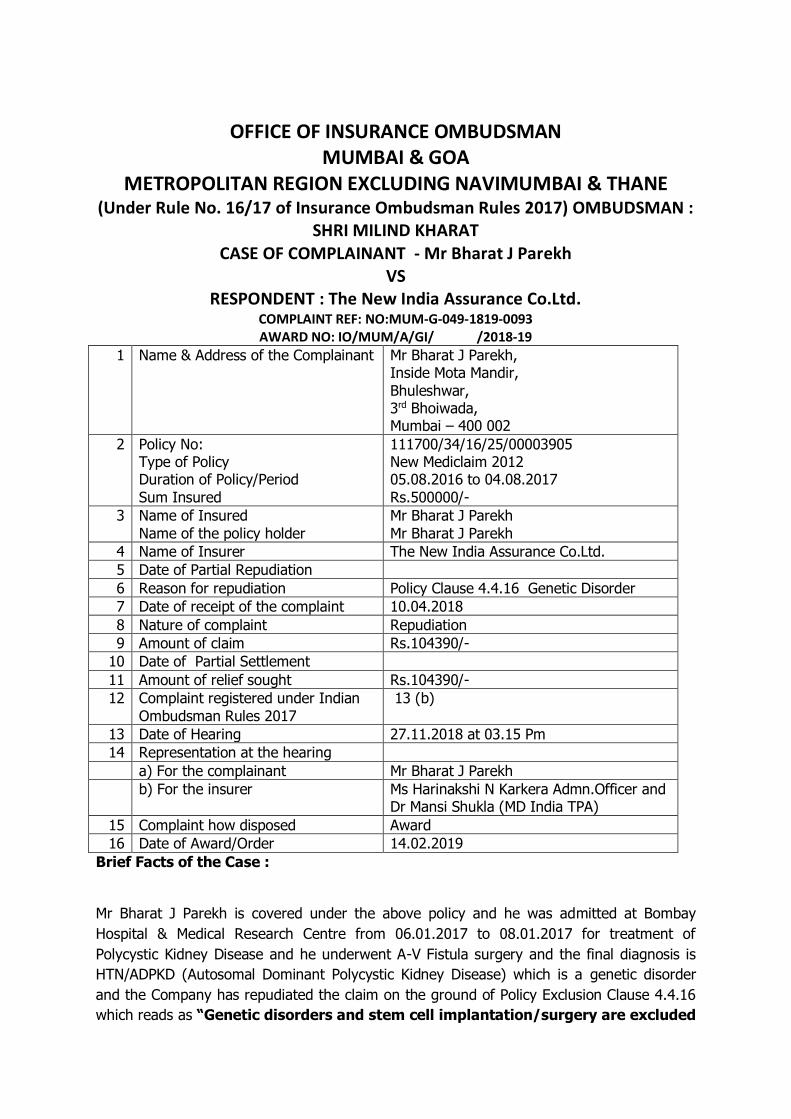

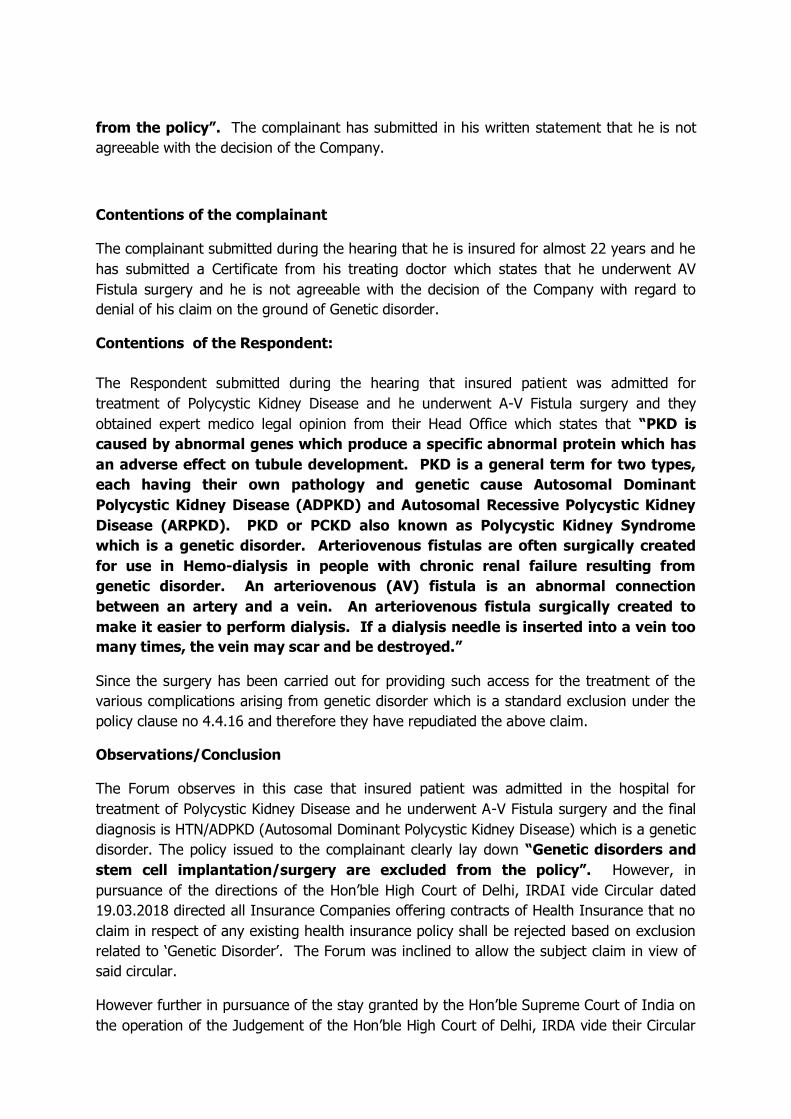

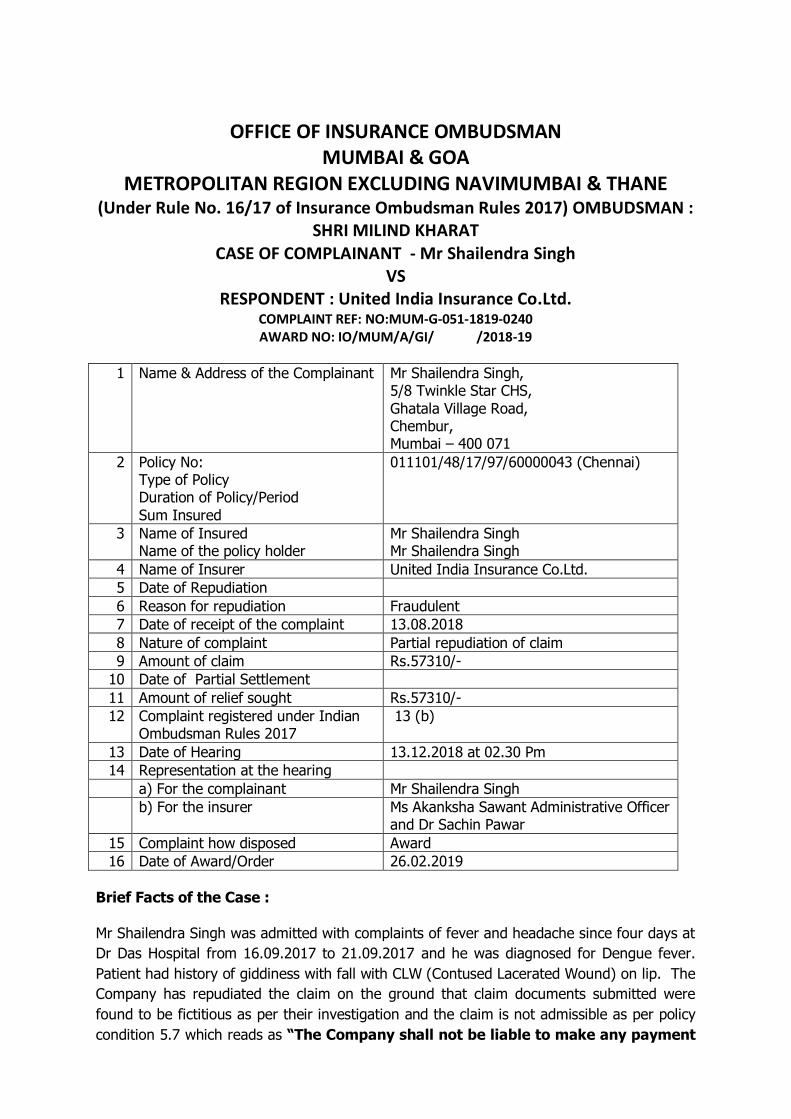

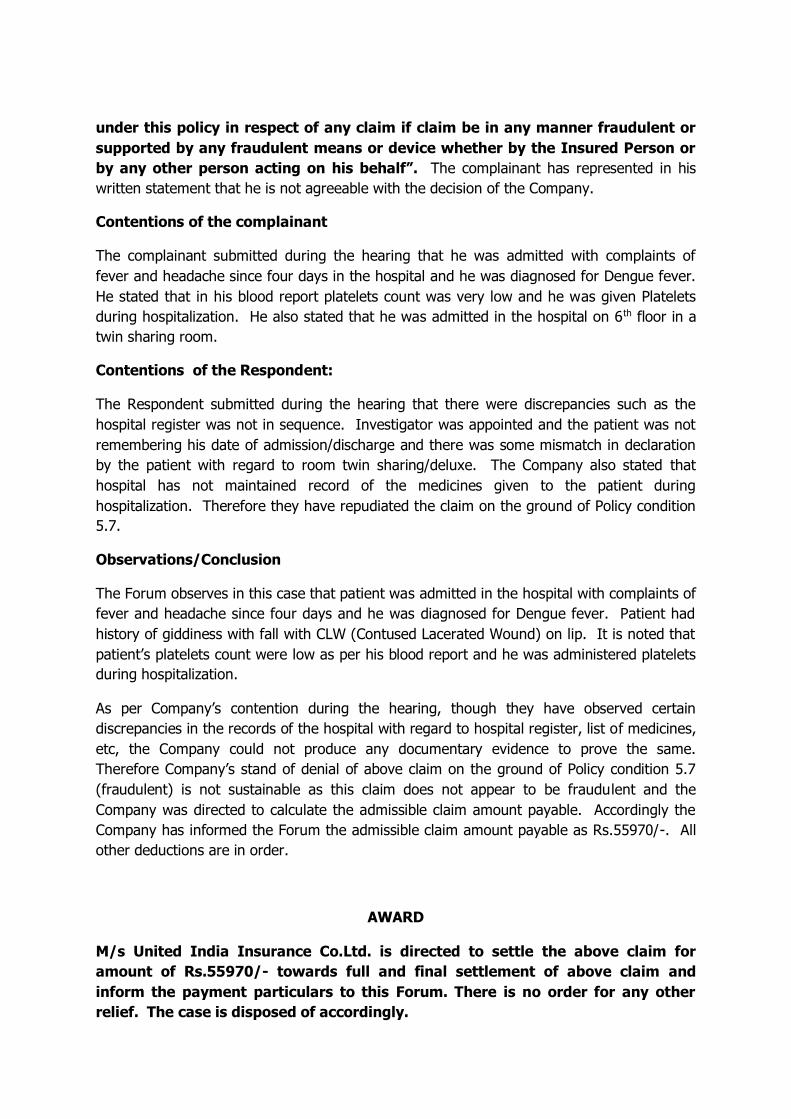

Embed Size (px)

Citation preview

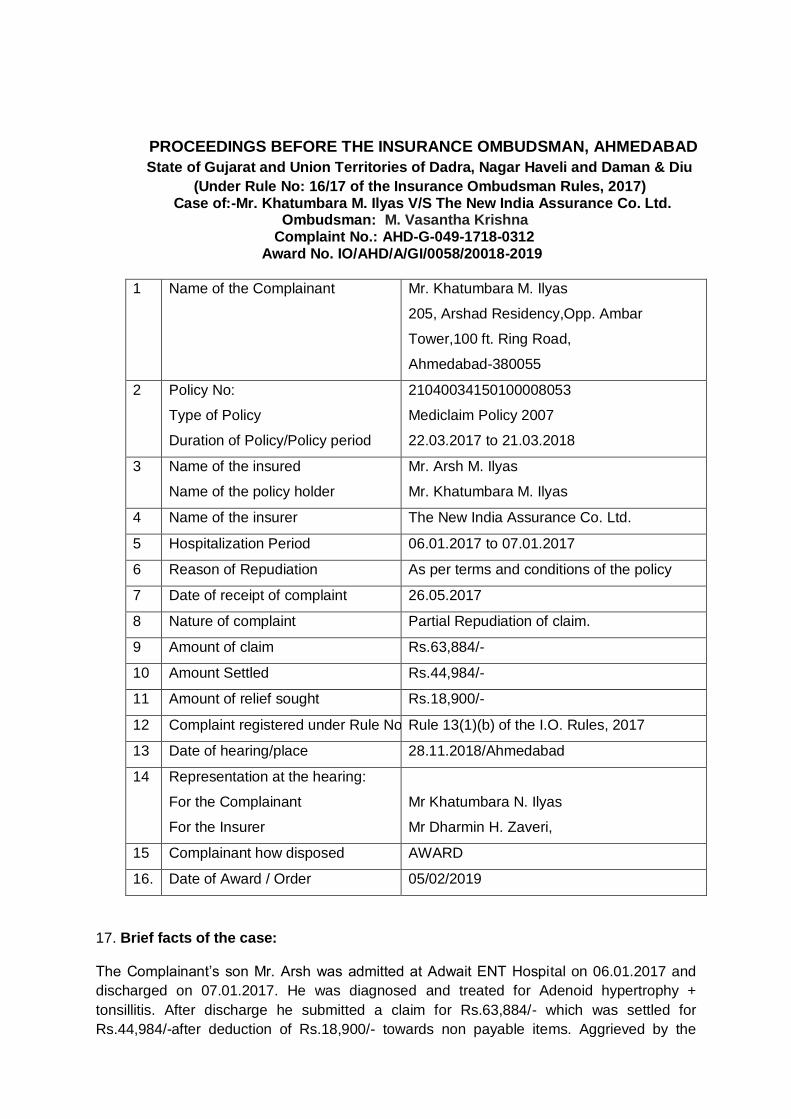

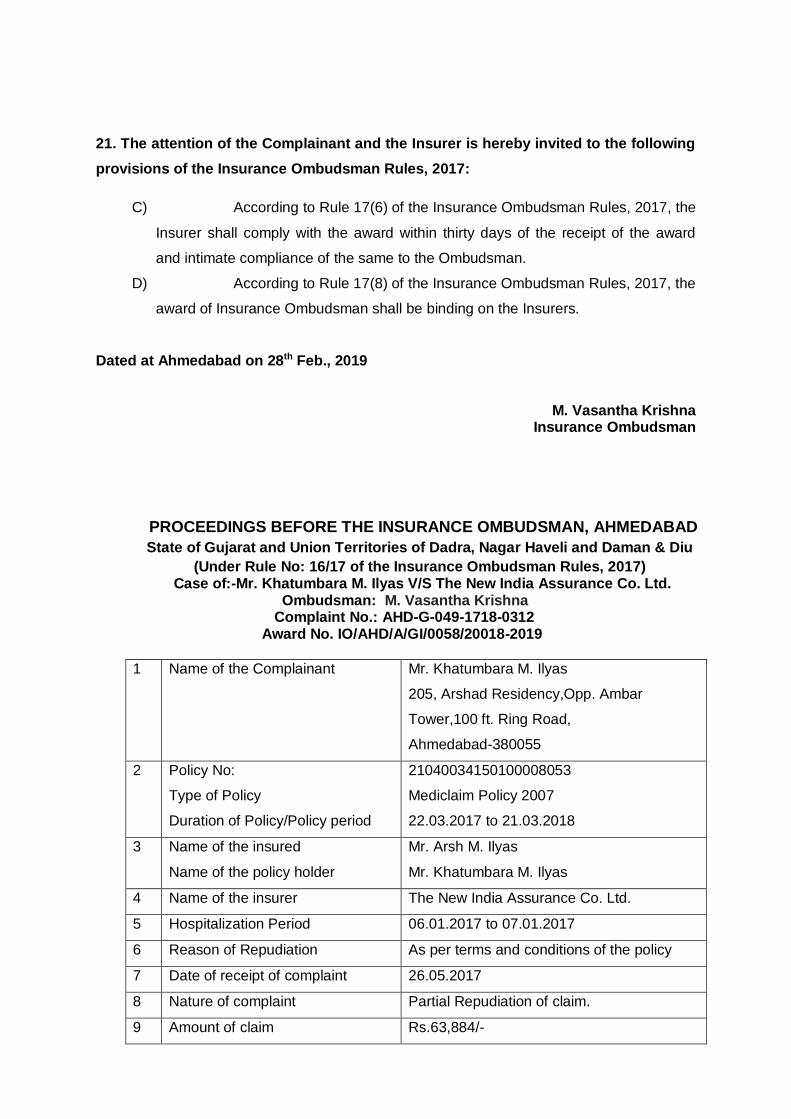

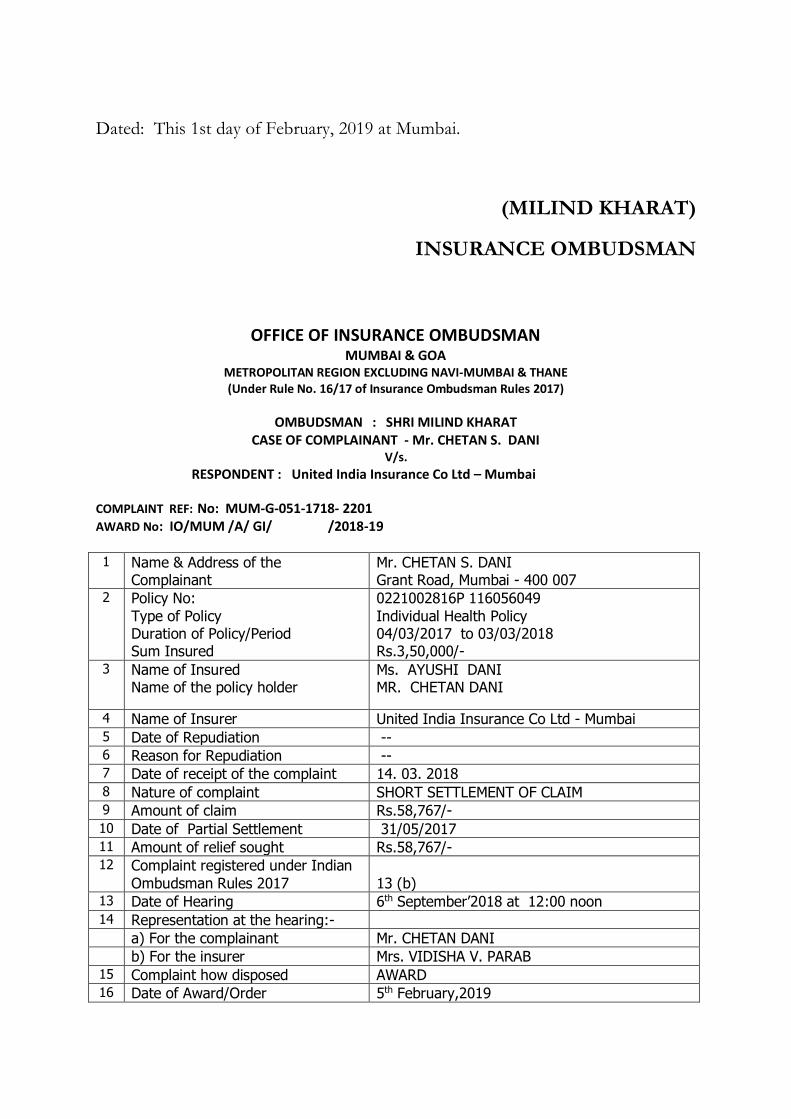

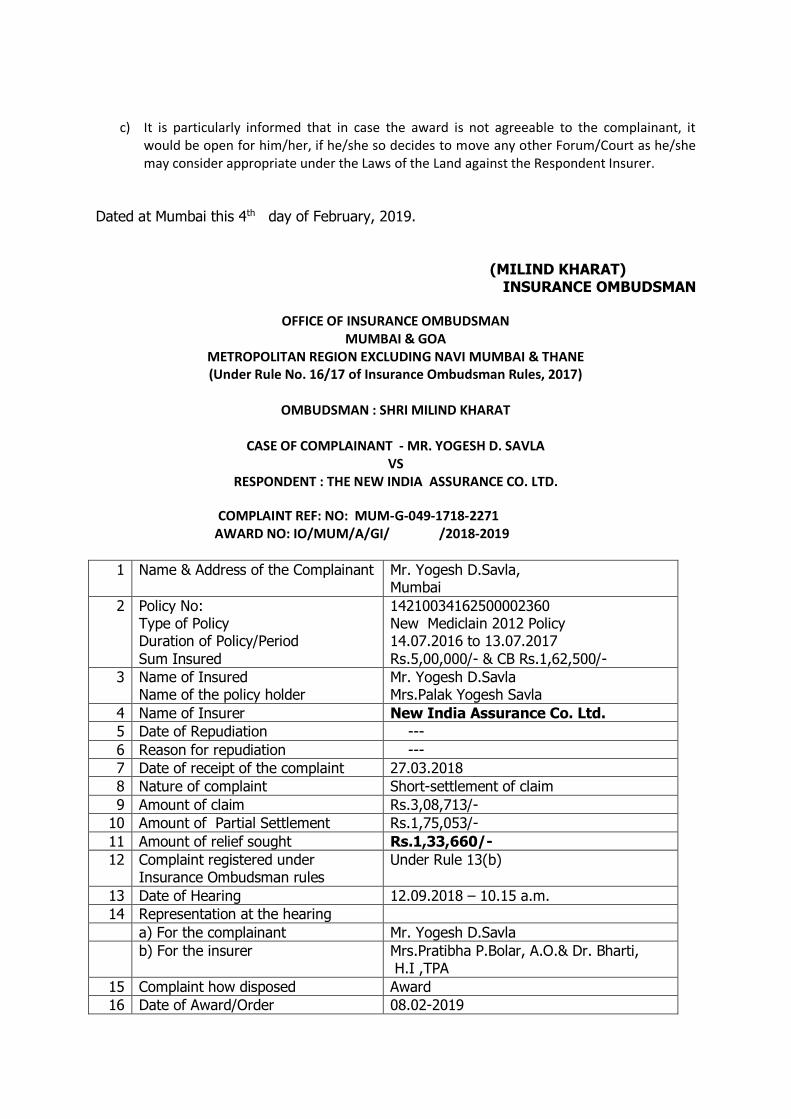

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Case of:-Mr. Khatumbara M. Ilyas V/S The New India Assurance Co. Ltd.

Ombudsman: M. Vasantha Krishna Complaint No.: AHD-G-049-1718-0312

Award No. IO/AHD/A/GI/0058/20018-2019

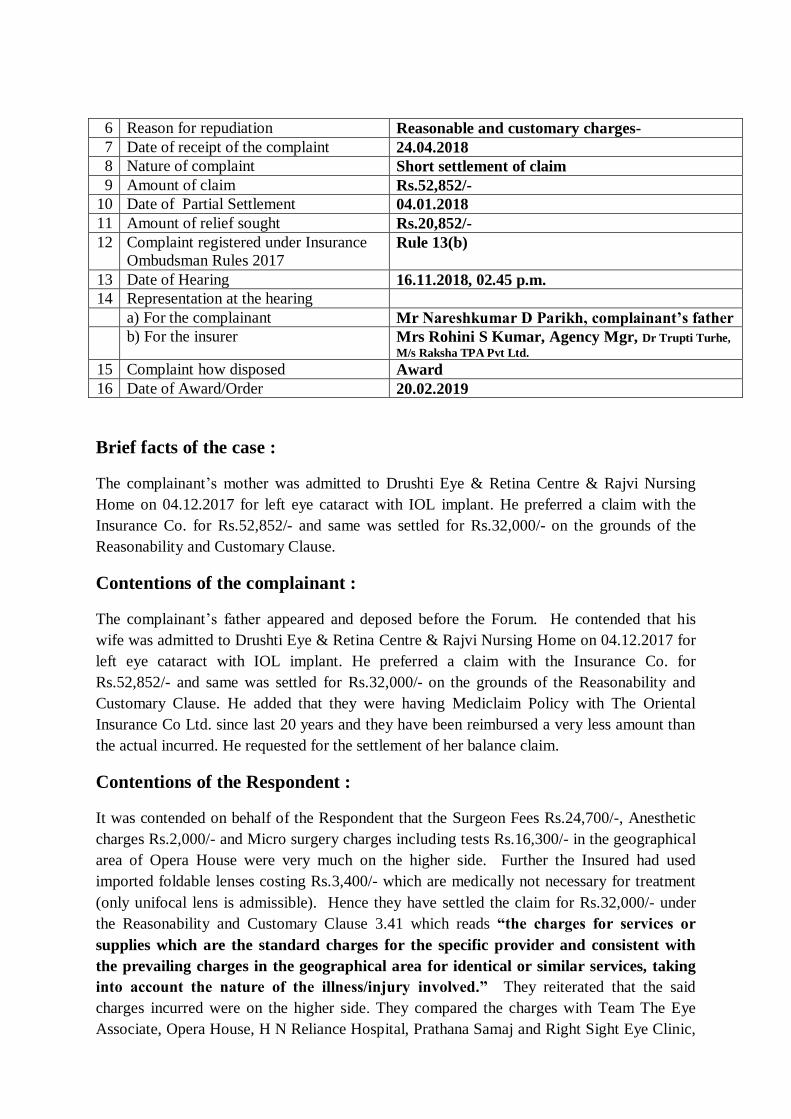

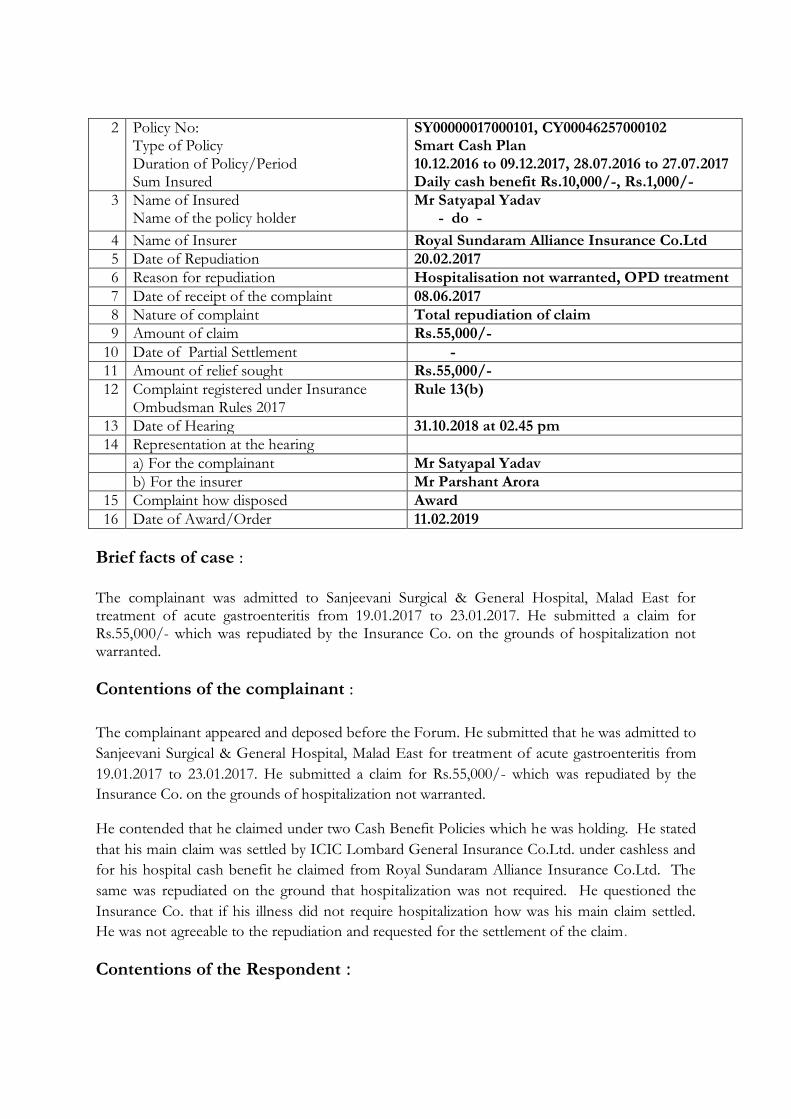

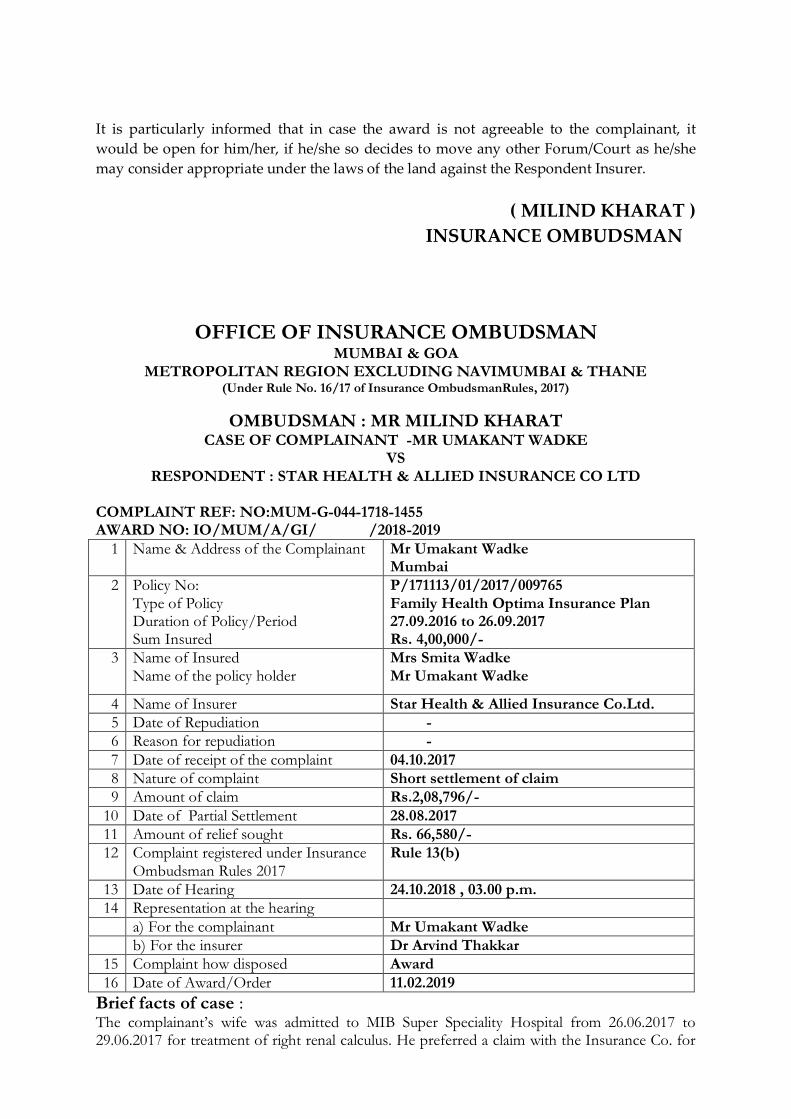

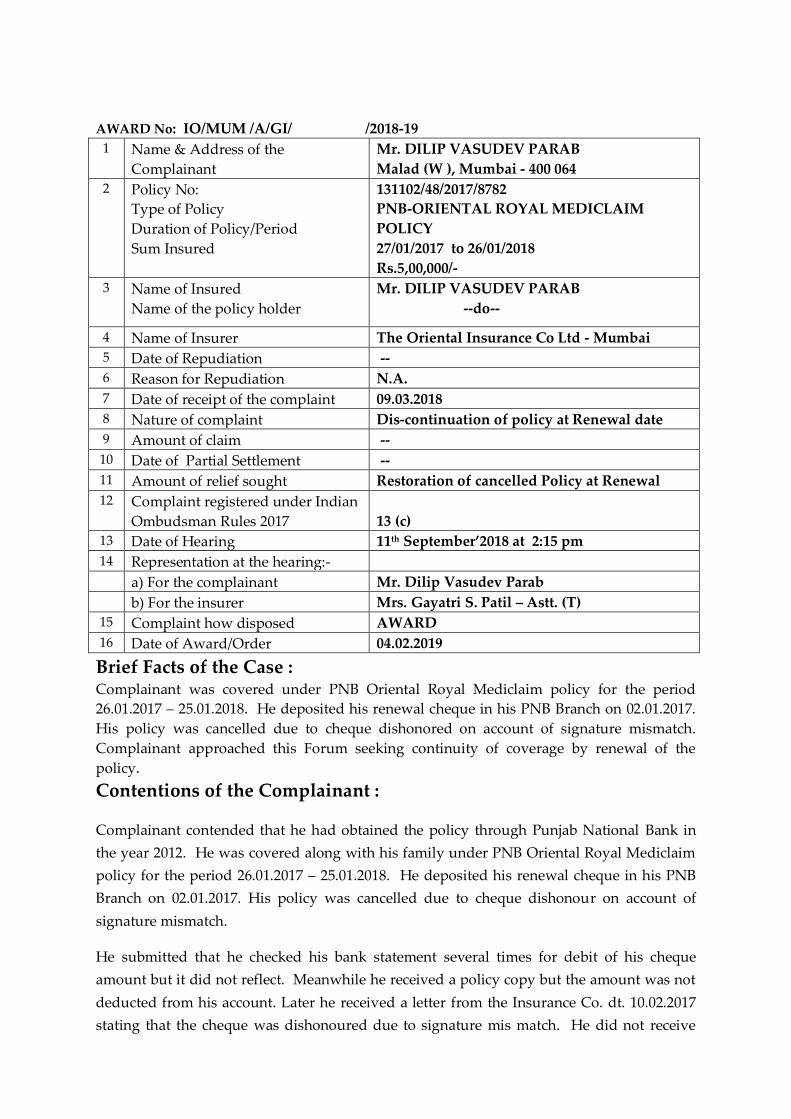

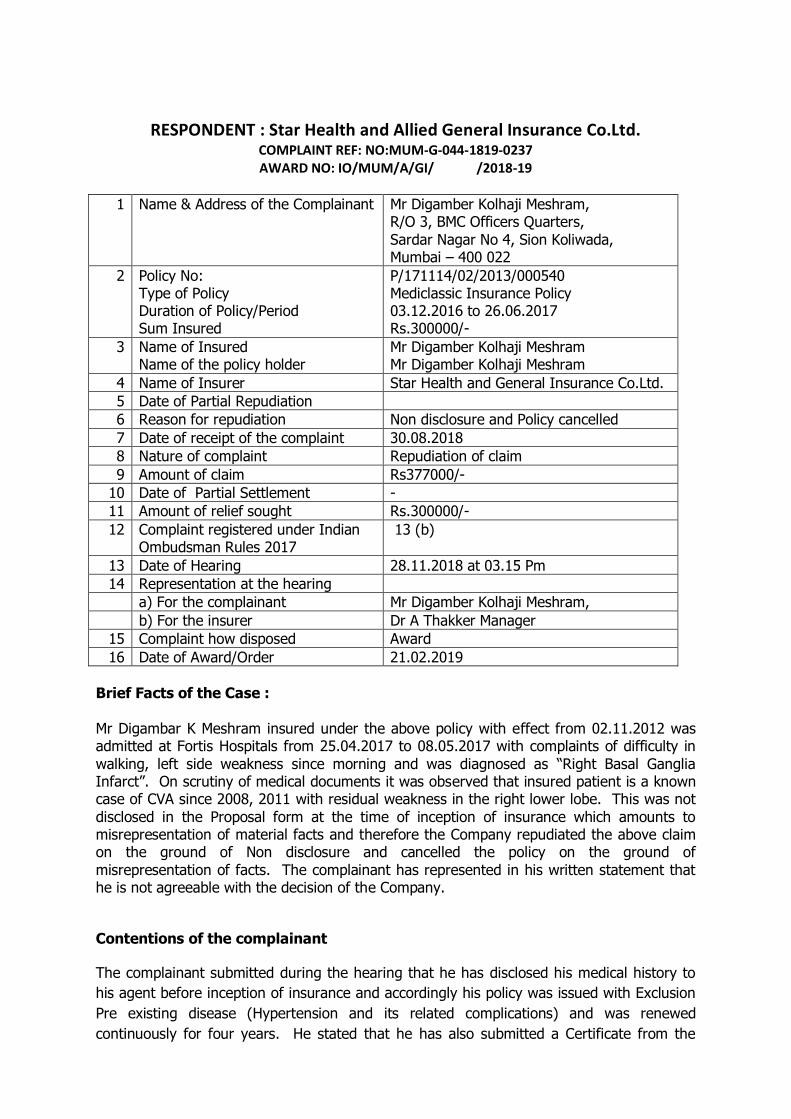

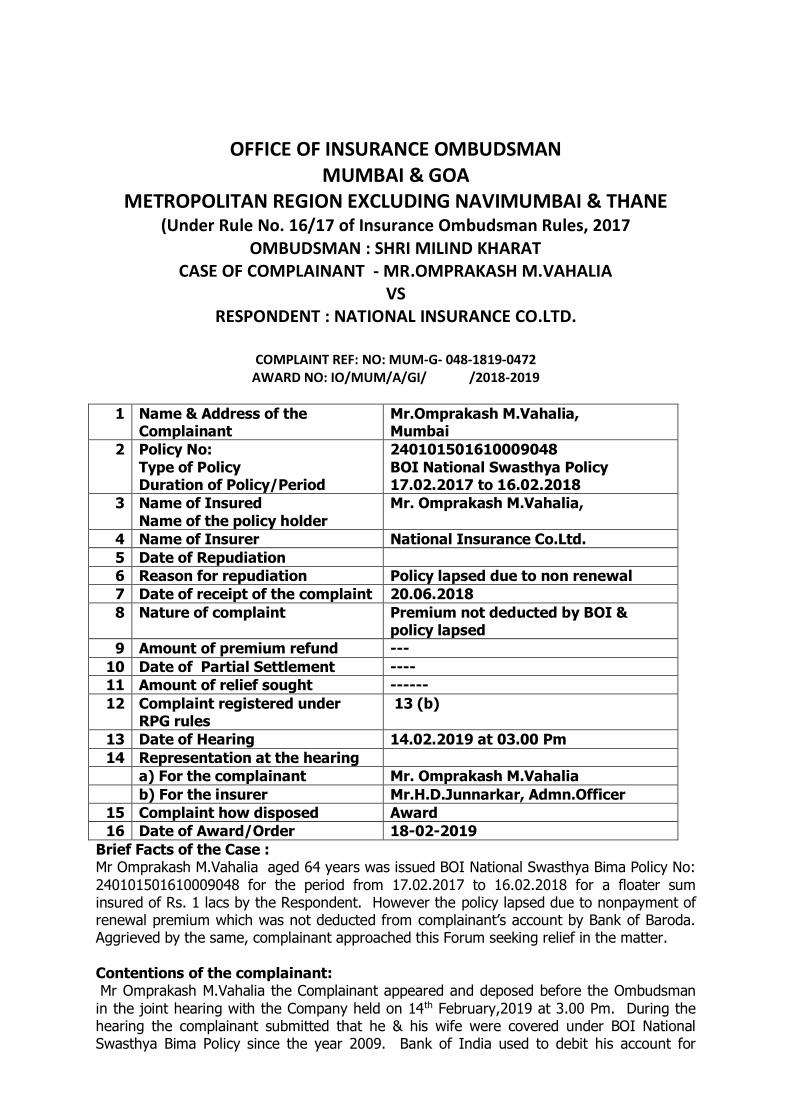

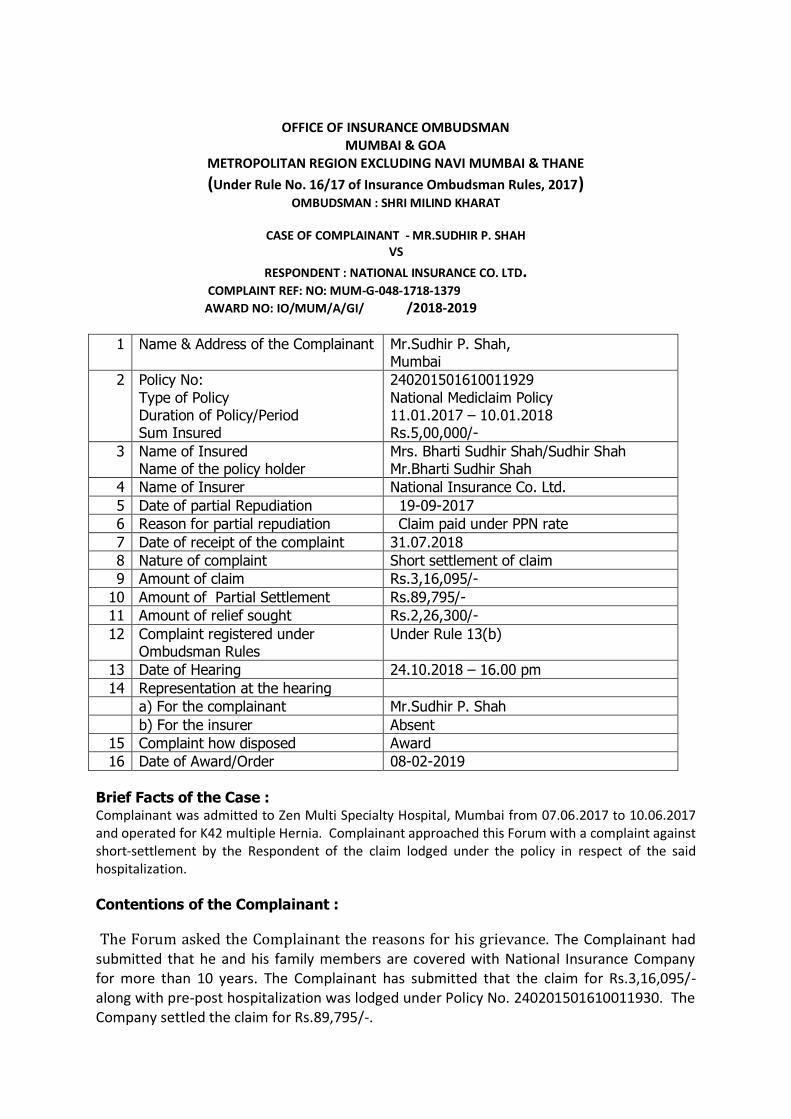

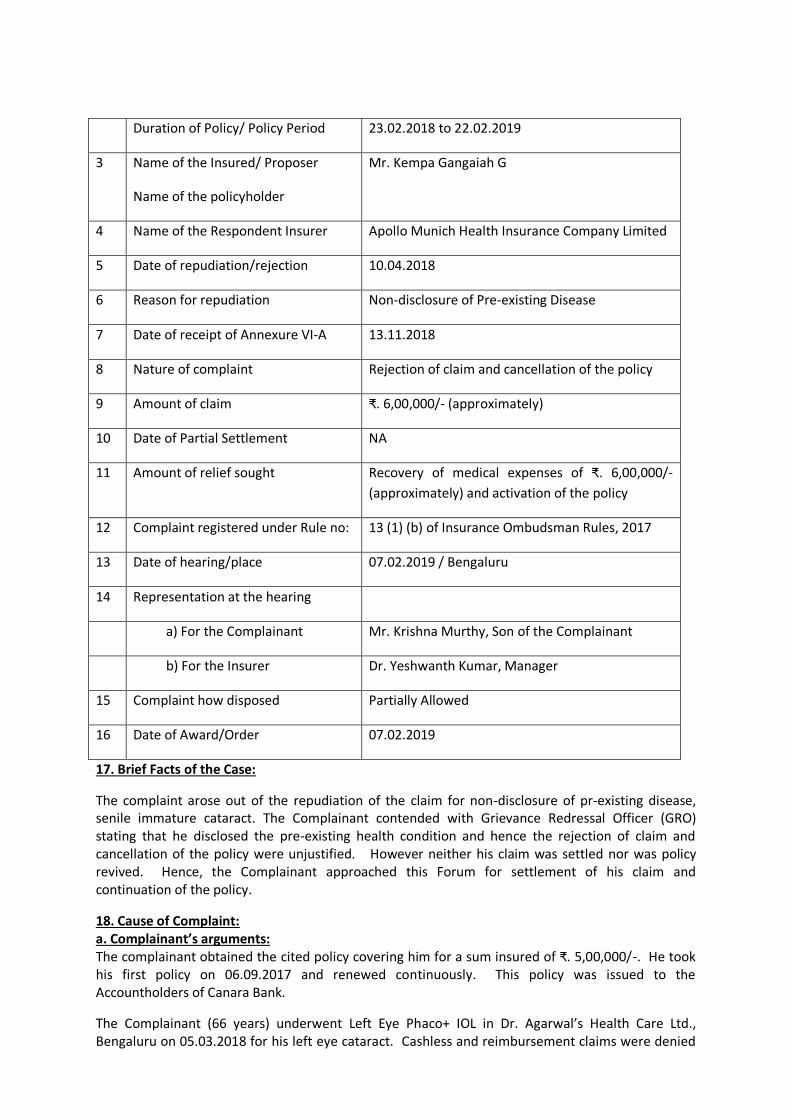

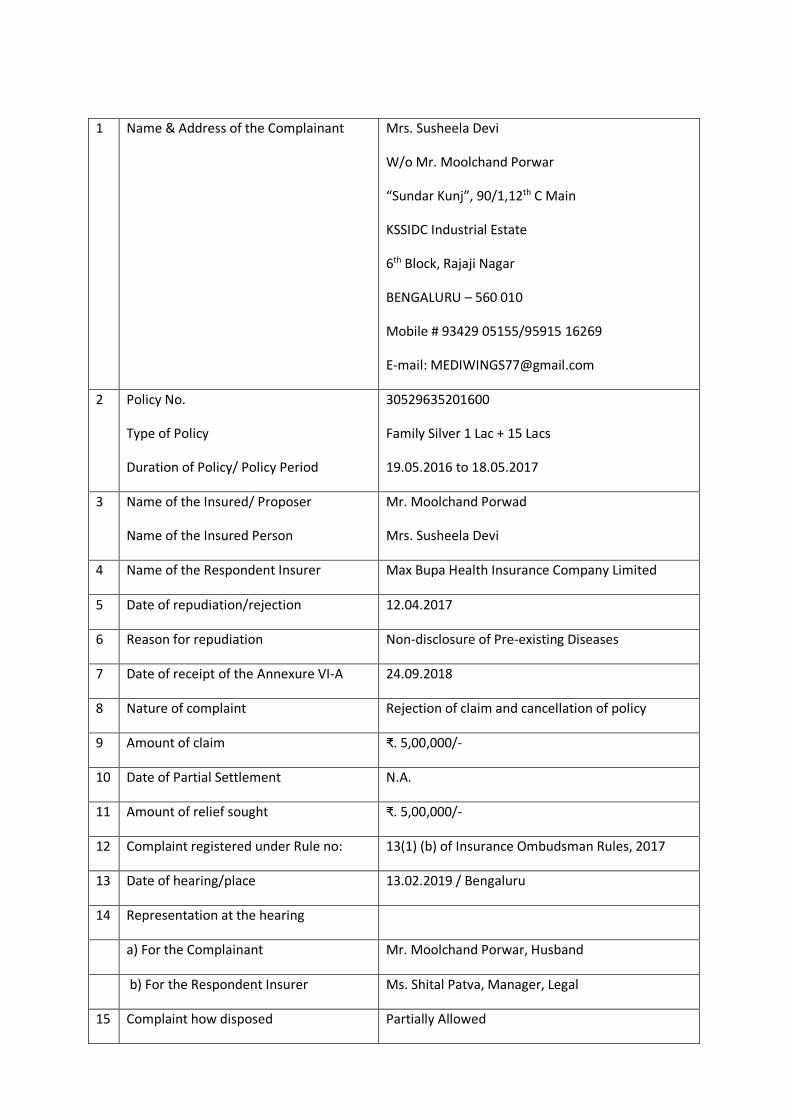

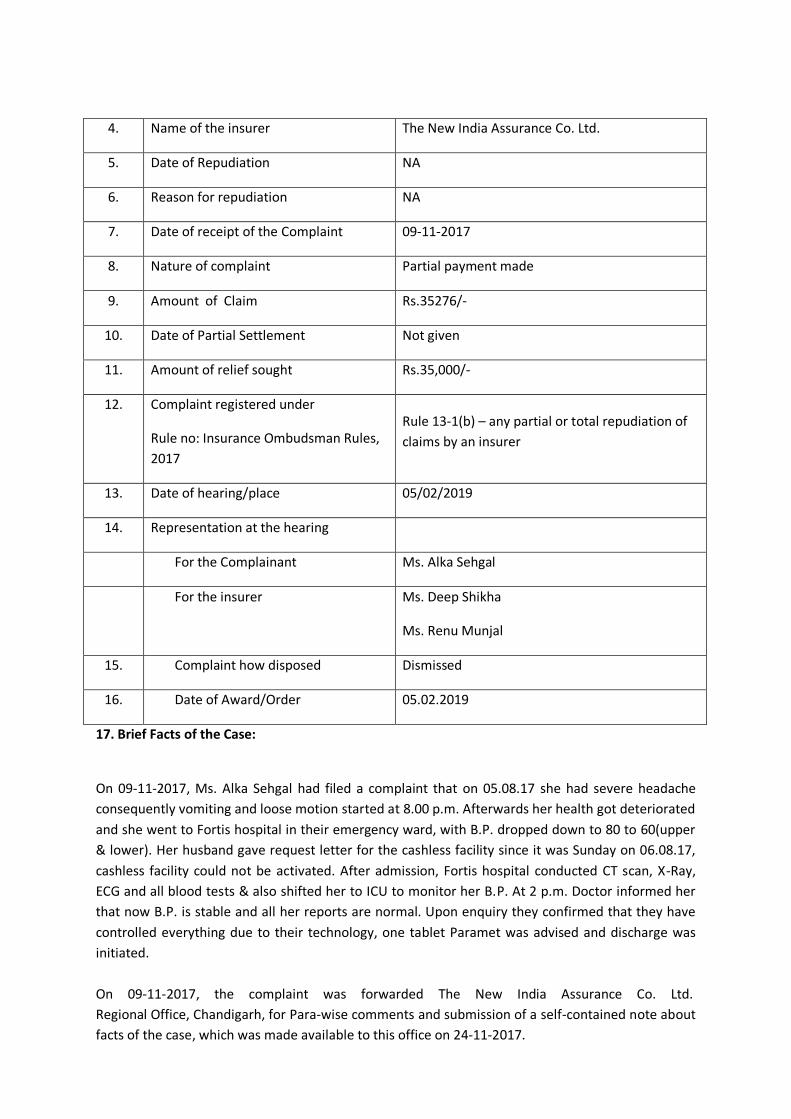

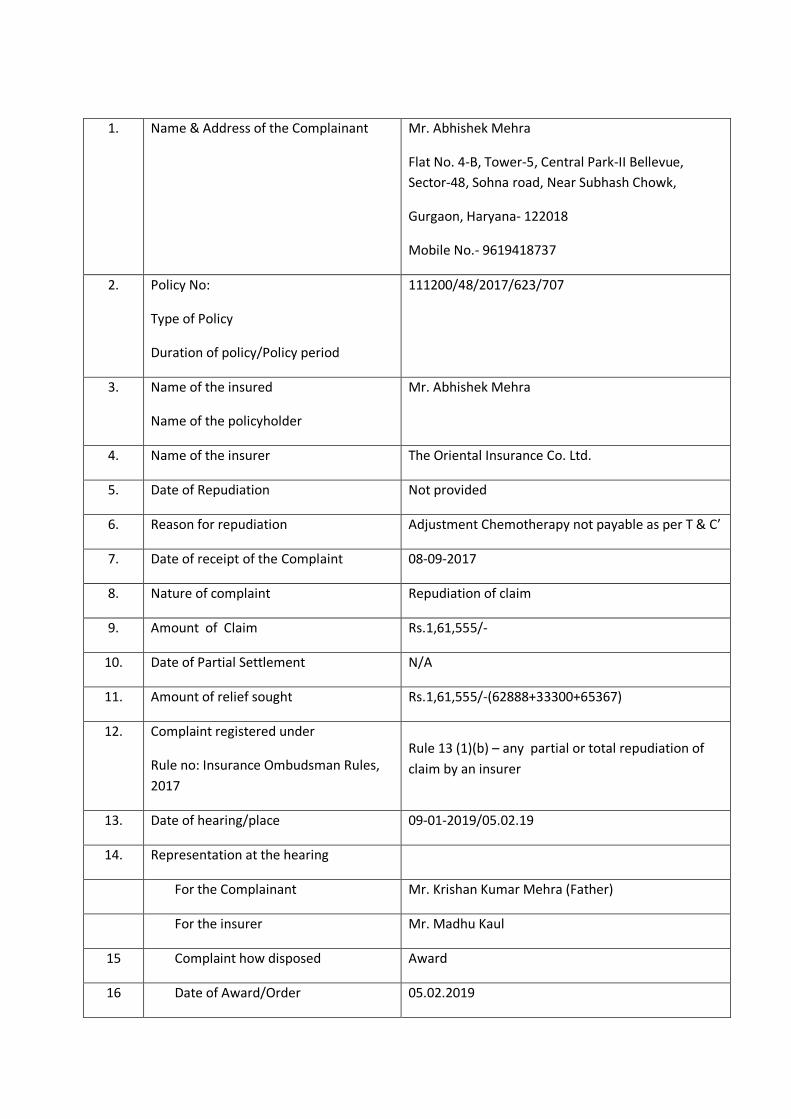

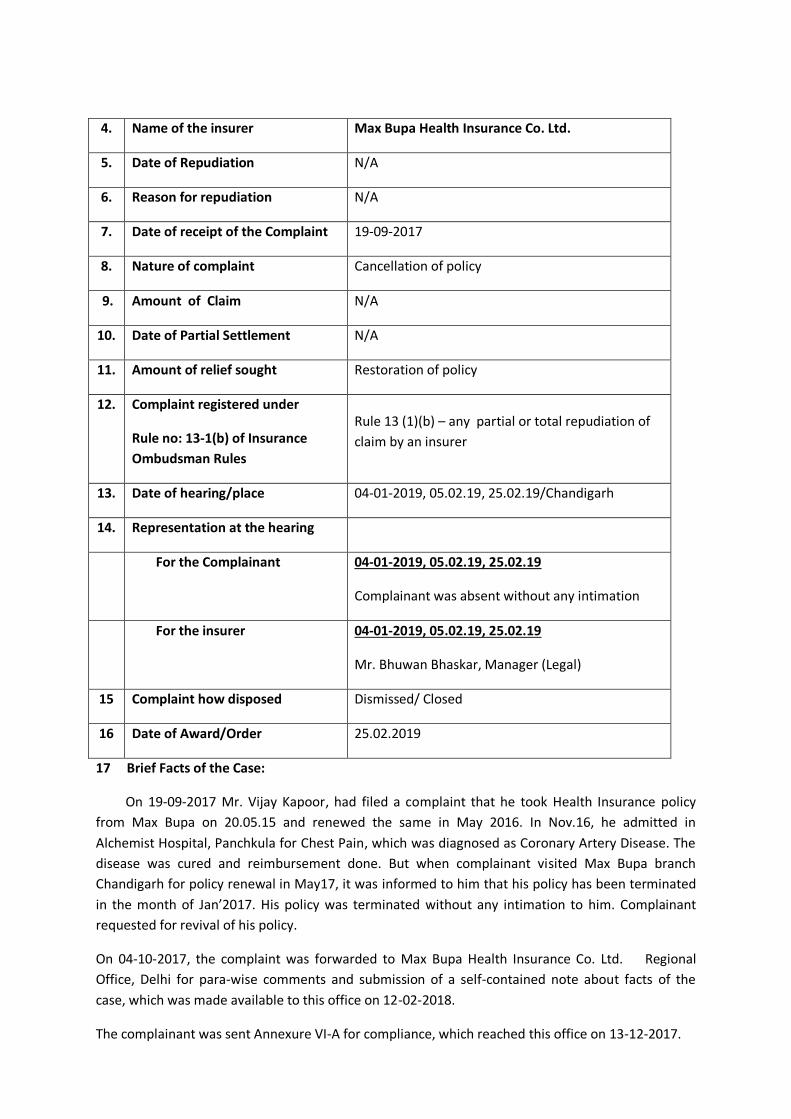

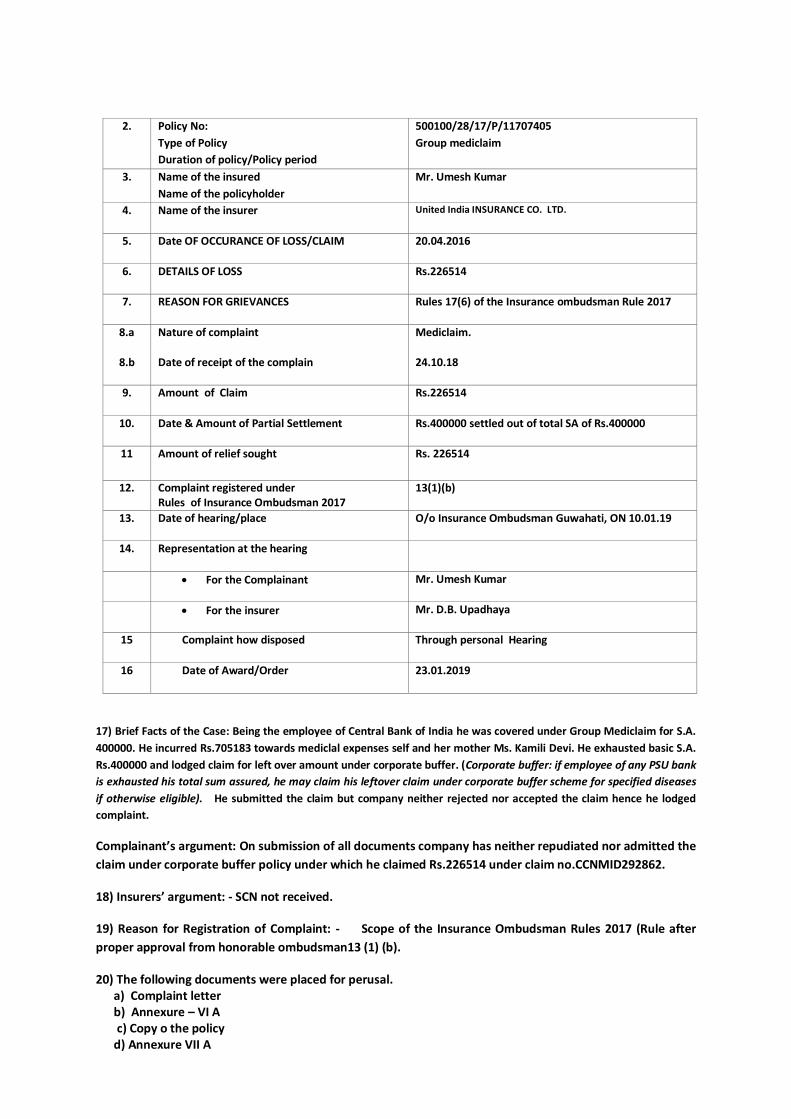

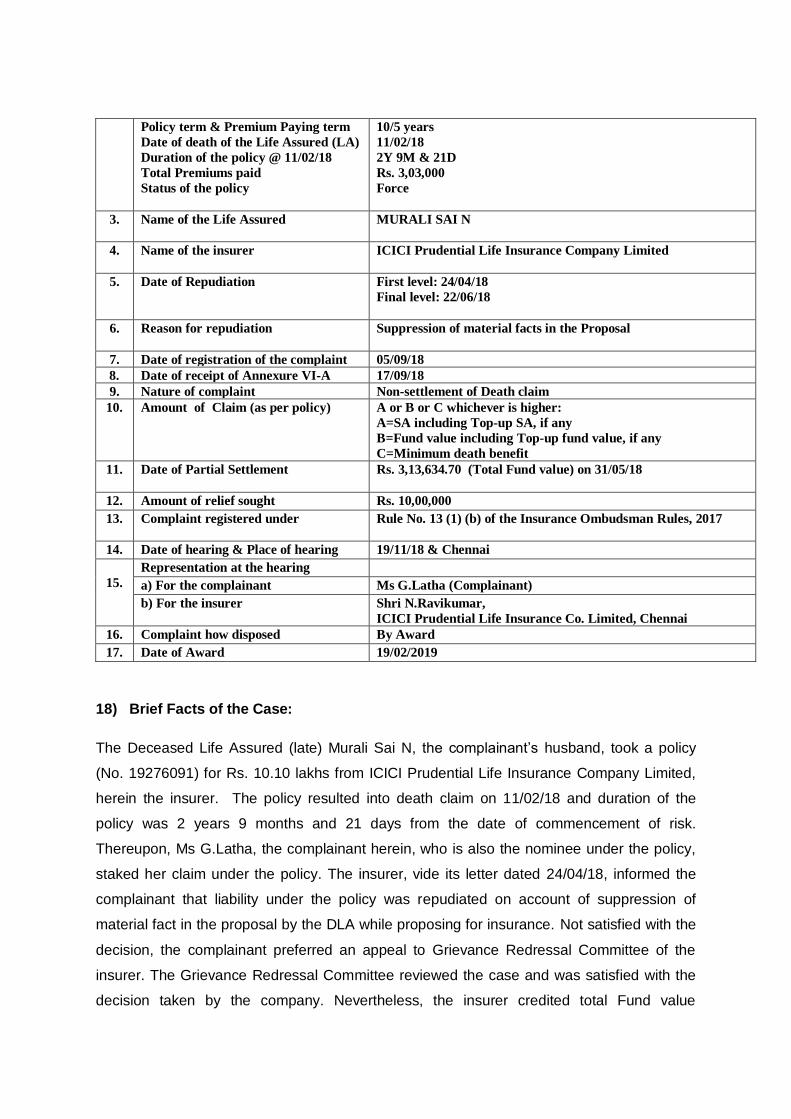

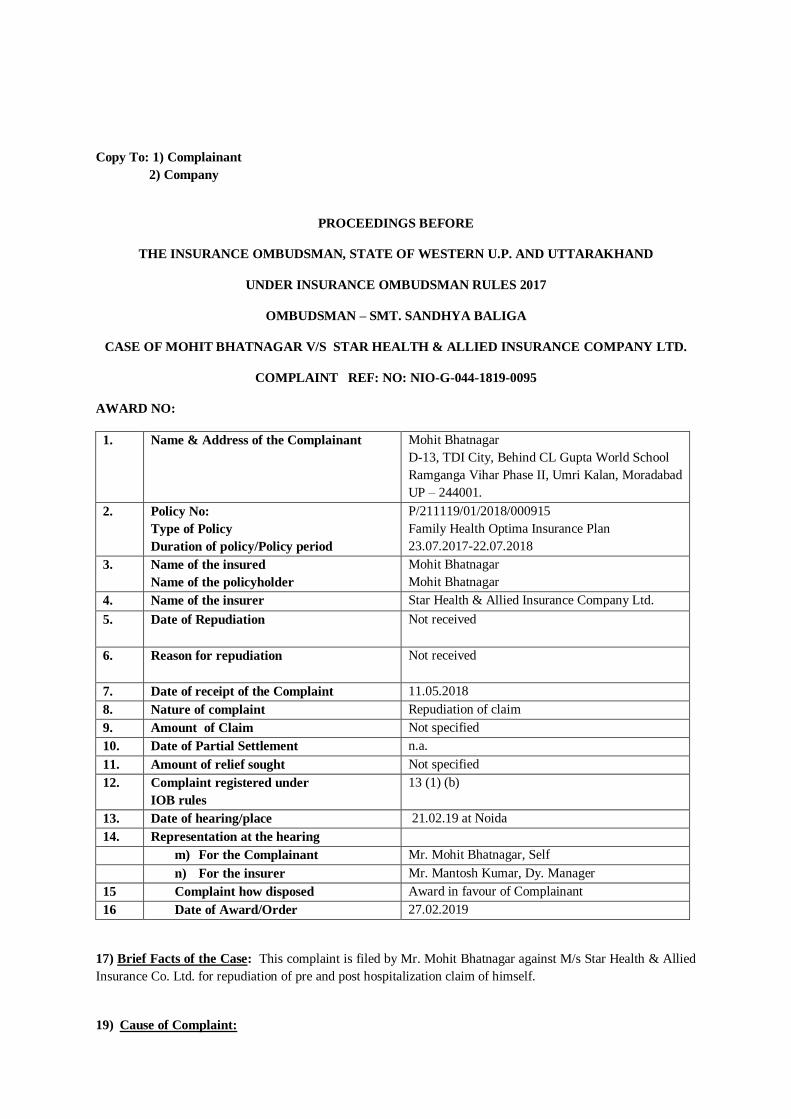

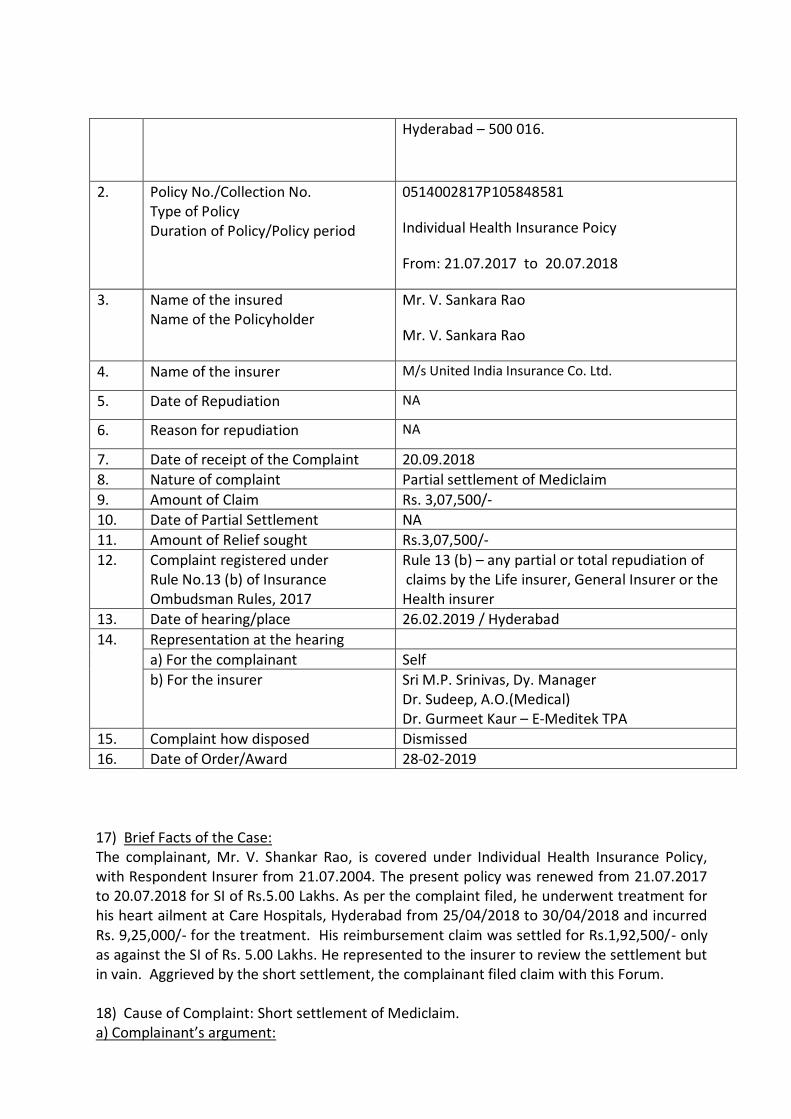

1 Name of the Complainant Mr. Khatumbara M. Ilyas

205, Arshad Residency,Opp. Ambar

Tower,100 ft. Ring Road,

Ahmedabad-380055

2 Policy No:

Type of Policy

Duration of Policy/Policy period

21040034150100008053

Mediclaim Policy 2007

22.03.2017 to 21.03.2018

3 Name of the insured

Name of the policy holder

Mr. Arsh M. Ilyas

Mr. Khatumbara M. Ilyas

4 Name of the insurer The New India Assurance Co. Ltd.

5 Hospitalization Period 06.01.2017 to 07.01.2017

6 Reason of Repudiation As per terms and conditions of the policy

7 Date of receipt of complaint 26.05.2017

8 Nature of complaint Partial Repudiation of claim.

9 Amount of claim Rs.63,884/-

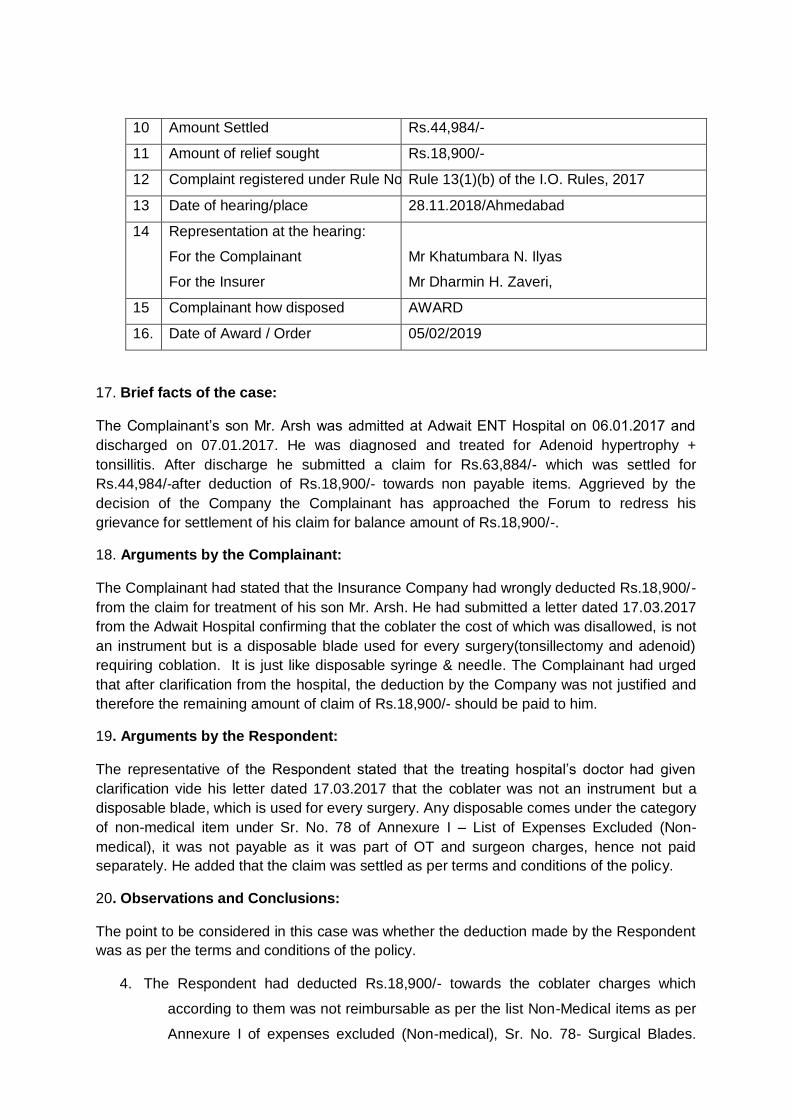

10 Amount Settled Rs.44,984/-

11 Amount of relief sought Rs.18,900/-

12 Complaint registered under Rule No. Rule 13(1)(b) of the I.O. Rules, 2017

13 Date of hearing/place 28.11.2018/Ahmedabad

14 Representation at the hearing:

For the Complainant

For the Insurer

Mr Khatumbara N. Ilyas

Mr Dharmin H. Zaveri,

15 Complainant how disposed AWARD

16. Date of Award / Order 05/02/2019

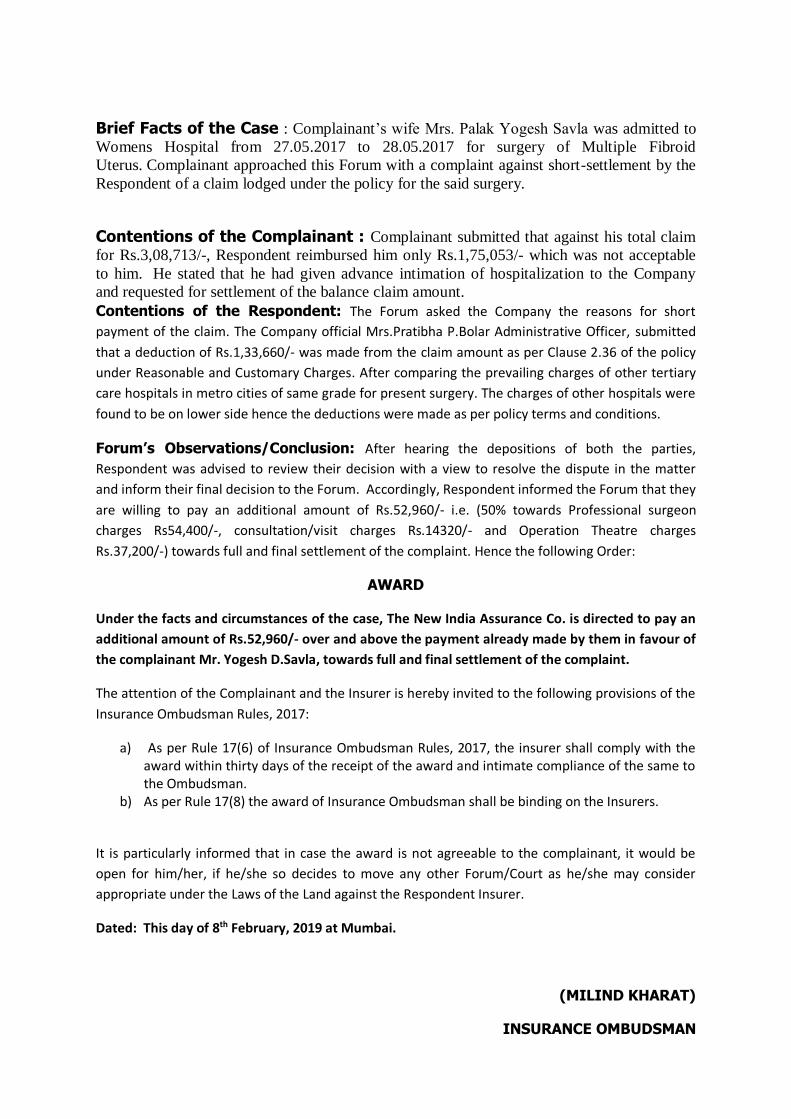

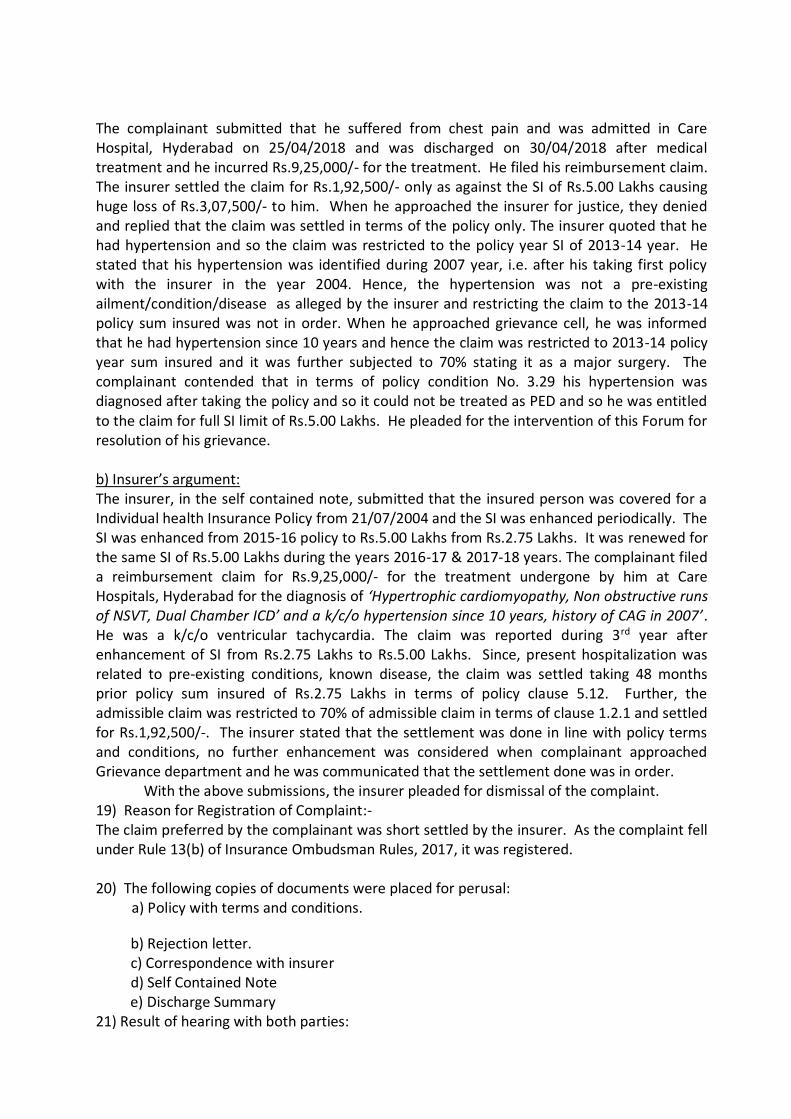

17. Brief facts of the case:

The Complainant’s son Mr. Arsh was admitted at Adwait ENT Hospital on 06.01.2017 and

discharged on 07.01.2017. He was diagnosed and treated for Adenoid hypertrophy +

tonsillitis. After discharge he submitted a claim for Rs.63,884/- which was settled for

Rs.44,984/-after deduction of Rs.18,900/- towards non payable items. Aggrieved by the

decision of the Company the Complainant has approached the Forum to redress his

grievance for settlement of his claim for balance amount of Rs.18,900/-.

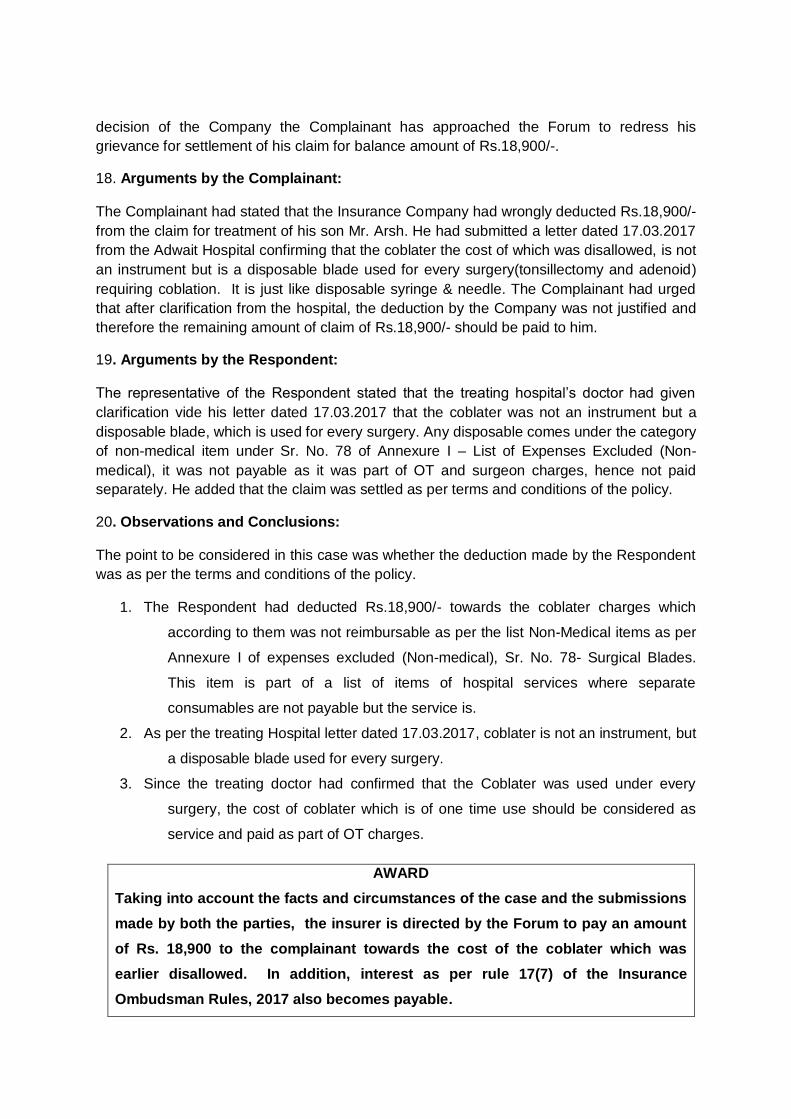

18. Arguments by the Complainant:

The Complainant had stated that the Insurance Company had wrongly deducted Rs.18,900/-

from the claim for treatment of his son Mr. Arsh. He had submitted a letter dated 17.03.2017

from the Adwait Hospital confirming that the coblater the cost of which was disallowed, is not

an instrument but is a disposable blade used for every surgery(tonsillectomy and adenoid)

requiring coblation. It is just like disposable syringe & needle. The Complainant had urged

that after clarification from the hospital, the deduction by the Company was not justified and

therefore the remaining amount of claim of Rs.18,900/- should be paid to him.

19. Arguments by the Respondent:

The representative of the Respondent stated that the treating hospital’s doctor had given

clarification vide his letter dated 17.03.2017 that the coblater was not an instrument but a

disposable blade, which is used for every surgery. Any disposable comes under the category

of non-medical item under Sr. No. 78 of Annexure I – List of Expenses Excluded (Non-

medical), it was not payable as it was part of OT and surgeon charges, hence not paid

separately. He added that the claim was settled as per terms and conditions of the policy.

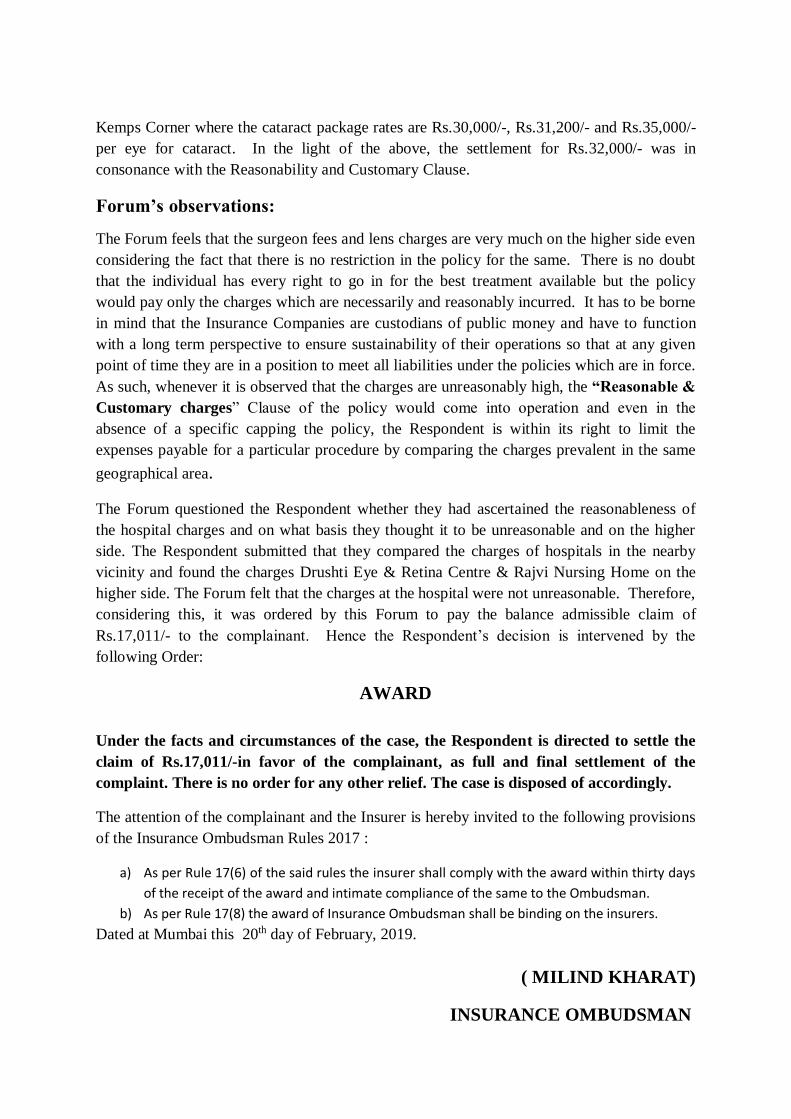

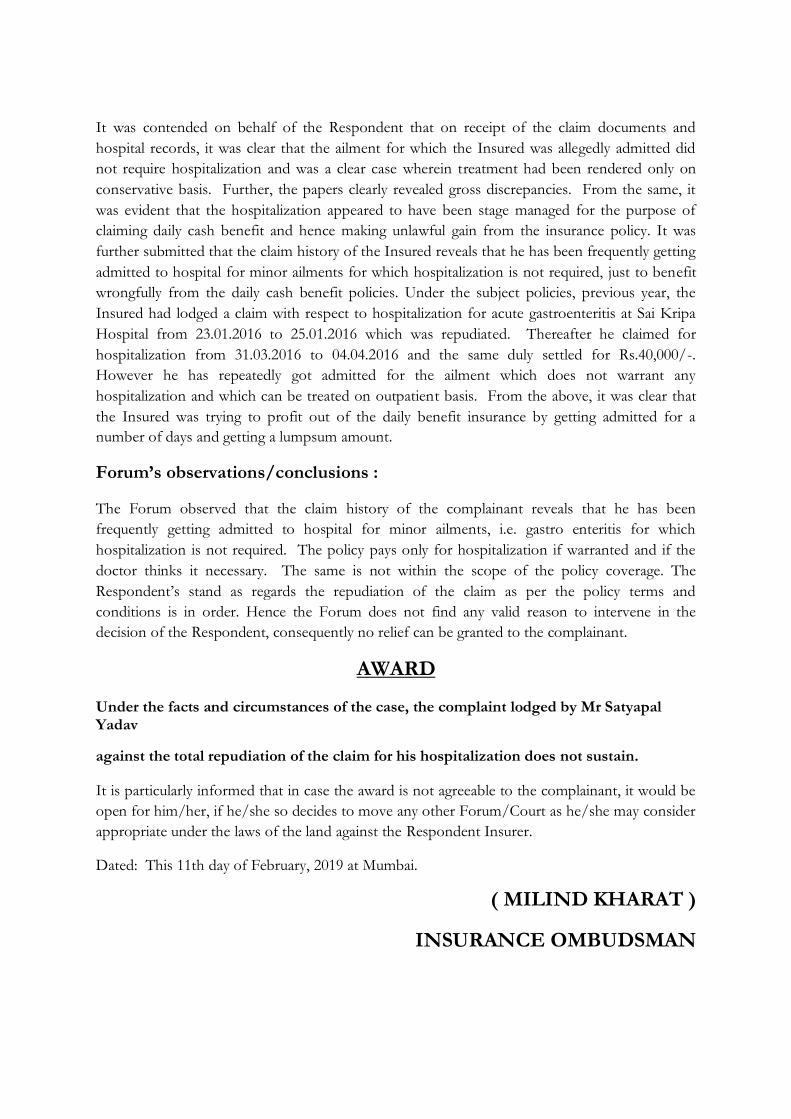

20. Observations and Conclusions:

The point to be considered in this case was whether the deduction made by the Respondent

was as per the terms and conditions of the policy.

1. The Respondent had deducted Rs.18,900/- towards the coblater charges which

according to them was not reimbursable as per the list Non-Medical items as per

Annexure I of expenses excluded (Non-medical), Sr. No. 78- Surgical Blades.

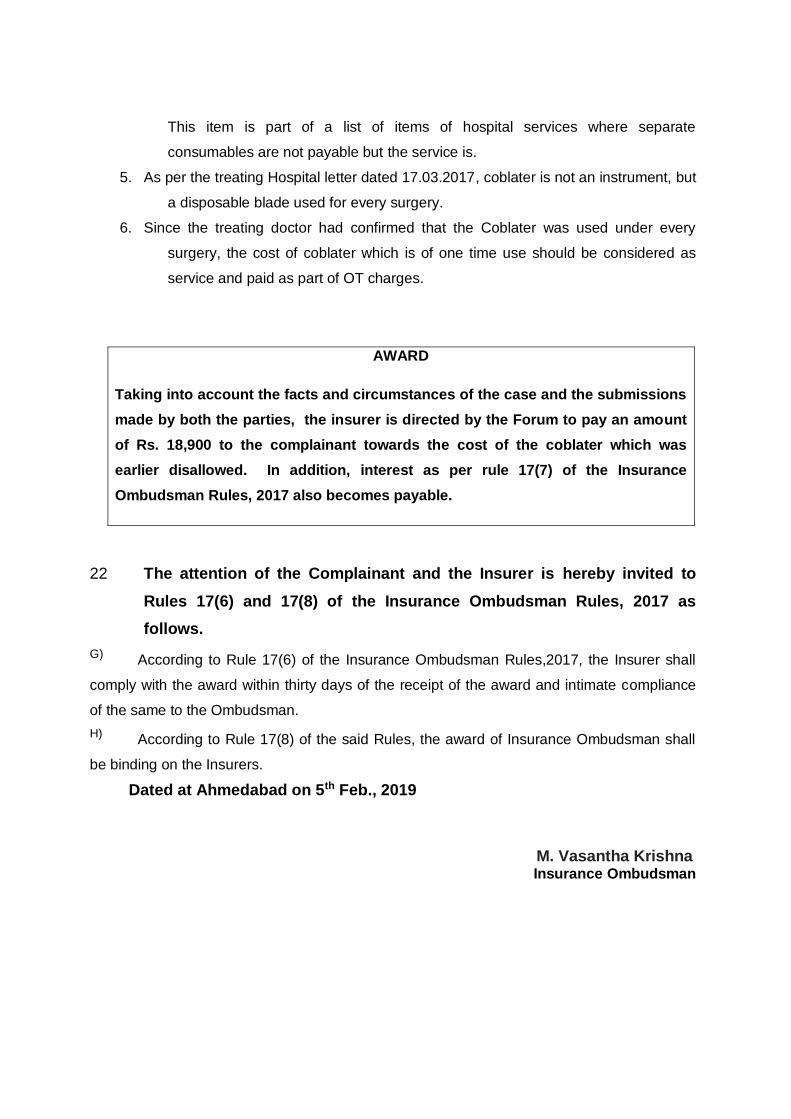

This item is part of a list of items of hospital services where separate

consumables are not payable but the service is.

2. As per the treating Hospital letter dated 17.03.2017, coblater is not an instrument, but

a disposable blade used for every surgery.

3. Since the treating doctor had confirmed that the Coblater was used under every

surgery, the cost of coblater which is of one time use should be considered as

service and paid as part of OT charges.

AWARD

Taking into account the facts and circumstances of the case and the submissions

made by both the parties, the insurer is directed by the Forum to pay an amount

of Rs. 18,900 to the complainant towards the cost of the coblater which was

earlier disallowed. In addition, interest as per rule 17(7) of the Insurance

Ombudsman Rules, 2017 also becomes payable.

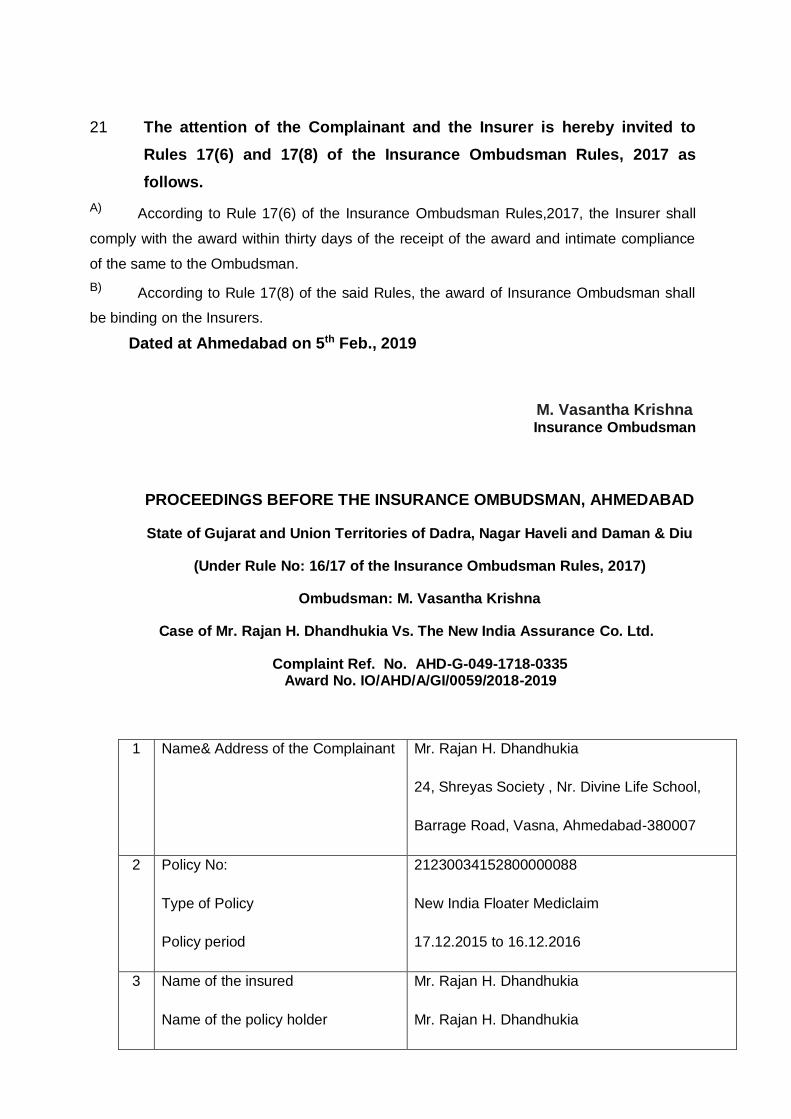

21 The attention of the Complainant and the Insurer is hereby invited to

Rules 17(6) and 17(8) of the Insurance Ombudsman Rules, 2017 as

follows.

A) According to Rule 17(6) of the Insurance Ombudsman Rules,2017, the Insurer shall

comply with the award within thirty days of the receipt of the award and intimate compliance

of the same to the Ombudsman.

B) According to Rule 17(8) of the said Rules, the award of Insurance Ombudsman shall

be binding on the Insurers.

Dated at Ahmedabad on 5th Feb., 2019

M. Vasantha Krishna

Insurance Ombudsman

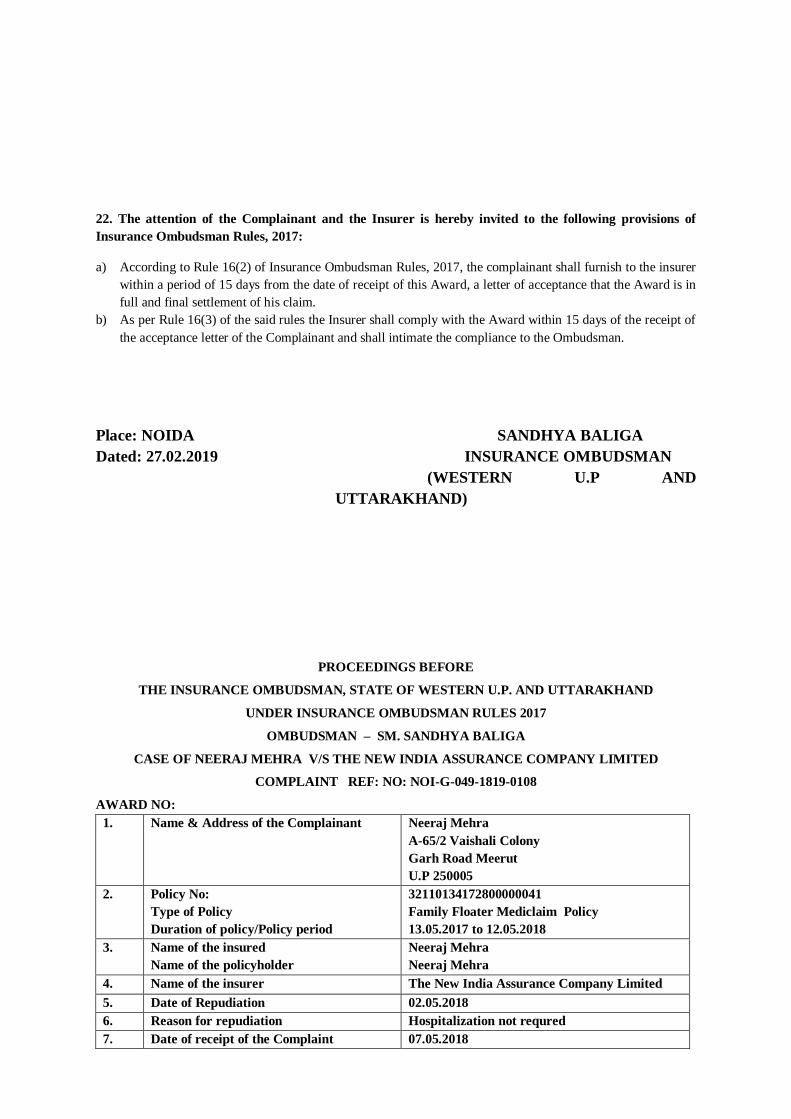

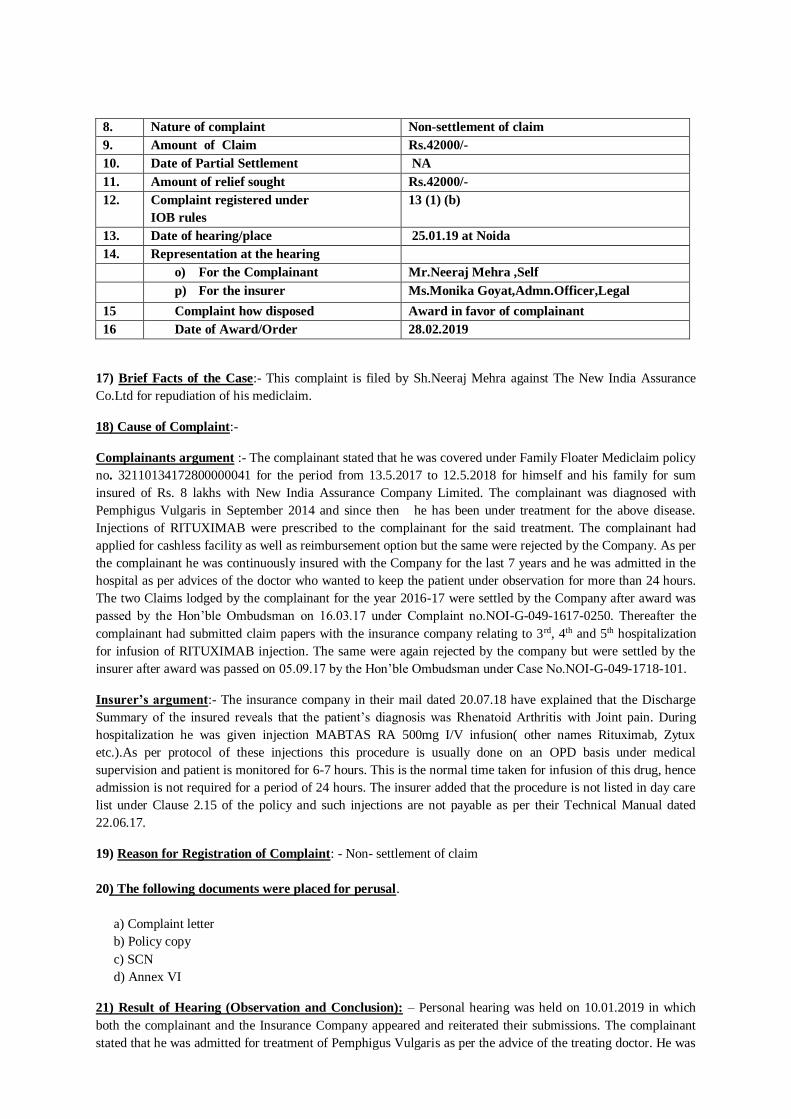

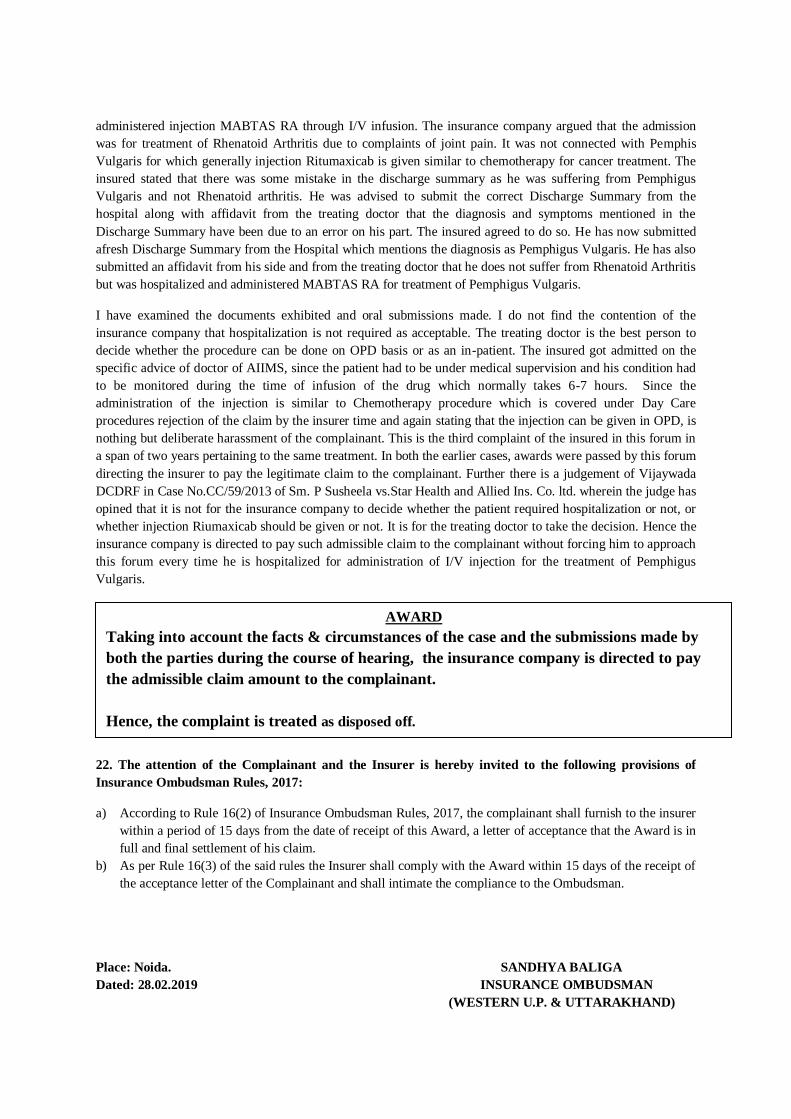

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017)

Ombudsman: M. Vasantha Krishna

Case of Mr. Rajan H. Dhandhukia Vs. The New India Assurance Co. Ltd.

Complaint Ref. No. AHD-G-049-1718-0335 Award No. IO/AHD/A/GI/0059/2018-2019

1 Name& Address of the Complainant Mr. Rajan H. Dhandhukia

24, Shreyas Society , Nr. Divine Life School,

Barrage Road, Vasna, Ahmedabad-380007

2 Policy No:

Type of Policy

Policy period

21230034152800000088

New India Floater Mediclaim

17.12.2015 to 16.12.2016

3 Name of the insured

Name of the policy holder

Mr. Rajan H. Dhandhukia

Mr. Rajan H. Dhandhukia

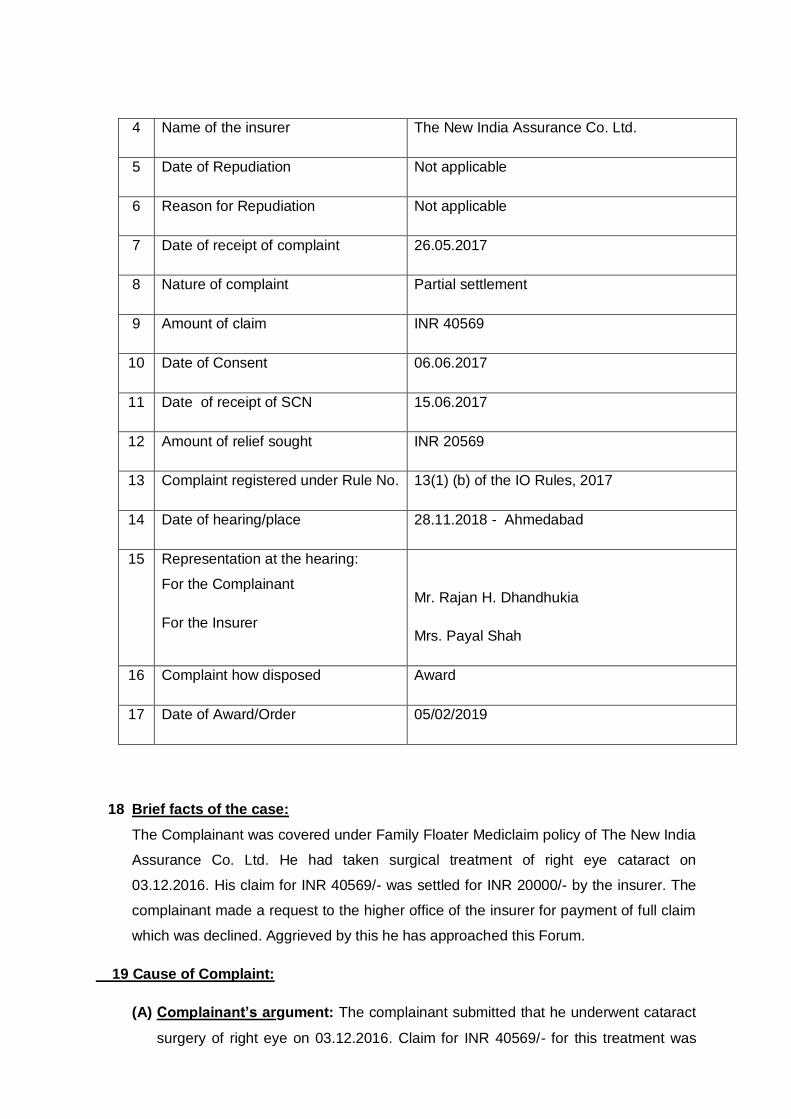

4 Name of the insurer The New India Assurance Co. Ltd.

5 Date of Repudiation Not applicable

6 Reason for Repudiation Not applicable

7 Date of receipt of complaint 26.05.2017

8 Nature of complaint Partial settlement

9 Amount of claim INR 40569

10 Date of Consent 06.06.2017

11 Date of receipt of SCN 15.06.2017

12 Amount of relief sought INR 20569

13 Complaint registered under Rule No. 13(1) (b) of the IO Rules, 2017

14 Date of hearing/place 28.11.2018 - Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr. Rajan H. Dhandhukia

Mrs. Payal Shah

16 Complaint how disposed Award

17 Date of Award/Order 05/02/2019

18 Brief facts of the case:

The Complainant was covered under Family Floater Mediclaim policy of The New India

Assurance Co. Ltd. He had taken surgical treatment of right eye cataract on

03.12.2016. His claim for INR 40569/- was settled for INR 20000/- by the insurer. The

complainant made a request to the higher office of the insurer for payment of full claim

which was declined. Aggrieved by this he has approached this Forum.

19 Cause of Complaint:

(A) Complainant’s argument: The complainant submitted that he underwent cataract

surgery of right eye on 03.12.2016. Claim for INR 40569/- for this treatment was

settled for only INR 20000/- after deduction of INR 20569/- by the insurer. The

complainant argued that he had to incur the expenses for the best available

treatment of cataract and the amount was within the sum insured. Hence, his claim

was payable in full. He urged the Forum to help him in getting his genuine claim.

(B) Insurer’s argument: The respondent’s representative submitted that the claim was

settled as per the policy condition No.3.3. According to this condition, liability for

payment of any claim relating to cataract for each eye shall not exceed 10% of the

sum insured or INR 50000/- whichever is less. The complainant was insured for INR

2,00,000/-. The claim was settled for INR 20000/- being 10% of the sum insured as

per the policy condition. He submitted that the settlement was correct.

20 Result of hearing with both parties(Observations& Conclusion):

The point to be considered was whether the deduction made under Condition No. 3.3

was correct.

Based on the submission of parties and the material made available to this Forum, the

following points emerged which were pertinent to decide the case:-

1. The policy condition categorically restricted the claim amount for cataract

treatment to 10% of sum insured.

2. The insurer had settled the subject claim for INR 20000/-(10% of sum insured

of INR 2 lacs)

3. The complainant argued during the hearing that the policy document issued to

him did not contain the condition 3.3 based on which his claim was restricted.

Hence same should not be applied to his claim. It is however observed that it is

clearly mentioned in the policy schedule that the policy is subject to terms and

conditions of New India Floater Mediclaim. In case the terms and conditions

were not attached to the policy issued to the complainant, nothing prevented

him from seeking the same from the insurer. Therefore, his argument is not

accepted by the Forum. In view of the foregoing, the settlement of claim by the

insurer is found to be in order by this Forum.

Thus the complaint is not allowed.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of hearing, the complaint is not

admitted and no relief is granted to the complainant.

21. If the Award is not acceptable to the Complainant, it would be open for him, to move any

other Forum/Court as he may consider appropriate under the Laws of the Land against the

Respondent Insurer.

Dated at Ahmedabad on 5th Feb., 2019

M.Vasantha Krishna Insurance Ombudsman

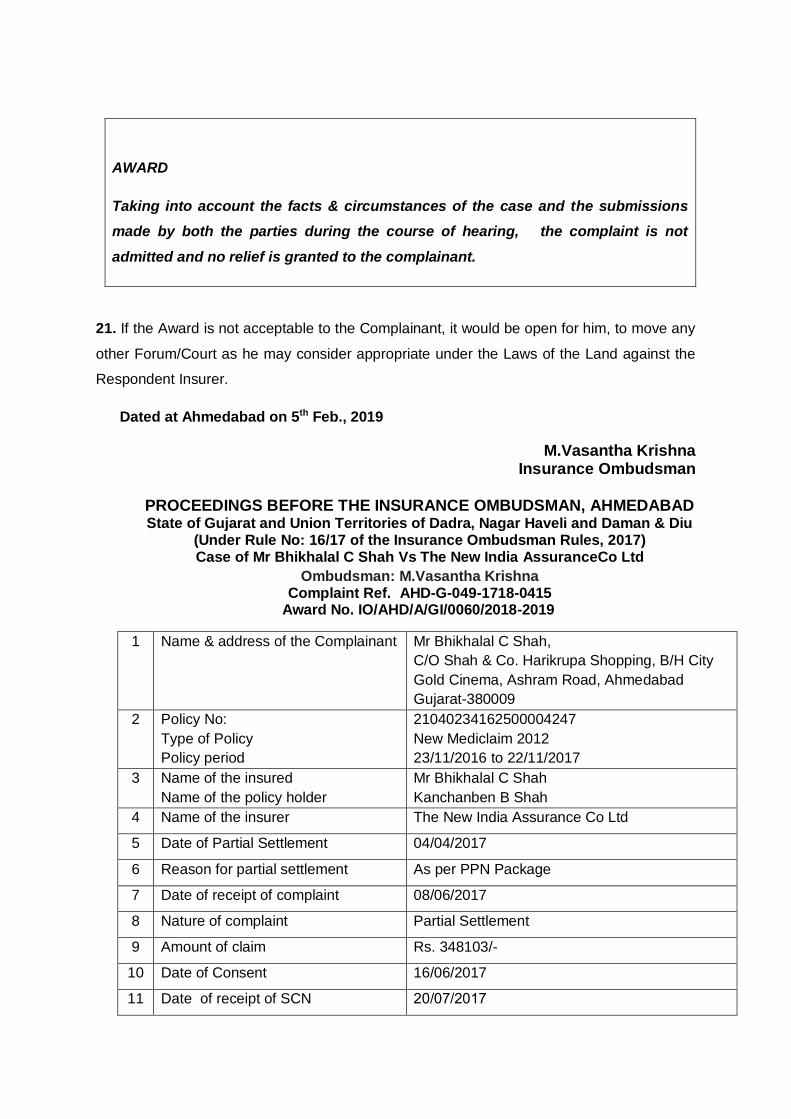

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Case of Mr Bhikhalal C Shah Vs The New India AssuranceCo Ltd

Ombudsman: M.Vasantha Krishna Complaint Ref. AHD-G-049-1718-0415

Award No. IO/AHD/A/GI/0060/2018-2019

1 Name & address of the Complainant Mr Bhikhalal C Shah,

C/O Shah & Co. Harikrupa Shopping, B/H City

Gold Cinema, Ashram Road, Ahmedabad

Gujarat-380009

2 Policy No:

Type of Policy

Policy period

21040234162500004247

New Mediclaim 2012

23/11/2016 to 22/11/2017

3 Name of the insured

Name of the policy holder

Mr Bhikhalal C Shah

Kanchanben B Shah

4 Name of the insurer The New India Assurance Co Ltd

5 Date of Partial Settlement 04/04/2017

6 Reason for partial settlement As per PPN Package

7 Date of receipt of complaint 08/06/2017

8 Nature of complaint Partial Settlement

9 Amount of claim Rs. 348103/-

10 Date of Consent 16/06/2017

11 Date of receipt of SCN 20/07/2017

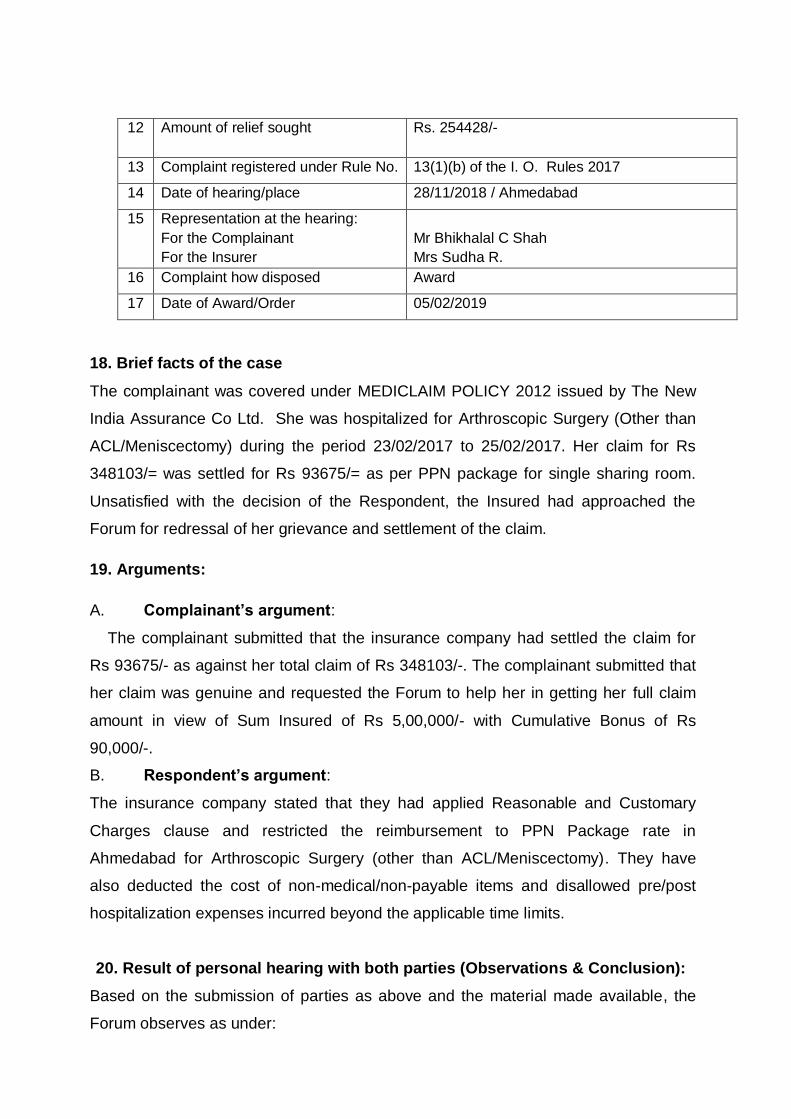

12 Amount of relief sought Rs. 254428/-

13 Complaint registered under Rule No. 13(1)(b) of the I. O. Rules 2017

14 Date of hearing/place 28/11/2018 / Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr Bhikhalal C Shah

Mrs Sudha R.

16 Complaint how disposed Award

17 Date of Award/Order 05/02/2019

18. Brief facts of the case

The complainant was covered under MEDICLAIM POLICY 2012 issued by The New

India Assurance Co Ltd. She was hospitalized for Arthroscopic Surgery (Other than

ACL/Meniscectomy) during the period 23/02/2017 to 25/02/2017. Her claim for Rs

348103/= was settled for Rs 93675/= as per PPN package for single sharing room.

Unsatisfied with the decision of the Respondent, the Insured had approached the

Forum for redressal of her grievance and settlement of the claim.

19. Arguments:

A. Complainant’s argument:

The complainant submitted that the insurance company had settled the claim for

Rs 93675/- as against her total claim of Rs 348103/-. The complainant submitted that

her claim was genuine and requested the Forum to help her in getting her full claim

amount in view of Sum Insured of Rs 5,00,000/- with Cumulative Bonus of Rs

90,000/-.

B. Respondent’s argument:

The insurance company stated that they had applied Reasonable and Customary

Charges clause and restricted the reimbursement to PPN Package rate in

Ahmedabad for Arthroscopic Surgery (other than ACL/Meniscectomy). They have

also deducted the cost of non-medical/non-payable items and disallowed pre/post

hospitalization expenses incurred beyond the applicable time limits.

20. Result of personal hearing with both parties (Observations & Conclusion):

Based on the submission of parties as above and the material made available, the

Forum observes as under:

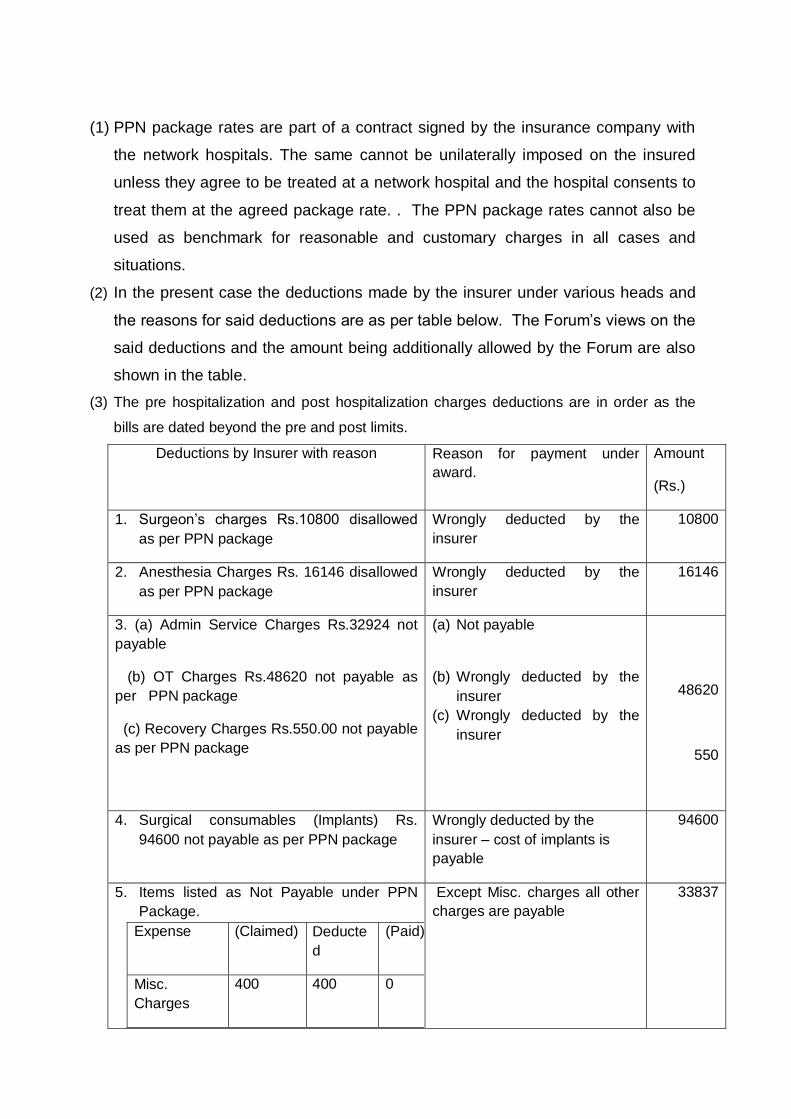

(1) PPN package rates are part of a contract signed by the insurance company with

the network hospitals. The same cannot be unilaterally imposed on the insured

unless they agree to be treated at a network hospital and the hospital consents to

treat them at the agreed package rate. . The PPN package rates cannot also be

used as benchmark for reasonable and customary charges in all cases and

situations.

(2) In the present case the deductions made by the insurer under various heads and

the reasons for said deductions are as per table below. The Forum’s views on the

said deductions and the amount being additionally allowed by the Forum are also

shown in the table.

(3) The pre hospitalization and post hospitalization charges deductions are in order as the

bills are dated beyond the pre and post limits.

Deductions by Insurer with reason Reason for payment under

award.

Amount

(Rs.)

1. Surgeon’s charges Rs.10800 disallowed

as per PPN package

Wrongly deducted by the

insurer

10800

2. Anesthesia Charges Rs. 16146 disallowed

as per PPN package

Wrongly deducted by the

insurer

16146

3. (a) Admin Service Charges Rs.32924 not

payable

(b) OT Charges Rs.48620 not payable as

per PPN package

(c) Recovery Charges Rs.550.00 not payable

as per PPN package

(a) Not payable

(b) Wrongly deducted by the

insurer

(c) Wrongly deducted by the

insurer

48620

550

4. Surgical consumables (Implants) Rs.

94600 not payable as per PPN package

Wrongly deducted by the

insurer – cost of implants is

payable

94600

5. Items listed as Not Payable under PPN

Package.

Expense (Claimed) Deducte

d

(Paid)

Misc.

Charges

400 400 0

Except Misc. charges all other

charges are payable

33837

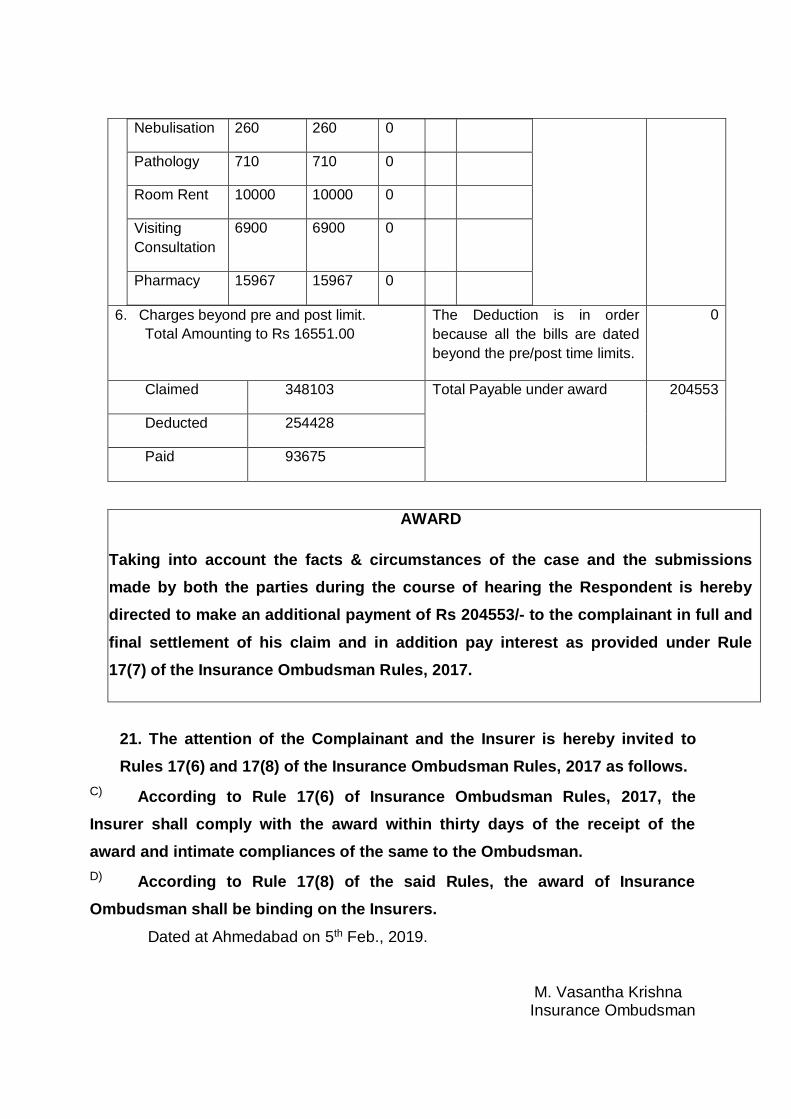

Nebulisation 260 260 0

Pathology 710 710 0

Room Rent 10000 10000 0

Visiting

Consultation

6900 6900 0

Pharmacy 15967 15967 0

6. Charges beyond pre and post limit.

Total Amounting to Rs 16551.00

The Deduction is in order

because all the bills are dated

beyond the pre/post time limits.

0

Claimed 348103 Total Payable under award 204553

Deducted 254428

Paid 93675

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of hearing the Respondent is hereby

directed to make an additional payment of Rs 204553/- to the complainant in full and

final settlement of his claim and in addition pay interest as provided under Rule

17(7) of the Insurance Ombudsman Rules, 2017.

21. The attention of the Complainant and the Insurer is hereby invited to

Rules 17(6) and 17(8) of the Insurance Ombudsman Rules, 2017 as follows.

C) According to Rule 17(6) of Insurance Ombudsman Rules, 2017, the

Insurer shall comply with the award within thirty days of the receipt of the

award and intimate compliances of the same to the Ombudsman.

D) According to Rule 17(8) of the said Rules, the award of Insurance

Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 5th Feb., 2019.

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Ombudsman: M. Vasantha Krishna

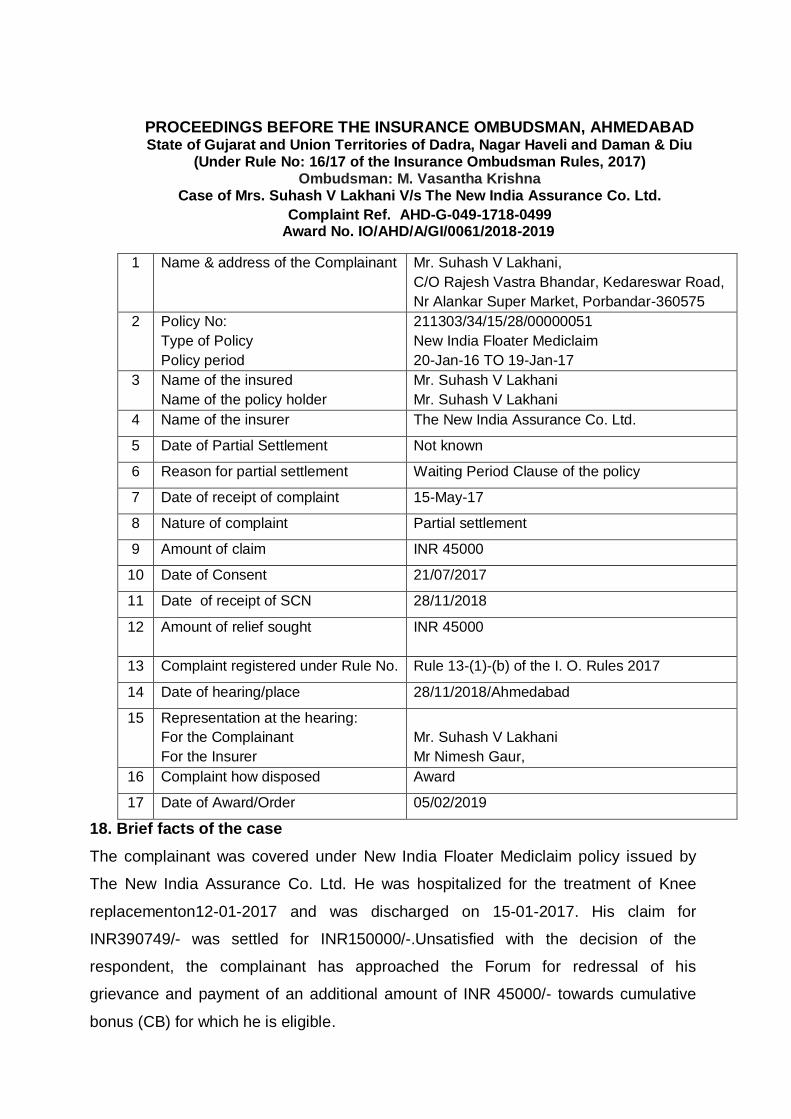

Case of Mrs. Suhash V Lakhani V/s The New India Assurance Co. Ltd.

Complaint Ref. AHD-G-049-1718-0499 Award No. IO/AHD/A/GI/0061/2018-2019

1 Name & address of the Complainant Mr. Suhash V Lakhani,

C/O Rajesh Vastra Bhandar, Kedareswar Road,

Nr Alankar Super Market, Porbandar-360575

2 Policy No:

Type of Policy

Policy period

211303/34/15/28/00000051

New India Floater Mediclaim

20-Jan-16 TO 19-Jan-17

3 Name of the insured

Name of the policy holder

Mr. Suhash V Lakhani

Mr. Suhash V Lakhani

4 Name of the insurer The New India Assurance Co. Ltd.

5 Date of Partial Settlement Not known

6 Reason for partial settlement Waiting Period Clause of the policy

7 Date of receipt of complaint 15-May-17

8 Nature of complaint Partial settlement

9 Amount of claim INR 45000

10 Date of Consent 21/07/2017

11 Date of receipt of SCN 28/11/2018

12 Amount of relief sought INR 45000

13 Complaint registered under Rule No. Rule 13-(1)-(b) of the I. O. Rules 2017

14 Date of hearing/place 28/11/2018/Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr. Suhash V Lakhani

Mr Nimesh Gaur,

16 Complaint how disposed Award

17 Date of Award/Order 05/02/2019

18. Brief facts of the case

The complainant was covered under New India Floater Mediclaim policy issued by

The New India Assurance Co. Ltd. He was hospitalized for the treatment of Knee

replacementon12-01-2017 and was discharged on 15-01-2017. His claim for

INR390749/- was settled for INR150000/-.Unsatisfied with the decision of the

respondent, the complainant has approached the Forum for redressal of his

grievance and payment of an additional amount of INR 45000/- towards cumulative

bonus (CB) for which he is eligible.

19 Arguments:

C. Complainant’s argument:

The complainant submitted that he had New India Floater Mediclaim policy issued

by The New India Assurance Co. Ltd. The sum insured under the impugned policy

was INR150000/- In the years 2013 and 2014. It was increased to INR 200000/= in

2015. His claim for INR 390749/- was approved for only INR 150000/- giving the

reason that the enhanced sum assured is not available for the claim as per condition

4.3.2 of the policy. As per the applicable condition, unless the Insured Person has

continuous Coverage in excess of 48 months with the company, the expenses related

to the treatment Joint Replacement due to Degenerative Condition and Age-related

Osteoarthritis and Osteoporosis are not payable. Thus the company has approved

the payment of INR 150000/= by way of cashless approval against the hospital bill of

INR 390000/= approximately. The complainant claims that he is entitled to a further

payment of INR 45000/- on account of CB earned under the policy. He has requested

the Forum to help him in getting the said amount released by the insurer as his claim

is genuine.

D. Respondent’s arguments:

The insurance company stated that they had settled the complainant’s claim as per

condition 4.3.2 of the policy. As per the said condition-“Unless the Insured Person has

continuous Coverage in excess of 48 months with the company, the expenses related

to the treatment Joint Replacement due to Degenerative Condition and Age-related

Osteoarthritis and Osteoporosis are not payable.”

Hence the additional sum insured of INR 1,50,000 due to increase in sum insured to

INR 2,50,000 in 2015 was not available for the payment of subject claim, since the

period of 48 months had not been completed since sum insured was increased

complainant’s claim of INR 3,90,749/- was therefore settled for INR 150000/=being

the sum insured under the policy prior to the said increase.

20. Result of personal hearing with both parties (Observations& Conclusion):

Based on the submission of parties as above and the material made available to this

Forum, the following points emerged which were pertinent to decide the case.

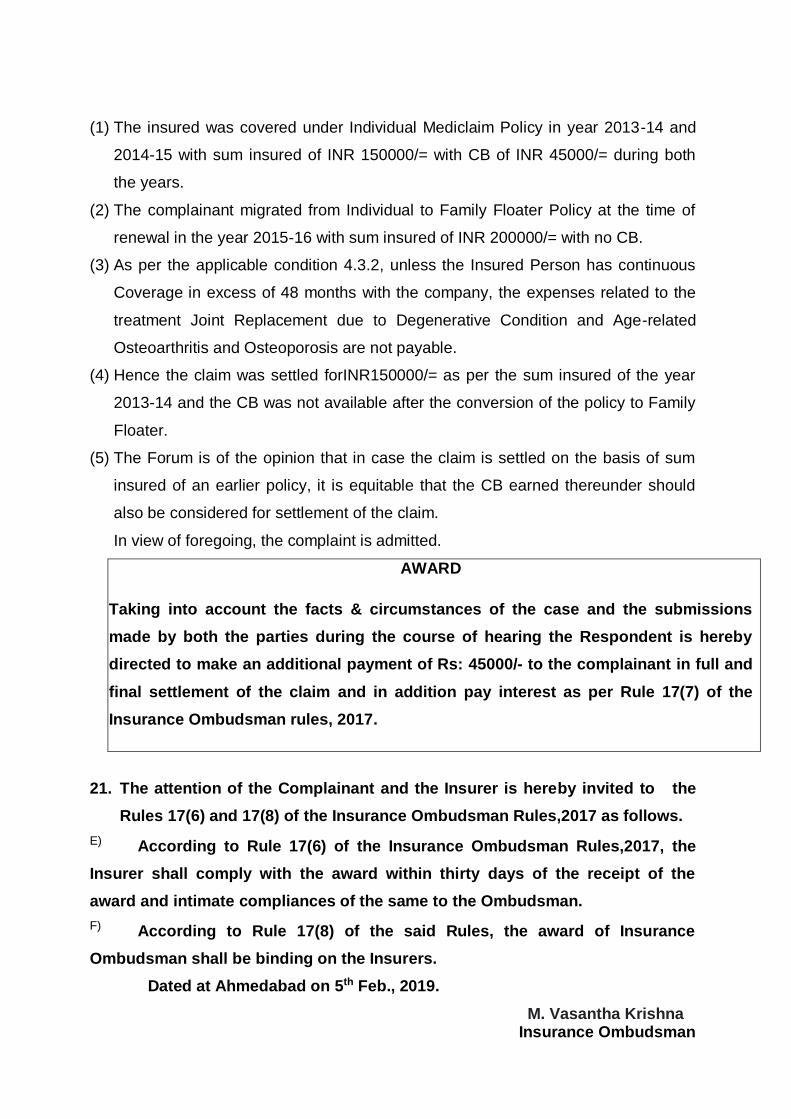

(1) The insured was covered under Individual Mediclaim Policy in year 2013-14 and

2014-15 with sum insured of INR 150000/= with CB of INR 45000/= during both

the years.

(2) The complainant migrated from Individual to Family Floater Policy at the time of

renewal in the year 2015-16 with sum insured of INR 200000/= with no CB.

(3) As per the applicable condition 4.3.2, unless the Insured Person has continuous

Coverage in excess of 48 months with the company, the expenses related to the

treatment Joint Replacement due to Degenerative Condition and Age-related

Osteoarthritis and Osteoporosis are not payable.

(4) Hence the claim was settled forINR150000/= as per the sum insured of the year

2013-14 and the CB was not available after the conversion of the policy to Family

Floater.

(5) The Forum is of the opinion that in case the claim is settled on the basis of sum

insured of an earlier policy, it is equitable that the CB earned thereunder should

also be considered for settlement of the claim.

In view of foregoing, the complaint is admitted.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of hearing the Respondent is hereby

directed to make an additional payment of Rs: 45000/- to the complainant in full and

final settlement of the claim and in addition pay interest as per Rule 17(7) of the

Insurance Ombudsman rules, 2017.

21. The attention of the Complainant and the Insurer is hereby invited to the

Rules 17(6) and 17(8) of the Insurance Ombudsman Rules,2017 as follows.

E) According to Rule 17(6) of the Insurance Ombudsman Rules,2017, the

Insurer shall comply with the award within thirty days of the receipt of the

award and intimate compliances of the same to the Ombudsman.

F) According to Rule 17(8) of the said Rules, the award of Insurance

Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 5th Feb., 2019.

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) OMBUDSMAN: M.VASANTHA KRISHNA

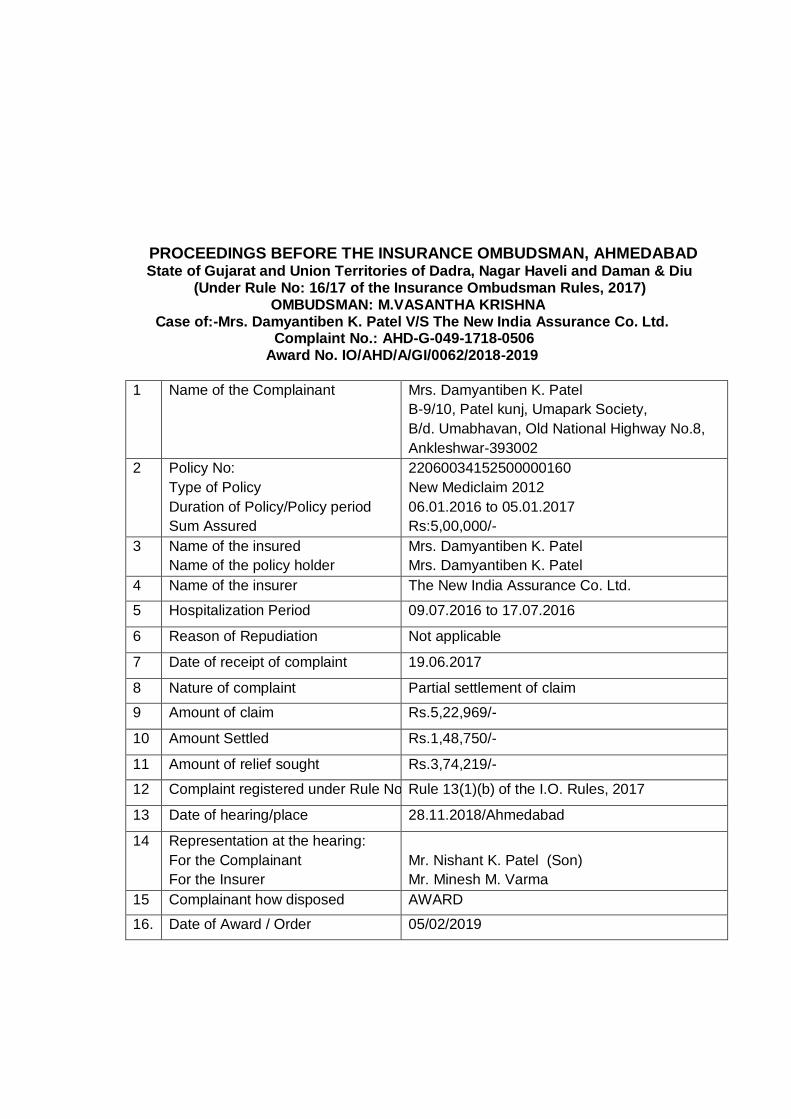

Case of:-Mrs. Damyantiben K. Patel V/S The New India Assurance Co. Ltd. Complaint No.: AHD-G-049-1718-0506

Award No. IO/AHD/A/GI/0062/2018-2019

1 Name of the Complainant Mrs. Damyantiben K. Patel

B-9/10, Patel kunj, Umapark Society,

B/d. Umabhavan, Old National Highway No.8,

Ankleshwar-393002

2 Policy No:

Type of Policy

Duration of Policy/Policy period

Sum Assured

22060034152500000160

New Mediclaim 2012

06.01.2016 to 05.01.2017

Rs:5,00,000/-

3 Name of the insured

Name of the policy holder

Mrs. Damyantiben K. Patel

Mrs. Damyantiben K. Patel

4 Name of the insurer The New India Assurance Co. Ltd.

5 Hospitalization Period 09.07.2016 to 17.07.2016

6 Reason of Repudiation Not applicable

7 Date of receipt of complaint 19.06.2017

8 Nature of complaint Partial settlement of claim

9 Amount of claim Rs.5,22,969/-

10 Amount Settled Rs.1,48,750/-

11 Amount of relief sought Rs.3,74,219/-

12 Complaint registered under Rule No. Rule 13(1)(b) of the I.O. Rules, 2017

13 Date of hearing/place 28.11.2018/Ahmedabad

14 Representation at the hearing:

For the Complainant

For the Insurer

Mr. Nishant K. Patel (Son)

Mr. Minesh M. Varma

15 Complainant how disposed AWARD

16. Date of Award / Order 05/02/2019

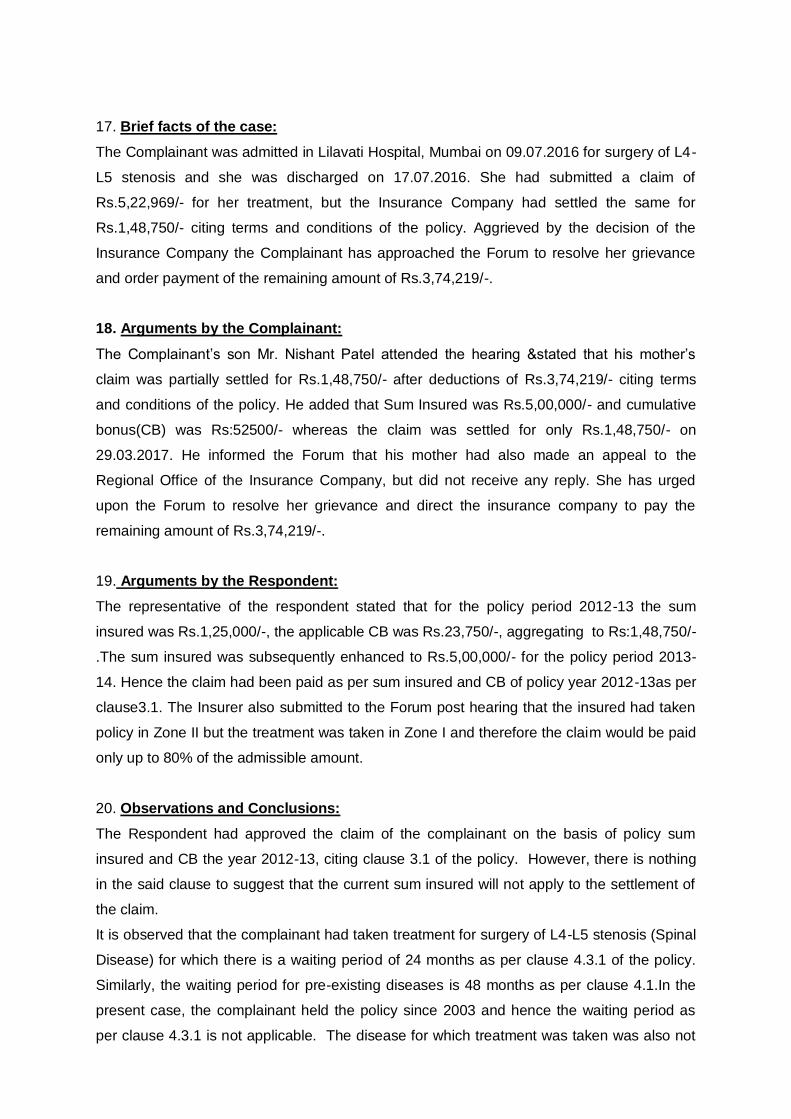

17. Brief facts of the case:

The Complainant was admitted in Lilavati Hospital, Mumbai on 09.07.2016 for surgery of L4-

L5 stenosis and she was discharged on 17.07.2016. She had submitted a claim of

Rs.5,22,969/- for her treatment, but the Insurance Company had settled the same for

Rs.1,48,750/- citing terms and conditions of the policy. Aggrieved by the decision of the

Insurance Company the Complainant has approached the Forum to resolve her grievance

and order payment of the remaining amount of Rs.3,74,219/-.

18. Arguments by the Complainant:

The Complainant’s son Mr. Nishant Patel attended the hearing &stated that his mother’s

claim was partially settled for Rs.1,48,750/- after deductions of Rs.3,74,219/- citing terms

and conditions of the policy. He added that Sum Insured was Rs.5,00,000/- and cumulative

bonus(CB) was Rs:52500/- whereas the claim was settled for only Rs.1,48,750/- on

29.03.2017. He informed the Forum that his mother had also made an appeal to the

Regional Office of the Insurance Company, but did not receive any reply. She has urged

upon the Forum to resolve her grievance and direct the insurance company to pay the

remaining amount of Rs.3,74,219/-.

19. Arguments by the Respondent:

The representative of the respondent stated that for the policy period 2012-13 the sum

insured was Rs.1,25,000/-, the applicable CB was Rs.23,750/-, aggregating to Rs:1,48,750/-

.The sum insured was subsequently enhanced to Rs.5,00,000/- for the policy period 2013-

14. Hence the claim had been paid as per sum insured and CB of policy year 2012-13as per

clause3.1. The Insurer also submitted to the Forum post hearing that the insured had taken

policy in Zone II but the treatment was taken in Zone I and therefore the claim would be paid

only up to 80% of the admissible amount.

20. Observations and Conclusions:

The Respondent had approved the claim of the complainant on the basis of policy sum

insured and CB the year 2012-13, citing clause 3.1 of the policy. However, there is nothing

in the said clause to suggest that the current sum insured will not apply to the settlement of

the claim.

It is observed that the complainant had taken treatment for surgery of L4-L5 stenosis (Spinal

Disease) for which there is a waiting period of 24 months as per clause 4.3.1 of the policy.

Similarly, the waiting period for pre-existing diseases is 48 months as per clause 4.1.In the

present case, the complainant held the policy since 2003 and hence the waiting period as

per clause 4.3.1 is not applicable. The disease for which treatment was taken was also not

a pre-existing disease. Hence the waiting period as per clause 4.1 is also not applicable.

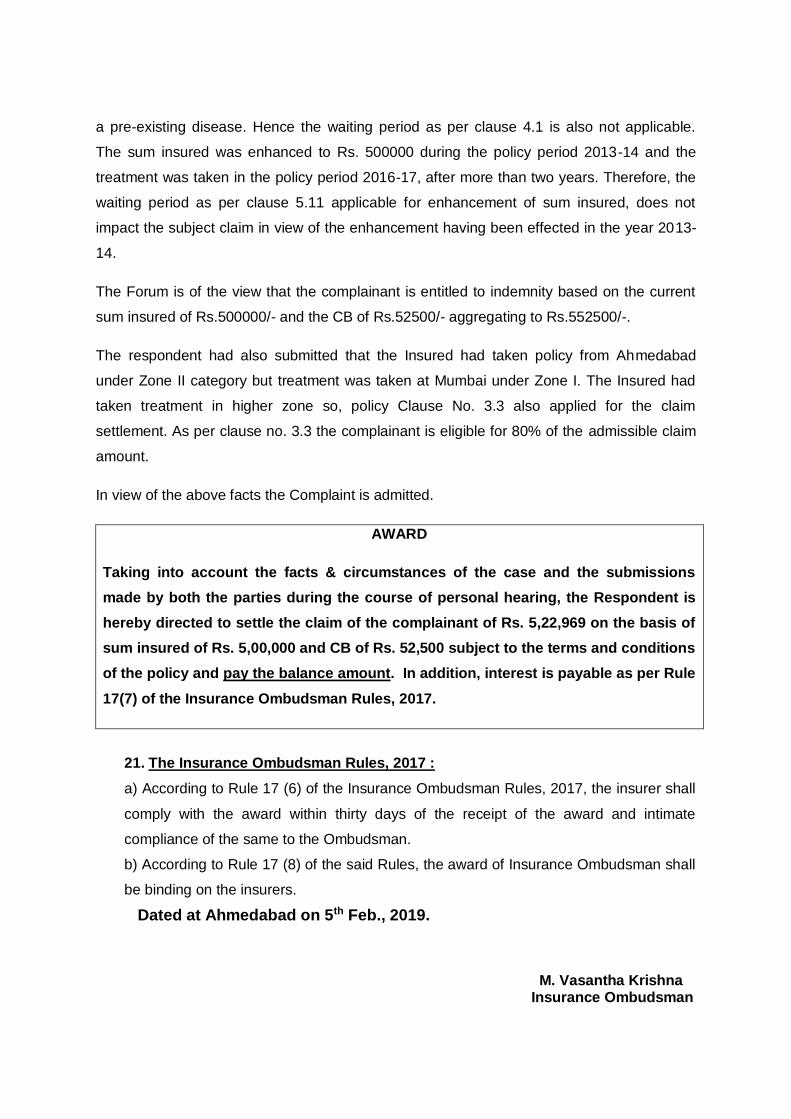

The sum insured was enhanced to Rs. 500000 during the policy period 2013-14 and the

treatment was taken in the policy period 2016-17, after more than two years. Therefore, the

waiting period as per clause 5.11 applicable for enhancement of sum insured, does not

impact the subject claim in view of the enhancement having been effected in the year 2013-

14.

The Forum is of the view that the complainant is entitled to indemnity based on the current

sum insured of Rs.500000/- and the CB of Rs.52500/- aggregating to Rs.552500/-.

The respondent had also submitted that the Insured had taken policy from Ahmedabad

under Zone II category but treatment was taken at Mumbai under Zone I. The Insured had

taken treatment in higher zone so, policy Clause No. 3.3 also applied for the claim

settlement. As per clause no. 3.3 the complainant is eligible for 80% of the admissible claim

amount.

In view of the above facts the Complaint is admitted.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of personal hearing, the Respondent is

hereby directed to settle the claim of the complainant of Rs. 5,22,969 on the basis of

sum insured of Rs. 5,00,000 and CB of Rs. 52,500 subject to the terms and conditions

of the policy and pay the balance amount. In addition, interest is payable as per Rule

17(7) of the Insurance Ombudsman Rules, 2017.

21. The Insurance Ombudsman Rules, 2017 :

a) According to Rule 17 (6) of the Insurance Ombudsman Rules, 2017, the insurer shall

comply with the award within thirty days of the receipt of the award and intimate

compliance of the same to the Ombudsman.

b) According to Rule 17 (8) of the said Rules, the award of Insurance Ombudsman shall

be binding on the insurers.

Dated at Ahmedabad on 5th Feb., 2019.

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017)

Ombudsman: M. Vasantha Krishna

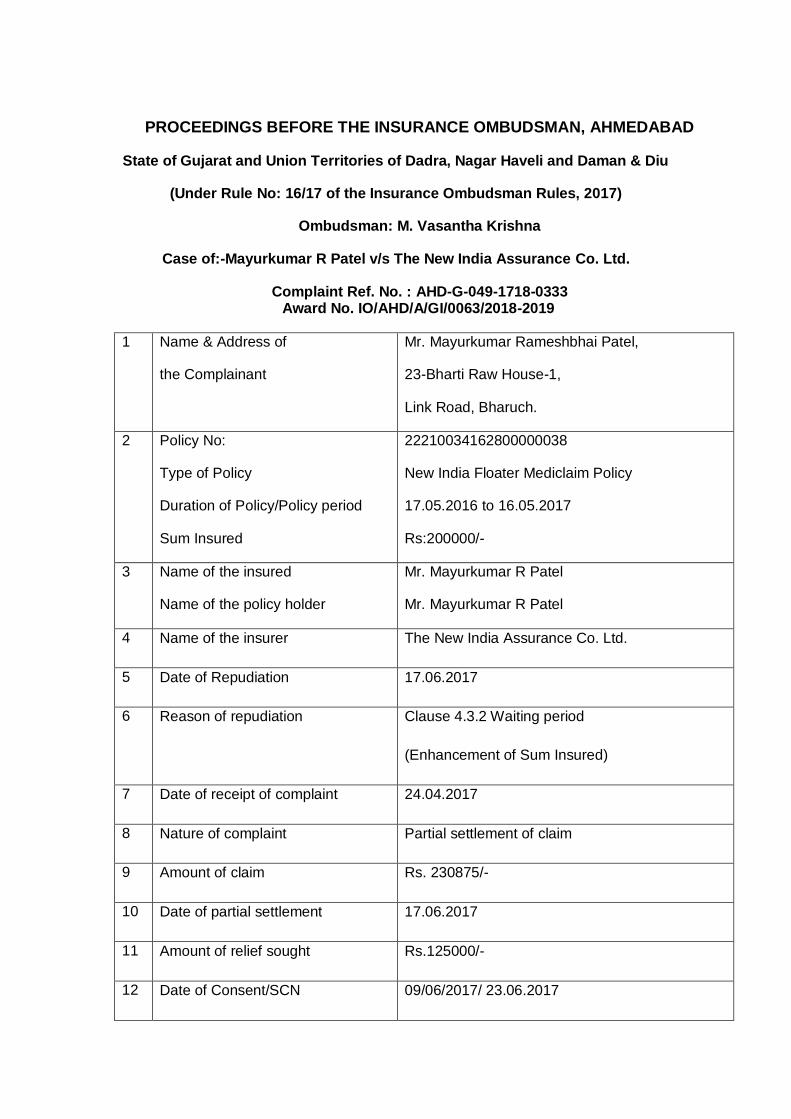

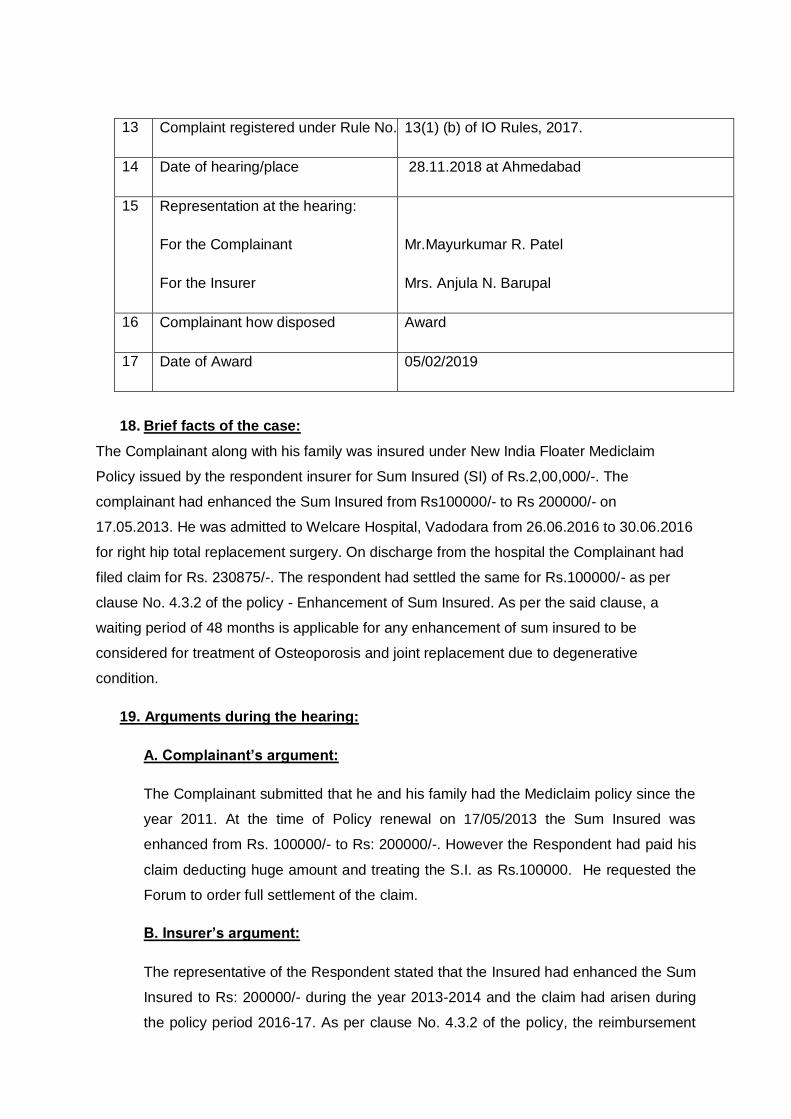

Case of:-Mayurkumar R Patel v/s The New India Assurance Co. Ltd.

Complaint Ref. No. : AHD-G-049-1718-0333 Award No. IO/AHD/A/GI/0063/2018-2019

1 Name & Address of

the Complainant

Mr. Mayurkumar Rameshbhai Patel,

23-Bharti Raw House-1,

Link Road, Bharuch.

2 Policy No:

Type of Policy

Duration of Policy/Policy period

Sum Insured

22210034162800000038

New India Floater Mediclaim Policy

17.05.2016 to 16.05.2017

Rs:200000/-

3 Name of the insured

Name of the policy holder

Mr. Mayurkumar R Patel

Mr. Mayurkumar R Patel

4 Name of the insurer The New India Assurance Co. Ltd.

5 Date of Repudiation 17.06.2017

6 Reason of repudiation Clause 4.3.2 Waiting period

(Enhancement of Sum Insured)

7 Date of receipt of complaint 24.04.2017

8 Nature of complaint Partial settlement of claim

9 Amount of claim Rs. 230875/-

10 Date of partial settlement 17.06.2017

11 Amount of relief sought Rs.125000/-

12 Date of Consent/SCN 09/06/2017/ 23.06.2017

13 Complaint registered under Rule No. 13(1) (b) of IO Rules, 2017.

14 Date of hearing/place 28.11.2018 at Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr.Mayurkumar R. Patel

Mrs. Anjula N. Barupal

16 Complainant how disposed Award

17 Date of Award 05/02/2019

18. Brief facts of the case:

The Complainant along with his family was insured under New India Floater Mediclaim

Policy issued by the respondent insurer for Sum Insured (SI) of Rs.2,00,000/-. The

complainant had enhanced the Sum Insured from Rs100000/- to Rs 200000/- on

17.05.2013. He was admitted to Welcare Hospital, Vadodara from 26.06.2016 to 30.06.2016

for right hip total replacement surgery. On discharge from the hospital the Complainant had

filed claim for Rs. 230875/-. The respondent had settled the same for Rs.100000/- as per

clause No. 4.3.2 of the policy - Enhancement of Sum Insured. As per the said clause, a

waiting period of 48 months is applicable for any enhancement of sum insured to be

considered for treatment of Osteoporosis and joint replacement due to degenerative

condition.

19. Arguments during the hearing:

A. Complainant’s argument:

The Complainant submitted that he and his family had the Mediclaim policy since the

year 2011. At the time of Policy renewal on 17/05/2013 the Sum Insured was

enhanced from Rs. 100000/- to Rs: 200000/-. However the Respondent had paid his

claim deducting huge amount and treating the S.I. as Rs.100000. He requested the

Forum to order full settlement of the claim.

B. Insurer’s argument:

The representative of the Respondent stated that the Insured had enhanced the Sum

Insured to Rs: 200000/- during the year 2013-2014 and the claim had arisen during

the policy period 2016-17. As per clause No. 4.3.2 of the policy, the reimbursement

for treatment of Osteoporosis was restricted to Sum Insured which was available

before 48 months. Accordingly, Sum Insured of Rs: 100000/- was considered for the

settlement of the claim.

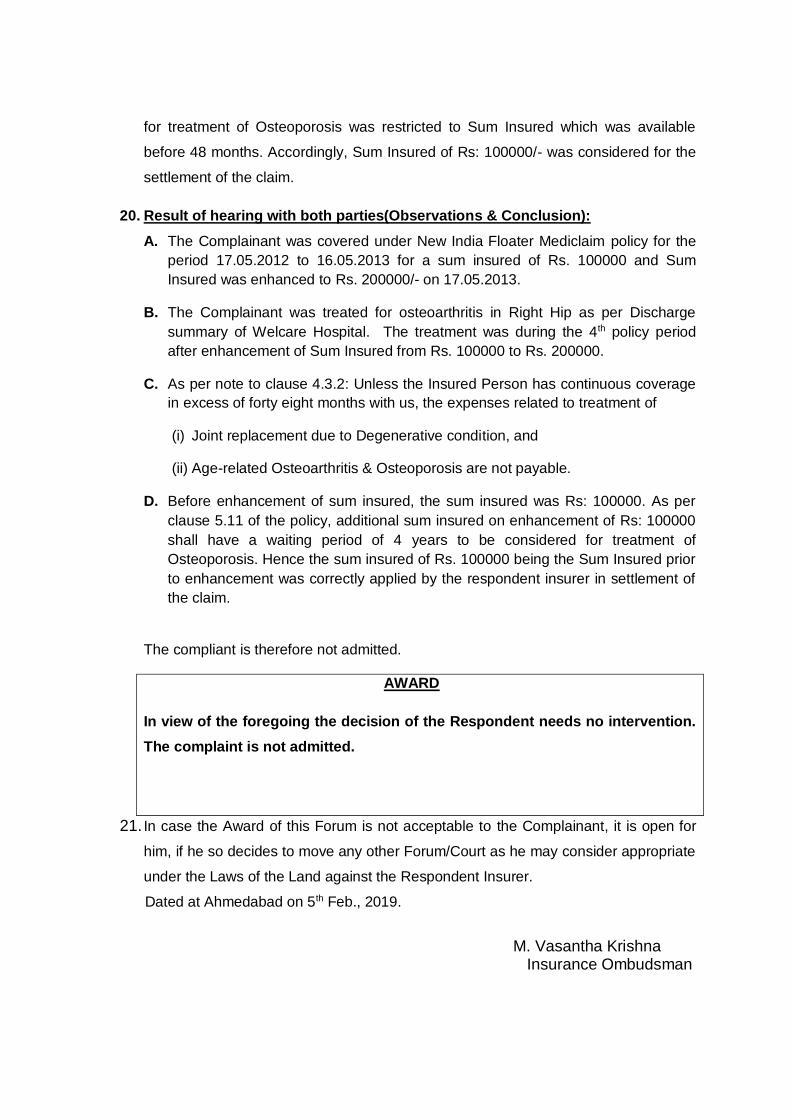

20. Result of hearing with both parties(Observations & Conclusion):

A. The Complainant was covered under New India Floater Mediclaim policy for the

period 17.05.2012 to 16.05.2013 for a sum insured of Rs. 100000 and Sum

Insured was enhanced to Rs. 200000/- on 17.05.2013.

B. The Complainant was treated for osteoarthritis in Right Hip as per Discharge

summary of Welcare Hospital. The treatment was during the 4th policy period

after enhancement of Sum Insured from Rs. 100000 to Rs. 200000.

C. As per note to clause 4.3.2: Unless the Insured Person has continuous coverage

in excess of forty eight months with us, the expenses related to treatment of

(i) Joint replacement due to Degenerative condition, and

(ii) Age-related Osteoarthritis & Osteoporosis are not payable.

D. Before enhancement of sum insured, the sum insured was Rs: 100000. As per

clause 5.11 of the policy, additional sum insured on enhancement of Rs: 100000

shall have a waiting period of 4 years to be considered for treatment of

Osteoporosis. Hence the sum insured of Rs. 100000 being the Sum Insured prior

to enhancement was correctly applied by the respondent insurer in settlement of

the claim.

The compliant is therefore not admitted.

AWARD

In view of the foregoing the decision of the Respondent needs no intervention.

The complaint is not admitted.

21. In case the Award of this Forum is not acceptable to the Complainant, it is open for

him, if he so decides to move any other Forum/Court as he may consider appropriate

under the Laws of the Land against the Respondent Insurer.

Dated at Ahmedabad on 5th Feb., 2019.

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017)

Ombudsman: M. Vasantha Krishna

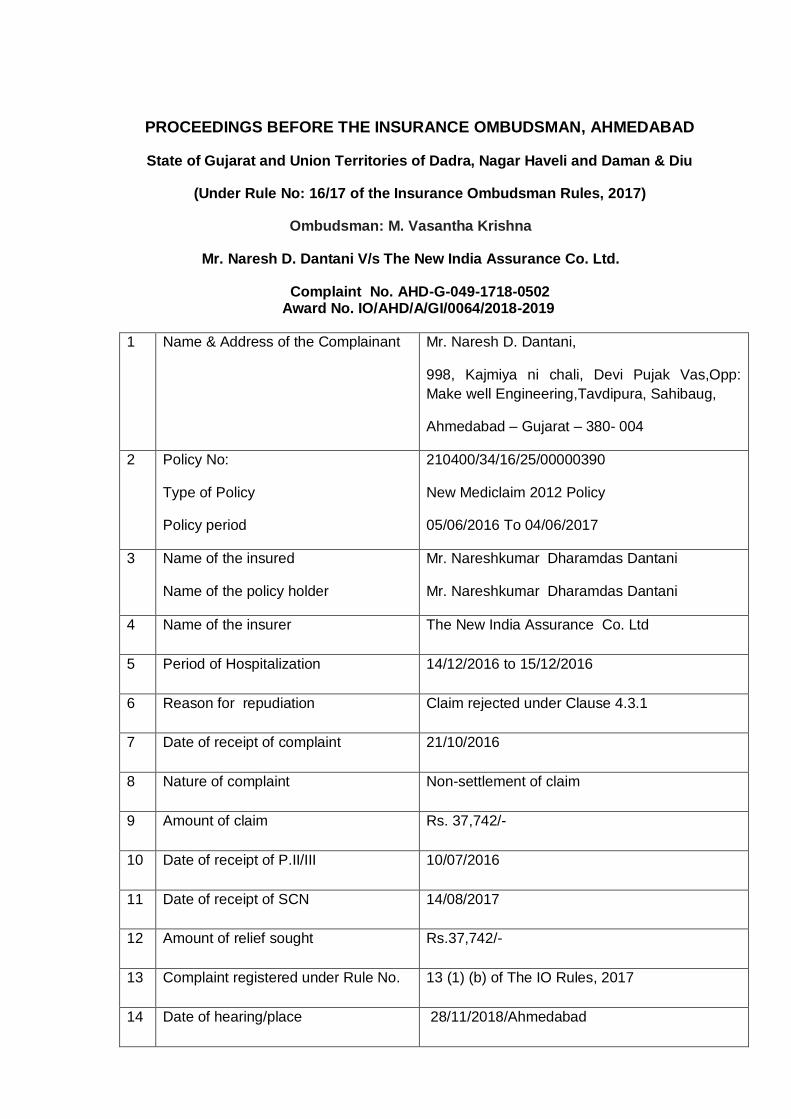

Mr. Naresh D. Dantani V/s The New India Assurance Co. Ltd.

Complaint No. AHD-G-049-1718-0502 Award No. IO/AHD/A/GI/0064/2018-2019

1 Name & Address of the Complainant Mr. Naresh D. Dantani,

998, Kajmiya ni chali, Devi Pujak Vas,Opp:

Make well Engineering,Tavdipura, Sahibaug,

Ahmedabad – Gujarat – 380- 004

2 Policy No:

Type of Policy

Policy period

210400/34/16/25/00000390

New Mediclaim 2012 Policy

05/06/2016 To 04/06/2017

3 Name of the insured

Name of the policy holder

Mr. Nareshkumar Dharamdas Dantani

Mr. Nareshkumar Dharamdas Dantani

4 Name of the insurer The New India Assurance Co. Ltd

5 Period of Hospitalization 14/12/2016 to 15/12/2016

6 Reason for repudiation Claim rejected under Clause 4.3.1

7 Date of receipt of complaint 21/10/2016

8 Nature of complaint Non-settlement of claim

9 Amount of claim Rs. 37,742/-

10 Date of receipt of P.II/III 10/07/2016

11 Date of receipt of SCN 14/08/2017

12 Amount of relief sought Rs.37,742/-

13 Complaint registered under Rule No. 13 (1) (b) of The IO Rules, 2017

14 Date of hearing/place 28/11/2018/Ahmedabad

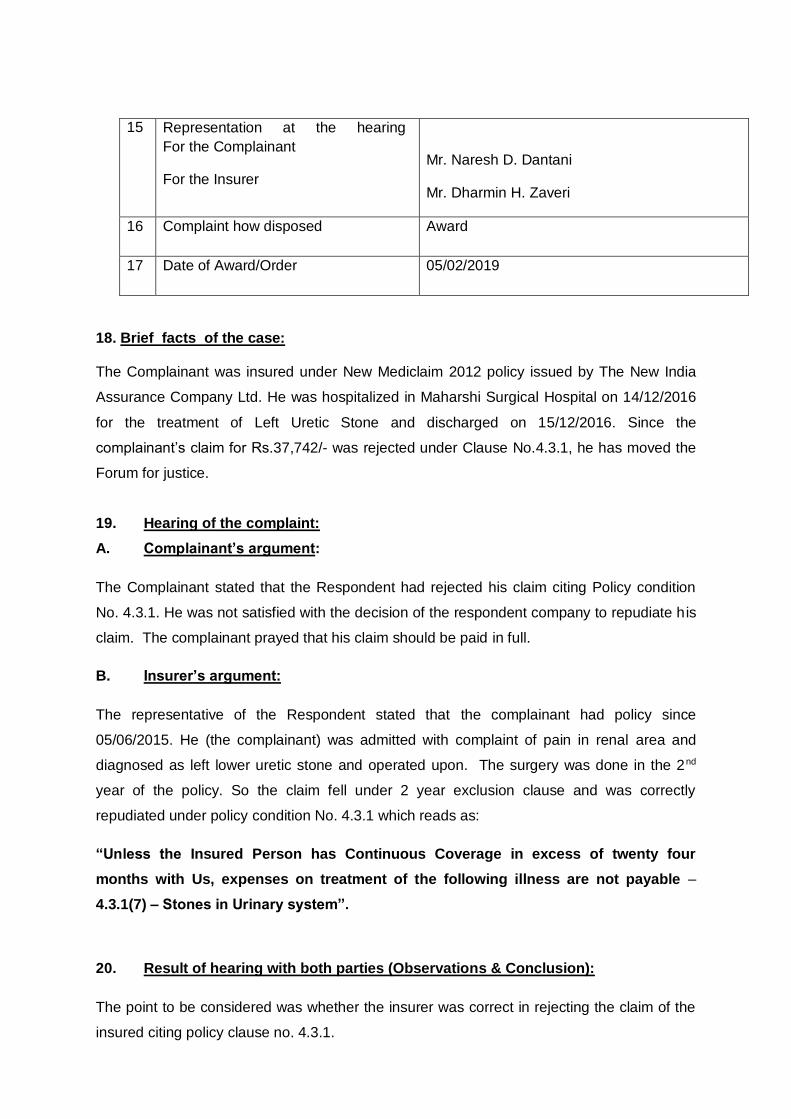

15 Representation at the hearing at

For the Complainant

For the Insurer

Mr. Naresh D. Dantani

Mr. Dharmin H. Zaveri

16 Complaint how disposed Award

17 Date of Award/Order 05/02/2019

18. Brief facts of the case:

The Complainant was insured under New Mediclaim 2012 policy issued by The New India

Assurance Company Ltd. He was hospitalized in Maharshi Surgical Hospital on 14/12/2016

for the treatment of Left Uretic Stone and discharged on 15/12/2016. Since the

complainant’s claim for Rs.37,742/- was rejected under Clause No.4.3.1, he has moved the

Forum for justice.

19. Hearing of the complaint:

A. Complainant’s argument:

The Complainant stated that the Respondent had rejected his claim citing Policy condition

No. 4.3.1. He was not satisfied with the decision of the respondent company to repudiate his

claim. The complainant prayed that his claim should be paid in full.

B. Insurer’s argument:

The representative of the Respondent stated that the complainant had policy since

05/06/2015. He (the complainant) was admitted with complaint of pain in renal area and

diagnosed as left lower uretic stone and operated upon. The surgery was done in the 2nd

year of the policy. So the claim fell under 2 year exclusion clause and was correctly

repudiated under policy condition No. 4.3.1 which reads as:

“Unless the Insured Person has Continuous Coverage in excess of twenty four

months with Us, expenses on treatment of the following illness are not payable –

4.3.1(7) – Stones in Urinary system”.

20. Result of hearing with both parties (Observations & Conclusion):

The point to be considered was whether the insurer was correct in rejecting the claim of the

insured citing policy clause no. 4.3.1.

Based on the submission of parties as above and the material made available to this Forum,

the following points emerged which were pertinent to decide the case:-

1. The Complainant was admitted in Maharshi Surgical Hospital, Ahmedabad for the

period from 14.12.16 to 15.12.16. He was operated for Lt. Ureteric Calculus. The

Complainant had lodged a claim for Rs 37,742/- The respondent had repudiated the

claim.

2. The Respondent had provided the Terms and Conditions of the policy. The policy was

in the 2nd year at the time of the claim/treatment. As per clause No. 4.3.1 of policy, a

waiting period of 2 years was applicable for the said ailment and procedure.

3. The subject Lt. Ureteric Calculus surgery took place within 2 year of the

Commencement of the policy.

4. The Respondent had correctly repudiated the claim.

5. The complainant submitted during the hearing that the policies issued to him did not

have the terms and conditions attached to them and should not be applied to deny his

claim. It is observed that the policy contained a clause that it is subject to the terms and

conditions of New Mediclaim 2012. Even assuming that the terms and conditions were

not attached as alleged by the complainant, nothing prevented him from obtaining the

missing terms and conditions from the insurer. Hence the Forum does not accept his

argument.

6. In view of the foregoing the complaint is not admitted.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by Complainant during the course of hearing the decision of the Respondent

needed no intervention. The complaint is therefore not admitted

21. In case the Order of this Forum is not acceptable to the Complainant, he can move any

appropriate Forum/Court of Law against the Respondent Insurer as he deems fit.

Dated at Ahmedabad on 5th Feb., 2019.

M. Vasantha Krishna

Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017)

Ombudsman: M. Vasantha Krishna

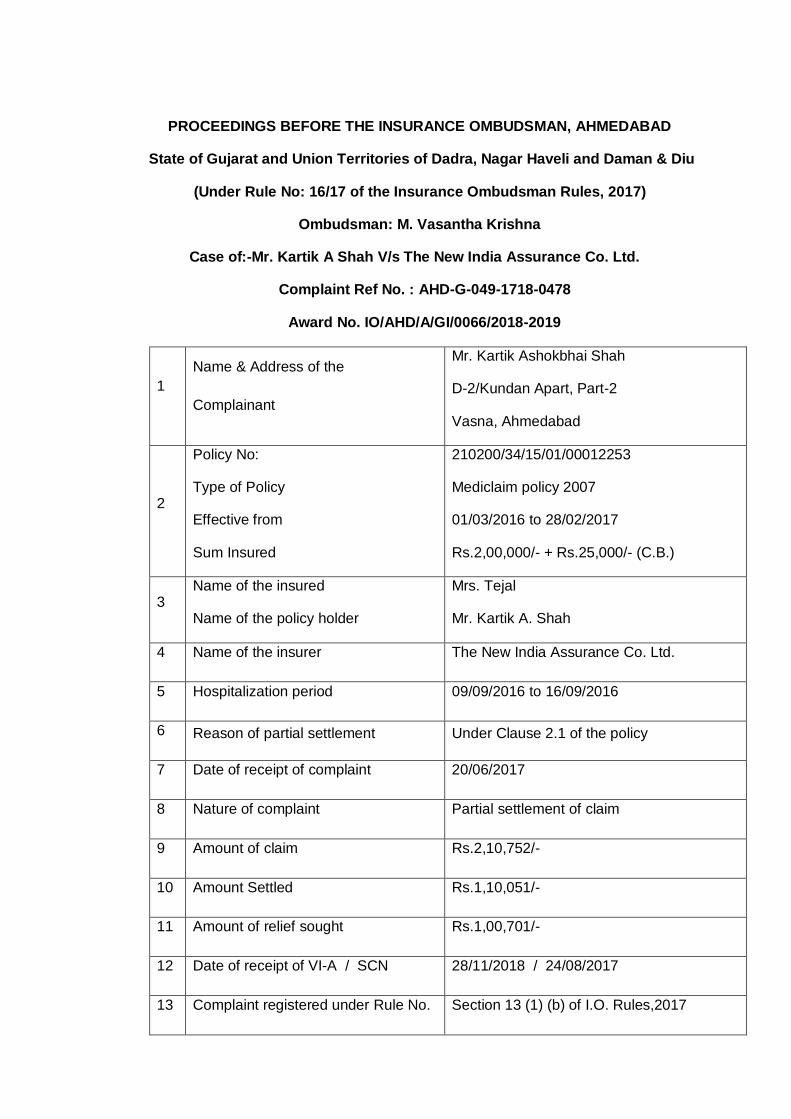

Case of:-Mr. Kartik A Shah V/s The New India Assurance Co. Ltd.

Complaint Ref No. : AHD-G-049-1718-0478

Award No. IO/AHD/A/GI/0066/2018-2019

1

Name & Address of the

Complainant

Mr. Kartik Ashokbhai Shah

D-2/Kundan Apart, Part-2

Vasna, Ahmedabad

2

Policy No:

Type of Policy

Effective from

Sum Insured

210200/34/15/01/00012253

Mediclaim policy 2007

01/03/2016 to 28/02/2017

Rs.2,00,000/- + Rs.25,000/- (C.B.)

3 Name of the insured

Name of the policy holder

Mrs. Tejal

Mr. Kartik A. Shah

4 Name of the insurer The New India Assurance Co. Ltd.

5 Hospitalization period 09/09/2016 to 16/09/2016

6 Reason of partial settlement Under Clause 2.1 of the policy

7 Date of receipt of complaint 20/06/2017

8 Nature of complaint Partial settlement of claim

9 Amount of claim Rs.2,10,752/-

10 Amount Settled Rs.1,10,051/-

11 Amount of relief sought Rs.1,00,701/-

12 Date of receipt of VI-A / SCN 28/11/2018 / 24/08/2017

13 Complaint registered under Rule No. Section 13 (1) (b) of I.O. Rules,2017

14 Date of hearing/place 28/11/2018 / Ahmedabad

15

Representation at the hearing:

For the Complainant

For the Insurer

Mr. Kartik A Shah

Miss Shikha Kashyap

16 Complainant how disposed Award

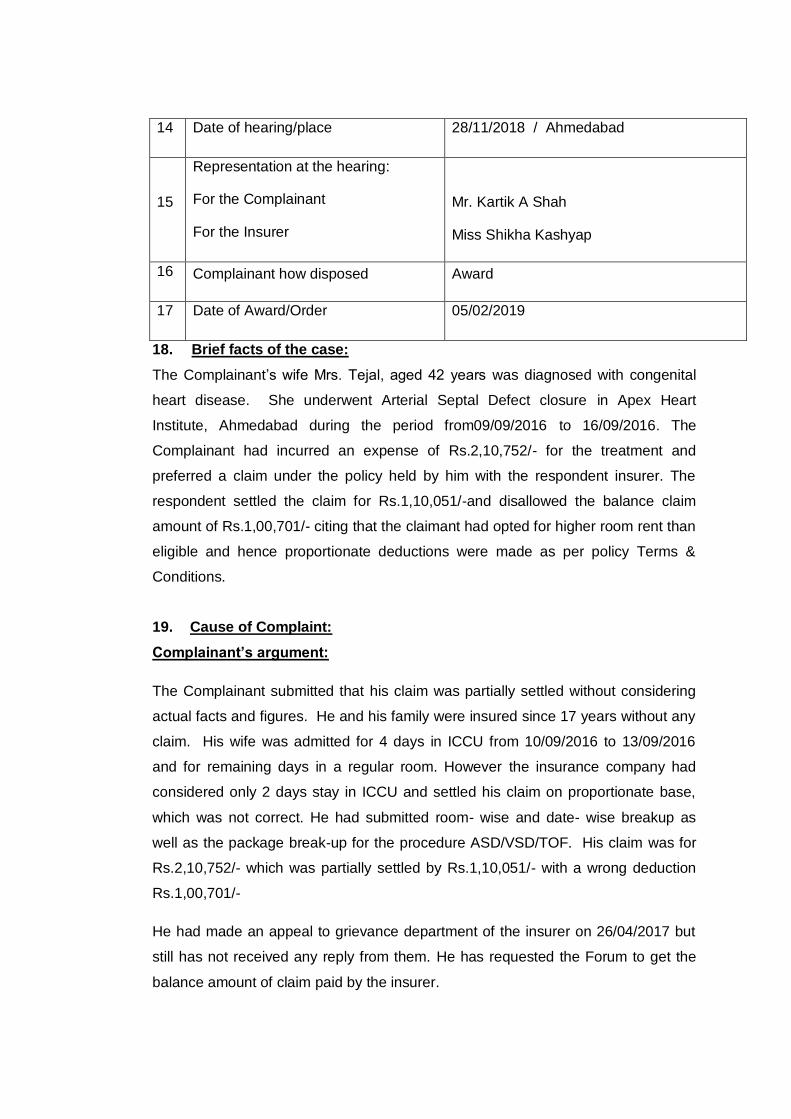

17 Date of Award/Order 05/02/2019

18. Brief facts of the case:

The Complainant’s wife Mrs. Tejal, aged 42 years was diagnosed with congenital

heart disease. She underwent Arterial Septal Defect closure in Apex Heart

Institute, Ahmedabad during the period from09/09/2016 to 16/09/2016. The

Complainant had incurred an expense of Rs.2,10,752/- for the treatment and

preferred a claim under the policy held by him with the respondent insurer. The

respondent settled the claim for Rs.1,10,051/-and disallowed the balance claim

amount of Rs.1,00,701/- citing that the claimant had opted for higher room rent than

eligible and hence proportionate deductions were made as per policy Terms &

Conditions.

19. Cause of Complaint:

Complainant’s argument:

The Complainant submitted that his claim was partially settled without considering

actual facts and figures. He and his family were insured since 17 years without any

claim. His wife was admitted for 4 days in ICCU from 10/09/2016 to 13/09/2016

and for remaining days in a regular room. However the insurance company had

considered only 2 days stay in ICCU and settled his claim on proportionate base,

which was not correct. He had submitted room- wise and date- wise breakup as

well as the package break-up for the procedure ASD/VSD/TOF. His claim was for

Rs.2,10,752/- which was partially settled by Rs.1,10,051/- with a wrong deduction

Rs.1,00,701/-

He had made an appeal to grievance department of the insurer on 26/04/2017 but

still has not received any reply from them. He has requested the Forum to get the

balance amount of claim paid by the insurer.

Insurer’s argument:

The Respondent’s representative submitted that the claimant was eligible for room

rent of Rs.2000/- per day (Rs.4000/- for ICU) as the sum insured was Rs.2,00,000/-.

Insured had availed higher room category of Rs.5500/- per day instead of eligible

Rs.2000/- per day and ICU charges of Rs.6000/- per day instead of Rs.4000/- per

day. Hence, insured was liable for proportionate deductions for other expenses as

per clause 2.1 of the policy Terms & Conditions.

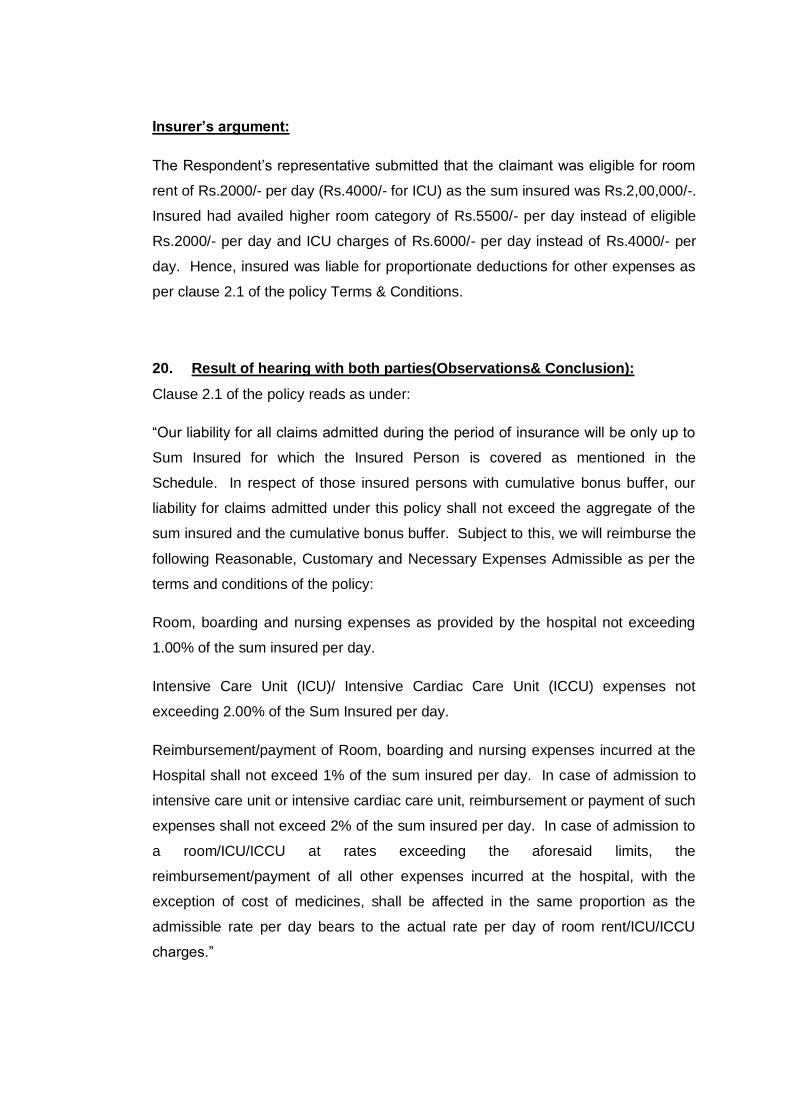

20. Result of hearing with both parties(Observations& Conclusion):

Clause 2.1 of the policy reads as under:

“Our liability for all claims admitted during the period of insurance will be only up to

Sum Insured for which the Insured Person is covered as mentioned in the

Schedule. In respect of those insured persons with cumulative bonus buffer, our

liability for claims admitted under this policy shall not exceed the aggregate of the

sum insured and the cumulative bonus buffer. Subject to this, we will reimburse the

following Reasonable, Customary and Necessary Expenses Admissible as per the

terms and conditions of the policy:

Room, boarding and nursing expenses as provided by the hospital not exceeding

1.00% of the sum insured per day.

Intensive Care Unit (ICU)/ Intensive Cardiac Care Unit (ICCU) expenses not

exceeding 2.00% of the Sum Insured per day.

Reimbursement/payment of Room, boarding and nursing expenses incurred at the

Hospital shall not exceed 1% of the sum insured per day. In case of admission to

intensive care unit or intensive cardiac care unit, reimbursement or payment of such

expenses shall not exceed 2% of the sum insured per day. In case of admission to

a room/ICU/ICCU at rates exceeding the aforesaid limits, the

reimbursement/payment of all other expenses incurred at the hospital, with the

exception of cost of medicines, shall be affected in the same proportion as the

admissible rate per day bears to the actual rate per day of room rent/ICU/ICCU

charges.”

1. The Respondent had submitted an investigation report dated 17/07/2017 of Dr.

S.J. Dumra who had scrutinized the claim file as also visited the hospital and

gave his opinion that the deduction was in order as per policy terms and

conditions.

2. The respondent had also submitted a certificate dated 25/07/2017 of Apex

hospital wherein it was stated the CTOT (Clinical Trials in Organ

Transplantation) charges were same for all categories and it was not connected

with room charge.

3. The complainant had incurred an expense of Rs.2,10,752/-. The surgery was

done under a package of Rs.1,85,000/- (which includes Room charges, OT,

Pathology/Investigation, CTOT charges, Surgeon and Physiotherapist charges).

A break-up was demanded by the respondent which was submitted by the

complainant.

4. As mentioned by the complainant in his representation, he received a discount

of Rs. 5,000 in the room rent/ICU charges with the result that the package cost

came down to Rs. 1,80,000 and the total expenditure to Rs. 2,05,752. Because

of the discount received, per day charges for Room and ICU were reduced to

Rs. 5,500 and Rs. 6,000 respectively against the eligible tariff of Rs. 2,000 and

Rs. 4,000.

5. Deductions made by the Respondent towards non-payable items were found to

be in order and there is no scope to interfere with the same. Reducing other

charges in proportion of the eligible rent/ICU charges to the actual (6000/11500)

as provided in the policy, the amount payable worked out to Rs. 1,09,801. Since

the Respondent has already paid an amount of Rs. 1,10,051, they have no

further liability.

6. In view of the above, the complaint is not admitted.

AWARD

Taking into account the facts & circumstances of the case and the

submissions made by both the parties during the course of hearing the

decision of the Respondent needed no intervention. The complaint is not

admitted.

21. If the award is not acceptable to the complainant, he may approach appropriate

court / forum for redressal of his grievance against the insurer, as he thinks fit.

Dated at Ahmedabad on 5th Feb., 2019

M. Vasantha Krishna Insurance Ombudsman

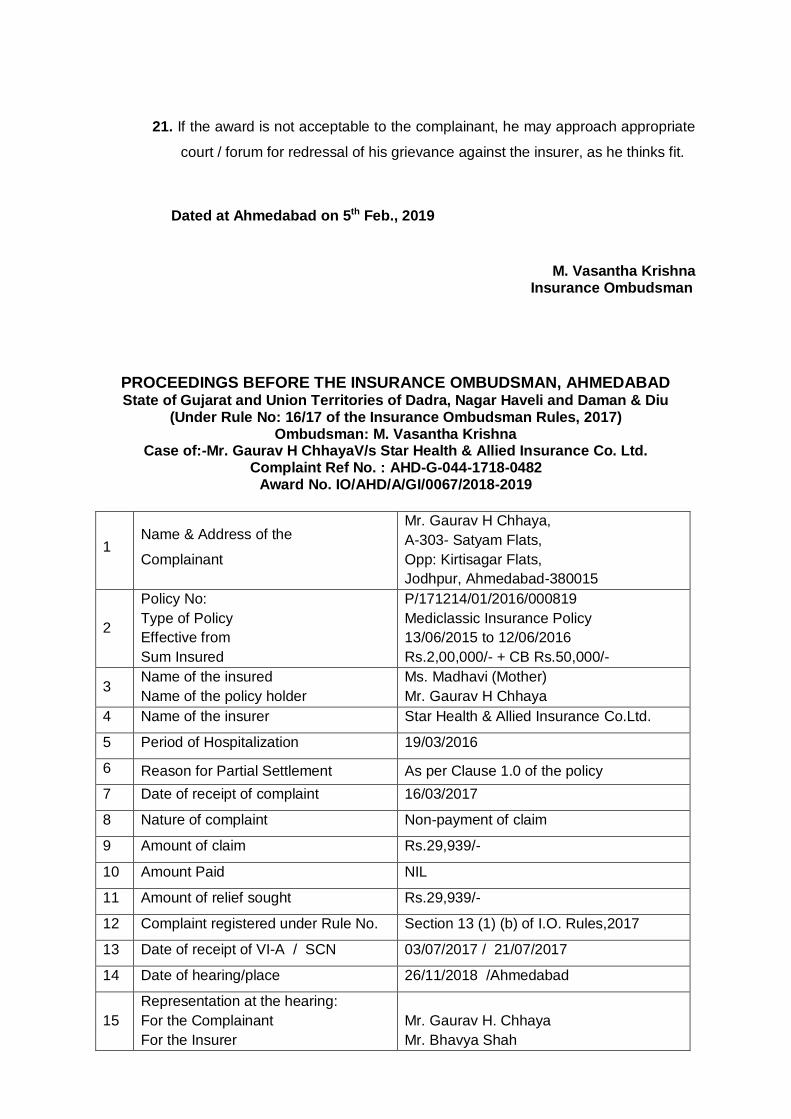

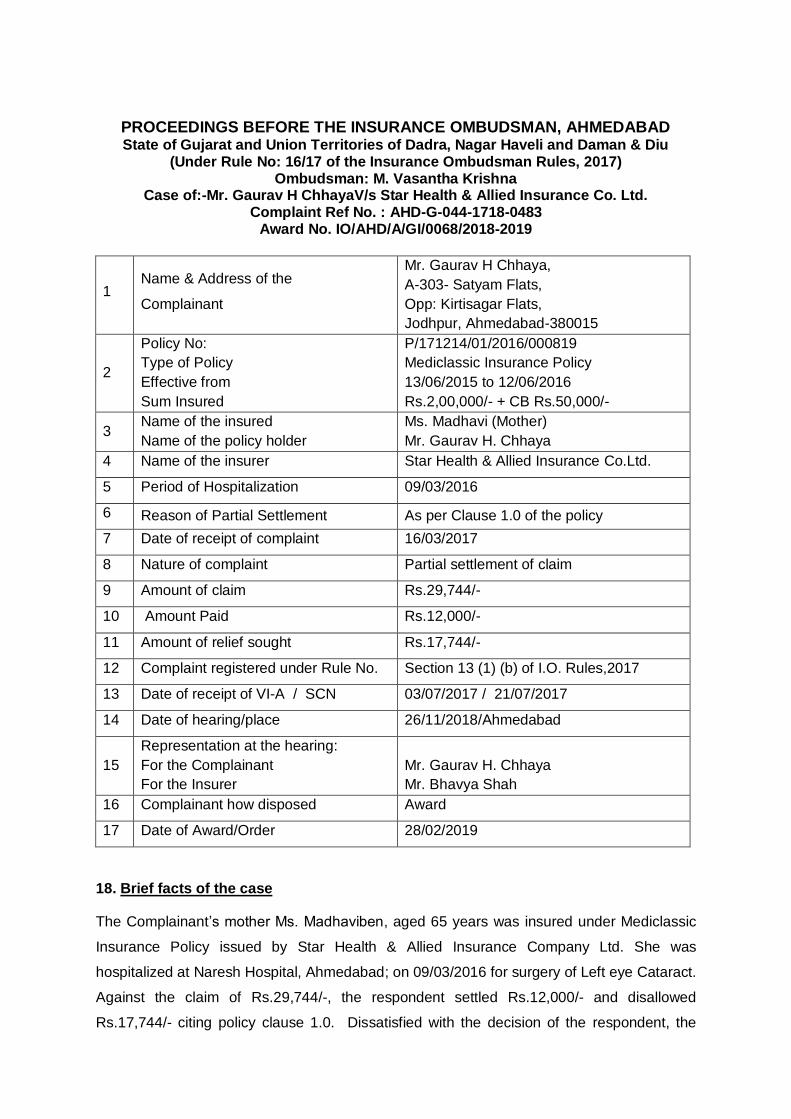

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Ombudsman: M. Vasantha Krishna

Case of:-Mr. Gaurav H ChhayaV/s Star Health & Allied Insurance Co. Ltd. Complaint Ref No. : AHD-G-044-1718-0482

Award No. IO/AHD/A/GI/0067/2018-2019

1 Name & Address of the

Complainant

Mr. Gaurav H Chhaya,

A-303- Satyam Flats,

Opp: Kirtisagar Flats,

Jodhpur, Ahmedabad-380015

2

Policy No:

Type of Policy

Effective from

Sum Insured

P/171214/01/2016/000819

Mediclassic Insurance Policy

13/06/2015 to 12/06/2016

Rs.2,00,000/- + CB Rs.50,000/-

3 Name of the insured

Name of the policy holder

Ms. Madhavi (Mother)

Mr. Gaurav H Chhaya

4 Name of the insurer Star Health & Allied Insurance Co.Ltd.

5 Period of Hospitalization 19/03/2016

6 Reason for Partial Settlement As per Clause 1.0 of the policy

7 Date of receipt of complaint 16/03/2017

8 Nature of complaint Non-payment of claim

9 Amount of claim Rs.29,939/-

10 Amount Paid NIL

11 Amount of relief sought Rs.29,939/-

12 Complaint registered under Rule No. Section 13 (1) (b) of I.O. Rules,2017

13 Date of receipt of VI-A / SCN 03/07/2017 / 21/07/2017

14 Date of hearing/place 26/11/2018 /Ahmedabad

15

Representation at the hearing:

For the Complainant

For the Insurer

Mr. Gaurav H. Chhaya

Mr. Bhavya Shah

16 Complainant how disposed Award

17 Date of Award/Order 28/02/2019

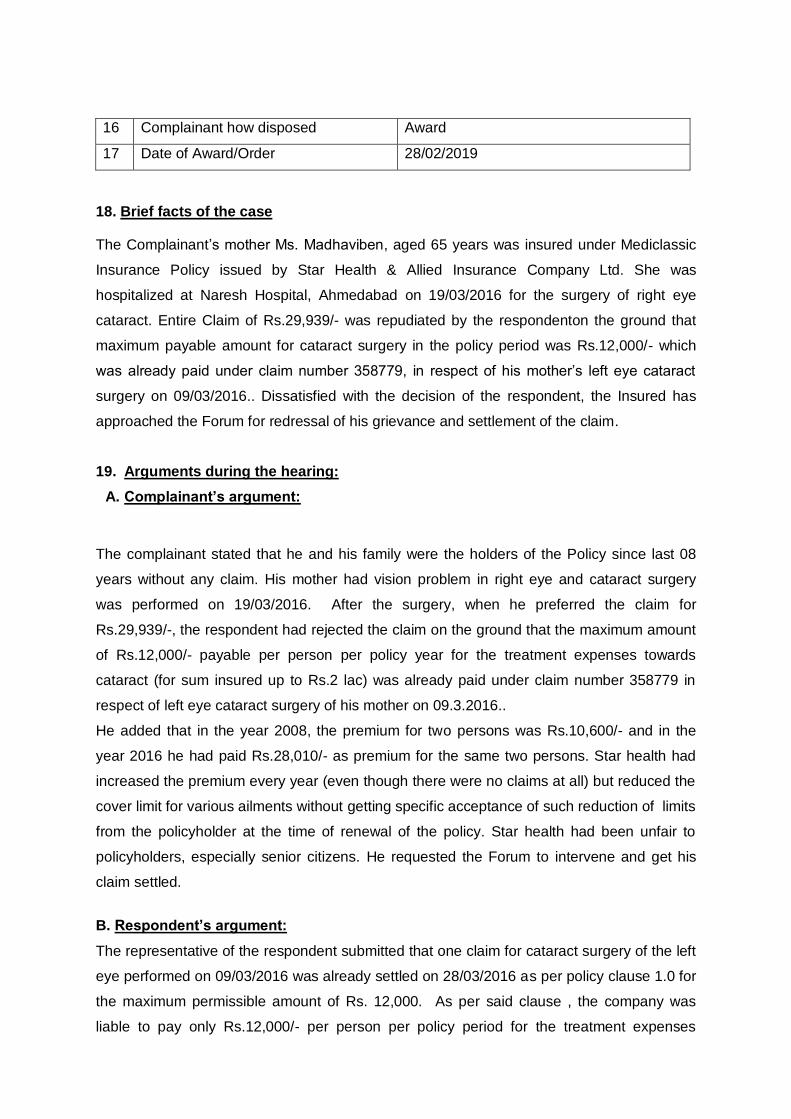

18. Brief facts of the case

The Complainant’s mother Ms. Madhaviben, aged 65 years was insured under Mediclassic

Insurance Policy issued by Star Health & Allied Insurance Company Ltd. She was

hospitalized at Naresh Hospital, Ahmedabad on 19/03/2016 for the surgery of right eye

cataract. Entire Claim of Rs.29,939/- was repudiated by the respondenton the ground that

maximum payable amount for cataract surgery in the policy period was Rs.12,000/- which

was already paid under claim number 358779, in respect of his mother’s left eye cataract

surgery on 09/03/2016.. Dissatisfied with the decision of the respondent, the Insured has

approached the Forum for redressal of his grievance and settlement of the claim.

19. Arguments during the hearing:

A. Complainant’s argument:

The complainant stated that he and his family were the holders of the Policy since last 08

years without any claim. His mother had vision problem in right eye and cataract surgery

was performed on 19/03/2016. After the surgery, when he preferred the claim for

Rs.29,939/-, the respondent had rejected the claim on the ground that the maximum amount

of Rs.12,000/- payable per person per policy year for the treatment expenses towards

cataract (for sum insured up to Rs.2 lac) was already paid under claim number 358779 in

respect of left eye cataract surgery of his mother on 09.3.2016..

He added that in the year 2008, the premium for two persons was Rs.10,600/- and in the

year 2016 he had paid Rs.28,010/- as premium for the same two persons. Star health had

increased the premium every year (even though there were no claims at all) but reduced the

cover limit for various ailments without getting specific acceptance of such reduction of limits

from the policyholder at the time of renewal of the policy. Star health had been unfair to

policyholders, especially senior citizens. He requested the Forum to intervene and get his

claim settled.

B. Respondent’s argument:

The representative of the respondent submitted that one claim for cataract surgery of the left

eye performed on 09/03/2016 was already settled on 28/03/2016 as per policy clause 1.0 for

the maximum permissible amount of Rs. 12,000. As per said clause , the company was

liable to pay only Rs.12,000/- per person per policy period for the treatment expenses

towards cataract for sum insured up to Rs.2,00,000/-. Since the present claim was in the

same policy period, noting was payable towards the same. In reply to a question whether

they had provided the terms and conditions to the insured he replied that he did not know.

20. Result of hearing with both parties (Observation & Conclusion):

Based on the submissions made by both the parties and the documents submitted, the

Forum observes as below.

1. The limit of Rs.12,000/- for cataract surgery was clearly mentioned in the policy terms

and conditions and there is no ambiguity about the same.

2. The complainant pointed out that the policy had a no claim bonus (cumulative bonus) of

Rs.50,000 and argued that if the claim exceeded the policy limit, the excess amount

should have been disbursed out of the bonus, which was not done in his case.

However, the Forum is of the opinion that the cumulative bonus can be utilised only

when the sum insured under the policy is not adequate to meet the claim. Moreover,

the manner in which indemnity for cataract surgery has been limited in the policy

precludes utilisation of cumulative bonus as demanded by the complainant. Having

expressed this view, the Forum would also point out that the policy is silent about how

cumulative bonus will be used in settlement of the claim and the insurer is advised to

make an explicit provision in this regard.

3. The complainant also stated that nowhere in Ahmedabad, which is a metro city, one can

get cataract surgery done at the low limit fixed by the insurer. While this is true, it

cannot be a basis for overlooking the specific capping of indemnity for cataract surgery

in the policy.

4. The complainant was continuously insured with the respondent since the year 2008 and

the first policy incepted on 13.06.2018. His main argument is that the respondent

insurer had unilaterally changed the policy limits for various ailments without notice and

without taking the consent of the policyholders. The Forum has looked in to this aspect

and has examined the policy wording for this product over the years. It is observed that

the policy version in 2008 had limited cataract surgery to Rs. 20,000 per eye and Rs.

30,000 in entire policy period and these limits applied irrespective of the sum insured

under the policy. It appears that the policy wording was revised in the year 2013 when

the current limits for cataract surgery linked to the sum insured have been incorporated.

On enquiry with the Head Office of the insurer, it was confirmed by them that

policyholders are notified whenever the product undergoes revision, as stipulated in the

product filing guidelines of the Regulator. However, they were unable to confirm that in

this specific case the customer was notified of the changes. In the absence of such

confirmation, it would be fair to allow the benefit of the pre-revision limits of cataract

surgery to the complainant. Since the applicable annual limit prior to revision was Rs.

30,000 for cataract surgery, and an amount of Rs. 20,000 is already exhausted by

means of the award given by this Forum in complaint no. AHD-G-044-1718-0483, the

insurer should pay an additional amount of Rs. 10,000 in settlement of the present

claim.

5. The complaint is therefore admitted.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of hearing, the Forum directs the

respondent insurer to pay an amount of Rs. 10,000 to the complainant in full and

final settlement of the claim. In addition, interest as per rule 17(7) of the

Insurance Ombudsman Rules, 2017 is also payable. The complaint is therefore

partially admitted.

21. The attention of the Complainant and the Insurer is hereby invited to the following

provisions of the Insurance Ombudsman Rules, 2017:

A) According to Rule 17(6) of the Insurance Ombudsman Rules, 2017, the

Insurer shall comply with the award within thirty days of the receipt of the award

and intimate compliance of the same to the Ombudsman.

B) According to Rule 17(8) of the Insurance Ombudsman Rules, 2017, the

award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 28th Feb., 2019

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Ombudsman: M. Vasantha Krishna

Case of:-Mr. Gaurav H ChhayaV/s Star Health & Allied Insurance Co. Ltd. Complaint Ref No. : AHD-G-044-1718-0483

Award No. IO/AHD/A/GI/0068/2018-2019

1 Name & Address of the

Complainant

Mr. Gaurav H Chhaya,

A-303- Satyam Flats,

Opp: Kirtisagar Flats,

Jodhpur, Ahmedabad-380015

2

Policy No:

Type of Policy

Effective from

Sum Insured

P/171214/01/2016/000819

Mediclassic Insurance Policy

13/06/2015 to 12/06/2016

Rs.2,00,000/- + CB Rs.50,000/-

3 Name of the insured

Name of the policy holder

Ms. Madhavi (Mother)

Mr. Gaurav H. Chhaya

4 Name of the insurer Star Health & Allied Insurance Co.Ltd.

5 Period of Hospitalization 09/03/2016

6 Reason of Partial Settlement As per Clause 1.0 of the policy

7 Date of receipt of complaint 16/03/2017

8 Nature of complaint Partial settlement of claim

9 Amount of claim Rs.29,744/-

10 Amount Paid Rs.12,000/-

11 Amount of relief sought Rs.17,744/-

12 Complaint registered under Rule No. Section 13 (1) (b) of I.O. Rules,2017

13 Date of receipt of VI-A / SCN 03/07/2017 / 21/07/2017

14 Date of hearing/place 26/11/2018/Ahmedabad

15

Representation at the hearing:

For the Complainant

For the Insurer

Mr. Gaurav H. Chhaya

Mr. Bhavya Shah

16 Complainant how disposed Award

17 Date of Award/Order 28/02/2019

18. Brief facts of the case

The Complainant’s mother Ms. Madhaviben, aged 65 years was insured under Mediclassic

Insurance Policy issued by Star Health & Allied Insurance Company Ltd. She was

hospitalized at Naresh Hospital, Ahmedabad; on 09/03/2016 for surgery of Left eye Cataract.

Against the claim of Rs.29,744/-, the respondent settled Rs.12,000/- and disallowed

Rs.17,744/- citing policy clause 1.0. Dissatisfied with the decision of the respondent, the

complainant has approached the Forum for redressal of his grievance and settlement of the

balance amount of claim for Rs.17,744/-.

19. Arguments during the hearing:

C. Complainant’s argument:

The complainant stated that he and his family were the holders of the Policyfor last 8 years

without any claim. His mother had some problem in left eye and cataract surgery was

performed on 09/03/2016. After the surgery, when he preferred the claim for Rs.29,744/-,

the respondent had settled only Rs.12,000/- and deducted Rs.17,744/- stating that a

maximum Rs.12,000/- is payable per person per policy year for the treatment expenses

towards cataract for sum insured up to Rs.2 lac.

He added that in the year 2008, the premium for two persons was Rs.10,600/- and in the

year 2016 he had paid Rs.28,010/- as premium for the same two persons. Star health had

increased the premium every year (even though there were no claims at all) but reduced the

cover limit for various ailments without getting specific acceptance of such reduction of limits

from the policyholder at the time of renewal of the policy. Star health had been unfair to

policyholders, especially senior citizens. He requested the Forum to intervene and get his

balance amount of claim paid.

D. Respondent’s argument:

The representative of the respondent stated that the claim was settled forRs. 12,000/- as per

policy clause 1.0. As per said clause , the Company was liable to pay only Rs.12,000/- per

person per policy period for the treatment expenses towards cataract for sum insured up to

Rs.2,00,000/-. In reply to a questionby the Forum whether they had provided the terms and

conditions to the insured, the representative of the insurer replied that he does not know.

20. Result of hearing with both parties(Observations& Conclusion):

Based on the submissions made by both the parties and the documents submitted, the

Forum observes as below.

6. The limit of Rs.12,000/- for cataract surgery was clearly mentioned in the policy terms

and conditions and there is no ambiguity about the same.

7. The complainant pointed out that the policy had a no claim bonus (cumulative bonus) of

Rs.50,000 and argued that if the claim exceeded the policy limit, the excess amount

should have been disbursed out of the bonus, which was not done in his case.

However, the Forum is of the opinion that the cumulative bonus can be utilised only

when the sum insured under the policy is not adequate to meet the claim. Moreover,

the manner in which indemnity for cataract surgery has been limited in the policy

precludes utilisation of cumulative bonus as demanded by the complainant. Having

expressed this view, the Forum would also point out that the policy is silent about how

cumulative bonus will be used in settlement of the claim and the insurer is advised to

make an explicit provision in this regard.

8. The complainant also stated that nowhere in Ahmedabad, which is a metro city, one can

get cataract surgery done at the low limit fixed by the insurer. While this is true, it

cannot be a basis for overlooking the specific capping of indemnity for cataract surgery

in the policy.

9. The complainant was continuously insured with the respondent since the year 2008 and

the first policy incepted on 13.06.2018. His main argument is that the respondent

insurer had unilaterally changed the policy limits for various ailments without notice and

without taking the consent of the policyholders. The Forum has looked in to this aspect

and has examined the policy wording for this product over the years. It is observed that

the policy version in 2008 had limited cataract surgery to Rs. 20,000 per eye and Rs.

30,000 in entire policy period and these limits applied irrespective of the sum insured

under the policy. It appears that the policy wording was revised in the year 2013 when

the current limits for cataract surgery linked to the sum insured have been incorporated.

On enquiry with the Head Office of the insurer, it was confirmed by them that

policyholders are notified whenever the product undergoes revision, as stipulated in the

product filing guidelines of the Regulator. However, they were unable to confirm that in

this specific case the customer was notified of the changes. In the absence of such

confirmation, it would be fair to allow the benefit of the pre-revision limits of cataract

surgery to the complainant. Since the applicable limit prior to revision was Rs. 20,000

per eye, the insurer should pay an additional amount of Rs. 8,000 in settlement of the

claim.

10. The complaint is therefore admitted.

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties during the course of hearing, the Forum directs the

respondent insurer to pay an additional amount of Rs. 8,000 to the complainant in

full and final settlement of the claim. In addition, interest as per rule 17(7) of the

Insurance Ombudsman Rules, 2017 is also payable. The complaint is therefore

partially admitted.

21. The attention of the Complainant and the Insurer is hereby invited to the following

provisions of the Insurance Ombudsman Rules, 2017:

C) According to Rule 17(6) of the Insurance Ombudsman Rules, 2017, the

Insurer shall comply with the award within thirty days of the receipt of the award

and intimate compliance of the same to the Ombudsman.

D) According to Rule 17(8) of the Insurance Ombudsman Rules, 2017, the

award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 28th Feb., 2019

M. Vasantha Krishna

Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

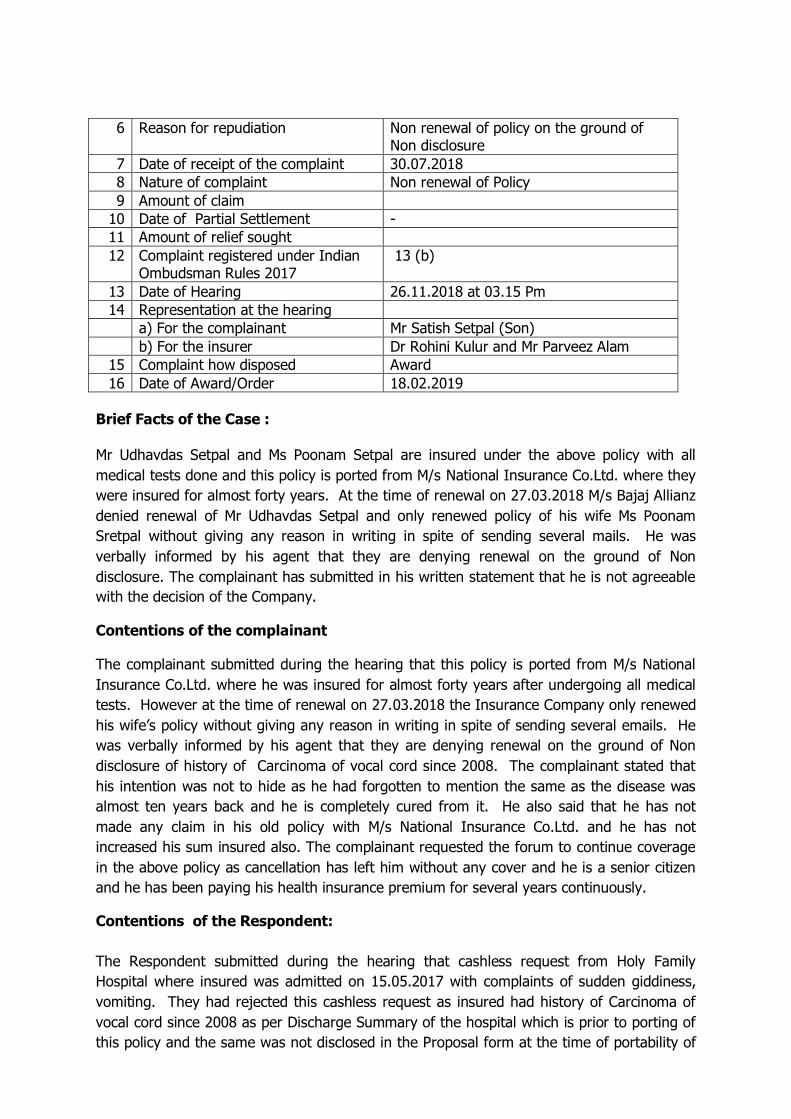

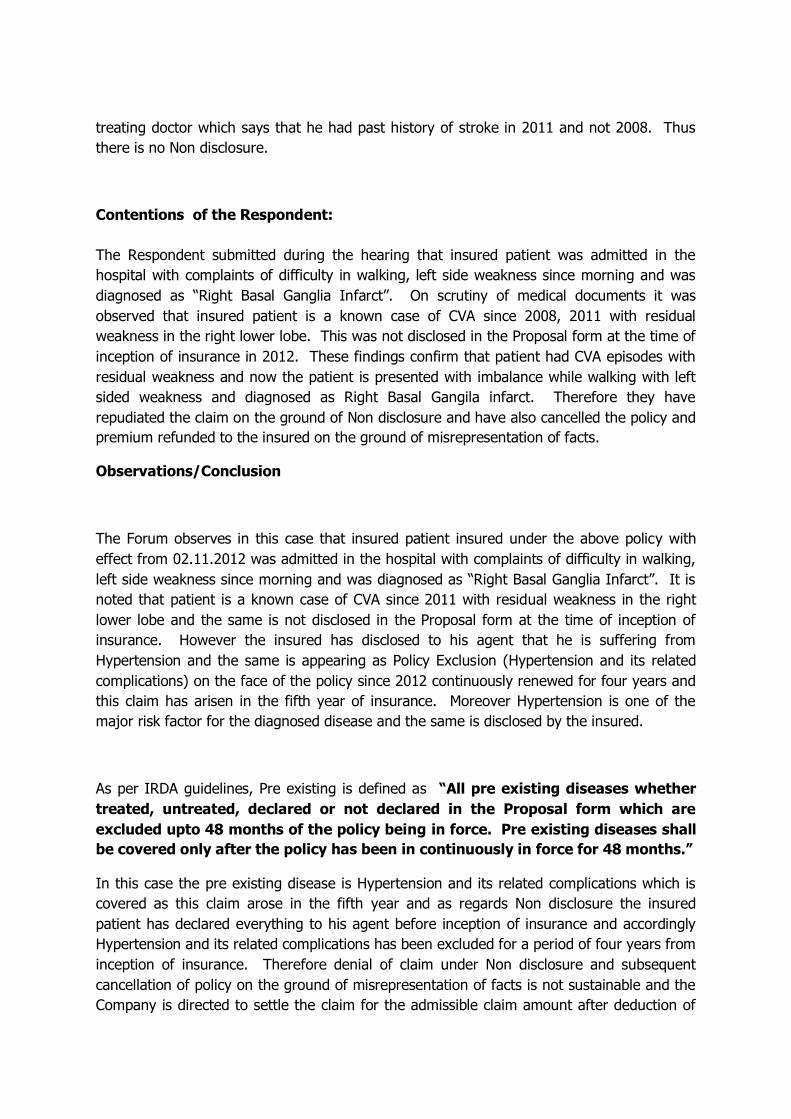

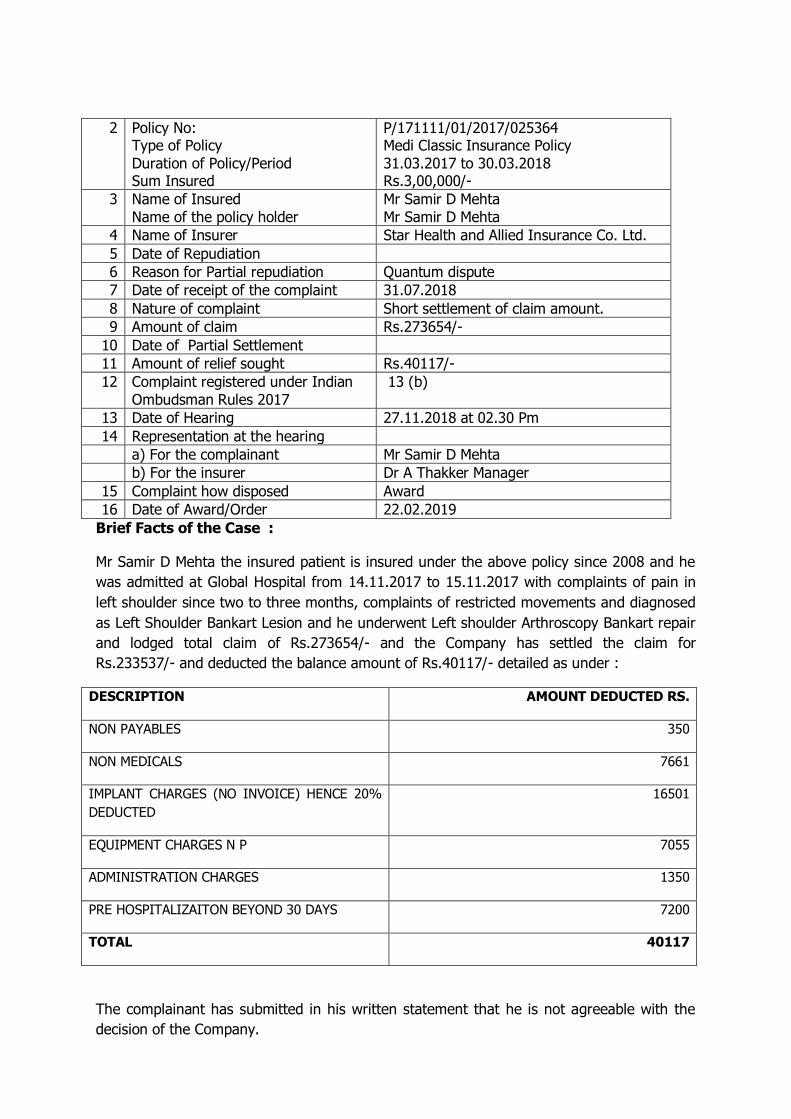

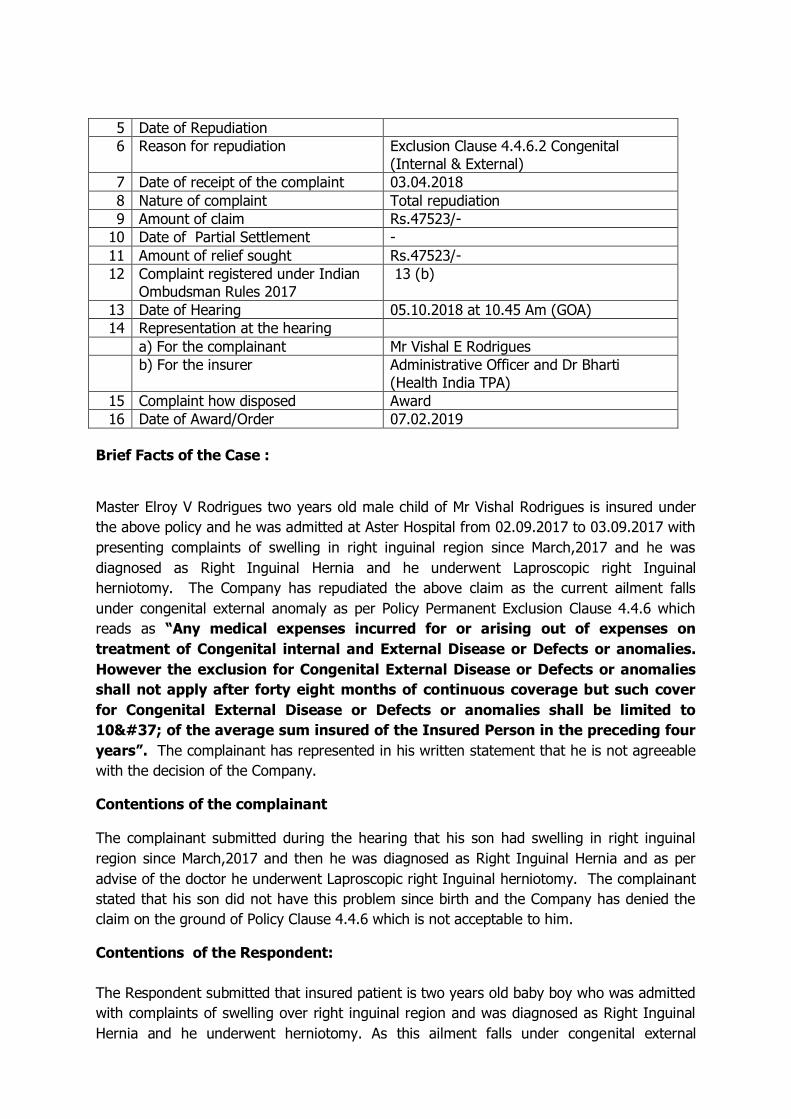

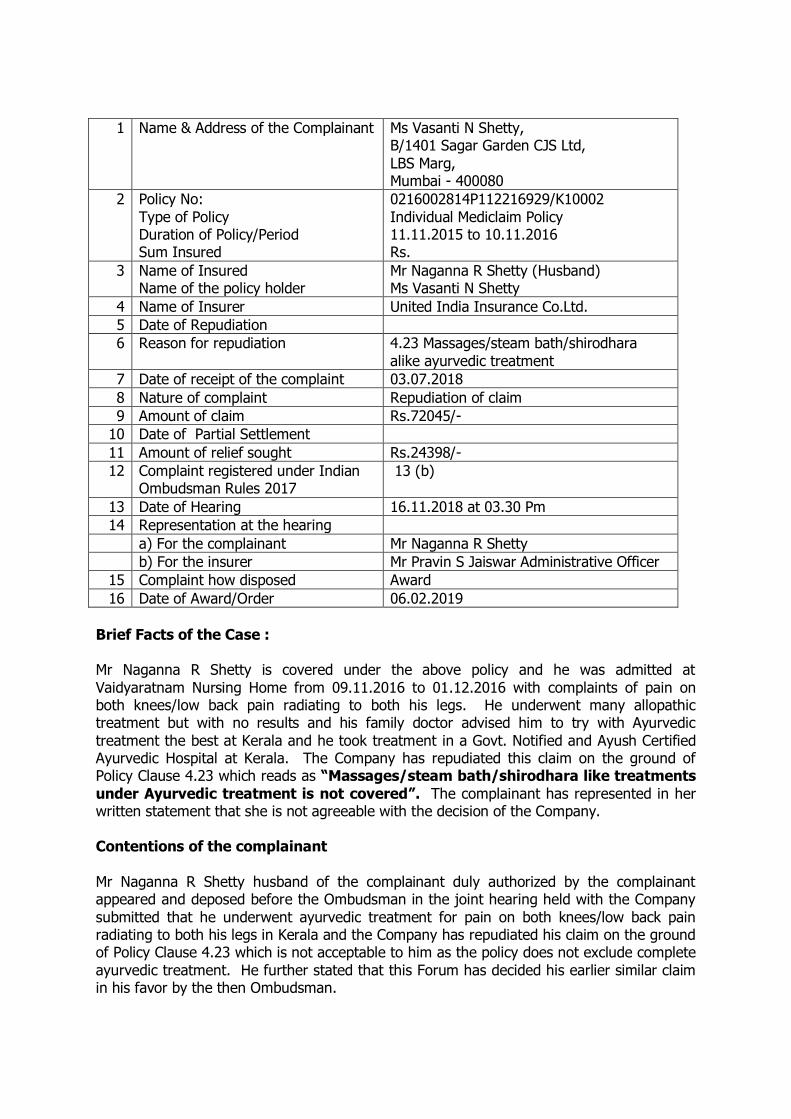

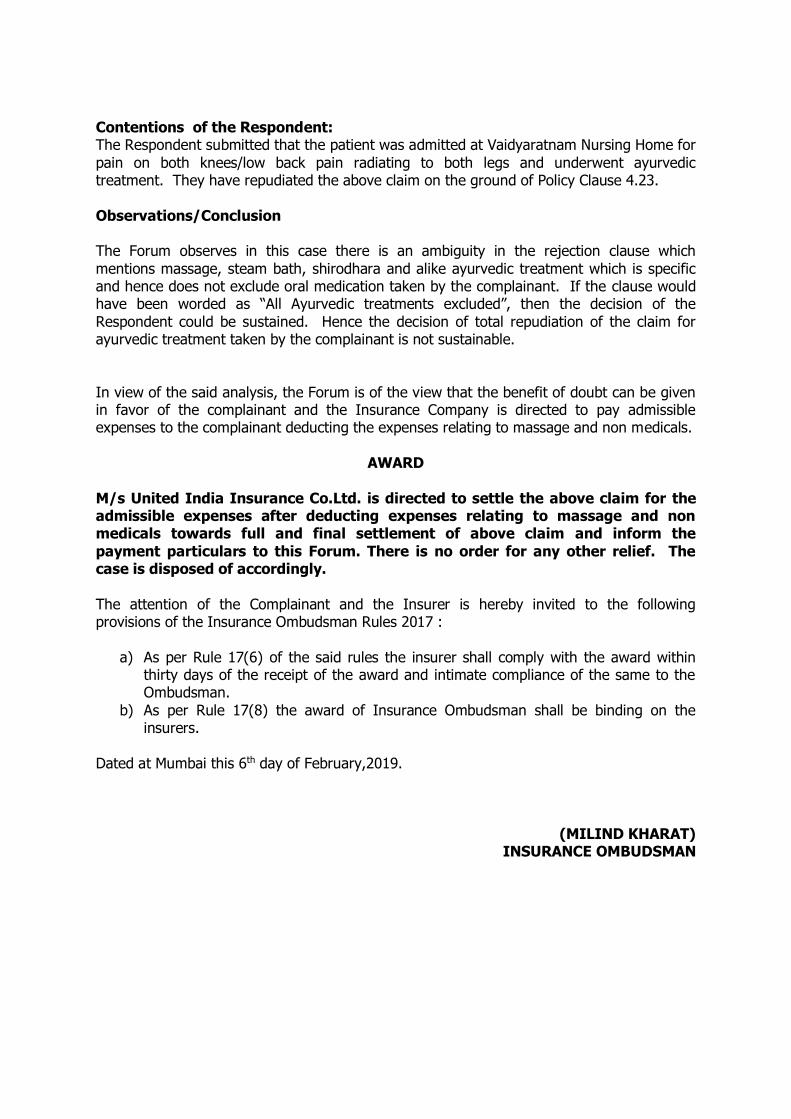

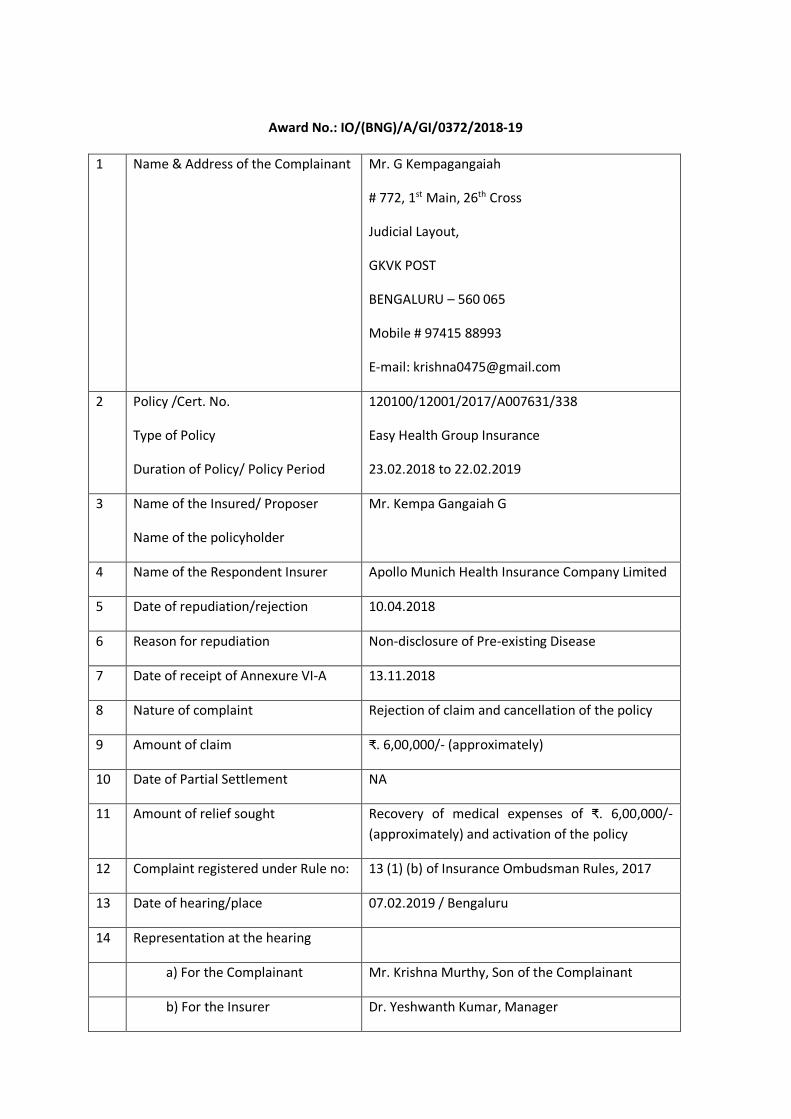

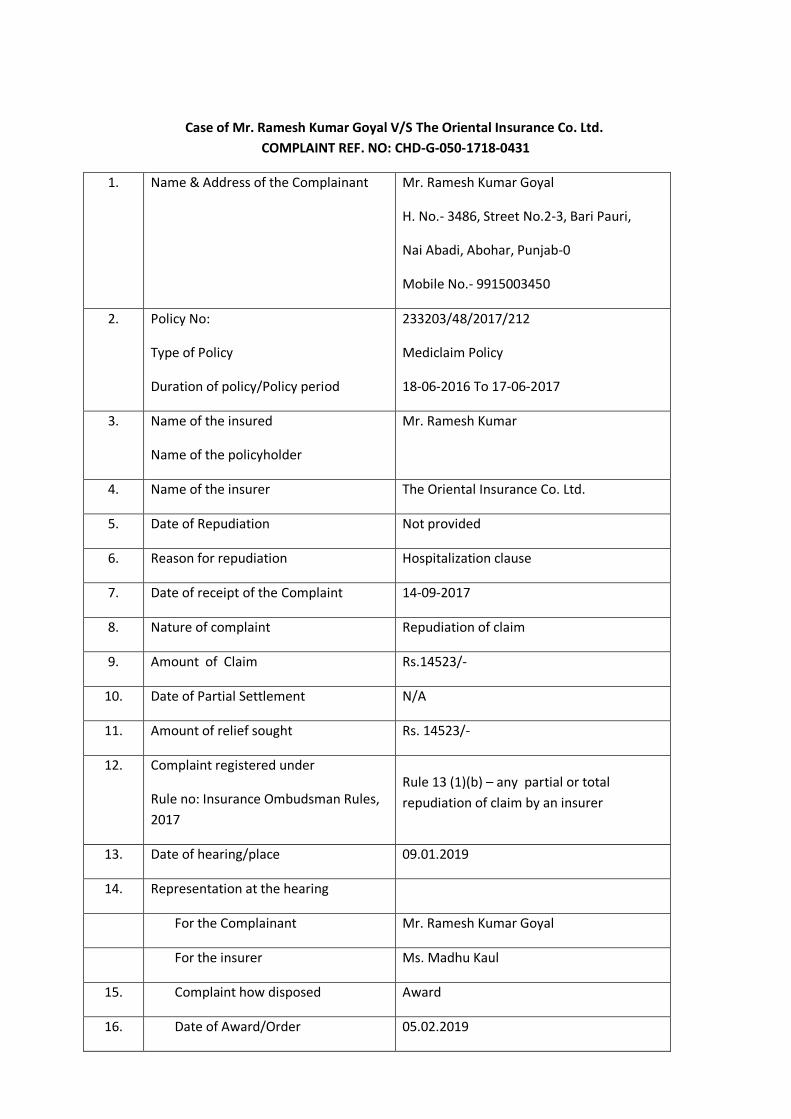

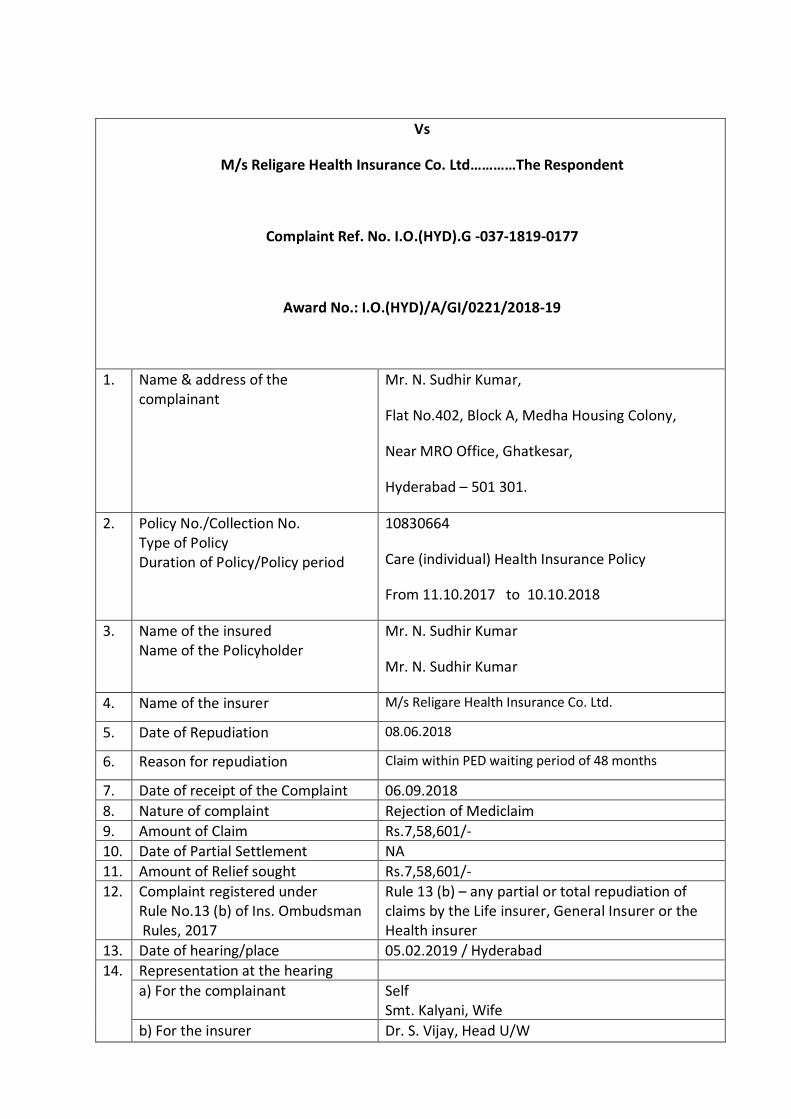

(Under Rule No: 16/17 of the Insurance Ombudsman Rules, 2017) Case of:-Mr. Khatumbara M. Ilyas V/S The New India Assurance Co. Ltd.

Ombudsman: M. Vasantha Krishna Complaint No.: AHD-G-049-1718-0312

Award No. IO/AHD/A/GI/0058/20018-2019

1 Name of the Complainant Mr. Khatumbara M. Ilyas

205, Arshad Residency,Opp. Ambar

Tower,100 ft. Ring Road,

Ahmedabad-380055

2 Policy No:

Type of Policy

Duration of Policy/Policy period

21040034150100008053

Mediclaim Policy 2007

22.03.2017 to 21.03.2018

3 Name of the insured

Name of the policy holder

Mr. Arsh M. Ilyas

Mr. Khatumbara M. Ilyas

4 Name of the insurer The New India Assurance Co. Ltd.

5 Hospitalization Period 06.01.2017 to 07.01.2017

6 Reason of Repudiation As per terms and conditions of the policy

7 Date of receipt of complaint 26.05.2017

8 Nature of complaint Partial Repudiation of claim.

9 Amount of claim Rs.63,884/-

10 Amount Settled Rs.44,984/-

11 Amount of relief sought Rs.18,900/-

12 Complaint registered under Rule No. Rule 13(1)(b) of the I.O. Rules, 2017

13 Date of hearing/place 28.11.2018/Ahmedabad

14 Representation at the hearing:

For the Complainant

For the Insurer

Mr Khatumbara N. Ilyas

Mr Dharmin H. Zaveri,

15 Complainant how disposed AWARD

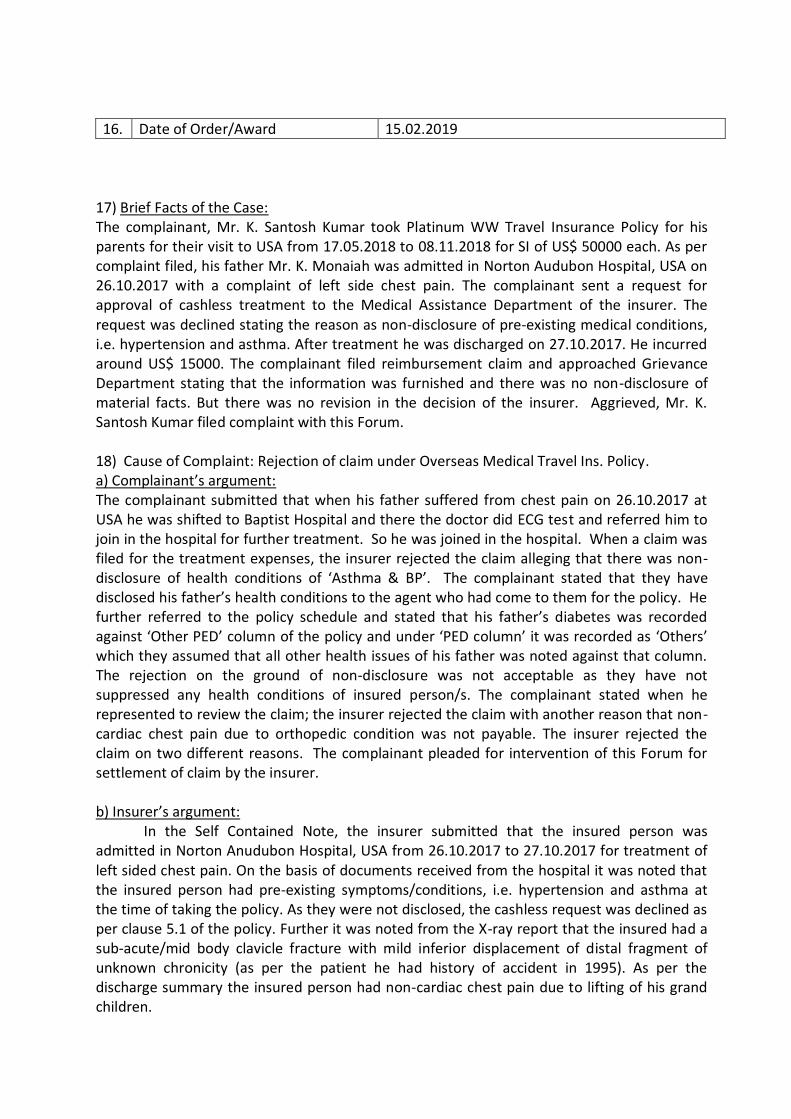

16. Date of Award / Order 05/02/2019

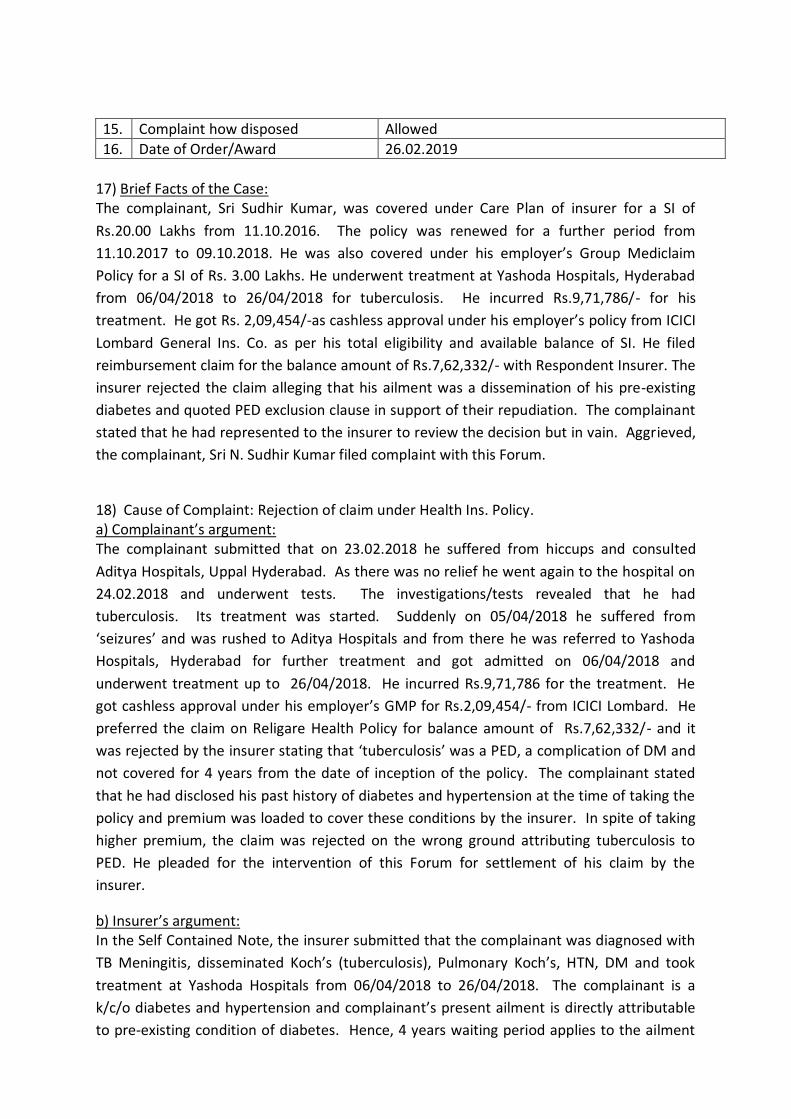

17. Brief facts of the case:

The Complainant’s son Mr. Arsh was admitted at Adwait ENT Hospital on 06.01.2017 and

discharged on 07.01.2017. He was diagnosed and treated for Adenoid hypertrophy +

tonsillitis. After discharge he submitted a claim for Rs.63,884/- which was settled for

Rs.44,984/-after deduction of Rs.18,900/- towards non payable items. Aggrieved by the

decision of the Company the Complainant has approached the Forum to redress his

grievance for settlement of his claim for balance amount of Rs.18,900/-.

18. Arguments by the Complainant:

The Complainant had stated that the Insurance Company had wrongly deducted Rs.18,900/-

from the claim for treatment of his son Mr. Arsh. He had submitted a letter dated 17.03.2017

from the Adwait Hospital confirming that the coblater the cost of which was disallowed, is not

an instrument but is a disposable blade used for every surgery(tonsillectomy and adenoid)

requiring coblation. It is just like disposable syringe & needle. The Complainant had urged

that after clarification from the hospital, the deduction by the Company was not justified and

therefore the remaining amount of claim of Rs.18,900/- should be paid to him.

19. Arguments by the Respondent:

The representative of the Respondent stated that the treating hospital’s doctor had given

clarification vide his letter dated 17.03.2017 that the coblater was not an instrument but a

disposable blade, which is used for every surgery. Any disposable comes under the category

of non-medical item under Sr. No. 78 of Annexure I – List of Expenses Excluded (Non-

medical), it was not payable as it was part of OT and surgeon charges, hence not paid

separately. He added that the claim was settled as per terms and conditions of the policy.

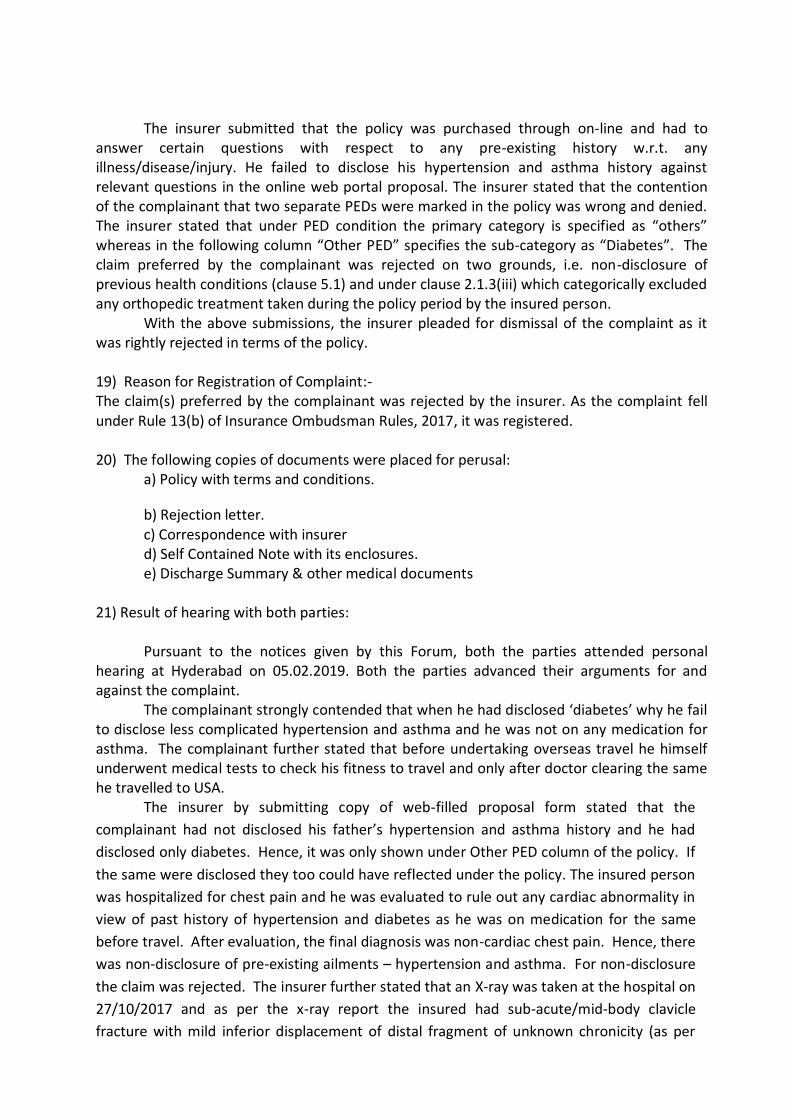

20. Observations and Conclusions:

The point to be considered in this case was whether the deduction made by the Respondent

was as per the terms and conditions of the policy.

4. The Respondent had deducted Rs.18,900/- towards the coblater charges which

according to them was not reimbursable as per the list Non-Medical items as per

Annexure I of expenses excluded (Non-medical), Sr. No. 78- Surgical Blades.

This item is part of a list of items of hospital services where separate

consumables are not payable but the service is.

5. As per the treating Hospital letter dated 17.03.2017, coblater is not an instrument, but

a disposable blade used for every surgery.

6. Since the treating doctor had confirmed that the Coblater was used under every

surgery, the cost of coblater which is of one time use should be considered as

service and paid as part of OT charges.

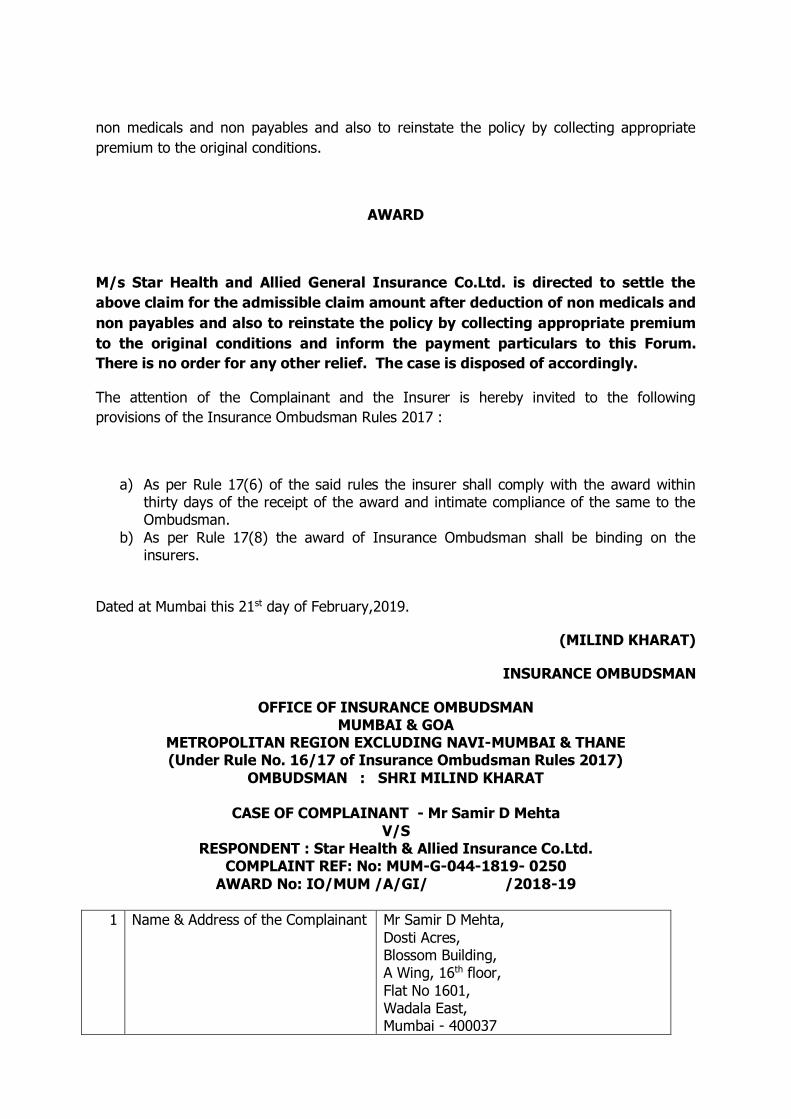

AWARD

Taking into account the facts and circumstances of the case and the submissions

made by both the parties, the insurer is directed by the Forum to pay an amount

of Rs. 18,900 to the complainant towards the cost of the coblater which was

earlier disallowed. In addition, interest as per rule 17(7) of the Insurance

Ombudsman Rules, 2017 also becomes payable.

22 The attention of the Complainant and the Insurer is hereby invited to

Rules 17(6) and 17(8) of the Insurance Ombudsman Rules, 2017 as

follows.

G) According to Rule 17(6) of the Insurance Ombudsman Rules,2017, the Insurer shall

comply with the award within thirty days of the receipt of the award and intimate compliance

of the same to the Ombudsman.

H) According to Rule 17(8) of the said Rules, the award of Insurance Ombudsman shall

be binding on the Insurers.

Dated at Ahmedabad on 5th Feb., 2019

M. Vasantha Krishna

Insurance Ombudsman

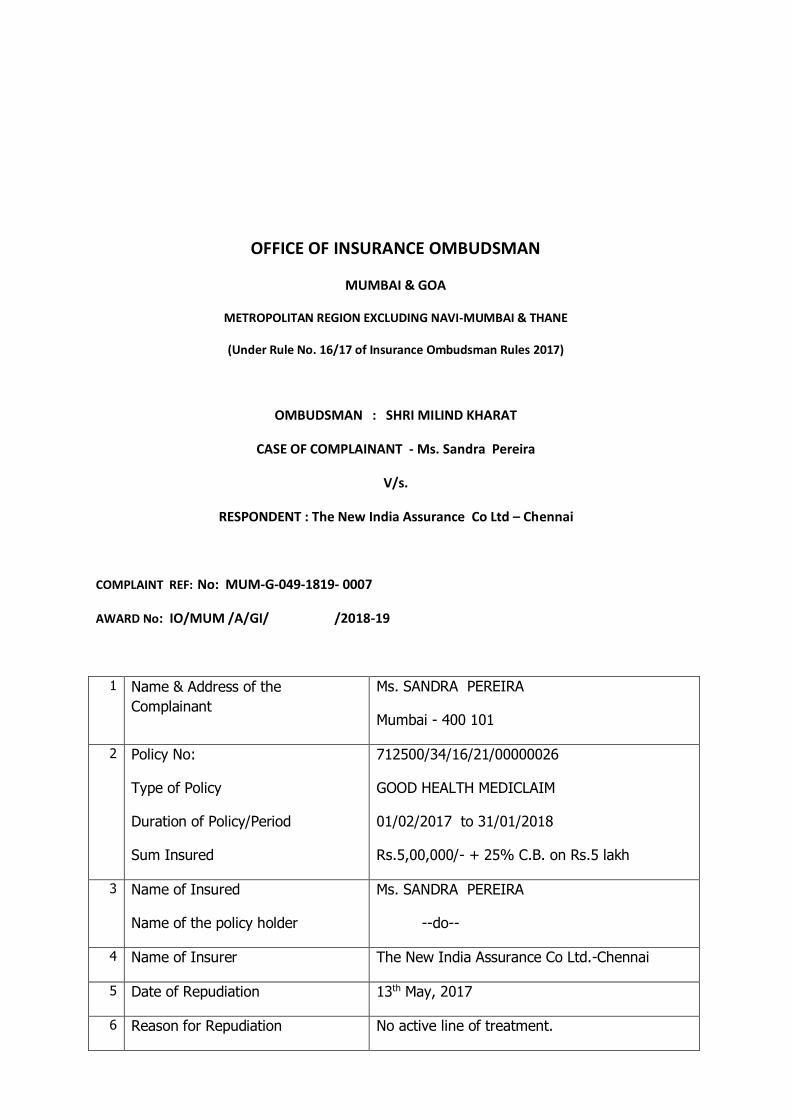

OFFICE OF INSURANCE OMBUDSMAN

MUMBAI & GOA

METROPOLITAN REGION EXCLUDING NAVI-MUMBAI & THANE

(Under Rule No. 16/17 of Insurance Ombudsman Rules 2017)

OMBUDSMAN : SHRI MILIND KHARAT

CASE OF COMPLAINANT - Ms. Sandra Pereira

V/s.

RESPONDENT : The New India Assurance Co Ltd – Chennai

COMPLAINT REF: No: MUM-G-049-1819- 0007

AWARD No: IO/MUM /A/GI/ /2018-19

1 Name & Address of the

Complainant

Ms. SANDRA PEREIRA

Mumbai - 400 101

2 Policy No:

Type of Policy

Duration of Policy/Period

Sum Insured

712500/34/16/21/00000026

GOOD HEALTH MEDICLAIM

01/02/2017 to 31/01/2018

Rs.5,00,000/- + 25% C.B. on Rs.5 lakh

3 Name of Insured

Name of the policy holder

Ms. SANDRA PEREIRA

--do--

4 Name of Insurer The New India Assurance Co Ltd.-Chennai

5 Date of Repudiation 13th May, 2017

6 Reason for Repudiation No active line of treatment.

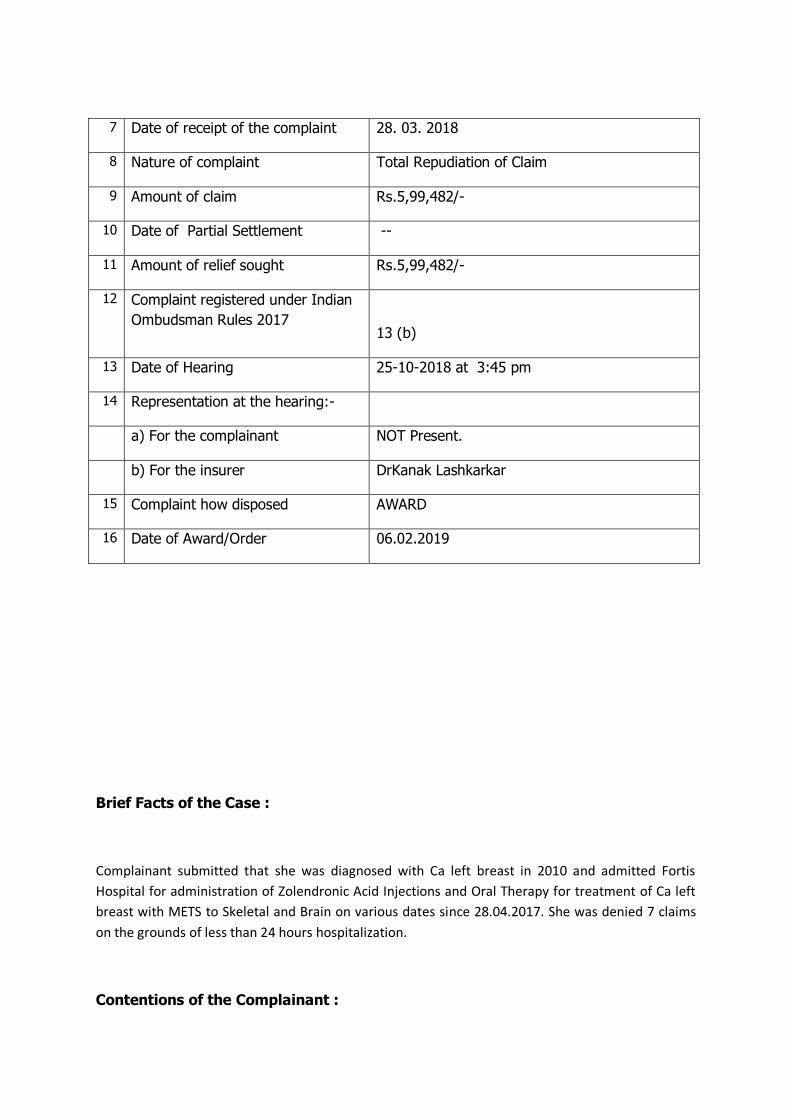

7 Date of receipt of the complaint 28. 03. 2018

8 Nature of complaint Total Repudiation of Claim

9 Amount of claim Rs.5,99,482/-

10 Date of Partial Settlement --

11 Amount of relief sought Rs.5,99,482/-

12 Complaint registered under Indian

Ombudsman Rules 2017

13 (b)

13 Date of Hearing 25-10-2018 at 3:45 pm

14 Representation at the hearing:-

a) For the complainant NOT Present.

b) For the insurer DrKanak Lashkarkar

15 Complaint how disposed AWARD

16 Date of Award/Order 06.02.2019

Brief Facts of the Case :

Complainant submitted that she was diagnosed with Ca left breast in 2010 and admitted Fortis

Hospital for administration of Zolendronic Acid Injections and Oral Therapy for treatment of Ca left

breast with METS to Skeletal and Brain on various dates since 28.04.2017. She was denied 7 claims

on the grounds of less than 24 hours hospitalization.

Contentions of the Complainant :

The complainant was not present for the hearing, so her written submissions were taken on record.

She submitted that she was diagnosed with Ca left breast in 2010 and underwent lumpectomy

surgery followed by chemotherapy and radiation. She had recurrence in the same breast in 2012

and had mastectomy. Thereafter, in July 2016 she experienced pain in her right leg and started to

limp. An MRI and various tests later showed that the cancer had metastasized to the skeletal and

brain. She immediately started treatment which involved radiation to the brain and femur followed

by IV chemotherapy and Zolendronic Acid Injections, where all her claims were settled. However,

now that she is on an oral chemo protocol, her claims have been repudiated as she is not an

inpatient. She pointed that when she was an inpatient for the Zolendronic Acid Injection, on a

monthly basis, her claims were once again repudiated as it was not chemotherapy but supportive

treatment. She stated that she did not agree with the Insurance Co.’s reasons for repudiating her

claims since her mainstay of treating cancer is chemotherapy and now she has reached a stage

wherein her treatment requires daily oral chemo. She clarified that it is still chemotherapy and the

side effects are the same and the only difference is that she is not required to be an inpatient and

the injections are still part of the current treatment protocol. She reiterated that she is still suffering

from cancer and the only thing that has changed is the treatment protocol. She lamented that at

this point in her treatment when she needed the most support due to the advancement of the

disease; she is being caused great stress which does not help her health condition. Complainant

argued that when the claims for the same treatment were paid earlier, the reason cited by the

Respondent for denial of the subject claims under the policy with same terms and conditions, is not

acceptable. She requested for settlement of the claims.

Contentions of the Respondent:

It was contended on behalf of the Respondent that Ms. Sandra Pereira was a diagnosed case of Ca

Left Breast and underwent treatment with Inj. Zolendronic. The Respondent submitted that on

scrutiny of the OPD papers they observed that Inj Zolendronic Acid (Zomketa/Reclast/Aclasta) is an

IV injection and is used in cancer with metastasis in bones. The same is not a chemotherapy drug, as

it is an immune-modulatory drug and supportive treatment in cancer and the same cannot be

considered under daycare procedure in fact this can be admissible as per-post claim of

chemotherapy treatment. The administered drug is not pharmacologically a chemo drug and hence

will not attract waiver of hospitalization.

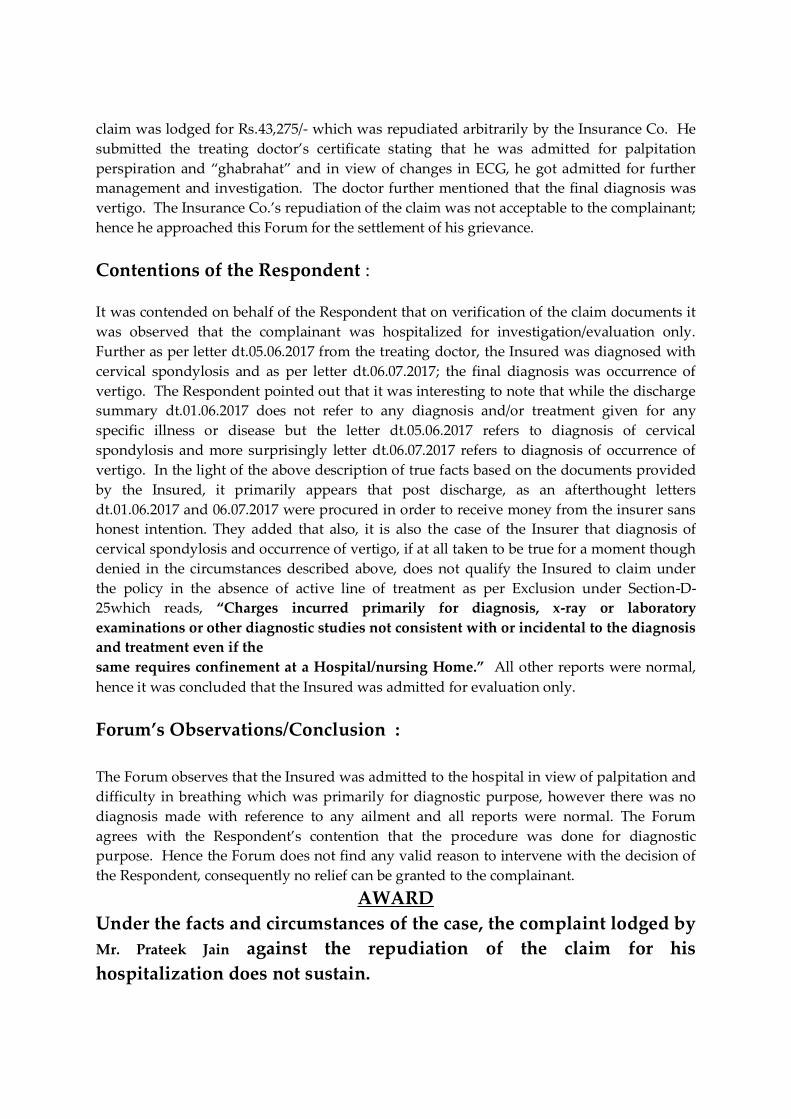

Forum’s Observations/Conclusion:

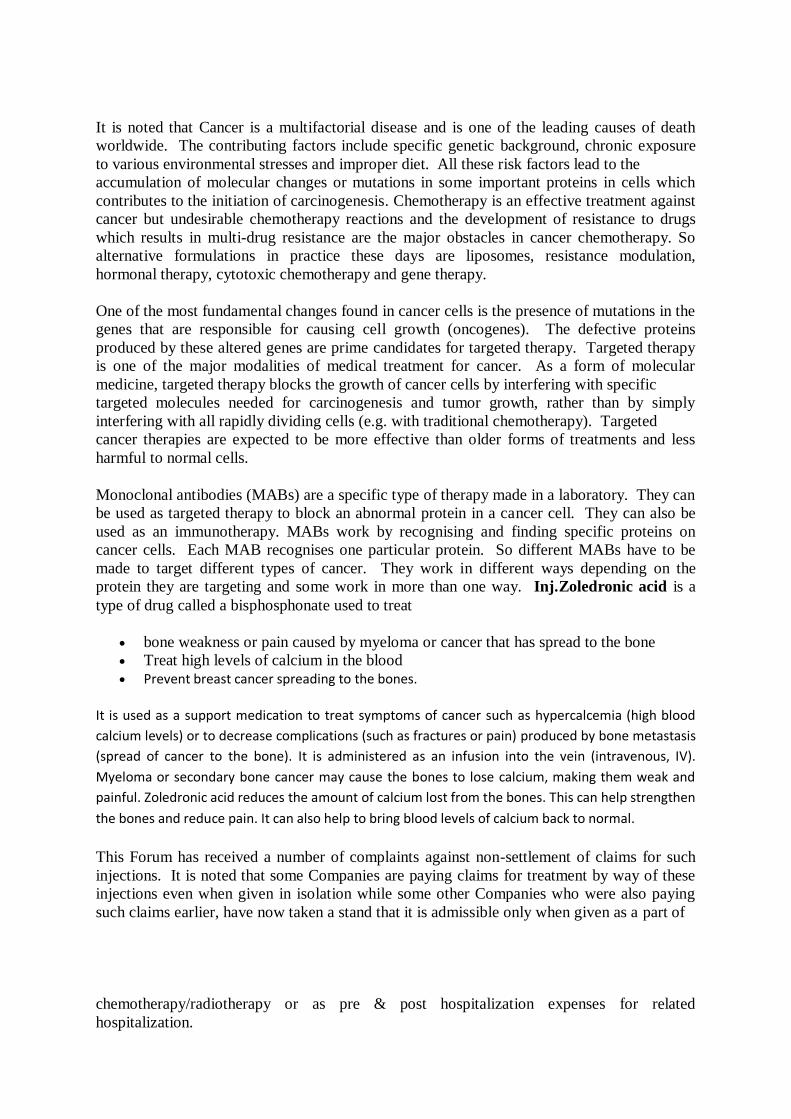

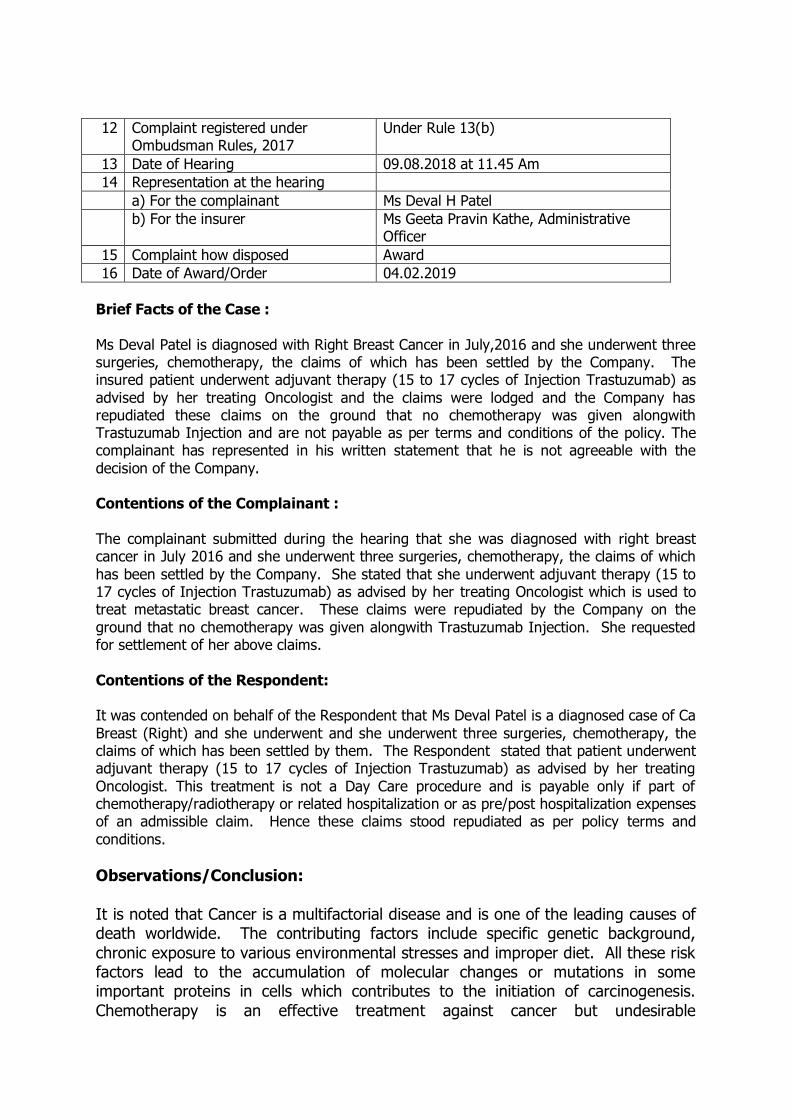

It is noted that Cancer is a multifactorial disease and is one of the leading causes of death

worldwide. The contributing factors include specific genetic background, chronic exposure

to various environmental stresses and improper diet. All these risk factors lead to the

accumulation of molecular changes or mutations in some important proteins in cells which

contributes to the initiation of carcinogenesis. Chemotherapy is an effective treatment against

cancer but undesirable chemotherapy reactions and the development of resistance to drugs

which results in multi-drug resistance are the major obstacles in cancer chemotherapy. So

alternative formulations in practice these days are liposomes, resistance modulation,

hormonal therapy, cytotoxic chemotherapy and gene therapy.

One of the most fundamental changes found in cancer cells is the presence of mutations in the

genes that are responsible for causing cell growth (oncogenes). The defective proteins

produced by these altered genes are prime candidates for targeted therapy. Targeted therapy

is one of the major modalities of medical treatment for cancer. As a form of molecular

medicine, targeted therapy blocks the growth of cancer cells by interfering with specific

targeted molecules needed for carcinogenesis and tumor growth, rather than by simply

interfering with all rapidly dividing cells (e.g. with traditional chemotherapy). Targeted

cancer therapies are expected to be more effective than older forms of treatments and less

harmful to normal cells.

Monoclonal antibodies (MABs) are a specific type of therapy made in a laboratory. They can

be used as targeted therapy to block an abnormal protein in a cancer cell. They can also be

used as an immunotherapy. MABs work by recognising and finding specific proteins on

cancer cells. Each MAB recognises one particular protein. So different MABs have to be

made to target different types of cancer. They work in different ways depending on the

protein they are targeting and some work in more than one way. Inj.Zoledronic acid is a

type of drug called a bisphosphonate used to treat

bone weakness or pain caused by myeloma or cancer that has spread to the bone

Treat high levels of calcium in the blood

Prevent breast cancer spreading to the bones.

It is used as a support medication to treat symptoms of cancer such as hypercalcemia (high blood

calcium levels) or to decrease complications (such as fractures or pain) produced by bone metastasis

(spread of cancer to the bone). It is administered as an infusion into the vein (intravenous, IV).

Myeloma or secondary bone cancer may cause the bones to lose calcium, making them weak and

painful. Zoledronic acid reduces the amount of calcium lost from the bones. This can help strengthen

the bones and reduce pain. It can also help to bring blood levels of calcium back to normal.

This Forum has received a number of complaints against non-settlement of claims for such

injections. It is noted that some Companies are paying claims for treatment by way of these

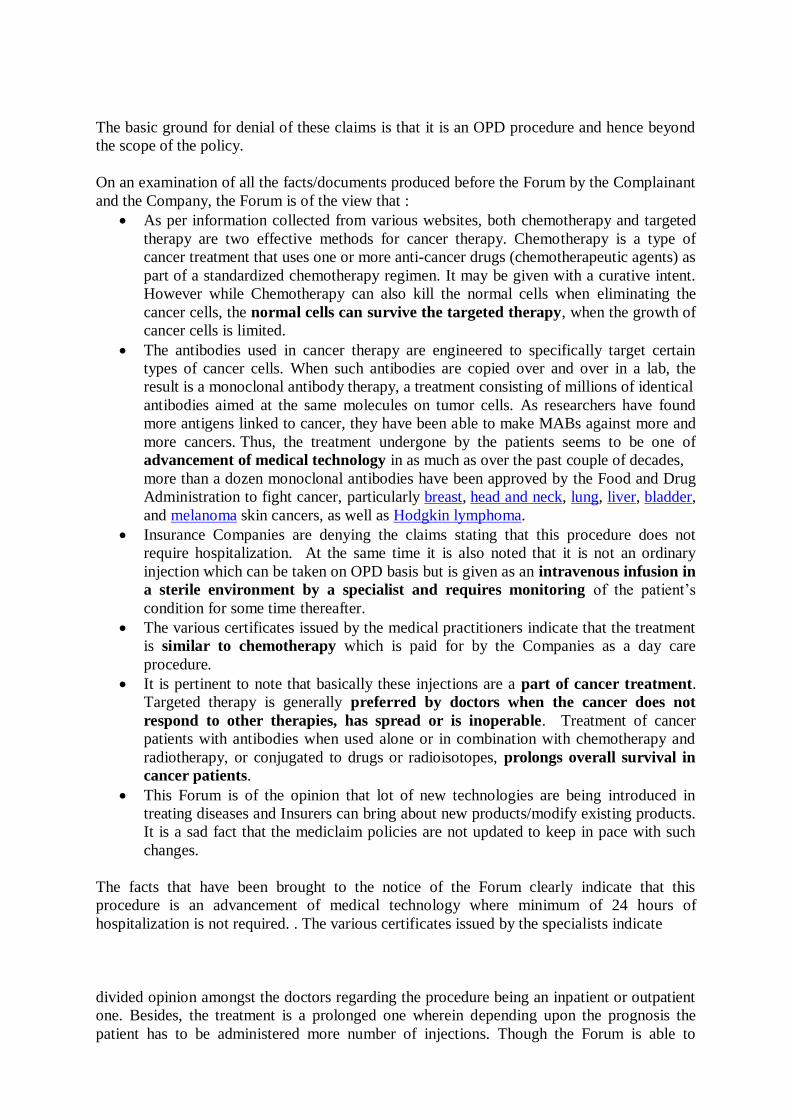

injections even when given in isolation while some other Companies who were also paying