Embed Size (px)

Citation preview

Secretarial Audit Practices –SEBI

Regulations

Vinod KothariVinod Kothari & Company

1006-1009 Krishna224 AJC Bose RoadKolkata – 700017Phone 033-22811276/ 22813742/ 22817715

403 – 406, Shreyas Chambers 175 D.N. Road, Fort, Mumbai-400 001Phone: +91 22 2261-4021/ 3044-7498

A/11, Huaz Khas (Opposite VatikaMedicare)New Delhi-110016Phone: 011- 41315340

www.vinodkothari.com/ www.india-financing.comEmail: [email protected]

Copyright

• The presentation is a property of Vinod Kothari & Company.

• No part of it can be copied, reproduced or distributed in any

manner, without explicit prior permission.

• In case of linking, please do give credit and full link

2

About Us

• Vinod Kothari & Company, Company Secretaries inPractice

▫ Based out of Kolkata, Mumbai & Delhi

• We are a team of consultants, advisors & qualifiedprofessionals having over 25 years of experience

3

Our Organization’s Credo:

Focus on capabilities; opportunities follow

Audit focus-

Board & general meeting

compliances

4

Audit Focus

• Focus to be determined on following basis:▫ Nature of Company

Listed, Unlisted, Public, Private with listed debt

▫ Shareholding pattern of the Company Promoter driven, Professionally driven, Extent of FDI, presence of PE investors with SHA

▫ Investments of the Company Subsidiaries and Associates of the Company Domestic and Overseas WOS/ JV

▫ Sector in which the Company is engaged Financial Service Sector, Manufacturing Sector, Non Financial Service Sector

▫ Sectoral laws applicable▫ Manner of raising funds

Term loans, CPs, NCDs, Sub-debt, Masala Bonds, ECB, Equity, Preference. Types of issuance undertaken for raising funds

▫ FPO, rights issue, private placement, QIP, public issue▫ Whether utilization of proceeds is being monitored by Audit Committee

5

Board Compliances

• Effectiveness of BM▫ Matters transacted, matters delegated (whether absolute delegation or

delegation with caveats), Reporting back of outcome of matters delegated.▫ Manner of recording of discussions and rationale in the minutes of Board

and Committee meeting Recording of dissents/ reservations.

▫ Nature of Committees constituted for carrying out the functions andpresence of as well as appropriateness of terms of reference

▫ Familiarization programmes for IDs and other directors – how the same isdone.

▫ Practice of discussing the action taken report at subsequent meetings.▫ Adequate details/ materials sent by way of agenda beforehand to ensure

the directors comes well read to the meetings.▫ Matters decided based on external opinion

• Checking corporate law compliances

6

General meeting compliances

• Whether mandatory items placed before shareholders?

• Whether manner of approval required under law was followed?

▫ Section 42, 180, 62 (1) (c), 188, under listing regulations etc

▫ OR/ SR, at the meeting/ postal ballot.

• Presence of chairman of NRC/ AC and SRC where applicable

• Presence of secretarial auditor, auditors etc.

• E-voting, Poll, ballot paper facility provision related compliances

• Post AGM compliances whether ensured w.r.t. dividend payment,filings etc

7

Composition of Board of directors

• Whether the Board is duly constituted▫ This refers to compliance with statutory provisions

Directors appointed as per provisions of law

Rotational/non rotational directors

Minimum number of independent directors

Woman director

▫ Proper balance of independent, non executive and executive directors This is a qualitative comment

Generally speaking, a minimum of 3 IDs is recommended

The need for executive directors is organisation-specific

Non executive, non independent directors They essentially represent shareholding blocks

Or lenders

▫ Changes during the year were compliant with the law

8

Quality of Board proceedings

• Adequacy of systems for seeking additional information by Board members

• Quality of Board minutes

▫ That dissenting members’ views are captured in the minutes

▫ Mostly Board minutes contain shallow minuting

• Board minutes

▫ These provide most relevant compliance points

▫ Board minutes indicate business/matters that require filing or furthercompliances

▫ However, Board minutes are not all

▫ There may be lots of matters which may not come to the board at all Delegated matters

Matters that escaped board attention

9

Compliance system

10

Adequacy of Compliance System

• Whether the company has an adequate compliance system?

• Whether the same commensurate with the size and operations of the

company.

• This should easily connect with the requirement of the compliance

report of CS in respect of compliance with applicable laws

• This report is placed before Board periodically

11

Elements of a compliance system- 1/2

• Identification of applicable laws to different business areas

▫ Production labour related law environment related laws

▫ Marketing intellectual property

trade mark and like laws

▫ Human resources All HR related laws, protection of women at work, etc

Sweeping statement that the HR department has complied with all HR laws is surely indicating apure self certification job

▫ Corporate Laws

▫ Fiscal laws

• Fixation of responsibility centers or “owners” of each law• Periodic reporting by the Owner of compliances or exceptions

12

Elements of a compliance system- 2/2

• Details of requirements of each of such laws

▫ Entry-point requirement for example, license, registration, etc

▫ Event-based compliances for example, approval to be taken for doing something, or some filing in

consequence of some event

▫ Regular compliances for example, periodic filings, renewal, etc.

• Corrective action on non compliances

• Reporting to the CS

• Reporting by the CS to the board

13

• Is the Board aware about compliance requirements?

• Is there is a maker-checker distinction?

•Does periodically, some outsider check compliances?

• Is the company periodically subjected to inspections by a regulator?

•Does internal audit cover compliances of some laws?

•How serious periodic compliance certificates merely rubber stamps, or do theyindicate seriousness?

•Whether any standard operating process has been formulated?

•Whether the company follows any checklist of compliances?

•What course of action is being followed for any non- compliances?

•Whether the company has a system in place to update with the newrequirements of law?

14

Quality of the compliance system

Required policies, plans, frameworks etc.

15

• Policy on material subsidiary• Related party transactions policy• Policy on determination of materiality of events• Nomination and Remuneration Policy• Succession Plan• Risk Management Plan• Board evaluation framework• Code of conduct for prohibition of insider trading• Code of fair disclosure of UPSI• Investor relation policy• Dividend distribution policy• Business Responsibility Policy• Vigil Mechanism• Archival Policy• Corporate Social Responsibility policy• Remuneration criteria for NEDs• Familiarisation programme for IDs

16

The list

Quality of policy and adherence to the

policies- 1/2

• Whether policies are mere reproduction of provisions of law or detail amechanism or process to be followed?

• Whether the policies cover certain crucial aspects? Some examples arecited hereunder:▫ Materiality policy

whether merely specifies subjective criteria or lists down objective criteria as well ( viz. 1%of turnover/ net worth or Rs. 100 crore ).

Does it adequately provide for recording of discussions basis which the authorised KMPsdecided to not disclose to stock exchange.

▫ RPT policy does it provide for transactions for which omnibus approval cannot be granted? Or

does it adequately distinguish between significant and immaterial RPTs?Contd..

17

Quality of policy and adherence to the

policies-2/2▫ Code of conduct for prohibition of insider trading

whether it provides for internal reporting mechanism by complianceofficer?

Pre-clearance limit – whether the same is determined on dual aspect –Eg. 1000 shares or value of Rs. 10 lakhs whichever is lower.

Is there a separate investor relation policy which provides for whoattends the investor meets, who addresses rumours, what is thesilent period etc.

• Whether the Company merely has a policy or an operatingguideline (which is a ready reference for the persons executing thepolicy)?

▫ This guideline may not be public domain.

18

Vigil Mechanism Policy

• Whether the policy defines what is wrongful act? To include▫ violation of law,▫ misuse or abuse of authority,▫ fraud or suspected fraud, any deliberate concealment of such abuse of

fraud,▫ infringement of Company’s rules,▫ misappropriation of funds, actual or suspected fraud,▫ substantial and specific danger to public health and safety or abuse of

authority or▫ violation of the company’s code of conduct or ethics policy

• Applicability of the Policy• Whether the mechanism for the manner of reporting, safeguards

against victimization of person who use such mechanism etc. isprovided?

• Whether the policy covers manner of disposal of a complaint?

19

Policy on Material Subsidiary

• Whether the Policy covers the process of determination of a subsidiary asmaterial?

• Whether the Policy provides for the specific compliances to be observed bythe company on having a material sub? Should include compliances relatedto▫ disposal of the shares in such sub▫ selling, disposing and leasing of assets▫ Composition of Board with 1 ID of hold co. in case of Material non-listed Indian

sub• Whether the Policy covers general compliances related to subsidiaries?

Should include compliances related to-▫ review the financial statements, in particular, the investments made by the

unlisted subsidiary company by audit committee▫ Placing of board meeting minutes of unlisted sub before the board of hold co▫ Placing of statement of all significant transactions and arrangements entered into

by the unlisted sub before the Board of hold co.

20

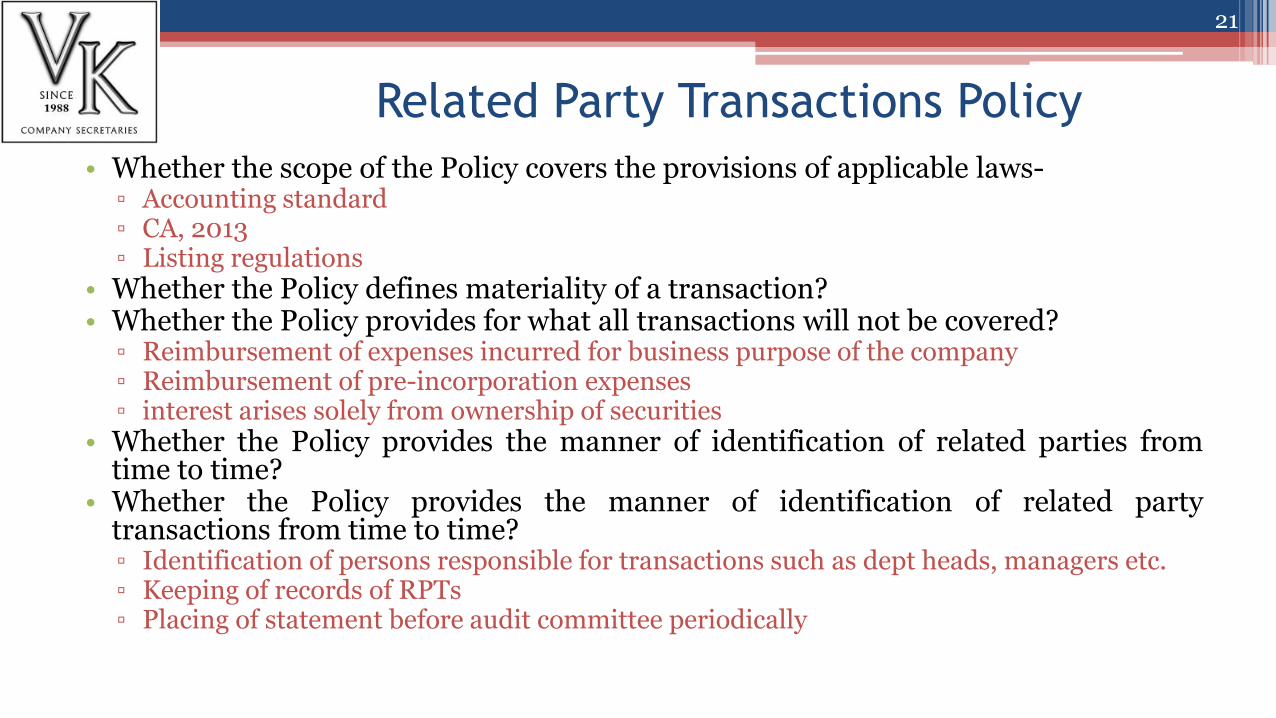

Related Party Transactions Policy

• Whether the scope of the Policy covers the provisions of applicable laws-▫ Accounting standard▫ CA, 2013▫ Listing regulations

• Whether the Policy defines materiality of a transaction?• Whether the Policy provides for what all transactions will not be covered?

▫ Reimbursement of expenses incurred for business purpose of the company▫ Reimbursement of pre-incorporation expenses▫ interest arises solely from ownership of securities

• Whether the Policy provides the manner of identification of related parties fromtime to time?

• Whether the Policy provides the manner of identification of related partytransactions from time to time?▫ Identification of persons responsible for transactions such as dept heads, managers etc.▫ Keeping of records of RPTs▫ Placing of statement before audit committee periodically

21

Related Party Transactions Policy

• Whether the Policy provides for the manner of review and approval ofthe RPTs

• Whether criteria for omnibus approval has been approved by theBoard? Whether the same has been incorporated in the Policy?

• Whether the Policy specifies the manner of approval for transactionsnot at arm’s length/ not in the ordinary course of business?

• Whether the Policy provides the concept of ordinary course ofbusiness?

• Whether the Policy covers how to determine arm’s length nature of atransaction?

• What all disclosures are required?▫ Board’s report▫ Corporate Governance Report▫ Annual affirmation to SE▫ Entry in registers

22

Nomination and Remuneration Policy

• Whether the Policy is clear on its scope?

• Whether the terms of reference of NRC is covered?

• What are the principles for selection of IDs?

• What is the overall criteria for selection of executives of thecompany?

• What are the general policies for remuneration?

23

Policy on Determination of Materiality

• Key principles of determination of materiality

• Deemed events

• Guidelines of determination of materiality

• Events based on guidelines

• Factors in arriving materiality decision

▫ Quantitative criteria may be based on

Price of shares, assets, turnover

• Guidance when an event is deemed to have occurred

• Manner of disclosure of events

• Person responsible for disclosure

• Preservation of records

24

Code of Practices and Procedures for Fair

Disclosure of UPSI• Definition of UPSI

• Person responsible for disclosure

• Functions of the Chief Investor Relations Officer

• Disclosure Policy

▫ Need to know basis

▫ Third party dealings

practices of making transcripts or records of proceedings of meetingswith analysts and other investor relations conferences on the website

• Dealing with market rumours

▫ Verification and response

25

Dividend Distribution Policy

• General policy of the company as regards dividend• Considerations relevant for decision of dividend pay-out▫ Statutory requirements▫ Agreements with lending institutions/ Debenture Trustees▫ Prudential requirements▫ Proposals for major capital expenditures etc▫ Extent of realized profits as a part of the IND AS profits of the Company▫ Expectations of major stakeholders, including small shareholders▫ Operating cash flow, net sales, return on invested capital,▫ Magnitude of earnings▫ Cost of borrowings

• External & internal factors• Circumstances under which dividend payout may or may not be

expected• Manner of utilisation of retained earnings

26

Compliances under Listing Regulations

27

In brief…

• Policy related compliances• Filing of information/ returns / publication of notice/ website related

compliances• Subsidiary related compliances▫ Key compliances under Reg. 24 covered in separate slide

• Related party transactions▫ Prior Audit Committee approval obtained?

Where subsequently ratified, was it on account of mere breach of limits grantedunder omnibus approval or delayed identification of related party?

Whether the list of related party is regularly updated.▫ IND-AS 24 preparedness in terms of identification of related parties.

Whether sufficient information is placed before AC to ascertain if the RPT is in theinterest of the company

▫ Any external agency certificate to evaluate if transactions were on arm’s length?

▫ Whether material RPT reported in quarterly CG report?▫ Whether material transactions approved by shareholders?

28

Compliances under Listing Regulations (1/2)

• Transfer of securities-

▫ Whether the company transfers securities in the name of transferee, properdocument has been lodged for transfer

▫ Whether the company has accepted registration of transfer upto book closure orrecord date?

• Date of Book Closure, for the purpose of Declaration of Dividend, issue ofrights share/bonus share or conversion of Debenture?

• Whether prior intimation of Board meeting Agenda has been made to Seswherever required?

29

• The CEO and the CFO of the company to certify the BOD that financialstatement and cash flow does not contain any material untrue or misleadingstatement and others

• Quarterly Compliance Report on Corporate Governance

• Certification on Compliance of condition of corporate governance

• Business Responsibility Statement

30

Compliances under Listing Regulations (2/2)

Compliances related to subsidiary-1/2

• Policy for determining 'material' subsidiary• Composition of Board▫ Atleast 1 ID of holding co in the material unlisted sub

• Review of financial statement by Audit committee▫ Particularly, investments made by the unlisted subsidiary

• Minutes of unlisted subsidiary▫ To be placed before Board of Hold co

• Statement of all significant transactions and arrangements of unlistedsubsidiary▫ Periodical placement before Board

• Not to dispose off shares of material subsidiary▫ resulting in reduction of its shareholding (either on its own or together with

other subsidiaries) to less than 50% without passing a special resolution▫ Not applicable for a scheme of arrangement duly approved by a Court/Tribunal.

31

Compliances related to subsidiary-2/2

• Sell, dispose, lease of assets of material sub▫ amounting to more than 20 % of its material sub on an aggregate basis during a

financial year▫ Unless prior SR▫ Not applicable for a scheme of arrangement duly approved by a Court/Tribunal.

• Disclosure to be provided in the Corporate Governance Report (forming partof Annual Report)-▫ Annual affirmations

on composition of Board of unlisted material sub and Compliance of Corporate Governance requirements with respect to subsidiary

• Disclosure of event related to subsidiary which are material for Hold Co toSE

• Disclosure of acquisition(s) (including agreement to acquire), Scheme ofArrangement (amalgamation/ merger/ demerger/restructuring), or sale ordisposal of subsidiary or any other restructuring.▫ Being deemed material event

32

Material events

• Reg 30 read with Schedule III▫ Deemed material events

No determination of materiality is required To be disclosed asap to SE First to disclosure to SE and then others

▫ Events to be material based on determination To check provisions in the Policy Whether the Policy is specific for the manner of determination

Subjective or objective criteria Whether Committee of KMPs is always responsible for determination of

materiality What factors are considered for such determination Whether any rule of thumb is provided internally for such determination To be disclosed asap to SE First to disclosure to SE and then others Minutisation of decision taken by the Committee

33

Disclosures & other compliances

under PIT Regulations

34

Checkpoints in brief

• Whether the employees are sensitized on the Code of conduct and requirement under theregulations?

• Whether the scope of employees covered under Code is very wide covering all employees?

▫ In that case, whether the company follows different practice in case of violation by adesignated employee versus an employee having no access to UPSI?

• Nature of violations under Code and action taken by Company.

• Whether an internal code of conduct governing dealing in securities has been made togovern the Designated Person?

• Mechanism adopted by Company to implement insider trading code

▫ Mobile app, software, intranet to ensure real time updation by employees as well ascompliance officer.

▫ How does information flows to compliance officer and how the same is reported byCompliance officer to chairman of Audit/ Board periodically.

35

Checkpoints in brief – grey list, analysts meet

• What is grey list?▫ Those securities (external companies) in respect of which executives

of the company may have UPSI

▫ Not only does the company bar trading on its own securities, but italso bars trading on external securities, based on likelihood of UPSIwith company’s executives

• Whether the Company maintains a grey list?▫ Is there a mechanism for the implementation of the same?

• Frequency of unscheduled meetings with analysts.▫ Whether transcripts put up on website, presentation shared with

Stock Exchange.

36

Checkpoints in brief – trading window

• Whether trading window is closed only when agenda for Board meeting isdispatched to directors and intimation of BM made to stock exchange?▫ Whether the company has the practice of differential closure of trading window (it

may be closed for a longer period for employees actually involved in a particularUPSI)

• Whether the company has prescribed a trading period known as trading window,and trading window shall be closed at the time where price sensitive information areunpublished▫ To ensure no trading in securities by the directors or designated employees during

closure of trading window• Whether the disclosures made by any person includes those relating to trading by

such person’s immediate relatives, and by any other person for whom such persontakes trading decisions?

• Whether the trading window has been closed when the compliance officerdetermined that a designated person or class of designated persons can reasonablybe expected to have possession of unpublished price sensitive information?

• Whether the disclosures made has been maintained by the company, for aminimum period of five years?

37

Checkpoints in brief – disclosure of holdings

• Whether any new promoter, key managerial personnel and director of company has furnished a disclosure of his holdings in the Company?

▫ within 7 days of appointment or becoming director/ promoter as the case may be

• Whether every promoter, employee and director of company disclosed to the company the number of securities acquired or disposed of where the value of the securities traded, individually or aggregates to a traded value in excess of Rs. 10 Lakh? ▫ within 2 trading days of such transaction

• Whether the company has notified to SEs, the particulars of such trading tothe stock exchange within two trading days of receipt of the disclosure?

▫ Whether company became aware of the transaction prior to receipt of aforesaiddisclosure?

▫ If so, whether 2 trading days is calculated from becoming aware of suchtransaction

38

Checkpoints in brief – two policies

• Whether the company has asked for the information as to the shareholding of a connected person in the company in such form and at such frequency as may be determined by the company in order to monitor compliance with these regulations?▫ May include those person to whom the company has to provide UPSI such as

management consultant ▫ Whether such person discloses as framework provided by the company?

• Whether the company has formulated and published on its official website, a code of practices and procedures for fair disclosure of unpublished price sensitive information as set out in Schedule A? ▫ Such as equality of access to information, disclosure of UPSI in need to know basis▫ Publication of transcripts of anlaysts meets, policies related to dividend etc.

• Whether the Company submitted disclosures to the listed entities where it holdsinvestment or is a promoter?

• Whether exempted acquisitions under were reported to stock exchange?

39

Checkpoints in brief- prompt disclosure

• Whether the code of practices and procedures for fair disclosure ofunpublished price sensitive information and every amendment thereto hasbeen promptly intimated to the stock exchanges where the securitiesare listed?

• Whether the board of directors has formulated a code of conduct adoptingthe minimum standards asset out in Schedule B ?

• Whether the Company has appointed a compliance officer to administer thecode of conduct and other requirements under these regulations. ?

40

Checkpoints in brief- reporting requirements

• Whether the Company has Designated a senior officer as a chief investor relationsofficer to deal with dissemination of information and disclosure of unpublished pricesensitive information?

• Whether the Board has stipulated any frequency of reporting by the compliance officer?• Whether the board of directors in consultation with the compliance officer specified the

designated persons to be covered by such code on the basis of their role and functionin the organisation?

• Roles and responsibilities of compliance officer▫ To set forth preservation and pre-clearance of designated employee and their

dependent trade and implementation of code of conduct▫ Maintenance of record of designated employee and changes thereunder

• Whether the compliance officer reported to the board of directors and in particular andprovided reports to the Chairman of the Audit Committee, if any, or to the Chairman ofthe board of directors at such frequency as may be stipulated by the board of directors?

• Whether the Compliance Officer has put in place appropriate procedure for Pre-Clearance of trade?

• Whether the compliance officer has confidentially maintained a list of such securities asa “restricted list” which shall be used as the basis for approving or rejectingapplications for preclearance of trades?

Whether the code of conduct contained norms for appropriate Chinese Walls

41

Checkpoints in brief- pre-clearance of trade

• Whether prior to approving any trades, the compliance officertakes declarations to the effect that the applicant for pre-clearance is not in possession of any unpublished price sensitiveinformation?

• Whether the code of conduct specified any reasonable timeframe,which in any event shall not be more than seven tradingdays, within which trades that have been pre-cleared have to beexecuted by the designated person, failing which fresh pre-clearance would be needed for the trades to be executed?

42

Checkpoints in brief- contra trade, violations

etc.• Whether the Designated persons have entered into any contra

trade as per the specified period as mentioned in the Code ofConduct which shall not be less not six months from the date oftrade in securities of the Company?

• Whether the code of conduct stipulated the sanctions anddisciplinary actions, including wage freeze, suspension etc., thatmay be imposed, by the persons required to formulate a code ofconduct for the contravention of the code of conduct?

• Whether any action has been initiated by SEBI against thecompany or any other of its promoter, director KMP, officer oremployee under PIT, regulation in present or past?

43

Contra Trade-1/3

• In case an employee or a director enters into Future & Option contractof Near/Mid/Far month contract, on expiry will it tantamount tocontra trade?

• If the scrip of the company is part of any Index, does the exposure tothat index of the employee or director also needs to be reported?

▫ Any derivative contract that is cash settled on expiry shall be considered tobe a contra trade.

▫ Trading in index futures or such other derivatives where the scrip is part ofsuch derivatives, need not be reported.

44

Contra Trade-2/3

• Whether contra trade is allowed within the duration of the trading plan?

▫ Any trading opted by a person under Trading Plan can be done only to the extentand in the manner disclosed in the plan, save and except for pledging of securities.

• Whether the restriction on execution of contra trade in securities isapplicable in case of buy back offers, open offers, rights issues, FPOs etc. bylisted companies?

▫ Buy back offers, open offers, rights issues, FPOs, bonus, etc. of a listed companyare available to designated persons also.

▫ Hence, restriction of ‘contra-trade’ shall not apply in respect of such matters.

45

Contra Trade-3/3

• Whether restriction on execution of contra trade is applicable only todesignated persons of a listed company or whether it would also apply to thedesignated employees of market intermediaries and other persons who arerequired to handle UPSI in the course of business operations?

▫ The code prescribed by the Regulations is same for

listed companies,

market intermediaries

and other persons who are required to handle UPSI in the course of business operations.

▫ Therefore, restrictions with regard to contra trade forming part of clause 10 ofcode of conduct shall apply to all according to the Regulations.

46

Pledge-1/2

• Whether SEBI's intent is to prohibit creation of pledge or invocation ofpledge for enforcement of security while in possession of UPSI?

• Whether creation of pledge or invocation of pledge is allowed whentrading window is closed?

▫ Yes.

▫ However, the pledgor or pledgee may demonstrate that the creation ofpledge or invocation of pledge was bona fide and prove their innocenceunder proviso to sub-regulation (1) of regulation 4 of the Regulations.

47

Pledge-2/2

• What should be the value of the pledge / revoke transaction for the purpose ofdisclosure?

• Is it the market value on date of the pledge / revoke transaction or is it the value atwhich the transaction has been carried out between the pledgor and pledgee?

• For instance, if the pledgor has availed a loan of Rs 10 Lacs against which he haspledged shares worth Rs 15 Lacs, would the transaction value be Rs 10 Lacs or Rs15 Lacs?

▫ For the purpose of calculation of threshold for disclosures relating to pledge underChapter III of the Regulations, the market value on the date of pledge/revoketransaction should be considered.

▫ In the above illustration, the value of transaction would be considered as 15 lakh rupees.

48

Miscellaneous- 1/2

• Who will be the approving authority for trades done by the Compliance Officer or hisimmediate relatives, as Insiders?

▫ The board of directors of the company shall be the approving authority in such cases and maystipulate such procedures as are deemed necessary to ensure compliance with these regulations.

• Whether separate code of conduct can be adopted for listed company and each ofintermediaries in a group?

▫ In case of a group, separate code may be adopted for listed company and each of intermediaries,as applicable to the concerned entity

• If a spouse is financially independent and does not consult an insider while taking tradingdecisions, is that spouse exempted from the definition of ‘immediate relative’?

▫ A spouse is presumed to be an ‘immediate relative’, unless rebutted so

49

Takeover Code

50

Checkpoints in brief

• Whether there were acquisition of shares in the company exceeding 25% ofthe paid up capital of the company ?

• Whether shareholder holding 25% of the paid up capital of the company hasacquired 5% or more share or voting rights in financial year?

• Whether any acquiree acquired shares or voting rights aggregating 5% ormore shares of the company?

• Whether share holder holding 5% or more shares in the company has anychanges in the shareholder holding 2% of total share holding ?

• Whether the promoter of the company along with PAC disclose their shareholding to the company

• Whether the promoter of the company disclose shares encumbered by him orby PAC

• Whether the promoter of the company to disclose invocation of sharesencumbered or release of pledge

51