Embed Size (px)

Citation preview

R E S E A R C H O N M O N E Y A N D F I N A N C E

Discussion Paper no 6

THE GLOBALISATION OF FINANCIAL CAPITAL, 1997-2008

Carlos Morera CamachoSchool of Economics, UNAM

José Antonio Rojas NietoInstituto de Investigaciones Económicas

15 March 2009

Research on Money and Finance Discussion Papers

RMF invites discussion papers that may be in political economy, heterodox economics, and economic sociology. We welcome theoretical and empirical analysis without preference for particular topics. Our aim is to accumulate a body of work that provides insight into the development of contemporary capitalism. We also welcome literature reviews and critical analyses of mainstream economics provided they have a bearing on economic and social development.

Submissions are refereed by a panel of three. Publication in the RMF series does not preclude submission to journals. However, authors are encouraged independently to check journal policy.

2

Carlos Morera Camacho, School of Economics (Facultad de Economía), National Autonomous University of Mexico (Universidad Nacional Autónoma de México—UNAM). José Antonio Rojas Nieto, Institute of Economic Research (Instituto de Investigaciones Económicas). This essay is part of a bigger study currently under way on the “The World Financial and Oil Markets, 1997-2007”. It has benefited from critical observations by Costas Lapavitsas, particularly with regard to credit. The development of the database and the figures received support from Lidia Salinas Islas, Isaac Torres and Iván Mendieta.

Research on Money and Finance is a network of political economists that have a track record in researching money and finance. It aims to generate analytical work on the development of the monetary and the financial system in recent years. A further aim is to produce synthetic work on the transformation of the capitalist economy, the rise of financialisation and the resulting intensification of crises. RMF carries research on both developed and developing countries and welcomes contributions that draw on all currents of political economy.

Research on Money and FinanceDepartment of Economics, SOAS

Thornhaugh Street, Russell SquareLondon, WC1H 0XG

Britain

www.soas.ac.uk/rmf

3

1.Thetransformationoftheworldeconomy

The world economy has experienced thirty years of dramatic changes, deriving

from the profoundeconomic turmoil that followed theoil crisesof 1973‐74 and

1980‐1981, the collapse of ‘actually existing socialism’, and the transformation of

China. Global and generalised restructuring took place as a result of these

developments. Gradually new characteristics emerged in a world economy

including, first, predominance of financial capital subject to dollar hegemony;

second, strong dynamism andnew characteristics of the world financial sector;

and third, intensified articulation between national financial markets and

monetary systems. To a large extent these characteristics flowed from the

deregulation and liberalisation measures implemented initially by the United

States and the United Kingdom between 1979 and 1982. But the majority of

industrialisedanddevelopingcountrieshavefollowedsuit.

Whathasemergedistheconsolidationofaninternationalfinancialspacethrough

which practically all national financial processes are obliged to pass in an

articulated manner. This imperative also applies to national productive and

commercial activities. Without a doubt, major technological changes have

sustainedthese transformations.Modernmicroelectronicsand theinternet have

enormous capacity to maximise volume and minimise costs of transmiting

information.Technicalchangeshavemadestructuraltransformationspossibleand

gavethemmomentum.

The transformation ofworldcapitalism hasfurtherbeensustainedbynumerous

and substantial changes in the processes of work, which have typically meant

generalised attacks on workers’ conditions.Without a doubt some of themost

importantchangesexperiencedbycapital inthelastthreedecadescorrespondto

bothwagedandunwaged labour(Munck,2002andAnderson,2006).Thesehave

included,first,substantialchangesinproductiontechnologies,particularlycontrol

andautomationofprocesses;second,theextensionofso‐calledtemporarylayoffs;

4

andthird,proliferationofflexibleformsofhiring.Workers’conditionshavebeen

adverselyaffectedthrough prices rising fasterthanwages, falls inmoneywages,

worseningconditionsofsocialsecurity, layoffs,oldageprovisionandretirement,

and finally, business insolvencies and bankruptcies (Moseley, 2007:2‐3; Gill

2002:643‐644).

Nevertheless—as demonstrated by theextremely critical conditions of 2008‐9—

global capital has not succeeded in re‐establishing the rhythms of growth and

profitabilitythatcharacterisedtheearlypost‐WorldWarII era.Onthecontrary,

the effects of continuous restructuring during the last thirty years have been

asymmetricalonproductionandcirculation.Thisasymmetryhasintensifiedsince

1998—infavourofcirculation.ThecurrentcrisiscomesatendofaboomintheUS

economy that lasted for nearly ten years, andwhich—as is now apparent—was

prolonged farbeyondwhat was justified by its true foundations. The (relatively

artificial) boom actually rested on an unprecedented expansion of credit to

government,tobusinessesandtoUShouseholds.Toestablishthispoint,consider

thefollowingaspectsoftheUSeconomy.

2.TherestorationofprofitabilityandtheperformanceoftheUSeconomy

Marxisttheoryidentifiesprofitastheengineofcapitalism,andassertsthattherate

ofprofittendstofallasaresultofintensifiedcapitalaccumulationrelativetothe

generation andappropriation of surplus value. However, theprocess is complex

since,ontheonehand,thereisatendencyfortherateofprofittofallbut,onthe

other, there are substantial increases in themass of profit. These two different

movementsmakedisputesamongallthefactionsofcapitalmorecontroversialand

violent(Marx,1976).

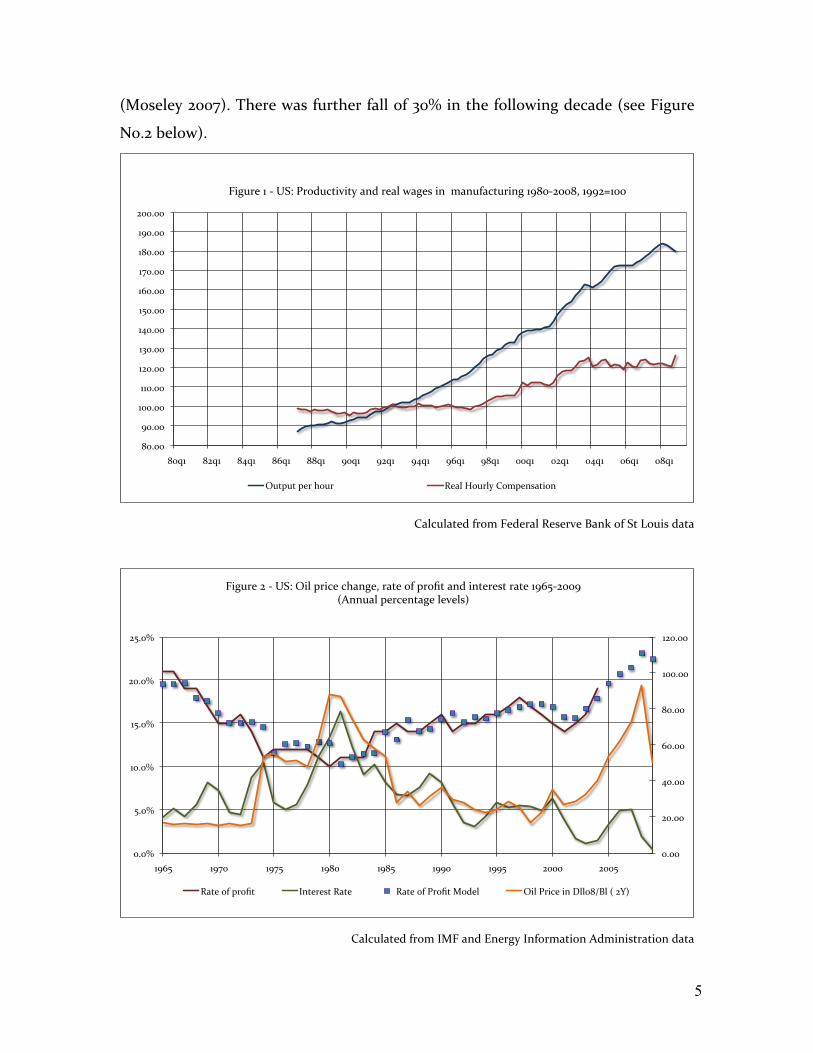

TheperformanceoftheUSeconomycanbeanalysedinlinewiththeevolutionof

therateofprofit.ThecrisisandstagnationphaseoftheUSeconomyinthe1970s

werebasedonafall intherateofprofitbyapproximately50%from1950 to 1970

5

(Moseley2007).Therewasfurtherfallof30%inthefollowingdecade(seeFigure

No.2below).

!"#""$

%"#""$

&""#""$

&&"#""$

&'"#""$

&("#""$

&)"#""$

&*"#""$

&+"#""$

&,"#""$

&!"#""$

&%"#""$

'""#""$

!"-&$ !'-&$ !)-&$ !+-&$ !!-&$ %"-&$ %'-&$ %)-&$ %+-&$ %!-&$ ""-&$ "'-&$ ")-&$ "+-&$ "!-&$

./0123$&$4$567$829:1;</=/<>$?@:$23?A$B?03C$/@$$D?@1E?;<12/@0$&%!"4'""!F$&%%'G&""$

H1<I1<$I32$J912$ K3?A$L912A>$M9DI3@C?</9@$

CalculatedfromFederalReserveBankofStLouisdata

!"!!#

$!"!!#

%!"!!#

&!"!!#

'!"!!#

(!!"!!#

($!"!!#

!"!)#

*"!)#

(!"!)#

(*"!)#

$!"!)#

$*"!)#

(+&*# (+,!# (+,*# (+'!# (+'*# (++!# (++*# $!!!# $!!*#

-./012#$#3#456#7.8#91.:2#:;<=/2>#1<?2#@A#91@B?#<=C#.=?212D?#1<?2#(+&*3$!!+##EF==0<8#921:2=?</2#82G28DH#

I<?2#@A#91@B?# J=?212D?#I<?2# I<?2#@A#K1@B?#L@C28# 7.8#K1.:2#.=#M88!'NO8#E#$PH#

CalculatedfromIMFandEnergyInformationAdministrationdata

6

Therecoveryoftherateofprofitbeganin1981,basedonintensifiedexploitationof

labour. Nevertheless, the circumstances of exploitation have also changed. The

changes in the labour process were expressed in what is known as

deterritorialisation—therelocationoftheproductionprocesstootherareasofthe

world economy where wages are lower—which was promoted in the 1990s.

However, themajorstrategyfor restoringthe rateof profit in theUnitedStates

wasfinancialisation,basedonanincreaseininternationaldebtandover‐expansion

ofcredit.Threemomentsstandoutintheevolutionofinternationaldebt:first,the

United States becoming a net debtor, beginning in 1986; second, the arrival of

crisis in Southeast Asia; and third, the impact of financial crisis of 2001on the

markets.

Inthesecondhalfofthe1990s, thepricesofrawmaterials, fuelandenergywere

relativelylow.Interest rateswereat theirlowest sinceWorldWarII. Substantial

increases in productivity took place in the USA (see diagram 1 above).

Consequently, therewas an impressive recovery of the profit rate in theUnited

States, thus expressing improvements in the overall profitability of the world

economy. However, dramatic and violent increases in the prices of the raw

materials,fuelsandenergyfollowedsoonafter.Ontheotherhand,andincontrast

topastexperience,interestratesnotonlyremainedlowbuttendedtofall.

Asaresult,manymainstreameconomistsconcludedthat theboomat theendof

the1990swasa landmark.Apparently,theUSeconomyhadleftbehindthelong

stagnation that began in the 1970s, and openeda newperiod ofhigheconomic

growth, increased employment, inflation reduction and moderate increases in

wages. Yet, the crisis of 2001 showed that things were different, and recession

establisheditselfonceagain.Recovery,beginningin2002,wasslow,andgrowthin

jobslaggedbehindoutput.Thedynamicofjoblossesandinsufficientemployment

opportunities to absorb new labour supplies has been extraordinarily severe.

Profound transformationshaveensued across the spheres of theworld economy

7

(realsector),aswellasinthefinancialandcommercialsystem(virtualsector)and

intechnologicaldevelopment(Lapavitsas,2008).

The international credit crisis that began in August 2007 has revealed the

magnitudeofthetransformationsthathavetakenplacenotonlyinbankingbutin

all formsofcapitalandthestate.The crisis itselfwas the result ofan enormous

expansionofmortgageloans,someofwhichweregrantedtothepoorestandmost

oppressed sections of the working class (Lapavitsas, 2008:40). Borrowers were

heavily black and Latino, giving to the crisis a racial dimension (Dymski,

2008:14‐25).US andEuropeanbankswereheavilyaffectedby thecollapse inthe

valueofthemortgage‐backedsecurities that theyhadcreated,andwhichturned

outto beasignificantportionoftheirassets.Theresultinginsolvencyprovokeda

credit crisis, andthe initial reaction of financial institutionswas tohoard funds,

therebyintensifyingthecrisis.

3. TheMexicanandAsianfinancialcrisesof the 1990s, and thesubsequent

evolutionoffinance

Therootsoftherecentcrisisandoftheevolutionoffinanceinthe2000saretobe

foundintheMexicancrisisof1995andtheSoutheastAsian(Thailand,Indonesia,

Malaysia,andPhilippines) crisisof1997‐8.Bothcrisesevolvedinsimilarfashion.

They began with a devaluation of the local currency as a result of high trade

deficits,whichhadreachedserious levelsbecauseofthelinkofthecurrencies to

the dollar in the first place. This was followed by short‐term capital flight and

collapseofweakfinancialmarkets.

Asaresult,therewasstrongcontractionofcreditandaseveredropinproduction,

to saynothingofthebrutalincreaseinthecost ofpublicforeigndebt.Therewas

alsoasharpriseinprivatesectordebt(banksandenterprises),whichinthecaseof

Mexicowastransferredtocaptivetaxpayersandtofiscal revenuefromoilprofits.

Simultaneously there was withdrawal of short‐term foreign and domestic

8

investmentsandinsolvencyoflocalbankingsystems,whichin somecases ledto

thecollapseofbothbanksandnationalcompanies.

TheMexican crisisandtheso‐called “tequilaeffect”werecontained.Thiscanbe

attributedtoseveralfactorsincluding,first,supportfromtheUnitedStates,which

was at the time experiencing considerable economic strength; second, theU.S.

originofthebulkofprivatecapitalflowstoMexico,whichpromptedimmediate

support by theClinton administration (Morera, 1998 and 2002); third, the trade

links of Mexico with the United States, in contrast to the intense trade

interdependenceamong theaffectedAsianeconomies;andfourth,thedeepening

oftheprivatisationprocessintelecommunicationsandtransportation,andevenin

areasforbiddenbythecountry’sconstitution,specificallyoilandelectricity.

In the case of Southeast Asia, the private and fragmentary character of the

economiestremendouslyhinderednegotiationsonhowtodealwith thecrisis.In

addition,themechanismsofcontagionintheAsianregionwereheavilylocatedin

the productive and commercial spheres, given that thedevelopment strategy of

theseeconomiessincethe1960swastoorientthemselvestowardforeignmarkets.

ForThailand, Indonesia,Malaysia, andthePhilippines, aswell as China in 1997,

approximately 50% of their trade was regional, and a similarproportion of this

regionaltradewaswithJapan.SouthKoreawasalsostronglyaffectedandentered

a recession (Chesnais, 1999: 9‐10). In addition, Russia’s external bankruptcy

occurredinmid‐1998,andsubsequentlyBrazil(UNCTAD,1999:59,71‐72).

Following theAsiancrisis,theinternational bankingsystembecamemoreclosely

articulatedwith both theprivateandpublic sectorsof thesecountries. Thenew

relationshipsincludedeasytermsofrefinancingagreedwiththenationalbanking

systems in these countries. Debts didnot disappearbut ratherincreasedas the

crisis was expressed as a drop in production, trade, and employment. Asia

accounts fora thirdofworldtradeandduringthe 1990s it representedtheonly

region that experienced sustained industrial growth, together with the United

9

States.ItispreciselyinthisregionwheremostU.S.industrial exportsaresold.In

1998, contraction inproductionandtradeaffected theU.S. economy and spilled

overtocountriesthatexportrawmaterials,includingoil.

However,in1999oilpricesbeganto rise,partlyduetothetremendousdynamism

of China and India, andpartlydue to the lowmarginofproduction capacity in

relation to the levels of world demand for crude. Consequently, capital flows

derivingfromoil profitsaswellasfromsavings inemergingeconomiesbeganto

flowtowarddevelopedcountriesandparticularly theUnitedStates.Thisallowed

theUS economiccycle to go beyondwhat the internal savings ratewould have

permitted.And it alsoprovidedfinance fortheenormousU.S.deficit. (BIS 2003,

2005andUNCTAD2005).

Against this background, global financial liberalisation and the ongoing

technologicalrevolutionfosteredanunprecedentedfinancial boom after 1998.At

the same time, it became impossible for monetary authorities to carry out

monitoringandevaluationoffinancialconditions.(NYT,2002).Thisboomreflects

the powerful development of banking and non‐banking financial institutions

across the world. The close articulation of these institutions with the world

financial center(theUnited States) is the reasonwhy the “momentary” crash of

key debtors in the late 1990s actually translated into further increases in

international banking assets. There was furtherglobal financial expansion after

1998,andconditionswerecreatedforanevengreatercrisis.

Underlying the phenomenal expansion of finance during the last ten years has

been the relentless liberalisation of interest rates, financial activities and

international capital flows. But note that the share of commercial banks (and

savingsinstitutions) in thetotal volumeof loanshasbeendeclining.During this

period,aswasmentionedabove,technologicalinnovationbecamemoreintensein

theareasoftelecommunicationsand information,aswell as inthenewsystems,

processesand instruments used byfinancial institutions. Thefinancial sector in

10

theUSAmadethemostintensiveuseoftechnologicalinformation,asmeasuredby

relativespendingoncomputerequipmentandsoftware.

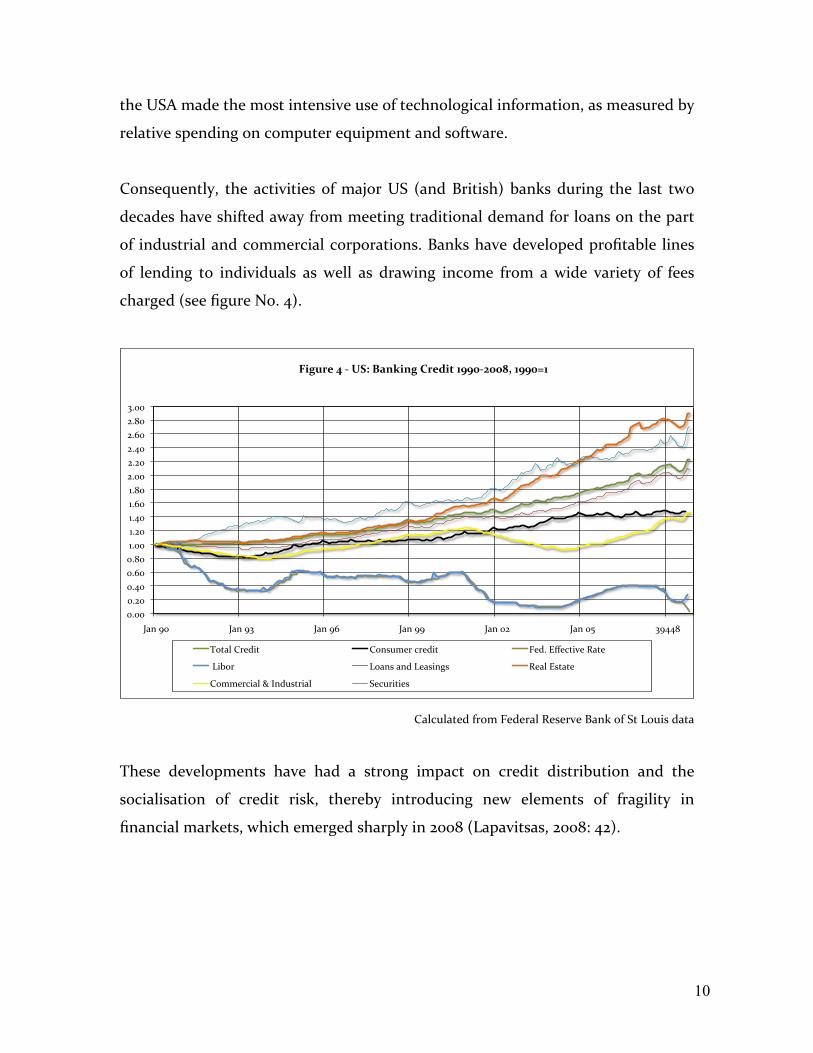

Consequently, the activities ofmajorUS (and British) banks during the last two

decadeshaveshiftedawayfrommeetingtraditional demandforloansonthepart

of industrial andcommercial corporations.Bankshavedevelopedprofitablelines

of lending to individuals as well as drawing income from awidevariety of fees

charged(seefigureNo.4).

!"!!#

!"$!#

!"%!#

!"&!#

!"'!#

("!!#

("$!#

("%!#

("&!#

("'!#

$"!!#

$"$!#

$"%!#

$"&!#

$"'!#

)"!!#

*+,#-!# *+,#-)# *+,#-&# *+,#--# *+,#!$# *+,#!.# )-%%'#

!"#$%&'(')'*+,'-./0"/#'1%&2"3'4556)76689'4556:4'

/01+2#345671# 30,89:54#;45671# <56"#=>5;17?5#@+15#

#A7B04# A0+,8#+,6#A5+87,C8# @5+2#=81+15#

30::54;7+2#D#E,698147+2# F5;9471758#

CalculatedfromFederalReserveBankofStLouisdata

These developments have had a strong impact on credit distribution and the

socialisation of credit risk, thereby introducing new elements of fragility in

financialmarkets,whichemergedsharplyin2008(Lapavitsas,2008:42).

11

4.Theroleofstockmarkets

Stock markets played a decisive role in the crises of 1997‐8 as well as in the

subsequentrecoveryoffinance,anditisimportanttoexaminethemmoreclosely.

The stock market is at the heart of fictitious capital, which takes the form of

financialassets,bothstocksandbonds.1 Inthismarketthespeedoftransmission

isalmost instantaneous,making itevenmoredifficultto foreseecrises.Asarule,

fallsoccurafterphasesofcalmandrecovery,andtheycanbelocalorregional,as

in Asia in 1997‐8, or worldwide, as in theUSA after2008. ThecollapseofWall

Streetin1997wasavoidedbymassivesharebuybacksbylargeconglomerates.

Butthecrisisof1997‐8also revealedtheconsequences,limits,andcontradictions

of financial liberalisation, dominated by large investment funds (pension funds

and mutual funds), major transnational corporations, international banks and

statedebt.Akeypillarofthisinternationaleconomyofcapital‐moneyvalorization

is the secondary capital market, which generates increasing volatility and

instability (Bannock y Manser, 2003:333). The origin and formation of fictitious

capital is to be found in this market, through the issuing of securities, the

formation of large companies via equity, and the immense accumulation of

financialassets.

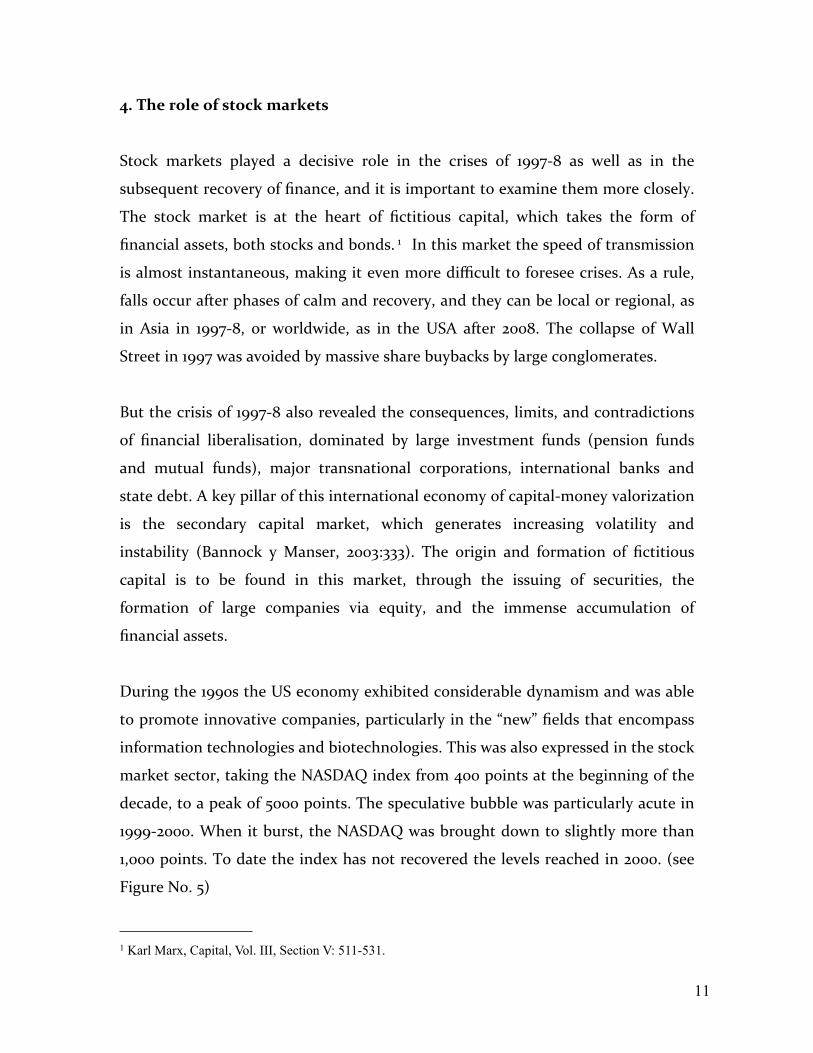

Duringthe1990stheUSeconomyexhibitedconsiderabledynamismandwasable

topromoteinnovativecompanies,particularlyinthe“new”fieldsthat encompass

informationtechnologiesandbiotechnologies.Thiswasalsoexpressedinthestock

marketsector,takingtheNASDAQindexfrom400pointsat thebeginningofthe

decade,to apeakof5000points.Thespeculativebubblewasparticularlyacutein

1999‐2000.Whenit burst, theNASDAQwasbrought downto slightlymorethan

1,000points.Todatetheindexhasnotrecoveredthelevelsreachedin2000.(see

FigureNo.5)

1 Karl Marx, Capital, Vol. III, Section V: 511-531.

12

!"!!#

!"$!#

!"%!#

!"&!#

!"'!#

!"(!#

!")!#

!"*!#

!"+!#

!",!#

$"!!#

$"$!#

$"%!#

$"&!#

$"'!#

$"(!#

!)-!%-$&#%,-!+-$$#$*-!&-$!#!(-$!-!+#%'-!'-!*#!+-$$-!(#%'-!(-!'#$$-$%-!%#!%-!*-!$#%&-!$-!!#$%-!+-,+#!'-!&-,*#%'-!,-,(#$&-!'-,'#

./0123#(#-#45#6789:#;<2:37#=>?/936@#A8B#C8>36#<>?#DE5AEF#@#$,,!-%!!,#G%!!!#H#$I#

A8B#C8>36# D<6?<J#

Source:YahooFinance

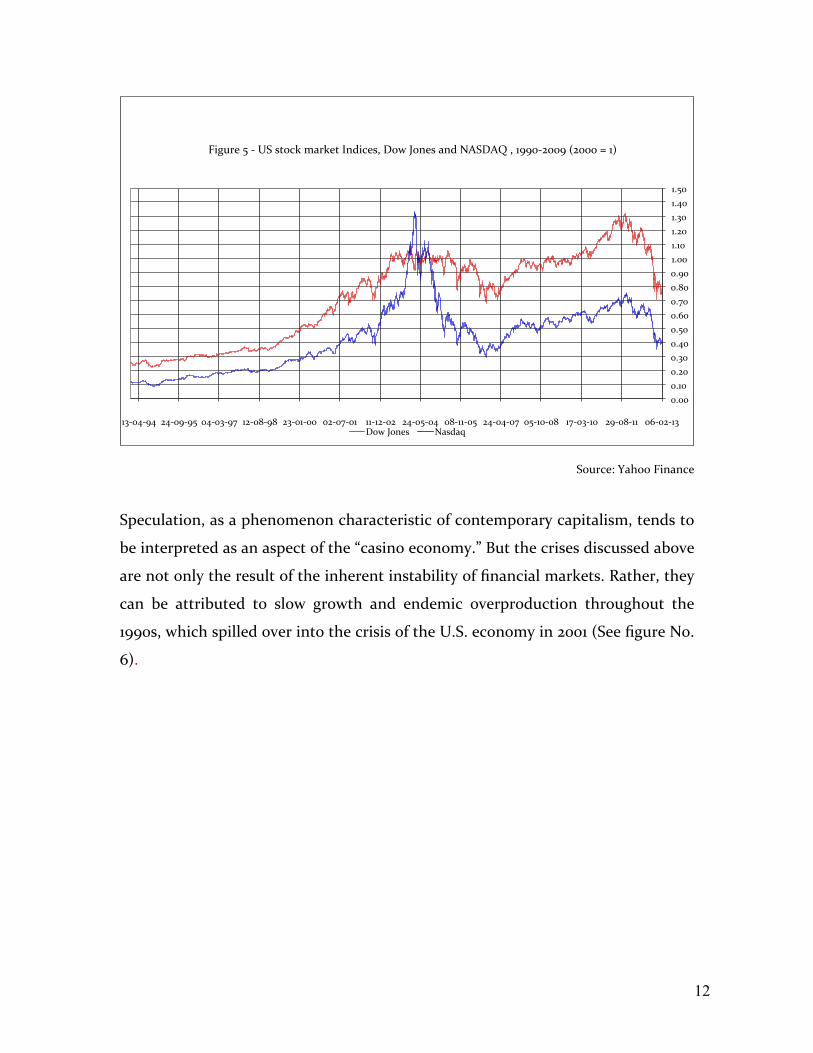

Speculation,asaphenomenoncharacteristicofcontemporarycapitalism,tendsto

beinterpretedasanaspectofthe“casinoeconomy.”Butthecrisesdiscussedabove

arenotonlytheresultoftheinherentinstabilityoffinancialmarkets.Rather,they

can be attributed to slow growth and endemic overproduction throughout the

1990s,whichspilledoverintothecrisisoftheU.S.economyin2001(SeefigureNo.

6).

13

!"#!$

!"%!$

&"!!$

&"&!$

&"'!$

&"(!$

&")!$

&"*!$

&"+!$

&",!$

&"#!$

-./$%!$ -./$%'$ -./$%)$ -./$%+$ -./$%#$ -./$!!$ -./$!'$ -./$!)$ -./$!+$ -./$!#$

!"#$%&'(')'*+',-.$/0%"12''3%4.$50"4-'1-.'61715"08'9::;)<;;='>?1-$1%8'9::;'@'9A'

0.1.2345$ 6789:2438/$

CalculatedfromFederalReserveBankofStLouisdata

Moreover, fictitious capital is a property title and, in the course of the

development of capitalism, property rights are continually reallocated. Mergers

and acquisitions were pronounced in the 1980s, up to the crash of 1987. They

recovered in the1990s andevolvedto theirhistoricpeak in2000. Following the

collapse of Wall Street and NASDAQ in 2000, mergers and acquisitions again

recovered theirdynamism,particularly after 2004. It appearsthat theprocess of

capitalconcentration(mergersandacquisitions)iscyclical,andhistoricallyoccurs

in periods of calm, following crisis and the recovery of the economy. As

concentration takes place, it brings changes in the control of capital and

rearrangesfinancialpowers,thusaffectingworldeconomicconditionsonalllevels.

14

5. Foreign direct investment, mergers and acquisitions, and the rising

poweroftransnationalcompanies

The new financial structure that has emerged encompasses complex processes

formedbyactorsandinstrumentsofaverydiversenature,bothintermsoftheir

originandtheiroperations.They include largecompanies and investmentbanks

specialising in the issuing andplacement of securities; mutual funds (small and

mediuminvestors);hedgefunds(companiesspecialisinginspeculativeshort‐term

operations); pension funds (workers’ retirement savings); insurance companies

andtreasuriesofthetransnationalcompanies.Thenewstructuresdevelopedina

contradictorymanner.Ontheonehand,theycheapenedcreditbut,ontheother,

theycreatednewelementsofinstability,suchasgreaterdispersion,volatility,and

capital speculation. In the emerging Latin Americanmarkets, for instance, they

initiallycheapenedcredit,butlatermadeitmoreexpensive.Butthereisnodoubt

that the so‐called globalisation of financial markets has led to an extraordinary

transnationalisationoftheholdingsofdebtsecurities.

Theresultofthisprocesswasthatforeigninvestmentemergedasthepredominant

form ofcapital transactionson an international scale. The relationship between

foreigndirectinvestmentandportfolioinvestmenthasvariedinthepast25years.

In 1981, fully 19% of the annual flows of private investment were portfolio

investment. However, the 1990s were characterised by growth of capital flows

towarddeveloping economiesmostlythrough institutional investors engaging in

speculative investment and intensifying the volatility of these economies.

Simultaneously,foreigndirectinvestmentbytransnationalcompaniesgrew.Inthe

secondhalfofthedecadeforeigndirectinvestmentbecamethepredominantform

of capital transactions, undertakenbytransnational companiesandinternational

financialgroupsintheformofmergers,strategicalliancesandprivatisations.

From 1993 to 1998 developing economies received 35.3% of total foreign direct

investment,thehighestpercentageinthepasttwodecades(UNCTAD,2002,p.7).

15

Thisfigure is evenmore significant ifwe considerthat the total flow of foreign

direct investment throughout 1990‐1995 remained at an annual average level of

slightlymorethan$225bn.However,in1996thefigureroseto$386bn,andin1997

to $478bn(Sturgeon, 2002;UNCTAD,2002,p.303).During 1995‐1998, developed

countrieschannelledanannualaverageof50%oftheseflowstowardmergersand

acquisitions,whilethecorrespondingfigureforthedevelopingcountrieswas31%.

Duringthisperiod,thefigurebecamedoublewhatithadbeenduringthefirsthalf

ofthedecade(UNCTAD,2002,pp.33,306and337).

Latin America was the most important recipient of foreign direct investment

aimed at mergers and acquisitions throughout the entire decade. Its annual

averageduring theentireperiodwas approximately57.5%. A total ofmorethan

$196bnwasearmarkedformergersandacquisitions, andmostoftheseresources

($125bn)wereinvestedduring1996‐8inBrazil,Argentina,andMexico.Duringthis

period,SouthAsia(India) andEastAsia (China,HongKong, Taiwan), aswellas

Southeast Asia (Indonesia, Republic of Korea, Philippines, Singapore, Thailand,

andMalaysia) also witnessed significant mergers and acquisitions ($44bn). The

largest volume of such resources was directed toward China, Hong Kong, and

SouthKorea.Nevertheless, the greatest volumeofmergersandacquisitionswas

registeredin1999‐2001,wheninvestmentalmostdoubled($82bn).2

The coming together of productive, financial, technological and organisational

factorsalteredtheprofileoftransnationalcorporationsandgavethemthegreatest

powerthey have everhad in the world economy. Theirpercentageshare of the

worldGDProsefrom17%inthemid‐1960s,to24%in1982,andtomorethan30%

in 1995. In that year therewere39,000 transnational companies (includingmore

than4,000 indeveloping countries) thatalreadydictatedthecourseoftheworld

economy, with 270,000 subsidiaries abroad (of which 119,000 operated in

developing countries).At present thereare60,000 transnational companieswith

2 Figures were calculated based on statistical information from UNCTAD, 2002.

16

800,000subsidiaries. Butthedegreeofconcentrationandcentralisationofcapital

is evengreater ifwe considerthat the 100 largest transnational companies (not

including banks and financial companies) controlled a third of foreign direct

investment.During1988‐1995,72%oftheseflowswenttomergersandacquisitions

of all types which, together with strategic alliances, were the international

transactionsthatgrewthemostrapidly.

6.ExtremeweaknessofUSindustryinthelate2000s

DuringthepasttwodecadesthebehaviourofU.S.industry(representingalmosta

thirdoftheworldtotal)hasbeenveryuneven.From1991tomid‐2000,industrial

production rose continuously at an annual average real rate of approximately

4.6%.Nonetheless, beginning in 1998, industrialproductiongrewat increasingly

lower rates, andduring the first fewmonths of 2001 at negative rates. Only in

mid‐2002(almost18monthslater)didratesofchangebecomepositiveagain.And

it was not until the beginning of 2004 that the level of industrial production

reachedagainthelevelsofthehalfof2000.Inall,USindustrialgrowthstagnated

forthreeandahalfyears.Theretreatandstagnationofindustryduringaperiodof

almost fortymonths was reflected in two indicators: first, in the stagnation of

industrialcapacityforalmostthirtymonths(seeFigureNo.6);andsecond,inthe

severefallofcapacityutilisation(MorerayRojas2008:112‐113)

InDecember2008thelevelofindustrialproductionintheUSAwasequivalent to

thatinthesummerof2004.ComparedtoDecember2007,thedropwasnearly8%.

Thiswas thebiggestfall inUS industrial productionsincethe springof1975.US

industrycurrentlystandsat theleveloffiveyearsagoandpresentsthedynamism

of thirtyfive years ago—a difficult predicament.Meanwhile, capacity utilisation

dropped to 73.6%. At its highest, between 1968 and 1973, years ofunrestrained

growth, capacity utilisation in the USA stood at nearly 90%. In the 1980s the

averagelevelofutilizationwasabove80%,andattimesitwasalmost5%higher.

17

Intheautumnof1982USindustryexperiencedoneoftheworstfallsinitshistory

butstillmanagedto recover.Nevertheless,capacityutilisationdroppedto amere

72%attheendofthatdecade,whileinthe1990s—inthewintersof1995and1997

—it achievedmaximum levels of85% during certainmonths. From 1998 to the

present,USindustrywasneverabletoreturntothoseutilisationlevels,evenwith

thedramaticexpansionofcreditinthe2000s,whichstretchedproductionbeyond

itsrealpotential.

Duringtheboomofthe2000sthemaximumlevelofcapacityutilisationlevelwas

registeredattheendof2006andthebeginningof2007.From that timeto 2009

therewasnot merely a deceleration but a cleardecline. The level inDecember

2008,aswasalreadymentioned, stoodat 73.6%,which isworsethanthedropat

theendof2001,butsimilartothelevelregisteredinSeptember1982.Thatwasthe

lowest level in recent US economic history, and furthermore, the most drastic

declinesince1975.Inshort,thefallhasbeentremendous(MoreraandRojas,2008:

112‐113)(seeDiagram6).

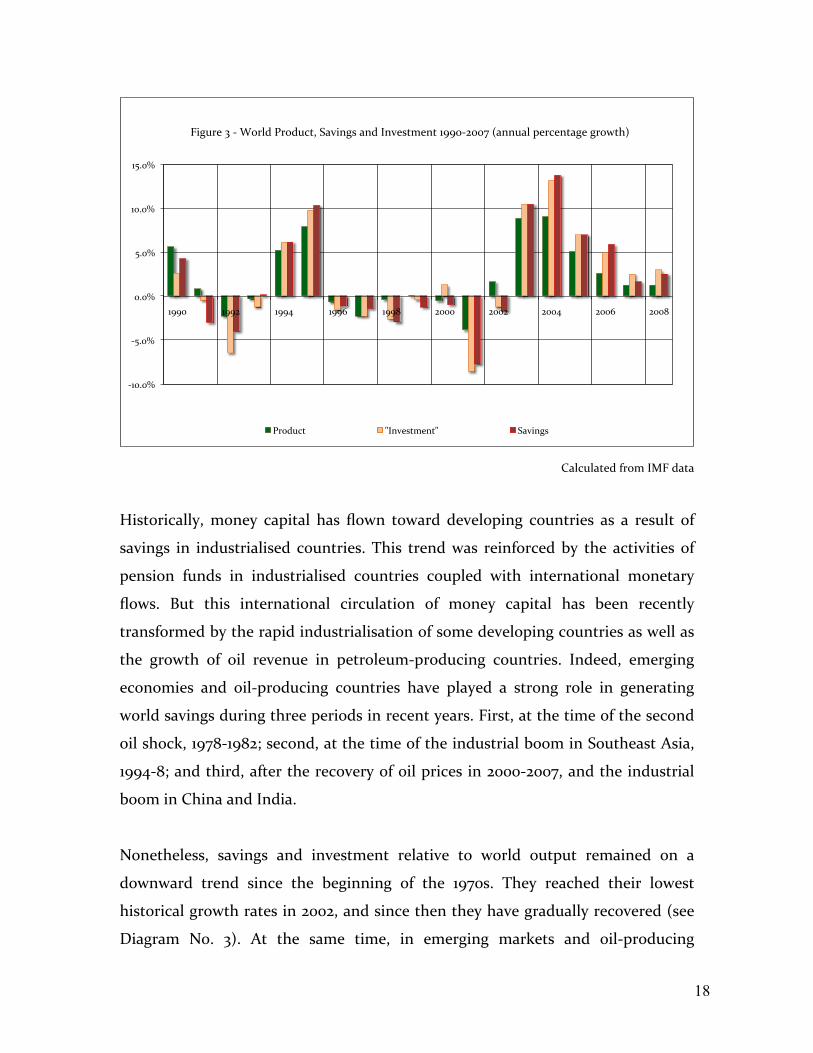

7.Savingsandinvestmentonaworldscale

The import of foreign direct investment, however, becomes clear only in the

context of global savings and investment. Relative to world GDP, international

savingsandinvestmenthaveprogressivelydeclinedoverthepastthirtyyears.The

share of industrialised countries in both savings and investment has remained

dominant, but their share relative to world value added has declined steadily,

falling from 26% in the 1970s to 20% in thenew millennium. (Morera y Rojas,

2008: 101‐102) At the same time, the emerging economies and oil‐producing

countrieshaveboostedtheirsharefromnegativeorverysmallnumbersto nearly

7%(seefigureno.3).

18

!"#$#%&

!'$#%&

#$#%&

'$#%&

"#$#%&

"'$#%&

"((#& "(()& "((*& "((+& "((,& )###& )##)& )##*& )##+& )##,&

-./012&3&!&45167&815709:;&<=>.?/@&=?7&A?>2@:B2?:&"((#!)##C&D=??0=6&E2192?:=/2&/15F:GH&

815709:& IA?>2@:B2?:I& <=>.?/@&

CalculatedfromIMFdata

Historically, moneycapital hasflown toward developing countriesas a result of

savings in industrialisedcountries.This trendwas reinforcedbythe activities of

pension funds in industrialised countries coupled with international monetary

flows. But this international circulation of money capital has been recently

transformedbytherapidindustrialisationofsomedevelopingcountriesaswellas

the growth of oil revenue in petroleum‐producing countries. Indeed, emerging

economies and oil‐producing countries have played a strong role in generating

worldsavingsduringthreeperiodsinrecentyears.First,atthetimeofthesecond

oilshock,1978‐1982;second,atthetimeoftheindustrialboominSoutheastAsia,

1994‐8;andthird,aftertherecoveryofoil pricesin2000‐2007,andtheindustrial

boominChinaandIndia.

Nonetheless, savings and investment relative to world output remained on a

downward trend since the beginning of the 1970s. They reached their lowest

historicalgrowthratesin2002,andsincethentheyhavegraduallyrecovered(see

Diagram No. 3). At the same time, in emerging markets and oil‐producing

19

countriesatendencytowardincreasingsavingsandinvestmentbegantwodecades

ago, except for the years of the Asian crisis. After 2000 the participation of

emerging economies and oil‐producing countries in world savings took an ever

greater importance, in view ofboomingoil prices and industrial development of

China and India (Morera and Rojas 2008: 125, IMF‐GFSR 2007, and UNCTAD,

2006).

Total savingsandinvestment havedoubledinthepast twentyyears. Specifically,

duringthepastfiveyears,savingsroseby50%andthesavingsratereached22.9%

ofworldoutput.Inbroaderhistoricalperspective,worldsavingsin1965amounted

tonearly$4.43tr(inconstant2007U.S.dollars,asfortherestofthefiguresinthis

section).Theythenfell but roseagainduringtheoilboomofthe1970s,reaching

almost $7.35tr in 1979, arateof24.7%.With thedrop inoil prices andthedebt

crisisin1982,worldsavingsexperiencedastrongdecline,fallingto$5.36trin1983,

arateof21.4%.In thecourseof the1980sand1990ssavingsbegan slowly to rise

again, reaching $8.95tr in 1997, corresponding to 23.1% ofworld GDP. This fell

subsequentlyandsavings reachedtheirlowest historical level in2002, at $7.68tr

and20.5%ofworldoutput(MoreraandRojas2008:101‐102).

Since2002savingshaveslowlyrecovered,reaching 22.9%ofworldGDP in2007,

standingatapproximately$11.09tr.Therecoveryofsavingsinthe2000swasdueto

theemergingeconomiesandoilproducingcountries,somethingunprecedentedin

thehistoryofcapitalism.Itwasalso aresult of theactivitiesofpensionfunds in

the USA, Great Britain and Japan (IFSL, 2007). Pension funds have played an

important role in savings and investment partly due to regulatory changes that

allowedentryofforeigncapital inareasandcountriespreviouslyclosed.Thisled

toproliferationofhigh‐risksecuritiesandfinancialassets(MoreraandRojas2008:

107).

Thecirculationofmoneycapitaltowardemergingmarketsisanexpressionofthe

internationaldynamicsofsavings,butalsoreflectstheconditionsofvalorisationin

20

emergingmarkets,namelydynamicindustrialisationandoilproduction.Howdid

theworldeconomy arriveat thisposition? It ispossible thatthisoutcomehasa

connection with the phenomenon of overproduction. However, for most

economists, thecatalystof thisdevelopment isthe qualitative transformation of

Asia, where savingshave increased but investmenthas fallen abruptly since the

endofthe 1990s. This, inturn,hasservedtofinancetheenormousdeficit inthe

US current account. Other economists also stress monetary and fiscal policies

deployedbyAsiancountries.However,thisdoesnotexplainwhyinvestmentflows

havebeendirectedtotheUnitedStateseventhoughotheremergingmarketsoffer

higherinterestrates.

The important point is that theworld financial system is structured under the

hegemonic power of the dollar.3 This was established in the 1980s, when the

United States reachedagreementswith representativesofothercapitalist states,

including the Plaza Accord and theLouvre Accord. It was strengthened in the

1990s when complex economic and political mechanisms were applied for the

purpose of facilitating the handling of world money capital. This includes

regulations and prudential interventions in the practices of the international

bankingsystemandfinancialmarkets.TheBankofInternational Settlementshas

played a vital role in this regard, centralising information and making

internationalbankscomplywithacceptedpracticesinfinancialmarkets.Therole

of the InternationalMonetaryFund hasbeen evenmoreimportant, sinceit has

influenced and designed the capital accumulation of entire countries through

regulatingaccesstoliquidfunds.

Thesepoliciesaccount forthedecreaseinworldinterest ratesthatfacilitatedthe

recoveryofinternationalfinancialflowsandtheendofthecrisis.This isalsothe

contextinwhichthebehaviourofworldsavingshaschanged.Threemajortrends

3 Carlos Morera and Antonio Rojas, “Notas sobre los cambios en la naturaleza del trabajo y la reorganización productiva y financiera mundial,” IIEc, UNAM, May 2007 (at press).

21

emerged in the past decade, as indicated by Jaime Caruana, director of the

MonetaryandCapitalMarketsDepartment oftheIMF:first, increases inforeign

capital flows, primarily toward emerging markets, second, the globalisation of

financial institutions, and third, the globalisation of financial markets (Caruana

2007). That is the background of thedramatic increase in foreign capital flows

(accumulationoffinancialassetswithinternationalinvestmentbanks,publicand

privatedebt portfolios, stocks and debt portfolios, loanportfolios, deposits and

foreigndirect investment).ByApril 2007, theseflowshad risen to $9tr, almosta

fifthofworldoutput(Caruana2007:119).

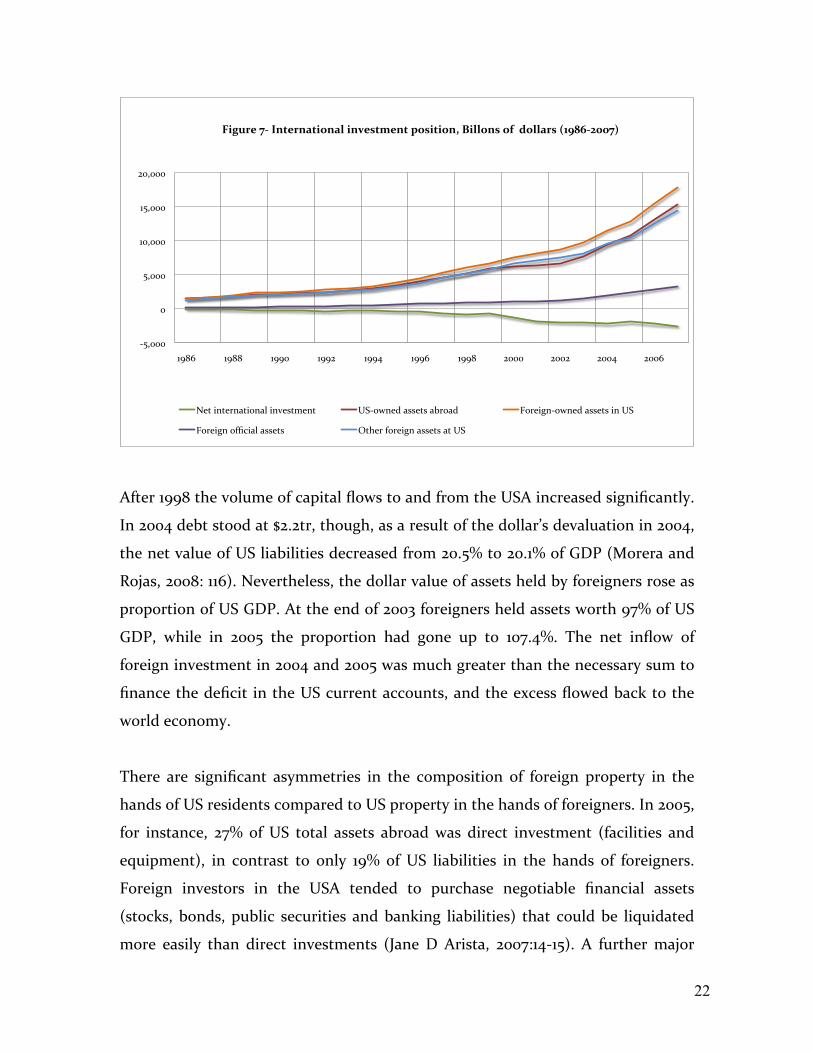

8. The accumulation of US foreign debt and its impact on developing

countries

The USA remained an international creditor until 1985, a position it had

maintainedsinceWorldWarI.However,itsstrengthasworldcreditorhadbeen

deteriorating for some time. From 1986 US foreign debt increased, and its

liabilitiescontinuedto risethroughoutthe1990s.At theendof1996USnetdebt

hadreached$456bn(includingmarketsecurities).Ayearlaterthedebthadrisen

to $776.5bn, equivalent to 13% of its GDP, and before the end of 2000 it had

become$1.3tr,equivalentto18%ofitsGDP,asisshowninfigure7.

22

!"#$$$%

$%

"#$$$%

&$#$$$%

&"#$$$%

'$#$$$%

&()*% &())% &(($% &(('% &((+% &((*% &(()% '$$$% '$$'% '$$+% '$$*%

!"#$%&'()'*+,&%+-,".+-/'"+0&1,2&+,'3.1",".+4'5"//.+1'.6''7.//-%1'89:;<)=>>(?'

,-.%/0.-102./3024%/05-6.7-0.% 89!3:0-;%266-.6%2<132;% =31-/>0!3:0-;%266-.6%/0%89%

=31-/>0%3?@/24%266-.6% A.B-1%C31-/>0%266-.6%2.%89%

After1998thevolumeofcapitalflowstoandfromtheUSAincreasedsignificantly.

In2004debtstoodat$2.2tr,though,asaresultofthedollar’sdevaluationin2004,

thenetvalueofUSliabilitiesdecreasedfrom20.5%to20.1%ofGDP(Moreraand

Rojas,2008:116).Nevertheless,thedollarvalueofassetsheldbyforeignersroseas

proportionofUSGDP.Attheendof2003foreignersheldassetsworth97%ofUS

GDP, while in 2005 the proportion had gone up to 107.4%. The net inflow of

foreigninvestmentin2004and2005wasmuchgreaterthanthenecessarysumto

financethedeficit intheUScurrent accounts,andtheexcessflowedbackto the

worldeconomy.

Therearesignificant asymmetries in thecomposition offoreign property in the

handsofUSresidentscomparedtoUSpropertyinthehandsofforeigners.In2005,

for instance, 27%ofUS total assetsabroadwasdirect investment (facilitiesand

equipment), incontrast to only 19%ofUS liabilities in thehandsof foreigners.

Foreign investors in the USA tended to purchase negotiable financial assets

(stocks,bonds, publicsecurities andbanking liabilities) thatcouldbeliquidated

more easily than direct investments (JaneD Arista, 2007:14‐15). A furthermajor

23

difference is that the Federal Reserve and other entities in theUS government

invested insignificant amounts in other countries. In contrast, foreign public

sectorshadinvestedapproximately$2.3trintheUSA in2005,around16%oftotal

foreign investment. By themiddle of the decade foreign public institutionshad

becomeimportantsourcesofcapitalflowstotheUnitedStates.

Largeflowsofprivate foreign investmentand rapidexpansion inworldliquidity

weretheresultofmonetarypoliciesinindustrialisedcountriesinresponsetothe

recessionof2001(BIS2004).Abundantliquidityandlowinterestratespropelleda

global search for greater returns. With a view to protecting profitability, the

Federal Reserve increased interest rates after 2004 and reduced the rate on

sovereignbonds, aprocess that lasted until September 2007. At the same time,

securitiesmarketsinemergingeconomieswerestimulated.Moreover,theFederal

Reserveencouragedcommercial loansindollarsinplaceof loansinyen, thereby

renewing speculative interest inUS financial securities. All these developments

took place while the international system of bank payments continued to be

dominatedby a few currencies, aboveall, the dollar, theeuro, the yenand the

pound.

As a consequence of these trends, foreign portfolio investment in emerging

economies reached high levels in the third quarter of 2005 (BIS, 2005c). The

increase in liquidity in theUnitedStates, Japan andmany emerging economies

intensified in 2005. The plethora of capital spilled over into other national

markets,andinsomecasesevenreturnedtothemarketswhereithadoriginated.

Still, excess liquidity was spread throughout the world economy, encouraging

growthofdomesticcreditintheUSAandelsewhere.

Thelinkbetweendomesticandforeigndebtwasfundamental,sincebothhavean

effect onUS andglobal demand. Rapid financial liberation in the1980s andthe

relaxation of prudential norms for granting loans exacerbated domestic debt

accumulation. US households went increasingly into debt during 1995‐2005,

24

associatedwith adecrease in the rate of saving and increases in consumption.4

Aware of easy credit availability, consumers considered access to credit as a

substitute forsavings, especially after2002,whendebt wasusedbothtoacquire

appreciating residential property and to extract liquidity for consumption.

Enterprisealso tookadvantageoflowratesinbondsmarketstoapplyforloansin

ordertorepurchasebondsorstocksin thesecondarymarket,thusstrengthening

theirprofitability.

In short, privatecapitalwas the driving force behind international capital flows

andanimportantsourceoftheexpansionofcredit intheUSA.Atthesametime,

excessive volumes of foreign private capital appeared, exacerbating investment

flows out of the USA, and increasing liquidity both in the USA and theworld

market.Moreover,massiveamountsofforeigngovernmentinvestmentstookplace

intheUSA.Foremergingeconomies,thesetrendshadconsiderablerepercussions,

driving monetary authorities in those countries to intensify the level of

intervention.Theaimwasto stopappreciationofdomesticcurrencyandcontain

domesticgrowthofmoneyandcredit.Consequently,theaccumulationofreserves

played a fundamental role in the processofexpansionand contraction, creating

furtherscopeforgenerationofinternationalliquidity(seeDiagram7).

To put itdifferently,thestrategiesusedbythe largeprivatefinancial institutions

dominating the international payments system to increase their profits also

intensified the vulnerability of emerging economies. As more developed and

developing countriesfreedtheircapital accountsinthe 1990s, thevalueoftheir

currenciescameincreasinglyto dependontheoperationsconductedbyfinancial

amongvariousfinancialinstrumentsandmarkets,ratherthandependingontrade

(Cornford,2005).Changesinthedifferentialsamonginterestratesdenominatedin

differentcurrenciesbecamethedriving forcebehindcapitalandforeigncurrency

4 Family debt increased from 65.7% of the GDP in 1995 to 92.1% at the end of 2005. Federal government debt, on the other hand, diminished during that same period from 49.2% to 37.2% of the GDP.

25

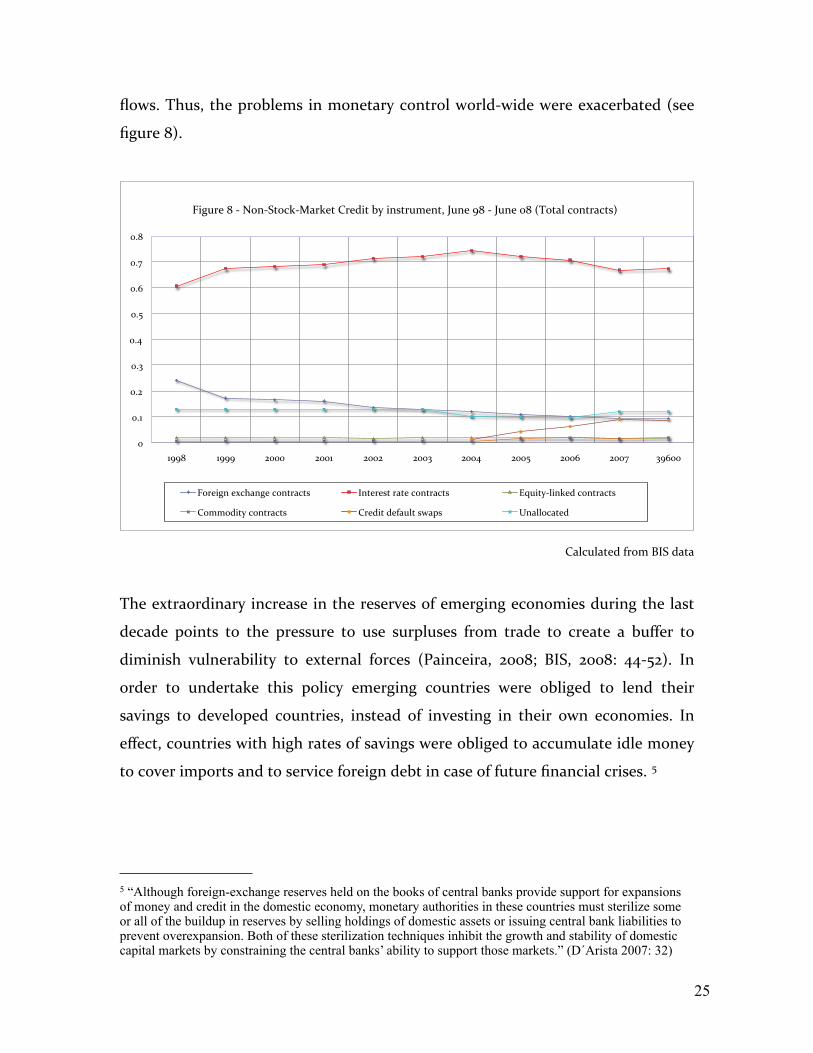

flows.Thus, theproblemsinmonetarycontrolworld‐widewereexacerbated(see

figure8).

!"

!#$"

!#%"

!#&"

!#'"

!#("

!#)"

!#*"

!#+"

$,,+" $,,," %!!!" %!!$" %!!%" %!!&" %!!'" %!!(" %!!)" %!!*" &,)!!"

-./012"+"3"45637859:3;<1:28"=12>.8"?@".6A810B268C"D062",+"3"D062"!+"EF58<G"95681<98AH""

-512./6"2I9J<6/2"95681<98A" K68212A8"1<82"95681<98A"" [email protected]:2>"95681<98A"

=5BB5>.8@"95681<98A" =12>.8">2N<0G8"AO<PA" Q6<GG59<82>"

CalculatedfromBISdata

Theextraordinaryincreaseinthereservesofemergingeconomiesduringthelast

decadepoints to the pressure to use surpluses from trade to create a bufferto

diminish vulnerability to external forces (Painceira, 2008; BIS, 2008: 44‐52). In

order to undertake this policy emerging countries were obliged to lend their

savings to developed countries, insteadof investing in their own economies. In

effect,countrieswithhighratesofsavingswereobligedtoaccumulateidlemoney

tocoverimportsandtoserviceforeigndebtincaseoffuturefinancialcrises.5

5 “Although foreign-exchange reserves held on the books of central banks provide support for expansions of money and credit in the domestic economy, monetary authorities in these countries must sterilize some or all of the buildup in reserves by selling holdings of domestic assets or issuing central bank liabilities to prevent overexpansion. Both of these sterilization techniques inhibit the growth and stability of domestic capital markets by constraining the central banks’ ability to support those markets.” (D´Arista 2007: 32)

26

Consequently,emergingeconomieslostsomecapacitytoinvestproductively.They

wereobligedtoconcentratemassivereservesasamechanismofcompensatingfor

the inflowofforeigncapital. Themassiveaccumulationofreservesstrengthened

theirrelianceonthedominantcurrencies,andparticularlyonthedollar,themain

internationalcurrency(Lapavitsas,2008:43).

9.Conclusion

Restoring the rate of profit has been the focus of efforts by both state and by

capital, since the crisis of the 1970s. Profound changes have taken place in the

social relations of production between capital and labour formore than three

decades. Thescopeof capitalist operationshas been considerably broadenedby

thecollapseoftheso‐calledsocialistregimesandtheprofoundtransformationof

China. But a most striking development is that, under the predominance of

banking capital and the hegemony of the US dollar, the strategy of

‘financialisation’wasimposedonallformsofcapital.

Vital to ‘financialisation’ were changes in the labour force as well as a

transformationofthestate.Thenatureofworkhasalteredandmanyofthesocial

advances achieved in earlier periods were reversed, particularly in education,

healthservices,andpension systems.Newfinancial institutions, operatingunder

thelogicofprivateprofitability, transformedthewageincomeofbothproductive

and unproductive labour into financial assets. Workers were thus subjected to

even greater exploitation. In addition, the state privatised strategic enterprises

underitscontrol,andallowedcentralbankstoplayastrategicroleindetermining

interest rates and operating monetary policy. These transformations generated

favourableconditionsforplacinggreatmassesofsavingsinthehandsofcapitalas

neverbefore,thusmakingitpossibletoexpandcredit tothelimit.Largepartsof

thiswealthcamefromdevelopingcountries.

27

Theworldeconomyhasbecomeintegratedindifferentways,alsoasaresultofthe

immensesocial,politicalandculturaltransformationsthathavetakenplace.Butat

presenttheworldeconomyisonceagainincrisis,perhapsoneoftheworstcrises

inthehistoryofcapitalism.Thisisthefirst fully‐fledgedcrisisofglobalisation,or

“financialisation”,withtheUnitedStatesattheepicentre.Despitethetriumphof

neo‐liberalism in recent years, the crisis presents an opportunity to put

alternativesinplaceandpreventamerereorganisationofneoliberal policiesand

methods.

28

Bibliography

Blackburn,R.2002.“LadebacledeEnronylacrisisdelosfondosdepensiones.”New

LeftReviewLtd/EdicionesAkal,S.A.,Vol.14,No.p.25.

Cornford,A.2005."ReflectionsonthePrediction,ManagementandMeasurementof

(PrimarilyFinancial)Risk."September30October1,Geneva.

Chesnais,F.1999.Lamundializaciónfinanciera.Génesis,costoydesafíos.Buenos

Aires:Losada.

D’AristáJane,“U.SDebit andglobal imbalance”, International JournalofPolitical

Economy,Vol.36,núm.4,2004,pp.12‐35.

Dicken,P. (1998).GlobalShiftTransformingtheWorldEconomy.PaulChapman

Publishing.Londres.

DosSantos,P.“Onthecontent ofbankingin thecontemporarycapitalism”,enA

CrisisofFinancialisation,HistoricalMaterialismyBrillPublishers,2008.

Dumenil, G., D. Lévy (2004). Capital Resurgent, Roots of the Neoliberal

Revolution.London‐Cambridge(Mass.).HarvardUniversityPress.

Dymski, G. “The Political Economy of the SubprimeMeltdown”, en A Crisis of

Financialisation,HistoricalMaterialismyBrillPublishers,2008,

Ergunes, N. “Financialisation in developing countries: A study of the Turkish

economy”,enACrisisofFinancialisation,HistoricalmaterialismyBrillPublishers,

2008.

29

Greenspan, A. (2003). "Address to the 21 st Annual Monetary Conference

CosponsoredbyTheEconomist and theCato Institute"(November).Availableat

thewww.federalreserve.gov/boarddoccs/speeches/2003/20031120/default.htm.

Gill,L.(2002).Fundamentosylímitesdelcapitalismo.Madrid.Trotta.

Itoh, M. “The Japanese and the American crises compared”, en A Crisis of

Financialisation,HistoricalMaterialismyBrillPublishers,2008.

Lall,S.2000.TheTechnological structureandperformanceofdevelopingcountry

manufacturedexports,1985‐98.Oxford.

Lapavitsas, C. 2005. “Power and Trust as Constituents of Money and Credit.”

HistoricalMaterialism,14(1):129‐154.

____________(2008) “Financialised Capitalism: Instability and financial

expropriation”, en A Crisis of Financialisation, Historical Materialism y Brill

Publishers,2008.

_____________The relevance of Hilferding’s ‘Finance Capital’ to financialised

capitalism,enACrisisofFinancialisation,HistoricalMaterialismyBrillPublishers,

2008.

Marx,C.(1976).ElCapital.MexicoCity:SigloXXIEditores.

Morera, C. (1998). El capital financiero enMéxico y la globalización : límites y

contradicciones.MexicoCity:EdicionesEra.

______C.(2002).“LanuevacorporacióntrasnacionalenMéxicoylaglobalización.”

pp.397‐434 inGlobalizaciónyalternativasincluyentesparael sigloXXI, editedby

30

DoloresdelaPeña,MarisolSimón,CarlosMorera.MexicoCity:UNAM(FE,CRIM,

IIEc,DGAPA)UAM‐Azcapozalco.

______yA.Rojas(2007).“Notassobreloscambiosenlanaturalezadeltrabajoyla

reorganizaciónproductivayfinancieramundial”.IIEc,UNAM,mayo de2007(en

prensa)

______ yA. Rojas (2008). “Mercadomundial de dinero y renta petrolera”, en La

guerra del fuego, coordinado por Guillaume Fontaine y Alicia Puyana, Facultad

LatinoamericanadeCienciasSociales(FLACSO)yMinisteriodecultura.

Moseley,F.2007.“IstheU.S.Economyheadedforahardlanding?”publishedbyFred

Moseley.[enerode2008]in:http://www.mtholyoke.edu/~fmoseley/

NSF (National Science Foundation) (2000). Science and Engineering Indicators

2000.Washington,D.C.

OCDE.2000a.DifferencesinEconomicGrowthacrosstheOECDinthe1990s:The

Role of Innovation and Information Technologies. Paris: OECD, Directorate for

Science,TechnologyandIndustry.

ONUDI.2002.Informesobreeldesarrollo industrialcorrespondientea2002/2003,

Competirmediantelainnovaciónyelaprendizaje.Vienna:ONUDI.

Painceira, J.P. “Financialisation and Financial crises: the role of developing

countries”,enACrisisofFinancialisation,HistoricalMaterialismyBrillPublishers,

2008.

Papadatos,D.“Central Banking incontemporarycapitalism:monetarypolicyand

itslimits”,enACrisisofFinancialisation,HistoricalMaterialismyBrillPublishers,

2008.

31

UNCTAD. 2002. “World Investment Report 2002: Transnational Corporations and

Export Competitiveness.” p. 345, New York and Geneva: published by the United

Nations.

UNCTAD. 2003. “World Investment Report 2003: FDI Policies for Development:

NationalandInternationalPerspectives.” p.297, NewYorkandGeneva,published

bytheUnitedNations.

NoteGraphicsdatabase:

The graphics of the United States of America have been elaborated with the

databaseoftheBoardofGovernorsoftheFederalReserveSystem:FlowsofFunds

Accounts,Statistics:ReleasesandHistoricalData.

EconomicsandFinancialWorld:

BIS (Bank for International Settlements) (2003, 2004, 2005, 2006, 2007, 2008)

AnnualReport.

______ (2005b y c, 2006, 2007) Quarterly Review of International banking and

FinancialmarketDevelopments.

IMF (InternationalMonetaryFund) (2006),Perspectivade la economíamundial

2005,WashingtonD.C.:IMF.

IMF(InternationalMonetaryFund)(2007),Global FinancialSabilityReport2007,

WashingtonD.C.:IMF.

WorldBankAnnualReport1998‐2007

32

Petroleum:

BPAnnualReportandAccounts2007

International Energy Annual (IEA) 2005, 2007, 2008, EIA Energy Information

AdministrationOfficialEnergyStatisticsfromtheU.S.Government.