to what it is today. More recently, much of

the research surrounding organic agriculture deals directly with the hypothesis that organic is

actually approaching the same industrialized system as conventional agriculture (Buck, Getz and

Guthman, 1997; Goodman and Watts, 1997; Leslie and Reimer, 1999). This organic

19

conventionalization--organic commodity chains being appropriated by agribusiness firms (Buck,

Getz and Guthman, 1997:301) is the basis for my argument: as the organic marketplace

continues to grow, it will become increasingly difficult for small organic farms to persist and

may eventually force them to adopt market chains that mimic industrialized agricultural food-

networks.

This study examines the relationship between the expansion of the organic marketplace

and small farm persistence through perceptions of success, risks and subsequent risk-

management strategies. Then it compares the various marketing chains through which organic

fruits and vegetables travel, and the inequalities that arise between small and large-scale

marketing chains.

The Agrarian Question

Based in Marxist-communist debate, the agrarian question is perhaps one of the most

significant influences in modern discussions on the demise of rural economies and small farm

existence in the United States. In the simplest form, it considers the “politics and political

economy of agrarian transitions to capitalism” (Goodman and Watts, 1997). According to

Goodman and Watts (1997), the transition from peasant agrarian practices to capitalist

agrarianism was framed by two processes: the first was the growth and vertical integration of a

global agricultural commodity network and subsequent international competition; the second was

the development of rural democracies that implemented regulatory policies (i.e. tariffs) for the

purpose of protecting the farming sector (Goodman and Watts, 1997). Karl Kautsky (Kautsky,

1899), a prominent scholar on the agrarian question, describes the capitalization of agriculture as

the progression from a laymen’s craft to a science (Lenin, 1964). Kautsky theorized that

dependence on technical agricultural production and industrial wage-labor of small peasants laid

the pathways to agricultural industrialization (Kautsky, 1899).

20

The agrarian debate rose again in recent history through the writings of Wendell Berry:

part poet, part scholar. Berry reinvigorated the romantic image of Thomas Jefferson’s agrarian

society and at the same time brought much-needed attention to the deterioration of America’s

agricultural resources. Much like Kautsky, Berry cites the increased dependence on technology

as part of the problem: “More and bigger machines, more chemical and methodological shortcuts

are needed because of the shortage of man-power on the farm…” (Berry, 2005:17). According

to Berry, the demise of small-scale producers and increasing technological advances go hand-in-

hand. As American agriculture became part of an international industrial complex, it

undermined the “independent, free-standing citizenry that Jefferson thought to be the surest

safeguard of democratic liberty”, and perhaps most importantly, threatened a culture based on

“intensive work, local energies, care and long-lived communities…that is…a dependable, long-

term food supply” (Berry, 2005:19).

The common theme among agrarianists is not necessarily that small farms are somehow

socially superior to large farms, but rather that the political economy of the agrarian tradition

must be taken into account when considering the value that a stable and active farming

community can lend to rural and urban communities. This goal can be achieved through

redirecting the agricultural resources back into the community based, family-oriented operation.

However, to better understand how organic production might help meet this goal, we also need

to examine the history of agriculture in the United States and how various events led to the

organic movement as we know it today.

Thomas Jefferson’s Agrarian Society and Agro-Industrialization

During the Revolutionary War, the subject of land tenure was of great significance to the

fledgling state governments. Policy makers sought to promote a freehold land tenure system

through five principal policies: 1) Eliminate elements of a feudalistic tenure system and refuse to

21

create new proprietary domains, 2) Encourage private business by giving land to private

individuals instead of maintaining state-owned operations, 3) Build communities of small

farmers by selling small units of land to individuals with limited capital, 4) States owning large

landholdings used the revenues from the sale of such holdings to pay off debts that incurred

during the war, and 5) Use land grants to individuals to entice them to enlist and serve in the

military forces during the war (Cochrane, 1993). However, it was not until the Land Ordinance

of 1785 before the freeholder system could come to fruition, and not without internal

governmental conflict. Thomas Jefferson and his followers sought to distribute small parcels of

public land to encourage a nation of small freehold farmers, while the opposing view held by

Alexander Hamilton was that the United States should industrialize and land disposal policies

should foster this goal (Cochrane, 1993). According to Renck (2002), Jefferson’s vision of the

agrarian society supported the production of food for American society, rather than tobacco for

English merchants. This agricultural system would ensure an independent citizenry, and free the

farmer from commercial technologies, slave labor, and specialization (Renck, 2002). Although

each landholder had his own agenda for the newly acquired land, regardless of the process, they

each had the same objective: to improve the land and sell it at a profit to the next wave of land-

hungry buyers. This strategy led the nation further away from Jefferson’s agrarian vision and

instead promoted extensive farmland consolidation into the hands of few (Troughton, 1985).

If Jefferson was so determined to realize his agrarian vision, why did agriculture become

industrialized instead? Several authors (Griswold, 1946; Hofstadter, 1955; Eisinger, 1949)

scrutinized Jefferson’s agrarian vision, calling it rather the ‘agrarian myth’, where the romantic

vision of a yeoman farmer did not reflect farmers’ true motivation. Rather, American farmers

sought profits and found markets for his goods (Appleby, 1982). Appleby (1982) however,

22

argues that the real impetus to the development of commercial agriculture was not Jefferson’s

failed vision, but the reality of Europe’s declining ability to feed herself from her own land.

American farmers tapped into an unusually brisk export market for grains easily grown in the

Midwest and Northeast. Once farmers discovered Europe’s appetite for American grown grains,

the development of towns and cities with corresponding processors, shippers, and miller

industries swiftly followed (Appleby, 1982).

Despite the trend away from Jefferson’s agrarian society, the sentiments towards farming

as a family-based, individualized lifestyle continued to pervade farm newsletters, Congressional

documents, and politician speeches throughout the 1920’s and 1930’s (Renck, 2002). Anderson

(1961) examined the continued attachment to agrarian sentiments and found that three basic

tenets still permeated the agriculture rhetoric: First, the idea that agriculture was still a superior

occupation to others, second that farming was a way of life, not a business, and lastly that

America should remain a community of small yeoman farmers. However, despite the moral

arguments for an agrarian society, economic arguments held sway and resulted in large-scale

enterprises being seen as businesses rather than farms. Thus, the farm as a business required

more industrial interdependency and urbanization, resulting in the beginning of the agricultural

complex we see today (Anderson, 1961).

The Beginnings of Agro-Industrialization

The onset of World War I prompted a steep increase in demand for American food

exports, thus doubling farm prices by 1920 (Floud and McCloskey, 1994). This created a

situation in which land suddenly became scarce, expensive, and subsequent large-scale buyouts

were commonplace so as to take advantage of the lucrative agriculture market. In addition to the

transfer of land to those with enough capital, more sophisticated industries cropped up to meet

the demands of increased agricultural supply and export (Cochrane, 1993). Since agriculture

23

commodities contributed so much to the overall American economy, the United States

Department of Agriculture (USDA) began stepping up efforts to maximize productivity through

research in horticulture, animal husbandry, and plant pathology. During the years 1897-1933,

scientific technology was introduced to the farming economy, with the most efforts concentrated

in mechanization (Binswanger, 1986). From these efforts the diesel powered tractor was born,

greatly improving efficiency and eliminating the need for much manual labor. At the same time,

more commercial fertilizers such as nitrogen and animal manures were used to improve soil

fertility and maximize yields (Cochrane, 1993). The Great Depression was to be the one of the

most important catalysts to agricultural industrialization by producing the need for policy reform

catering to farm enterprises (Earle, 1988).

The start of the Great Depression in 1930 heavily dampened agricultural production, and

sent farm prices spiraling downward (Cochrane, 1993). In reaction, the United States

government instituted a series of policy reforms known as the New Deal. According to Orden,

Paarlberg and Roe (1999) the programs constituted a radical change from a labor intensive to

technology- and capital-driven agricultural industry, thus setting the stage for an even greater

divide between large-scale agriculture and the small farmer (Worster, 1979). Thanks to the New

Deal programs, the agriculture sector grew again. The New Deal era policy reforms did not end

at the close of the crisis; rather, they continued through various farm subsidies that attracted farm

lobbists, corporate interests, and other agriculture-dependent industries (Troughton, 1985).

Coupled with a strong presence in the political arena and access to agrotechnologies, the large-

scale farm prospered more so during the next 50 years than in any other time in history (Ellis and

Biggs, 2001). The shift from “surplus production and financial return” to “lower unit cost of

24

production” in spite of overproduction essentially challenged the ability for small and mid-scale

farms to compete in the market (Troughton, 1985:260).

Today, the issue of agroindustrialization and the decline of small farms continues to be at

the forefront of social, economic and political debates. Despite research dedicated to boost small

farm survival, the reality is that more of our agricultural resources are concentrated in fewer

hands. According to the USDA Commission on Small Farms (1998), while 94% of U.S. farms

are considered small (sales of $250,000 or less), they only capture 41% of farm receipts.

Furthermore, over 80% of total farms in the U.S. reported sales of less than $50,000, making

them some of the poorest small businesses in our economy (Economic Research Service, 2008).

Recently, however, society has come to realize the benefits that small farms have for our health,

rural economies, and social fabric. Many new developments resulted from this concern, among

them the rise of farmers’s markets, community supported agriculture, and direct-retail marketing.

In addition, farmers began to address the environmental issues of industrial agriculture by

participating in sustainable production methods and utilizing less chemical inputs. One branch

of sustainable agriculture resulted in the USDA-regulated, “organic” label. This study examines

how the label has grown in popularity and what it means for small farm persistence.

Evolution of Organics

Modern organic farming evolved worldwide through three stages: emergence, expansion

and growth (Shi-ming and Sauerborn, 2006). Even as mainstream agriculture progressed deeper

into a technology- and chemical- driven industry, the roots for organic agriculture were also

taking shape. As discussed, the early 1900’s saw some of the most rapid advancement in

chemical and synthetic inputs in farming with corresponding increased yields to validate such an

approach. However, proponents of more system-based production emphasized the importance of

a holistic approach, in which each farmer created his own ecological system. This became

25

known as “alternative agriculture” and was considered a parallel to industrial agriculture

(Edwards, 1990). The majority of literature and debate during this time period focused however

on broad-scale natural methods (i.e. composting), and dwelled less on the environmental and

social threats posed by industrial agriculture (Browne, 1855; Howard, 1943; Rodale, 1945;

Steiner, 1958). It was not until the environmental movement started in the 1960’s that society

questioned the impact of industrial agriculture on not only the farm, but in the contamination of

our common waterways, soils, air, and food. This created a political and environmental

awareness in which organic agriculture was in a prime position to enter its second stage:

expansion.

The 1960’s and 1970’s was the setting to a strong backlash against many industries seen

as destructive to the environment. Modern agriculture was one of these industries and much

attention was paid to the detrimental affects pesticides and synthetic fertilizers had on both the

environment and one’s health. Rachel Carson’s book, “Silent Spring” (1962), set an alarm off

about the dangers of uncontrolled pesticide to animal and human populations. Her now proven

thesis on the wide-spread destruction of Dichloro-Diphenyl-Trichloroethane (DDT) (a broad-

spectrum pesticide) is thought to have launched the environmental movement, especially in

association with agricultural practices. Since Carson’s book, various studies have shown links

between many aggressive illnesses and exposures to pesticides (Falck, et al., 1992; Zahm and

Ward, 1998). Thus, armed with scientific evidence supporting the idea that a more natural and

healthy approach to farming was necessary, farmers and consumers across the country began to

embrace the sustainable farm, and showed their support through increased participation in direct-

retail consumption like farmer’s markets and Community-Supported Agriculture (CSA).

Simultaneously, the idea of organic agriculture gained clout among policy makers and farmers

26

nationwide, and standards were set among a handful of certifiers such as California Certified

Organic Farmers and Oregon-Washington Tilth Organic Producers Association in the 1970’s

(Baker, 2002). Beyond the United States, organic agriculture expanded internationally as well,

with the formation of several non-government organizations such as the International Federation

of Organic Agriculture Movements (IFOAM), Federation Nationale d’ Agriculteurs Biologiques

(FNAB) and Forschungsinstitut fuer Biologischen Landbau (FiBL), dedicated to standardizing

and marketing organic products (FAO, 2000). These organizations played an important role in

supporting international recognition of organic agriculture’s scientific and soci-economic

legitimacy. Finally, in 1980, the USDA published a large-scale investigation on organic

agriculture in the United States, in which the definition and guidelines for organic agriculture

were given, and an action plan was called for further development in the organic market (Shi-

ming and Sauerborn, 2006; USDA, 1980).

The emergence and expansion of organic agriculture was important for regaining small

farms in the agricultural landscape. Since organic agriculture started largely through direct-retail

and local marketing chains, the small farmer had immediate access to the market and more

control over price and crop variety (Tovar, Martin and Gomez Cruz, 2005). Local food systems

required “developing connections between consumers and growers, boosting ethical capital and

social capital around food supply chains, educating consumers about the source of their food and

the impacts of different production” (Seyfang, 2006:386), and small organic farms were keen to

make these connections.

Since 1980, the organic movement has grown to what it is now: a multi-billion dollar

market with internationally recognized regulations and standards. You can now walk into most

grocery stores and find products labeled as “USDA Organic”. According to USDA estimates,

27

U.S. certified cropland doubled between 1992 and 1997 to 1.3 million acres. By 2005, every

state in the U.S. had some amount of certified acreage, with a total of 4 million certified acres

(Economic Research Service, 2008). In the most recent comprehensive report released by

IFOAM (2008), it was found that nearly 76 million acres were managed organically in 138

countries in 2006. The rate at which organic agriculture has grown domestically and

internationally has caused growing pains for the market, especially for small farmers that rely on

local and direct retail marketing schemes. This growth has also led to another body of research

pertaining to the social and economic ramifications of organic agriculture and the onset of the so-

called “organic industrialization”, or the appropriation of organic by agribusinesses (Guthman,

2000).

Organic Industrialization

Research surrounding the industrialization of organics focuses on several different

processes in which industrialization is manifested. The most common evidence includes

concentrated forms of corporate ownership and management, capital- and technology-intensive

production methods, vertically integrated distribution networks, and implementation of formula

standards (DeLind, 2000; Tovar, Martin and Gomez Cruz, 2005; Whatmore, 2000). Each of

these facets of the industrialization argument helps to explain the dichotomy between small and

large-scale organic producers, as each group has unique advantages and disadvantages in terms

of organic production and marketing.

Concentrated Corporate Ownership

It is a common misconception that all organic products sold at the grocery store come

from small, local producers. More likely, especially for many of the brands seen in major store

chains (Cascadian Farms, Horizon, and Kashi Organics), it was produced by mega-food

companies like Kellogg, Delta Foods, and General Mills. This trend towards large-scale organic

28

product brands stimulated research in the topology of organic producers in California. Several

studies (Goodman, 2000; Goodman et al, 1987; Guthman, 2000; Klonksy, 2000) focusing on

California’s organic market sector reveal that “many farmers [are] firmly in the grip of industrial

appropriation” (Goodman, 2000:216). For example, Earthbound Farms based in California

started out as a 2.5 acre farm, and is now the largest organic produce operation in North

America, with over 150 contracted growers and 30,000 acres under its control (Whitney, 2007).

Such a production concentration leads to agribusiness “appropriation” of the organic market,

where agribusinesses move farm processes more easily and profitably into the factory (i.e. food

processing), and thus reduce existing organic producers’ profits. Subsequent competition

between small producers and agribusinesses creates economies of scale and reaffirms the axiom

of ‘get big or get out’ (Guthman, 2004). Such large scale production then dicates processing and

distribution networks capable of moving massive amounts of fresh produce from one side of the

world to the other. These spatial and economic inequalities between large and small-scale

commodity chains are another facet of organic industrialization, and the differences between the

two help to further explain the squeeze on small producers.

Vertically Integrated Distribution Networks

According to Leslie and Reimer (1999:402), viewing commodity analyses as a whole

“provide a space for political action by reconnecting producers and consumers”. The spatial

nature of commodity chain analyses is important to understanding the market for small organic

farms, and can lead to regionally specific policies targeted at the special characteristics of such

farms (Leslie and Reimer, 1999). Similarly, Raynolds (2004) explores the organic market using a

commodity chain network analysis. The author suggests that “the rise of mainstream retailers

and food corporations in organic markets is encouraging the growth of large scale corporate

producers that uphold industrial and commercial conventions in meeting mounting product

29

volume and standardized quality expectations” (Raynolds, 2004:737), thus leading small-scale

farms to integrate themselves in the social-based movements to maintain viability. However, it

may be unrealistic to rely solely on social movements to ensure the persistence of small organic

farms.

Eades (2006) finds that organic enterprises have clustered in certain parts of the U.S. due

to favorable conditions such as proximity to metropolitan areas, economies based in farming, and

locations in relation to organic support establishments. These support establishments start on a

small scale such as a single town (Eades, 2006), and eventually morph into a more involved

network of “interconnected companies, specialized suppliers, service providers, firms in related

industries, and associated institutions in a particular field” (Porter, 2000:15). While initially such

an industry cluster is seen to be especially beneficial to small and medium-sized farms, after

certain levels of advancement it creates stiff competition and lowers barriers to market entry and

reduces risk for larger scale farms (Eades, 2006). The rise of organic baby salad mix exemplifies

this process, where the original few growers relied on only one or two packing and shipping

suppliers. As the popularity of these mixes grew, larger growers began out-competing smaller

growers because they bought bulk packaging and streamlined the processing, after which they

were able to offer significantly lower prices (Fromartz, 2006). Because the market was already

well developed for organic mixes, there was little risk to entering the market for larger growers.

Studies conducted in European organic markets (Kjeldsen, 2006, Seyfang, 2006, Renting,

2003) show that social and spatial settings for organic food networks have changed significantly

in the favor of large commodity chain enterprises. According to Kjeldsen (2006), local scale

networks are not economically viable because of uneven spatial distribution of organic

production and consumptions. Furthermore, the local scale is also considered socially unjust due

30

to the lopsided distribution of workloads and economic risks among producers (Kjeldsen, 2006).

As the time-space relationship of organic food chains increase in size and scope, “access to

markets is increasingly conditioned by the capacity to meet specific criteria, concerning the

variety and appearance of products…, and the capacity for flexible delivery” (Renting, 2003,

397). As seen with the rise of conventional mass-production agriculture, meeting the needs of

increasing demand for organic products creates a decidedly uneven development of food chains

that may eventually put a squeeze on the small producer.

Capital- and Technology- Heavy Production Methods

According to Guthman (2004) California agribusiness growers “tend to practice a

shallower form of agroecology” by relying on input substitution, monocropping, and wide-scale

release of predatory insects. These methods replace more traditional or time-consuming methods

such as composting, crop rotation and diversity, and growing ‘trap’ plants (as to attract insects

away from commercial crops). The same was observed in Mexico, where Tovar, Martin and

Gomez Cruz (2005) found that large and small landholders tend to diverge in their farming

practices as well, where technology used on small farms was mostly indigenous knowledge and

inputs were usually generated on-farm. Large producers, on the other hand, were more likely to

use capital-intensive technology and externally manufactured organic inputs. The input-

substitution approach is further supported by the existing economic system, where the products

more likely to be developed, marketed and sold are seen as “commodifiable solutions” (Allen

and Kovach, 2000:224). Commercially produced input products are expensive and often hard to

come by; small producers encounter barriers not only through lack of capital, but also through

inabilities to buy in bulk-a practice appreciated by manufacturers and retailers alike. As noted by

Allen and Kovach (2000), these commodifiable solutions are part and parcel to meeting the

31

needs of international certifying agencies such that ‘certified organic’ becomes a series of

formula standards easily managed and followed by large-scale agribusinesses.

Implementation of Formula Standards

The first official proposal from the USDA on the National Organic Progam (NOP) was

released in December 1997, outlining the rules and regulations to be associated with the USDA

‘certified organic’ label. The rule was met with over 300,000 comments, more than any other

piece of legislation in history and with the majority of comments focusing on the negative

content of the rule (Vos, 2000). Currently national standards rely on a long list of acceptable

organic inputs and technology, and fail to speak to the socially and environmentally sustainable

practices that the organic movement was originally created to address (Allen and Kovach, 2000).

This is essentially what Guthman calls “organic-lite”, or substitution of conventional chemical

inputs for certified organic inputs (Guthman, 2004:301). Similarly, Klonsky (2000) claims that

formula standards will either lead to “organic by neglect” where no active management is used,

or at the other extreme, an over-reliance on commercial substitutes, including non-renewable

resources. Recently it was found that organic input substitution may cause increased levels of

heavy metals in the soil, a side effect considered to be negative and aligned with the essence of

organic agriculture (Tracy and Baker, 2009).

As industrial agribusiness appropriation has continued, some argue that organic

regulations have changed to allow conventional agribusiness firms easy access to the lucrative

organic market (DeLind, 2000). Allen and Kovach (2000) note the economic pressure on

certifying agencies to overlook violations of the rules in order to maintain important clients.

After studying the California certication agencies, Guthman (1998) predicted that universal

standards would “favor those (typically larger) growers wishing to distribute across state lines

and likewise clear the way for agribusiness capital to become more deeply involved in organic

32

foods” (144). California is not the only setting where organic industrialization is occurring;

several studies in Mexico show “dual certification templates” with one certification process

associated with small, peasant landholders and another more suited for large agribusinesses

enterprises (Gonzalez and Nigh, 2005; Tovar, Martin and Gomez Cruz, 2005). Gonzalez and

Nigh (2005) cite the inroads of large agribusinesses into the Mexican organic coffee sector a

direct result of international certification standards, since certifying agencies make no

differentiation between smallholder environmental philosophies and large-scale technical and

economic agendas. Other international players in organic production such as China and Japan

name further regulation and standardization as the main mechanism in which they will be

allowed to enter the market at a more lucrative level (Shi-ming and Sauerborn, 2006). The

combination of increasingly regulated standards and subsequent competition between

agribusinesses and small-scale producers greatly contributes to the organic industrialization

position; whether small farms can maintain market viability despite trends towards

industrialization is an important question to address.

Each facet of the industrialization argument poses a risk to the small farmer: how can a

small farmer enter the international marketing chain with limited ability to meet the production

volume and safety standards required by corporate distribution entities? How will the small

organic farmer increase yield without employing costly input-substitution methods? Finally, how

will a small farmer compete in an international marketplace when regulations make it

increasingly easier for agribusinesses to enter the market? Most organic farms deal with these

risks on a day-to-day basis, and yet continue to persist or even are considered highly successful

(Milestad and Darnhofer, 2003).

33

CHAPTER 3 RESEARCH QUESTIONS, METHODS, AND RESULTS

Research Questions

Small farms are a traditional part of the rural landscape, and organic agriculture is one

method in which they have regained their standing in the agricultural community. However, as

the organic market continues to grow at double-digit rates, it is essential to ask how that same

growth may affect the livelihoods of small organic farmers. As the organic market grows, it has

taken on qualities of conventional agriculture (Guthman, 1998) that often fail to include the

small farmer as viable part of the future of organic agriculture. This study addresses the

difficulties small farmers will face as the organic market expands and attracts larger agribusiness

firms.

Chapter 1 discussed the significant reasons for examining Florida’s small organic farms and

their place in the growing market. Thus, the following research questions guiding this study are:

1. What are the most important market factors contributing to the persistence of Florida’s small organic farms in a growing organic marketplace?

2. What indicators of organic industrialization are present in Florida’s organic marketplace?

Taken together, these questions explore the current dynamics of the Florida organic marketplace,

as well as future trends that may be of importance to the organic grower, both large and small-

scale. Through extensive interviews, market chain analyses, and review of current market

surveys, the factors contributing to the success or persistence of small-scale growers were

identified, along with other classifying characteristics of the most successful farmers. In addition

to this information, the market was analyzed for indicators of organic industrialization, as

discussed in Chapter 2.

34

Methodological Framework

Risk Analysis and Organic Farm Decision-Making

Because the organic market is relatively young and has developed at such a rapid pace,

much of the traditional research pertaining to prices, supply and demand, and risk analysis does

not exist for organic farms, let alone small organic farms. Many conventional agribusinesses

depend on this type of analysis to determine market strategies, crop plans, and other important

decisions. Risk perceptions and analysis is essential for making informed decisions, especially

as markets become uncertain. Much of the research regarding risk analysis pertains to firm

decisions and the expected return of decisions made in an uncertain environment (Weber and

Milliman1997). However, these theoretical frameworks lend themselves well to the agricultural

field because the environment is inherently uncertain because risk sources can be found

internally to the firm and externally as well.

When researching small organic farms, the perception of risk is an important aspect to

concentrate on, as there are very few studies that have even identified true sources of risk to

organic farms. One study compares risk perceptions of conventional vs. organic dairy farms

(Flaten, 2005). Flaten and others (2005) suggest that organic farmers are less risk averse than are

conventional farmers. Perhaps this is a reflection on the idea that organic farming is particularly

more risky due to its relative young market and underdeveloped management strategies. This

research shows that much of what organic farmers do on a day to day basis to manage

uncertainties comes from trial and error rather than deep-ended production research. Thus, to

hope to be successful at organic farming, one must be willing to take risk to achieve results.

While these studies offer insightful information to the complexity of risk and decision

making on organic farms, they lack the perspective of the especially unique small organic farm.

35

Success on the Farm: What Does it Mean?

For the purpose of this study, an index was created to quantify perceived levels of success

at the farm level. On the surface, success seems to be a unitary concept, dealing wth the

financial aspect of the farm. Income, sales, and costs would be the makeup of a ‘success

quotient’ for the farm if finances were the only thing contributing to perceived success.

However, the vast majority of research in farm success and attitudes use not only financial

indicators, but social indicators as well. This study uses a series of indicators, both of the

financial and social aspect to help quantify each farmer’s average success level. Following is an

explanation at how I arrived at these indicators.

The first success indicator is entirely monetary: whether the farm (on average) made a net

income of $20,000.00 each fiscal year. There is no official agreement in the literature as to an

acceptable farm income; rather, there is a set federal poverty line from which a household can

determine its eligibility for various social and economic benefits. The 2008 Federal Poverty

Guidelines states that the poverty line for a household size of three or four is between $17,600

and $21,200. According to the U.S. Census Bureau, average household size is 3.14. Thus, the

financial indicator of $20,000 was selected based on poverty thresholds and average household

size, but also for the ‘roundness’ of the number in terms of ease of recall or quick calculations.

The second and third indicators reflect the farm’s ability to either provide employment

for one half of the household (i.e. one wage-earner) or employment for the entire household (i.e.

two or more wage-earners). These are both economic and socially based; on one hand, a farm’s

ability to provide employment reflects financial stability, on the other it also reflects an increased

quality of life that results from being able to focus completely on the farm rather than having to

rely on outside employment. Flaten and others (2005) notes that quality of life is an important

attitude that mediates farmers’ negative perceptions towards farming. Although Brookfield

36

(2008) argues that pluriactivity (taking off-farm activities in addition to farm work) is actually

one reason why small farms continue to survive, a common goal among many farm operators is

to have the farm provide complete household income (Harper and Eastman, 1980).

The fourth indicator of success is the ability to expand in acreage or invest in

infrastructure (i.e. buy equipment, machinery, develop irrigation). The ability to expand

production by either putting more acreage into crops or by investing in technology is a common

overall goal for most farm operators (Harper and Eastman, 1980). Furthermore, Weiss (1999)

finds that an incremental increase in farm size results in a direct increased chance of survival.

The 2007 report from the International Food Policy Research Institute claims the ability for a

small farm to survive in a global market hangs on access to technology that allows entrance to

the mainstream markets (i.e. food safety equipment) (Hazell, Poulton and Wiggins, 2007).

The fifth and sixth indicators of success deal with abstract concepts that encompass many

hard to quantify attitudes and situations; nonetheless, they are significant to perceptions of

success. They are: ‘farm provides the lifestyle that myself and my family enjoy’, and ‘I am able

to continue farming at the current level’. These take into account economic and social benefits

of the farm while simultaneously encompassing broader reasons for a decline in quality of life or

ability to continue farming (such as illness in the family, life emergencies, etc). Harper and

Eastman (1980) found that quality of life and ability to continue farming are complementary

goals, as a decline in one indicator results in a decline in the other. These indicators are just as

significant as direct financial ones because organic farmers are rarely completely motivated by

profit (Willock, 1999); thus with their inclusion a more complete picture as to what success

means can be derived.

37

Agriculture Market Chains

The study of market chains in agro-food networks is widespread and ranges from the

local to global scales. One of the more prominent schools of thought places the vertical

marketing system as the unit of analysis, in which the various players coordinate through

cooperation to obtain a common goal of improved efficiency (Dimitri and Greene, 2002). A

market chain consists of players, usually starting at the manufacturer and ending in the

consumer, with any number of intermediaries in between (i.e. packers, distributors, retailers)

(Ferris et.al, 2006). Following Goodman and Redcliffe’s (1990) critique of agriculture market

chains, the farmer, although an integral part of the chain, becomes sidelined in the production

process and is replaced by external capital. In this way, the system becomes part of an agro-

industrial complex. The present study takes into account the different players in the organic

market chain in Florida and analyses how small farms fit into that chain. The purpose of the

analysis is to map out from who the players acquire organic produce and to who and where they

resell the product. It is also to determine a broad understanding of the added value a product

obtains as it is sold down the chain.

Methods

This study was executed in three phases: Collection and Analysis of Organic Market

Data, Farmer Interviews, and Market-Chain Analysis. Although each phase was conducted

consecutively, the data derived from each preceeding section addresses the research questions.

Collection and Analysis of Organic Market Data, Surveys, and Reports

Because the organic market is growing at a 16-20% annual rate, there are numerous

sources of reliable industry data and reports from which to derive an overall idea of the organic

market for all types of growers. First and foremost, the USDA’s Economic Research Service

38

makes comprehensive organic production datasets available on its website. They can be

compared to conventional wholesale and farmgate prices for the same product in major markets

(i.e. Boston, New York, San Francisco) (Economic Research Service, 2008). The Organic Trade

Association (OTA) was also a reliable and comprehensive source for current market research and

organic industry reports (Organic Trade Association, 2008). This information was used to relate

the most important success factors identified in the farmer interviews to the current organic

industry in Florida.

Farmer Interviews

Population and sampling design

There are 75 certified organic fruit and vegetable growers currently farming in Florida.

Two main reasons for population inclusion in the study were: participation in the organic market

and non-niche crop production. These reasons satisfy the research questions by ensuring

participants offer experience in the organic market and interactions between consumers, growers,

and other market players. Most farmers grew exclusively fruits and vegetables, however there

was a portion of growers that in addition to their fruit and vegetable production, had expanded

into other commodities or value-added products, such as livestock, eggs, and processed foods.

These were included in the survey as to exemplify different market opportunities pursued by

organic growers beyond traditional row crops. However, no questions were asked pertaining to

any production or marketing outside of vegetables and fruits.

After sorting farmers based on market participation and crop production, 32 growers

were interviewed. The population was sent an initial letter outlining the study specifications and

objectives, and an interview was requested. Because most growers are evenly distributed

throughout Florida, I divided the state into four regions: South Florida, South-Central Florida,

North-Central Florida, and North Florida and Panhandle. The state was divided into these

39

regions for administrative purposes but also for similar agriculture climates. Figure 3-1 displays

the research sites and the administrative regions.

Figure 3-1. Research sites and administrative areas

Execution of interviews

Most interviews took place in-person either on the farm or in the farmer’s business office.

The interview was semi-structured, with questions broken into four sections: Farm Profile,

Market Chain Description, Market Risks/Factors, and Attitudes about Organic Farming.

Questions in the Farm Profile were close-ended, while the questions in the remaining sections

were mostly open-ended. See appendix for full questionnairre. Characteristics from the Farm

Profile are displayed in Table 3-1.

40

Table 3-1. Farm profile topics Topic # Certified acres # Acres leased vs. owned Increase or decreasing acreage Crops grown Main crops Time certified organic Time farming Type of business structure Sales venues Perceptions of success

The ‘success index’, as discussed, was comprised of economic and social indicators. The

farmers were asked to rate from one to five their perceived level of success with each indicator,

after which they were asked to rate their overall success, based on the indicators and other

factors not included in the success index. The rating system was as follows: 1-very unsuccessful,

2-somewhat unsuccessful, 3-neither successful nor unsuccessful, 4-somewhat successful, and 5-

very successful. These indicator ratings were averaged to produce an overall success score for

each farmer; this score acts as the dependent variable on which other data was analyzed.

The Market Chain Description was open-ended and brief. The farmers were asked to

describe their typical market chain as far as they had knowledge. Most farmers did not know

exactly where their product went after sold to wholesale distributors, and so some market chains

were not analyzed. However, this section of the interview broke down into greater detail each

farmer’s overall marketing structure, by percentage of sales to various market outlets, number of

accounts (if applicable), and spatial distribution patterns. It also clarified the major distirbution

companies doing business in Florida.

41

The Market Risks/Factors section was open-ended. It consisted of a list of questions

designed to draw out issues related to each market risk or factor. Market factors are those that

develop outside of the farm organization, and thus cannot be directly controlled by the farmer.

The risks used in the interview were modeled after the study conducted by Flaten and others

(2005), although some modifications were made. For example, Flaten and others (2005)

included 33 risks to dairy farm operations; however, some of these risks are considered to be

internal to the farm system (i.e. illness in the family, disease and pest problems, crop yield

variability) or only applicable to animal production. These risks were not used in the interview.

The remaining risks were determined to be external to the farm system, and highly susceptible to

changes in the organic market. This study differs from Flaten and others (2005) in that it is far

more qualitative and relies more on open-ended interview data. For this reason, I combined

many of the risks in Flaten and others (2005) to make a succinct list of twelve market risks.

Table 3-2 shows these risks and how they were assessed.

Table 3-2. Farm risks and assessment values Risk Assessment valuessessment Values Changes in market share Decrease/increase Competition Low/high Access to the market Poor/excellent Labor availability and costs Poor/excellent Land prices and development Ability to expand Input availability and price Decrease/increase Organic price premiums Decrease/increase Consumer preferences for organic Government programs for organic farms Certification standards

Decrease/increase Helpful/unhelpful Helpful/unhelpful

The farmers were asked to discuss any constraints or opportunities each market risk

offered. After discussing each market risk, they were asked to identify the top two most

significant threats to their success, and the top one or two factors that ensured their success.

42

After identifying the most significant threats, the farmers were asked to describe their

management strategies in response to these threats.

Questions in the Attitudes about Organic Farming section were a mixture of open and

close-ended questions. They were designed to determine the reasons why a farmer chose to be

certified organic, and their future in organic farming. Table 3-3 show the topics discussed.

Table 3-3. Attitudes and future for organic farming topics Topic Reasons for certification Importance of staying certified Farm plan in case of difficulty Plan for certification in one, five, ten years Possible reason for decertification

Market Chain Analysis

Population and sampling design

The organic market players in Florida consist for the most part of harvesters, packers,

processors, marketers, distributors, retailers, and end-customers. Each point in the chain is made

of market players, who must be certified by a USDA accredited certifying agency to buy,

process, or resell organic produce (Ferris, et al., 2006; Quality Certification Services, 2008). I

determined the population through the local certification agency, business records and internet

searches. Taken together, these three sources yielded approximately 50 market players.

The sampling design for this portion of the study was modeled after Ferris and other’s.

(2006) “Rapid Market Analysis” methodology. The objectives of this methodology are: To gain

a view of how a commodity sub-sector is arranged, operated and performed, identify sub-sector

constraints and opportunities, and identify specific market chains that are most suitable for a

producer group. The data was gathered through semi-structured informal interviews with a

minimum of 3-5 actors at each stage of the market chain. At least one market chain analysis was

43

performed for a market traditionally dominated by large-scale producers, and another was

performed on a market traditionally available to small-scale producers. A total of 20 players

were interviewed. A copy of the interview guide can be found in the appendix. Figure 3-2 shows

a generalized market chain sampling design.

Figure 3-2. Generalized rapid market sampling design. A) Raw farm product. B) Market chain through which product travels. C) Final packaged and labeled product.

Execution of interviews

The interview consisted of six open-ended questions. The first asked the respondent to

identify how they fit into the organic market chain. The response was usually within the various

players identified above. The second question asked the respondent to identify from whom they

bought or aquired organic produce. Probes included information pertaining to the size, scope

and type of producer. The third question asked the respondent to identify to whom they are

selling the aquired product (if applicable), with probes to further identify if it was wholesalers,

brokers, processors, or end-customers, and the size and scope of the next buyers. The fourth and

fifth questions asked the respondent to identify reasons, characteristics, or preferences for doing

A

B

C

44

business with certain types and sizes of producers or businesses. These two questions help to

categorize the more likely producers to be included in each market chain and why. The final

question asked the respondent to identify the typical price mark-up from aquiring the product to

reselling it to the next player. Most respondents denied answering this question, claiming

confidentiality reasons.

Results

Farm Profiles

Aggregate profile