Embed Size (px)

Citation preview

Paper to be presented at the DIME-DRUID ACADEMY Winter Conference 2011

on

Comwell Rebild Bakker, Aalborg, Denmark, January 20 - 22, 2011

THE LINK BETWEEN CORPORATE PHILANTHROPY AND PRODUCT FAILURE

Borbala KulcsarPhD Candidate (2009-2012) Department of Business Administrat

Andrea FosfuriDepartment of Business Administration - Universidad Carlos I

Marco GiarratanaDepartment of Business Administration - Universidad Carlos I

Abstract:Title: The Link between Corporate Philanthropy and Product FailureName: Borbála KulcsárAffiliation: PhD Candidate, Universidad Carlos III de MadridYear of enrolment: 2009Expected final date: 2012E-mail address: [email protected]

In the last two decades firms have increasingly invested in philanthropic activities (CECP, 2008: McKinsey Quarterly, 2008), however the real aim and motivationto engage in such actions remained unclear. Previous research is characterized by the lack of a consistent theoretical grounding (Margolis & Walsh, 2003: Garriga &Melé, 2004) and inconsistent empirical findings of the identification of tangible and intangible benefits of social investments (Orlitzky et al., 2003: Margolis et al.,2007). Recently Godfrey (2005) tackled this issue and suggested that corporate philanthropy creates among the stakeholder groups of the firm a moral capital. Thismoral capital will act as insurance for shareholders by protecting the firms intangible assets and so contribute to shareholder wealth (Godfrey, 2005: 778). FollowingGodfrey s theoretical foundation we aim to provide empirical evidence on this conceptualization and fill an important research gap in the existing literature. Wehypothesize that the higher the contribution to charitable giving of a firm, the less product failure it will suffer. We base this relationship on the moral capital andincreased reputation of the firm that charitable giving creates among customers. Through this fairness perception (Xia et al., 2004) customers will become more toleranttoward responsible firms and their products which in turn will prevent product failure. Our main variable, product failure, is measured by failed trademarks obtainedfrom the USPTO database, whereas we use data from the KLD STAT database community dataset for our independent variable, charitable giving. Furthermore weincluded a set of control variables from the COMPUSTAT database. Our panel dataset covers a nine year period from 2000 to 2008. We selected our firm samplefrom the S&P 500, including in total 173 firms with 1557 firm year observation. To analyze our hypothesis empirically, we used the negative binomial regressionmethod. Our results are consistent with our hypothesis where we observe firms with higher charitable contribution to suffer less product failure indicating a crucialrole of corporate philanthropy in firm decisions.

JEL - codes: M14, L14, D21

1

The Link Between Corporate Philanthropy and Product Failure

Borbála Kulcsár1, Andrea Fosfuri

1 and Marco S. Giarratana

1

1 Universidad Carlos III de Madrid, Getafe (Madrid), Spain

[email protected], [email protected], [email protected]

Abstract - In the last two decades firms have increasingly invested in philanthropic

activities, however the real aim and motivation to engage in such actions remained unclear.

A recent theoretical research by Godfrey (2005) suggested that corporate philanthropy

creates moral capital and act as insurance for the firm by building a strong relationship with

stakeholder groups. We aim to provide empirical evidence on this conceptualization and

hypothesize that the higher the contribution to charitable giving of a firm, the less product

failure it will suffer, moreover that this relation will be more visible in industries focusing

primarily on individual consumers. Selecting our firm sample from the S&P 500 and using

data from the USPTO and KLD databases, we find significant results confirming partially

our hypotheses.

2

I. Introduction

To build and maintain a valuable corporate identity is a critical issue for firms. A good

image associated with well defined values and principles can provide several benefits to the

firm. It can nurture an overall good reputation; strengthen stakeholder relationship and

increase firm performance (Fombrun, 1996). To achieve and maintain a valuable corporate

identity firms often engage in philanthropic actions. A recent example is the large U.S.

company PepsiCo, which invested 4,1 million dollars over the past three years through its

foundation to the Waterpartner‟s Water Credit program to help and solve the worlds water

and sanitary problems as part of the Global Water Challenge. The Global Water Challenge

is a coalition of 24 leading companies in the world, such as Coca-Cola, Dow-Chemicals

and Procter & Gamble among others, donating for the same cause in collaboration with

foundations, NGOs and research organizations (CECP1, 2009).

We consider and examine corporate philanthropy as part of a larger mechanism of

corporate social responsibility (Carroll, 1999; Godfrey, 2005; Wang et al., 2008). Social

responsibility of corporations is defined2 as “the continuing commitment by business to

behave ethically and contribute to economic development while improving the quality of

life of the workforce and their families as well as the local community and society at large.”

Carroll (1999: 289) in his article described corporate philanthropy as a component of

corporate social responsibility as following: “For CSR to be accepted by the conscientious

business person, it should be framed in such a way that the entire range of business

responsibilities constitute total CSR: economic, legal, ethical and philanthropic.

Furthermore, these components of CSR might be depicted as a pyramid. To be sure all of

these kinds of responsibilities existed to some extent but it has only been in recent years

that ethical and philanthropic functions have taken a significant place.”

Previous theoretical (Margolis and Walsh, 2003; Garriga and Melé 2004; Porter and

Kramer, 2002; Donaldson and Dunfee 1994) and empirical research (Carroll et al., 1987,

Burke and Logsdon, 1996; Waddock and Graves 1997; Hillman and Keim 2001; Orlitzky

1 CECP Committee Encouraging Corporate Philanthropy, The Corporate Philanthropist 2009/2010 spring/summer

edition.

2 World Business Council for Sustainable Development, 2000.

3

et al. 2003) on corporate philanthropy is exhaustive, however somewhat ambiguous in the

results. Researchers analyze the social-business link from different viewpoints and disagree

on the real aim of philanthropic activities (Garriga and Melé 2004; Margolis and Walsh,

2003). Researchers argue that different findings in empirical research are primarily due to

the lack of a common theoretical grounding which would serve as a base to further research

and explain the motivation of firms to engage in social and philanthropic actions.

A recent work by Godfrey (2005) tackles this issue and emphasizes moral capital

building as a crucial element of corporate philanthropy. As Godfrey theorizes in his work,

corporate philanthropy in general creates positive moral capital among stakeholder groups.

This moral capital will act as insurance-like protection for the firm to preserve relational

based intangible assets, moreover it will increase shareholder wealth (2005: 777). As also

Fombrun and Shanley (1990) observed, firms which engage in philanthropic actions have

higher reputational value to consumers than other firms. When making product choices

consumers will trust more firms which invest in philanthropic actions through increased

reputational value than compared to other firms. We aim to provide empirical evidence

about this theoretical concept. We analyze the relationship between corporate philanthropic

actions and product failure.

Although firms spend significant amounts of resources on new product development

process and study the market conditions, the failure rate after new product introduction still

lies between 40-90% (Gourville, 2005). Therefore it is important to study this phenomenon

not only to increase product success but also to strategically consider corporate

philanthropy as an efficient tool to strengthen firm image. To represent this relationship we

hypothesize that firms which are highly involved in charitable giving, a well known form of

corporate philanthropy, will experience less product failure. Moreover that this relation will

be stronger for firms which are focusing on individual consumers, than for those firms

which are primarily targeting business entities as their focal consumers. These hypotheses

are explained through positive moral capital building which will influence customers

purchase decisions (Godfrey, 2005). We argue that those firms which are consciously

“doing good” and emphasize social and philanthropic actions can overcome critical

situations, by “insuring” themselves with a strong philanthropic involvement. These actions

4

will enhance reputation and will influence consumer‟s product choice to avoid product

failure. We study this phenomenon by observing the philanthropic actions of the largest

U.S. firms (S&P 500) using the KLD database and their product failures represented by

failed trademarks from the USPTO covering a nine year period, between 2000 and 2008.

We analyze our hypotheses through accessing the negative binomial regression model. Our

results partially confirm our hypotheses. We found evidence about increasing philanthropic

actions reducing the product failure of the firms. However our results show no support of

this relationship being stronger for firms targeting individual consumers.

In the following sections we will further analyze this connection between corporate

philanthropy and product failure and give further insight into our theoretical foundation and

empirical findings.

II. Corporate Philanthropy

Philanthropy defined by the Financial Accounting Standards Board (1993) is “an

unconditional transfer of cash or other assets to an entity or a settlement or cancellation of

its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an

owner.” As a part of corporate philanthropy, charitable giving is considered to be one of the

most important tools of firm contributions, which by definition is “an active effort to

promote human welfare in form of cash or non-cash related corporate donation to non-

profit organizations from firm profits or resources” (Merriam-Webster dictionary).

The history of corporate charitable giving originated in the 19th

century. From this time

until the beginning of the 20th

century firms mainly focused on the well-being of their

employees and their communities (Trost, 2006). Since then corporate giving has evolved

and gained territory involving all the stakeholder groups of the firm. With the economic

crisis in 2008 a slight decrease could be observed in the rate of corporate giving which

nowadays starts to rise again. Firms have recently increased their investments in

philanthropic actions and plan to further globalize them in the future (CECP, 2009).

5

When firms are engaging in different philanthropic actions they are likely to emphasize

them publicly. For instance the CECP3 is organizing yearly the International Corporate

Philanthropy Day, to promote firms philanthropic actions, give information about their

previous philanthropic involvements and experiences benefiting from the added media

interest to enhance future actions. However, as we can observe philanthropic actions of the

firms are often publicized, about the real aim and motivation behind these actions we know

little. Carroll (1999) examined in his work the aim of the corporation to engage in social

and philanthropic actions since the 1950s. The author argued that it was then when large

firms started to implement and act socially conscious in their decision making processes,

realizing the importance of the society as an important factor in the functioning of the

corporation on the long run. Carroll (1999) identified the different sources of motivations of

the firms to engage in such actions as economic, legal, ethical and philanthropic in nature.

To further examine the motivations of the firms, Garriga and Melé (2004) conducted an

extensive overview of the theoretical research on firm social involvement and made a

categorization. Firstly, the authors mentioned those studies which identify profit

maximization as the only obligation of the corporation towards the society. Pursuant to this

observation, a study by Porter and Kramer (2002) pointed out the importance of strategic

assessment of philanthropic actions into the firm‟s core capabilities in which philanthropy

is an instrument to achieve the ultimate goal of profit maximization by improving the

competitive context of the firm, fostering collaboration and influencing local market

features. Their premise emphasizes competitive advantage through the alignment of

philanthropic and business activities. Fostering the idea of strategic philanthropy, O`Brian

(2001) developed the Socially Anchored Competencies model (SAC). The model

demonstrates how business and social benefits can be achieved by merging the core

competencies and social objectives of the firm fitting with stakeholder interests. An

additional dimension of the model describes the possibility of creating strategic alliances

with non-profit organizations to foster and implement adequate social projects. Other form

to promote corporate philanthropy as a tool to enhance corporate performance is cause-

related marketing (Varadarajan and Menon, 1988). Through advertising customers are

3 CECP: Committee Encouraging Corporate Philanthropy

6

attracted to make donations related to purchase. Following the categorization of Garriga

and Melé (2004), the work of Donaldson and Dunfee (1994) argued the importance of the

politically correct assessment of social actions and developed the Integrative Social

Contract Theory (ISCT). The model focuses on the wider context of a business situation,

including cultural, social and institutional differences and argues that a macro social

contract involving higher rules provide the base for any social engagement framed by

institutions and by the moral consent of the participants. The third category of theoretical

studies on corporate philanthropy identified by Garriga and Melé (2004) considered that

social claims coming from different stakeholder groups of the firm must be integrated into

the business. Freeman (1984:39) identified first the stakeholder groups of the firm and

defined stakeholders as “those groups who have a stake in or claim on the firm. Specifically

I include suppliers, customers, employees, stockholders, and local community….”.

Building on stakeholder theory Barnett (2005) introduced a construct defined as the

Stakeholder Influence Capacity (SIC) of the firm. Barnett stated that firms engage in

philanthropic actions to enhance their relationships with stakeholder groups. These actions

can not only enhance firm relations but also improve financial performance. Firms will

benefit from stakeholder focus by building trust and avoiding risk and uncertainty.

Obtaining different results from philanthropic actions will mainly depend on previous

stakeholder relationships. The last category of previous theoretical studies considered by

Garriga and Melé (2004) focused on the ethical considerations of social actions and is

closely related to stakeholder involvement. Donaldson and Preston (1995) emphasized the

normative base of the theory; the authors mentioned the „philosophical ethics‟ between the

firm and the society. As also a report of the American Law Institute4 (1992: 72) stated:

“The modern corporation by its nature creates interdependencies with a variety of groups

with whom the corporation has a legitimate concern, such as employees, customers,

suppliers, and members of the communities in which the corporation operates.” Here we

can also observe the „normative‟ connection between stakeholders and the firm to behave

ethically and mutually responsible.

4 American Law Institute report, Principles of Corporate Governance (1992: 72).

7

The above described multi-faceted potential of corporate social and philanthropic

actions also manifested itself in previous empirical research as one could observe differing

results focusing mainly to entangle the relationship between social and financial benefits of

the firm (Carroll et al., 1987, Burke and Logsdon, 1996). For instance while Aupperle et. al.

(1985) found a negative relationship between social responsibility and financial

performance, Hillman and Keim (2001) obtained mixed results on how stakeholder

management and social issue participation measured by the KLD dataset, is affecting

shareholder value using regression analysis. However, a meta-analysis covering 52 studies

by Orlitzky et al. (2003) found an overall positive relationship between firm‟s social actions

and financial performance. The study moreover examined the mediator effect of firm

reputation stating that firms which contribute to philanthropic activities aim to create a

positive firm image and increase firm reputation. Fombrun and Shanley (1990) found also

that those firms which are more involved in charitable giving will earn higher public

evaluation based on findings analyzing the Fortune Magazine‟s reputational survey. Such

as in a recent study Lev et al. (2010) observed, there exist a positive relationship between

charitable giving and firm sales mediated by customer satisfaction and sensitivity.

As these results show, analyzing empirically corporate social and philanthropic actions

related to firm performance can result ambiguous and difficult for a general interpretation.

This ambiguity is probably due to the lack of a well defined theoretical grounding (Garriga

and Melé, 2004, Carroll, 1999) which would give the foundation for further research.

The theoretical work of Godfrey (2005) models a generalized grounding for the

philanthropy-performance link drawing on risk management principles and insurance

theory. It argues how philanthropic activity will generate positive moral capital, when the

actions are evaluated positively by the affected stakeholder groups (2005:782). The model

shows how philanthropic actions provide insurance-like protection to the firm‟s intangible

assets by mitigating negative valuations (2005:783). The argument of Godfrey (2005) on a

causal relationship of philanthropic actions and performance relies on the reputational value

of the firm (Fombrun, 1996). Reputational value becomes important by influencing

stakeholder actions and decisions on investment. The author also examines how moral

capital provides insurance for a firm´s relational capital unless the harm was caused

8

consciously or by negligence (2005: 788). For instance consumers can be more skeptical

towards firms for which the motive to engage in philanthropic actions is perceived as „self-

serving‟ or the products are perceived as harmful for the society. An example5 is Altria

Group, which owns the brand Marlboro. Altria Group has one of the most elevated

corporate philanthropic investments. In the past decade it donated over 1 billion dollar in

cash donations focusing mainly on health and disaster recovery issues. In the year 2004

Altria Group donated 113 million dollars in cash and so occupied the third place of

Business Week’s ranking of best corporate philanthropist firms. However in the case of

Altria Group even with the great amounts of donations can result difficult to build a

positive firm image given their profile of producing a lethal product.

As we have mentioned it before, unless the harm is perceived as caused consciously or

by negligence, corporate philanthropy will strengthen a well defined corporate image.

Consumers will associate organizational values with firm products and therefore

consumption will be influenced by the positive and negative actions of the firm. For this

reason, it is important for firms to realize the benefits of philanthropic investments as it can

have an effect on product success (Burke and Logsdon, 1996). As Husted and Allen (2007)

also mention, consumers observe social and philanthropic activities of the firm. Therefore

an increased participation in such actions will positively influence value creation of the

firm by increasing consumer loyalty, product success and attracting new consumers.

Positive firm associations through corporate philanthropic activities can favorably influence

consumer reactions towards the firm‟s products (Brown and Dacin, 1997). Consumers will

associate firm social and philanthropic actions with its products if there is a clear

connection between the actions and the representation of the product. Therefore the

visibility of such actions is crucial to obtain a positive evaluation of firm reputation which

will relate to better performing products given the consumers trust in the company (Burke

and Logsdon, 1996). This will in turn shift the focus towards consumers and emphasize

relational-capital.

5 http://www.businessweek.com/magazine/content/05_48/b3961607.htm

9

Such an observation of an existing relationship between corporate philanthropic actions

and product failure has not been addressed before. Through our concept and the applied

theoretical mechanism we prove empirically how philanthropic actions can affect firm

evaluation and prevent product failure. To examine this link is important to prove tangible

benefits of philanthropic actions through the improvement of new products failure rate,

which is considered to lie between 40 % and 90 % after market introduction (Gourville,

2005).

III. Product failure

New product development is a complex process of firms. It not only requires adequate

resources, but also a comprehensive knowledge and management of internal and external

capabilities. Previous literature on NPD6 is exhaustive and has implications for instance in

the fields of marketing (Souder, 1988; Gupta et al., 1986), knowledge management (Katila

and Ahuja, 2002) and open innovation (von Hippel, 1998).

The complexity of the NPD process manifests itself in firm decisions as one has to take

into account several viewpoints. For this reason we find various studies in the previous

literature focusing on the success/failure factors of the new product development process

(Griffin and Page, 1993; Montoya-Weiss and Calantone, 1994; Cooper and Kleinschmidt,

1995; Henard and Szymanski, 2001). A successful product introduction depends on

different aspects as for instance meeting customer needs, technological preparedness and

cooperation between intra-organizational units (Dougherty, 1992). Firms need to align their

product development process with the overall firm strategy creating synergy between the

two in order to obtain a viable product (Cooper and Kleinschmidt, 1995).

Although, when firms launch a new product to the market there is always a possibility

to fail. Statistical demonstrations shows that even though firms invest high amounts of

time, money and effort in developing a new product, one can observe higher rate of new

product failure than new product success (Patrick, 1997). If failure occurs it can negatively

6 NPD: new product development

10

affect firms‟ financial performance, cause bad publicity or increase costs (Davidson and

Worrell, 1992). Product failure can be due to several reasons given the complexity of the

development process on the organizational level. Possible causes of failure can arise from

the developer‟s side or from the consumer‟s side. Problems which contribute to product

failure from the developer‟s side are often related to product design, product quality and

safety. As Bloch (1995) stated in his work, the design of a product can be substantial in its

positioning in the marketplace, moreover it has to fulfill societal responsibilities. Beamish

and Bapuji (2008) studied product failure due to quality and safety problems. The authors

pointed out that these problems can affect firm reputation, as the example of the major US

toy company Mattel showed. The other reason why new products fail is the inaccurate

assessment of consumer preferences. As Joshi and Sharma (2004) stated in their work

creating a reliable stock of customer knowledge will largely enhance new product

performance. Cooper and Kleinschmidt (1995) found that consumer focus of firms is a key

factor of new product development success. To understand consumer preferences and build

consumer knowledge, firms have to interact with consumers and provide adequate

information about firm activities and its products. To reduce uncertainty surrounding

consumers, firms are likely to engage in common actions. As Dougherty (1992) stated

previously, collective action is important for both parties: “Innovation requires collective

action, or efforts to create shared understandings from disparate perspectives.” (1992:192).

Therefore one can find extensive literature on consumer involvement in production design

and organizational activities (Kaulio, 1998; Grudin, 1994; von Hippel, 1986). Involving

consumers in product development provides the firm with a better knowledge about

consumer needs, creativity and problem solving options.

As we have mentioned it before, consumer perception of firm activities can shape the

overall verdict of the firm and affect consumption. Firms have to provide information and

interact with consumers in order to avoid product failure. Signaling a positive image of the

firm through corporate philanthropy will contribute to a higher tolerance among consumers.

As Auger et al. (2003) argued, ethical features of the product have an influence on

consumers purchase decisions. Such as Lee et al. (2009) mentioned, corporate philanthropy

based on altruistic motives will positively influence the attitude of consumers and influence

purchase decisions. The authors argue that consumers will obtain a positive signal from

11

corporate philanthropic actions and therefore approach products from firms engaged in

such activities. Considering these previous findings in the following section we present our

hypotheses.

IV. Hypotheses

Customers often evaluate a product from organizational associations (Brown and Dacin,

1997) and rely on public information. When making purchase decisions consumers expect

firms to behave ethical and truthful with their business environment and the society in

general (Creyer and Ross, 1997). For this reason firms aim to signal a positive image

towards consumers by investing in philanthropic activities (Godfrey, 2005; Peloza, 2005).

Contributing to charities is one way for firms to represent a socially responsible behavior.

To obtain a positive evaluation from the consumer, Xia et al. (2004) describes a conceptual

framework of price fairness perception in a consumer-firm relationship. The framework

demonstrates that the base of any such relationship involves trust. At an initial stage where

consumers have no previous purchase experience with the seller firm will base their trust on

the firm‟s image which can be deducted from public information of the firm‟s goodwill. A

positive image will be a signal for initial trust which later, after repeated purchase, will

convert to trustworthiness of the firm, based on knowledge and interpersonal relationship

(2004: 5).

Moreover a positive image of the firm will make consumers tolerant towards firm

deficiencies and prevent product failure. As Knox and Maklan (2004) stated, when a firm is

trusted by stakeholders and is pursuing social and philanthropic actions will reduce risks

arising from safety issues, product recalls and possible loss of corporate reputation.

Therefore firm donations may also behave as an insurance policy of the firm (Godfrey,

2005; Klein and Dawar, 2004). Consumers will accept product offerings and stand to firms

strategic decisions creating a closer link with the firm. This link will enhance the firms‟

relationship-based intangible assets (Godfrey, 2005).

Through this argument, we claim that a firm with strong philanthropic presence

emphasizing charitable giving will signal a positive and socially responsible behavior to

12

stakeholder groups, including consumers. This behavior of the firm will form an initial trust

among consumers and enhance the trustworthiness of the firm and its products. Consumers

when making purchase decisions will choose product from a firm with a positive image

over other firms‟ products. Consumers will become more tolerant towards responsible firms

which will support the viability of their products and prevent product failure. Therefore we

hypothesize that increasing investment in charitable giving of the firm will result in less

product failure.

Hypothesis 1: The higher the contribution to charitable giving of a firm, the less product

failure it will suffer.

Previously researchers argued that firms should apply different marketing practices

depending whether they are oriented towards individual consumer or industry market

(Webster, 1978). Coviello and Brodie (2001) argued that firms producing for consumer

market engage more in transaction marketing, using tools of advertising, sales promotion

and public relation. Such marketing communication focusing on branding and visual brand

identity will enhance consumer loyalty. Therefore those firms which are focusing on

individual consumers and are contributing to charitable giving will suffer less product

failure, given a better association of philanthropic actions with the firm identity through its

visibility.

As a study by Lev et. al. (2010) argues, corporate philanthropy and the visibility of

the firm‟s goodwill will be better observed and higher evaluated for those firms which sell

their products to individual consumers rather than to businesses, industry members.

Separating two categories high and low individual consumer sensitivity given the firms

target consumers (Lev et al., 2010) we identify due to the characteristics of our dataset the

category “consumer goods” as the industry of specified high individual consumer sensitive

and all other categories as specified low individual consumer sensitive.

13

We hypothesize that firms which focus on individual consumers and are engaging in

philanthropic actions namely charitable giving, will achieve better product performance

than other firms, through the better visibility and proximity between philanthropic actions

and individuals as target consumers.

Hypothesis 2: Firms with high individual consumer sensitivity contributing to charitable

giving will suffer less product failure than firms with low individual consumer sensitivity

contributing to charitable giving.

V. Methodology and Data

We selected our firm sample from the S&P 500 of largest U.S. firms list for the year

2006. At the end of our sample period in 2008 we identified 173 firms which remained

consistent along our period and became no object to bankruptcy, merger or acquisition and

were also concurrent with the KLD7 database S&P 500 identification through the same

period between 2000 and 2008. Therefore in our final sample we included the selected 173

firms with 1557 firm year observation. We chose the S&P 500 firm list for our study to

capture the visibility of the largest charitable donations and to dispose the majority of the

trademarks filed in the United States. Our dataset is a balanced panel dataset, where each

firm is observed the same number of times covering our nine year period from 2000 to

2008.

Our general model is Y ≈ ƒ(X, β). Where Y represents our count dependent variable,

product failure, X our explanatory variable charitable giving and β is a vector of

parameters. We use negative binomial regression model for our data analysis. We chose

this model to capture the over dispersion in our sample, having greater variance than mean

given that the Poisson model would be inappropriate holding the criterion of mean and

variance equality (Greene, 2003). The likelihood ratio test of our negative binomial model

7 KLD: Kinder, Lydenberg, Domini Research and Analytics Inc.

14

also confirms our model choice. Moreover we applied the Hausman test on our data to

decide whether to use random or fixed effects specification in our model. The results of the

test led to the rejection of the null hypothesis of uncorrelation between regressors and

random effects (p-value less than 0.01%). Therefore we applied the fixed-effects negative

binomial regression model to test both of our hypotheses. We conducted our empirical

analysis with the STATA 10 statistical software.

Variables

Product failure. Our dependent variable is product failure, which we measure by failed

trademarks. The Lanham Act defines a trademark as “any word, name, symbol, or device,

or any combination thereof used by a person to distinguish his or her goods or services

from those sold by others.”8 Trademark failure can occur due to abandonment, improper

licensing and genericity as determined by law9. We consider in our recent study trademark

failure due to abandonment, which is defined as the discontinuous use of the trademark

with no intent to resume its use, as well as the non-use of the trademark for three

consecutive years10

. The discontinuous use of a trademark is decided upon the

circumstances and abandonment will be legally exercised with the aim to prevent the

occupation of potentially useful marks. As in a legal form the commercialization and

marketing activities of the firm related to the products are represented by trademarks, it is

crucial to actively use the trademark to maintain its visibility for the public and enhance the

firm-product association among consumers. Therefore our proxy of product failure

represented by failed trademarks is relevant and reliable, strongly related to the consumer-

focus of the firms.

Although trademarks exist and are legally clarified since the 19th

century (Trademark

protection Act of 1881) their use for empirical research is quite recent. Previously

8 Lanham Act, 15 U.S.C.,1127

9 Lanham Act, 15 U.S.C. 1064; 15 U.S.C. 1058

10 http://cyber.law.harvard.edu/metaschool/fisher/domain/tm.htm

15

researchers mostly relied on patent data to measure product development and product

innovation (Katila and Ahuja, 2002) whereas nowadays we find a growing number of

studies using trademark data as a measure of innovation effort (Mendonca et al., 2004) or

branding effort of the firms (Krasnikov et al., 2009). Our product level data contains

trademark data from the USPTO11

with 68.184 trademarks.

Charitable giving. Our explanatory variable is charitable giving. Charitable giving is a

determining focus of firms representing the firm‟s visibility of goodwill. We have collected

data on charitable giving from The KLD12

Research and Analytics Inc. The KLD STATS13

dataset covering the S&P 500 represents positive and negative issues for each company

yearly from 1991 with a binary (1/0) yes/no value. KLD rates the social, environmental and

governance performance of the companies using positive and negative indicators, strengths

and concerns. Companies are rated in seven major qualitative issue areas: environment,

community, corporate governance, diversity, employee relations, human rights and product

quality and safety.14

Data on the strengths of the community area are represented by the

categories of charitable, non-US charitable and innovative giving, support for education

and housing, volunteer programs and other strengths. From these community strength

variables we specifically selected the charitable giving15

variable as our measure for

philanthropic activity, represented by a binary 0/1 variable. Taking the value 1 if firmi has

consistently given over 1.5% of trailing three-year net earnings before taxes (NEBT) to

charity, or has otherwise been notably generous in its giving, and 0 otherwise.

11 USPTO: United States Patent and Trademark Office

12 KLD: Kinder, Lydenberg, Domini Research and Analytics Inc.

13 KLD STATS: Statistical Tool for the Analysis of Trends in Social and Environmental Performance

14 Information obtained from the official KLD website, see in References.

15 KLD Stats data description about Charitable Giving: The company has consistently given over 1.5% of trailing three-

year net earnings before taxes (NEBT) to charity, or has otherwise been notably generous in its giving.

16

Control variables

Firm specific control variables were obtained from the Compustat database. Return on

equity (ROE) was calculated as the net income after tax divided by the shareholder equity.

We use this variable to control for firm performance and for firm reputation. As Fombrun

and Shanley (1990) mentioned in their work corporate reputation is represented partially by

the financial performance of the firm arising mainly from accounting data. The number of

employees (Employees) is considered to capture the size of the firm. The variable R&D

expenditure (R&D expenditure) represents all costs incurred during the year that relate to

the development of new products or services, this variable is important to control for the

different levels of R&D investments among the firms. The variable sales (Sales) represent

the net sales of the firm, controlling for the size of the firms. For all the above mentioned

variables we take the natural logarithm. Advertising expenses (Advertising dummy)

represents advertising media (i.e., radio, television, and periodicals) and promotional

expenses with a binary 0/1 variable, which takes the value 1 if the given company had

advertising expenses for our given years and 0 otherwise. Moreover we included as a

control variable the total number of trademarks (Trademark Total #) as obtained from the

USPTO database. Finally we created two dummy variables, time dummy variables (Time

dummy) for each year from 2000 to 2008 and sector dummy variables (Sector dummy)

including ten different sectors identified by the aggregate economic sector type16

to control

for the different industrial sectors included in our sample.

VI. Results

In Table 1 and in Table 2 we represent the descriptive statistics of our variables and

the corresponding correlation matrix.

16

Compustat Economic Sector (codes): Materials (1000), Consumer Discretionary (2000), Consumer Staples (3000),

Health Care (3500), Energy (4000), Financials (5000), Industrials (6000), Information Technology (8000),

Telecommunication Services (8600), Utilities (9000).

17

Table 1. Descriptive statistics

Table 1. contains the number of observation, mean, standard deviation and maximum

and minimum values for our key variables. We can observe that an average firm in our

sample owns 31 trademarks. Moreover those product failures for an average firm, which we

represent by failed trademarks, are nearly 14 products.

Table 2. Correlation matrix

In Table 3 we show the results of our first hypothesis where we test the relationship

between charitable giving and product failure of the firms. We applied fixed effects

18

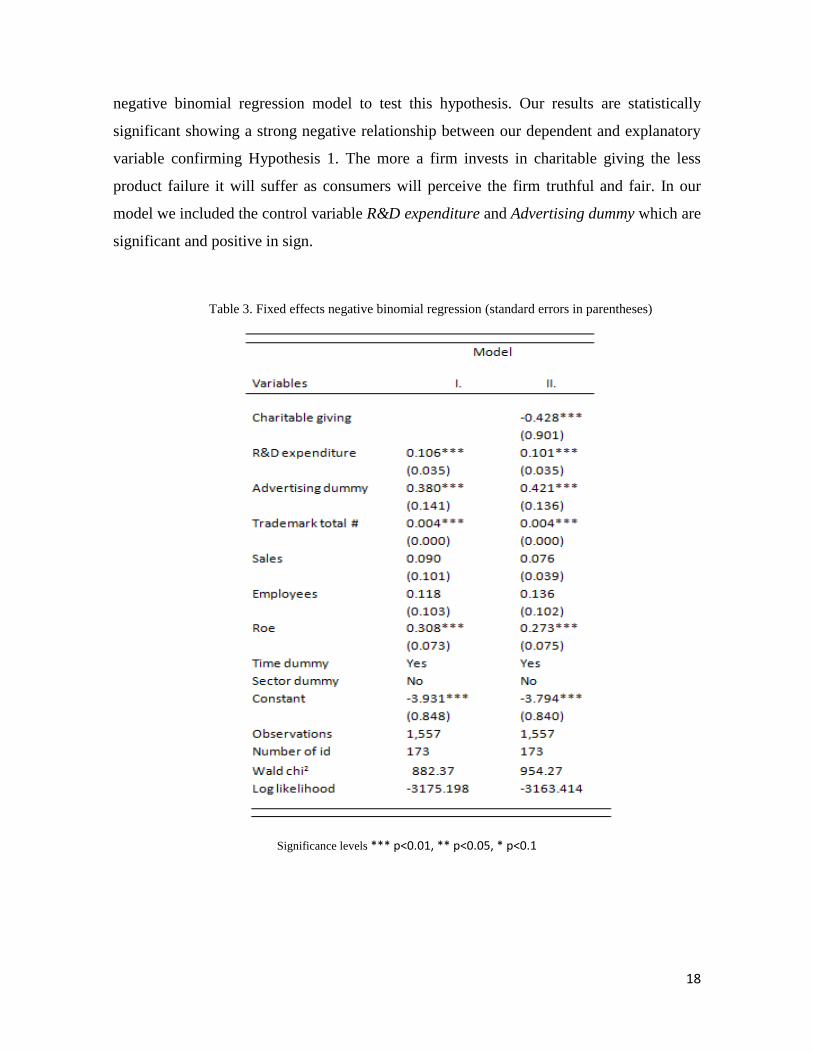

negative binomial regression model to test this hypothesis. Our results are statistically

significant showing a strong negative relationship between our dependent and explanatory

variable confirming Hypothesis 1. The more a firm invests in charitable giving the less

product failure it will suffer as consumers will perceive the firm truthful and fair. In our

model we included the control variable R&D expenditure and Advertising dummy which are

significant and positive in sign.

Table 3. Fixed effects negative binomial regression (standard errors in parentheses)

Significance levels *** p<0.01, ** p<0.05, * p<0.1

19

In Table 4 following the industry classification by Sharpe17

(1982) we again conducted

a fixed effects negative binomial regression to test our second hypothesis, to observe the

influence of charitable giving on product failure taking into account the target consumers of

the firm, depending whether it is an individual consumer or a business to business

relationship. After applying the classification of Sharpe (1982) to our firms due to their

primary SIC codes, we use the specification by Lev et al. (2010) regarding high or low

individual consumer sensitivity. One category the “consumer goods” is specified in our

model as high individual consumer sensitive, all other categories are specified as low

individual consumer sensitive. Before testing Hypothesis 2 we conducted a T-test on the

Beta coefficients of the two groups high and low consumer sensitive firms, where we

obtained confirmation about the distinction between these groups (Prob > chi2 = 0.0393).

The results we represent in Table 4 are not supporting our second hypothesis, showing

statistically significant results about a stronger relationship for low individual consumer

sensitive firms associated with stronger visibility of firm identity through charitable

contribution and the product failure of the firms. We observe less product failure in firms

with low individual consumer sensitivity than for firms with high individual sensitivity.

In our models, among firms with low individual consumer sensitivity our explanatory

variable Charitable giving is more significant than for firms with high individual consumer

sensitivity. This result can probably be due to „consumer firms‟ having more accurate

information about the „seller firm‟ through a vertically integrated relationship between the

two firms, where the similarity of philanthropic strategy could play an important role.

Moreover it could be the case that firms as end consumers engage more likely in

relationships with firms having a good corporate image to enhance their own reputation.

For this reason it will be a crucial aspect for the „seller firm‟ to possess a strong corporate

17

Industry classification by Sharpe (1982) on 4-digit SIC codes: (1) Basic Industries: 1000-1299,1400-1499, 2600-2699,

2800-2829, 2870-2899, 3300-3399; (2) Capital goods: 3400-3419, 3440-3599 exc. 3523, 3670-3699, 3800-3849, 5080-

5089, 5100-5129,7300-7399; (3) Construction: 1500-1599, 2400-2499, 3220-3299, 3430-3439, 5160-5219; (4) Consumer

goods: 0000-0999, 2000-2399, 2500-2599, 2700-2799, 2830-2869, 3000-3219, 3420-3429, 3523, 3600-3669, 3700-3719,

3751, 3850-3879, 3880-3999, 4813, 4830-4899, 5000-5079, 5090-5099, 5130-5159, 5220-5999, 7000-7299, 7400-9999;

(5) Energy: 1300-1399, 2900-2999; (6) Finance: 6000-6999; (7) Transportation: 3720-3799 exc. 3751, 4000-4799; (8)

Utilities:4800-4829 exc. 4813, 4900-4999; (9) Others: all other SIC codes.

20

philanthropic attitude. However these possible explanations should further be tested to

obtain stronger evidence about our result for the second hypothesis.

Table 4. Fixed effects negative binomial regression (standard errors in parentheses)

Significance levels *** p<0.01, ** p<0.05, * p<0.1

21

VII. Conclusion

To achieve social recognition and enhance a positive corporate image firms

increasingly focus on different stakeholder groups and tend to create a closer relationship

with them. Investing in corporate philanthropy, which is considered to be an important part

of corporate social responsibility (Carroll, 1997), will support a positive public evaluation

and increase the truthfulness of the firm. A recent theoretical work by Godfrey (2005)

highlighted moral capital building as a mechanism to obtain positive public evaluation

through corporate philanthropic actions. Moral capital building will create protection for

the firm‟s intangible assets such as stakeholder relations and accordingly increase

shareholder wealth.

In our recent study we focus on one particular stakeholder group, the group of

consumers. We aim to prove that firms which are investing in corporate philanthropic

actions namely charitable giving will affect positively consumer‟s perception about firm

products and so prevent product failure. Xia et al. (2004) argued that trust and cognition of

fairness will influence consumers to engage in any relation with the firm. Building on these

arguments we first hypothesize that firms will suffer less product failure if they invest in

charitable giving. Secondly we hypothesize that this relationship will be more visible for

firms focusing on individual consumers.

We measure product failure with failed trademarks obtained from the USPTO database

which is a recent measure in the strategic management literature. Our results are partially

confirming our hypotheses. We found that firms which engage in charitable giving suffer

less product failure. However our results showed no support about this effect being more

significant for firms with higher individual consumer sensitivity.

Our results imply a general conclusion of consumer response to firm actions, that a

positive action will be rewarded. In our future research we aim to focus on the economic

benefits of charitable giving and find further evidence of the tangible benefits of corporate

philanthropy.

22

References

Auger, P., Burke, P., Devinney, T. M., and Louviere, J. J.: (2003), 'What Will Consumers

Pay for Social Product Features?' Journal of Business Ethics 42(3): 281-304.

Aupperle, K., Carroll, A., and Hatfield, J., (1985). An empirical examination of the

relationship between corporate social responsibility and profitability, Academy of

Management Journal, 28: 446-463.

Barnett, M.L. (2005). Stakeholder influence capacity and the variability of financial returns

to corporate social responsibility. Academy of Management Review, 32(3): 794–816.

Beamish, P.W. & Bapuji, H. (2008) Toy Recalls and China: Emotion vs. Evidence.

Management and Organizational Review, 4(2): 197-209.

Bloch, P.H. (1995) Seeking The Ideal Form Product Design and Consumer Response.

Journal of Marketing, 59(3): 16-30.

Brown, T.J. & Dacin, P.A. (1997) The Company and The Product: Corporate Associations

and Consumer Product Responses. Journal of Marketing. 61(1): 68-84.

Burke, L. & Logsdon, J.M. (1996). How Corporate Social Responsibility Pays off. Long

Range Planning, 29(4): 495-502.

Calvano, L. (2008). Multinational Corporations and Local Communities: A Critical

Analysis of Conflict. Journal of Business Ethics, 82: 793-805.

Carroll, A.B., Hoy, F. and Hall, J. (1987). The Integration of Corporate Social Policy Into

Strategic Management, In S.P.Sethi & C.M. Falbe (eds), Business and Society: Dimensions

of Conflict and Cooperation, 449-470, Lexington, MA: Lexington Books.

Carroll, A.B. (1999) Corporate Social Responsibility. Business and Society 38(3): 268-295.

CECP, (2008). Business‟s Social Contract: Insights from CEOs on achieving efficient

philanthropy Research Study, Based on the research by McKinsey & Company,

http://www.corporatephilanthropy.org/pdfs/research_reports/SocialContract.pdf. Accessed

on June 21, 2009.

Clotfelter, C.T. (1985). Federal Tax Policy and Charitable Giving. The University of

Chicago Press.

Cooper, R.G. & Kleinschmidt, E.J. (1995). Benchmarking the Firms Critical Success

Factors in New Product Development, Journal of Product Innovation Management, 12:

374-391.

23

Coviello, N.E. & Brodie, R.J. (2001), Contemporary Marketing Practices of Consumer and

Business-to-Business Firms: How Different Are They? Journal of Business and Industrial

Marketing. 16 (5): 382–400.

Crane, A. (2001). Unpacking The Ethical Product. Journal of Business Ethics.30: 361-373.

Creyer, E. H., & Ross, W. T. (1997). The influence of firm behavior on purchase intention:

do consumers really care about business ethics? Journal of Consumer Marketing, 14: 421-

432.

Davidson W.N. & Worrell D.L. (1992). Research Notes and Communications: The Effect

of Product Recall Announcement On Shareholder Wealth. Strategic Management Journal.

13(6): 467-473.

Donaldson, T. & Dunfee, T.W. (1994) Toward a unified conception of business ethics:

Integrative social contracts theory, The Academy of Management Review, 19(2): 252-284.

Donaldson, T. & Preston, L.E. (1995). The Stakeholder Theory of the Corporation:

Concepts, Evidence, and Implications. The Academy of Management Review, 20(1): 65-91.

Dougherty, D. (1992) Interpretive Barriers To Successful Product Innovation In Large

Firms. Organization Science. 3(2): 179-202.

Ellen, P.M., Webb, D.J. and Mohr L.A. (2006). Building Corporate Associations:

ConsumerAttributions for Corporate Socially Responsible Programs. Journal of The

Academy of Marketing Science. 34 (2): 147-157.

Freeman, R.E. (1984). Strategic management: A stakeholder approach. Boston, MA:

Pitman.

Fombrun, C. J. (1996). Reputation: Realizing Value from The Corporate Image.Business

School Press, Boston, Massachusetts.

Fombrun, C.J. & Shanley, M. (1990) What‟s in a name? Reputation building and corporate

strategy., Academy of Management Journal. 33(2): 233-258.

Garriga, E. & Melé, D. (2004). Corporate Social Responsibility Theories: Mapping the

Territory, Journal of Business Ethics, 53: 51-71.

Greene, W.H. (2003) Econometric Analysis, New York University, Prentice Hall

Griffin, A. & Page, A.L. (1993) An Interim Report On Measuring Product Development

Success and Failure. Journal of Product Innovation Management. 10:291-308.

Grudin J. (1994). Groupware and social dynamics: Eight challenges for developers.

Communications of the ACM. 37(1): 92-105.

24

Godfrey, P.C. (2005). The Relationship Between Corporate Philanthropy and Shareholder

Wealth: A Risk Management Perspective, Academy of Management Rreview, 30(4): 777-

798.

Gourville, J.T. (2005) The Curse of Innovation: Why Innovative New Products Fail. MSI

Report 05-044.

Gupta K.A., Raj S.P., and Wilemon D. (1986). A Model for Studying R&D-Marketing

Interface in the Product Innovation Process, Journal of Marketing. 50: 7-17.

Hansen, M.T. & Nohria, N. (2004) How to build collaborative advantage. MIT Sloan

Management Review, 46(1): 22-30

Henard, D.H. & Szymanski, D.M. (2001) Why Some New Products Are More Successful

Than Others?, Journal of Marketing Research, 38:362-375.

Hillman, A.J. & Keim, G.D. (2001). Shareholder Value, Stakeholder Management, and

Social Issues: What's the Bottom Line? Strategic Management Journal, 22(2): 125-139

Husted, B.W. & Allen, D.B. (2007) Strategic Corporate Social Responsibility and Value

Creation Among Large Firms, Long Range Planning, 40:594-610.

Joshi, A. W. & Sharma, S. (2004) Customer Knowledge Development: Antecedents and

Impact on New Product Performance. Journal of Marketing. 68(4): 47-59.

Katila, R. & Ahuja G. (2002). Something Old, Something New: A Longitudinal Study of

Search Behavior and New Product Introduction. The Academy of Management Journal.

45(6): 1183-1194.

Kaulio, M.A. (1998) Customer, Consumer and User Involvement In Product Development:

A Framework and a Review of Selected Methods. Total Quality Management and Business

Excellence. 9(1):141-149.

Klein J, & Dawar N. (2004). Corporate social responsibility and consumers‟ attributions

and brand evaluations in a product-harm crisis. International Journal of Research in

Marketing, 21(3): 203–217.

Knox, S. & Maklan, A. (2004) Corporate Social Responsibility: Moving Beyond

Investment Towards Measuring Outcomes. European Management Journal, 22 (5): 508-

516.

Kotchen, M.J. & Moon J.J. (2008) Corporate Social Responsibility for Irresponsibility.

Working paper, University of California-Santa Barbara.

Krasnikov, A. Saurabh, M. and Orozco, D. (2009). Evaluating the Financial Impact of

Branding Using Trademarks: A framework and Empirical Evidence. Journal of Marketing.

(73): 154-166.

25

Lee, H, Park, T., Koo Moon H., Yang, Y. and Kim, C. (2009) Corporate philanthropy,

attitude towards corporations, and purchase intentions: A South Korea study. Journal of

Business Research. 62: 939-946.

Levinthal D. A. & Purohit D. (1989). Durable goods and Product Obsolescence. Marketing

Science Vol. 8 (1): 35-56.

Lev B., Petrovits C. & Radhakrishnan S., (2010), Is Doing Good Good for You? Yes,

Charitable Contributions Enhance Revenue Growth. Strategic Management Journal 31(2):

182-200.

Margolis J.D. & Walsh J.P. (2003). Misery loves companies: Rethinking social initiatives

by business, Administrative Science Quarterly, 48: 268-305.

Mendonca, S., Santos Pereira, T. and Mira Godinho, M. (2004) Trademarks as an Indicator

of Innovation and Industrial Change. LEM Working Paper Series.

Mitchell, R.K., Agle, B.R., and Wood, D.J. (1997). Toward a theory of stakeholder

identification and salience: Defining the principle of whom and what really counts.

Academy of Management Review, 22: 853-886.

Montoya-Weiss, M.M. & Calantone, R. (1994). Determinants of new product performance:

A review and meta-analysis. Journal of Product Innovation Management. 11(5): 397-417.

O‟Brien, D. (2001). Integrating Corporate Social Responsibility with Competitive Strategy,

The Center for Corporate Citizenship at Boston College, Boston, MA

Orlitzky, M., Schmidt, F.L., and Rynes, S.L. (2003). Corporate social and financial

performance: A meta-analysis. Organization Studies. 24: 403–441.

Patrick, J., (1997). How to Develop Successful New Products. NTC Business Books, NTC

Publications, Oxon.

Peloza, J. (2005). Corporate Social Responsibility as Reputation Insurance, Paper presented

at the 2nd Annual Corporate Social Performance Conference, Haas School of Business,

University of California, Berkeley, April.

Porter, M.E. & Kramer, M.R. (2002). The Competitive Advantage of Corporate

Philanthropy. Harvard Business Review. 80 (December): 57-68.

Sharpe, W. F. (1982) Factors in New York exchange security returns, 1933-1979. Journal

of Portfolio Management. (8):5-19.

Sorenson, O. (2000). Letting the Market Work for You: An Evolutionary Perspective on

Product Strategy. Strategic Management Journal. 21(5): 577-592.

26

Souder, W.E. (1988) Managing Relations between R&D and Marketing in New Product

Development Projects, Journal of Product Innovation Management, 5(1): 6-19

Strahilevitz, M. (1999). The effects of product type and donation magnitude on willingness

to pay more for a charity-linked brand. Journal of Consumer Psychology, 8(3): 215-241.

Szymanski, D.M. (2001) Customer Satisfaction: A Meta-Analysis of the Empirical

Evidence. Journal of the Academy of Marketing Science 29:16-35.

Trost, S.C. (2006) An Examination of Corporate Charitable Contributions: Evidence from

Firm, Managerial, and Community Factors. Doctoral Dissertation, University of Virginia,

Department of Economics.

Varadarajan, P.R. & Menon, A. (1988) Cause-Related Marketing: A Coalignment of

Marketing Strategy and Corporate Philanthropy. Journal of Marketing. 52:58-74.

von Hippel E. (1998). Economics of Product Development by Users: The Impact of

“Sticky” Local Information. Management Science 44(5): 629-644.

von Hippel E. (1986). Lead Users: A Source of Novel Product Concepts. Management

Science 32(7): 792-805.

Waddock, S.A. & Graves, S.B. (1997). The Corporate Social Performance-Financial

Performance Link. Strategic Management Journal, 18(4): 303-319.

Wang, H., Choi, J. and Li, J. (2008) Too Little or Too Much? Untangling The Relationship

Between Corporate Philanthropy and Firm Financial Performance. Organizational Science

19(1): 143-159.

Webster, F. (1978). Management Science in Industrial Marketing. The Journal of

Marketing. 42: 21-27.

Xia, L., Monroe K.B., and Cox, J.L. (2004). The Price Is Unfair! A Conceptual Framework

of Price Fairness Perceptions. Journal of Marketing 68: 1–15.