Embed Size (px)

Citation preview

56

R.N.I. No. MAHENG/2012/47145Postal Registration No. MCS/153/2019-21 • MR/Tech/WPP-355/South/2019

st rd thPublished on 1 (Day) of every month • Posted at Patrika Channel Sorting Office, Mumbai - 400001 • Posting date: 3 & 4 of every month

`15/-|MARCH 2019 VOLUME: 7 • ISSUE NO. 12 •|BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF) MUMBAI, INDIA

FORUM VIEWS

In support with

Tokyo, Japan

INSIDEBBF GLOBAL CONNECTS' SOUTH KOREA | JAPAN

th st28 January - 1 February 2019

2 3 FORUM VIEWS - MARCH 2019

EXECUTIVE COMMITTEE

Uttam BagriChairman

Anurag BansalVice-Chairman

Purav Fozdar Secretary

Harin MehtaJt. Secretary

Lalit MundraJt. Treasurer

GOVERNING BOARD 201BOMBAY STOCK EXCHANGE BROKERS’FORUM (BBF) GOVERNING BOARD 2018 - 19

Kamlesh D ShroffTreasurer

GOVERNING BOARD MEMBERS

AnjanaVijay Shah

AshokAjmera

AnupGupta

HemantDesai

HemantMajethia

ArpitAgarwal

JayToshniwal

Jitendra KumarPanda

KetanMarwadi

KishorKansagra

KushalA. Shah

MadhaviVora

NiravGandhi

RajivChoksey

NithinKamath

ParthNyati

VirenderMansukhani

MehulPatel

NareshRana

MahavirLunawat

BOMBAY STOCK EXCHANGEBROKERS' FORUM (BBF)OFFICIAL MASCOT

CEO & COO DESK06

SEMINARS & EVENTS CONDUCTEDBY BBF FOR THE PROGRESS OFJANUARY - FEBRUARY 2019

48

14 BULLS & BEARS: NFRA - THE NEWWATCHDOG FOR ACCOUNTANCYAND AUDIT PRACTICES

4 FORUM VIEWS - MARCH 2019

Disclaimer: This magazine is meant for information purposes only and does not constitute any opinion or guidelines or recommendation on any course of action to be followed by the reader(s). It is not intended to be used as trading or investment advice by anybody and should not in any way be treated as a recommendation. The information contained in this magazine does not constitute or form part of and should not be construed as, any offer for purchase or sale of any product or service. While the information in the magazine has been compiled from sources believed to be reliable and in good faith, readers may note that the contents thereof including text, graphics, links or other items are provided without warranties of any kind. BSE Brokers' Forum expressly disclaims any warranty as to the accuracy, correctness, reliability, timeliness, merchantability or fitness for any particular purpose, of this magazine. BSE Brokers' Forum shall also not be liable for any damage or loss of any kind, howsoever caused as a result (direct or indirect) of the use of the information or data contained in this magazine. Any alteration, transmission, photocopied distribution in part or in whole or reproduction of any form of this magazine or any part thereof without prior consent of BSE Brokers' Forum is prohibited.

Printed, Published and Edited by Dr. VISPI RUSI BHATHENA, PhD (h.c.)& Dr. V. ADITYA SRINIVAS on behalf of BSE BROKERS' FORUM,

printed at KSHITIJ PRINTERS, 49, Parsi Panchayat Road,Ashok Ind. Estate, 1st, Floor, Andheri (East) Mumbai - 400 069.

and published from BSE BROKERS' FORUM, 808 A,P. J. TOWERS, DALAL STREET, FORT, MUMBAI - 400 001.

Editor: Dr. V. ADITYA SRINIVASDesign by: Harshad Gajera | Photographer: Sanjeev Dubey

BSE Brokers’ Forum Steering CommitteeUttam Bagri (Chairman)

Anurag Bansal (Vice - Chairman)Purav Fozdar (Secretary)

Harin Mehta (Jt. Secretary)Kamlesh D Shroff (Treasurer)Lalit Mundra (Jt. Treasurer)

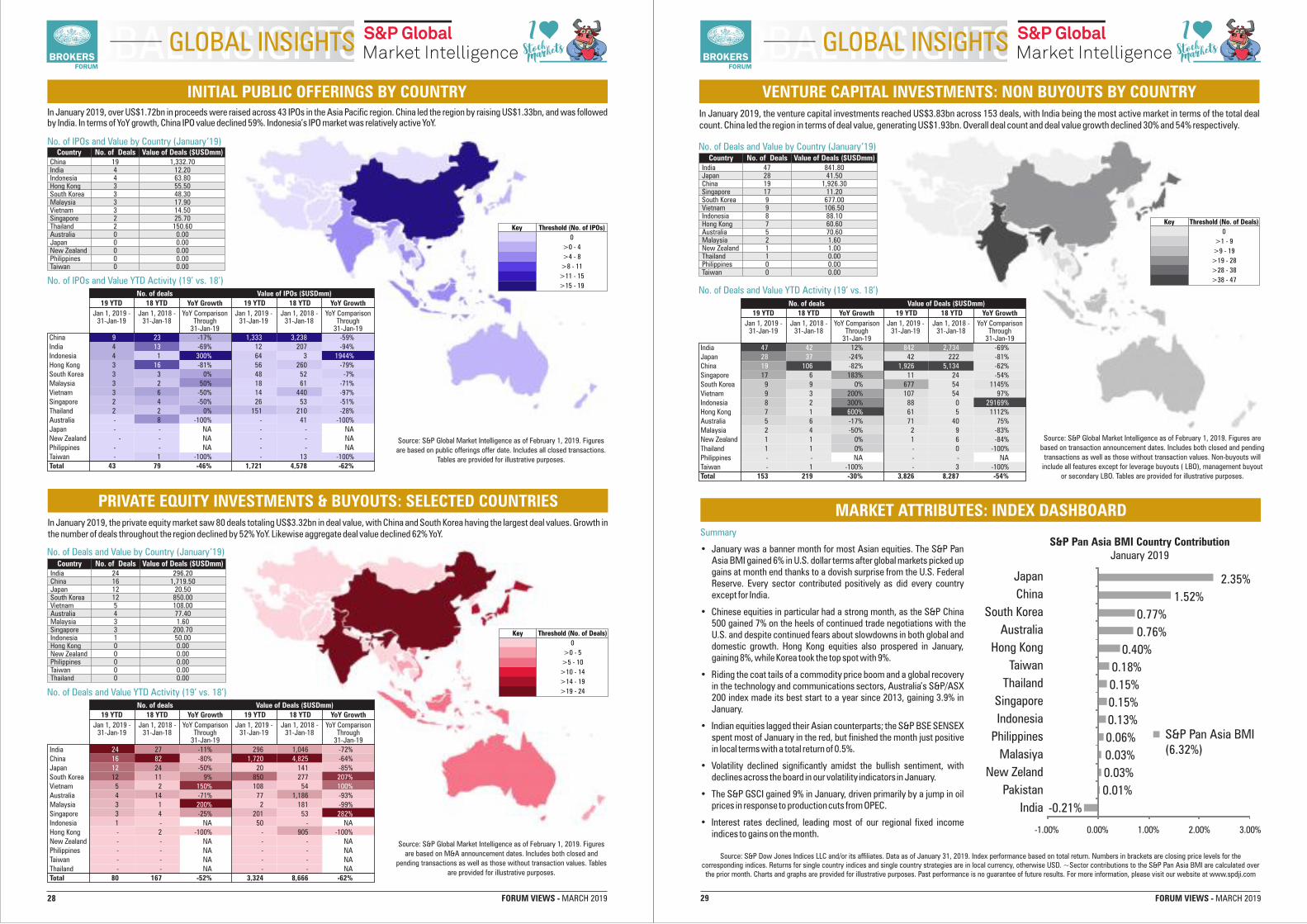

26 ASIA-PACIFIC MARKETSMONTHLY HIGHLIGHTSAND INSIGHTS

THE UNDERPINNINGS OFEMPLOYMENT CREATIONIN INDIA: AN OVERVIEW

20

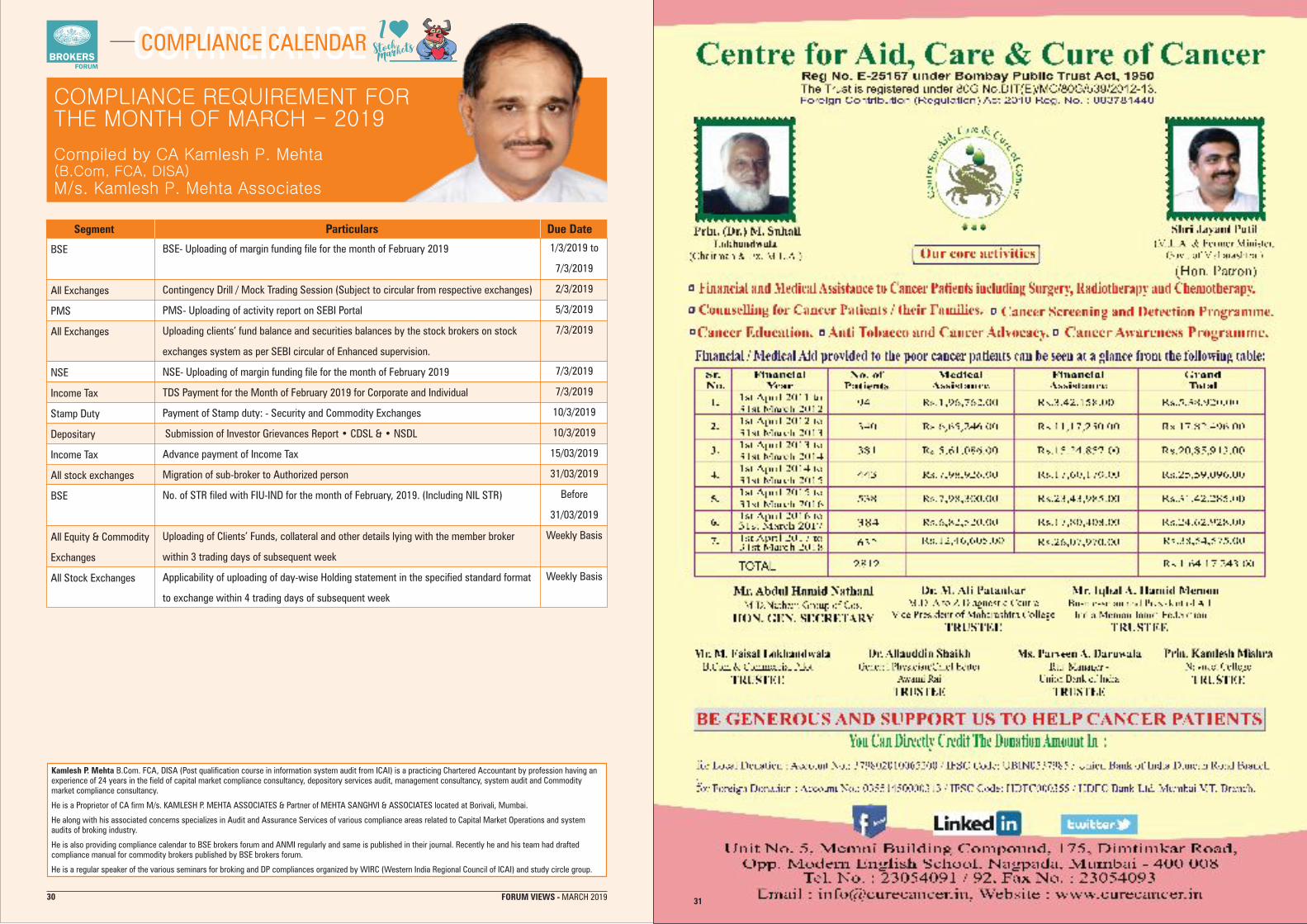

COMPLIANCE CALENDARMARCH 201930

24 ENTERPRISE SOFTWARE OPTIONS:LEGACY VS. CLOUD PART 2

PHILOSOPHY & SELF MANAGEMENT:SCULPT YOUR FUTURE50

CIRCULARS34

WELLNESS Q&A:OSTEOPOROSIS51

REGULATORYPULSE32

HEALING INSTITUTE: CILANTRO: THE 'SUPER HERB’52

S&P BSE SENSEX DURINGTHE MODI ADMINISTRATION’SBUDGET SESSIONS

22

MARCH 2019 CONTEMARCH 2019 CONTENTS

Follow us on: @bsebrokersforum /bsebrokersforum/brokersforumofindia /bsebrokers’forum

Write to us:We would be happy to hear from you! Do send in your suggestions, feedback and comments via email to

[email protected] | Visit us: www.brokersforumofindia.com

FITNESS CLINIC: TOBACCO & DIABETES:AN UNDERCOVER RELATIONSHIP?54

UNIFIED REGULATORY AUTHORITYFOR IFSC - INTERNATIONAL FINANCIALSERVICES CENTRES AUTHORITY

40

CEO 4.0 EMPATHY : KEY TOFULFILLING RELATIONSHIPS -PERSONAL OR PROFESSIONAL

46

BUDGET- ARE WE GETTINGRICH OR POOR?42ARTICLE ON: EMPLOYEESPROVIDENT FUND43

07 BBF GLOBAL CONNECTS -ONE BBF ONE WORLD

5

In support with

SOUTH KOREACONNECTS'

JAPAN

BOMBAY STOCK EXCHANGE BROKERS' FORUM (BBF)

AND

th th st st28 - 30 January 2019, South Korea | 31 January - 1 February 2019, Japan

Tokyo, Japan

7

ceo & coo message

6 FORUM VIEWS - MARCH 2019

WelcomeDr. Vispi RusiBhathena,PhD (h.c.)

to magazine.Forum Views

The Interim Budget 2019 tried to touch various

segments of the economy especially the common man.

INTERIM BUDGET - tried to place money into common man’s hand!

The Interim Budget 2019 tried to touch various segments of the economy especially the common man. The key features which attracted the attention were the increased income tax exemption limit from current Rs. 2.5 lakhs to Rs. 5 lakhs. This would put more money into the hands of the common man for demand and consumption and thus contribute to the GDP growth of the country.

The other features like SME having GST number would be getting 2% interest subvention loan till Rs. 1 crore, it will also help SME segment to get credit and thus create jobs at the grass root level.

The SME companies have also been given the preference in all the Government projects where the 25% of the procurement will have to be done from the SME companies. This will give lots of business opportunity for the SME companies and thus add to their business and help the economy grow. SME's contribute around 40% of the total exports and around 45% of the total production is done by the SME segment.

The defense budget has been extended to Rs. 3 lakh crores which will also give lots of impetus to "MAKE IN INDIA" and thus create lakhs of jobs in the manufacturing segment. This will also save precious foreign exchange of the country and thus contribute to making the Balance of Payment very strong. The "BRAND INDIA" will also get boost from this and thus create many jobs at the grass root level.

RBI has reduced the Repo Rate from 6.5% to 6.25% which will reduce the cost of capital and thus contribute on the consumption side and also on the credit off-take side. The reduced cost of borrowing would also include corporates to expand and thus create jobs in the economy. The CPI data has still reduced from 2.19% to 2.05% and rise in Index of Industrial Production (IIP) data from 0.5% to 2.4% as the manufacturing expanded to 2.7% thus raising hopes that the demand in the manufacturing segment is rising. The reduced CPI and the increased IIP index will further give room to RBI to reduce the interest rates in the coming months and thus stimulate the economy.

BBF - Investor Education & Awareness Initiatives

On the BBF Front:

BBF - Representations

Reporting of auction and pay-in/payout shortages data Further suggestions and request for a review meeting

14 Jan SEBI

Represented ToTopicDate

BBF - Seminars and Events

Date Institutions

South Indians' Welfare Society College

South Indians' Welfare Society College

(Batch 1-2)

Lala Lajpat Rai College of Commerce

and Economics

Laxmichand Golwala College of Commerce &

Economics (Batch 1-2)

P. P. Savani University (Batch 1-3)

SDJ International College (Batch 1-4)

M. L. Dahanukar College of Commerce

(Batch 1-4)

Lala Lajpat Rai Institute of Management

(Batch 1-2)

A. E. Kalsekar Degree College of Arts

Science and Commerce

Oriental College of Education (Batch 1-4)

Vivek College of Commerce (Batch 1-3)

K. J. Somaiya College of Arts and Commerce

(Batch 1-4)

Jashbhai Maganbhai Patel College of

Commerce (Batch 1-4)

SVKM's Narsee Monjee Institute of

Management Studies - NMIMS

South Indians' Welfare Society College

PU's Education Services (Batch1-2)

15 Jan

16 Jan

16 Jan

21 Jan

22 Jan

23 Jan

28 Jan

29 Jan

30 Jan

4 Feb

5 Feb

6 Feb

11 Feb

12 Feb

13 Feb

13 Feb

Dr. Aditya Srinivas

a new life line to the global capital markets; the FII's in Indian markets have invested Rs. 6000 crores in the first week of February and thus they have turned net buyers. The year 2018 saw that despite FII's being net sellers to the tune of Rs. 32000 crores, the BSE SENSEX gave 5.6% return as the Indian Mutual Funds

The US Federal Reserve in its meeting held on 31st January 2019 also indicated that they are not in any hurry to increase interest rates in the USA. This will give

invested Rs. 1,20,000 crores. This shows that the Indian stock markets have become independent as retail investors are putting money through SIP (Systematic Investment Plan) and thus contributing into the growth of the Indian stock markets.

Seminar on Surveillance Measures includingGSM/ASM (With BSE Ltd.) | Mumbai

13 Feb

TopicDate

Investment Outlook 2019 | Ahmedabad22 Feb

CAMP for Single Registration (With BSE Ltd.)15 & 18 Feb

Bombay Stock Exchange Brokers’ Forum (BBF) Connects TourSouth Korea and Japan - January 2019

BACKGROUND

The growth of the Indian economy requires Capital infusion at all levels, from smaller businesses to larger infrastructural projects. Foreign Portfolio Investors (FPI) and Foreign Direct Investors (FDI) are an important source of inflow for this capital.

Various Indian entities including government, businesses and intermediaries approach potential investors throughout the world. However, the list of such potential investors is not readily available and this leads to lots of hits and misses.

The Bombay Stock Exchange Brokers Forum (BBF) is one of the apex trade bodies of the securities firms in India. BBF is also a member of various international forums like Asia Securities Forum (ASF), International Council of Securities Associations (ICSA) and International Forum for Investor Education (IFIE). At these forums, we are in touch with local financial market bodies of various jurisdictions around the world.

Using the rapport and relations built with these members, BBF has embarked upon a mission to target potential investors of various jurisdictions who would be interested in investing in Indian assets. We began our journey with South Korea and Japan.

In case of South Korea, we partnered with Korea Financial Investment Association (KOFIA), the Self-Regulatory Organization (SRO) of securities firms and asset management companiesof South Korea.In case of Japan, we partnered with Japan Securities Dealers Association (JSDA), the SRO of securities firms in Japan.

FORMAT OF THE BBF CONNECTS TOUR

The tour was conducted in the last week of January 2019. The format followed in both the countries was:

Day 1 - Public seminarDay 2 - One to one meetings of the attendees with the delegates

The venues were the KOFIA conference room at Seoul, South Korea and JSDA conference room at Tokyo, Japan.

All attendees were invited by our local partners viz. KOFIA and JSDA, since their understanding of the home market would be deeper than any other agency.

INDIAN DELEGATION

The Indian delegation consisted of office bearers of BBF, an Indian Custodian, an Indian Tax expert, an Indian Mutual Fund representative and a Stock Exchange representative. Attempt was made to have a composition that covered the entire gamut of investing in India with a particular emphasis on Indian Capital and Financial Markets.

INDIAN Delegation along with KOFIA representatives at Seoul (28-Jan-2019)

Indian delegation - left to right (Mr. Myungsoo Sim -KOFIA, Mr. Vinay Purohit -SHCIL, Mr. Ujwal Damani -BBF, Mr. V. Bala-India INX, Mr. R. Anand -SHCIL, Mr. Uttam Bagri -Chairman BBF, Mr. Young Won Kwon -Chairman KOFIA, Mr. GaurabParija -IDFC AMC, Mr. Anurag

Bansal -Vice Chairman BBF, Mr. Vineet Potnis -SHCIL, Mr. Sangchul Park -KOFIA, Mr. Manoj Purohit -Deloitte, Ms. Hanni Kang -KOFIA)

8 FORUM VIEWS - MARCH 2019

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

9 FORUM VIEWS - MARCH 2019

HIGHLIGHTS• Program was supported by both the Indian Embassy in Seoul and the Indian Embassy in Tokyo. The Indian

ambassadors at both places took personal interest in the outreach program.

• The Seoul seminar saw around 125 attendees, while the Tokyo seminar had around 80 attendees. The interest was more than envisaged by the local support partners themselves.

KEY OBSERVATIONS

• Securities firms in South Korea and Japan follow an omnibus structure where the client’s funds and securities are held by the securities firms and they invest in dozens of other jurisdictions in the name of the securities firm without needing to register their final clients.

• Among the High Net-worth Individual (HNI)’s of foreign jurisdictions, there is a significant resistance in registering with the income tax authority of any other country and therefore they find taking Indian Permanent Account Number (PAN) extremely challenging.

• There is a general perception that Indian Markets are very complex and most attendees had opinions of Indian Markets which were dated. Most were not aware of the latest structures and regulations and some queries were very basic.

• There were many tax related queries. The attendees were happy to be made aware of the Indian Double Tax Avoidance Treaty (DTAA) with South Korea and Japan and the benefits under the same.

• The ageing population and very low interest rates in both the countries lead to most attendees being highly curious of the higher interest rates in India combined with a young population.

• The option of coming in the International Financial Services Centre (IFSC) at Gujarat International Finance Tec-City (GIFT) was very much appreciated. However, the interest towards investing in Indian Equities rather than Derivative instruments was more.

• There was repeated interest shown in investing in Indian Fixed Income Securities starting with Indian Government Securities and queries on the how were commonplace. There were also queries on style and manner of hedging the currency risks.

• Some foreign entities who had ventured into India in the past have not had a good experience primarily because of lack of local domain knowledge. However, they are still open to consider India once more.

• Interest was shown by entities in setting up their Indian operations either in form of 100% owned subsidiaries or taking strategic (open to both majority or minority) stakes in Indian financial firms.

• Both the countries are happy to promote listing of Indian Securities on their market with special interest shown for Japanese Securities Receipts (JDR)

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

11 FORUM VIEWS - MARCH 2019

SOME LIGHT MOMENTS28th January | Korea | Seminar & Dinner with Ambassador at Republic Day Function

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

10 FORUM VIEWS - MARCH 2019

Indian Delegation with H.E. Smt. Sripriya Ranganathan, Ambassador of India to South Korea

Indian Delegation with H.E. Shri Sanjay Kumar Verma, Ambassador of India to Japan

SUGGESTIONS- The omnibus account structure is used by many participants for many jurisdictions. India must consider creating

some midway to take care of (KYC) requirements and at the same time not disrupt the existing style of operations of the foreign entities, esp. for well regulated entities in countries like South Korea and Japan.

- The level of understanding and knowledge of the Indian Capital Markets is woefully inadequate. More frequent knowledge sessions and reach outs are essential for potential investors to get excited about India and consider India as a serious Investment option.

OUR MESSAGE TO POTENTIAL FORIEGN INVESTORSAt all levels of interactions, the delegation stressed upon the need for all global firms to setup dedicated Indian investment teams with local talent to the extent possible for higher chances of success.

SPECIFIC DEALS UNDER DISCUSSION - One large Asset Management Company in South Korea is contemplating setting up Mutual Fund Operations in

India.

- A medium size securities firm in Japan is contemplating taking a minority stake in an Indian securities firm and using the same as a vehicle to route Japanese Investments into India

- Some Korean & Japanese firms are looking at investing into Indian Government Securities

- One Korean firm is looking at Real estate opportunities in India on a buy and rent model

The indicative size of above deals is in the range of USD 10 - 30 million

Going AheadWe believe the above is a trickle which can become a flood if dealt well. It is critical that Foreign Investors in India get right advice and earn reasonable returns since their experiences create a significant word of mouth message in their rather tight-knit financial community.

BBF will continue its endeavors to improve awareness of Investment Opportunities in India in general and Indian Capital Markets in particular in the above jurisdictions and more.

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

13 FORUM VIEWS - MARCH 2019

31st January | Japan | Stock Exchanges visit, Seminar Networking Dinner

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

12 FORUM VIEWS - MARCH 2019FORUM VIEWS - MARCH 2019

29th January | Korea | Visit to KSD & Networking Dinner

BBF GLOBAL CONNECTBBF GLOBAL CONNECTS’

14 FORUM VIEWS - MARCH 2019

NFRA - THE NEW WATCHDOG FORACCOUNTANCY AND AUDIT PRACTICES

By Prachi JainAdvocate, RegStreet Law Advisors

BULLS & BEARSBulls & Bears

1he Ministry of Corporate Affairs (“MCA”) videnotification dated October 01, 2018 notified sub-section (1) and (12) of Tsection 132 of the Companies Act, 2013 (“Companies Act”

or the “Act”) with immediate effect. These sections empower the Central Government to constitute a National Financial Reporting Authority (“NFRA”) for making recommendations on accounting policies and auditing standards to the Central Government. In view thereof, the MCA notified the National Financial Reporting

2Authority Rules, 2018 (“NFRA Rules”) videnotification dated November 13, 2018 effective from November 14, 2018.Former IAS officer Mr. Rangachari Sridharan was appointed as the first chairman of NFRA.

WHY NFRA?

In the wake of several high profile accounting scams, establishing NFRA is necessary for enforcement of auditing standards and ensuring the quality of audits to strengthen the independence of audit firms, among others.

Statistical analyses carried out by MCA revealed as follows:

• Of the 1,972 cases taken up by the Disciplinary Committee/Board of Discipline of the Institute of Chartered Accountants of India (‘ICAI’), only in the matter relating to Satyam Computers have the members been permanently removed. Only in 14 of these cases, has a penalty of one year or more been imposed on the members.. In majority of the cases, the members had been found not guilty. Further, in majority of the cases where members have been found guilty, they have been merely reprimanded or cautioned.

• 1226 cases were closed at prima facie stage by the Board of Discipline/Disciplinary Committee. Of these, 117 cases were referred by various Government agencies/regulators. 49 of these cases were referred by MCA/SEBI and the professional involved were found to be not guilty at the prima facie stage. The closure of these cases took from 1-4 years.

• Only 4 percent of the 746 cases which proceeded beyond the prima facie stage before the Disciplinary Committee/Board of Discipline of the ICAI since 2007 have been on a suo-moto

basis. Other than Satyam matter, only in 6 of these cases have the Members been found guilty and they have been reprimanded or cautioned.

• 137 of 746 cases taken up for considered beyond the prima facie stage by the Disciplinary Committee/Board of Discipline were based on complaints by government/regulatory agencies. The Committee found members guilty in 54 of these cases, of which in 5 cases, the Committee imposed a penalty of name removal for one year or more and/or fine.

Accordingly, it may be noticed that in various cases, ICAI failed miserably in fulfilling its responsibility to even investigate into the acts and affairs of the auditors and at a later stage to even punish and proceed against such defaulting auditors. Further, cases involving investigation by ICAI took long to conclude, due to which the purpose behind the auditor(s) being investigated was defeated altogether.

In various other cases, ICAI even failed to take preliminary action on cases, which were referred by MCA, for examining the role of auditor and possible misconduct with regard to 132 listed companies identified by SEBI for suspected abnormal price rise, wherein such price rise was not supported by the fundamentals of the companies. Such was the lethargic and irresponsive behavior of ICAI despite several reminders.

It is relevant here to recall the scam in the matter of United Spirits Limited (USL) wherein fraud during the years 2010 to 2013 was detected pursuant to the forensic audit conducted by PricewaterhouseCoopers (PwC) UK with the assistance of PwC India. Ironically, Price Waterhouse was the auditor for USL till 2010-11. However, till date ICAI has not taken any action against the errant auditors.

One must not forget the PNB Scam case, wherein various media articles state that if there was a breakdown of checks and balances in PNB, the auditor should have been the first one to point it out. One of these articles goes on to further state that the technology auditors of the bank need to be asked how come two technical systems, SWIFT, and the core banking system, do not

3talk to each other. It is a case of system failure .

ICAI is a body vested with limited powers of initiating disciplinary proceedings against auditors only and not against audit firms which ultimately failed to deter audit firms from acting hand in glove with the management of the companies.

CONSTITUTION OF NFRA

1) Reservations by ICAI

While the recommendations for constitution of NFRA as a separate and independent body for overseeing the implementation of widely accepted international accounting and

In the wake of several high profile accounting scams, establishing

NFRA is necessary for enforcement of auditing

standards and ensuring the quality of audits to strengthen the

independence of audit firms, among others.

15 FORUM VIEWS - MARCH 2019

BULLS & BEARSBulls & Bears auditing practices by auditors as well as bodies corporate were

4made, according to the 37th report of the Standing Committee on Finance dated December, 2016 several representations were made by the ICAI flagging of inter - aliathe following points of concerns:

a) Multiple Regulatory Bodies: Creating NFRA would result in two regulatory bodies (ICAI and NFRA) governing the same audit profession. This would result in duplication of efforts, and add huge costs with no significant incremental benefits. This would also change the self-regulated profession to an externally regulated body.

b) The ICAI Context: A major objective for constitution of NFRA is to ensure that the functions of setting accounting and auditing standards as well as enforcement of the same are not carried out by the same body. It is important to note that like the Securities and Exchange Board of India (“SEBI”) which is a body constituted by an act of the Parliament, performing dual functions of laying down its own regulations and overseeing the enforcement of the same, similarly ICAI has also been constituted by an act of the Parliament.

Accordingly, the constitution of NFRA needs to be re-examined in the mentioned contexts where relevant mechanisms and units have been enabled by and/or within the ICAI organisation to deliver the twin objectives of robust policy making and unbiased enforcement in a timely manner.

c) Relevance of NFRA in the context of the Companies Act, 2013: The objective of NFRA is to regulate audit quality and protect public interest. These, in any case, are also the main objectives of ICAI which strives to be a world class regulator.

d) Auditing Standards: ICAI as a world class regulator would be more aligned to market needs, international practices and risks and to be able to define and improve auditing standards rather than NFRA.

e) Disciplinary Mechanism: The Disciplinary Committee of ICAI normally completes the process in a reasonable period of about three to four years.

f) International benchmarks: The Public Companies Accounting Oversight Board (PCAOB) of the US may be regarded as a possible closely comparable body to NFRA, if notified. It is relevant to note that PCAOB has evoked mixed responses in its ability to improve audit quality. The PCAOB budget for 2016 is estimated at $250 million and is enabled by 750 audit staff. The challenges of availability of trained and qualified audit staff and the cost thereof may need to be appreciated ahead of the decision to notify NFRA.

g) Uniform administration: Scale based differentiation of regulating authority may result in conflicting judgements on the same issue. Seamless coordination may always not be possible between NFRA and ICAI due to the multiplicity of disciplinary issues that may be handled by both agencies.

2) Clarifications by MCAIn response to the reservations of the ICAI received, the Ministry of Corporate Affairs (‘MCA’) issued inter - alia the following clarifications / reply in order to support its proposal of constituting NFRA, taking into consideration the practices followed by developed economies world over:

clarifications / reply in order to support its proposal of constituting NFRA, taking into consideration the practices followed by developed economies world over:

a) The enforcement of the auditing standards and ensuring the quality of audits moved from self-regulating bodies, in the wake of the accounting scams worldwide, to independent regulators like the Public Company Accounting Oversight Board (PCAOB) and Financial Reporting Council (FRC) in the US and UK respectively. Other major countries have also followed suit. It was recognised in these jurisdictions that establishing regulators, independent ofthose it regulates, would strengthen the independence of audit firms, quality of audits, and enhance investor and public confidence in financial disclosures of companies.

b) World over, the number of independent audit regulators have increasedover a period as one could see from the membership of International Forum of Independent Audit Regulators (IFIAR) which was established in 2006 by independent audit regulators from 18 jurisdictions and now covers 51 jurisdictions (including PCAOB and FRC). IFIAR, inter alia, promotes international collaboration between the regulators. The oversight structure of auditors within ICAI has not been recognized as independent by IFIAR and India is not represented on this body.

c) SEBI had engaged M/s Oliver Wyman (OW), an international consultant to revisit the structural and organisational issues, re-prioritize areas of focus and to look at the technological and manpower needs of SEBI. OW in its report hadinter-alia stated that "Currently the Institute of Chartered Accountants of India (ICAI) is responsible for maintenance of accounting, auditing and ethical standards. However the ICAI's oversight is passive in nature and with limited focus on active investigations. In addition, oversight is rendered challenging given the large number of auditors in India (around 15000 vs around 3000 in USA). Scope to enhance the quality of audit has been recognised by multiple supervisory bodies including SEBI, RBI and Comptroller & Auditor General of India. In the long term, we recommend that SEBI drive the case for establishing a separate regulator for auditors which is independent of audit profession. This body must be set up with a clearly defined mandate, adequate resources for active monitoring and appropriate enforcement process. In the near term it is recommended that SEBI provide inputs for the role of function of National Financial Reporting Authority with respect to supervision of auditors (providing services to listed companies) and mechanisms for interaction with SEBI".

d) Accordingly, once the authority is constituted and starts functioning, it would be recognized in international forums also, and some of the difficulties being expressed viz parity in respect of legal action/liability of Indian partners/firms vis-à-vis global/multinational and other similar aspects would evolve to match international practices.

NFRA RULESAs compared to the powers vested on the National Advisory Committee on Accounting Standards established as per section 210A of the erstwhile Companies Act, 1956 which was mainly constituted to advise the Central Government on the formulation and laying down of accounting policies and accounting standards for adoption by companies or class of companies under the said

16 FORUM VIEWS - MARCH 2019

BULLS & BEARSBulls & Bears

ACTIONS BY SEC AGAINST THE AUDITORS

1

Sr.No.

Summary of the matter

act, the NFRA is endowed with widespread powers, ranging from making recommendations to the Central Government on accounting standards and auditing practices to be followed to taking actions, imposing penalties on auditors, audit firms and / or bodies corporate for any violations or negligence.

NFRA has been constituted as a quasi-judicial body with larger powers than National Advisory Committee on Accounting Standards. In a nutshell NFRA shall be responsible for recommending auditing and accounting standards, to monitor and enforce compliances with the said standards and oversee the quality of service and suggest measures for improvement unlike National Advisory Committee on Accounting Standards which only advised on accounting standards.

1) Applicability of the NFRA Rules The categories of entities to which the NFRA Rules are applicable, has been provided in Rule 3 (1) of the NFRA Rules, as follows:

1) Companies whose securities are listed on any stock exchange in India or outside India;

2) Unlisted public companies fulfilling any of the following criteria as on the 31st March of immediately preceding Financial Year:a) having paid-up capital of not less than Rs. 500 crores or;b) having annual turnover of not less than Rs. 1000 crores or;c) having, in aggregate, outstanding loans, debentures and

deposits of not less than Rs. 500 crores.3) Insurance companies, banking companies, companies

engaged in the generation or supply of electricity, companies governed by any special Act or bodies corporate incorporated by an Act in accordance clauses (b), (c), (d), (e) and (f) of section 1(4) of the Act;

4) Body Corporate/Companies/Persons or any class of them referred by Central Government to the Authority in public interest; and5) Body Corporate which is:a) Incorporated or registered outside India, which is a

subsidiary company or associate company of the company or body corporate registered in India as referred in point (1) to (4) above; and

b) Whose income or net worth exceeds 20% of the consolidated income or consolidated networth of such company or the body corporate.

Also, the companies and bodies corporate covered by the Rules shall continue to be governed by the Authority for a period of three years after it ceases to be listed or its paid-up capital or turnover or aggregate of loans, debentures and deposits falls below the limit stated therein.

2) Non-Applicability of the NFRA Rules Considering the provisions of applicability of the Rules, following companies shall not be governed by the NFRA:

1) Private Companies (unless referred by Central Government to the NFRA in public interest); and

2) Unlisted public companies with paid-up capital or turnover or aggregate of loans, debentures and deposits below the limit stated under Rule 3(1).

Note: The NFRA Rules however require all the existing bodies corporate, other than the companies governed by the NFRA Rules to inform NFRA the particulars of its auditors as on November 14, 2018 (date of commencement of NFRA Rules) within a period of 30 days from the date of commencement of the NFRA Rules.

3) Functions, duties and powers of NFRAThe NFRA has been cast with the responsibility inter - aliaof protecting the public interest and the interests of investors, creditors and others associated with the companies or bodies corporate governed under rule 3, as discussed above, by establishing high quality standards of accounting and auditing and exercising effective oversight of accounting functions performed by the companies and bodies corporate and auditing functions performed by auditors.

NFRA is also responsible for recommending accounting or auditing standards for the approval of the Central Government, after taking into consideration the recommendations and additional information received from ICAI for new accounting standards or auditing standards or amendment of the existing standards.

4) Jurisdiction of NFRANFRA has also been empowered to investigate into any matter of professional or other misconduct under section 132 (4) of the Act, either suomotu (after recording reasons in writing), or after receiving reference from the Central Government or on the basis of its compliance or oversight activities.

Further, actions in respect of professional or other misconduct against auditors of companies referred to in Rule 3 above, shall be initiated by NFRA only and no other institute or body shall initiate any proceedings against such auditors. Accordingly, on the commencement of these rules, no other institute or body can initiate or continue any proceedings in such matters of misconduct where the Authority has initiated an investigation.

Accordingly, the action in respect of cases of professional or other misconduct against auditors of companies or bodies corporate other than those referred to in rule 3 above, shall continue to be proceeded with by the ICAI as per provisions of the Chartered Accountants Act, 1949 and the regulations made thereunder.

Audit Failures: Maintaining Professional Skepticism

On October 18, 2016, Ernst & Young LLP (“E&Y”) agreed to pay more than $11.8 million to settle charges that it failed to adequately conduct an audit of its client, Weatherford International (“Weatherford”), permitting Weatherford to inflate its earnings and issue false financial statements in violation of

5U.S. Generally Accepted Accounting Principles (“GAAP”) .

The SEC alleged that E&Y did not follow audit and professional care standards established by the PCAOB and, as a result, failed to detect that Weatherford had overstated its earnings by use of deceptive non-GAAP intercompany tax accounting practices.

These standards required, as part of the planning and execution of an audit, that auditors continually exercise professional skepticism with “a questioning mind and a critical assessment of audit evidence”.

Despite these standards and regular reminders from E&Y’s own National Office that expanded procedures were necessary to comply with PCAOB standards for audits of income tax accounting, the E&Y audit team failed to question numerous suspicious tax adjustments that were brought to its attention and instead relied completely on the client’s explanation of them.

17 FORUM VIEWS - MARCH 2019

BULLS & BEARSBulls & Bears

JURISDICTION OF SEBI ON AUDITORS

While the NFRA Rules have clearly addressed the issues relating to the jurisdiction of NFRA vis-à-visICAI with respect to the action against auditors for professional misconduct, an ambiguity which still persists is with respect to the jurisdiction of SEBI on the said misconduct.

In order to protect the interest of the issuers, intermediaries, pool investment vehicles, investors in the securities market, etc. who avail the services of the auditors inter - alia relating to issueof certificates or reports as required under the respective SEBI regulations, SEBI has released a consultation paper dated July 13,

102018 regarding SEBI (Fiduciaries in the Securities Market)(Amendment)Regulations. The recommendations made in the said consultation paper are yet to come into effect.

The said consultation paper is based on the recommendation of the Committee on Corporate Governance headed by Mr. UdayKotak, which is of the view that given SEBI’s mandate to protect the interests of investors in the securities market and regulating listed entities, SEBI should have clear powers to act against auditors and other third party fiduciaries with statutory duties under securities law, subject to appropriate safeguards. This power ought to extend to act against the impugned individual(s), aswell as against the firm in question with respect to their functions concerning listed entities. This power should be provided in case of gross negligence as well, and not just in case of fraud/connivance.

It may be recollected that Bombay High Court had affirmed the jurisdiction and powers of SEBI in Price Waterhouse & Co. vs. SEBI ((2010) 103 SCL 96 (Bom.) to act against auditors in cases where they were complicit in fraud.

In several cases, SEBI as a market watchdog, responsible for protecting the interest of the investors has taken actions against the auditor / audit firms as follows:

According to the SEC, E&Y’s blind acceptance of the client’s unrealistic explanations also violated the PCAOB’s principles of professional skepticism that warn that “an auditor should not be satisfied with less than persuasive evidence because of a belief that management is honest.”

Lack of Independence: Too Close for Comfort

About a month before the E&Y audit failure settlement related to Weatherford, E&Y also settled the first ever enforcement actions for auditor independence violations stemming from partner-client relationships. The SEC charged that the auditor-client relationships of two partners-one romantic-ultimately affected their independence. The SEC not only faulted the partners involved in the improperly close relationships but also the firm itself for failing to perform a reasonable inquiry or raise concerns about the relationships despite awareness of facts

6suggesting impropriety .

Two separate actions were filed against two separate engagement teams-both involving independence impeding conduct stemming from too-close client-auditor relations. The first action involved a romantic relationship between the engagement partner and the Chief Accounting Officer of the client. The SEC noted that their relationship was “marked by a high level of personal intimacy, affection and friendship, near-daily communications about personal and romantic matters (as well as work-related matters), and the occasional exchange of gifts of minimal value on holidays such as Valentine’s Day and birthdays.” The second action occurred because of a client-auditor relationship that the SEC deemed to be excessively friendly.The conduct involved the relationship partner and Chief Financial Officer of the client taking frequent, overnight out-of-town trips, sporting events and socializing to “an excessive degree.”

In both of the independence failure actions, the SEC highlighted the auditor’s role in protecting the public trust, and emphasized that it is the “auditor’s opinion that furnishes investors with critical assurance that the financial statements have been subjected to a rigorous examination by an objective, impartial, and skilled professional, and that investors, therefore, can rely on them.”

7E&Y in the said case agreed to pay $9.3 million to settle charges .

In 2001, the SEC charged Arthur Andersen LLP and four of its then current and former partners, including a regional practice director, with fraud in connection with Andersen’s audits of the annual financial statements of Waste Management, Inc. for the years 1992 through 1996. The Commission alleged that those financial statements, on which Arthur Andersen LLP issued materially false and misleading audit reports, overstated Waste Management’s pre-tax income by more than $1 billion.

To settle these allegations, Andersen agreed to entry of the first antifraud injunction against a major accounting firm in more than 20 years, and to pay the then largest-ever civil penalty

8against a Big Five accounting firm - $7 million .

In 2003, the SEC filed a civil injunctive action against KPMG LLP and five of the firm’s partners - including the head of the firm’s department of professional practice - in connection with the years 1997 to 2000 audits of Xerox Corp., alleging that they issued materially false and misleading audit reports on Xerox’s financial statements, which had used manipulative accounting practices to close a $3 billion “gap” between actual operating results and results reported to the investing public.

2

3

4

The firm agreed to settle the allegations two years later by paying $22 million and, later that year, and in the following year, the SEC announced settlements with the five partners that included penalties and suspensions from practice before the

9SEC of varying lengths for four of the partners .

1

Sr.No.

Summary of the matter

Ritesh Properties and Industries Limited

On discovering that the auditor - Shri Shashi Bhushan, Proprietor of M/s. Bhushan Aggarwal & Co. made false and misleading disclosures in the financial statements of Ritesh Properties and Industries Limited,detrimental to the interest of the investors, SEBI vide its order dated February 17, 2016 prohibited himfrom,directly or indirectly, issuing any certificate required under securities laws and the applicable provisions of the Companies Act 2013 - administered by SEBI for a period of one year.

WhatsApp Leak Case

SEBI began a probe in November 2017 after a media report surfaced with respect to circulation of unpublished price sensitive information in various private WhatsApp groups about certain companies before their official announcements.

2

18 FORUM VIEWS - MARCH 2019

BULLS & BEARSBulls & Bears

In order to bring the auditors within the ambit of SEBI in the capacity of ‘fiduciaries’, SEBI amended the regulations relating to prevention of insider trading, which now requires such auditors in the capacity of fiduciary to adopt a separate code of conduct for prevention of trading based on unpublished price sensitive information which may be obtained during execution of work assignments. Further, amendments have also been carried out in the regulations relating to prevention of fraudulent and unfair trade practices, which now considers trades carried out by fiduciaries on behalf of their clients without such client’s knowledge or instructions or misutilizing or diverting funds or securities held in fiduciary capacity as fraudulent and unfair trade practice. Such amendments have been carried out pursuant to the recommendations of the Committee on Fair Market Conduct which was chair by Mr. T.K. Viswanathan.

As stated above, though SEBI has issued amendment in the prevention of insider trading regulations and prohibition of manipulative and unfair trade practices regulations in this regard, and also seems to be in the process of notifying other amendments to SEBI regulations, the question which really lies here isindealing with situations relating to overlapping of powers by various regulators, judicial and quasi-judicial authorities against the defaulting auditor(s) in the times to come.

LESSONS FROM THE NFRA’S AMERICAN COUNTERPARTThe establishment of the NFRA can benefit from a look at its US counterpart: the Public Companies Accounting Oversight Board. The PCAOB was established in similar circumstances, after the Enron and other audit scandals. The Sarbanes Oxley Act of 2002 relocated the mandate of oversight of audit firms of public companies from American Institute of Certified Public Accountants, in the same way as the ICAI, which no longer enjoys that mandate in India. One may observe this shift from self-regulation of accountants to an independent regulatory body and identify similar concerns behind such a move.

Given the similar circumstances, it could be of assistance to analyse certain practices of the PCAOB as a regulatory body:

1) CompositionThe NFRA Rules prescribe that the NFRA will be composed inter - aliaof representatives of SEBI, RBI and the ICAI. These are regulatory bodies often responsible for the discharge of various

In order to further investigate into the matter SEBI had also called for internal investigation report from these companies, besides carrying out its independent investigation and conducting search and seizure operations at various places, including on the premises of various market entities, as well as auditors of such companies.

Satyam Scam Case

SEBI, on finding Price Waterhouse guilty of making misstatements in the financial statements in collusion with the management of the scam tainted Satyam Computer Services Limited, vide its order dated January 10, 2018 barred its network entities from issuing audit certificates to any listed company and intermediaries in India for two years. Further, Price Waterhouse Bangalore and its two erstwhile partners-S. Gopalakrishnan and Srinivas Talluri - had been directed to jointly and severally disgorge the wrongful gains of Rs. 13,09,01,664 with interest.

3

statutory duties and in the midst of such regulation this may give rise to certainsituations leading to conflicts of interest. The Sarbanes Oxley Act therefore does not prescribe such a composition but merely states that members must be:

“from among prominent individuals of integrity and reputation who have a demonstrated commitment to the interests of investors and the public, and an understanding of the responsibilities for and nature of the financial disclosures required of issuers under the securities laws and the obligations of accountants with respect to the preparation and issuance of audit reports with respect to such disclosures” (Section 101)

While the United States model may not sound ideal, one may consider the possibility of having former members of these institutions which shall ultimately meet the objective with which NFRA is constituted at the same time also avoiding situations leading to conflicts of interest.

The number of members who are or have been certified public accounts have been limited to 2 members on the PCAOB by the US legislation. Such limit seems to be imposed with intent to ensure views of various experts belonging from various different fields are available at the disposal of the PCAOB. The NFRA’s objectivity is of prime concern in the given circumstances, and this limit may be prudent.

2) EnforcementThe NFRA can conduct investigations suomotu upon reference by the Government in cases where there is suspected misconduct. This mandate extends to imposing fines, penalties and suspension of audit firms; powers that were never granted to the ICAI. The PCAOB extends these powers further to debar individuals’ association with registered audit firms. This acts as a deterrent to individuals acting in violation of regulations, and may be considered when further legislating on the powers of the NFRA.

3) Audit InspectionsThe PCAOB enjoys complete discretion in selecting audits, and often question audit firms about potential issues identified in their work. These firms are given an opportunity to respond and in the case of an unsatisfactory response, the audit deficiency is included in the public parts of the PCAOB inspection report. This ensures that audit firms discharge their obligations with care inter - aliato protect their reputation. The NFRA may use a similar approach to have a significant regulatory effect, communicating audit deficiencies to all the relevant stakeholders in the market place.

4) DisclosuresAs mentioned above, the PCAOB publishes portions of the audit inspection reports, to underline negligent behavior on the part of audit firms. Certain non-public parts of the inspection reports, which contain quality control lapses, are published if the audit firm fails to address them within a period of 12 months. The

11PCAOB has also adopted a new standard (effective 2019), requiring auditors to report critical audit matters in which the auditors had to confront the management. Such practices must be adopted by the NFRA as well.

RegStreet is a boutique law firm based in Mumbai. The firm’s focus areas are Capital Markets& Commodities, General Corporate Commercial, Financial Regulatory Practice, Compliance & Investigation, Litigation & Dispute Resolution and

Policy & Advisory Practice. More details can be seen at www.regsla.com and they can be reached at [email protected].

19 FORUM VIEWS - MARCH 2019

BULLS & BEARSBulls & Bears the financial reporting process. The actions of SEBI, MCA and NFRA bring a renewed focus on this role of auditors. This move has the potential to strengthen the first line of defense against violations of securities laws and allied regulations.

JURISDICTION OF NCLT ON AUDITORSNCLT, in exercise of its powers under section 147 (3) of the Companies Act, 2013.vide its order dated February 06, 2019, barred Mr. Mukesh Choksi, proprietor of Mukesh Choksi& Company from being appointed as an auditor of any company for a period of five years. Such order comes subsequent to the statement ‘I don’t know’ made under oath by the auditor while replying to questions like whether he was aware when the last annual general meeting of Zen Shaving was held and where the company's factory is located. Mr. Mukesh Choksi has been held guilty of signing off on a company’s books without inspection and colluding with its promoters in a fraudulent manner. This is the first time the NCLT has passed an order barring an auditor in such a fashion.

CONCLUSIONOver the past decade, the scope of duties and responsibilities of auditors in listed companies and market intermediaries has expanded vastly. Auditors have a role to play in different spheres and in each of them, the regulatory authorities attempt to regulate and monitor the actions of auditors. While such bodies are necessary to safeguard the interests of investors and public at large, there is an increased likelihood of jurisdictions of these authorities overlapping.

There have been numerous instances of auditors indulging with the management of companies to defraud the public. The intention behind stringent laws is to deter auditors and audit firms from such negligence and professional misconduct.

Professional accountants and auditors have always been on the front lines in their roles as public watchdogs and gatekeepers of

References• http://egazette.nic.in/WriteReadData/2018/190358.pdf• http://egazette.nic.in/WriteReadData/2018/192907.pdf• https://www.moneycontrol.com/news/business/comment-the-pnb-

scam-questions-for-the-bank-the-auditors-the-rbi-and-the-government-2512503.html

• http://164.100.47.193/lsscommittee/Finance/16_Finance_37.pdf• https://www.lexology.com/library/detail.aspx?g=c1997e6a-94d7-

46dc-8f48-7d5353dad988• https: / /www.cadwalader.com/resources/c l ients - f r iends -

memos/enforcement-at-the-gates-sec-action-against-big-four-firm-and-new-international-standards-highlight-the-role-of-accountants-as-financial-gatekeepers

• https://www.sec.gov/news/pressrelease/2016-187.html• https://www.sec.gov/news/headlines/andersenfraud.htm• https://www.sec.gov/news/speech/ceresney-enforcement-focus-on-

auditors-and-auditing.html#_ftn21• https://www.sebi.gov.in/reports/reports/jul-2018/consultation-paper-

on-proposed-sebi-fiduciaries-in-the-securities-market-amendment-regulations-_39541.html

• https://pcaobus.org/News/Releases/Pages/auditors-report-standard-adoption-6-1-17.aspx

he importance of India’s in the global economy becomes increasingly Tevident in the larger context of

slowing down growth particularly in advanced countries and China. According to the World Economic Outlook report by IMF, October 2018 s growth rates in most advanced economies will slow down, although there has been a recovery of growth prospects and employment post crisis. The projection cited by the report is, ``among advanced economies, the subdued outlook for potential growth reflects, to a large extent, slower labour force growth due to population aging... While labour productivity growth is expected to improve in the medium term, the slight acceleration will only partially offset the slower increases in labour input.’’

For three decades one of the highlights of the world economy was the rapid expansion of the Chinese economy was the growth engine which powered a fair proportion of world economic growth. Undeniably the importance of China’s economy will continue, in accompaniment the resonant significance of India as possibly the world’s next growth engine is imminent. Therefore what happens in India will become increasingly important for the world economy during the ensuing years. According to the world economic outlook report by the IMF, (October 2018) global economic growth, “... growth in the emerging market and developing economy group is set to remain steady at 4.7 percent in 2018-19. Over the medium term, growth is projected to rise to slightly less than 5 percent. Beyond 2019, the aggregate growth rate for the group reflects offsetting developments as growth moderates to a sustainable pace in China, while it improves in India (owing to structural reforms and a still-favourable demographic dividend)...’’

This article for the Econ Buzz views an important aspect of India’s emerging growth narrative- the main trends underlying employment creation in the

This article for the Econ Buzz views

an important aspect of India’s emerging growth

narrative - the main trends underlying

employment creation in the

Indian economy.

THE UNDERPINNINGS OFEMPLOYMENT CREATIONIN INDIA: AN OVERVIEW

By Professor Piya MahtaneyEconomist / Author

20 FORUM VIEWS - MARCH 2019

INSIGHTS - ECOINSIGHTS - ECONBUZZ

Indian economy. During the recent weeks there has been some discussion and debate about the country’s unemployment rate, without delving into the numerical details and discrepancies of various calculations made this article focuses on the crux of the matter which is that creating more jobs is a challenge that confronts the Indian economy. According to the economic survey, 2017-18, “The other issue is the challenge of employment. The lack of consistent, comprehensive, and current data impedes a ser ious assessment... Even so, it is clear that providing India’s young and burgeoning labour force with good, high productivity jobs will remain a pressing medium term challenge. An effective response will encompass multiple levers and strategies, above all creating a climate for rapid economic growth on the strength of the only two truly sustainable engines-private investment and exports’’

to an industrial economy this has certainly not meant that agriculture was relieved of its role as an important provider of employment. This feature stands in veritable contrast to the experience of a number of advanced countries where the emergence of an industrial sector absorbed the surplus labour released from the agricultural sector.

Furthermore, as we have seen unlike in the developed world the transition(in terms of sectoral importance) made by the Indian economy and some other developing countries from an agricultural to an industrial and then to a services sector was certainly not fuelled by a generalized increase in per capita income across all socio-economic categories.

In essence the impetus that would come from a surge in demand for products of the agricultural sector and for those from the manufacturing and services sector will unequivocally propel an increase in employment creation. This was a sequence that occurred in a limited way and not as a generalized phenomenon in the Indian context.

Recapitulating a commonly cited axiom - 1the Engel’s law to understand changing

consumption and demand profiles as incomes rise could aid analysis about the link between sectoral transition and the shift in employment patterns. Simply stated, the basic principle of this law is that as incomes rise individuals tends to allocate a smaller proportion of their expenditure towards food. Income elasticity of demand for food declines when incomes rise.

According to the latest National Sample Survey Organization expenditure on food items accounted for 43 per cent of total consumption expenditures in urban India (during 2004-05). This represents a significant decline from the share of 64 per cent that food expenditures had in total expenditures of urban India over the 1972-73.

At this point it would be useful to describe the main underpinnings of employment in India. India is a highly industrialized country, and according to the precepts of conventional economic thought (many of which have been validated) this should have meant a receding importance of the agricultural sector. Although for all practical purposes we can say that India has made the transition from an agricultural

21 FORUM VIEWS - MARCH 2019

Piya Mahtaney completed her second Master’s in Development Economics from Leicester University in England she embarked on a career in journalism with the Times of India. She was an assistant editor in Metropolis on Saturday, subsequent to which she joined as senior feature writer in Economic Times. As an economist that reported, analyzed and wrote on a wide range of socio-economic issues, writing a book about economic development and the emerging trends of globalisation seemed almost inevitable

The books that she has authored are as follows:• India China and Globalization (2nd ed), Palgrave

Macmillan (England), December 2014• Globalization and Sustainable Economic

Development, Palgrave Macmillan (U.S), August 1st 2013

• Institute of South East Asian Studies (Singapore) published an edition (August 2010) of my book India China and Globalisation.

• The first edition of India China and Globalisation was published by Palgrave Macmillan (England, 2007)

• Globalisation Con Game or Reality was published by Alchemy Publishers, India (2004) 2004.

• The first book titled Economic Con Game, Development fact or Fiction was published by Pelanduk Publications (Malaysia) in 2002.

INSIGHTS - ECONBUZZINSIGHTS - ECONBUZZ

expansion of the country ’s vast unorganized sector. Herein we have an instance of compressed growth which arises from the deficiency of purchasing power and not from a natural decline of expenditure allocations towards food and related products. This accentuates the imperatives of achieving an expansion of income across an entire gamut of socio-economic categories in India. Given that it is likely that India will have an average growth rate of 7 to 8 per cent per annum over the next few years and in this context the imminent question that arises is whether this would result in employment or not. Even if one were to be cold bloodedly pragmatic a fundamental fact is that the Indian economy does cannot afford the option of jobless growth.

The next article will focus on institutional reform.

and it was not as competitive and efficient as it is in current times there was at some stage a declining demand for manufactures and an increasing one for the output of the services sector. Once again the transition to the services sector, in terms of its 50 per cent contribution to the GDP at this stage of the country’s per capital income growth is rather unusual. Economic experience has demonstrated that the emergence of the services sector as the most important one occurs at when a country’s per capita incomes are high. Undeniably India’s per capita incomes have increased significantly but it cannot be considered high. (At this point in time India is a middle- income country)

Expectedly in the higher income categories individuals would allocate a higher proportion of their incomes to services. Consonant with this, an increase in the employment absorption of those who comprise the skilled and educated segments of the population by the services sector is hardly surprising.

However what is rather unique is the importance that the service or the tertiary sector has had in providing employment to those in the lower income groups. The service sector has acted as a safety net of sorts; At the lower end this sector has provided an avenue of livelihood to millions (who would otherwise have been without any means of sustenance) and it consists of a fairly diverse spectrum of service providers that have little or no skill. As a matter of fact a sizable proportion of this segment constitutes the informal economy of the country. More often than not the wages that the labour force in country’s informal economy receives is highly inadequate and is more often than not lower than the minimum wage (for the same task in the organized sector). Constrained or compressed demand for products of the agricultural sector does place limits on the demands for manufactures.

When demand for food is low as a result of a lack of purchasing power it represents a potential for growth which will obviously remain untapped until incomes among the poor increase. Consequently employment growth has been far from satisfactory and it is this feature that has fuelled the

1. Engel’s law: Consequent to rising incomes, the share of expenditures for food declines It must be noted that Engel found, based on surveys of families' budgets and expenditure patterns, that the income elasticity of demand for food was relatively low. The resulting shift in expenditures affects demand patterns and employment structures. Engel's Law does not suggest that the consumption of food products remains unchanged as income increases. It suggests that consumers increase their expenditures for food products (in percentage terms) less than their increases in income

In rural India too, the proportion of spending on food in total expenditures has reduced from 73 per cent over 1972-73 to 55 per cent over 2004-05. Although the survey does indicate that the Engel’s law does apply in certain income groups of the country’s population, it also cites that 10 per cent of the India’s rural population lives on just Rs 9 per day and 10 per cent of its urban population subsist on a slightly higher Rs13 a day.

Furthermore the expenditure on food as a proportion of total consumption is lower in states with a higher per capita expenditure and vice versa.

Thus unlike in the advanced countries Engel’s law does not apply to a fairly significant proportion of the low income groups in developing countries. Although it would be convenient to describe a landless labourer who can barely afford two square meals as someone with a low elasticity of demand it would be outrageous to consider this to be the result of Engel’s law operating. By no means does the subsistence and small farmer comprise a small minority of India’s agricultural economy, as a matter of fact it constitutes a significant proportion of the rural population.

For those in the primary sector that are unemployed or employed at wages that are highly inadequate it would take sometime for Engle’s law to operate because incomes would have to increase by a certain extent before the proportion of expenditure allocated to food and other agricultural products declines. Those who currently live on the margins of subsistence will have a higher income elasticity of demand for food in the initial stages of a rise in income. When demand for food is low as a result of a lack of purchasing power it represents a potential for growth which will obviously remain untapped until incomes among the poor increase.

The story of compressed demand continues even as we view the manufacturing* and services segment*. Over the last four decades the strides notched by Indian manufacturing has been remarkable. Even as it traversed a phase during which its progress was dampened

Ved Malla is Associate Director, Product Management at S&P BSE Indices, responsible for managing Equity and Strategy Indices in India and its neighboring countries. His objective is to expand business in the region through identifying local market trends and ensuring new products and services are aligned to the market’s needs. In addition, he is responsible for compliance and corporate secretarial work.

He has over 11 years of experience in the financial services industry. Prior to joining S&P BSE Indices, he worked with the two leading Indian stock exchanges (NSE and BSE) for about 10 years, playing an integral role in the growth of their index and market data productions. Previously, Ved was associated with Birla Sunlife Mutual Fund, where he was part of the compliance department.

He has a Master of Business Administration in Marketing from the Narsee Monjee Institute of Management Studies (NMIMS), Mumbai. He also received his Company Secretary certificate from the Institute of Company Secretaries of India.

very year in India, the Finance Minister presents the Union Budget, which is perhaps the most important economic Eactivity in the country. “Budget Day” comes with a lot of

expectations, and it therefore has a bearing on the capital markets in both the pre- and post-budget sessions. The days before and after the budget session usually bring volatility to the capital markets.

With “Budget Day”just around the corner, attention is turning tothe Finance Minister as he gears up to announce the last budget of this administration on Feb. 1, 2019. This will be consideredan “interim budget” rather than a regular budgetbecause India will havenational elections in a few months, and the next finance minister gets to make the final decisions after a new administration is formed. The interim budget will be crucial for the government consideringthe recent debacle in the state elections in December 2018, whichmay have an impact on the sops that are rolled out in this budget; hence, the people have higher expectations than usual during this budget session.

The S&P BSE SENSEX’s total return index value increased from 27,648.13 on Jan. 31, 2014, to 52,335.86 on Jan. 31, 2019, and the highest close was at 55,975.53 on Aug. 28, 2018 (see Exhibit 1). This represents a five-year CAGR of 17.30% for the period.

INSIGHINSIGHTS

22 FORUM VIEWS - MARCH 2019

The budget may be the most important economic activity affecting capital markets in India, and its relevance is

captured by the movement of the S&P BSE SENSEX.

S&P BSE SENSEX DURING THE MODIADMINISTRATION’S BUDGET SESSIONS

By Ved MallaAssociate Director, Product Management,S&P BSE Indices

DISCLAIMER: The S&P BSE Indices (the “Indices”) are published by Asia Index Private Limited (“AIPL”), which is a joint venture among affiliates of S&P Dow Jones Indices LLC (“S&P DJI”) and BSE Limited (“BSE”). Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. BSE® and SENSEX® are registered trademarks of BSE. These trademarks have been licensed to AIPL.

Past performance of an Index is no guarantee of future results. AIPL, S&P DJI and BSE (the “AIPL Cmpanies”) make no representation or warranty that investment products based on any Index will accurately track index performance or provide positive investment returns. The AIPL Companies do not make investment recommendations and do not sponsor, endorse, sell, promote or manage any investment fund or other investment vehicle that seeks to provide an investment return based on the performance of any Index. Performance returns for an Index do not reflect payment of charges or fees an investor may pay for investable instruments. AIPL Companies receive compensation in connection with licensing Indices to third parties. AIPL Companies. For more information on any of Indices please visit http://www.asiaindex.co.in/.

To conclude, we can say that the budget sessions tend to be volatile for capital markets in India. The pre-budget movement has historically been influenced by market participant expectations for the budget, while the post-budget movement tends to be based on the actual budget presented by the Finance Minister. The budget may be the most important economic activity affecting capital markets in India, and its relevance is captured by the movement of the S&P BSE SENSEX.

56000

51000

46000

41000

36000

31000

26000

31-J

an-1

4

1-M

ay-1

4

1-A

ug-1

4

1-N

ov-1

4

1-Fe

b-15

1-M

ay-1

5

1-A

ug-1

5

1-N

ov-1

5

1-Fe

b-16

1-M

ay-1

6

1-A

ug-1

6

1-N

ov-1

6

1-Fe

b-17

1-M

ay-1

7

1-A

ug-1

7

1-N

ov-1

7

1-Fe

b-18

1-M

ay-1

8

1-A

ug-1

8

1-N

ov-1

8

S&P BSE SENSEX...

S&

P B

SE

SEN

SEX

Tot

al R

etur

ns

Exhibit 1: S&P BSE SENSEX Total Return

Source: S&P Dow Jones Indices LLC. Data from Jan. 31, 2014, to Jan. 31, 2019. Index performance based on total return in INR. Past performance is no guarantee of future results.Chart is provided for illustrative purposes.

PERIOD BUDGETDATE PRE-

BUDGET

RETURNS (%) VOLATILITY(MONTHLY) (%)

POST-BUDGET

PRE-BUDGET

POST-BUDGET

10-Jul-14

28-Feb-15

29-Feb-16

01-Feb-17

01-Feb-18

01-Feb-19

2014-2015

2015-2016

2016-2017

2017-2018

2018-2019

2019-2020

-0.28

-1.14

-6.88

3.88

6.39

0.02

-0.22

-5.88

7.86

4.36

-5.27

NA

3.97

3.81

5.96

2.51

1.99

3.28

3.68

3.92

5.01

2.41

3.92

NA

Exhibit 2: 30-Day Pre- and Post-Budget Day MonthlyReturns and Volatility of the S&P BSE SENSEX

Source: S&P Dow Jones Indices LLC. Data from June 9, 2014, to Jan. 31, 2019. Past performance is no guarantee of future results.Tableis provided for illustrative purposes.

In Exhibit 2, we can see that in most years, the S&P BSE SENSEX witnessed high volatility in the 30-day pre- and post-budget sessions. The highest 30-day pre- and post-budget volatility was observed in 2016. The lowest volatility in the 30-day pre-budget session was seen in 2018.

23

CLOUD BASEDSURVEILLANCE& MONITORING

#ADVERTORIAL

By Siddharth BeraManaging DirectorEpitome Corporation Pvt. Ltd.

Our tiny “Epitome Encoder” app is auto

start, auto connect and redundant app which

start sending stream on booting of the device.

2) Cloud Tablet for Exam Surveillance: For Exam there is a smart role based and administrative auto monitoring system with secured encoding app, decoding video management interface and the most secured cloud based recording and live streaming.• 100% transparency in process.• Secured live monitoring from control

room make the process easy.• No scope of examination being

disturbed. • Avoid any malpractices in the

examinations hall.• Confirm all the identity in examinations

room always with proof. • Enable the examinations centers with

central administrative real time monitoring and avoid the physical checking by authorities.

3) Election Polling booth Monitoring via Cloud Tablet: For Election there is a smart role based and administrative auto monitoring system with secured encoding app, decoding video management interface and the most

Contact us: [email protected]

Telephone: +91 98795 44338 Website: http://epitomesolutions.in

Log on www.epitomesolutions.in to know about the services they offer.

secured cloud based recording and live streaming.

This application is the tiniest, low weight, auto start and auto reconnect app. This app will immediately start on the booting of device and start sending stream with capture of default camera. No man power required to operate, setup etc. Just mounting the tablet with power on will make the application run.

Component:• Cloud tablet with streaming app.• Video management portal.• CDN streaming cloud.• Cloud or local device recording.

Benefits of Election Polling Booth Monitoring Via Cloud Tablet• No Compromise. The central authority

can directly monitor the polling live without any delay. 100% improvement on security and work efficiency.

• No scope of election being disturbed.• No chance of discontinuation of any

movement during live.• Avoid any malpractice in the polling

booth.• Fully transparency in end to end

process.• Enable the central election commission

department to see each activity live whenever needed.

pitome’s cloud based surveillance and monitoring systems is easy to Euse, self-managed which don’t

required any dedicated manpower to use and operate. Just plug in the tablet and using available internet connectivity (2G/3G/4G or Wi-Fi) you are on secured mode of Go Live. Our tiny “Epitome Encoder” app is auto start, auto connect and redundant app which start sending stream on booting of the device. Back hand services will contentiously monitor the status and in any case of internet disconnect it will start offline recording and in case of reconnect of internet it will auto start sending live stream.

Epitome’s cloud based surveillance technology eliminate the use of dedicated system(s) or a dedicated server(s) or video recording system for any business. This is the most reliable system for online monitoring from anywhere to everywhere. Cloud based surveillance system allows the user to use an easy server process and be Online in the cloud in no time, and with the security & safeguards.

This product is most suitable to sectors like City surveillance, Election, Examination, Shops, Malls, Streets, Traffic signals etc.

1) Cloud Camera:Cameras are cloud-based Wi-Fi video monitoring devices with live streaming and remote viewing that makes it easy to stay connected with whatever you care for most from the people in your life, to your business, from wherever you are.• Stay connected with your children or

parents.• Secure your Belongings• Keeping an eye on your business, 24/7

• Watch all of your cameras at once• Anywhere, anytime access with the

Camera app• Easy Deployment with High Speed

Wireless Internet Access

ENTERPRISE SOFTWARE OPTIONS:LEGACY VS. CLOUD PART 2

By Jayesh ShahPromoter, Prism Cybersoft Private Limited

TECH-SPEAKTECH-SPEAK

With SaaS, a provider licenses an application to

customers either as a service on

demand, through a subscription, in a “pay-as-you-go”

model, or (increasingly) at no

charge. This approach to

application delivery is part of the utility computing model where all of the

technology is in the "cloud" accessed

over the Internet as a service.

24 FORUM VIEWS - MARCH 2019

n the last article we had discussed about Enterprise vs Saas a brief from Ithe last issue. Similarly, the business

you run is not the same as it was when you started it. There are lot of reasons to fix your legacy system . The real cost of running such software is the major one among them.

Legacy system also involves lots of updates and changes , Infrastructure maintenance and staff training . Regardless of the chosen approach and technique, software modernization is a complex, labor intensive and risky process. Yet, the results are well-worth the risk .SaaS allows for an economic shift to relatively low-cost subscriptions that include upgrades and maintenance (an operational expenditure).

Customer satisfaction: SAAS plays an important role in customer satisfaction.

By outsourcing the technological preconditions, we’re able to save time and focus on what customers really need. It’s axiomatic that great customer satisfaction drives customer loyalty . Today, all that has changed. Using the resources available in the cloud - virtually unlimited amounts of cheap storage, sophisticated analytics, and machine learning, to name a few - it’s now possible to gain detailed, actionable insights as never before. We can truly know our customers.

How is SaaS different from an ASP?: SaaS evolved from the application service provider (ASP) model. When ASPs sprang up in the 1990s, they offered essentially the same thing SaaS vendors offer today: hosted applications delivered over the Internet. The problem ASPs ran into was that they tried to be all things to all people, and they buckled under the weight of their own infrastructure. In trying to serve the

local area network or personal computer. With SaaS, a provider licenses an application to customers either as a service on demand, through a subscription, in a “pay-as-you-go” model, or (increasingly) at no charge. This approach to application delivery is part of the utility computing model where all of the technology is in the "cloud" accessed over the Internet as a service.

What is Software as a service? :It is a software licensing and delivery model in which software is licensed on a subscription basis and is centrally hosted. It is sometimes referred to as "on-demand software", SaaS is typically accessed by users using a thin client via a web browser. Software as a service (SaaS) sometimes referred to as “software on demand,” is software that is deployed over the internet and/or is deployed to run behind a firewall on a

Cloud ClientsWeb Browser,

Mobile app, thin client

SAAS (Application)Emails, Games,Any application