Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=663841

1

OUTSIDE ENTREPRENEURIAL CAPITAL*

Forthcoming in the Economic Journal, 2009

Andy Cosh, Douglas Cumming and Alan Hughes

This paper investigates factors that affect rejection rates in applications for outside finance among different

types of investors (banks, venture capital funds, leasing firms, factoring firms, trade customers and suppliers,

partners and working shareholders, private individuals and other sources), taking into account the non-

randomness in a firm’s decision to seek outside finance. The data support the traditional pecking order theory.

Further, the data indicate that firms seeking capital are typically able to secure their requisite financing from at

least one of the different available sources. However, external finance is often not available in the form that a

firm would like.

JEL Classification: G21, G22, G23, G24, G31, G32, G35

* We owe special thanks the Editor (Leonardo Felli), two anonymous referees, and the seminar participants at York University, the 2006 Financial Management Association Annual Conference and the 2008 Kauffman Foundation Conference on Entrepreneurial Finance.

Electronic copy available at: http://ssrn.com/abstract=663841

2

This paper engages four interrelated empirical questions. First, what are the characteristics of privately

held entrepreneurial firms that seek external [‘outside’] finance, and what drives the request for capital

from the different potential sources of external finance: banks, venture capitalists, private individuals,

leasing, factoring, suppliers/customers, partners/working shareholders, among other sources? Second,

what are the factors that lead to rejection or acceptance of requests for external finance, given this non-

randomness in the types of firms that seek external finance (in the spirit of Heckman, 1976, 1979)?

Third, as various forms of financing are far from being perfect substitutes, are there differences in the

ability of firms to obtain capital from the different available sources? Fourth, can firms obtain all of their

desired capital from the different available sources, even if it is not in the form they would like?

It is widely recognized that the decision to seek external finance and the type of financing sought

is related to information asymmetries faced by investors regarding the entrepreneurial firm’s quality (see

for example, Jensen and Meckling, 1976).1 Where entrepreneurs have information that investors do not

have, external equity finance (which dilutes the entrepreneurs’ ownership share) is (given unused debt

capacity) indicative of a low quality firm (Myers and Majluf, 1984; see also Myers, 2000). This stream of

research has derived a standard pecking order theory, in that firms prefer to finance new projects with

internal cash flows first, and then if necessary, thereafter seek external debt capital and lastly seek

external equity capital. This rank ordering, however, might be distorted by the fact that external sources

of capital could add value to their investee firms. For example, Garmaise (2000) shows that if investors

are known to possess a greater ability to assess project quality relative to that of the entrepreneurial team,

external equity finance is indicative of a high quality firm. Also De Meza and Webb (1987, 1992) argue

that banks may not be ill informed relative to new firms and show that if we abandon the Stiglitz and

Weiss (1981) assumption of mean preserving spreads of risk then their rationing results do not hold (see

also De Meza and Webb, 1999, 2000). In our paper, we test these theoretical propositions by first taking

into account the preliminary question of what drives the decision of a firm to seek external financing. We

then empirically analyze the matching of different types of firms and investors, taking into account the

non-randomness in the types of firms that sought outside capital.

Our analysis builds on an important but largely segmented literature in financial intermediation

and entrepreneurial finance (briefly surveyed in section 1). Academic studies of the interaction between

firms and their sources of capital focus, almost exclusively, on a single source of capital. Separate

streams of literature have emerged in bank finance, lease finance, venture capital finance, private

individual investor finance, supplier finance, etc. In theoretical work, the need to focus on one (or in

1 This work also stems from seminal papers on adverse selection, including Ackerlof (1970), Stiglitz and

Weiss (1981), and De Meza and Webb (1987, 1992).

3

exceptional cases, two) external capital sources is directly attributable to theoretical tractability (one

cannot model everything). In empirical work, the focus on one or two capital sources is largely

attributable to data availability, since datasets are typically derived from investors, particularly in the case

of non-publicly traded businesses.

In building on this prior literature, the key component of our analysis is that we introduce a very

large dataset derived from private entrepreneurial firms themselves, and not from their investors. This

empirical approach provides a number of advantages for the purpose of addressing the three central

research questions outlined above. Perhaps most importantly, because we observe firms that did, and did

not, seek external finance, we avoid Heckman (1976, 1979) sample selection problems in analyzing the

role of external investors in facilitating the development of entrepreneurial firms. Prior work on topic

(see section 1) is typically derived from one type of investor and thereby fails to consider the non-random

selection process among those entrepreneurial firms that seek external finance, and the non-random

selection process among different types of potential investors.

A second key component of our analysis is that we have a very detailed and broad-based dataset

from 2520 UK entrepreneurial firms in the period spanning 1996-1997 the majority of which were formed

in the 1980s and early 1990s (specific details are provided in section 3). A number of firms in the sample

sought external finance from a wide variety of potential outside investors, and some successfully obtained

external finance. This diversity in the data is of interest, as it allows us to carry out unique analyses of the

decision to seek external finance from a broad spectrum of different investors. By contrast, datasets

derived from investors typically provide insights into only those firms that applied for external finance

with that investors, and further, typically only those firms that were successful in obtaining finance.

These limitations in all empirical prior work based on data from investors and not investees are overcome

in our analysis of the new data introduced herein. We are therefore able to investigate issues that have

been previously considered empirically intractable.

The data indicate the following primary key results. First, we identify factors that lead firms to

seek external finance. Controlling for a large number of other factors, we find the most significant

determinant of applications for external finance to be capital expenditures / profits. A firm is

approximately 1% more likely to seek external finance when capital expenditures are 20 times that of

profits relative to 10 times profits. This indicates support for the traditional pecking order in which firms

finance new projects internally before seeking external finance. Corporations are approximately 6% more

likely to seek external finance than partnerships or sole proprietorships. It is also quite noteworthy that,

on a ranking from 1-4 with 4 being the highest growth orientation, an increase in the ranking by 1 point

tends to increase the probability of an application for external finance by approximately 11%. Further,

4

firms that face 1000 competitors are approximately 2% more likely to apply for external finance than

firms that face 100 competitors.

Second, we show systematic characteristics drive the amount of external finance actually sought,

controlling for the non-randomness in the decision to seek external finance in the first place in the spirit of

Heckman (1976, 1979). Firms seek a greater amount of external finance when then have greater capital

expenditures / profits and higher profit margins. Firms with more debt / assets also seek more external

finance, but this effect is concave (that it, it increases at a decreasing rate and follows and inverted-U

pattern).

In the third step of the analyses, we consider the percentage of external finance obtained. Larger

firms in terms of their total assets are much more likely to obtain a higher percentage of the total amount

of finance sought. For instance, a firm with £1 million in assets will obtain approximately 5% more of

their desired capital than the average firm with £375,000 in assets. This is highly suggestive that smaller

firms face a capital gap in terms of being able to obtain all of their desired capital. A firm that recently

developed a novel innovation, by contrast, tends to obtain less of their desired capital. More specifically,

a firm that was started within 7 years of applying for external finance and recently developed an

innovation will obtain approximately 8% less of their desired capital, but older firms that recently

developed an innovation are not statistically likely to receive less of their desired capital. Conversely,

older firms that are less profitable and/or have not yet implemented professional directors are less likely

to obtain all of their desired capital (albeit smaller firms do not face these limitations for profits and/or

professional directors).

We further explore these three main steps in the analyses outlined above by considering the

differences between banks and venture capital funds, as well as other sources of capital, including hire

purchase or leasing firms, factoring / invoice discounting firms, trade customers / suppliers, partners /

working shareholders, private individuals (often referred to as “angel investors” (Harrison and Mason,

2000)) and other sources. Among the 952 of 2520 firms (38%) in our sample that did seek external

finance in the 1996-1997 period considered, 775 approached banks, 474 approached leasing firms, 151

approached factoring / invoice discounting firms, 138 approached partners / working shareholders, 87

approached venture capital funds, 83 approached private individuals, and 53 approached trade customers /

suppliers (and 67 approached other sources).2 It is of interest that outright rejection rates were highest

among venture capital funds (46% rejection), and much higher than that for banks (17% outright 2 We refer to a firm “approaching” a potential source as making more than a trivial effort (for example, it

involves more that just mailing in a business plan to the potential source for consideration), consistent with our

survey evidence and related survey work undertaken by the Centre for Business Research at the University of

Cambridge.

5

rejection). The lowest rejection rate was among leasing firms (5%). Banks comprised the median and

mean highest percentage of outside finance in terms of which type of source was approached and which

type of source provided the finance. Among the 952 firms that did apply for external finance, the median

number of different sources approached was 2 (and mean was 1.96). Also, firms with greater capital

expenditures / profits are more likely to approach a greater number of different types of sources of

finance. For the subset of the oldest firms (established before 1980 in our sample), profit margins are

significantly negatively related to the number of different sources of capital approached.

The new data and statistics introduced in this paper provide completely new evidence on the

importance of external capital for entrepreneurial firms, and the comparative importance of different

sources of capital. It is noteworthy that, among the 38% of firms that made non-trivial efforts to obtain

external finance in our sample, the mean percentage of finance obtained (relative to the amount sought)

was 80.7%, and the median percentage was 100%. The data do not indicate the presence of a substantial

capital gap for the majority of firms seeking entrepreneurial finance; rather, firms seeking capital are able

to secure their requisite financing from at least one of the many different available sources. There are,

however, differences in firms’ ability to obtain finance in the form that they would like. Even after

controlling for selection effects, the data indicate banks are more likely to provide the desired amount of

capital to larger firms with more assets. Leasing firms, factor discounting / invoicing firms, trade

customers / suppliers and partners / working shareholders are more likely to provide the desired capital to

firms with higher profit margins. Profit margins are not statistically relevant to venture capital funds and

private individual investors; smaller firms are more likely to obtain finance from private individuals,

while young innovative firms seek external capital from venture capital funds.

This paper is organized as follows. Section 1 briefly reviews the related literature. Section 2

introduces the data considered in this paper, and presents a number of new facts pertaining to

entrepreneurial finance. The testable hypotheses within the context of our new data and the prior

literature are outlined in section 3. Summary statistics and multivariate analyses are provided in section

4. Thereafter, limitations, alternative explanations and future research are discussed in section 5.

Concluding remarks follow.

1. Related Literature

In this paper we study the choice between internal versus external entrepreneurial finance, with regard to

a wide variety of sources of outside capital. Because we consider a number of different types of

investors, our work is related to a plethora of papers along segmented streams of research in financial

intermediation and entrepreneurial finance. While it is of course beyond the scope of our paper to review

6

the entire literature herein, 3 we nevertheless provide a brief perspective of the contribution of our

analyses in the context of recent related prior work.

At the most generalizable level, a firm’s decision to seek external finance is related to information

asymmetries faced by investors regarding the entrepreneurial firm’s quality (see Jensen and Meckling,

1976; Stiglitz and Weiss, 1981; De Meza and Webb, 1987, 1992; Cosh and Hughes, 1994; De Meza,

2002; Carpenter and Petersen, 2002a,b). Myers and Majluf (1984) and Myers (2000) have derived a

pecking order that results from such information asymmetries between entrepreneurs and investors,

whereby firms first finance new projects with internal cash flows,4 and obtain external finance only where

necessary because external finance is more costly when investors face information asymmetries. External

debt finance is preferred to external equity finance in the traditional pecking order since equity involves a

dilution of the entrepreneur’s ownership share. Recent theoretical work, however, has shown this pecking

order is reversed where investors have superior knowledge about the commercialization process of an

entrepreneur’s invention, and/or add value to the entrepreneur’s project (Garmaise, 2000).

Pre-IPO outside entrepreneurial capital may be provided by banks, venture capitalists, private

individuals, leasing, factoring, suppliers/customers, partners/working shareholders, among other sources.

Different streams of the academic literature have become segmented by each of these different investor

types for reasons of theoretical tractability and data availability. Nevertheless, the fundamental questions

considered in the segmented literature significantly overlap in two primary ways that are pertinent to our

empirical analyses. First, there is a stream of literature on the ability of an investor to mitigate

informational problems associated with small (and/or high-tech) businesses, and this has been considered

in the context of banks (e.g., Berger et al., 2001; Berger and Udel, 1998), venture capital finance (e.g.,

Gompers and Lerner, 1999), angel finance (Wong, 2003; Harrison and Mason, 2000), lease finance

(Porter, 1995; Myers et al., 1976, Yusopova, 2002), supplier finance (e.g., Tamari, 1970), etc. Second,

there is a stream of literature on the contribution of the investor to not only screen good from bad

investees, but also assist in the development of the investee firm, which has been the focus of the

literature in both angel finance (Wong, 2003; Harrison and Mason, 2000) and venture capital finance

(e.g., Bergmann and Hege, 1998; Gompers and Lerner, 1999; Kortum and Lerner, 2000; Bascha and

Walz, 2001; Mayer et al., 2005; Hege et al., 2003; Neus and Walz, 2005, Riyanto and Schwienbacher,

2006; Schwienbacher, 2007).

3 There are nevertheless recent surveys of the entrepreneurial finance and venture capital literature, including

Denis (2004), Gompers and Lerner (2001), Smith and Smith (2000) and Berger and Udell (1998), as well as recent

surveys of the banking literature, including Gorton and Winton (2003) and Berger and Humphrey (1997).

4 Relatedly, Carpenter et al. (1998) show that cash flow is a key determinant of inventory investment.

7

While some of the issues we consider have been addressed in prior work that is segmented by

investor type, there is comparatively less rigorous data and evidence about the comparative ability of

different types of investors to mitigate informational problems associated with outside finance, and the

comparative importance of different sources of capital to different types of entrepreneurial firms.

Moreover, given the fact that there is a non-randomness associated with the types of firms seeking

external capital (in the spirit of Heckman, 1976, 1979), it is difficult to assess the importance of different

types of investors to entrepreneurial firms without a comparative sample of firms that did not seek any

external finance, and without knowledge of alternative sources of external finance sought by the firms.

We seek to overcome some of these limitations in our analysis. We also keep in mind areas in which we

face limitations ourselves, and thereby point to avenues for future research (discussed in detail in section

5 below).

Our comparative focus is somewhat related to recent work that has made significant steps in

comparing two types of financial intermediaries. The recent literature has primarily been focused on

comparing banks to venture capital funds.5 Theoretical contributions in this regard invariably conclude

that venture capitalists are more skilled than bank managers at screening potential investees, and

providing greater value-added to their investee firms (Keuschnigg and Nielsen, 2004; Udea, 2004). These

propositions are consistent with the large literature that focuses on venture capital funds themselves (e.g.,

Gompers and Lerner, 1999, 2001a,b; Berger and Udell, 2002; Carpenter and Peterson, 2002; Cressy,

1996, 2002; Manigart et al., 2006; Wright and Lockett, 2003; Casamatta, 2003; Casamatta and

Haritchabalet, 2007; Schmidt, 2003; Hsu, 2004; Kortum and Lerner, 2000; Kanniainen and Keuschnigg,

2003, 2004; Keuschnigg, 2004). This work is also consistent with a literature comparing banks and

venture capitalists; however, that empirical work does not consider other types of potential investors, and

does not consider the non-random selection process among those entrepreneurial firms that have sought

external finance, and the non-random selection process across different types of investors. In other

words, that work is not immune from the Heckman (1976, 1979) sample selection bias.6 Our dataset

enables these limitations to be overcome, and enables a broader array of different types of investors to be

considered, among other things described throughout the subsequent sections of this paper.

5 In a recent theoretical contribution, Chemmanur and Chen (2003) provide an analysis on interaction

between angel investors and venture capitalists; however, no prior paper has empirically tested their model. In a

recent empirical contribution, Cassar (2004) focuses on different sources of capital for small firms, but does not

consider selection effects in the spirit of Heckman (1976, 1979), and does not consider the interplay between access

to outside capital and the development of the entrepreneurial firm.

6 Heckman (1976, 1979) shows that when this incidental truncation is accounted for in regression analyses,

any or all of the sign, magnitude, and statistical significance of regression coefficients may change.

8

Finally, it is noteworthy that our empirical analysis of outside entrepreneurial capital is related to

a very large theoretical and empirical literature on the decision of a privately held business to go public

(see, e.g., Ritter and Welch, 2002, for a recent review of that literature). Our analysis significantly differs

from the IPO literature in that we focus on the much earlier decision in the life-cycle of a private business

to seek external private finance, long before it would be in a position to go public (and many firms might

not want to go public). And as mentioned, our data are not constrained by consideration of only one or

two types of potential investors; rather, all types of external sources of capital for early stage businesses

are assessed. The data introduced in this paper are described in the next section.

2. Testable Hypotheses 2.1. Primary Hypotheses

Our empirical analysis focuses on three primary hypotheses which are outlined in this section. Our first

hypothesis pertains to the pecking order theory of capital structure. In particular, we are interested in

knowing whether entrepreneurial firms do in fact prefer to finance projects internally with their own

profits prior to seeking external finance. Traditional pecking order theory (Myers and Majluf, 1984) is

consistent with this prediction, since entrepreneurs have information that investors do not have, and

therefore the information asymmetry faced by outside investors makes external finance more costly. By

similar reasoning, external equity finance is more costly than external debt finance since equity involves

the dilution of the entrepreneurs’ ownership interest in the firm, and offers of equity finance therefore

signal low quality.

Hypothesis 1a [Pecking Order and Decision to Seek External Funds]: Firms with greater profit margins

are less likely to seek external finance, or at least will seek less external capital and use internal profits to

fund projects. Among firms that do seek external finance, firms with greater profit margins will seek debt

finance prior to equity finance.

Hypothesis 1b [Pecking Order and Success with Obtaining External Funds Sought]: Firms with greater

profit margins are more likely to obtain the external finance sought.

Our second central hypothesis considers the decision to seek finance as a function of

entrepreneurial firm as well as investor characteristics. The costs of seeking and obtaining external

capital are higher where entrepreneurial firms exhibit greater informational asymmetries. That is, the

search costs for capital, as well as the terms offered to the investor, are less favorable for firms for which

9

investors have more difficulty mitigating information problems and expected agency costs. Among

younger and innovative firms for which these costs are more pronounced (as generally viewed in the

literature; see e.g., Noe and Rebello, 1996), firms will only be willing to incur these costs if they have

significant growth objectives. Hence, growth orientated firms are naturally more attracted to external

finance as a result of their willingness to incur search costs and bear the price of external capital (Kon and

Storey, 2003).

Just as entrepreneurial firm characteristics matter in respect of external financing decisions, we

might also expect differences across different sources of capital. It is widely regarded that venture capital

funds have a comparative advantage in mitigating information asymmetries and agency costs (relative to

banks, leasing and factoring firms) will be more likely to finance businesses for which risks are more

pronounced, but potential returns are higher (see, e.g., Berger and Udell, 1998).

Hypothesis 2a [Growth]: Firms for which growth is the most significant objective will be, all else being

equal, more likely to seek external finance.

Hypothesis 2b [Banks versus Venture Capital Funds]: Venture capital funds are more likely to finance

riskier firms with high growth objectives than banks and other sources of external capital.

With the wide range of sources of external entrepreneurial capital (banks, venture capital funds,

leasing firms, factoring firms, trade customers and suppliers, partners and working shareholders, private

individuals and other sources), it is natural to expect that many firms will likely raise the money that they

want though not in the form that they would like. Clearly, raising some money is better than being denied

access to the capital market, but the various forms of financing are far from perfect substitutes and may

imply (undesirable) constraints of various sorts, such as obtaining value added advice from a more

reputable source of capital. For instance, relative to other types of sources of capital, venture capital

funds typically provide more intensive financial, administrative, marketing, and strategic advice, and

facilitate a network of professional advisors to enable the entrepreneurial firm to succeed. Our data

(described below in section 3) enables us to identify which types of firms are more likely to face certain

constraints in obtaining their desired form of capital. We may expect that firms with less favorable

prospects will face greater constraints in obtaining their desired form of capital.

Hypothesis 3 [Desired Source of Capital]: Firms seeking more capital relative to their profits and firms

with lower profit margins will have to approach a greater number of different forms of finance to obtain

their desired capital, and will have greater difficulty in obtaining their desired level of external finance.

10

2.2. Control Variables

In considering the three primary hypotheses we control for a number of potentially relevant factors. First,

we consider the innovativeness of the industry, as well as the innovativeness of the firm. Innovation is

associated with asset intangibility, since high-tech firms are typically more innovative and have more

intangible assets (Kortum and Lerner, 2000). Higher asset intangibility is associated with more

pronounced information asymmetries and agency costs, as well as potential hold-up costs, thereby

increasing the costs of external finance (Gompers and Lerner, 1999). On one hand, therefore, we would

expect the costs of obtaining external finance to be greater among more innovative firms. On the other

hand, the potential benefits to external equity financiers are larger the more innovative the firm. This is

particularly true among a smaller subset of investors that add value to their investees. This value added

can come in a variety of forms, including but not limited to advice pertaining to strategy, marketing,

financing, administrative and human resource policy, as well as facilitating a network of contacts for

firms that includes, but is not limited to, accountants, suppliers, customers, lawyers, and investment

bankers. For example, one recent theoretical paper (Garmaise, 2000) predicts the traditional pecking

order is exactly reversed when investors do provide value added and have superior skills at assessing the

value of the entrepreneurial project. 7 Hence, in our empirical analyses we consider differences in

financing obtained from banks and venture capitalists.

Second, we control for the effect of industry structure on financing decisions. In his popular

work on industry structure, Porter (1998) identifies five categories of factors that can give rise to

differences in risk-adjusted rates of return across industries. These factors include supplier power, buyer

power, barriers to entry, threat of substitutes and the degree of rivalry. The economic importance of some

of these factors has been identified in the literature on a firm’s financing decisions. In short, risk-adjusted

rates of return tend to be lower in industries for which there is more competition, and a stronger presence

of larger dominant competitors; therefore, it is less attractive for investors to provide external capital to

entrepreneurial firms in those industries, and the terms offered by investors will be less attractive.

Third, we control for the possibility that entrepreneurial firms started by females face greater

hurdles in seeking external capital (Marlow and Patton, 2005). On one level, this could simply be

unjustified or “actual” sex discrimination. On another level, there might be characteristics of firms started 7 For example, as discussed in Garmaise (2000), investors might be more skilled in valuing the project than

the entrepreneur where the investor has experience and market information pertaining to the commercialization of a

scientific idea, and the entrepreneur’s comparative advantage over the investor only lies in the scientific process that

led to the idea.

11

by females that are systematically different relative to firms started by males, such as the firm’s growth

objectives, the professional qualifications of the firm’s directors, the firm’s innovative activities and

industry sector, among numerous other systematic differences. If so, then information asymmetries faced

by outside investors might systematically differ across firms started by males and females, thereby

causing systematic differences in the costs and benefits of seeking external capital by female versus male

led firms. We might label this second perspective as “apparent” (not actual) sex discrimination whereby

information problems and firm characteristics give rise to the appearance of discrimination between males

versus females, but such discrimination is directly attributable to those characteristics and not

independently related to the maleness or femaleness of the firm’s founding CEO. Either way, we do

consider and control for these alternative theories in our empirical analyses.

Finally, in our empirical tests we also control for legal form (corporation versus partnership or

sole proprietorship), firm age, capital expenditures, insider ownership (including CEO and board

ownership), debt levels (relative to assets) prior to seeking external finance in the period considered, and a

variety of reasons why the entrepreneurial firm was established (including reasons ranging from a desire

to avoid unemployment to running a business, implementing an invention and wealth ambitions). Each of

these variables (among others discussed immediately below) are pertinent as control variables, since they

directly relate to a firm’s need/desire for external capital for reasons discussed in prior literature

summarized above in section 1. The specifics in our data are outlined in detail immediately below in

section 3. Empirical tests follow in section 4.

3. Data and Summary Statistics

Our data come from a very detailed survey of 2520 UK entrepreneurial firms in the period spanning

1996-1997. The data were collected by the Centre for Business Research at the University of Cambridge,

as described in detail by Cosh and Hughes (1998). The median start-up year of the firms in the data herein

was 1983, where 697 started in the 1990s, 920 started in 1980s, and 964 started prior to 1980.

The sampling frame for the survey was all independent businesses in manufacturing and business

services with less than 500 employees in Great Britain including businesses partnerships and sole

proprietors. The achieved sample was 2520 firms based on size stratified approach to avoid swamping the

sample with micro businesses. The unit response rate was 25%. A response bias analysis in terms of age

employment turnover pre tax profit and legal status revealed that older manufacturing firms were

somewhat less likely to respond. There was no response bias of any kind in service business responses,

nor any bias in manufacturing firms responses in terms of age profitability or legal status. A spatial

analysis revealed that the achieved sample was representative of the regional distribution of the small

12

business population in Great Britain (complete details on survey design and sample selection issues are

provided in Bullock and Hughes, 1998).8

Summary statistics of the data, as well as correlations across different variables, are provided in

Tables 1-3. Table 1 indicates that there were 37.8% (952 of 2520) firms in the data that did seek external

finance in the 1996-1997 period. The average amount of external finance sought was £467,667, and the

median amount sought was £100,000. The average amount obtained was almost 81% of that which was

sought, and the median percentage obtained was 100%. Overall, therefore, the data do not suggest a

shortage of external capital for firms that make more than a trivial effort in applying for capital.

[Insert Tables 1-3 About Here]

Table 1 summarizes a variety of explanatory variables used in the empirical analyses. In order to

explain external financing decisions in the 1996-1997 financial year, we use lagged (1995) balance sheet

items, including lagged assets and lagged long term debt / assets. For firms that were started in 1996-

1997, these items are assigned the value ‘0’. We do not use contemporaneous balance sheet values since

any external financing obtained would directly show up in our left-hand and right-hand-side variables.

Also, Table 1 indicates statistics from firms’ income statement (including profits and profit margin) and

cash flow statement (capital expenditure). These items are measured for the 1996-1997 financial year

because in applications for external finance, firms will present the most recent quarter’s income and cash

flow statements (alongside all historical statements), as well as projected future income and cash flows.

As such, it is appropriate to consider the most recent year’s information. There is not an endogeneity

problem as applications for external finance and obtaining external finance does not impact profitability,

8 In some cases survey responses contained missing values. These values were interpolated with comparable

available information such as asset sizes, profit margins, age and the like so that we make use of the full sample of

2520 firms in the analysis. If interpolation was not possible for a survey respondent, then median values were used.

We also considered other techniques to handle missing data. For example, in one specification we considered a two-

step probit estimate in which the first step considers whether a full set of information was available and the second

set then estimates the regression for alternative forms of finance. We also considered regressions with fewer

explanatory variables, which in turn increases the sample size where certain excluded variables have missing

observations. Either way, the results are quite robust. Alternative specifications are available on request. Also, note

that an earlier version of this paper (available on request) was distributed with a smaller sample population of 1900

firms. The current version draws from a sample of 2520 firms. While there are some differences in the results with

the larger sample, the main results are consistent.

13

turnover or profit margin in the same year.9 Similarly, applying for or obtaining finance will not lead to

an innovation in the same year (albeit, it may lead to an innovation in subsequent years as the new capital

is spent on R&D projects, as indicated by, e.g., Kortum and Learner, 2000), and hence our innovation

variable is measured in the contemporaneous period. In sum, we use lagged balance sheet items to avoid

direct endogeneity in analyzing external capital raised relative to debt and assets, and current cash flow

and income statement items to account for the fact that firms provide potential sources of external capital

with their most recent quarter’s profitability information as well as projected cash flows and profits. In

our multivariate analyses, we do not simultaneously consider current and historical values of cash flow

and income statements as these items are highly correlated over time (correlations are greater than 0.7 for

each of these variables from one year to the next10).

Table 2 reports the number of firms in our data that did seek external finance by the type of

source of finance, as well as the percentage of all their external capital obtained from the source. Among

the firms in our sample that did seek external finance, 775 approached banks, 474 approached leasing

firms, 151 approached factoring / invoice discounting firms, 138 approached partners / working

shareholders, 87 approached venture capital funds, 83 approached private individuals, 53 approached

trade customers / suppliers, and 67 approached other sources. It is of interest that outright rejection rates

were highest among venture capital funds (46% rejection), and much higher than that for banks (17%

outright rejection). The lowest rejection rate was among leasing firms (5%). Banks comprised the

median and mean highest percentage of outside finance in terms of which type of source was approached

and which type of source provided the finance. In fact, banks comprised the only type of source for

which the median percentage of a firm’s total external capital was greater than 0% (for banks, the median

percentage is 34%; see Table 2).

A number of the correlations in Table 2 provide insights into the different characteristics of the

different types of investors. Banks are statistically more likely to finance profitable businesses, while the

correlations in Table 2 show private individuals are statistically more likely to fund unprofitable

businesses. Venture capital funds tend to finance innovative firms in innovative industries; unlike banks,

9 There is one potential exception to this statement: contemporaneous capital expenditures might be

endogenous to obtaining external finance if firms are cash constrained. However, the data indicate firms most often

obtain their desired cash flows (albeit not always in the form that they would like). Hence, we use the current

capital expenditures to account for planned growth (i.e., not historical capital expenditures which reflect historical

growth) and to account for the fact that firms provide to potential sources of external capital their most recent

quarter profits and capital expenditures, as well as expected profits and capital expenditures.

10 These high correlations give rise to results that are robust when we use lagged values.

14

as would be expected, because banks provide debt finance, have very large portfolios, and typically use

preset criteria in ascertaining whether the firm is a suitable risk for a loan.

The data indicate venture capital funds are more likely to finance businesses with higher turnover

and greater total assets, which is in contrast to private individuals. Consistent with Gompers and Lerner

(1999), venture capital funds also finance companies with a greater proportion of professional directors

(hence potentially better governance) and higher growth objectives, which is similar to financing from

private individuals. Venture capital funds finance firms with smaller percentages of shares allocated to

CEOs are board members, and firms established to implement an invention. Venture capital fund

managers have small portfolios (often no more than 5 investees per fund manager; see Kanniainen and

Keuschingg, 2003, 2004; Cumming, 2006), and provide significant screening pre-investment and value-

added post investment in their investee firms.

Hire purchase, or leasing, firms are more likely to finance older businesses with high capital

expenditures, little innovation, a smaller proportion of professional directors, and firms started by males

and not females. Leasing businesses act in ways that are somewhat analogous to banks. The main

difference is that the leasing business typically ties the financing provided to some other product provided

to the firm.

Factor / invoice discounting firms provide cash advances on the basis of an unpaid invoice, so

that a firm may meet cash shortages.11 This type of financing tends to be used by firms with fewer

professional directors, as well as firms with high growth objectives and lower profit levels. The type of

finance provided by an invoice discounting firm is such that they do not have concerns with information

problems associated with the quality of the firm that obtains the finance, but rather, with the firm or

customer with the unpaid invoice.

Trade customers / suppliers are more likely to finance younger firms with growth objectives are

those that have recently developed an innovation. There are proprietary rights associated with innovative

industries and smaller innovative firms face potential hold up problems from sources of capital. The data

are suggestive that smaller innovative firms are not concerned with these hold-up problems from the

larger suppliers in their respective industries. Suppliers can be a natural source of capital for some

developing firms securing a supply chain for developing their own products.

Partners / working shareholders are more likely to be a significant source of capital for firms with

high levels of debt / assets. Firms with excess leverage may secure additional capital from sources of

capital that face comparatively few informational problems, such as existing partners / working

shareholders.

11 See http://www.bizhelp24.com/business_finance/business_finance_factoring.htm.

15

Finally, the category of “other private individuals” in Table 2 or “angel investors” indicates

similar patterns as with the venture capital funds. Angel investors finance small, young and as-yet

unprofitable businesses, albeit firms with strong management and high quality directors.

Table 3 provides additional correlation statistics across various variables that are used in the

multivariate empirical analyses in the next section. The matrix gives further insights into the data, and

provides guidance in terms of considering issues of collinearity in the regressions in section 4.

4. Multivariate Empirical Analyses

This section provides multivariate tests of these theoretical propositions by first considering the extent of

finance sought in subsection 4.1, taking into account (in the spirit of Heckman, 1976, 1979) the first step

non-randomness in the decision to seek outside capital. Subsection 4.2 considers the percentage of

external capital obtained. Thereafter, we provide tests of differences across the alternative sources of

capital (banks, venture capital funds, leasing firms, factoring firms, trade customers and suppliers,

partners and working shareholders, private individuals and other sources). Section 5 discusses potential

limitations and alternative explanations, and suggests avenues for future research. Concluding remarks

follow in section 6.

4.1. Which Firms Seek External Finance, and the Amount of External Finance Sought

In this subsection we examine the factors that affect the amount of external finance while taking into

account the factors that lead firms to seek external finance in the first place. We report eight alternative

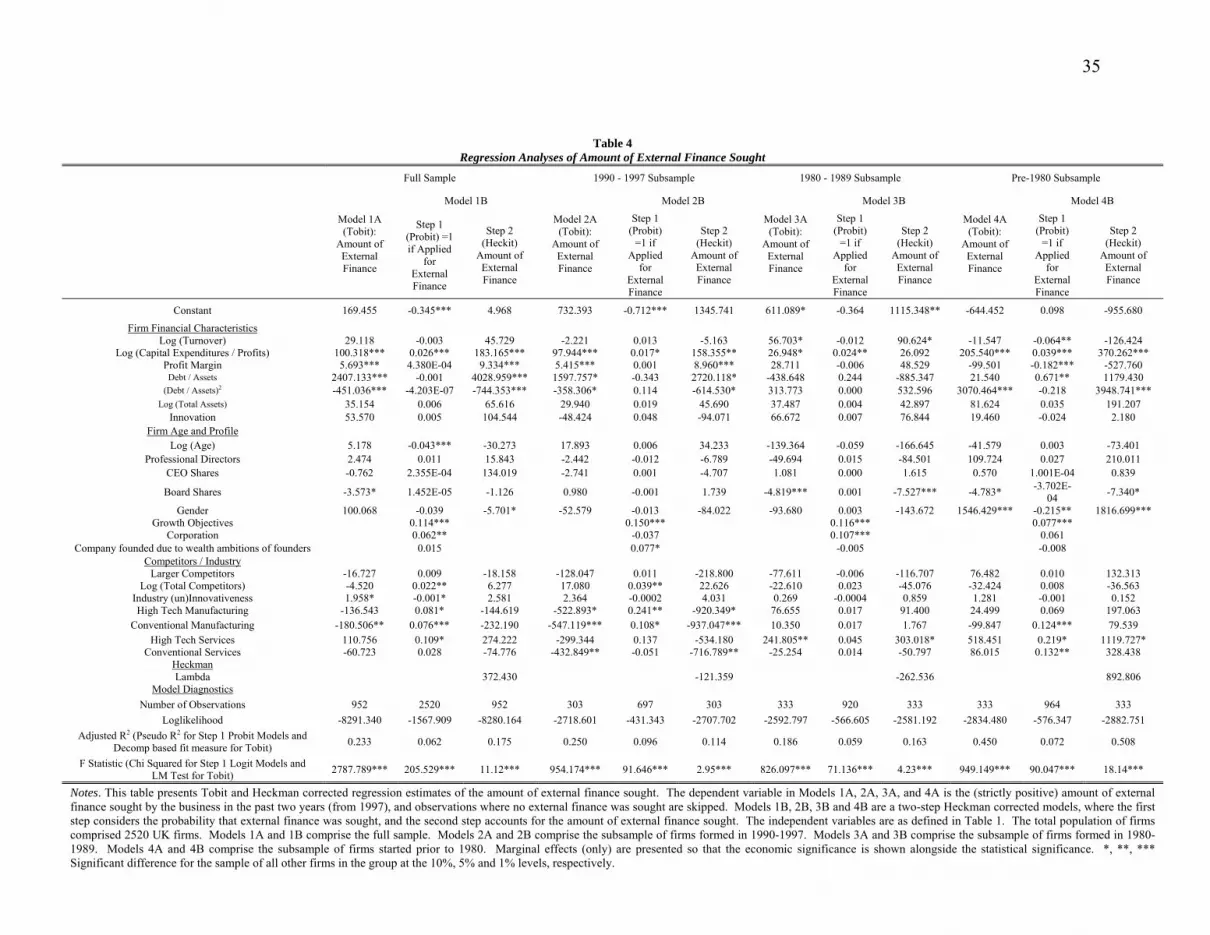

specifications in Table 4, based on variables defined in Table 1. Models 1A, 2A, 3A and 4A are Tobit

models in which the left-hand-side variable is the amount of external capital that was sought. The Tobit

specification is used to account for the fact that the left-hand-side variable is bounded below by zero. The

right-hand-side variables comprise variables for firm financial characteristics, firm age and profile and

competitors / industry, as specified in Table 4. Model 1A encompasses the full sample. Model 2A

considers the subsample of firms started in 1990-1997. Model 3A considers the subsample of firms

started in 1980-1989. Model 4A considers the subsample of firms started prior to 1980. These

subsamples are used to show robustness to different time periods for two reasons. First, we only observe

applications for external finance in 1996 and 1997, and firms started at different points in will be at

different stages in their life-cycle and thereby may have a different likelihood of applying for external

finance at any give point in time. Second, there may be survivorship bias in the typical sense that older

firms observed are the ones that survived. The different models are presented to show robustness. Except

16

where otherwise noted below, the results are quite robust (albeit in some cases less significant in the

subsamples, which is likely due to the smaller sample sizes).

Models 1B, 2B, 3B and 4B are two-step Heckman corrected models whereby the first step is a

Probit model that estimates the probability a firm applied for outside capital, and the second step is the

amount of external capital sought. The identification variables (see, e.g., Puhani, 2000) in the first step

(excluded in the second step) Heckman regression include, first, growth objectives because it is natural

that self-proclaimed growth firms (as opposed to ‘life-style’ firms) are more likely to apply for external

capital. The growth objectives variable is not included in the second step because it is a variable that is

qualitative (not easily quantifiable by the people and institutions sourcing the capital) and hence more

closely related to the decision to apply for finance rather than how much finance (entrepreneurs know that

their application for capital is evaluated on the basis of quantifiable criteria and not by their level of

ambition and hence the amount sought will more likely reflect quantitative criteria).12 By contrast, the

other variables such as capital expenditures / profits more closely capture both the decision to apply for

finance and the amount of finance sought. The second restriction is a little similar to the first, and refers

to the wealth ambitions of the founders. The rationale for this restriction is similar to the first restriction.

The third identifying restriction was whether or not the firm was incorporated (instead of a partnership or

sole proprietorship. We would expect corporations would be more likely to apply for external finance. In

earlier drafts we considered other restrictions and found results consistent with those reported here;

alternative specifications are available on request.

[Insert Table 4 About Here]

In Table 4 step (1) of Models 1B, 2B, 3B and 4B, the data indicate that firms that do seek external

finance have the following characteristics: they have lower turnover (Model 4B), higher capital

expenditures / profits (Models 1B, 2B, 3B and 4B), and higher growth objectives (Models 1B, 2B, 3B and

4B). In terms of the economic significance, a firm is approximately 1% more likely to seek external

finance when capital expenditures are 20 times that of profits relative to 10 times profits (see step 1 of

Models 1B, 2B, 3B and 4B). The relation between capital expenditures / profits and external finance

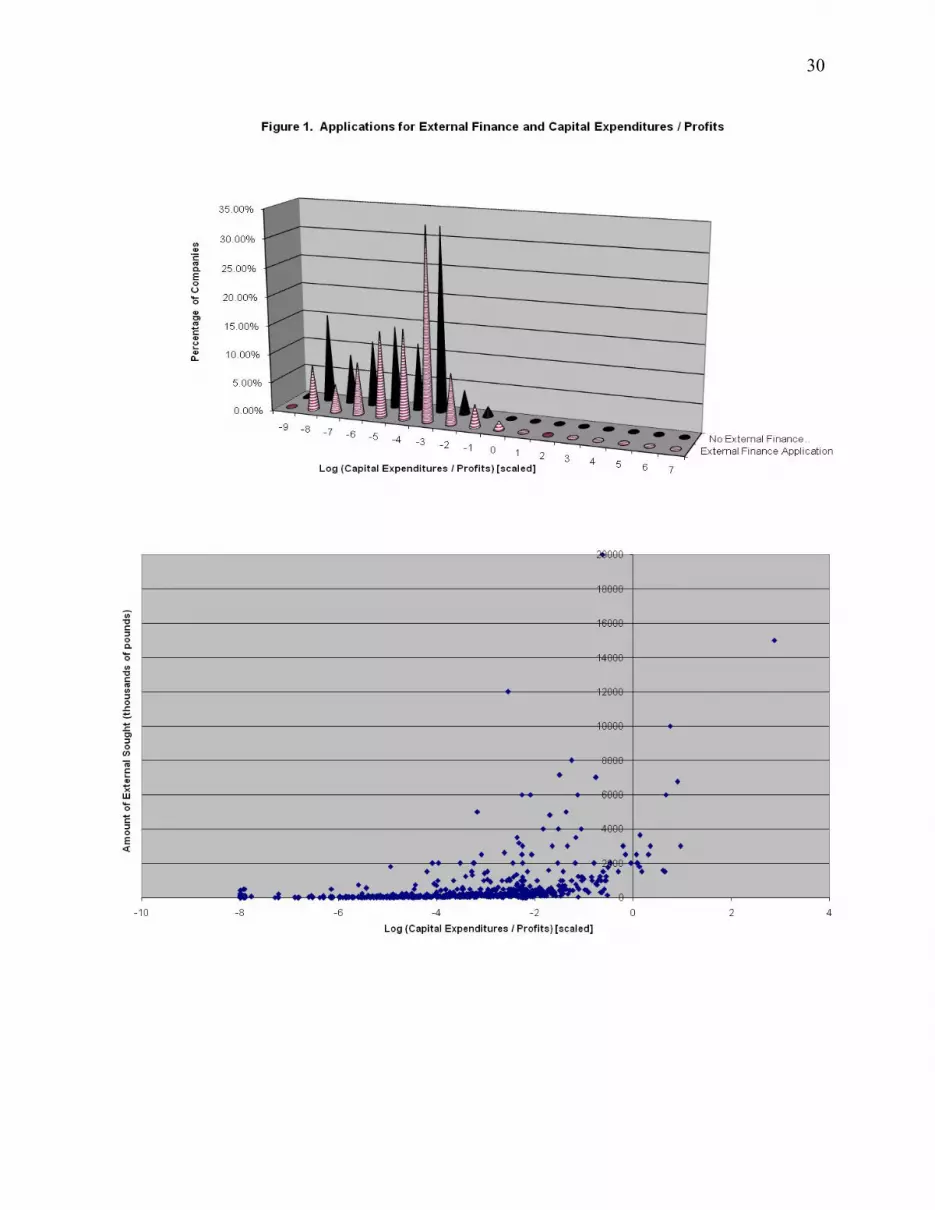

applications is also graphically illustrated in Figure 1. This indicates support for the traditional pecking

order in which firms finance new projects internally before seeking external finance (see Hypothesis 1a

outlined above in subsection 2.1). Firms applying for external finance also tend to be smaller firms (as

12 Regardless, note that we nevertheless considered the growth objectives variable for the second step and it

was insignificant and did not materially affect the other results reported in Table 4.

17

proxied by turnover) with a strong growth orientation (in support of Hypothesis 2a). The statistical

significance of the effect of turnover, however, is not robust and only significant in Model 4B which

shows that a firm with ₤1,000,000 turnover is 1.9% more likely than a firm with ₤2,000,000 turnover to

apply for external finance. The effect of growth ambition, by contrast, is robust in all of the specifications

presented in Table 4. The economic significance associated with growth ambition is such that on a

ranking from 1-4 with 4 being the highest growth orientation, an increase in the ranking by 1 point tends

to increase the probability of an application for external finance by approximately 11%.

[Insert Figure 1 About Here]

There are some differences in firm-specific and market factors that lead to applications for

external finance. Corporations are approximately 6% more likely to seek external finance that

partnerships or sole proprietorships. Firms that face 1000 competitors are approximately 2% more likely

to apply for external finance than firms that face 100 competitors. Also, Table 4 indicates industry

differences in applications for external finance.

Table 4 Models 1A, 2A, 3A, 4A and step 2 of Models 1B, 2B, 3B and 4B present regression

evidence that indicates systematic characteristics drive the amount of external finance actually sought.

The results are presented for Tobit and Heckman specifications as well as different time periods for firms’

founding dates. Note that we also considered the robustness of our results to outlier observations (as

identified by Cook’s distances and leverage plots). The results are robust. For instance, removing the

outliers apparent in Figure 2, we do not find any material differences in the regression results reported in

the Tables. Additional specifications are available on request.

[Insert Figure 2 About Here]

Table 4 shows that (with the sole exception of Model 3B) greater levels of capital expenditures /

profits give rise to firms seeking more external finance (consistent with Hypothesis 1a), and this effect is

the most statistically robust and economically significant driver of the amount of external finance sought.

The economic significance is such that a doubling of capital expenditure / profits gives rise to an

additional £55,138 in external capital sought (based on Model 1B in Table 4). The positive relation

between capital expenditures / profits and the amount of external finance sought is also depicted

graphically in the data in Figure 2. Note that we have expressed the right-hand-side variables in logs. (A

linear specification either in terms of capital expenditures / profits, or capital expenditures minus profits,

also gives rise to a statistically significant and positive relation with the amount of capital sought.) The

18

nonlinear specification models the relation as a concave specification, such that a firm’s application for

external capital increases at a decreasing rate as capital expenditures / profits increases. The intuition for

this non-linear relation is that at very high levels of capital expenditures, firms are not as likely to apply

for an equal amount of external finance as this would reduce the probability that such amounts would be

granted by the financier. This issue is further addressed in the next subsection.

There is little evidence that size is correlated with the amount of external finance sought. The

only statistically significant evidence is a positive relation between turnover and the amount of external

finance sought, but this effect is statistically significant only in Models 3A and 3B in Table 4. Assets are

unrelated to the amount of external finance sought in all specifications.

Consistent with Hypothesis 1a, the data provide evidence of a relation between profit margins and

the amount of external finance sought for the entire sample and the subsample of firms started after 1990

(Models 1A, 1B, 2A and 2B in Table 4). Profit margins, however, are negatively related to the extent of

external finance sought for older firms started before 1990 (Models 4A and 4B). These results are

perhaps explained by the fact that older firms with a longer track record exhibit comparatively less

information asymmetry for providers of external finance and thereby not be discouraged from seeking

additional capital despite lower profit margins.

We further control for the capital structure of the firm by including debt/assets as well as a

squared term for debt / assets. Generally, the data indicate via both of these variables enables that there is

an inverted U-shaped pattern in the relation between debt/assets and the amount of external finance

sought given the positive and significant coefficients for debt/assets and the negative and significant

coefficients for the squared variable for debt/assets (both effects are most robust in Models 1A, 1B, 2A

and 2B in Table 4). This inverted U-shaped relation is intuitive. Firms with a track record with providers

of external debt finance will be able to seek additional capital from those sources of capital that have

already carried out due diligence to screen out bad loans. However, firms with too much debt relative to

their asset base will be discouraged from seeking significant amounts of external capital due to increased

expected bankruptcy costs, particularly for the case of additional debt finance. As well, external sources

that had previously provided debt to the firm may have covenants in place that restrict the amount of

additional external capital that the firm can seek.

4.2. The Percentage of External Finance Obtained

Table 5 presents evidence from OLS and Heckman-corrected regressions that indicate systematic

characteristics drive the percentage of external finance obtained. The left-hand-side variable is

transformed so that it is not bounded between 0 and 100%, in a standard way of modeling fractions (see,

19

e.g., Bierens, 2003). Specifically, if Y is a dependent variable that is bounded between 0 and 1 (i.e., a

fraction), then a possible way to model the distribution of Y conditional on a vector X of predetermined

variables, including 1 for the constant term, is to assume that

)'exp(11

)'exp(1)'exp(

UXUXUXY

−−+=

+++

=ββ

β

where U is an unobserved error term. Then

UXYY +=− '))1/(ln( β

which, under standard assumptions on the error term U can be estimated by OLS.

Consistent with the presentation in Table 4, Table 5 presents eight models. Models 5A, 6A, 7A

and 8A are OLS specifications that do not account for Heckman selection effects. Models 5A, 5B, 5C

and 5D are Heckman models that do account for Heckman selection effects for the decision to seek

external finance in the first place. The first step of the Heckman corrected models in Table 5 is identical

to the first step models in Table 4. As well, as in Table 4, Table 5 also reports the models for the full

sample (Models 5A and 5B), the subsample for firms started in 1990-1997 (Models 6A and 6B), firms

started in 1980-1989 (Models (7A and 7B) and firms started prior to 1980 (Models (8A and 8B).13

[Insert Table 5 About Here]

The most robust result in Table 5 is that larger firms, in terms of their total assets, are much more

likely to obtain a higher percentage of the total amount of finance sought. This effect is statistically

significant in all of the different models presented in Table 5 (among various others considered but not

reported for reasons of succinctness). In terms of the economic significance, a firm with £1 million in

assets will obtain approximately 5% more of their desired capital than the average firm in the sample

which has assets of £375,000 (see Table 1). Overall, this shows generally that small firms tend to face a

problem in obtaining all of their desired external capital. This evidence is highly suggestive of a capital

gap. It is possible that size is correlated with unobserved features of the quality of the application for

external finance (that is, unobservable over-and-above the variables considered in the regressions 13 We considered other right-hand-side variables. For example, we considered the extent of external finance

sought, and those results (not reported for reasons of succinctness) generally showed a negative relation between the

extent of external finance sought and the percentage of finance obtained. We do not report specifications with the

extent of external finance sought as a right-hand-side variable in Table 5 because that variable is a choice variable

(analyzed as a dependent variable in Table 4 as discussed above). Regardless, the inclusion/exclusion of this

variable does not materially impact the other results reported in Table 5 and discussed immediately below.

Additional specifications are available on request.

20

presented in Table 5). The correlation between assets and the residuals in the regressions in Table 5 is

0.00 and the residuals have statistical properties that are not materially different from the normal

distribution; therefore, there is no reason to believe that size is picking up unobserved features of the

quality of the loan applications. We may infer from the data that smaller applicants in terms of size are

disadvantaged in terms of obtaining all of their desired capital.

Table 5 further indicates that a firm that recently developed a novel innovation (a technologically

new or significantly improved product) tends to obtain less of their desired capital. This effect is

statistically significant in the full sample (Models 5A and 5B and the subsample of firms started after

1990 (Models 6A and 6B). The economic significance is such that a firm that was started within 7 years

of applying for external finance and recently developed an innovation will obtain approximately 8% less

of their desired capital. Older firms started prior to 1990 that recently developed an innovation, by

contrast, do not have the same difficulties in obtaining their desired capital.

Table 5 shows older firms started prior to 1990 do nevertheless face problems in obtaining their

desired finance when they have few professional directors and/or lower profit margins. First, older firms

started prior to 1990 that do not have professional directors tend to obtain approximately 1% of their

desired finance, and this effect is statistically significant at the 10% level in Models 7A and 7B (for the

subsample of firms started in the 1980s), and significant at the 5% level in Models 8A and 8B (for the

subsample of firms started prior to 1980). Second, in regards to profit margins for firms started prior to

1980, higher profit margins are positively and significantly related to the percentage of finance obtained,

consistent with Hypothesis 1b. If profit margins increase from 0 to the mean level of 0.909 (Table 1),

then a firm is likely to increase the percentage of external capital obtained by approximately 4%.

In sum, the evidence in Table 5 shows asset sizes matter most for obtaining the desired level of

external finance. Small firms that have recently developed a novel innovation tend to obtain less of their

desired capital. This is expected as smaller innovative firms exhibit more pronounced information

asymmetries when applying for external capital. Larger firms that do not have professional directors

and/or are less profitable tend to obtain less of their desired finance. This is also expected as larger firms

that have not put in place professional governance mechanisms and/or are less financially successful are

less attractive candidates for external finance. The next section below considers whether there are

differences in firms’ ability to obtain their desired finance across the different sources of capital.

4.3. Differences across Alternative Sources of Capital

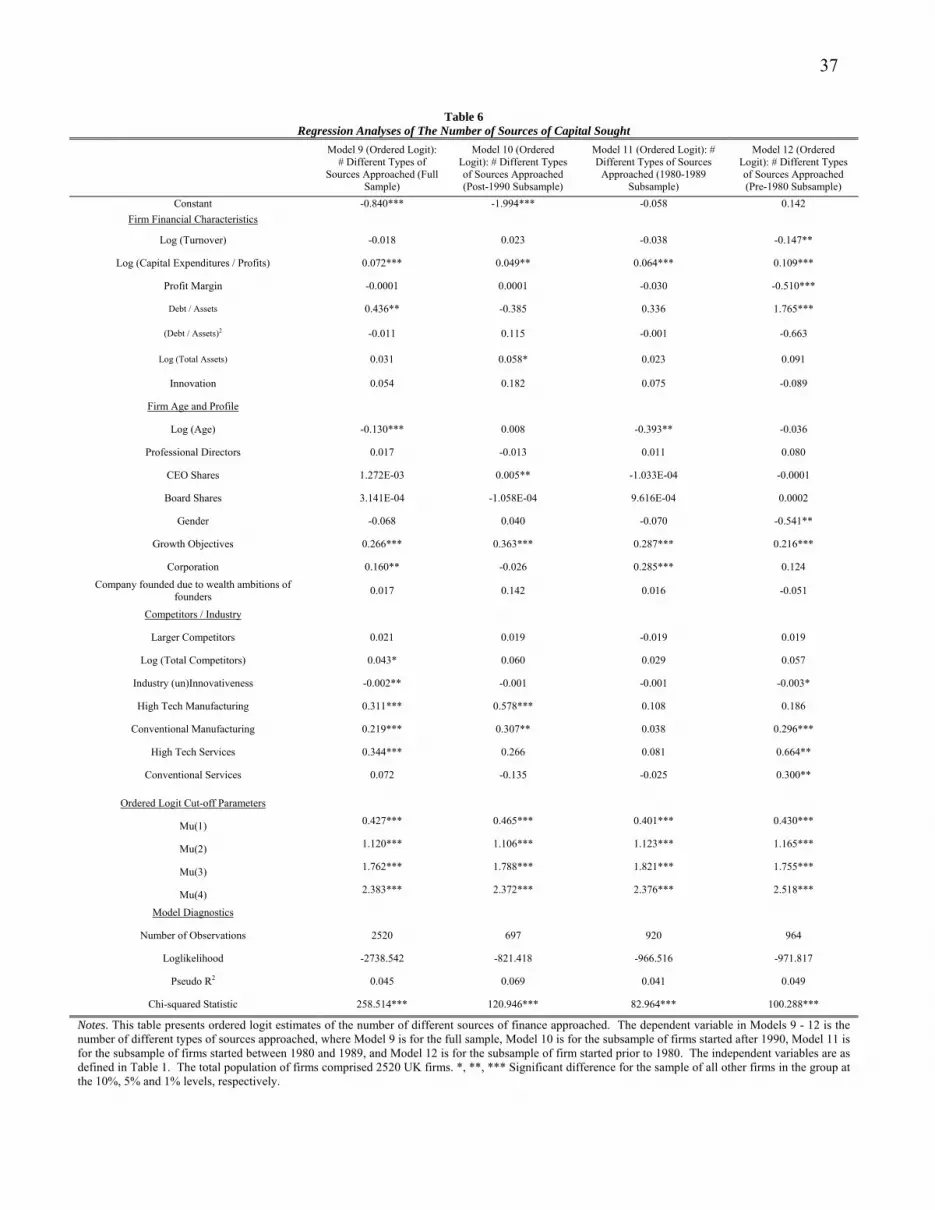

Before formally examining specific sources of capital, we first consider ordered logit evidence on the

number of different sources of capital sought in Table 6. This evidence in Table 6 provides a context in

21

which to examine differences across different sources of capital. The evidence in Table 6 is strongly

consistent with Hypothesis 2a. Firms with significant growth objectives are more likely to approach a

greater number of sources of capital, and this effect is statistically significant at the 1% level in each of

the Models 9-12. A firm with a higher ranking by 1 on a scale of 1-4 is approximately 1% more likely to

apply to an additional type of source of capital. This is economically significant in view of the fact that

among the 952 of 2520 firms that did apply for external finance, the median number of different sources

approached was 2 (and mean was 1.96) (Tables 1 and 2).

[Insert Table 6 About Here]

Also, much of the evidence in Table 6 is strongly consistent with Hypothesis 3. First, firms are

more likely to approach a greater number of different sources of capital when their capital expenditures /

profits are greater, as shown in all specifications in Table 6. This is consistent with Hypothesis 3.

Second, there is evidence from Model 12 in Table 6 for firms started before 1980 with lower profit

margins must approach a greater number of different sources of external capital. It is natural that new

firms may not yet have achieved profitability and hence current profit margins are less important for

external finance for young firms relative to their more established counterparts. Third, firms with higher

levels of debt / assets approach a greater number of different sources of capital for the full sample (Model

17) and the subsample of firms started before 1980. As with profit margins, we would expect debt/asset

levels to play a pronounced role in external capital for more established firms.

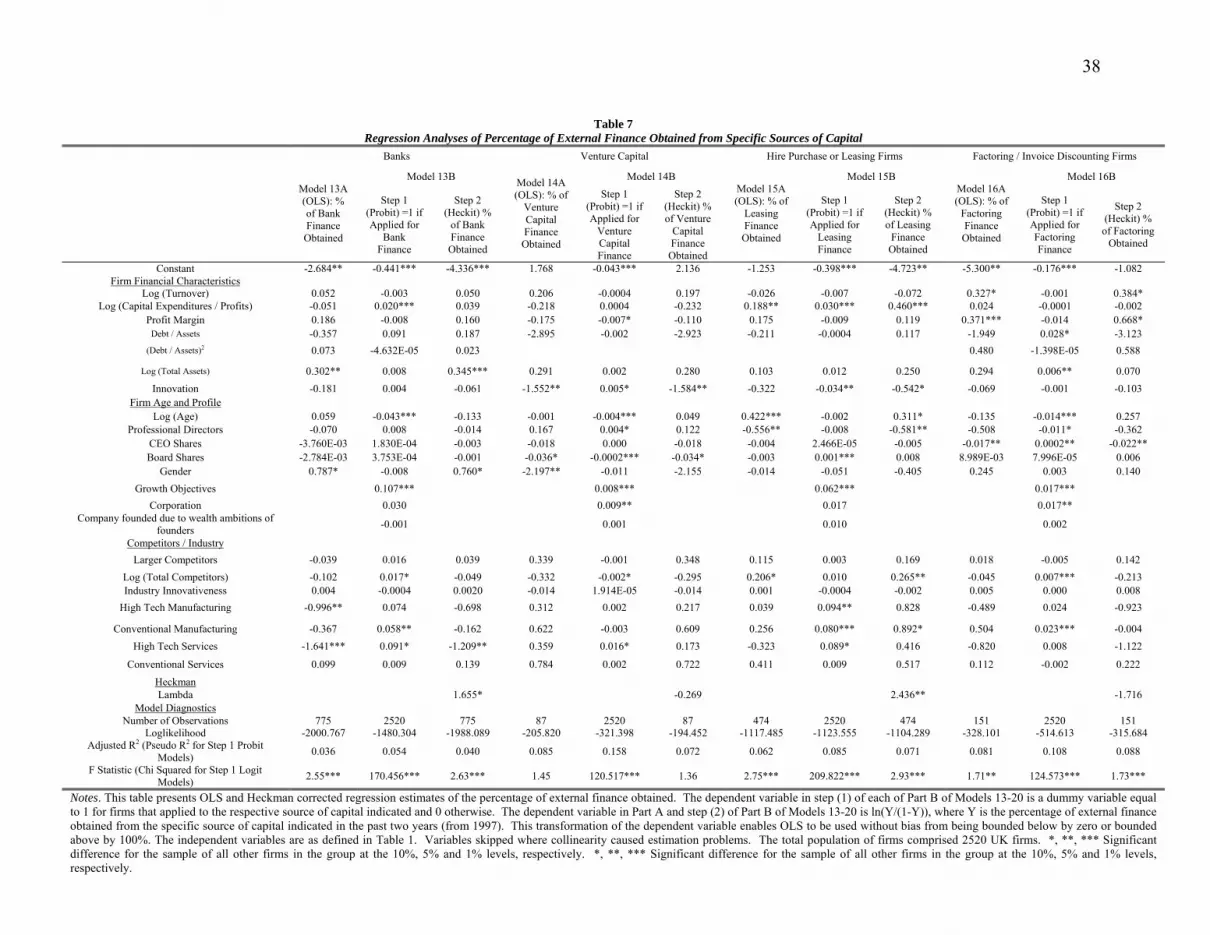

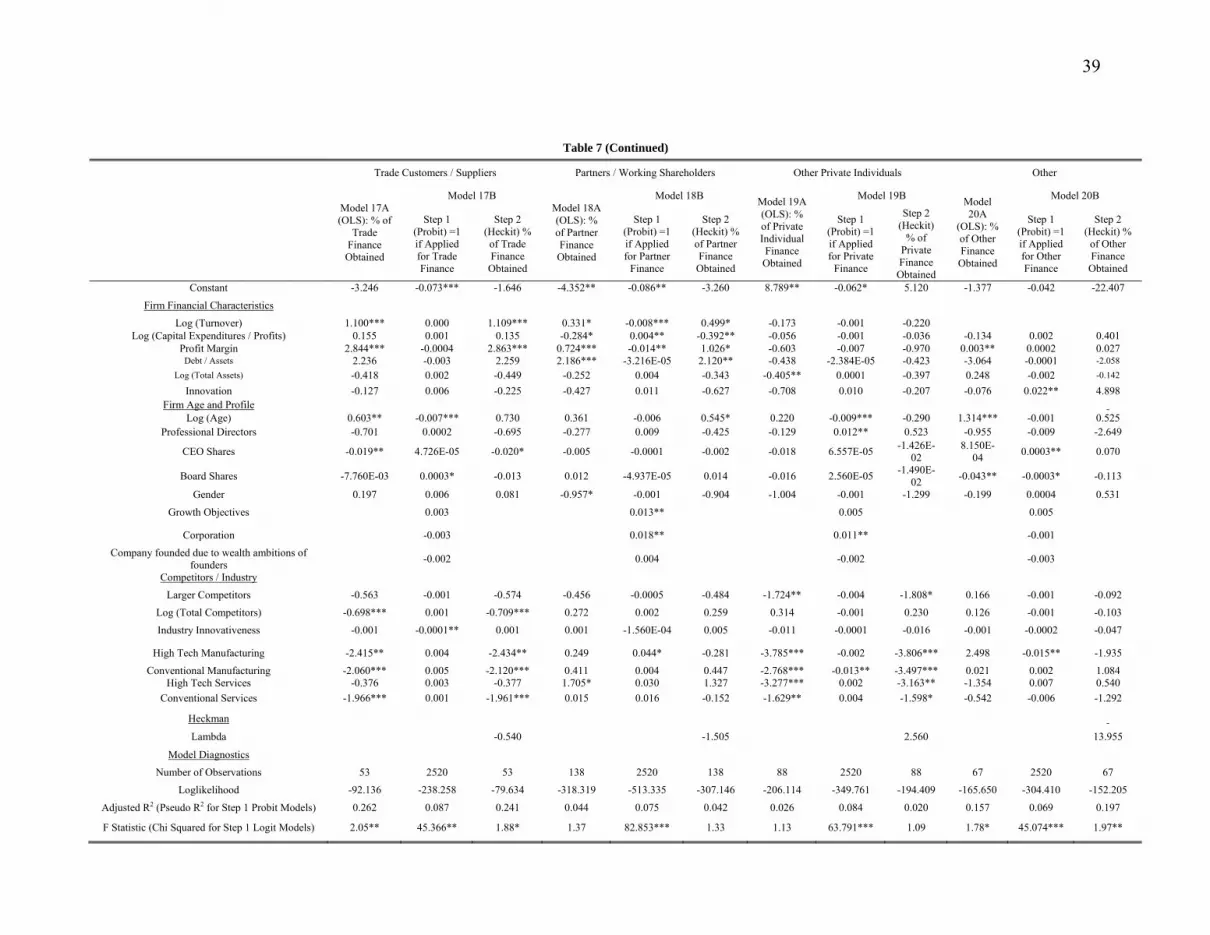

Table 7 Panels A and B explores further the issues addressed above by considering the

differences between banks, venture capital funds, hire purchase / leasing firms, factoring / invoice

discounting firms, trade customers / suppliers, partners / working shareholders, private individuals and

other sources of capital. 14 As discussed above in subsection 2.1 (Hypothesis 2b), among the

approximately 38% of 2520 firms in our sample that did seek external finance in the 1996-1997 period

considered, 775 approached banks, and only 87 approached venture capital funds (the other sources

approached were identified in section 2 and Table 2 above). Outright rejection rates were highest among

venture capital funds (46% rejection), and much higher than that for banks (17% outright rejection).

Table 7 addresses in a multivariate context whether the factors leading to financing by these distinct

sources were materially different across each of the 8 different sources of capital. 14 Models 13-20 are presented for the full sample of firms. The results from the subsamples by different years

in which the firms were founded did not give rise to materially different inferences that could be drawn from the

data, and are hence excluded for reasons of succinctness (otherwise there were be an extra 24 regression models).

These regression results are nevertheless available on request.

22

[Insert Table 7 About Here]

Table 7 presents in Part A OLS models for the percentage of external capital obtained from each

particular source of finance. Also, to show robustness, Table 7 presents in Part B Heckman-corrected

estimates of the percentage of external capital obtained from each of the 8 different sources of capital.

The first step of Part B of each Model for the Heckman regressions is a probit model that determines

whether the firm sought external capital from the particular source in question. The percentage term left-

hand-side variables make use of the transformation as described in Table 5 and accompanying text above.

Likewise, the right-hand-side variable specifications are consistent with Table 5.

The Part B Step 1 regressions in Table 7 show firms with significant growth objectives are more

likely to apply for external finance from banks, venture capital funds, leasing firms, factoring/invoice

discounting firms and partners/working shareholders. This is consistent with Hypothesis 2a that growth

objectives are a significant determinant of the decision to seek external capital. In the Part B Step 1

regressions in Table 7 there are also notable differences in terms of which firms apply for different types

of finance. Firms with greater capital expenditures / profits are only more likely to apply for bank

finance, lease finance and partner/working shareholder finance and not finance from other types of

sources of capital. These results are consistent with Hypotheses 1a and 2b. Bank and lease finance are

sources of debt capital, and we conjectured that entrepreneurs generally seek debt prior to equity in order

to avoid dilution of their ownership shares. Partner/working shareholder finance is external capital, but

capital from preexisting sources that had already financed the firm. Partners/working shareholders face

fewer information asymmetries relative to other sources of capital in carrying out due diligence as

partners/working shareholders have a relationship with the firm. The cost of external capital is smaller

when information problems are less pronounced. As well, note that less profitable firms are more likely

to apply for venture capital and partner/working shareholder finance. This is expected since venture

capital funds are partners/working shareholders are better able to carry out due diligence and mitigate

adverse selection problems than other sources of capital.

The Part A and Step 2 of Part B regressions in Table 7 consider the percentage of finance

obtained. Consistent with Hypothesis 1b, profit margins are a statistically significant variable for

successfully obtaining the desired amount of external finance from factoring/invoice discounting firms,

trade customers/suppliers and partners/working shareholders, but not the other sources of capital.

Larger firms in terms of asset sizes are more likely to obtain bank finance, but asset size does not

impact the percentage of finance obtained from other sources. In terms of the economic significance, a

firm with £1 million in assets will obtain approximately 8% more of their desired capital than the average

23

firm in the sample which has assets of £375,000 (see Table 1). Problems associated with capital gaps for

smaller firms are therefore pronounced with banks, but this positive relation between assets and

percentage of desired capital obtained is not statistically significant with other sources of capital. By

contrast, in the case of private individuals as a source of capital there is even evidence that smaller firms

obtain a higher proportion of their desired capital (Model 19A), but this effect is not statistically

significant after controlling for selection effects. The models are more robust in showing private

individuals provide a greater percentage of their desired capital to smaller firms facing larger competitors.

Banks provide high tech services firms with 28% less of their desired capital. This result is

consistent with Hypothesis 2b in that banks provide less capital to smaller risky ventures. Further, the

data indicate that banks provide male founded firms with 18% less of their desired capital relative to

female founded firms. There is much evidence (e.g., Jianakoplos and Bernasek, 1998) that females are

more risk averse than males, and hence this evidence is consistent with the prediction in Hypothesis 2b

that banks provide less capital to riskier ventures.

It is noteworthy from the Part B Step 1 regressions in Table 7 that firms that recently developed a

new innovation are more likely to apply for venture capital finance, consistent with Hypothesis 2b.

Venture capital funds attract innovative companies that require value-added assistance and exhibit high

information asymmetries and growth prospects (e.g., Berger and Udell, 2002; Carpenter and Peterson,

2002; Cressy, 1996, 2002). Also, the data show venture capital is more sought after by younger firms

with professional directors and more intensive growth objectives (Step 1 of Model 14B). This is intuitive

as professional directors provide the governance required to mitigate information asymmetries and agency

costs associated with financing early stage high-tech companies (Gompers and Lerner, 1999). However,

venture capital funds provide firms with 4% less of their desired capital when they have recently

developed a new innovation. Venture capital funds invariably stage their investments, and stage more

frequently for high-tech innovative firms, in order to mitigate information asymmetries and agency costs.

When the board members hold a greater percentage of the equity shares in the firm, venture

capital funds provide a smaller percentage of the desired capital. A change from the mean level of 86%

equity held by the board to 50%, for example, increases the percentage of desired finance provided by

venture capitalists by approximately 8%. This result is likely attributable to the fact that venture

capitalists demand significant equity shares in their firms and a reduction in equity held by board

members implies there is greater scope for outside equity to be sold to the venture capitalists. A greater

equity share held by the CEO, however, does not reduce the percentage of venture capital obtained as it is

relatively more important to maintain a high CEO ownership share to mitigate moral hazard problems.

In sum, the evidence in Table 7 shows there are systematic differences in firms’ ability to obtain

their desired capital in the form that they would like. Even after controlling for selection effects, the data

24

indicate banks are more likely to provide the desired amount of capital to larger firms with more assets.

Leasing firms, factor discounting / invoicing firms, trade customers / suppliers and partners / working

shareholders are more likely to provide the desired capital to firms with higher profit margins. The data

further show smaller firms are more likely to obtain finance from private individuals, and innovative

firms seek external capital from venture capital funds. These results are generally consistent with the

hypotheses set out in subsection 2.1 above.

5. Additional Robustness Checks, Extensions and Future Research

This paper introduced a very expansive and detailed new dataset which significantly extends the literature

on the financing decisions of entrepreneurial firms. The data are quite unique in that they are derived

from the entrepreneurial firms themselves, and not the financial institutions that provided the financing.

This enables a broad perspective on which firms seek external finance, from which types of institutions

do they seek capital, how much is sought, and how much is obtained. The data enable selection effects in

the spirit of Heckman (1976, 1979) to be considered in a unique way in the literature on entrepreneurial

capital sourcing decisions.

The introduction of new data invariably gives rise to questions about sample selection and

robustness. However in this case we have a very large sample spanning the full size range of small and

medium sized entrepreneurial firms which is free from response bias in terms of key finance related

factors such as size age or profitability. Complete details on survey design and sample selection issues

are provided in Bullock and Hughes (1998). In our econometric tests we explicitly considered sample

selection issues with regard to different types of firms applying for external finance among other things.

The robustness of our results was explicitly considered. Additional details regarding the data and

additional econometric tests are available on request.

It is noteworthy that our data are derived from a “snapshot” of a cross-section of entrepreneurial

firms in period leading up to 1997. The CBR data used here are however part of a unique panel data set

which tracks the same firms through time. In future work with we will to exploit this aspect of the data to

see what happened to the businesses in subsequent years after they obtained external finance. How was

the money spent? Did some firms fail in subsequent years due to the fact that they did not obtain all of

their requisite capital? Did obtaining external finance enable the businesses to become more profitable in

the years subsequent to obtaining external finance?

Our data indicated an absence of a capital gap in that most firms applying for external finance

were able to obtain their requisite capital. As such there does not appear to be a generic finance gap in the

UK entrepreneurial business sector, at least in terms of the quantity of external finance available in the

25

market. Nevertheless, the ex post analysis of the impact of external finance on subsequent entrepreneurial

firm performance (which would be post-1997 in our data, for example), would shed light on the quality of

external finance (in the spirit of Storey and Wynarczyk, 1996). While that type of ex post question poses

some interesting issues worthy of future data collection efforts, we must leave it for future research.

6. Summary and Conclusion

This paper investigated the internal versus external financing decisions among a very unique dataset

comprising 2520 early stage privately held UK firms in 1996-1997. We first identified factors that lead

firms to seek external finance. The most robust evidence indicated that firms with higher capital

expenditures / profits and firms with stronger growth objectives were much more likely to seek external

finance. We then demonstrated the existence of systematic differences in the amount of external finance

actually sought across businesses. We found a strong and robust relation between a firm’s capital

expenditures / profits and the amount of external finance actually sought. Overall, we view the evidence

as providing strong support for the traditional pecking order theory which predicts that firms prefer to

finance new projects internally prior to seeking external capital.

The data also indicated systematic differences in the percentage of external finance obtained

relative to that sought in ways that are consistent with information asymmetries faced by providers of

external capital. Smaller firms are more likely to obtain finance from private individuals. By contrast,

even after controlling for selection effects, one of the most important factors in regards to obtaining the

desired level of bank finance is a firm’s assets. Small firms without significant assets have difficulty

obtaining bank finance. Young, high growth innovative firms without significant assets or profits seek

capital from venture capital funds, but venture capital is not widely available and rejection rates are quite

high. High profits are not important for obtaining venture capital but are important for obtaining the

desired capital from leasing firms, factor discounting / invoicing firms, trade customers / suppliers and

partners / working shareholders.

We noted that, among the 38% of firms that made non-trivial efforts to obtain external finance in