Embed Size (px)

Citation preview

NB

ER

WO

RK

[NG

PA

PE}

SER

IES

RA

TIO

NA

L

SPE

aJL

TIV

E 3

JBB

LE

S IN

AN

E0(

CH

NG

E R

AT

E T

A3E

T Z

ON

E

Wif

lem

H.

Bei

ter

Paol

o A. Pesenti

Wor

kim

Paper No. 3467

NA

TIO

NA

L

JRE

PU O

F E

OJN

CM

IC R

ESE

AR

UI

1050

Mas

sach

uset

ts A

venu

e C

ambr

idge

, NA

02

138

Oct

ober

199

0

We

wou

ld l

Bce

to

than

k T

orst

en P

erss

on,

thri

stoç

tier

Sim

s,

the

part

icip

ants

at

the

War

wic

k Su

mse

r Res

earc

h W

orks

hop

on 'E

xcha

re R

ates

ax

Fina

ncia

l M

arke

ts",

Jul

y 9-

27,

1990

, in

par

ticul

ar P

enzo

Ave

sani

, G

iuse

ppe

Ber

tola

, A

rdy

Cap

lin,

Ber

nard

tmas

, M

arcu

s M

iller

, R

ick

van

der

Ploe

g,

Paul

Wel

ler

ani t

he p

artic

ipan

ts a

t the

Inte

rnat

iona

l Fi

nanc

e W

orks

hop

at Y

ale,

in

pa

rtic

ular

Gia

ncar

lo C

orse

tti, V

ittor

io G

rilli

, E

cidi

i Ham

ada

and

Nou

rie]

. R

oubi

ni.

Paol

o Pe

sent

i w

ould

lik

e to

ack

elge

fina

ncia

l su

ppor

t fr

om t

he

Mat

e pe

r gl

i St

udi

Mon

etar

i, B

anca

ri e

Fin

anzi

ari

L.

Ein

audi

, Rom

e.

Thi

s pa

per

is p

art o

f N

BE

R' s

res

earc

h pr

cgra

m i

n In

tern

atio

nal

Stis

lies.

ny

op

inio

ns e

ress

i are

thos

e of

the

auth

ors

and

not

thos

e of

the

Nat

iona

l B

erea

u of

Eco

nom

ic R

esea

rch.

NB

ER

Wor

king

Pa

per

#346

7 O

ctob

er 1

990

RA

TIO

NA

L S

PEJI

AT

IVE

JB

BL

ES

IN A

N E

XQ

1PN

GE

R

AT

E T

AJE

I Z

ON

E

The

rec

ent

theo

ry o

f ex

chan

ge

rate

dyn

amic

s w

ithin

a t

arge

t zon

e ho

lds

that

exc

iiari

je r

ates

und

er a

cur

renc

y ba

rd a

re l

ess

resp

ansi

ve to

furd

asen

tal

shoc

ks t

han

exch

ange

rate

s un

der

a fr

ee f

loat

, pr

ovid

ed t

hat

the

inte

rven

tion

rule

s of

the

Cen

tral

Ban

k(s)

are

cat

uwn

kncM

ledg

e.

The

se r

esul

ts a

re d

eriv

ed

afte

r hav

ing

assu

med

a p

rior

i th

at e

xces

s vo

latil

ity du

e to

ratio

nal b

ubbl

es

does

not

occ

ur in

the

for

eign

exc

hang

e m

arke

t. In

this

pape

r we

cons

ider

inst

ead

a se

tup

in w

hich

the

exis

tenc

e of

spe

cula

tive

beha

vior

is a

dat

um t

he

Cen

tral

Ban

k ha

s to

dea

l w

ith.

We

show

tha

t th

e de

fens

e of

the

targ

et z

one

in t

he p

rese

nce

of b

ubbl

es i

s vi

able

if

the

Cen

tral

Ban

k ac

com

imxl

ates

spec

ulat

ive

atta

cks w

hen

the

latte

r ar

e co

nsis

tent

with

the

sur

viva

l of

the

targ

et z

one

itsel

f an

d ex

pect

atio

ns a

re s

elf-

fulf

illir

. T

hese

reB

ults

hol

d

for

a la

rge

clas

s of

exn

geno

us a

nd f

unda

men

tal-

depe

nden

t bub

ble

proc

esse

s.

We

show

tha

t th

e in

stan

tane

ous v

olat

ility

of

exch

ange

ra

tes

with

in a

bar

d is

no

t ne

cess

arily

les

s th

an th

e vo

latil

ity un

der f

ree

floa

t an

d an

alyz

e th

e

ixpl

icat

ions

for

inte

rest

rat

e di

ffer

entia

l dy

nam

ics.

Will

em F

l. B

aite

r Pa

olo

A.

Pese

nti

Ipar

toen

t of

Eco

nom

ics

Cep

arbn

ent o

f E

cono

mic

s Y

ale

Uni

vers

ity

Yal

e U

nive

rsity

19

72 Y

ale

Stat

ion

1972

Yal

e St

atio

n N

ew H

aven

, C

I 06

520—

1972

N

ew H

aven

, cr

065

20—

1972

I. I

ntro

duct

ion

The

rec

ent

liter

atur

e on

exc

hang

e ra

te t

arge

t zo

nes

insp

ired

by

Kru

gman

's

sem

inal

ar

ticle

on

the

subj

ect

(Kru

gman

[199

0])

repr

esen

ts

a su

cces

sful

mar

riag

e of

polic

y re

leva

nce a

nd t

echn

ical

inno

vatio

n. F

orm

al t

arge

t zon

es l

ike

the

exch

ange

rat

e

arra

ngem

ents

of th

e E

urop

ean M

onet

ary

Syst

em a

nd i

nfor

mal

tar

get z

ones

bet

wee

n th

e

U.S

. do

llar,

the

Japa

nese

yen

and

the

D—

Mar

k si

nce

the

mid

dle o

f th

e la

st d

ecad

e w

ere

a pr

omin

ent f

eatu

re o

f the

exc

hang

e ra

te s

yste

m o

f the

Eig

htie

s and

pro

mis

e to

be

so

for t

he N

inet

ies.

T

he t

echn

ical

mod

elin

g in

nova

tion

cons

ists

in

the

appb

catio

n of th

e

theo

ry o

f re

gula

ted

Bro

wni

an m

otio

n (s

ee e

.g.

Mal

liari

s an

d B

rock

[19

82],

Har

riso

n

[198

5], D

ixit

[198

8], K

arat

zas

and

Shre

ve [

1988

], D

umas

[1

989]

and

Flo

od a

nd G

arbe

r

[198

9]) to

the

stud

y of

the

beha

vior

of

a fl

oatin

g ex

chan

ge

rate

that

is c

onst

rain

ed

by

appr

opri

ate i

nter

vent

ions

not

to s

tray

out

side

som

e gi

ven

rang

e or t

arge

t zon

e.

The

lite

ratu

re o

n th

is s

ubje

ct i

s gr

owin

g ve

ry f

ast.

Am

ong

the

man

y re

cent

cont

ribu

tions

are

Kru

gman

[198

7], K

rugm

an

and

Rot

embe

rg [1

990]

, Mill

er a

nd W

elle

r

[198

8a,b

; 19

89;

1990

a,b,

c],

Mill

er a

nd S

uthe

rlan

d [1

990]

, Fro

ot a

nd O

bstf

eld

[198

9a,b

],

Ber

tola

an

d C

abal

lero

[1

989,

199

0],

Kle

in [

1989

], S

vens

son

[198

9; 1

990a

,b],

Pes

enti

[190

0], D

elga

do a

nd D

umas

[19

90],

Lew

is [1

990]

, A

vesa

ni [

1990

], Ic

hika

wa,

M

iller

and

Suth

erla

nd [1

990]

, and

Sm

ith a

nd S

penc

er [

1990

].

A c

omm

on

elem

ent

in a

ll of

the

se a

naly

ses

is t

hat

a "f

unda

men

tals

onl

y"

solu

tion

is c

hose

n fo

r th

e ex

chan

ge r

ate:

The

exc

hang

e ra

te, a

non—

pred

eter

min

ed s

tate

vari

able

, is e

xpre

ssed

as

a fu

nctio

n of

the

curr

ent a

nd e

xpec

ted

futu

re v

alue

s of

the

fund

amen

tals

onl

y.

The

lite

ratu

re i

n fa

ct

conc

entr

ates

on

mod

els

with

a

sing

le

fund

amen

tal.

Thi

s fu

ndam

enta

l is g

over

ned

by r

egul

ated

Bro

wni

an m

otio

n, th

at i

s by

unre

gula

ted

Bro

wni

an m

otio

n as

lon

g as

the

fund

amen

tal s

tays

with

in t

he lo

wer

and

uppe

r in

terv

entio

n th

resh

olds

and

by

(int

erm

itten

t) i

nter

vent

ions

tha

t ke

ep

the

fund

amen

tal

with

in t

hese

thr

esho

lds

whe

neve

r th

e un

regu

late

d B

row

nian

m

otio

n

thre

aten

s to

tak

e th

e fu

ndam

enta

l ou

tsid

e th

e in

terv

entio

n lim

its (

and

thus

the

—2—

exch

ange

ra

te o

utsi

de i

ts t

arge

t zo

ne).

T

his

perm

its t

he c

urre

nt

valu

e of

the

spot

exch

ange

ra

te to

be

expr

esse

d as

a n

on—

linea

r fun

ctio

n of

the

cur

rent

val

ue o

f th

e

fund

amen

tal o

nly.

The

firs

t ste

p in

this

arg

umen

t, th

e de

cisi

on to

sol

ve f

or th

e cu

rren

t val

ue o

f th

e

exch

ange

ra

te a

s a

func

tion

only

of

the

cur

rent

an

d ex

pect

ed fu

ture

val

ues

of t

he

fund

amen

tal,

mea

ns th

at s

pecu

lativ

e bu

bble

s ar

e ru

led o

ut.

In d

ynam

ic

linea

r ra

tiona

l exp

ecta

tions

mod

els

the

argu

men

ts

for

rulin

g ou

t

spec

ulat

ive

bubb

les

are

wel

l—kn

own,

if n

ot n

eces

sari

ly w

holly

con

vinc

ing.

In

man

y of

the

mos

t po

pula

r m

odel

s th

e bu

bble

pr

oces

ses

are

non—

stat

iona

ry.'

The

se

non—

stat

iona

ry

bubb

le p

roce

sses

th

en

lead

to

non

—st

atio

nary

be

havi

or o

f st

ate

vari

able

s su

ch a

s as

set

pric

es.

Unb

ound

ed g

row

th o

r de

clin

e in

the

se s

tate

vari

able

s for

cons

tant

val

ues o

f th

e fu

ndam

enta

ls is

arg

ued

to v

iola

te,

even

tual

ly, c

erta

in o

ften

onl

y

impl

icitl

y st

ated

feas

ibili

ty co

nstr

aint

s.2

Bla

ncha

rd [1

979]

ha

s de

velo

ped

an e

xam

ple

of a

non—

stat

iona

ry (

stoc

hast

ic o

r

dete

rmin

istic

) lin

ear b

ubbl

e th

at h

as a

fini

te ex

pect

ed l

ifet

ime.

T

he p

roba

bilit

y of

the

bubb

le su

rviv

ing

for

a gi

ven

peri

od o

f tim

e de

clin

es w

ith th

e le

ngth

of th

at p

erio

d at

a co

nsta

nt e

xpon

entia

l ra

te a

nd a

ppro

ache

s ze

ro a

sym

ptot

ical

ly

(see

als

o B

lanc

hard

and

Fisc

her

[198

9, c

hapt

er 5

]).

Alth

ough

th

e bu

bble

rem

ains

non

-sta

tiona

ry a

nd i

ts

expe

cted

val

ue g

row

s ex

pone

ntia

lly

with

out b

ound

, th

e fi

nite

exp

ecte

d lif

etim

e of

this

bubb

le m

ay m

ake

it le

ss v

ulne

rabl

e to

the

stan

dard

cri

tique

of n

on-s

tatio

nary

bub

bles

.

Mill

er a

nd W

elle

r [1

990a

[ an

d M

iller

, W

elle

r an

d W

illia

mso

n [1

989]

use

the

Bla

ncha

rd

bubb

le

to a

naly

ze e

xcha

nge

rate

beh

avio

r (b

oth

with

and

with

out a

tar

get

zone

) in

a

stoc

hast

ic ve

rsio

n of

the

Dor

nbus

ch o

vers

hoot

ing

mod

el (

Dor

nbus

ch

[197

6]).

Cer

tain

no

n—lin

ear m

odel

s al

so p

osse

ss n

on—

stat

iona

ry b

ubbl

e so

lutio

ns.

For

inst

ance

, the

def

latio

nary

an

d in

flat

iona

ry b

ubbl

es

stud

ied

by H

ahn

[198

2] a

nd b

y

Obs

tfel

d an

d R

ogof

f [1

983]

, al

thou

gh o

btai

ned

in n

on—

linea

r m

odel

s,

are

also

non—

stat

iona

ry.

In m

ore

gene

ral

non—

linea

r mod

els

it it

how

ever

qui

te c

omm

on t

o

—3—

find

stat

iona

ry b

ubbl

es.3

The

exc

hang

e ra

te t

arge

t zo

ne m

odel

pot

entia

lly p

rovi

des

a pa

rtic

ular

ly h

appy

non—

linea

r br

eedi

ng g

roun

d fo

r sp

ecul

ativ

e bu

bble

s.

Prov

ided

the

targ

et z

one

is

cred

ible

, th

at i

s pr

ovid

ed

ther

e is

cer

tain

ty th

at t

he i

nter

vent

ions

requ

ired

to

defe

nd

the

targ

et z

one

will

ta

ke

plac

e,

the

exch

ange

ra

te c

an n

eith

er ri

se n

or f

all

with

out

boun

d.

The

re a

re i

nfin

itely

man

y in

terv

entio

n ru

les

that

are

com

patib

le w

ith t

he

defe

nse

of a

giv

en t

arge

t zo

ne.

For

a ra

tiona

l sp

ecul

ativ

e bu

bble

to

exis

t, th

e

inte

rven

tion

rule

mus

t of c

ours

e be

con

sist

ent,

both

with

in th

e ta

rget

zon

e an

d at

the

boun

dari

es, w

ith th

e be

havi

or o

f th

e (r

egul

ated

) fun

dam

enta

ls.

Thi

s pa

per d

evel

ops

a

sim

ple

and

intu

itive

int

erve

ntio

n ru

le th

at e

ncom

pass

es a

s a

spec

ial

case

the

sol

utio

n

with

out

a bu

bble

, ye

t is

ge

nera

l en

ough

to

perm

it a

wid

e ra

nge

of e

xoge

nous

and

fund

amen

tal—

depe

nden

t de

term

inis

tic or

sto

chas

tic b

ubbl

es.

With

thi

s in

terv

entio

n

rule

the

argu

men

ts a

gain

st b

ubbl

es l

ose

thei

r bite

. A

non

—st

atio

nary

bub

ble

does

not

now

im

ply

non—

stat

iona

ry b

ehav

ior o

f th

e ex

chan

ge r

ate.

T

his

argu

men

t is

not

new

.

As

earl

y as

198

7 W

illia

m H

. B

rans

on,

in c

onve

rsat

ion

and

disc

ussi

on,

repe

ated

ly ra

ised

the

poss

ibili

ty th

at ta

rget

zon

es m

ight

lead

to "

inde

term

inac

y" of

the

exc

hang

e ra

te.

Thi

s pa

per c

an b

e vi

ewed

as

an a

naly

tical

conf

irm

atio

n of h

is c

onje

ctur

e.

In t

he n

ext

Sect

ions

we

expo

sit

the

sim

ples

t ve

rsio

n of

the

cred

ible

tar

get

zone

mod

el a

nd a

naly

ze its

beh

avio

r with

or

with

out s

pecu

lativ

e bu

bble

s.

II.

A T

arge

t Zon

e M

odel

With

or W

ithou

t Spe

cula

tive

Bub

bles

.

(a) T

he M

odel

.

Our

ana

lysi

s of

the

pla

ce a

nd r

ole

of s

pecu

lativ

e bu

bble

s in

an

exch

ange

rat

e

targ

et z

one

requ

ires

the

exch

ange

ra

te t

o be

a no

n—pr

edet

erm

ined

(fo

rwar

d—lo

okin

g)

—4—

,

stat

e va

riab

le,

but

does

not

m

ake

furt

her

dem

ands

on

de

scri

ptiv

e re

alis

m.

We

ther

efor

e fe

el

com

fort

able

in

usi

ng

Occ

am's

ra

zor

and

follo

win

g th

e bu

lk

of t

he

liter

atur

e on

tar

get

zone

s by

cas

ting

the

anal

ysis

in

ter

ms

of th

e si

mpl

est

poss

ible

linea

r in

tert

empo

ral s

ubst

itutio

n eq

uatio

n fo

r th

e ex

chan

ge

rate

and

a (

cont

inuo

us

time)

rand

om w

alk

with

dri

ft f

or th

e un

regu

late

d fun

dam

enta

l. (N

otab

le d

epar

ture

s

from

the

cult

of e

xtre

me

sim

plic

ity

are

Mill

er a

nd W

elle

r [1

988a

,b;

1989

; 19

90a,

b,c]

who

ana

lyze

stoc

hast

ic ve

rsio

ns o

f the

rich

er D

ornb

usch

ove

rsho

otin

g m

odel

.)

The

exc

hang

e ra

te p

roce

ss i

s gi

ven

in e

quat

ion

(1).

(1)

s(t)

dt =

f(t)

dt +

a'E

tds(

t)

a >

0.

Her

e s(

t)

is th

e na

tura

l lo

gari

thm

of t

he s

pot

nom

inal

exc

hang

e ra

te a

nd f(

t)

the

fund

amen

tal

dete

rmin

ant

of

the

exch

ange

ra

te.

Et

is

the

mat

hem

atic

al

expe

ctat

ion o

pera

tor c

ondi

tiona

l on

the

info

rmat

ion

avai

labl

e at t

ime

t to

the

priv

ate

sect

or a

nd th

e re

gula

tor.

Bot

h sO

) an

d f(

t)

are

assu

med

to b

e ob

serv

able

at ti

me

t,

i.e.

Ets

(t) =

sO)

and

Etf

(t) =

f(t)

, an

d th

e st

ruct

ure

of th

e m

odel

is

know

n.

For

the

purp

ose

of th

is p

aper

, the

econ

omic

int

erpr

etat

ion

of

f(t)

is

irr

elev

ant

exce

pt i

nsof

ar a

s it

affe

cts

the

cred

ibili

ty of

our

ass

umpt

ion t

hat,

with

eert

alnt

y, th

e

targ

et z

one

will

be

succ

essf

ully

def

ende

d.

A c

omm

on i

nter

pret

atio

n of

f is

in t

erm

s of

rela

tive

nom

inal

mon

ey s

tock

s m

inus

rela

tive

real

—in

com

e—re

late

d de

man

ds

for

real

mon

ey b

alan

ces,

i.e

.

* *

f=m

—m

—

k(y—

y )

whe

re

m i

s th

e lo

gari

thm

of th

e ho

me

coun

try n

omin

al m

oney

sto

ck,

y th

e lo

gari

thm

of h

ome

coun

try

real

out

put

and

k is

the

(co

mm

on)

inco

me

elas

ticity

of

mon

ey

dem

and.

St

arre

d va

riab

les

deno

te fo

reig

n qu

antit

ies,

In

thi

s ca

se

a de

note

s th

e

—5—

inve

rse o

f the

(com

mon

) in

tere

st s

emi—

elas

ticity

of m

oney

dem

and.

4

If th

e tw

o na

tiona

l rea

l out

puts

are

gov

erne

d by

exo

geno

us B

row

nian

mot

ion,

inte

rven

tion

mea

ns ch

ange

s in

the

rela

tive

mon

ey s

uppl

ies b

roug

ht a

bout

by

mon

etar

y

fina

ncin

g of

pub

lic

sect

or f

inan

cial

def

icits

, th

roug

h op

en m

arke

t op

erat

ions

or

by

unst

erili

zed

fore

ign

exch

ange

m

arke

t in

terv

entio

n.

As

show

n in

Bui

ter

[198

9] s

uch

inte

rven

tion

polic

ies

will

in

gene

ral

requ

ire

adju

stm

ents

to p

rim

ary

(non

—in

tere

st)

fisc

al

surp

luse

s to

be

sust

aina

ble

inde

fini

tely

fr

om a

tec

hnic

al p

oint

of

view

(i.e

. in

orde

r to

prev

ent e

ither

exh

aust

ion

of f

orei

gn e

xcha

nge

rese

rves

or u

nbou

nded

grow

th of

the

publ

ic d

ebt)

. A

pro

of th

at t

hey

are

polit

ical

ly f

easi

ble

and

cred

ible

is

beyo

nd t

he

scop

e of

this

pap

er.

In th

e ab

senc

e of

inte

rven

tion,

the

(unr

egul

ated

) fun

dam

enta

l f w

ould

fol

low

a

Bro

wni

an m

otio

n pr

oces

s w

ith d

rift

p an

d in

stan

tane

ous v

aria

nce c

.

di(t

) =

pdt

+ u1

dW1(

t)

clf>

0.

W1(

t)

is a

sta

ndar

d W

iene

r pr

oces

s (d

Wf

e 1 im

w

here

is

at

-to

inde

pend

ently

and

norm

ally

dist

ribu

ted

with

zer

o m

ean

and

unit

vari

ance

).

We

now

al

low

fo

r in

terv

entio

n at

the

upp

er a

nd l

ower

bo

unda

ries

of

the

exch

ange

rat

e ta

rget

zon

e. T

he re

gula

ted f

unda

men

tal

is g

over

ned

by

(2)

df(t

) =

pdt

+ yI

Wf(

t) —

dlu

+ d

lt

and I a

re t

he c

umul

ativ

e int

erve

ntio

ns

at th

e up

per

and

low

er b

ound

s of

the

exch

ange

rat

e ta

rget

zon

e, g

iven

by

5u an

d s1

resp

ectiv

ely

with

—

<

<

5u

< .

A

deta

iled s

peci

fica

tion

of th

ese

inte

rven

tions

is g

iven

bel

ow.

—6-

—

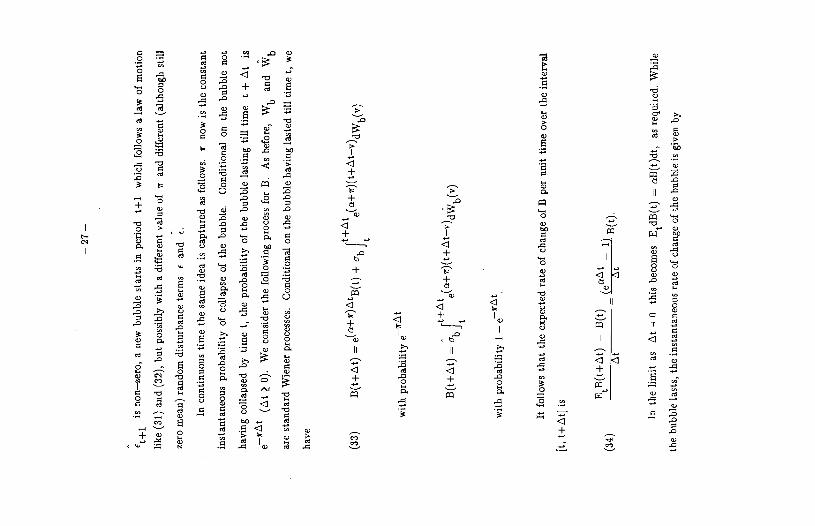

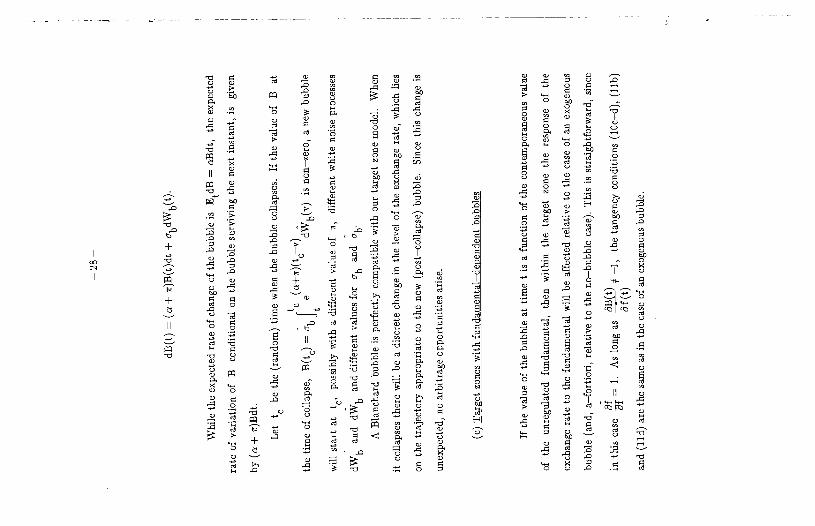

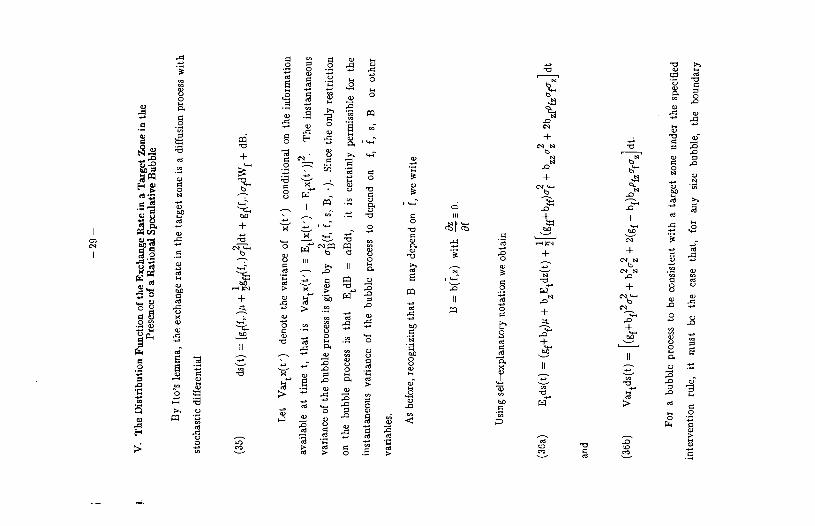

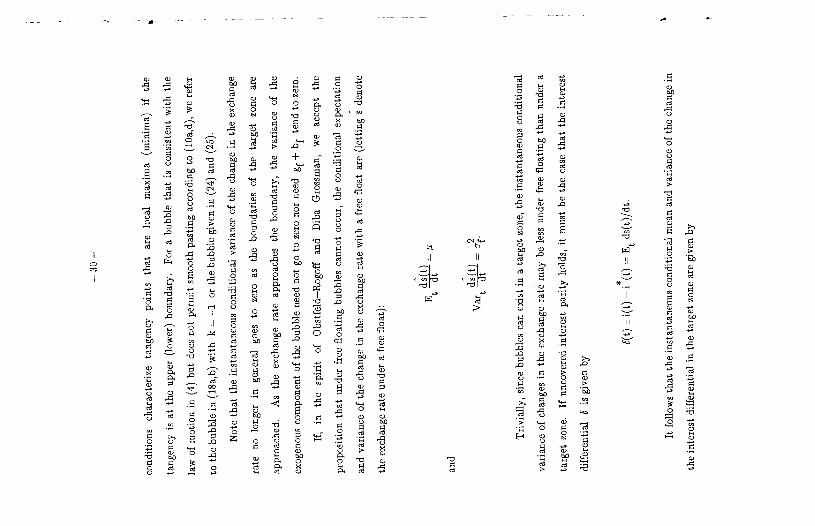

(b)

The

Sol

utio

n

The

gen

eral

sol

utio

n of

(1)

is

give

n in

equ

atio

n (3

).

B(t

) is

the

val

ue o

f th

e

spec

ulat

ive

bubb

le a

t tim

e t.

(3)

5(t)

=

i: E

tf(v)

e(v_

t)dv

+ B

(t).

The

bub

ble

B(t

) ca

n be

an

y st

ocha

stic

or

st

rict

ly d

eter

min

istic

pro

cess

satis

fyin

g

(4)

B(t

)dt

= a'

Etd

B(t

).

Not

e tha

t si

nce

s(t)

is

part

of t

he in

form

atio

n se

t at t

, so

is B

(t).

W

e re

stri

ct

B, w

here

it i

s st

ocha

stic

, to

follo

w a

dif

fusi

on p

roce

ss.

Exc

ept f

or t

he c

ase

of t

he

"Bla

ncha

rd b

ubbl

e",

all

exam

ples

w

ill

in f

act

rest

rict

it

furt

her

to b

e a

twic

e

cont

inuo

usly

di

ffer

entia

ble

func

tion o

f Bro

wni

an m

otio

ns.

Fina

lly,

it is

impo

rtan

t to

note

that

the

aut

hori

ties a

re a

ssum

ed t

o be

una

ble t

o

inte

rven

e di

rect

ly in

the

bub

ble

proc

ess

(and

in

deed

in t

he e

xcha

nge

rate

pro

cess

).

The

y ca

n on

ly r

egul

ate t

he fu

ndam

enta

l £

In t

he i

nter

ior

of th

e ta

rget

zon

e, t

he g

ener

al s

olut

ion

for

s as

a f

unct

ion

of

curr

ent f a

nd c

urre

nt B

is g

iven

by5

.A2(

f(t)

—C

(t))

(5

) s(

t) =

f(t)

+ B

(t) +

+

A1(

t)e

+ A

2(t)

w

ith

—

/7 +

2nc

2 crf

—7—

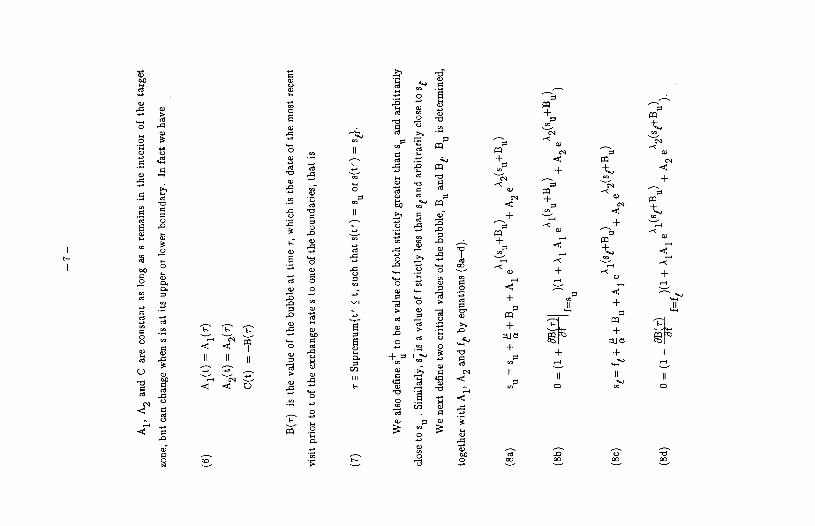

A1,

A2

and

C a

re c

onst

ant

as l

ong

as s

rem

ains

in t

he i

nter

ior

of t

he t

arge

t

zone

, hut

can

cha

nge

whe

n s

is a

t its

upp

er o

r lo

wer

bou

ndar

y.

In fa

ct w

e ha

ve

(6)

A1(

t) =

A1(

r)

A2(

t) =

A2(

r)

C(t

) =

—B

(r)

B(r

) is

the

val

ue o

f th

e bu

bble

at t

ime

r, w

hich

is th

e da

te o

f the

mos

t rec

ent

visi

t pri

or to

t of

the

exch

ange

rat

e s

to o

ne o

f th

e bo

unda

ries

, th

at i

s

(7)

r a S

upre

mum

{t' �

t, su

ch th

at s

(t')

= 5u

or S

O')

=

We

also

def

ine s to

be

a va

lue

off

both

str

ictly

gre

ater

than

s an

d ar

bitr

arily

clos

e to

. S

imila

rly,

s

is a

valu

e of

f st

rict

ly le

ss t

han

5 an

d ar

bitr

arily

clo

se to

s.

We

next

def

ine

two

criti

cal v

alue

s of

the

bubb

le,

Bu

and

Bt

Bu

is d

eter

min

ed,

toge

ther

with

A1,

A2

and

by e

quat

ions

(8a

—d)

.

A(s

-l-B

) A

(s-4

-B)

(8a)

5u

5u+

+B

uie

1 u

u+A

e 2

u u

(8b)

=

(1

+ 5u

X +

i A1

eA1(

5u+

+ A

2 eA

2(5u

)

A(s

+B

)

A(s

1-i-B

)

(Sc)

si

=ft

++

Bu+

Aie

1 u+

A2e

2 u

(Sd)

=

(1

+

+ A

1A1

eA1(

51+

+ A

2 eA

2(5)

.

—8—

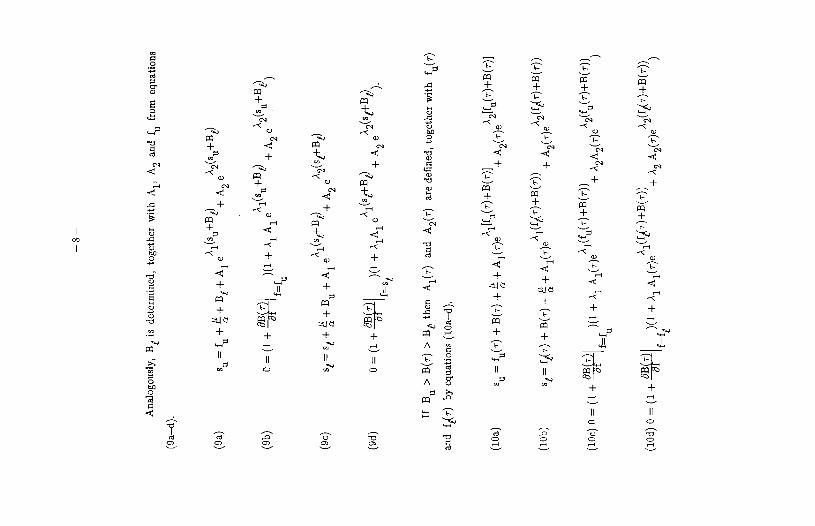

Ana

logo

usly

, B

1 is

det

erm

ined

, to

geth

er w

ith A

1,

A2

and

f fr

om e

quat

ions

U

(9a-

d).

(9a)

s

= f

+

+ B

1 +

A1

eA1

1)

A2 e2

1)

U

U

a

(9b)

0

= (1

+

)(1

+ A

1 A

1 eA

1(5u

1) +

A2 e2

1))

U

A

(s1-

l-B

1)

(9c)

s1

= 8

1+ +

B

+ A

1 e1

(11)

+ A2

e 2

A (s

1+B

1) +

A2 e2

1)).

(9

d)

0 =

(1 +

f=

s1 +

A1A

1 e

1

If B

> B

(r)

> B

1, th

en

A1(

r) an

d A

2(i-

) ar

e de

fine

d, t

oget

her w

ith f

(r)

and

f1(r

) by

equ

atio

ns (l

Oa—

d).

A [f

(r)+

B(r

)]

(ba)

s

=f (

r)+

B(r

)++

A1(

r)e

l +

A2(

r)e

u u

a

(lob

) =

f1(r

) + B

() +

+

A1(

r)e

+ A

2(r)

e A

(bc)

0 =

(1 +

)(

1 +

A1

A1(

r)e

+ A

2A2(

r)e 2(

TT

) U

(lO

d) 0

= (1

+ q

T)-

)(l +

A1 A

1(r)

e'' + A

2 A

2(r)

e )

—9.

-.

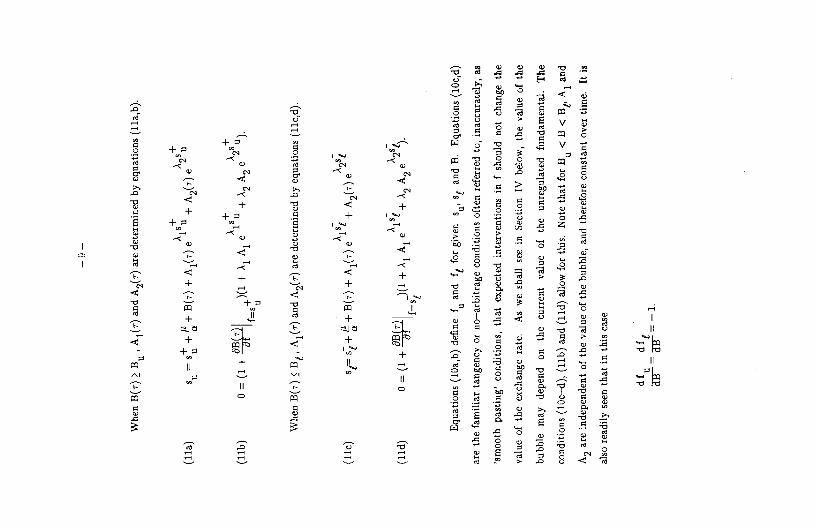

Whe

n B

(r) � B

u A

1(r)

and

A2(

r) a

re d

eter

min

ed by

equ

atio

ns (l

la,b

).

(ha)

s =

s +

+ B

(r)

Ai(

r) e

iu +

A2(

r) eA

250

(ub)

0

= (1

+

+ A

1 A

1 ei

u +

A2

A2

eA25

).

Whe

n B

(r)

B1

, A

1(r)

and A

2(r)

are

dete

rmin

ed b

y eq

uatio

ns (l

ic,d

).

- .\i

A

s1

(hic

) 5r

s1 +

+

B(r

) + A

1(r)

e +

A2(

r) e

(lid

) 0

= (

1 +

+

A

1 el

l + A

2 A

2 e2

1).

Equ

atio

ns (i

oa,b

) de

fine

u

and

f1 fo

r giv

en

8u' s

1 an

d B

. E

quat

ions

(ioc

,d)

are

the

fam

iliar

tang

ency

or n

o—ar

bitr

age

cond

ition

s of

ten

refe

rred

to, i

nacc

urat

ely,

as

'sm

ooth

pa

stin

g' c

ondi

tions

, th

at e

xpec

ted

inte

rven

tions

in f

shou

ld

not

chan

ge t

he

valu

e of

the

exc

hang

e ra

te.

As

we

shal

l se

e in

Sec

tion

IV b

elow

, th

e va

lue

of t

he

bubb

le

may

dep

end

oo

the

curr

ent

valu

e of

th

e un

regu

late

d fu

ndam

enta

l. T

he

cond

ition

s (1

0c—

d), (

iib) a

nd (l

id) a

llow

for

thi

s.

Not

e th

at fo

r B0

< B

C B

t A1

and

A2

are

inde

pend

ent o

f the

val

ue o

f the

bub

ble,

and

the

refo

re c

onst

ant o

ver t

ime.

It

is

also

read

ily se

en t

hat

in th

is c

ase

df

d11

—10

—

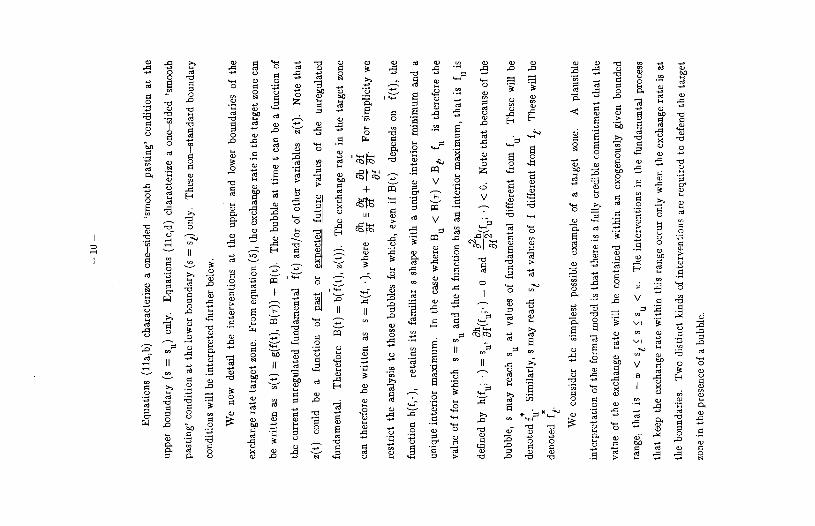

Equ

atio

ns (l

la,b

) ch

arac

teri

ze a

one

—si

ded

'sm

ooth

pas

ting'

con

ditio

n at

the

uppe

r bo

unda

ry (

s =

on

ly.

Equ

atio

ns (l

lc,d

) ch

arac

teri

ze a

one

—si

ded

'sm

ooth

past

ing'

con

ditio

n at

the

low

er b

ound

ary

(s =

on

ly.

The

se n

on—

stan

dard

bou

ndar

y

cond

ition

s w

ill b

e in

terp

rete

d fu

rthe

r be

low

.

We

now

det

ail

the

inte

rven

tions

at

the

uppe

r an

d lo

wer

bo

unda

ries

of

the

exch

ange

rat

e ta

rget

zon

e.

From

equ

atio

n (5

), t

he e

xcha

nge

rate

in th

e ta

rget

zon

e ca

n

be w

ritte

n as

5(

t) =

g(f

(t),

B(r

)) +

B(t

).

The

bub

ble

at ti

me

t can

be

a fu

nctio

n of

the

curr

ent u

nreg

ulat

ed fu

ndam

enta

l f(

t) a

nd/o

r of

oth

er v

aria

bles

z(t

).

Not

e th

at

z(t)

co

uld

be a

fun

ctio

n of

nM

or

exoe

cted

fqe

valu

es o

f th

e un

regu

late

d fu

ndam

enta

l. T

here

fore

B(t

) =

b(f

(t),

z(t)

).

The

exc

hang

e ra

te i

n th

e ta

rget

zon

e

can

ther

efor

e be

wri

tten

as

5 =

h(f,

•), w

here

a

+ . Fo

r sim

plic

ity

we

Of

rest

rict

the

ana

lysi

s to

tho

se b

ubbl

es f

or w

hich

, ev

en i

f B(t

) de

pend

s on

1(

t),

the

func

tion

h(f,

.),

reta

ins

its f

amili

ar s

sha

pe w

ith a

uni

que

inte

rior

min

imum

an

d a

uniq

ue i

nter

ior

max

imum

. In

the

cas

e w

here

Bu

< B

(r) c

B,

u is

the

refo

re th

e

valu

e of

f fo

r w

hich

s =

5u an

d th

e h

func

tion

has

an i

nter

ior m

axim

um, t

hat

is u

is

defi

ned

by h

(fu;

)

= 5u

' =

0

and

•) <

0.

Not

e th

at b

ecau

se of

the

bubb

le,

s m

ay r

each

5u

at v

alue

s of

fun

dam

enta

l dif

fere

nt f

rom

u•

The

se w

ill

be

deno

ted f

. Sim

ilarl

y, s

may

reac

h s

at v

alue

s of

f d

iffe

rent

fro

m f

The

se w

ill b

e

deno

ted

f1.

We

cons

ider

th

e si

mpl

est

poss

ible

exa

mpl

e of

a t

arge

t zo

ne.

A p

laus

ible

inte

rpre

tatio

u of

the

form

al m

odel

is th

at t

here

is a

fully

cre

dibl

e co

mm

itmen

t tha

t the

valu

e of

the

exch

ange

ra

te w

ill b

e co

ntai

ned

with

in a

n ex

ogen

ousl

y gi

ven

boun

ded

rang

e, t

hat i

s —

z C

s

s 5u

< z

. T

he in

terv

entio

ns in

the

fun

dam

enta

l pro

cess

that

kee

p th

e ex

chan

ge r

ate

with

in th

is ra

nge o

ccur

onl

y w

hen

the e

xcha

nge

rate

is at

the

boun

dari

es.

Tw

o di

stin

ct k

inds

of

inte

rven

tions

are

requ

ired

to d

efen

d th

e ta

rget

zo

ne in

the

pres

ence

of a

bubb

le.

11 —

The

fir

st i

s a

pair

of

infi

nite

sim

al re

flec

ting

inte

rven

tions

, _dl

u <

0 a

t th

e

uppe

r bou

ndar

y if

f =

u an

d dI

1> 0

at t

he l

ower

bou

ndar

y of

the

targ

et z

one

if

=

The

se n

egat

ive i

nfin

itesi

mal

inte

rven

tions

at th

e up

per b

ound

ary

s =

s a

nd

posi

tive

infi

nite

sim

al in

terv

entio

ns a

t the

low

er b

ound

ary

s =

5, c

orre

spon

d to

the

orig

inal

sch

eme

anal

yzed

by

Kru

gman

[1

990]

. II

inte

rven

tions

in t

he i

nter

ior

of th

e

targ

et

zone

("

intr

amar

gina

l" i

nter

vent

ions

) w

ere

perm

itted

, a

pair

of

refl

ectin

g

inte

rven

tions

of

exog

enou

sly

give

n fi

nite

mag

nitu

des,

_A

Iu <

0

and

Al1

> 0

co

uld

be a

llow

ed (

see

Floo

d an

d G

arbe

r [19

89])

.

The

sec

ond

clas

s of

inte

rven

tions

com

pris

es i

nter

vent

ions

of f

inite

mag

nitu

de,

that

are

fun

ctio

ns o

f the

cha

nge

in th

e m

agni

tude

of th

e bu

bble

sin

ce t

he p

revi

ous

visi

t

to th

e bo

unda

ries

. T

hey

too

occu

r onl

y w

hen

the

exch

ange

rat

e is

at t

he b

ound

arie

s of

the

targ

et z

one.

T

hey

alw

ays

are

in t

he o

ppos

ite

dire

ctio

n fr

om t

he in

fini

tesi

mal

(typ

e I)

int

erve

ntio

ns at

the

sam

e bo

unda

ry.

We

inte

rpre

t th

ese

(typ

e II

) di

scre

te

inte

rven

tions

as

th

e pa

ssiv

e

acco

mm

odat

ion

of r

atio

nal

spec

ulat

ive

atta

cks

at t

he b

ound

arie

s of

the

tar

get

zone

,

that

are

con

sist

ent

with

the

sur

viva

l of

the

targ

et z

one.

W

e re

fer t

o su

ch s

tock

—sh

ift

port

folio

res

huff

ies

as "

sust

aini

ng"

or "

frie

ndly

" sp

ecul

ativ

e at

tack

s.

The

beh

avio

r of

the

regu

late

d fun

dam

enta

l is

give

n in

equ

atio

ns (1

2a) t

o (1

2c).

The

co

nditi

ons

in (

12a)

, (1

2b),

(12

c(a)

) an

d (1

2c(y

))

are

the

stan

dard

one

s fo

r

regu

late

d Bro

wni

an m

otio

n (s

ee e

.g.

Har

riso

n ]1

985,

p.

80])

. If

>

u an

d if

f =

whe

n =

5u' t

hey

char

acte

rize

a r

efle

ctin

g ba

rrie

r at

f =

u (

give

n by

(12

a),

(12b

)

and

(12c

(a))

. If

f1 c

s an

d if

f =

f1

whe

n s

= s,

th

ey c

hara

cter

ize

a re

flec

ting

barr

ier a

t f =

f1 g

iven

by

(12a

), (

12b)

and

(12

c('y

)).

The

oth

er c

ondi

tions

ar

e no

n-st

anda

rd a

nd a

re r

equi

red

for

our

anal

ysis

of

ratio

nal

bubb

les

in a

targ

et

zone

. If

>

5u'

they

cha

ract

eriz

e (d

iscr

ete)

acco

mm

odat

ed

spec

ulat

sve

atta

cks

from

f =

f to

I =

u' fo

llow

ed b

y (i

nfin

itesi

mal

)

refl

ectio

n at

f =

u (

give

n by

(12

a),

(12b

) an

d (1

2c(f

i)).

If

f1 <

s,

they

cha

ract

eriz

e

—12

—

acco

mm

odat

ed sp

ecul

ativ

e atta

cks

from

f

= f

to

I =

f, fo

llow

ed b

y re

flec

tion a

t

=1

(giv

en

by (

12a)

, (1

2b)

and

(12c

(6))

. If

f0

�

s,

they

cha

ract

eriz

e

acco

mm

odat

ed

spec

ulat

ive a

ttack

s fr

om I =

I (to

I =

s (g

iven

by

(12a

), (

12b)

and

(12c

(c))

. If

I � s

, th

ey c

hara

cter

ize

acco

mm

odat

ed

spec

ulat

ive a

ttack

s fr

om I

=

to I

= s

(giv

en b

y (1

2a),

(12

b) a

nd l

2c(s

)).

The

rea

sons

for

thes

e no

n—st

anda

rd

feat

ores

will

bec

ome

clea

r be

low

.

We

rest

rict

atte

ntio

n to

sta

rtin

g st

ates

s

and

star

ting

date

t

= 0

and

defi

ne t

as th

e in

stan

t im

med

iate

ly be

fore

t, th

at is

t_e

lim (

t—ht

) t-

4O

at>

o

The

regu

late

d fun

dam

enta

l is fo

rmal

ly d

efin

ed a

s fo

llow

s:

(12a

) 1(

t) e

pt +

dW

1—10

(t)

+ I/

t) fo

r all

t � 0

(12b

) 1n

and

I ar

e co

nsta

nt if

s1 <

s <

(12c

) jO

an

d I v

ary

whe

n =

or

s

= s

(I

) 1f

f0 >

5 an

d 1

< 5

then

:

(a)

II s

= s

and

I = 1

then

1U

is

cont

inuo

us

and

incr

easi

ng.

(jl)

If

s(t

) =

s an

d 1(

t) =

10,

then

1(

t) =

f0(t

) an

d (a

) ap

plie

s he

ncef

orth

.

('y)

II s

= s1

an

d I =

1 th

en I

is co

ntin

uous

and

incr

easi

ng.

( II

s(t_

) =

s1 an

d 1(

t) =

1,

then

1(t

) =

f/t)

and

()

appl

ies

henc

efor

th.

— 1

3—

(ha)

1f

f � s

then

(c)

If s

(t_)

= s

then

1(t

) =

s

If s

= s

then

(y)

or (

8)

appl

y.

(JIb

) If

1� s

then

(77)

If

s(t)

= s

then

1(t

) =

s1

If s

= s

then

(a)

or

(fi)

app

ly.

It w

ill h

e ap

pare

nt t

hat,

for

any

size

bub

ble

we

can

calc

ulat

e exa

ctly

bot

h th

e

mag

nitu

des

of th

e pa

ssiv

e or

acc

omm

odat

ing

disc

rete

int

erve

ntio

ns re

quir

ed to

allo

w

the

targ

et z

one

to s

urvi

ve a

nd th

e va

lues

of

the

fund

amen

tals

at w

hich

they

will

occ

ur.

In o

ur

rudi

men

tary

mod

el,

ther

e is

no

pos

sibi

lity

of t

he s

pecu

lativ

e bu

bble

infl

uenc

ing

the

beha

vior

of th

e fu

ndam

enta

l. A

bub

ble

in th

is m

odel

can

onl

y in

flue

nce

the

exch

ange

ra

te d

irec

tly.

If th

e pr

oces

s go

vern

ing

the

unre

gula

ted

fund

amen

tal

incl

uded

th

e ex

chan

ge

rate

as

an a

rgum

ent

then

, be

caus

e th

e bu

bble

af

fect

s th

e

exch

ange

ra

te,

it w

ill

indi

rect

ly i

nflu

ence

th

e be

havi

or o

f th

e fu

ndam

enta

l. A

n

inte

rest

ing

anal

ysis

of

a m

odel

in

whi

ch t

he b

ubbl

e af

fect

s th

e ex

chan

ge

rate

bot

h

dire

ctly

and

ind

irec

tly th

roug

h th

e fu

ndam

enta

l is

ana

lyze

d by

Mill

er—

Wel

ler [

1990

a]

and

by M

iller

, Wel

ler

and

Will

iam

son

[198

9].

Fina

lly,

the

beha

vior

of

the

auth

oriti

es at

the

edge

s of

the

tar

get

zone

can

be

sum

mar

ized

as

fol

low

s:

"Ref

lect

w

hen

this

is

suff

icie

nt;

acco

mm

odat

e whe

n th

is i

s

nece

ssar

y.

Ill.

Smoo

th P

astin

g a

Bub

bly E

xcha

nge R

ate

Con

side

r the

cas

e of

an e

xoge

nous

bub

ble,

tha

t is

one

tha

t do

es n

ot d

epen

d on

1.

The

bub

ble

can

be ei

ther

det

erm

inis

tic

or s

toch

astic

. T

he g

raph

ic re

pres

enta

tion o

f

this

cas

e is

sho

wn

in F

igur

es la

and

lb.

We

now

def

ine

the

bubb

le e

ater

of

the

exch

ange

rat

e fo

r a

give

n va

lue

of th

e

— 1

4—

bubb

le,

B(t

). T

he b

ubbl

e ea

ter

of s

fo

r B

(t)

satis

fies

equ

atio

n (5

) w

ith

A1,

A2

and

C

dete

rmin

ed by

equ

atio

ns (6

) an

d (l

Oa—

d) f

or th

e ac

tual

ly p

reva

iling

va

lue

of

the

bubb

le, t

hat

is f

or

C(t

) =

—B

(t).

T

hat

is t

he b

ubbl

e ea

ter

of

s fo

r B

=

B is

give

n by

—

A1(

f + B

) A

2(f +

B)

(13a

) s=

f++

B+

A1e

+

A2e

—

A1(

f +

B)

A2(

f +

B)

(13b

) 5u

=fu

+ +

B + A

1 e

u +

A2e

u

A (f

+

B)

A2(

f +

B)

(13c

) O

=l+

A1A

1e 1

u +

A2A

2e

u

—

A1(

f1 +

B)

A2(

f1 +

B)

(13d

) s1

=f,

+-j

-B +

A1e

+

A2e

A1(

f1+

B)

A2(

f1+

B)

(13e

) O

=1+

A1A

1e

+A

2A2e

Thi

s bu

bble

ea

ter

shif

ts

cont

inuo

usly

w

ith

B;

an in

crea

se (

decr

ease

) in

B

corr

espo

nds

to a

n eq

ual h

oriz

onta

l di

spla

cem

ent

to t

he le

ft (

righ

t) o

f th

e gr

aph.

N

ote

that

the

bubb

le e

ater

giv

es a

ref

eren

ce t

raje

ctor

y on

ly

and

does

not

sho

w t

he a

ctua

l

mov

emen

t of

f an

d s

whe

n B

ch

ange

s un

less

Bu

> B

(r)

> B

1 an

d ei

ther

s =

an

d f=

f or

s=

s1 a

nd f

=f1

. W

hen

s is

in t

he in

teri

or o

f th

e ta

rget

zon

e an

d B

u >

B(r

) > B

1, its

pos

ition

ca

n be

def

ined

with

ref

eren

ce t

o th

e pe

riod

r bu

bble

eat

er,

that

is

the

bubb

le

eate

r

corr

espo

ndin

g to

the

valu

e of

B t

hat p

reva

iled a

t the

pre

viou

s (m

ost

rece

nt) v

isit

of

ui oq 03 sAnqe lnq) 'j jo q2u aqj o; aq osjt w

oo j 'ojqqnq gems A

puapgjns t °a

au!! .ç aq jo 24211 a; o3 si 434JM 'J =

; axoq'T v A

npunoq zaddn 042 03

Aoua2utl jo lulod e oe 'T

a + (1a ';)2 =

g £q uaA

I2 '1 ioj ;aoa aqquq 0112 '(ui2uo alp q2rIoflp 01511 ,ç alp uo si qotqA

t) "iJ Jo 3J0 01J3 02 51

J O

jII{M 3043 03°N

;o; 10300 oqqnq 0112 0AO

O 0a —

1a 100!310A

0 ' + (a ')2 =

qdei2aipuoarT

put u put

20813043'11J=J put

°J=j

;o; uoddoq w

oo siq; °s

puxq joddu 531 o 0201 a2uoqoxo 012 s2uuq

1H

02 ojqqnq

042 JO otis alp us aseanui w

e 1104M suodctsq T

eqht .ioprsuoo M

ON

A

repunoq IO

MO

j 0112

30 9jj

3ulod Aoua2w

e3 t put Arepunoq ;oddn 0l

0u 3uiod A

ouo2ut t swq 4314M

+ (0a 'J)2 =

s A

q UO

A!2 '0

IOJ

10200 oqqnq 042 31e;s eJ ain2sj uj

Aouonuo 0111 JO

uoireiooidop

popadxa ss 3043 '5 JO

oPuoqo jo 0201 popodxo OA

i3iSOd 0 0A

04 J4M O

uiJ Ji 043 JO 3J31

012 02 tusod Any

AO

UO

IIUO

042 Jo uOiltl001dcFe

po330dxa we 43!M

Si 3eq 's Jo a2wsqo

JO 0201 pa300dxa O

A!202011 0 q2!M

p0301301st oq 1PM 0114

.91' 043 JO 342!

042 03 3uiOd L

ull

'3p — s)o =

spa aousg

J = s

UIPIIO

013 4200143 0114 .91' 013 JO 212!; 012 03 504 (0

a;tuep.rooo put 0J ossiosqo) [0 0] usod oqi '(js <

°j q3!M) ojqqnq jrem

s o ;oj

us aqqnq aAs3ssO

cI v Jo osoo 043 10tS11O3 L

juo OM

'L3SA

OIq JO

ots ioj V

a 5 a) s 02

renba 10 11043 1030012 J stq ojqqnq oA

i3o8ou o2itj o put (1q < a <

o) s 11042 °1

504 ajqqnq O

A!3020u

'Asno2otuy °H

<

H ! 3043

115 03 rnba 10 1101{3

8101

oeq ajqqnq aAs3s od o2rei y

°a > a >

o ! 3043 11043 1030012 J

JO O

fijEA

0 0A2

(p—oi)

suolsonbo 4O0M

loJ 0110 51 ajqqnq oAslisod item

s y oqquq O

A!3!SO

d 0a2rej o Jo 3013 q o;n2sj 'ajqqnq aA

r3ssod j[tlS1 0 JO 0503 042

S3uOSO

ldOl

02 0102!J

•1a + (0a 'flP =

Lq U

OA

! s s

JO uo131sod 100300 012 '1H

5! a JO

Ofl[O

A [n30t 01J2

2 011112

30 J! U041

=

0 L3it1auo2 Jo 5501 315042!M

) 0a +

(0a 'j)2 = s

pa3ouap aq

UR

O

iOJ

10200 aqqnq 041 0H

aq

H Jo O

O10A

301J3 301 50fl0U

flO4 01j3 JO

ouo 02

— PT

—

—16

—

of

hi).

*2

w

ill

alw

ays

be to

the

lef

t of

ll•

From

11

*1 (o

r 11

2)

ther

e is

a

disc

rete

inte

rven

tion

(a s

tock

—sh

ift i

ncre

ase

in f

) w

hich

, at

a c

onst

ant

exch

ange

rat

e

= s,

mov

es t

he s

yste

m t

o Q

, the

poin

t of

tang

eocy

of

the

bobb

le e

ater

of

B1

and

the

uppe

r lim

it of

the

targ

et z

one.

T

he h

oriz

onta

l dis

tanc

e be

twee

n an

d hi

is

jus

t eq

ual

to t

he d

iffe

renc

e be

twee

n B

1 an

d B

°, i

.e.

— fj

= B

1 —

B°.

Mor

eove

r,

the

hori

zont

al d

ista

nce

betw

een

(1 an

d f

is a

lway

s gr

eate

r th

an t

he

dist

ance

bet

wee

n 11

0 an

d T

hese

tw

o di

stan

ces

wou

ld b

e eq

ual

only

if th

e sl

ope

of

the

bubb

le e

ater

wer

e 45

de

gree

s, w

hich

is n

ot p

ossi

ble.

*1

N

ote

that

at

Il

the

smoo

th p

astin

g (o

r no

—ar

bitr

age)

con

ditio

ns

(lO

a—d)

are

not s

atis

fied

. A

t Il

l in

Fig

ure

la th

e sm

ooth

pas

ting

cond

ition

s ar

e sa

tisfi

ed a

nd t

he

expe

cted

ra

te o

f cha

nge

of th

e ex

chan

ge r

ate

is n

egat

ive

(Ili

is to

the

righ

t of

the

45

line

thro

ugh

the

orig

in).

Il

l is

the

refo

re

cons

iste

nt w

ith c

redi

ble

inte

rven

tion

to

prev

ent

s fr

om ri

sing

abo

ve

s.d.

T

his

is n

ot th

e ca

se w

ith th

e la

rge b

ubbl

e sh

own

in

Figu

re l

b.

Ill

is to

the

left

of t

he 4

5* l

ine

thro

ugh

the

orig

in a

nd t

here

fore

rep

rese

nts

a po

sitiv

e ex

pect

ed

rate

of c

hang

e of

the

exc

hang

e ra

te,

inco

nsis

tent

w

ith

a cr

edib

le

defe

nse

of th

e up

per

limit

of th

e ta

rget

zon

e. In

this

cas

e th

e in

terv

entio

n rul

e le

ads

to

the

follo

win

g sc

enar

io.

From

Il

l a

one—

off

disc

rete

(st

ock-

shif

t) in

crea

se i

n f

brin

gs

the

syst

em to

11u

' tha

t is

the

poi

nt [

st,

su],

an a

rbitr

arily

sm

all

dist

ance

to th

e ri

ght

of t

he in

ters

ectio

n of

s =

an

d th

e 45

0 lin

e th

roug

h th

e or

igin

. Si

nce

s is

kep

t

cons

tant

at

s =

8n'

ther

e ar

e no

arb

itrag

e pro

fits

. Fr

om 1

l the

syst

em, w

ith A

1 an

d

A2

now

def

ined

by

the

one—

side

d 's

moo

th p

astin

g' c

ondi

tions

giv

en in

(lla

,b),

can

now

agai

n m

ove i

nto

the

inte

rior

of

the

targ

et z

one.

In F

igui

e lb

, the

gra

ph o

f s w

ith A

1 an

d A

2 de

term

ined

by

(ha)

and

(lib

) an

d B

= B

u de

note

d s'

, coi

ncid

es w

ith t

he b

ubbl

e ea

ter

of B

u Fo

r a

slig

htly

larg

er

valu

e of

B

, the

gra

ph o

f s

with

A

1 an

d A

2 de

term

ined

by

tbe

one

-sid

ed s

moo

th

past

ing

cond

ition

s (ha

) and

(lib

) is

deno

ted

s' '.

A la

rger

valu

e of

s

yiel

ds s

'' A

s B

go

es to

infi

nity

the

gra

ph o

f s

appr

oach

es a

vert

ical

line

thro

ugh

t1u

—17

—

Not

e th

at,

by c

onst

ruct

ion,

we

alw

ays

have

a l

ocal

max

imum

at t

he ta

ngen

cy

poin

t f2

(fo

r fin

ite v

alue

s of

B).

For

pos

itive

unr

egul

ated

real

izat

ions

of

f, s

tand

ard

infi

nite

sim

al re

flec

tion

stop

s th

e re

gula

ted

valu

e of

f f

rom

ris

ing

beyo

nd s.

For

nega

tive r

ealiz

atio

ns of

the

unre

gula

ted f

, the

sys

tem

mov

es (

give

n B

) in

to th

e in

teri

or

of th

e ta

rget

zon

e.

As

in t

he c

ase

of a

sm

all

bubb

le,

a va

riat

ion

in t

he v

alue

of th

e

bubb

le i

n th

e in

teri

or o

f the

targ

et zo

ne re

pres

ents

a ve

rtic

al d

ispl

acem

ent o

f the

gra

ph

of th

e ex

chan

ge r

ate

(with

con

stan

t val

ues

of A

1 an

d A

2).

With

a l

arge

bub

ble,

the

shap

e of

the

grap

h ch

ange

s ev

ery

time

the

exch

ange

rat

e vi

sits

the

bou

ndar

ies a

t a n

ew

valu

e of

B.

Sinc

e th

e bu

bble

gro

ws

expo

nent

ially

(i

n ex

pect

atio

n)

we

expe

ct

mor

e fr

eque

nt

inte

rven

tions

at

the

uppe

r (l

ower

) bo

unda

ry if

the

cur

rent

va

lue

of t

be b

ubbl

e is

posi

tive

(neg

ativ

e) th

an w

ith

a ze

ro b

ubbl

e.

We

cons

ider

the

se r

esul

ts

to b

e qu

ite

intu

itive

. O

ne

wou

ld e

xpec

t an

exc

hang

e ra

te s

ubje

ct t

o a

posi

tive

and

grow

ing

(in

expe

ctat

ion)

bub

ble

to s

pend

a lo

t of

time

at th

e up

per

boun

dary

of

the

targ

et z

one,

with

the

aut

hori

ties

inte

rven

ing

to c

ount

erac

t not

onl

y th

e un

regu

late

d fu

ndam

enta

l

but a

lso

the

bubb

le.

It i

s ap

pare

nt t

hat

whe

n s

reac

hes

5u w

ith

a la

rge

bubb

le,

the

stoc

k—sh

ift

incr

ease

in

f m

ust t

ake

the

syst

em to

a p

ositi

on s

tric

tly t

o th

e ri

ght

of t

he 4

50 l

ine

thro

ugh

the

orig

in.

On

the

450

line

the

expe

cted

rat

e of

dep

reci

atio

n is

zero

. If

we

impo

se t

he 's

moo

th p

astin

g' c

ondi

tions

w

hen

f =

= 5u

' (sm

all)

posi

tive r

ealiz

atio

ns o

f

incr

emen

ts

in t

he u

nreg

ulat

ed f

unda

men

tal

will

be

offs

et w

ith i

nfin

itesi

mal

refl

ectin

g

inte

rven

tions

. Neg

ativ

e re

aliz

atio

ns o

f df

wou

ld b

ring

the

sys

tem

to th

e le

ft o

f the

450

line

thro

ugh

the

orig

in,

that

is

to a

poi

nt w

ith a

pos

itive

exp

ecte

d ra

te o

f ch

ange

of s

.

Thi

s is

of

cour

se i

ncon

sist

ent w

ith

a cr

edib

le d

efen

se o

f the

tar

get

zone

. If

pri

vate

agen

ts

belie

ved

that

the

aut

hori

ties

wer

e st

abili

zing

th

e ex

chan

ge

rate

at 'e