Embed Size (px)

Citation preview

Risk-Based Supervision:

Offsite Monitoring

21st MAS Banking Supervisors

Training Programme

8 Dec 2015

Lam Yen Chiew

Banking Department III

Monetary Authority of Singapore Slide 2 of 50

Risk-Based Supervision

Monetary Authority of Singapore Slide 3 of 50

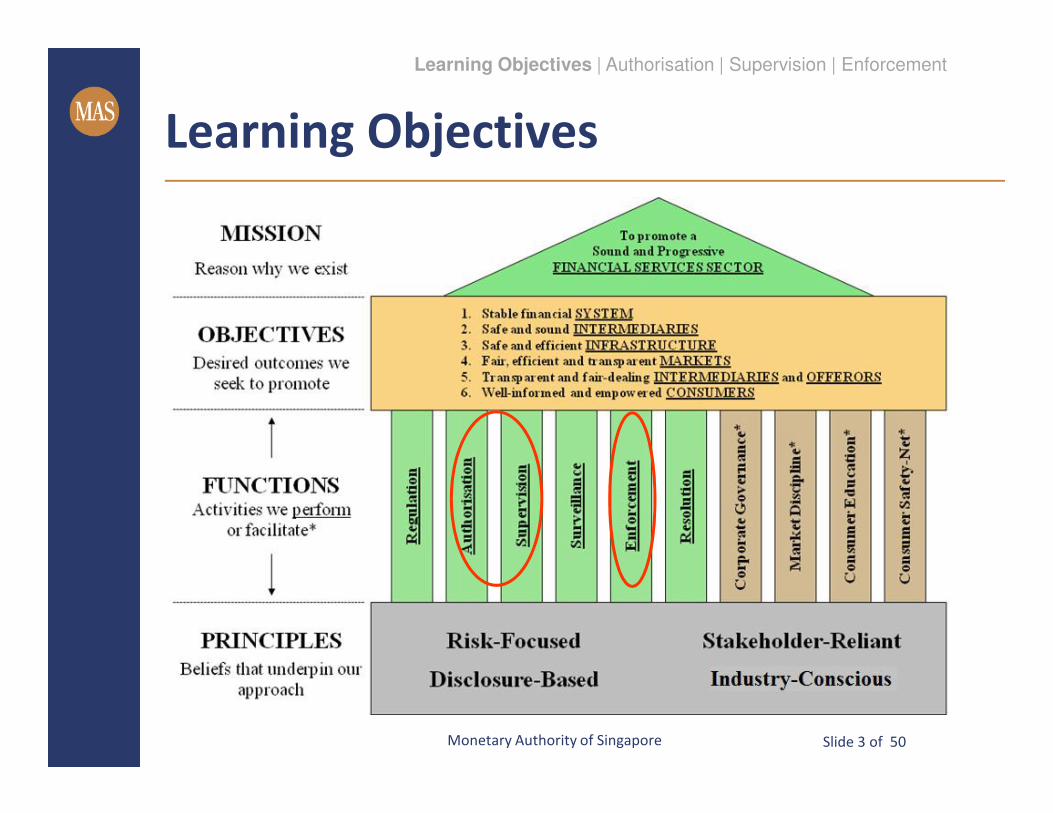

Learning Objectives

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 4 of 50

� Authorisation1. Use of the word “Bank”

2. Admission Criteria

3. Case Study: Bank of Credit and Commerce

International (BCCI)

Learning Objectives

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 5 of 50

� Supervision1. Monitoring and Intervention Indicators

2. Appointment of External Auditors

3. Engagements with Home Supervisor

4. Engagements with Bank Management

Learning Objectives

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 6 of 50

� Enforcement1. Types of enforcement actions

2. Interactions with other agencies

3. Examples of enforcement actions

Learning Objectives

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 7 of 50

Maintain Systemic Stability

Protect Depositor Interests

Safeguard Singapore’s Reputation as a Sound

Financial Centre

Authorisation

Authorisation is our first line of defense

against problem banks

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 8 of 50

� MAS is the “gatekeeper” for institutions

that wish to offer financial services in

Singapore

� Authorisation function performed by

offsite supervisory team

Authorisation

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 9 of 50

� Use of the Word “Bank”:

Section 5

1. Cord Blood Bank

2. Riverbank Restaurant

3. Food Bank

Authorisation

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 10 of 50

� Licencing criteria

1. Financial Strength, Track Record and Reputation

2. Home Country Supervision

3. Business Strategy/Plans

4. Risk Management

Authorisation

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 11 of 50

� Assessment Process:

1. Verify the information

2. Seek Home Supervisor’s comments/confirmation

3. Conduct checks with other Supervisors

4. Obtain inputs from FDD on developmental benefits

to Singapore

5. Seek Management approval

Authorisation

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 12 of 50

� The following outcomes are possible:1. Approve

2. Approve with conditions

3. Defer

4. Reject

Authorisation

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 13 of 50

� Bank of Credit and Commerce

International (BCCI)1. Applied offshore branch license in 1973

2. Resubmitted application in 1980 and 1982

3. Rejected in 1983

Case Study: BCCI

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 14 of 50

The Bank of Credit and Commerce

International (BCCI) was an international

bank founded in 1972. The Bank was

registered in Luxembourg with head offices

in Karachi and London. A decade after

opening, BCCI had over 400 branches in 78

countries, and assets in excess of

US$20 billion, making it the 7th largest

private bank in the world.

Case Study: BCCI

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 15 of 50

BCCI came under the scrutiny of numerous

financial regulators and intelligence agencies

in the 1980s due to concerns that it was

poorly regulated. Subsequent investigations

revealed that it was involved in massive

money laundering and other financial

crimes, and illegally gained the controlling

interest in a major American bank.

Case Study: BCCI

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 16 of 50

BCCI became the focus of a massive

regulatory battle in 1991, and, on 5 July of

that year, customs and bank regulators in

seven countries raided and locked down

records of its branch offices.

Case Study: BCCI

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 17 of 50

Investigators in the US and the UK revealed

that BCCI had been "set up deliberately to

avoid centralized regulatory review, and

operated extensively in bank secrecy

jurisdictions. Its affairs were extraordinarily

complex. Its officers were sophisticated

international bankers whose apparent

objective was to keep their affairs secret, to

commit fraud on a massive scale, and to

avoid detection."

Case Study: BCCI

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 18 of 50

� MAS is responsible for the prudential

supervision of financial institutions

� Supervisory tools:1. Onsite inspection

2. Offsite monitoring

Supervision

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 19 of 50

Offsite Monitoring

Off-Site Assessments

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 20 of 50

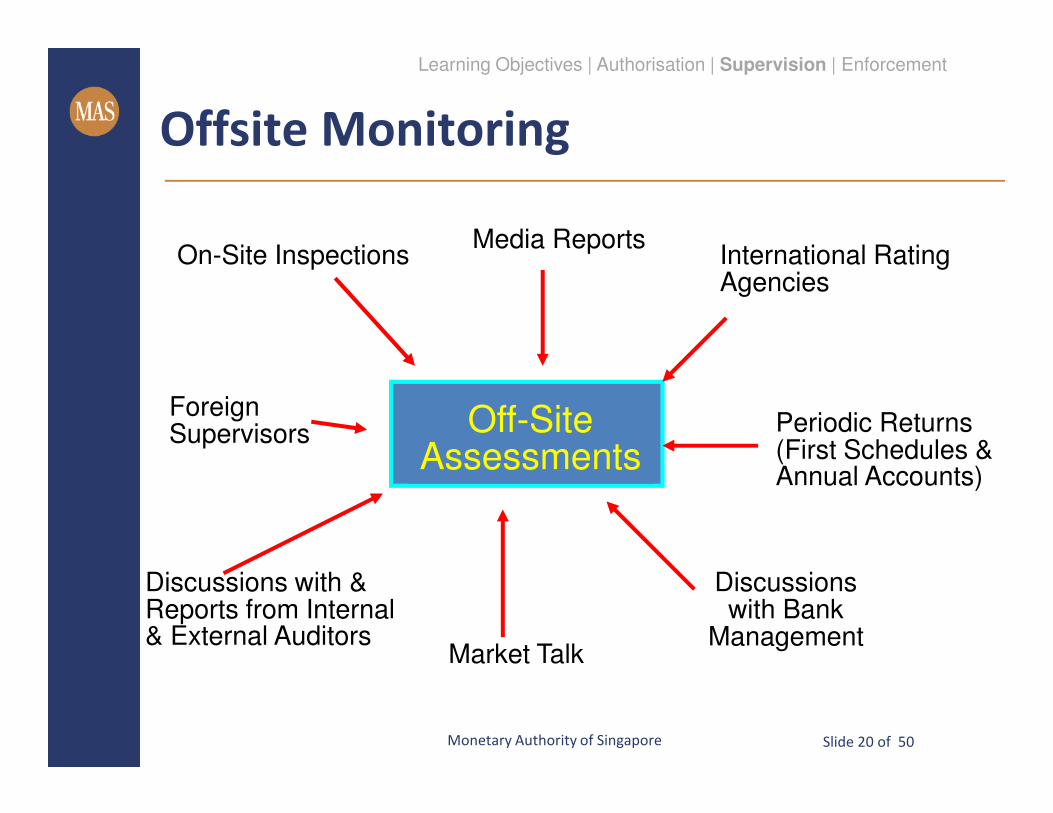

Offsite Monitoring

Off-Site Assessments

Foreign Supervisors

Market Talk

Discussions with & Reports from Internal & External Auditors

Periodic Returns (First Schedules & Annual Accounts)

International Rating Agencies

Media ReportsOn-Site Inspections

Discussions with Bank

Management

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 21 of 50

Offsite Monitoring

� Monitoring and Intervention Indicators

� Appointment of External Auditors

� Engagement with Home Supervisor

� Engagement with Bank Management

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 22 of 50

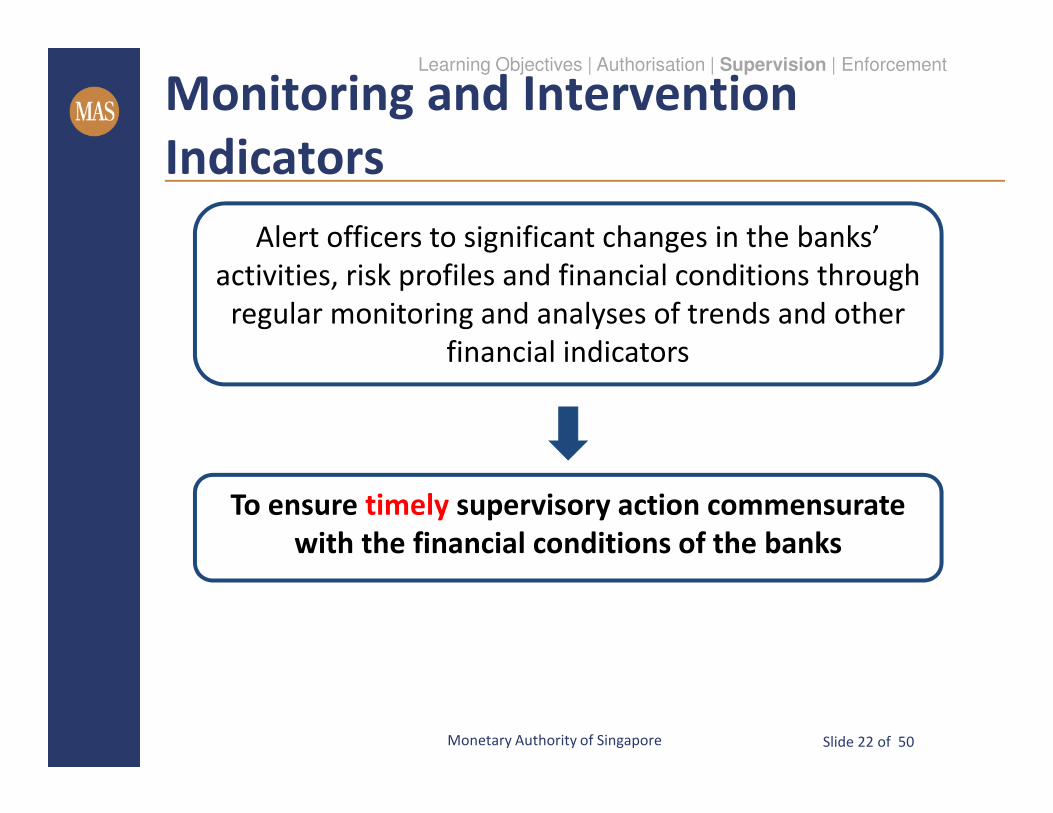

Monitoring and Intervention

Indicators

Alert officers to significant changes in the banks’

activities, risk profiles and financial conditions through

regular monitoring and analyses of trends and other

financial indicators

To ensure timely supervisory action commensurate

with the financial conditions of the banks

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 23 of 50

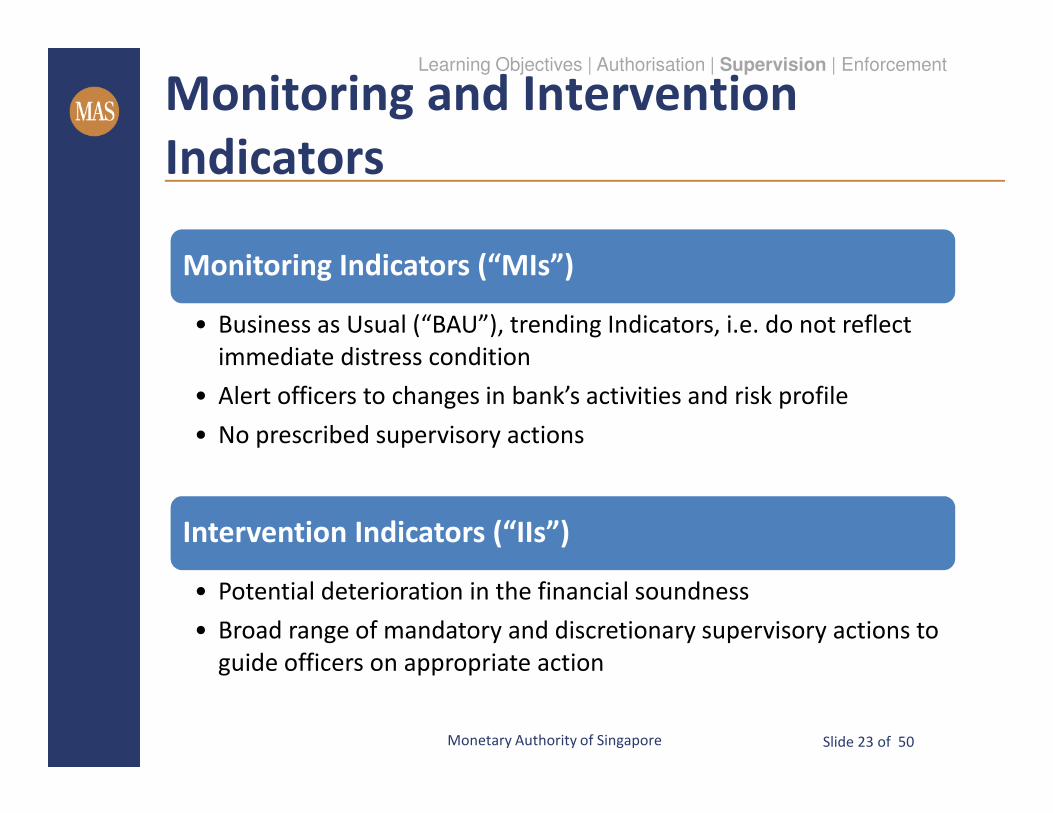

Monitoring and Intervention

Indicators

Monitoring Indicators (“MIs”)

• Business as Usual (“BAU”), trending Indicators, i.e. do not reflect

immediate distress condition

• Alert officers to changes in bank’s activities and risk profile

• No prescribed supervisory actions

Intervention Indicators (“IIs”)

• Potential deterioration in the financial soundness

• Broad range of mandatory and discretionary supervisory actions to

guide officers on appropriate action

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 24 of 50

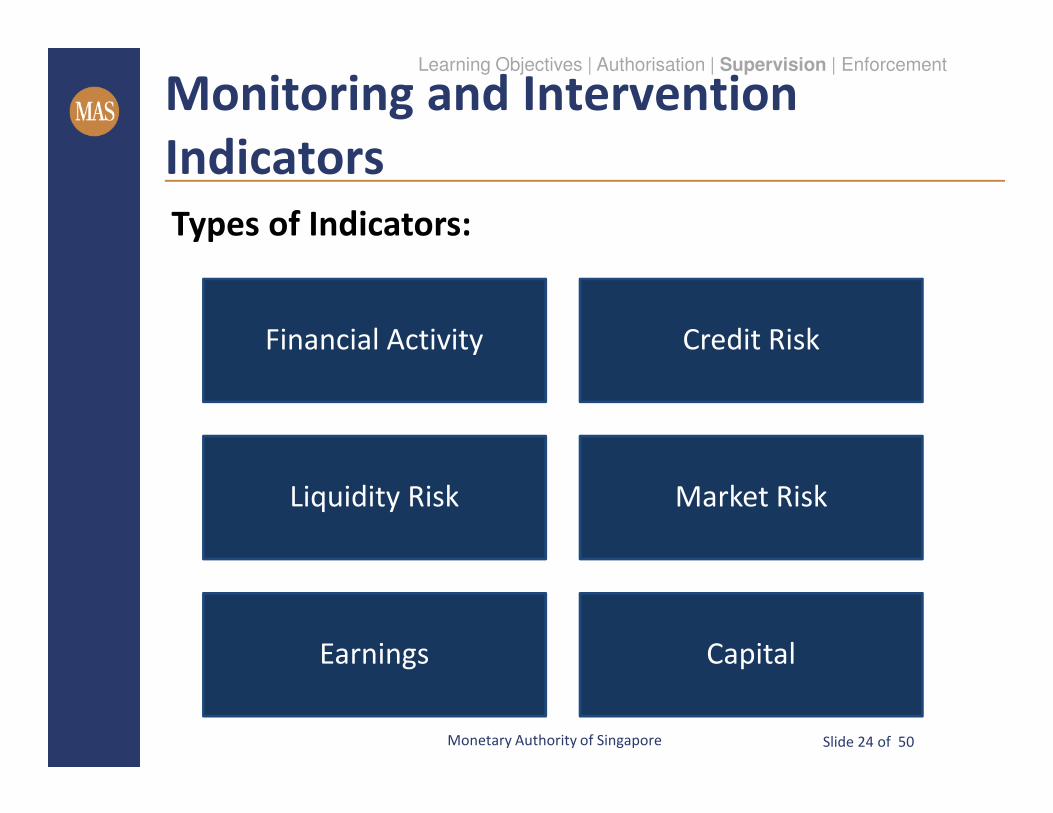

Monitoring and Intervention

Indicators

Financial Activity Credit Risk

Liquidity Risk Market Risk

Earnings Capital

Types of Indicators:

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 25 of 50

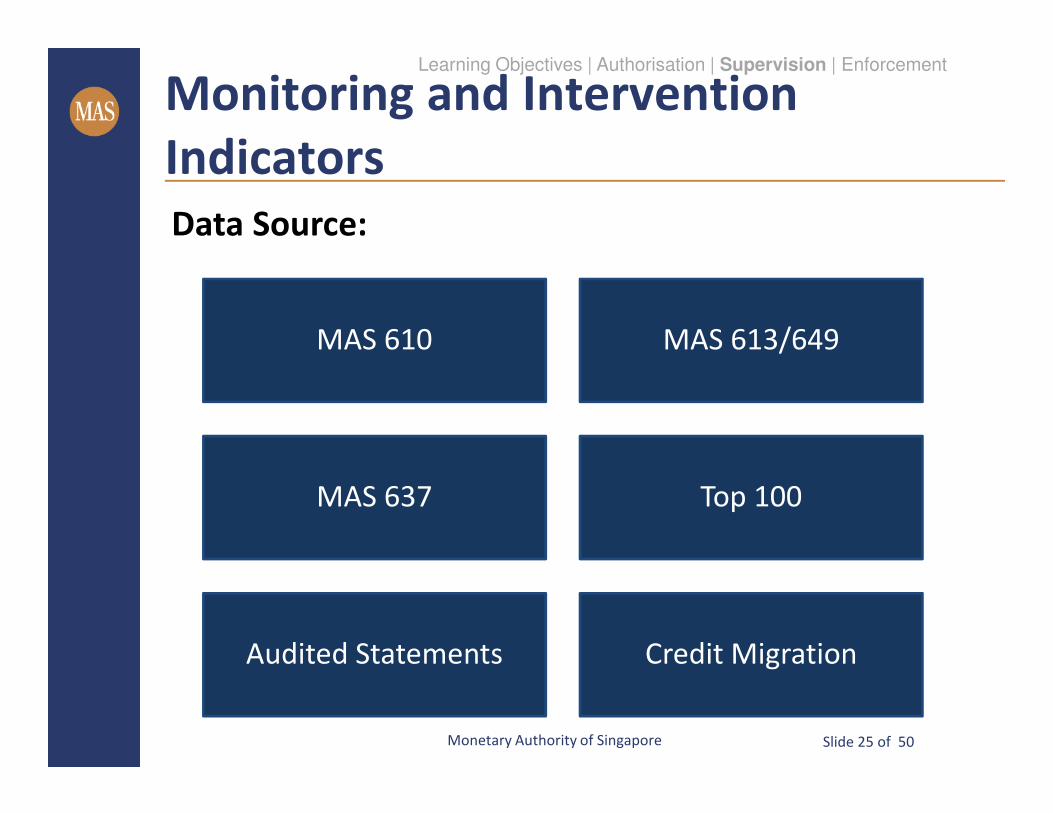

Monitoring and Intervention

Indicators

MAS 610 MAS 613/649

MAS 637 Top 100

Audited Statements Credit Migration

Data Source:

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 26 of 50

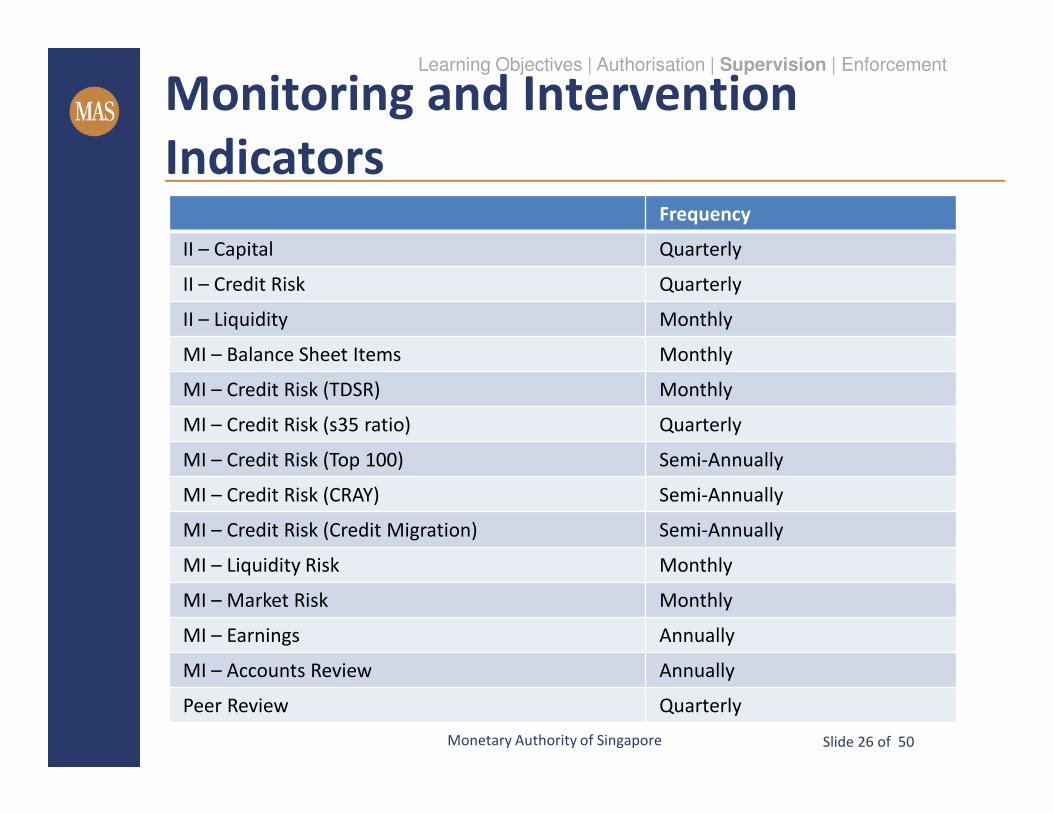

Frequency

II – Capital Quarterly

II – Credit Risk Quarterly

II – Liquidity Monthly

MI – Balance Sheet Items Monthly

MI – Credit Risk (TDSR) Monthly

MI – Credit Risk (s35 ratio) Quarterly

MI – Credit Risk (Top 100) Semi-Annually

MI – Credit Risk (CRAY) Semi-Annually

MI – Credit Risk (Credit Migration) Semi-Annually

MI – Liquidity Risk Monthly

MI – Market Risk Monthly

MI – Earnings Annually

MI – Accounts Review Annually

Peer Review Quarterly

Monitoring and Intervention

Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 27 of 50

� Intervention Indicators (“IIs”) are critical

indicators to alert us of potential

deterioration in bank’s financial soundness1. Capital (Solvency Risk)

2. Credit Risk

3. Liquidity Risk

Intervention Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 28 of 50

� Prescribed triggers serve as guide to- Investigate reasons for threshold breaches

- Take into account reasons and extent of severity of

breaches

- Consider corresponding mandatory and discretionary

supervisory actions to be taken

Intervention Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 29 of 50

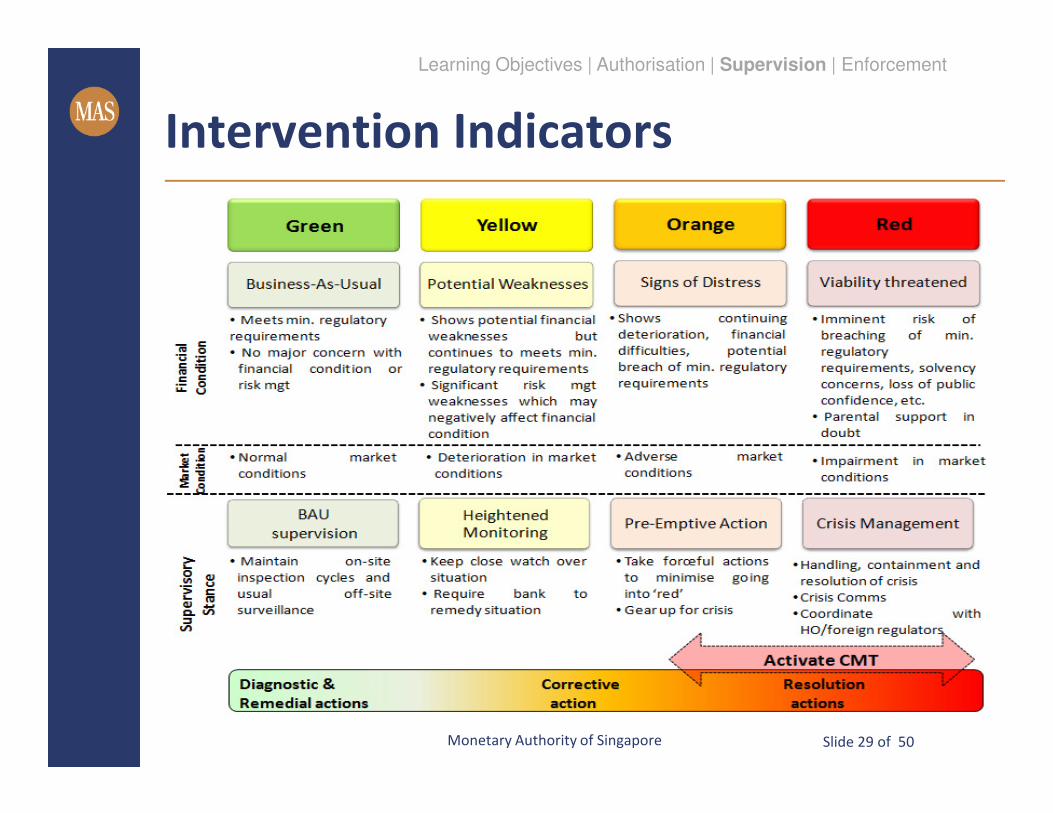

Intervention Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 30 of 50

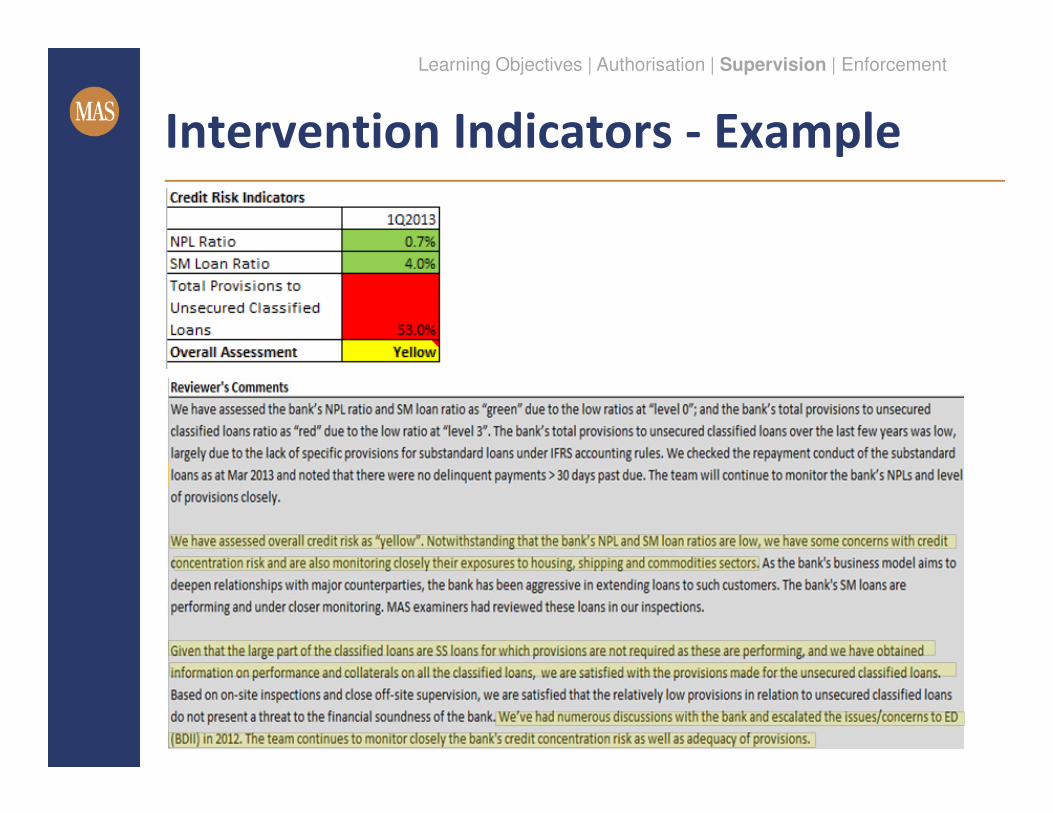

Intervention Indicators - Example

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 31 of 50

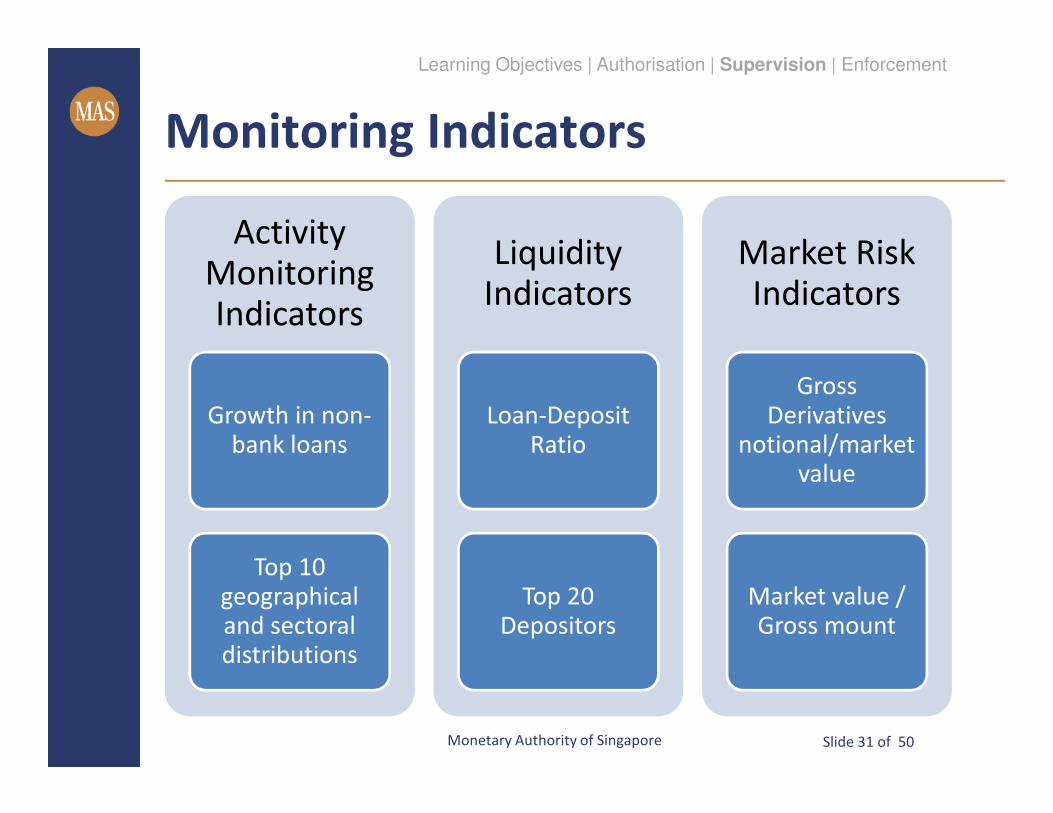

Activity Monitoring Indicators

Growth in non-bank loans

Top 10 geographical and sectoraldistributions

Liquidity Indicators

Loan-Deposit Ratio

Top 20 Depositors

Market Risk Indicators

Gross Derivatives

notional/market value

Market value / Gross mount

Monitoring Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 32 of 50

� Triggers are calibrated to serve as a guide

� Go beyond explaining the cause of

variance and assess whether there are any

concerns

� Assess the changes against understanding

of bank’s business activities and risk profile

� Follow up with the bank, where necessary

Monitoring Indicators

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 33 of 50

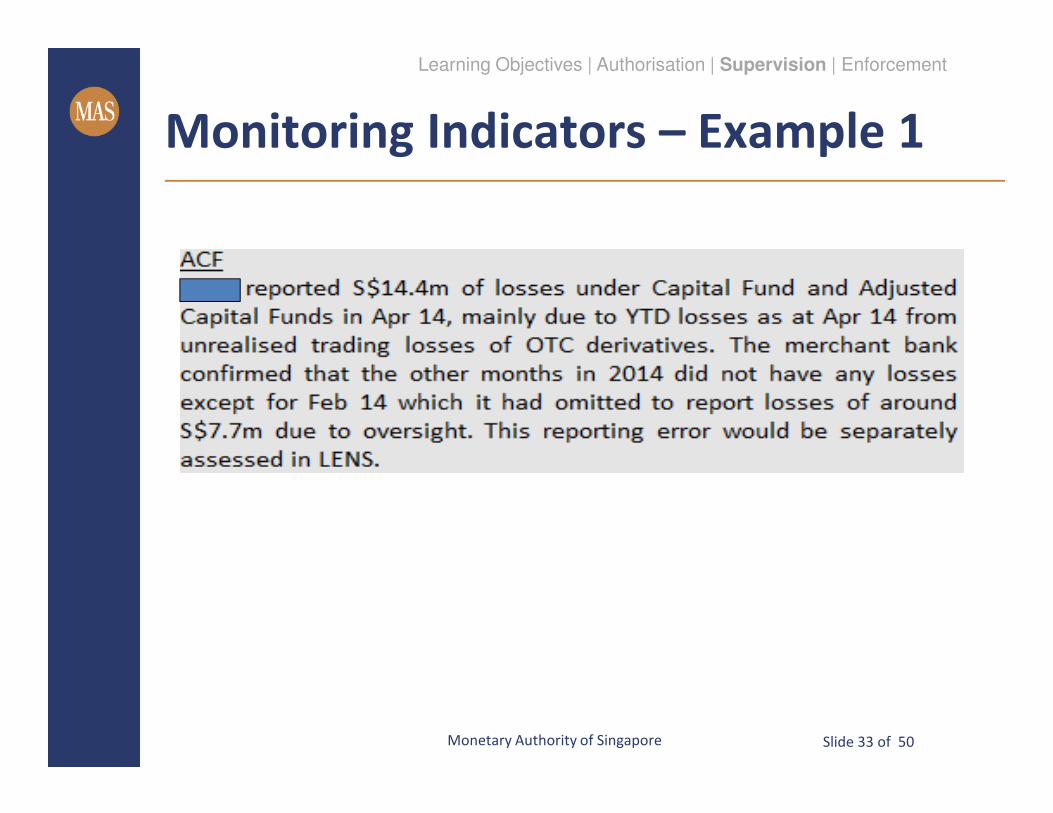

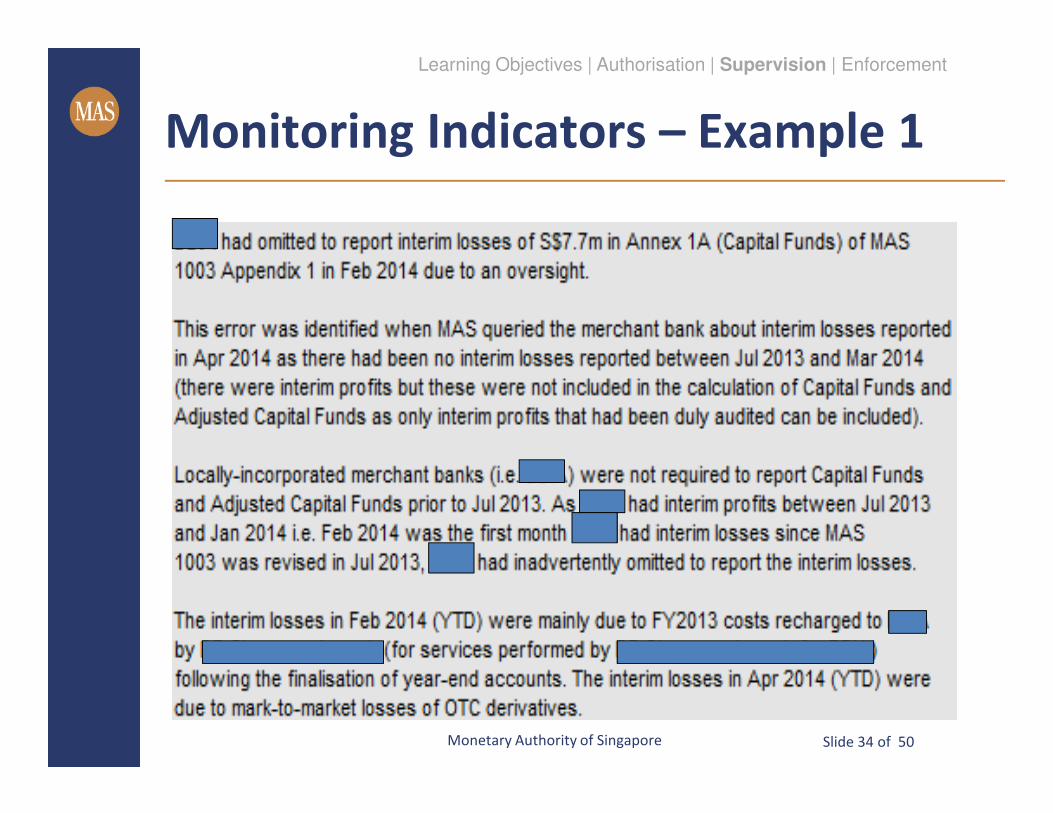

Monitoring Indicators – Example 1

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 34 of 50

Monitoring Indicators – Example 1

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 35 of 50

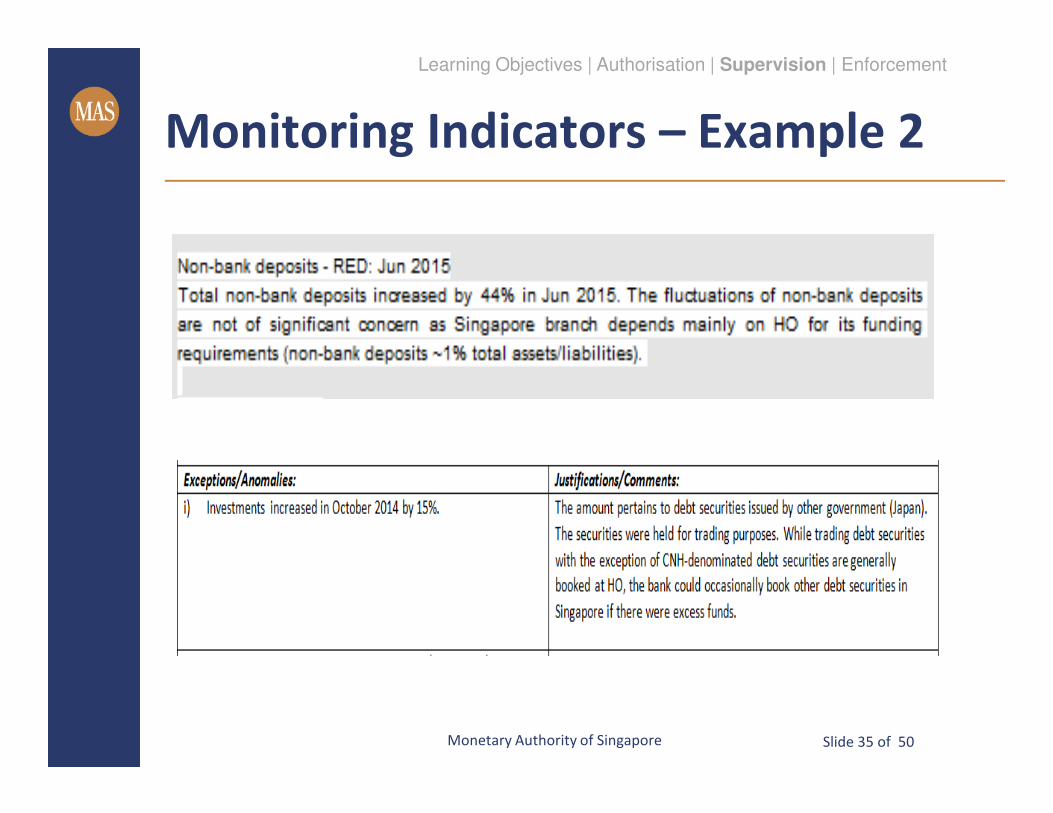

Monitoring Indicators – Example 2

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 36 of 50

� In addition to review of individual bank’s

indicators, peer review is performed to

identify whether the bank is an outlier

� Peer Group Criteria1. Similar business activities and risk profiles

2. Geographical Region or Country

Peer Review

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 37 of 50

� MI reports of 2 banks with distinct

business activities

� Identify the nature of banking activities for

each bank

� Identify the funding profile of the bank

� Identify significant changes/trends and

consider possible explanations/concerns

Monitoring Indicators - Exercise

Monetary Authority of Singapore Slide 38 of 50

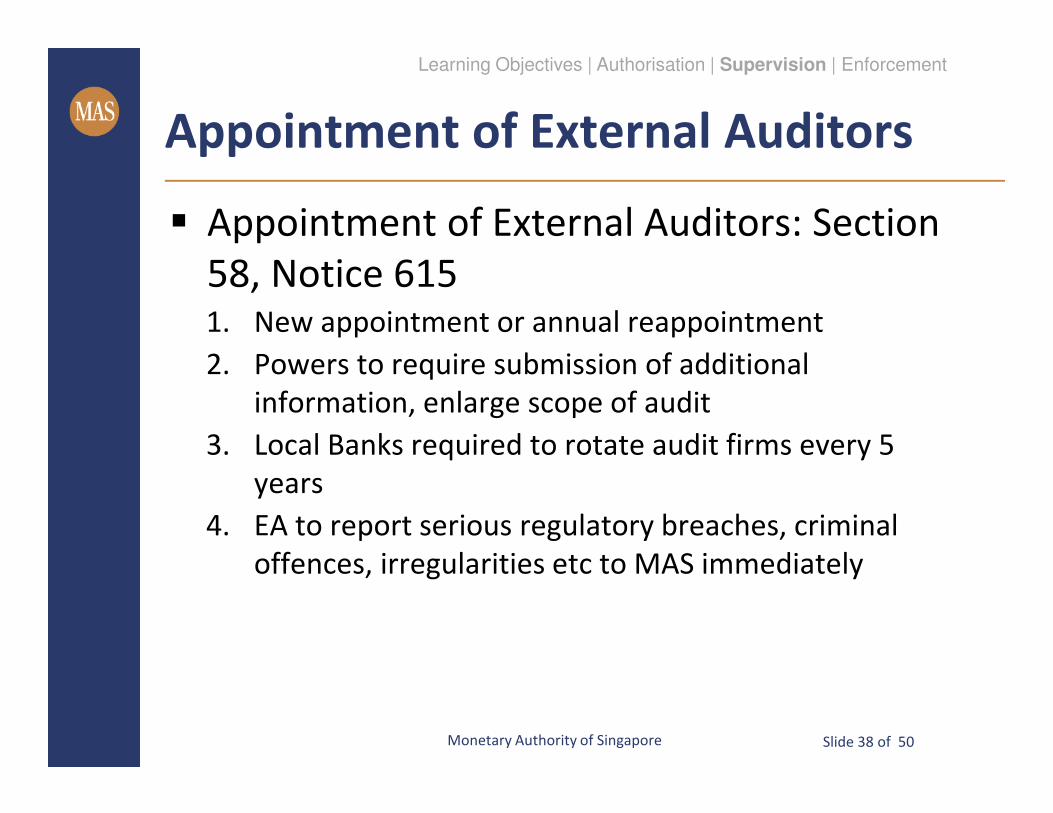

Appointment of External Auditors

� Appointment of External Auditors: Section

58, Notice 6151. New appointment or annual reappointment

2. Powers to require submission of additional

information, enlarge scope of audit

3. Local Banks required to rotate audit firms every 5

years

4. EA to report serious regulatory breaches, criminal

offences, irregularities etc to MAS immediately

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 39 of 50

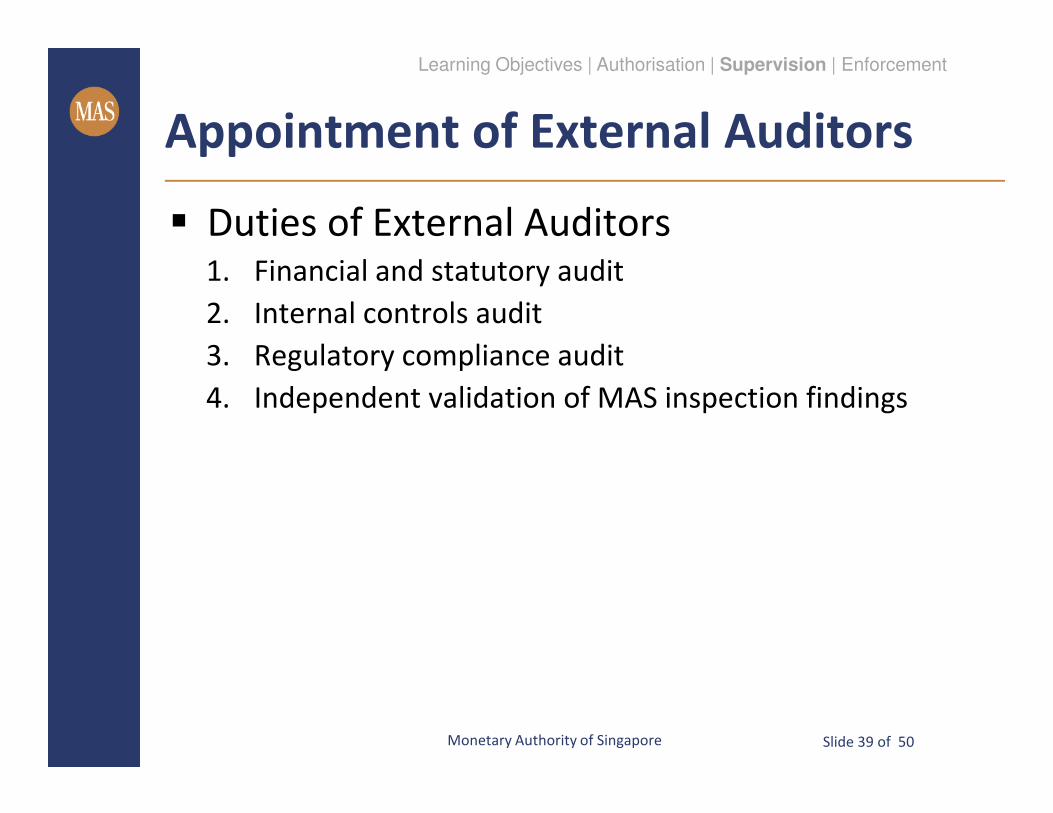

Appointment of External Auditors

� Duties of External Auditors1. Financial and statutory audit

2. Internal controls audit

3. Regulatory compliance audit

4. Independent validation of MAS inspection findings

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 40 of 50

Appointment of External Auditors

� Factors for consideration1.

2.

3.

4.

5.

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 41 of 50

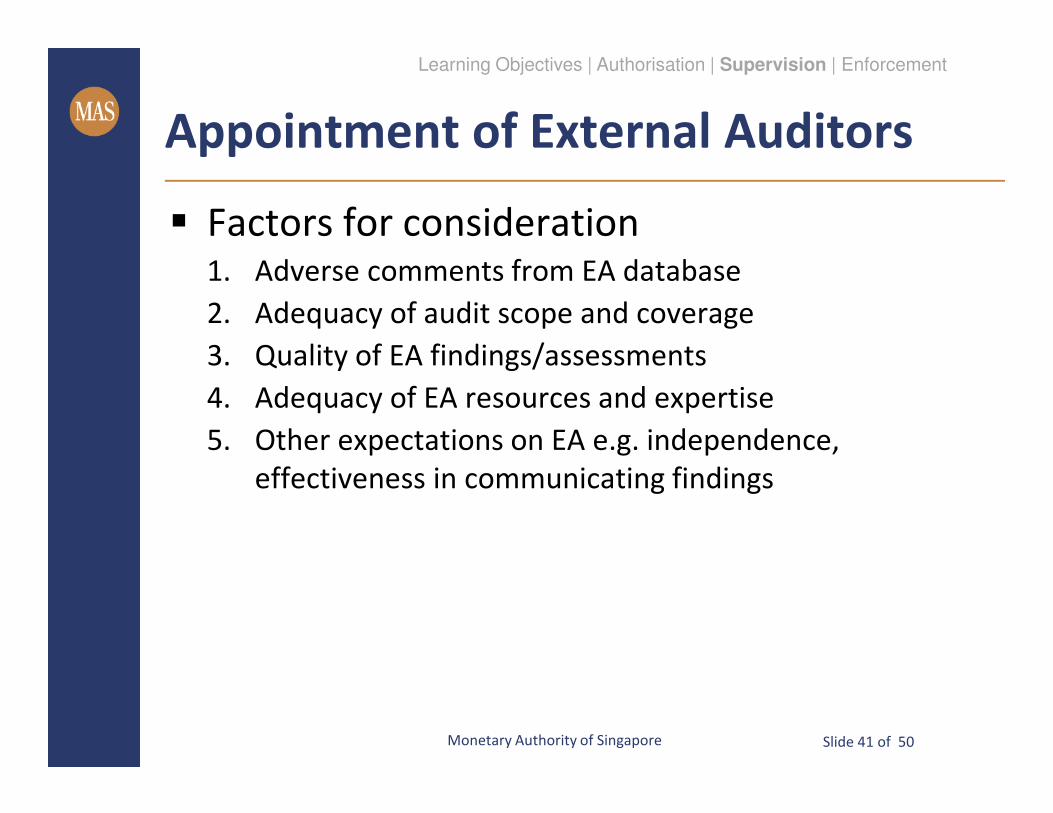

Appointment of External Auditors

� Factors for consideration1. Adverse comments from EA database

2. Adequacy of audit scope and coverage

3. Quality of EA findings/assessments

4. Adequacy of EA resources and expertise

5. Other expectations on EA e.g. independence,

effectiveness in communicating findings

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 42 of 50

Engagement with External Auditors

� Regular communication with external

auditors1. After the issuance of annual financial statements

2. Approval of (re)appointment

3. Pre-inspection

4. CRAFT assessment

5. Industry-level

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 43 of 50

Engagement with Home Supervisor

� Maintain regular communication

� Participation in supervisory colleges

� Home Supervisor can conduct inspection

of Singapore office

� Sharing of information with Home

Supervisor e.g. MAS inspection reports

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 44 of 50

� Business updates/developments

� CRAFT Disclosure

� Visits by Head Office management staff

� Head Office Internal Auditors

Engagement with Bank

Management

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 45 of 50

Enforcement

� MAS is empowered to take action against

those institutions and individuals who

breach prudential and market conduct

requirements.

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 46 of 50

Enforcement Actions

� Warning or reprimand letters

� Penalties, fines, additional capital requirements

� Removal of senior executives

� Impose ring-fencing measures / restrict activities

� Revocation of licence

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 47 of 50

Interactions with other Agencies

� Attorney-General’s Chambers

� Commercial Affairs Department

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 48 of 50

Enforcement - Examples

� Theft of bank statements belonging to

some Private Banking clients of Bank A

� MAS’ supervisory actions against banks in

relation to benchmark submissions

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 49 of 50

Enforcement - Examples

� MAS takes supervisory action against

Bank B for breakdown of the bank’s

mainframe-storage area network

� MAS reprimands Bank C for failure of its

online and branch banking systems

Learning Objectives | Authorisation | Supervision | Enforcement

Monetary Authority of Singapore Slide 50 of 50

Thank You