Embed Size (px)

Citation preview

75

STATE AID CONTRIBUTION TO RESTORING THE EUROPEAN

FINANCIAL SECTOR

INGRID MAGDA ROŞCA

University of Girona

Plaça Sant Domènec, 3

SPAIN

ANA-CRISTINA BÂLGĂR

Institute for World Economy

Centre for European Studies Department

Romanian Academy

13 Calea 13 Septembrie, 050711, Bucharest

ROMANIA

Abstract: As the general economic context created by exacerbation of the global

financial crisis has heavily affected the European Union (EU) banking sector, taking into

account the systemic nature of this sector and its importance for the European economy,

substantial government support took off, in the form of state aid directed primarily to the

financial sector. Thus, while many Member States have proclaimed the introduction of new

measures with the purpose of supporting their financial institutions and contributing

effectively to providing common financial market stability, the European Commission has

emphasized the urgency that such help is conducted at EU level. Accordingly, since the

economic situation in several Member States was critical and there was a serious risk of a

potential negative impact on the overall European financial market, the European

Commission considered as appropriate to adopt a series of regulations in order to combat the

crisis in the banking sector more specifically. Hence, through the coordinated effort of

national authorities and the measures taken by each Member State, correlated with the

European Commission’s State aid control discipline and guidance for general schemes, as

well as for ad-hoc interventions at country level, it became possible not only to recover the

confidence in the financial markets, but also to stabilize and restore them, avoiding single

market distortions and mitigating moral hazard.

In the light of the above, this paper firstly aims to present and analyze through a

comparative approach the total amount of national State aid measures that has been given to

the European financial sector since the start of the crisis to the present, and, furthermore, to

assess the form and type of the aid granted to the financial sector, by comparing the actual

aid level of the different measures. Subsequently, our article will focus on the effectiveness

and efficiency of policy interventions, considering the fact that state aid to the financial sector

has accounted for the bulk of the overall EU State aid during the crisis. Finally, the paper

will address the role of the unprecedented amount of state aid used by the member states for

their financial sectors in restoring the financial stability and the normal functioning of the

European financial market.

Key words: State aid, financial crisis, EU financial sector, economic crisis,

bankruptcy, institutions.

76

I. Introduction

According to the literature in the field (Meiklejohn, 1999), state aid is usually

considered as a "public response" aiming to correct or compensate for ineffective results in

the functioning of markets (market failures). Viewed from such a perspective, state aid may

be associated with public goods, externalities, imperfect mobility of production factors, or

network systems that can generate network effects (i.e. the proper functioning of

industries/companies can be a positive externality to other industries/firms).

In the specific case of the financial sector, its features present distinct elements of

network externalities. Thus, given the importance of financial institutions and their high level

of interconnectedness, there is major potential of triggering a systemic risk that would create

imbalances in the entire financial system. Under such circumstances, the role of state aid to

the financial sector is to reduce the risks associated with bank assets, by increasing bank

solvency, enhancing confidence in the financial system and, finally, ensuring the flow of

finance to the real economy

Also, given that any state aid may, by its nature, produce negative spill-over effects on

other financial institutions that do not receive it (Naes-Schmidt et al., 2011) - including those

in other Member States - the European Commission has undertaken a number of regulations

to ensure that the Community is based on appropriate and efficient mechanisms to minimize

such distortions and the potential abuse of the preferential situations (distortion of

competition) or the risk of moral hazard. 23

II. The importance and need to support the financial sector in crisis

The systemic nature of the financial sector activity is enhanced by the main actors

operating in the financial markets (European Banking Federation - EBF, 2010), namely major

institutions which, due to their size and the functions they perform, have a significant share at

international and national level and, therefore, their possible failure would generate an

interruption of work by major financial services providers, with severe consequences for the

economy as a whole.

As such, the first arguments in favour of taking the appropriate measures to maintain

financial stability in the EU Member States reside in the plight of the previously sound banks

affected by the deepening crisis, the high degree of integration and interdependence of the

European financial markets and the severe repercussions that might have the potential to lead

to the bankruptcy of financial institutions relevant to the system, once the crisis has

intensified.

The activity of the financial sector makes a vital contribution to economy as a whole,

as both companies and consumers turn to the financial system to obtain loans, to deposit their

savings, or undertake various financial transactions. According to specific studies (EBF,

2010), in recent years about 85% of the external financing in the EU private sector has been

1 In economic theory, the phenomenon of moral hazard is defined as a situation in which the financial institution gets

involved in a risky event or strategy in the market, knowing that it is protected against that risk and some other party will

incur the cost, namely based on potential action of government bailout.

77

based on bank loans24, which met liquidity needs of major importance for entrepreneurship,

stimulating economic growth.

Another argument that justified the stepping up of support measures for the financial

sector is the essential functions it performs for the real economy. Through its role, state aid to

individual financial firms facing difficulties will help to:

(i) restore the general confidence in the banking sector - which will generate better

customer interaction with the financial institutions;

(ii) improve the confidence in the interbank markets – generating more efficient

interaction between banking institutions;

(iii) restore the financial sector and improve its ability to support real economy.

It must also be pointed out that all the other specific objectives of state aid to the

financial sector should be circumscribed to these three basic principles. For example, the

initiative to rescue an individual financial institution requires Member States to primarily

consider protecting depositors (Objective 1), stabilizing financial markets (Objective 2),

lending support to firms and consumers (Objective 3). That is why action at national and EU

level will focus, primarily, to protect the financial system.

III. Redirecting State aid in the economic context of the financial crisis

The financial crisis was a huge challenge for the EU regulation in the field of state aid.

Designed as a set of regulations aiming at maintaining a fair level of competition in the Single

Market, with the onset of the crisis, the system had to adapt itself to exceptional

circumstances. The size and nature of state aid and the number of measures and schemes

examined by the European Commission since 2008 have been unprecedented in the history of

the Union, causing a paradigm shift in the rulemaking field (Sutton et al, 2010).

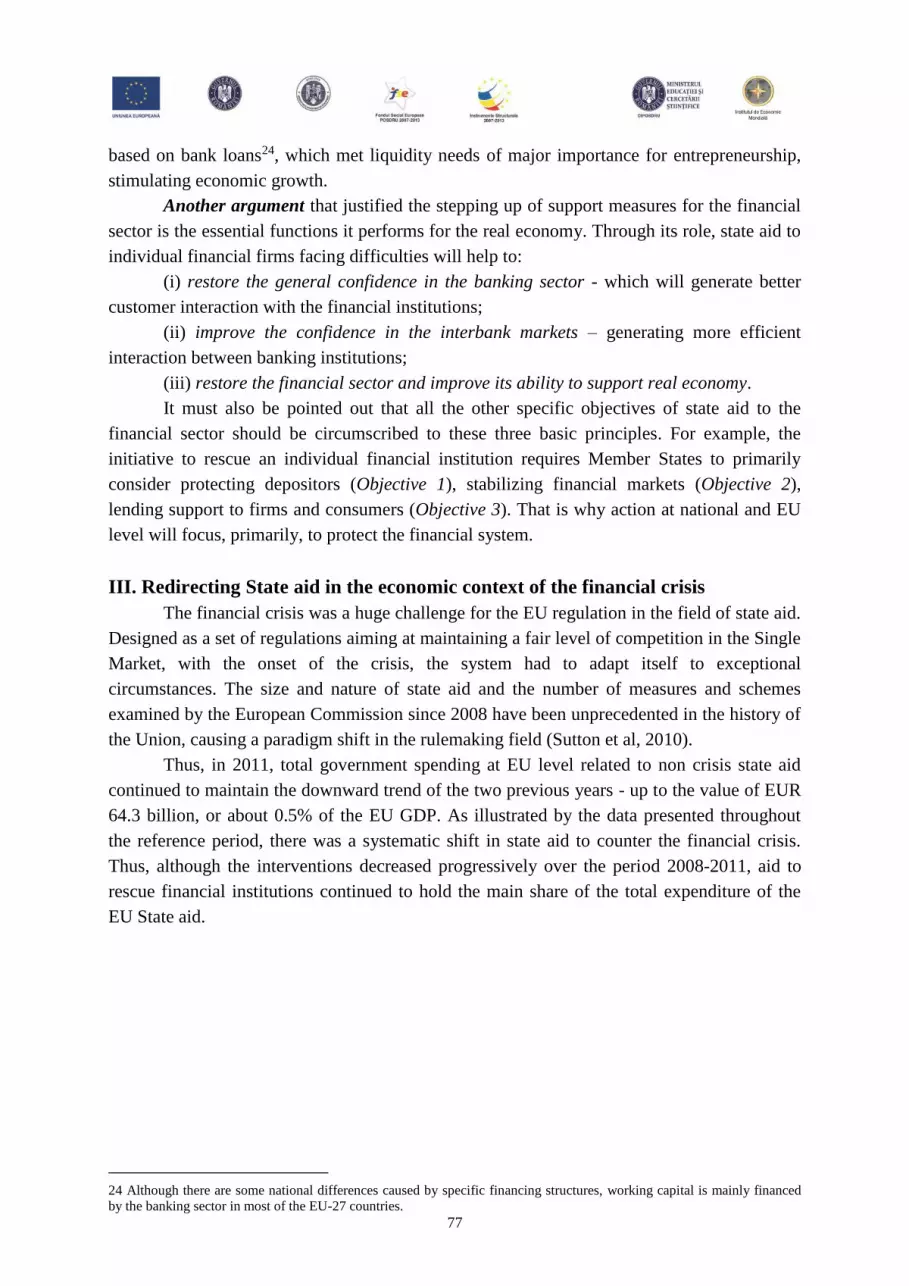

Thus, in 2011, total government spending at EU level related to non crisis state aid

continued to maintain the downward trend of the two previous years - up to the value of EUR

64.3 billion, or about 0.5% of the EU GDP. As illustrated by the data presented throughout

the reference period, there was a systematic shift in state aid to counter the financial crisis.

Thus, although the interventions decreased progressively over the period 2008-2011, aid to

rescue financial institutions continued to hold the main share of the total expenditure of the

EU State aid.

24 Although there are some national differences caused by specific financing structures, working capital is mainly financed

by the banking sector in most of the EU-27 countries.

78

Graph 1: Annual overall amount of State aid granted in the EU, during 2008-2011

(billion EUR)

73.9

3457.5

3531.4

75.8

541.7

617.5

71.3

383.6

454.9

64.3

273.7

338

0500

10001500

20002500

30003500

4000

2008

2009

2010

2011

TOTAL State aid

State aid related to the crisis

Non crisis State aid*

Source: DG Competition Database (2012);

Note (*): Data covers all State aid measures, except for the rail sector.

Although Member States have continued their efforts to reduce the overall level of aid,

this decrease was due to budget restrictions applied in many EU-27 countries. Obviously, this

reduction of costs contributed to the overall trend of declining State aid during 2008-2011.

IV. State aid in support of the financial sector

IV.1. Brief presentation of financial sector vulnerabilities against the

background of the EU crisis

The disturbances in the EU financial markets, which continued in 2011, have imposed

extensive intervention from the European governments, designed to help mitigate the negative

effects of the shock. In this respect, state aid to financial institutions has been instrumental in

the process of restoring confidence in the financial sector and avoiding triggering a systemic

crisis.

Although tensions in sovereign bond markets could be alleviated by adopting political

decisions crucial to the EU and by providing, in 2012, through the European Central Bank

(ECB), a massive influx of liquidity for the EU banking sector, the EU banking sector has still

remained fragile, as banks continued to face a wide range of pressures. These included the

need to strengthen the capital base in order to create a limit to face the risks of default and

devaluation, with negative impact on the banks’ balance sheets. Strengthening the capital base

of financial institutions must be achieved without disrupting the credit needs of real economy.

With the increased risk associated with sovereign bonds, banks must increase their

capital in order to cover the risk of the portfolios held. But since the decline in investor

confidence has reduced the ability of banks to raise private capital, it was necessary to

strengthen the capital base of public funds. However, given that the European banks’ portfolio

primarily comprises national bonds, the financial situation at the level of the Member States

further deteriorates after the state’s intervention in the banking sector, increasing the risk

79

related to sovereign bond portfolios, the consequence of which being the need to mobilize

additional capital25.

Given the worsening sovereign debt crisis in mid-2011, the Member States and the

European Commission reached an agreement on a package of measures to strengthen the

capital of banks and provide guarantees for their debt (so-called "banking package").

Subsequently, on December 1st, 2011, the European Commission extended the measures

relating to State aid for the financial sector in crisis and considered developing a set of

permanent state aid measures to banks, applicable after the stabilization of the current

situation26.

IV. 2. The amount of State aid approved and used in the financial sector27

In order to remedy the serious disturbances in the financial markets of the Member

States, between October 1st, 2008 and October 1st, 2012, the European Commission adopted

350 decisions on the financial services sector, which authorized the modification or extension

of over 50 state aid schemes and targeted 90 financial institutions. Measures meant to counter

the financial crisis have been approved for all the Member States, except Bulgaria, the Czech

Republic, Estonia, Malta and Romania.

Box 1: The main types of state aid measures granted to the financial and banking system

As shown by academic literature (Sutton et. Al, 2010), state aid to the financial sector can be supplied in four

main forms:

1. Government guarantees for deposits, bonds or liabilities of financial institutions. In the current exceptional

circumstances, it may prove to be necessary to assure the persons holding deposits with financial institutions that

they will not suffer losses, so as to limit the possibility of massive withdrawals under the effects of growing

panic and the related unwanted negative side effects on healthy banks. Therefore, in the context of a systemic

crisis, the general guarantees that protect retail deposits and retail debt may represent a legitimate component of

the response given by public authorities. General guarantees for the protection of deposits may be extended to

cover a wide range of bank assets, in order to avoid bottlenecks in the financial system. Also, national

governments may also guarantee certain categories of bank loans and bonds, in order to maintain the capacity of

bank institutions to mobilize funds.

2. Recapitalization - government measures of support to strengthen the capital base of the financial institutions

or to facilitate the injection of private capital by other means, so as to prevent negative systemic effects.

3. A special form of losses absorption in the financial system is the creation of the so-called "bad-banks" to take

over the impaired assets of the financial institutions into bankruptcy. Public impaired asset relief aid represent

state aid to the extent that, due to them, the beneficiary bank no longer has to incur a loss or create a reserve for a

potential loss related to these assets and/or to deploy regulatory capital for other uses.

4. Nationalization of banks - currently troubled financial institutions are taken over wholly or largely by the

state. The nationalization process itself is not a form of state aid, but capital injections for saving an ailing bank

are.

Source: Synthesis performed by the authors based on the literature in the field.

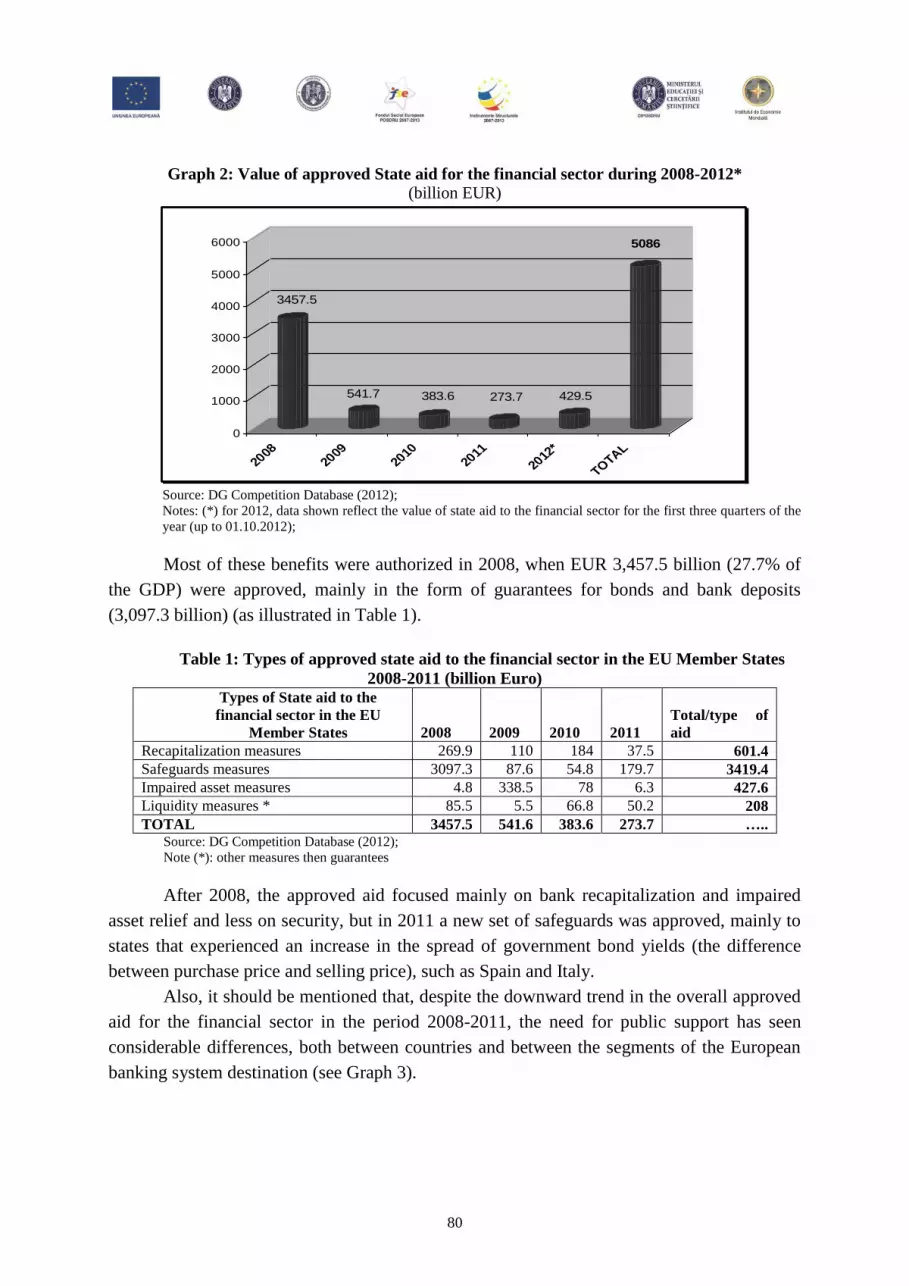

Thus, between October 2008 and October 2012, the European Commission approved

aid for the financial sector totalling EUR 5,086 billion (representing approximately 40.3% of

the EU GDP) (Graph 2).

25 In the academic literature, this phenomenon of chained effects is known as "sovereign feedback loop".

26 ECOFIN Council Conclusions of November 8th, 2011.

27 State aid for the financial sector is expressed as: (i) the amount of aid committed (the volume of assumed aid) - maximum

aggregate amount of State aid measures adopted by Member States and approved by the European Commission (this value

indicates the maximum authorized volume to support Member States but not the amounts used) and (ii) the value of used aid,

which is the actual amount of the aid measures implemented by Member States.

80

Graph 2: Value of approved State aid for the financial sector during 2008-2012*

(billion EUR)

3457.5

541.7 383.6 273.7 429.5

5086

0

1000

2000

3000

4000

5000

6000

2008

2009

2010

2011

2012

*

TOTA

L

Source: DG Competition Database (2012);

Notes: (*) for 2012, data shown reflect the value of state aid to the financial sector for the first three quarters of the

year (up to 01.10.2012);

Most of these benefits were authorized in 2008, when EUR 3,457.5 billion (27.7% of

the GDP) were approved, mainly in the form of guarantees for bonds and bank deposits

(3,097.3 billion) (as illustrated in Table 1).

Table 1: Types of approved state aid to the financial sector in the EU Member States

2008-2011 (billion Euro) Types of State aid to the

financial sector in the EU

Member States 2008 2009 2010 2011

Total/type of

aid

Recapitalization measures 269.9 110 184 37.5 601.4

Safeguards measures 3097.3 87.6 54.8 179.7 3419.4

Impaired asset measures 4.8 338.5 78 6.3 427.6

Liquidity measures * 85.5 5.5 66.8 50.2 208

TOTAL 3457.5 541.6 383.6 273.7 ….. Source: DG Competition Database (2012);

Note (*): other measures then guarantees

After 2008, the approved aid focused mainly on bank recapitalization and impaired

asset relief and less on security, but in 2011 a new set of safeguards was approved, mainly to

states that experienced an increase in the spread of government bond yields (the difference

between purchase price and selling price), such as Spain and Italy.

Also, it should be mentioned that, despite the downward trend in the overall approved

aid for the financial sector in the period 2008-2011, the need for public support has seen

considerable differences, both between countries and between the segments of the European

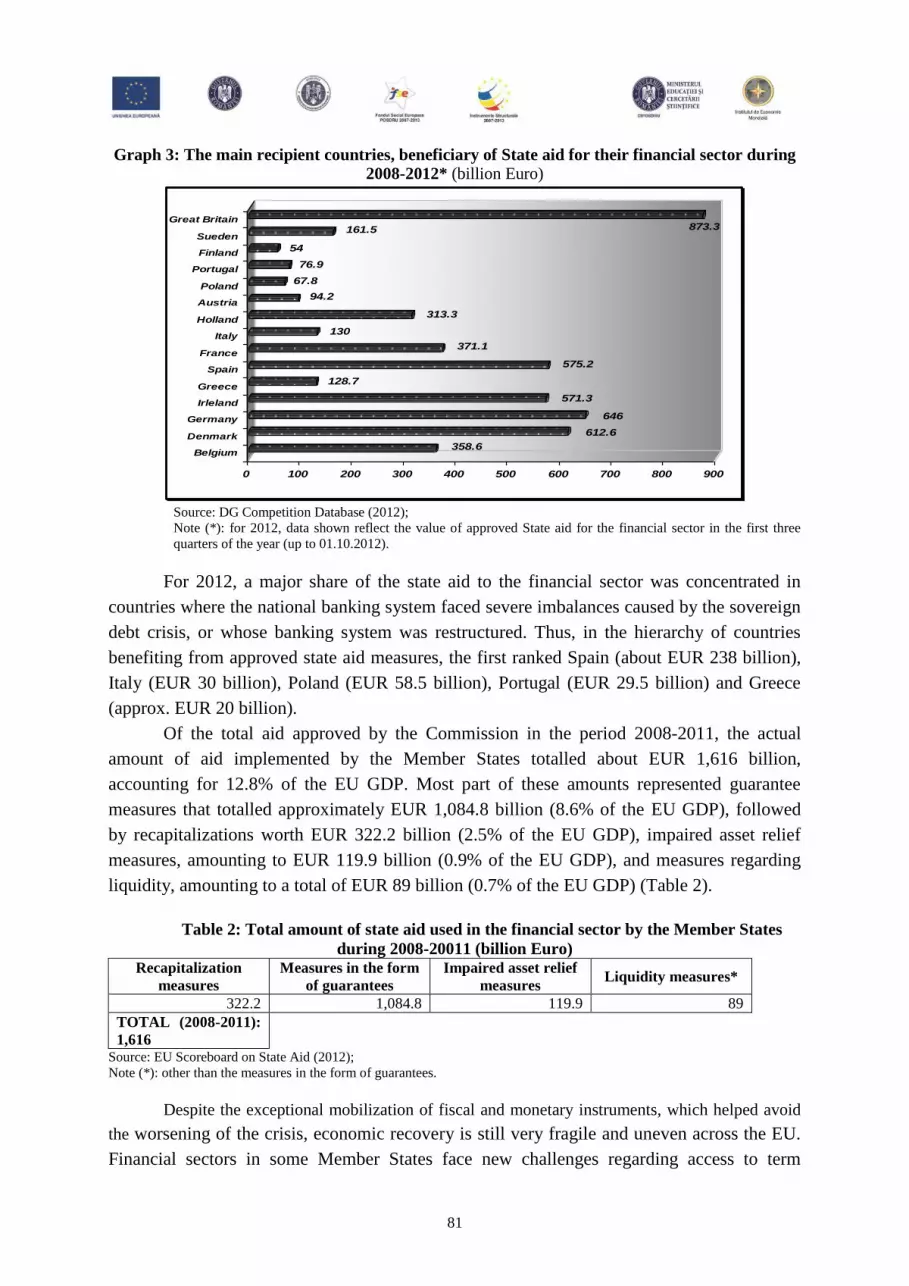

banking system destination (see Graph 3).

81

Graph 3: The main recipient countries, beneficiary of State aid for their financial sector during

2008-2012* (billion Euro)

358.6

612.6

646

571.3

128.7

575.2

371.1

130

313.3

94.2

67.8

76.9

54

161.5 873.3

0 100 200 300 400 500 600 700 800 900

Belgium

Denmark

Germany

Irleland

Greece

Spain

France

Italy

Holland

Austria

Poland

Portugal

Finland

Sueden

Great Britain

Source: DG Competition Database (2012);

Note (*): for 2012, data shown reflect the value of approved State aid for the financial sector in the first three

quarters of the year (up to 01.10.2012).

For 2012, a major share of the state aid to the financial sector was concentrated in

countries where the national banking system faced severe imbalances caused by the sovereign

debt crisis, or whose banking system was restructured. Thus, in the hierarchy of countries

benefiting from approved state aid measures, the first ranked Spain (about EUR 238 billion),

Italy (EUR 30 billion), Poland (EUR 58.5 billion), Portugal (EUR 29.5 billion) and Greece

(approx. EUR 20 billion).

Of the total aid approved by the Commission in the period 2008-2011, the actual

amount of aid implemented by the Member States totalled about EUR 1,616 billion,

accounting for 12.8% of the EU GDP. Most part of these amounts represented guarantee

measures that totalled approximately EUR 1,084.8 billion (8.6% of the EU GDP), followed

by recapitalizations worth EUR 322.2 billion (2.5% of the EU GDP), impaired asset relief

measures, amounting to EUR 119.9 billion (0.9% of the EU GDP), and measures regarding

liquidity, amounting to a total of EUR 89 billion (0.7% of the EU GDP) (Table 2).

Table 2: Total amount of state aid used in the financial sector by the Member States

during 2008-20011 (billion Euro) Recapitalization

measures

Measures in the form

of guarantees

Impaired asset relief

measures Liquidity measures*

322.2 1,084.8 119.9 89

TOTAL (2008-2011):

1,616 Source: EU Scoreboard on State Aid (2012);

Note (*): other than the measures in the form of guarantees.

Despite the exceptional mobilization of fiscal and monetary instruments, which helped avoid

the worsening of the crisis, economic recovery is still very fragile and uneven across the EU.

Financial sectors in some Member States face new challenges regarding access to term

82

funding and asset quality caused by the economic recession and the decline in public and

private sector indebtedness.

IV3. Specific tools for State aid intended for the financial sector

A. Governmental guarantee measures for deposits, bonds or liabilities granted to

financial institutions

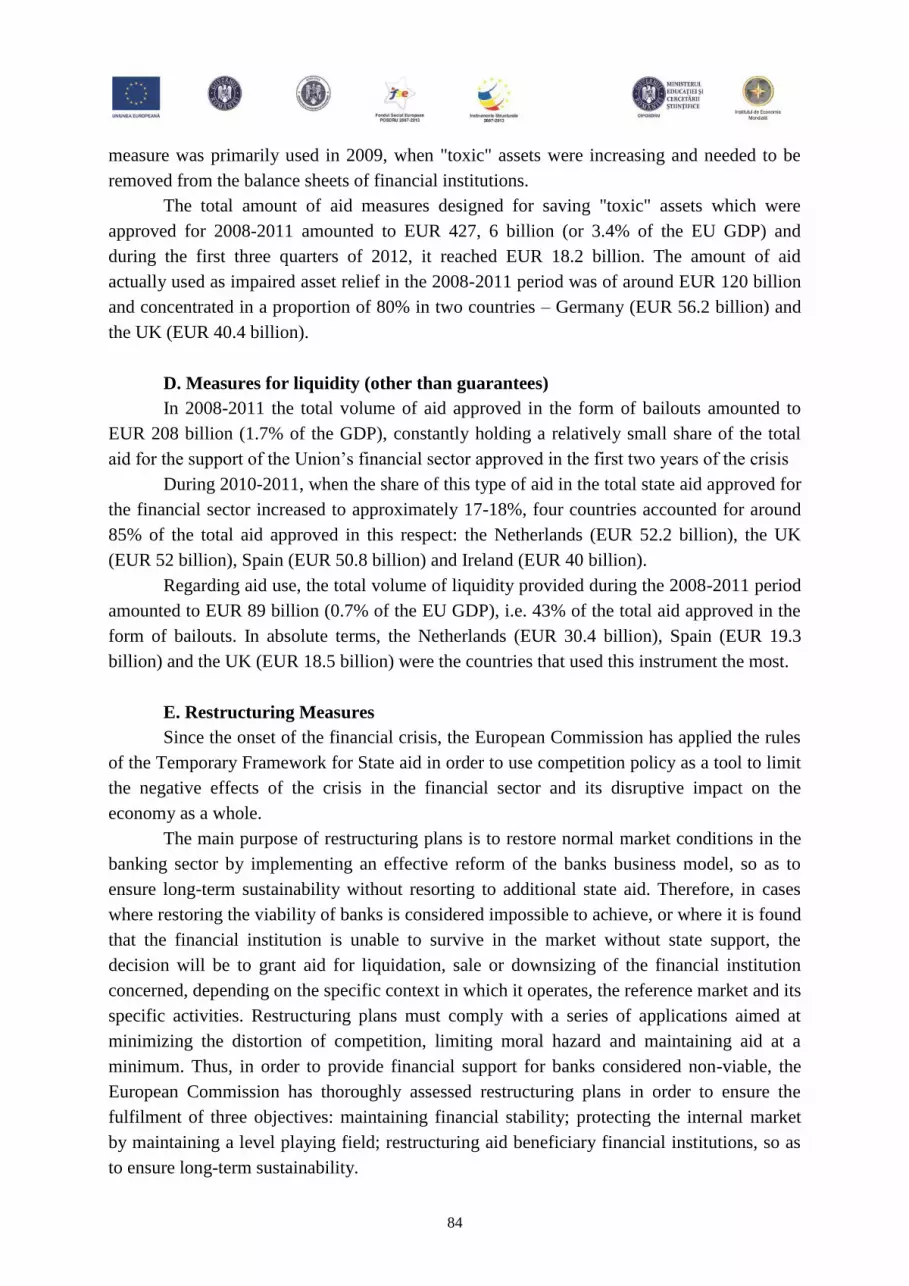

Guarantees were the main tool used by the Member States in their response to the

crisis faced by the European financial sector (Graph 4). As noted above, most of the guarantee

schemes were approved in the early stages of the global crisis - from the autumn of 2008 to

mid 2009 - and have proven effective in addressing the negative aspects created by the

liquidity shortage and the confidence loss that temporarily blocked the interbank market,

causing a sudden increase in funding costs. If during the 2008-2011 interval, the member

states approved guarantees totalling 3419.4 billion (see Table 1), in the first three quarters of

2012, these totalled EUR 227.2 billion (amounting to 3,446.6 billion for the entire October

2008-October 2012 period, accounting for a share of 28.9% of the EU GDP).

Graph 4: The amount of guaranties and their share in the total crisis aid approved by the

Member States, 2008-2011 (billion Euro and %)

89.1%

(3097.3 bn.)

16.2%

(87.6 bn)54.9%

(54.9 bn.)

69.3%

(179.7 bn.)

0

500

1000

1500

2000

2500

3000

3500

2008 2009 2010 2011

Value Share in total State aid EU 27

Source: DG Competition Database (2012).

The largest part of the total aid approved in 2012 in the form of guarantees, was

represented by two guarantee schemes re-introduced by Spain (amounting to EUR 119

billion) and Italy (EUR 30 billion), followed by the extension of the length and value of the

guarantee schemes launched by Greece and Portugal in 2011. Also, in the same period the

UK, Denmark and Latvia introduced new guarantee schemes, and two relevant financial

groups received ad-hoc measures - Dexia (Franco-Belgian financial group) and WestLB

(Germany).

As regards the value of aid in the form of guarantees actually used in the EU Member

States during 2008-2011, this amounted to EUR 1,084.8 billion (8.6% of GDP), and

represented a 32% share of the total measures of this type approved at the Member States

83

level. The main countries that used guarantees were Ireland (EUR 284 billion), the UK (EUR

158.2 billion), Denmark (EUR 145 billion) and Germany (EUR 136 billion).

B. Recapitalization measures

As indicated by the data shown in Table 1, during 2008-2011, the total recapitalization

measures approved by the European Commission amounted to EUR 601 billion. The highest

value for capital injections was approved in 2008 (about 270 billion), but the highest share in

the total crisis aid approved in the EU (48%) was recorded in 2010.

Regarding the share of capital injections in the national GDP, Ireland is the leader

country with the largest budget approved (approx. 58% of the GDP), followed by Spain

(19.5%) and Greece (16%). The deterioration of sovereign market conditions in several EU

countries, which started in the second half of 2011, was directly transmitted to the European

banking system, which was already undergoing major restructuring. As such, banks that were

holding Spanish and Italian government bonds in their portfolios incurred substantial losses in

the financial markets, as a result of the decrease in the value of these assets.

Moreover, the involvement of the public sector in restructuring Greece’s public debt

caused an additional deterioration of Greek sovereign bonds. As a consequence, in the autumn

of 2011, the European Banking Authority (EBA) conducted an assessment of the capital need

(a survey that included 71 European banks), in order to restore confidence in the EU financial

market. As a result of this assessment, which showed that a group of 27 banks had a capital

deficit of around EUR 76 billion, EBA issued a formal recommendation in December that

year, providing that by mid 2012, all financial institutions had to create a reserve of around

9% of the entire capital held.

However, most of these banks have demonstrated their ability to raise capital from

private investors without having to rely on public support.

According to a 2011 report by EBA, three Portuguese banks, an Italian bank and one

in Slovenia appealed to government support.

Regarding the amount of aid for recapitalization actually used in 2008-2011, this

amounted to about EUR 322.2 billion (2.5% of the EU GDP), accounting for 54% of all the

measures approved for the same period. The United Kingdom (EUR 82.4 billion), Germany

(EUR 63.2 billion) and Ireland (EUR 62.8 billion) are among the countries with the largest

capital injections.

C. Impaired asset relief measures

As shown in the literature, (IMF, 2013), the implementation of impaired asset relief

measures is adequate to the extent that there is a high degree of uncertainty relating to the

actual value of certain assets, and where it is likely for the market to overestimate the long-

term real risk posed by such assets, as was the case at the onset of the financial crisis for

certain categories of assets.

As during the period 2010-2011 the uncertainty regarding the actual value of asset

classes decreased, state aid in the form of impaired asset relief measures decreased in intensity

(recapitalization being the proper measure in this financial climate). Therefore, this type of

84

measure was primarily used in 2009, when "toxic" assets were increasing and needed to be

removed from the balance sheets of financial institutions.

The total amount of aid measures designed for saving "toxic" assets which were

approved for 2008-2011 amounted to EUR 427, 6 billion (or 3.4% of the EU GDP) and

during the first three quarters of 2012, it reached EUR 18.2 billion. The amount of aid

actually used as impaired asset relief in the 2008-2011 period was of around EUR 120 billion

and concentrated in a proportion of 80% in two countries – Germany (EUR 56.2 billion) and

the UK (EUR 40.4 billion).

D. Measures for liquidity (other than guarantees)

In 2008-2011 the total volume of aid approved in the form of bailouts amounted to

EUR 208 billion (1.7% of the GDP), constantly holding a relatively small share of the total

aid for the support of the Union’s financial sector approved in the first two years of the crisis

During 2010-2011, when the share of this type of aid in the total state aid approved for

the financial sector increased to approximately 17-18%, four countries accounted for around

85% of the total aid approved in this respect: the Netherlands (EUR 52.2 billion), the UK

(EUR 52 billion), Spain (EUR 50.8 billion) and Ireland (EUR 40 billion).

Regarding aid use, the total volume of liquidity provided during the 2008-2011 period

amounted to EUR 89 billion (0.7% of the EU GDP), i.e. 43% of the total aid approved in the

form of bailouts. In absolute terms, the Netherlands (EUR 30.4 billion), Spain (EUR 19.3

billion) and the UK (EUR 18.5 billion) were the countries that used this instrument the most.

E. Restructuring Measures

Since the onset of the financial crisis, the European Commission has applied the rules

of the Temporary Framework for State aid in order to use competition policy as a tool to limit

the negative effects of the crisis in the financial sector and its disruptive impact on the

economy as a whole.

The main purpose of restructuring plans is to restore normal market conditions in the

banking sector by implementing an effective reform of the banks business model, so as to

ensure long-term sustainability without resorting to additional state aid. Therefore, in cases

where restoring the viability of banks is considered impossible to achieve, or where it is found

that the financial institution is unable to survive in the market without state support, the

decision will be to grant aid for liquidation, sale or downsizing of the financial institution

concerned, depending on the specific context in which it operates, the reference market and its

specific activities. Restructuring plans must comply with a series of applications aimed at

minimizing the distortion of competition, limiting moral hazard and maintaining aid at a

minimum. Thus, in order to provide financial support for banks considered non-viable, the

European Commission has thoroughly assessed restructuring plans in order to ensure the

fulfilment of three objectives: maintaining financial stability; protecting the internal market

by maintaining a level playing field; restructuring aid beneficiary financial institutions, so as

to ensure long-term sustainability.

85

As such, in the context of the financial crisis, all Irish banks received state aid and

were undergoing for a restructuring process. For example, Anglo Irish Bank received

substantial government aid and the restructuring plan submitted to the European Commission

by the national authorities was approved in 2011, when it was decided to liquidate the bank

together with the National Building Society (NBS).

In the Netherlands, two major banks are subject to restructuring (ING and ABN

Amro), and ATE Bank of Greece was split into two distinct structures - part of the assets

being transferred to Piraeus Bank, and the other part taken over by a "toxic" assets bank.

V. The impact of State aid to the financial sector on free competition

V.1. Did State aid manage to maintain a level playing field?

For the European Union, one of the relevant challenges brought up by the financial

crisis, was the development and use of policies, instruments and leverages meant to counter

the negative effects of the crisis while maintaining and ensuring a level playing field in the

internal market. Therefore, a major concern of EU analysts (Sutton et. al, 2010) is whether the

crisis state aid framework managed to create such a level playing field.

A first obstacle identified by European experts (European Commission, 2011) to state

aid efficiency was the Member States awareness of the specific rules. Thus, some EU

countries have a broader experience in using state aid, while the new Member States face EU

bureaucracy. Also, financial institutions in certain Member States were better structured,

while in others the need for greater public support was more acute. The use of the different

state aid instruments varied according to the specific national financial system - most Member

States implemented schemes for the entire banking sector, a small number of countries used

individual measures of support, and some states granted the state aid.

Differences in the implementation of aid measures by Member States can be

illustrated by comparing the financial system in two EU countries placed at opposite poles:

Germany and Greece. While the first country displayed relatively reduced financial sector

imbalances, because only a few financial institutions had been affected by the crisis, Greece

faced major problems in the context of its entire financial sector being affected, a situation

which could not be solved by relaying solely on public resources. In essence, this example

illustrates the difficulty of maintaining a fair competitive framework in the field of state aid to

the financial sector, if fundamental differences between Member States exist. A possible

explanation for the occurrence of such disparities in the competitive environment lies not only

in the application of national policies or the inadequate knowledge of EU rules on state aid,

but in deficient bank management.

This negative aspect cannot be approached by means of state aid instruments, the only

action that may be taken by the European Commission being to monitor whether the

implementation of state aid is done in accordance with the legal framework and with the

guidelines, in order to ensure uniform conditions for granting state aid in all Member States.

86

V.2. The stringency of Community rules on state aid

During the financial crisis, state aid rules have been a lot more relaxed, but this was an

essential condition for ensuring the functioning of the financial sector and of the real economy

(Nicolaides & Rusu, 2010). Against the backdrop of the crisis, the financial sector of the

Member States needed broader support, therefore, the Member States granted more aid, and

the European Commission has approved it. However, despite the need for increased funding

and the fact that the aid was not unlimited, specialists (Lyons&Zhu, 2013) also voiced

opinions concerning a certain enhanced "generosity" of the European Commission, which

approved excessive state aid.

Thus, between 2002-2007, the state aid for the financial sector granted by the Member

States accounted for an annual share of around 2% of the GDP; in 2008 this aid represented

27.6% of the EU GDP and for the entire period 2008-2012, around 40.3% of the GDP. Of

course there is the argument that these amounts reflected the extraordinary size of the

financial crisis, but there are instances where the aid granted failed to prove its usefulness,

thus triggering the natural question whether a more careful and reluctant examination might

have been required. However, during the crisis, the European Commission has relaxed its

"first and last" principle, as stated in its guidelines on state aid to the financial sector.

According to this principle, state aid should be granted only once for a period of 10 years for

each of the beneficiaries, unless "restructuring aid follows the granting of rescue aid as part

of a single restructuring operation"28.

V.3. The moral hazard

Due to the fact that in a functional market economy any inefficient undertaking is self-

excluded from the market, rescuing a financial institution from bankruptcy might have

potential negative effects caused by the moral hazard phenomenon – i.e. the failure of the

institution concerned to assume responsibility, which means that in such a case state aid could

also be seen as negative incentive. Also, state aid to distressed banks may represent a cost-

sharing funding, both detrimental to competitors that operate without aid and to the other

Member States. Therefore, state aid failing banks can be a way of distorting competition29. In

this sense, how can the granting of state aid to financial institutions in difficulty be

nevertheless justified? Firstly, the systemic importance of banks (unlike other companies)

must be highlighted, as their bankruptcy could lead to major effects on the entire economic

system. Also, if the financial institution in question is of systemic relevance, it may generate a

negative spiral, with impact on other banks at global level (as was the case with the

bankruptcy of Lehmann Brothers, 2008).

In many cases, the problem of moral hazard is difficult to avoid. Since the failure of

major banking groups during the financial crisis was often the result of undertaking risky

28 Communication From The Commission - Community Guidelines On State Aid For Rescuing And Restructuring Firms In

Difficulty, C 244/02/2004, Brussels.

29 Europe Press Release, 4 June 2008: State aid: Commission approves restructuring of Sachsen LB- frequently asked

questions, http://europa.eu/rapid/press-release_MEMO-08-363_en.htm

87

activities or of mismanagement, experts criticise the "rewarding" of such banks by granting

them state aid. Therefore, the European Commission tried to establish penalties, requiring the

beneficiary institutions to share the financial burden, and even if such sanctions might not

entirely prevent the adoption of a risky behaviour, they still could help reduce its occurrence.

VI. Conclusions

Following the overall assessment of EU policy on state aid to the financial sector, it

may be concluded that the containment of the effects of the international crisis was the result

of a joint effort of national governments, central banks and international authorities.

Thus, at EU and national level, measures to stabilize the financial sector and support

the real economy benefited all "players" in the financial sector and the economic actors as

well. However, certain financial institutions or sectors needed a more substantial support,

which generated disparities and lack of coordination, which was completely inconsistent with

the provisions and conclusions of the Eurogroup meeting of October 12th, 200830.

In certain Member States the turmoil in the banking system was more acute and some

banks required direct support beyond the national schemes implemented. As a result, these

banks started a process of restructuring and reduced their activity according to the rules

imposed by the European Commission, while other banks were not at all affected.

Consequently, it can be seen how the financial crisis has "reshaped" the structure of the

European financial system.

In this newly created perspective, the question of how financial institutions operate on

the single market may seem rhetorical. For some financial institutions a competitive

environment has been set by the financial crisis itself. Although to a certain extent the

responsibility for the difficulties faced by the institutions of the financial system lies mainly

with the banks and the failures in their business management, in some cases the national

authorities have proven to be limited in their development of coherent financing plans and in

their ability to respond more quickly to the negative signals given by the market.

30 The conclusions have stipulated that unilateral and uncoordinated action in this area may undermine efforts to restore

financial stability.

88

References: [1]DG Competition, available on-line at: www.ec.europa.eu/competition/state_aid

[2]European Commission (2015): Scoreboard on State Aid, Brussels

[3]European Commission (2012): Facts and Figures on State Aid in the EU Member States,

Brussels

[4]European Commission (2011), Competition, The Effects of temporary State Aid Rules Adopted

in the Context of the Financial and Economic Crisis, Commission Staff Working Papers, Brussels

[5]European Banking Federation, EBA (2010), Finding the Right Balance of the New Basel

Framework, RP/EV/WW/GG, www.bis.org/publ/bcbs165/europeanbanking

[6]International Monetary Fund (IMF) Survey online: European Union Financial Sector – Europe-

Wide Approach Will Make Financial System Safer, 15.03.2013,

http://www.imf.org/external/pubs/ft/survey

[7]International Monetary Fund (IMF) (2013), European Union: Financial System Stability

Assessment, Country Report No. 13/75, Washington DC

[8]Lyons, B., Zhu, M. (2013), Compensating Competitors or Restoring Competition? EU

Regulation of State Aid for Banks During the Financial Crisis, Journal of Industry, Competition

and Trade, March 2013, Volume 13, Issue 1

[9]Meiklejohn, R. (1999), European Economy, study published by European Commission,

chapter 1 – The economics of State aid, Number 3, p. 25, Brussels

[1o]Naess-Schmidt, H. S., Harnoff, F., Hansen M. B. (2011), State Aid: Crisis Rules for the

Financial Sector and the Real Economy, D.G for Internal Policies, European Parliament, Brussels

[11]Nicolaides, P., Rusu, I. E (2010), The Financial Crisis and the State Aid, The Antitrust

Bulletin, Vol. 55, No. 4/Winter 2010, The Journal of American and Foreign Antitrust and Trade

Regulation

[12]Sutton, A., Lannoo, K., Napoli, C. (2010), Bank State Aid in the Financial Crisis.

Fragmentation or Level Playing Field?, Centre for European Policy Study, Brussels

Acknowledgements

This paper has been financially supported within the project entitled “Horizon 2020 -

Doctoral and Postdoctoral Studies: Promoting the National Interest through Excellence,

Competitiveness and Responsibility in the Field of Romanian Fundamental and Applied

Scientific Research”, contract number POSDRU/159/1.5/S/140106. This project is co-

financed by European Social Fund through Sectoral Operational Programme for Human

Resources Development 2007-2013. Investing in people!