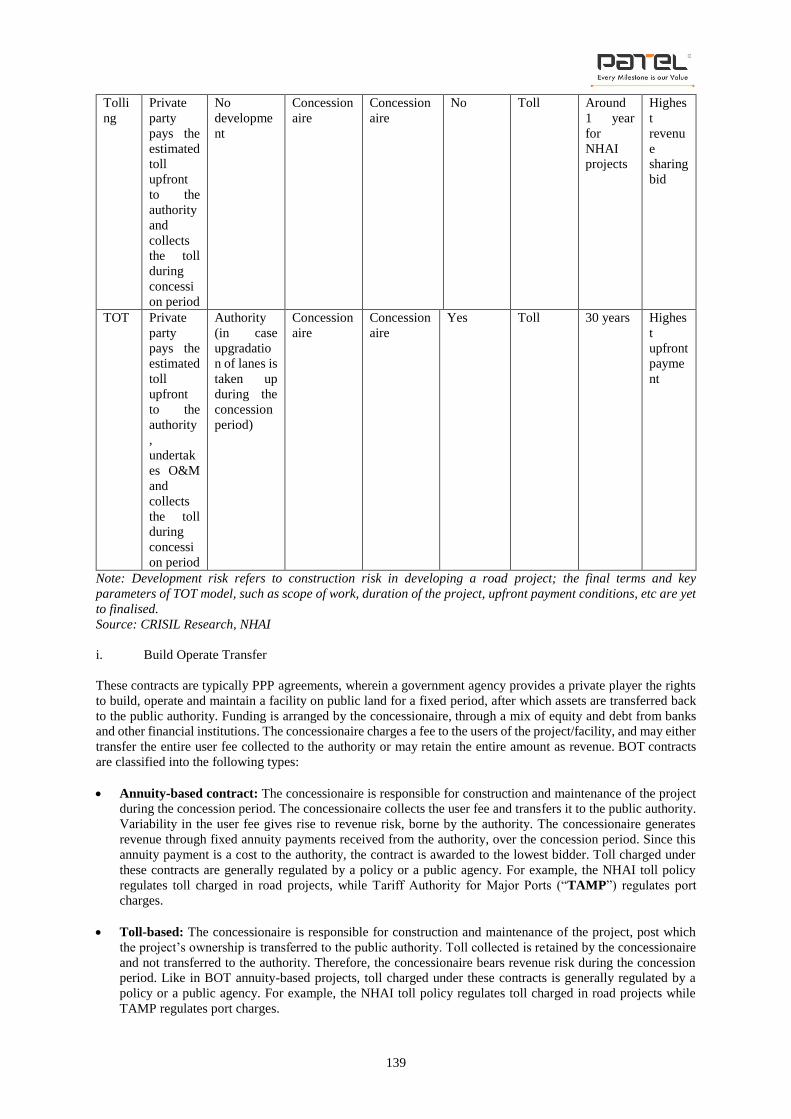

Embed Size (px)

Citation preview

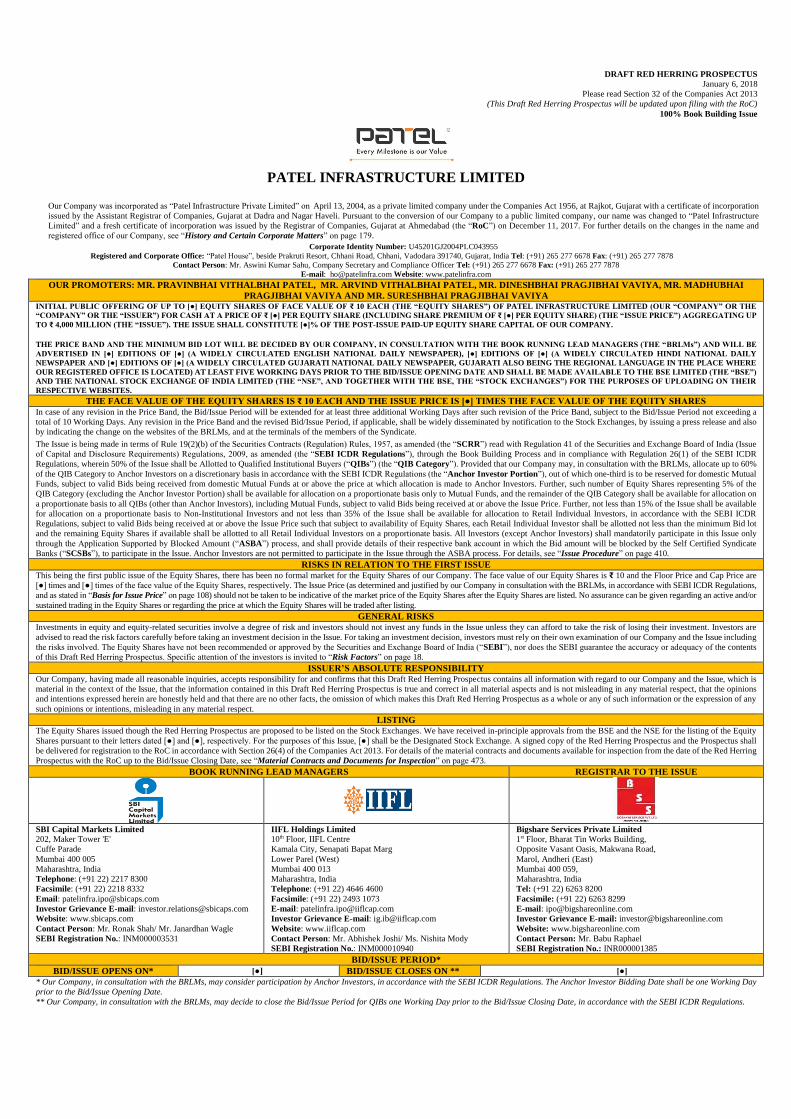

PATEL INFRASTRUCTURE LIMITED

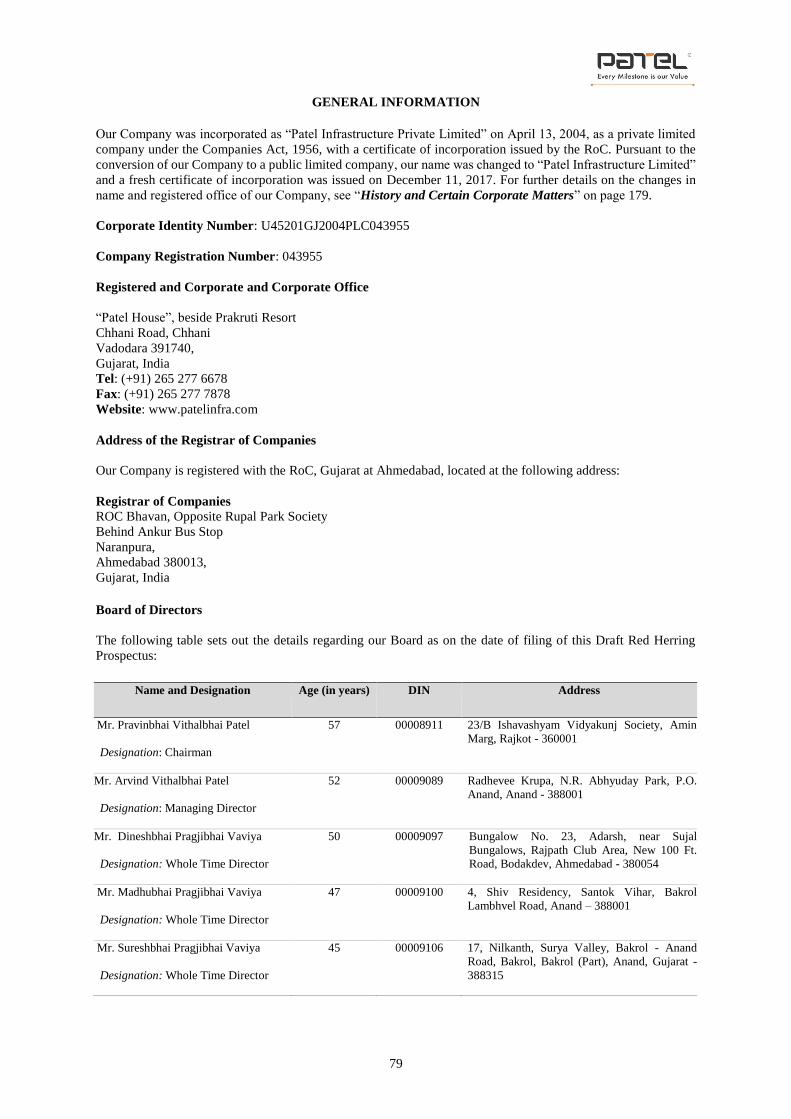

Our Company was incorporated as “Patel Infrastructure Private Limited” on April 13, 2004, as a private limited company under the Companies Act 1956, at Rajkot, Gujarat with a certificate of incorporation

issued by the Assistant Registrar of Companies, Gujarat at Dadra and Nagar Haveli. Pursuant to the conversion of our Company to a public limited company, our name was changed to “Patel Infrastructure

Limited” and a fresh certificate of incorporation was issued by the Registrar of Companies, Gujarat at Ahmedabad (the “RoC”) on December 11, 2017. For further details on the changes in the name and

registered office of our Company, see “History and Certain Corporate Matters” on page 179.

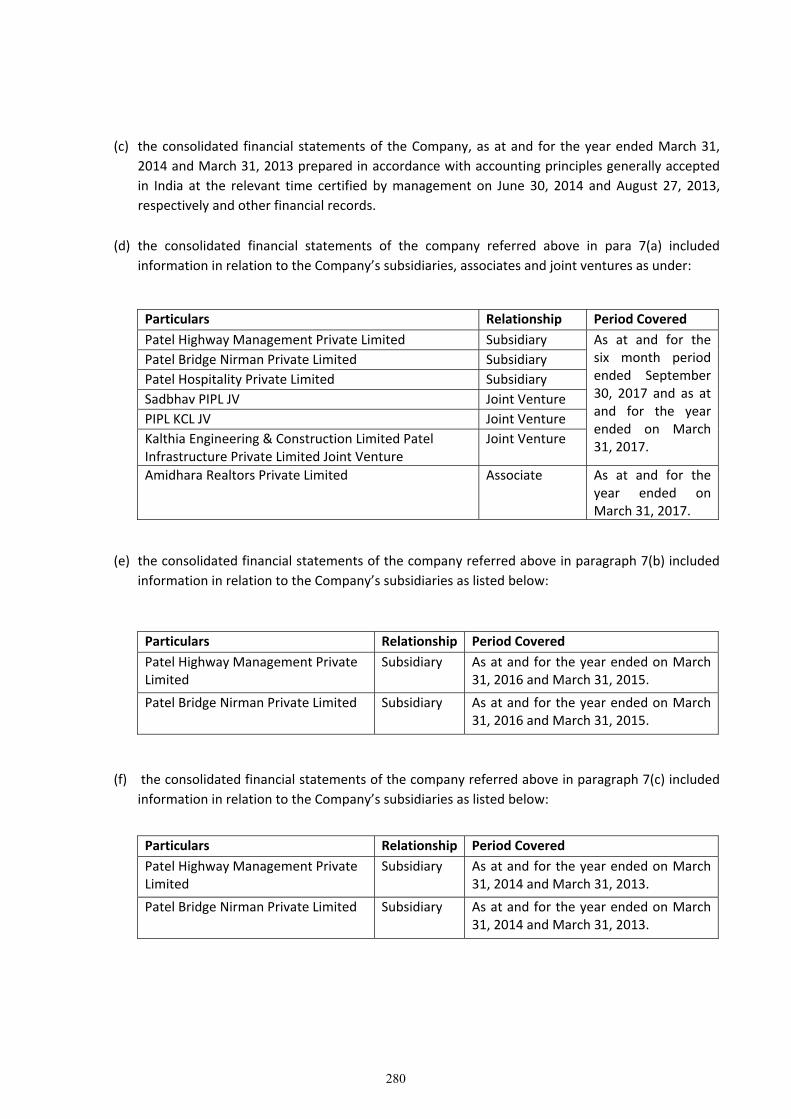

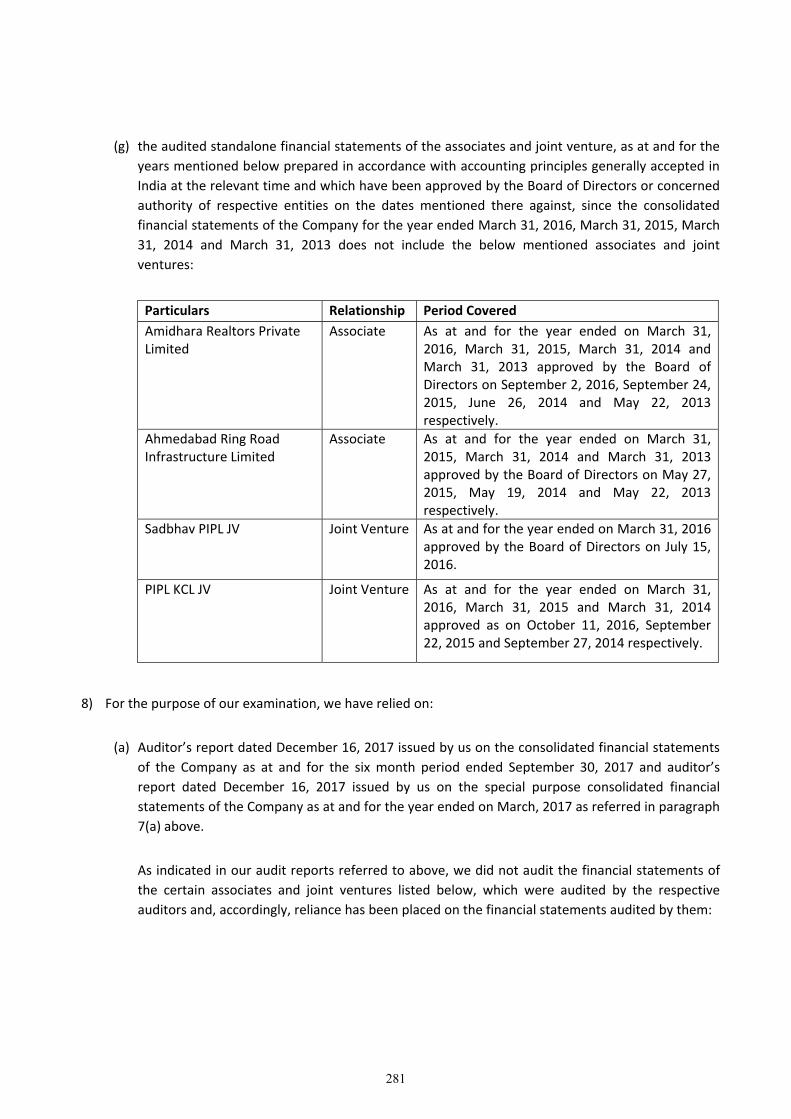

Corporate Identity Number: U45201GJ2004PLC043955

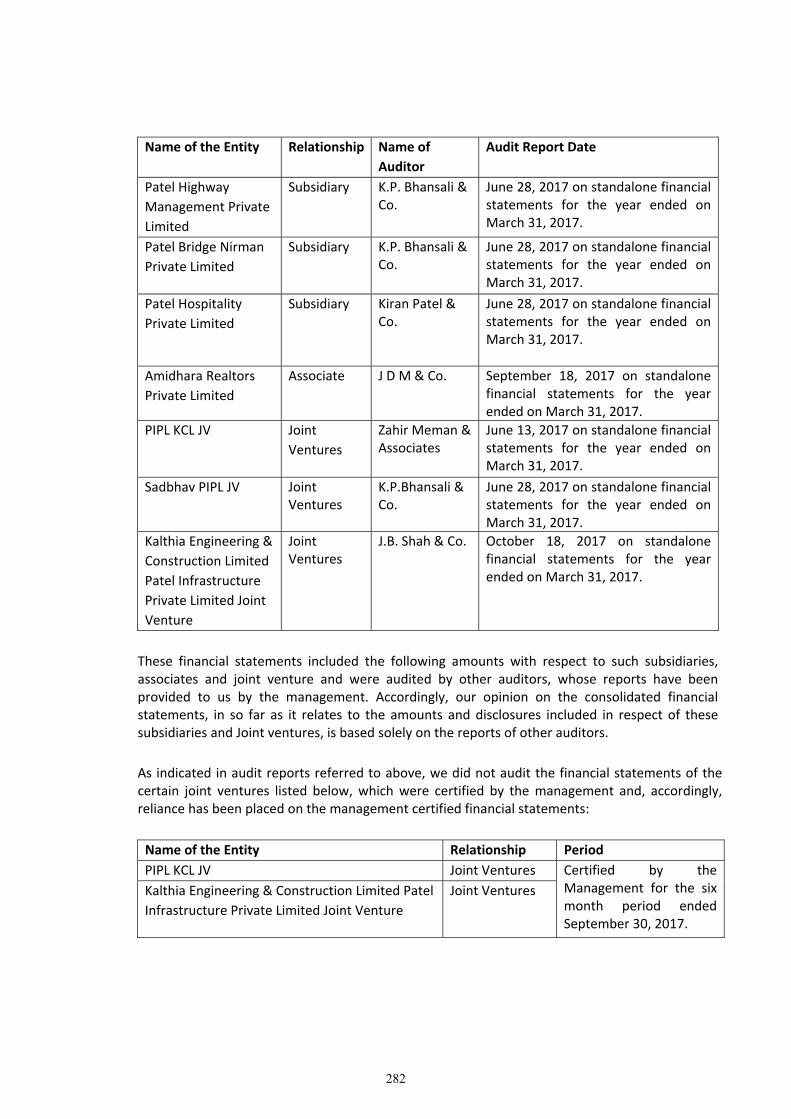

Registered and Corporate Office: “Patel House”, beside Prakruti Resort, Chhani Road, Chhani, Vadodara 391740, Gujarat, India Tel: (+91) 265 277 6678 Fax: (+91) 265 277 7878 Contact Person: Mr. Aswini Kumar Sahu, Company Secretary and Compliance Officer Tel: (+91) 265 277 6678 Fax: (+91) 265 277 7878

E-mail: [email protected] Website: www.patelinfra.com

OUR PROMOTERS: MR. PRAVINBHAI VITHALBHAI PATEL, MR. ARVIND VITHALBHAI PATEL, MR. DINESHBHAI PRAGJIBHAI VAVIYA, MR. MADHUBHAI

PRAGJIBHAI VAVIYA AND MR. SURESHBHAI PRAGJIBHAI VAVIYA INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (THE “EQUITY SHARES”) OF PATEL INFRASTRUCTURE LIMITED (OUR “COMPANY” OR THE

“COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF ₹ [●] PER EQUITY SHARE (INCLUDING SHARE PREMIUM OF ₹ [●] PER EQUITY SHARE) (THE “ISSUE PRICE”) AGGREGATING UP

TO ₹ 4,000 MILLION (THE “ISSUE”). THE ISSUE SHALL CONSTITUTE [●]% OF THE POST-ISSUE PAID-UP EQUITY SHARE CAPITAL OF OUR COMPANY.

THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY OUR COMPANY, IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (THE “BRLMs”) AND WILL BE

ADVERTISED IN [●] EDITIONS OF [●] (A WIDELY CIRCULATED ENGLISH NATIONAL DAILY NEWSPAPER), [●] EDITIONS OF [●] (A WIDELY CIRCULATED HINDI NATIONAL DAILY

NEWSPAPER AND [●] EDITIONS OF [●] (A WIDELY CIRCULATED GUJARATI NATIONAL DAILY NEWSPAPER, GUJARATI ALSO BEING THE REGIONAL LANGUAGE IN THE PLACE WHERE

OUR REGISTERED OFFICE IS LOCATED) AT LEAST FIVE WORKING DAYS PRIOR TO THE BID/ISSUE OPENING DATE AND SHALL BE MADE AVAILABLE TO THE BSE LIMITED (THE “BSE”)

AND THE NATIONAL STOCK EXCHANGE OF INDIA LIMITED (THE “NSE”, AND TOGETHER WITH THE BSE, THE “STOCK EXCHANGES”) FOR THE PURPOSES OF UPLOADING ON THEIR

RESPECTIVE WEBSITES.

THE FACE VALUE OF THE EQUITY SHARES IS ₹ 10 EACH AND THE ISSUE PRICE IS [●] TIMES THE FACE VALUE OF THE EQUITY SHARES

In case of any revision in the Price Band, the Bid/Issue Period will be extended for at least three additional Working Days after such revision of the Price Band, subject to the Bid/Issue Period not exceeding a

total of 10 Working Days. Any revision in the Price Band and the revised Bid/Issue Period, if applicable, shall be widely disseminated by notification to the Stock Exchanges, by issuing a press release and also

by indicating the change on the websites of the BRLMs, and at the terminals of the members of the Syndicate.

The Issue is being made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended (the “SCRR”) read with Regulation 41 of the Securities and Exchange Board of India (Issue

of Capital and Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”), through the Book Building Process and in compliance with Regulation 26(1) of the SEBI ICDR

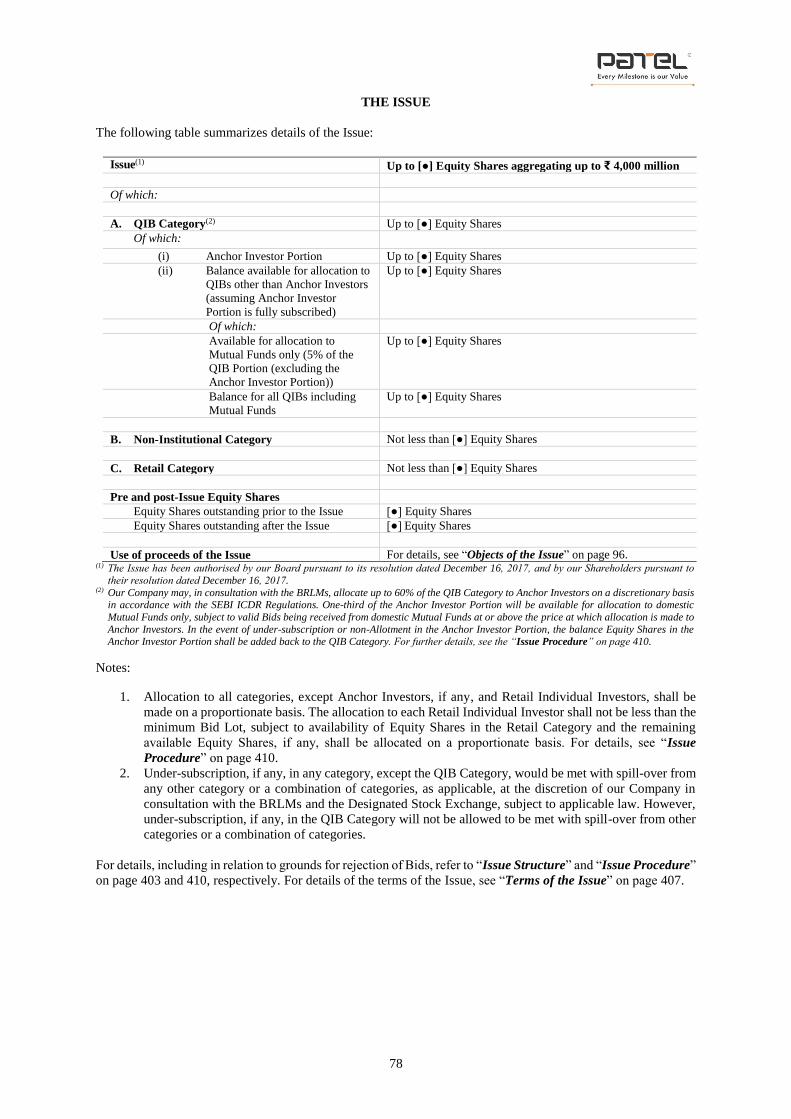

Regulations, wherein 50% of the Issue shall be Allotted to Qualified Institutional Buyers (“QIBs”) (the “QIB Category”). Provided that our Company may, in consultation with the BRLMs, allocate up to 60%

of the QIB Category to Anchor Investors on a discretionary basis in accordance with the SEBI ICDR Regulations (the “Anchor Investor Portion”), out of which one-third is to be reserved for domestic Mutual

Funds, subject to valid Bids being received from domestic Mutual Funds at or above the price at which allocation is made to Anchor Investors. Further, such number of Equity Shares representing 5% of the

QIB Category (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis only to Mutual Funds, and the remainder of the QIB Category shall be available for allocation on

a proportionate basis to all QIBs (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Issue shall be available

for allocation on a proportionate basis to Non-Institutional Investors and not less than 35% of the Issue shall be available for allocation to Retail Individual Investors, in accordance with the SEBI ICDR

Regulations, subject to valid Bids being received at or above the Issue Price such that subject to availability of Equity Shares, each Retail Individual Investor shall be allotted not less than the minimum Bid lot

and the remaining Equity Shares if available shall be allotted to all Retail Individual Investors on a proportionate basis. All Investors (except Anchor Investors) shall mandatorily participate in this Issue only

through the Application Supported by Blocked Amount (“ASBA”) process, and shall provide details of their respective bank account in which the Bid amount will be blocked by the Self Certified Syndicate

Banks (“SCSBs”), to participate in the Issue. Anchor Investors are not permitted to participate in the Issue through the ASBA process. For details, see “Issue Procedure” on page 410.

RISKS IN RELATION TO THE FIRST ISSUE

This being the first public issue of the Equity Shares, there has been no formal market for the Equity Shares of our Company. The face value of our Equity Shares is ₹ 10 and the Floor Price and Cap Price are

[●] times and [●] times of the face value of the Equity Shares, respectively. The Issue Price (as determined and justified by our Company in consultation with the BRLMs, in accordance with SEBI ICDR Regulations,

and as stated in “Basis for Issue Price” on page 108) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or

sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS

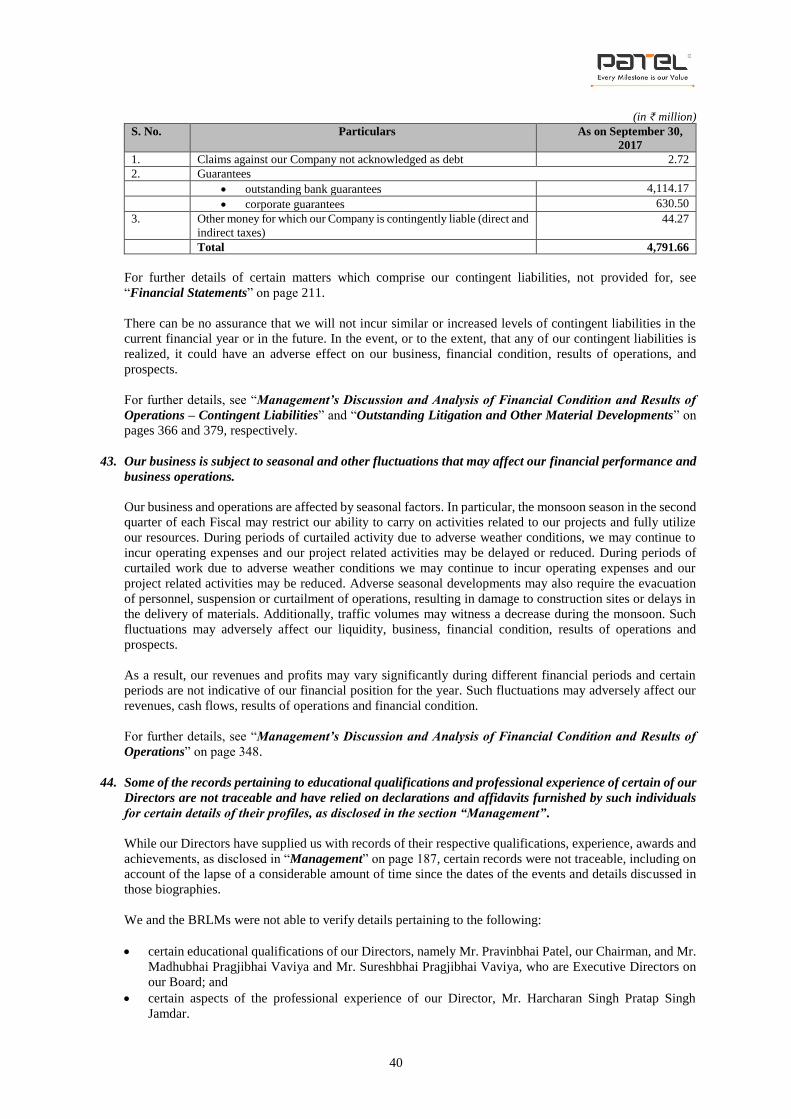

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their investment. Investors are

advised to read the risk factors carefully before taking an investment decision in the Issue. For taking an investment decision, investors must rely on their own examination of our Company and the Issue including

the risks involved. The Equity Shares have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does the SEBI guarantee the accuracy or adequacy of the contents

of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 18.

ISSUER’S ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Issue, which is

material in the context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions

and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any

such opinions or intentions, misleading in any material respect.

LISTING

The Equity Shares issued though the Red Herring Prospectus are proposed to be listed on the Stock Exchanges. We have received in-principle approvals from the BSE and the NSE for the listing of the Equity

Shares pursuant to their letters dated [●] and [●], respectively. For the purposes of this Issue, [●] shall be the Designated Stock Exchange. A signed copy of the Red Herring Prospectus and the Prospectus shall

be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring

Prospectus with the RoC up to the Bid/Issue Closing Date, see “Material Contracts and Documents for Inspection” on page 473.

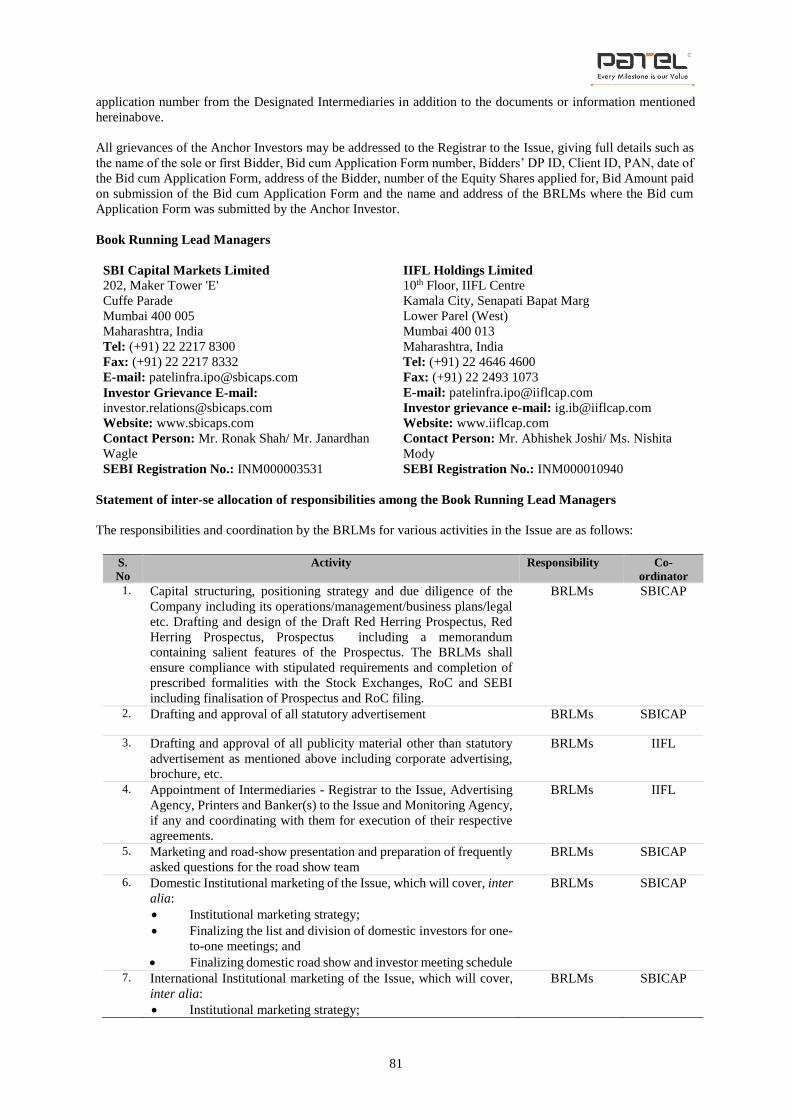

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

SBI Capital Markets Limited 202, Maker Tower 'E'

Cuffe Parade

Mumbai 400 005

Maharashtra, India

Telephone: (+91 22) 2217 8300

Facsimile: (+91 22) 2218 8332

Email: [email protected]

Investor Grievance E-mail: [email protected]

Website: www.sbicaps.com

Contact Person: Mr. Ronak Shah/ Mr. Janardhan Wagle

SEBI Registration No.: INM000003531

IIFL Holdings Limited

10th Floor, IIFL Centre

Kamala City, Senapati Bapat Marg

Lower Parel (West)

Mumbai 400 013

Maharashtra, India

Telephone: (+91 22) 4646 4600

Facsimile: (+91 22) 2493 1073

E-mail: [email protected]

Investor Grievance E-mail: [email protected]

Website: www.iiflcap.com

Contact Person: Mr. Abhishek Joshi/ Ms. Nishita Mody

SEBI Registration No.: INM000010940

Bigshare Services Private Limited

1st Floor, Bharat Tin Works Building,

Opposite Vasant Oasis, Makwana Road,

Marol, Andheri (East)

Mumbai 400 059,

Maharashtra, India

Tel: (+91 22) 6263 8200

Facsimile: (+91 22) 6263 8299

E-mail: [email protected]

Investor Grievance E-mail: [email protected]

Website: www.bigshareonline.com

Contact Person: Mr. Babu Raphael

SEBI Registration No.: INR000001385

BID/ISSUE PERIOD*

BID/ISSUE OPENS ON* [●]] BID/ISSUE CLOSES ON ** [●]

* Our Company, in consultation with the BRLMs, may consider participation by Anchor Investors, in accordance with the SEBI ICDR Regulations. The Anchor Investor Bidding Date shall be one Working Day

prior to the Bid/Issue Opening Date.

** Our Company, in consultation with the BRLMs, may decide to close the Bid/Issue Period for QIBs one Working Day prior to the Bid/Issue Closing Date, in accordance with the SEBI ICDR Regulations.

DRAFT RED HERRING PROSPECTUS

January 6, 2018

Please read Section 32 of the Companies Act 2013

(This Draft Red Herring Prospectus will be updated upon filing with the RoC)

100% Book Building Issue

TABLE OF CONTENTS

SECTION I - GENERAL ..................................................................................................................................... 1

DEFINITIONS AND ABBREVIATIONS ..................................................................................................... 1 CERTAIN CONVENTIONS, USE OF FINANCIAL INFORMATION AND MARKET DATA AND

CURRENCY OF PRESENTATION ............................................................................................................ 13 FORWARD-LOOKING STATEMENTS ................................................................................................... 16

SECTION II - RISK FACTORS ....................................................................................................................... 18

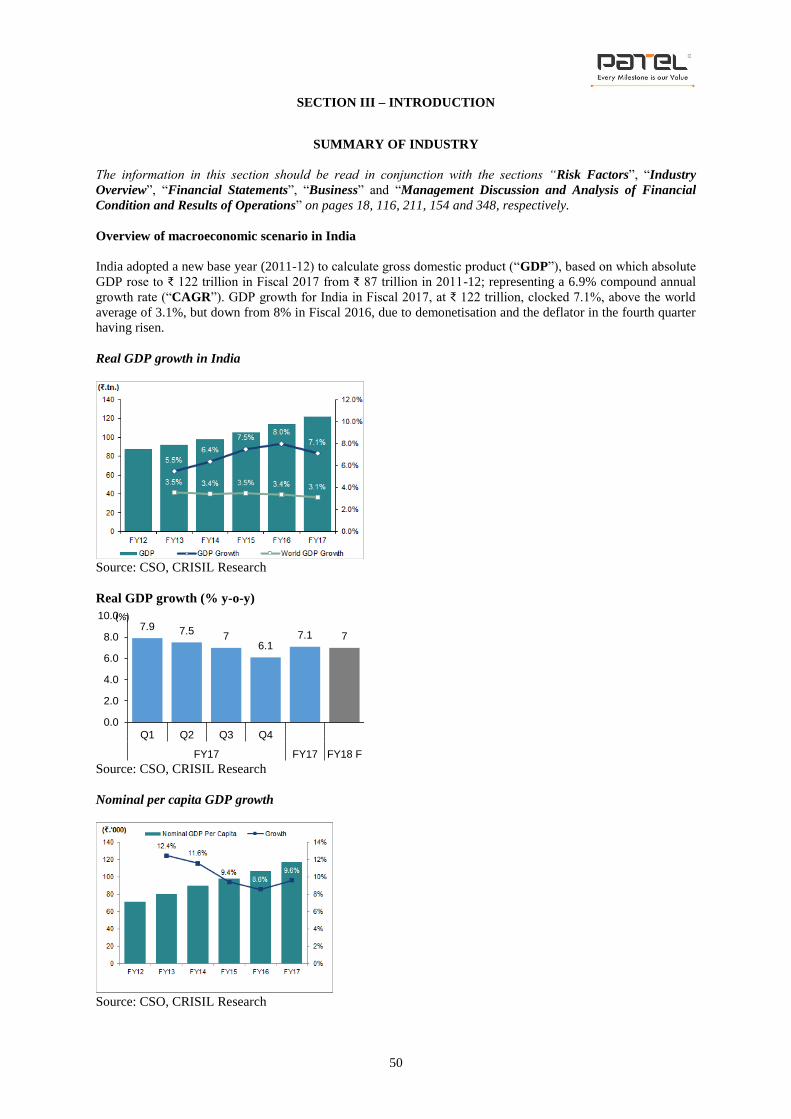

SECTION III – INTRODUCTION ................................................................................................................... 50

SUMMARY OF INDUSTRY ........................................................................................................................ 50 SUMMARY OF BUSINESS ......................................................................................................................... 64 SUMMARY FINANCIAL INFORMATION .............................................................................................. 71 THE ISSUE .................................................................................................................................................... 78 GENERAL INFORMATION ....................................................................................................................... 79 CAPITAL STRUCTURE .............................................................................................................................. 87 OBJECTS OF THE ISSUE ........................................................................................................................... 96 BASIS FOR ISSUE PRICE ........................................................................................................................ 108 STATEMENT OF TAX BENEFITS .......................................................................................................... 112

SECTION IV: ABOUT THE COMPANY ..................................................................................................... 116

INDUSTRY OVERVIEW ........................................................................................................................... 116 BUSINESS .................................................................................................................................................... 154 KEY REGULATIONS AND POLICIES IN INDIA................................................................................. 175 HISTORY AND CERTAIN CORPORATE MATTERS ......................................................................... 179 MANAGEMENT ......................................................................................................................................... 187 PROMOTERS AND GROUP COMPANY ............................................................................................... 203 DIVIDEND POLICY ................................................................................................................................... 209 RELATED PARTY TRANSACTIONS ..................................................................................................... 210

SECTION V – FINANCIAL INFORMATION ............................................................................................. 211

FINANCIAL STATEMENTS..................................................................................................................... 211 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS

OF OPERATIONS ...................................................................................................................................... 348 SUMMARY OF SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IND (AS) ........ 370 FINANCIAL INDEBTEDNESS ................................................................................................................. 375

SECTION VI – LEGAL AND OTHER INFORMATION ........................................................................... 379

OUTSTANDING LITIGATION AND OTHER MATERIAL DEVELOPMENTS .............................. 379 GOVERNMENT AND OTHER APPROVALS ........................................................................................ 385 OTHER REGULATORY AND STATUTORY DISCLOSURES ........................................................... 388

SECTION VII – ISSUE RELATED INFORMATION ................................................................................. 403

ISSUE STRUCTURE .................................................................................................................................. 403 TERMS OF THE ISSUE ............................................................................................................................. 407 ISSUE PROCEDURE.................................................................................................................................. 410

SECTION VIII – MAIN PROVISIONS OF ARTICLES OF ASSOCIATION .......................................... 456

SECTION IX – OTHER INFORMATION .................................................................................................... 473

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ................................................ 473 DECLARATION ......................................................................................................................................... 474

1

SECTION I - GENERAL

DEFINITIONS AND ABBREVIATIONS

Unless the context otherwise indicates or implies, the following terms shall have the meanings provided below in

this Draft Red Herring Prospectus, and references to any statute, legislation, act, rules, regulations, guidelines,

policies, circulars, notifications or clarifications will include any amendments or re-enactments thereto, from time

to time. In case of any inconsistency between the definitions given below and the definitions contained in the

General Information Document (as defined below), the definitions given below shall prevail.

The words and expressions used but not defined in this Draft Red Herring Prospectus will have the same meaning

as assigned to such terms under the Companies Act, 2013 (together the “Companies Act, 2013”), the Securities

and Exchange Board of India Act, 1992 (“SEBI Act”), the SEBI ICDR Regulations, the SCRA, the Depositories

Act and the rules and regulations made thereunder.

Unless the context otherwise indicates, all references to “the Company”, “our Company” or “the Issuer” are

references to Patel Infrastructure Limited, a company incorporated in India under the Companies Act, 1956 with

its registered and corporate office situated at “Patel House”, beside Prakruti Resort, Chhani Road, Chhani,

Vadodara 391740, Gujarat, India and references to “we”, “us” and “our” are references to our Company,

together with its Subsidiaries, Associates and Joint Ventures (as defined below).

Company Related Terms

Term Description

AoA/ Articles of

Association/ Articles

The articles of association of our Company, as amended

Audit Committee The audit committee of our Board, as disclosed in “Management” on page 187

Auditors/ Statutory

Auditors

The statutory auditor of our Company, being M/s Surana Maloo & Co., Chartered

Accountant

Board/ Board of Directors The board of directors of our Company, or a duly constituted committee thereof

Chairman The chairman of our Board

Compliance Officer Compliance officer of our Company appointed in terms of the SEBI ICDR

Regulations

CSR Committee The corporate social responsibility committee of our Board, as disclosed in

“Management” on page 187

Director(s) The director(s) on our Board

Equity Shares The equity shares of our Company of face value of ₹ 10 each

Equity Shareholders/

Shareholders

The holders of the Equity Shares

Group Company The group company of our Company as described in “Promoters and Group

Company” on page 203, which have been identified based on the policy adopted

by our Board pursuant to which a group company is any company which is covered

under the Accounting Standard 18 issued by the Institute of Chartered Accountants

of India (“AS 18”) as per the restated consolidated financial information as of and

for the Fiscals ended March 31, 2013, 2014, 2015, 2016, 2017 and the six months

ended September 30, 2017, and any other company as considered material by our

Board

KMP/ Key Management

Personnel

Key management personnel of our Company in terms of Regulation 2(1)(s) of the

SEBI ICDR Regulations and Section 2(51) of the Companies Act, 2013, as disclosed

in “Management” on page 187

Materiality Policy The policy adopted by our Board on December 16, 2017 for identification of group

companies of our Company, outstanding litigation and outstanding dues to

creditors in respect of our Company, pursuant to the disclosure requirements under

the SEBI ICDR Regulations

MoA/ Memorandum

of Association

The memorandum of association of our Company, as amended

Nomination and

Remuneration Committee

The nomination and remuneration committee of our Board, as disclosed in

“Management” on page 187

Order Book Our Company’s order book as of a particular date comprising the estimated revenues

from the unexecuted portions of all our ongoing projects i.e. the total contract value

2

of such ongoing projects secured by us as reduced by the value of work billed until

the date of such order book

PBNPL Patel Bridge Nirman Private Limited

PCTHPL Patel Cholopuram-Thanjavur Highway Private Limited

PDJHPL Patel Darah-Jhalawar Highway Private Limited

PHMPL Patel Highway Management Private Limited

PHPL Patel Hospitality Private Limited

PSCHPL Patel Sethiyahopu-Cholopuram Highway Private Limited

Promoters The promoters of our Company, namely Mr. Pravinbhai Vithalbhai Patel, Mr.

Arvind Vithalbhai Patel, Mr. Dineshbhai Pragjibhai Vaviya, Mr. Madhubhai

Pragjibhai Vaviya and Mr. Sureshbhai Pragjibhai Vaviya

Promoter Group Persons and entities constituting the promoter group of our Company, pursuant to

Regulation 2(1)(zb) of the SEBI ICDR Regulations

Registered and Corporate

Office

The registered and corporate office of our Company, situated at “Patel House”,

beside Prakruti Resort, Chhani Road, Chhani, Vadodara 391740, Gujarat, India

Restated Consolidated

Financial Information

Restated consolidated statement of assets and liabilities as at March 31, 2013,

2014, 2015, 2016, 2017 and the six months ended September 30, 2017 and restated

consolidated statement of profit and loss and restated consolidated statement of

cash flows for each of the Fiscals ended March 31, 2013, 2014, 2015, 2016, 2017

and the six months ended September 30, 2017 of our Company, its subsidiaries,

associates and joint ventures, as applicable during the relevant periods, read along

with all the schedules, annexures and notes thereto, which have been prepared in

accordance with the requirements of the Companies Act, 2013 and Indian GAAP

and restated in accordance with the SEBI ICDR Regulations and included in

“Financial Statements” on page 211

Restated Financial

Information

Collectively, the Restated Consolidated Financial Information and Restated

Standalone Financial Information

Restated Standalone

Financial Information

Restated standalone statement of financial information as at March 31, 2013, 2014,

2015, 2016, 2017 and the six months ended September 30, 2017 and restated

standalone statement of profit and loss and restated standalone statement of cash

flows for each of Fiscals ended March 31, 2013, 2014, 2015, 2016, 2017 and the

six months ended September 30, 2017 of our Company read along with all the

schedules, annexures and notes thereto, which have been prepared in accordance

with the requirements of the Companies Act, 2013 and Indian GAAP and restated

in accordance with the SEBI ICDR Regulations and included in “Financial

Statements” on page 211

Stakeholders’

Relationship Committee

The stakeholders’ relationship committee of our Board, as disclosed in

“Management” on page 187

Subsidiary or Subsidiaries A subsidiary of our Company as of the date of this DRHP, in accordance with the

Companies Act, 2013, namely, PHMPL, PBNPL, PHPL, PCTHPL, PSCHPL and

PDJHPL

Issue Related Terms

Term Description

Acknowledgment Slip The slip or document issued by the Designated Intermediary(ies) to a Bidder as proof

of registration of the Bid cum Application Form

Allotted/Allotment/Allot Unless the context otherwise requires, the issue and allotment of the Equity Shares to

successful Bidders pursuant to the Issue

Allottee A successful Bidder to whom the Equity Shares are Allotted

Allotment Advice The note or advice or intimation of Allotment, sent to each successful Bidder who has

been or is to be Allotted the Equity Shares after approval of the Basis of Allotment

by the Designated Stock Exchange

Anchor Investor A QIB, who applies under the Anchor Investor Portion in accordance with the

requirements specified in the SEBI ICDR Regulations and the Red Herring

Prospectus

Anchor Investor

Allocation Price

The final price at which the Equity Shares will be allocated to Anchor Investors in

terms of the Red Herring Prospectus and the Prospectus, which will be a price equal

to or higher than the Issue Price but not higher than the Cap Price. The Anchor

3

Term Description

Allocation Issue Price will be decided by our Company, in consultation with the

BRLMs

Anchor Investor

Application Form

An application form, whether physical or electronic, used by Anchor Investors,

which will be considered as the application for Allotment in terms of the Red

Herring Prospectus and the Prospectus

Anchor Investor Bidding

Date

The date one Working Day prior to the Bid/Issue Opening Date on which Bids by

Anchor Investors shall be submitted and allocation to the Anchor Investors shall be

completed

Anchor Investor Issue

Price

The final price at which the Equity Shares will be Allotted to Anchor Investors in

terms of the Red Herring Prospectus and the Prospectus, which will be a price equal

to or higher than the Issue Price but not higher than the Cap Price. The Anchor

Investor Issue Price will be decided by our Company, in consultation with the

BRLMs

Anchor Investor Pay-in

Date

With respect to Anchor Investor(s), it shall be the Anchor Investor Bidding Date,

and in the event the Anchor Investor Allocation Price is lower than the Issue Price,

not later than two Working Days after the Bid/ Issue Closing Date

Anchor Investor Portion Up to 60% of the QIB Category, which may be allocated by our Company, in

consultation with the BRLMs, to Anchor Investors, on a discretionary basis, in

accordance with SEBI ICDR Regulations. One-third of the Anchor Investor Portion

shall be reserved for domestic Mutual Funds, subject to valid Bids being received

from domestic Mutual Funds at or above the Anchor Investor Allocation Price

Application Supported by

Blocked Amount/ ASBA

The application (whether physical or electronic) by an ASBA Bidder to make a Bid

authorizing the relevant SCSB to block the Bid Amount in the relevant ASBA

Account

ASBA Account A bank account maintained with an SCSB and specified in the ASBA Form which

will be blocked by such SCSB to the extent of the appropriate Bid Amount in

relation to a Bid by an ASBA Bidder

ASBA Bidder All Bidders other than Anchor Investors

ASBA Form An application form, whether physical or electronic, used by Bidders bidding

through the ASBA process, which will be considered as the application for

Allotment in terms of the Red Herring Prospectus and the Prospectus

Banker(s) to the Issue The Escrow Collection Bank, the Refund Bank and the Public Issue Account Bank,

collectively

Basis of Allotment The basis on which the Equity Shares will be Allotted to successful Bidders under the

Issue, as described in “Issue Procedure” on page 410

Bid(s) An indication to make an offer during the Bid/Issue Period by a Bidder (other than an

Anchor Investor), or on the Anchor Investor Bidding Date by an Anchor Investor,

pursuant to submission of a Bid cum Application Form, to subscribe for or purchase

our Equity Shares at a price within the Price Band, including all revisions and

modifications thereto, to the extent permissible under the SEBI ICDR Regulations, in

terms of the Red Herring Prospectus and the Bid cum Application Form

Bid Amount The highest value of the optional Bids as indicated in the ASBA Form and payable

by the Bidder or as blocked in the ASBA Account of the Bidder, as the case may

be, upon submission of the Bid in the Issue

Bid cum Application Form The form in terms of which the Bidder shall make a Bid, including ASBA Form, and

which shall be considered as the application for the Allotment pursuant to the terms

of the Red Herring Prospectus and the Prospectus

Bid Lot [●] Equity Shares

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red Herring

Prospectus and the Bid cum Application Form and unless otherwise stated or implied,

includes an Anchor Investor

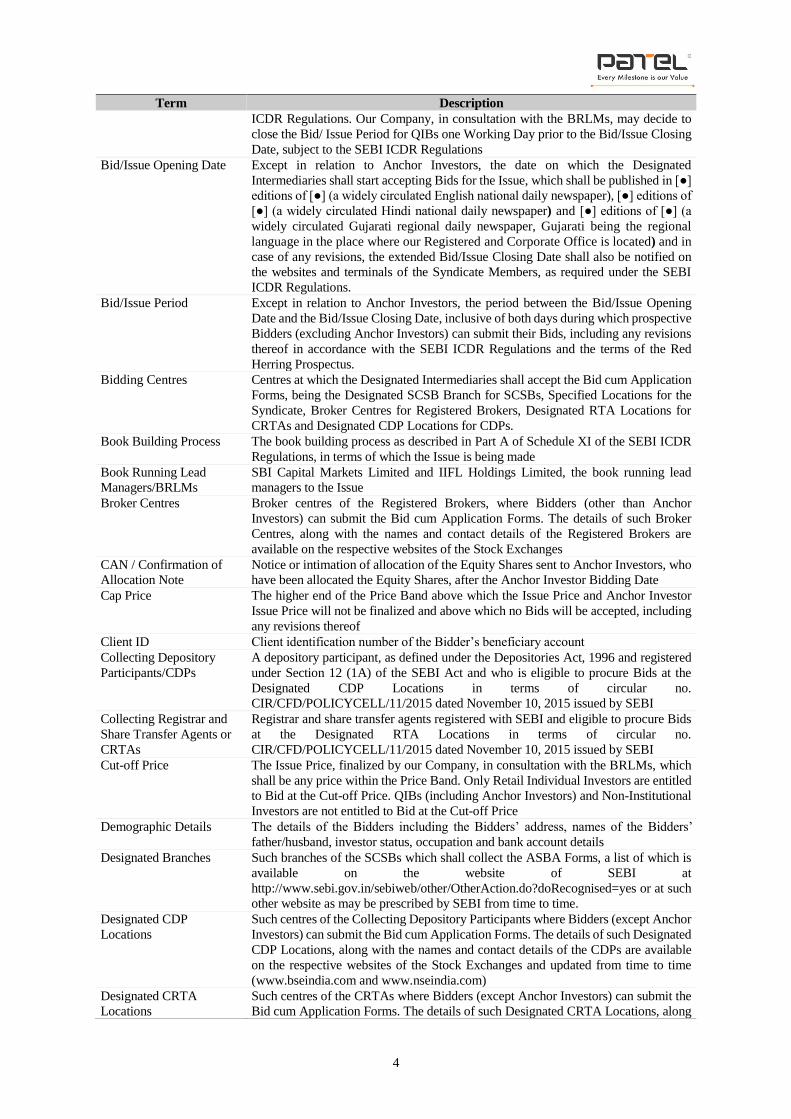

Bid/Issue Closing Date Except in relation to Anchor Investors, the date after which the Designated

Intermediaries shall not accept any Bids for the Issue, which shall be published in [●]

editions of [●] (a widely circulated English national daily newspaper), [●] editions of

[●] (a widely circulated Hindi national daily newspaper) and [●] editions of [●] (a

widely circulated Gujarati regional daily newspaper, Gujarati being the regional

language in the place where our Registered and Corporate Office is located) and in

case of any revisions, the extended Bid/Issue Closing Date shall also be notified on

the websites and terminals of the Syndicate Members, as required under the SEBI

4

Term Description

ICDR Regulations. Our Company, in consultation with the BRLMs, may decide to

close the Bid/ Issue Period for QIBs one Working Day prior to the Bid/Issue Closing

Date, subject to the SEBI ICDR Regulations

Bid/Issue Opening Date Except in relation to Anchor Investors, the date on which the Designated

Intermediaries shall start accepting Bids for the Issue, which shall be published in [●]

editions of [●] (a widely circulated English national daily newspaper), [●] editions of

[●] (a widely circulated Hindi national daily newspaper) and [●] editions of [●] (a

widely circulated Gujarati regional daily newspaper, Gujarati being the regional

language in the place where our Registered and Corporate Office is located) and in

case of any revisions, the extended Bid/Issue Closing Date shall also be notified on

the websites and terminals of the Syndicate Members, as required under the SEBI

ICDR Regulations.

Bid/Issue Period Except in relation to Anchor Investors, the period between the Bid/Issue Opening

Date and the Bid/Issue Closing Date, inclusive of both days during which prospective

Bidders (excluding Anchor Investors) can submit their Bids, including any revisions

thereof in accordance with the SEBI ICDR Regulations and the terms of the Red

Herring Prospectus.

Bidding Centres Centres at which the Designated Intermediaries shall accept the Bid cum Application

Forms, being the Designated SCSB Branch for SCSBs, Specified Locations for the

Syndicate, Broker Centres for Registered Brokers, Designated RTA Locations for

CRTAs and Designated CDP Locations for CDPs.

Book Building Process The book building process as described in Part A of Schedule XI of the SEBI ICDR

Regulations, in terms of which the Issue is being made

Book Running Lead

Managers/BRLMs

SBI Capital Markets Limited and IIFL Holdings Limited, the book running lead

managers to the Issue

Broker Centres Broker centres of the Registered Brokers, where Bidders (other than Anchor

Investors) can submit the Bid cum Application Forms. The details of such Broker

Centres, along with the names and contact details of the Registered Brokers are

available on the respective websites of the Stock Exchanges

CAN / Confirmation of

Allocation Note

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who

have been allocated the Equity Shares, after the Anchor Investor Bidding Date

Cap Price The higher end of the Price Band above which the Issue Price and Anchor Investor

Issue Price will not be finalized and above which no Bids will be accepted, including

any revisions thereof

Client ID Client identification number of the Bidder’s beneficiary account

Collecting Depository

Participants/CDPs

A depository participant, as defined under the Depositories Act, 1996 and registered

under Section 12 (1A) of the SEBI Act and who is eligible to procure Bids at the

Designated CDP Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Collecting Registrar and

Share Transfer Agents or

CRTAs

Registrar and share transfer agents registered with SEBI and eligible to procure Bids

at the Designated RTA Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Cut-off Price The Issue Price, finalized by our Company, in consultation with the BRLMs, which

shall be any price within the Price Band. Only Retail Individual Investors are entitled

to Bid at the Cut-off Price. QIBs (including Anchor Investors) and Non-Institutional

Investors are not entitled to Bid at the Cut-off Price

Demographic Details The details of the Bidders including the Bidders’ address, names of the Bidders’

father/husband, investor status, occupation and bank account details

Designated Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which is

available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes or at such

other website as may be prescribed by SEBI from time to time.

Designated CDP

Locations

Such centres of the Collecting Depository Participants where Bidders (except Anchor

Investors) can submit the Bid cum Application Forms. The details of such Designated

CDP Locations, along with the names and contact details of the CDPs are available

on the respective websites of the Stock Exchanges and updated from time to time

(www.bseindia.com and www.nseindia.com)

Designated CRTA

Locations

Such centres of the CRTAs where Bidders (except Anchor Investors) can submit the

Bid cum Application Forms. The details of such Designated CRTA Locations, along

5

Term Description

with the names and contact details of the CRTAs are available on the respective

websites of the Stock Exchanges (www.nseindia.com and www.bseindia.com) and

updated from time to time

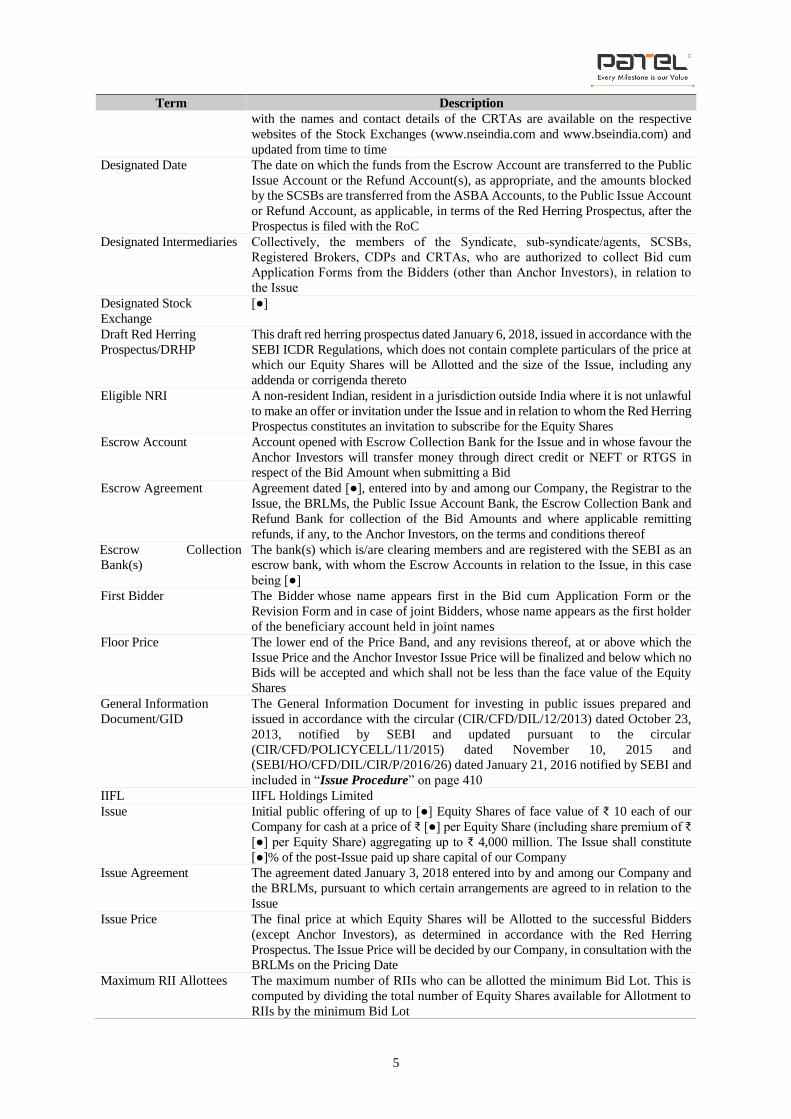

Designated Date The date on which the funds from the Escrow Account are transferred to the Public

Issue Account or the Refund Account(s), as appropriate, and the amounts blocked

by the SCSBs are transferred from the ASBA Accounts, to the Public Issue Account

or Refund Account, as applicable, in terms of the Red Herring Prospectus, after the

Prospectus is filed with the RoC

Designated Intermediaries Collectively, the members of the Syndicate, sub-syndicate/agents, SCSBs,

Registered Brokers, CDPs and CRTAs, who are authorized to collect Bid cum

Application Forms from the Bidders (other than Anchor Investors), in relation to

the Issue

Designated Stock

Exchange

[●]

Draft Red Herring

Prospectus/DRHP

This draft red herring prospectus dated January 6, 2018, issued in accordance with the

SEBI ICDR Regulations, which does not contain complete particulars of the price at

which our Equity Shares will be Allotted and the size of the Issue, including any

addenda or corrigenda thereto

Eligible NRI A non-resident Indian, resident in a jurisdiction outside India where it is not unlawful

to make an offer or invitation under the Issue and in relation to whom the Red Herring

Prospectus constitutes an invitation to subscribe for the Equity Shares

Escrow Account Account opened with Escrow Collection Bank for the Issue and in whose favour the

Anchor Investors will transfer money through direct credit or NEFT or RTGS in

respect of the Bid Amount when submitting a Bid

Escrow Agreement Agreement dated [●], entered into by and among our Company, the Registrar to the

Issue, the BRLMs, the Public Issue Account Bank, the Escrow Collection Bank and

Refund Bank for collection of the Bid Amounts and where applicable remitting

refunds, if any, to the Anchor Investors, on the terms and conditions thereof

Escrow Collection

Bank(s)

The bank(s) which is/are clearing members and are registered with the SEBI as an

escrow bank, with whom the Escrow Accounts in relation to the Issue, in this case

being [●]

First Bidder The Bidder whose name appears first in the Bid cum Application Form or the

Revision Form and in case of joint Bidders, whose name appears as the first holder

of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, and any revisions thereof, at or above which the

Issue Price and the Anchor Investor Issue Price will be finalized and below which no

Bids will be accepted and which shall not be less than the face value of the Equity

Shares

General Information

Document/GID

The General Information Document for investing in public issues prepared and

issued in accordance with the circular (CIR/CFD/DIL/12/2013) dated October 23,

2013, notified by SEBI and updated pursuant to the circular

(CIR/CFD/POLICYCELL/11/2015) dated November 10, 2015 and

(SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January 21, 2016 notified by SEBI and

included in “Issue Procedure” on page 410

IIFL IIFL Holdings Limited

Issue Initial public offering of up to [●] Equity Shares of face value of ₹ 10 each of our

Company for cash at a price of ₹ [●] per Equity Share (including share premium of ₹

[●] per Equity Share) aggregating up to ₹ 4,000 million. The Issue shall constitute

[●]% of the post-Issue paid up share capital of our Company

Issue Agreement The agreement dated January 3, 2018 entered into by and among our Company and

the BRLMs, pursuant to which certain arrangements are agreed to in relation to the

Issue

Issue Price The final price at which Equity Shares will be Allotted to the successful Bidders

(except Anchor Investors), as determined in accordance with the Red Herring

Prospectus. The Issue Price will be decided by our Company, in consultation with the

BRLMs on the Pricing Date

Maximum RII Allottees The maximum number of RIIs who can be allotted the minimum Bid Lot. This is

computed by dividing the total number of Equity Shares available for Allotment to

RIIs by the minimum Bid Lot

6

Term Description

Monitoring Agency [●]

Monitoring Agency

Agreement

Agreement dated [●], 2018 entered into by and between our Company and the

Monitoring Agency

Mutual Fund Portion 5% of the QIB Category (excluding the Anchor Investor Portion) or [●] Equity Shares

which shall be available for allocation to Mutual Funds only, on a proportionate basis,

subject to valid Bids being received at or above the Issue Price

Net Proceeds Proceeds of the Issue that will be available to our Company, i.e., gross proceeds of

the Issue, less Issue Expenses to the extent applicable to the Issue

Non-Institutional Category The portion of the Issue, being not less than 15% of the Issue or [●] Equity Shares,

available for allocation on a proportionate basis to Non-Institutional Investors subject

to valid Bids being received at or above the Issue Price

Non-Institutional

Investors/NIIs

All Bidders, including Category III FPIs that are not QIBs (including Anchor

Investors) or Retail Individual Investors, who have Bid for Equity Shares for an

amount of more than ₹ 200,000 (but not including NRIs other than Eligible NRIs)

Price Band Price band of the Floor Price of ₹ [●] and a Cap Price of ₹ [●], including any revisions

thereof. The Price Band and the minimum Bid Lot size for the Issue will be decided

by our Company, in consultation with the BRLMs, and advertised in [●] editions of

[●] (a widely circulated English national daily newspaper), [●] editions of [●] (a

widely circulated Hindi national daily newspaper) and [●] editions of [●] (a widely

circulated Gujarati regional daily newspaper, Gujarati being the regional language in

the place where our Registered and Corporate is located) at least five Working Days

prior to the Bid/Issue Opening Date, with the relevant financial ratios calculated at

the Floor Price and at the Cap Price and shall be made available to the Stock

Exchanges for the purpose of uploading on their websites

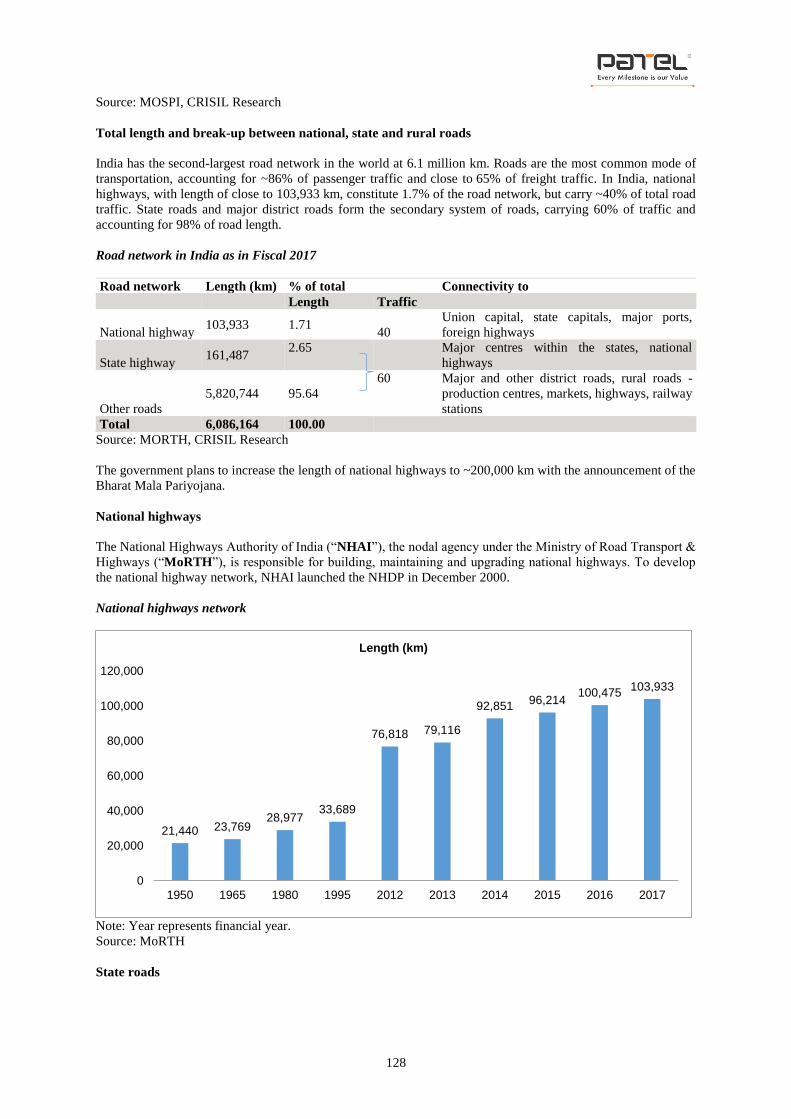

Pricing Date The date on which our Company, in consultation with the BRLMs, shall finalize the

Issue Price

Prospectus The Prospectus to be filed with the RoC for this Issue on or after the Pricing Date in

accordance with the provisions of Section 26 of the Companies Act 2013 and the

SEBI ICDR Regulations, containing the Issue Price, the size of the Issue and certain

other information, including any addenda or corrigenda thereto

Public Issue Account(s) The account(s) to be opened with the Banker(s) to the Issue under Section 40(3) of

the Companies Act 2013 to receive monies from the Escrow Account(s) and the

ASBA Accounts on the Designated Date

Public Issue Account

Bank

The bank(s), with whom the Public Issue Accounts in relation to the Issue, in this

case being [●]

QIB Category The portion of the Issue, being 50% of the Issue or [●] Equity Shares to be Allotted

to QIBs on a proportionate basis, including the Anchor Investor Portion (in which

allocation shall be on a discretionary basis, as determined by our Company, in

consultation with the BRLMs), subject to valid Bids being received at or above the

Issue Price

Qualified Institutional

Buyers or QIBs

A qualified institutional buyer as defined under Regulation 2(1)(zd) of the SEBI

ICDR Regulations

Red Herring Prospectus or

RHP

The red herring prospectus to be issued in accordance with Section 32 of the

Companies Act 2013 and the SEBI ICDR Regulations, which will not have complete

particulars of the price at which the Equity Shares shall be Allotted and which shall

be registered with the RoC at least three Working Days before the Bid/Issue

Opening Date and will become the Prospectus after filing with the RoC after the

Pricing Date, including any addenda or corrigenda thereto

Refund Account(s) Account(s) opened with the Refund Bank from which refunds, if any, of the whole or

part of the Bid Amount shall be made to Anchor Investors

Refund Bank(s) The Bankers to the Issue with whom the Refund Account(s) will be opened, in this

case being [●]

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other

than the members of the Syndicate and eligible to procure Bids in terms of circular

number CIR/CFD/14/2012 dated October 14, 2012, issued by SEBI

Registrar Agreement The agreement dated January 3, 2018, entered into by and among our Company and

the Registrar to the Issue in relation to the responsibilities and obligations of the

Registrar to the Issue pertaining to the Issue

7

Term Description

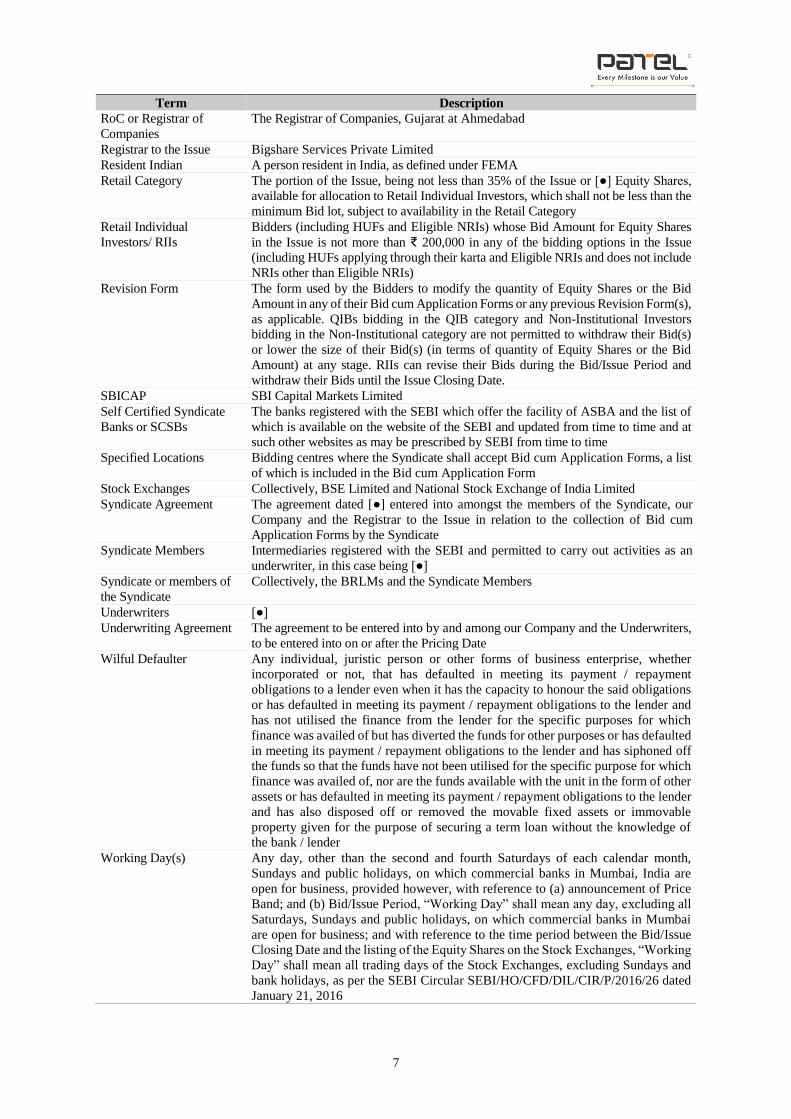

RoC or Registrar of

Companies

The Registrar of Companies, Gujarat at Ahmedabad

Registrar to the Issue Bigshare Services Private Limited

Resident Indian A person resident in India, as defined under FEMA

Retail Category The portion of the Issue, being not less than 35% of the Issue or [●] Equity Shares,

available for allocation to Retail Individual Investors, which shall not be less than the

minimum Bid lot, subject to availability in the Retail Category

Retail Individual

Investors/ RIIs

Bidders (including HUFs and Eligible NRIs) whose Bid Amount for Equity Shares

in the Issue is not more than ₹ 200,000 in any of the bidding options in the Issue

(including HUFs applying through their karta and Eligible NRIs and does not include

NRIs other than Eligible NRIs)

Revision Form The form used by the Bidders to modify the quantity of Equity Shares or the Bid

Amount in any of their Bid cum Application Forms or any previous Revision Form(s),

as applicable. QIBs bidding in the QIB category and Non-Institutional Investors

bidding in the Non-Institutional category are not permitted to withdraw their Bid(s)

or lower the size of their Bid(s) (in terms of quantity of Equity Shares or the Bid

Amount) at any stage. RIIs can revise their Bids during the Bid/Issue Period and

withdraw their Bids until the Issue Closing Date.

SBICAP SBI Capital Markets Limited

Self Certified Syndicate

Banks or SCSBs

The banks registered with the SEBI which offer the facility of ASBA and the list of

which is available on the website of the SEBI and updated from time to time and at

such other websites as may be prescribed by SEBI from time to time

Specified Locations Bidding centres where the Syndicate shall accept Bid cum Application Forms, a list

of which is included in the Bid cum Application Form

Stock Exchanges Collectively, BSE Limited and National Stock Exchange of India Limited

Syndicate Agreement The agreement dated [●] entered into amongst the members of the Syndicate, our

Company and the Registrar to the Issue in relation to the collection of Bid cum

Application Forms by the Syndicate

Syndicate Members Intermediaries registered with the SEBI and permitted to carry out activities as an

underwriter, in this case being [●]

Syndicate or members of

the Syndicate

Collectively, the BRLMs and the Syndicate Members

Underwriters [●]

Underwriting Agreement The agreement to be entered into by and among our Company and the Underwriters,

to be entered into on or after the Pricing Date

Wilful Defaulter Any individual, juristic person or other forms of business enterprise, whether

incorporated or not, that has defaulted in meeting its payment / repayment

obligations to a lender even when it has the capacity to honour the said obligations

or has defaulted in meeting its payment / repayment obligations to the lender and

has not utilised the finance from the lender for the specific purposes for which

finance was availed of but has diverted the funds for other purposes or has defaulted

in meeting its payment / repayment obligations to the lender and has siphoned off

the funds so that the funds have not been utilised for the specific purpose for which

finance was availed of, nor are the funds available with the unit in the form of other

assets or has defaulted in meeting its payment / repayment obligations to the lender

and has also disposed off or removed the movable fixed assets or immovable

property given for the purpose of securing a term loan without the knowledge of

the bank / lender

Working Day(s) Any day, other than the second and fourth Saturdays of each calendar month,

Sundays and public holidays, on which commercial banks in Mumbai, India are

open for business, provided however, with reference to (a) announcement of Price

Band; and (b) Bid/Issue Period, “Working Day” shall mean any day, excluding all

Saturdays, Sundays and public holidays, on which commercial banks in Mumbai

are open for business; and with reference to the time period between the Bid/Issue

Closing Date and the listing of the Equity Shares on the Stock Exchanges, “Working

Day” shall mean all trading days of the Stock Exchanges, excluding Sundays and

bank holidays, as per the SEBI Circular SEBI/HO/CFD/DIL/CIR/P/2016/26 dated

January 21, 2016

8

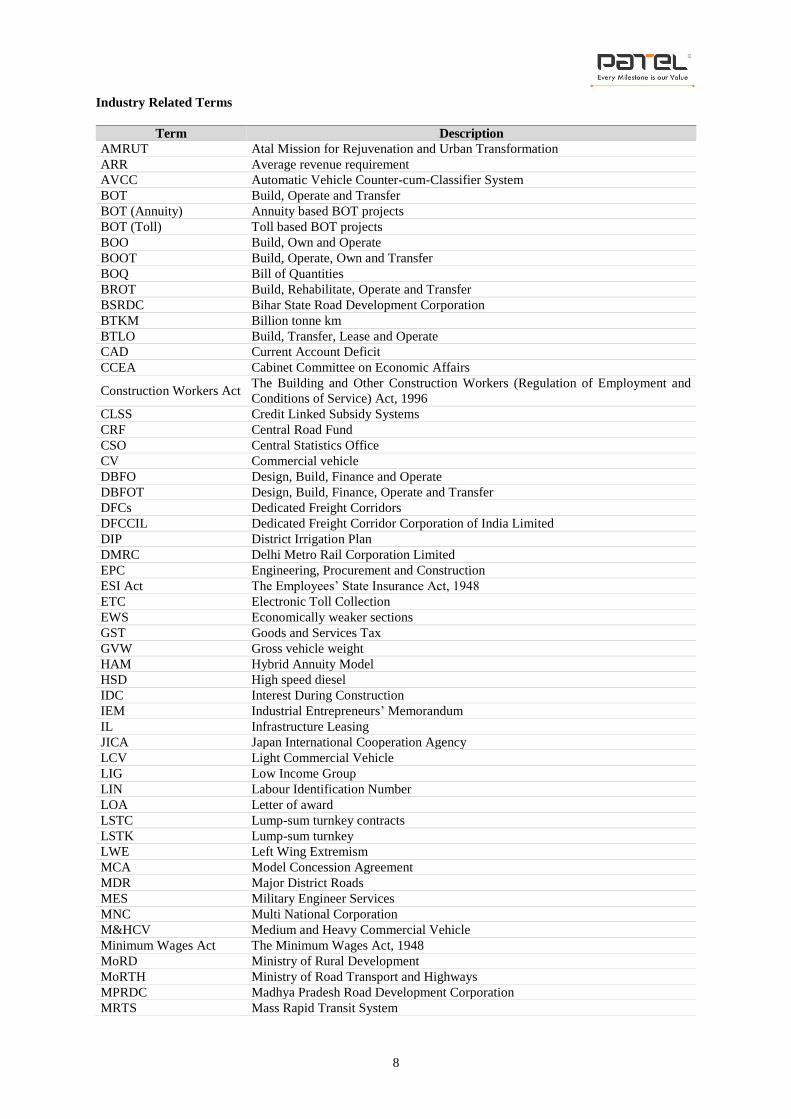

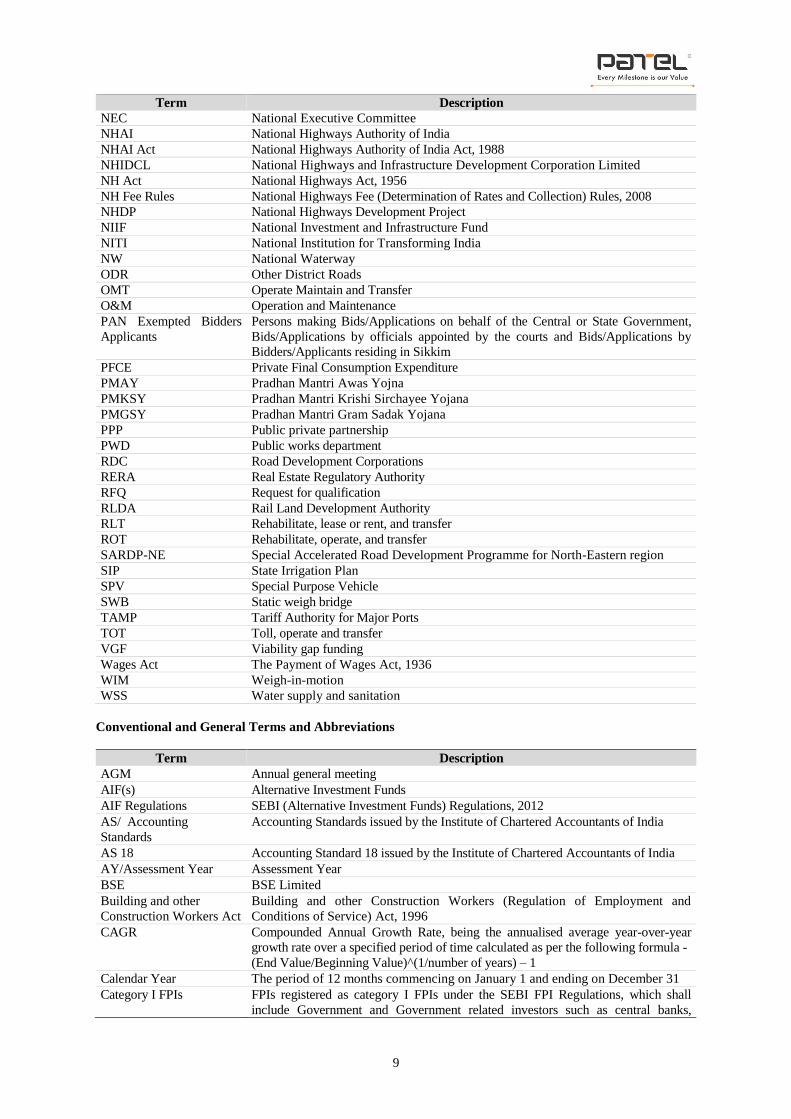

Industry Related Terms

Term Description

AMRUT Atal Mission for Rejuvenation and Urban Transformation

ARR Average revenue requirement

AVCC Automatic Vehicle Counter-cum-Classifier System

BOT Build, Operate and Transfer

BOT (Annuity) Annuity based BOT projects

BOT (Toll) Toll based BOT projects

BOO Build, Own and Operate

BOOT Build, Operate, Own and Transfer

BOQ Bill of Quantities

BROT Build, Rehabilitate, Operate and Transfer

BSRDC Bihar State Road Development Corporation

BTKM Billion tonne km

BTLO Build, Transfer, Lease and Operate

CAD Current Account Deficit

CCEA Cabinet Committee on Economic Affairs

Construction Workers Act The Building and Other Construction Workers (Regulation of Employment and

Conditions of Service) Act, 1996

CLSS Credit Linked Subsidy Systems

CRF Central Road Fund

CSO Central Statistics Office

CV Commercial vehicle

DBFO Design, Build, Finance and Operate

DBFOT Design, Build, Finance, Operate and Transfer

DFCs Dedicated Freight Corridors

DFCCIL Dedicated Freight Corridor Corporation of India Limited

DIP District Irrigation Plan

DMRC Delhi Metro Rail Corporation Limited

EPC Engineering, Procurement and Construction

ESI Act The Employees’ State Insurance Act, 1948

ETC Electronic Toll Collection

EWS Economically weaker sections

GST Goods and Services Tax

GVW Gross vehicle weight

HAM Hybrid Annuity Model

HSD High speed diesel

IDC Interest During Construction

IEM Industrial Entrepreneurs’ Memorandum

IL Infrastructure Leasing

JICA Japan International Cooperation Agency

LCV Light Commercial Vehicle

LIG Low Income Group

LIN Labour Identification Number

LOA Letter of award

LSTC Lump-sum turnkey contracts

LSTK Lump-sum turnkey

LWE Left Wing Extremism

MCA Model Concession Agreement

MDR Major District Roads

MES Military Engineer Services

MNC Multi National Corporation

M&HCV Medium and Heavy Commercial Vehicle

Minimum Wages Act The Minimum Wages Act, 1948

MoRD Ministry of Rural Development

MoRTH Ministry of Road Transport and Highways

MPRDC Madhya Pradesh Road Development Corporation

MRTS Mass Rapid Transit System

9

Term Description

NEC National Executive Committee

NHAI National Highways Authority of India

NHAI Act National Highways Authority of India Act, 1988

NHIDCL National Highways and Infrastructure Development Corporation Limited

NH Act National Highways Act, 1956

NH Fee Rules National Highways Fee (Determination of Rates and Collection) Rules, 2008

NHDP National Highways Development Project

NIIF National Investment and Infrastructure Fund

NITI National Institution for Transforming India

NW National Waterway

ODR Other District Roads

OMT Operate Maintain and Transfer

O&M Operation and Maintenance

PAN Exempted Bidders

Applicants

Persons making Bids/Applications on behalf of the Central or State Government,

Bids/Applications by officials appointed by the courts and Bids/Applications by

Bidders/Applicants residing in Sikkim

PFCE Private Final Consumption Expenditure

PMAY Pradhan Mantri Awas Yojna

PMKSY Pradhan Mantri Krishi Sirchayee Yojana

PMGSY Pradhan Mantri Gram Sadak Yojana

PPP Public private partnership

PWD Public works department

RDC Road Development Corporations

RERA Real Estate Regulatory Authority

RFQ Request for qualification

RLDA Rail Land Development Authority

RLT Rehabilitate, lease or rent, and transfer

ROT Rehabilitate, operate, and transfer

SARDP-NE Special Accelerated Road Development Programme for North-Eastern region

SIP State Irrigation Plan

SPV Special Purpose Vehicle

SWB Static weigh bridge

TAMP Tariff Authority for Major Ports

TOT Toll, operate and transfer

VGF Viability gap funding

Wages Act The Payment of Wages Act, 1936

WIM Weigh-in-motion

WSS Water supply and sanitation

Conventional and General Terms and Abbreviations

Term Description

AGM Annual general meeting

AIF(s) Alternative Investment Funds

AIF Regulations SEBI (Alternative Investment Funds) Regulations, 2012

AS/ Accounting

Standards

Accounting Standards issued by the Institute of Chartered Accountants of India

AS 18 Accounting Standard 18 issued by the Institute of Chartered Accountants of India

AY/Assessment Year Assessment Year

BSE BSE Limited

Building and other

Construction Workers Act

Building and other Construction Workers (Regulation of Employment and

Conditions of Service) Act, 1996

CAGR Compounded Annual Growth Rate, being the annualised average year-over-year

growth rate over a specified period of time calculated as per the following formula -

(End Value/Beginning Value)^(1/number of years) – 1

Calendar Year The period of 12 months commencing on January 1 and ending on December 31

Category I FPIs FPIs registered as category I FPIs under the SEBI FPI Regulations, which shall

include Government and Government related investors such as central banks,

10

Term Description

Governmental agencies, sovereign wealth funds and international or multilateral

organizations or agencies

Category II FPIs FPIs registered as category III FPIs under the SEBI FPI Regulations, which shall

include appropriately regulated broad based funds such as mutual funds, investment

trusts, insurance/reinsurance companies, appropriately regulated persons such as

banks, asset management companies, investment managers/ advisors, portfolio

managers, broad based funds that are not appropriately regulated but whose

investment manager is appropriately regulated: Provided that the investment manager

of such broad based fund is itself registered as Category II foreign portfolio investor,

university funds and pension funds and university related endowments already

registered

Category III FPIs FPIs registered as category III FPIs under the SEBI FPI Regulations, which shall

include all other FPIs not eligible under category I and II foreign portfolio investors,

such as endowments, charitable societies, charitable trusts, foundations, corporate

bodies, trusts, individuals and family offices

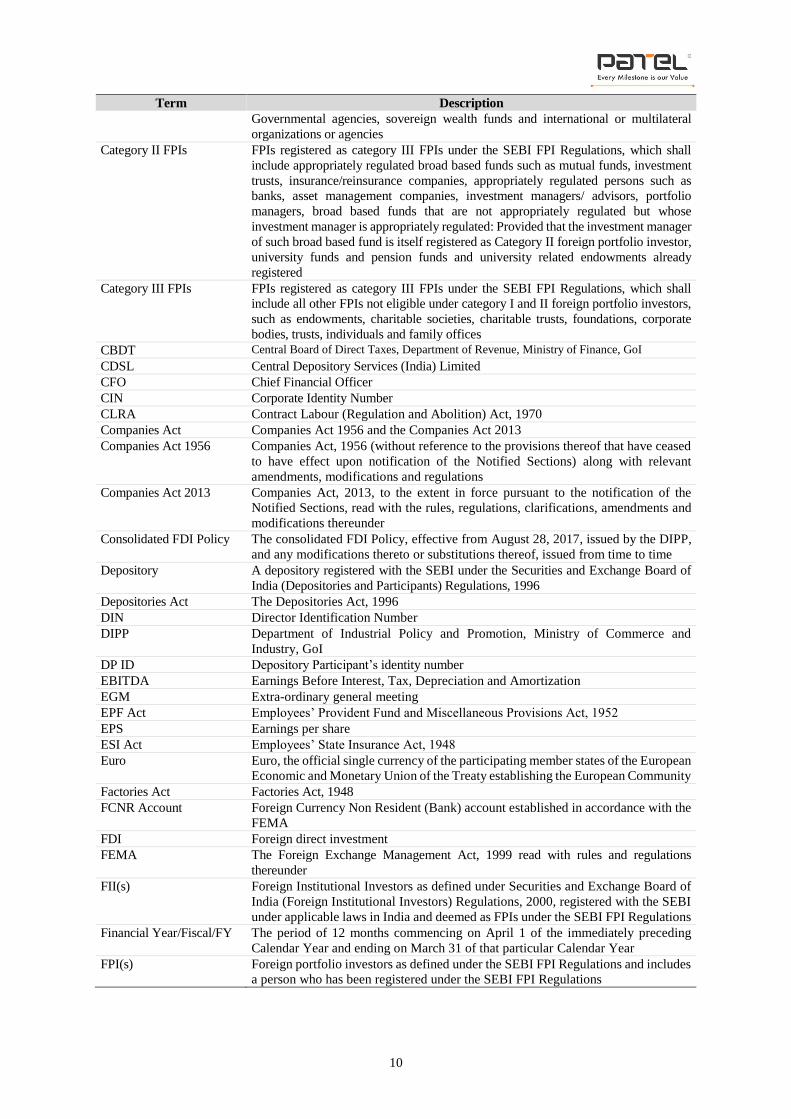

CBDT Central Board of Direct Taxes, Department of Revenue, Ministry of Finance, GoI

CDSL Central Depository Services (India) Limited

CFO Chief Financial Officer

CIN Corporate Identity Number

CLRA Contract Labour (Regulation and Abolition) Act, 1970

Companies Act Companies Act 1956 and the Companies Act 2013

Companies Act 1956 Companies Act, 1956 (without reference to the provisions thereof that have ceased

to have effect upon notification of the Notified Sections) along with relevant

amendments, modifications and regulations

Companies Act 2013 Companies Act, 2013, to the extent in force pursuant to the notification of the

Notified Sections, read with the rules, regulations, clarifications, amendments and

modifications thereunder

Consolidated FDI Policy The consolidated FDI Policy, effective from August 28, 2017, issued by the DIPP,

and any modifications thereto or substitutions thereof, issued from time to time

Depository A depository registered with the SEBI under the Securities and Exchange Board of

India (Depositories and Participants) Regulations, 1996

Depositories Act The Depositories Act, 1996

DIN Director Identification Number

DIPP Department of Industrial Policy and Promotion, Ministry of Commerce and

Industry, GoI

DP ID Depository Participant’s identity number

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization

EGM Extra-ordinary general meeting

EPF Act Employees’ Provident Fund and Miscellaneous Provisions Act, 1952

EPS Earnings per share

ESI Act Employees’ State Insurance Act, 1948

Euro Euro, the official single currency of the participating member states of the European

Economic and Monetary Union of the Treaty establishing the European Community

Factories Act Factories Act, 1948

FCNR Account Foreign Currency Non Resident (Bank) account established in accordance with the

FEMA

FDI Foreign direct investment

FEMA The Foreign Exchange Management Act, 1999 read with rules and regulations

thereunder

FII(s) Foreign Institutional Investors as defined under Securities and Exchange Board of

India (Foreign Institutional Investors) Regulations, 2000, registered with the SEBI

under applicable laws in India and deemed as FPIs under the SEBI FPI Regulations

Financial Year/Fiscal/FY The period of 12 months commencing on April 1 of the immediately preceding

Calendar Year and ending on March 31 of that particular Calendar Year

FPI(s) Foreign portfolio investors as defined under the SEBI FPI Regulations and includes

a person who has been registered under the SEBI FPI Regulations

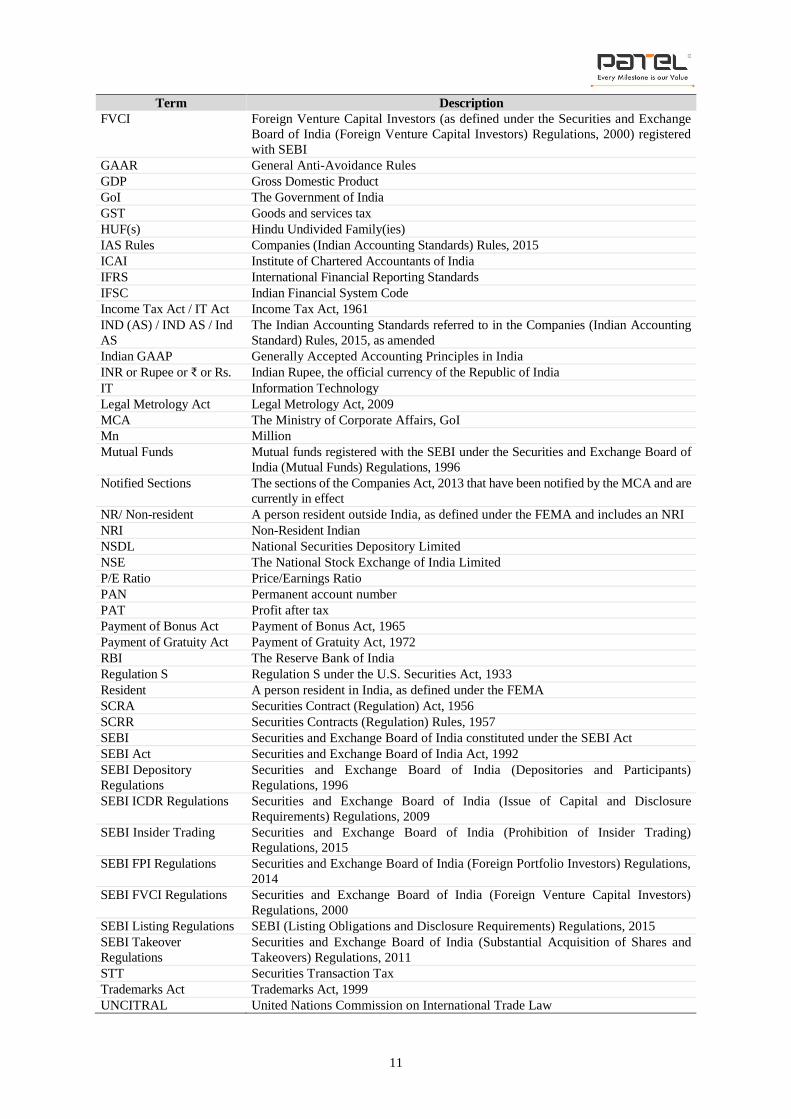

11

Term Description

FVCI Foreign Venture Capital Investors (as defined under the Securities and Exchange

Board of India (Foreign Venture Capital Investors) Regulations, 2000) registered

with SEBI

GAAR General Anti-Avoidance Rules

GDP Gross Domestic Product

GoI The Government of India

GST Goods and services tax

HUF(s) Hindu Undivided Family(ies)

IAS Rules Companies (Indian Accounting Standards) Rules, 2015

ICAI Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

IFSC Indian Financial System Code

Income Tax Act / IT Act Income Tax Act, 1961

IND (AS) / IND AS / Ind

AS

The Indian Accounting Standards referred to in the Companies (Indian Accounting

Standard) Rules, 2015, as amended

Indian GAAP Generally Accepted Accounting Principles in India

INR or Rupee or ₹ or Rs. Indian Rupee, the official currency of the Republic of India

IT Information Technology

Legal Metrology Act Legal Metrology Act, 2009

MCA The Ministry of Corporate Affairs, GoI

Mn Million

Mutual Funds Mutual funds registered with the SEBI under the Securities and Exchange Board of

India (Mutual Funds) Regulations, 1996

Notified Sections The sections of the Companies Act, 2013 that have been notified by the MCA and are

currently in effect

NR/ Non-resident A person resident outside India, as defined under the FEMA and includes an NRI

NRI Non-Resident Indian

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

P/E Ratio Price/Earnings Ratio

PAN Permanent account number

PAT Profit after tax

Payment of Bonus Act Payment of Bonus Act, 1965

Payment of Gratuity Act Payment of Gratuity Act, 1972

RBI The Reserve Bank of India

Regulation S Regulation S under the U.S. Securities Act, 1933

Resident A person resident in India, as defined under the FEMA

SCRA Securities Contract (Regulation) Act, 1956

SCRR Securities Contracts (Regulation) Rules, 1957

SEBI Securities and Exchange Board of India constituted under the SEBI Act

SEBI Act Securities and Exchange Board of India Act, 1992

SEBI Depository

Regulations

Securities and Exchange Board of India (Depositories and Participants)

Regulations, 1996

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009

SEBI Insider Trading Securities and Exchange Board of India (Prohibition of Insider Trading)

Regulations, 2015

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations,

2014

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investors)

Regulations, 2000

SEBI Listing Regulations SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015

SEBI Takeover

Regulations

Securities and Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulations, 2011

STT Securities Transaction Tax

Trademarks Act Trademarks Act, 1999

UNCITRAL United Nations Commission on International Trade Law

12

Term Description

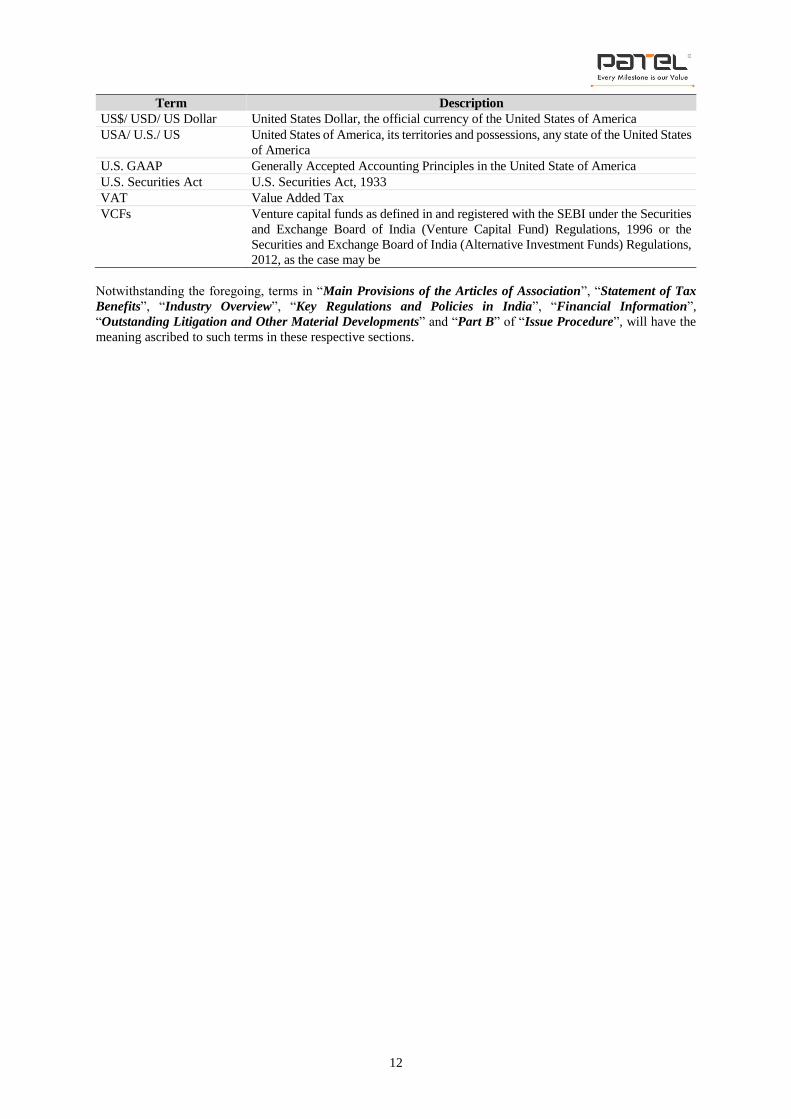

US$/ USD/ US Dollar United States Dollar, the official currency of the United States of America

USA/ U.S./ US United States of America, its territories and possessions, any state of the United States

of America

U.S. GAAP Generally Accepted Accounting Principles in the United State of America

U.S. Securities Act U.S. Securities Act, 1933

VAT Value Added Tax

VCFs Venture capital funds as defined in and registered with the SEBI under the Securities

and Exchange Board of India (Venture Capital Fund) Regulations, 1996 or the

Securities and Exchange Board of India (Alternative Investment Funds) Regulations,

2012, as the case may be

Notwithstanding the foregoing, terms in “Main Provisions of the Articles of Association”, “Statement of Tax

Benefits”, “Industry Overview”, “Key Regulations and Policies in India”, “Financial Information”,

“Outstanding Litigation and Other Material Developments” and “Part B” of “Issue Procedure”, will have the

meaning ascribed to such terms in these respective sections.

13

CERTAIN CONVENTIONS, USE OF FINANCIAL INFORMATION AND MARKET DATA AND

CURRENCY OF PRESENTATION

Certain Conventions

All references in this Draft Red Herring Prospectus to “India” are to the Republic of India.

Financial Data

Unless indicated otherwise, the financial data in this Draft Red Herring Prospectus is derived from our Restated

Standalone Financial Information as of and for the Fiscals ended March 31, 2013, 2014, 2015, 2016, 2017 and the

six months ended September 30, 2017 and our Restated Consolidated Financial Information and as of and for the

Fiscals ended March 31, 2013, 2014, 2015, 2016, 2017 and the six months ended September 30, 2017, and the

respective notes, schedules and annexures thereto, prepared in accordance with the Companies Act and restated

in accordance with the SEBI ICDR Regulations and included elsewhere in this Draft Red Herring Prospectus.

Our Company’s financial year commences on April 1 of the immediately preceding Calendar Year and ends on

March 31 of that particular Calendar Year, so all references to a particular financial year are to the 12 month

period commencing on April 1 of the immediately preceding Calendar Year and ending on March 31 of that

particular calendar year.

There are significant differences between the Indian GAAP, the International Financial Reporting Standards (the

“IFRS”) and the Generally Accepted Accounting Principles in the United States of America (the “U.S. GAAP”).

Accordingly, the degree to which the financial information included in this Draft Red Herring Prospectus will

provide meaningful information is entirely dependent on the reader’s level of familiarity with Indian accounting

practices. Any reliance by persons not familiar with Indian accounting practices, the Indian GAAP, the Companies

Act and the SEBI ICDR Regulations on the financial disclosures presented in this Draft Red Herring Prospectus

should accordingly be limited. We have not attempted to quantify the impact of the IFRS or the U.S. GAAP on

the financial data included in this Draft Red Herring Prospectus, nor do we provide a reconciliation of our financial

information to those under the U.S. GAAP or the IFRS and we urge you to consult your own advisors regarding

such differences and their impact on our financial data.

On February 16, 2015, the Ministry of Corporate Affairs issued the Companies (Indian Accounting Standards)

Rules, 2015 (“IAS Rules”) for the purpose of enacting changes to Indian GAAP that are intended to align Indian

GAAP further with IFRS. The IAS Rules provide that the financial information of the companies to which they

apply shall be prepared and audited in accordance with the Indian Accounting Standard (“IND (AS)”), although

certain class of companies may voluntarily implement IND (AS) for the accounting period beginning from April

1, 2015.

We have not made any attempt to quantify or identify the impact of the differences between Indian GAAP and

IND (AS) as applied to our financial information and it is urged that you consult your own advisors regarding the

impact of difference, if any, on financial data included in this Draft Red Herring Prospectus. However, we have

included certain principal differences between Indian GAAP and IND (AS) for the details of which, see

“Summary of Significant Differences Between Indian GAAP and IND (AS)” on page 370. Potential investors

should consult their own advisers for an understanding of the principal differences between the existing Indian

GAAP and the IND (AS), and how these differences might affect the financial statements appearing in this

document. See “Risk Factors – Significant differences exist between Indian GAAP and IND (AS), on one hand,

and other accounting principles, such as U.S. GAAP and IFRS, on the other hand, which may be material to

investors’ assessments of our financial condition” on page 44.

Certain figures contained in this Draft Red Herring Prospectus, including financial information, have been subject

to rounding adjustments. All decimals have been rounded off to two decimal points. In certain instances, (i) the

sum or percentage change of such numbers may not conform exactly to the total figure given; and (ii) the sum of

the numbers in a column or row in certain tables may not conform exactly to the total figure given for that column

or row. However, where any figures that may have been sourced from third-party industry sources are rounded

off to other than two decimal points in their respective sources, such figures appear in this Draft Red Herring

Prospectus as rounded-off to such number of decimal points as provided in such respective sources.

Industry and Market Data

14

We have commissioned a report titled “Road Sector in India” dated December, 2017, prepared by CRISIL, for the

purpose of confirming our understanding of the industry in connection with the Issue. Further, in this regard,

CRISIL has issued the following disclaimer:

“CRISIL Research, a division of CRISIL Limited (CRISIL) has taken due care and caution in preparing this report

(Report) based on the Information obtained by CRISIL from sources which it considers reliable (Data). However,

CRISIL does not guarantee the accuracy, adequacy or completeness of the Data/Report and is not responsible for

any errors or omissions or for the results obtained from the use of Data/Report. This Report is not a

recommendation to invest/disinvest in any entity covered in the Report and no part of this Report should be

construed as an expert advice or investment advice or any form of investment banking within the meaning of any

law or regulation. CRISIL especially states that it has no liability whatsoever to the subscribers / users /

transmitters / distributors of this Report. Without limiting the generality of the foregoing, nothing in the Report is

to be construed as CRISIL providing or intending to provide any services in jurisdictions where CRISIL does not

have the necessary permission and/or registration to carry out its business activities in this regard. Patel

Infrastructure Limited will be responsible for ensuring compliances and consequences of non-compliances for

use of the Report or part thereof outside India. CRISIL Research operates independently of, and does not have

access to information obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Ltd

(CRIS), which may, in their regular operations, obtain information of a confidential nature. The views expressed

in this Report are that of CRISIL Research and not of CRISIL's Ratings Division/CRIS. No part of this Report may

be published/reproduced in any form without CRISIL's prior written approval.”

Aside from the above, unless stated otherwise, industry and market data used throughout this Draft Red Herring

Prospectus has been derived from certain industry sources. Industry publications generally state that the

information contained in such publications has been obtained from sources generally believed to be reliable, but

their accuracy, adequacy or completeness and underlying assumptions are not guaranteed and their reliability

cannot be assured. Accordingly, no investment decisions should be made based on such information. Although

we believe that the industry and market data used in this Draft Red Herring Prospectus is reliable, it has not been

independently verified by us, the BRLMs, or any of our or their respective affiliates or advisors, and none of these

parties makes any representation as to the accuracy of this information. The data used in these sources may have

been reclassified by us for the purposes of presentation. Data from these sources may also not be comparable. The

extent to which the industry and market data presented in this Draft Red Herring Prospectus is meaningful depends

upon the reader’s familiarity with and understanding of the methodologies used in compiling such data. There are

no standard data gathering methodologies in the industry in which we conduct our business and methodologies

and assumptions may vary widely among different market and industry sources.

Such data involves risks, uncertainties and numerous assumptions and is subject to change based on various

factors, including those discussed in “Risk Factors” on page 18.

Currency and Units of Presentation

All references to “Rupees” or “₹” or “Rs.” or “INR” are to Indian Rupees, the official currency of the Republic

of India. All references to “US$”, “U.S. Dollar”, “USD” or “U.S. Dollars” are to United States Dollars, the

official currency of the United States of America. All reference to “Euro” or “€” is to Euro, the official currency

of the European Union.

In this Draft Red Herring Prospectus, our Company has presented certain numerical information. All figures have

been expressed in millions. One million represents ‘10 lakhs’ or 1,000,000. However, where any figures that may

have been sourced from third-party industry sources are expressed in denominations other than millions in their

respective sources, such figures appear in this Draft Red Herring Prospectus expressed in such denominations as

provided in such respective sources.

Exchange Rates

This Draft Red Herring Prospectus contains conversions of U.S. Dollars and other currency amounts into Indian

Rupees that have been presented solely to comply with the requirements of the SEBI ICDR Regulations. These

conversions should not be construed as a representation that such currency amounts could have been, or can be

converted into Indian Rupees, at any particular rate, or at all.

15

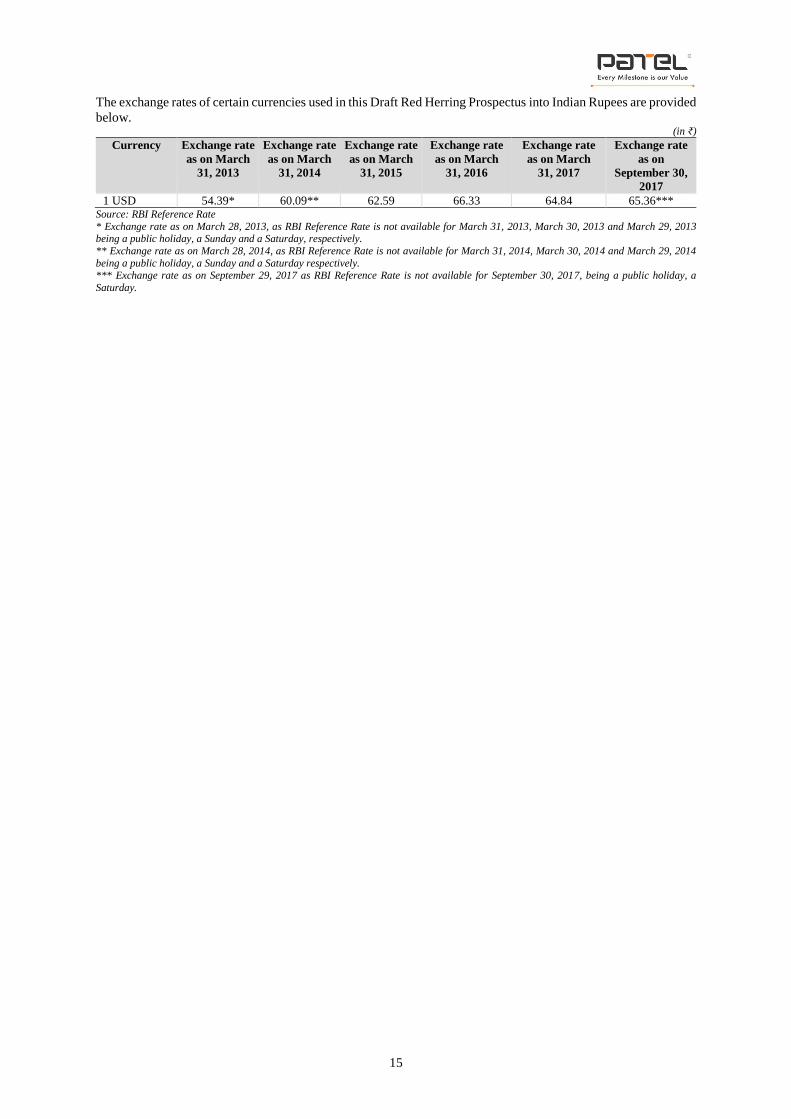

The exchange rates of certain currencies used in this Draft Red Herring Prospectus into Indian Rupees are provided

below. (in ₹)

Currency Exchange rate

as on March

31, 2013

Exchange rate

as on March

31, 2014

Exchange rate

as on March

31, 2015

Exchange rate

as on March

31, 2016

Exchange rate

as on March

31, 2017

Exchange rate

as on

September 30,

2017

1 USD 54.39* 60.09** 62.59 66.33 64.84 65.36*** Source: RBI Reference Rate

* Exchange rate as on March 28, 2013, as RBI Reference Rate is not available for March 31, 2013, March 30, 2013 and March 29, 2013 being a public holiday, a Sunday and a Saturday, respectively.

** Exchange rate as on March 28, 2014, as RBI Reference Rate is not available for March 31, 2014, March 30, 2014 and March 29, 2014

being a public holiday, a Sunday and a Saturday respectively. *** Exchange rate as on September 29, 2017 as RBI Reference Rate is not available for September 30, 2017, being a public holiday, a

Saturday.

16

FORWARD-LOOKING STATEMENTS

This Draft Red Herring Prospectus contains certain “forward-looking statements”. These forward looking

statements include statements which can generally be identified by words or phrases such as “aim”, “anticipate”,

“believe”, “expect”, “estimate”, “intend”, “likely to”, “objective”, “plan”, “propose”, “will continue”, “seek to”,

“will pursue” or other words or phrases of similar import.

These forward-looking statements are based on our current plans, estimates and expectations and actual results

may differ materially from those suggested by such forward-looking statements. All forward-looking statements

are subject to risks, uncertainties and assumptions about us that could cause actual results to differ materially from

those contemplated by the relevant forward-looking statement. This may be due to risks or uncertainties associated

with our expectations with respect to, but not limited to, regulatory changes pertaining to the industries in India

in which we have our businesses and our ability to respond to them, our ability to successfully implement our

strategy, our growth and expansion, technological changes, our exposure to market risks, general economic and

political conditions in India, which have an impact on our business activities or investments, the monetary and

fiscal policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates,

equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in

domestic laws, regulations and taxes, changes in competition in our industry and incidence of any natural

calamities and/or acts of violence. Important factors that would cause actual results to differ materially include,

including, but not limited to:

Infrastructure projects are typically awarded to us on satisfaction of prescribed pre-qualification criteria and

following a competitive bidding process. Our business and our financial condition may be adversely affected

if new infrastructure projects are not awarded to us or if contracts awarded to us are prematurely terminated.;

Our Order Book may not be representative of our future results and our actual income may be significantly

less than the estimates reflected in our Order Book, which could adversely affect our business, financial

condition, results of operations and prospects.;

Based on our Order Book as on October 31, 2017, 82.72% of our business comprising highway and other road

projects are awarded by various Government or Government-funded agencies. Any adverse change in

government policies or focus, or delay in payment may lead to our contracts being foreclosed, terminated,

restructured or renegotiated;

Our projects are exposed to various implementation and other risks and uncertainties, which may adversely

affect our business, financial condition, results of operations, and prospects;

We may be exposed to liabilities arising under our warranties or from defects during construction, which may

adversely affect our business, financial condition, results of operations and prospects;

Our Company, Subsidiaries, Directors, Promoters, Group Company and joint ventures are involved in certain

outstanding legal proceedings, which if determined adversely, may adversely affect our business, financial

condition, results of operations and prospects;

We have, until date, not completed execution of any project under the recently introduced hybrid annuity

model for implementing a highway project. We cannot assure you that we will be successful in executing the

project or if we will achieve better returns as compared to our existing EPC projects, or any returns at all;

Our business has been relatively concentrated in northern and western India and our Order Book shows relative

concentration in southern and northern India. Consequently, we are exposed to risks emanating from

economic, regulatory and other changes in these locations which we may not be able to successfully manage

may adversely affect our business, financial condition, results of operations, and prospects;

Our actual cost in executing an EPC contract may vary substantially from the assumptions underlying our bid.

We may be unable to recover all or some of the additional expenses, which may have an adverse effect on our

business, financial condition, results of operations, and prospects; and

We have significant working capital requirements. If we experience insufficient cash flows to enable us to

make required payments on our debt or fund working capital requirements, there may be an adverse effect on

our business, financial condition, results of operations and prospects.

For a further discussion of factors that could cause our actual results to differ, see “Risk Factors”, “Business” and

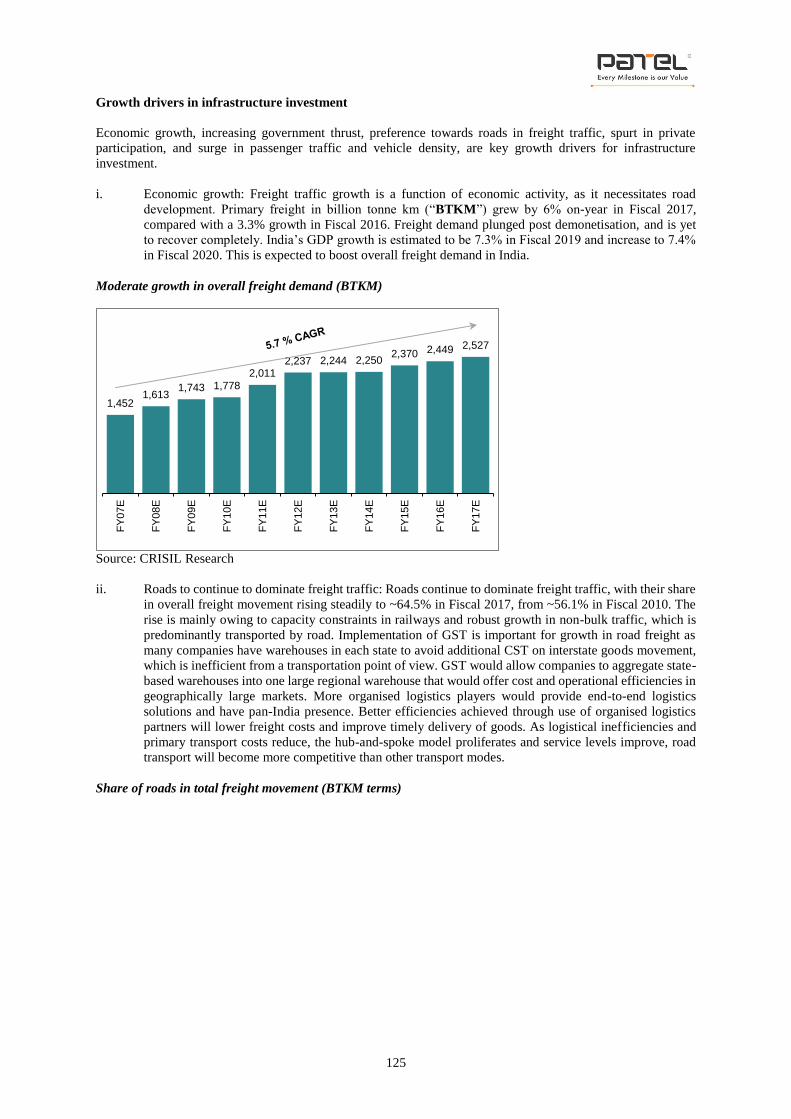

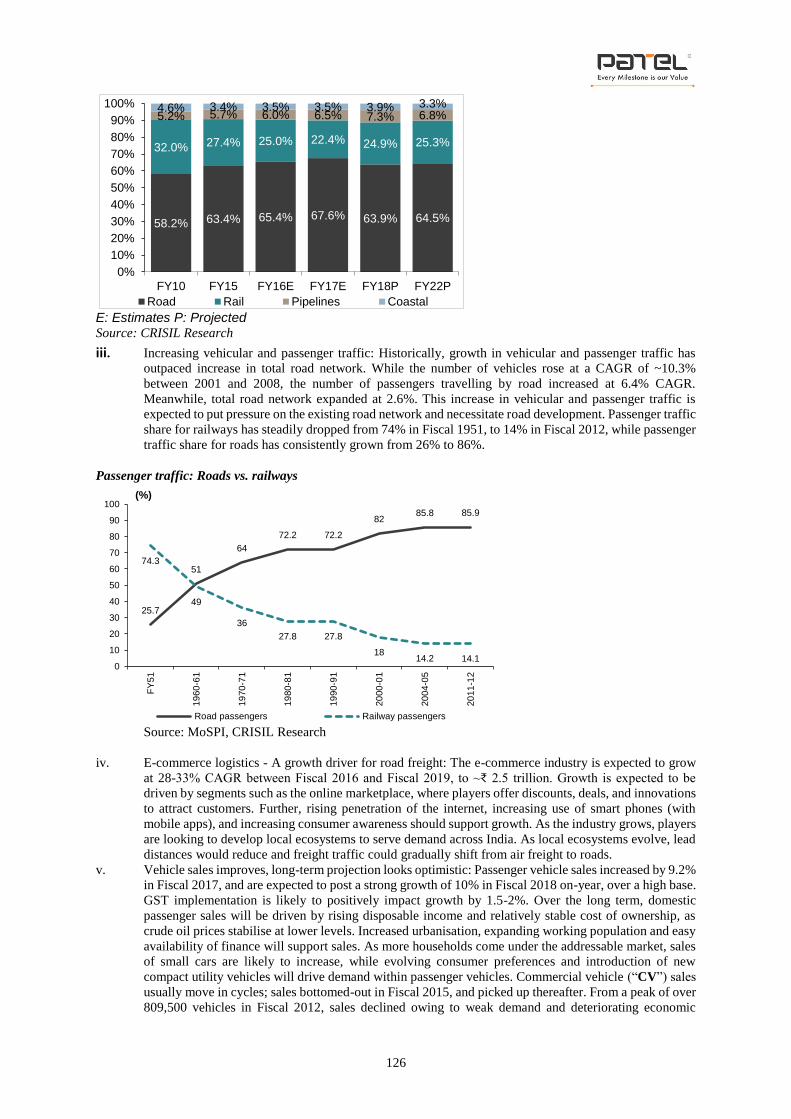

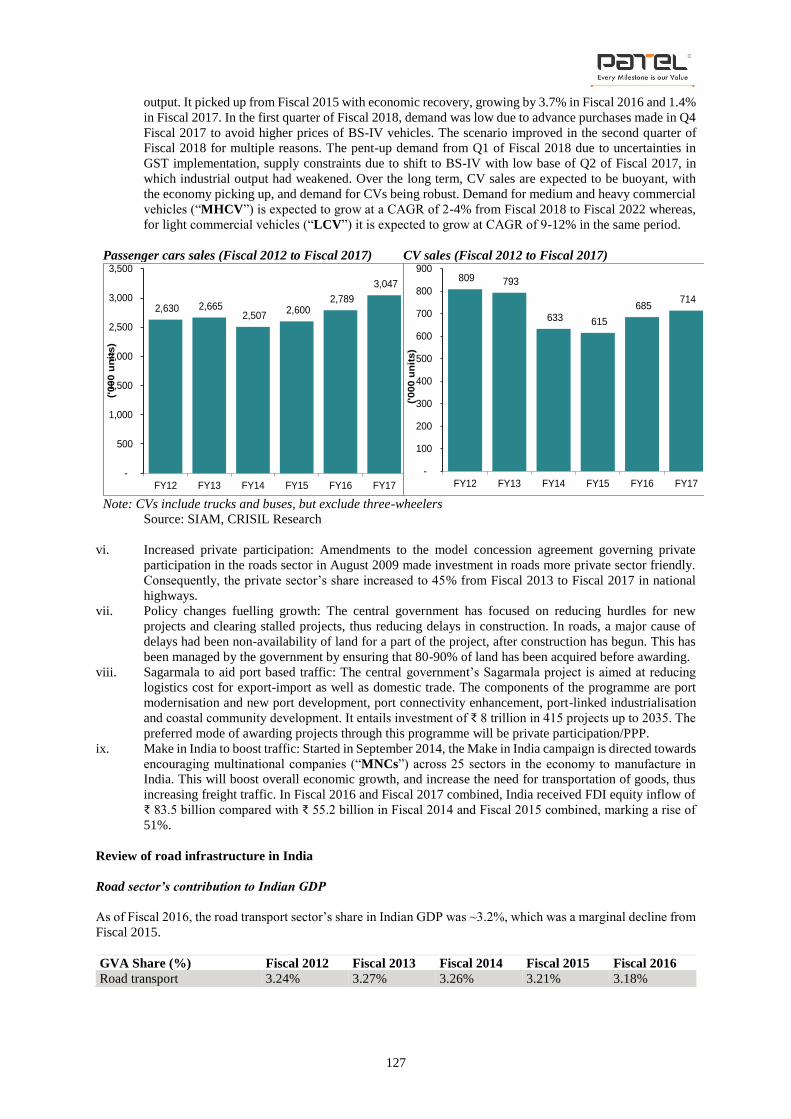

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 18, 154