Embed Size (px)

Citation preview

www.cbre.com.cn Third Quarter 2011

© 2011, CB Richard Ellis, Inc.

People‘s Republic of China

TABLE OF CONTENTS

ECONOMIC BACKGROUND

To rein in the liquidity that has pushed up inflation, China hiked the required reserve ratio (RRR) for banks once more in the third quarter of the year, raising it to a new high of 6.56%. The slowdown in fixed asset investment growth to 25% for the first eight months in 2011 consequently dragged down China’s economic growth. Though consumption maintained steady growth, whether the recovery of foreign trade would continue in the midst of a global economy downturn is yet to be seen. The leading indicator, the purchasing managers’ index (PMI), fell gradually from April this year, yet rebounded slightly in August and September due to seasonal effects. The mediocre performance of this index reflects a cautious outlook for the economy in the short to medium term.

Asset price inflation did not accelerate, mainly because the number of cities with flat or downward housing price on a month-on-month basis increased to 47 in August, from 31 in July and 26 in June. This mitigates pressure for the government to roll out a more aggressive money-tightening policy. It is more likely that the People’s Bank of China (PBoC) will continue its stance of moderate liquidity tightening for the rest of the year. However the government may look to relax lending to SME’s as it seeks to address “shadow” lending concerns. Amidst external economic volatility both in the U.S. and the Eurozone, the RMB is expected to continue its slow but steady upward trend to balance the negative impact on export growth with inflationary pressure. Thus, the exchange rate policy should still favour the property market over the short period.

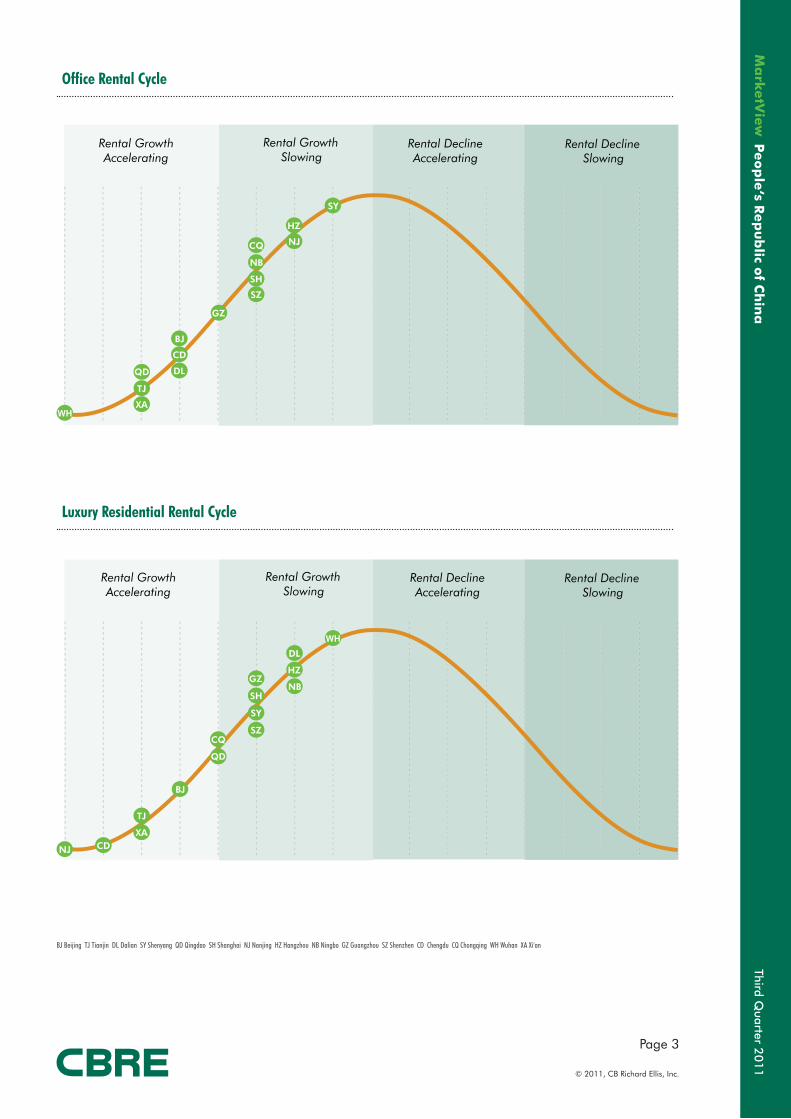

The office rental market generally showed continued growth in the third quarter of the year on the back of across-the-board rental growth in the previous quarter. First-tier cities in particular demonstrated growth from the high base of the first half of the year, with quarterly gains of around 4% to 9%. Inflating costs, coupled with unavailability of property alternatives remain major challenges for MNCs looking to consolidate large operations under one roof, pushing some occupiers to turn to decentralized areas.

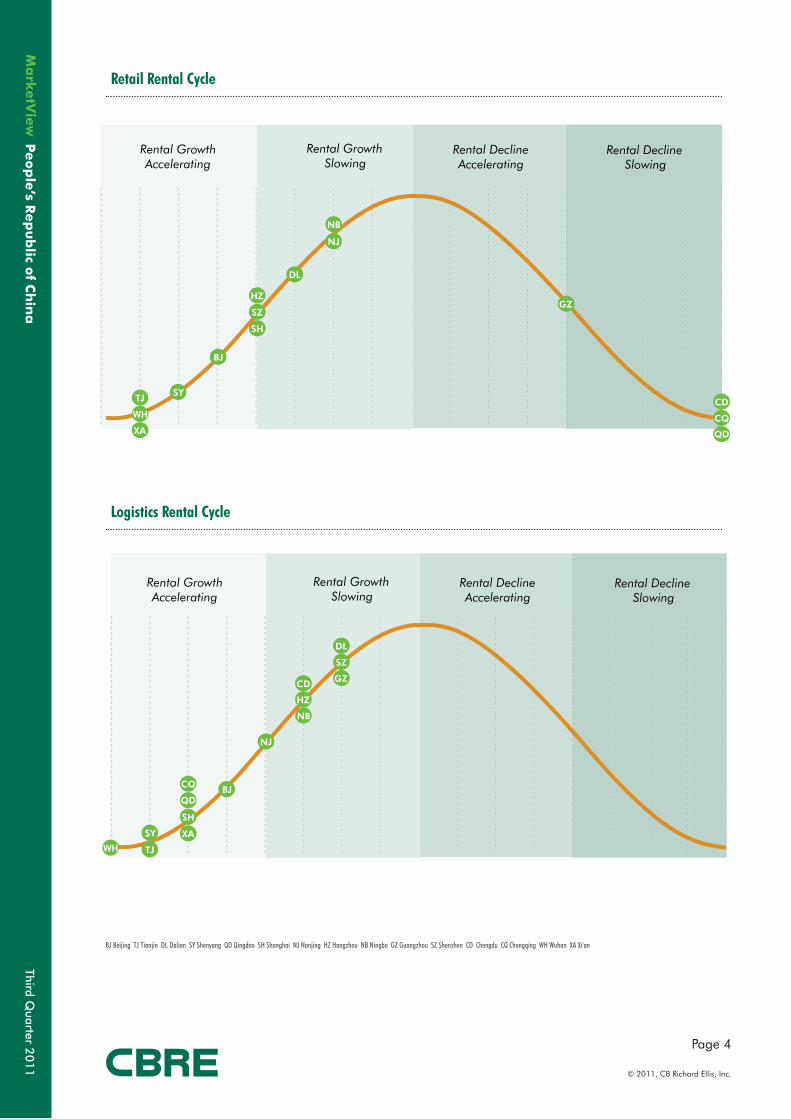

Although some cities, including Beijing, Shenyang and Wuhan, faced adequate retail property supply (each above 100,000 sm for the quarter), the prime retail market across China closed September largely on a positive note, as demand and take-up increased notably. Twelve of 15 cities we cover recorded brisk growth in rentals amidst buoyant market sentiment. Even new projects coming onto the market were well sought after as reflected in the low vacancy rates.

There have been a series of recent housing purchase restrictions across nearly all the cities we cover, with the exception of Chongqing, which adopted a separate pilot scheme of property tax and subsequent measures to reinforce the implementation of such restrictions in mid-2011. As a result luxury residential transacted volumes were severely dampened, while prices held firm. Only Qingdao, Hangzhou and Nanjing recorded tentative signs of price corrections amidst prevailing wait-and-see market sentiment. In contrast to this, the logistics property market marched on, highlighted by rising demand for modern facilities across second-tier cities, often driven by the cost advantage of inland regions. Cities with strategic positions such as Wuhan and Chongqing are deemed dominant nodes within the logistics landscape, offering access to a mature supply chain, and witnessed notable upward pressure on rentals for logistics facilities.

2 Feature Story3 Office Rental Cycle

Luxury Residential Rental Cycle4 Retail Rental Cycle

Industrial Rental Cycle5 Prime Office Rents/Prices

Luxury Apartment Rents/Prices6 Prime Retail Rents

Logistics Rents

7 NORTH CHINA8-9 Beijing10 Tianjin11 Dalian12 Shenyang13 Qingdao

14 EAST CHINA15-16 Shanghai17 Nanjing18 Hangzhou19 Ningbo

20 SOUTH CHINA21-22 Guangzhou23 Shenzhen

24 CENTRAL & WEST CHINA25-26 Chengdu27 Chongqing

28 Wuhan

29 Xi’an

MARKET PERFORMANCE

Third Quarter 2

01

1

Page 2

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

FEATURE STORY

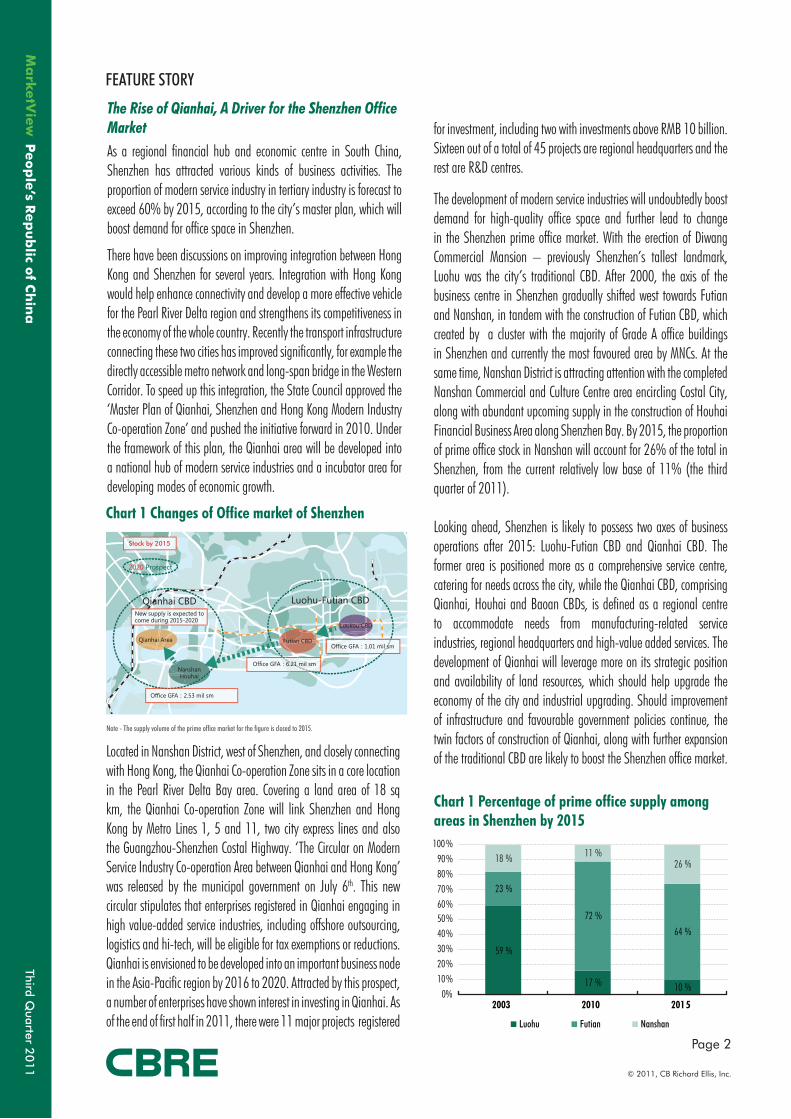

As a regional financial hub and economic centre in South China, Shenzhen has attracted various kinds of business activities. The proportion of modern service industry in tertiary industry is forecast to exceed 60% by 2015, according to the city’s master plan, which will boost demand for office space in Shenzhen.

There have been discussions on improving integration between Hong Kong and Shenzhen for several years. Integration with Hong Kong would help enhance connectivity and develop a more effective vehicle for the Pearl River Delta region and strengthens its competitiveness in the economy of the whole country. Recently the transport infrastructure connecting these two cities has improved significantly, for example the directly accessible metro network and long-span bridge in the Western Corridor. To speed up this integration, the State Council approved the ‘Master Plan of Qianhai, Shenzhen and Hong Kong Modern Industry Co-operation Zone’ and pushed the initiative forward in 2010. Under the framework of this plan, the Qianhai area will be developed into a national hub of modern service industries and a incubator area for developing modes of economic growth.

Chart 1 Percentage of prime office supply among areas in Shenzhen by 2015

The Rise of Qianhai, A Driver for the Shenzhen Office Market

The development of modern service industries will undoubtedly boost demand for high-quality office space and further lead to change in the Shenzhen prime office market. With the erection of Diwang Commercial Mansion – previously Shenzhen’s tallest landmark, Luohu was the city’s traditional CBD. After 2000, the axis of the business centre in Shenzhen gradually shifted west towards Futian and Nanshan, in tandem with the construction of Futian CBD, which created by a cluster with the majority of Grade A office buildings in Shenzhen and currently the most favoured area by MNCs. At the same time, Nanshan District is attracting attention with the completed Nanshan Commercial and Culture Centre area encircling Costal City, along with abundant upcoming supply in the construction of Houhai Financial Business Area along Shenzhen Bay. By 2015, the proportion of prime office stock in Nanshan will account for 26% of the total in Shenzhen, from the current relatively low base of 11% (the third quarter of 2011).

Looking ahead, Shenzhen is likely to possess two axes of business operations after 2015: Luohu-Futian CBD and Qianhai CBD. The former area is positioned more as a comprehensive service centre, catering for needs across the city, while the Qianhai CBD, comprising Qianhai, Houhai and Baoan CBDs, is defined as a regional centre to accommodate needs from manufacturing-related service industries, regional headquarters and high-value added services. The development of Qianhai will leverage more on its strategic position and availability of land resources, which should help upgrade the economy of the city and industrial upgrading. Should improvement of infrastructure and favourable government policies continue, the twin factors of construction of Qianhai, along with further expansion of the traditional CBD are likely to boost the Shenzhen office market.

Chart 1 Changes of Office market of Shenzhen

Note - The supply volume of the prime office market for the figure is closed to 2015.

Located in Nanshan District, west of Shenzhen, and closely connecting with Hong Kong, the Qianhai Co-operation Zone sits in a core location in the Pearl River Delta Bay area. Covering a land area of 18 sq km, the Qianhai Co-operation Zone will link Shenzhen and Hong Kong by Metro Lines 1, 5 and 11, two city express lines and also the Guangzhou-Shenzhen Costal Highway. ‘The Circular on Modern Service Industry Co-operation Area between Qianhai and Hong Kong’ was released by the municipal government on July 6th. This new circular stipulates that enterprises registered in Qianhai engaging in high value-added service industries, including offshore outsourcing, logistics and hi-tech, will be eligible for tax exemptions or reductions. Qianhai is envisioned to be developed into an important business node in the Asia-Pacific region by 2016 to 2020. Attracted by this prospect, a number of enterprises have shown interest in investing in Qianhai. As of the end of first half in 2011, there were 11 major projects registered

for investment, including two with investments above RMB 10 billion. Sixteen out of a total of 45 projects are regional headquarters and the rest are R&D centres.

2020 Prospect

Qianhai CBD Luohu-Futian CBDNew supply is expected to

come during 2015-2020

Stock by 2015

Office GFA:2.53 mil sm

Office GFA:6.21 mil sm

Office GFA:1.01 mil smQianhai Area

NanshanHouhai

Futian CBD

Luokou CBD

59 %

17 % 10 %

23 %

72 %

64 %

18 % 11 %26 %

0%10%20%30%40%50%60%70%80%90%

100 %

2003 2010 201 5

Luohu Futian Nanshan

Third Quarter 2

01

1

Page 3

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Office Rental Cycle

Luxury Residential Rental Cycle

BJ Beijing TJ Tianjin DL Dalian SY Shenyang QD Qingdao SH Shanghai NJ Nanjing HZ Hangzhou NB Ningbo GZ Guangzhou SZ Shenzhen CD Chengdu CQ Chongqing WH Wuhan XA Xi'an

CD

WH

SY

XA

SH

DLQD

BJ

GZ

SZ

TJ

NJCQ

HZ

NB

Rental Growth Accelerating

Rental Growth Slowing

Rental Decline Accelerating

Rental Decline Slowing

CD

WH

SY

XA

SH

DL

QD

BJ

GZ

SZ

TJ

NJ

CQ

HZ

NB

Rental Growth Accelerating

Rental Growth Slowing

Rental Decline Accelerating

Rental Decline Slowing

Third Quarter 2

01

1

Page 4

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Retail Rental Cycle

Logistics Rental Cycle

BJ Beijing TJ Tianjin DL Dalian SY Shenyang QD Qingdao SH Shanghai NJ Nanjing HZ Hangzhou NB Ningbo GZ Guangzhou SZ Shenzhen CD Chengdu CQ Chongqing WH Wuhan XA Xi'an

CDWH

SY

XA

SH

DL

QD

BJ

GZSZ

TJ

NJ

CQ

HZ

NB

Rental Growth Accelerating

Rental Growth Slowing

Rental Decline Accelerating

Rental Decline Slowing

CD

WH

SY XA

SH

DL

QDBJ

GZ

SZ

TJ

NJ

CQ

HZ

NB

Rental Growth Accelerating

Rental Growth Slowing

Rental Decline Accelerating

Rental Decline Slowing

Third Quarter 2

01

1

Page 5

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Prime Office Rents/Prices

Luxury Apartment Rents/Prices

Price

s (RM

B ps

m)

Price

s (RM

B ps

m)

Rent

s (R

MB

psm

/mon

th)

Rent

s (R

MB

psm

/mon

th)

Q-O-Q CHANGE (%)

Q-O-Q CHANGE (%)

RENTS*

PRICES**

RENTS*

PRICES**

Beiji

ng

Dalia

n

Qing

dao

Tianj

in

Shen

yang

Shan

ghai

Hang

zhou

Nanj

ing

Ning

bo

Guan

gzho

u

Shen

zhen

Chen

gdu

Chon

gqin

g

Xi‘an

Wuha

n

Beiji

ng

Dalia

n

Qing

dao

Tianji

n

Shen

yang

Shan

ghai

Hang

zhou

Nanji

ng

Ning

bo

Guan

gzho

u

Shen

zhen

Chen

gdu

Chon

gqing Xi‘an

Wuha

n

N O R T H

N O R T H

E A S T

E A S T

S O U T H

S O U T H

W E S T

W E S T

CENTRAL

CENTRAL

# On net floor basis, excluding management fees* On gross floor basis, excluding management fees Database adjustment

0

50

100

150

200

250

300

0

10,000

20,000

30,000

40,000

50,000

60,000

0

50

100

150

200

250

300

350

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

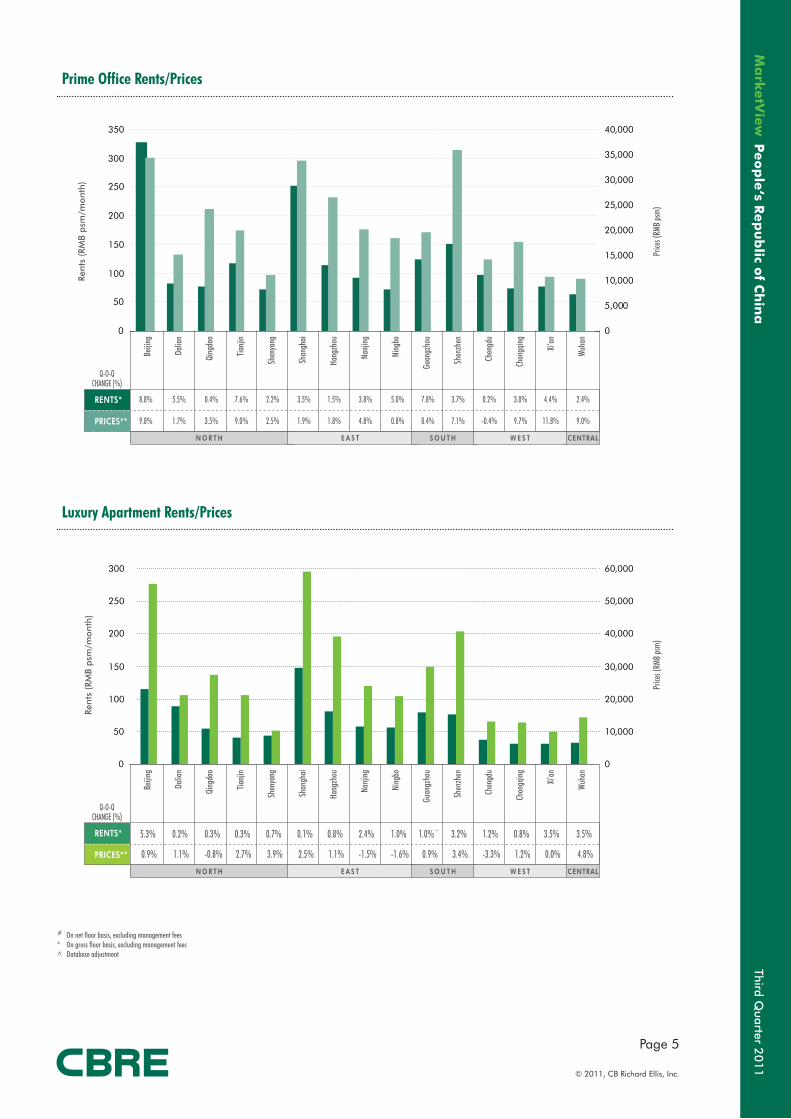

8.8% 5.5% 0.4% 7.6% 2.2% 3.5% 1.5% 3.8% 5.0% 7.8% 3.7% 0.2% 3.0% 4.4% 2.4%

9.8% 1.7% 3.5% 9.0% 2.5% 1.9% 1.8% 4.8% 0.8% 8.4% 7.1% -0.4% 9.7% 11.8% 9.0%

5.3% 0.2% 0.3% 0.3% 0.7% 0.1% 0.8% 2.4% 1.0% 1.0%^ 3.2% 1.2% 0.8% 3.5% 3.5%

0.9% 1.1% -0.8% 2.7% 3.9% 2.5% 1.1% -1.5% -1.6% 0.9% 3.4% -3.3% 1.2% 0.0% 4.8%

Third Quarter 2

01

1

Page 6

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Prime Retail Rents

Logistics Rents

Gro

und

Floo

r Re

nts

(RM

B ps

m/d

ay)

Rent

s (R

MB

psm

/mon

th)

Q-O-Q CHANGE (%)

Q-O-Q CHANGE (%)

GROUND FLOORRENTS#

RENTS*

Beiji

ng

Dalia

n

Qing

dao

Tianj

in

Shen

yang

Shan

ghai

Hang

zhou

Nanj

ing

Ning

bo

Guan

gzho

u

Shen

zhen

Chen

gdu

Chon

gqin

g

Xi‘an

Wuha

n

Beiji

ng

Dalia

n

Qing

dao

Tianji

n

Shen

yang

Shan

ghai

Hang

zhou

Nanji

ng

Ning

bo

Guan

gzho

u

Shen

zhen

Chen

gdu

Chon

gqing Xi‘an

Wuha

n

N O R T H E A S T S O U T H W E S T CENTRAL

N O R T H E A S T S O U T H W E S T CENTRAL

# On net floor basis, excluding management fees* On gross floor basis, excluding management fees

0

10

20

30

40

50

60

0

5

10

15

20

25

30

35

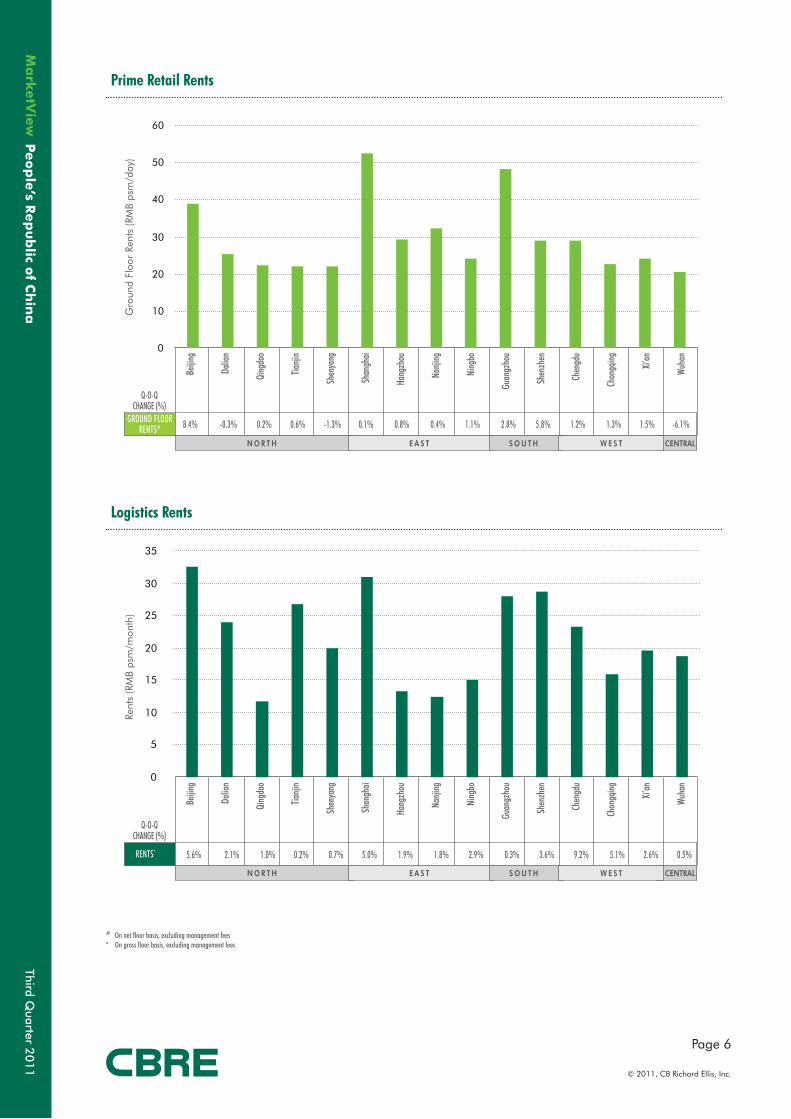

8.4% -0.3% 0.2% 0.6% -1.3% 0.1% 0.8% 0.4% 1.1% 2.8% 5.8% 1.2% 1.3% 1.5% -6.1%

5.6% 2.1% 1.0% 0.2% 0.7% 5.0% 1.9% 1.8% 2.9% 0.3% 3.6% 9.2% 5.1% 2.6% 0.5%

Third Quarter 2

01

1

Page 7

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

NORTH CHINAThe Beijing office market continued to show growth this quarter. Rents grew 8.8% q-o-q, and vacancy rates further dropped 0.8 percentage points to 6.8%. With insufficient supply expected in the next two to three years, the bullish market should continue. Dalian also experienced strong growth, with demand from new tenants, such as in financial institutions, and expansion of existing tenants. This brought up the rent level to RMB 81.7 psm per month, a 5.5% growth q-o-q. In the Tianjin market, due to high quality new supply coming on stream and continued demand for quality space, we witnessed a substantial 7.6% average rent growth q-o-q overall. In general, the Northern China office market demonstrated strong rental growth in the quarter due to the supply-demand imbalance for most cities.

In the third quarter we saw diverse performance of the retail market in northern cities. Backed by strong demand and more experienced retail operators and developers, the Beijing market witnessed an 8.4% quarterly rent growth and 0.4% vacancy decrease, even with 112,000 sm of new supply coming on board. With the exception of Shenyang, other northern cities have had a relatively quiet third quarter. Because of the 388,000-sm of new supply, the vacancy rate in Shenyang rose 4.7 percentage points to 18.8%, while rent decreased 1.3% q-o-q.

During the quarter all four emerging northern cities we monitor presented a slow growth in the industrial property market. The rent growth ranged from 2.1% to 0.1%. Land transaction prices edged down slightly for most markets, except Tianjin, which had a 0.5% q-o-q increase. Beijing

RENTAL

Beijing Dalian Qingdao Tianjin Shenyang

Office

Luxury Residential

Retail

Industrial

BEIJINGTIANJIN

QINGDAO

SHENYANG

DALIAN

industrial witnessed a strong quarter, with rent growth of 5.6% q-on-q for logistics and 2.5% for manufacturing plant.

Under the impact of the government policies, the luxury residential market has cooled for most cities. Shenyang was the only market to have a 3.9% q-o-q price increase, while the price appreciations for all other markets were limited. Luxury housing rentals increased materially in Beijing, with 5.3% q-o-q, backed by strong demand from expatriate staff of MNCs.

Third Quarter 2

01

1

Page 8

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

0

50

100

150

200

250

Q1

93

Q3

93

Q1

94

Q3

94

Q1

95

Q3

95

Q1

96

Q3

96

Q1

97

Q3

97

Q1

98

Q3

98

Q1

99

Q3

99

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Office Luxury Residential Retail Industrial

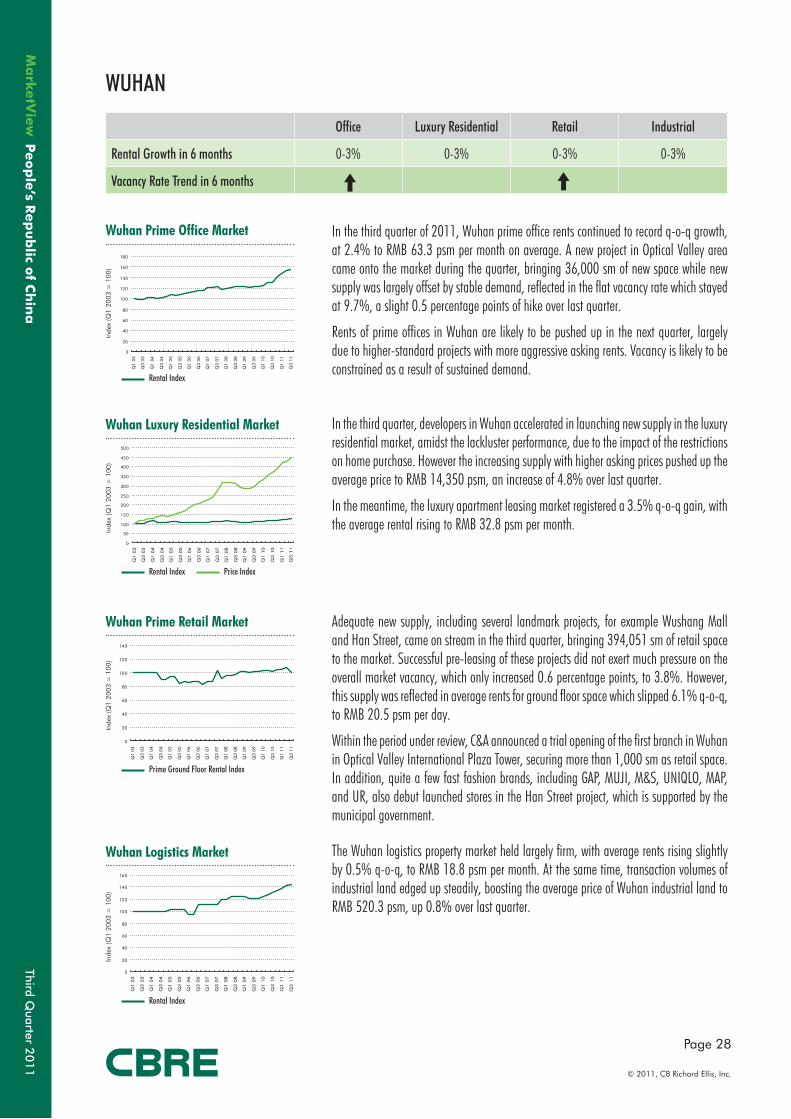

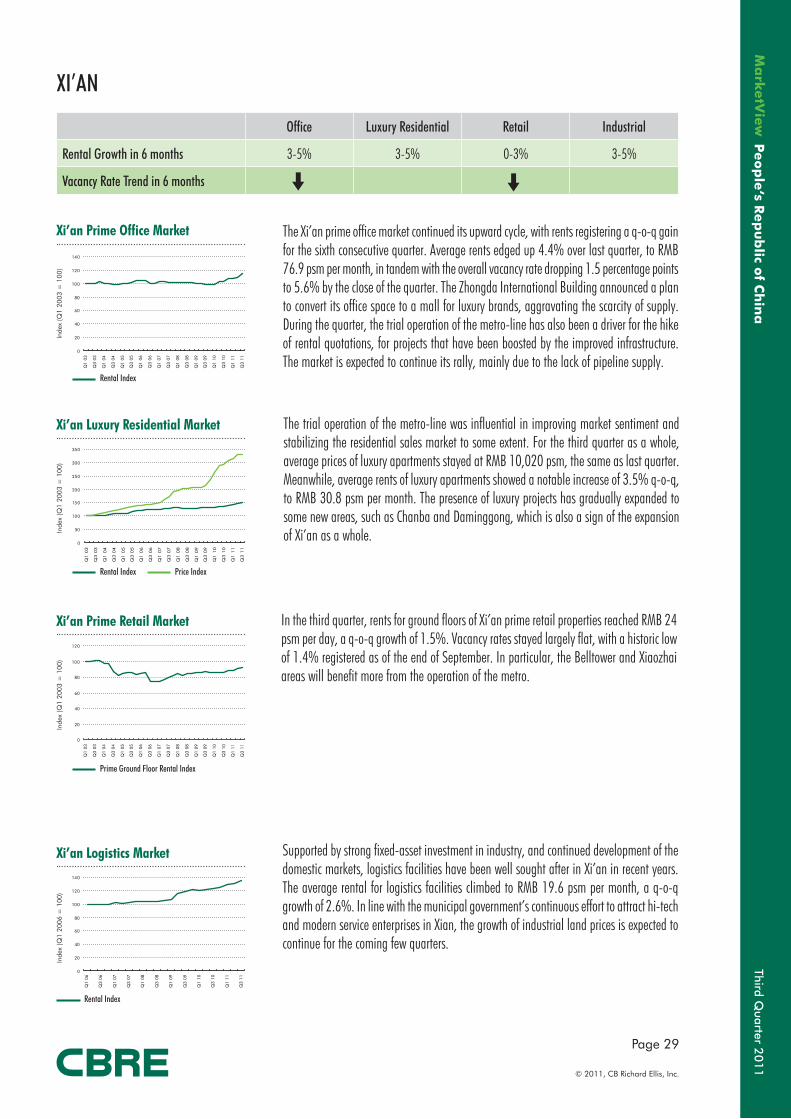

Rental Growth in 6 months 8-10% 3-5% 5-8% 5-8%

Vacancy Rate Trend in 6 months

Beijing Prime Office Market

Rental Index Price Index

Rental Index Price Index

Inde

x (Q

1 19

93 =

100

)

Beijing Luxury Residential Market

Inde

x (Q

1 20

00 =

100

)

BEIJING

The Beijing prime office market extended its rally into the third quarter of the year. Two new projects - Phase II of Phoenix Plaza located in Lufthansa Area and Indigo in Jiuxianqiao Area - completed in the quarter, providing 46,000 and 56,000 sm of office space, respectively, resulting in slight relief of the short supply in the market. Pent-up demand, which was constrained by limited rental office space, helped take up most of the new supply in the quarter and net absorption amounted to 160,000 sm, slightly down over the previous quarter, yet still high. The overall vacancy rate in the market dipped by 0.8% q-o-q, to 6.8%. Meanwhile, rentals continued to rise in the context of the short supply. At the end of this quarter, the quoted rentals for prime offices in Beijing surged by 8.8% q-o-q to RMB 327.6 psm per month.

It is expected that for the remainder of this year, Beijing will see only one office project completed, with a GFA of 75,000 sm. However, new office supply is far below market demand, and the pressure of tight supply will persist for some time. The trend of continuing high demand is obvious, and the market vacancy rate will continue to fall with the gradually reducing vacant space, which suggests that rentals for offices in Beijing will retain a rising momentum in the fourth quarter.

Despite the boost effect of September as a traditional peak season, the luxury residential sales market turned sluggish in the third quarter, clouded by purchase restrictions that began in early 2011. The municipal government remained cautious in issuing pre-sale licences for luxury residential projects, which is causing the delay of launches for some luxury residential projects with relative high prices. On the other hand, most developers have speeded up their sales schedules in order to improve sales performance and cash flow in tandem. New supply increased over last quarter, mostly however at lower pricing levels. Residential projects located in the core area with reasonable prices can still attract homebuyers and achieved favourable market response. Average asking prices for luxury apartments was up 0.9% q-o-q to RMB 55,277 psm for the third quarter, with a slowing growth trend.

Sustained economic growth in China has driven a large number of multinational companies to increase investment into the country, leading to a continuous growth of the number of expatriate staff relocating to Beijing. This is maintaining the demand for luxury residential units. Vacancy rates continued to fall and have stimulated a rise in rents. In addition, high inflation and soaring housing prices contributed somewhat to rent increases. In the third quarter of 2011, the average rent of Beijing luxury apartments rose by 5.3% q-o-q to RMB 115.7 psm per month.

Third Quarter 2

01

1

Page 9

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

0

20

40

60

80

100

120

Q1

98

Q3

98

Q1

99

Q3

99

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Prime Ground Floor Rental Index

Rental Index

Beijing Prime Retail Market

Inde

x (Q

1 19

98 =

100

)

Beijing Logistics Market

Inde

x (Q

1 20

07 =

100

)

BEIJINGIn the third quarter of 2011, two new projects, Fenzhongsi iShine City and Oak Bay Living Mall I, were opened, offering a total of 112,000 sm of new supply to the market. Meanwhile, demand continued to edge up and outstripped supply in the market. As a result, the overall vacancy rate decreased slightly by 0.4 percentage points over the last quarter to 9.5%.

More and more projects began to lift their rental levels on the back of strong demand in the market. As a result, the average rental for ground floor space increased significantly by 8.4% q-o-q to RMB 38.9 psm per day. Major transactions recorded in the market included Hollister leasing 1,180 sm in Indigo and opening its first shop in Beijing. H&M, Gap and Moussy also took up 2,320, 1,145 and 484 sm respectively in Indigo. I.T committed to about 3,000 sm in Parkview Green. Lane Crawford signed with Yintai Parklife to open its second store in Beijing. High quality projects, including Shin Kong Place, The Mall at Oriental Plaza and Joy City Xidan, were actively adjusting their tenant mix to attract new brands in Beijing.

The rental level is expected to continue to improve in the next few quarters. In the future, more projects may choose to adjust their tenant mix, as the performance of some projects has achieved distinct improvement after restructuring of their tenant mix.

In the third quarter, Beijing industrial land prices changed pattern from that seen in previous quarters and only increased slightly by 1.2% q-o-q, to RMB 1,948 psm. Average rents of manufacturing, logistics and R&D facilities continued to expand, by 2.5%, 5.6% and 1.9% q-o-q respectively, to RMB 44.4, 32.6 and 106.4 psm per month.

During the quarter, Yicheng International Centre and Hulongsen III Phase II in the BDA area were completed, adding a total of 148,882 sm of new supply. IT and pharmaceutical companies continued to expand in Beijing. HP and Intel leased 8,900 and 5,000 sm, respectively, in UBP Central Plaza. Novo Nordisk and Protgen committed to 10,500 and 7,000 sm in Zhongguancun Life Science Park. Electronic commerce continued to dominate the logistics market demand. One example is VipShop who recently took 25,000 sm in Beijing Capital Highway.

In the next few quarters, rental levels are expected to continue to improve. Owing to the increasing difficulty in sourcing quality space across most major industrial clusters that are fully occupied, quite a few companies had to relocate to developments outside these major clusters, with lower standards, or in emerging industrial areas. It is expected that there will be increasing deals completed in these areas in ensuing months.

0

20

40

60

80

100

120

140

Q1

07

Q2

07

Q3

07

Q4

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Q4

10

Q1

11

Q2

11

Q3

11

Third Quarter 2

01

1

Page 10

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Tianjin Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Tianjin Prime Retail Market

Tianjin Logistics Market

Tianjin Luxury Residential Market

TIANJIN

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 0-3% 3-5% 0-3%

Vacancy Rate Trend in 6 months

With the erection of Jinta Office Building in Heping District, a total of 203,900 sm of new space entered the prime office market in the third quarter. High asking rents for new projects is considered to be a major driver for pushing rents up by 7.6% q-o-q, to RMB 119.6 psm per month. Nevertheless, abundant space delivered by the new projects lifted the overall vacancy rate to 23.1%, a remarkable rise of 11.6 percentage points.

There is no new supply in the pipeline for the rest of the year. This should help the market stabilise somewhat with vacancy rates moderating.

Despite being overshadowed by tightening controls, the Tianjin residential market continued to show increases in the third quarter of the year. The sale transaction volume of luxury apartments rose, with average prices’ marked up by 2.7% q-o-q, reaching RMB 21,069 psm for the close of the quarter.

The luxury residential leasing market remained on an upward trajectory, with average rentals of apartments recording a q-o-q gain of 0.7%, standing at RMB 40.5 psm per month.

The Tianjin prime retail market continued to improve with average rentals on ground floor units up by 0.6% to RMB 21.9 psm per day. Supporting the drop in overall vacancy rate to 11.4%, down by 1.5 percentage points q-o-q, was that more retailers continued to enter into the Tianjin market. Major leasing transactions included Sundan’s leasing 300 sm in Isetan to open its first shop in Tianjin. In addition, Sundan also committed to 2,400 sm in Galaxy Mall. Godiva, emoi and Pepper Lunch also have plans to secure their footholds in Tianjin in Isetan. In addition, several brands belonging to Inditex, as well as UNIQLO, H&M and WE, have also signed with Tianjin Aqua City.

The Tianjin industrial property market maintained steady growth during the past quarter. Average rents of logistics facilities edged up 0.2% q-o-q, to RMB 26.8 psm per month, while industrial land prices surged by 0.5%, to RMB 451.6 psm. Recently, e-commerce companies have led the growing demand for new logistics facilities. Dangdang signed an agreement with Tianjin Jingbin industry Park to locate its north China headquarters in the park, while Amazon took 100,000 sm in GLP Wuqing Park. With no sign of demand abating, it is expected that the rental levels will continue to rise in the future.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

50

100

150

200

250

300

350

400

450

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

180

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

10

30

50

70

90

110

130

150

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 11

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Dalian Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Dalian Prime Retail Market

Dalian Logistics Market

Dalian Luxury Residential Market

DALIAN

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 0-3% 0-3% 0-3%

Vacancy Rate Trend in 6 months

Dalian prime office market remained active during the third quarter of 2011, as manifested by steadily increasing demand both for new business setups and expansion. Driven by the high asking rents for new properties, the average rentals edged up by 5.5% q-o-q to RMB 81.7 psm per month, whereas the overall vacancy rate increased 0.4 percentage points to 11.7% over last quarter. The occupational demand from financial service companies remained robust; for instance, Yingda Property Insurance recently leased 1,300 sm in International Ocean Building.

Modern Service Headquarters Tower, with an office GFA of 54,000 sm on Xi’an Road, is scheduled to be launched at the end of this year, which is projected to lift the overall vacancy level in the last quarter.

Influenced by the combined effect of purchase restrictions, credit crunches and other curbing measures, the transaction volume of Dalian luxury apartment remained in its declining trend, dragging down the upward momentum of prices in tandem, which mounted to RMB 21,158 psm, up 1.1% over the second quarter.

Meanwhile, driven by the decreased demand in Dalian residential sales market and the positive effect from tourist season, the luxury residential leasing market was recorded a rise of 0.2% q-o-q to RMB 88.5 psm per month for average rents.

Dalian prime retail property market remained somewhat stable recently, with rentals on the ground floor registering a minor decrease of 0.3% q-o-q on average, to RMB 25.5 psm per day. Due to adjustments of tenant mix for some retail projects during the quarter, the vacancy rate increased 0.3 percentage points to 6.8%. The biggest Zara store in North-east China, located in Qiulin Women’s Store, kicked off operation with more than 2,000 sm of retail space, demonstrating continuous expansion demand of international brands in Dalian.

As the pipeline supply for the whole year of 2011 has been rare, the vacancy rate is expected to gear down in the future, and rentals will keep a stable ascendant trend.

In the third quarter, the Dalian logistics facilities market experienced a mild rise in rents for most projects. The demand of logistics facilities remained stable, rendering support to a 2.1% q-o-q gain for average rents, reaching RMB 23.9 psm per month. Owing to a lack of transactions of premium sites, the average industrial land price recorded a mild decline of 0.3% at the same time, to RMB 518 psm. In this quarter, industrial land transactions were mainly recorded in Ganjingzi District.

Looking ahead, on the basis of adequate supply, rentals of Dalian logistics facilities are expected to remain stable in the short term. In addition, it is unlikely we will experience marked changes in prices for Dalian industrial land in the near future.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

40

80

120

160

200

240

280

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 12

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Shenyang Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Shenyang Prime Retail Market

Shenyang Logistics Market

Shenyang Luxury Residential Market

SHENYANG

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 3-5% 0-3% 0-3%

Vacancy Rate Trend in 6 months

The CR Building and Huaqiang Square were launched, with a GFA of 103,500 sm, in the third quarter, alleviating the shortage of supply in the prime office market. The overall vacancy rate of the market rebounded by 1.6 percentage points, to 11.9%. Nevertheless, the high quotation of rents for the CR Building lifted average rent of the market to RMB 72.3 psm per month, up 2.2% q-o-q.

North Media Building is scheduled to complete by the end of this year with GFA space of 87,000 sm. On account of the supply pipeline, the overall vacancy rate will tend to climb up over the short term.

The influence of curbing measures was more evident in the third quarter. Coupled with sluggish sales volume, the Shenyang luxury apartment saw a slowdown in price growth, which moderated by 3.9% q-o-q, reaching RMB 10,153 psm. In the meantime, approximately 70% of transactions were recorded outside the Second Ring Road area, which has not been affected by home purchase restrictions thus far.

The Shenyang luxury leasing market remained fairly stable during the same period, with rents inflating 0.7% q-o-q, to RMB 44.1 psm per month.

In the third quarter of the year, the Shenyang prime retail market remained buoyant. Nevertheless, new space amounting to GFA 388,000 sm, by Longemont Shopping Centre, lifted the overall vacancy rate by 4.7 percentage points, to 18.8%, albeit partly offset by the strong performance in market net absorption. International chain brands increased their expansion in the Shenyang market. For instance, during the quarter, Burberry opened its third Shenyang store in Mixc.

By the end of this quarter, average asking rents for ground floor space fell to RMB 22 psm per day, 1.3% down over the middle of the year, mainly influenced by the increased supply.

The Shenyang industrial market stayed largely stable in the third quarter, with average asking rents of logistics facilities marginally inflating by 0.7% q-o-q to RMB 20 psm per month. The industrial land sales price also stayed stable at RMB 341.7 psm, mainly attributable to sufficient new supply in the market.

Looking ahead, given sufficient supply of modern logistics facilities in the pipeline, such as GLP’s Hunnan Logistics Park - which is expected to start operation in 2012 - rents in the sector are likely to see calm performance over the short term.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

160

180

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 13

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Qingdao Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Qingdao Prime Retail Market

Qingdao Logistics Market

Qingdao Luxury Residential Market

QINGDAO

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 0-3% 0-3% 0-3%

Vacancy Rate Trend in 6 months

The Qingdao prime office market stayed buoyant during the quarter. The citywide average asking rent continued its upward trend for the fourth consecutive quarter, up 0.4% q-o-q to RMB 76.7 psm per month. The rental increase was firmly underpinned by a sustained high level of leasing activity, up to 43,124 sm in terms of quarterly take-up. To quote a few examples, GE and Hanhua Guarantee committed to 638 and 420 sm, respectively, in Shangri-la Centre, while two SOEs both leased a 1,502-sm unit in Zhongshang Plaza. Zhongshang Plaza was completed with 41,304 sm of space supplied to the market. However, the overall vacancy rate dropped 0.3 percentage points to 11.5%.

An additional 120,000 sm of prime office space will be completed in the next six months, including Capland Centre and IMC Centre.

The impact of the restrictions on home purchase gradually filtered through to the luxury residential sector, as manifested in price corrections for projects located in the outer areas. Average prices thus came under pressure, down 0.8% q-o-q to RMB 27,277 psm. On the other hand, projects in the central areas largely held firm.

During the same period, the luxury leasing sector remained buoyant, with average rents reaching RMB 55 psm per month, up 0.3% q-o-q.

In the quarter, the Qingdao prime retail property market experienced a mild rise for most projects. Rentals on ground floors registered a minor increase of 0.2% q-o-q on average, to RMB 22.4 psm per day. Without the addition of new space, vacancy edged down further by 0.3 percentage points to 7.8%. Demand remained steady - in line with expansions of more international brands. For instance, Christian Audigier and Agnes b newly established their presences in Hisense Plaza during this quarter.

Zendai Thumb Plaza, located in Laoshan District and Rocky City in Licun respectively debuted in a pre-leasing seminar in the quarter. Pre-lease for these two projects proceeded well and is expected to attract more brands into the Qingdao market.

Average rents of Qingdao logistics facilities recorded a quarterly gain of 1%, to RMB 11.7 psm per month. Industrial land prices stayed generally firm, but average prices dropped marginally by 0.7% to RMB 327.9 psm. The bulk of land sales transactions were concentrated in Chengyang district and Laixi county. The largest industrial land transaction in terms of land area recorded for the third quarter was the acquisition of a 225,928-sm site in Laixi County by Nestle (Qingdao) for a total consideration of RMB 32.98 million.

In light of adequate supply in the pipeline, both rents and land prices are expected to witness a stable trend in the near future.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

350

400

450

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 14

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

NANJING SHANGHAI

HANGZHOUNINGBO

EAST CHINAThere is no sign of abatement in the office market across East China; all four cities we cover in the region registered positive gain in rentals during the quarter. The external economic volatility did not reduce market demand, as evidenced by a new high of net absorption in Shanghai for this year, which has supported continuous rental growth. Meanwhile, the prime retail property market fared well, underpinned by sustaining high growth of personal incomes in the region.

Despite the fact that autumn is usually a season when the market warms up, some corrections have appeared. The earlier scenario, where prices held stable or even edged up amidst shrinking transactions, has started giving way to deeper price cuts by developers to speed up the rebuilding of cash flow. As a result, both Hangzhou and Nanjing recorded downturns in prices for the first time since 2009. At the same time, more home seekers have chosen to keep renting rather than purchasing, in anticipation of a fall in prices, contributing to the continuing rise in rents. For industrial properties, fuelled by better than expected performance in the manufacturing sector, the logistics facilities market continued to gather steam across the board. The expansion of the industrial market has attracted more developer interest. For example, in the region, GLP newly expanded to Hangzhou and Suzhou via a joint venture recently established, while DB Schenker Logistics also announced expansion across China, both in the coastal regions and the interior areas.

RENTAL

Shanghai Hangzhou Nanjing Ningbo

Office

Luxury Residential

Retail

Industrial

Third Quarter 2

01

1

Page 15

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Shanghai Prime Office Market

Rental Index Price Index

Rental Index Price Index

Shanghai Luxury Residential Market

SHANGHAI

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 5-8% 0-3% 3-5% 3-5%

Vacancy Rate Trend in 6 months

The third quarter saw continued rental growth of the Shanghai prime office market, with average asking rents increasing by 3.5% q-o-q, to RMB 252.9 psm per month. Puxi and Pudong, respectively, registered quarterly rental growth of 3.2% and 3.8%.

New supply this quarter totalled 166,700 sm, down significantly from the peak of the previous quarter. Of all the four new projects delivered, Eco City 1788 Nanjing Road West has been attracting a lot of attention in the market. The Grade A office building is located at the west end of Nanjing Road West, and had over 70% of its 68,000-sm space pre-leased upon delivery, demonstrating continuously strong demand for high-quality space in the traditional CBDs of the city. The quarterly net absorption reached 356,244 sm, up 16% q-o-q, more than double the same period last year. Supported by brisk take-up, the citywide vacancy rate dropped 2.3 percentage points to 7.9%, the lowest since the outbreak of the global financial crisis in mid-2008.

Multinational companies continued to lead the leasing activities, in particular for Grade A projects. Akzo Nobel committed to more than 15,000 sm in Eco City 1788 Nanjing Road West, and Owens Corning leased about 3,300 sm in Kerry Parkside.

In the next six months, approximately 420,000 sm of space is expected to enter the market, 40% lower than the past six months. The focus of new supply is gradually moving from east of Huangpu River to its west bank, which will somewhat alleviate the undersupplied condition in downtown Puxi. With continued business expansion by both foreign and domestic occupiers, the vacancy rate will consolidate at the current low range.

With no sign of the stringent monetary policies loosening in the third quarter, the residential market remained largely lukewarm. Nevertheless, increasing supply of some higher-priced projects was the major reason for a further hike in the average asking price of the Shanghai luxury residential market to RMB 59,051 psm, up 2.5% q-o-q. To avert risks of policy uncertainty in the next year, more developers joined the queue to launch projects after they accelerated efforts to achieve approvals for pre-sale. A few examples were The Bund 9, Star River and Dong Jiao Zi Yuan, all with price tags around RMB 70,000 to 100,000 psm. As for volume, transacted units still maintained the average level seen in the preceding quarter; not dampened yet, evidently.

On the leasing front, with no new supply coming on stream, rents of the luxury residential properties stayed largely flat at RMB 148.4 psm per month, a slight increase of 0.1% q-o-q.

Inde

x (Q

1 19

93 =

100

)In

dex

(Q1

2000

= 1

00)

0

50

100

150

200

250

Q1

93

Q3

93

Q1

94

Q3

94

Q1

95

Q3

95

Q1

96

Q3

96

Q1

97

Q3

97

Q1

98

Q3

98

Q1

99

Q3

99

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 16

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Prime Ground Floor Rental Index

Rental Index

Shanghai Prime Retail Market

Shanghai Logistics Market

SHANGHAIShanghai prime retail market experienced buoyant leasing activities in the quarter under review. Notable retailers continued to grab any available prime spaces. Apple opened on September 24th its largest China store in Henderson Metropolitan, after acquiring four floors, while several Japanese fashion brands also arrived in Shanghai for the first time, such as beberose’s two stores in Jiu Guang Department Store and Raffle City. Cloud Nine also welcomed Charles & Keith’s 117-sm shop on its second floor and concluded a leasing commitment with Dutch fast fashion brand WE. From the landlord side, several prime retail venues are actively repositioning their tenant mix to improve their offering. Plaza 353 on Nanjing East Road is undergoing a large-scale adjustment, inducing Swatch to open a distinctive Mega Store on the ground floor, and Zara will expand its original two-floor spaces to three floors. In addition, the first shop for Optical 88 and 96 New York from Korea will also locate there. Just one step away, Bund Plaza will accommodate the first China flagship store of Forever 21 across four floors, nearly as large as its New York flagship store. Consequently, overall vacancy rate fell further, by 0.3 percentage points to 5.5%. On the other hand, rental quotations remained relatively smooth, with ground floor rental climbing only by 0.1% q-o-q to RMB 52.5 psm per day.

In the remaining quarter of 2011, around 100,000 sm of prime space is expected to come on stream and the market maintains full confidence in new projects in core positions. It is also foreseeable that rentals may see further appreciation at the year-end as a number of contracts come up for renewal.

The Shanghai industrial property market further rallied, with the average land price increasing by 2.1% q-o-q to a record high of RMB 1,732 psm, amidst buoyant market sentiment.

Online retailers and auto industry-related companies like Yihaodian, etc., continued to represent the main demand for logistics properties, for which the average rent increased by 5% over last quarter, to RMB 30.9 psm per month. Meanwhile, a batch of online retailers, such as Alibaba and 360Buy, are expanding their warehouse footprint by self-building across China. In the manufacturing sector, municipal governments chose to co-operate with developers to provide standard manufacturing facilities to attract tenants with high-quality space. Average factory rent has risen by 2.3% q-o-q to RMB 27.1 psm per month. Average rents of business parks stayed stable at RMB 96 psm per month in the third quarter, albeit amidst increasing demand.

The strong demand is expected to continue into the fourth quarter, which bolsters the upward trend for both capital values and rentals of industrial properties. Some residential developers and manufacturers have been attracted to opportunities in the segment amidst loosening control and less competition.

Inde

x (Q

1 19

98 =

100

)In

dex

(Q1

2007

= 1

00)

0

20

40

60

80

100

120

140

Q1

98

Q3

98

Q1

99

Q3

99

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

Q1

07

Q2

07

Q3

07

Q4

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Q4

10

Q1

11

Q2

11

Q3

11

Third Quarter 2

01

1

Page 17

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Nanjing Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Nanjing Prime Retail Market

Nanjing Logistics Market

Nanjing Luxury Residential Market

NANJING

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 3-5% 0-3% 0-3% 0-3%

Vacancy Rate Trend in 6 months

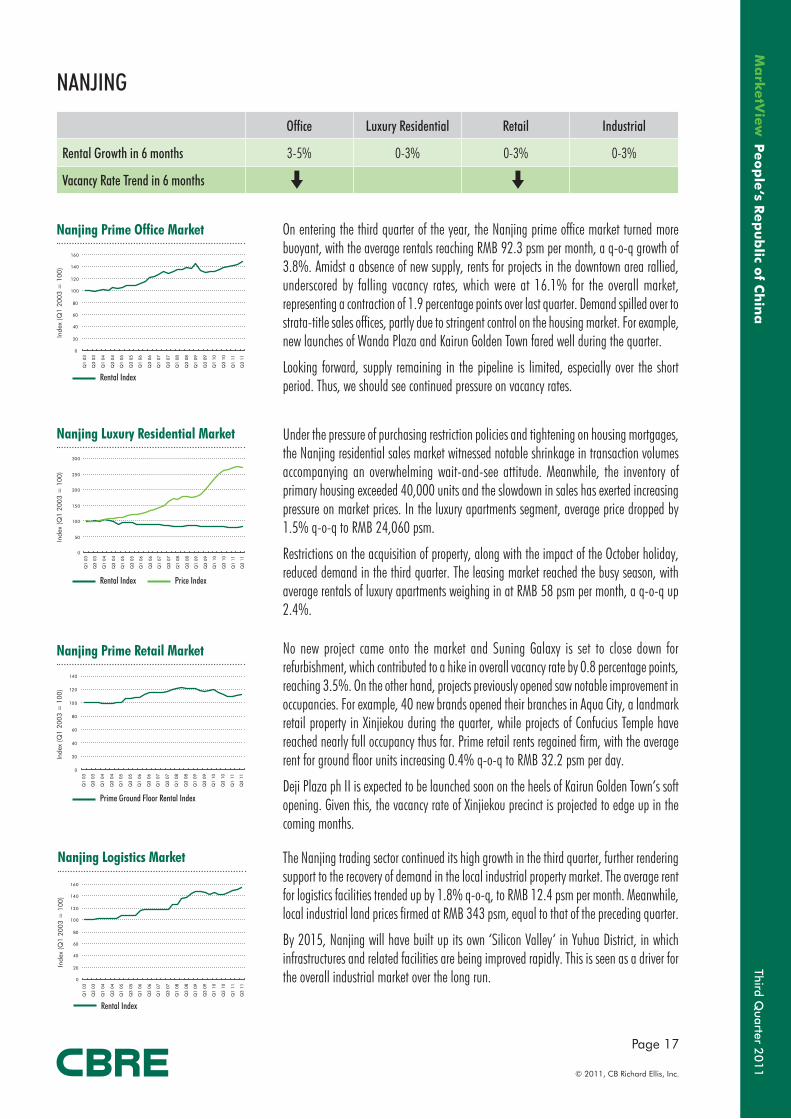

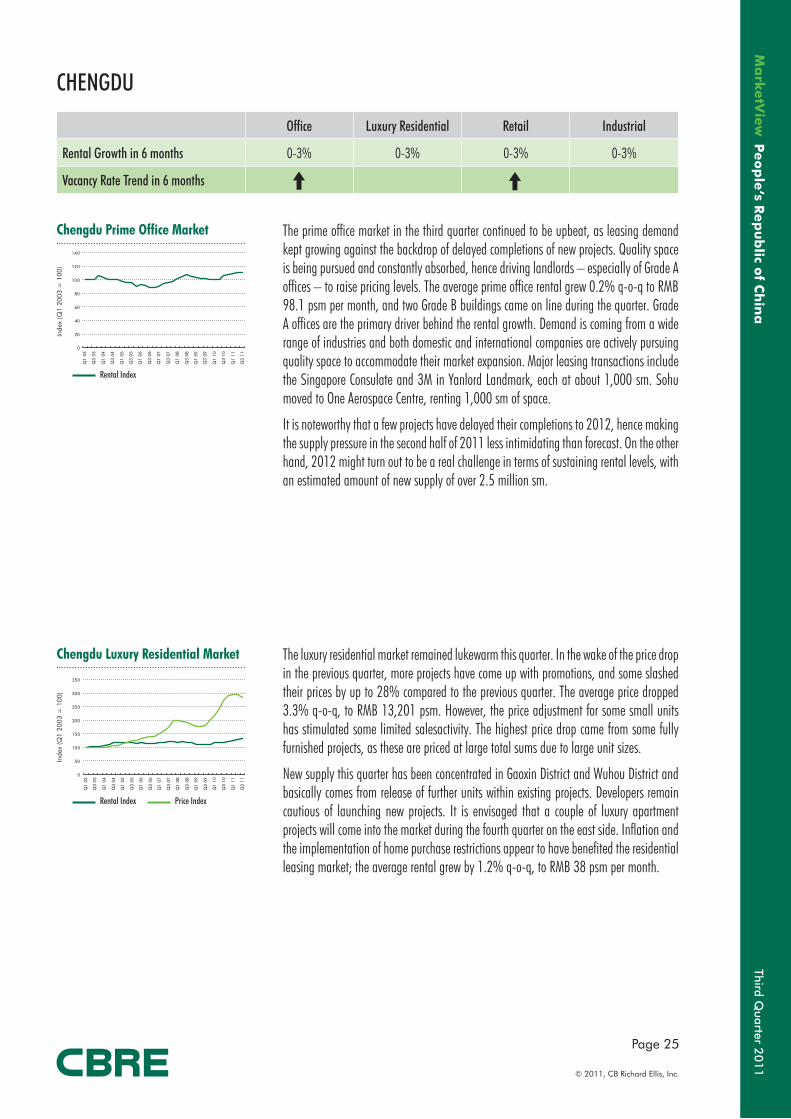

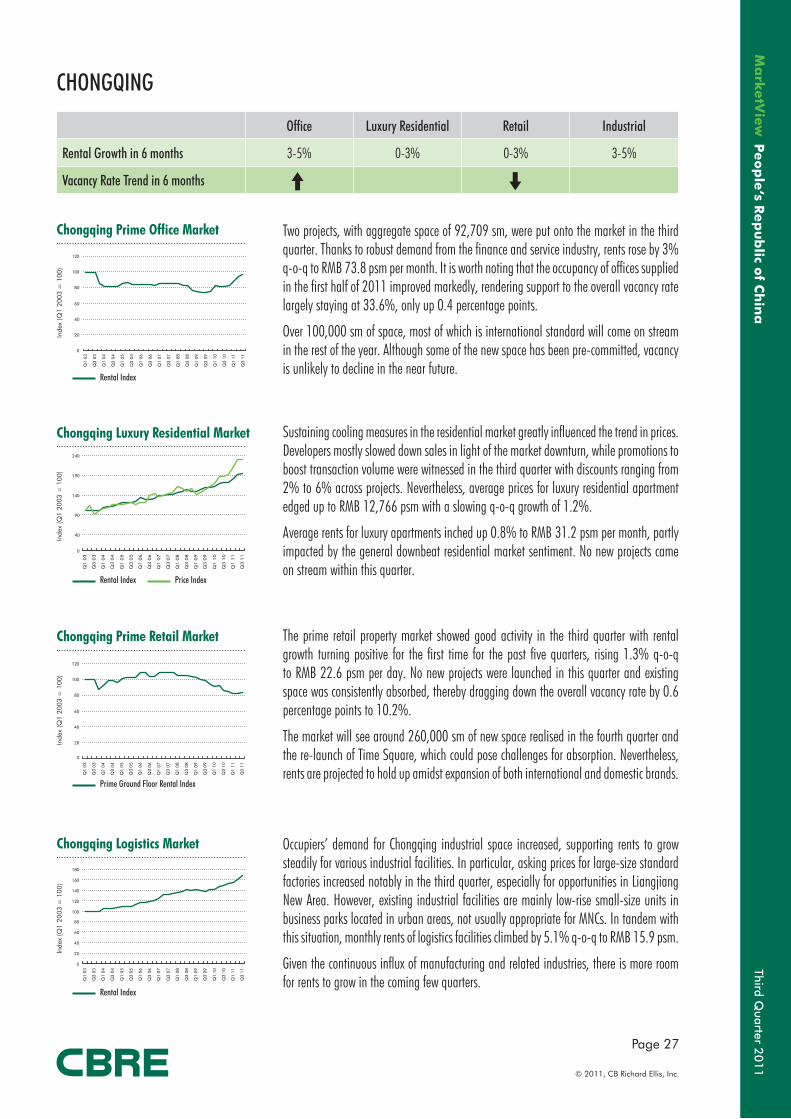

On entering the third quarter of the year, the Nanjing prime office market turned more buoyant, with the average rentals reaching RMB 92.3 psm per month, a q-o-q growth of 3.8%. Amidst a absence of new supply, rents for projects in the downtown area rallied, underscored by falling vacancy rates, which were at 16.1% for the overall market, representing a contraction of 1.9 percentage points over last quarter. Demand spilled over to strata-title sales offices, partly due to stringent control on the housing market. For example, new launches of Wanda Plaza and Kairun Golden Town fared well during the quarter.

Looking forward, supply remaining in the pipeline is limited, especially over the short period. Thus, we should see continued pressure on vacancy rates.

Under the pressure of purchasing restriction policies and tightening on housing mortgages, the Nanjing residential sales market witnessed notable shrinkage in transaction volumes accompanying an overwhelming wait-and-see attitude. Meanwhile, the inventory of primary housing exceeded 40,000 units and the slowdown in sales has exerted increasing pressure on market prices. In the luxury apartments segment, average price dropped by 1.5% q-o-q to RMB 24,060 psm.

Restrictions on the acquisition of property, along with the impact of the October holiday, reduced demand in the third quarter. The leasing market reached the busy season, with average rentals of luxury apartments weighing in at RMB 58 psm per month, a q-o-q up 2.4%.

No new project came onto the market and Suning Galaxy is set to close down for refurbishment, which contributed to a hike in overall vacancy rate by 0.8 percentage points, reaching 3.5%. On the other hand, projects previously opened saw notable improvement in occupancies. For example, 40 new brands opened their branches in Aqua City, a landmark retail property in Xinjiekou during the quarter, while projects of Confucius Temple have reached nearly full occupancy thus far. Prime retail rents regained firm, with the average rent for ground floor units increasing 0.4% q-o-q to RMB 32.2 psm per day.

Deji Plaza ph II is expected to be launched soon on the heels of Kairun Golden Town‘s soft opening. Given this, the vacancy rate of Xinjiekou precinct is projected to edge up in the coming months.

The Nanjing trading sector continued its high growth in the third quarter, further rendering support to the recovery of demand in the local industrial property market. The average rent for logistics facilities trended up by 1.8% q-o-q, to RMB 12.4 psm per month. Meanwhile, local industrial land prices firmed at RMB 343 psm, equal to that of the preceding quarter.

By 2015, Nanjing will have built up its own ‘Silicon Valley‘ in Yuhua District, in which infrastructures and related facilities are being improved rapidly. This is seen as a driver for the overall industrial market over the long run.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 18

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

Hanghzou Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Hangzhou Prime Retail Market

Hangzhou Logistics Market

Hangzhou Luxury Residential Market

HANGZHOU

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 0-3% 3-5% 3-5%

Vacancy Rate Trend in 6 months

The influx of ample new supply of up to GFA 200,000 sm in the third quarter, comprising two Grade A office projects in Qianjiang New City, posed a degree of pressure onto the Hangzhou prime office market. However, the overall vacancy rate was contained, with only 1.1 percentage points increase over last quarter, closing at 17.3% by the quarter. Meanwhile, rentals rose by 1.5% q-o-q, to RMB 114 psm per month, underpinned by bullish market sentiment. The pressure from increasing supply in Qianjiang New City is not likely to ease in the fourth quarter of the year, given that an aggregate of around 400,000 sm of new space will be put onto the market before the year’s end. However, the outlook for projects across the traditional areas is still positive.

The combined effect of curbing measures from both central and municipal governments started to impact the Hangzhou housing market more evidently. In the third quarter, the average sales price of luxury apartments lost its upward momentum, falling by 0.8% over the last quarter, to RMB 39,211 psm. Yet with their values supported by limited supply, the prices of luxury residential projects are unlikely to plummet.

In the quarter, the luxury residential leasing sector continued to show growth, with rentals rising by 0.8% q-o-q to RMB 80.1 psm per month.

During the third quarter of the year, there was a limited amount of prime retail space completed in Qianjiang New City ,around GFA 50,000 sm, , while the market maintained its upward trajectory, albeit at a slower pace. Average rentals for ground floor areas rose by 0.8% q-o-q, to RMB 29.3 psm per day. The vacancy rate of the overall market hovered at a low base, slightly up by 0.6 percentage points from the end of first half of the year, to 1.4%.

Several projects in the pipeline have been put off until next year, with no sign of a change in the upward momentum for rental levels.

Perhaps influenced by the operation of the high-speed railway network, Hangzhou has experienced a closer connection with the Shanghai economics area recently, which has boosted the demand for industrial facilities. Industrial land prices continued their growth with a 4.1% q-o-q gain in the third quarter, hitting a new high of RMB 402.3 psm. Rapid development of industries related to domestic consumption, such as e-commerce, increased demand for warehouses. The average rental of logistics facilities was boosted to RMB 16.2 psm per month, up by 1.9% q-o-q.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

350

400

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 19

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Ningbo Prime Office Market

Rental Index

Rental Index Price Index

Prime Ground Floor Rental Index

Rental Index

Ningbo Prime Retail Market

Ningbo Logistics Market

Ningbo Luxury Residential Market

NINGBO

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 0-3% 0-3% 0-3% 3-5%

Vacancy Rate Trend in 6 months

The third quarter of 2011 saw a spike of prime office supply in Ningbo, with 53,154 sm of office space delivered within the period under review. In spite of this market rentals witnessed a increase during the quarter, up 5% q-o-q to RMB 72.1 psm per month. Occupancy rates across the market continued to see improvement, supported by the solid demand from private enterprises. The overall vacancy rate was recorded at 19.1%, an increase of 0.9 percentage points over last quarter.

Looking to the fourth quarter, the adequate supply pipeline, of around 100,000 sm for the fourth quarter of 2011, especially in Yinzhou South New City and East New City, will inevitably elevate the vacancy rates in these areas, which should also rein in further growth of rents.

Due to the ongoing controls over the market, demand for luxury housing in the Ningbo sales market fell to a level equal to that of the previous trough in 2008. With so many new launches, some developers reacted to the slack market condition by reducing asking prices. As such, the average sales price of luxury apartments reduced by 1.6% q-o-q, to RMB 20,922 psm. The performance of projects in central area, however, outpaced that of other emerging areas.

During the same period, average rents in the luxury residential leasing market continued to grow by 1% q-o-q, to RMB 56.6 psm per month.

As no new projects were completed in this quarter, the Ningbo prime retail market remained tight, with a vacancy rate at 1% as at the end of September, a slight drop of 0.5 percentage points. Ningbo’s strong consumption power has continued to draw attention from both overseas and domestic retailers. A few brands, including GOME, KFC, Nike, and luxury brands such as Breguet and Chaumet, all secured new stores recently in the Ningbo market. Rentals were thus underscored to RMB 24.1 psm per day for ground floor space on average, up 1.1% q-o-q. It is worth noting that projects in emerging areas such as Jiangbei still suffered from a lack of critical mass, and experienced slack sales as a result.

New supply in prime locations is expected to remain limited and the supply-demand imbalance in the market will not be alleviated in the near future.

In the third quarter of 2011, the Ningbo industrial market fared well, supported by robust demand from the rapidly expanding manufacturing industry, especially from small and medium enterprises across Zhejiang. Recently, increasing new set-ups and expansion of high-tech enterprises, especially for R&D use and demand from e-commerce, have bolstered the growth in demand for industrial facilities. Against this background, industrial land prices increased by 3.3% q-o-q, to RMB 531 psm during the period under review, while rentals for logistics facilities edged up by 2.9% q-o-q, to RMB 15 psm per month. Under the government’s plan for developing seven logistics parks in Ningbo and aiming to turn the city into a logistics hub in the region, there should be upside for rentals of logistics properties over the medium to long term.

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

Inde

x (Q

1 20

03 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

160

180

200

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

350

400

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

20

40

60

80

100

120

140

160

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 20

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub

lic of C

hin

a

GUANGZHOU SHENZHEN

SOUTH CHINAUnderpinned by strong demand, the prime property sectors in Guangzhou and Shenzhen continued to rally over the third quarter of the year. Rental growth for office markets accelerated across these two cities, pushed by demand from domestic enterprises and new highs of net absorption. Prime retail rents in Shenzhen increased 5.8% for ground floor space, thanks to a continuous drop in vacancy rate as a consequence of the lack of supply. In Guangzhou, vacancy rates also hovered below 8%, despite the influx of supply seen in the past consecutive four quarters.

Luxury residential sales prices firmed up despite slack sales volume, due to the stringent control over the housing market. Developers maintained caution and were reluctant to launch new projects onto the market, which led to further reductions in transacted volumes. In Shenzhen, there were tentative signs that some developers have increased supply of units onto the market at the end of the quarter to meet pent-up demand; the market’s response is yet to be seen. Prime logistics premises were sought after by enterprises from various manufacturing sectors, with rentals being further driven up.

RENTAL

Guangzhou Shenzhen

Office

Luxury Residential

Retail

Industrial

Third Quarter 2

01

1

Page 21

© 2011, CB Richard Ellis, Inc.

Peo

ple

‘s Rep

ub

lic of C

hin

a

Guangzhou Prime Office Market

Rental Index Price Index

Rental Index Price Index

Guangzhou Luxury Residential Market

GUANGZHOU

Office Luxury Residential Retail Industrial

Rental Growth in 6 months 3-5% 0-3% -3-0% 0-3%

Vacancy Rate Trend in 6 months

Despite strong supply coming onto the market during the quarter, robust demand outstripping supply continued to fuel rental growth in the market, which sped up in the recent half-year. By the end of the quarter, the average rent soared 7.8% q-o-q to RMB 124.4 psm per month. In particular, Grade A offices continued to outperform Grade B ones, with a 9.3% q-o-q gain in average rentals, amounting to RMB 155.3 psm per month. Pearl River New City (PRNC) stood out in rental terms among all areas, at RMB 157.7 psm per month.

Four Grade A offices with 298,500 sm of space, were completed this quarter, one in PRNC and the rest in Tianhe Sports Centre Area. Two towers of TaiKoo Hui were completed in the quarter, one fully occupied by HSBC and the ratio of pre-commitment for the other amounting to 50%. The robust net absorption was also evidenced by the fact that 23 of the total of 39 floors of another new building, Evergrande Centre in PRNC, were selected for self-use as the headquarters of the developer. Against this background, the overall vacancy rate was drawn down 0.4 of a percentage point, to 12%.

Domestic tenants remained as a major force underpinning the segment. For example, Agile leased around 15,000 sm in Guangzhou International Finance Centre, while Southern Power Grid expanded by 1,900 sm in Poly Centre in PRNC. TaiKoo Hui continued to be favoured by MNCs, as Rider Levette Bucknall recently took 1,000 sm in this newly completed scheme.

Under ongoing regulatory control, the Guangzhou luxury residential sales market was largely stable in the third quarter, with the average price of luxury apartment recording a slight growth of 0.9% q-o-q to RMB 29,865 psm. High-end housing sales remained subdued, largely due to the scarcity of new projects. During the quarter, Star River Shenghui in Panyu District was the only luxury apartment scheme newly launched for pre-sale, with a price tag approximately RMB 25,000 psm.

On the leasing front, rents for luxury apartments registered mild growth of 1% q-o-q, to RMB 79.5 psm per month. The demand from expatriate families reduced due to a drop in family numbers, impacting the performance of large-size apartment units and villas as well. This led to a scale-back of average rents for villas by 3.7% q-o-q. Looking ahead, new residential units from the Liede Redevelopment Scheme and Kingold luxury scheme in Pearl River New City, as well as R&F Tangning Garden and CITIC Xiguanhai in Liwan District, the former city downtown, are expected to be launched in the fourth quarter.

Inde

x (Q

1 20

00 =

100

)In

dex

(Q1

2003

= 1

00)

0

20

40

60

80

100

120

140

160

Q1

00

Q3

00

Q1

01

Q3

01

Q1

02

Q3

02

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

0

50

100

150

200

250

300

350

Q1

03

Q3

03

Q1

04

Q3

04

Q1

05

Q3

05

Q1

06

Q3

06

Q1

07

Q3

07

Q1

08

Q3

08

Q1

09

Q3

09

Q1

10

Q3

10

Q1

11

Q3

11

Third Quarter 2

01

1

Page 22

© 2011, CB Richard Ellis, Inc.

Peo

ple

’s Rep

ub