Embed Size (px)

Citation preview

Strategic management practices of Sri Lankan commercial banks

HASALAKA EDIRISINGHE

BSc (Colombo University, Sri Lanka)

MBA (Deakin University, Melbourne, Australia) This thesis is submitted to the fulfilment of the requirements for the degree of Doctor of Business Administration Australian Graduate school of Entrepreneurship, Swinburne University of Technology, Australia.

2008

Declaration This thesis contains no material which has been accepted at any other

University for the award of a degree, and to the best of my knowledge and

belief, the thesis contains no material previously published or written by

another person or persons , except where due reference is made.

_________________________

Hasalaka Edirisinghe

AGSE Swinburne University of Technology Melbourne, Australia (March 2008)

i

Acknowledgements

The completion of this thesis was greatly assisted by a number of people, to whom I am

very grateful. Firstly, I would like to thanks Professor Chris Christodoulou for the

enthusiasm and trust he showed toward both myself and this project. His advice and

guidance were much appreciated throughout my research project and also during the

preparation of this thesis. You were a terrific supervisor. Thank you.

I would also like to thank my second supervisor Professor Chris Selvarajah for his

assistance throughout my research project.

A special mention of appreciation must go to all the senior bank executives who willingly

participated in this research study. Without your help this study might not have been

completed.

Finally, I must thank my father E.M.Jayasinghe and my mother Sumana Edirisinghe, for

their encouragement and assistance during my many years of study. You both have worked

really hard to provide me a good education. I love you and will be forever grateful.

ii

TABLE OF CONTENTS DECLARATION i ACKNOWLEDGEMENTS ii LIST OF ABBREVIATIONS xvi LIST OF TABLES xvii LIST OF FIGURES xxvi ABSTRACT xxxii PART ONE INTRODUCTION AND 1 BACKGROUND AND LITERATURE REVIEW Chapter 1 Introduction 2 1.1 Introduction 2 1.2 Background to the research 2

1.3 Research objectives 4

1.4 Research process 5 1.5 Structure of the thesis 7

1.6 Significance of the Research 9

Chapter 2 Background on Sri Lanka and the banking 11

industry in Sri Lanka 2.1 Introduction 11

2.2 Background on Sri Lanka 11

2.3 Financial sector in Sri Lanka 12

2.3.1 Central Bank of Sri Lanka 13

2.3.2 Supervision of Banks 14

2.3.3 Licensed commercial Banks (LCB) 15

2.3.4 Challenges faced by the Commercial banking sector 16

2.3.5 Risks being a Bank in Sri Lanka 17

2.4 Macro economic environment of Sri Lankan commercial 19 banks

2.5 Chapter Summary 20

iii

Chapter 3 Literature review 22 3.1 Introduction 22

3.2 The history of strategy 22

3.3 The definition of strategy 23

3.4 The evolution of strategic management 26

3.5 Strategy Levels 29

3.6 Strategic Management process 30

3.7 The Environment 32

3.7.1 External environment 33

3.7.1.1 General Environment 34

3.7.1.1.1 Political and legal environment 34

3.7.1.1.2 Demography 35

3.7.1.1.3 Socio-cultural 35

3.7.1.1.4 Economic 36

3.7.1.1.5 Technological 36

3.7.1.1.6 Global 37

3.7.1.2 Industry environment 37

3.7.1.2.1 Threat of entry 39

3.7.1.2.2 The threat of substitutes 40

3.7.1.2.3 Bargaining power of suppliers 40

3.7.1.2.4 Bargaining power of buyers 41

3.7.1.2.5 Rivalry among the existing competitors 41

3.7.1.3 Competitor analysis 42

3.7.2 Internal environment 43

3.7.2.1 Organizational structure 44

3.7.2.2 Organizational Ownership 46

3.7.2.3 Organizational Size 47

3.7.2.4 Organizational culture 48

3.7.2.4.1 Sub cultures 51

3.7.2.5 Management style 51

3.7.2.6 Stakeholder expectations 53

3.7.2.7 Resource base view of the company 56

iv

3.8 Strategic planning 58

3.8.1 Vision and Mission statements 60

3.8.2 Objectives and Goals 61

3.8.3 Analytical tools and techniques 62

3.9 Strategic thinking 65

3.10 Corporate level strategies 67

3.10.1 Diversification strategies 68

3.10.2 International strategy 71

3.10.3 Acquisitions and merger strategies 73

3.10.4 Research and development strategies 74

3.10.5 Turnaround strategies 75

3.10.6 Divestiture strategy 76

3.11 Chapter Summary 77 PART TWO THEORETICAL FRAMEWORK AND 79 METHODOLOGY Chapter 4 Theoretical framework and research questions 80 4.1 Introduction 80

4.2 Theoretical framework 80

4.3 Research questions 83

4.4 Summary 83 Chapter 5 Methodology 85 5.1 Introduction 85

5.2 Population definition 85

5.3 Survey Approach 85

5.3.1 Primary data 85

5.3.2 Secondary data 86

5.4 Instrument development 86

5.4.1 Pre-test of the questionnaire and the final questionnaire 87

5.5 Data collection procedure 88

5.5.1 Introductory letter and the letter of consent 89

5.5.2 Interview process 89

v

5.6 Response rate 90

5.7 Data analysis 90

5.8 Framework for analysis 91

5.9 Chapter Summary 93

PART THREE DATA ANALYSIS 94 Chapter 6 Characteristics of sample companies 95 6.1 Introduction 95

6.2 Industry participation 95

6.3 Respondent aspects 96

6.4 Ownership Aspects 97

6.5 Size aspects 97

6.6 Planning system aspects 100

6.7 Characteristics of the sample companies by 101 ownership, planning and size aspects

6.8 Chapter Summary 102 Chapter 7 Company structure, company 103

ownership and company size 7.1 Introduction 103

7.2 Organizational Structure 103

7.2.1 Organizational structure 104

7.2.2 Organizational levels 104

7.2.3 Number of units at corporate level 105

7.2.4 Highest positions at corporate level 105

7.2.5 Organizational units at second level 106

7.2.6 Highest positions at second level 106

7.2.7 Highest positions at third level 107

7.2.8 Second management level units 108

7.2.9 The lowest level of profit centre 108

7.2.10 Structural types 109

7.2.11 Structural changes in last five years 109

7.2.12 Important structural changes made 110 (during last five years)

vi

7.2.13 Main reasons for the structural changes 111

7.2.14 Applicability of the current organization structure 112 for the next five years

7.2.15 Major structural changes expected by the bank for the 113 next five years

7.3 Ownership 114

7.3.1 Changes in company ownership 116 (during last five years)

7.3.2 The main reasons for the changes in your 117 company’s ownership

7.3.3 The major factors that supported the above 117 ownership changes

7.3.4 Successful rate of the ownership changes 118

7.3.5 Strategic importance of the ownership changes 119

7.3.6 Expected ownership changes in next five years 119

7.4 Size of the Banks 120

7.4.1 Bank satisfaction on company performance 120 compared to their size

7.4.2 The main barriers faced by the banks to 121 enhance their bank size

7.5 Chapter Summary 122 Chapter 8 Organizational culture, management style and 124

stakeholder expectations 8.1 Introduction 124

8.2 Organizational culture 124

8.2.1 The importance of the management of the 124 organizational culture

8.2.2 Top management satisfaction with the current 125 organizational culture

8.2.3 The groups who influenced the company culture 125 (over the last five years)

8.2.4 The major characteristics of company culture 126

8.2.5 Most important actions on company culture 128

8.2.6 The nature of the cultural changes 130

8.2.7 The main reasons for the cultural changes 130

8.2.8 Major cultural changes made by the banks 132

vii

8.2.9 The major factors which supported the 134 cultural changes

8.2.10 Major factors which made cultural 136 changes difficult

8.2.11 The banks that experienced problems when 138 implementing cultural changes

8.2.12 Success of the company’s culture changes 139

8.2.13 Expected cultural changes by the commercial banks 140

8.2.14 Presence of sub cultures 141

8.2.15 The major reasons for development of sub cultures 142

8.2.16 Top management perception about the sub cultures 142

8.2.17 Top management preferences on company culture 143

8.2.18 The influence of company culture on 143 company strategies

8.3 Management style 144

8.3.1 Key characteristics of management style 144

8.3.2 The groups who influenced the management style 145

8.3.3 The effect of management style on follower’s 146 performance and job satisfaction

8.3.4 The influence of management style on 147 company performance

8.3.5 The influence of management style on 148 company strategies

8.3.6 The problems faced by the banks in their current 148 management style (over the last five years)

8.3.7 The major problems faced by the banks in their 149 current management style

8.3.8 The power distance between managers and 150 subordinates

8.3.9 Internal politics 150

8.3.10 Top management perception about the 151 internal politics

8.4 Stakeholder expectations 152

8.4.1 Major Stakeholder groups of the banks 152

8.4.2 Stakeholder expectations of the Sri Lankan banks 153

8.4.3 The level of top management interests aligned with 154 the overall stakeholders’ interests

viii

8.4.4 Company action on stakeholder groups 154

8.4.5 Stakeholder expectation influence on 155 company strategies

8.5. Current resources of the commercial banks 156

8.5.1 Major capabilities of the commercial banks 157

8.5.2 The capabilities which are crucial to the 159 success of the business

8.6 Chapter summary 160

Chapter 9 External environment 164 9.1 Introduction 164

9.2. Demand environments 164

9.3 Competitive environment 167

9.4 Competition and market share 169

9.5 Company customers 171

9.5.1 Company dependence on its major 100 customers 173

9.5.2 The percentage of banks revenues from their 100 174 largest customers

9.6 Company competitors 175

9.6.1 Competitors influence on company strategies 177

9.7 Company business and the government 178

9.8 Company suppliers (Sources of funds) 180

9.9 Company’s business sector 184

9.10 Political and legal environments 185

9.10.1 Current government’s involvement on 188 bank’s operations

9.10.2 Impact of Sri Lankan laws and regulations 189 on bank’s operations

9.11 Impact of Sri Lankan economy on banks operations 191

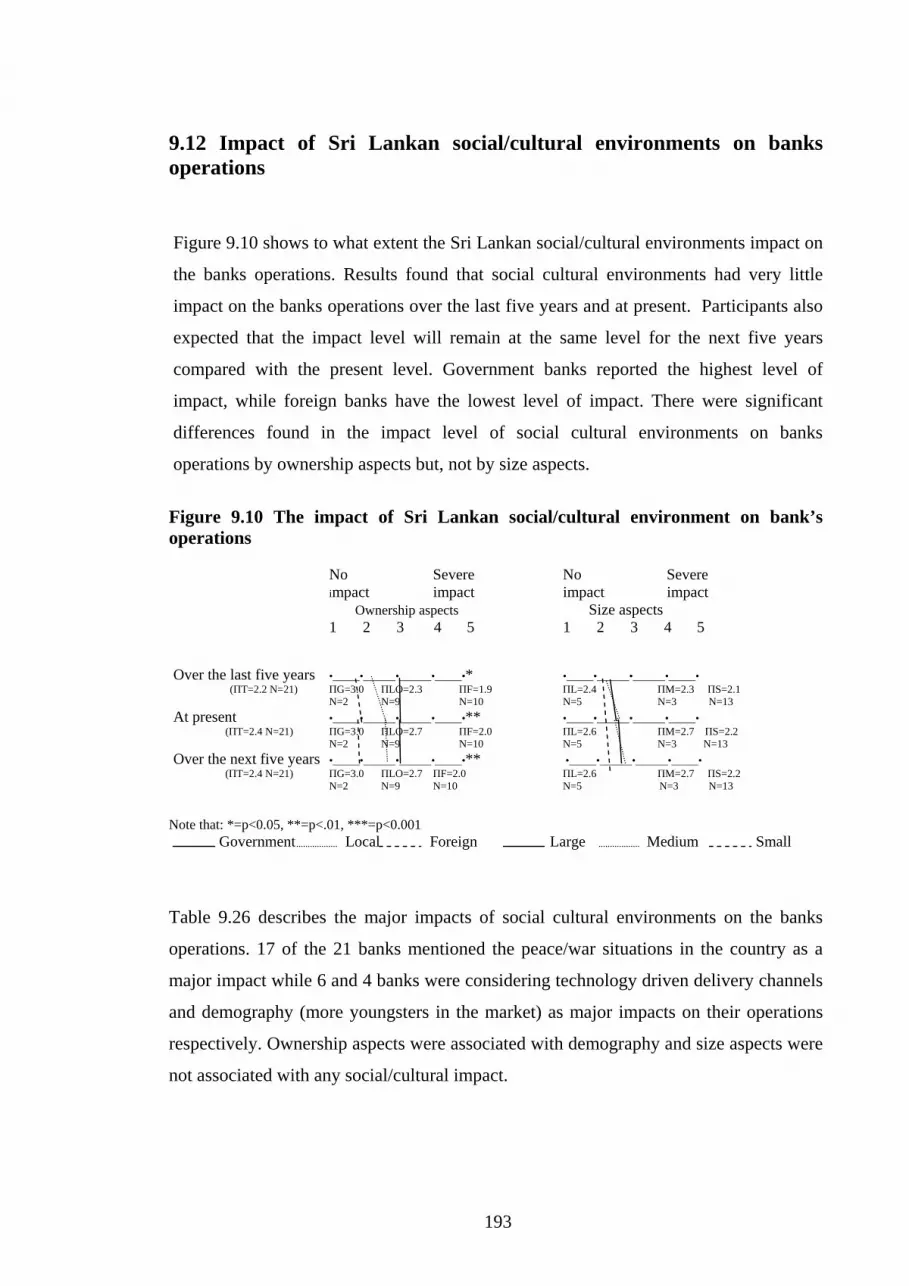

9.12 Impact of Sri Lankan social/cultural environments on 193 banks operations

9.13 The impact of technology available in Sri Lanka 194 on banks operations

9.14 Chapter Summary 195

ix

Chapter 10 Mission, vision and long term goals at corporate 199 and second levels

10.1 Introduction 199

10.2 Company mission statement 199

10.2.1 Stated elements in the mission statement 199

10.2.2 Influential groups on banks mission statements 200

10.2.3 Appropriateness of mission statements for the next 203 five years

10.3 Vision statement 204

10.3.1 Influential groups on formulating banks current vision 205 statement

10.4 Corporate long term goals 206

10.5 Second level long term goals 216

10.6 Chapter summary 221 Chapter 11 Planning and planning systems 224

11.1 Introduction 224

11.2 Planning systems 224

11.2.1 Relationship between plans 225

11.3 Corporate plans 225

11.3.1 Update and progress review of corporate plan 225

11.3.2 Effort spent on the types of planning activities 225

11.3.3 Forecast development 227

11.3.4 Major headings of corporate plan 232

11.3.5 Access to corporate plan 233

11.3.6 Computer models/systems to support 234

corporate planning

11.3.7 Corporate planning department 236

11.4 Second level planning 240

11.4.1 Major headings of second level long term plans 241

11.4.2 Computer models/system to support second 242

level planning

11.5 Third level and fourth level long term business plans 243

11.6 Contingency planning 243

x

11.7 Various functions of corporate planning 244

11.8 Nature of the banks planning process 247

11.9 Planning process and external analysis 250

11.10 Coordination issues involved in the banks 254 planning process

11.11 Personal involvement in the corporate 257 planning process

11.11.1 Roles of various personnel in the 258 planning process

11.12 Major problems of current planning process 261

11.13 Expected changes in the strategic management 261 approach

11.14 Importance of informal planning 262

11.15 Planning effectiveness 263

11.16 Contribution of formal planning 263

11.17 The extent that the banks strategically managed 264

11.18 Chapter summary 264

Chapter 12 Strategic thinking capabilities 268 12.1 Introduction 268

12.2 Employee participation and risk taking behaviour 268

12. 3 Systems perspective 269

12.4 Strategic intent 270

12.5 Thinking in time 271

12.6 Intelligent opportunism 272

12.7 Classification for strategic thinkers 273

12. 8 Chapter summary 274

Chapter 13 Analytical tools/ techniques, corporate strategies 277 and the management of quality

13.1 Introduction 277

13.2 Analytical tools and techniques which influence bank’s 277 strategies

13.2.1 Environment and resource analysis techniques 277 (over the last five years)

xi

13.2.2 Planning techniques (over the last five years) 278

13.2.3 Environment and resource analysis techniques 279 (over the next five years)

13.2.4 Planning techniques (over the next five years) 281

13.3 Benchmarking 282

13.3.1 Benchmark groups 282

13.3.2 Major dimensions of banks benchmark process 283

13.4 Resource allocation decisions 284

13.4.1 The importance of criteria in evaluating expenditure 285 proposals

13.5 Corporate strategies 287

13.5.1 Product/market growth strategies 288

13.5.1.1 Company’s strategies concerning new products 290 and service introductions

13.5.1.2 Organizational responsibility for new products 291 and markets

13.5.2 Research and development strategies 292

13.5.2.1 Support staff for R& D strategies 293

13.5.3 International strategies 294

13.5.4 Acquisition strategies 298

13.5.5 Divestiture strategies 300

13.5.6 Merger strategies 302

13.5.7 Turnaround strategies 304

13.6 Management of quality 306

13.6.1 Strategic approaches towards the quality in banks 307

13.6.2 Personnel responsible for addressing the major 308 strategic quality issues

13.6.3 The extent that the employees are involved 309 in the quality approach

13.6.4 Total quality management strategies 310

13.7 Chapter Summary 312

xii

PART FOUR COMPARISONS WITH 315 PREVIOUS STUDIES AND THE MAJOR RESEARCH FINDINGS

Chapter 14 Comparison with previous studies 316 14.1 Introduction 316

14.2 Background of the previous studies 316

14.3 Formalized strategic planning 317

14. 3.1 Relationship between plans 317

14.3.2 Corporate planning effort 318

14.3.3 Corporate planning effort spent on Forecasting 319

14.3.4 Use of computer models/systems 320

14.3.5 Nature of corporate planning 321

14.4 Chapter summary 325

Chapter 15 Major research findings and further 328 research directions

15.1 Introduction 328

15.2 Major Research findings of the research 328

15.2.1 Research question 1 328

15.2.1.1 Respondents characteristics 329

15.2.1.2 Vision and mission statements 329

15.2.1.3 Long term goals at corporate and second level 330

15.2.1.4 Corporate strategies and processes 331

15.2.2 Research question 2 332

15.2.2.1 Organizational structure 332

15.2.2.2 Ownership 333

15.2.2.3 Size 333

15.2.2.4 Organizational Culture 333

15.2.2.5 Management style 334

15.2.2.6 Stakeholder’s expectation 335

15.2.2.7 Resources, capabilities and key success factors 335

xiii

15.2.3 Research question 3 336

15.2.3.1 Demand environment 336

15.2.3.2 Competitive environment 336

15.2.3.3 Industrial factors 337

15.2.3.3.1 Competition and market share 337

15.2.3.3.2 Major customers 337

15.2.3.3.3 Company suppliers 337

15.2.3.3.4 New entrants 338

15.2.3.4 General environmental factors 338

15.2.3.4.1 Political and legal factors 338

15.2.3.4.2 Economic factors 338

15.2.3.4.3 Social cultural factors 339

15.2.3.4.4 Technology factors 339

15.2.4.1 Research question 4 part1 339

15.2.4.1.1 Strategic planning at corporate level 339

15.2.4.1.2 Strategic planning at second level 342

15.2.4.1.3 Contingency planning 342

15.2.4.1.4 Third level and fourth level planning 342

15.2.4.2 Research question 4 part 2 343

15.2.5 Research question 5 344

15.2.5.1 Company structure 344

15.2.5.2 Organizational culture and management style 344

15.2.5.3 Mission and Vision statements 345

15.2.5.4 Long term goals 346

15.2.5.5 Planning and planning systems 347

15.2.5.6 Corporate strategy and processes 350

15.2.5.7 Management of quality 351

15.2.6 Research question 6 351

15.3 The unique features associated with different 352 categories of banks

15.3.1 Government banks 352

15.3.2 Locally owned banks 354

15.3.3 Foreign owned banks 357

15.3.4 Large banks 359

xiv

15.3.5 Medium sized banks 362

15.3.6 Small sized banks 364

15.4 The unique features associated with strategic 366 management practices in Sri Lankan banks

15.5 Significance of the study 367

15.5.1 Contribution to theory 367

15.5.2 Contribution to practice 368

15.5.3 Contribution to the methodology 368

15.6 Limitations of the study 368

15.7 Future directions 369

15.8 Chapter Summary 369

References 370

Appendix 1: Research questionnaire 389

Appendix 2: Introductory letter and letter of consent 495

xv

LIST OF ABBREVIATIONS & And % Percentage П Mean/Average etc et cetera F Foreign owned G Government owned L Large banks LO Locally owned banks M Medium sized banks N Number S Small sized banks T Total CBSL Central Bank of Sri Lanka FSP Formalized strategic planning MST Moderate strategic thinkers MSBU Multiple strategic business units NFSP Non formalized strategic planning NPL Non performing loans SLSM Sri Lanka stock market SSBU Single strategic business units SST Strong strategic thinkers WST Weak strategic thinkers

xvi

LIST OF TABLES Table 2.1: Core functions of the Central Bank 14 Table 2.2: Financial indicators of the LCB’s 16 Table 2.3: Economy Growth prospects 20 Table 3.1: Mintzberg’s ten schools for strategy 26 Table 3.2: The evolution of the research about leadership 52 Table 3.3: Core arguments for stakeholder responsibility 55

and its practical implications

Table 3.4: Checklist for the PEST analysis 62 Table 3.5: Firm capabilities and diversification strategies 70 for different country resource environments Table 6.1: Banks that participated in this study 95 Table 6.2: Respondents job titles 96 Table 6.3: Description of the three categorize in 97 ownership aspects Table 6.4: Ownership characteristics of the participating 97 companies in terms of ownership aspects Table 6.5: Of these size measures, is one of these 99 considered most important? Table 6.6: Most important size measures of the 99 participating bank Table 6.7: Classification for size aspects 100 Table 6.8: Participating banks in terms of size aspects 100 Table 6.9: Does your company have a formalized 101 strategic planning system at the corporate level? Table 6.10: Characteristics of the sample companies 101 by ownership, planning and size aspects Table 7.1: Could you please provide us with an 103 organization chart of your company?

xvii

LIST OF TABLES (CONTINUED) Table 7.2: Organizational structure 104 Table 7.3: Organizational levels 105 Table 7.4: Number of units at corporate level 105 Table 7.5: Highest positions at corporate level 106 Table 7.6: Organizational units at second level 106 Table 7.7: Highest positions at the second level 107 Table 7.8: Highest positions at the second level 107 Table 7.9: Are the second management level units 108 defined as profit centres? Table 7.10: The lowest level of profit centre 108 Table 7.11: Structural type 109 Table 7.12: Organizational structure changed during last five years 110

Table 7.13: Year of structural change 110 Table 7.14: Important structural changes made 111 (during last five years) Table 7.15: The main reasons for the structural changes 112 Table 7.16: Applicability of the current organizational structure 113 Table 7.17: Major structural changes expected by the 114 banks for the next five years Table 7.18: Bank sell its shares in SLSM 115 Table 7.19: Shareholder pattern of the commercial banks 115

listed under SLSM Table 7.20: Company sell its shares in overseas stock market 115 Table 7.21: Changes in company ownership (during last five years) 116 Table 7.22: The main reasons for the changes in your company’s ownership 117

Table 7.23: The major factors that supported the above ownership changes 118

Table 7.24: Changes in company ownership (For the next five years) 120

xviii

LIST OF TABLES (CONTINUED) Table 7.25: Do you think you need to enhance the size 121 of your bank to gain more profits? Table 7.26: The main barriers that you have to enhance your bank’s size 122 Table 8.1: The major characteristics of company culture 127 Table 8.2: The banks which changed their company cultures 130 (over the last five years) Table 8.3: The nature of the cultural changes 130 Table 8.4:The main reasons for the company culture changes 131 Table 8.5: Major cultural changes made by the banks 133 (over the last five years) Table 8.6: The major factors which supported the cultural changes 135 Table 8.7: Major factors which made cultural changes difficult 136 Table 8.8: The banks which experienced the problems when 138 implementing cultural changes Table 8.9: The problems experience by the banks 138 when implemented cultural changes Table 8.10: Do you expect any major changes in your 140 company’s culture in the next five years? Table 8.11: Expected major culture changes by the Sri Lankan 141 commercial banks Table 8.12: Do you have sub cultures in your company? 141 Table 8.13: The major reasons for development of sub cultures 142 Table 8.14: Do you think development of subcultures weaken 143 or undermine the organization? Table 8.15: Preferred types of company cultures 143 Table 8.16: Key characteristics of management style 145 Table 8.17: The banks which are having significant problems 148 with its current management style

xix

LIST OF TABLES (CONTINUED) Table 8.18: The major problems faced by the banks 149 in their current management style Table 8.19: Major Stakeholder groups 152 Table 8.20: Stakeholder expectations 153 Table 8.21: Current recourses of the commercial banks 157 Table 8.22: Major capabilities of the commercial banks 158 Table 8.23: The capabilities which are crucial to the success 160 of the business in the Sri Lankan banking sector Table 9.1: Predictability of bank’s revenues/sales 165 (during last five years) Table 9.2: Predictability of bank’s revenues/sales 165 (for the next five years) Table 9.3: Market growth rates of the banks sales/revenues 166 (last five years) Table 9.4: Market growth rates of the banks sales/revenues 166 (next five years) Table 9.5: Competitive environment 167 (During last five years) Table 9.6: Predictability of the banks competitor environments 168 (last five years) Table 9.7: Predictability of the banks competitor environments 169 (next five years) Table 9.8: Most important markets 170 (during last five years) Table 9.9: Most important markets 171 (during next five years) Table 9.10: Major customer groups 172 (last five years)

xx

LIST OF TABLES (CONTINUED) Table 9.11: Major customer groups for the next five years 173 Table 9.12: The percentages of average banks revenues 175 from their 100 largest customers in terms of ownership and size aspects Table 9.13: Banks major competitors 176 (for the last five years) Table 9.14: Banks major competitors 177 (for the next five years) Table 9.15: Government regulations on banks businesses 178 Table 9.16: Changes expected by the banks 179 in the government regulations Table 9.17: Major sources of funds (last five years) 180 Table 9.18: Major sources of funds (next five years) 181 Table 9.19: Main categories which banks major sources 183 of funds felt into (last five years) Table 9.20: Main categories which banks major sources 183 of funds felt into (next five years) Table 9.21: Possible new entrants to the banking industry 184 Table 9.22: Current impacts of the Sri Lankan government 187 policies on bank’s operations

Table 9.23: Current government’s involvement on bank’s operations 189 Table 9.24: Current impacts of the Sri Lankan laws 191 and regulations on bank’s operations Table 9.25: Current impact of the Sri Lankan 192 economy on bank’s operations Table 9.26: Current impacts of the Sri Lankan 194 social cultural environment on bank’s operations

xxi

LIST OF TABLES (CONTINUED) Table 9.27: Current impacts of the available technology 195 in Sri Lanka on bank’s operations Table 10.1: Does your banks have a mission statement? 199 Table 10.2: Stated elements in mission statement 200 Table 10.3: Changes made by the banks 202 Table 10.4: Average years that the banks will 204 continue their current mission statements Table 10.5: Characteristics of vision statement 205 Table 10.6: Average years that the banks will continue 206 their current vision statements Table 10.7: Does your bank has corporate long term goals 207 Table 10.8: Quantitative long term goals 207 Table 10.9: Does your bank has qualitative goals? 208 Table 10.10: Qualitative long term goals 208 Table 10.11: Processes of formulating banks long-term goals 210 Table 10.12: Have your corporate level goals changed 212 in the last five years Table 10.13: Major changes made by the banks 213 Table 10.14: Banks continuation periods of the current goals 214

Table 10.15: Does your banks have second level long term goals 216 Table 10.16: Units of measurements 217 Table 10.17: Banks processes for formulating 219 second level long term goals

xxii

LIST OF TABLES (CONTINUED) Table 11.1: The banks which had planning systems at corporate level 224 Table 11.2: Banks which had a planning system at second level 224 Table 11.3: Relationship between the plans 225 Table 11.4: Update of corporate plans 226 Table 11.5: Frequency of reviewing the progress of corporate plans 226 Table 11.6: Banks which purchased external forecasts 229 Table11.7: Major headings of corporate long range plan 232 Table 11.8: Organizational personnel who have access to banks corporate 233

plan Table 11.9: The models and systems used by the banks for 235 their corporate planning Table 11.10: Banks which had a corporate planning department 237 Table 11.11: Document used by the corporate planning department 240 Table 11.12: Does your bank has second level long term plans? 240 Table 11.13: Major headings of second level long term plans 241 Table 11.14: Organizational levels that has contingency planning 244 Table 11.15: Banks expected changes in the strategic management 262 approaches in the next five years Table 12.1: Classification for the strategic thinkers 273 Table 12.2: Categorized strategic thinking capabilities of size 274 and ownership aspects Table 12.3: Overall strategic thinking capabilities of the banks 275 Table 13.1: Three major dimensions of banks benchmarking process 284 Table 13.2: Supporting staff of R& D strategies 293 Table 13.3: Percentage of revenue allocations 294

xxiii

LIST OF TABLES (CONTINUED) Table 13.4: Does your company have international operations? 294 Table 13.5: Bank’s revenues take place outside Sri Lanka 295 Table 13.6: Three major business types of overseas revenues 295 Table 13.7: Three most important overseas markets of the banks 296 (Over the last five years) Table 13.8: Major reasons overseas markets were chosen 296 Table 13.9: Three most important overseas markets of the banks 297 (Over the next five years) Table 13.10: Did your bank make any significant acquisitions 299 during last five year? Table 13.11: Banks which divested, liquated or eliminated any 300 important operations Table 13.12: Banks which merge with other companies 302 Table 13.13: Has your company made any significant turnarounds 304 in the last five years? Table 13.14: Strategic approach towards quality in the banks 307 Table 13.15: Personals responsible for addressing the major 308 strategic quality issues Table 14.1: Population and the sample size of the current and previous 316

studies Table 14.2: Percentages of formal and non formal planners 317

Table 14.3: Relationship between corporate and short term plans 318

Table 14.4: Corporate planning effort spent on different planning activities 319

Table 14.5: Corporate plan effort spent in forecasting areas 319

Table 14.6: Forecast transmission from corporate to second level 320

Table 14.7: The models and systems used by the companies for 321 their corporate planning

xxiv

LIST OF TABLES (CONTINUED)

Table 14.8: Nature of corporate planning process 322

Table 14.9: Corporate planning co-ordination with other planning 322

Table 14.10: Various functions of the corporate planning 323

Table 14.11: Corporate Planning effort put on external analysis 324

Table 14.12: Quality of information received from various departments 325 for corporate planning

xxv

LIST OF FIGURES Figure 1.1: Research process 6

Figure 2.1: Geography of Sri Lanka 11

Figure 3.1: Generic Perspectives on strategy 24

Figure 3.2: The strategy making Pyramid 30 Figure 3.3: Elements of strategic management 32

Figure 3.4: Elements of industry structure 39

Figure 3.5: Components of competitor analysis 43

Figure 3.6: The reciprocal influence view of strategy and 50 environment as moderated by organizational culture Figure 3.7: Stakeholder categories 56

Figure 3.8: Relationship between company resources 58 and core competencies Figure 3.9: The BCG matrix 65

Figure 3.10: The elements of strategic thinking 67

Figure 4.1: Theoretical Framework (strategic management processes) 82 Figure 5.1: Framework for analysis 92 Figure 6.1: Size measures 98 Figure 7.1: Successful rate of ownership change (over the last five years) 118

Figure 7.2: Strategic importance of the ownership changes 119 (Over the last five years)

Figure 7.3: Bank satisfaction level on company performance 120 compared to their size Figure 8.1: Importance of the management of company culture 124 Figure 8.2: Top management satisfaction with the 125 current organizational culture Figure 8.3: The groups who influenced the culture 126 (over the last five years) Figure 8.4: Most important actions on company culture 128

xxvi

LIST OF FIGURES (CONTINUED)

Figure 8.5: Success of the company’s culture changes 139 Figure 8.6: The influence of company culture on company strategies 144 Figure 8.7: The groups who influenced the management style 146 Figure 8.8: The effect of management style on 147 follower’s performance and job satisfaction Figure 8.9: The influence of management style on company performance 147

Figure 8.10: The influence of management style on company strategies 148 Figure 8.11: The power distance between managers and subordinates 150 Figure 8.12: The level of internal politics in Sri Lankan commercial banks 151 Figure 8.13: Top management perception about the internal politics 151

Figure 8.14: The level of top management interests 154 aligned with the overall stakeholders’ interests Figure 8.15: Company action on stakeholder groups 155 Figure 8.16: Influence of stakeholder expectations on company strategies 155 Figure 9.1: Company dependence on its major 100 customers 174 Figure 9.2: Competitors influence on company strategies 178 Figure 9.3: Satisfaction levels of the banks on government regulations 179 Figure 9.4: Dependency levels of the banks on their major sources of funds 182 Figure 9.5: Difficulty of entry into banking businesses 185 Figure 9.6: The extent government policies impact on banks operations 186

Figure 9.7: Government involvements in banks operations 188

Figure 9.8: Impact of Sri Lankan laws and regulations on bank’s operations 190 Figure 9.9: The impact of the Sri Lankan economy on bank’s 192 operations

xxvii

LIST OF FIGURES (CONTINUED)

Figure 9.10: The impact of Sri Lankan social/cultural 193 environment on bank’s operations Figure 9.11: The impact of technology available in 194 Sri Lanka on bank’s operations Figure 10.1: Influential groups on formulating banks 201 current mission statement Figure 10.2: Major factors that influenced the changes in banks 202

mission statements Figure 10.3: Appropriateness of mission statements for the next five years 203 Figure 10.4: Influential groups on formulating banks current vision 206

statements

Figure 10.5: Groups influence on the formulation of banks long-term goals 209

Figure 10.6: Important roles of corporate long term goals 212

Figure 10.7: Factors influenced the changes of banks corporate level goals 214

Figure 10.8: Banks achievement of their corporate goals 215 (during last five years)

Figure 10.9: Major reasons for banks achievements 216

Figure 10.10: The groups who influenced the formulation of second 218

level long term goals

Figure 10.11: Major roles of the second level long term goals 220

Figure 10.12: Quality of the second level long term goals 220 Figure 11.1: Effort spent on the types of planning activities 227 Figure 11.2: Effort expended by corporate 228 planning in forecast development Figure 11.3: Transmission of forecasts from corporate 230 level to second level

Figure 11.4: Impact on the corporate planning if external forecasts 231

purchased were not available

xxviii

LIST OF FIGURES (CONTINUED) Figure 11.5: Difficulty faced by the second level units 231 to obtain information they currently receive from the corporate planning Figure 11.6: Added value of the corporate plan over 234 the second level plans Figure 11.7: Use of computer models/systems to support 235 corporate planning Figure 11.8: The usefulness of computer models/systems 236 for corporate planning Figure 11.9: The extent that line personnel were rotated 237 through the corporate planning department Figure 11.10: Extent of chief corporate planner attend meetings 238 Figure 11.11: The authority of the corporate planning department 238 Figure 11.12: The performance of the corporate planning group 239 Figure 11.13: The extent annual budgets for the second level units 242 were integrated with the long term plans of these units Figure 11.14: Use of computer models/system to support 242 second level planning Figure 11.15: Usefulness of computer models/systems 243 Figure 11.16: Various functions of corporate planning 245 Figure 11.17: Nature of the banks planning process 248

Figure 11.18: Planning process and external analysis 251 Figure 11.19: Coordination issues involved in the banks planning process 255 Figure 11.20: CEO’s personal involvement in the corporate 257 planning process Figure 11.21: Board of director’s involvement in the corporate 257 planning process

xxix

LIST OF FIGURES (CONTINUED)

Figure 11.22: How supportive the board of directors regarding 258 corporate planning activities Figure 11.23: Roles of various personnel in the planning process 259 Figure 11.24: Importance of informal planning 262 Figure 11.25: Planning effectiveness of the banks 263 Figure 11.26: Contribution of formal planning 263 Figure 11.27: The extent that the banks strategically managed 264 Figure 12.1: Employee’s participation and their risk taking behaviors 269 Figure 12.2: The relationship of the interdependencies included in the 270

banks value creation process Figure 12.3: Strategic intent 271 Figure 12.4: Banks thinking in time 272 Figure 12.5: Intelligent opportunism 273 Figure 13.1: The influence of environment and resource analysis techniques 278 (over the last five years) Figure 13.2: The influence of Planning techniques (over the last five years) 279 Figure 13.3: The influence of environment and resource analysis techniques 280 (over the next five years) Figure 13.4: The influence of Planning techniques (over the next five years) 281 Figure 13.5: Influence of benchmarking on banks strategies 282 (over the last five years) Figure 13.6: Benchmark groups and the level of benchmarking 283 Figure 13.7: The importance of the long-term resource allocation decisions 285 Figure 13.8: The importance of criteria in evaluating expenditure proposals 286 Figure 13.9: Formalization of corporate strategies 287

xxx

LIST OF FIGURES (CONTINUED) Figure 13.10: The explicit part of banks corporate strategies 288 Figure 13.11: Product/market growth strategies 289 Figure 13.12: Company’s strategies concerning new products and service 290 introductions Figure 13.13: Organizational responsibility for new products and markets 291 Figure 13.14: Research and development strategies 292 Figure 13.15: Global orientation and the international strategies 298 Figure 13.16: Acquisition strategies 299 Figure 13.17: Acquisition strategies (next five years) 300 Figure 13.18: Major reasons for divestitures strategies 301 Figure 13.19: Future roles of divestiture strategies 302 Figure 13.20: Major aims of mergers 303 Figure 13.21: Future roles of merger strategies 304 Figure 13.22: Turnaround strategies 305 Figure 13.23: Future roles of turnaround strategies 305 Figure 13.24: The importance of management of quality 306 Figure 13.25: The extent that the management of quality 306 addressed as a strategic issue Figure 13.26: The extent that the employees are involved in 309 the quality approach Figure 13.27: Total quality management strategies 310

xxxi

ABSTRACT Strategic management addresses the question of why some organizations succeed and

others fail. While the field of strategic management has developed rapidly, no one has

attempted to investigate the strategic management practices of a particular industry in Sri

Lanka. Hence, this research aims to explore the strategic management practices of the Sri

Lankan commercial banks and to provide original knowledge about the strategic

management practices of a particular industry in a developing country.

Licensed commercial banks dominate the financial sector in Sri Lanka and as at 31st

December 2005 there were 22 commercial banks operating in Sri Lanka. The Banking

sector has shown a significant expansion during the last five years. Despite the significant

expansion, the banking industry in Sri Lanka is currently going through a period of rapid

change due to new products and services being introduced by the banking industry as a

result of globalization and the adoption of new technologies. Therefore, an exploration of

the current strategic management practices of the Sri Lankan commercial banks will be

extremely important for every commercial bank in the Sri Lankan banking industry.

The prominent authors in the field of strategic management fall in to two main categories in

the way they look at strategy, namely the “strategic planning” or the “strategic thinking”

approach. This study aims to investigate both the strategic planning and the strategic

thinking capabilities of the Sri Lankan commercial banks. However, the major priority of

this research is to investigate the strategic planning practices which are currently playing a

major role in the strategic management practices of the Sri Lankan commercial banks.

Because of the exploratory nature of the study research objectives were stated instead of

research hypotheses. The large number of variables that were expected to be investigated in

this study, together with no prior knowledge about how the variables would behave in the

Sri Lankan banking industry meant that this study was developed around key research

questions. The theoretical framework for this study is based predominately on previous

research studies but was adapted to the Sri Lankan banking industry and in accord with the

major research questions of this research study.

xxxii

Except for one commercial bank all the commercial banks in Sri Lanka participated in this

study, a response rate of 95.5%. The primary data was collected through personal

interviews using a questionnaire with senior executives who were responsible for their

corporate planning. The respondents were categorized according to ownership, size, and

planning system aspects.

Except for one bank all the banks had a formalized strategic planning system at their

corporate level. Thus, whether it is a large, medium or small sized bank strategic planning

systems played a major role in these banks strategic management processes. However, the

top management of most of these banks were also aware of the importance of having strong

strategic thinking capabilities. It would appear that the banks preferred to have formalized

strategic planning systems and also seek to develop strategic thinking capabilities.

Overall banks spent most of their strategic planning effort on action planning or operational

planning for the next 1 to 3 years. Most of the effort spent on forecast development was in

the areas of domestic economy, laws and regulations for the financial services sector,

industry level demand, and competitive analysis and in these areas the forecasts were

transmitted to a reasonably high degree from corporate level to second level. The

responsibilities for a number of strategic analyses were decentralized to the operations,

marketing and second level managers to some degree but the corporate level was mainly

responsible for competitive, supplier, customer, political, social and cultural analyses

whereas operations people were mainly responsible for technological analyses.

The medium sized, large, locally owned and government owned banks were identified as

being moderate strategic thinkers whereas the small sized and foreign owned banks were

identified as being weak strategic thinkers. There were no strong strategic thinkers

identified amongst the banks. Strategic thinking capabilities such as strategic intent and

intelligent opportunism were identified as low in most banks. Thus, there is much room to

improve the strategic thinking capabilities of Sri Lankan commercial banks.

Corporate strategies such as mergers, acquisitions, and divestitures did not play a major

role in most banks corporate planning during the last five years and are also not expected to

play a significant role in the next five years. However, a reasonable number of banks had

executed turnaround strategies during the last five years. Benchmarking has also played a

xxxiii

reasonably high role in these banks during the last five years. The management of quality is

also considered as important and is being addressed as a strategic issue to a great extent.

There are number of significant contributions from of this research study. First, this study

has identified and discussed the overall strategic management characteristics of Sri Lankan

commercial banks and their expected changes to their strategic management practices in

the next five years. This will also help corporate level managers in Sri Lankan commercial

banks to compare their strategic management practices with other banks. Secondly, the

theoretical framework developed for this study provides the foundation for other research

studies to potentially investigate the strategic management practices of other industries in

Sri Lanka. Finally, the database developed in this study will help other researchers who

plan to do further research into Sri Lankan commercial banks.

xxxiv

PART ONE INTRODUCTION AND BACKGROUND TO THE RESEARCH AND LITERATURE REVIEW Chapter 1: Introduction Chapter 2: Background on Sri Lanka and the banking industry in Sri Lanka Chapter 3: Literature review

1

Chapter 1: Introduction 1.1 Introduction This chapter will discuss the background to the research, research objectives, research

process, structure of the thesis, and the significance of the research.

1.2 Background to the research

The development of the field of strategic management within the last two decades has

been dramatic (Hoskisson, Hitt, Wan & Yiu 1999) and it grows larger every day.

Because of the nature of the strategy it does not contain universal truths that can be

documented through scientific theorems and proofs (Chinowsky & Byrd 2001).

According to Anand & Singh (1997) a significant amount of the empirical studies in

strategy were concerned about the scope of the firm and its performance implications.

However, strategic management generally addresses the question of why some

organizations succeed or fail, and it covers the causes for company’s success or failure

(Porter 1991). While the field of strategic management developing rapidly, no one has

attempted to investigate the strategic management practices of a particular industry in

Sri Lanka. This research aims to explore the strategic management practices of the Sri

Lankan commercial banks and therefore, it will provide insight knowledge about the

strategic management practices of a particular industry in a developing country.

Licensed commercial banks dominate the financial sector in Sri Lanka and as at 31st

December 2005 there were 22 commercial banks operating in Sri Lanka (Central Bank

2005a). The Banking sector has shown a significant expansion during the first half of

2007 and that includes an increase in assets, loans and deposits by 203 billions rupees

which was a 9.5% increase compared to the previous year (Central Bank 2007). Despite

the significant expansion, the banking industry in Sri Lanka is currently going through a

period of rapid change due to new products and services introduced by banking industry

as a result of globalization and the adoption of new technologies. Therefore, exploring

the current strategic management practices of the Sri Lankan commercial banks will be

extremely important for every bank in the Sri Lankan banking industry.

2

Since no organization has unlimited resources, strategists must decide which alternative

strategies benefit the firm most (Fred 1997).Thus, a strategy “reflects managerial

choices among alternatives and signals organizational commitment to particular

products, markets, competitive approaches, and ways of operating the enterprise”

(Thompson & Strickland 2003, p10). Furthermore, different organizations in different

environments are likely to emphasize different aspects of the strategic management

process (Johnson & Scholes 1999). Therefore, investigating the strategic management

practices in Sri Lankan commercial banks, which no one has attempted earlier, is simply

not an easy task.

The major argument in the field of strategic management during last three decades was

whether the strategic management process must be a planning or a thinking process.

Wilson (1998) identifies that, during last three decades strategic planning has been an

on again and off again affair for most companies, even though the need for strategic

thinking has increased rather than decreased. The data from the studies conducted by

Christodoulou (1984), Bonn (1996) showed that in Australian large companies strategic

planning plays a major role however, it has undergone substantial changes since the

early 1980s (Bonn & Christodoulou 1996). Taylor (1997) asserts that strategic planning

is back but, with changes like Mintzberg would have wanted such as less bureaucracy,

more emphasis on implementation and innovation, and fewer staff planners etc.

Therefore, despite its criticism strategic planning still plays a major role in firms.

Collis & Montgomery (1995) assert that because of global competition and

technological changes the markets move faster and faster and that strategic planning is

too static and too slow to adopt the new strategies which match to environmental

changes. Mintzberg (1994) thinks strategic planners should not create strategies but,

they can supply data to help managers think strategically. Mintzberg (1994) further

believes strategic thinking as a synthesizing process, that involves intuition and

creativity, whose outcome is “an integrated perspective of the enterprise”. Simpson

(1998) claims strategic planning is a waste of time because of number of reasons such

as it focuses more attention on the market than on competition, set aggressive top-down

targets instead of developing bottom up financial forecasts etc.

3

Liedtka (1998) asserts “it is individual who think strategically not organizations and in

order to think strategically individuals require a supporting context to manage the

strategic conversations that occur within it and therefore, strategic planning systems can

play an important role in this process”. Thus, companies can have formalized strategic

planning systems and they also can encourage the strategic thinking capabilities inside

their organizations. This study aims to investigate both the strategic planning and the

strategic thinking capabilities of the Sri Lankan commercial banks. However, the major

priority of this research is to investigate the strategic planning practices which are

currently playing a major role in strategic management practices of the Sri Lankan

commercial banks. Christodoulou (1984), Bonn (1996), Nimmanphatcharin (2002),

Kakanamveetil (2004), and Angkasuvana (2005) questionnaires will be redeveloped and

redesigned so as to investigate the Sri Lankan commercial banks strategic planning

practices, and Liedtka’s (1998) elements of strategic thinking model will be used to

analyze their strategic thinking capabilities. Research objectives will be developed

instead of research hypotheses because of the exploratory nature of this research study.

1.3 Research objectives

This research study seeks to explore the strategic management practices of the Sri

Lankan commercial banks and all the major areas of the banks strategic management

activities will be covered. The major objectives of this research are given below.

• To develop a theoretical framework to explore the strategic management

practices in Sri Lankan commercial banks based predominately on the research

conducted by Christodoulou (1984), Bonn (1996), Nut-tapon (2002),

Kakanamveetil (2004), and Angkasuvana (2005).

• To investigate the current strategic management practices of the Sri Lankan

commercial banks and to also identify the future (for the next five years)

strategic management practices that the commercial banks in Sri Lanka expect to

adopt to compete with the other banks in the Sri Lankan banking industry.

• To identify the major internal and external factors that can affect the banks

strategic management practices. The internal environmental factors will include

factors such as ownership, size, planning systems, organizational culture,

4

management style, stakeholder expectations and key capabilities etc. and the

external factors will include factors such as demand environment, suppliers,

political, economic, social, and technological environments etc.

• To investigate the strategic management practices by investigating the banks

strategic planning and strategic thinking capabilities.

• To compare the strategic management practices of Sri Lankan commercial banks

with the studies done in other countries so as to find out the differences of the

strategic management practices between the commercial banks in Sri Lanka and

the companies in other countries.

• To create a data base that will helpful for the future researchers who are willing

to do more research into the Sri Lankan commercial banks.

1.4 Research process

Figure 1.1 illustrates the research process of this research study which aims to explore

the strategic management practices of the Sri Lankan commercial banks. As at 31st

December 2005 there were 22 commercial banks doing business in Sri Lanka and all

those banks were selected as the population for this study. The first step of this research

is to study the banking industry in Sri Lanka and find out the external environmental

factors that can affect their practices. Then a literature review about the field of strategic

management will be undertaken and the literature review will identify the important

concepts and the issues in the field of strategic management important for this study.

Then the theoretical framework will be developed to address the major research

questions and it will be mainly based on the previous research conducted by

Christodoulou (1984), Bonn (1996), Nimmanphatcharin (2002), Kakanamveetil (2004),

and Angkasuvana (2005). Development of the questionnaire will be the next step and

the primary data will be collected through the personal interviews with the senior

executives who are responsible for their (banks) corporate planning. SPSS software will

be used for the primary data analysis and the interpretation of the data will be the next

step. The major research findings of this study will be compared with the major research

findings of the research carried out in other countries. Then the unique features of the

strategic management practices by ownership and size aspects and the unique features

of the strategic management practices in Sri Lankan commercial banks will be

5

summarized. Finally, limitations and the possible directions for future research will be

mentioned.

Figure 1.1 Research process

Study the Sri Lankan banking industry in Sri Lanka and find out the external factors that affect the Strategic management practices of the commercial banks

Literature Review and development of theoretical framework

Development of questionnaire

Data analysis and data interpretation

Compare the major research finding of the research with other research studies and summarize the unique features of the strategic management practices by ownership and size aspects and also identify the unique features of the strategic management practices in Sri Lankan commercial banks.

Identify the limitations of the research and several directions for future research.

Secondary data Primary Data

Conduct personal interviews

6

1.5 Structure of the thesis

This thesis contains 15 chapters and a brief description of each chapter is given below.

Chapter1 Chapter1 will explain the background to the research, research objectives, research

process and the significance of the research study.

Chapter 2

Chapter 2 will discuss the financial sector in Sri Lanka, especially the Central Bank and

the commercial banks of Sri Lanka and highlight the major external environmental

factors that can affect the strategic management practices of the Sri Lankan Commercial

Banks.

Chapter 3

Chapter 3 will provide a literature review of the field of strategic management and

discuss the major relevant theories which are important for the study of Strategic

management practices of Sri Lankan Commercial Banks.

Chapter 4

Chapter 4 will provide the theoretical framework developed for this research study

which is based predominately on the research studies conducted by Christodoulou

(1984), Bonn (1996), Nimmanphatcharin (2002), Kakanamveetil (2004), and

Angkasuvana (2005).

Chapter 5

Chapter 5 will explain the methodology adopted for this study under the major headings

of population definition, survey approach, instrument development, pre test of the

questionnaire, data collection procedure, data analysis and the framework for data

analysis.

7

Chapter 6

Chapter 6 will investigate the major characteristics of the sample companies such as

industry participation, respondent aspects, size aspects, ownership aspects and planning

system aspects.

Chapter 7

Chapter 7 will investigate 3 major internal environmental characteristics of the Sri

Lankan commercial banks more thoroughly and those characteristics will be the

company structure, company size and company ownership.

Chapter 8

Chapter 8 will analyze the organizational culture, management style and stakeholder

expectations of the Sri Lankan commercial banks and perceive whether there are any

significant differences either by ownership, or size aspects.

Chapter 9

Chapter 9 will analyze the external environments of the Sri Lankan commercial banks

and those external environmental dimensions include the demand environment, market

competition, market share, company competitors and customers, company business and

government policies, major sources of funds and banks political, economic, social,

technological, legal environments etc. Any significant difference of the external

environmental dimensions either by size or ownership aspects will be highlighted.

Chapter 10

Chapter 10 will discuss the mission, vision and the corporate level and second level

long term goals of the Sri Lankan commercial banks and find out if there are any

significant differences either by size or ownership aspects.

Chapter 11

Chapter 11 will investigate the planning and planning systems at corporate level and

second level of the Sri Lankan commercial banks and highlight the significant

differences either by size, ownership aspects.

8

Chapter 12

Chapter 12 will investigate the strategic thinking capabilities of the Sri Lankan

commercial banks and highlight the significant differences either by size, ownership

aspects

Chapter 13

Chapter 13 will analyze the analytical tools and techniques which are used to develop

the banks strategies, corporate strategies and the management of quality of the Sri

Lankan commercial banks. Any significant differences by ownership, size aspects also

will be highlighted.

Chapter 14

This chapter will compare the major research findings of this research study with the

major research findings of other research studies carried out in other countries namely

Australia, India, and Thailand. The differences of the strategic management practices

between the countries will be highlighted.

Chapter 15

This chapter will discuss the major research findings of this research in terms of 6 major

research questions. This chapter also summarizes the unique features of the strategic

management practices by ownership and size aspects and the unique features of the

strategic management practices in Sri Lankan commercial banks. At the end of the

chapter the significance of the research and the limitations of the research will be stated.

1.6 Significance of the Research

Firstly, most of the concepts and theories in the domain of strategic management have

been developed in western countries but, this research study is specially designed to

explore the strategic management practices in Sri Lankan commercial banks and

therefore, this research will provide insight knowledge about strategic management

practices of a particular industry in a developing country.

9

Secondly, this study identifies the importance of strategic thinking capabilities in the

banks strategic management process which was lacking in the previous studies of

Christodoulou (1984), Bonn (1996), Nimmanphatcharin (2002), Kakanamveetil (2004),

and Angkasuvana (2005).

Finally, the major research findings of this study will provide the opportunity for the

individual banks to compare and assess their strategic management practices with other

banks in the Sri Lankan banking industry. That will help the individual banks to identify

the shortcomings and strengths of their strategic management practices.

10

Chapter 2: Background on Sri Lanka and the banking industry in Sri Lanka

2.1 Introduction This chapter will provide background on Sri Lanka and the banking industry of Sri

Lanka. Furthermore, the major external environmental factors that can affect the

strategic management practices of Sri Lankan commercial banks will be discussed.

2.2 Background on Sri Lanka Sri Lanka is an island situated in the Indian Ocean to the east of the southern tip of the

Indian subcontinent which is separated by the Palk Strait, a strip of shallow water 18

miles across its narrowest point. It has a total area of 66,000 squire kilometres and a

population of 20.7 millions. The capital of Sri Lanka is Sri Jayawardanepura Kotte and

the major cities with higher population are Colombo, Gampaha, Kurunegala, Kandy,

Kaluthara, and Ratnapura respectively. The geography of Sri Lanka is shown in figure

2.1.

Figure 2.1 Geography of Sri Lanka

Sri Lanka

11

The origins of Sinhalese are from the north Indian Aryans who came to the island in

500 BC. The other significant ethnic group the Tamils is from Dravidian origin.

Buddhism arrived to the country in 300 BC and provided the foundation to develop a

greater civilization around the cities of Anuradhapura and then Polonnaruwa. All the

kings who governed the country during these eras gave Buddhism a higher priority.

Buddhists- Sinhalese civilization in Sri Lanka came under attack during the colonial

eras of the Portuguese, the Dutch and the British. Sri Lankan politics since

independence from the British has been strongly democratic and all the governments

have been elected democratically.

74% of the Sri Lankan population is Buddhist Sinhalese, 13% Tamils, and 7% Muslims.

The official languages of Sri Lanka are Sinhala, Tamil and English. Sri Lanka is

struggling with a civil war since 1983, and the fights are still occurring in the northern

part of the country between the government forces and the LTTE (a guerilla

organization who fights for a part of the country). About 65,000 people have been killed

but they could not find a permanent solution to end the crisis permanently. The civil war

has caused a major setback to the development of the country. The ceasefire signed by

the government and the LTTE in 2002 gave the opportunity for the all citizens in the

country to enjoy the benefits of a peaceful environment but, unfortunately it has come to

an end in 2005.

Sri Lanka has a high level of literacy (93%) and a life expectancy of 73 years despite its

low income per capita. Sri Lanka is a developing country and its services sector

produces 55% of the GDP. The fastest growing sector which is manufacturing is

dominated by the garment industry, while the agricultural sector produces 18% of the

GDP and more than one of the third of the workforce is involved in the agricultural

sector.

2.3 Financial sector in Sri Lanka

The financial sector in Sri Lanka consists of financial institutions such as licensed

commercial banks, licensed specialized banks, registered finance companies, primary

dealers, the employee’s provident fund, insurance companies and financial markets

12

such as the foreign exchange market, the money and capital market, other informal

financial markets and the financial infrastructure consisting of the legal framework

underlying the financial system and the payment and settlement system (Central Bank

2005a). Even though there are so many financial institutions, the financial sector in Sri

Lanka is dominated by the licensed commercial banks and the licensed specialized

commercial banks which have 57% of the total assets and 94% of the total deposit

liabilities. The Central Bank of Sri Lanka is responsible for the smooth functioning of

the financial sector.

2.3.1 Central Bank of Sri Lanka

The Central Bank of Sri Lanka was established in 1949 by the monetary act and it

started operations on the 28th August 1950. The objectives of Central Bank was

amended by the monetary law act in 2002 and the newly established core objectives of

the Central Bank are maintaining economic and price stability, and maintaining

financial system stability (Central Bank 2005b). A higher degree of autonomy has been

given to the Central Bank to achieve their objectives and it closely works with the

Ministry of Finance when making policy decisions.

To safeguard price stability, the Central Bank needs to introduce and implement policies

to control imports and exports. Price stability of the country directly influences the

inflation rate and when price stability is high there is usually a low inflation rate for the

country. When the inflation remains low consumers and producers can make their

decisions more confidently and this is usually the basis for long term economic growth

for the country (Central Bank 2005a).

The Central Bank of Sri Lanka (2005a) defined financial system stability as “the

effective functioning of the financial system which create a favorable environment for

depositors, encourages efficient financial intermediation and the effective functioning of

markets and hence promotes investment and economic growth”. Central Bank also

recognized that lack of financial system ability increases bank failures. The core

functions of the Central Bank of Sri Lanka are listed in Table 2.1.

13

Table 2.1 Core functions of the Central Bank

Core functions of the Central Bank

Conduct of monetary policy Conduct of exchange rate policy Management of the official foreign reserves of Sri Lanka Issue and distribution of currency. The central bank has the exclusive right to issue banknotes and coins that are legal tender in Sri Lanka. Licensing, regulation and supervision of banks, finance companies and primary dealers in government securities. Provision of clearing and settlement facilities to financial institutions (commercial banks and primary dealers) holding settlement accounts with the Central Bank. Acting as the economic advisor, banker and fiscal agent of the government.

Source: Objectives, functions and organization, Central Bank 2005

2.3.2 Supervision of Banks

The Central Bank is responsible for the regulating and supervising of banks in the Sri

Lankan financial system to safeguard the depositors and investors. According to the

Banking Act and Monetary Law act, the Central Bank is the licensing authority for

banks and it issues two types of licenses, for the commercial banks and specialized

banks. Only commercial banks are able to maintain current accounts and the specialized

banks can maintain only savings accounts. The supervisory functions of Central Bank

include the issue orders on the licensing, operations and closure of banks, the prudential

requirements relating to banks, the resolution of weak banks and the enforcement of

regulatory actions (Central Bank 2005b).

14

2.3.3 Licensed commercial Banks (LCB)

Licensed commercial banks (LCB) have been the most important financial institutions

in Sri Lankan financial sector in terms of assets and the magnitude of financial services

provided. LCB accounted 46% of the total financial sector assets and 81% of the

banking systems assets (Central Bank 2005a). According to financial stability review of

the Central Bank of Sri Lanka (2006), there were six large commercial banks in the Sri

Lankan banking industry which in total have 81% of the total licensed commercial

banks assets. These six banks include 2 government owned banks and 4 locally owned

banks.

Table 2.2 shows the financial indicators of the LCB from 2001-2006. It is worth

mentioning that most of the LCB’s credits distributed to the trading, consumption,

housing and property development sectors respectively. The volume of LCB’s non

performing loans (NPL) and NPL ratios have reduced during last few years and that can

be highlighted as a major development in the banking industry. Return on asset ratio

increased 0.8 to 1.8 from 2002 to 2006. However, banks liquidity ratio has gone down

from 30.9% to 23.9% during the period of 2002-2006. During the period of 2002 and

2003 Sri Lanka’s commercial banks overall return on equity and liquidity ratios were

higher and that is mainly due to the economic growth reported by the Sri Lanka’s

financial sector because of the cease fire agreement between the government and the

LTTE. Thus, it is worth noting that the war between the government and LTTE has a

major influence on the country’s economy.

15

Table 2.2 Financial indicators of the LCB’s

Micro Prudential Indicators of the Banking Sector

2001 2002 2003 2004 2005 2006

Licensed Commercial Banks

1. Capital Adequacy Ratio - Tier I Capital Ratio (%)

7.8 9.3 8.9 9.3 12.2 10.5

2. Capital Adequacy Ratio - Total Capital Ratio (%)

8.6 10.3 10.3 10.3 12.8 11.7

3. Gross NPA as a % of Total Loans & Advances

15.3 14.5 12.5 8.9 6.8 5.4

4. Net NPA as a % of Capital Funds 134.7 93.7 52.3 29.8 16.5 12.6 5. Sectoral Credit Distribution (%) Trading 40.5 37.7 36.8 35.7 32.6 29.1 Financial 3.2 3.3 4.2 4.8 5.2 6.1 Agriculture 4.7 4.7 4.5 3.8 4.3 3.9 Industry 10.5 11.6 10.9 10.0 9.7 8.8 Tourism 1.3 1.4 1.4 1.3 1.5 1.5 Housing & Property Development 14.0 14.1 14.0 14.3 14.4 16.2 Consumption 11.6 12.5 14.1 16.3 17.3 19.4 Others 14.2 14.7 14.0 13.7 15.0 15.0 6. Return on Assets (%) 0.8 1.1 1.4 1.4 1.7 1.8 7. Return on Equity (%) 15.5 20.5 21.1 18.3 16.8 18.5 8. Liquidity Ratio, % (DBU) 30.9 33.2 26.1 26.3 24.2 23.9 9. Net Open Position (NOP), % of Capital Funds

5.4 3.1 (5.6) 2.8 0.01 0.01

Source: Financial system stability Report 2006, Central Bank of Sri Lanka

2.3.4 Challenges faced by the Commercial banking sector

Piyasena & Corera (2006) identify that Sri Lankan capital markets are underdeveloped

and that they have not posed serious competition to the banking sector hence

commercial banks were able to maintain a high percentage of assets in the financial

sector. According to Ahamed (2006) Sri Lankan financial markets have somewhat

lagged behind the rest of their regional counterparts. Madurapperuma (2006)

categorizes 24 banking functions that the commercial banks in Sri Lanka currently are

performing such as financial intermediation, diversification of credit risk, asset stripping

etc., and points that banking industry is not dying but, other financial institutions and

16

instruments such as merchant and investments banks, insurance companies, leasing

companies, unit trusts, portfolio fund managers are trying to replace banks. However,

Madurapperuma (2006) concludes that mindset and the habits of the people in Sri Lanka

had led to an existence of a dominant banking system and it will take some time to

replace it by other financial institutions and by other instruments. Abeyaratna (2005)

mentions non-banking organizations involved in taking deposits have been growing

both in terms of numbers as well as volume, and claims that it is a potential threat for

the commercial banks which depend on retail deposits to mobilize funding for their

growing asset portfolios. Thus, we can expect more developments in financial markets

in Sri Lanka in the near future which directly influence the percentage of total assets

owned by the commercial banks. Hence, banks will need to deliver higher returns for

their shareholders in order to keep them with the banks in the future and to achieve that

goal banks will need to use their assets more efficiently to get maximum returns.

Perera (2006) asserts that commercial banks in Sri Lanka have to deal with an

increasing pace of change in the competitive environment within which they operate

and he proposes four key elements for the banks to adopt to successfully face those

changes such as risk management, technology, service excellence, and relationship

management. Kumara (2006) claims that despite the technology spread in the field of

banking, Sri Lankan people preferred the service with a human touch rather internet

banking and this highlight the importance of branch banking with higher technology.

Therefore, banks need to open branches through out the island to gain more customers

as most of the consumers of Sri Lankan commercial banks preferred not to use internet

banking facilities but, like to visit branches for their needs.

2.3.5 Risks being a Bank in Sri Lanka

Madurapperuma (2005) recognizes three broad categories of risks that the commercial

banks can face such as credit risk, market risk and operational risk. Credit risk is the

risk of loss due to a debtor’s non-payment of a loan or other line of credit and this might

be the most significant risk that a bank can face. Market risk comes from the changes in

the market prices such as exchange rates, interest rates, and equity and commodity

prices. Operational risk can be defined as the risk of loss resulting from failed internal

17

processes, people and systems or from external events. Banks have to take risk when

they do business and those risks leads to gains or losses. Madurapperuma (2005),

Parekh & Jayasinghe (2006) identifies the importance of capital adequacy and asset

quality to deal with these risks.

The credit growth rate remained at 21% at the end of year 2006 and it has been at a high

level during the recent past (Central Bank 2006). The growth of credit was due to higher

credits demanded from consumption and housing and construction industries. The

volume of non performing loans (NPL) and the ratio of NPL to total loans in the past

few years have reduced but, there has been a slight increase in last few months in the

year of 2006. Commercial Banks reported having higher provision covers for their NPL

and it was reported that government banks have a provision cover of 80% of the NPL

(Central Bank 2006). Thus, the Central Bank thinks there is no credit risk for the Sri

Lankan commercial banks in the short term but is planning to introduce policies to

restrict the execution rights of banks for the loans of above Rs. 5 million as a solution to

reduce the credit risk of the banks.

The banking industry is highly dependent on interest income and therefore, fluctuations

in interest rates heavily influence the banks success or failure (Central Bank 2006).

Inflation influences the interest rates and Central Bank allows banks to increase their

interest rates for deposits and lending’s gradually in response to the inflation rates. It

was reported that the banking sector in Sri Lanka have not been adversely affected by

the fluctuations in interest rates and banks continue to maintain their high profits further

(Central Bank 2006).

In addition to operational risks which can occur due to human errors and system failures

the Central Bank of Sri Lanka identified two other kinds of operational risks which can

heavily influence the banking industry in Sri Lanka (Central Bank 2006). First risk is

the concentration of shareholder power of large and medium sized locally owned banks.

There is a trend to acquire banks significant shareholdings through indirect ways and

create a monopoly in the banking industry by one or very few businessmen and that can

adversely affect the performance of the entire banking industry in Sri Lanka. To address

this issue Central Bank has introduced a new share ownership policy for banks which

allows a maximum shareholder limit at 15% while retaining the threshold limit at 10%

18

and shareholdings exceeding 15% need to get the approval from the Monetary Board

only for special situations (Central Bank 2006). The second kind of risk involves the

large financial firms which have banks as part of their company. Large number of cross

shareholdings, common directors and inter group transactions which lead to abuse of

power can adversely affect the banking system in Sri Lanka (Central Bank 2006).

2.4 Macro economic environment of Sri Lankan commercial banks

The global economy growth rate in the year 2005 and 2006 were 4.9% and 5.1%

respectively and it was expected to grow 4.9% in the year 2007 (see table 2.3).

Therefore, global financial market conditions remain positive for the Sri Lankan

financial system and all the major export markets are expected to grow steadily in the

year 2007 and also major import markets such as India, China and South Korea are

expected to grow more rapidly. However, Central Bank of Sri Lanka identified some

risks that can influence the Sri Lankan financial system negatively in the longer term.