Embed Size (px)

Citation preview

PAYMENT BACKLOGS - PROBLEM OF THE MANAGEMENT IN

THE POLISH SMALL AND MEDIUM-SIZED ENTERPRISES

PhD Elżbieta Wysłocka

Częstochowa University of Technology Management Faculty

Abstract

In the recent years payment backlogs have become more and more serious obstacle for the

development of the Polish entrepreneurship. It should be also noted that the lack of control

over this phenomenon has a negative impact not only on the activities of companies, with

emphasis on small entities, but also on the economic circulation as a whole. Therefore, it

becomes extremely important to monitor systematically the sizes of the payment backlogs as

well as their changes over time, and to take steps to reduce them. Currently in Poland the

companies are waiting for the money earned by them for almost half a year which results in

the fact that they themselves have problems with payments.

The literature on the emergence of payment backlogs and settlement of trade credit is getting

richer but there are still some aspects of the problem that have not been investigated yet. This

study examines the determinants of granting the trade credit as well as the reasons for which

these credits were not regulated in 2011-2012 in Poland. In addition, the study analyzes the

impact of the above mentioned on the financial condition of small and medium-sized

enterprises operating in Poland.

This paper discusses also the main theoretical and empirical works on the trade credit and the

payment backlogs. Based on the data presented in the quarterly reports of BIG (Credit

bureau), a number of entrepreneurs who have a negative opinion of the phenomenon of

delayed payments and changes in the Index of the Safety of the Economic Activity are

examined. The necessary steps that need to be taken in order to improve the situation,

especially of the small and medium-sized Polish enterprises, are also discussed.

1. Introduction

To discuss issues related to payment backlogs the concept of trade credit which underlies

the phenomenon of backlog must also be mentioned. Trade credit is without a doubt one of

the most important factors driving the economy for both trade and production. It is

impossible to find an industry or kind of business activity, which does not use trade credit.

Trade credit provides the opportunity to purchase necessary products at payment deferred to a

later date, agreed with supplier. On the one hand, selling on credit is one of tools to increase

sales and profit for vendors. It allows to attract customers who do not have adequate funds for

cash purchases. For suppliers, deferment of payment increases the probability of maintaining

customers and hedges cash flow in future. In addition, suppliers can reduce transaction costs

associated with implementation of any trade (Rodríguez-Rodríguez, 2008).

On the other hand, trade credit is used by companies that have too little equity, and have

difficulties in accessing bank credit. Then trade credit, also known as commercial credit, is

for them a source of raising funds to finance current operations. Suppliers often extend the

term of a loan in comparison with offered by other suppliers, in order to attract new

customers. Participation in trade credit in financing of Polish enterprises is significantly

higher than the share of bank credit. In small and medium-sized enterprises represents the

primary source of working capital financing. However, there is no general theory of trade

credit, and it is difficult to explain the reasons why companies decide to accept such trade

policy.

Granting trade credit can be confirmed by agreement between parties, the general terms

of sale, or may arise only from the due date specified on an invoice. Therefore does not

require any particular legal form. It is a preferred alternative to loans granted by credit

institutions. Loans granted by banks are often subject to a complicated procedure that

requires the borrower to meet several conditions. Trade credit eliminates the path of bank

lending and allows trade between partners. It is competitive to bank loans also because of

costs. Referred to as the cheapest loan, as it means that the buyer has opportunity to sell

goods even before the due date, and thus does not need to engage within that period own

funds or working capital loans. It may therefore for some time exploits someone else's

resources, or create a reserve fund to preserve the payment terms, and financial liquidity.

Recognition as a cheapest loan, however, is dependent on the use jointly a cash discount

(rebate). Used without the support of such instrument can become not very cheap, but also

not very complicated, and therefore attractive and quick to obtain.

Note, however, that seller is the party that bears a high risk of trade credit agreement.

Therefore, in practice, such a loan should be granted to companies in which you have full

confidence, having a base for long-term cooperation. Trade credit is designed for customers,

for which there is no doubt that it will complete its commitments and settle payment within a

specified period (Biadacz, 2012). Customers without verified credibility should be treated

with care - at the beginning of cooperation cannot count on receiving deferred payments, and

only after some time, such mechanism can be applied (Czekaj and Dresler, 1995, Rubik,

2011). There are opportunities for additional protection of a deferred payment, which can

overcome the fear of misconduct in the repayment of loan. The seller may require from the

buyer an adequate protection in the form of charged penalty interest on arrears included in

contract, blank promissory note, guarantee, pledge or bank guarantee. It must be remembered

that supply of trade credit, especially among small and medium-sized enterprises (SMEs), is

the result of both customer needs but also opportunities to build strategic advantage. In times

of economic slowdown and financial difficulties of many enterprises, the demand for trade

credit can be increased, leading to a further increase in risk. (Paul and Boden, 2011).

Trade credit protection are measures taken to ensure the repayment of deferred payment.

Untimely repayment of liabilities is very common. Overdue payments are a major problem in

the economy, and effective recovery is often necessary to maintain the existence on the

market.

2. Review of the literature

Trade credit is widely discussed in the literature, although still many issues related to this

topic need to be clarified. Initially, studies were conducted on the effect of government's

monetary policy and share of trade credit instead of a conventional credit channel in working

capital of enterprises (Meltzer, 1960, Nadiri, 1969). Brechling and Lipsey (1963) found that

the value of trade credit generally increases during periods of tightened monetary policy.

A similar approach was represented in more recent works (Ramey, 1992; Norrbin and

Reffett, 1995; Nilsen, 2002).

There are several ways proposed to explain motives of granting trade credit. One is the

financial motive. Emery (1984), Mian and Smith (1992), Schwartz (1974) argue that firms

that are able to obtain funds at low cost offer trade credit to companies exposed to higher

financing costs. Emery (1984) sees trade credit as a short, more profitable investment than

securities. But there is no empirical evidence on the impact of granting credit to profitability

of companies. Trade credit has an impact on the level of investment in current assets and

thereby have a significant impact on profitability and liquidity of a company. Managers can

improve profitability through increased investment in receivables (Martínez-Sola et al.,

Forthcoming).

One of the major advantages of trade credit is to reduce the transaction costs that are

incurred in an immediate payment on delivery of goods (Nadiri, 1969). Emery (1987)

develops a positive theory of trade credit from its use as a response to financial deterministic

fluctuations in demand. This shows that the reduction of cost and not revenue growth is a

source of benefits for both the buyer and seller.

Alphonse at. al. (2006) states that there are arguments for considering a bank loan and

trade credit as financial resources called in the literature “substitutable”.

According to Schwartz and Whitcomb (1978, 1979), Emery (1987), Freixas, (1993),

Biais and Gollier (1997), Jain (2001) and others notice that trade credit is popular because

suppliers have an information advantage over banks. In the course of business, the supplier

will receive information about the borrower which other lenders can obtain at a cost. This is

especially true when clients-borrowers are small, young and not very transparent companies

(Beger and Udell, 1995; Wilner, 2000). So in future, information asymmetry can lead to

greater use of trade credit (Stiglitz and Weiss, 1981). In many studies it is emphasized that

despite the prevalence of bank credit, the relationship between banks and enterprises are labor

intensive (Belletante and Levratto, 1995). Those companies that have alternative sources of

funding are less prone to search for debt financing (the substitution effect) (Garcia-Teruel and

Martinez-Solano, 2010).

A significant trend of theoretical studies presented in the literature concerns the financial

difficulties associated with repayment of trade credit as well as complications arising in the

event of liquidation of the company (Frank and Maksimovic, 1998; Wilner, 2000; Cuñat,

2002). This phenomenon is particularly intensified during the financial crisis, when many

companies began having trouble in maintaining liquidity. This causes gridlock which tends to

begin with a customer or buyer refusing to pay for service or product to its contractor (service

provider) or seller of goods. The resulting debt, if it persists for a long time (especially if the

contractor or vendor is a small company), cause difficulties in maintaining liquidity to pay

employees of a contractor (seller) and often problems with survival. This results sometimes in

delays or, in extreme cases, suspending payment of amounts due by a contractor (seller) to

their contractors and in consequence in a transfer of part of original commitment to another

counterparty. This process can continue to the next and even the next market players (Paul

and Boden, 2008, Wilson, 2008).

The reason for occurrence of original debt can be both financial problems that are not

attributable to the first recipient of services or commodities (e.g. due to unforeseen

misfortunes), and planned or unlawful actions. The injured contractor (vendor) provides in

fact a loan until the settlement, however it is often the case, that it does not charge any

interest, in fear of permanently losing the client, especially if it is associated with more stable

relationship (e.g. long-term services or delivery of goods). It also happens so that the payer

includes statutory interest of such a “credit” in the cost of its operations.

Payment delays occur especially often in periods of economic stagnation, or under

conditions of high inflation, when extension of payment period may work in favor of debtor

(and a loss for creditor). It is exactly during the recession when “small businesses are most

affected by the credit crunch”, and “there is a clear link between the delay and the rate of

insolvency and bankruptcy” (Wilson, 2008). There is also a link between payment delays and

the size of a company (Peel et al., 2000). Big companies are the worst payers, and small do

not have power to enforce their claims. Also results of Peel et al. (2000) research show the

relation between problems faced by small businesses with the size of company and its life

cycle. The study show that although the problem of maintaining liquidity refers to any

company, regardless of its size, it is the smallest companies which should particularly care

about it most. One should keep in mind that small businesses are not miniature large

companies or their reduced versions, but differ from large firms in many ways, two of which

are particularly important from the point of view of liquidity management. First of all the

owner of business combines two functions - ownership and management. Second, small firms

compared to large firms have limited resources, such as finance and management skills.

Therefore, the requirements of small business management differ from those which relate to

large companies, management tools used by large companies are not always effective in the

context of small businesses. (Ekanem, 2010).

Very often, small and medium-sized enterprises believe that liquidity management

problem does not affect them, and that this issue is valid only in large corporations. This kind

of thinking is fundamentally flawed. It is exactly SME sector, with difficult access to capital,

which should control the stream of money flowing in and out the company in a particularly

balanced way. In practice, often it turns out that company is profitable, but having liquidity

problems, it must close down. In the pessimistic scenario, it will be a bankruptcy. Research

has shown that poor management of credit is a major problem for small businesses which feel

powerless against late payment by debtors (Peel at al., 2000).

Efficient and effective liquidity management is essential if a company wants to survive

and make a profit, and this issue becomes particularly important in the case of small firms.

Every company in the market must engage in sale in order to operate. Previously, however,

has to buy raw materials, materials, goods, etc. For this purpose, it should settle existing

obligation. For this needs money. The source of cash are primarily: payments from

customers, sales, debt coming from outside, or payments from owners, grants and other

benefits. If company obtains cash, it can regulate commitments made in past. This will

facilitate the acquisition of new inventory that will be used to achieve new sales. As one can

see, it is a closed circle, which creates a profit for a company, and in which each step is listed

as liquidity management. In this case, the process is common to both small and large

companies. The only difference is a scale.

If your business is beginning to have problems with liquidity, it means that you need to

take serious corrective action. Why? Studies in literature suggest that such problems can lead

to insolvency and, consequently, into bankruptcy. Business practice and experience explain it

much easier and more operationally.

When a company has no cash flow, it cannot regulate obligations already incurred. A

supplier who does not receive payment for the first time, will probably trust his partner in

trade and execute next order. If, however, this situation repeats itself, the first move will be to

close the customer credit limit. Then, the recipient will have to make purchases in cash,

which he lacks. And if he fall behind with payments to a greater number of suppliers, the

only solution may be to file for a bankruptcy. This will allow existing creditors to recover, at

least part of amounts due. In cases where the customer has established collateral on its assets

it may lose it.

Problems with suspension of supplies to experienced companies and “well positioned on

the market” can be overcome. They will find another supplier. And it is likely that creditors

will not file for bankruptcy of their business partner, hoping that it will soon pay off its debt.

Moreover, in a highly competitive market, there are always new suppliers interested in

working with someone who is known to have payment problems with other companies.

However, new suppliers can be as unreliable as the recipient and not implement contracts on

time, not guarantee quality of goods, materials or services. At this point, there is another

negative factor for the lack of liquidity. McMahon and Stanger (1995) argue that the

difference in liquidity between large and small companies results from the fact that the

shortage of working capital are a common problem for small businesses. This may be a result

of limited access to capital markets for small business and / or due to a nature of the business.

Most often in case of suppliers of poor quality, customers suffering from lack of liquidity

will not be satisfied with the cooperation and terminate contract. This in turn will reduce the

supplier’s revenues in the context of lack of timely payment. But it's worth to see how this

process affects the relationships with the customers of ‘business in trouble’. If you do not

receive deliveries of new partners on time, it fails to comply with orders to their customers,

and even lose the chance of widening the market. Deloof (2003) argues that trade credit is a

cheap source of financing for customers, on the other hand money providers are frozen in

working capital. Deloof (2003) also points out that although the delay in payments to vendors

can be a cheap and flexible source of financing for consumers, it is the delay in payment of

invoices which can be very expensive. Therefore, effective management of these components

is essential.

The consequence of a shortage of liquidity is a chain of interrelated phenomena which

occur but are sometimes unrecognized by companies. But not only the shortage of liquidity is

problem. If company have excess liquid funds, the opportunity costs is incurred. It could

invest it and earn interest income. Therefore liquidity management takes the form of a cash

management and credit management. Although the most important aspect of managing cash

flow is avoiding increased liquidity problems, the management of credit policy, which applies

not only to grant and borrow loans to customers and suppliers, but also involves the

assessment of individual customers credit periods allowed and steps taken to ensure the

payments are received on time are also important (Poutziouris et al., 1999). Ekanem, (2010)

argues that effective management of working capital is significant in terms of both liquidity

and profitability. Poor management of working capital means that funds are tied up

unnecessarily in useless assets and thereby reduce liquidity, and limit ability to invest in

productive assets.

3. Financial crisis and problem with liquidity in corporates

The crisis, recession, economic downturn – these are words that have often appeared in

the press, radio and television for some time. Does the current economic situation impact the

financial position of firms? Time of economic downturn is a period when the issue of

liquidity becomes particularly important. Even a successful company can have difficulties if

contractors are late with payments, and margins are falling.

Survey results published by Roland Berger Strategy Consultants1 on global trends in

restructuring show how strongly the economic crisis affects companies operating in different

sectors and different geographic regions. In the study 14 managers from different sectors of

economy have comment on how to improve financial situation. Research reveals that during

the crisis, 40% of companies had serious liquidity problems, and to maintain it companies

had to fight mainly using the ad hoc operational solutions. Impact of the crisis on the

financial condition of companies based on their financial flexibility was analyzed by Bancel,

Mittoo, (2011), and they found that companies with large financial flexibility were more

resistant to effects of crisis. They believe that managers benefit from a number of sources, in

addition to a small leverage to increase financial flexibility. At the same time it was noted

that companies were primarily focused on cost reductions. During the crisis, tested companies

decreased average personnel costs by 9%.

Financial flexibility represents the company's ability to respond effectively to unexpected

disturbances of their cash flow or investment opportunities. Managers around the world have

pointed achieving financial flexibility as the primary purpose of their decisions on capital

structure (Graham and Harvey, 2001, Bancel and Mittoo, 2004). In times of economic

slowdown, the effective management of working capital becomes especially important for

small businesses. “The credit crunch” ongoing since 2008 has been defined as a sudden

decrease in overall availability of loans and borrowings, or a sudden increase in cost of

obtaining loans from banks (Ding et al., 2008). As a result, owner-managers have more

difficulties in raising funds for working capital due to higher borrowing costs that are the

result of falling property values and decrease in owner-managers ability to provide the

necessary collateral, and perceptions that banks are afraid to even more risk than was

previously (Ekanem, 2010). Graham and Harvey (2001) report that U.S. managers have

identified the need to maintain financial flexibility as a main driving force behind the

company's debt policy, and Bancel and Mittoo (2004) confirmed this finding in the study of

European managers in 16 countries.

Research and interviews conducted by Bancel and Mittoo (2011) among French financial

executives in 2009 on financial flexibility and the impact of global financial crisis (GFC)

confirms strong or very strong impact of GFC on the liquidity, the fall in demand and cost

reduction as main effects of crisis, and the reluctance of banks to lend in times of crisis.

According to the Report of Roland Berger Strategy Consultants (2010), structural

solutions and external financing were much less important than cost reduction and

operational activities undertaken to protect liquidity in times of crisis. Only 34% of

companies surveyed took new loans. In the USA (36%) and China (43%) observed the

highest number of companies benefiting from government support programs. As the biggest

problems associated with financing are reduced levels of limits in trade credit insurance and

worse credit conditions. Companies also complained about the refusal for new lines of credit,

particularly in Central and Eastern Europe (28%) and the Middle East (31%). The least

problems with obtaining financing affected companies from China and Japan. About 50% of

companies affected by the reduction in trade credit insurance and credit lines were in a

critical situation. For about half of surveyed companies, credit conditions deteriorated during

the crisis. The areas in which credit conditions have worsened are the interest rate (56%),

financial requirements (54%), information requirements (51%), security requirements (46%).

Higher interest rates are especially important for companies in the U.S., Western Europe and

1 Available on webpage

http://www.rolandberger.pl/media/pdf/Roland_Berger__International_Restructuring_Study_20100619.pdf

Central Eastern Europe. The least visible deterioration in credit conditions were in Japan. The

research of Roland Berger Strategy Consultants (2010) show that the crisis should led to four

main conclusions. First, a need to create greater liquidity reserves and continuously optimize

working capital. Second, in a time of crisis equity of many companies became strained by

declines in turnover. To avoid this in future companies need to reduce leverage and increase

equity. They can also “slim down” the balance sheet, by using such measures as alternative

forms of investment (factoring) and selling less important assets. Third, firms have to prepare

a flexible cost structure adapted to possible declines in sales volume. Additionally, they

should make early warning systems. And fourth, even during the crisis, companies can’t

forget about building a base for better times. Road to development by excessive cutting costs

should be avoided. In parallel with necessary reduction, strategies for future growth ought to

be planned. The crisis is the best time to explore and exploit the weaknesses of competitors.

4. Payment backlogs in Poland

Payment delays have become in recent years more and more serious obstacle to

development of Polish entrepreneurship. It should be noted that the lack of control over this

phenomenon has a negative impact not only on activities of individual companies, but also

throughout the course of trade. Therefore, it becomes crucial to systematically monitor the

size of payment gridlock and their changes over time. This task has been performed for

number of years by InfoMonitor Economic Information Office, issuing a quarterly report on

the security business in Poland (BIG Report). The data come from the BIG Reports of

sentiment among Polish entrepreneurs. In March 2013 the 21 edition of the report was

published, and for the fifth time it included the results of enlarged group of companies of six

industries: financial services providers, mass services providers, construction industry,

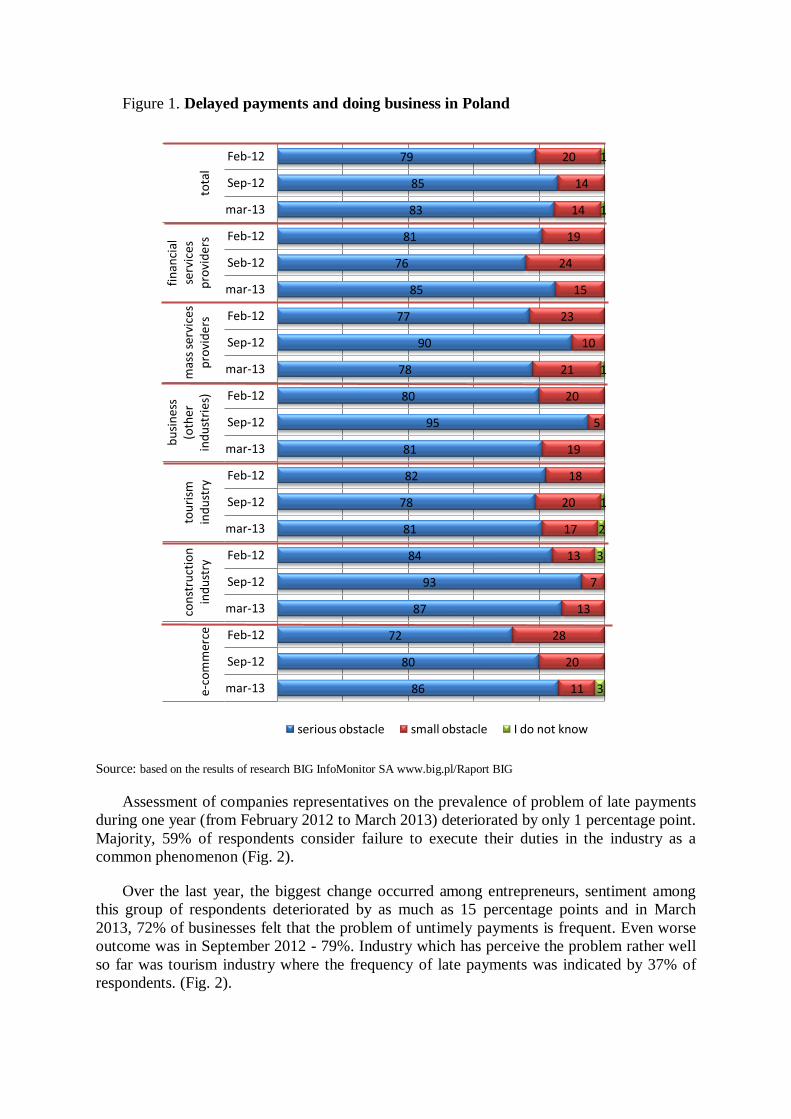

tourism industry, e-commerce and businesses (other industries). Figure 1 shows the effect of

untimely payments to conduct business in Poland, according to the BIG report. Compared to

the study of February 2012, the companies sentiment have deteriorated, but much worse

mood prevailed in September 2012. Currently 83% of all respondents believe that the

payment of invoices not in accordance with terms of payment is a major obstacle to doing

business. It is about 4 percentage points worse result than in February 2012. In all sectors, the

problem of delayed payments is considered to be a strong impediment to doing business.

Mass service representatives have experienced the problem to a least degree, although 78% of

respondents in this group believe that it is a serious barrier. Payment delays, however, are the

biggest obstacle to doing business for representatives of construction industry. As much as

87% of its representatives indicate it.

Figure 1. Delayed payments and doing business in Poland

Source: based on the results of research BIG InfoMonitor SA www.big.pl/Raport BIG

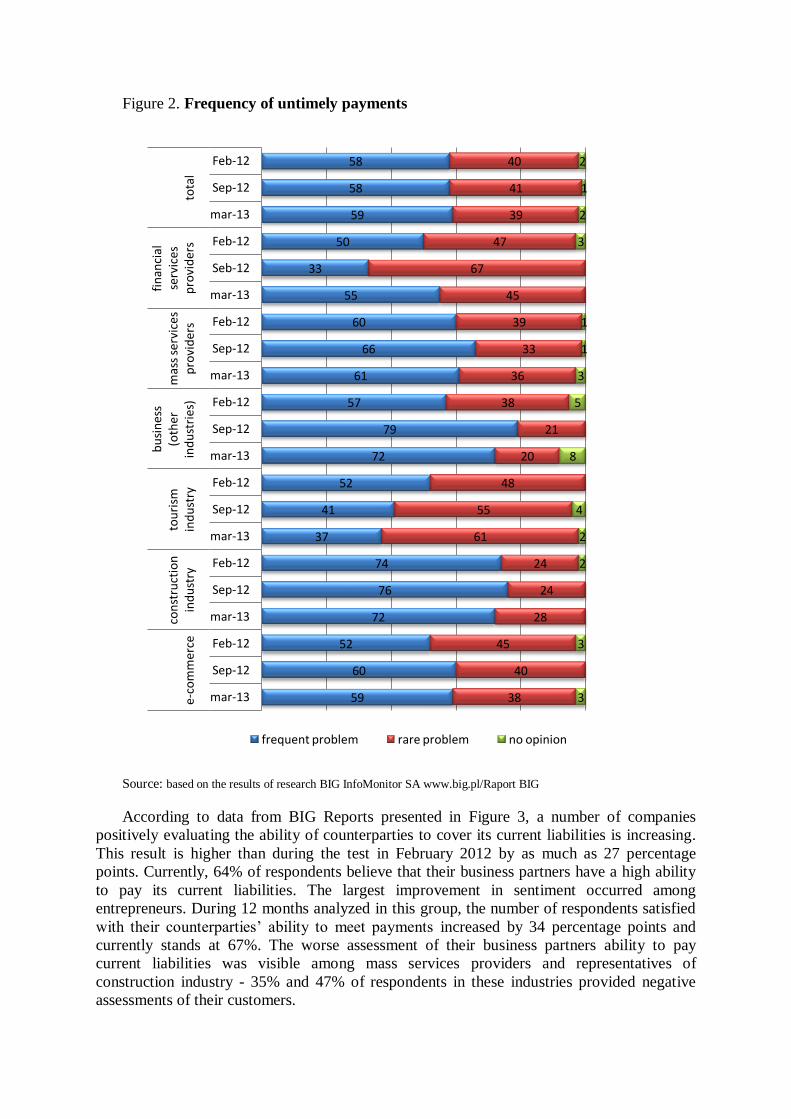

Assessment of companies representatives on the prevalence of problem of late payments

during one year (from February 2012 to March 2013) deteriorated by only 1 percentage point.

Majority, 59% of respondents consider failure to execute their duties in the industry as a

common phenomenon (Fig. 2).

Over the last year, the biggest change occurred among entrepreneurs, sentiment among

this group of respondents deteriorated by as much as 15 percentage points and in March

2013, 72% of businesses felt that the problem of untimely payments is frequent. Even worse

outcome was in September 2012 - 79%. Industry which has perceive the problem rather well

so far was tourism industry where the frequency of late payments was indicated by 37% of

respondents. (Fig. 2).

79

85

83

81

76

85

77

90

78

80

95

81

82

78

81

84

93

87

72

80

86

20

14

14

19

24

15

23

10

21

20

5

19

18

20

17

13

7

13

28

20

11

1

1

1

1

2

3

3

Feb-12

Sep-12

mar-13

Feb-12

Seb-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

tota

l

fin

anci

al

serv

ices

p

rovi

der

s m

ass

serv

ices

p

rovi

der

s

bu

sin

ess

(oth

er

ind

ust

ries

) to

uri

sm

ind

ust

ry

con

stru

ctio

n

ind

ust

ry

e-c

om

mer

ce

serious obstacle small obstacle I do not know

Figure 2. Frequency of untimely payments

Source: based on the results of research BIG InfoMonitor SA www.big.pl/Raport BIG

According to data from BIG Reports presented in Figure 3, a number of companies

positively evaluating the ability of counterparties to cover its current liabilities is increasing.

This result is higher than during the test in February 2012 by as much as 27 percentage

points. Currently, 64% of respondents believe that their business partners have a high ability

to pay its current liabilities. The largest improvement in sentiment occurred among

entrepreneurs. During 12 months analyzed in this group, the number of respondents satisfied

with their counterparties’ ability to meet payments increased by 34 percentage points and

currently stands at 67%. The worse assessment of their business partners ability to pay

current liabilities was visible among mass services providers and representatives of

construction industry - 35% and 47% of respondents in these industries provided negative

assessments of their customers.

58

58

59

50

33

55

60

66

61

57

79

72

52

41

37

74

76

72

52

60

59

40

41

39

47

67

45

39

33

36

38

21

20

48

55

61

24

24

28

45

40

38

2

1

2

3

1

1

3

5

8

4

2

2

3

3

Feb-12

Sep-12

mar-13

Feb-12

Seb-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

tota

l

fin

anci

al

serv

ices

p

rovi

der

s m

ass

serv

ices

p

rovi

der

s

bu

sin

ess

(oth

er

ind

ust

ries

) to

uri

sm

ind

ust

ry

con

stru

ctio

n

ind

ust

ry

e-co

mm

erce

frequent problem rare problem no opinion

Figure 3. Business partners ability to meet current liabilities

Source: based on the results of research BIG InfoMonitor SA www.big.pl/Raport BIG

In March 2013 the share of firms that receive more than 75% of payment on time was

40% (Figure 4). In relation to the study in September the group of companies that have

received 90% of receivables on time increased and reached the level of 16% of all surveyed

companies, which was the same in the year before. It is worth noting that in September last

year, they accounted for 14% of respondents. Still financial services providers assess their

financial situation most positively, where 54% of respondents receives between 76% and

100% payments on time. The second position in terms of receiving compensation are

companies from tourism industry, among which nearly half (49%) receives from 76% to

100% of payments on time. The slowest payment flow to other businesses and e-commerce

industry, among which 25% and 26% of firms receive less than one-fourth of payments.

61

37

31

61

35

20

58

40

35

65

42

32

73

36

27

49

35

47

63

33

25

2

5

5

3

5

1

4

3

2

5

1

4

8

3

2

6

10

5

8

37

59

64

36

65

75

41

56

62

33

54

67

23

56

70

49

59

43

37

62

67

Feb-12

Sep-12

mar-13

Feb-12

Seb-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

tota

l

fin

anci

al

serv

ices

p

rovi

der

s m

ass

serv

ices

p

rovi

der

s

bu

sin

ess

(oth

er

ind

ust

ries

) to

uri

sm

ind

ust

ry

con

stru

ctio

n

ind

ust

ry

e-c

om

mer

ce

definitely low I do not now definitely high

Figure 4. The share of receivables paid on time

Source: based on the results of research BIG InfoMonitor SA www.big.pl/Raport BIG

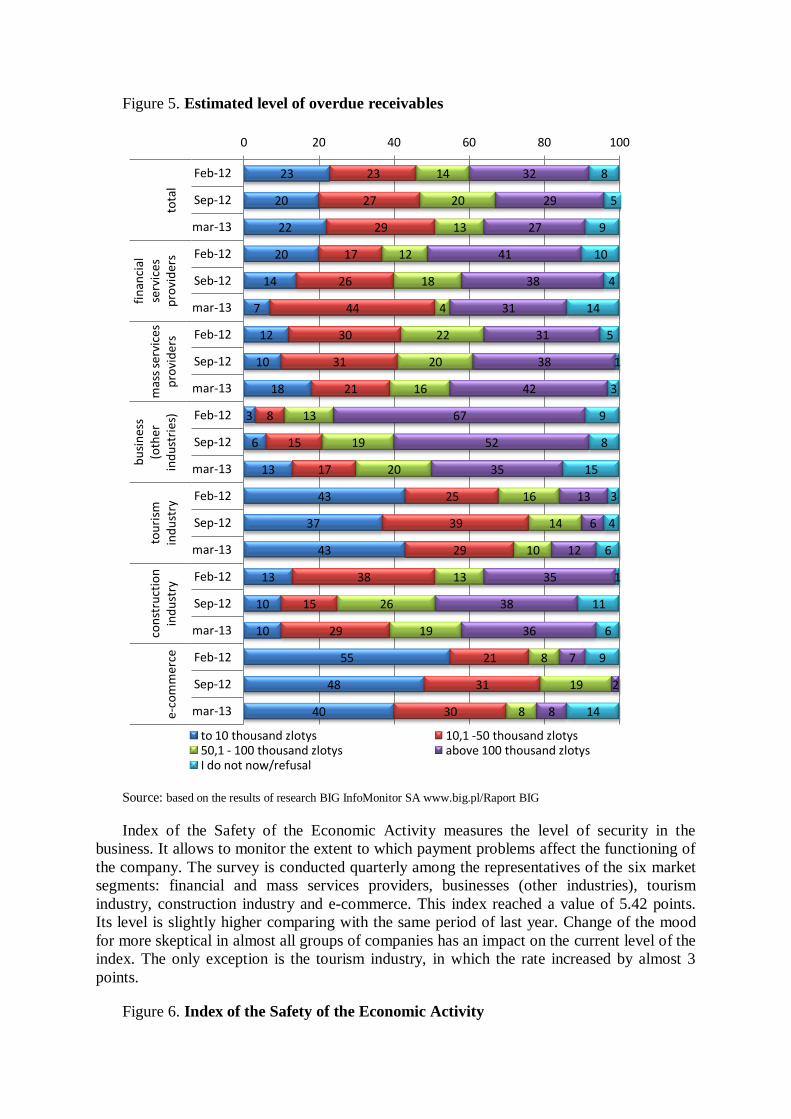

During the year under review the number of respondents who believe that the amount of

overdue receivables exceeds 100 thousand zlotys decreased by 5 percentage points to 27%

(Fig. 5). There is an improvement among entrepreneurs, although as much as 35% of them

expect late payments exceeding 100 thousand zlotys. A year ago, this group was higher by 32

percentage points. In this group of surveyed firms, the largest number of companies refused

to answer (15%). The smallest problems with overdue receivables have representatives in the

field of e-commerce, in which up more than 100 thousand relate to 8% of respondents.

9

7

7

16

5

2

1

4

4

12

1

9

4

11

3

10

6

12

8

10

17

8

7

8

1

1

10

7

3

7

18

20

16

5

1

5

6

10

1

12

11

9

19

19

18

10

8

15

19

13

19

17

32

16

18

16

11

34

29

23

13

23

24

25

28

25

20

27

8

40

36

31

25

11

30

28

29

31

20

33

34

18

30

18

22

23

24

20

27

33

23

33

25

15

20

19

37

30

25

19

13

21

20

15

20

16

14

16

29

29

21

10

9

14

13

16

10

8

7

24

10

9

9

27

11

12

1

2

2

4

3

11

2

6

1

1

2

0 10 20 30 40 50 60 70 80 90 100

Feb-12

Sep-12

mar-13

Feb-12

Seb-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

tota

l

fin

anci

al

serv

ices

p

rovi

der

s m

ass

serv

ices

p

rovi

der

s b

usi

nes

s (o

ther

in

du

stri

es)

tou

rism

in

du

stry

co

nst

ruct

ion

in

du

stry

e-

com

mer

ce

from 0% to 10% from 11% to 25% from 26% to 50% from 51% to 75% from 76% to 90% above 90% I do not now/refusal

Figure 5. Estimated level of overdue receivables

Source: based on the results of research BIG InfoMonitor SA www.big.pl/Raport BIG

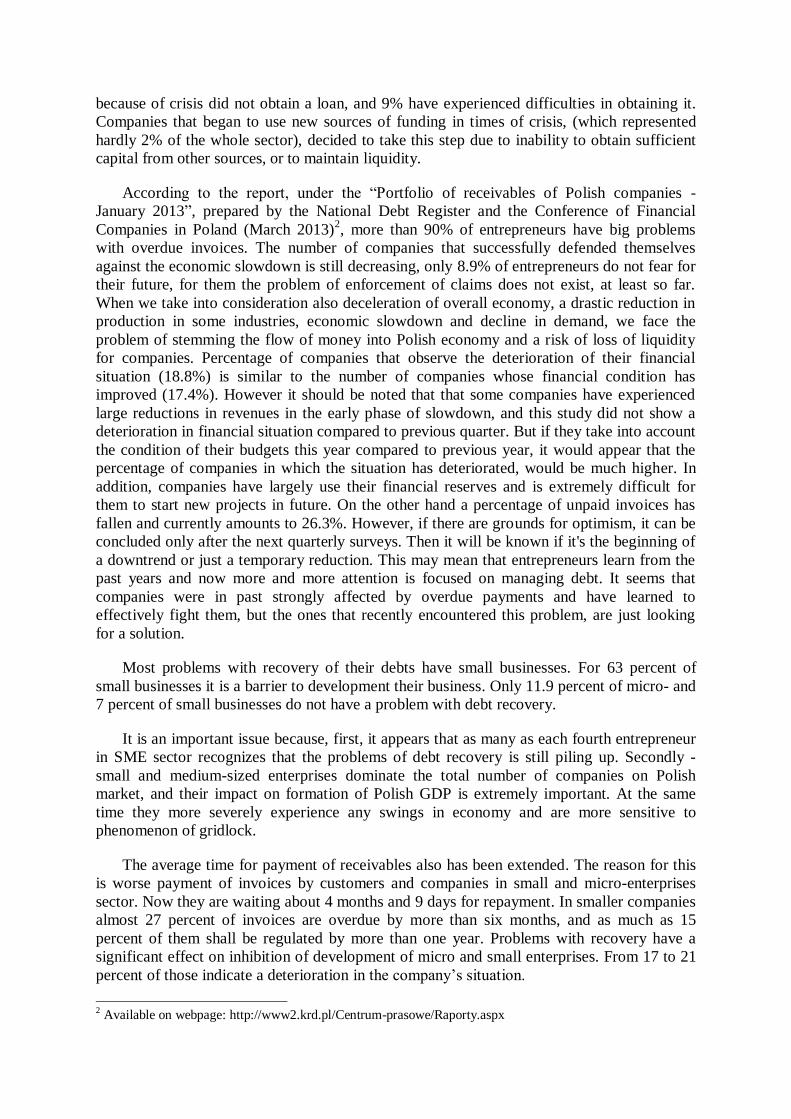

Index of the Safety of the Economic Activity measures the level of security in the

business. It allows to monitor the extent to which payment problems affect the functioning of

the company. The survey is conducted quarterly among the representatives of the six market

segments: financial and mass services providers, businesses (other industries), tourism

industry, construction industry and e-commerce. This index reached a value of 5.42 points.

Its level is slightly higher comparing with the same period of last year. Change of the mood

for more skeptical in almost all groups of companies has an impact on the current level of the

index. The only exception is the tourism industry, in which the rate increased by almost 3

points.

Figure 6. Index of the Safety of the Economic Activity

23

20

22

20

14

7

12

10

18

3

6

13

43

37

43

13

10

10

55

48

40

23

27

29

17

26

44

30

31

21

8

15

17

25

39

29

38

15

29

21

31

30

14

20

13

12

18

4

22

20

16

13

19

20

16

14

10

13

26

19

8

19

8

32

29

27

41

38

31

31

38

42

67

52

35

13

6

12

35

38

36

7

2

8

8

5

9

10

4

14

5

1

3

9

8

15

3

4

6

1

11

6

9

14

0 20 40 60 80 100

Feb-12

Sep-12

mar-13

Feb-12

Seb-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

Feb-12

Sep-12

mar-13

tota

l

fin

anci

al

serv

ices

p

rovi

der

s m

ass

serv

ices

p

rovi

der

s

bu

sin

ess

(oth

er

ind

ust

ries

) to

uri

sm

ind

ust

ry

con

stru

ctio

n

ind

ust

ry

e-c

om

mer

ce

to 10 thousand zlotys 10,1 -50 thousand zlotys 50,1 - 100 thousand zlotys above 100 thousand zlotys I do not now/refusal

Source: BIG InfoMonitor SA www.big.pl / BIG report

Index of the Safety of the Economic Activity in various sectors also brings a pessimistic

signals. Apart from a slight increase in the value of the index in the tourism sector, by 2.69

points, all other industries record a decrease of this index. The situation is even worst in the

construction industry, where the index still oscillates around 0 points.

The results of research, for example on financial resources of companies, the level of

knowledge and use of various financing sources by companies in SME sector, published by

the Polish Agency for Enterprise Development (PARP) in a work titled “Investment

processes and strategies of companies in times of crisis” (W. Orlowski at. al. 2010) show that

for micro companies operating at least at the trans-regional level and companies in low and

medium urbanized areas (except the province of Lodz and Mazowieckie) the decline in

profitability and delayed payments from customers, which may result in a loss of liquidity are

equally severe. Relatively few, only 9% of companies in SME sector declares that because of

crisis they had trouble obtaining a loan.

Among the threats to overall operations of companies, issues related to economic crisis

(fall in the number of customers, market fluctuations, delayed payments) do not stand out in

the foreground. It seems that current situation is more dangerous for micro-firms than for the

rest of the sector. The issue which is most severe for companies, is the tax burden (generally

44% of companies complain about it and in transportation industry – half of enterprises).

Every third respondent mentions risks arising from excessive or unfair competition.

Identifying threats only with competition, which is the case in more than 40% of companies

in Eastern Poland, may be a false diagnosis of problem, because large competition often goes

along with the success of companies, which may result from the need to make more sound

decisions and take a proactive attitude. Every third Polish entrepreneur sees the threat of

unpredictable market fluctuations. The larger the company, the more frequent perception of

economic instability as a real threat.

More than half of companies declared that economic crisis has not affected the change in

a way they use different sources of funding. Such answer was given by enterprises operating

in low and medium urban areas (with exception of central Poland). Perceiving sources of

capital as stable is associated with intense planning of investments. Only 3% of companies

25,71

22,19

20,7

21,06

10,34

3,81 1,44

7,26

14,89

9,28

13,52

13,37

6,56

13,34

11,34

11,51

5,36

11,12

2,93

8,56

5,42

0

5

10

15

20

25

30

Ind

ex

of

the

Saf

ety

of

the

Eco

no

mic

A

ctiv

ity

because of crisis did not obtain a loan, and 9% have experienced difficulties in obtaining it.

Companies that began to use new sources of funding in times of crisis, (which represented

hardly 2% of the whole sector), decided to take this step due to inability to obtain sufficient

capital from other sources, or to maintain liquidity.

According to the report, under the “Portfolio of receivables of Polish companies -

January 2013”, prepared by the National Debt Register and the Conference of Financial

Companies in Poland (March 2013)2, more than 90% of entrepreneurs have big problems

with overdue invoices. The number of companies that successfully defended themselves

against the economic slowdown is still decreasing, only 8.9% of entrepreneurs do not fear for

their future, for them the problem of enforcement of claims does not exist, at least so far.

When we take into consideration also deceleration of overall economy, a drastic reduction in

production in some industries, economic slowdown and decline in demand, we face the

problem of stemming the flow of money into Polish economy and a risk of loss of liquidity

for companies. Percentage of companies that observe the deterioration of their financial

situation (18.8%) is similar to the number of companies whose financial condition has

improved (17.4%). However it should be noted that that some companies have experienced

large reductions in revenues in the early phase of slowdown, and this study did not show a

deterioration in financial situation compared to previous quarter. But if they take into account

the condition of their budgets this year compared to previous year, it would appear that the

percentage of companies in which the situation has deteriorated, would be much higher. In

addition, companies have largely use their financial reserves and is extremely difficult for

them to start new projects in future. On the other hand a percentage of unpaid invoices has

fallen and currently amounts to 26.3%. However, if there are grounds for optimism, it can be

concluded only after the next quarterly surveys. Then it will be known if it's the beginning of

a downtrend or just a temporary reduction. This may mean that entrepreneurs learn from the

past years and now more and more attention is focused on managing debt. It seems that

companies were in past strongly affected by overdue payments and have learned to

effectively fight them, but the ones that recently encountered this problem, are just looking

for a solution.

Most problems with recovery of their debts have small businesses. For 63 percent of

small businesses it is a barrier to development their business. Only 11.9 percent of micro- and

7 percent of small businesses do not have a problem with debt recovery.

It is an important issue because, first, it appears that as many as each fourth entrepreneur

in SME sector recognizes that the problems of debt recovery is still piling up. Secondly -

small and medium-sized enterprises dominate the total number of companies on Polish

market, and their impact on formation of Polish GDP is extremely important. At the same

time they more severely experience any swings in economy and are more sensitive to

phenomenon of gridlock.

The average time for payment of receivables also has been extended. The reason for this

is worse payment of invoices by customers and companies in small and micro-enterprises

sector. Now they are waiting about 4 months and 9 days for repayment. In smaller companies

almost 27 percent of invoices are overdue by more than six months, and as much as 15

percent of them shall be regulated by more than one year. Problems with recovery have a

significant effect on inhibition of development of micro and small enterprises. From 17 to 21

percent of those indicate a deterioration in the company’s situation.

2 Available on webpage: http://www2.krd.pl/Centrum-prasowe/Raporty.aspx

Smaller market players do not have the ability to induce the debtor to pay a debt.

Companies in SME sector cannot afford to maintain the recovery department or paying

lawyers - must look for other ways to efficient recovery of outstanding receivables.

One of them is the annual social action organized by National Debt Register under the

name of Big Spring Cleaning Debts. During the action each of the companies that have

problems with debtors can free add them to the National Debt Register (KRD). Companies

that sign an agreement with KRD before April 30 will be able to add to the register as many

of their debtors as they want free of charge. From 11 to 31 March 2013 more than three

thousand entrepreneurs benefited from this possibility. In the previous eight editions of the

action 38 417 companies from across the country who have managed to recover a total of

nearly PLN 1.2 billion attended.

In the past few months, the value of invoices issued in the invoices market has doubled.

Currently, these claims are worth around PLN 180 million. The phenomenon of finding

methods to recovery will continue. Under the new rules for e-court only those claims which

have become due and payable no later than three years from the application to the court will

be processed. Meanwhile in Polish companies there are millions of uncollected receivables,

so-called small invoices with few years of history. They amount to 400, 500, 800 zlotys. Not

enough to hire a debt collection company for execution and e-court will not accept them. And

these commitments should be paid. What's more - these seemingly minor liabilities are

estimated at a total of about 4 billion zlotys. Therefore, debt markets or debtors registers will

continue to grow in popularity.

5. Payment gridlocks and new legal regulations in Poland

From 1 January 2013 the income tax laws in Poland were supplemented by regulations to

combat the phenomenon of gridlock. Under the new rules, a taxpayer is required to revise the

deductible amount in case of failure to pay the invoice or other document within 30 days

from the date of payment date agreed by the parties. However, if the payment is more than 60

days, a reduction in costs of revenues by the amount of documents shall take place at the end

of 90 days from the date of completion of this amount to deductible amounts. Of course

regulations regarding tax cost adjustments will not apply to taxpayer who did not include

amounts of the invoice or other document in tax costs. Thus, the outstanding amounts of

invoice or other document will not trigger the obligation to correct the tax costs. The new

rules should be applied to amount due on the invoice or other document which have been

included in the cost of tax from 1 January 2013

Changes were also made to the VAT law. Since the VAT system in the EU are

harmonized, it means that the member states are obliged to respect compatibility of national

legislation with regulations under EU law. Therefore it was not possible to introduce a

general principle of the settlement of VAT invoice after a payment as this would be contrary

to EU law which was proposed by some groups of interest. The new rules provide that a

company that has not made a payment of obligation under the invoice, which deducted the

tax, will have to make a VAT adjustment within 150 days from the closing date of payment.

After paying these invoices VAT can be re-deductible in a tax return.

Again, this change has the effect of reducing gridlock and improving the liquidity of

companies. However, contrary to principles set out in the Income Tax Act, the adjustment

shall be made only after 150 days and what is more calculated after expiry of date for

payment specified on the invoice. It may therefore happen that the real adjustment of added

tax will be only after 240 days of invoice date (the date of the invoice due 90 days + 150 days

from the provision of the VAT Act). This penalty is obviously more severe for companies

where there is a surplus of VAT due on added, i.e. VAT payable. Companies that have an

overpayment of VAT may not feel the negative effects of adjustment of added tax. These

principles also apply to invoices issued in 2012, which due date fell within the period from

4 August 2012 to 31 December 2012.

For all taxpayers (except for those who have chosen a cash VAT) a certain ”relief” if an

invoice is not paid by a contractor within 150 days from the due date of payment has been

provided. In this case, a taxpayer, who has shown VAT payable on a declaration can

“correct” it after 150 days mentioned above. Procedures for using that advantage by

removing the obligation to inform the debtor of its intention to make adjustments, and about

the fact of its occurrence were simplified. However, a reduction of tax due can be applied

only if on the day of revision the debtor is an active VAT taxpayer (this was also the case in

2012) and cannot be in the process of bankruptcy or liquidation (added regulation). A debtor

who has not paid the due within 5 months is often already in the bankruptcy or liquidation

proceedings have been initiated, and this means that the relief will not be possible to apply.

Please note that the relief relates to invoices for which a period of two years from the date of

issuing them has not expired counting from the end of the year in which the invoice is issued.

Taxpayers whose gross turnover (revenues) in 2012 amounted to less than 1.2 million

euros (4.922.000 PLN gross) will be able to choose in 2013 an adjusted cash basis method of

settlement. In this method, the tax on each invoice documenting the sale arises only on the

date of payment. To date, the use of cash basis was not very popular, because only gave the

deferred payment of VAT on invoices not paid for 90 days from date of invoice. Beginning in

2013, choosing a cash basis, VAT due on all invoices issued to customers who are payers of

VAT is to be shown in the VAT and paid into the Tax Office account after payment of

invoice by the customer.

This part of cash basis policy concerning the settlement of VAT due is quite favorable.

Payment of tax only at the time when we receive the payment is very reasonable and safe

option for the company. This principle is especially beneficial for companies whose

contractors extend payment terms or don’t pay at all. Also, companies that have longer

payment terms of sales invoices, e.g. 30, 60 days can experience great benefit from the

application of this principle. Although the amount due on an invoice is not overdue the

company using a cash basis shows and pay VAT a month or two later than the firm which did

not choose this method. Slightly worse the situation is with the sale of individuals carrying

out business activities and companies not registered for VAT. In this case, if after 180 days

from the date goods were supplied or services provided the invoice is not paid, the VAT due,

will need to be applied and paid. In this case, a significant potential to delay payment of tax

due is achieved, but after half a year it has to be paid.

With effect from 8 March 2013 a new law came into force on dates of payment in

commercial transactions, which replaced the law of the same name which was in force since

2003. It aims to discipline debtors to pay on time, preventing the phenomenon of gridlock

and gratuitous lending of own business at the expense of customers waiting to receive debts.

Act on payment terms in commercial transactions has replicated some of solutions present for

years in regulations, but also introduces a lot of new not known before. The new rules apply

from 28 April and are designed to adjust Polish law to requirements of Directive of the

European Parliament and Council 2011/7/EU of 16 February 2011 on combating late

payment in commercial transactions. It should be noted that according to experts, the EU

intervention can be an important limitation of freedom of contract. What's more, it can lead to

an increase in operating costs of enterprises. The act entered to law in Poland contains many

new features, such as reimbursement for recovery costs from the debtor or clear rules for

calculation of interest in case of installment payments. Importantly, the transactions

concluded before this Act entered into force are subject to current regulations.3 The new law

aims to combat the deepening problem of gridlock by introducing more discipline rules to

parties. According to the law period of settlement between parties should not exceed 60

calendar days and 30 days of tax office settlement unless agreed otherwise and that it is not

grossly unfair to any party. Exceeding 60 days will be treated as delay, provided that the

creditor proves that circumstances of the contract were grossly unfair. After completing

contractual obligations, creditors shall be entitled to default interest in amount specified in the

Act or the amount agreed upon between the parties. The Act is also a provision by which the

creditor will be able to recover costs incurred during the investigation of debtor's debts. This

will be fixed compensation in amount of 40 euros. It is to be calculated from the time when

interest for late payment become due.

The new rules will also cover the business of member states of the European Union,

member states of the European Free Trade Association (EFTA) - parties to the Agreement on

the European Economic Area or the Swiss Confederation.

Attempts to legal sanctioning of late payments in UK show that only 2% of small and

medium-sized enterprises use their right to charge interest (Wilson, 2008). According to

experts, the EU intervention can be a significant restriction of freedom of contract. What's

more, it can lead to an increase in operating costs of enterprises.

4. Conclusions

An overview of prior research on use of trade credit liquidity management in particular

small and medium-sized enterprises, and causes of mechanisms of gridlock, and analysis of

collected and presented research on delayed payment of trade receivables presented in this

framework enable to draw some conclusions. Namely, companies that have easier access to

external funds are often large companies, which more willingly and easily grant credit to

commercial customers who have difficulties in obtaining financing.

Despite the improvement in situation since February 2012, 83% of surveyed Polish

entrepreneurs perceive problems with payment gridlock in business as definitely burdensome

for business. More than half of respondents believe that the phenomenon of delayed

payments among companies in their industry is frequent. The share of claims paid on time is

assessed by financial service providers as most favourable, and other business representatives

and construction industry firms worst, where about 70% of their claims is not paid on time.

The result is that approximately 35% of companies wait for overdue payments, the sum of

which exceeds 100.000 zlotys.

Despite the importance of these results for ongoing research on trade credit, the study

should be broadened in order to identify reasons.

Company's development, especially investment and raising technological level, requires

adequate funding. Studies have shown that while in past two decades there has been

significant development of Polish financial market, SME sector seem to hardly notice

3 Act of 8 March 2013 on dates of payment in commercial (Journal of Laws, pos. 403)

relatively broad opportunities available for them. Practice shows that on the one hand

companies typically use a fairly conservative method of financing, on the other hand are able

to engage in risky financial instruments, which are difficult to understand.

It is very common that companies have very limited knowledge of the possible sources of

financing. Only simplest ways are known (own funds, bank loans, leasing) and also EU funds

because of unique moment in history of country's economic development. This low

awareness of possibility of finding funding actually affects the small use of existing sources.

The vast majority of companies said they did not use any sources of funding, or that it is

based only on its own resources. Among users of external financing outweigh indications

regarding bank loan or lease. It should be admitted that this should not be surprising if we

take into account the specific characteristics of SME sector.

It should also be noted that among SME sector companies there is relatively little trust in

external financing. While most agree that a bank loan can be a source of financing for the

company, however the opinion that a company can reach for it only in case of serious

problems is dominant. This reflects the widespread phenomenon of concerns about taking

credit for SMEs, which is considered a risky operation for a company.

Slightly less distrust prevails in relation to different types of grants. This is not the fear of

risk, which is a dominant factor but the fear of complex and time-consuming formalities.

Therefore, efforts are needed not only to increase the confidence of SMEs to external

financing, but also to increase the owners' knowledge on modern alternative sources of

financing companies.

References

Alphonse, P., Ducret, J., Séverin, E. (2006), “When Trade Credit Facilitates Access to Bank

Finance: Evidence from U.S. Small Business Data”, Working Paper, Université de Nancy,

University of Valenciennes and University of Lille.

Bancel, F., Mittoo, U.R. (2011), “Financial flexibility and the impact of the global financial

crisis: Evidence from France”, International Journal of Managerial Finance Vol. 7(2), pp:

179-216.

Bancel, F., Mittoo, U.R. (2004), “Cross-country determinants of capital structure choice: a

survey of European firms”, Financial Management, Vol. 33, pp: 103-132.

Belletante, B., Levratto, N. (1995), “Le financement des PME: quels champs pour quels

enjeux?”, Revue Internationale des PME, Vol. 8 No. 3-4, pp: 5-42.

Berger, A.N., Udell, G.F. (1995), “Relationship Lending and Lines of Credit in Small Firm

Finance”, Journal of Business, Vol. 68, pp: 351-381.

Biadacz, R. (2012), Currency Exchange Risk in International Trade Transactions, in:

Dilemmas of the Contemporary Economy Facing Global Changes, Edited by J. Kaczmarek,

T. Rojek, Publish. House: Foundation of the Cracow University of Economics, Cracow, pp:

91-104.

Biais, B., Gollier, C. (1997), “Trade credit and credit rationing”, The Review of Financial

Studies, Vol. 10 No. 4, pp: 903-937.

BIG Report InfoMonitor SA. Available at: www.big.pl/Raport BIG (accessed 12 February

2013).

Brechling, F., Lipsey, R. (1963), “Trade credit and monetary policy”, Economic Journal,

Vol. 73 No. 2, pp: 618-641.

Cuñat, V. (2002), Trade credit: suppliers as debt collectors and insurance providers,

Universitat Pompeu Fabra and Financial Markets Group (LSE), Barcelona and London.

Czekaj, J., Dresler, W. (1995), Podstawy zarządzania finansami firm, PWN, Warsaw (in

Polish).

Deloof, M. (2003), “Does working capital management affect profitability of Belgian

firms?”, Journal of Business Finance & Accounting, Vol. 30 No. 3/4, pp: 573-587.

Ding, W., Domac, I., Giovanni, F. (2008), “Is there a credit crunch in the Far East?”, The

World Bank, available at:

www.worldbank.org/html/dec/Publications/Workpapers/WPS1900series/wps1959/wps1959.p

df (accessed 12 February 2013).

Ekanem, I. (2010) “Liquidity management in small firms: a learning perspective”, Journal of

Small Business and Enterprise Development, Vol. 17 Iss: 1, pp: 123 – 138.

Emery, G. W. (1984), “A pure financial explanation for trade credit”, Journal of Financial

and Quantitative Analysis, Vol. 19 No. 3, pp: 271-285.

Emery, G. W. (1987), “An Optimal Financial Response to Variable Demand”, Journal of

Financial and Quantitative Analysis, Vol. 22 Iss.02, pp: 209-225.

Frank, M., Maksimovic, V. (1998), Trade credit, collateral, and adverse selection, University

of British Columbia, Vancouver and University of Maryland, Baltimore, MD.

Freixas, X. (1993), “Short term credit vs accounts receivable financing”, Economic Working

Papers Series, Pompeu Fabra University, Barcelona, March.

García-Teruel, P. J., Martínez-Solano, P. (2010), “Determinants of trade credit: A

comparative study of European SMEs”, International Small Business Journal, June, Vol. 28

No. 3, pp: 215-233.

Graham, J., Harvey, C. (2001), “The theory and practice of corporate finance: evidence from

the field”, Journal of Financial Economics, Vol. 60, pp: 187-243.

Jain, N. (2001), “Monitoring Costs and Trade Credit”, Quarterly Review of Economics and

Finance, Vol. 41 No 1, pp: 89-110.

Martínez-Sola, C., García-Teruel, P. J., Martínez-Solano, P. “Trade credit and SME

profitability”, Small Business Economics, Forthcoming, available at:

http://www.aeca.es/pub/on_line/comunicaciones_xvicongresoaeca/cd/150b.pdf

McMahon, R., Stanger, A. (1995), “Understanding the small enterprise financial objective

function”, Entrepreneurship Theory and Practice, Vol. 19 (4), pp: 21-39.

Meltzer, A. H. (1960), “Mercantile credit, monetary policy, and size of firms”, Review of

Economics and Statistics, Vol. 42 (4), pp: 429-437.

Mian, S., Smith, C. Jr (1992), “Accounts receivable management policy: theory and

evidence”, The Journal of Finance, Vol. 47 No.1, pp: 169-200.

Nadiri, M. (1969), “The determinants of trade credit in the US total manufacturing sector”,

Econometrica, Vol. 37 No. 3, pp: 408-423.

Nilsen, J. (2002), “Trade credit and the bank lending channel”, Journal of Money, Credit, and

Banking, Vol. 34 No.1, pp: 226-253.

Norrbin, S., Reffett, K. (1995), “Trade credit in a monetary economy”, Journal of Monetary

Economics, Vol. 35 No. 3, pp: 413-430.

Orłowski, W., Pasternak, R., Flaht, K., Szubert, D. (2010), Procesy inwestycyjne i strategie

przedsiębiorstw w czasach kryzysu, PARP - Unia Europejska Europejski Fundusz Społeczny,

pp: 62-63 (in Polish).

Paul, S.Y., Boden, R. (2008), “The secret life of UK trade credit supply: setting a new

research agenda”, The British Accounting Review, Vol. 40 No.3, pp.272-281.

Paul, S. Y., Boden, R. (2011), “Size matters: the late payment problem”, Journal of Small

Business and Enterprise Development, Vol. 18 Iss 4, pp: 732-747.

Peel, M.J., Wilson, N., Howorth, C. (2000), “Late payment and credit management in the

small firm sector: some empirical evidence”, International Small Business Journal, Vol. 18

No. 2, pp: 17-37.

Poutziouris, P., Chittenden, F., Michaelas, N. (1999), The Financial Affairs of Private

Companies: Research, Manchester Business School, Manchester.

Ramey, V. (1992), “The source of fluctuations in money: evidence from trade credit”,

Journal of Monetary Economics, Vol. 30, pp: 171-193.

Report “Portfolio of receivables of Polish companies - January 2013”, National Debt Register

and the Conference of Financial Companies in Poland (March 2013), available at:

http://www2.krd.pl/Centrum-prasowe/Raporty.aspx (accessed April 2013).

Report Roland Berger Strategy Consultants (2010), available at:

http://www.rolandberger.pl/media/pdf/Roland_Berger__International_Restructuring_Study_2

0100619.pdf (accessed 10 February 2013).

Rodríguez-Rodríguez, O. M., (2008), “Firms as credit suppliers: an empirical study of

Spanish firms”, International Journal of Managerial Finance, Vol. 4 No. 2, pp: 152-173.

Rubik, J., (2011), Rola faktoringu w zarządzaniu płynnością finansową jednostki, Zeszyty

Naukowe Uniwersytetu Szczecińskiego No. 668, seria Finanse, Rynki finansowe,

Ubezpieczenia No. 41, Szczecin, pp: 472-479 (in Polish).

Schwartz, R. (1974), “An economic model of trade credit”, Journal of Finance and

Quantitative Analysis, Vol. 9 No. September, pp: 643-57.

Schwartz, R. A., Whitcomb, D. (1978), Implicity Transfers in the Extension of Trade Credit,

[in:] Kenneth E. Boulding and Thomas F. Wilson, eds. The channels of redistribution

through the financial system. New York, pp: 191-208.

Schwartz, R. A. Whitcomb, D. (1979), The Trade Credit Decision, [in:] James L. Bicksler,

ed. Handbook of Financial Economics, Amsterdam: North-Holland, pp. 257-273.

Stiglitz, J. Weiss, A. (1981): “Credit Rationing in Markets with Imperfect Information”,

American Economic Review, Vol. 71, pp: 393-410.

St-Pierre, J., Bahri, M. (2006), “The use of the accounting beta as an overall risk indicator for

unlisted companies”, Journal of Small Business and Enterprise Development, Vol. 13 Iss. 4,

pp: 546-561.

The Act of March 8, 2013 on payment periods in commercial transactions (DzU. poz. 403)

(in Polish).

Wilner, B. (2000), “The exploitation of relationships in financial distress: the case of trade

credit”, The Journal of Finance, Vol. 55 No.1, pp.153-178.

Wilson, N. (2008), An Investigation into Payment Trends and Behaviour in the UK: 1997-

2007, CMRC Centre, Leeds University Business School, Leeds.