Embed Size (px)

Citation preview

Open economies review 6:303-321 (1995) © 1995 Kluwer Academic Publishers. Printed in The Netherlands.

Price Adjustment in Open Economies

TORBEN M. ANDERSEN AND NIELS LYNGGARD HANSEN Department of Economics and Centre for International Economics, University of Aarhus, Aarhus, Denmark

Key words: price adjustment, foreign competition, nominal rigidities

Abstract

The adjustment of product prices in open economies is analyzed by use of a model encompassing different product market structures and quarterly data for Denmark, Germany, the Netherlands, Norway, and Sweden. In general, support is found in favor of a specialized production model implying that prices are affected by internal and external factors. Price adjustment displays substantial inertia and is in the short run driven by real shocks to both supply and demand, as well as being characterized by nominal rigidities, whereas in the long run relative prices are driven solely by supply variables.

The adjustment of product prices to demand and supply shocks is crucial both for the business-cycle implications and the effectiveness of different forms of policy intervention. For open economies the most crucial factor determining price adjust- ment is the extent of competition or substitutability between domestic and foreign goods.

The open macroeconomics literature features different product market structures ranking from so-called small open economy models, where output prices are given from outside, to models where prices are given as a markup on domestic labor costs. Clearly, conclusions are critically dependent on the specific product market model used.

The empirical literature concerned with price adjustment in open economies is modest. Either aspects of open economies are not explicitly introduced (a notable exception is Alogoskoufis, Martin, and Pittis 1990) or more disaggregate studies (see e.g., Geroski 1992) suffer from the problem that no distinction is made between nominal and relative price adjustment.

This paper therefore has the twofold purpose of testing different models of prod- uct market structures in open economies, as well as providing insight on the ad- justment of prices to demand and supply shocks being either real or nominal.

Imperfect competition usually modeled in the form of monopolistic competition has proved to be a useful vehicle for open and closed macroeconomic analyses (see Benassy 1993, Silvestre 1993, Dixon and Rankin 1994, and Dixon 1994 for introductions and surveys). Using this framework in the present context has the double advantage of being easily manageable and capturing different product mar- ket models as special cases.

304 ANDERSEN AND HANSEN

The remainder of the paper is organized as follows. Section 1 sets up a monopo- listic competitive product market model and outlines how different special cases correspond to product market assumptions frequently used in the literature. Issues relating to empirical estimations of the pricing model are discussed in section 2. Section 3 presents the data, and the empirical results are reported in section 4. Concluding remarks are in section 5.

1. Product market pricing in open economies

Since the focus here is on the aggregate interaction between domestic and foreign product prices, it suffices to consider a two-good model: a domestic produced and a foreign produced good. The price of the foreign good in domestic currency is P*, and this price is exogenous to the domestic economy. This presumes a fixed exchange rate and that the domestic country exerts a negligible effect on the world economy. The demand for the domestically produced good is given as

Dt = D (,_Pt ' Z (1)

where P is the price of domestic goods, and Z is a (vector of) real state variables, and t index time. 1

If domestic and foreign goods are perfect substitutes, that is,

a D P*/P c - aP*/P D - 00,

we have a small open economy, while in general goods are imperfect substitutes, and we have a specialized production model.

The technology available for the production of the domestic good can be sum- marized by the amount of labor needed to produce Y units of output

Lt = F(Yt, At) (2)

where Y is output, L is the use of labor, and A is a general productivity meas- ure (could reflect the influence of both pure technological progress and capital accumulation).

The domestic firm decides on prices and production taking the wage and foreign prices for given, and the problem is thus

M a x Pt D I,.. Pt ' Z - W t F [,.. Pt ' Z , A Pt

where W is the nominal wage rate.

PRICE ADJUSTMENT IN OPEN ECONOMIES 305

The first-order condition to this problem can be written

Pt I, ~'P~ t~ = WtFy L p , A , Z e ~ p t , Z

The optimal price determined by (3) can in implicit form be written

(3)

Pt = P(Wt, Pt, Zt, At) (4)

It is noted that the nominal price P is homogeneous of degree 1 in nominal wages and foreign prices,

)~Pt = P(;kWt, ;kPt, Zt, At) V k > 0

This reflects that imperfect competition in itself does not contribute to the explana- tion of nominal rigidities. The price decision determines therefore the relative price between domestic and foreign goods or the terms of trade as is seen from (5) by setting X = YP* implying

P,/P;' = P(W,/P;, 1, z,, A0 (5)

Terms of trade are therefore determined by cost changes and real shocks to supply (A) and demand (Z).

The implied employment level can be written

(6)

It should be noted that the model easily could be generalized to allow for more than one representative domestic and foreign firm without altering anything quali- tatively (see Andersen 1994b and Aizenman 1989). Moreover, it is worth pointing out that even under perfect competition in the sense of price-taking firms, the price equation would depend on the same variables as in (3).

Some special cases are noteworthy: 1. under a small open economy assump- tion (nonspecialized production, e -~ oo), we get

Vt = Vt (7)

2. under constant-returns-to-scale Fy(Y, A) = ~A), we get markup pricing,

Pt = 1 (_p~ Wtq~(At)

e ~_Pt' Z

(8)

306 ANDERSEN AND HANSEN

which if the elasticity is constant (e = ~) implies that prices are purely cost- determined.

These two special cases bring out that two aspects are important in analyzing pricing behavior, namely, properties of the demand function and of the production technology. It is also important to distinguish between, on the one hand, real shocks to either demand (Z) or costs (A) and, on the other hand, nominal shocks. The latter is often identified with demand shocks. This is not correct although nominal rigidities in Keynesian type models imply that nominal demand shocks have real effects. Section 3 discusses how to separate the different types of shocks in the empiricial analysis.

Alogoskoufis, Martin, and Pittis 1990 consider product market pricing in open economies in an attempt to evaluate the degree of product specialization. They proceed by testing whether prices are determined by costs as in (8) or by foreign prices as in (7). Pricing according to (7) is taken to imply nonspecialization, while (8) is assumed to imply specialization. The latter interpretation is only warranted if the technology has constant-returns-to-scale. Since this cannot be taken for granted, we have to start with the more general specification (4).

It should be noted that the so-called Scandinavian model of inflation (see e.g., Bruce and Purvis 1985) comes in as the special case where both (7) and (8) are fulfilled. The Scandinavia model presumes output prices (of tradables) to be deter- mined by foreign prices as in (7). Given prices, the development of productivity determines the room left for wages so as not to jeopardize the profitability of firms,

W t = P ; ~ ( A t ) - 1 (9)

Hence, the Scandinavian model requires both (7) and (8) to hold, although (8) should not be given a markup interpretation in this case.

To sum up the issues of particular interest in the empirical analysis, we find that analyzing the extent to which prices are affected by foreign prices or domestic fac- tors sheds light on the product market structure. Moreover, the response of prices to real shocks, to demand and supply, and to nominal shocks is relevant for business- cycle questions and policy questions.

2. Issues in empirical implementation

To proceed with an empirically workable model, the following analysis is based on a log-linear version (x = ]~X) of the pricing equation (4)

Pt = 7;'0 -I- '/l'lW t -Jr- "/r2p t + ~3Zt q'- "/l'4a t

where

7 / ' 1 + 7 / ' 2 = 1

so as to preserve the homogeneity property.

PRICE ADJUSTMENT IN OPEN ECONOMIES 307

2.1. Nominal rigidities

The model set-up explains relative output prices in terms of real variables, that is, there are no nominal rigidities, cf. (5), as is also seen by rewriting the price equation as

Pt - Pt = % + 7rl(Wt - - Pt) + "/r3zt -k 7 r 4 a t

where the homogeneity property ~rl + 7r2 = 1 is used. Different theories have been suggested to explain nominal rigidities, and since

policy issues are crucially dependent on nominal adjustment (see Andersen 1994a), we shall devote some effort to test nominal issues.

The preceding reform ulation exploited the homogeneity property. If this property is not fulfilled--i.e., 7r 1 + ~r2 = p where p ~ 1--the relative output price could be written

Pt - - P t = 71"0 + 7r l (wt - - Pt ) + 7r3zt + 7r4at + ~ - - 1 ) p t

Including the level of foreign prices in the relative price equation and testing whether the coefficient to Pt is significantly different from zero is thus a simple and straight- forward way to test whether there are nominal ridigities.

2.2. Exogenous variables

An indicator for the level of foreign demand has been constructed on the basis of total imports to a group of neighboring countries. This variable captures the state variable in demand z, and this series is labeled d.

The productivity variable a is a proxied by average labor productivity y - 1. The theoretical model was set up to highlight product market interaction via the

demand side. There is, of course, another linkage in the form of the inpqt-output network. Foreign prices influence domestic prices via costs of production (e.g., raw materials). Raw material prices are labeled pin and the resulting price equation then reads

Pt - - P t = 71"0 + ~ l ( W t - - P t ) + 7r3dt + r4(Yt - It) + r5(P~ n - Pt )

To sum up, the relative price equation underlying the empirical analysis can be written

Pt - - Pt = 71"0 + 71"l(Wt - - P t ) + "/l'3dt + 7r4(Yt - - lt) + 7r5(,P~ n - - P t ) + 7r6Pt ( 1 0 )

where Pt is introduced as a separate variable allowing us to test for nominal rigidities.

The following special cases are encompassed in (10) and can be tested.

308 ANDERSEN AND HANSEN

2.3. Markup pricing

An implication of the simple markup pricing model is that prices are determined solely by wages corrected for productivity changes, that is, r l = -~r4 = 1 and -/1"3=71"5='/1"6=0.

A necessary but not sufficient condition for this is that the wage share is station- ary. We first test for this, and then proceed to a more formal test of whether the wage share is unaffected by domestic costs and demand factors.

2.4. Small open economy

If the small open economy assumption or the nonspecialization assumption is ful- filled, then relative producer prices (P/P*) should be unaffected by domestic cost and demand factors (~1 = 71"3 = 714 = "/r5 = 71"6 = 0).

We first consider whether the relative output prices are stationary, and next test whether domestic costs and demand factors influence price competitiveness.

2.5. Specialization

Finally, we attempt to formulate a general model based on the pricing equation (10).

3. Data and preliminary data analysis

The empirical analysis is based on data from the following five countries: Denmark, Germany, the Netherlands, Norway, and Sweden.

We use quarterly data for manufacturing industries. The samples are determined by the availability of the data-series, and lie in the period between 1960 and 1990. The series are producer prices, p; wages, w; productivity, y - 1; foreign prices in domestic currency, p*; raw material prices, pro; and as indicator for demand pressure, foreign demand for domestic exports, d. For further information on these series, see the more detailed Data Appendix.

Before proceeding to a more formal econometric estimation of the price equa- tion, we present some time-series properties of the series used.

In testing for the orders of integration we use the following regression:

P

Axt = ~0 + alt + "yxt_l +~-~j ~lAXt_i i=t

where we allow for a deterministic time trend only in the cases where this consti- tutes a relevant alternative to the stochastic trend. Critical values are taken from MacKinnon 1991.

PRICE ADJUSTMENT IN OPEN ECONOMIES 309

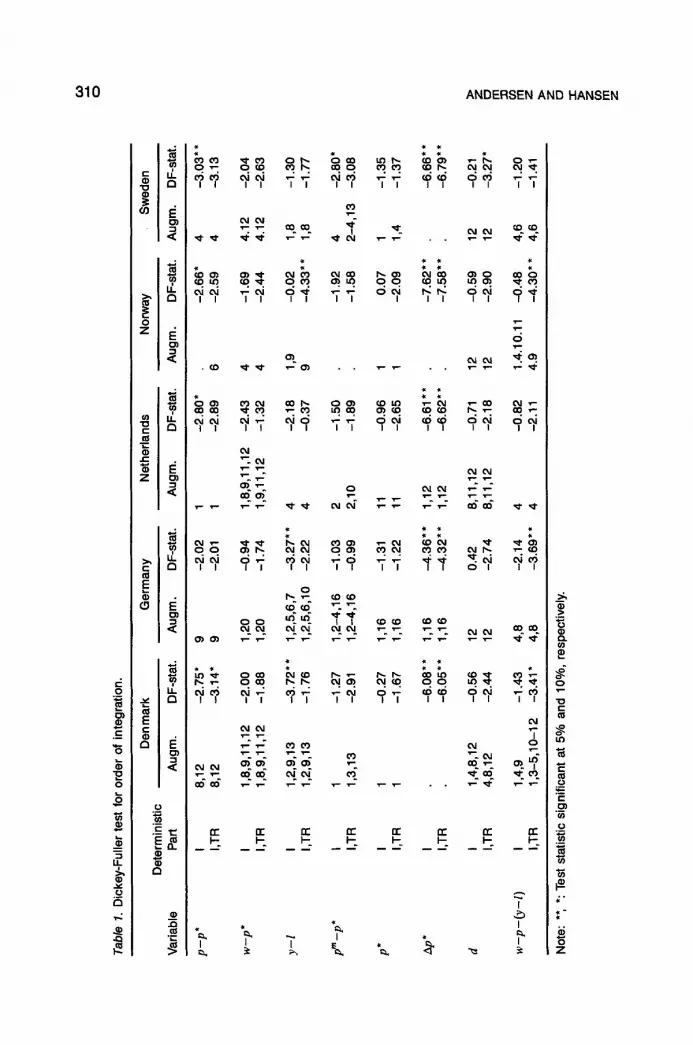

These results seem rather comforting vis-&-vis the cointegration approach (see Table 1), since it is hard to reject that all involved variables are 1(1), that is, difference stationary. This apparently also pertains to nominal producer prices, which are clearly not 1(2), hence this suggests no indication of nominal rigidities in terms of the presence of the inflation rate in the cointegration relations, or second differ- ences in the error-correction relations. We will check whether this is confirmed in estimations below.

4. The empirical price model

In this section we present econometric estimations of the price equation (10) based on the Engle-Granger two-step method. Hence, we start by considering long-run relationships before proceeding to the estimations of an error-correction model.

4.1. Long-run estimations

The cointegration estimations will be based on the following specification

Pt -- Pt = 7to + "/rl(wt - P t ) + "tr3dt + ~4(Yt - It) + ~'5(p[ ~ - P t ) + "n'6Pt + Et ( 1 1 )

where e is an I(0) disequil ibrium term. First we look at the time-series properties of domestic relative to foreign prices,

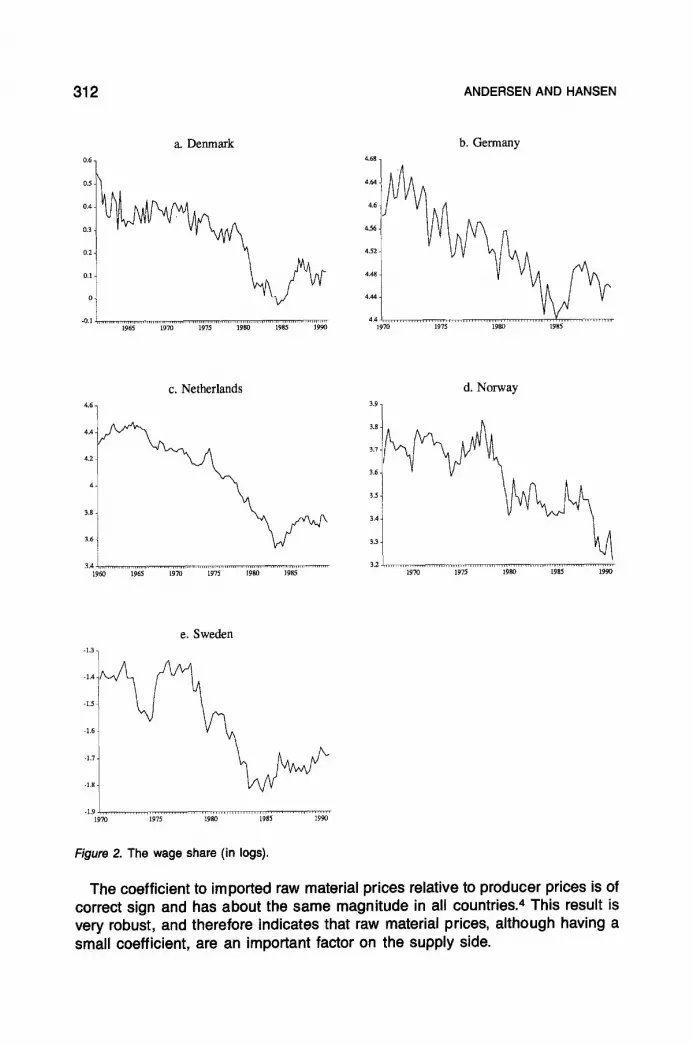

p - p*, and the wage share, w - p - y + 1, which corresponds to ~rl = ~r3 = ~r4 = 7r5 = ~'6 = 0, and 7r 1 = ~r4 = 1, and ~r 3 = ~'5 = ~r6 = 0, respectively. Stationarity of these variables is a necessary condition for the small open economy model and the simple markup pricing model. Furthermore, stationarity of both variables is a necessary condition for the Scandinavian model of inflation. Figure 1 shows domes- tic producer prices relative to foreign producer prices for the five countries, while Figure 2 depicts wage shares.

These figures show no clear evidence in favor of stationarity of either the relative prices or the wage shares. This is confirmed by the unit root tests in Table 1, where only relative prices in Sweden are stationary at a 5% critical level. Note, however, that relative prices tend to be more stable than wage shares, indicating that open- ness is an important feature.

The results of the cointegration estimations are reported in Table 2. In all countries except the Netherlands there seems to be cointegration. 2 In the

case of the Netherlands the finite sample properties of these cointegration tests should be noted as well as the fact that the results look very similar to those for the other countries.

The cointegration estimations clearly indicate that foreign prices are important,3 especially in the smaller, and more open economies like Denmark, the Netherlands, Norway, and Sweden. Foreign prices, however, also seem to be important in Ger- many. This is seen most clearly by noting that if the relative price equation is rewrit- ten as a nominal price equation for p, then the coefficient to foreign price p* would be 1 - ~rl - 7r5, which would be in the range 0.68 to 0.78, except for Germany where it is 0.45.

310 A N D E R S E N A N D H A N S E N

c 0

,9,m .m

0

I.L

0

O,I 00 ~0 c ~ ~

• (D

0

0

T-- T-- T-- T -

~ T -

o o

o

• .- m-

(o I.-

t~0 ¢o T- ~-.

o) o )

o l t'~l • -- T - = . T - m.- I - ~--

0 ) o0

od o

r r r r r r r r r r n" r r n -

~h

t~l OJ T-- T--

I

I

I

(I) Q. (0 e

0

"(3 c

t~

o

r..

0

Z

PRICE ADJUSTMENT IN OPEN ECONOMIES 311

1.2

1.18 t 1.16

1.14

1.12

1.1 ~ ~

1.1715

1.02

a. Denmark

1961 1965 1970 1875 1980 1988 1990

b. Germany 2.58

2.84

2.52

2.5

2.48

2.46

2.44

2 42

1970 1975 1980 1985

z~ 1 2,~ i

2A4

2.42

2,4

2,38

2.36

2.34

2.32

2,8

c. Netherlands

2.28 1960 1965 1970 1975 t980 1985 1990

1.44

1.42

1.4

1.38

1.36

1.94

1.32

1.3

1.28

1.26

1.24

d, Norway

1970 1975 1980 1988 1990

1.44

1.42

1,4

1,38

1.36

L34

1.32

1.8

1.28

1.26

L24

e. Sweden

1970 1975 1980 1985 1990

Figure 1. Relative output prices (in logs).

In addition, productivity in all countries has a coefficient that numerically is smaller than the one to wages. This implies that changes in terms of trade cannot be ex- plained by changes in the wage share.

0.6

0.5

0.4

0.3

0.2

0.1

0

-0.1 2 1965 1970 1975 1980 1985 1990

a. Denmark

d. Norway

4.68

4.6

4.56 t 4.52

4.48

4.44

4.4 ,H 1970

b. Germany

1975 1980 1985

4.6-

4.4-

4.2

4-

3.8

3.6

3.%

c. Netherlands 3.9-

3.8.

3.7-

3.6-

3.5.

3.4

3.3

3.2 1965 1970 1979 I980 1985

312 ANDERSEN AND HANSEN

1970 1975 1980 1985 1990

+1.3

-1.5

-1.6 t -1.7

-L8

-1.9

e. Sweden

1970 1979 1980 1985 1990

Figure 2. The wage share (in logs).

The coefficient to imported raw material prices relative to producer prices is of correct sign and has about the same magnitude in all countries. 4 This result is very robust, and therefore indicates that raw material prices, although having a small coefficient, are an important factor on the supply side.

PRICE ADJUSTMENT IN OPEN ECONOMIES 313

0 c~

~r

(J

..~ ,'r

0

p,

W

0

0 '~" z ~

I

I

~ o ~

I

d d ~ o I I

d d ~ d

~ m

m ~ a ~ I

p.~o 0 0 0

o o c~

0 0 0

0 0 0

E"

CO

o. CO

L~

I

O

<

a~

" o

o

a~

t,.-

8. ""

t~

,,..- _.=

m

~o

-~ +

- O

314 ANDERSEN AND HANSEN

Nominal rigidities (nonhomogeneities) do not seem to be a long-run property, since p* is not significant in any country.

It was difficult to find any influence from the demand pressure variable, whether measured by exogenous variables like foreign demand for domestic exports, or more endogenous variables like exports of manufacturing goods or domestic ab- sorption. Several combinations and detrending procedures were used, but nothing seemed to work in any country. This indicates that, in the long run, prices are unaf- fected by the demand factors. We will now investigate whether this holds also in the short run.

4.2. Error.correction models

In the proces of estimating an error-correction model, we allow for a more liberal approach, employing the general-to-specific procedure. The reason is, of course, that our a priori opinions about the adjustment process, and hence the lag struc- ture, are rather weak. Nominal rigidities are allowed and tested for. At this step we therefore start out from a very general equation

A(L)A(p t - P t ) = °to + B(L)A(wt - Pt) + C(L)A(y t - l t )

+ D(L)A(P~ n - P t ) + E(L)Adt + F ( L ) A p t + ")'cet_ 1 + (12)

where A(L), B(L), C(L), D(L), E(L), and F(L) are lag polynomia, and ce the disequi- librium term from the cointegration relationship.

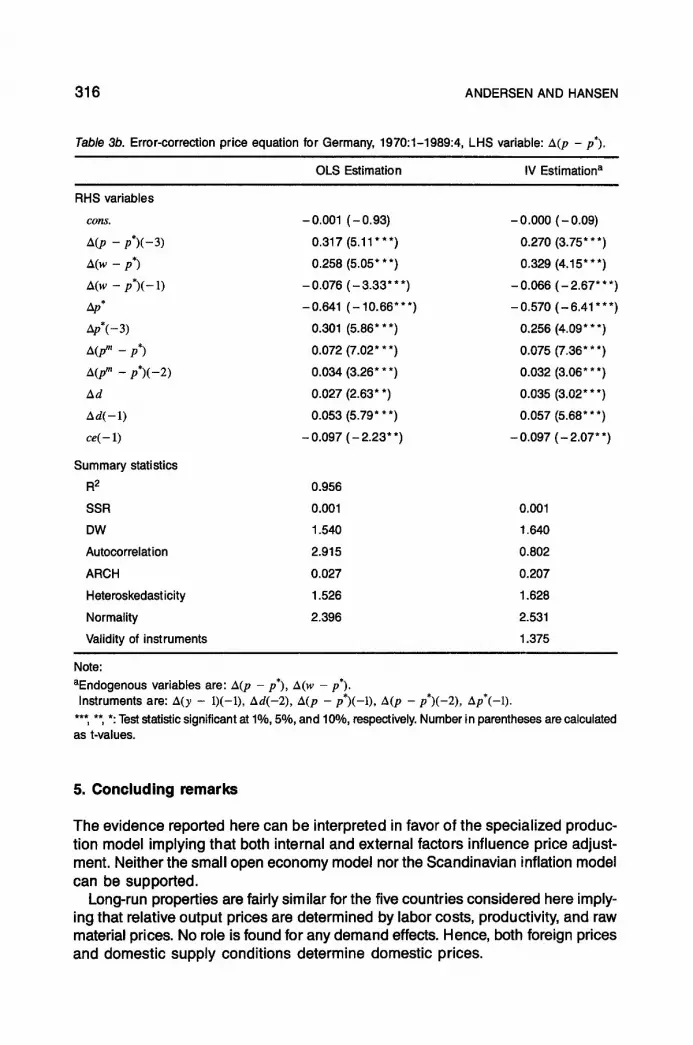

Since some of the variables, especially wages and average labor productivity, might be considered endogenous and thereby give rise to a simultaneity bias, we have also applied the instrumental variable estimation method. It seems indeed that some of the variables are endogenous, in that some of the coefficients have changed. In general, however, these differences seem to be minor, and significance at the 50/0 critical level is never changed. We also present summary statistics for several misspecification tests. At a SO/o critical level, these tests indicate no kind of misspecification in any of the equations, s,6 The results are reported in Table 3, giving the specific form for each country reached from the general forms by the usual sequential procedure.

An interesting general finding is that prices in the short run adjust less than in the long run to domestic supply-side variables, that is, real wages, productivity, and raw material prices. This suggests that openness or the competitive position to foreign products exerts an important influence on price-setting in the short run.

This is also reflected by finding that the variable capturing world demand (d) is found to influence prices in the short run. Although the effect is not overwhelming, it is significant and shows that (real) demand factors influence prices contrary to the simple markup pricing model. This finding is of particular interest since most empirical studies usually have difficulties in capturing any demand-side effects (see, e.g., Geroski 1992).

PRINCE ADJUSTMENT IN OPEN ECONOMIES 315

Table 3a. Error-correction price equation for Denmark, 1970:1-1990:4, LHS variable: A(p - p*).

OLS Estimation IV Estimation a

RHS variables

cons. 0.001 (0.22) 0.000 (0.13)

A(w - p*) 0.389 (4.66"**) 0.395 (3.72"**)

A(p" - p*) 0.219 (8.03* **) 0.219 (8.03* **)

Ap* - 0.276 ( - 3.06" * *) - 0.270 ( - 2.55" * *)

Ad(-1) 0.062 (2.25* *) 0.063 (2.08"*)

ce ( - ] ) -0 .164 ( - 3 . 4 0 * * * ) -0 .164 ( - 3 . 4 0 * * * )

Summary statistics

R 2 0.690

SSR 0.006 0.006

DW 1.830 1.820

Autocorrelation b 2.678 0.660

ARCH c 0.660 0.671

Heteroskedast icity d 1.219 1.218

Normality e 1.450 1.447

Validity of instruments f 1.329

Notes:

aEndogenous variables are: A(p - p*), A(w - p*). Instruments are: A(w - p*)(-1), A(w - p*) ( -2) , A(p - p*)( -2) , A(p m - p*)(-1),

Ad(-2), Ap*(-1), Ap*(-2).

bLM-test of autocorrelation of order 1 to 4, x 2 (4)-distributed.

CLM-test of ARCH of order 4, F-distributed.

dF-test based on White (1980).

eBera-Jarque test for normality, x 2 (2)-distributed.

fx2-test of validity of instruments.

*** ** *: Test statistic significant at 1%, 5%, and 10%, respectively. Number in parentheses are calculated as t-values.

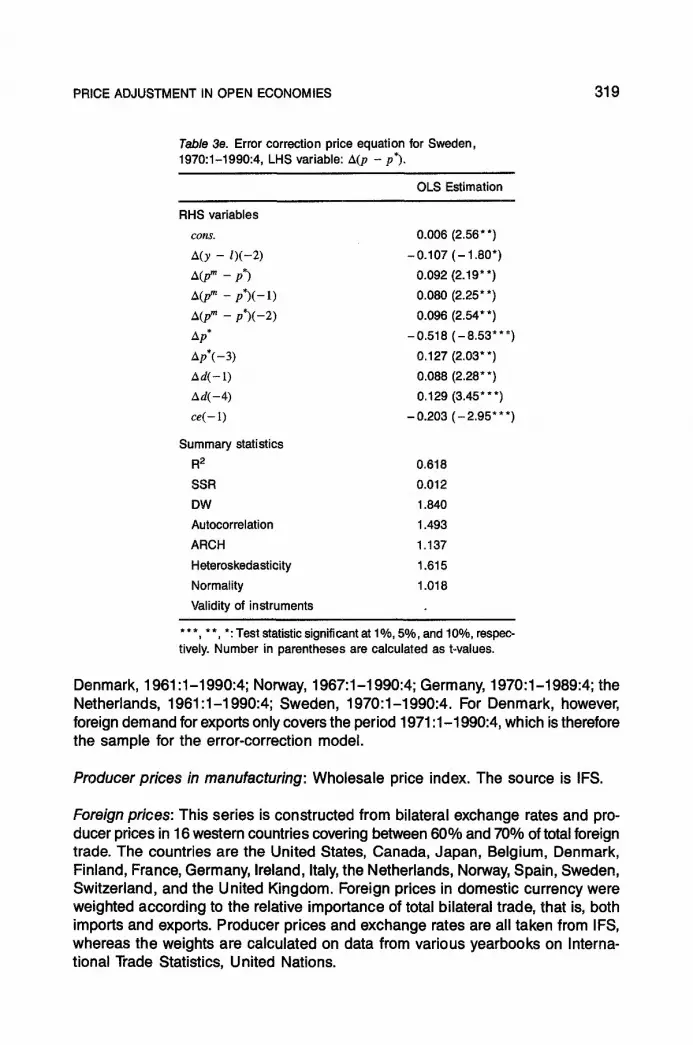

The analysis of short-run nominal rigidities follows the procedure outlined above by analyzing whether price changes, Ap*, matter. We also test whether price accel- eration A2p * matters since this may better capture inflation surprises. 7 Contrary to the long run, we find a strong indication of short-run nominal rigidities, in that Ap" exerts a significant influence on short-run price adjustments in all countries.

Finally, it is seen that relative prices, in all countries, correct for about 10-20% of long run disequilibrium. This means that adjustment to changes in explanatory variables is fairly sluggish, that is, there is substantial inertia in price adjustment.

3 1 6 ANDERSEN AND HANSEN

Table 3b. Error-correction price equation for Germany, 1970:1-1989:4, LHS variable: ~ ( p - p*).

OLS Estimation IV Estimation a

RHS variables

cons. - 0.001

A(p - p*)(-3) 0.317

A(w - p*) 0.258

A(w - p*)(- 1) - 0.076

~p* - 0.641

,~o*(-3) 0.301

A(p m -- p*) 0.072

A ( p m -- p*)(--2) 0 .034

,~d 0.027

A d ( - l ) 0.053

c e ( - 1) - 0 .097

Summary statistics

R 2 0.956

SSR 0.001

DW 1.540

Autocorrelation 2.915

ARCH 0.027

Heteroskedast icity 1.526

Normality 2.396

Validity of instruments

( - 0.93) - 0 .000 ( - 0.09)

(5.11 * * * ) 0.270 (3 .75"** )

(5 .05"* * ) 0.329 (4 .15"* * )

( - 3.33" * *) - 0.066 ( - 2 .67* * *)

( - 10 .66"* * ) - 0.570 ( - 6.41 * * * )

(5 .86"* * ) 0,256 (4 .09"** )

(7 .02** *) 0.075 (7 .36** *)

(3 .26** *) 0.032 (3 .06** *)

(2.63* *) 0.035 (3 .02** *)

(5 .79"* * ) 0.057 (5 .68"** )

( - 2 .23"* ) - 0.097 ( - 2 .07"*)

0.001

1.640

0.802

0.207

1.628

2.531

1.375

Note: aEndogenous variables are: ,~(p - p*), A(w - p*). Instruments are: A(y - 1)(-1), ~d(-2), ~(p - p*)(-;), ~(p - p*)(-2), ~p*(-]).

*** **, *: Test statistic significant at 1%, 5o, and 10%, respectively. Number in parentheses are calculated as t-values.

5. Concluding remarks

The evidence reported here can be interpreted in favor of the special ized produc- tion model implying that both internal and external factors influence price adjust- ment. Neither the small open economy model nor the Scandinavian inflation model can be supported.

Long-run properties are fairly similar for the five countries considered here imply- ing that relative output prices are determined by labor costs, productivity, and raw material prices. No role is found for any demand effects. Hence, both foreign prices and domestic supply conditions determine domestic prices.

PRICE ADJUSTMENT IN OPEN ECONOMIES 317

T a b / e 3 c . Error-corm~'tion price equation for the Netherlands, 1961:1-1990:4, LHS variable: ~,(p - p*).

OLS Estimation IV Estimation a

RHS variables

cons. 0.004

,~(p - p*)(- 1) 0.162

~(w - p*) 0.191

~(w - p*)(-1) -0.131

~ ( y - 1)(-1) 0.050

~(y - 1)(-4) -0,046

,~p* - 0.564

~(pm _ p*) 0.086

Ad 0.029

id69_1 b - 0.044

ce(- 1) -0,117

Summary statistics

R 2 0.808

SSR 0.005

DW 2.040

Autocorrelation 0.564

,ARCH 0,462

Heteroskedasticity 0.829

Normality 9.864

Validity of instruments

(4.10"**) 0.005 (3.88***)

(2.80* **) 0.165 (2.79***)

(4.60***) 0.161 (2.67***)

( -3 .15" * * ) -0.128 ( -3 .06*** )

(2.04* *) 0.050 (2.03* *)

( - 1.76") -0.043 ( - 1.58)

( - 10.50"**) -0.589 ( -9 .09" * * )

(2,47* *) 0.091 (2,49* *)

(2.03" *) 0.028 (1.71 *)

( -6 .32" * * ) - 0,044 ( -6 .14" * * )

( -4 .30 " * * ) - 0.122 ( -4 .33" * * )

0.005

2.020

0.074

0.432

0.840

10.341

0.967

Notes:

aEndogenous variables are: ~(p - p*), z~(w - p*). Instruments are: ~(w - p*)(-2), ~(w - p*)(-3), ~(w - p*)(-4), ,~(y - 1)(-3), Ad(-1), Ad(-3),

~(p - p*)(-3), zl(p - p*)(-4), A(p m -- p*)(--2), &p*(--1), Zip*(--3), ~p*(--4).

bid69_I is an impulse dummy taking the value 1 in 1969:1.

***, **, *: Test statistic significant at 1%, 5%, and 10%, respectively. Number in parentheses are calculated as t-values.

The short-run dynamics show that price adjustment is fairly sluggish, and that it is characterized by nominal rigidities. Moreover, real demand affects price adjust- ment in the short run. This finding is particularly important since most empirical price studies usually find it difficult to capture any demand effects. This is usually interpreted in favor of some form of markup pricing. The evidence reported here does not support simple markup pricing models either in the long run or in the short run. One important difference between the present study and most other studies is an explicit distinction between nominal and real variables.

318 ANDERSEN AND HANSEN

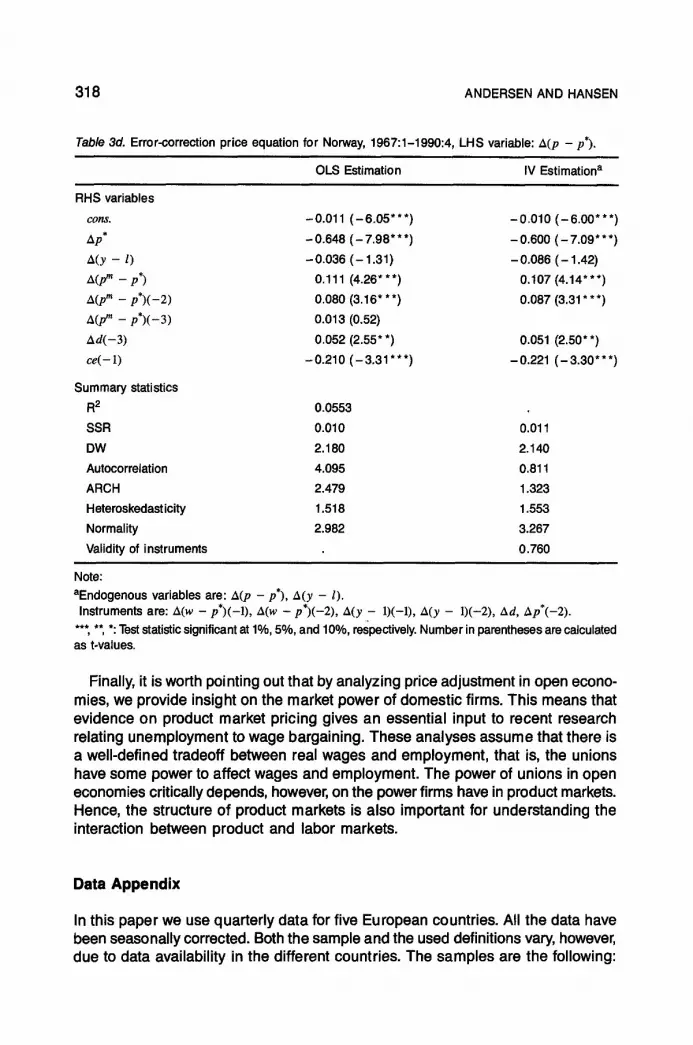

Table 3d. Error-correction price equation for Norway, 1967:1-1990:4, LHS variable: A(p - p*).

OLS Estimation IV Estimation a

RHS variables

CONS.

Ap* ,~(y - i) ,~(y" - p')

A(p m - p*)(-2)

,a(p" - p*) ( -3 )

Ad(-3)

ce(- 1)

Summary statistics R 2

SSR

DW

Autocorrelation

ARCH Heteroskedasticity

Normality

Validity of instruments

- 0.011 ( - 6.05* * *) - 0.010 ( - 6.00" * *)

- 0.648 ( - 7.98* * *) - 0.600 ( - 7.09* * *)

-0.036 (-1.31) -0.086 (-1.42) 0.111 (4.26* **) 0.107 (4.14"**)

0.080 (3.16" **) 0.087 (3.31 * **) 0.013 (0.52)

0.052 (2.55* *) 0.051 (2.50"*)

-0.210 (-3.31 ***) -0.221 (-3.30***)

0.0553

0.010 0.011

2.180 2.140

4.095 0.811

2.479 1.323 1.518 1.553

2.982 3.267

0.760

Note: aEndogenous variables are: A(p - p*), A(y - l). Instruments are: A(w - p*)(-1), A(w - .o*)(-2), A(y - 1)(-1.), A(y - ].)(-2), Ad, Ap*(-2).

*** ** *: Test statistic significant at 1%, 5%, and 10%, respectively. Number in parentheses are calculated as t-values.

Finally, it is worth pointing out that by analyzing price adjustment in open econo- mies, we provide insight on the market power of domest ic firms. This means that evidence on product market pricing gives an essential input to recent research relating unemployment to wage bargaining. These analyses assume that there is a well-defined tradeoff between real wages and employment, that is, the unions have some power to affect wages and employment. The power of unions in open economies critically depends, however, on the power firms have in product markets. Hence, the structure of product markets is also important for understanding the interaction between product and labor markets.

D a t a A p p e n d i x

In this paper we use quarter ly data for five European countries. All the data have been seasonally corrected. Both the sample and the used definitions vary, however, due to data availability in the different countries. The samples are the following:

PRICE ADJUSTMENT IN OPEN ECONOMIES 319

Tab le 3e. Error correction price equation for Sweden, 1970:1-1990:4, LHS variable: Z~(p - p * ) ,

OLS Estimation

RHS variables

cons. 0.006 (2.56**)

A(y - l ) ( -2) -0.107 ( - 1.80")

A(p~ - p*) 0.092 (2.19"*)

A(p ~ - p* ) ( - l ) 0.080 (2.25**)

A(p,, - p*)(-2) 0.096 (2.54"*)

~p* -0.518 ( -8.53***)

~p*(-3) 0.127 (2.03* *)

~ d ( - 1 ) 0.088 (2 .28* *)

Ad(-4) 0.129 (3.45* **)

ce(- i ) - 0 . 2 0 3 ( - 2 . 95* * *)

Summary statistics

R 2 0.618

SSR 0.012

DW 1.840

Autocorrelation 1.493

ARCH 1.137

Heteroskedasticity 1.615

Normality 1.018

Validity of instruments

***, **, *: Test statistic significant at 1%, 5%, and 10%, respec- tively. Number in parentheses are calculated as t-values.

Denmark, 1961:1-1990:4; Norway, 1967:1-1990:4; Germany, 1970:1-1989:4; the Netherlands, 1961:1-1990:4; Sweden, 1970:1-1990:4. For Denmark, however, foreign demand for exports only covers the period 1971:1-1990:4, which is therefore the sample for the error-correction model.

Producer prices in manufacturing: Wholesale price index. The source is IFS.

Foreign prices: This series is constructed from bilateral exchange rates and pro- ducer prices in 16 western countries covering between 60% and 70% of total foreign trade. The countries are the United States, Canada, Japan, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, the Netherlands, Norway, Spain, Sweden, Switzerland, and the United Kingdom. Foreign prices in domestic currency were weighted according to the relative importance of total bilateral trade, that is, both imports and exports. Producer prices and exchange rates are all taken from IFS, whereas the weights are calculated on data from various yearbooks on Interna- tional Trade Statistics, United Nations.

320 ANDERSEN AND HANSEN

Wages: Hourly earnings manufacturing industries, taken from IFS, and with index 1980 -- 100. For Denmark only male workers in manufacturing industries, including construction, are regarded, whereas Norwegian wages cover females too, but ex- cluding apprentices and foremen. The Swedish series covers mining, quarrying, and manufacturing. For the Netherlands hourly earnings cover all activities.

Imported raw material prices: Denmark: Price of imported raw materials, OECD Main Economic Indicators. Norway: Import-based raw material price, index 1989 = 1, Bank of Norway databank of Norwegian Economic Time-Series. Germany: Import prices, raw materials, and intermediates (including energy), 1985 = 100, German Institute of Economic Research, quarterly national accounts. Sweden: (Im- port prices, taken from the SNEPQ data base, FIEF, Stockholm). Netherlands: im- port prices, taken from IFS.

Productivity: Constructed from production and employment in manufacturing. For all five countries the data are taken from IFS, have index 1980 = 100, and are seasonally adjusted. For Denmark employment is given by total hours worked by wage earners in manufacturing industries. For Germany production, unlike employ- ment, includes construction while in the Netherlands production excludes construc- tion and installation establishments whereas employment covers manufacturing, mining, and public utilities. Norwegian industrial production covers mining, manu- facturing, electricity, and gas, whereas employment covers all insured wage earners and salaried employees in industry, except foreign seamen. Finally, production in Sweden covers mining, quarrying, and manufacturing.

Foreign demand for domestic export: This series was constructed from total imports in 16 western countries, using the same weighting scheme as for foreign prices. Import series are taken from IFS, except for Germany where data are from quar- terly national accounts, German Institute for Economic Research.

Acknowledgments

An earlier version of this paper was presented at a Paris workshop, "Wage and Price Formation and Unemployment Persistence," financed by a SPES grant (DK-0024). We gratefully acknowledge skillful research assistance by Christian M~ller Dahl.

Notes

1. This setup can easily be derived from a Dixit-Stiglitz (1977) setup of product differentiation (see, e.g., Andersen 1994b).

2. We also tested whether there was cointegration when one variable was omitte ,~, This would be an indication of there being more than one cointegration relationship. This was not the case in any of the countries.

PRICE ADJUSTMENT IN OPEN ECONOMIES 321

3. Remember that under the small open economy assumption, the coefficient to w - p*, ~r 1, will be zero.

4. One exception is the Netherlands, where the price of imported raw materials is insignificant, prob- ably due to the Netherlands being a net exporter of oil.

5. Recursive estimations were performed too. These gave no serious indication of instability. 6. We have included a dummy in the first quarter 1969 for the Netherlands. This is explained by the

introduction of the VAT. Estimates are almost invariant to this dummy, but if it is omitted, we get very bad misspecification tests.

7. If producer prices follow an T(2) process--say inflation follows a random walk--that is, ~2p = u Z=p = ~P-1 + u, u is a white noise process, then £p = P-I + &P-1 '~ P - Ep = ~2p. If instead prices themselves follow a random walk, then price surprises, that is, expectational errors, are given by p - E p = Ap.

References

Aizenman, J. (1989) "Monopolistic Competition, Relative Prices, and Output Adjustment in the Open Economy," Journal of International Money and Finance 8, 5-28.

Alogoskoufis, G., C. Martin, and N. Pittis (1990) "Pricing and Product Market Structure in Open Eco- nomics: An Empirical Test," CEPR Discussion Paper No. 486.

Andersen. T.M. (1994a) Price Rigidity--Causes and Macroeconomic Implications. Oxford: Clarendon Press.

Andersen, T.M. (1994b) "Nominal Price and Wage Adjustment to Foreign Price Changes," Working Paper, Department of Economics, University of Aarhus.

Andersen, T.M. and N.L. Hansen (1992) "Cyclical Properties of Wages and Prices in Open Economies," Memo 1992-10, Institute of Economics, University of Aarhus.

Benassy, J.P. (1993) "Non-Clearing Markets: Microeconomic Concepts and Macroeconomic Applica- tions," Journal of Economic Literature 31,732-761.

Bruce, N. and D.D. Purvis (1985) "The Specificaiton and Influence of Goods and Factor Markets in Open Economy Macroeconomic Models." In R.W. Jones and P.B. Kenen (eds), Handbook of Interna- tional Economics. Amsterdam: Elsevier Science Publishers.

Dixit, A. and J.E. Stiglitz (1977) "Monopolistic Competition and Optimum Product Diversity," American Economic Review 67, 297-308.

Dixon, H. (1993) "Imperfect Competition and Open Economy Macroeconomics:' In van der Ploeg (ed), Handbook of International Economics. Oxford: Basil Blackwell.

Dixon, H. and N. Rankin (1994) "Imperfect Competition and Macroeconomics: A Survey," Oxford Eco- nomic Papers, 46, 171-199.

Geroski, RA. (1992) "Price Dynamics in UK Manufacturing: A Microeconomic View," Economica 59, 403-419.

MacKinnon, J.G. (1991) "Critical Values for Cointegration Tests." In R.F. Engle and C.W.J. Granger (eds), Long-Run Economic Relationships. Oxford: Oxford University Press, pp. 267-276.

Silvestre, J. (1993) "The Market-Power Foundations of Macroeconomic Policy" Journal of Economic Literature 31, 105-141.

White, H. (1980) "A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity," Econometrica 48, 817-838.