Embed Size (px)

Citation preview

A R G U S R E S E A R C H C O M P A N Y • 6 1 B R O A D W A Y • N E W Y O R K, N.Y. 1 0 0 0 6

W E E K L Y S T A F F R E P O R T

Withfivemonthsremainingin2021,economicfundamentalsgenerallyarepositive,creatinganenvironmentforfurtherstock-marketgainsintoyear-end.Theeconomyandpublichealthhavestagedaremarkablecomebackfromthedepthsofthepandemic-in-ducedeconomicshutdown.Thecalendarsecond-quarterearningsseasonhasblownawayalready-highexpectations,reflectingacombinationofmaximumrecoverymomentumandcomparisonsagainstayear-earlierperiodwhenthenationwasineconomicshutdown. Ongoingmonetarystimulus,viaQEandultra-lowshort-termrates,continues.TheFedlikelywouldtaperitsmassiveQEprogramlongbeforeitactuallyraisedthefedfundsrate.Bysignalingthatitintendstostaythecourseonaccommodativemonetarypolicy,andbypositingthatanyinflationspikewastransitory,theFedhasdispelledinflationfearsandallowedbullstoinvestwithconfidence. ThebiggestcurrentconcernsaretheresurgenceinCOVID-19inunder-vaccinatedareas,andelevatedvaluationsnotonlyinthestockmarketbutinmostassetclasses.Aslongastheeconomycankeepexpandingandearningskeepgrowing,valuationconcernsshouldmoderateovertime.

The Economy, Interest Rates and EarningsTheadvancereportof2Q21GDPshowedgrowthof6.5%,edgingupfrom6.3%forthefirstquarter.TheU.S.economyinthefirsthalfof2021carriedstrengthforwardfromthesecondhalfof2020,whichfeatured4.2%growthinthefourthquarterand30%inabounce-backthirdquarter. During2Q21,keyGDPdrivers includedpersonalconsumptionexpenditures(PCE),non-residentialfixedinvestment,exports,andstateandlocalgovernmentspending.TheselattertwocategorieshavebothcomebackfrommultiplequartersinwhichtheircontributiontoGDPgrowthwasbelowthelong-termtrend.Growthdriverswereoffsetpartlybydecreasesinprivateinventoryinvestment,residentialfixedinvestment,andfederalgovernmentspending.Theselattertwocategoriesweremainstaysintheeconomy’sdarkesthoursduringtheworstofthepandemic. Upuntil2Q21,U.S.grossdomesticproductonanannualizedbasisremainedbelowthepre-pandemicpeak.Whileweoriginallytargeteda“round-triprecovery”intheeconomytothesecondhalf,inspring2021wemovedupourtargetbasedonsignsofacceleratingmomentumasvaccinationssurged.Infact,current-dollarGDPin2Q21reached$22.72trillion,up13%year-over-yearandabovethepriorall-timehighreachedin4Q19.

(continued on next page)

August 9, 2021Vol. 88, No. 10

IN THIS ISSUE

SECTION 1Economic & Market CommentaryTechnical Trends Commentary

SECTION 2Focus StocksChanges in RatingsGrowth & Value StocksUtilityScopeStocks to Avoid

SECTION 3Economic CalendarSpecial Situations & ScreensMaster List ChangesRecent Argus BUY Upgrades

Trying to Get to Normal: Our Monthly Survey of the Economy, Interest Rates, and Markets

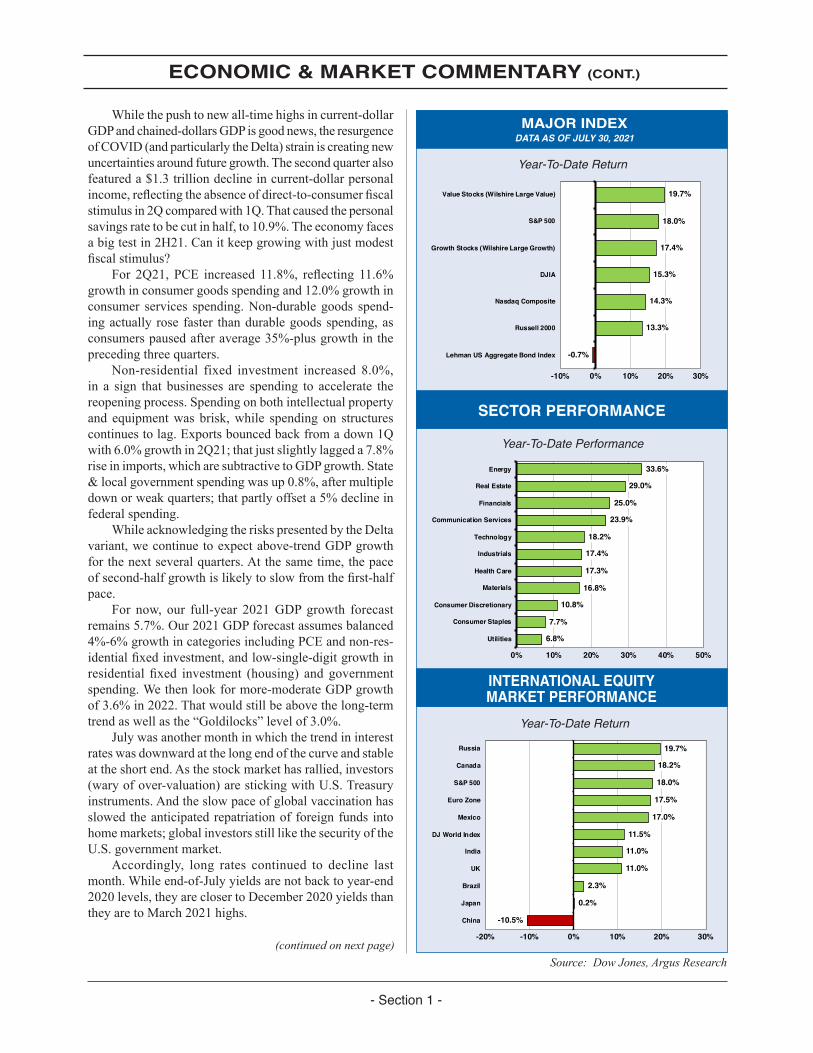

Whilethepushtonewall-timehighsincurrent-dollarGDPandchained-dollarsGDPisgoodnews,theresurgenceofCOVID(andparticularlytheDelta)strainiscreatingnewuncertaintiesaroundfuturegrowth.Thesecondquarteralsofeatureda$1.3trilliondeclineincurrent-dollarpersonalincome,reflectingtheabsenceofdirect-to-consumerfiscalstimulusin2Qcomparedwith1Q.Thatcausedthepersonalsavingsratetobecutinhalf,to10.9%.Theeconomyfacesabigtestin2H21.Canitkeepgrowingwithjustmodestfiscalstimulus? For 2Q21, PCE increased 11.8%, reflecting 11.6%growthinconsumergoodsspendingand12.0%growthinconsumer services spending.Non-durable goods spend-ingactually rose faster thandurablegoodsspending,asconsumerspausedafteraverage35%-plusgrowthintheprecedingthreequarters. Non-residential fixed investment increased 8.0%,in a sign that businesses are spending to accelerate thereopeningprocess.Spendingonbothintellectualpropertyand equipmentwas brisk,while spendingon structurescontinuestolag.Exportsbouncedbackfromadown1Qwith6.0%growthin2Q21;thatjustslightlylaggeda7.8%riseinimports,whicharesubtractivetoGDPgrowth.State&localgovernmentspendingwasup0.8%,aftermultipledownorweakquarters;thatpartlyoffseta5%declineinfederalspending. WhileacknowledgingtheriskspresentedbytheDeltavariant,wecontinuetoexpectabove-trendGDPgrowthforthenextseveralquarters.Atthesametime,thepaceofsecond-halfgrowthislikelytoslowfromthefirst-halfpace. For now, our full-year 2021GDPgrowth forecastremains5.7%.Our2021GDPforecastassumesbalanced4%-6%growthincategoriesincludingPCEandnon-res-identialfixedinvestment,andlow-single-digitgrowthinresidential fixed investment (housing) and governmentspending.Wethenlookformore-moderateGDPgrowthof3.6%in2022.Thatwouldstillbeabovethelong-termtrendaswellasthe“Goldilocks”levelof3.0%. Julywasanothermonthinwhichthetrendininterestrateswasdownwardatthelongendofthecurveandstableattheshortend.Asthestockmarkethasrallied,investors(waryofover-valuation)arestickingwithU.S.Treasuryinstruments.Andtheslowpaceofglobalvaccinationhasslowedtheanticipatedrepatriationofforeignfunds intohomemarkets;globalinvestorsstilllikethesecurityoftheU.S.governmentmarket. Accordingly, long rates continued to decline lastmonth.Whileend-of-Julyyieldsarenotbacktoyear-end2020levels,theyareclosertoDecember2020yieldsthantheyaretoMarch2021highs.

ECONOMIC & MARKET COMMENTARY (CONT.)

MAJOR INDEXDATA AS OF JULY 30, 2021

SECTOR PERFORMANCE

INTERNATIONAL EQUITY MARKET PERFORMANCE

Source: Dow Jones, Argus Research

- Section 1 -

Year-To-Date Return

Year-To-Date Return

Year-To-Date Performance

(continued on next page)

19.7%

18.0%

17.4%

15.3%

14.3%

13.3%

-0.7%

-10% 0% 10% 20% 30%

Value Stocks (Wilshire Large Value)

S&P 500

Growth Stocks (Wilshire Large Growth)

DJIA

Nasdaq Composite

Russell 2000

Lehman US Aggregate Bond Index

33.6%

29.0%

25.0%

23.9%

18.2%

17.4%

17.3%

16.8%

10.8%

7.7%

6.8%

0% 10% 20% 30% 40% 50%

Energy

Real Estate

Financials

Communication Services

Technology

Industrials

Health Care

Materials

Consumer Discretionary

Consumer Staples

Utilities

19.7%

18.2%

18.0%

17.5%

17.0%

11.5%

11.0%

11.0%

2.3%

0.2%

-10.5%

-20% -10% 0% 10% 20% 30%

Russia

Canada

S&P 500

Euro Zone

Mexico

DJ World Index

India

UK

Brazil

Japan

China

ECONOMIC & MARKET COMMENTARY (CONT.)

Asareminder,the10-yearTreasuryyieldrosesharplyfrom0.9%attheendof2020to1.75%bytheendofthefirstquarterof2021.Thelongyieldgenerallyhasbeentrendinglowereversince,however.The10-yearyieldendedJulyat1.24%afterendingJuneat1.48%. TheFederalReserve’spolicy-settingarm,theFederalOpenMarketCommittee (FOMC),met inmid-Julyandhelditsbenchmarkinterestrate(thefedfundsrate)nearzero.Thatwasasexpected.InvestorswerewaitingtoseeiftherewereanychangesintheFed’sstanceorevennuancesincurrentaccommodativepolicy. UnlikeinJune,whentheFedseemedtobemullingapotentialdownshiftinquantitativeeasing,theJulysessiondidnotgiveinvestorsmuchtochewon.Inaunanimouslyapproved statement, the FOMC said that the economycontinuestostrengthen.ChairmanJeromePowellsaidtheFedisnotclosetoconsideringaratehike.TheFedwantstosee“substantialfurtherprogress”onemploymentandwould countenancehigher inflationbefore beginning totightenpolicy.InitialtighteninginpolicymostlikelywouldbeareductioninQEratherthananoutrightratecut. Weconcurthatrecentelevatedinflationnumberscon-tainedsomedistortionsthatmaybeoverstatingthelong-termpricetrend.Butinflationinherentlyisunpredictable,andtheFedmayneedtoamenditsagendainresponsetoreal-timeinflationdataacross2021and2022. Assumingtheeconomyistrulyexpandingagain,the10-yearcannotstaydownforever.Welookforthe10-yearyieldtobreakabove2.0%eventually,perhapsassoonasyear-end2021--thoughmorelikelyatsomepointin2022. Second-quarterearningsseasonhasbeenanunmitigat-edsuccess.ThefinalweekofJuly,whichwasthebusiestsingleweek of the earnings season,was even strongerthan thefirst twoweeks.Withabout60%ofcompanieshavingreported,S&P500earningsfromcontinuingoper-ationsfor2Q21areupmorethan70%year-over-year,onamarket-cap-weighted percentage-change basis.WhileBloombergandFactSethavecalculatedslightlydifferentpercentagechanges,bothconcurthat2Q21earningsgrowthisthestrongestsincetherecoveryquarterof4Q09follow-ingtheGreatRecessionof2008-2009. Earnings are being pushed up by amultitude offactors, reflecting thecombinationofpositiveeconomicfundamentals,vaccine-andreopening-inducedoptimism,fiscalandmonetarystimulus,andmore.Earningsin1H21alsobenefitedfromrecoveryinsectorssuchasEnergyandIndustrials,whichweresubtractiveto2020earningsbutarecontributingstronglyin2021. Weprioritizeperformanceonayear-over-yearbasisoverperformanceagainstconsensusestimates,giventhatthelattercanbesteeredbycompanyexecutives.Butthenumberofcompaniestoppingconsensushasbeenremark-able,andperhapshistorical,inthe2Q21earningsseasontodate.Approximately88%ofcompanieshavepostedsec-ond-quarterEPSthatexceededpre-reportingexpectations.Andthescaleoftheearningsbeatisnotable.Companies

haveoutperformedexpectationsnotbyafewpercentagepoints,butbyover20%comparedwithconsensusestimates. About85%ofcompanieshaveexceededconsensusrevenue expectations.With the “scarcityof everything”spurred by high demand in an accelerating recovery,companieshavepricingpower.Higherpriceareenablingcompanies tooffsethigher inputcosts,whichotherwisewouldbenegativelyimpactingmargins. Afterfirst-halfEPSgrowthexceeded50%,welookformore-moderatebutstillabove-trendEPSgrowthof18%inthesecondhalfof2021.Companieswillbeconfront-ingmore-challengingcompsbeginningwiththird-quarter2021earnings,tobereportedinmid-October.Currently,consensusexpectationsareforthird-quartergrowthinthemid-20%range,andfourth-quartergrowthinthehigh-teenspercentagerange. InMay2021,andforathirdtimethisyear,weraisedour2021estimateofS&P500earningsfromcontinuingoperationsto$182pershare,fromaprior$177.Wealsoraisedour2022estimateofS&P500earningsfromcon-tinuingoperationsto$205pershare,fromaprior$201.Wearelikelytoraiseourforecastsonceagainafter2Q21EPSresultsarefinalized.

Domestic and Global MarketsLatein2020,thestockmarketbeganitsrotationawayfromgrowth-centricsectorsthathadlongledthemarket,andtowardcyclical,interest-ratesensitive,andinflation-benefi-ciarysectors.Theshiftwaspredicatedontheviewthattherecoveringeconomywouldfavorcyclicalsectors,includingIndustrialandRealEstate;thatrisingdemandwouldpushup interest rates,benefitingFinancialServices; and thatrisingpriceswouldfavor“wealthintheground”sectorsincludingEnergyandBasicMaterials. Fortheyear-to-date,thatthesishascertainlyplayedout.Fiveofthesixtopsectorsin2021remaincyclical,havebene-fitedfromrisingrates,orareperceivedashigherinflationplays. In the secondquarter, and particularly in late JunethroughJuly,themarketstagedapartialre-rotationbacktogrowth.Onthatbasis,asoftheendofJuly,growthhasclosedthegapwithvalue.AndtheNasdaqhasnearlypulledevenwiththeblue-chipDJIA. Julywasagoodmonth for stocks,andvirtuallyallindicesandinvestingstylesimprovedmonth-over-month.WilshireLarge-CapValue,up17.7%asoftheendofJune,is nowon topwith a 19.7%gain.WilshireLarge-CapGrowthcontinuestoclosethegapwithValue,whichitnowlagsbylessthan200bpsyear-to-date.ThisistheclosestithasbeentotheWilshireValueallyear. NextistheS&P500,up18.0%foryear.TheS&P500overtooktheDJIAbeforemidyearandhassincewideneditsadvantage.TheDowisup15.3%year-to-date.It’sunusualtosaythis lateinthesummer,but theNasdaqisdeeplylagging theblue-chip indexes.TheNasdaq isup14.3%year-to-date,whichputsitbehindnotonlytheS&P500butalsotheDJIA.

- Section 1 -

Themarketappearstohavelostitsattractiontosmall-caps,perhapsonfearsthatanycorporatetaxhikewouldhitthiscategoryharder.Thesmall-capRussell2000isup13.3%,havingshedalmost400bpsofgaininthepastfewmonths. TheBarclayBloombergU.S.Bondindex,whichdeliv-ered7.2%totalreturnin2020,isdown0.7%fortheyear.Thatisanimprovementafterbeingdown3.0%asoftheendofMarch.Ifratesatthelongerendofthecurveresumetheir rise, fixed-income total return is likely toweakenfurther.Giventherecentdeclineinlongyields,wedonotlookformassiveunderperformanceinbondsthisyear. Sevenmonthsintothetradingyear,everysectorintheS&P500ispositive.TherotationalwinnersinEnergy,BasicMaterials,FinancialServices,andRealEstateremaininfront.Butgrowthsectorshavealsoparticipatedintherallyandhavebeensomeofthestrongestmarketperformersoflate. Someof the year-to-datewinners have given backin the past twomonths.These includeBasicMaterials,Industrials, and Financial Services. Fortunately, thesesectorshadexcessgainstospare.EventhoughitstumbledinJuly,Energyremainsthemarketleaderwitha34%gainyear-to-date,eventhoughthatisdownfromthemid-40%range.FinancialServices andRealEstate arenextwithupper-20%gains.Bothsectorshavebeensubjecttosomeprofit-taking,yetbotharehangingontoleadershipspots. Growthsectorshaveralliedandareclosinginontheleaders.CommunicationsServiceisupinmid-20%rangewhileTechnologyisinthehighteens.Otherdouble-digitwinnersincludeHealthcare,Industrials,BasicMaterials,andConsumerDiscretionary. Inourview,year-end2020rotationthathascarriedinto2021ishealthy.InvestorsrotatedoutofsectorssuchasTechnologythatlookedover-extendedatyear-end2020,andintoareassuchasEnergy,FinancialServices,andRealEstatewheretheysawvalue. Wenowseesignsofare-rotationintotheoldgrowthfavorites.Buttheoriginalrotationintocyclical,ratesensi-tiveandwealthinthegroundsectorsisnotover.MuchastheoriginalrotationtooksomeoftheheatoffTechnologyandallowedinvestorstoloveTechstocksanew,wecouldseerecentsoftnessasearly-2021rotationfavoritesgivewaytoarenewedaffectionforthesemulti-yearunderperformersasreopeningcontinuestodrivegrowth. ThetrendinU.S.long-terminterestrateshasshowncorrelationwithsectorrotationintheU.S.equitymarket.Cyclical reopening stocks, inflation beneficiaries, andFinancialServicesstocksallralliedinthespringmonthsasratesmovedhigher.Asnoted,rateshavebeenmovingdowninrecentmonths,andthatisallowinggrowthstockstorotatebackontofavor. In July,Technology sectorweighting rosemonth-over-monthforthefirsttimesincelatewinter.Techstocksreached27.8%ofS&P500sectorweight,up40bpsmonth-over-month.Healthcarealsoexpandedmonth-over-monthby40bps,toa13.4%weighting.Electiveproceduresthatweredeferredduringthepandemichaveresumed;atthe

sametime,companiescontinuetobattleCOVID-19’snewvariants.CommunicationServicesalsoedgedhigher,ledbymediaandinternetstocks. Thesegainscameattheexpenseofearly-yearwin-ners,whereinvestorsshowedwillingnesstotakeprofits.FinancialServicesweightingslidlowerby40bpsto10.9%,as falling interest rates reduced the net interestmarginavailable to banks.ConsumerDiscretionary also shedmarketweight.Whilethisisconsideredagrowthsector,areasincludinghospitality,leisure,restaurants,andretailhaveledthemarketonreopening.AcombinationofDeltaconcernandstrongperformanceappearstohavepromptedsomeprofit-takinginthoseareas. OtherreopeningbeneficiariessuchasEnergyandIn-dustrialalsobackeddownslightlyinJuly.Despitemodestpullbacksinthereopeningtrade,mostofthesesectorsarebiggerthantheywereayearago.Wecontinuetobelievethatthebalancedadvanceinthemarket,inwhichgrowthsectorstag-teamreopeningsectors,hasprovidedhealthybalancethatisastrongsupportfortheoverallstockmarketatcurrentlevels. AsvaccinesproliferateintheU.S.andahandfulofdeveloped nations, the pandemic continues to presentchallengesintheworldatlarge.ManymajorinternationalmarketsweakenedinJuly,however.Ourcompositeof11globalboursesonaveragewasup10.9%attheendofJuly,versusup12.2%atmidyear. Japanisbarelypositiveyear-to-date,withtheOlym-picsprovidingnotailwind.Chinaisdown11%inapartlyself-inflicteddecline,asthegovernmenttakesaimattopTechstocks. Thebest-performingthemeamongourglobalindicesis theAmericas,whereCanadaandMexicocontinue tobuildonearly-yearstrength.Europeand theUKtookastepback,asdidtheBRICs.

ConclusionThe highly infectiousDelta variant ofCOVID-19 hascausedasurgeofinfectionsandhigherhospitalizations.Butbecause it ismainlyhittingahealthierandyoungerpopulation,themortalityrateisnotasfearsomeasinthefirstwavesofthepandemic.Outbreaksalsoarelocalizedtomainlyunvaccinatedstatesandregions.Peopleintheseareasarestartingtogetvaccinatedingreaternumbers. ExitingJuly,theS&P500hadbankeda17%gainsofarin2021.Whenstocksaredoingthiswellthisfaralongintheyear,theytendtofinishwithbetter-than-averageupside.Inthisenvironment,mostinvestorswillholdthroughthetypicallyslowAugust-Septemberperiodandthenlookforadditionalfireworksinthefinalthreemonthsoftheyear.Withsomanyinvestorsinthegreensofarin2021,andwithbearsatsomepointneedingtocapitulateandbuytheyear’swinners,furthergainscanbecomeaself-fulfillingprophecy.

JimKelleher,CFA,DirectorofResearch

ECONOMIC & MARKET COMMENTARY (CONT.)

TECHNICAL TRENDS COMMENTARY

- Section 1 -

Julyendedwithaboutofselling,butbullsconsidereditoverdueprofit-takingafteranothersuccessfulmonth.EvenwithFriday’swashout,theS&P500rose2.3%inJuly.Thatmarkedsixstraightmonthsofappreciationforthebluechipindex(onlyJanuaryhasbeennegativein2021)andwasthebestmarketmonthsinceApril. InJuly,stocksweredoingwhattheyaresupposedtodo.Since1980,theS&P500hasaveragedagainof1.1%inJuly,whichmakesitbyfarthebestsummermonth.Oddly,Julyhasbeendownnearlyasmanytimesasithasbeenupsince1980.ButJulyhashadsomebigwinners,including2010(up7.5%)and2013(up4.9%). As far as investors are concerned, the only troublewithJulyisthatitisfollowedbyAugustandSeptember.Since1980,Augusthasaveragedalackluster0.05%gain.

September has the distinction of being the onlymonthamongthe12toaverageanegativereturnsince1980.Overthepast41years,theS&P500hasdeclinedonaverageby0.69%inSeptember. The silver lining for stocks, assuming theymake itthrough theAugust-September stretchwithmost of theyear-to-dategainsintact,istheOctober-Decemberperiod.DespiteOctober’sfearsomereputation, this three-monthstretchtypicallyisthemarket’sbestallyear. Since1980,theS&P500hasaveragedagainof4.4%intheOctober-Decemberperiod.IftheU.S.stockmarketcanaddanother4%tothe17%advanceyeartodate,that20%-plusgainfor theyearwouldmore thandouble theaverage10.5%returnsince1980.

JimKelleher,CFA,DirectorofResearch

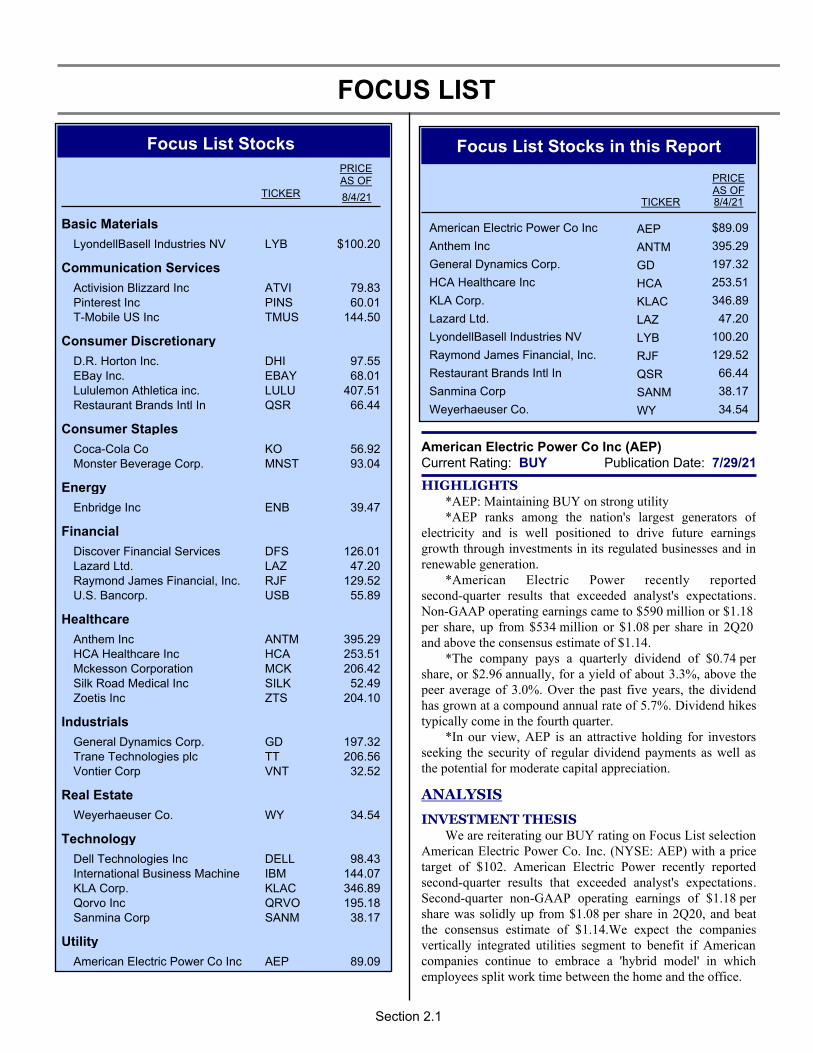

FOCUS LIST

Focus List Stocks

TICKER

PRICEAS OF

8/4/21

Basic Materials

LyondellBasell Industries NV LYB $100.20

Communication Services

Activision Blizzard Inc ATVI 79.83Pinterest Inc PINS 60.01T-Mobile US Inc TMUS 144.50

Consumer Discretionary

D.R. Horton Inc. DHI 97.55EBay Inc. EBAY 68.01Lululemon Athletica inc. LULU 407.51Restaurant Brands Intl In QSR 66.44

Consumer Staples

Coca-Cola Co KO 56.92Monster Beverage Corp. MNST 93.04

Energy

Enbridge Inc ENB 39.47

Financial

Discover Financial Services DFS 126.01Lazard Ltd. LAZ 47.20Raymond James Financial, Inc. RJF 129.52U.S. Bancorp. USB 55.89

Healthcare

Anthem Inc ANTM 395.29HCA Healthcare Inc HCA 253.51Mckesson Corporation MCK 206.42Silk Road Medical Inc SILK 52.49Zoetis Inc ZTS 204.10

Industrials

General Dynamics Corp. GD 197.32Trane Technologies plc TT 206.56Vontier Corp VNT 32.52

Real Estate

Weyerhaeuser Co. WY 34.54

Technology

Dell Technologies Inc DELL 98.43International Business Machine IBM 144.07KLA Corp. KLAC 346.89Qorvo Inc QRVO 195.18Sanmina Corp SANM 38.17

Utility

American Electric Power Co Inc AEP 89.09

Focus List Stocks in this Report

PRICEAS OF

TICKER 8/4/21

American Electric Power Co Inc AEP $89.09

Anthem Inc ANTM 395.29

General Dynamics Corp. GD 197.32

HCA Healthcare Inc HCA 253.51

KLA Corp. KLAC 346.89

Lazard Ltd. LAZ 47.20

LyondellBasell Industries NV LYB 100.20

Raymond James Financial, Inc. RJF 129.52

Restaurant Brands Intl In QSR 66.44

Sanmina Corp SANM 38.17

Weyerhaeuser Co. WY 34.54

American Electric Power Co Inc (AEP)Publication Date: 7/29/21Current Rating: BUY

HIGHLIGHTS*AEP: Maintaining BUY on strong utility*AEP ranks among the nation's largest generators of

electricity and is well positioned to drive future earnings growth through investments in its regulated businesses and in renewable generation.

*American Electric Power recently reported second-quarter results that exceeded analyst's expectations. Non-GAAP operating earnings came to $590 million or $1.18 per share, up from $534 million or $1.08 per share in 2Q20 and above the consensus estimate of $1.14.

*The company pays a quarterly dividend of $0.74 per share, or $2.96 annually, for a yield of about 3.3%, above the peer average of 3.0%. Over the past five years, the dividend has grown at a compound annual rate of 5.7%. Dividend hikes typically come in the fourth quarter.

*In our view, AEP is an attractive holding for investors seeking the security of regular dividend payments as well as the potential for moderate capital appreciation.

ANALYSIS

INVESTMENT THESISWe are reiterating our BUY rating on Focus List selection

American Electric Power Co. Inc. (NYSE: AEP) with a price target of $102. American Electric Power recently reported second-quarter results that exceeded analyst's expectations. Second-quarter non-GAAP operating earnings of $1.18 per share was solidly up from $1.08 per share in 2Q20, and beat the consensus estimate of $1.14.We expect the companies vertically integrated utilities segment to benefit if American companies continue to embrace a 'hybrid model' in which employees split work time between the home and the office.

Section 2.1

FOCUS LISTThe company is well positioned to drive future earnings

growth through investments in its regulated businesses, with planned transmission investments funded through equity and debt offerings. AEP is also benefiting from recently implemented cost-reduction programs, which, along with favorable rate case decisions, should contribute to stable earnings growth over the next few years. We also like the company's consistent record of dividend growth, with a 5.7% compound annual increase over the last five years. The current yield is about 3.3%, above the peer average of 3.0%.

We also like AEP over the long term, as the company ranks among the nation's largest generators of electricity, with substantial exposure to states with strong population growth, like Texas.

RECENT DEVELOPMENTSAEP shares have underperformed the S&P 500 over the

past three months, with a gain of 2% compared to a gain of 5% for the S&P. Over the past year, the shares have also underperformed, climbing 7% compared to a gain of 36% for the S&P. The shares have underperformed the Utility Sector ETF (IDU) over the last year, but have outperformed over the past 5- and 10-year periods. The stock's beta is 0.26.

American Electric Power recently reported second-quarter results that exceeded analyst's expectations. The company reported second-quarter non-GAAP operating earnings of $590 million or $1.18 per share, up from $534 million or $1.08 per share in 2Q20. Non-GAAP EPS beat the consensus estimate of $1.14. Positive drivers included better rates, higher transmission revenue, and new investment growth. These positives were partially offset by an increase in O&M expense, an increase in depreciation, and unfavorable weather. GAAP EPS increased to $1.16 from $1.05 per share in the prior-year period on roughly the same drivers. Revenue came to $3.8 billion, up 10% from the prior-year-period.

On the 2Q conference call, management reaffirmed its 2021 adjusted EPS guidance of $4.55-$4.75. It also reaffirmed its long-term EPS growth forecast of 5%-7% from a 2019 base.

EARNINGS & GROWTH ANALYSISKey 2Q operating metrics for American Electric Power

are summarized below.

In the Vertically Integrated Utilities segment, total second-quarter KWH sales increased 2.3% year-over-year to 25.8 billion, reflecting a 6.5% decline in residential sales, a 10.1% increase in commercial, an 11.8% increase in industrial, and a 8.9% decrease in wholesale. Segment operating earnings fell 10.9% to $228 million, or $0.45 per share, due to higher O&M, higher depreciation and amortization, and higher taxes. The higher O&M was the result of a true-up during the quarter.

In the Transmission & Distribution segment, operating revenue increased 6.6% to $1.10 billion. Operating EPS increased to $0.31 from $0.29. The results reflected an increase in O&M that was more than offset by lower depreciation and amortization.

Second-quarter earnings in the AEP Transmission Holdco segment rose to $0.34 per share from $0.19 a year earlier due to increased transmission investment.

As the company scales back its nonregulated business, earnings and dividend growth should become more predictable. The company will also be able to use proceeds from the sale of nonregulated assets to strengthen its regulated business and expand its generation of renewable energy. Asset sales have slowed recently, as the generation and marketing segment has retired coal assets and brought renewable assets online. Total MWhs generated in the segment has declined 22% since 2018, as coal generation has been cut in half and renewable generation has increased.

Management has projected capital spending of $37.0 billion through 2025, with substantially all of it earmarked for regulated businesses or contracted renewables.

Turning to our estimates, we are maintaining our 2021 adjusted EPS estimate of $4.74. We are also maintaining our 2022 estimate of $5.05. Our long-term earnings growth rate estimate is 6%.

FINANCIAL STRENGTH & DIVIDENDOur financial strength rating on American Electric Power

is Medium, the middle rank on our five-point scale. The company achieves average to above-average scores on our three main financial strength criteria - debt-to-capital, interest coverage, and profitability. Moody's and S&P rate the company's debt at Baa2 and BBB+, respectively.

At the end of 2Q21, the company had $313 million in cash, down from $393 million at the end of 2020. Total debt stood at $30.7 billion, up from $29.0 billion at the end of 2020. The debt/capital ratio was 59%, above the peer average of 54%. During 2020, EBITDA covered interest expense by a factor of 5.4, above the peer average of 5.1.

The company pays a quarterly dividend of $0.74, or $2.96 annually, for a yield of about 3.4%, above the peer average of 3.0%. Management expects to grow the dividend at a 5%-7% annual rate going forward - the same pace as projected EPS growth. Over the past five years, the dividend has grown at a compound annual rate of 5.7%. Our 2021 dividend estimate is $3.00 and our 2022 estimate is $3.16.

MANAGEMENT & RISKSNicholas Akins is the chairman, president and CEO of

Section 2.2

FOCUS LISTAmerican Electric Power. He is the sixth CEO in the company's 114-year history. He joined AEP in 2000 after his former company, Central and South West Corp., was acquired by AEP. Julie Sloat is the CFO and Lisa Barton is the COO.

Key risks for electric utility stocks include commodity price fluctuations, adverse weather conditions, regulatory issues (especially construction cost recovery), and environmental and safety liabilities. Lastly, the capital-intensive nature of the industry creates ongoing liquidity risk.

COMPANY DESCRIPTIONAmerican Electric Power is a major U.S. electric utility,

delivering electricity to more than 5.5 million customers in 11 states. AEP ranks among the nation's largest generators of electricity. It owns 22,000 megawatts of generating capacity, with an estimated 45% of generating capacity from coal; 24% from nuclear; 18% from natural gas; and 13% from renewables. The company is expanding its use of renewable energy. AEP also owns the nation's largest electricity transmission system, a network of over 40,000 miles.

VALUATIONWe think that AEP shares remain attractively valued at

current prices near $89, above the midpoint of the 52-week range of $75-$94.

The shares trade at 18.8-times our 2021 EPS estimate, below the midpoint of the five-year historical range of 17.0-21.3 and below the peer average of 20.5. AEP also trades at a price/book multiple of 2.1, below the peer average of 2.3. We view AEP as an attractive holding for investors seeking regular dividend payments as well as the potential for moderate capital appreciation. Our target price is $102.

On July 28, BUY-rated AEP traded at $88.99, down $0.40. (Angus Kelleher-Ferguson, 7/28/21)

Anthem Inc (ANTM)Publication Date: 8/4/21Current Rating: BUY

HIGHLIGHTS*ANTM: Raising EPS estimates on continued

outperformance*Anthem continues to benefit from rising enrollments in

its Government segment, rate increases, and the 2019 launch of its in-house pharmacy benefit manager, IngenioRx.

*Management now expects 2021 adjusted EPS of more than $25.50, raised from its earlier guidance of more than $25.10 and representing growth of at least 13%.

*We are boosting our 2021 adjusted EPS estimate to $25.70 from $25.20 and our 2022 estimate to $28.50 from $28.45.

*We believe that ANTM is attractively valued at 15-times our 2021 EPS estimate, below the peer average of 17.

ANALYSIS

INVESTMENT THESISWe are maintaining our BUY rating on Focus List

selection Anthem Inc. (NYSE: ANTM), a leading health insurer. As an independent licensee of the Blue Cross and Blue Shield Association, this well-managed company provides affiliated health and specialty insurance plans for government and commercial clients. While the company continues to face pressure in its Commercial & Specialty business, it has outperformed throughout the pandemic, benefiting from growth in Medicare and Medicaid, rising enrollments in its Government segment, and the launch of its in-house pharmacy benefit manager, IngenioRX. The company has also pursued a number of acquisitions that we believe will bolster its competitive position. As such, with the stock trading at 15-times our 2021 EPS estimate, below the peer average of 17, we view ANTM as attractively valued. Our target price is $435.

RECENT DEVELOPMENTSOver the last three months, ANTM shares have

underperformed, gaining 3% compared to a 5% gain for the S&P 500. However, they have outperformed over the past year, rising 46% compared to a 34% gain for the index. They have also outperformed over the past five years, with a gain of 208% versus a 102% advance for the S&P 500. The beta on ANTM is 1.05, near the average of 1.01 for a peer group that includes CVS, HUM, and UNH.

Anthem has relied in part on acquisitions to drive growth. On June 30, 2021, it completed its acquisition of MMM Holdings, LLC and affiliated companies from InnovaCare Health L.P. With more than 275,000 Medicare Advantage members and over 314,000 Medicaid members, MMM operates Puerto Rico's largest Medicare Advantage plan and is one of the fastest-growing vertically integrated healthcare organizations in the U.S. Financial terms of the transaction were not disclosed. On April 29, Anthem completed its acquisition of myNEXUS Inc., a home-based nursing management company. The company deploys a user-friendly platform that allows healthcare providers to automate the home visit authorization process, speed time to care, and increase provider effectiveness. The platform delivers integrated clinical support services for approximately 1.7 million Medicare Advantage members in 20 states. Financial terms were not disclosed.

The company has also benefited from collaborations with other organizations. On May 19, Anthem announced that through its collaboration with health information company Epic, it would facilitate the secure, bi-directional exchange of health information between healthcare providers and its own affiliated health plans. The increased exchange of health data will also help to streamline administrative processes, such as prior authorizations; enhance care management; and notify

Section 2.3

FOCUS LISTproviders of significant health events.

Anthem has responded to the COVID-19 pandemic by creating digital tools for its members. These include C19 Explorer, which provides dashboards on infection rates and community risk scores to aid in reopening plans; C19 Navigator, which provides Anthem's employer customers with clinical insights and predictions; and Biometric Passport, which allows employers to assess the safety of employees re-entering the workplace without compromising health data privacy. It also includes tools for individuals such as Sydney Care, which provides real-time access to health information, telehealth services, and information on testing locations; ianacare, which allows users to coordinate practical help such as dropping off groceries and picking up medications; and PsychHub, which provides a range of mental health resources for people coping with pandemic-related stress. In addition, the portal includes access to Aunt Bertha, a social care network that helps connect individuals and families to more than 35,000 reduced-cost social services such as food delivery and help with paying bills.

ANTM reported 2Q21 results on July 21 that topped analyst expectations for both earnings and revenue. This was the sixth consecutive quarter of better-than-expected EPS. Adjusted EPS fell to $7.03 from $9.20 in 2Q20, but came in $0.69 ahead of consensus. Total operating revenue rose 14% to $33.3 billion, beating the consensus by $86 million. The increase reflected higher premium revenue due to growth in Medicare and Medicaid, as well as pharmacy product revenue from IngenioRX and rate increases to cover the overall cost trend, but was partially offset by the repeal of the health insurance tax. Medical enrollment totaled 44.3 million members, up 4.5% from 2Q20, driven by growth in the Government segment. The benefit expense ratio rose 890 basis points to 86.8%, reflecting an increase in both non-COVID and COVID-related healthcare costs. The companywide operating margin fell 520 basis points to 6.3%.

Along with the 2Q21 results, management updated its outlook for 2021. It now expects adjusted 2021 EPS of more than $25.50, raised from its earlier guidance of more than $25.10 and representing growth of at least 13%. Management also expects operating revenue of roughly $137 billion, raised from its earlier estimate of $135 billion and representing about 13% growth, and total end-of-year medical enrollment of 44.8-45.3 million, raised from a prior estimate of 44.1-44.7 million.

EARNINGS & GROWTH ANALYSISAnthem provides health insurance for both government

and commercial clients in the following customer groups: National Accounts, Local Groups, Individuals, Medicare Programs, Medicaid, Federal Employee Programs, BlueCard, and Specialty Products.

The company has a record of consistent growth. In 2Q, total revenue rose 16% to $33.9 billion, consisting primarily of operating revenue, as well as contributions from investment income and gains on financial instruments. Premiums, which accounted for roughly 86% of operating revenue, rose 14% to $28.5 billion. Product revenue, which accounted for 9% of operating revenue, rose 20% to $3.0 billion. Administrative fees and other revenue, which accounted for 5%, rose 10% to $1.7 billion. By segment, operating revenue grew 18% to $6.2 billion at IngenioRx, 16% to $20.1 billion in the Government Business, and 9% to $9.6 billion in the Commercial & Specialty business. The operating margin rose 70 basis points to 6.5% at IngenioRx, but fell 730 basis points to 8.3% in the Commercial & Specialty business and 510 basis points to 4.3% in the Government segment.

We are raising our 2021 adjusted EPS estimate to $25.70 from $25.20, reflecting the company's updated guidance, better-than-expected 2Q21 earnings, and continued gains in medical enrollment. Our revised estimate implies full-year earnings growth of 14%. We are also raising our 2022 EPS estimate to $28.50 from $28.45 to reflect the higher EPS base in 2021. Our revised estimate implies growth of 11%.

FINANCIAL STRENGTH & DIVIDENDOur financial strength rating on ANTM is Medium, the

midpoint of our five-point scale. The company receives average marks on our three main financial strength criteria: fixed-cost coverage, debt levels, and profitability.

As of June 30, 2021, Anthem had cash and equivalents of $5.3 billion, down from $5.7 billion at the end of 2020. Total debt rose to $24.2 billion from $20.0 billion, and accounted for 41% of total capital, up from 38% but below the peer average of 47%. We view average levels as 50%-55%. Operating income covered interest expense by a factor of 10.2, down from 16.7 in 2Q20; our view of an average interest coverage ratio is 10-12. The 2Q adjusted profit margin was 5.2%, down from 8.1% in 2Q20. Second-quarter operating cash flow was $1.7 billion, down from $5.5 billion in the prior-year period. Moody's rates the company's debt as Baa2/stable and S&P rates it as A/stable.

Anthem has a share buyback program. During the second quarter, it repurchased 1.3 million shares for $480 million. As of June 30, 2021, it had $5.2 billion remaining on its buyback authorization.

The company pays a dividend. It raised its quarterly payout by 19% in January 2021 to $1.13 per share, or $4.52 annually, for a yield of about 1.2%. Our dividend estimates are $4.52 for 2021 and $5.20 for 2022.

MANAGEMENT & RISKSGail K. Boudreaux has served as the president and CEO

of Anthem since November 2017. She previously served as the

Section 2.4

FOCUS LISTCEO of United Healthcare, a division of UnitedHealth Group, where she increased membership by more than 8 million members in six years. John E. Gallina has served as executive VP and CFO since June 2016. He joined the company in 1994. Prior to becoming CFO, Mr. Gallina served as the senior VP and CFO of the Commercial and Specialty Business Division. Elizabeth E. Tallett is Anthem's chair and has been a member of the board since 2013.

Investors in ANTM shares face risks. The company must accurately predict healthcare costs in order to set appropriate premiums. Its business could also be impacted by changes in funding for Medicare and Medicaid programs, and by other factors that could reduce enrollment. In addition, Anthem faces a range of regulatory, compliance, and legal risks, including ongoing lawsuits. The company also faces risks related to COVID-19.

COMPANY DESCRIPTIONBased in Indianapolis, Anthem is one of the largest health

insurance companies in the U.S. As an independent licensee of the Blue Cross and Blue Shield Association, the company serves members in California, Colorado, Connecticut, Georgia, Indiana, Kentucky, Maine, Missouri, Nevada, New Hampshire, New York, Ohio, Virginia, and Wisconsin, as well as specialty plan members in other states. The company also provides services to the federal government in connection with the Federal Employee Program. The company is a component of the S&P 500 and has 83,400 employees.

INDUSTRYOur rating on the Healthcare sector is Over-Weight.

Consumers are now more willing to spend on lifestyle enhancements along with necessary spending on life-saving treatments. In addition, the survival of the Affordable Care Act has kept the ranks of insured U.S. citizens above the historical average, further increasing consumer spending on healthcare services and products. Meanwhile, companies with experience in diagnostic testing, vaccines, and antiviral medicines, as well as suppliers of protective equipment and other hospital products, should benefit from efforts to contain the coronavirus pandemic.

The sector accounts for 13.0% of the S&P 500, and includes companies in the pharmaceuticals, medical devices, healthcare services, and insurance industries. The sector is underperforming the market thus far in 2021, with a gain of 12.9%. It underperformed in 2020, with a gain of 11.4%, and in 2019, with a gain of 18.7%.

VALUATIONAt current prices near $394, ANTM shares are trading

near the high end of their 52-week range of $244-$406. From a technical standpoint, the stock has performed particularly well since its October 2020 golden cross, when its 50-day moving average rose above its 200-day, rising 45% since that time.

To value the stock on a fundamental basis, we use peer and historical multiple comparisons, as well as a discounted cash flow model. The shares are trading at 15-times our 2021 EPS estimate, in line with the five-year historical average but below the industry average of 17. Given the company's continued outperformance during the pandemic, rising enrollments, new in-house PBM, and regular dividend hikes, we believe that ANTM shares warrant a premium valuation. Our target price of $435 implies a multiple of 17-times our 2021 EPS estimate, in line with the peer average, and a potential gain, including the dividend, of 12% from current levels.

On August 3, BUY-rated ANTM closed at $395.29, up $5.00. (Jasper Hellweg, 8/3/21)

General Dynamics Corp. (GD)Publication Date: 7/30/21Current Rating: BUY

HIGHLIGHTS*GD: Attractive yield and improved growth prospects*General Dynamics recently posted 2Q EPS that topped

consensus expectations, and management raised guidance, as we had expected.

*Management has signaled confidence in the near-term outlook with an 8% dividend increase. The shares yield about 2.5%.

*From a technical standpoint, the shares have reversed a long-term bearish pattern of lower highs and lower lows and are now in a bullish pattern of higher highs and higher lows that dates to October 2020.

*Our 12-month target price is $225.

ANALYSIS

INVESTMENT THESISOur rating on General Dynamics Corp. (NYSE: GD) is

BUY. We are encouraged by the recent progress in the Aerospace segment, as order rates are improving. Over the long term, GD management is focused on driving growth through modest sales increases, margin improvement, and share buybacks. The company also aggressively returns cash to shareholders through increased dividends (most recently with a hike of 8%). From a technical standpoint, the shares have reversed a long-term bearish pattern of lower highs and lower lows and are now in a bullish pattern of higher highs and higher lows that dates to October 2020. Compared to the peer group, GD's multiples are generally below industry averages, which we think offers value. Blending our valuation approaches, we arrive at a price target of $225, or 18-times projected 2022 earnings, closer to the industry average.

RECENT DEVELOPMENTSGD shares have performed in line with market over the

last quarter, gaining 6%. They have underperformed over the past year, with a gain of 32% compared to a gain of 36% for the S&P 500 index. GD has underperformed both the market

Section 2.5

FOCUS LISTand the industry ETF IYJ over the past five-year period. The beta on GD is 1.13.

General Dynamics recently posted 2Q EPS that rose 20% from the prior year and topped consensus expectations. On July 28, the company reported 2Q revenue of $9.2 billion, flat year-over-year. The consolidated operating margin widened by 140 basis points from the prior year to 10.4%. EPS from continuing operations came to $2.61; the consensus was $2.54. For the first half, the company has earned $5.09 per share.

General Dynamics typically provides guidance at the beginning of the year and then updates it at midyear. At the beginning of the year, the company projected 2021 EPS of $11.00-$11.05, essentially flat with 2020. At midyear, the company raised its projected 2021 EPS to $11.50.

EARNINGS & GROWTH ANALYSISGD has four primary business segments: Aerospace (19%

of 2Q revenue), which includes the Gulfstream jet business; Combat Systems (21%), which builds tanks and other land combat equipment; Marine Systems (28%), which builds nuclear-powered submarines and combat-logistics ships; and Technologies (34%), which provides IT services to the Department of Defense and intelligence agencies as well as communications and surveillance services.

All segments posted revenue growth in 2Q, except for Aerospace which fell 18%. Marine Systems (+3%) grew as the U.S. Navy expanded its fleet; Combat Systems rose 8%, with growth in both domestic and international markets; and Technologies grew 3% as new programs ramped up.

The Aerospace segment, which includes Gulfstream business jets, is the one that analysts have been watching closely. Over the past two years, Gulfstream has been transitioning to new aircraft (from the G550 to the G600, the G650 and next year the G700), and, after a manufacturing problem with a supplier, demand was finally starting to build in 4Q19. Then the pandemic struck, reducing deliveries for 2020. But the business now seems poised to return to more consistent growth. The book-to-bill ratio for Gulfstream rose to 2.1 in 2Q21, up from 1.34 in 1Q21, 0.96 in 4Q20, 0.9 in 3Q20, 0.5 in 2Q20, and 1.1 in 1Q20. Management now expects 120 Gulfstream deliveries in 2021, up from its prior forecast of 112-117; first-half deliveries totaled 49.

The total backlog for GD at the end of 2Q was flat with the prior quarter at $89 billion, and the estimated potential contract value (representing management's estimate of the value of unfunded indefinite-delivery, indefinite-quantity (IDIQ) contracts and unexercised options) was $41 billion. At the end of the period, the total potential contract value -- the sum of all backlog components -- was a healthy $130 billion, but down 1.5% year-over-year. Marine Systems is the segment with the largest backlog, including contracts for the

Virginia-class attack submarine and the future Columbia-class ballistic-missile submarine.

On the expense side, the pro forma operating margin was 10.4% in 2Q21, up 140 basis points from the prior year. Margins widened in all four business segments.

Turning to our estimates, based on the improvement in the book-to-bill ratio in Aerospace and growth in the other businesses, we are raising our 2021 adjusted EPS forecast to $11.50 from $11.20. Our estimate is in line with management's guidance, and implies year-over-year growth of 5%. We expect results to improve in 2022, as the new Gulfstream 700 is delivered, and are raising our 2022 EPS forecast to $12.50 from $12.30. Our five-year earnings growth rate forecast is 8%.

FINANCIAL STRENGTH & DIVIDENDOur financial strength rating on General Dynamics is

Medium, the midpoint on our five-point scale. The company receives average scores on our main financial strength criteria: leverage, fixed-cost coverage, cash flow generation, and profitability.

GD had cash and cash equivalents of $3 billion and total debt of $14.3 billion at the end of the quarter. The total debt/capital ratio was 48%. Operating earnings covered interest expense by a factor of 9 last year. In 2020, the cash conversion ratio was a 91%, indicating relatively high-quality earnings.

GD pays a dividend, which it usually raises in 1Q. As expected, it raised the payout by 8% in 1Q21, to $1.19, or $4.76 for the year. We think the dividend is secure and likely to grow, as it has for 24 consecutive years. Our dividend estimates are $4.76 for 2021 and $5.14 for 2022.

GD also uses excess cash to buy back stock.

MANAGEMENT & RISKSPhebe Novakovic has been the chairman and CEO of

General Dynamics since 2013. Ms. Novakovic was formerly the COO. She has also held management roles in GD's Marine Services business and in the planning and development division. Jason Aiken is the CFO.

Investors in GD shares face numerous risks. General Dynamics is a key supplier to the U.S. military (approximately two thirds of sales) and thus vulnerable to debates over, and potential cuts in, domestic and international defense spending. The company is subject to a number of procurement laws and regulations, and evolving U.S. government procurement policies and increased emphasis on cost over performance could adversely affect General Dynamics' business. The Defense industry is competitive, with other deep-pocketed players.

Section 2.6

FOCUS LIST

The shares have been as impacted by the political changes in Washington, D.C. The conventional wisdom is that Defense stocks perform better under Republican administrations.

GD mitigates risks related to U.S. government spending through its strong position in the business jet space and its international business, which accounts for about 20% of revenue. That said, the business jet market is affected by global economic and stock market trends, which are outside of management's control.

COMPANY DESCRIPTIONGeneral Dynamics is a defense contractor with leading

market positions in business aviation and aircraft services, land and amphibious combat systems, mission-critical information systems and technologies, and shipbuilding and marine systems. The company is headquartered in Falls Church, Virginia. GD shares are a component of the S&P 500. The company has 100,000 employees.

VALUATIONWe think that GD shares are attractively valued at current

prices near $197, near the high end of their 52-week range of $129-$199. From a technical standpoint, the shares have recently reversed a long-term bearish pattern of lower highs and lower lows and are now in a bullish pattern of higher highs and higher lows that dates to October 2020.

To value the stock on a fundamental basis, we use peer and historical multiple comparisons, as well as a dividend discount model. GD shares are trading at 16-times projected 2022 earnings, near the midpoint of the historical range of 10-20. On a price/sales basis, the shares are trading at the low end of their five-year range of 1.0-2.2. The dividend yield of about 2.5% is above the S&P 500 yield, signaling value. Compared to the peer group, GD's multiples are generally below industry averages. Blending our valuation approaches, we arrive at our price target of $225, or 18-times projected 2022 earnings, closer to the industry average.

On July 29, BUY-rated GD closed at $198.14, up $2.63. (John Eade, 7/29/21)

HCA Healthcare Inc (HCA)Publication Date: 8/2/21Current Rating: BUY

HIGHLIGHTS*HCA: Raising target to $275*HCA recently reported 2Q21 revenue and earnings that

exceeded consensus expectations - the third straight quarter of better-than-expected results.

*Management noted that coronavirus patients fell from an average of 10% of total admissions in the first quarter of 2021 to about 3% in the second quarter.

*HCA has raised its 2021 guidance. It now expects full-year diluted EPS of $16.30-$17.10, up from its earlier

estimate of $13.30-$14.30 and implying growth of 40%-47%.*We believe that the stock is undervalued at 15-times our

2021 EPS estimate, below the peer average of 17.

ANALYSIS

INVESTMENT THESISWe are maintaining our BUY rating on HCA Healthcare

Inc. (NYSE: HCA), one of the largest hospital companies in the U.S. The company has improved efficiency and lowered costs during the pandemic, which has resulted in higher profit margins. It is also benefiting from vaccine distribution, with COVID-19 patients declining as a percentage of total admissions and renewed growth in outpatient surgeries. Reflecting these positives, management has raised its 2021 guidance.

Given the continued aging of the U.S. population, we like HCA's reach within the healthcare services market and believe that it is well positioned for long-term growth. As such, with the stock trading at 15-times our 2021 estimate, we view HCA as attractively valued. Our revised target price of $275 (raised from $240) implies a projected 2021 P/E of 17, in line with the peer average, and a potential return, including the dividend, of about 11% from current levels.

RECENT DEVELOPMENTSHCA shares have outperformed the market over the past

quarter, rising 22% compared to a gain of 5% for the S&P 500. The shares have also outperformed over the past year, rising 94% compared to a 36% increase for the index. Over the past five years, HCA's 222% return exceeds the 102% increase for the S&P. The beta on HCA is 1.05.

Like many companies, HCA has been affected by the pandemic, although the impact has moderated over the past several months. During the second quarter, COVID-19 patients represented roughly 3% of admissions, down from 10% in the first quarter. (Management has noted that coronavirus patients typically have greater-than-average acuity and a longer length of stay, resulting in above-average revenue per admission.)

HCA has grown in part through acquisitions. On July 1, 2021, the company completed its $400 million purchase of a majority stake in Brookdale Health Care Services from Brookdale Senior Living Inc. HCA now has an 80% stake in Brookdale Health Care Services. HCA is also divesting certain assets. On May 13, it announced plans to sell the Redmond Regional Medical Center, a hospital in north Georgia, to AdventHealth for $635 million. On May 3, it also announced that it would sell four hospitals in Georgia to Piedmont Healthcare for $950 million. These hospitals are not located in HCA's core geographic markets. The sales will give the company greater financial flexibility and provide resources that can be used for new acquisitions. Both transactions are expected to close in 3Q21.

Section 2.7

FOCUS LISTHCA recently reported 2Q21 revenue and earnings that

exceeded consensus expectations - the third straight quarter of better-than-expected results. On July 20, HCA reported 2Q21 diluted EPS of $4.37, up from $3.23 in 2Q20 and $1.21 above consensus. Revenue rose 30% to $14.4 billion, beating the consensus by $823 million, while adjusted EBITDA rose 21% to $3.2 billion. The adjusted EBITDA margin was 22.3%, down from 24.1% in the prior-year period. The profit margin rose to 10.0% from 9.8%. The diluted share count fell nearly 3% from the prior year to 333 million.

Along with the 2Q results, management updated its 2021 guidance. It now expects revenue of $57.0-$58.0 billion, raised from its earlier estimate of $54.0-$55.5 billion and representing growth of 11%-13%; adjusted EBITDA of $12.1-$12.5 billion, raised from $10.85-$11.35 billion and representing growth of 21%-25%; and diluted EPS of $16.30-$17.10, raised from $13.30-$14.30 and representing growth of 40%-47%.

EARNINGS & GROWTH ANALYSISHCA posted growth across all operating metrics in 2Q. On

a reported basis, admissions rose 18%, equivalent admissions rose 27%, revenue per equivalent admission rose 3%, inpatient revenue per admission increased 3%, inpatient surgeries rose 15%, outpatient surgeries rose 53%, and emergency room visits rose 40%. On a same-facility basis, admissions rose 18%, equivalent admissions rose 27%, revenue per equivalent admission rose 3%, inpatient revenue per admission increased 2%, inpatient surgeries rose 15%, outpatient surgeries rose 53%, and emergency room visits rose 41%.

Turning to our estimates, based on the company's strong 2Q results and management's revised guidance, we are raising our 2021 EPS estimate to $16.30 from $14.00, implying growth of 43% for the year. We are also raising our 2022 EPS estimate to $17.25 from $15.20. The revision reflects the higher projected earnings base in 2021 and implies growth of 6% from our 2021 estimate.

FINANCIAL STRENGTH & DIVIDENDOur financial strength rating on HCA Healthcare is

Medium, the midpoint on our five-point scale. At the end of 2Q21, HCA had cash and equivalents of $1.1 billion, down from $1.8 billion at the end of 2020. Total debt was $34.3 billion, up from $32.7 billion. Debt rose to 95% of total capital from 92%, remaining well above the peer average of 64%. Second-quarter income before taxes of $2.1 billion was up 36% and covered interest expense by a factor of 5.5, up from 4.0 in 2Q20. Operating cash flow fell to $2.2 billion from $8.7 billion in 2Q20, although we note that the 2Q20 results included $822 million of government stimulus income and $5.0 billion of contract liabilities-deferred revenue. Moody's withdrew its rating on the company's debt on June 24, 2021. Standard & Poor's rates the debt as BB+/positive, raised from BB+/stable on July 29, 2021.

HCA pays a dividend, which it reinstated in 4Q20 after suspending payments in 2Q20 due to the pandemic. The quarterly dividend of $0.48 per share, or $1.92 annually, yields about 0.8%. Our dividend estimates are $1.92 for 2021 and $2.10 for 2022.

The company has a stock repurchase program, which it reinstated with its 4Q20 results after suspending buybacks in March 2020. During the second quarter of 2021, HCA repurchased 11.261 million shares of common stock for roughly $2.3 billion. As of June 30, 2021, it had $5.0 billion remaining on its repurchase authorization.

MANAGEMENT & RISKSSamuel N. Hazen became HCA's CEO on January 1, 2019

following the retirement of former chairman and CEO R. Milton Johnson. Mr. Hazen previously served as HCA's president and COO, and has worked at the company for almost 37 years.

Thomas F Frist III is the company's chairman. Mr. Frist is the son of HCA founder Thomas Frist, Jr. and has served on the board since 2006.

HCA investors face risks related to the company's high leverage, with a debt/cap ratio above 90%. They also face risks related to intense competition, currency headwinds, and regulatory changes in the healthcare industry. The company also faces risks related to the COVID-19 pandemic, including volumes declines, and potential liquidity issues.

COMPANY DESCRIPTIONHCA Healthcare (formerly HCA Holdings) is one of the

largest hospital companies in the U.S. The company operates 187 hospitals and 122 freestanding surgery centers and provides extensive outpatient and ancillary services. It operates hospitals in 21 U.S. states, as well as in the UK; its largest presence is in Florida and Texas. HCA is a component of the S&P 500.

VALUATIONHCA shares have performed particularly well since the

coronavirus selloff in March 2020, more than quadrupling since that time. The shares also achieved a golden cross in September 2020, as the 50-day moving average rose above the 200-day. Since then, the stock has gained more than 80%.

HCA shares appear attractively valued at 15-times our 2021 EPS estimate, below the peer average of 17. We think that higher multiples are warranted given the company's strong 2Q results, renewed dividend payments and stock repurchases, and positive 2021 outlook. Our revised target price is $275.

On July 30, BUY-rated HCA closed at $248.20, up $0.30. (Jasper Hellweg, 7/30/21)

Section 2.8

FOCUS LIST

KLA Corp. (KLAC)Publication Date: 8/2/21Current Rating: BUY

HIGHLIGHTS*KLAC: Solid quarterly performance, further growth

ahead*KLA Corp. topped fiscal 4Q21 consensus expectations

and reported strong double-digit year-over-year growth in sales and non-GAAP EPS.

*KLA saw continued strength in foundry and logic demand in the quarter. Memory demand also continues to improve as data storage customers meet rising end-user demand.

*KLA has announced a 17% increase in its quarterly dividend, to $1.05 per common share from a prior $0.90. KLA's board has also authorized a new $2 billion share-repurchase program.

*With demand strengthening and now exceeding pre-pandemic production levels in many markets, KLAC shares appear attractive at current levels.

ANALYSIS

INVESTMENT THESISBUY-rated KLA Corp. (NGS: KLAC), formerly

KLA-Tencor, rallied by 9% in a declining market on 7/30/21 after besting consensus expectations and reported strong year-over-year growth in fiscal 4Q21 sales and non-GAAP EPS. Non-GAAP EPS rose more than 60% annually while exceeding consensus expectations by $0.43.

The company has meaningfully stepped up its shareholder return program. KLA has announced a 17% increase in its quarterly dividend, to $1.05 per common share from a prior $0.90. KLA's board has also authorized a new $2 billion share-repurchase program. Despite the dynamic environment and growth investing, the company has consistently returned value to shareholders.

KLA saw continued strength in foundry and logic demand in the quarter. Memory demand also continues to improve as data storage customers meet rising end-user demand. The company continues to build on its industry leading market share in process control and metrology.

KLA's newer products continue to drive momentum in the market place. Service revenue is rising as a percentage of sales, reflecting past growth in the installed base, and the EPC business is addressing fast-growing new markets in the electronics value chain.

KLA provided above-consensus guidance for fiscal 1Q22. Semiconductor capital equipment stocks are relatively outperforming in response to urgent need for new semiconductor fab capacity amid worldwide semiconductor shortages. The group is also rallying on prospects for ongoing

infrastructure investment and potentially more favorable trade relations.

With demand strengthening and now exceeding pre-pandemic production levels in many markets, KLAC shares appear attractive at current levels. For the long-term investor, KLAC appears particularly attractive based on our discounted free cash flow model. We are reiterating our BUY rating on KLAC and 12-month target price of $390, raised from $360.

RECENT DEVELOPMENTSKLAC is up 35% in 2021, and peers are up 35%. KLAC

appreciated 45% in 2020, while the WFE peer-group advanced 49%. KLAC rose 99% in 2019, slightly below the 100% WFE peer-group gain and ahead of the 54% gain for Argus-covered semiconductor companies. KLAC shares declined 15% in 2018, compared to a 25% decline for the peer group of Argus-covered semiconductor capital equipment companies; the peer group includes Applied Materials and Lam Research. KLAC rose 37% in 2018, trailing gains of 56% for the peer group, while tracking the 38% gain in the Philadelphia Semiconductor index. KLAC advanced 13% in 2016.

For fiscal 4Q21 (calendar 2Q21), KLA Corp. posted revenue of $1.92 billion, which was up 32% annually and 7% sequentially; the Orbotech acquisition is now fully anniversaried. Revenue was toward the high end of management's wide guidance range of $1.76-$1.96 billion and above the consensus forecast of $1.87 billion. Non-GAAP EPS of $4.43 rose 63% year-over-year and $0.58 sequentially. Non-GAAP EPS exceeded the high end of management's wide $3.47-$4.35 guidance range and the $4.00 consensus call.

CEO Rick Wallace noted that the June 2021 quarter continued recent momentum and strength for KLA. The company more than met its top- and bottom-line goals and 'progressed against its long-term strategic objectives.' KLA is seeing increased customer demand across each of its major product groups.

Highlights in the quarter included continued strength and breadth in foundry & logic, and continuing improvement in memory demand; growing market share in process control; and a rising contribution from services revenue. Secular demand trends continue to shape multiple markets, fueled by the accelerating digitization of end markets and industries.

KLA is also seeing a heightened focus on the strategic nature of customers' investments as they seek to maximize leading-edge development, optimize facilities utilization and respond to regional trends. Process control intensity is building, and KLA is retaining its market leadership in the areas of metrology and inspection where its market share is four-times that of its nearest competitor.

Section 2.9

FOCUS LISTIncreasingly, semiconductor capital equipment companies

are seeking to harness the power of AI to make metrology and inspection more efficient. While rival introduced AI-based metrology solutions in spring 2021, KLA introduced metrology & inspection systems utilizing AI more than a year ago. In July 2020, KLA introduced its eSL10 e-beam patterned-wafer defect inspection system that employs deep leaning algorithms. According to recent industry data from Gartner, the total optical inspection market in 2020 grew at double the rate of the overall WFE market, and KLA believes it gained several points of market share.

Key drivers in the current environment include data center, 5G infrastructure and smartphone growth, and client (PC) products to support remote work & learn, virtual collaboration, entertainment & gaming, and other aspects of the remote and/or hybrid lifestyle. These digital transformations in turn are accelerating next generation technologies including high performance computing, AI and accelerated migration to the cloud.

KLA now has four reportable segments. Semiconductor process controls (SPC) revenue of $1.58 billion (83% of total) increased 37% annually and 5% sequentially. KLA is now reporting foundry & logic as one category, to mute any 'noise' related to brief shifts in customer demand; this also aligns with peer-group reporting.

Within SPC, Foundry & Logic shipments (68% of total) rose 55% annually. Memory revenue (32% of SPC total) was up 9% year-over-year and 8% sequentially. Given a multitude of end-use demand drivers, the memory business can quickly pivot from fast growth to inventory digestion at customers with a few quarters. Within memory, according to CFO Bren Higgins, the split remains approximately 55% NAND and 45% DRAM.

On a product basis for 4Q21, the core business of wafer inspection (38% of revenue) was up 51% annually and 3% quarter-over-quarter. Patterning revenue (22% of total) increased 39% annually and 7% sequentially.

Services (23% of total) grew 16% year-over-year and 4% quarter-over-quarter. Among the other reportable segments, Specialty Semiconductor Processes revenue (4% of total) dipped 1% year-over-year. PCB, display and content inspection (10% of total) surged 26% annually and a more than seasonally strong 30% sequentially.

On a regional basis, traditional WFE top customer Korea (13% of revenue) dipped 18% after growing 87% annually in 3Q21; 4Q21 featured seasonal weakness after the Samsung and LG seasonal smartphone launches. Another traditional giant, Taiwan (28% of total), grew 42%, reflecting strength at TSMC. New powerhouse China (32% of revenue) delivered 62% growth, after two straight weak quarters. The U.S., at

11% of the total, was up 32% annually. The U.S. has been among the fastest-growing end markets for KLA over the past year. We believe cloud data center recovery and the new iPhone cycle are driving domestic growth.

China has been the strongest regional market for WFE companies in recent years. In December 2020, the U.S. Justice Department added China's chip production giant Semiconductor Manufacturing International Corp. (SMIC) to the entities list. Anticipation of that designation likely drove a pull-forward in semiconductor capital equipment sales to SMIC and other Chinese companies. Among the three semiconductor capital equipment companies in Argus coverage, KLA has the least Chinese exposure.

For calendar 2021, KLA now expects industry growth in the mid-to-high 30% range, up from the earlier mid-to-high 20% forecast, off a $61 billion base for calendar 2020. Amid strength across all major SPC end markets, KLA expects the best demand growth to come from memory.

Based on KLA's backlog and sales funnel visibility, KLA sees 'sustainable' demand across the calendar year. With demand strengthening and KLA back to pre-pandemic production levels in many markets, KLAC shares appear attractive at current levels. For the long-term investor, KLAC appears particularly attractive based on our discounted free cash flow model.

EARNINGS & GROWTH ANALYSISFor fiscal 4Q21 (calendar 2Q21), KLA Corp. posted

revenue of $1.92 billion, which was up 32% annually and 7% sequentially; the Orbotech acquisition is now fully anniversaried. Revenue was toward the high end of management's wide guidance range of $1.76-$1.96 billion and above the consensus forecast of $1.87 billion.

The non-GAAP gross margin tightened sequentially to 62.0% in 4Q21 from 62.9% in 3Q21 but edged up from 60.3% a year earlier. The non-GAAP operating margin was sequentially lower at 40.2% in 4Q21 from 40.8% in 3Q21 but was up meaningfully from 35.5% a year earlier.

Non-GAAP EPS of $4.43 rose 63% year-over-year and $0.58 sequentially. Non-GAAP EPS exceeded the high end of management's wide $3.47-$4.35 guidance range and the $4.00 consensus call.

For all of the June 2021 fiscal year, revenue of $6.9 billion increased 24%, from $5.81 billion for FY20. Non-GAAP EPS of $14.56 rose 41% from $10.35 in FY20.

For fiscal 1Q22, KLA projected revenue of $1.92-$2.12 billion, which at the $2.02 billion midpoint would be up 31% annually and 5% sequentially. KLA also projected non-GAAP EPS of $4.01-$4.89; at the $4.45 midpoint, EPS would be up

Section 2.10

FOCUS LISTmore than 45% annually. Midpoint guidance for 4Q21 topped the $1.91 billion revenue consensus and the $4.14 non-GAAP EPS consensus.

We are boosting our fiscal 2022 non-GAAP EPS forecast to $17.64 per diluted share from $16.16. We are implementing a FY23 non-GAAP EPS projection of $19.09. Our five-year earnings growth rate forecast is 11%.

FINANCIAL STRENGTH & DIVIDENDOur financial strength rating for KLAC is Medium-High.

The company has strengthened its shareholder return policies and is an active repurchaser of its stock.

Cash & investments were $2.50 billion at the end of fiscal 2021. Cash was $1.63 billion at the end of FY20, $1.74 billion at the end of FY19 (following the Orbotech deal), $3.06 billion at the end of FY18, $3.02 billion at the end of FY17, and $2.49 billion at the end of FY16.

Debt was $3.44 billion at the close of fiscal 2021. Debt was $3.44 billion at the close of FY20, $3.42 billion at the close of FY19, $2.77 billion at the end of FY18, $2.68 billion at the end of FY17, and $3.06 billion at the end of FY16.

Cash flow from operations was $2.19 billion in FY21. Cash flow from operations was $1.78 billion in FY20, $1.15 billion in FY19, $1.23 billion in FY18, $1.08 billion in FY17, and $760 million in FY16.

In July 2021, KLA raised its quarterly dividend by 17%, to $1.05 per share. In August 2020, KLA in 2020 raised its quarterly dividend by $0.05, to $0.90 per share. In September 2019, KLA raised its quarterly dividend by 13%, to $0.85 per share; and in June 2018, it raised its quarterly dividend by 27% to $0.75 per share. Those increases follow a 9.3% hike to $0.59 per share in September 2017. In late December 2014, KLAC declared a special cash dividend of $16.50 per share. Excluding the special dividend, KLA has grown its dividend at a 15% compound annual rate since 2007.

Our dividend estimates are $3.80 for FY22 and $4.00 for FY23.

MANAGEMENT & RISKSCEO Rick Wallace has been with KLAC for 29 years,

starting as an applications engineer in 1998 and subsequently serving in several management positions. Bren Higgins has been CFO since 2013. He joined KLAC in 1999 and was previously division controller and VP of Corporate Finance. Ahmad Khan is EVP of Global Products; as head of process controls, he may be in line to be the next CEO.

A main risk for KLA Corp., as for other semiconductor capital equipment companies, is the possibility of a general economic downturn and a corresponding dip in semiconductor

production related to the COVID-19 pandemic. We believe that KLAC has the financial strength, market leadership, and growth characteristics to weather this storm and emerge a stronger player. We also believe the pandemic could drive a permanent increase in the percentage of hours worked away from the office. That should drive long-term demand for semiconductors that power connected devices used in remote applications and in the home. Finally, KLA's process controls business has proved more stable than other WFE niches during prior economic downturns.

The now completed acquisition of Orbotech carries numerous risks, including potential misalignment in corporate culture, and participation in weak-return industries. However, we believe that the deal makes strategic sense as it positions KLA-Tencor in adjacent industries within the electronics supply chain, with limited to no overlap in geography, customers, or product categories. We also believe the acquisition was reasonably priced.

KLAC is subject to the usual risks of cyclicality in the semiconductor-equipment industry. As revenues slow, margins also typically suffer, leading to sharp declines in earnings. Industry downturns may be precipitated by economic recessions, and may also be affected by changes in demand for consumer products (mobile phones, tablets, and PCs), as well as for data center communications systems, and industrial uses.

Similarly, the company must be ready with new products when the next cyclical upturn arrives - if new semiconductor equipment arrives too soon before the upturn, it may be viewed as out-of-date when semiconductor sales accelerate; if it arrives too late, it may result in the loss of equipment sales to competitors.

The company also faces customer-concentration risk, as it relies on a small number of large customers with significant bargaining power. KLAC also faces risks from regulation and unfavorable currency translation, as well as from the debt incurred to support capital expenditures and acquisitions. Like its peers, it also faces the challenge of attracting top technical talent.

COMPANY DESCRIPTIONKLA Corp. is a leading supplier of process-control and

yield-management solutions for the semiconductor and related nanoelectronics industries. The company's tools help integrated circuit manufacturers manage yield throughout the semiconductor manufacturing process. KLA provides chip and wafer manufacturing products, including defect inspection and review, metrology solutions, lithography software, and other offerings. In addition, KLA provides power device, LED, micromechanical systems, and other products for the display market. KLA Corp. was formerly known as KLA-Tencor Corp. and changed its name in July 2019.

Section 2.11

FOCUS LIST

VALUATIONKLAC shares trade at 19.7-times our FY22 non-GAAP

EPS forecast and at 18.1-times our FY23 projection; the two-year average forward P/E of 18.9 is above the five-year (FY16-FY20) trailing multiple of 14.6. The shares, which have historically traded at a 25% discount to the market multiple, currently trade at a two-year forward relative P/E of 0.85, or at a 15% discount to the market multiple. Other historical comparables signal undervaluation; our price-based historical comparable valuation points to a value in the mid-$260s, in a stable to rising trend though below current prices.

KLAC trades at a modest premium to peers on price/sales, and in line with peers on absolute and relative P/E and EV/EBITDA; KLAC has historically commanded premiums to its peer group. Peer indicated value is around $335, in a rising trend and close to current prices. Our discounted free cash flow analysis values the stock above $550, in a rising trend and well above current prices.

Our blended valuation estimate exceeds $440, in a rising trend. Appreciation to our 12-month target price of $390 (raised from $360), along with the 1.0% annual yield, implies a risk-adjusted return in excess of our total forecast return for the broad market and is thus consistent with a BUY rating.

On July 30, BUY-rated KLAC closed at $348.16, up $28.73. (Jim Kelleher, CFA, 7/30/21)

Lazard Ltd. (LAZ)Publication Date: 8/2/21Current Rating: BUY

HIGHLIGHTS*LAZ: Raising target to $54 following 1Q results*On July 30, Lazard reported adjusted 2Q21 earnings of

$1.28 per share, up from $0.66 a year earlier and well above the consensus of $0.88.

*Revenue rose 51%, with a 61% increase in financial advisory revenue and a 40% gain in asset management fees.

*Business confidence continues to improve, and we expect ongoing good demand for Lazard's experience in capital structure, capital raising, debt negotiations and restructuring.

*Our target price of $54 implies a multiple of 12-times our upwardly revised EPS estimate for 2021.

ANALYSIS

INVESTMENT THESISWe are reiterating our BUY rating on Lazard Ltd. (NYSE:

LAZ) with a target price of $54 following the company's 2Q earnings report. Revenues were up sharply, driven by strong growth in both financial advisory and asset management fees.

Business confidence has improved markedly in recent quarters, and we continue to see good demand for Lazard's experience in capital structure, capital raising, debt

negotiations and restructuring.

In our view, Lazard remains a compelling secular growth story with a clean balance sheet and a focused business model.

We see room for P/E multiple expansion as operating margins and market share increase. Our target price of $54 implies a multiple of 12-times our revised 2021 EPS estimate. The dividend also yields a generous 4.1%.

RECENT DEVELOPMENTSLAZ shares are up 60% over the past year, compared to a

35% advance for the broad market.

On July 30, Lazard reported adjusted 2Q21 earnings of $1.28 per share, up from $0.66 a year earlier and well above the consensus of $0.88. Revenue rose 51% to $821 million, with a 61% increase in financial advisory revenue and a 40% gain in asset management fees. Adjusted net income was up 94% to $146 million.

Increased M&A and restructuring activity helped the financial advisory segment, while a 32% rise in average AUM (to $276 billion) benefited the asset management segment.

EARNINGS & GROWTH ANALYSISBusiness confidence continues to improve along with

vaccinations and the re-opening of world economies. Accordingly, we continue to see good demand for Lazard's experience in capital structure, capital raising, debt negotiations and restructuring - as companies work to strengthen their financial and operational efficiency. Management continues to note that confidence in the future and low interest rates is resulting in constructive M&A discussions. We believe that Lazard's broad and deep coverage - by geography and industry - distinguishes it from boutiques, while its focus on advisory distinguishes it from large banks. We now look for a 17% rise in revenues in 2021, up from a previous 9% following a very strong 2Q.

In the asset management business, average AUM declined 4% in 2020, hurt by a sharp fall in the second quarter during the height of the coronavirus pandemic. However, a healthy rebound in asset values since then has boosted management fees, and we expect new strategies and product extensions to further aid the segment.

Compensation was 59.5% of revenue in 2020, up from 57.5% a year earlier. The company expects to achieve a compensation ratio in the mid- to high 50s on both an awarded and an adjusted basis. Noncompensation expense was only 17.1% of revenue in 2020, down from 19.6% a year earlier, aided by lower business development and travel costs; the company's goal is to keep this ratio between 16% and 20%.

Given continued improvement in AUM and the M&A

Section 2.12