Embed Size (px)

Citation preview

Winning the retail war

Retail point of view

Introduction Page 3

Innovatefaster Page 7

Getgeeky Page 9

Personalizecontent Page 10

Donotcopy Page 10

Sellwhattheycan’tsell Page 11

Upcloseandpersonal Page 12

OpenFlagshipsandC-Stores Page 13

Propositionordie Page 14

Marketplacerules,OK Page 16

Samegame,differentrules Page 18

Showing results for “how to compete with the internet pure plays”

Showing 1 - 11 of 11 results

Introduction 3

Innovate faster 6

Get geeky 8

Personalize content 9

Do not copy 11

Sell what they can’t sell 13

Up close and personal 14

Open Flagships and C-Stores 14

Proposition or die 16

Marketplace rules, OK 17

Same game, different rules 17

Key to star ratings

Most relevant

Least relevant

Amazon, Google, eBay and other big online pure plays have changed the rules of the retail game, challenging the rest of the industry to replicate their radical new approach to technology, innovation and execution—or perish. Getting ahead of the game, however, will require much more: Nothing short of a unique value proposition with truly exceptional customer service at its core.

Winning the retail war: How to compete with the internet pure plays

252 of 252 people found the following point of view helpful

Winning the retail war 3

If you’re not already worried about Amazon and its online imitators, you should be. For cash-strapped consumers in a largely price-transparent marketplace the pure plays are increasingly vendors of choice—and small wonder. They offer significantly easier access to a wider range of products for less money and more convenience.

Having shown that size does, in fact, matter the global footprint of these online behemoths continues to expand.

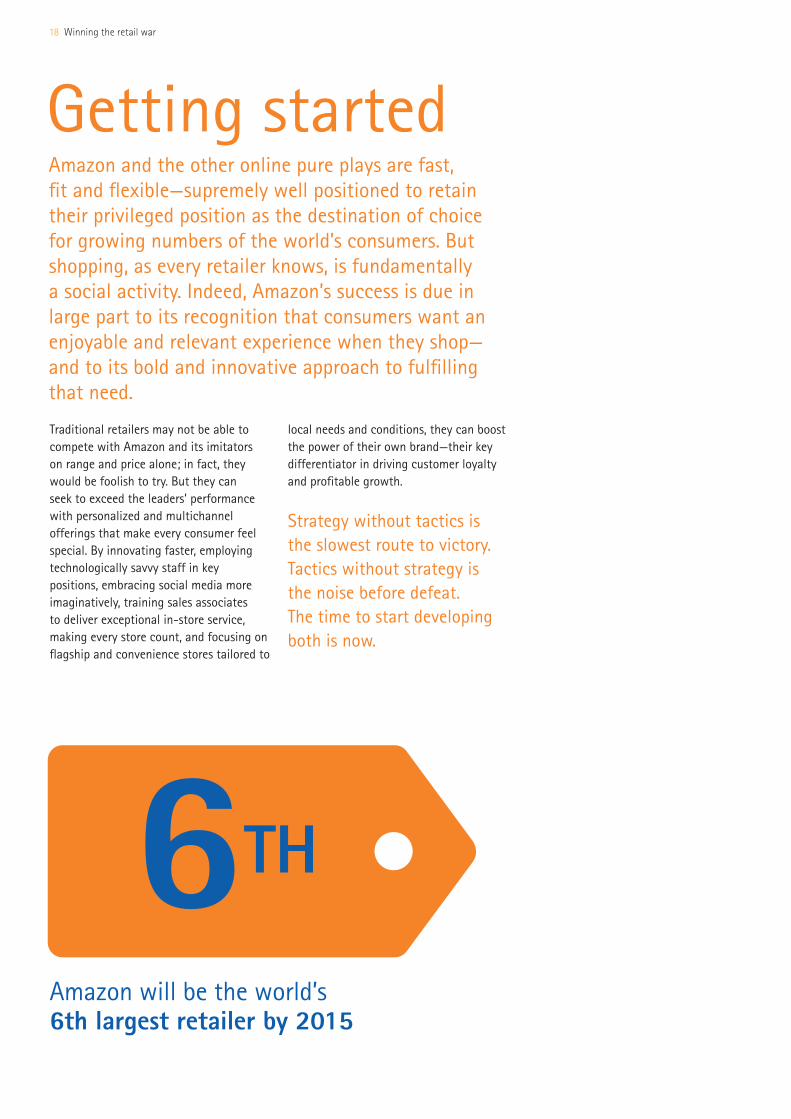

Amazon, for example, is not only theworld’s leading online retailer, but nowalso boasts 10 percent of the North American media market1. If the company maintains its current growth trajectory Amazon will be the world’s 6th largest retailer by 2015, with revenues of more thanUS$100billion2. eBay, for its part, is growing strongly in emerging markets and trialing (through its PayPal division) innovative payment methods, especially in m-commerce. And Google has generated a CAGR of 22 percent over the past 5 years3.

European Cross-border E-commerce: The Challenge of Achieving Profitable Growth

February 2012

Readers may also be interested in

Retail @ the Edge: New Opportunities for Customers and Retailers

June 2012

Making Mobile POS Happen: Five Ways Stores Can Better Compete and Grow May 2012

What we can learn from ‘The Art of War’

Back in the 6th century BC, the Chinese military strategist Sun Tzu developed a set of core concepts and principles that remain highly relevant for retailers struggling to compete against online pure plays.

Five principles from ‘The Art of War’

AgilityBe ready to react to opportunities at speed.

Understand your relative strengths and weaknessAssess the opportunities and threats that are specific to your company, your sector and your customers, and flex over time as the market evolves.

PreparationAlways consider and quantify the unknown.

Disciplined organizationAdopt an organization structure that best utilizes all your resources and capital to focus on the customer experience.

First in the field has an advantageBut the market is continually changing. Always consider where you can innovate and differentiate yourself.

1

2

3

4

5

4 Winning the retail war

Meanwhile, a stream of new ventures demonstrate that the barriers to entry in online retailing are low. Witness, for example, lazada.com, the latest offering from Germany’s digital entrepreneurs, the Samwer brothers, which offers such potentially huge markets as Indonesia, Malaysia and the Philippines a service which copies Amazon’s. Or consider 360buy.com, now the largest B2C online retailer in China.

So should traditional retailers turn bricks into clicks and become online pure plays too? Smart retailers know better. They know that the purely online business model has some significant weaknesses—not least, the fact that it cannot reach the many millions of consumers, especially in emerging markets, who are unbanked. Add to that the looming threat of tighter online sales taxes in the US and other developed markets, and a revolutionary retail proposition starts to look a lot less invincible.

10%

Amazon, for example, is not only the world’s leading online retailer, but now also boasts 10 percent of the North American media market

Winning the retail war 5

The fact is that traditional retailers can compete with and even beat the online pure plays. And that’s essentially because they offer the brands that shoppers want; and, via their stores, the social contact that still defines shopping.

Today’s customers don’t just want to shop online. They also expect to be able to shop in-store, with mobile devices or through call centers—whichever channel offers them the convenience of access and value that they seek at the time. Their key demand is for a seamless experience across channels. If traditional retailers can deepen and sustain their innate strengths, and learn to match the online pure plays

for innovation, technology and execution, they will have developed the cross-channel power to drive success.

That will require a seismic shift in strategic thinking for most companies— as well as the application of some core (and timeless) strategic principles (see The Art of War sidebar).

It will also require a new mindset— a different way of thinking about customers, competitors and the business itself. Our experience suggests that there are ten steps to success—and that three of them are critical changes that all players must make, just to stay in the game.

A consistent customer experience

Most recent quotes

I knew that free delivery is where the world is going to be in 3 years’ time, but I just wanted to get there right away.

by Nick Robertson, CEO ASOS

Delivery

The online pure plays don’t just innovate—they do so at speed. Amazon, Apple, Facebook and Google are the top four most innovative companies worldwide4 and all are playing in the retail space. Amazon CEO Jeff Bezos encourages employees to “place bets” on good ideas, even if they fail, and to mix those big bets with incremental innovations. In fact, according to Bezos, “Ninety-plus percent of the innovation at Amazon is incremental…and much less risky.”

Since everything that Amazon does starts and ends with the customer and the customer experience, Bezos also ensures that all innovation initiatives focus on meeting a customer need, either recognized or anticipated.

Amazon has built an outstandingly robust culture of innovation. But what makes the company really interesting is its willingness to innovate in multiple dimensions simultaneously—not only new product-and-service innovations (consider the Kindle e-reader, for example), but also innovations in operating model and revenue generation. Small, agile “two pizza” project teams—named for their ability to survive on just two pizzas (not more)—help sustain Amazon’s legendary level of innovation; as does the fact that in 2011 a global workforce of just 56,000 managed to generate US$48 billion in sales.

In the current retail environment of rapid technological and cultural change, retailers who thrive will be those who are able to experiment their way to success—innovating, testing, discarding the failures, building on the successes, and implementing them at speed and scale.

1. Innovate fasterMost recent quotes

Yes, you should wake up every morning terrified with your sheets drenched in sweat, but not because you’re afraid of our competitors. Be afraid of our customers, because those are the folks who have the money. Our competitors are never going to send us money.

October 2007 by Jeff Bezos, CEO Amazon

Terrified

6 Winning the retail war

Staying in the game

The online pure plays don’t just innovate—they do so at speed. Amazon, Apple, Facebook and Google are the top four most innovative companies worldwide and all are playing in the retail space.

1 Amazon 2 Apple 3 Facebook 4 Google

How do the pure plays innovate faster than the rest?

Amazon’s two-pizza team rule“If a project team can eat more than two pizzas, it’s too large”

Two Pizzas

One character represents 1,000 employees in the visual shown above

56,000

In 2011 a global workforce of 56,000 generated $48bn in sales

$48billion

Winning the retail war 7

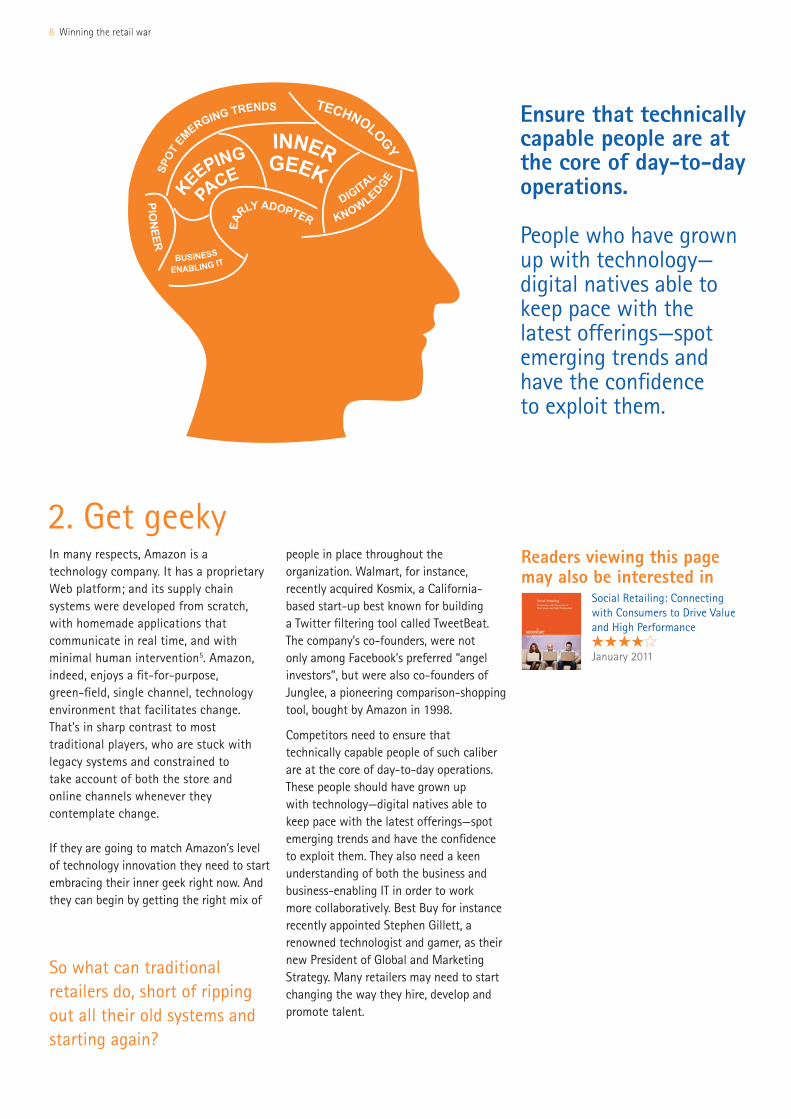

In many respects, Amazon is a technology company. It has a proprietary Web platform; and its supply chain systems were developed from scratch, with homemade applications that communicate in real time, and with minimal human intervention5. Amazon, indeed, enjoys a fit-for-purpose, green-field, single channel, technology environment that facilitates change. That’s in sharp contrast to most traditional players, who are stuck with legacy systems and constrained to take account of both the store and online channels whenever they contemplate change.

If they are going to match Amazon’s level of technology innovation they need to start embracing their inner geek right now. And they can begin by getting the right mix of

So what can traditional retailers do, short of ripping out all their old systems and starting again?

people in place throughout the organization. Walmart, for instance, recently acquired Kosmix, a California-based start-up best known for building a Twitter filtering tool called TweetBeat. The company’s co-founders, were not only among Facebook’s preferred “angel investors”, but were also co-founders of Junglee, a pioneering comparison-shopping tool, bought by Amazon in 1998.

Competitors need to ensure that technically capable people of such caliber are at the core of day-to-day operations. These people should have grown up with technology—digital natives able to keep pace with the latest offerings—spot emerging trends and have the confidence to exploit them. They also need a keen understanding of both the business and business-enabling IT in order to work more collaboratively. Best Buy for instance recently appointed Stephen Gillett, a renowned technologist and gamer, as their new President of Global and Marketing Strategy. Many retailers may need to start changing the way they hire, develop and promote talent.

Readers viewing this page may also be interested in

Social Retailing: Connecting with Consumers to Drive Value and High Performance

January 2011

Ensure that technically capable people are at the core of day-to-day operations. People who have grown up with technology—digital natives able to keep pace with the latest offerings—spot emerging trends and have the confidence to exploit them.

8 Winning the retail war

2. Get geeky

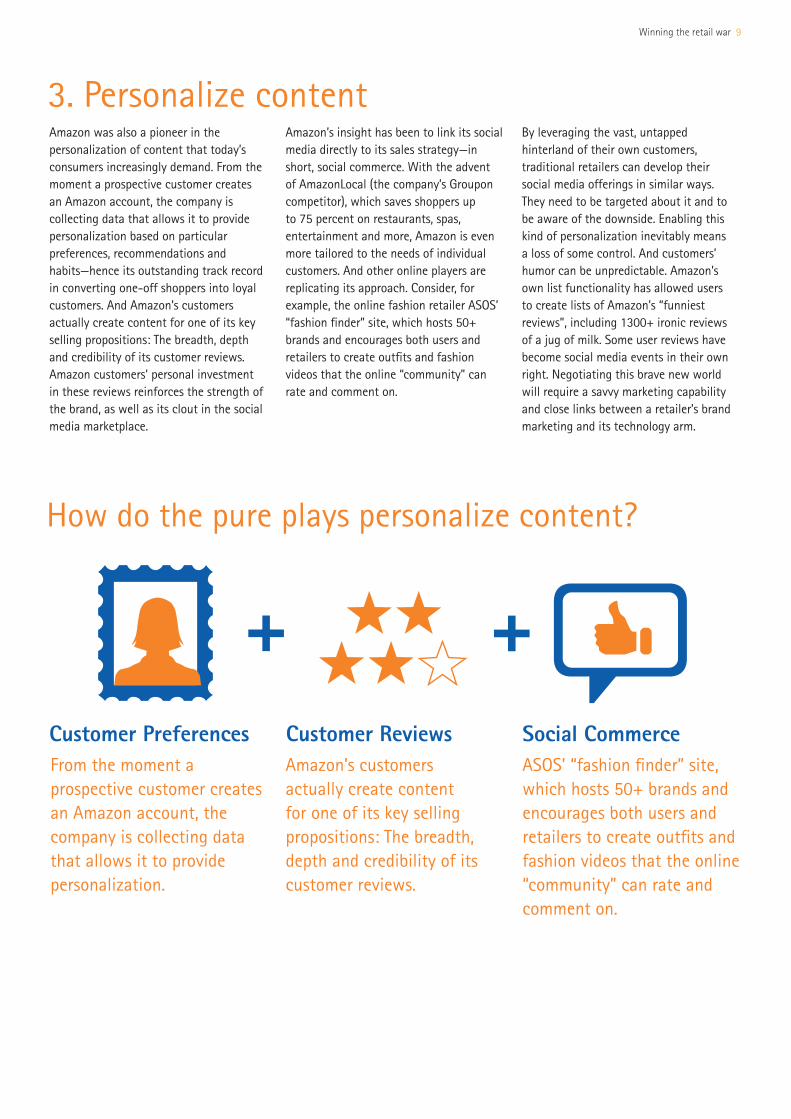

Amazon was also a pioneer in the personalization of content that today’s consumers increasingly demand. From the moment a prospective customer creates an Amazon account, the company is collecting data that allows it to provide personalization based on particular preferences, recommendations and habits—hence its outstanding track record in converting one-off shoppers into loyal customers. And Amazon’s customers actually create content for one of its key selling propositions: The breadth, depth and credibility of its customer reviews. Amazon customers’ personal investment in these reviews reinforces the strength of the brand, as well as its clout in the social media marketplace.

Amazon’s insight has been to link its social media directly to its sales strategy—in short, social commerce. With the advent of AmazonLocal (the company’s Groupon competitor), which saves shoppers up to 75 percent on restaurants, spas, entertainment and more, Amazon is even more tailored to the needs of individual customers. And other online players are replicating its approach. Consider, for example, the online fashion retailer ASOS’ “fashion finder” site, which hosts 50+ brands and encourages both users and retailers to create outfits and fashion videos that the online “community” can rate and comment on.

By leveraging the vast, untapped hinterland of their own customers, traditional retailers can develop their social media offerings in similar ways. They need to be targeted about it and to be aware of the downside. Enabling this kind of personalization inevitably means a loss of some control. And customers’ humor can be unpredictable. Amazon’s own list functionality has allowed users to create lists of Amazon’s “funniest reviews”, including 1300+ ironic reviews of a jug of milk. Some user reviews have become social media events in their own right. Negotiating this brave new world will require a savvy marketing capability and close links between a retailer’s brand marketing and its technology arm.

How do the pure plays personalize content?

From the moment a prospective customer creates an Amazon account, the company is collecting data that allows it to provide personalization.

Amazon’s customers actually create content for one of its key selling propositions: The breadth, depth and credibility of its customer reviews.

ASOS’ “fashion finder” site, which hosts 50+ brands and encourages both users and retailers to create outfits and fashion videos that the online “community” can rate and comment on.

Customer Preferences Customer Reviews Social Commerce

Winning the retail war 9

3. Personalize content

Add to your wish list

69bnValue in dollars of retail stock turnover for eBay

of the innovation at Amazon is incremental…and much less risky.

OVER 90%

10 Winning the retail war

99%Percent of Net-a-Porter deliveries that are dispatched within 24 hours of the order being received

Readers viewing this page may also be interested in

Retail Pricing is about to get Personal

December 2011

The Connected Store: Delivering a > Shopping Experience

February 2012

So much for survival—but how can traditional retailers actually get ahead, perhaps even shaping the retail revolutions of the future? We believe that the winners will learn seven additional lessons.

Getting aheadWinning the retail war 11

Up Close and Personal

October 2011

Trying to be “another Amazon” is tempting—but far from advisable, and not only because Amazon’s strengths are so formidable. Traditional retailers have unique strengths of their own. And by recognizing and capitalizing on them they can build equally effective value propositions.

Take Amazon’s reputation for unmatched range and prices. That is true in some categories, but not all; in short, not every retailer is threatened. In grocery, for example, Amazon’s sales are increasing, but more than half are still in health and beauty care, not in fresh or ambient food6. Moreover, entering chilled foods would challenge Amazon’s ability to build relationships with meat, dairy and other fresh food suppliers—an area where older-established, more experienced grocery retailers hold a clear advantage.

To be sure, where there is substantial product overlap it’s tough for traditional retailers to copy, let alone beat, Amazon’s range and algorithmic re-pricing (which has also been extended to marketplace sellers). What’s more, while traditional retailers have lagged in creating effective loyalty programs—programs that encourage customers to announce their arrival in a store, for example, or that work seamlessly across channels—Amazon has forged ahead with Amazon Prime, which awards users “free” 1 or 2 day shipping in return for a fixed annual fee. (Students don’t pay any costs for 6 months, and for new mothers and caregivers Prime remains free for longer, with special discounts on baby products).

Estimates vary as to how successful Prime has been in keeping customers loyal and driving them to buy more. But according to one analyst, although only 4 percent of all Amazon customers were using Prime in 2011, the service is growing by 20 percent year-on-year. Moreover, once they join Prime, Amazon customers’ gross merchandise volume almost doubles in their first year of membership, which means that for every one million Prime members, Amazon’s revenues increase by 1.5 percent7.

Yet none should forget that brand is a key driver of customer loyalty—and even online shoppers will choose to buy from a familiar and trusted name. Despite its remarkable range of products, Amazon doesn’t yet enjoy the brand heritage and loyalty in all markets, compared to the likes of Marks & Spencer in the UK, Zara or Ikea in continental Europe or UNIQLO in Asia.

1. Do not copy

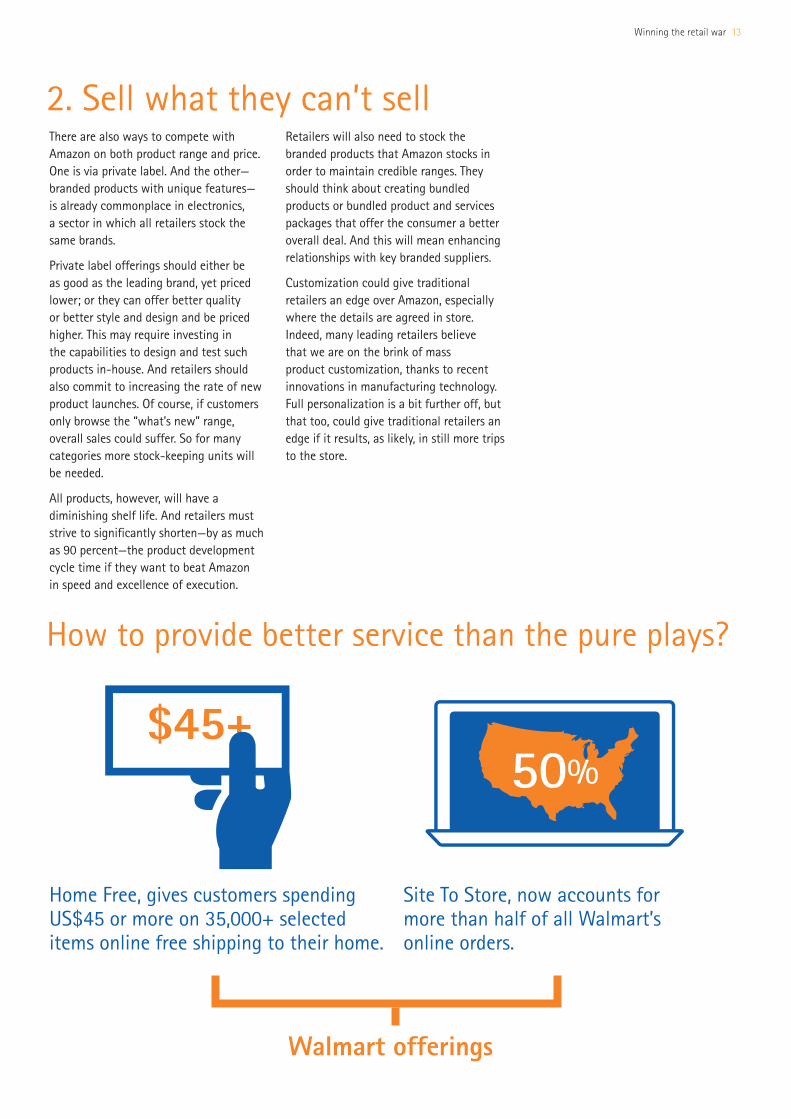

And some are beginning to do so. Case in point: Walmart, which offers its US customers several different delivery options. One such, Home Free, gives customers spending US$45 or more on 35,000+ selected items online free shipping to their home. Another, Site To Store, a Click & Collect service which offers free delivery to any Walmart store in the contiguous US, now accounts for more than half of all the company’s online orders and generates around US$3.5 billion in revenues. While Pick Up Today, a free Click & Reserve service that allows a customer to order store items online and pick them up at their Walmart store that same day or the next day if the order is made after 6:00 p.m. local time, has resulted in a 22 percent increase in basket size8.

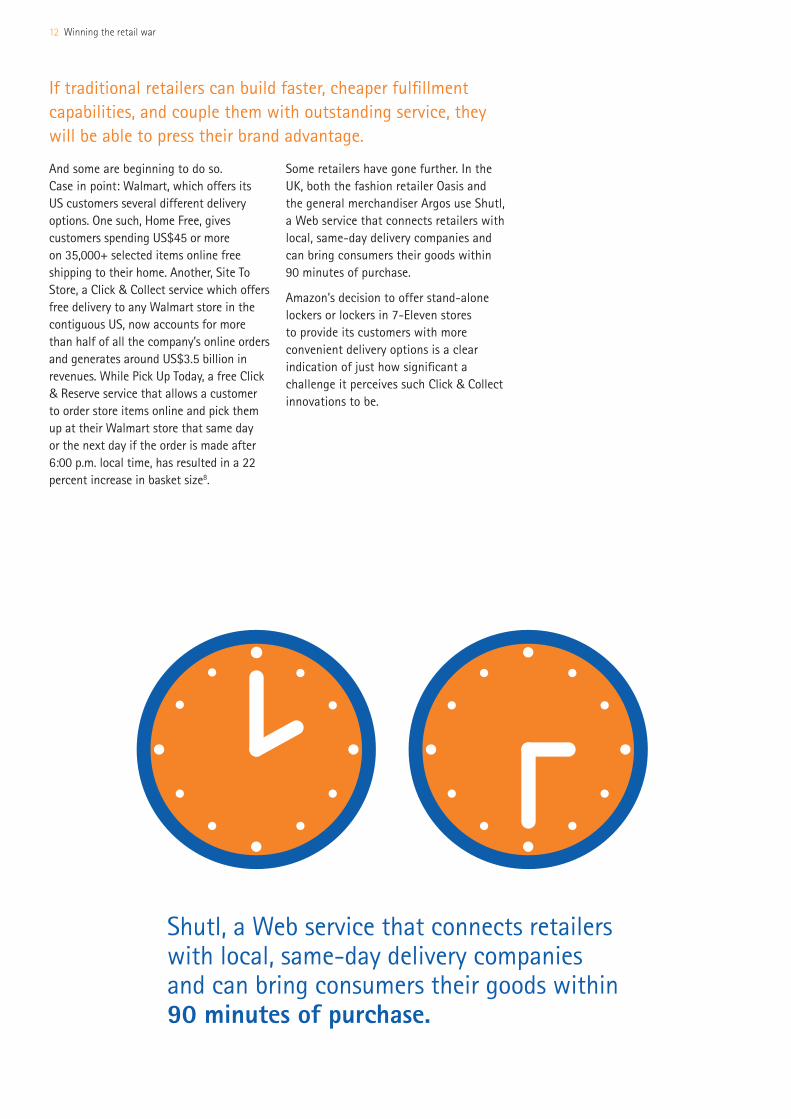

Some retailers have gone further. In the UK, both the fashion retailer Oasis and the general merchandiser Argos use Shutl, a Web service that connects retailers with local, same-day delivery companies and can bring consumers their goods within 90 minutes of purchase.

Amazon’s decision to offer stand-alone lockers or lockers in 7-Eleven stores to provide its customers with more convenient delivery options is a clear indication of just how significant a challenge it perceives such Click & Collect innovations to be.

Shutl, a Web service that connects retailers with local, same-day delivery companies and can bring consumers their goods within 90 minutes of purchase.

12 Winning the retail war

If traditional retailers can build faster, cheaper fulfillment capabilities, and couple them with outstanding service, they will be able to press their brand advantage.

There are also ways to compete with Amazon on both product range and price. One is via private label. And the other—branded products with unique features— is already commonplace in electronics, a sector in which all retailers stock the same brands.

Private label offerings should either be as good as the leading brand, yet priced lower; or they can offer better quality or better style and design and be priced higher. This may require investing in the capabilities to design and test such products in-house. And retailers should also commit to increasing the rate of new product launches. Of course, if customers only browse the “what’s new” range, overall sales could suffer. So for many categories more stock-keeping units will be needed.

All products, however, will have a diminishing shelf life. And retailers must strive to significantly shorten—by as much as 90 percent—the product development cycle time if they want to beat Amazon in speed and excellence of execution.

Retailers will also need to stock the branded products that Amazon stocks in order to maintain credible ranges. They should think about creating bundled products or bundled product and services packages that offer the consumer a better overall deal. And this will mean enhancing relationships with key branded suppliers.

Customization could give traditional retailers an edge over Amazon, especially where the details are agreed in store. Indeed, many leading retailers believe that we are on the brink of mass product customization, thanks to recent innovations in manufacturing technology. Full personalization is a bit further off, but that too, could give traditional retailers an edge if it results, as likely, in still more trips to the store.

How to provide better service than the pure plays?

Home Free, gives customers spending US$45 or more on 35,000+ selected items online free shipping to their home.

Site To Store, now accounts for more than half of all Walmart’s online orders.

$45+50%

Winning the retail war 13

2. Sell what they can’t sell

Walmart offerings

Customer service will be a critical weapon in the battle to compete with Amazon. And traditional retailers need to think about how they can differentiate their service by applying the personal touch at every stage of the customer purchase journey. Consumers tolerate longer fulfillment times online in return for free delivery—giving traditional players an opportunity to press home their key advantages: The social interplay and instant gratification that shoppers can enjoy, via sales associates, in-store.

That will mean providing welcoming sales associates who can help customers pick just the right product for their needs. Shoppers are unlikely to return unless they remember their store visit as an enjoyable and fulfilling experience. So store associates need to be exceptionally skilled in the discipline of selling. If customers make it clear that they don’t want help, for example, they should back off. Moreover, any add-on services that they may require—wrapping, for instance—

should be as efficient as possible. Best Buy’s Geek Squad, which provides all round technology assistance, is a good example of the top-notch customer service skills that sustain such efficiency.

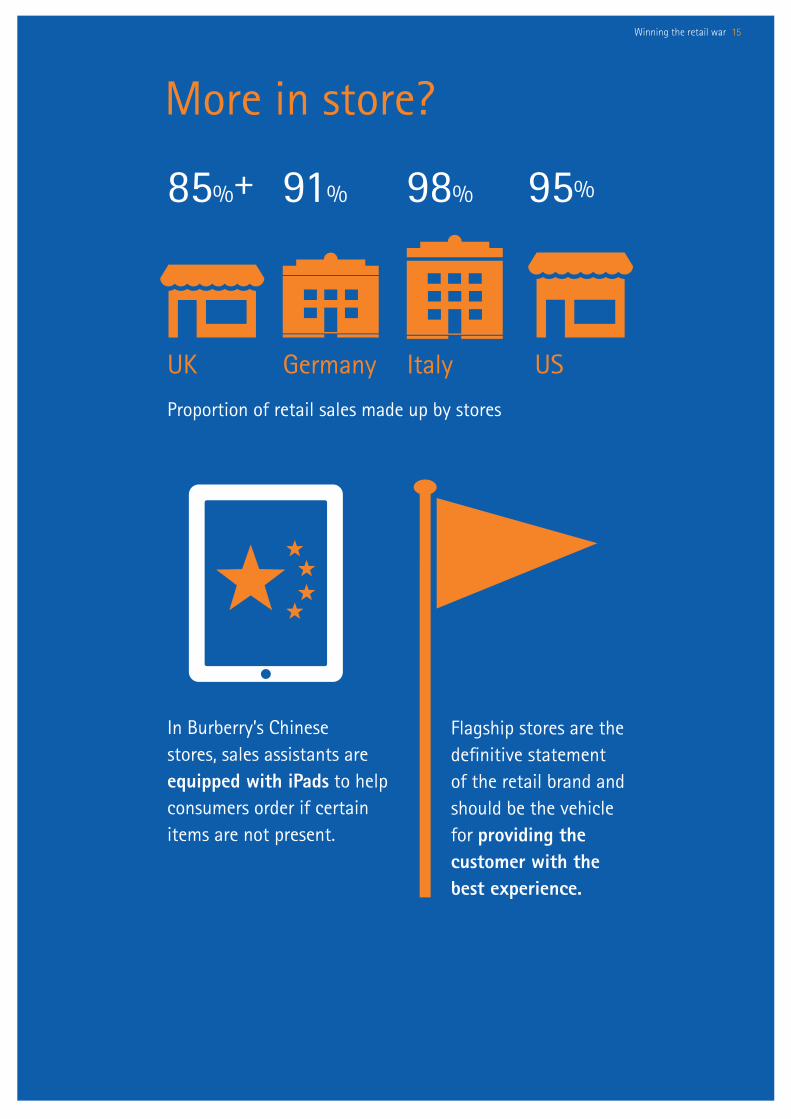

Delivering exceptional customer service will inevitably require a coordinated approach to managing store staff—from recruitment, training and deployment, to performance measurement, appraisals and compensation. Apple, for instance, has made a concerted effort to put customer service at the heart of its destination retail outlets. And some non-technology retailers are following suit. Burberry, for example, blends innovative use of social media (over 11 million Facebook fans who enjoy special perks associated with the brand) with a multi-channel approach to customer service. In Burberry’s China stores, sales assistants are equipped with iPads to help consumers order if certain items are not present.

In many countries, stores still account for the bulk of retail sales. In the UK, for instance, the proportion is more than 85 percent and in other European countries it’s even higher: 91 percent in Germany, and a whopping 98 percent in Italy, while in the US stores account for 95 percent of all sales. Stores, indeed, clearly differentiate traditional retailers from Amazon and its ilk and that suggests there is a strong argument for reshaping the portfolio, closing some stores and opening even more stores in two particular “formats”—flagship and convenience.

Flagship stores are the definitive statement of the retail brand and should be the vehicle for providing the customer with the best experience the brand can offer: A strong, but not necessarily complete range; great customer service; add-on services; spectacle and entertainment; full multichannel integration. The fact that even online businesses are now opening flagship stores—for example, Kiddicare (the baby

products website from Morrison’s – a UK retailer) took over 10 of the former Best Buy Europe big box stores—is clear proof of their powerful potential.

Convenience stores, located close to customers and stocking high-volume items, are usually thought of in conjunction with food, and several leading global grocers—Walmart, France’s Carrefour, Tesco and the Dutch company Ahold among them—have successfully expanded a concept that first proved popular with time-starved consumers in developed markets into Asia and Latin America. Convenience has wider applications, however. In the UK, for example, the fashion retailer House of Fraser has opened two innovative Internet-only stores of around 1,500 sq ft in locations where the company does not have a full 90,000 sq ft store. Critically, because they will also function as a collection and return point for online orders, convenience stores also need to be fully multichannel integrated.

Readers may also be interested in

Overstored: How Retailers Can Retain a Profitable Physical Store Network in the Face of Growing Migration to Digital Channels

July 2012

RILA and Auburn University Re-leases State of the Retail Supply Chain Report February 2012

Creating a > Experience Through Mobility: Key Steps to Help Retailers Realize the Promise of Mobile September 2011

14 Winning the retail war

4. Open flagships and C-Stores

3. Up close and personal

Winning the retail war 15

Proportion of retail sales made up by stores

85%+ 91% 98% 95%

UK Germany Italy US

In Burberry’s Chinese stores, sales assistants are equipped with iPads to help consumers order if certain items are not present.

More in store?

Flagship stores are the definitive statement of the retail brand and should be the vehicle for providing the customer with the best experience.

Readers viewing this page may also be interested in

How to Make Your Company Think Like a Customer

March 2012

In a world where customers expect a seamless shopping experience, across channels, closing all stores and becoming an online-only business is plainly not an option—to the contrary. For a retailer with many stores, these assets should be a core component of the strategy to compete. And that means the value that the store’s proposition offers to customers—whether flagship or convenience—has to be the best it can possibly be.

Value = benefits – price. Stores have traditionally added value by editing the range in terms of breadth, depth, quality, and design, as well as via the store environment, the level of interaction with staff, availability of services and the convenience of the experience in terms of immediate availability of product and location. Now, they are adding a new value: Integration with other channels.

Customers frustrated by long waits at the post office sorting center or the delivery company depot to collect their package can now choose from a variety of more convenient options. In France, for instance, hypermarkets allow customers to order online and then “drive through” to pick up. While in the UK ASOS has partnered with collect+ to allow customers to select

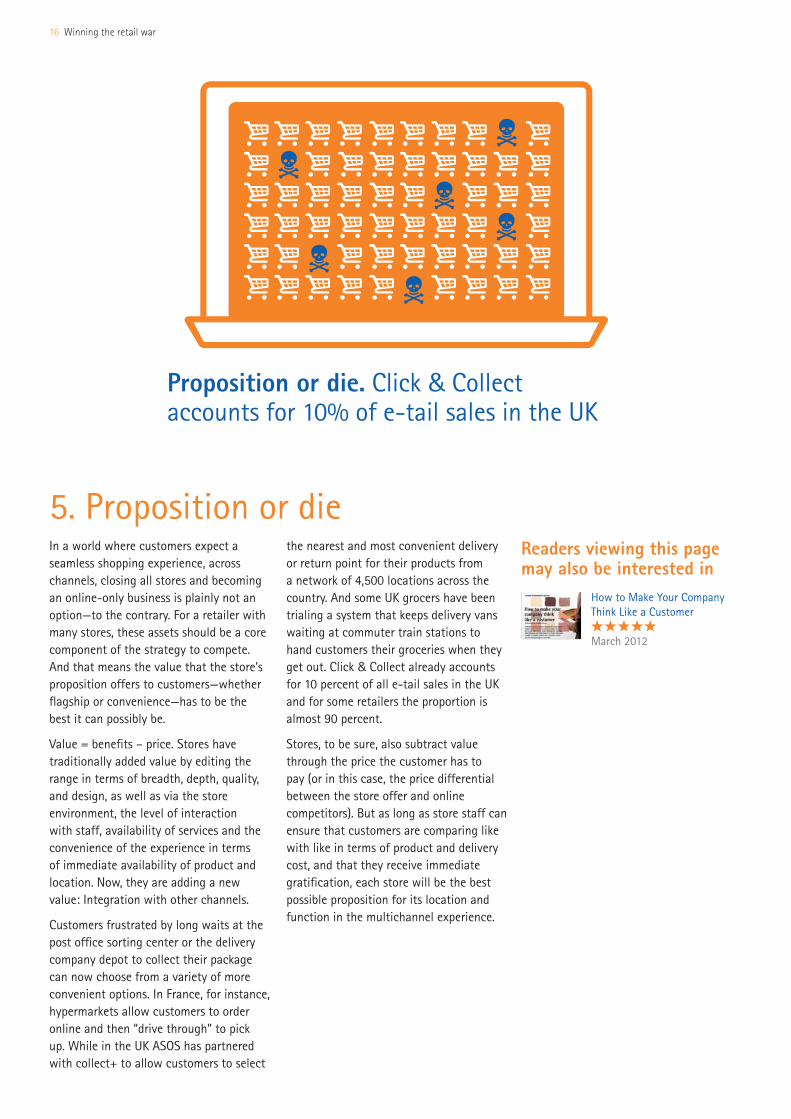

the nearest and most convenient delivery or return point for their products from a network of 4,500 locations across the country. And some UK grocers have been trialing a system that keeps delivery vans waiting at commuter train stations to hand customers their groceries when they get out. Click & Collect already accounts for 10 percent of all e-tail sales in the UK and for some retailers the proportion is almost 90 percent.

Stores, to be sure, also subtract value through the price the customer has to pay (or in this case, the price differential between the store offer and online competitors). But as long as store staff can ensure that customers are comparing like with like in terms of product and delivery cost, and that they receive immediate gratification, each store will be the best possible proposition for its location and function in the multichannel experience.

Proposition or die. Click & Collect accounts for 10% of e-tail sales in the UK

16 Winning the retail war

5. Proposition or die

One of Amazon’s key advantages is its Marketplace, which gives it the ability to make money from the so-called long tail—the much larger number of “niche” items that do not constitute best sellers. By holding stock in relatively few places and aggregating demand over a wide geographic area, the company is able to fulfill demand at substantially lower cost than bricks-and-mortar retailers anyway. And it can sell virtual goods—e-books and music downloads—for which the holding and delivery costs are zero, especially profitably. Its Marketplace, however, conveys additional advantages. Because individual Marketplace sellers hold the stock for Amazon, consumers get easy access to items for which there is limited demand—and Amazon can charge the sellers for using its fulfillment system.

Traditional general merchandisers need to replicate the Amazon Marketplace, letting 3rd parties hold stock and charging them a commission on sales in return for bringing them customers. They can differentiate themselves from Amazon by finding different 3rd party sellers or integrating fulfillment with their Click & Collect operations. That will be challenging—especially if they have to deliver a truckload of Marketplace Click & Collect sales to each store. And they will be hard pressed to match Amazon’s strategy of watching what sells on its Marketplace very closely and switching the fast sellers into own-bought product. The benefits of rising to the challenge, however, promise to be huge.

Amazon does not play by the same rules as traditional retailers. Indeed, it differs in two specific ways that have conveyed distinct advantages.

First, Amazon’s insistence on working across a 5-7 year investment horizon has enabled it to take bolder initiatives in developing its market leadership. Witness Amazon’s recent US$750 million investment in a warehouse-systems provider – more than its earnings from continuing operations in the whole of FY11. Private companies, of course, can take a similar stance: the hard discount supermarket chain Aldi, for example, has been known to invest a whole year’s profits in lowering prices. But investors generally do not tolerate such behavior in public companies.

Secondly, Amazon has multiple revenue streams that leverage its core technology assets, strengthening its risk tolerance and deepening its ability to re-invest and grow. According to the company’s most recent quarterly results, 17 percent of its revenues come from services—3rd party seller fees including commissions and

related shipping fees (some 39 percent of the units Amazon sells are from 3rd party vendors who pay either an annual subscription fee or a nominal amount per item sold), digital content subscriptions, and non-retail activities. The non-retail activities include platform services and application hosting and advertising. According to the cloud consulting company DeepField networks, one in three Internet users now access the Amazon Cloud daily. In addition, one percent of all Internet consumer traffic passes through Amazon-managed infrastructure.

Few traditional, publicly quoted retailers will be in a position to replicate Amazon’s enviably extended investment horizon—but building additional revenue streams is a realistic option. Consider, for example, how Tesco has shown that trusted retail brands can be stretched beyond the retail core, into banking and mobile telephony.

Readers may also be interested in

Accenture Technology Vision 2012: Emerging Technology Trends for IT Leaders

May 2012

From Analog to Digital: How to Transform the Business Model July 2012

Winning the retail war 17

6. Marketplace rules, OK

7. Same game, different rules

Most recent quotes

Our marketplaces business has turned the corner, shifting from defense to offense, and is delivering accelerating results.

by John Donahoe, CEO eBay

Accelerating

Amazon and the other online pure plays are fast, fit and flexible—supremely well positioned to retain their privileged position as the destination of choice for growing numbers of the world’s consumers. But shopping, as every retailer knows, is fundamentally a social activity. Indeed, Amazon’s success is due in large part to its recognition that consumers want an enjoyable and relevant experience when they shop—and to its bold and innovative approach to fulfilling that need.

Getting started

Traditional retailers may not be able to compete with Amazon and its imitators on range and price alone; in fact, they would be foolish to try. But they can seek to exceed the leaders’ performance with personalized and multichannel offerings that make every consumer feel special. By innovating faster, employing technologically savvy staff in key positions, embracing social media more imaginatively, training sales associates to deliver exceptional in-store service, making every store count, and focusing on flagship and convenience stores tailored to

local needs and conditions, they can boost the power of their own brand—their key differentiator in driving customer loyalty and profitable growth.

Strategy without tactics is the slowest route to victory. Tactics without strategy is the noise before defeat. The time to start developing both is now.

18 Winning the retail war

6TH

Amazon will be the world’s 6th largest retailer by 2015

Get in touchAccenture has a dedicated team focused on the issues retailers face competing in the online economy – for more information please contact:

EuropeRick [email protected]

North AmericaNatt [email protected]

Asia PacificRaymond [email protected]

1 Nomura Equity Research, November 2011

2 Kantar Retail – “Digital Retailing in a Brick and Mortar World” – September 20, 2011

3 “eBay aims for lead in mobile payments race”, Financial Times, April 2012

http://www.ft.com/cms/s/0/a4379d7c-899d-11e1-85b6-00144feab49a.html#axzz1tRUpVPFl Google.com Annual reports

4 Amazon is No 4 on Fast Company’s 2012 list and No 2 on Forbes’ 2012 list; Square and Twitter are No 5 and No 6 5 ‘From Scratch: Amazon Keeps Supply Chain Close To Home’, Beth Bacheldor, March 2004

6 PlanetRetail Amazon profile 2012

7 http://www.practicalecommerce.com/articles/3043-Amazon-Prime-5-Million-Members-20-Percent-Growth; http://www.bloomberg.com/news/2012-02-14/amazon-said-to-have-fewer-prime-subscribers-than-estimated-shares-decline.html?utm_medium=referral&utm_source=pulsenews

8 http://seekingalpha.com/article/287722-wal-mart-stores-ceo-discusses-q2-2012-results-earnings-call-transcript

http://www.prnewswire.com/news-releases/wal-mart-completes-national-rollout-of-site-to-storesm-service-52716142.html

About Accenture Accenture is a global management consulting, technology services and outsourcing company, with more than 244,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$25.5 billion for the fiscal year ended Aug. 31, 2011. Its home page is www.accenture.com.

Follow us on Twitter @AccentureSocial

Learn more at www.accenture.com/retail

Copyright © 2012 Accenture. All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

Rights to trademarks referenced herein, other than Accenture trademarks, belong to their respective owners. We disclaim proprietary interest in the marks and names of others.