Embed Size (px)

Citation preview

ASIAN DEVELOPMENT BANK TAR: IND 30536

TECHNICAL ASSISTANCE

TO

INDIA

FOR THE

STRENGTHENING HOUSING FINANCE INSTITUTIONS PROJECT

July 1997

CURRENCY EQUIVALENTS(as of 30 June 1997)

Currency Unit - Rupee/s (Re/Rs)Rel .00

= $0028$1.00

= Rs35.80

For the calculations in this Report, an exchange rate of Rs35.6 = $1.00 has beenused. This was the rate prevailing at the time of Fact-finding for the technicalassistance.

ABBREVIATIONS

CFIEAEWSHDFCHFCHFIHUDCOIRAILIGNGONHBTA

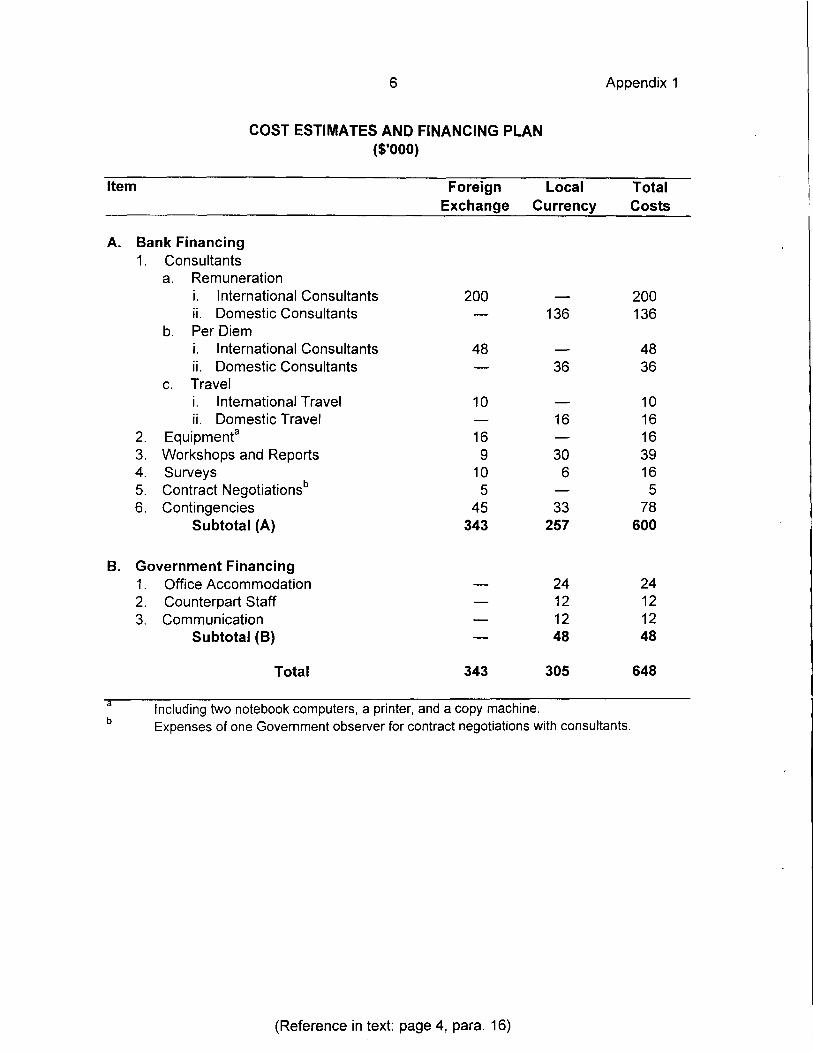

Community-based Financial InstitutionExecuting AgencyEconomically Weaker SectionHousing Development Finance CorporationHousing Finance CompanyHousing Finance InstitutionHousing and Urban Development Corporation, LtdInsurance Regulatory Authority of IndiaLow-income GroupNongovernment OrganizationNational Housing BankTechnical Assistance

NOTES

(i) The fiscal year of the Government ends on 31 March.(ii) In this Report, '$" refers to US dollars.

I. INTRODUCTION

1. In 1996, the Government of India requested the Bank to provide technicalassistance (TA) for strengthening housing finance institutions (HFls) in the country. Inresponse to the request, a Bank Fact-finding Mission visited India in February 1997. TheMission had discussions with representatives of Government agencies, HFIs, researchinstitutions, bilateral aid agencies, nongovernment organizations (NGOs), and members ofsavings and credit groups in rural and urban areas, and reached an understanding with theGovernment on the objectives, scope, cost estimates, financing plan, implementationarrangements, and the terms of reference for the consulting services under the TA.1

II. BACKGROUND AND RATIONALE

2. The Government has given high development priority to housing since the firstFive-year Plan. However, unfulfilled housing needs are still high, especially among low-incomegroups (LIGs) and economically weaker sections (EWSs) 2 in the country. In preparation of theNinth Five-year Plan (1997/98-2001/02), a Sub-Group on Financing of Urban HousingDevelopment estimated that the housing shortage by the end of the Eighth Plan was about 8million units. During the Ninth Plan another 9 million units will be needed, resulting in a totaldemand of about 17 million housing units by the year 2002. Of the total unfulfilled demand,LIGs and EWSs account for more than 80 percent. The Sub-Group estimated that the financialresources required to eliminate the housing shortage would be about Rsl,214 billion ($34billion). The Bank has provided TA for formulating the urban development strategy, includinghousing, in the Ninth Plan.3

3. In the early five-year planning periods, a variety of interventions by Central andstate agencies to reduce the housing shortage for LIGs and EWSs through budgetary supportmet limited success. Most of the programs were implemented by state housing boards andslum improvement boards with little concern for cost recovery or sustainability. The role of suchagencies is still important in some states where they are being reorganized and are acting asfacilitators in line with the National Housing Policy. The Government has undertaken severalother institutional and policy measures to encourage the establishment of market-orientedHFIs.

4. The National Housing Bank (NHB), established in 1988 and owned by theReserve Bank of India, is responsible for promoting, regulating, and providing refinancing andequity support for private housing finance companies (HFCs). The principal financing activity ofNHB has been promoting the growth of HFCs through refinancing and equity investment.Recently, NHB expanded its operations into the retail housing finance market and has beenactively promoting the development of a secondary mortgage market. As an apex institution inhousing finance, NHB plays a crucial role in developing a sound and effective housing financesystem. Facing the increasingly competitive housing finance market in the wake of financialderegulation in the country, NHB needs to review its objectives, functions, and operations todevelop its long-term business strategies.

The TA first appeared in ADB Business Opportunities in January 1997.2

EWS is officially defined as a household with a monthly income below Rs2,100; LIG is a household with amonthly income between Rs2,100 and Rs4,500.TA No. 2098-IND: Urban Sector Proffle, for $400,000, approved on 14 June 1994.

2

5. The Housing Development Finance Corporation (HDFC), a private institution,was the only large HFC until recently when Government liberalization and support mechanismswere initiated. Over the past two decades, HDFC has expanded rapidly with loan approvalsgrowing at an annual rate of 42 percent. HDFC is a listed public company with a triple A rating,and the bulk of its lending goes to middle- and upper-income groups. The Housing and UrbanDevelopment Corporation (HUDCO) - a Central Government undertaking - and various stateagencies have been responsible for providing shelter for low-income families. Since itsinception, HUDCO has committed Rs129 billion ($3.7 billion) to housing development projects,which will provide over 6 million housing units. More than 90 percent of the units are targeted atLIGs and EWSs.

6. External funding agencies have provided substantial assistance to HUDCO,HDFC, and NHB. The United States Agency for International Development (USAID) provided a$150 million loan to HDFC in 1983 for operational expansion, and a $6.4 million technicalassistance grant to NHB for a five-year capacity-building program, which will end this year.Recently, USAID provided a $40 million line of credit to NHB with the objectives of mobilizingmarket-derived resources, strengthening NHB's regulatory functions, and expanding the supplyof housing finance to LIGs and EWSs. Subsequent to the International Finance Corporation'sinitial equity investment in HDFC, the World Bank approved a loan of $250 million to HDFC in1988, which enabled HDFC to expand rapidly into wider geographic areas and build up itsinstitutional capacity. Since 1984, the German Kreditanstalt für Wiederaufbau has assistedHUDCO and HDFC through grants, loans, and credit lines in lending to LlGs and EWSs inurban and rural areas. The assistance will enable HUDCO to build 350,000 low-cost housingunits for EWS families, and HDFC to extend housing assistance to about 85,000 households.

7. While the efforts of the Government, HUDCO, HDFC, NHB, and external fundingagencies have provided significant financing assistance to LIGs and EWSs, financial flows to[IC and EWS households still lag behind the growth of the housing finance market. AlthoughLIGs and EWSs account for more than 80 percent of the unfulfilled housing needs and 49percent of the total housing finance requirement, the share of households below the annualmedian income 1 in housing loans is only 13.5 percent. Studies show that the fact that themajority of the formal 2 HFIs have not been able to effectively reach the low-income segments ofthe housing finance market often reflects their inappropriate approach and lending structure,rather than affordability of the loans to the poor. For loan considerations, the formal HFIs relyon standard appraisal procedures, which are cumbersome to the poor and provide larger loanswhereas the poor prefer smaller amounts.

8. Inadequate support from formal financial institutions for the finance needs ofLIGs and EWSs has led to a large number of community-based financial institutions (CFI5)entering the field of housing finance. More than 32,000 credit cooperative societies and about1,400 cooperative banks with more than 3,400 branches throughout India provide basicfinancial services to the LIGs and EWSs. However, few of these CFIs have been able toprovide sustainable housing finance to the poor, partly because of lack of access to adequatefinancial resources available only from formal financial institutions, and partly because of theirlack of managerial skills.

In 1996, this was estimated at Rs40,000,The formal sector includes all financing institutions under Government regulations, while the informal sectorcovers community-based financial institutions, NGOs, and individual moneylenders.

'I

9. To increase financial flows for housing to low-income households, the linkagesbetween informal credit networks and formal financial institutions need to be expanded. HFIstend to consider lending to CFIs as cost-ineffective and risky because the size of loans to low-income families is usually small and therefore entails higher operating overheads. In addition,low-income families normally cannot produce the conventional security to meet the lendingrequirements of HFls.

10. To enable formal HFIs to more effectively reach the low-income segments of thepopulation, there is a need to (i) develop a consistent and systematic methodology to evaluatethe CFIs and NGOs; (ii) provide HFIs with guidelines on lending to CFIs; (iii) study themechanism of providing reasonable coverage to the risks that formal HFIs will have to bear inreaching the low-income market; and (iv) assist major HFIs' ongoing training programs in"training the trainers" of key personnel in both the formal and informal HFls.

11. One mechanism for risk coverage is the establishment of a housing loaninsurance fund. Such a fund will provide insurance to both primary and secondary lenders in thehousing finance market. A lending program that consciously expects 2 to 3 percent of all loansmade to result in default should result in approval of more qualified applicants than a programthat endeavors to eliminate all prospective defaulters. An initial study on India's mortgageinsurance market shows that a properly designed insurance scheme will make housing financemore affordable, and can therefore expand the market by about 15 percent.

12. The slow development of the linkage between the formal and informal housingfinance sectors also reflects a lack of incentives for CFIs and NGOs to enter the formal sector.CFls and NGOs need to look beyond their service delivery functions, reduce the cost of theiroperations, improve operating efficiencies, and expand operational coverage. There is thereforea need to find ways of incorporating incentives into the housing finance programs of CFls andNGOs, as well as examine the role of NHB in promoting the efficiency of the formal and theinformal housing finance sectors.

13. The TA will support the Bank's overall strategic objectives to assist theGovernment in increasing economic efficiency, achieving higher levels of sustainable economicgrowth, and reducing poverty. In operational terms, the Bank's strategy in finance and capitalmarkets will assist in developing a sound financial system conducive to efficient mobilizationand allocation of resources, including reforming the housing finance system throughenhancement of competition and deregulation, strengthening the nonbanking informal sector,and supporting housing loan securitization. The Bank's housing finance sector strategy as wellas its strategic objectives, and the Government's National Housing Policy are all consistent.The Bank's housing sector strategy focuses on (i) creating a conducive policy framework formerging the informal and formal approaches to provision of housing and modernizing thehousing finance systems, (ii) improving access of the poor to housing, and (iii) enhancinginstitutional capacity at all levels to improve efficiency in the delivery of housing finance. TheBank's current Country Assistance Plan for India includes the Bank's first loan to the housingfinance sector. Low-income groups are the major targeted beneficiaries of the proposed loan.Consequently, the TA is closely linked to the Bank's sector operations, as the findings of the TAwill help the financial institutions reach the targeted groups.

4

III. THE TECHNICAL ASSISTANCE

A. Objectives

14. The TA will assist the Government n promoting financial flows to the housingsector by (I) facilitating the integration of formal and informal financial institutions, particularlycommunity-based organizations, through development of suitable mechanisms to promotemutual understanding and formal business linkages; (ii) assessing the feasibility, efficiency, andoperational aspects of a housing loan insurance fund covering community-based housingfinance insurance as well as general mortgage insurance; (iii) determining the actionsnecessary to strengthen NHB as the apex HFI and a regulator in the sector; (iv) providingtraining assistance to HFIs through HUDCO for the development of community-based housingfinance; and (v) examining ways and means to promote a bigger role for the private sector inthe development of housing finance.

B. Scope

15. The TA will comprise three parallel parts. Part A will focus on the (i) promotion ofmutual understanding between HFIs and CFls on one hand and NGOs on the other throughdevelopment of a consistent and systematic methodology for HFls to evaluate CFls and NGOs,and for the latter to understand the operational requirements of formal financial institutions; (ii)design and implementation in selected communities of pilot projects to test the recommendedmethodology; (iii) development of necessary guidelines for NHB with respect to refinancingHFIs' lending to CFIs; and (iv) providing "training for the trainers" through workshops for thestaff of key HFIs that on-lend to CFIs. Part B will focus on the feasibility of establishing ahousing loan insurance fund. The study will evaluate legal, organizational, operational, andfinancial aspects of the fund, and recommend detailed implementation and operationalprocedures including the role of the Government and the private sector. Part C will evaluate theoperational effectiveness of NHB. The study will develop benchmarks in the key result areas ofNHB, which will measure its future performance vis-à-vis its mission statement.

C. Cost Estimates and Financing Plan

16. The estimated cost of the TA is $648,000 equivalent, comprising $343,000 inforeign exchange cost and $305,000 equivalent in local currency cost. The Bank will provide agrant of $600,000 to finance the foreign exchange cost and $257,000 equivalent of the localcurrency cost. The Government will finance the remaining $48,000 equivalent, which will coverthe cost of counterpart staff, communications, and office rentals. The details of cost estimatesand financing arrangements are presented in Appendix 1.

0. Implementation Arrangements

17. The Department of Economic Affairs of the Ministry of Finance will be theExecuting Agency (EA) for the TA. A Project Office will be established in NHB. A generalmanager in NHB will serve concurrently as the Project Director for the implementation of theTA. Counterpart staff from NHB, HUDCO, and HDFC will be working in the Project Officetogether with the TA consultants. The training for staff of HFIs in lending to CFIs will make useof the facilities of Habitat Polytech, which is HUDCO's training arm for CFI and NGO lending.The EA will ensure that adequate office space and qualified counterpart staff are available to

5

the consultants, and will coordinate with other Government agencies in providing necessarysupport to the consultants, including access to information and project sites, and facilities.

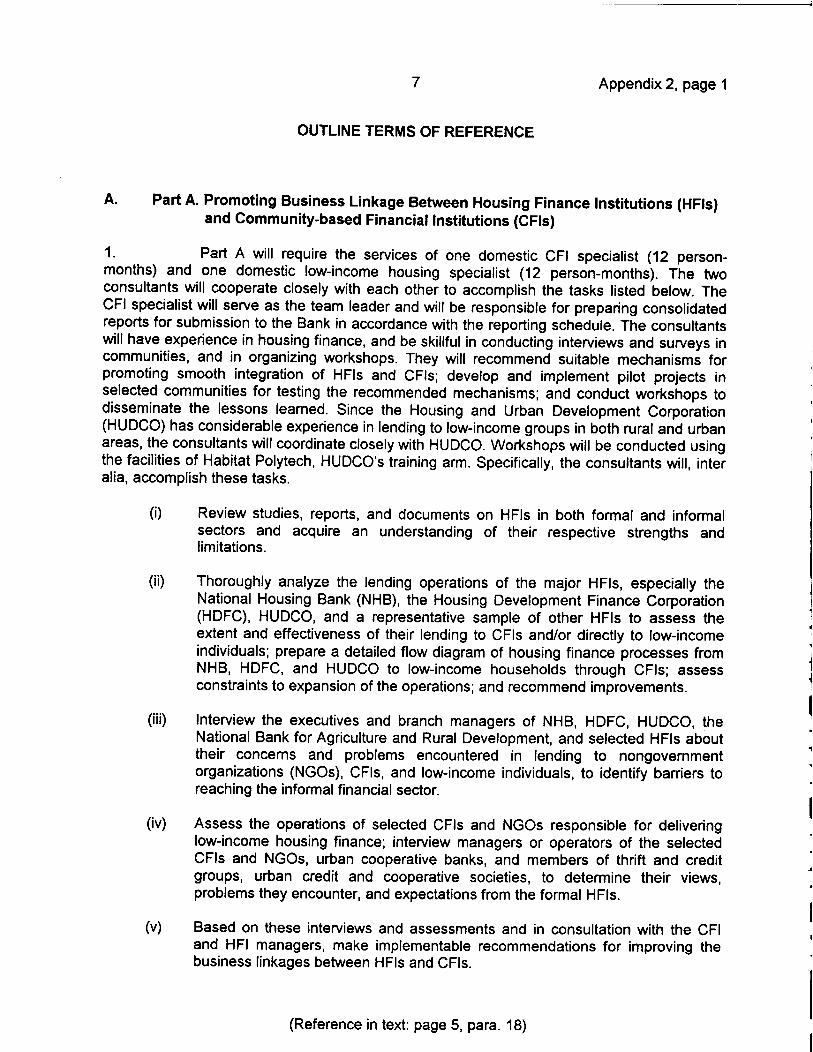

18. The TA will be carried out over 14 months by two international and four domesticindividual consultants, with expertise in housing finance, financial institution development andmanagement, mortgage insurance, and housing finance through CFIs. About 40 person-monthsof consulting services (about 8 person-months international and 32 person-months domestic)will be required. The consultants will be recruited in accordance with the Bank's Guidelines onthe Use of Consultants and other arrangements satisfactory to the Bank on the engagement ofdomestic consultants. Outline terms of reference on consulting services are given in Appendix2. To ensure timely implementation, essential office equipment will be procured by theconsultants under the TA following direct purchase procedures satisfactory to the Bank.

19. The consultants for each part of the TA will submit to the Bank a separateinception report one month after commencement of services. The consultants for Part A willsubmit an interim report within six months on findings and recommendations for discussion at aworkshop with participation of representative stakeholders. A draft final report will be submittedwithin 12 months, presenting the initial assessment of the pilot projects. The consultants forPart B will submit an interim report, within two months of commencement of services,describing the preliminary findings for discussion at a workshop with participation of concernedGovernment agencies and representatives of HFIs, CFIs, and private institutional investors. Adraft final report for Part B will be submitted within five months. For Part C, the consultants willsubmit an inception report within one month after commencement of services, and a draft finalreport within three months. The final reports for all three parts will be submitted one month afterthe receipt of consolidated comments from the Bank and the Government. The TA is expectedto be completed in October 1998.

IV. THE PRESIDENT'S DECISION

20. The President, acting under the authority delegated by the Board, has approvedthe provision of technical assistance, on a grant basis, to the Government of India in an amountnot exceeding the equivalent of $600,000 for the purpose of the Strengthening Housing FinanceInstitutions Project, and hereby reports such action to the Board.

6

Appendix 1

COST ESTIMATES AND FINANCING PLAN($'OOO)

Item

Foreign Local

Total

Exchange Curren

Costs

A. Bank Financing1. Consultants

a. RemunerationI. International Consultants 200 - 200ii. Domestic Consultants - 136

136

b. Per Diemi. International Consultants 48 - 48ii. Domestic Consultants - 36

36

c. Traveli. International Travel 10 - 10ii. Domestic Travel - 16

16

2. Equipment816 - 163. Workshops and Reports 9 30

39

4. Surveys 10 6

165. Contract Negotiationsb 5 - 56. Contingencies 45 33

78

Subtotal (A) 343 257

600

B. Government Financing1. Office Accommodation - 24

24

2. Counterpart Staff - 12

123. Communication - 12

12

Subtotal (B) - 48

48

Total 343 305

648

Including two notebook computers, a printer, and a copy machine.b Expenses of one Government observer for contract negotiations with consultants.

(Reference in text: page 4, para. 16)

7 Appendix 2, page 1

OUTLINE TERMS OF REFERENCE

A. Part A. Promoting Business Linkage Between Housing Finance Institutions (HFI5)and Community-based Financial Institutions (CFIs)

1. Part A will require the services of one domestic CFI specialist (12 person-months) and one domestic low-income housing specialist (12 person-months). The twoconsultants will cooperate closely with each other to accomplish the tasks listed below. TheCFI specialist will serve as the team leader and will be responsible for preparing consolidatedreports for submission to the Bank in accordance with the reporting schedule. The consultantswill have experience in housing finance, and be skillful in conducting interviews and surveys incommunities, and in organizing workshops. They will recommend suitable mechanisms forpromoting smooth integration of HFIs and CFls; develop and implement pilot projects inselected communities for testing the recommended mechanisms; and conduct workshops todisseminate the lessons learned. Since the Housing and Urban Development Corporation(HUDCO) has considerable experience in lending to low-income groups in both rural and urbanareas, the consultants will coordinate closely with HUDCO. Workshops will be conducted usingthe facilities of Habitat Polytech, HUDCO's training arm. Specifically, the consultants will, interalia, accomplish these tasks.

(i) Review studies, reports, and documents on HFIs in both formal and informalsectors and acquire an understanding of their respective strengths andlimitations.

(ii) Thoroughly analyze the lending operations of the major HFIs, especially theNational Housing Bank (NHB), the Housing Development Finance Corporation(HDFC), HUDCO, and a representative sample of other HFIs to assess theextent and effectiveness of their lending to CFIs and/or directly to low-incomeindividuals; prepare a detailed flow diagram of housing finance processes fromNHB, HDFC, and HUDCO to low-income households through CFIs; assessconstraints to expansion of the operations; and recommend improvements.

(iii) Interview the executives and branch managers of NHB, HDFC, HUDCO, theNational Bank for Agriculture and Rural Development, and selected HFIs abouttheir concerns and problems encountered in lending to nongovernmentorganizations (NGOs), CFIs, and low-income individuals, to identify barriers toreaching the informal financial sector.

(iv) Assess the operations of selected GEls and NGOs responsible for deliveringlow-income housing finance; interview managers or operators of the selectedCFls and NGOs, urban cooperative banks, and members of thrift and creditgroups, urban credit and cooperative societies, to determine their views,problems they encounter, and expectations from the formal HFIs.

(v) Based on these interviews and assessments and in consultation with the CFIand HFI managers, make implementable recommendations for improving thebusiness linkages between HFIs and CFIs.

(Reference in text: page 5, para. 18)

8 Appendix 2, page 2

(vi) Design a set of quantifiable performance indicators for evaluating the operatingand management efficiencies of CFls to give a quantified measure of the CFI'scapacity for handling additional funds from external sources. These indicatorswill include, but will not be limited to, the number of years in operation, number ofmembers or staff, net worth, sources and costs of capital, turnover, lendingterms and conditions, defaults and arrears, profitability, staffing cost, otheroverheads, adequacy of bookkeeping, etc. (This task will be coordinated closelywith the international mortgage insurance specialist and the domestic HFIspecialist.)

(vii) Based on the above analyses and categorization of CFls and in consultation withthe managers or operators of CFls and HFls, (a) develop suitable lendingprocedures for HFls corresponding to each category of CFI, and (b) prepareoperational manuals guiding CFIs in following the recommended procedures.(This task will be coordinated closely with the international mortgage insurancespecialist and the domestic HFI specialist.)

(viii) Present the findings, conclusions, and recommendations to a workshop withrepresentatives from NHB, HUDCO, HDFC, selected HFls and CFls, andlow-income groups (LIG5). Using the feedback from the workshop, design pilotprojects, and assist selected HFls in implementing them, applying differentlending models and aiming at enhancing the linkages between the formalfinancing institutions and CFls in selected communities.

(ix) Document the initial findings of the pilot projects, prepare recommendations forlaunching similar projects countrywide, and conduct a workshop presenting thefindings and recommendations to the participating stakeholders.

(x) Based on the results of the pilot projects and feedback from the workshop, assistNHB in developing guidelines for formal financing institutions' lending to CFIs,and in expanding such lending throughout the country.

(xi) Assess the training needs of HUDCO and the CFIs for meeting low-incomehousing requirements over the near term or midterm, and recommend aninstitutional and human resource development program for HUDCO.

(xii) Using the results of the above activities, prepare training materials on housingfinance to low-income groups through CFls, and implement a training programutilizing the training materials prepared.

(xiii) Undertake institutional assessment of HUDCO's borrowing institutions that areinvolved in low-income housing finance, such as the state housing boards;identify their institutional weakness and obstacles to effective and efficientlending to low-income groups; and recommend necessary actions by HUDCOand the borrowing institutions for improvement.

2. A central theme of Part A is to identify the incentives for the HFls to reach theCFls, and for the CFls to interlink with the HFls, and to build these incentives into thelending/borrowing mechanism of HFls and CFIs. In this context, the consultants will undertake a

9 Appendix 2, page 3

survey, supplemented with interviews, on the operations of individual moneylenders in selectedcommunities. A similar set of indicators as for the CFIs will be developed to make acomparison. Such comparison is expected to give a better understanding of the operationalweaknesses of the CFIs.

B. Part B. Feasibility of Establishing a Housing Loan Insurance Fund

3. The consulting services in Part B require the input of one international expertwith expertise in mortgage insurance (5 person-months) and one domestic HFI specialist (5person-months). To enhance financial flows to the housing finance sector in general and to low-income housing finance in particular, the consultants will determine the feasibility of establishinga housing loan insurance fund, preferably with private sector participation. The internationalexpert will serve as the team leader and will be responsible for preparing consolidated reportsfor submission to the Bank in accordance with the reporting schedule. The consultants willcoordinate with each other in pursuing the listed tasks.

(i) Review studies, reports, and documents on housing finance in India, particularlylow-income housing finance, secondary mortgage market development, andmortgage insurance; and review risk management programs and mortgageinsurance schemes in other countries.

(ii) Review and assess the current and planned lending operations of the majorHFls, especially NHB, HDFC, and HUDCO, to determine the extent of theirexposures to CFIs and low-income individuals, and their need for insurance forsuch exposures.

(iii) Assess and quantify the risks of lending to CFIs and NGOs by analyzing the loanquality and operational efficiency of selected CFIs and NGOs; estimate the riskpremium needed to cover each type of CFI and NGO; and assess theaffordability of home loan insurance to CFIs and NGOs, and their willingness topay for such insurance. (This task will be carried out in collaboration with the CFIspecialist and the domestic low-income housing specialist.)

(iv) Assess the impact of a mortgage insurance scheme on the development of asecondary mortgage market, and the need of HFIs and institutional investors forsuch a scheme.

(v) Based on the above activities, outline the business strategies for the housingloan insurance fund; estimate the market potential, the amount of capital neededfor a housing loan insurance fund, and the expected rate of return on capital.

(vi) Review relevant legal documents and Government financial regulations, andprepare a plan for capital contribution, in consultation with concernedGovernment agencies including NHB, the Ministry of Finance, Reserve Bank ofIndia, Insurance Regulatory Authority of India (IRAI), and selected HFIs.

(vii) Examine the role of the private sector in the proposed insurance fund; comparedifferent scenarios including fully privately owned and operated, jointly owned by

10 Appendix 2, page 4

the private and public sectors and privately operated, publicly owned andprivately operated, and publicly owned and operated; and assess the suitabilityof Bank investment in the fund under each of the scenarios.

(viii) Conduct a workshop on the impediments to the development of a sound housingloan insurance fund, with participants from concerned Government agencies,NHB, selected HFIs and CFIs, potential securitization underwriters, institutionalinvestors, and the Bank; and obtain agreement among the participants on theneed for such a fund, and actions to be taken by participants to improve thedevelopmental environment for the fund.

(ix) Undertake product design for the fund, covering primary and secondarymortgage lending as well as housing loans to CFls; determine the price for eachproduct with due consideration of the long-term financial viability of the fund, thecost and benefit to the originating lenders, and affordability to the CFls, LIGs,and the economically weaker sections (EWS5) of society; prepare underwritingpolicy statement and detailed acceptance and rejection guidelines; assess theavailability and cost of the expertise needed for insurance underwriting, actuarialanalysis and marketing, and prepare a human resources development program;develop a medium-term marketing plan on the basis of market assessment andresource requirements; establish guidelines and procedures for claimssettlement; identify potential reinsurers for the fund to share the cost ofcatastrophic claims; and prepare sound investment guidelines for the fund, withthe objectives of safety, liquidity, and profitability.

(x) Develop a set of indicators to monitor and assess the performance of theinsurance fund against the targets as outlined in the preceding operationalguidelines.

(xi) Discuss and agree with concerned Government agencies, lRAl, and potentialinvestors of the fund on a timetable for setting up the fund.

4. The guiding principle in designing and operating the insurance fund will be itsuse only as the relief of last resort, and applicability to only certain types of risk. Theunderwriting policies and claims settlement guidelines must be designed in such a way that thefund will not be viewed as encouraging imprudent lending.

C. Part C. Institutional Strengthening of NHB

5. The consulting services for Part C require the input of one international housingfinance specialist (3 person-months) and one domestic financial management specialist (3person-months). The consultants will coordinate with the consultants for the other parts of theTA to determine the role of NHB in integrating the formal HFls with the community-basedhousing finance networks, and the relationship between NHB and the proposed housing loaninsurance fund. The international consultant will serve as the team leader and will beresponsible for preparing consolidated reports for submission to the Bank in accordance withthe reporting schedule. The consultants will work closely with each other to accomplish thesetasks.

11 Appendix 2, page 5

(i) Review all the relevant documents, studies, and reports regarding NHB'smandate, functions, and performance, including its corporate plan (Vision 2002)and annual reports.

(ii) Review the functions of NHB as a regulator of the housing finance system, apromoter of HFIs, a financier for housing loans, and a trainer of housing financemanagers in the context of developing a sound housing finance system in thecountry; analyze NHB's strengths and weaknesses in performing thesefunctions; and identify NHB's comparative advantages in the context of financialderegulation in the country.

(iii) Interview representatives of various NHB lending windows, including HFIs,scheduled commercial banks, cooperative banks, and regional rural banks, tosolicit views on NHB's role in the development of the housing finance system.

(iv) Review NHB's loan portfolio and assess its lending modalities and quality ofoutstanding loans; examine NHB's long-term financial positions, including itsprojected business growth and sources of financing; and assess NHB'scorporate structure and the capacity of its human resources.

(v) Explore other actions NHB should take to facilitate the integration of formalfinancial institutions with the informal housing finance sector, such as amendingthe legislation to give NHB necessary foreclosure authority in case of loandefaults.

(vi) Using the results of the foregoing tasks, prepare a medium-term businessstrategy that will maximize NHB's impact on the development of a sound,effective, and efficient housing finance system.