Embed Size (px)

Citation preview

Statement of Financial AccountingStandards No. 52

Foreign Currency Translation

Financial Accounting Standards Board

ORIGINAL

PRONOUNCEMENTS

AS AMENDED

Copyright © 2010 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be repro-duced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, with-out the prior written permission of the Financial Accounting Foundation.

Statement of Financial Accounting Standards No. 52Foreign Currency Translation

STATUS

Issued: December 1981

Effective Date: For fiscal years beginning on or after December 15, 1982

Affects: Amends ARB 43, Chapter 12, paragraph 5Deletes ARB 43, Chapter 12, paragraphs 7 and 10 through 22Deletes APB 6, paragraph 18Amends APB 22, paragraph 13Supersedes FAS 1Supersedes FAS 8Supersedes FAS 20Supersedes FIN 15Supersedes FIN 17

Affected by: Paragraph 13 amended by FAS 130, paragraph 29Paragraph 14A added by FAS 133, paragraph 527(a)Paragraphs 15, 16, 31(b), and 162 amended by FAS 133, paragraphs 527(b), 527(c), 527(g), and

527(h), respectivelyParagraphs 17 through 19 deleted by FAS 133, paragraph 527(d)Paragraph 21 replaced by FAS 133, paragraph 527(e)Paragraphs 22 and 23 amended by FAS 96, paragraph 204, and FAS 109, paragraph 287Paragraph 24 amended by FAS 96, paragraph 204; FAS 109, paragraph 287; and FAS 135,paragraph 4(l)

Paragraphs 26, 31, 34, and 46 amended by FAS 135, paragraph 4(l)Paragraph 30 amended by FAS 133, paragraph 527(f), and FAS 161, paragraph 4Paragraph 45 amended by FAS 154, paragraph C10Paragraph 48 amended by FAS 96, paragraph 205(p); FAS 109, paragraph 288(r); and FAS 142,paragraph D6

Paragraph 101 effectively amended by FAS 141, paragraphs 44 through 46, and amended byFAS 141(R), paragraph E15, and FAS 164, paragraph E6

Other Interpretive Pronouncement: FIN 37

AICPAAccounting Standards Executive Committee (AcSEC)

Related Pronouncement: SOP 93-4

Issued Discussed by FASB Emerging Issues Task Force (EITF)

Affects: No EITF Issues

Interpreted by: Paragraph 11 interpreted by EITF Topic No. D-55Paragraph 13 interpreted by EITF Issue No. 01-5Paragraph 15 interpreted by EITF Issue No. 96-15Paragraph 21 interpreted by EITF Issue No. 97-7Paragraph 26 interpreted by EITF Topic No. D-12Paragraph 46 interpreted by EITF Issues No. 92-4 and 92-8 and Topic No. D-56

Related Issues: EITF Issues No. 87-12, 88-18, and 96-11 and Topics No. D-4 and D-71

FAS52

FAS52–1

SUMMARY

Application of this Statement will affect financial reporting of most companies operating in foreign coun-tries. The differing operating and economic characteristics of varied types of foreign operations will be distin-guished in accounting for them. Adjustments for currency exchange rate changes are excluded from net in-come for those fluctuations that do not impact cash flows and are included for those that do. The requirementsreflect these general conclusions:

• The economic effects of an exchange rate change on an operation that is relatively self-contained andintegrated within a foreign country relate to the net investment in that operation. Translation adjustmentsthat arise from consolidating that foreign operation do not impact cash flows and are not included in netincome.

• The economic effects of an exchange rate change on a foreign operation that is an extension of the parent’sdomestic operations relate to individual assets and liabilities and impact the parent’s cash flows directly.Accordingly, the exchange gains and losses in such an operation are included in net income.

• Contracts, transactions, or balances that are, in fact, effective hedges of foreign exchange risk will be ac-counted for as hedges without regard to their form.

More specifically, this Statement replaces FASB Statement No. 8, Accounting for the Translation of For-eign Currency Transactions and Foreign Currency Financial Statements, and revises the existing accountingand reporting requirements for translation of foreign currency transactions and foreign currency financial state-ments. It presents standards for foreign currency translation that are designed to (1) provide information that isgenerally compatible with the expected economic effects of a rate change on an enterprise’s cash flows andequity and (2) reflect in consolidated statements the financial results and relationships as measured in the pri-mary currency in which each entity conducts its business (referred to as its “functional currency”).

An entity’s functional currency is the currency of the primary economic environment in which that entityoperates. The functional currency can be the dollar or a foreign currency depending on the facts. Normally, itwill be the currency of the economic environment in which cash is generated and expended by the entity. Anentity can be any form of operation, including a subsidiary, division, branch, or joint venture. The Statementprovides guidance for this key determination in which management’s judgment is essential in assessing thefacts.

A currency in a highly inflationary environment (3-year inflation rate of approximately 100 percent ormore) is not considered stable enough to serve as a functional currency and the more stable currency of thereporting parent is to be used instead.

The functional currency translation approach adopted in this statement encompasses:

a. Identifying the functional currency of the entity’s economic environmentb. Measuring all elements of the financial statements in the functional currencyc. Using the current exchange rate for translation from the functional currency to the reporting currency, if

they are differentd. Distinguishing the economic impact of changes in exchange rates on a net investment from the impact of

such changes on individual assets and liabilities that are receivable or payable in currencies other than thefunctional currency.

Translation adjustments are an inherent result of the process of translating a foreign entity’s financial state-ments from the functional currency to U.S. dollars. Translation adjustments are not included in determining netincome for the period but are disclosed and accumulated in a separate component of consolidated equity untilsale or until complete or substantially complete liquidation of the net investment in the foreign entity takesplace.

Transaction gains and losses are a result of the effect of exchange rate changes on transactions denominatedin currencies other than the functional currency (for example, a U.S. company may borrow Swiss francs or aFrench subsidiary may have a receivable denominated in kroner from a Danish customer). Gains and losses onthose foreign currency transactions are generally included in determining net income for the period in whichexchange rates change unless the transaction hedges a foreign currency commitment or a net investment in aforeign entity. Intercompany transactions of a long-term investment nature are considered part of a parent’s netinvestment and hence do not give rise to gains or losses.

FAS52 FASB Statement of Standards

FAS52–2

Statement of Financial Accounting Standards No. 52

Foreign Currency Translation

CONTENTS

ParagraphNumbers

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1− 3Standards of Financial Accounting and Reporting:

Objectives of Translation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4The Functional Currency. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5− 10The Functional Currency in Highly Inflationary Economies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Translation of Foreign Currency Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12− 14Foreign Currency Transactions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14A− 16Forward Exchange Contracts [Deleted]Transaction Gains and Losses to Be Excluded from Determination of Net Income . . . . . . . . . . . . . . 20Hedges of Firm Commitments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Income Tax Consequences of Rate Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22− 24Elimination of Intercompany Profits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Exchange Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26− 28Use of Averages or Other Methods of Approximation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30− 32Effective Date and Transition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33− 38

Appendix A: Determination of the Functional Currency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39− 46Appendix B: Remeasurement of the Books of Record into the Functional Currency . . . . . . . . . . . . . . . . 47− 54Appendix C: Basis for Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55−149Appendix D: Background Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150−161Appendix E: Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

INTRODUCTION

1. FASB Statement No. 8, Accounting for the Trans-lation of Foreign Currency Transactions and ForeignCurrency Financial Statements, was issued in Octo-ber 1975 and was effective for fiscal years that beganon or after January 1, 1976. In May 1978, the Boardissued an invitation for public comment on State-ments 1−12, each of which had been in effect for atleast two years. Foreign currency translation* wasthe subject of most of the comments received. InJanuary 1979, the Board added to its agenda a projectto reconsider Statement 8. This Statement is the re-sult of that project.

2. This Statement establishes revised standards of fi-nancial accounting and reporting for foreign cur-rency transactions in financial statements of a re-

porting enterprise (hereinafter, enterprise). It alsorevises the standards for translating foreign currencyfinancial statements (hereinafter, foreign currencystatements) that are incorporated in the financialstatements of an enterprise by consolidation, combi-nation, or the equity method of accounting. Transla-tion of financial statements from one currency to an-other for purposes other than consolidation,combination, or the equity method is beyond thescope of this Statement. For example, this Statementdoes not cover translation of the financial statementsof an enterprise from its reporting currency into an-other currency for the convenience of readers accus-tomed to that other currency.

3. This Statement supersedes FASB StatementNo. 8, Accounting for the Translation of Foreign

*Terms defined in the glossary (Appendix E) are in boldface type the first time they appear in this Statement.

FAS52Foreign Currency Translation

FAS52–3

Currency Transactions and Foreign Currency Finan-cial Statements,1 FASB Statement No. 20, Account-ing for Forward Exchange Contracts, FASB Inter-pretation No. 15, Translation of Unamortized PolicyAcquisition Costs by a Stock Life Insurance Com-pany, and FASB Interpretation No. 17, Applying theLower of Cost or Market Rule in Translated Finan-cial Statements.

STANDARDS OF FINANCIALACCOUNTINGAND REPORTING

Objectives of Translation

4. Financial statements are intended to present infor-mation in financial terms about the performance, fi-nancial position, and cash flows of an enterprise. Forthis purpose, the financial statements of separate en-tities within an enterprise, which may exist and oper-ate in different economic and currency environments,are consolidated and presented as though they werethe financial statements of a single enterprise. Be-cause it is not possible to combine, add, or subtractmeasurements expressed in different currencies, it isnecessary to translate into a single reporting cur-rency2 those assets, liabilities, revenues, expenses,gains, and losses that are measured or denominatedin a foreign currency.3 However, the unity pre-sented by such translation does not alter the underly-ing significance of the results and relationships of theconstituent parts of the enterprise. It is only throughthe effective operation of its constituent parts that theenterprise as a whole is able to achieve its purpose.Accordingly, the translation of the financial state-ments of each component entity of an enterpriseshould accomplish the following objectives:

a. Provide information that is generally compatiblewith the expected economic effects of a ratechange on an enterprise’s cash flows and equity

b. Reflect in consolidated statements the financialresults and relationships of the individual consoli-dated entities as measured in their functionalcurrencies in conformity with U.S. generally ac-cepted accounting principles.

The Functional Currency

5. The assets, liabilities, and operations of a foreignentity shall be measured using the functional cur-rency of that entity. An entity’s functional currency isthe currency of the primary economic environment inwhich the entity operates; normally, that is the cur-rency of the environment in which an entity primarilygenerates and expends cash. Appendix A providesguidance for determination of the functional cur-rency. The economic factors cited in Appendix A,and possibly others, should be considered both indi-vidually and collectively when determining the func-tional currency.

6. For an entity with operations that are relativelyself-contained and integrated within a particularcountry, the functional currency generally would bethe currency of that country. However, a foreign enti-ty’s functional currency might not be the currency ofthe country in which the entity is located. For ex-ample, the parent’s currency generally would be thefunctional currency for foreign operations that are adirect and integral component or extension of theparent company’s operations.

7. An entity might have more than one distinct andseparable operation, such as a division or branch, in

1The following pronouncements, which were superseded or amended by Statement 8, are also superseded or amended by this Statement: para-graphs 7 and 10–22 of Chapter 12, “Foreign Operations and Foreign Exchange,” of ARB No. 43; paragraph 18 of APB Opinion No. 6, Status ofAccounting Research Bulletins; and FASB Statement No. 1, Disclosure of Foreign Currency Translation Information. The last sentence of para-graph 5 of ARB 43, Chapter 12, is amended to delete “and they should be reserved against to the extent that their realization in dollars appears tobe doubtful,” and paragraph 13 of APB Opinion No. 22, Disclosure of Accounting Policies, is amended to delete “translation of foreign curren-cies” as an example of disclosure “commonly required with respect to accounting policies.”2For convenience, this Statement assumes that the enterprise uses the U.S. dollar (dollar) as its reporting currency. However, a currency otherthan the dollar may be the reporting currency in financial statements that are prepared in conformity with U.S. generally accepted accountingprinciples. For example, a foreign enterprise may report in its local currency in conformity with U.S. generally accepted accounting principles.If so, the requirements of this Statement apply.3To measure in foreign currency is to quantify an attribute of an item in a unit of currency other than the reporting currency.Assets and liabilitiesare denominated in a foreign currency if their amounts are fixed in terms of that foreign currency regardless of exchange rate changes.An asset orliability may be both measured and denominated in one currency, or it may be measured in one currency and denominated in another. To illus-trate: Two foreign branches of a U.S. company, one Swiss and one German, purchase identical assets on credit from a Swiss vendor at identicalprices stated in Swiss francs. The German branch measures the cost (an attribute) of that asset in German marks. Although the correspondingliability is also measured in marks, it remains denominated in Swiss francs since the liability must be settled in a specified number of Swissfrancs. The Swiss branch measures the asset and liability in Swiss francs. Its liability is both measured and denominated in Swiss francs. Al-though assets and liabilities can be measured in various currencies, rights to receive or obligations to pay fixed amounts of a currency are, bydefinition, denominated in that currency.

FAS52 FASB Statement of Standards

FAS52–4

which case each operation may be considered a sepa-rate entity. If those operations are conducted in differ-ent economic environments, they might have differ-ent functional currencies.

8. The functional currency (or currencies) of an en-tity is basically a matter of fact, but in some instancesthe observable facts will not clearly identify a singlefunctional currency. For example, if a foreign entityconducts significant amounts of business in two ormore currencies, the functional currency might notbe clearly identifiable. In those instances, the eco-nomic facts and circumstances pertaining to a par-ticular foreign operation shall be assessed in relationto the Board’s stated objectives for foreign currencytranslation (paragraph 4). Management’s judgmentwill be required to determine the functional curren-cy in which financial results and relationships aremeasured with the greatest degree of relevance andreliability.

9. Once the functional currency for a foreign entityis determined, that determination shall be used con-sistently unless significant changes in economic factsand circumstances indicate clearly that the functionalcurrency has changed. Previously issued financialstatements shall not be restated for any change in thefunctional currency.

10. If an entity’s books of record are not maintainedin its functional currency, remeasurement into thefunctional currency is required. That remeasurementis required before translation into the reporting cur-rency. If a foreign entity’s functional currency is thereporting currency, remeasurement into the reportingcurrency obviates translation. The remeasurementprocess is intended to produce the same result as ifthe entity’s books of record had been maintained inthe functional currency. The remeasurement of andsubsequent accounting for transactions denominatedin a currency other than the functional currency shallbe in accordance with the requirements of this State-ment (paragraphs 15 and 16). Appendix B providesguidance for remeasurement into the functionalcurrency.

The Functional Currency in Highly InflationaryEconomies

11. The financial statements of a foreign entity in ahighly inflationary economy shall be remeasured asif the functional currency were the reporting cur-rency. Accordingly, the financial statements of thoseentities shall be remeasured into the reporting cur-

rency according to the requirements of paragraph 10.For the purposes of this requirement, a highly infla-tionary economy is one that has cumulative inflationof approximately 100 percent or more over a 3-yearperiod.

Translation of Foreign Currency Statements

12. All elements of financial statements shall betranslated by using a current exchange rate. For as-sets and liabilities, the exchange rate at the balancesheet date shall be used. For revenues, expenses,gains, and losses, the exchange rate at the dates onwhich those elements are recognized shall be used.Because translation at the exchange rates at the datesthe numerous revenues, expenses, gains, and lossesare recognized is generally impractical, an appropri-ately weighted average exchange rate for the periodmay be used to translate those elements.

13. If an entity’s functional currency is a foreign cur-rency, translation adjustments result from the proc-ess of translating that entity’s financial statementsinto the reporting currency. Translation adjustmentsshall not be included in determining net income butshall be reported in other comprehensive income.

14. Upon sale or upon complete or substantiallycomplete liquidation of an investment in a foreignentity, the amount attributable to that entity and accu-mulated in the translation adjustment component ofequity shall be removed from the separate compo-nent of equity and shall be reported as part of the gainor loss on sale or liquidation of the investment for theperiod during which the sale or liquidation occurs.

Foreign Currency Transactions

14A. FASB Statement No. 133, Accounting for De-rivative Instruments and Hedging Activities, ad-dresses the accounting for freestanding foreign cur-rency derivatives and certain foreign currencyderivatives embedded in other instruments. ThisStatement does not address the accounting for deriva-tive instruments.

15. Foreign currency transactions are transactionsdenominated in a currency other than the entity’sfunctional currency. Foreign currency transactionsmay produce receivables or payables that are fixed interms of the amount of foreign currency that will bereceived or paid.Achange in exchange rates betweenthe functional currency and the currency in which atransaction is denominated increases or decreases the

FAS52Foreign Currency Translation

FAS52–5

expected amount of functional currency cash flowsupon settlement of the transaction. That increase ordecrease in expected functional currency cash flowsis a foreign currency transaction gain or loss thatgenerally shall be included in determining net in-come for the period in which the exchange ratechanges. Likewise, a transaction gain or loss (meas-ured from the transaction date or the most recent in-tervening balance sheet date, whichever is later) real-ized upon settlement of a foreign currencytransaction generally shall be included in determin-ing net income for the period in which the transactionis settled. The exceptions to this requirement for in-clusion in net income of transaction gains and lossesare set forth in paragraph 20 and pertain to certain in-tercompany transactions and to transactions that aredesignated as, and effective as, economic hedges ofnet investments.

16. For other than derivative instruments (State-ment 133), the following shall apply to all for-eign currency transactions of an enterprise and itsinvestees:

a. At the date the transaction is recognized, each as-set, liability, revenue, expense, gain, or loss aris-ing from the transaction shall be measured andrecorded in the functional currency of the record-ing entity by use of the exchange rate in effect atthat date (paragraphs 26−28).

b. At each balance sheet date, recorded balancesthat are denominated in a currency other than thefunctional currency of the recording entity shallbe adjusted to reflect the current exchange rate.

17−19. [These paragraphs have been deleted. SeeStatus page.]

Transaction Gains and Losses to Be Excludedfrom Determination of Net Income

20. Gains and losses on the following foreign cur-rency transactions shall not be included in determin-ing net income but shall be reported in the same man-ner as translation adjustments (paragraph 13):

a. Foreign currency transactions that are designatedas, and are effective as, economic hedges of a netinvestment in a foreign entity, commencing as ofthe designation date

b. Intercompany foreign currency transactions thatare of a long-term-investment nature (that is,settlement is not planned or anticipated in theforeseeable future), when the entities to the trans-action are consolidated, combined, or accounted

for by the equity method in the reporting enter-prise’s financial statements.

Hedges of Firm Commitments

21. The accounting for a gain or loss on a foreigncurrency transaction that is intended to hedge anidentifiable foreign currency commitment (for ex-ample, an agreement to purchase or sell equipment)is addressed by paragraph 37 of Statement 133.

Income Tax Consequences of Rate Changes

22. Interperiod tax allocation is required in accord-ance with FASB Statement No. 109, Accounting forIncome Taxes, if taxable exchange gains or tax-deductible exchange losses resulting from an entity’sforeign currency transactions are included in net in-come in a different period for financial statement pur-poses from that for tax purposes.

23. Translation adjustments shall be accounted for inthe same way as temporary differences under the pro-visions of Statement 109 [and] APB Opinion 23.APB Opinion No. 23, Accounting for IncomeTaxes—Special Areas, provides that deferred taxesshall not be provided for unremitted earnings of asubsidiary in certain instances; in those instances,deferred taxes shall not be provided on translationadjustments.

24. Statement 109 requires income tax expense to beallocated among income before extraordinary items,extraordinary items, adjustments of prior periods (orof the opening balance of retained earnings), and di-rect entries to other equity accounts. Some transac-tion gains and losses and all translation adjustmentsare reported in other comprehensive income. Any in-come taxes related to those transaction gains andlosses and translation adjustments shall be allocatedto other comprehensive income.

Elimination of Intercompany Profits

25. The elimination of intercompany profits that areattributable to sales or other transfers between entitiesthat are consolidated, combined, or accounted for bythe equity method in the enterprise’s financial state-ments shall be based on the exchange rates at thedates of the sales or transfers. The use of reasonableapproximations or averages is permitted.

Exchange Rates

26. The exchange rate is the ratio between a unit ofone currency and the amount of another currency forwhich that unit can be exchanged at a particular time.

FAS52 FASB Statement of Standards

FAS52–6

If exchangeability between two currencies is tempo-rarily lacking at the transaction date or balance sheetdate, the first subsequent rate at which exchangescould be made shall be used for purposes of thisStatement. If the lack of exchangeability is other thantemporary, the propriety of consolidating, combin-ing, or accounting for the foreign operation by the eq-uity method in the financial statements of the enter-prise shall be carefully considered.

27. The exchange rates to be used for translation offoreign currency transactions and foreign currencystatements are as follows:

a. Foreign Currency Transactions—The applicablerate at which a particular transaction could besettled at the transaction date shall be used totranslate and record the transaction. At a subse-quent balance sheet date, the current rate is thatrate at which the related receivable or payablecould be settled at that date.

b. Foreign Currency Statements—In the absence ofunusual circumstances, the rate applicable toconversion of a currency for purposes of divi-dend remittances shall be used to translate for-eign currency statements.4

28. If a foreign entity whose balance sheet date dif-fers from that of the enterprise is consolidated orcombined with or accounted for by the equitymethod in the financial statements of the enterprise,the current rate is the rate in effect at the foreign enti-ty’s balance sheet date for purposes of applying therequirements of this Statement to that foreign entity.

Use of Averages or Other Methods ofApproximation

29. Literal application of the standards in this State-ment might require a degree of detail in record keep-ing and computations that could be burdensome aswell as unnecessary to produce reasonable approxi-mations of the results. Accordingly, it is acceptable touse averages or other methods of approximation. Forexample, the propriety of using average rates totranslate revenue and expense amounts is noted inparagraph 12. Likewise, the use of other time- andeffort-saving methods to approximate the results ofdetailed calculations is permitted.

Disclosure

30. The aggregate transaction gain or loss includedin determining net income for the period shall be dis-closed in the financial statements or notes thereto.Certain enterprises, primarily banks, are dealers inforeign exchange. Although certain gains or lossesfrom dealer transactions may fit the definition oftransaction gains or losses in this Statement, theymay be disclosed as dealer gains or losses rather thanas transaction gains or losses.

31. An analysis of the changes during the period inthe accumulated amount of translation adjustmentsreported in equity shall be provided in a separate fi-nancial statement, in notes to the financial statements,or as part of a statement of changes in equity. At aminimum, the analysis shall disclose:

a. Beginning and ending amount of cumulativetranslation adjustments

b. The aggregate adjustment for the period result-ing from translation adjustments (paragraph 13)and gains and losses from certain hedges and in-tercompany balances (paragraph 20) (Para-graph 45(c) of Statement 133 specifies additionaldisclosures for instruments designated as hedgesof the foreign currency exposure of a net invest-ment in a foreign operation.)

c. The amount of income taxes for the period allo-cated to translation adjustments (paragraph 24)

d. The amounts transferred from cumulative trans-lation adjustments and included in determiningnet income for the period as a result of the sale orcomplete or substantially complete liquidation ofan investment in a foreign entity (paragraph 14).

32. An enterprise’s financial statements shall not beadjusted for a rate change that occurs after the date ofthe enterprise’s financial statements or after the dateof the foreign currency statements of a foreign entityif they are consolidated, combined, or accounted forby the equity method in the financial statements ofthe enterprise. However, disclosure of the rate changeand its effects on unsettled balances pertaining toforeign currency transactions, if significant, may benecessary.

4 If unsettled intercompany transactions are subject to and translated using preference or penalty rates, translation of foreign currency statementsat the rate applicable to dividend remittances may cause a difference between intercompany receivables and payables. Until that difference iseliminated by settlement of the intercompany transaction, the difference shall be treated as a receivable or payable in the enterprise’s financialstatements.

FAS52Foreign Currency Translation

FAS52–7

Effective Date and Transition

33. This Statement shall be effective for fiscal yearsbeginning on or after December 15, 1982, althoughearlier application is encouraged. The initial applica-tion of this Statement shall be as of the beginning ofan enterprise’s fiscal year. Financial statements forfiscal years before the effective date, and financialsummaries or other data derived therefrom, may berestated to conform to the provisions of para-graphs 5−29 of this Statement. In the year that thisStatement is first applied, the financial statementsshall disclose the nature of any restatement and its ef-fect on income before extraordinary items, net in-come, and related per-share amounts for each fiscalyear restated. If the prior year is not restated, disclo-sure of income before extraordinary items and netincome for the prior year computed on a pro formabasis is permitted.

34. The effect of translating all of a foreign entity’sassets and liabilities from a foreign functional cur-rency into the reporting currency at the current ex-change rate as of the beginning of the year for whichthis Statement is first applied shall be reported inother comprehensive income. The effect of remeasur-ing a foreign entity’s deferred income taxes and lifeinsurance policy acquisition costs at the current ex-change rate (paragraph 54) as of the beginning of theyear for which this Statement is first applied shall bereported as an adjustment of the opening balance ofretained earnings.

35. Amounts deferred on forward contracts that(a) under Statement 8 were accounted for as hedgesof identifiable foreign currency commitments to re-ceive proceeds from the use or sale of nonmonetaryassets translated at historical rates, and (b) are can-celed at the time this Statement is first applied, shallbe included in the opening balance of the cumulativetranslation adjustments component of equity up tothe amount of the offsetting adjustment attributableto those nonmonetary assets.

36. Financial statements for periods beginning on orafter the effective date of this Statement shall includethe disclosures specified by paragraphs 30−32. To theextent practicable, those disclosures shall also be in-cluded in financial statements for earlier periods thathave been restated pursuant to paragraph 33.

37. Financial statements of enterprises that firstadopt this standard for fiscal years ending on or be-fore March 31, 1982 shall disclose the effect ofadopting the new standard on income before extraor-dinary items, net income, and related per-shareamounts for the year of the change. Those disclo-sures are not required for financial statements of en-terprises that first adopt this standard for subsequentfiscal years.

38. The Board expects to issue an Exposure Draftproposing an amendment of FASB StatementNo. 33, Financial Reporting and Changing Prices, tobe consistent with the functional currency approachto foreign currency translation. Prior to issuance of afinal amendment of Statement 33, enterprises thatadopt this Statement and that are subject to the re-quirements of Statement 33 shall have either of thefollowing options:

a. They may prepare the supplementary informa-tion based on this Statement and on the proposedamendment of Statement 33.

b. They may prepare the supplementary informa-tion based on the application of Statement 8 andon the provisions of existing Statement 33. (Un-der this option, historical cost information basedon the application of Statement 8 shall be pre-sented in the supplementary information forcomparison with the constant dollar and currentcost information.)

Enterprises that would become subject to the re-quirements of Statement 33 as a result of adoptingthis Statement are exempt from the requirementsof Statement 33 until the effective date of thisStatement.

The provisions of this Statement neednot be applied to immaterial items.

This Statement was adopted by the affırmativevotes of four members of the Financial AccountingStandards Board. Messrs. Block, Kirk, and Morgandissented.

Messrs. Block, Kirk, and Morgan dissent to the is-suance of this Statement. They start from a premisedifferent from that underlying this Statement. Theybelieve that more meaningful consolidated results are

FAS52 FASB Statement of Standards

FAS52–8

attained by measuring costs, cost recovery, and ex-change risk from a dollar perspective rather thanfrom multiple functional currency perspectives. Ac-cordingly, the dissenters do not believe that thisStatement improves financial reporting. In their opin-ion, improved financial reporting would have re-sulted from an approach that:

a. Adopted objectives of translation that retainedthe concept of a single consolidated entity and asingle unit of measure (that is, all elements ofU.S. consolidated financial statements would bemeasured in dollars rather than multiple func-tional currencies)

b. Avoided creating direct entries to equityc. Essentially retained Statement 8’s translation

method, with an exception being translation oflocally sourced inventory at the current rate

d. Recognized all gains and losses in net income(that is, no separate and different accounting fortransaction gains or losses and translation adjust-ments), but allowed for a separate and distinctpresentation of those gains and losses within theincome statement

e. Recognized additional contractual arrangements(for example, operating leases and take-or-paycontracts) that effectively hedged an exposed netmonetary liability position.

The dissenters recognize that such an approachwould not satisfy all of the critics of Statement 8, butthey believe it would have avoided the more far-reaching implications of the functional currencytheory. They acknowledge that translating certain in-ventories at current rates departs from historical costin dollars. However, they would accept that departureon pragmatic grounds as part of a solution to an ex-ceedingly difficult problem.

As further discussed in subsequent paragraphs,the dissenting Board members do not support thisStatement because in their opinion it:

a. Builds on two incompatible premises and, as a re-sult, produces anomalies and a significant but un-warranted reporting distinction between transac-tion gains and losses and translation adjustments

b. Adopts objectives and methods that are at vari-ance with fundamental concepts that underliepresent financial reporting

c. Incorrectly assumes that an aggregation of the re-sults of foreign operations measured in functionalcurrencies and expressed in dollars, rather thanconsolidated results measured in dollars, assists

U.S. investors and creditors in assessing futurecash flows to them

d. Will not result in similar accounting for similarcircumstances.

Incompatibility of Underlying Premises

The standards for translating foreign currency fi-nancial statements set forth in this Statement stemfrom two premises that are incompatible with eachother. The first premise is that it is a parent compa-ny’s net investment in a foreign operation that is sub-ject to exchange rate risk rather than the foreign op-eration’s individual assets and liabilities. The secondpremise is that translation should retain the relation-ships in foreign currency financial statements asmeasured by the functional currency. The premise ofa parent company’s exposed net investment reflects adollar perspective of exchange rate risk, and that callsfor a dollar measure of the effects of exchange ratechanges. The premise of retaining the relationships ofmeasurements in functional currency financial state-ments calls for a functional currency measure of theeffects of exchange rate changes.

The dissenting Board members note that althoughthe translation process can retain certain intraperiodrelationships reported in functional currency finan-cial statements, it cannot retain interperiod functionalcurrency relationships when exchange rates change.Further, when an exchange rate changes between thedollar and a foreign currency, the value of any hold-ings of that currency changes and, from a dollar per-spective, the resulting gain or loss is either real, or un-real, in its entirety. However, to implement thefunctional currency perspective, the standards resultin a division of that gain or loss into two components.One is considered in measuring consolidated net in-come and the other is considered a translation adjust-ment. Thus, the standards require a transaction gainin income on a foreign operation’s holdings of a thirdcurrency when that currency strengthens in relationto the functional currency, even if the third currencyhas weakened in terms of dollars. That gain will bereported in consolidated net income despite the factthat it does not exist in dollar terms and can neverprovide increased dollar cash flows to U.S. investorsand creditors. The standards inherently recognize thatfact by requiring a compensating debit translation ad-justment. (Examples that further illustrate these con-cerns are contained in paragraphs 111−113 of theAu-gust 28, 1980 Exposure Draft, Foreign CurrencyTranslation.)

FAS52Foreign Currency Translation

FAS52–9

The dissenters believe that the need for a transla-tion adjustment that adjusts consolidated equity to thesame amount as would have resulted had all foreigncurrency transactions of foreign operations beenmeasured in dollars demonstrates the incompatibilityof the two underlying premises. They believe that in-compatibility is further demonstrated by the differingviews of the nature of translation adjustments de-scribed in paragraphs 113 and 114. In the dissenters’opinion, translation adjustments are, from a dollarperspective, gains and losses as defined in FASBConcepts Statement No. 3, Elements of FinancialStatements of Business Enterprises, which should bereported in net income when exchange rates change.The dissenters believe that from a functional cur-rency perspective, translation adjustments fail tomeet any definition of an element of financial state-ments because they do not exist in terms of func-tional currency cash flows.

Relationship to Preexisting FundamentalConcepts

The dissenters believe the two premises underly-ing this Statement (discussed above) challenge andreject the dollar perspective that underlies existingtheories of historical cost and capital maintenance,inflation accounting, consolidation, and realization.The rejection of the dollar perspective has ramifica-tions far beyond this project and was unnecessary ina translation project.

While not explicitly stated, today’s accountingmodel includes the capital maintenance concept thatincome of a consolidated U.S. entity exists only afterrecovery of historical cost measured in dollars. Forexample, prior to this Statement, the gain on the saleby a foreign operation of an internationally priced in-ventory item or a marketable security would havebeen measured by comparing the dollar equivalentsales price with the fixed dollar equivalent historicalcost of the item. This Statement changes that. It re-measures the dollar equivalent cost while the item isheld (measured by changes in the exchange rate be-tween the foreign currency and the dollar) and treatsthat remeasurement as a translation adjustment, sel-dom if ever to be reported in net income. Under thisStatement, consolidated net income, although ex-pressed in dollars, does not represent the measure ofincome after maintaining capital measured in dollars.The dissenters believe that U.S. investors’ and credi-tors’ decisions are based on a dollar perspective ofcapital maintenance. Not only does this Statementchange income measurement and capital mainte-

nance concepts in the primary financial statementsbut it also implies the need to modify the measure-ment of changes in current costs (sometimes referredto as holding gains or losses) in Statement 33 and,likewise, to change that Statement’s requirements forconstant dollar accounting to constant functional cur-rency accounting.

This Statement abandons the long-standing prin-ciple that consolidated results should be measuredfrom a single perspective rather than multiple per-spectives. The dissenters believe (for the reasons setforth in paragraphs 83−95 of Statement 8) that asingle perspective is essential for (a) valid additionand subtraction in the measurement of financial posi-tion and periodic net income and (b) the understand-ability and representational faithfulness of consoli-dated results presented in dollars and described asbeing prepared on the historical cost basis. The dis-senters believe that readers of financial statements arebetter served by having consolidated financial state-ments prepared in terms of a common benchmark—a single unit of measure. This means to the dissentersthat the translation process is one of remeasurementof the individual items of foreign financial statements(not net investments) into dollars—much in the sameway as Statement 33 presently requires a remeasure-ment of individual items of financial statements (notnet investments) from nominal dollar measures intoconstant dollars.

The Statement introduces a concept of realization(paragraphs 71, 111, 117, and 119) different from anypreviously applied in consolidated financial state-ments. It requires the results of foreign operations tobe measured in various functional currencies andthen translated into dollars and included in consoli-dated net income. It defers recognizing in net incomethe effects of exchange rate changes from a dollarperspective on the individual assets and liabilities ofthose same foreign operations until an indefinite fu-ture period that will almost always be beyond thepoint in time that those individual assets and liabili-ties have ceased to exist. As a result, the dollar effectsof a rate change on current operating revenues arerecognized when they occur by reporting in the trans-lated income statement an increased or decreaseddollar equivalent for those revenues versus the dollarequivalent of identical revenues generated before therate change. However, the effects of the same ratechange on the uncollected receivables from thoseprevious revenue transactions are not included in netincome until liquidation of the foreign operation. Bynot recognizing in net income the effects of exchangerate changes on existing receivables, this Statement

FAS52 FASB Statement of Standards

FAS52–10

results in sales denominated in a foreign currency be-ing accounted for as if they had been denominated indollars. That result is a focal point of the criticismmade in this Statement (paragraph 75) about State-ment 8. However, unlike this Statement, Statement 8recognized that foreign currency sales are not de-nominated in dollars and therefore it required that theeffects of exchange rate changes on all foreign cur-rency denominated receivables be recognized in netincome. To do otherwise places the enterprise in theanomalous position of having recognized the entireeffect of the rate change on a current transactionwhile holding in suspense its effect on a previoustransaction until liquidation of the foreign operation.

This Statement accepts the use of the Statement 8methodology (that is, using the dollar as the func-tional currency) for some foreign operations (includ-ing all operations in highly inflationary economies),but at the same time criticizes that methodology. Itasserts that the Statement 8 methodology results inaccounting as if all transactions were conducted inthe economic environment of the United States andin dollars (paragraphs 74, 75, and 86). The dissentersbelieve such views were convincingly rebutted inparagraphs 94 and 95 of Statement 8, as follows:

Some respondents to the Exposure Draftcriticized that objective as an attempt to ac-count for local and foreign currency transac-tions of foreign operations as if they weredollar transactions or, to a few respondents, asif they were dollar transactions in the UnitedStates. In the Board’s judgment, those criti-cisms are not valid. Neither the objective northe procedures to accomplish it change thedenomination of a transaction or the environ-ment in which it occurs. The proceduresadopted by the Board are consistent with thepurpose of consolidated financial statements.The foreign currency transactions of an enter-prise and the local and foreign currency trans-actions of its foreign operations are translatedand accounted for as transactions of a singleenterprise. The denomination of transactionsand the location of assets are not changed;however, the separate corporate identitieswithin the consolidated group are ignored.Translation procedures are merely a means ofremeasuring in dollars amounts that are de-nominated or originally measured in foreigncurrency. That is, the procedures do not at-tempt to simulate what the cost of a foreignplant would have been had it been located inthe United States; instead, they recognize the

factors that determined the plant’s cost in theforeign location and express that cost indollars.

If translation procedures were capable ofchanging the denomination of an asset or li-ability from foreign currency to dollars, noexchange risk would be present.

Effects on Cash Flow Assessments

The dissenters believe that U.S. investors andcreditors should be provided with information abouta multinational enterprise’s performance measured indollars because that is the currency in which, ulti-mately, the enterprise makes cash payments to them.Foreign exchange exposure to a U.S. investor orcreditor is the exposure to increased or decreased po-tential dollar cash flows caused by changes in ex-change rates between foreign currencies and the dol-lar. Changes in exchange rates between two foreigncurrencies are not relevant, except to the extent thateach such foreign currency’s exchange rate for thedollar changes.

Supporting the functional currency perspective isthe assenters’ view (paragraphs 73, 75, 97, and else-where) that a translated functional currency incomestatement better provides U.S. investors and creditorswith information necessary in assessing future cashflows than does an income statement whose compo-nents have been measured from a dollar perspective.The dissenting view is that a translated functionalcurrency income statement is inappropriate becauseit can include items that (a) do not exist for the con-solidated enterprise (for example, transaction gainson intercompany trade receivables or monetary itemsdenominated in dollars) or (b) are incorrectly meas-ured (for example, a gain on a holding of a third cur-rency that significantly strengthens against the dollarbut only moderately strengthens against the func-tional currency). It can also exclude items that do ex-ist for the consolidated enterprise (for example, again on a monetary asset denominated in a foreignoperation’s functional currency when that currencystrengthens against the dollar).

The dissenters see no persuasive reasoning to sup-port the belief that external users want or need toknow the amount of transaction gains or losses asmeasured from the perspective of the manager of theforeign operation (that is, in functional currency),while at the same time wanting a balance sheet that ismeasured from a dollar perspective—a balance sheetthat denies the usefulness of the foreign perspective.(The previously referenced examples in the August

FAS52Foreign Currency Translation

FAS52–11

1980 Exposure Draft also further illustrate thisconcern.)

Similar Accounting for Similar Circumstances

The dissenters believe that the criteria in para-graph 42 for deciding between the Statement 8 trans-lation method and the current rate method areinappropriate (for the reasons set forth in para-graphs 140−151 of Statement 8). They also believethat application of those criteria will not result insimilar accounting for similar situations.

Likewise, the absence of effective criteria thatwould objectively indicate when foreign currencytransactions (paragraph 20(a)) and forward exchangecontracts (paragraph 21) are hedges creates the possi-bility that transaction gains or losses that should bereported in net income currently may instead be re-ported as translation adjustments or deferred ashedges of commitments.

The variety of permissible methods of transitionfrom the existing Statement 8 requirements may also

result in similar circumstances being accounted fordifferently. Mr. Morgan believes the transition para-graphs should have required that the amount neces-sary to adjust from the Statement 8 basis to the newbasis be reported as the opening translation adjust-ment in equity for the first year in which the newStatement becomes effective. To restate any yearprior to the effective date of this Statement may fosteran inappropriate conclusion, namely, that those re-stated results are the results an entity might have ex-perienced had the new Statement been in effect forearlier periods. There is considerable evidence thatmany enterprises alter their hedging of foreign ex-change exposure depending on the accounting stand-ards currently in effect. Thus, restated financial state-ments for those entities, whether required or donevoluntarily, could not accurately reflect what mighthave happened had this Statement been in effect. Vol-untary restatement also diminishes the comparabilityof financial reporting among companies. In Mr. Mor-gan’s view, the Board should have prohibited restate-ment as a method of transition to this new Statement.

Members of the Financial Accounting Standards Board:

Donald J. Kirk,Chairman

Frank E. Block

John W. MarchRobert A. MorganDavid Mosso

Robert T. SprouseRalph E. Walters

Appendix A

DETERMINATION OF THE FUNCTIONALCURRENCY

39. An entity’s functional currency is the currency ofthe primary economic environment in which the en-tity operates; normally, that is the currency of the en-vironment in which an entity primarily generates andexpends cash. The functional currency of an entity is,in principle, a matter of fact. In some cases, the factswill clearly identify the functional currency; in othercases they will not.

40. It is neither possible nor desirable to provide un-equivocal criteria to identify the functional currencyof foreign entities under all possible facts and cir-cumstances and still fulfill the objectives of foreigncurrency translation. Arbitrary rules that might dic-tate the identification of the functional currency ineach case would accomplish a degree of superficialuniformity but, in the process, might diminish the rel-evance and reliability of the resulting information.

41. The Board has developed, with significant inputfrom its task force and other advisors, the followinggeneral guidance on indicators of facts to be consid-ered in identifying the functional currency. In thoseinstances in which the indicators are mixed and thefunctional currency is not obvious, management’sjudgment will be required in order to determine thefunctional currency that most faithfully portrays theeconomic results of the entity’s operations andthereby best achieves the objectives of foreign cur-rency translation set forth in paragraph 4. Manage-ment is in the best position to obtain the pertinentfacts and weigh their relative importance in deter-mining the functional currency for each operation. Itis important to recognize that management’s judg-ment is essential and paramount in this determina-tion, provided only that it is not contradicted by thefacts.

42. The salient economic factors set forth below, andpossibly others, should be considered both individu-ally and collectively when determining the functionalcurrency.

FAS52 FASB Statement of Standards

FAS52–12

a. Cash flow indicators(1) Foreign Currency—Cash flows related to the

foreign entity’s individual assets and liabili-ties are primarily in the foreign currency anddo not directly impact the parent company’scash flows.

(2) Parent’s Currency—Cash flows related to theforeign entity’s individual assets and liabili-ties directly impact the parent’s cash flows ona current basis and are readily available forremittance to the parent company.

b. Sales price indicators(1) Foreign Currency—Sales prices for the for-

eign entity’s products are not primarily re-sponsive on a short-term basis to changes inexchange rates but are determined moreby local competition or local governmentregulation.

(2) Parent’s Currency—Sales prices for the for-eign entity’s products are primarily respon-sive on a short-term basis to changes in ex-change rates; for example, sales prices aredetermined more by worldwide competitionor by international prices.

c. Sales market indicators(1) Foreign Currency—There is an active local

sales market for the foreign entity’s products,although there also might be significantamounts of exports.

(2) Parent’s Currency—The sales market ismostly in the parent’s country or salescontracts are denominated in the parent’scurrency.

d. Expense indicators(1) Foreign Currency—Labor, materials, and

other costs for the foreign entity’s products orservices are primarily local costs, eventhough there also might be imports fromother countries.

(2) Parent’s Currency—Labor, materials, andother costs for the foreign entity’s products orservices, on a continuing basis, are primarilycosts for components obtained from thecountry in which the parent company islocated.

e. Financing indicators(1) Foreign Currency—Financing is primarily

denominated in foreign currency, and fundsgenerated by the foreign entity’s operationsare sufficient to service existing and normallyexpected debt obligations.

(2) Parent’s Currency—Financing is primarilyfrom the parent or other dollar-denominated

obligations, or funds generated by the foreignentity’s operations are not sufficient to serviceexisting and normally expected debt obliga-tions without the infusion of additional fundsfrom the parent company. Infusion of addi-tional funds from the parent company for ex-pansion is not a factor, provided funds gener-ated by the foreign entity’s expandedoperations are expected to be sufficient toservice that additional financing.

f. Intercompany transactions and arrangementsindicators(1) Foreign Currency—There is a low volume of

intercompany transactions and there is not anextensive interrelationship between the op-erations of the foreign entity and the parentcompany. However, the foreign entity’s op-erations may rely on the parent’s or affiliates’competitive advantages, such as patents andtrademarks.

(2) Parent’s Currency—There is a high volumeof intercompany transactions and there is anextensive interrelationship between the op-erations of the foreign entity and the parentcompany. Additionally, the parent’s currencygenerally would be the functional currency ifthe foreign entity is a device or shell corpora-tion for holding investments, obligations, in-tangible assets, etc., that could readily be car-ried on the parent’s or an affiliate’s books.

43. In some instances, a foreign entity might havemore than one distinct and separable operation. Forexample, a foreign entity might have one operationthat sells parent-company-produced products and an-other operation that manufactures and sells foreign-entity-produced products. If those two operations areconducted in different economic environments, thosetwo operations might have different functional cur-rencies. Similarly, a single subsidiary of a financialinstitution might have relatively self-contained andintegrated operations in each of several differentcountries. In circumstances such as those describedabove, each operation may be considered to be an en-tity as that term is used in this Statement; and, basedon the facts and circumstances, each operation mighthave a different functional currency.

44. Foreign investments that are consolidated or ac-counted for by the equity method are controlled by orsubject to significant influence by the parent com-pany. Likewise, the parent’s currency is often usedfor measurements, assessments, evaluations, projec-tions, etc., pertaining to foreign investments as part of

FAS52Foreign Currency Translation

FAS52–13

the management decision-making process. Suchmanagement control, decisions, and resultant actionsmay reflect, indicate, or create economic facts andcircumstances. However, the exercise of significantmanagement control and the use of the parent’s cur-rency for decision-making purposes do not deter-mine, per se, that the parent’s currency is the func-tional currency for foreign operations.

45. Once a determination of the functional currencyis made, that decision shall be consistently used foreach foreign entity unless significant changes in eco-nomic facts and circumstances indicate clearly thatthe functional currency has changed. (FASB State-ment No. 154, Accounting Changes and Error Cor-rections, paragraph 5, states that “adoption or modifi-cation of an accounting principle necessitated bytransactions or events that are clearly different in sub-stance from those previously occurring” is not achange in accounting principle.)

46. If the functional currency changes from a foreigncurrency to the reporting currency, translation adjust-ments for prior periods should not be removed fromequity and the translated amounts for nonmonetaryassets at the end of the prior period become the ac-counting basis for those assets in the period of thechange and subsequent periods. If the functional cur-rency changes from the reporting currency to a for-eign currency, the adjustment attributable to current-rate translation of nonmonetary assets as of the dateof the change should be reported in other comprehen-sive income.

Appendix B

REMEASUREMENT OF THE BOOKS OFRECORD INTO THE FUNCTIONALCURRENCY*

Introduction

47. Paragraph 12 of this Statement requires that allof a foreign entity’s assets and liabilities shall be

translated from the entity’s functional currency intothe reporting currency using the current exchangerate. Paragraph 12 also requires that revenues, ex-penses, gains, and losses be translated using the rateson the dates on which those elements are recognizedduring the period. The specified result can be reason-ably approximated by using an appropriatelyweighted average exchange rate for the period. If anentity’s books of record are not maintained in itsfunctional currency, this Statement (paragraph 10) re-quires remeasurement into the functional currencyprior to the translation process. If a foreign entity’sfunctional currency is the reporting currency, remea-surement into the reporting currency obviates transla-tion. The remeasurement process should produce thesame result as if the entity’s books of record had beeninitially recorded in the functional currency. To ac-complish that result, it is necessary to use historicalexchange rates between the functional currency andanother currency in the remeasurement process forcertain accounts (the current rate will be used for allothers), and this appendix identifies those accounts.To accomplish that result, it is also necessary to rec-ognize currently in income all exchange gains andlosses from remeasurement of monetary assets andliabilities that are not denominated in the functionalcurrency (for example, assets and liabilities that arenot denominated in dollars if the dollar is the func-tional currency).

48. The table below lists common nonmonetary bal-ance sheet items and related revenue, expense, gain,and loss accounts that should be remeasured usinghistorical rates in order to produce the same result interms of the functional currency that would have oc-curred if those items had been initially recorded inthe functional currency.

*The guidance in this appendix applies only to those instances in which the books of record are not maintained in the functional currency.

FAS52 FASB Statement of Standards

FAS52–14

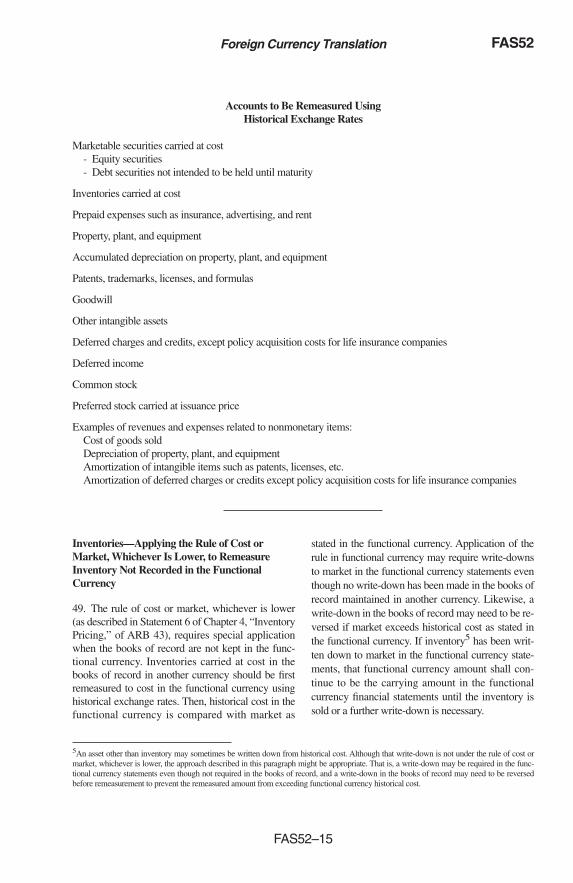

Accounts to Be Remeasured UsingHistorical Exchange Rates

Marketable securities carried at cost- Equity securities- Debt securities not intended to be held until maturity

Inventories carried at cost

Prepaid expenses such as insurance, advertising, and rent

Property, plant, and equipment

Accumulated depreciation on property, plant, and equipment

Patents, trademarks, licenses, and formulas

Goodwill

Other intangible assets

Deferred charges and credits, except policy acquisition costs for life insurance companies

Deferred income

Common stock

Preferred stock carried at issuance price

Examples of revenues and expenses related to nonmonetary items:Cost of goods soldDepreciation of property, plant, and equipmentAmortization of intangible items such as patents, licenses, etc.Amortization of deferred charges or credits except policy acquisition costs for life insurance companies

Inventories—Applying the Rule of Cost orMarket, Whichever Is Lower, to RemeasureInventory Not Recorded in the FunctionalCurrency

49. The rule of cost or market, whichever is lower(as described in Statement 6 of Chapter 4, “InventoryPricing,” of ARB 43), requires special applicationwhen the books of record are not kept in the func-tional currency. Inventories carried at cost in thebooks of record in another currency should be firstremeasured to cost in the functional currency usinghistorical exchange rates. Then, historical cost in thefunctional currency is compared with market as

stated in the functional currency. Application of therule in functional currency may require write-downsto market in the functional currency statements eventhough no write-down has been made in the books ofrecord maintained in another currency. Likewise, awrite-down in the books of record may need to be re-versed if market exceeds historical cost as stated inthe functional currency. If inventory5 has been writ-ten down to market in the functional currency state-ments, that functional currency amount shall con-tinue to be the carrying amount in the functionalcurrency financial statements until the inventory issold or a further write-down is necessary.

5An asset other than inventory may sometimes be written down from historical cost. Although that write-down is not under the rule of cost ormarket, whichever is lower, the approach described in this paragraph might be appropriate. That is, a write-down may be required in the func-tional currency statements even though not required in the books of record, and a write-down in the books of record may need to be reversedbefore remeasurement to prevent the remeasured amount from exceeding functional currency historical cost.

FAS52Foreign Currency Translation

FAS52–15

50. Literal application of the rule of cost or market,whichever is lower, may require an inventory write-down6 in functional currency financial statements forlocally acquired inventory7 if the value of the cur-rency in which the books of record are maintainedhas declined in relation to the functional currency be-tween the date the inventory was acquired and thedate of the balance sheet. Such a write-down may notbe necessary, however, if the replacement costs orselling prices expressed in the currency in which thebooks of record are maintained have increased suffi-ciently so that market exceeds historical cost asmeasured in functional currency. Paragraphs 51−53illustrate this situation.

51. Assume the following:

a. When the rate is BR*1 = FC2.40, a foreign sub-sidiary of a U.S. company purchases a unit of in-ventory at a cost of BR500 (measured in func-tional currency, FC1,200).

b. At the foreign subsidiary’s balance sheet date, thecurrent rate is BR1 = FC2.00 and the current re-placement cost of the unit of inventory is BR560(measured in functional currency, FC1,120).

c. Net realizable value is BR630 (measured in func-tional currency, FC1,260).

d. Net realizable value reduced by an allowance foran approximately normal profit margin is BR550(measured in functional currency, FC1,100).

Because current replacement cost as measured in thefunctional currency (FC1,120) is less than historicalcost as measured in the functional currency(FC1,200), an inventory write-down of FC80 isrequired in the functional currency financialstatements.

52. Continue to assume the same information in thepreceding example but substitute a current replace-ment cost at the foreign subsidiary’s balance sheet

date of BR620. Because market as measured in thefunctional currency (BR620 × FC2.00 = FC1,240)exceeds historical cost as measured in the functionalcurrency (BR500 × FC2.40 = FC1,200), an inven-tory write-down is not required in the financialstatements.

53. As another example, assume the information inparagraph 51, except that selling prices in terms ofthe currency in which the books of record are main-tained have increased so that net realizable value isBR720 and net realizable value reduced by an allow-ance for an approximately normal profit margin isBR640. In that case, because replacement cost meas-ured in functional currency (BR560 × FC2.00 =FC1,120) is less than net realizable value reduced byan allowance for an approximately normal profitmargin measured in functional currency (BR640 ×FC2.00 = FC1,280), market is FC1,280. Becausemarket as measured in the functional currency(FC1,280) exceeds historical cost as measured in thefunctional currency (BR500 × FC2.40 = FC1,200),an inventory write-down is not required in the func-tional currency financial statements.

Deferred Taxes and Policy Acquisition Costs

54. Statement 8 required certain deferred taxes thatdo not relate to assets or liabilities translated at cur-rent rates to be translated at historical rates.8 Interpre-tation 15 required unamortized policy acquisitioncosts of a stock life insurance company to be trans-lated at historical rates.9 In Statement 33, the Boarddecided that, because of the close relationship ofthose accounts to related monetary items, a monetaryclassification should be used for the purposes of con-stant dollar accounting. For similar reasons, theBoard decided to retain the classification requiredby Statement 33 for the purposes of remeasurementof an entity’s books of record into its functionalcurrency.

6This paragraph is not intended to preclude recognition of gains in a later interim period to the extent of inventory losses recognized from marketdeclines in earlier interim periods if losses on the same inventory are recovered in the same year, as provided by paragraph 14(c) ofAPB OpinionNo. 28, Interim Financial Reporting, which states: “Inventory losses from market declines should not be deferred beyond the interim period inwhich the decline occurs. Recoveries of such losses on the same inventory in later interim periods of the same fiscal year through market pricerecoveries should be recognized as gains in the later interim period. Such gains should not exceed previously recognized losses. Some marketdeclines at interim dates, however, can reasonably be expected to be restored in the fiscal year. Such temporary market declines need not berecognized at the interim date since no loss is expected to be incurred in the fiscal year.”7An inventory write-down also may be required for imported inventory.

*BR = Currency in which the books of record are maintainedFC = Functional currency

8Statement 8, paragraphs 50−52.9Interpretation 15, paragraph 4.

FAS52 FASB Statement of Standards

FAS52–16

Appendix C

BASIS FOR CONCLUSIONS

CONTENTS

ParagraphNumbers

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55Nature of the Problem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56− 69Objectives of Translation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70− 76The Functional Currency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77− 84Consolidation of Foreign Currency Statements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85− 93Translation of Foreign Currency Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94−101Translation of Operations in Highly Inflationary Economies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102−109Translation Adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110−119Transaction Gains and Losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120−127Foreign Currency Transactions That Hedge a Net Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128−130Transaction Gains and Losses Attributable to Intercompany Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . 131Foreign Currency Transactions That Hedge Foreign Currency Commitments . . . . . . . . . . . . . . . . . . . . . . . 132−133Income Tax Consequences of Rate Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134−135Elimination of Intercompany Profits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136−137Exchange Rates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138−139Use of Averages or Other Methods of Approximation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140Disclosure. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141−144Effective Date and Transition. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145−149

Appendix C

BASIS FOR CONCLUSIONS

Introduction

55. This appendix reviews considerations that weredeemed significant by members of the Board inreaching the conclusions in this Statement. TheBoard members who assented to this Statement didso on the basis of the overall considerations; indi-vidual members gave greater weight to some factorsthan to others.

Nature of the Problem

56. Operations and transactions of an enterpriseare affected by the changing prices of goods andservices it buys and sells relative to a unit of currency,which is usually also the measuring unit for financialreporting.

57. If the enterprise operates in more than one cur-rency environment, it is affected by the changingprices of goods and services in more than one eco-nomic environment and, additionally, by changes inrelative prices among the several units of currency inwhich it conducts its business.

58. The accounting model, generally referred to asthe historical cost model, does not generally recog-nize the effect of changing prices of goods and serv-ices until there has been an exchange transaction,usually a sale or purchase. In general, then, it doesnot recognize unrealized holding gains resulting fromchanges in the price of goods and services relative tothe unit of currency.

59. For enterprises conducting activities in morethan a single currency, the practical necessities of fi-nancial reporting in a single currency require that thechanging prices between two units of currency be ac-commodated in some fashion. People generally agreeon this practical necessity but disagree on conceptsand details of implementation. As a result, there is

FAS52Foreign Currency Translation

FAS52–17

significant disagreement among informed observersregarding the basic nature, information content, andmeaning of results produced by various methods oftranslating amounts from foreign currencies into thereporting currency. Each method has strong propo-nents and severe critics.

60. In dealing with this dilemma, the Board wasfaced with the following basic choices:

a. Changing the accounting model to one that rec-ognizes currently the effects of all changingprices in the primary financial statements

b. Deferring any recognition of changing curren-cy prices until they are realized by an actualexchange of foreign currency into the reportingcurrency

c. Recognizing currently the effect of changing cur-rency prices on the carrying amounts of desig-nated foreign assets and liabilities

d. Recognizing currently the effect of changing cur-rency prices on the carrying amounts of all for-eign assets and liabilities.

61. Alternative (a) runs counter to the Board’s ap-proach in Statement 33, which fosters experimenta-tion with supplemental reporting to test the feasibil-ity, usefulness, and cost of various techniques forreporting the effects of changing prices. Accordingly,the Board did not consider a change in the primary fi-nancial statement model to be a reasonable alterna-tive for this project on foreign currency translation.

62. Alternative (b) has little or no support from theBoard or its constituents. All transactions and bal-ances would be translated at historical exchangerates—a formidable clerical task—until conversionto the parent’s currency occurred. Postponing recog-nition would fail to reflect the effects of possibly verysignificant economic events at the time they oc-curred, particularly those that affect transactions thatmust be settled under changed currency prices. Mostwould consider this a retreat rather than an advancetoward more useful financial reporting.

63. Alternative (c) is the approach taken in State-ment 8. Although some believe this approach is con-ceptually consistent with the historical cost model,others do not agree. In any event, this approach hasproduced results that the Board and many constitu-ents believe do not reflect the underlying economicreality of many foreign operations and thereby pro-duces results that are not relevant. A summary of themore common criticisms of Statement 8 is includedin paragraphs 153−156 of Appendix D.