Embed Size (px)

Citation preview

C r e a t i v e I n d u s t r i e s S e r i e s N o . 4

National Studieson

Assessing the Economic Contributionof the Copyright-Based Industries

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

1

Ta b l e o f C o n t e n t s

The Economic Contribution of Copyright-Based Industries in Australia 3

The Economic Contribution of Copyright-Based Industries in Kenya 25

The Economic Contribution of Copyright-Based Industries in Malaysia 107

The Economic Contribution of Copyright-Based Industries in the Netherlands 195

The Economic Contribution of Copyright-Based Industries in Peru 227

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

2

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

3

The Economic Contribution of Copyright-Based Industries

in Australia

Prepared for the Australian Copyright Council by Price Waterhouse Coopers

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

4

C o n t e n t s

Key findings 6

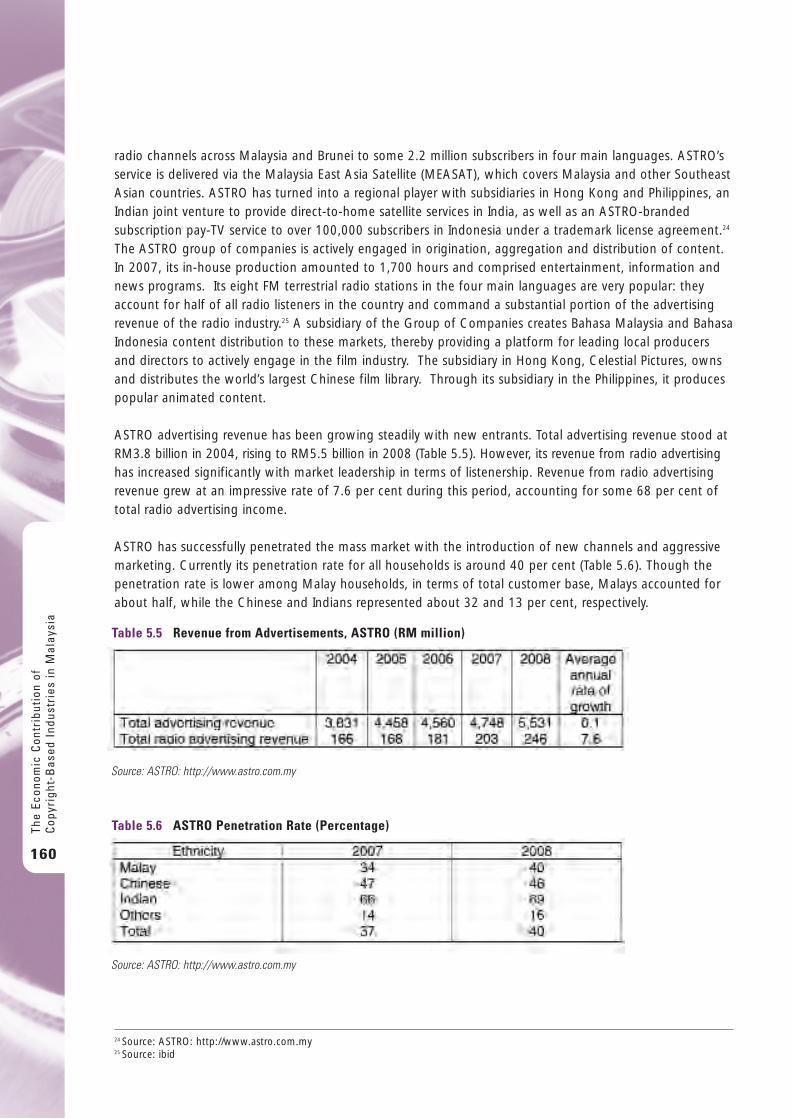

Introduction 81 Value added by copyright industries 132 Employment in copyright industries 163 Trade in copyright products 21

Sources 24

This Report has been prepared by PricewaterhouseCoopers (PwC) at the request of the Australian CopyrightCouncil (ACC) in our capacity as advisors in accordance with the Terms of Reference and the Terms andConditions contained in the Consultant Agreement between ACC and PwC.

The information, statements, statistics and commentary (together the “Information”) contained in this reporthave been prepared by PwC from publicly available material. The Consultants may in their absolute discretion,but without being under any obligation to do so, update, amend or supplement this document. PwC hasbased this report on information received or obtained, on the basis that such information is accurate. The Information contained in this report has not been subject to an Audit.

Comments and queries can be directed to: Jeremy Thorpe Partner – Economics and Strategy PricewaterhouseCoopers 210 Sussex Street Sydney NSW 2000 Phone: (02) 8266 3730 Email: [email protected]

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

5

K e y f i n d i n g s

Copyright is a key piece of infrastructure that supports the industries that comprise a modern economyThe World Intellectual Property Organization (WIPO) has identified four classes of copyright industries:• Core – industries that exist only because of copyright and are primarily involved in the creation,

manufacture, production, broadcast and distribution of copyrighted works.• Partial – a portion of the industries’ activities are related to copyright through manufacture,

performance, exhibition, broadcast, communication or distribution and sales.• Interdependent – involved in the manufacture, performance, broadcast and communication in order

to support and facilitate the creation of copyrighted works and other protected subject matter.• Non-dedicated support – duties are included in this group where part of the activities are related to

broadcast, communication, distribution and sales in protected subject matter and they are not includedin the core copyright industries.

Copyright industries comprise a substantial proportion of the Australian economyIn the most recent year for which data is available (2006/07), Australia’s copyright industries:• employed 837,507 people, which constituted 8.0% of the Australian workforce• generated economic value equal to 10.3% of gross domestic product ($97.7 billion)• generated $6.873 billion in exports, equal to 4.1% of total exports.

Australia’s copyright industries have grown considerably over the past 12 yearsOver the period 1995/96 to 2006/07 the real (i.e. inflation adjusted) compound annual growth rate (CAGR)for the copyright industries averaged 4.7%, with the core copyright industries growing 5.1% per year. This compares to a CAGR for gross domestic product (GDP) of 3.6% over the same period.

Productivity growth in Australia’s copyright industries has resulted in significant real wages growthSpurred by digitisation, the value generated in Australia’s copyright industries has increased in real termsover the period 1995/96 to 2006/07 from $85,512 to $116,742 per employee. As a result, the real averagewage for people employed in the copyright industries increased from $51,572 in 1995/96 to $61,355 in2006/07.

Australia remains a significant net importer of copyright goods and servicesWhile exports of copyright products has grown in real terms by 0.6% per year over the period 1995/96 to2006/07, imports have grown at 2.1%. In 2006/07 Australia had a trade deficit of just under $20.8 billionin the copyright industries.

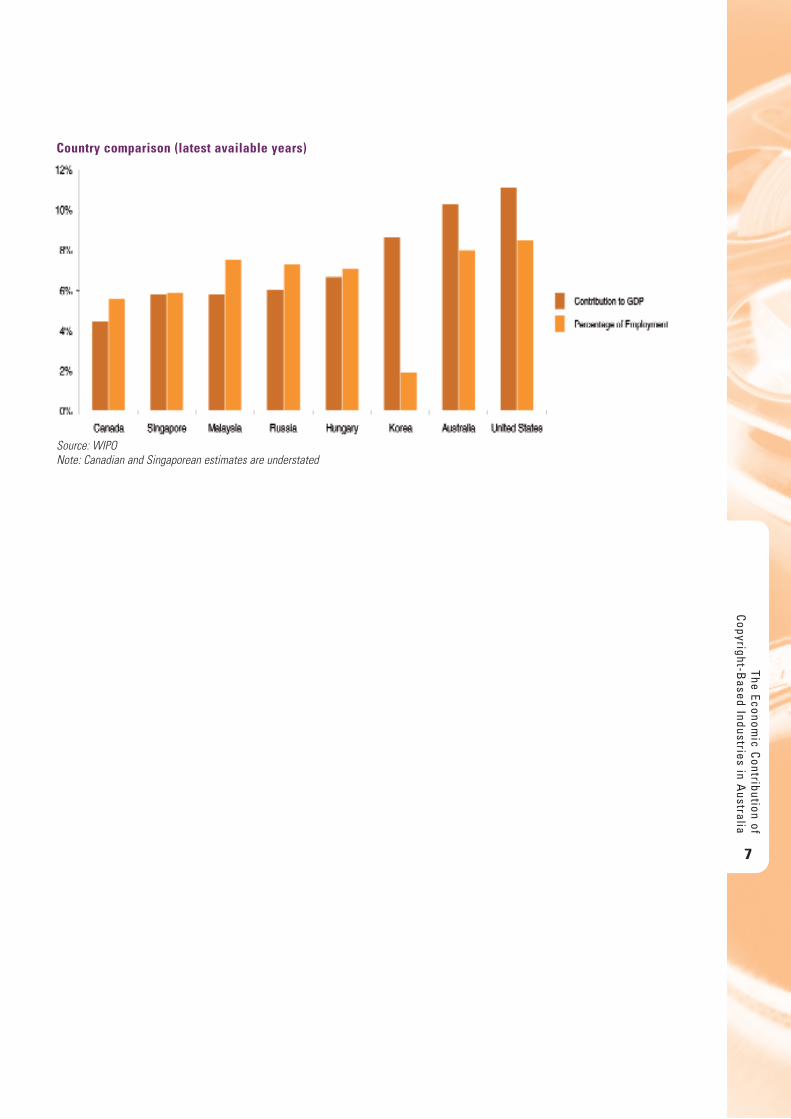

Australia’s economy has a relatively high dependence on copyright industriesIn comparison with other economies that have been analysed using the same WIPO framework as used inthis report, the Australian economy appears to have a greater copyright intensity than average in terms ofboth value added by, and employment in, the copyright industries.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

6

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

7

Country comparison (latest available years)

Source: WIPONote: Canadian and Singaporean estimates are understated

I n t r o d u c t i o n

Copyright was once viewed as a specialist branch of law focused primarily on the protection of artisticexpression and hence focused on the protection of artistic creations such as music, literature, paintings, and so on.

Such a narrow conception overlooked the fact that copyright was born as a result of the advent of the first technology for the production of copies of works (i.e. printing with movable type). The subsequentdevelopment of copyright has been shaped by ongoing technological developments and their associatedcommercial exploitation.

In the past decade interest in the economic impact of copyright has been driven by a number of inter-related factors:• The shift to a services economy — while Australia is commonly perceived as being an economy reliant

upon agriculture and resources, in fact it has evolved to one reliant on services. For example, theAustralian Services Roundtable (2008, p. 8) notes that, “In Australia, services account for 78 percent ofGDP and 60 percent of domestic investment. Services employ 8.5 of every 10 Australians, with all netjob growth over the past two decades taking place within the services sector.” Services industries aredisproportionately users and/or producers of copyright material and so the growth in services hasoccurred in conjunction with the growth of copyright industries.

• The mainstream adoption of the Internet, digital production and distribution — Australians haveembraced the use of the Internet, with usage increasing from 33.8% of the population in 2000 to74.3% in December 2007 (Internet World Stats 2008). This is significant, as use of information andcommunications technologies has significantly increased the scope of the subject matter for copyrightprotection, with the ongoing growth of Internet usage and digital delivery of copyright materialsdrawing copyright into the lives of all members of society.

• There is an increasing understanding of the value attached to intangible assets, including copyright —much of the value of the leading companies in the world today resides in their portfolio of intangibleassets. For example, PwC research in the United Kingdom shows that total intangible assets comprise,on average, some 80% of companies’ value (Hadjiloucas 2007). This has caused business to focus itsattention on copyright and intellectual property more greatly.

• Copyright, and intellectual property protection more generally, has been embedded as a mandatoryelement in international trade negotiations — this has resulted in both a standardised set of expectationsand an acknowledgement of the importance of trade in copyright products.

Consistent with this greater interest in better understanding the size and economic contribution of thoseindustries which rely, to varying degrees, on protections afforded by copyright law, this study uses a recentlypublished global framework (WIPO 2003) to better understand the economic contribution of Australia’scopyright industries.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

8

S t u d y m e t h o d o l o g y

A global framework

An important development since the last study of the economic contribution of Australia’s copyrightindustries (ACG 2001) has been the development of a standardised global framework by the WorldIntellectual Property Organization (WIPO) (WIPO 2003).

WIPO sought to develop a common framework so that the myriad of country-specific studies that had beenindependently prepared could be made more transparent methodologically, and the results more directlycomparable. As a result, WIPO endorsed:• a new framework for classifying particular industries as being within the ‘copyright industries’.

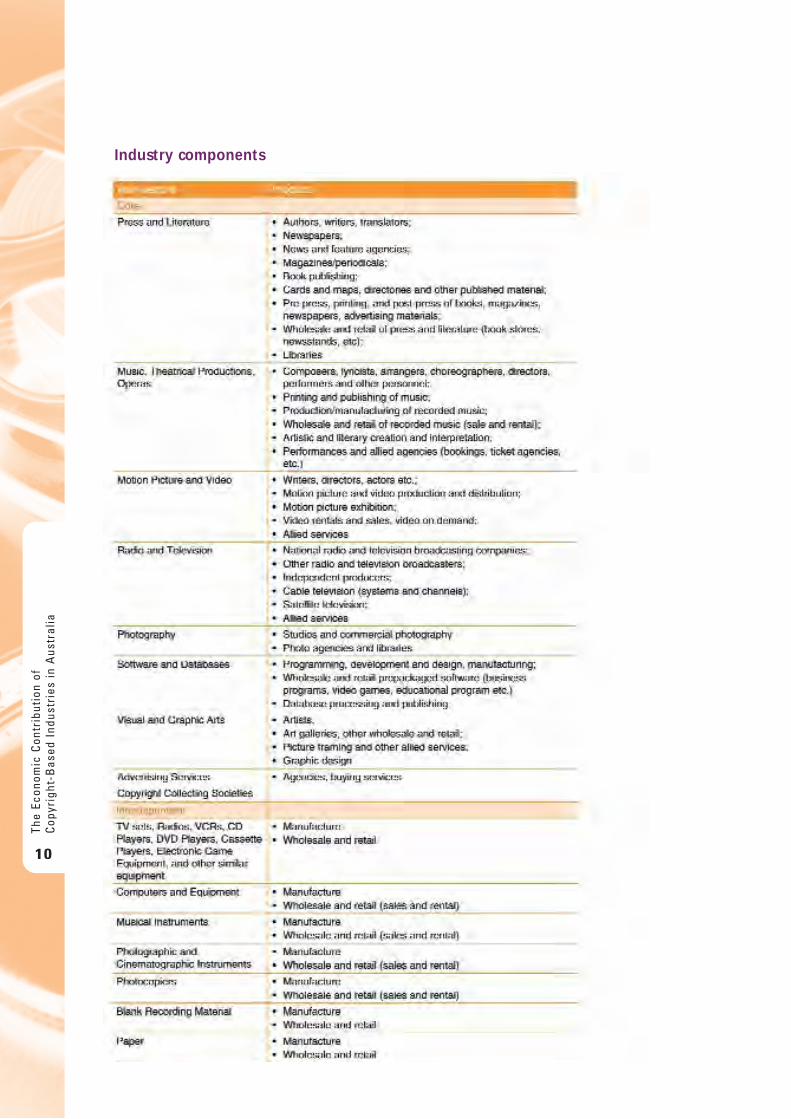

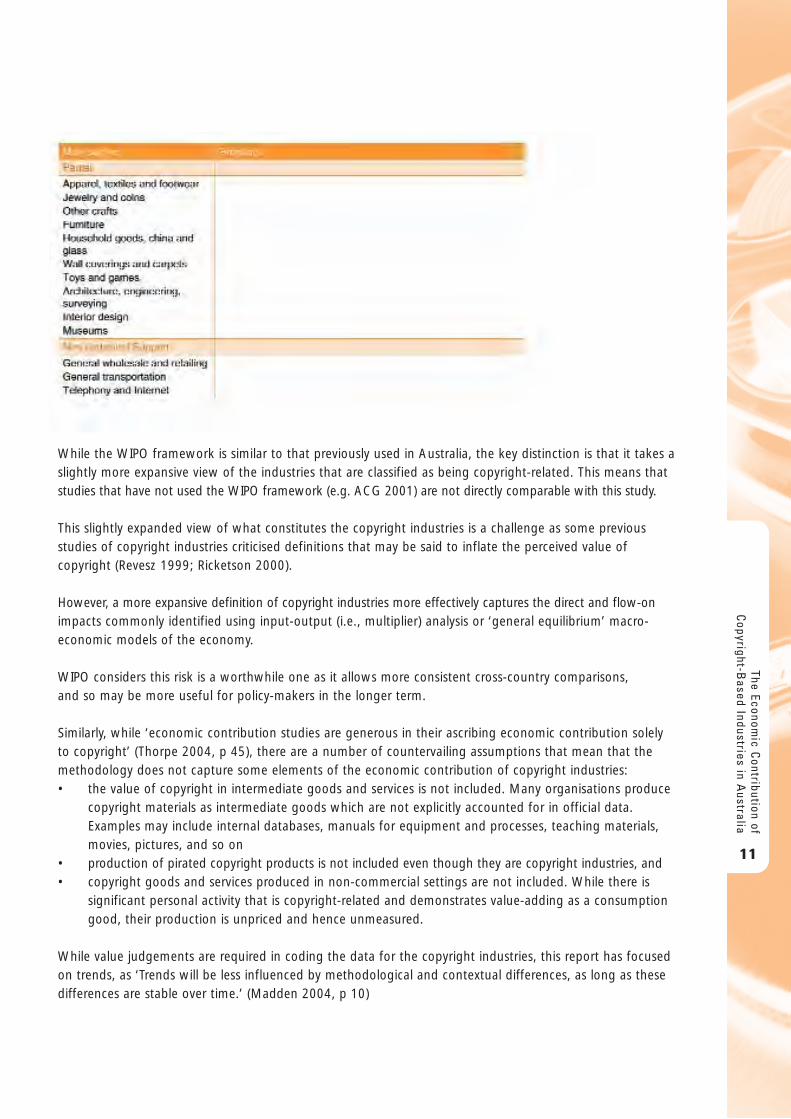

It grouped industries into four groups — core, partial, non-dedicated support, and interdependent —which, combined, form the ‘total’ copyright industries. The following table provides a summary of the classifications.

• generic set of performance indicators. Consistent with most previous studies, the suggested focus is on ‘value add’, trade in copyright products and employment.

The following table provides a brief description of the four copyright industry groups. The table on thefollowing page provides a greater level of detail of the specific sectors and products that comprise thecopyright industries.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

9

Industry components

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

10

While the WIPO framework is similar to that previously used in Australia, the key distinction is that it takes aslightly more expansive view of the industries that are classified as being copyright-related. This means thatstudies that have not used the WIPO framework (e.g. ACG 2001) are not directly comparable with this study.

This slightly expanded view of what constitutes the copyright industries is a challenge as some previousstudies of copyright industries criticised definitions that may be said to inflate the perceived value ofcopyright (Revesz 1999; Ricketson 2000).

However, a more expansive definition of copyright industries more effectively captures the direct and flow-onimpacts commonly identified using input-output (i.e., multiplier) analysis or ‘general equilibrium’ macro-economic models of the economy.

WIPO considers this risk is a worthwhile one as it allows more consistent cross-country comparisons, and so may be more useful for policy-makers in the longer term.

Similarly, while ‘economic contribution studies are generous in their ascribing economic contribution solelyto copyright’ (Thorpe 2004, p 45), there are a number of countervailing assumptions that mean that themethodology does not capture some elements of the economic contribution of copyright industries:• the value of copyright in intermediate goods and services is not included. Many organisations produce

copyright materials as intermediate goods which are not explicitly accounted for in official data.Examples may include internal databases, manuals for equipment and processes, teaching materials,movies, pictures, and so on

• production of pirated copyright products is not included even though they are copyright industries, and• copyright goods and services produced in non-commercial settings are not included. While there is

significant personal activity that is copyright-related and demonstrates value-adding as a consumptiongood, their production is unpriced and hence unmeasured.

While value judgements are required in coding the data for the copyright industries, this report has focusedon trends, as ‘Trends will be less influenced by methodological and contextual differences, as long as thesedifferences are stable over time.’ (Madden 2004, p 10)

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

11

It should also be remembered that, even though the focus of this report is upon quantification of thecopyright industries:

The true cultural value of copyright cannot be fully captured by measuring the value-added in thecultural industries however accurate those measures are because there are external benefits that arenot priced through the marketplace; the national culture, a creative environment and freedom ofexpression are examples of non-appropriable benefits. (Towse 2000, p 115)

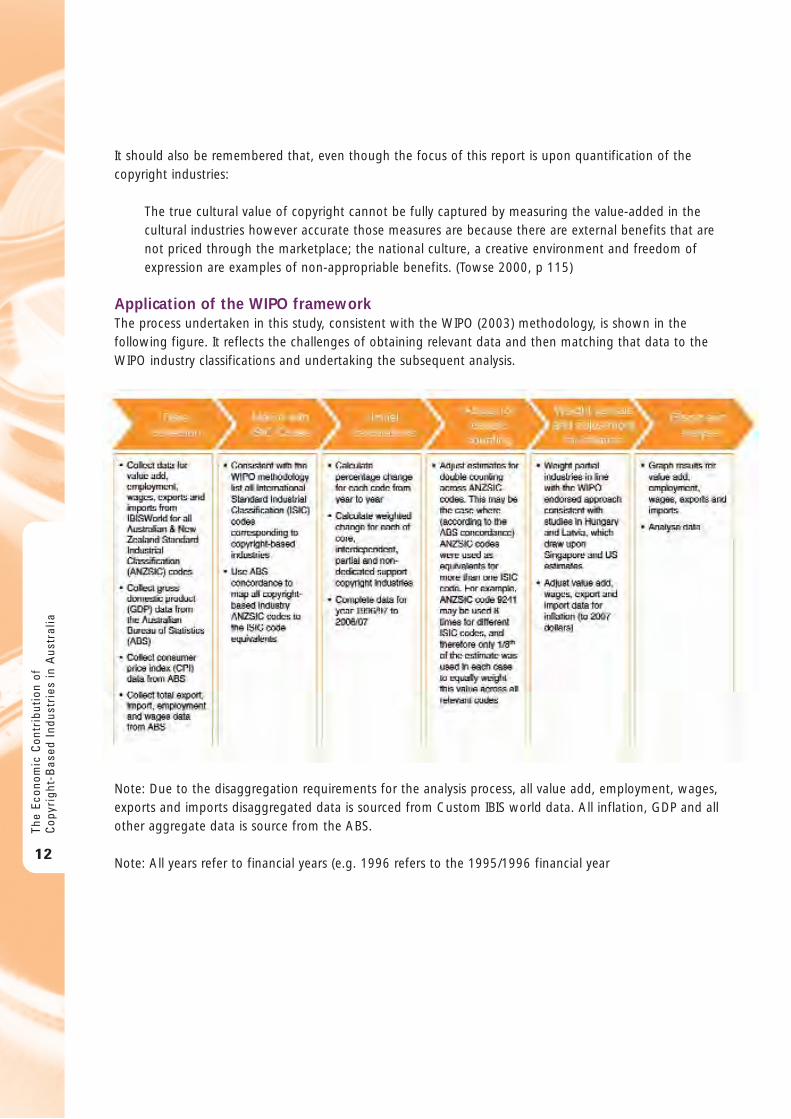

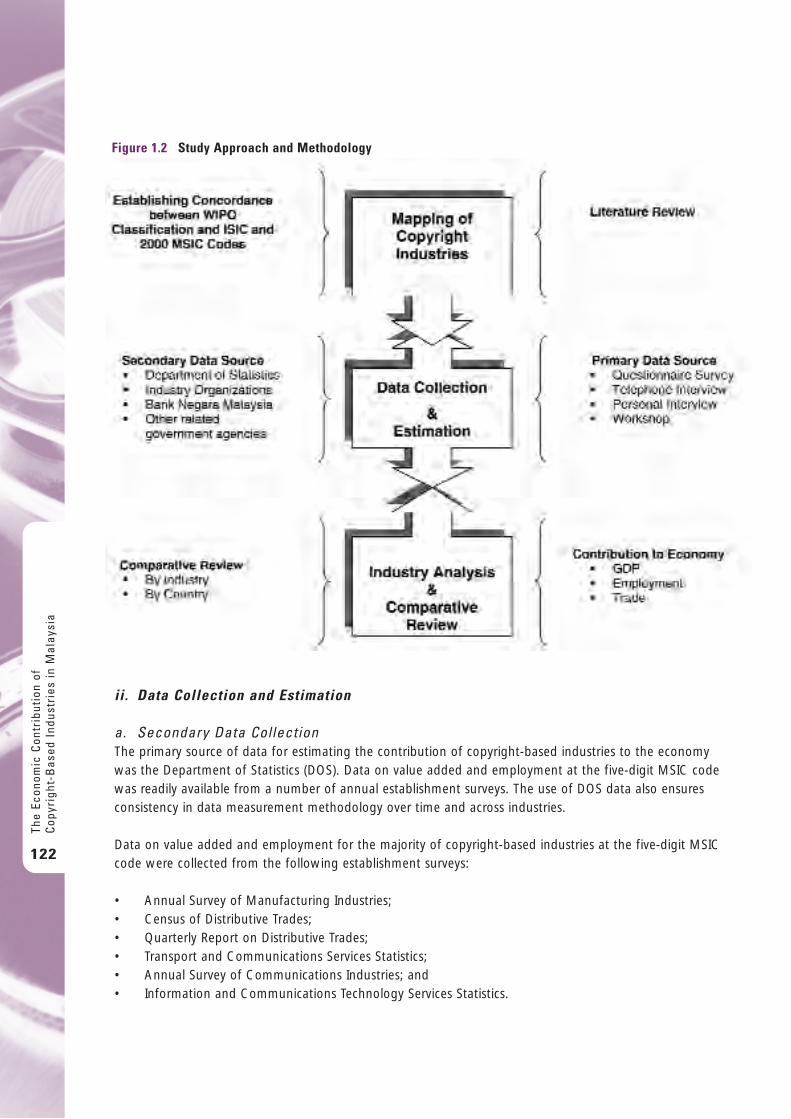

Application of the WIPO frameworkThe process undertaken in this study, consistent with the WIPO (2003) methodology, is shown in thefollowing figure. It reflects the challenges of obtaining relevant data and then matching that data to theWIPO industry classifications and undertaking the subsequent analysis.

Note: Due to the disaggregation requirements for the analysis process, all value add, employment, wages,exports and imports disaggregated data is sourced from Custom IBIS world data. All inflation, GDP and allother aggregate data is source from the ABS.

Note: All years refer to financial years (e.g. 1996 refers to the 1995/1996 financial year

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

12

1 . Va l u e a d d e d b y c o p y r i g h t i n d u s t r i e s

The key measure of an industry’s economic contribution is its ‘value add’. Value added is the value of grossoutputs of a particular industry less the value of inputs from other industries. The sum of all industries’ valueadd is the nation’s gross domestic product (GDP). Thus, looking at the value add of Australia’s copyrightindustries provides a measure of the relative importance of the copyright industries.

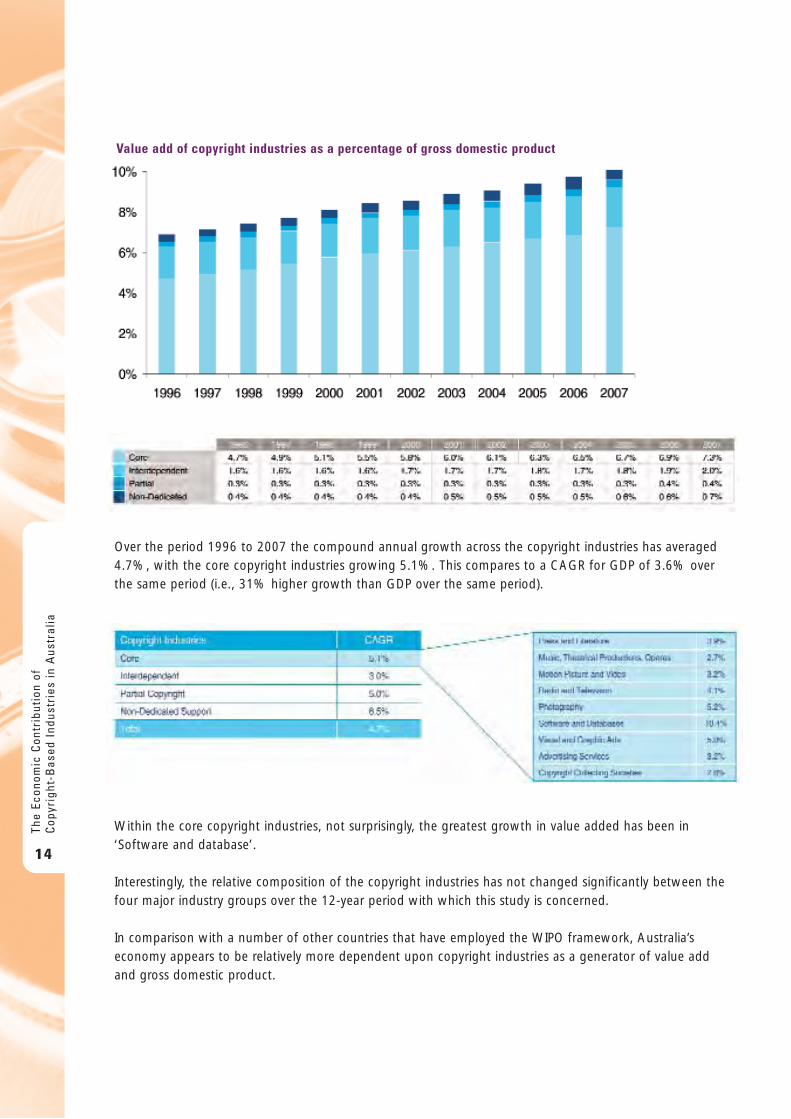

As shown in the figure below, there has been considerable growth in the value added by the copyrightindustries, increasing in real (i.e. inflation adjusted) terms from $58.9 billion in 1995/96 to $97.8 billion in 2006/07.

While the dollar value of copyright industries’ value add increased by about 66.0% over 12 years (seeprevious figure), the copyright industries’ contribution to gross domestic product increased by only 48.4%(see figure below). This relatively lower view of copyright industry growth reflects the real growth over thesame period in a number of major non-copyright industries (e.g., mining and resources).

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

13

Value add of copyright industries ($2007, $million)

Over the period 1996 to 2007 the compound annual growth across the copyright industries has averaged4.7%, with the core copyright industries growing 5.1%. This compares to a CAGR for GDP of 3.6% overthe same period (i.e., 31% higher growth than GDP over the same period).

Within the core copyright industries, not surprisingly, the greatest growth in value added has been in‘Software and database’.

Interestingly, the relative composition of the copyright industries has not changed significantly between thefour major industry groups over the 12-year period with which this study is concerned.

In comparison with a number of other countries that have employed the WIPO framework, Australia’seconomy appears to be relatively more dependent upon copyright industries as a generator of value addand gross domestic product.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

14

Value add of copyright industries as a percentage of gross domestic product

Real compounding annual growth rate (CAGR) of value add (2002 – 2007)

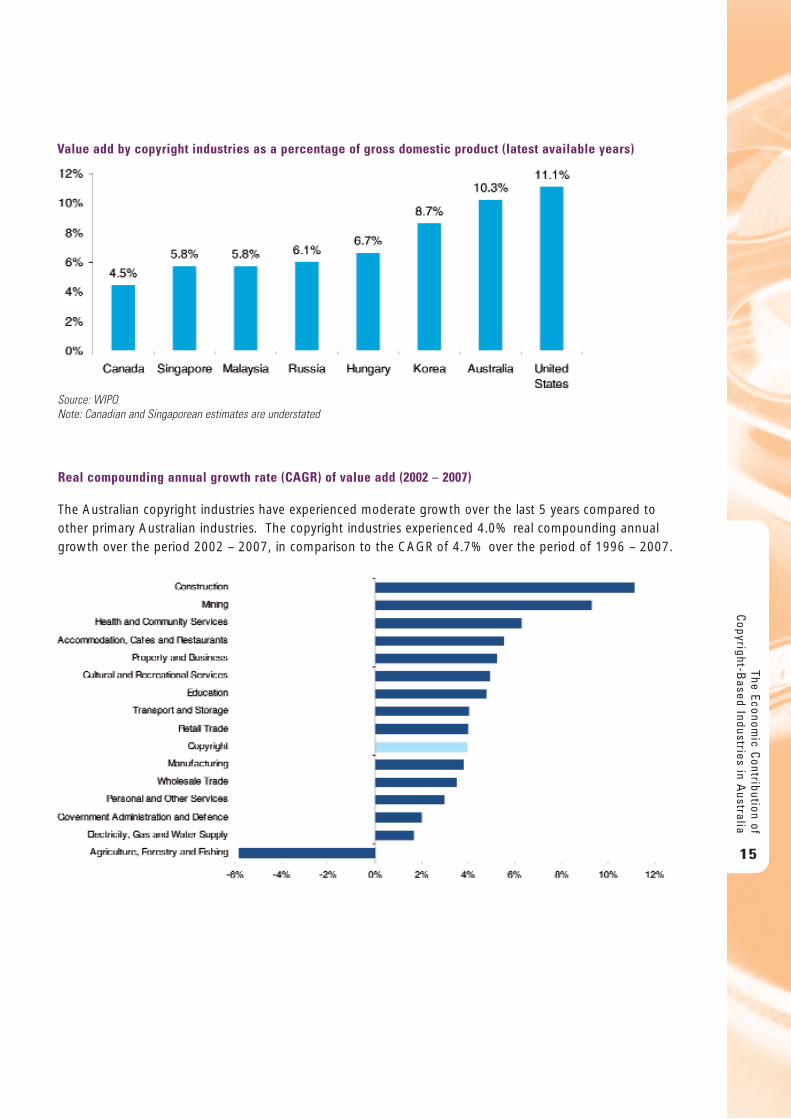

The Australian copyright industries have experienced moderate growth over the last 5 years compared toother primary Australian industries. The copyright industries experienced 4.0% real compounding annualgrowth over the period 2002 – 2007, in comparison to the CAGR of 4.7% over the period of 1996 – 2007.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

15

Value add by copyright industries as a percentage of gross domestic product (latest available years)

Source: WIPONote: Canadian and Singaporean estimates are understated

2 . E m p l o y m e n t i n c o p y r i g h t i n d u s t r i e s

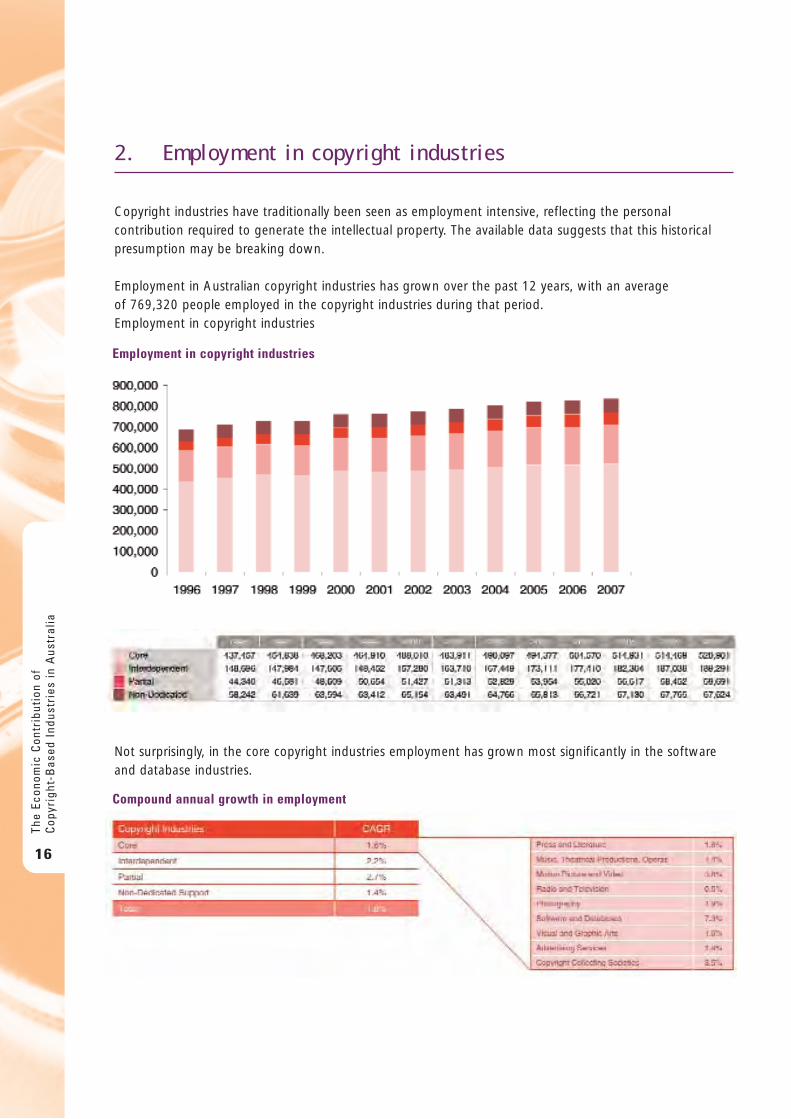

Copyright industries have traditionally been seen as employment intensive, reflecting the personalcontribution required to generate the intellectual property. The available data suggests that this historicalpresumption may be breaking down.

Employment in Australian copyright industries has grown over the past 12 years, with an average of 769,320 people employed in the copyright industries during that period.Employment in copyright industries

Not surprisingly, in the core copyright industries employment has grown most significantly in the softwareand database industries.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

16

Employment in copyright industries

Compound annual growth in employment

The relative distribution across the four copyright sectors has remained almost constant over the 12 years analysed.

While employment in the copyright industries has increased over time, as a percentage of the workforce thecopyright industries now employ a slightly lower percentage of the workforce (8.0% versus 8.3% in 1996).This reflects a combination of efficiencies in the copyright industries (largely due to digitisation) and strongemployment growth in non-copyright industries (such as mining and resources).

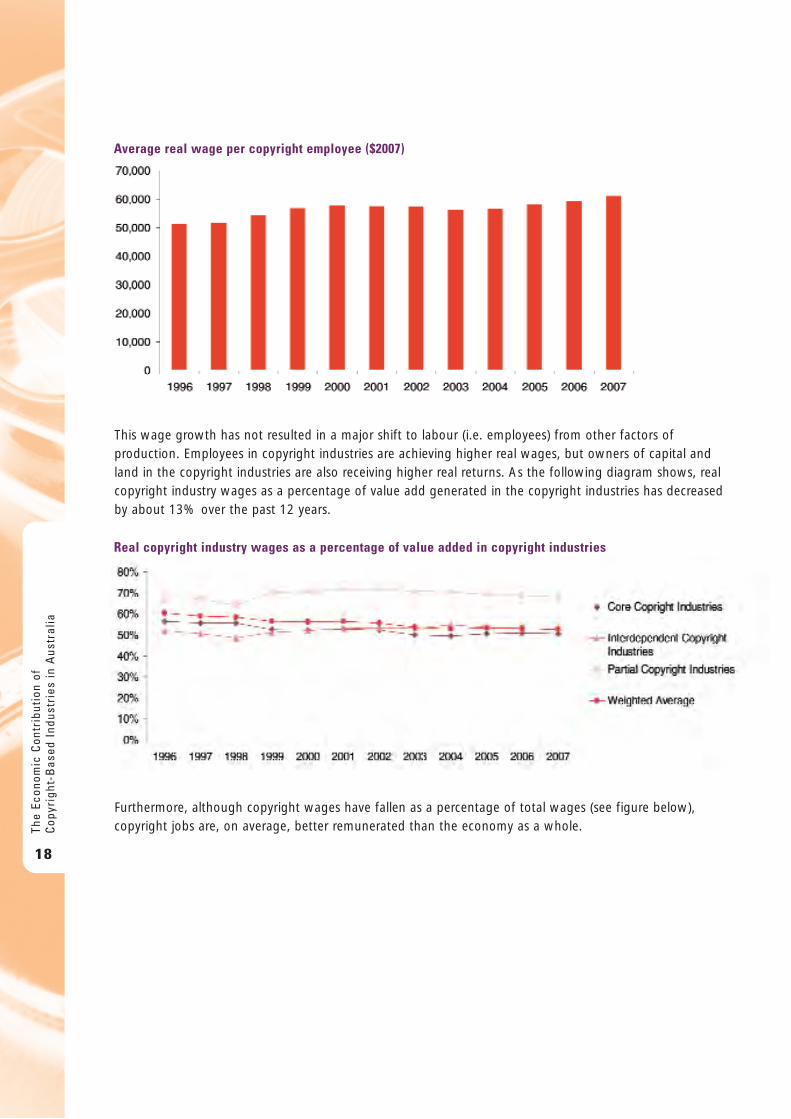

As the following table shows, real wages growth in Australia’s copyright industries has exceededemployment growth.

Indeed, the last 12 years have seen average wages in the copyright industries grow in real terms, from$51,572 in 1995/96 to $61,355 in 2006/07 per employee.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

17

Employment in copyright industries as a percentage of employed persons

This wage growth has not resulted in a major shift to labour (i.e. employees) from other factors ofproduction. Employees in copyright industries are achieving higher real wages, but owners of capital andland in the copyright industries are also receiving higher real returns. As the following diagram shows, realcopyright industry wages as a percentage of value add generated in the copyright industries has decreasedby about 13% over the past 12 years.

Furthermore, although copyright wages have fallen as a percentage of total wages (see figure below),copyright jobs are, on average, better remunerated than the economy as a whole.Th

e Ec

onom

ic C

ontr

ibut

ion

ofC

opyr

ight

-Bas

ed I

ndus

trie

s in

Aus

tral

ia

18

Average real wage per copyright employee ($2007)

Real copyright industry wages as a percentage of value added in copyright industries

The real increase in copyright wages reflects the labour productivity growth that has been evident in the copyright industries over the period 1995/96 to 2006/07.

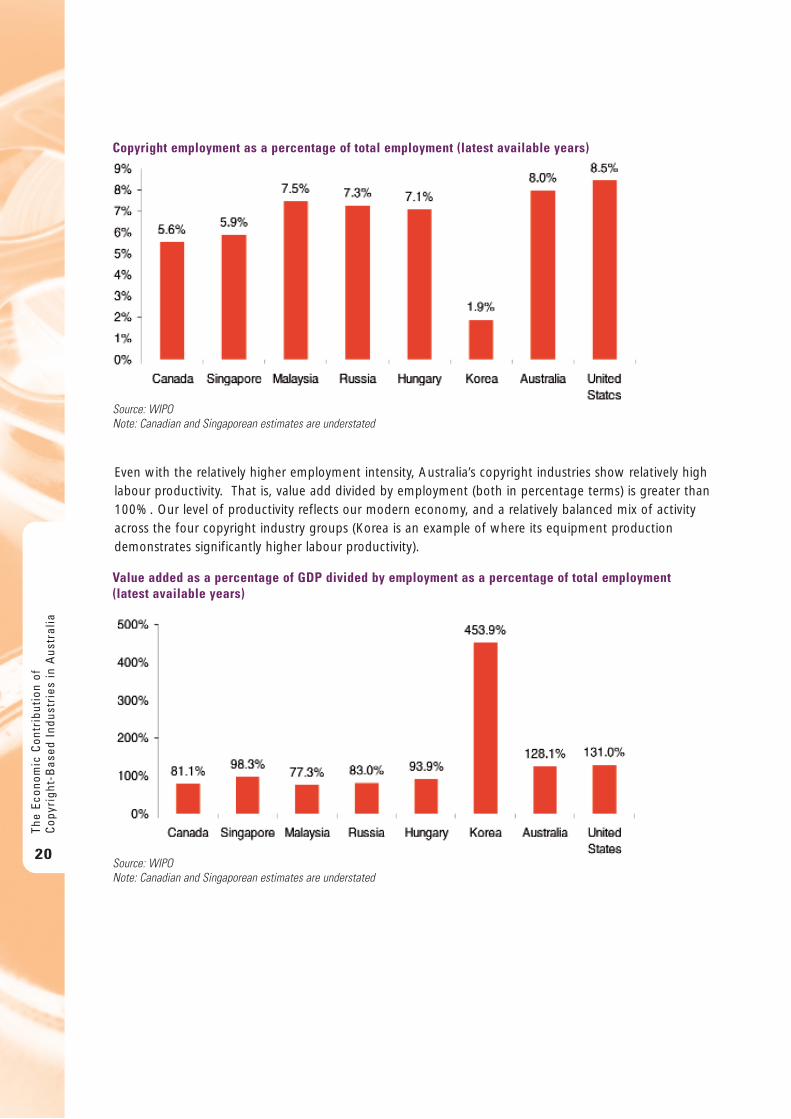

In comparison with a number of other country studies that have employed the WIPO framework (see figureimmediately below), Australia’s employment intensity appears stronger. That is, we have a higher percentageof the workforce employed in copyright industries.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

19

Copyright wages as a percentage of total wages

Real value add per employee ($2007)

Even with the relatively higher employment intensity, Australia’s copyright industries show relatively highlabour productivity. That is, value add divided by employment (both in percentage terms) is greater than100%. Our level of productivity reflects our modern economy, and a relatively balanced mix of activityacross the four copyright industry groups (Korea is an example of where its equipment productiondemonstrates significantly higher labour productivity).

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

20

Copyright employment as a percentage of total employment (latest available years)

Source: WIPONote: Canadian and Singaporean estimates are understated

Value added as a percentage of GDP divided by employment as a percentage of total employment (latest available years)

Source: WIPONote: Canadian and Singaporean estimates are understated

3 . Tr a d e i n c o p y r i g h t p r o d u c t s

It has always been understood that Australia is a net importer of copyright products. This reflects both our small size in the world economy and the fact we are an English speaking country, and hence drawsignificantly upon the cultural output of the United States and United Kingdom.

ImportsAs the following figure shows, Australian consumption of overseas copyright-related products has grownover the past 12 years, but not in an even pattern of growth. Imports grew and peaked in 2000/01, thenfell through to 2003/04, at which time import growth rose again.

Imports have grown across the three types of copyright industries. Within the core copyright industries mostgrowth has come in the software and database industry.

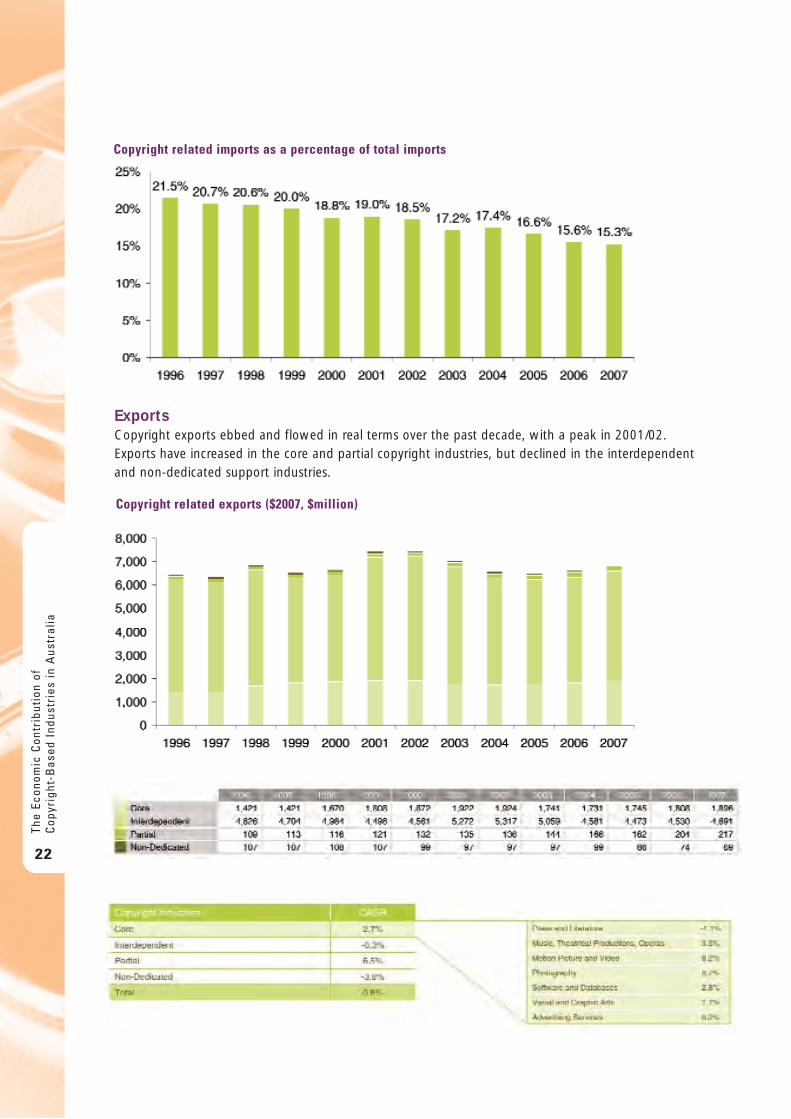

Copyright related imports, as a percentage of total imports, have fallen relatively consistently over the last12 years.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

21

Copyright related imports ($2007, $million)

ExportsCopyright exports ebbed and flowed in real terms over the past decade, with a peak in 2001/02.Exports have increased in the core and partial copyright industries, but declined in the interdependent and non-dedicated support industries.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

22

Copyright related imports as a percentage of total imports

Copyright related exports ($2007, $million)

Despite this growth in real exports in the last few years, copyright exports declined as a percentage of total exports. This relative performance is a reflection of the boom in the Australian resources sector.

The net position

Taking both exports and imports into account, the figure below shows Australia’s net trade in copyright products.

The Economic C

ontribution ofC

opyright-Based Industries in A

ustralia

23

Copyright related exports as a percentage of total exports

Copyright related net imports ($2007, $million)

S o u r c e s

ABS (Australian Bureau of Statistics) 2008, 13500DO001 200804 - Australian Economic Indicators, Apr 2008

ABS, Labour Force Survey (All applicable years)

ABS 2007, 5439.0 - International Merchandise Imports, Australia, Jun 2007

ABS 2007, 5206.0 - Australian National Accounts: National Income, Expenditure and Product

ABS 1993, 1292.0 - Australian and New Zealand Standard Industrial Classification (ANZSIC)

ACG (Allen Consulting Group) 2001, The Economic Contribution of Australia’s Copyright Industries, Sydney

Australian Services Roundtable 2008, Securing Australia’s Place in the Global Services Economy: Submissionto the Mortimer Review - Export Policies and Programs, Canberra, July

Tony Hadjiloucas (Director, PwC Valuation & Strategy, London) 2007, ‘The increasing importance ofintangibles in industry’, speech presented in Buenos Aires, October

IBISWorld 2008, Custom Data

Internet World Stats 2008, Australia, available at http://www.internetworldstats.com/sp/au.htm

Christopher Madden 2004, Making Cross-country Comparisons of Cultural Statistics: Problems and Solutions- International Comparisons of Cultural Sectors: An Exploratory Investigation, Working Paper 2, AustraliaCouncil for the Arts, Sydney, October

PricewaterhouseCoopers 2007, Exploiting Intellectual Property in a Complex World, Technology ExecutiveConnections, Vol. 4., available athttp://www.pwc.com/extweb/pwcpublications.nsf/docid/F5DBAFA7B3F4501D852570830007AD84/$File/tecv4ip.pdf

John Revesz, 1999, ‘Trade-Related Aspects of Intellectual Property Rights’, Staff Research Paper, ProductivityCommission, Canberra

Sam Ricketson 2000, Intellectual Property Administration and Policy in Australia: An Examination of theAustralian Situation, Past and Present, and Recommendations for Future Change, Monash University,Melbourne

Jeremy Thorpe 2004, ‘Some challenges for copyright-related quantification’, Review of Economic Researchon Copyright Issues, Vol 1, No 1, pp 41-50

Ruth Towse 2000, ‘Cultural economics, copyright and the cultural industries’ Society and Economy inCentral and Eastern Europe, Vol 22, No 4, pp 107-126

WIPO (World Intellectual Property Organisation) 2003, Guide on Surveying the Economic Contribution of theCopyright-Based Industries, Geneva

WIPO 2006, National Studies on Assessing the Economic Contribution of the Copyright based Industries,Creative Industries Series No. 1, Geneva

WIPO 2008, National Studies on Assessing the Economic Contribution of the Copyright based Industries,Creative Industries Series No. 2, Geneva

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in A

ustr

alia

24

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

25

The Economic Contribution of Copyright-Based Industries

in Kenya

Dickson Nyariki1

Oliver WasongaCalleb OtienoEric OgadhoCharles IkutwaJulius Kithinji March 20091 The main author is an Associate Professor and teaches economics at the University of Nairobi; P.O. Box 29053-00625, Nairobi; emailaddress [email protected], [email protected]

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

26

Ta b l e o f C o n t e n t s

Acknowledgements 31

Summary 32

1. INTRODUCTION 351.1 Background and Context 351.2 Objectives and Structure of the Study 361.3 Scope of Study 37

2. COPYRIGHT POLICY AND LAW IN KENYA 382.1 Policies Related to Creative and Copyright Industries 382.2 Copyright Law 38

2.2.1 The Subject Matter and Beneficiaries of Copyright Law 382.2.2 Overview of the Kenyan Copyright Law 392.2.3 Economic Considerations of the Kenyan Copyright Law 40

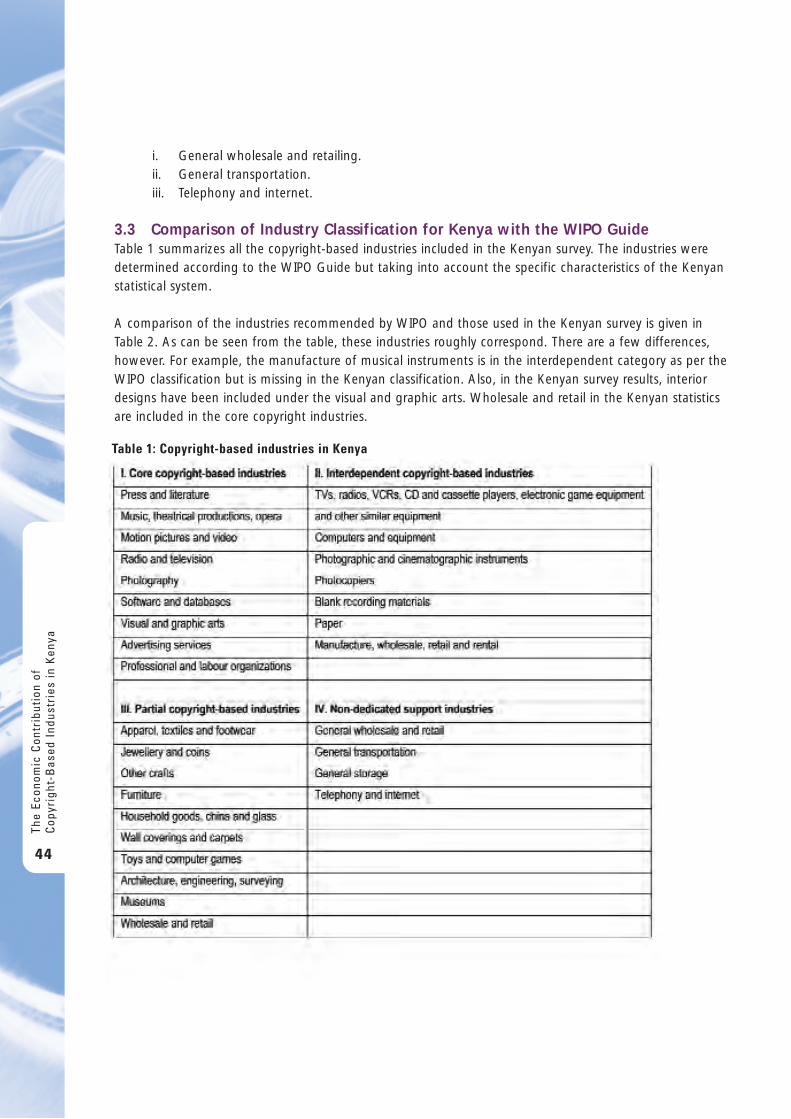

3. COPYRIGHT-BASED INDUSTRIES IN KENYA 423.1 Composition of Copyright-Based Industries 423.2 Types of Copyright-Based Industries 42

3.2.1 Core Copyright-Based Industries 423.2.2 Interdependent Copyright-Based Industries 433.2.3 Partial Copyright-Based Industries 433.2.4 Non-Dedicated Support Industries 43

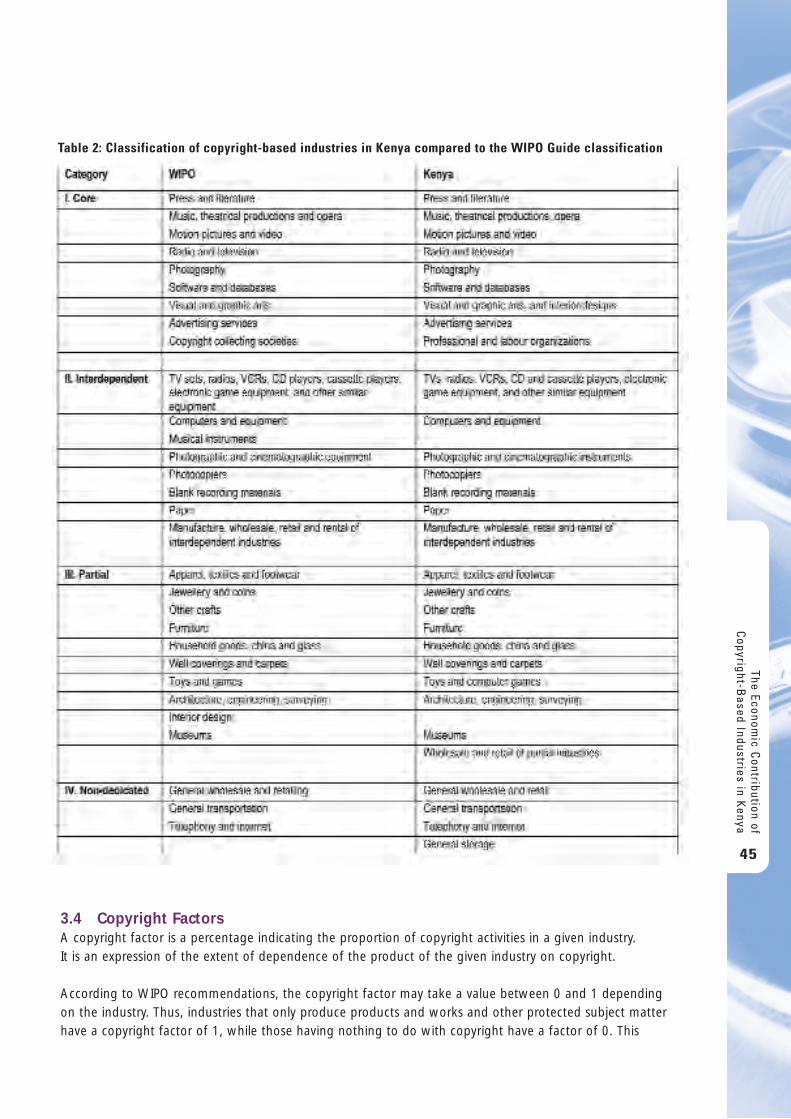

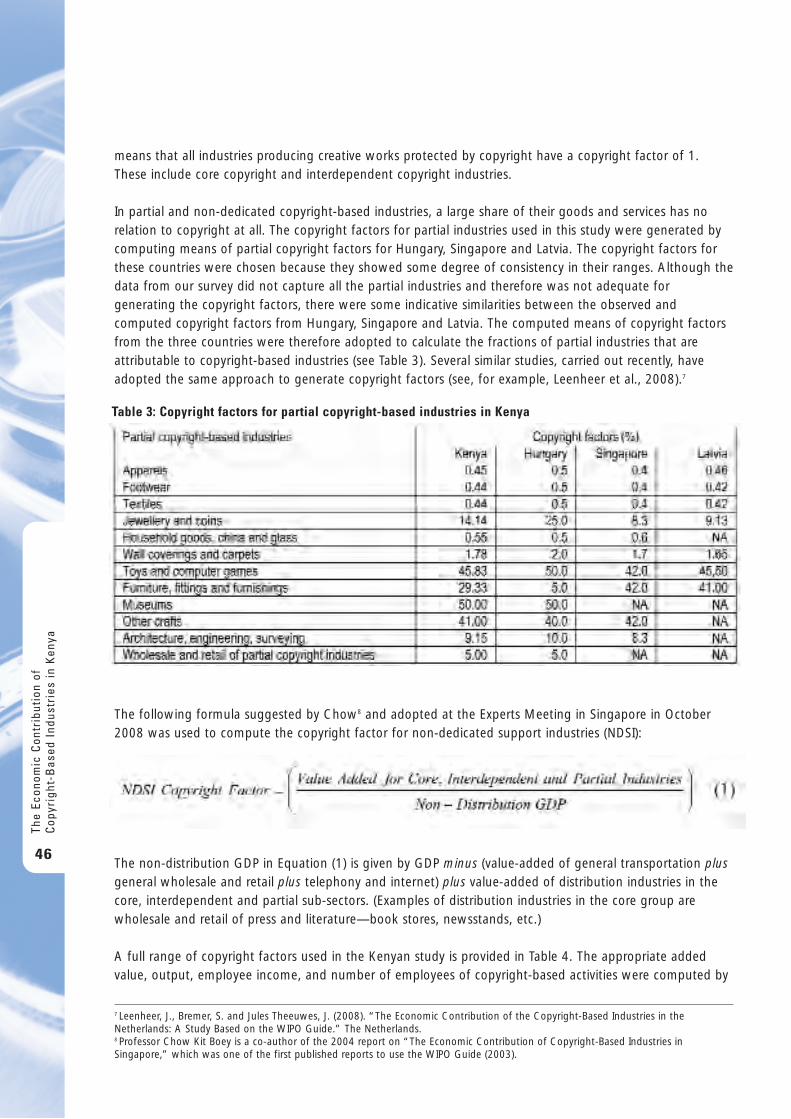

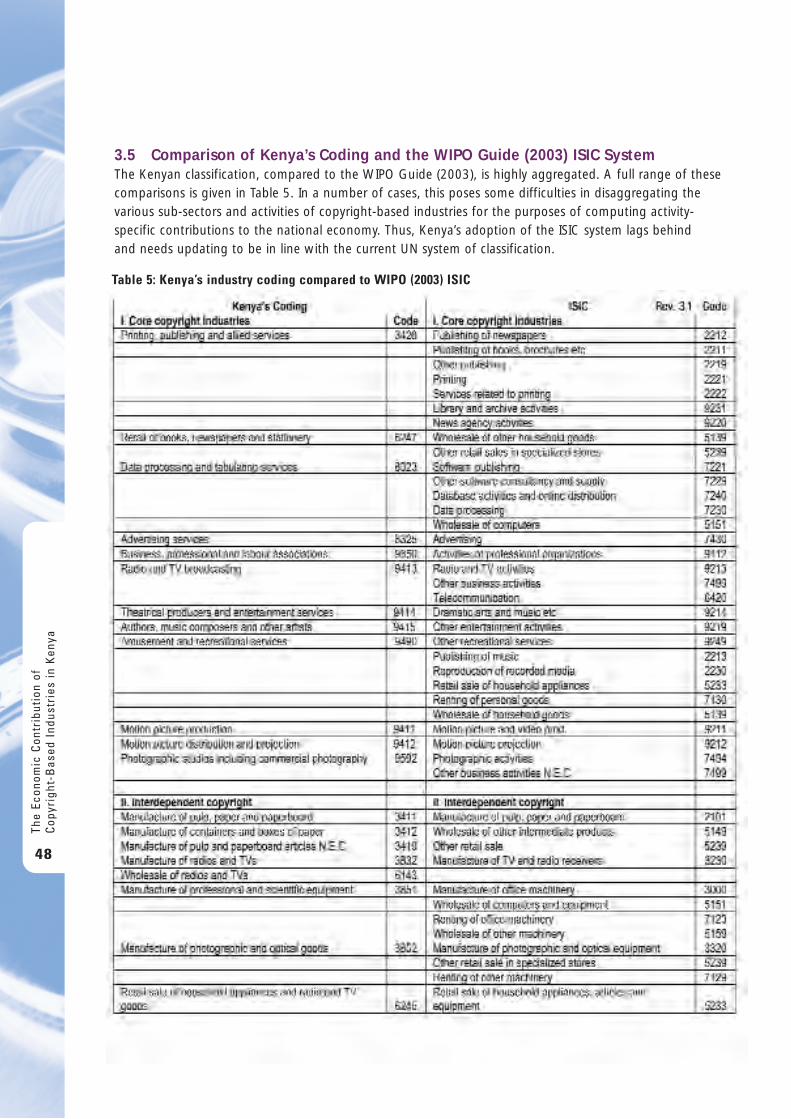

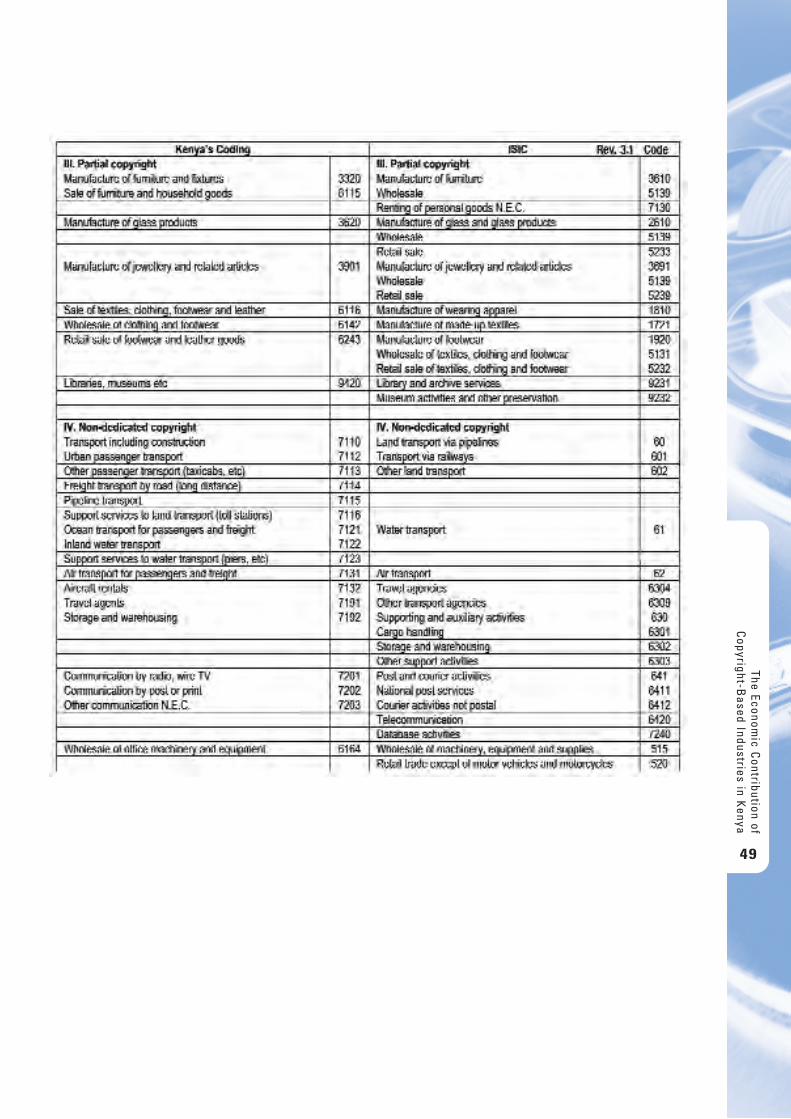

3.3 Comparison of Industry Classification for Kenya with the WIPO Guide 443.4 Copyright Factors 453.5 Comparison of Kenya’s Coding and the WIPO Guide (2003) ISIC System 48

4. DATA COLLECTION AND METHODS OF ANALYSIS 504.1 Sources of Information 504.2 Methodology 50

4.2.1 Data Collection 504.2.2 Dealing with Missing Data 504.2.3 Calculation of Indicators of Economic Contribution 51

4.3 Survey Challenges 52

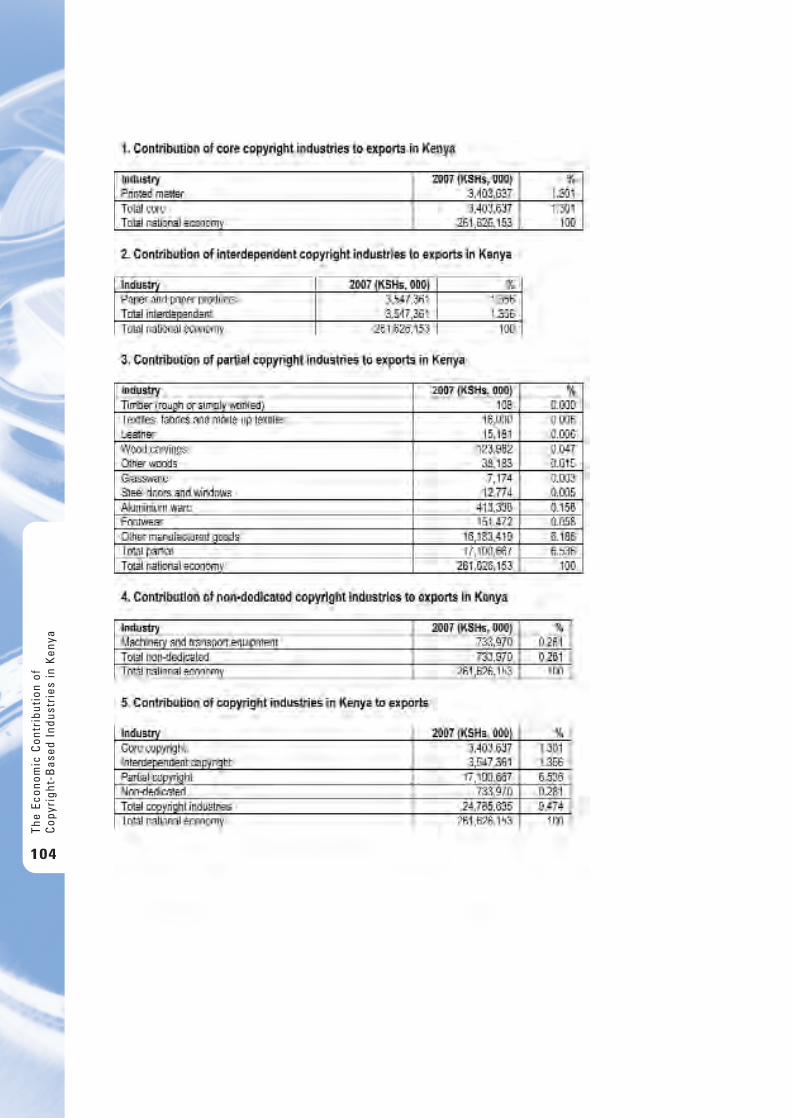

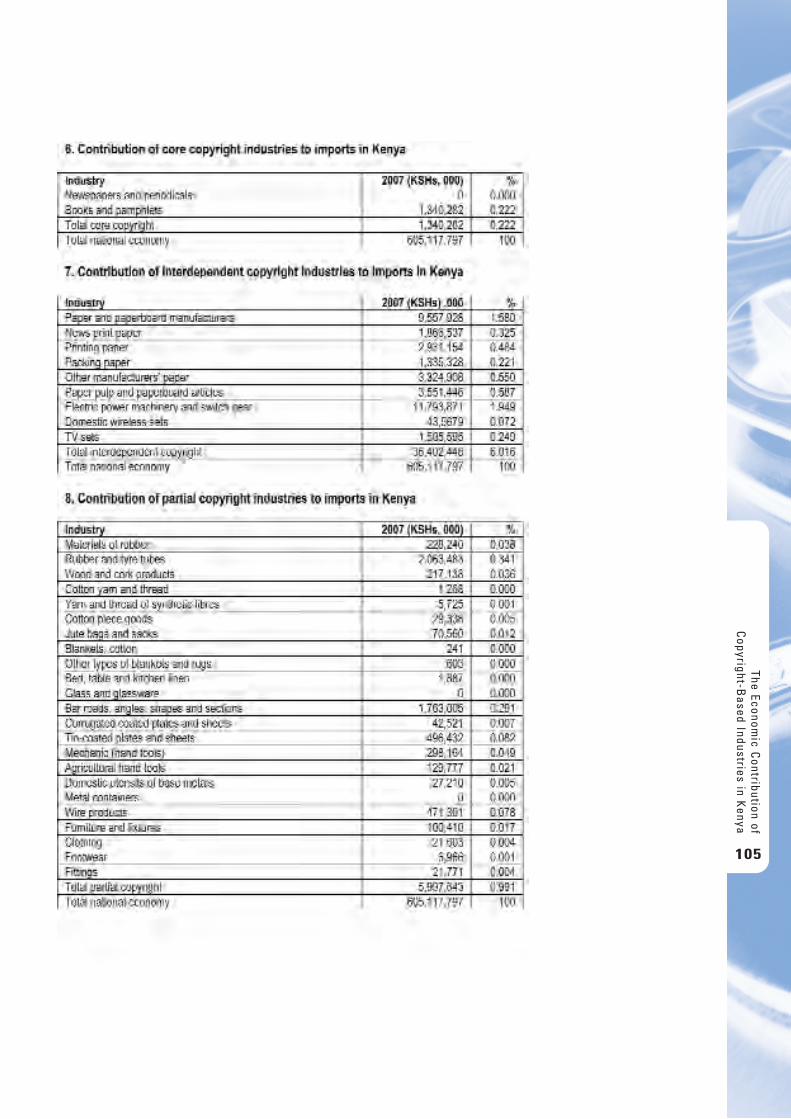

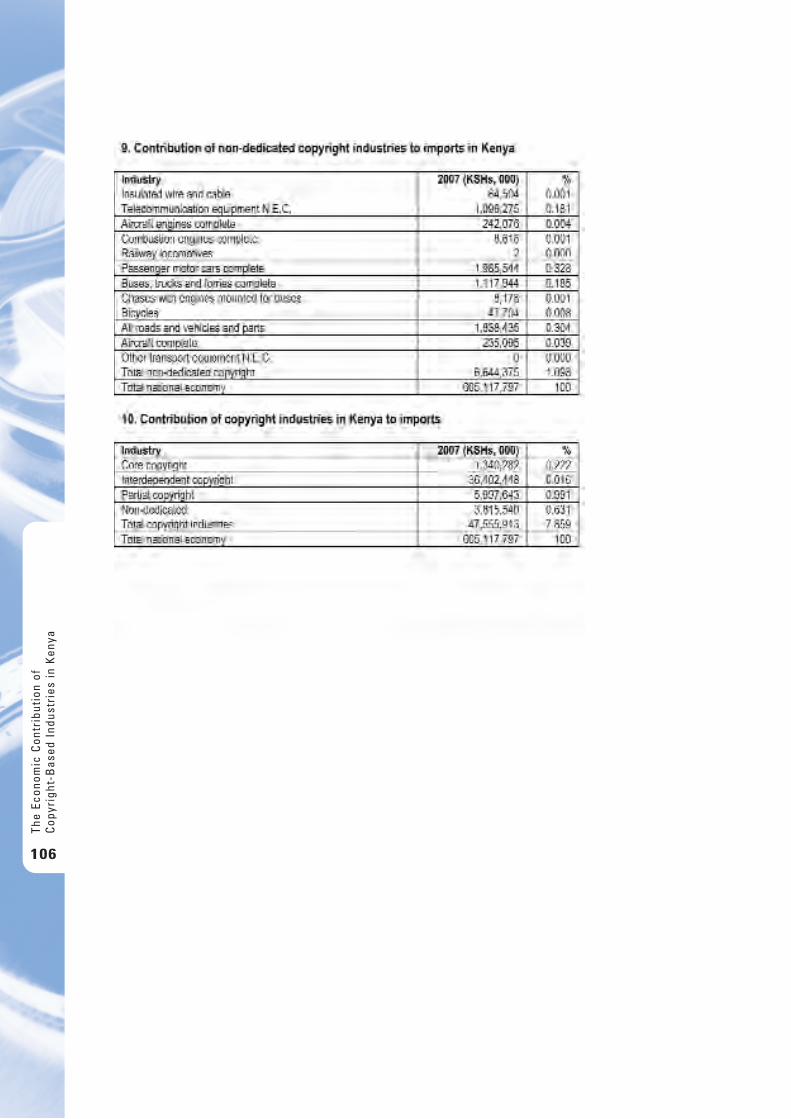

5. ECONOMIC CONTRIBUTION OF COPYRIGHT-BASED INDUSTRIES IN KENYA IN 2007 545.1 Overall Performance of Copyright-Based Industries 545.2 Economic Contribution of Copyright-Based Industries Compared to Other Sectors 585.3 Economic Contribution of Decomposed Core Copyright-Based Industries 615.4 Economic Contribution of Interdependent Copyright-Based Industries 665.5 Economic Contribution of Partial Copyright-Based Industries 705.6 Economic Contribution of Non-Dedicated Support Industries 735.7 Foreign Trade in Copyright-Based Goods and Services 755.8 International Comparisons 78

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

27

6. THE DEVELOPMENT OF SOME CORE COPYRIGHT-BASED INDUSTRIES IN KENYA 816.1 Press and Literature 81

6.1.1 The Press Market 816.1.2 The Book Market 84

6.2 Music, Theatrical Productions and Opera 846.2.1 The Music Industry 84

6.2.2 Theatres 866.3 Film Production and Video 866.4 Radio and Television 876.5 Collective Management Societies 896.6 Institutions set up to safeguard the interests of their members 91

7. CONCLUSIONS AND RECOMMENDATIONS 92

APPENDIX 94

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

28

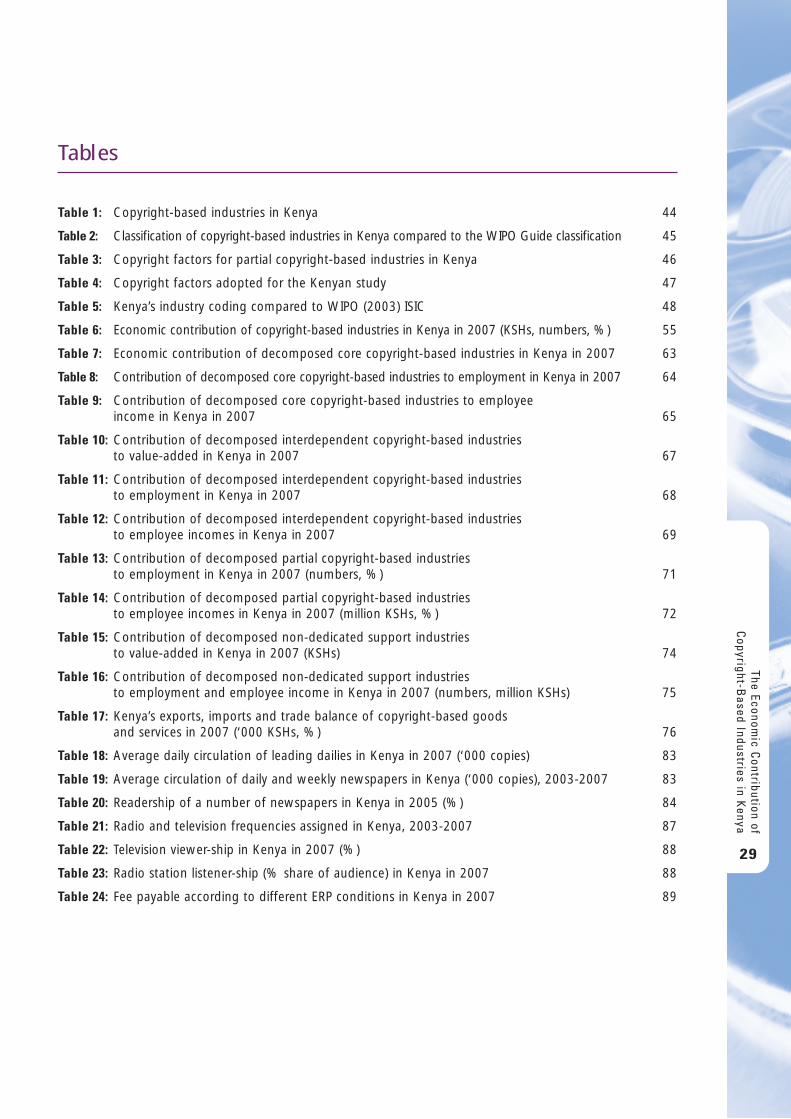

Ta b l e s

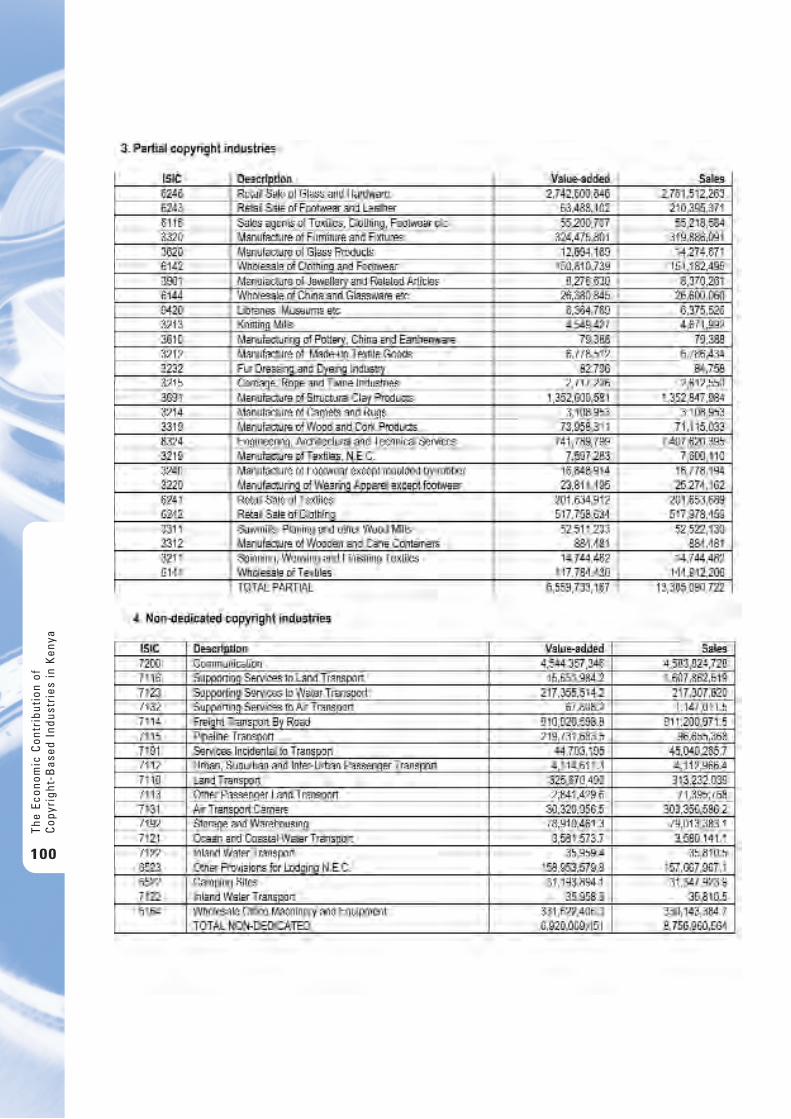

Table 1: Copyright-based industries in Kenya 44

Table 2: Classification of copyright-based industries in Kenya compared to the WIPO Guide classification 45

Table 3: Copyright factors for partial copyright-based industries in Kenya 46

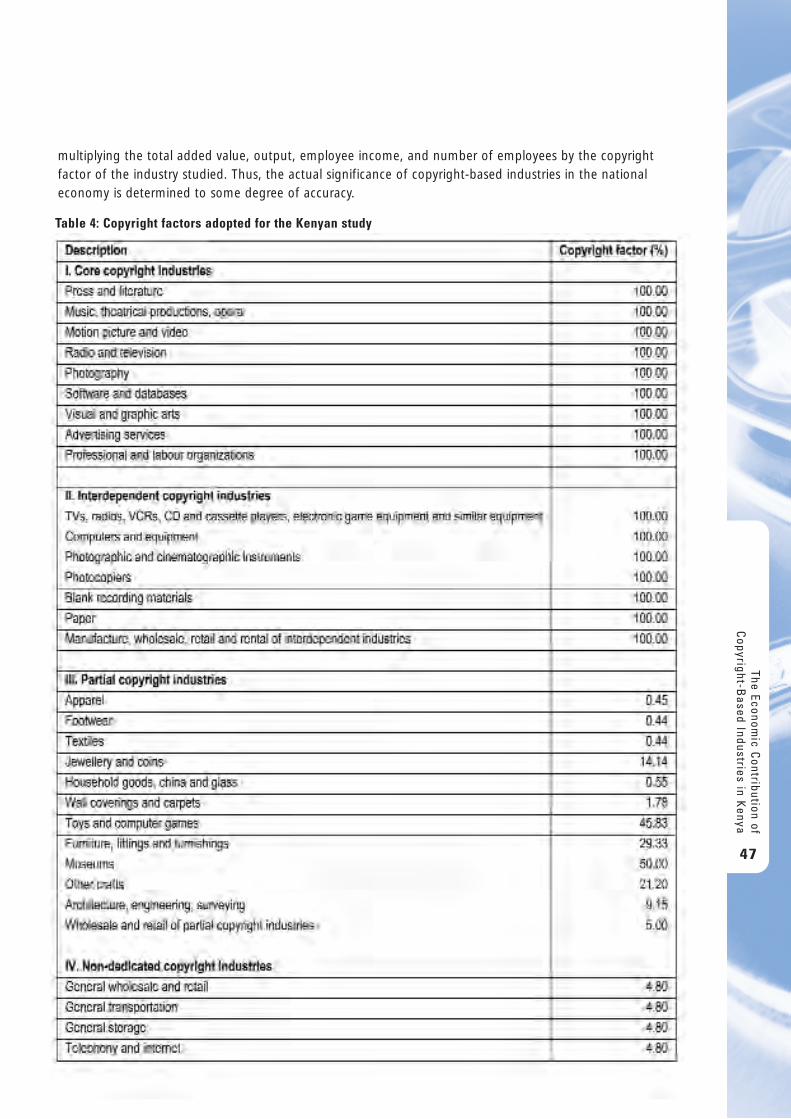

Table 4: Copyright factors adopted for the Kenyan study 47

Table 5: Kenya’s industry coding compared to WIPO (2003) ISIC 48

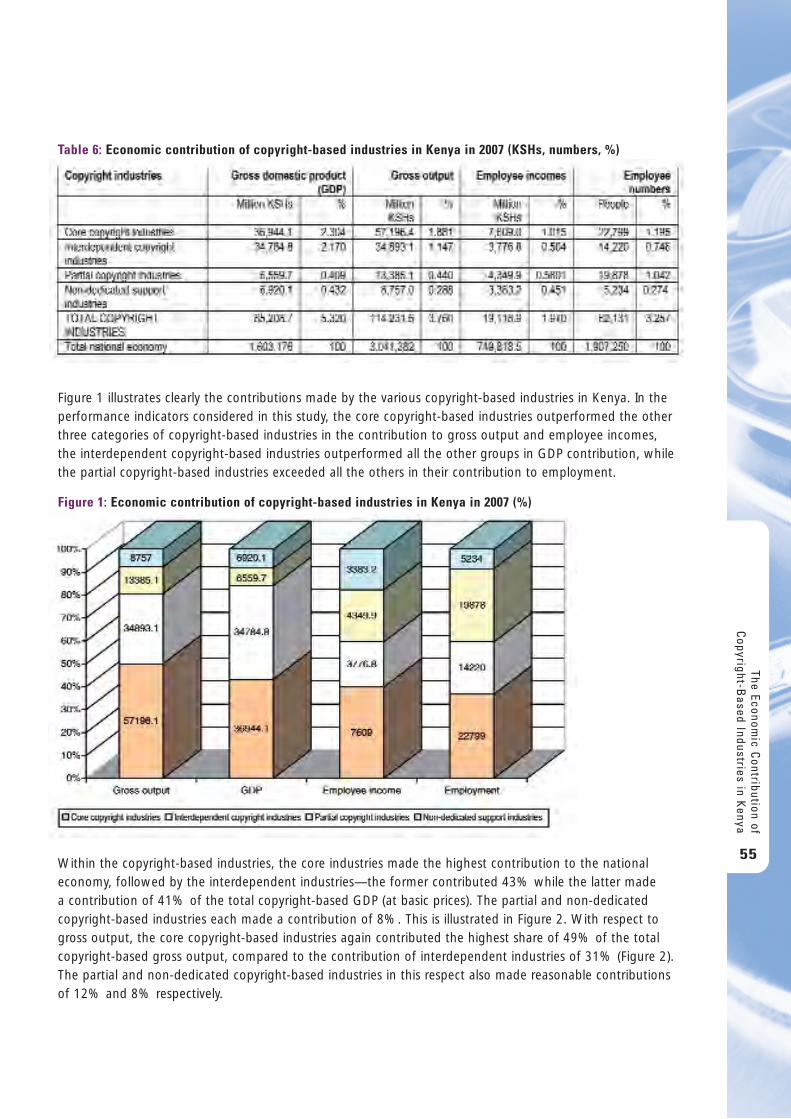

Table 6: Economic contribution of copyright-based industries in Kenya in 2007 (KSHs, numbers, %) 55

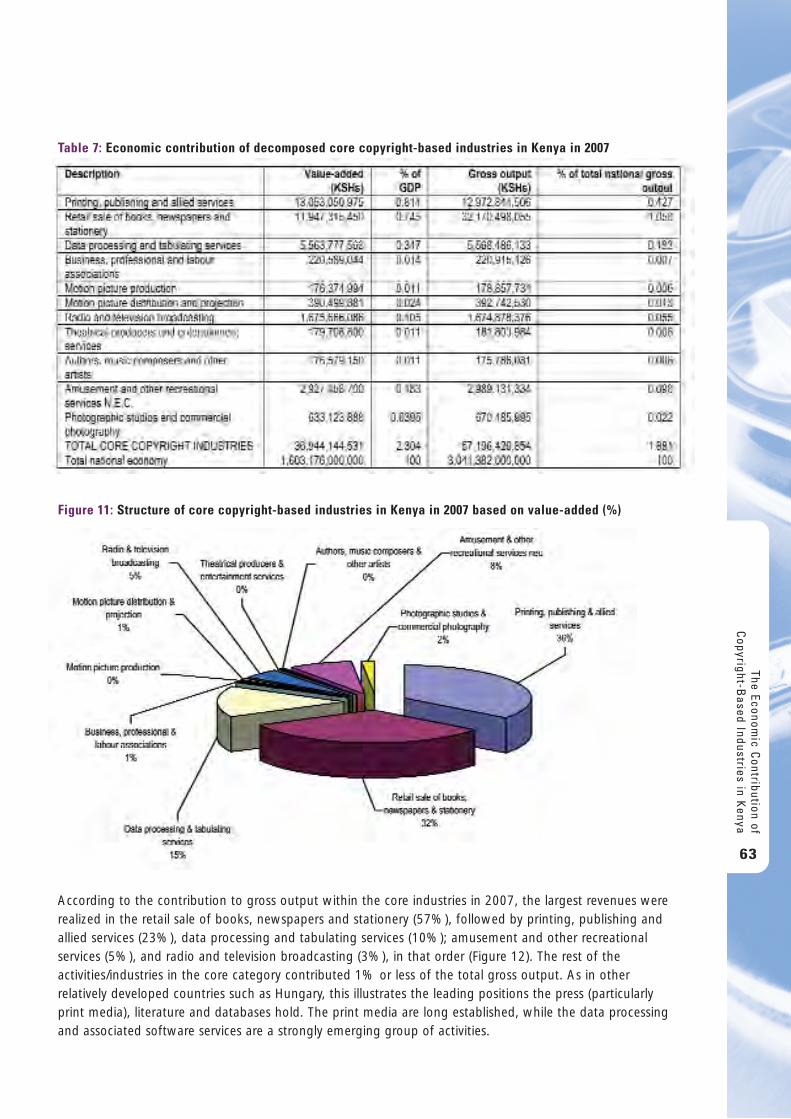

Table 7: Economic contribution of decomposed core copyright-based industries in Kenya in 2007 63

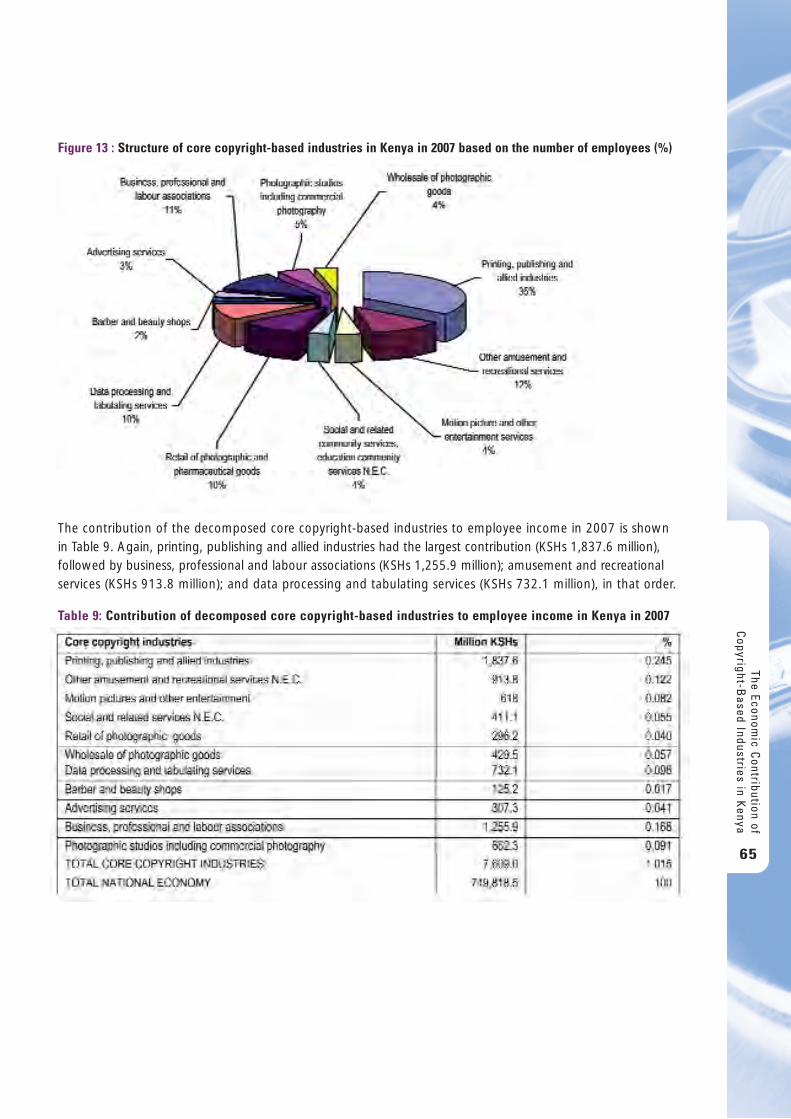

Table 8: Contribution of decomposed core copyright-based industries to employment in Kenya in 2007 64

Table 9: Contribution of decomposed core copyright-based industries to employeeincome in Kenya in 2007 65

Table 10: Contribution of decomposed interdependent copyright-based industriesto value-added in Kenya in 2007 67

Table 11: Contribution of decomposed interdependent copyright-based industriesto employment in Kenya in 2007 68

Table 12: Contribution of decomposed interdependent copyright-based industriesto employee incomes in Kenya in 2007 69

Table 13: Contribution of decomposed partial copyright-based industriesto employment in Kenya in 2007 (numbers, %) 71

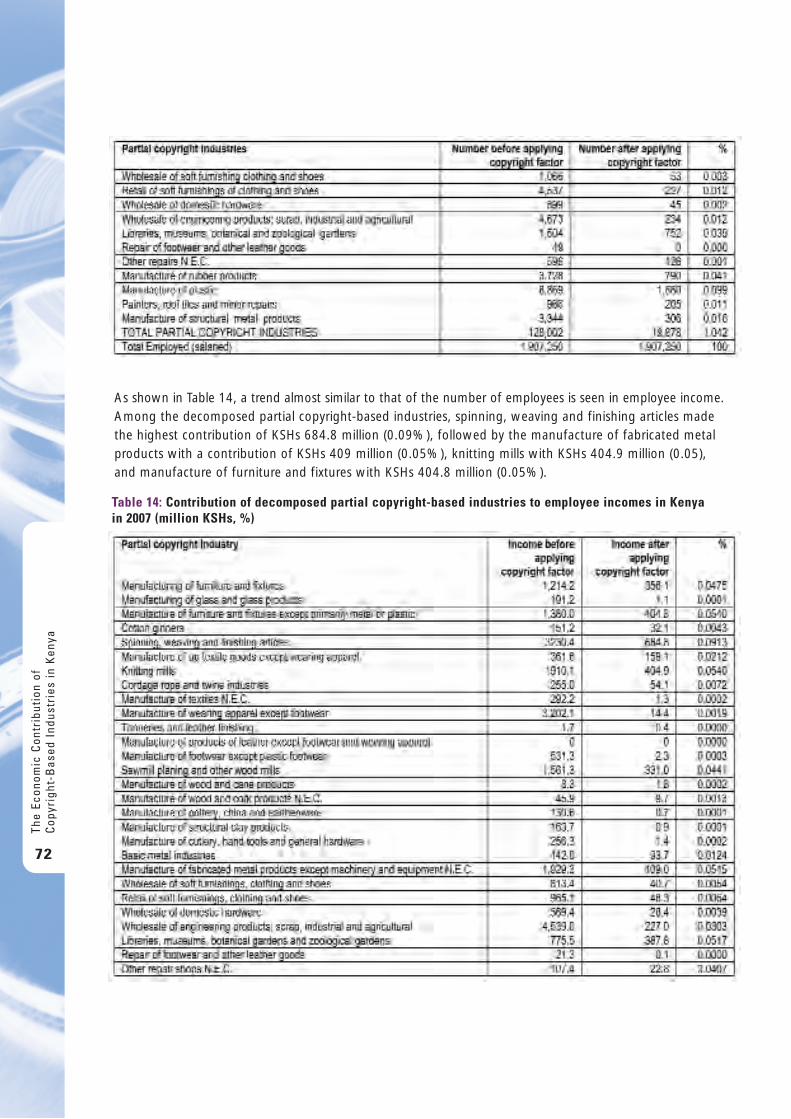

Table 14: Contribution of decomposed partial copyright-based industriesto employee incomes in Kenya in 2007 (million KSHs, %) 72

Table 15: Contribution of decomposed non-dedicated support industriesto value-added in Kenya in 2007 (KSHs) 74

Table 16: Contribution of decomposed non-dedicated support industriesto employment and employee income in Kenya in 2007 (numbers, million KSHs) 75

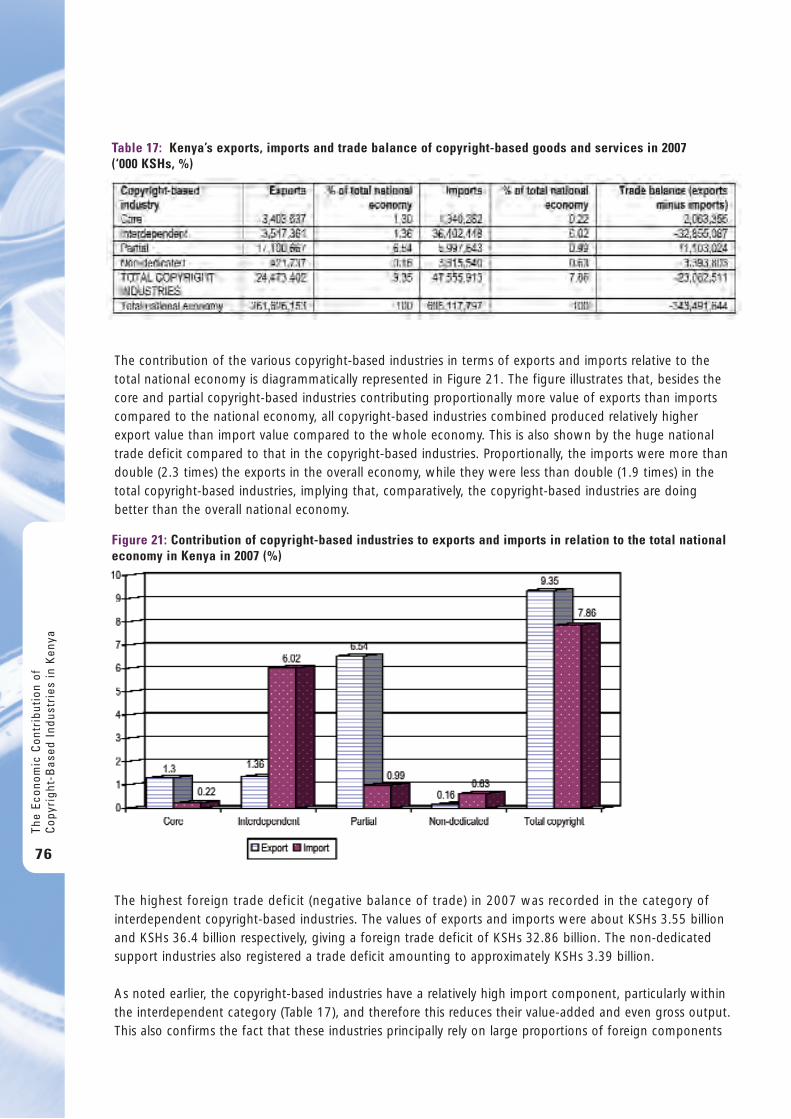

Table 17: Kenya’s exports, imports and trade balance of copyright-based goodsand services in 2007 (‘000 KSHs, %) 76

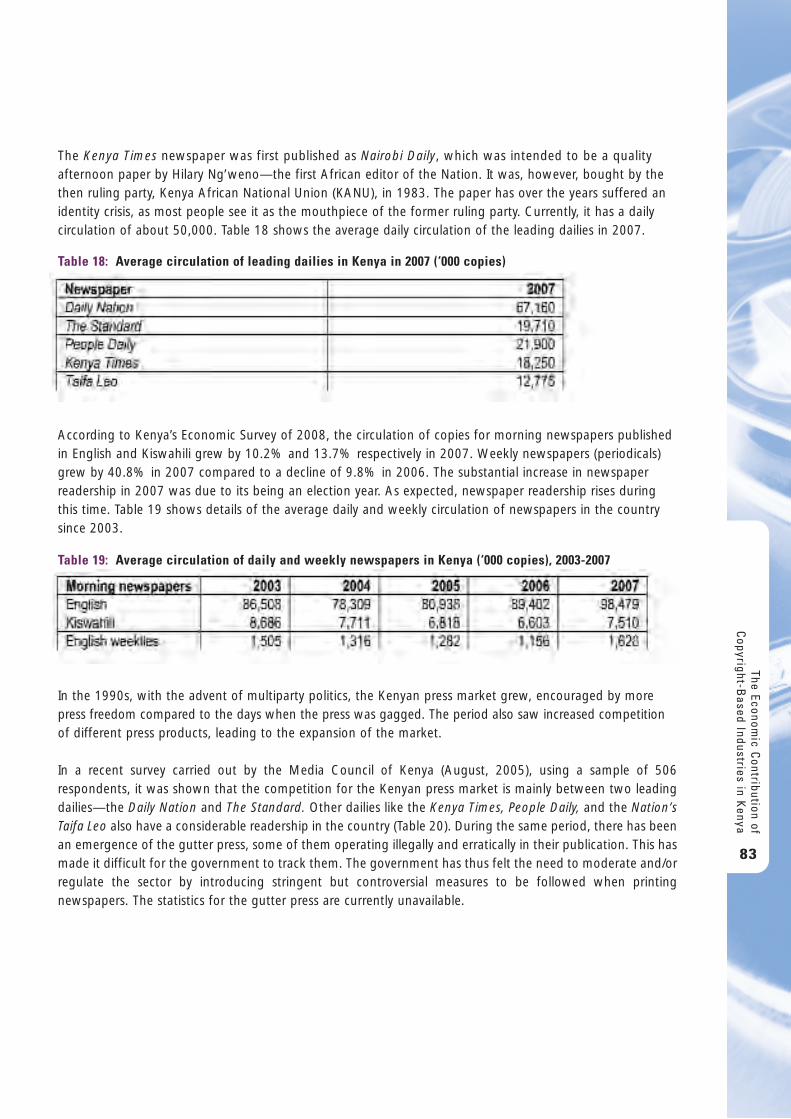

Table 18: Average daily circulation of leading dailies in Kenya in 2007 (‘000 copies) 83

Table 19: Average circulation of daily and weekly newspapers in Kenya (‘000 copies), 2003-2007 83

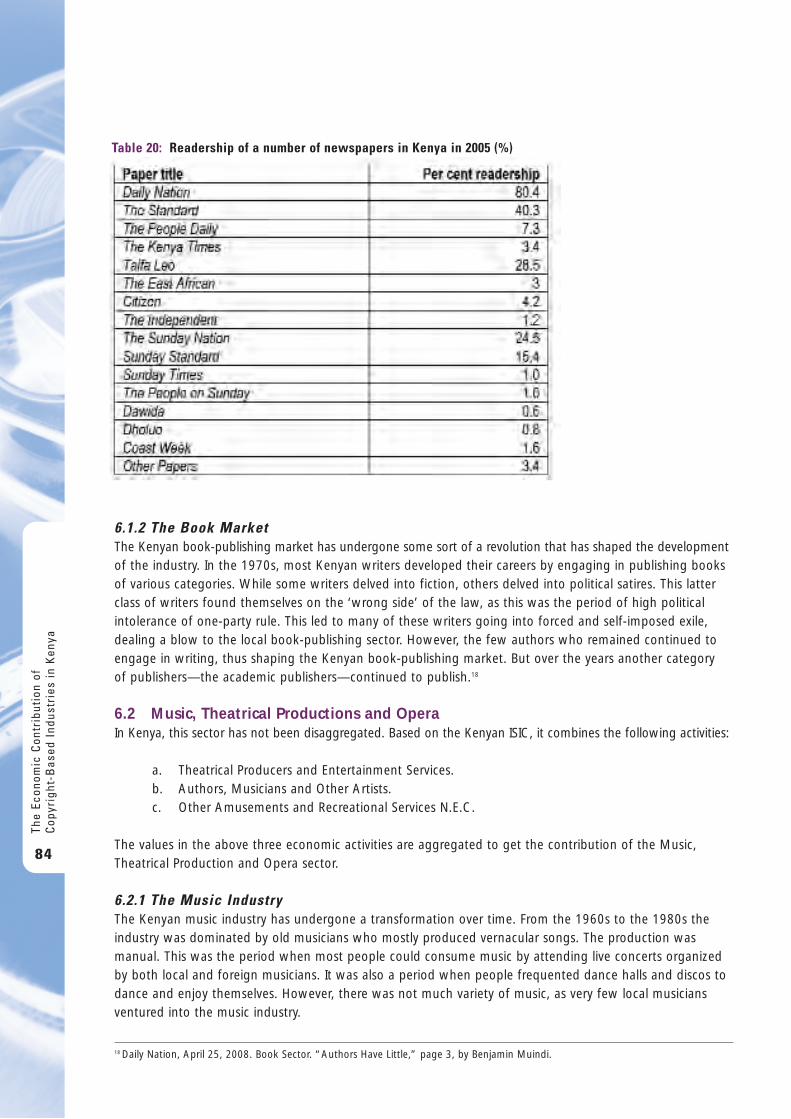

Table 20: Readership of a number of newspapers in Kenya in 2005 (%) 84

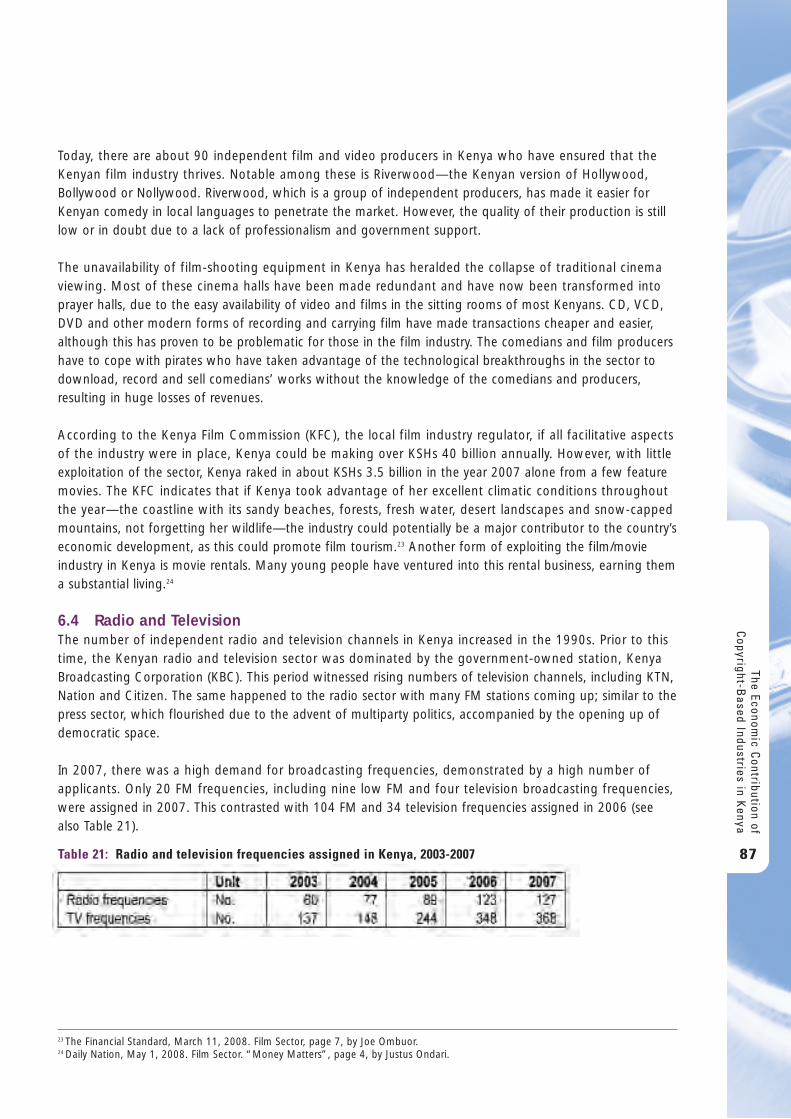

Table 21: Radio and television frequencies assigned in Kenya, 2003-2007 87

Table 22: Television viewer-ship in Kenya in 2007 (%) 88

Table 23: Radio station listener-ship (% share of audience) in Kenya in 2007 88

Table 24: Fee payable according to different ERP conditions in Kenya in 2007 89

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

29

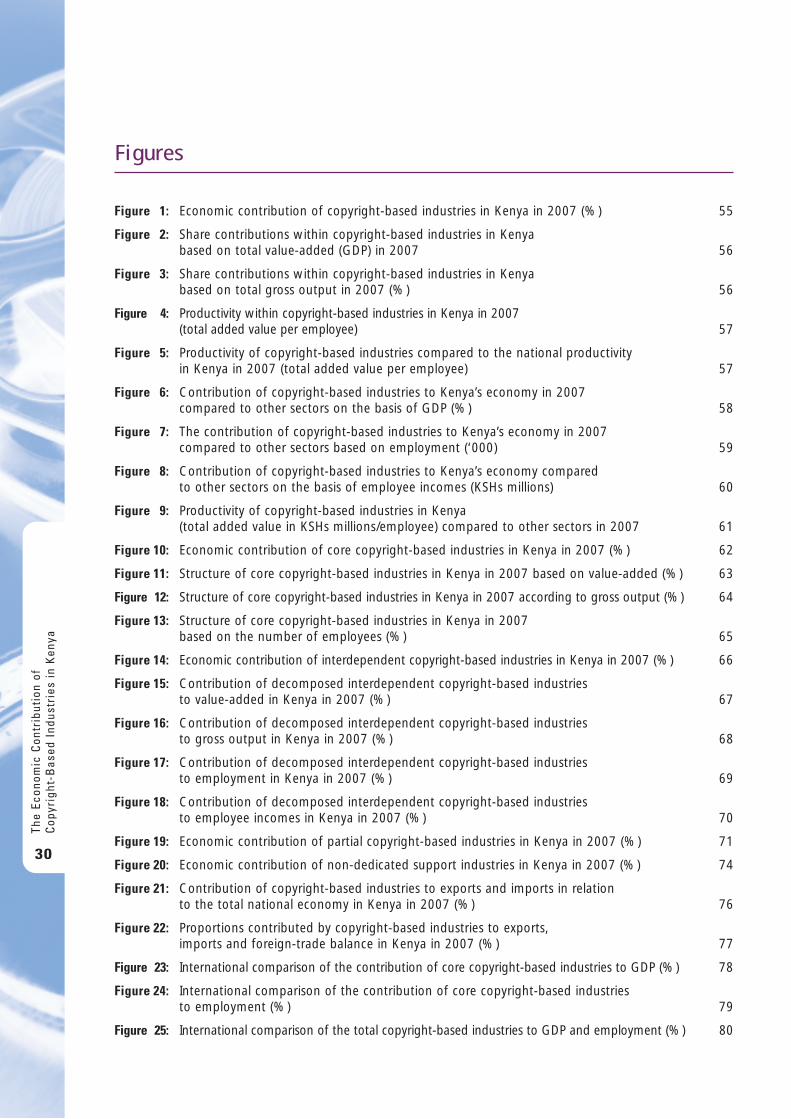

F i g u r e s

Figure 1: Economic contribution of copyright-based industries in Kenya in 2007 (%) 55

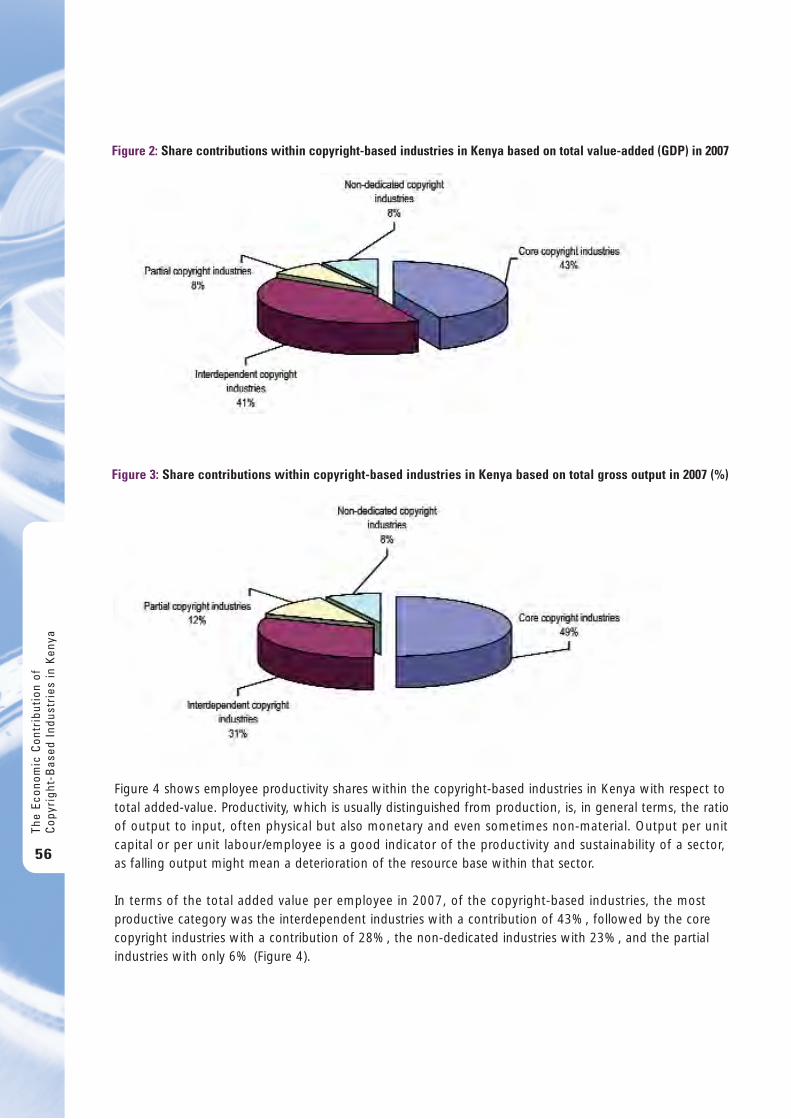

Figure 2: Share contributions within copyright-based industries in Kenyabased on total value-added (GDP) in 2007 56

Figure 3: Share contributions within copyright-based industries in Kenyabased on total gross output in 2007 (%) 56

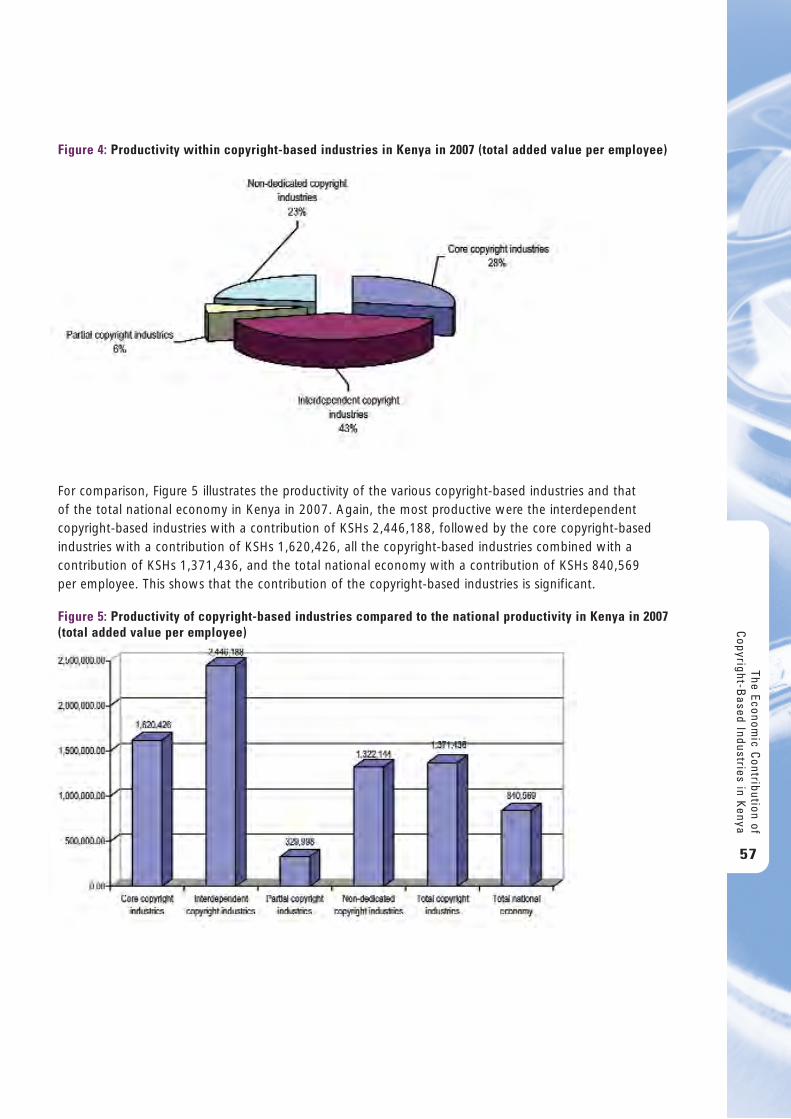

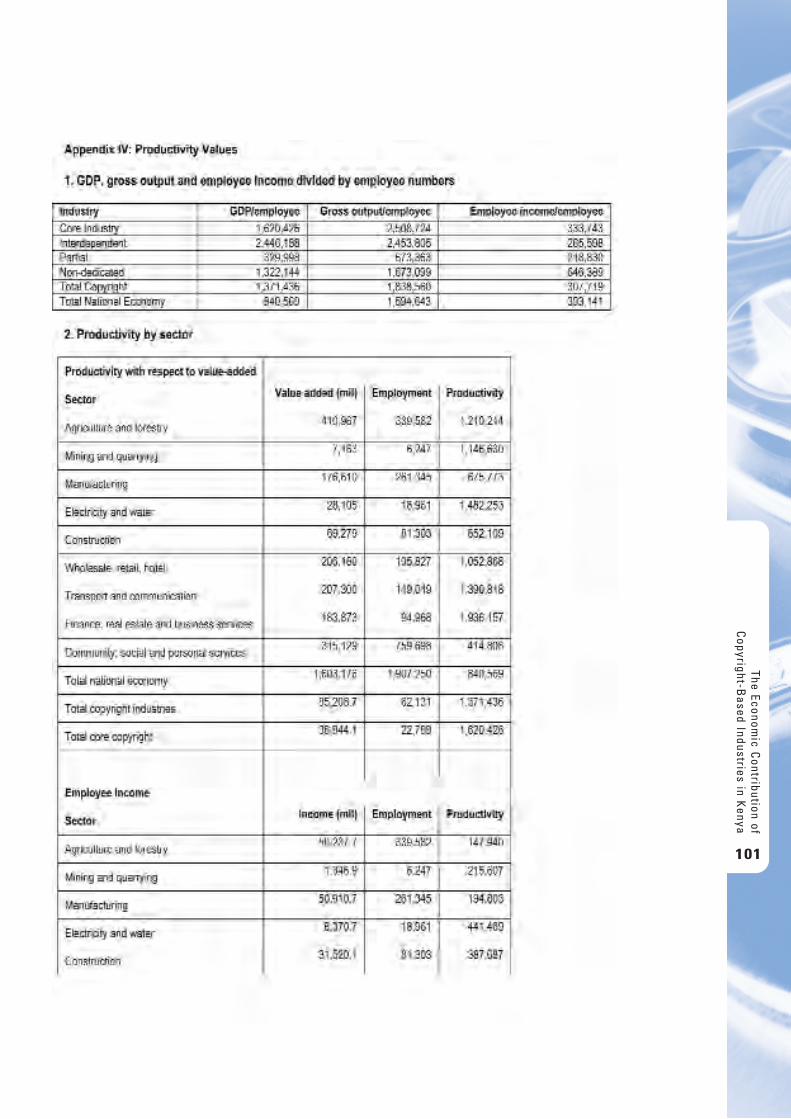

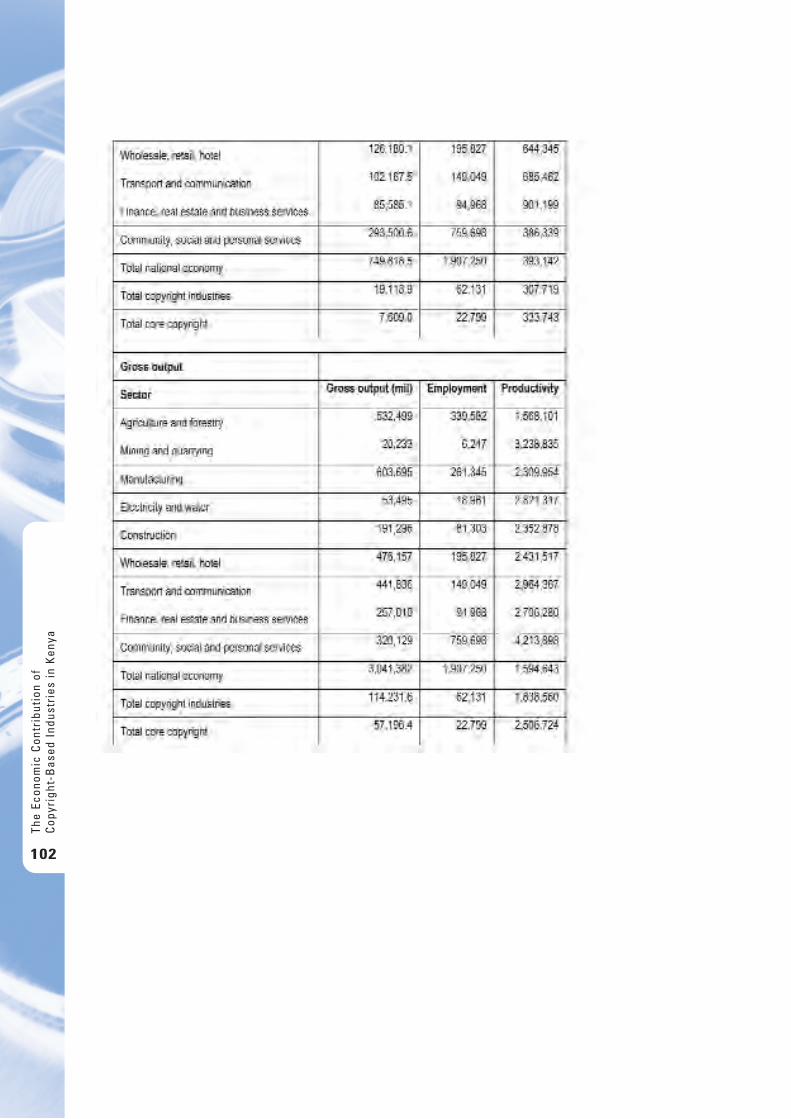

Figure 4: Productivity within copyright-based industries in Kenya in 2007 (total added value per employee) 57

Figure 5: Productivity of copyright-based industries compared to the national productivityin Kenya in 2007 (total added value per employee) 57

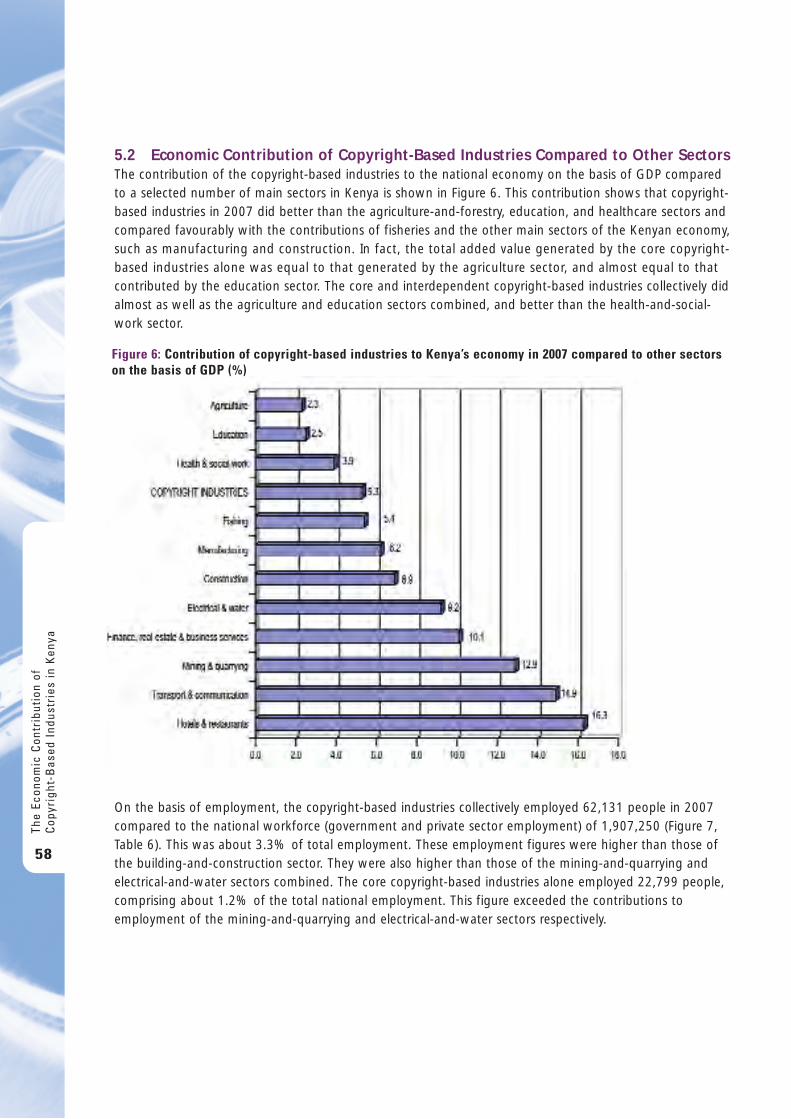

Figure 6: Contribution of copyright-based industries to Kenya’s economy in 2007compared to other sectors on the basis of GDP (%) 58

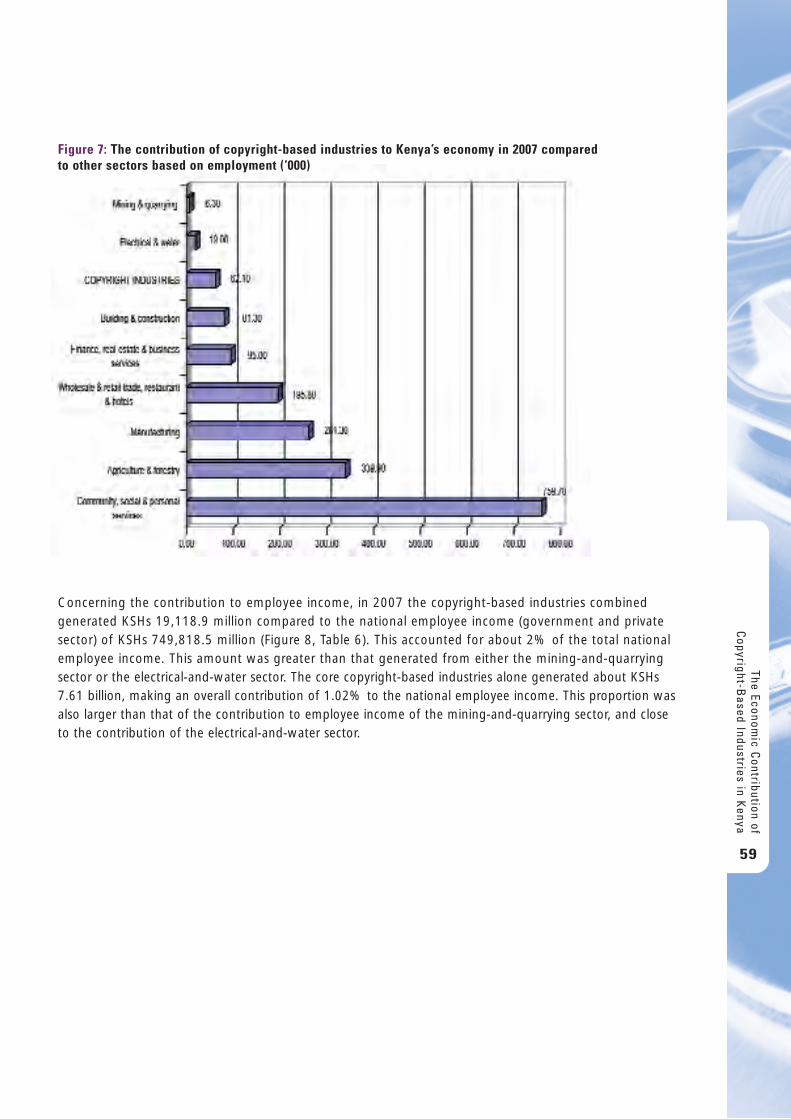

Figure 7: The contribution of copyright-based industries to Kenya’s economy in 2007compared to other sectors based on employment (‘000) 59

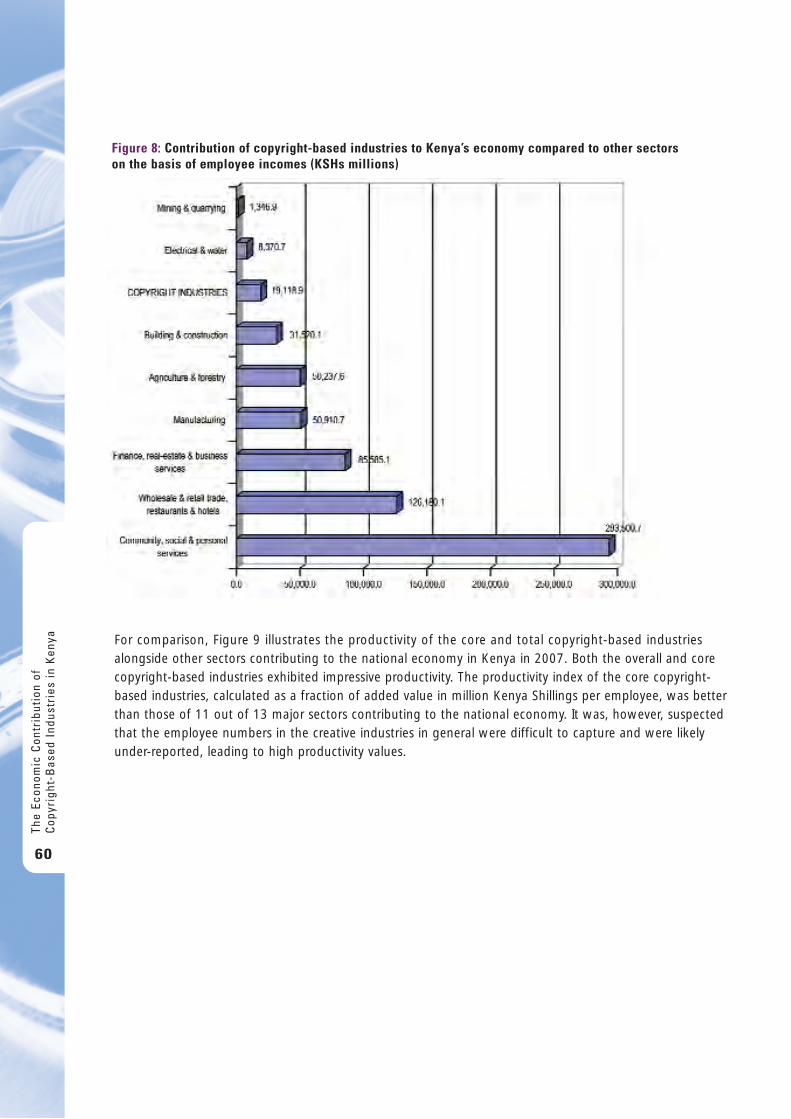

Figure 8: Contribution of copyright-based industries to Kenya’s economy comparedto other sectors on the basis of employee incomes (KSHs millions) 60

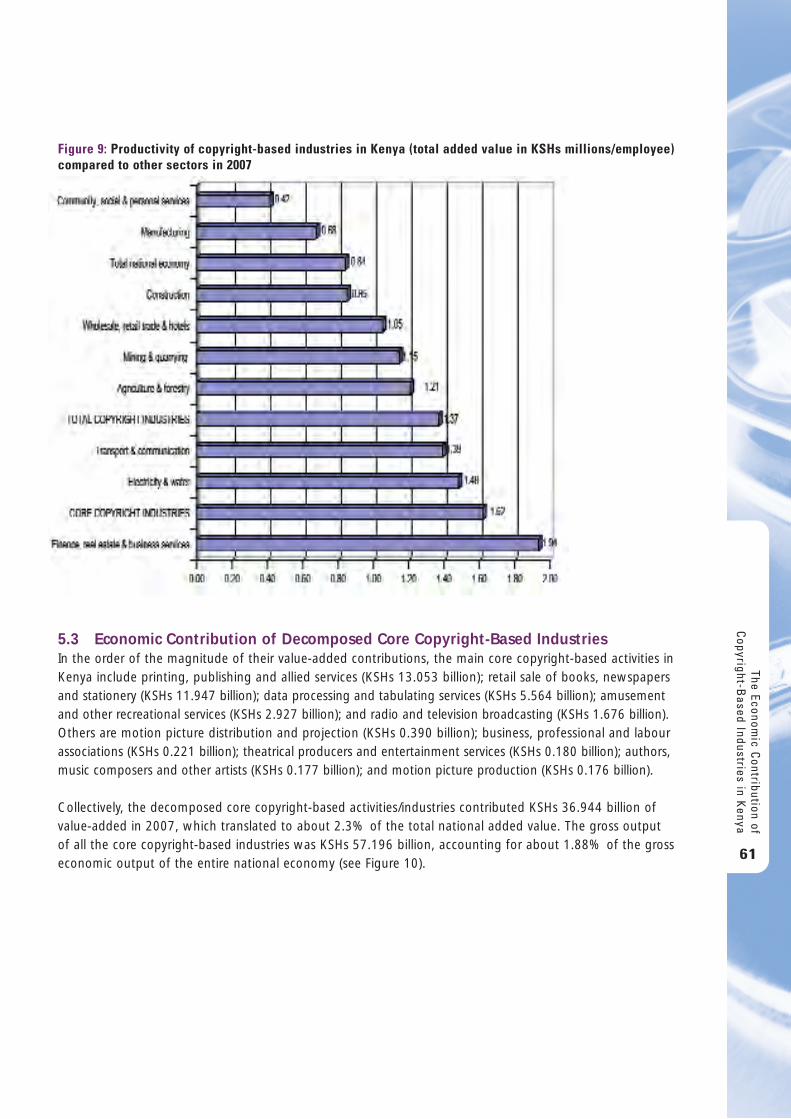

Figure 9: Productivity of copyright-based industries in Kenya(total added value in KSHs millions/employee) compared to other sectors in 2007 61

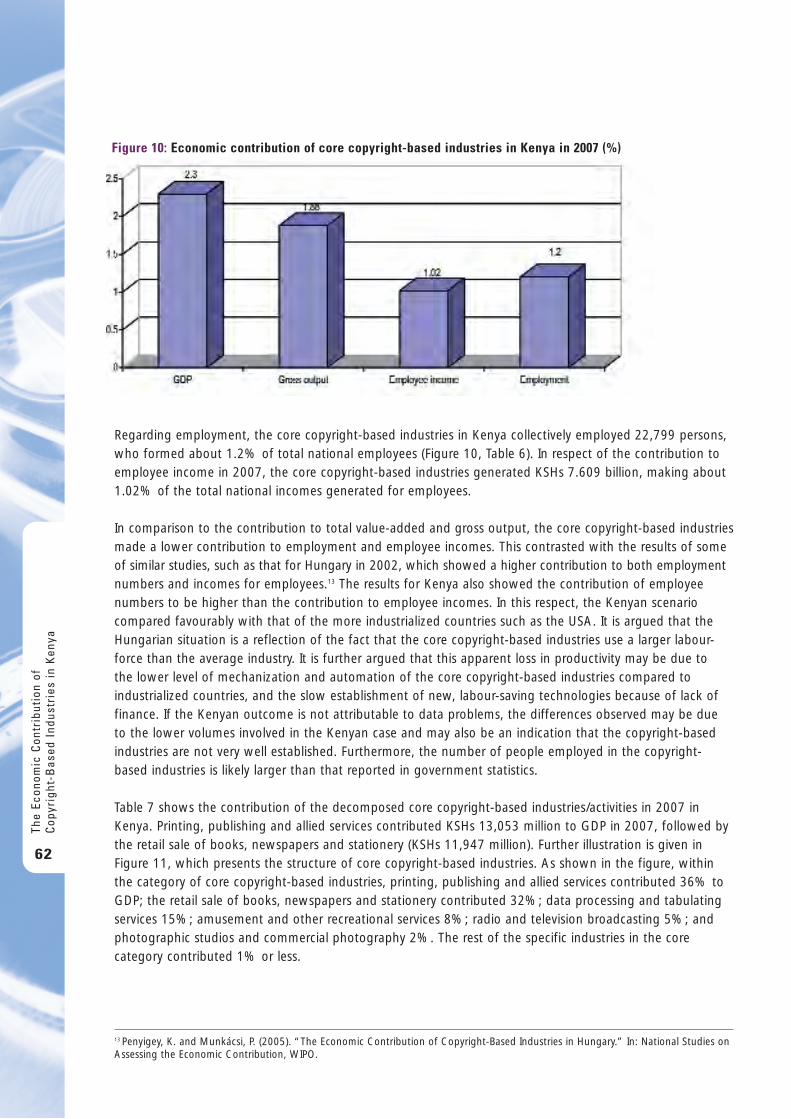

Figure 10: Economic contribution of core copyright-based industries in Kenya in 2007 (%) 62

Figure 11: Structure of core copyright-based industries in Kenya in 2007 based on value-added (%) 63

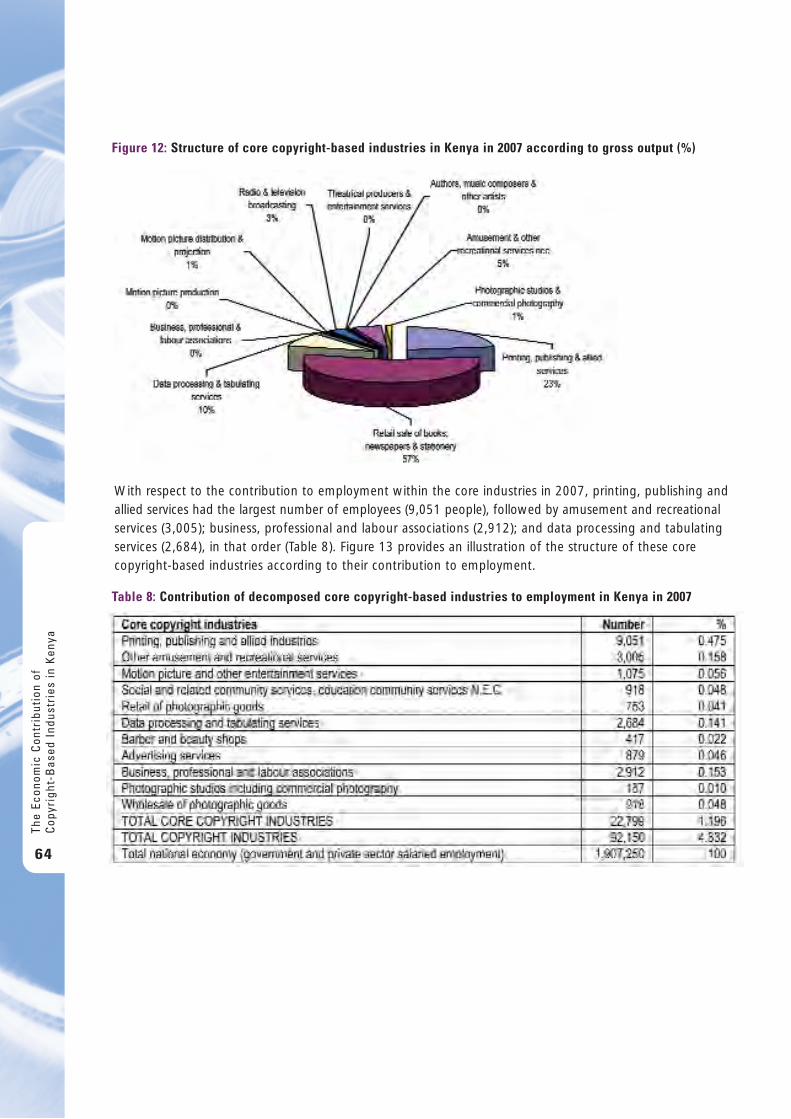

Figure 12: Structure of core copyright-based industries in Kenya in 2007 according to gross output (%) 64

Figure 13: Structure of core copyright-based industries in Kenya in 2007 based on the number of employees (%) 65

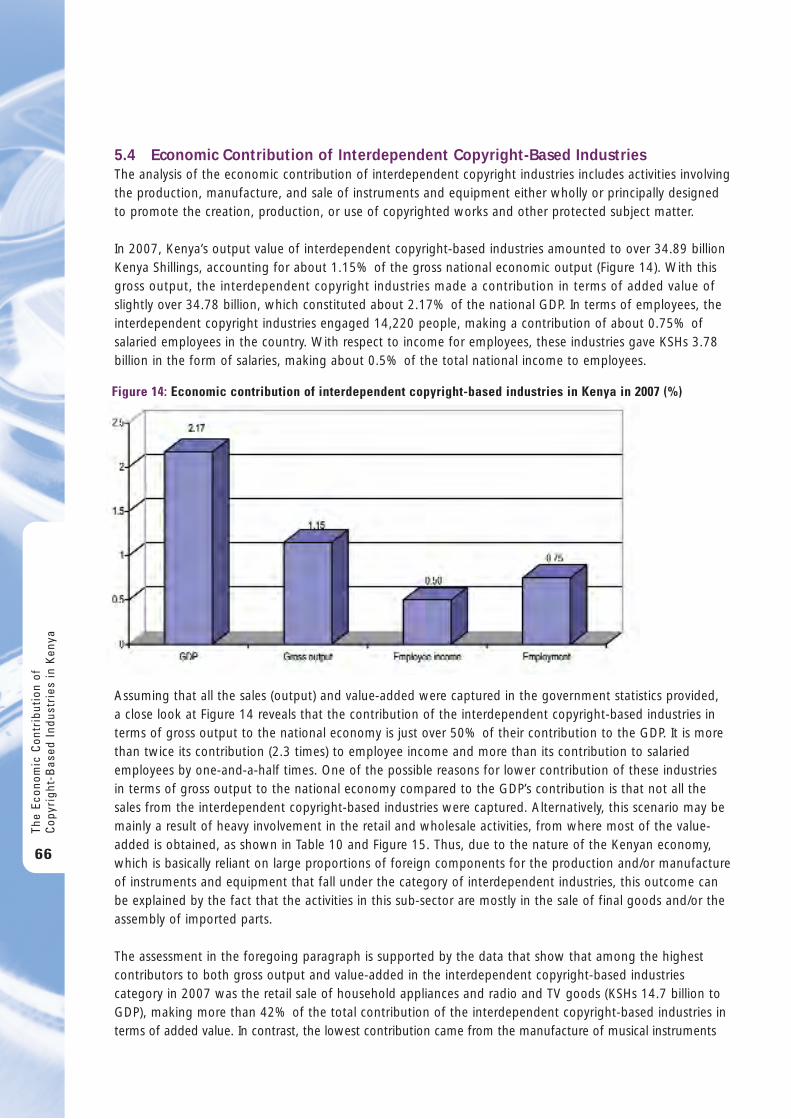

Figure 14: Economic contribution of interdependent copyright-based industries in Kenya in 2007 (%) 66

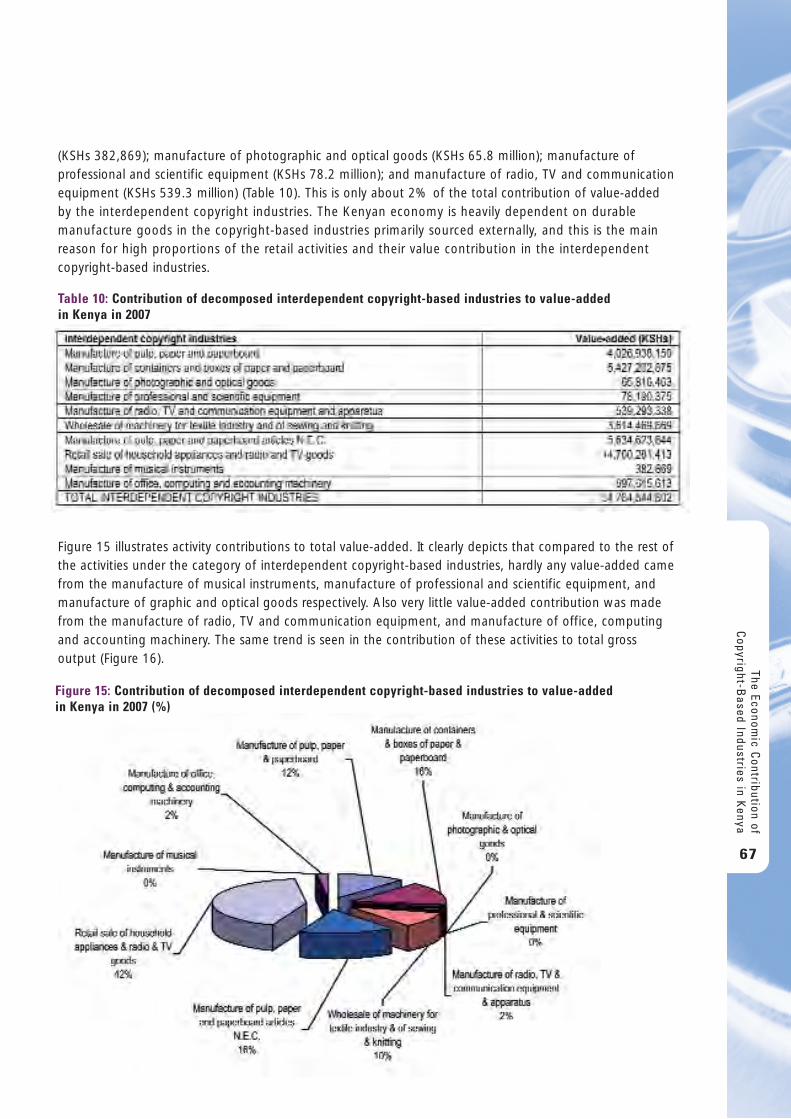

Figure 15: Contribution of decomposed interdependent copyright-based industriesto value-added in Kenya in 2007 (%) 67

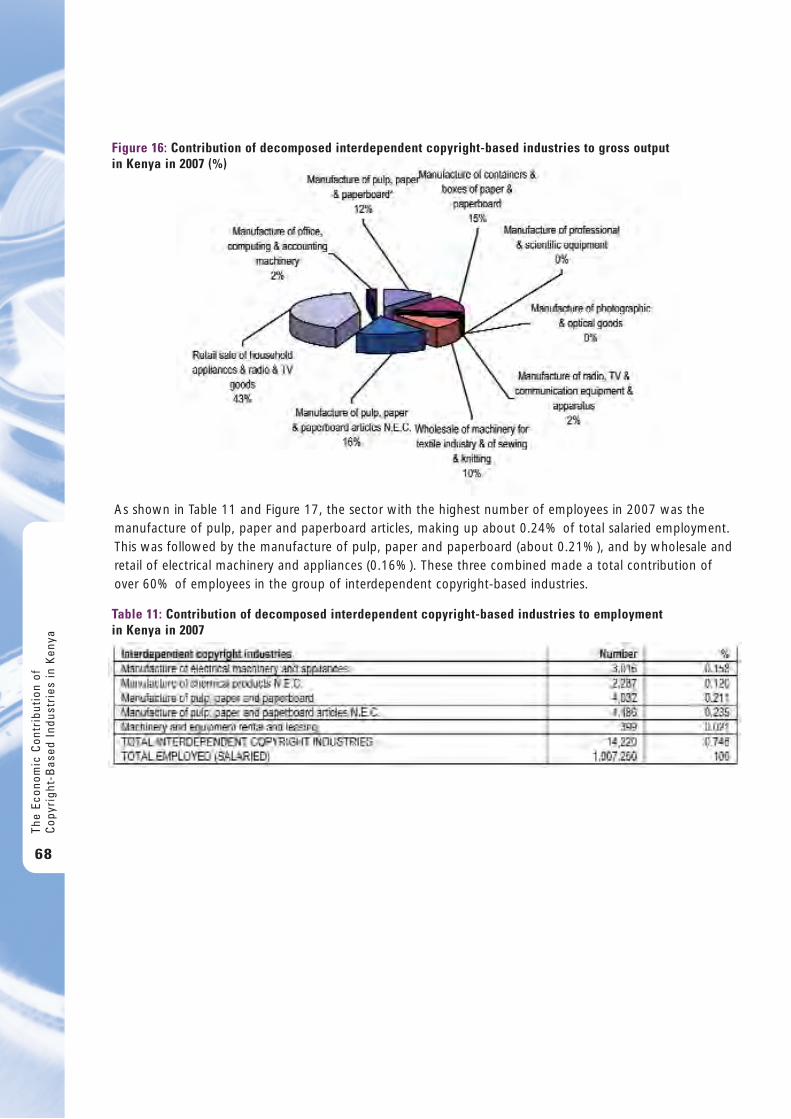

Figure 16: Contribution of decomposed interdependent copyright-based industriesto gross output in Kenya in 2007 (%) 68

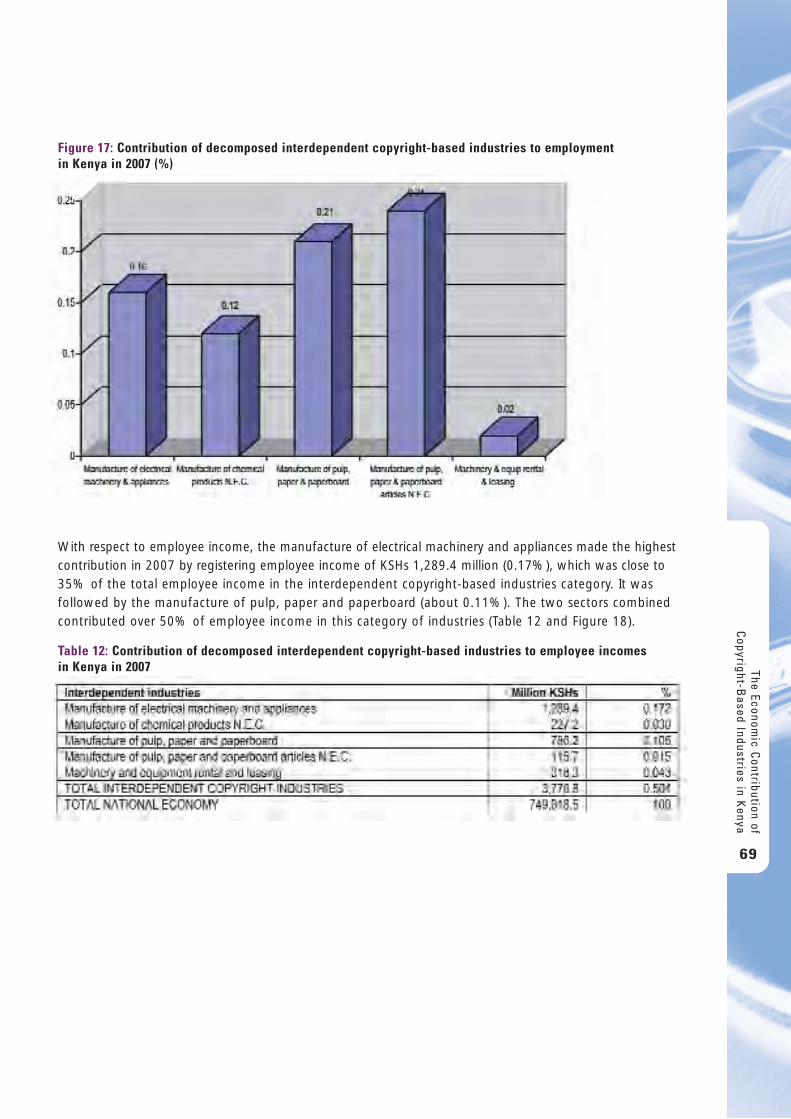

Figure 17: Contribution of decomposed interdependent copyright-based industriesto employment in Kenya in 2007 (%) 69

Figure 18: Contribution of decomposed interdependent copyright-based industriesto employee incomes in Kenya in 2007 (%) 70

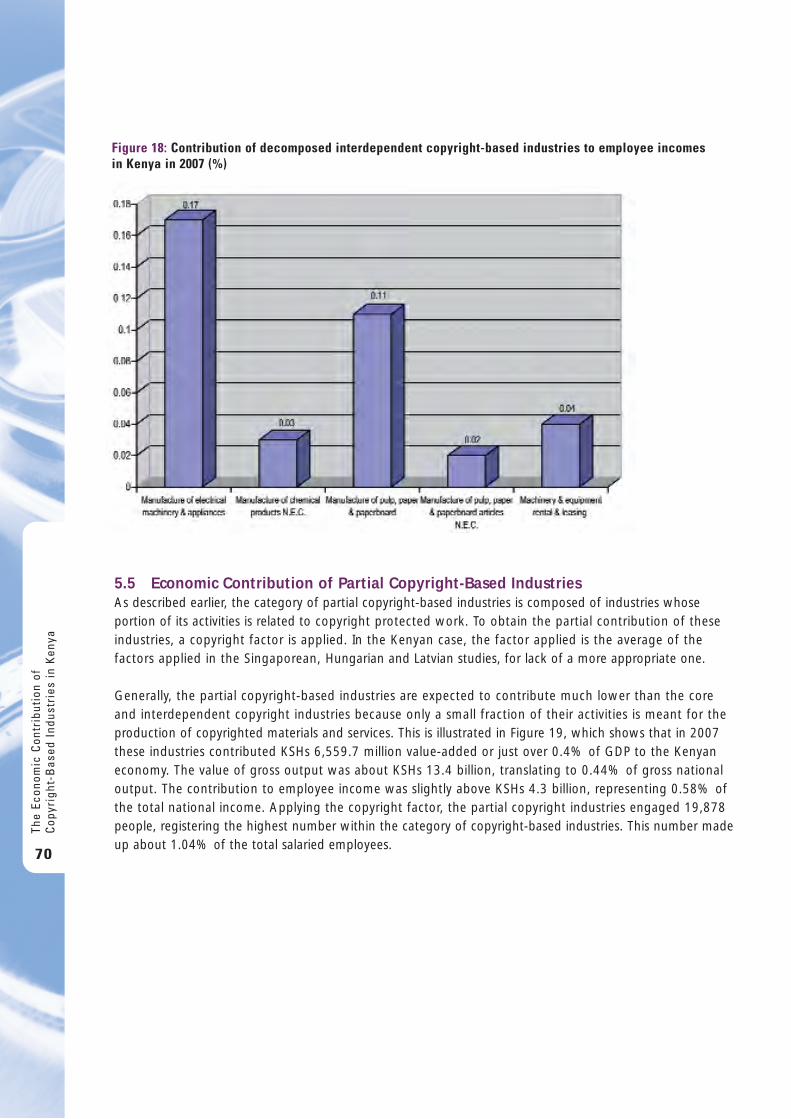

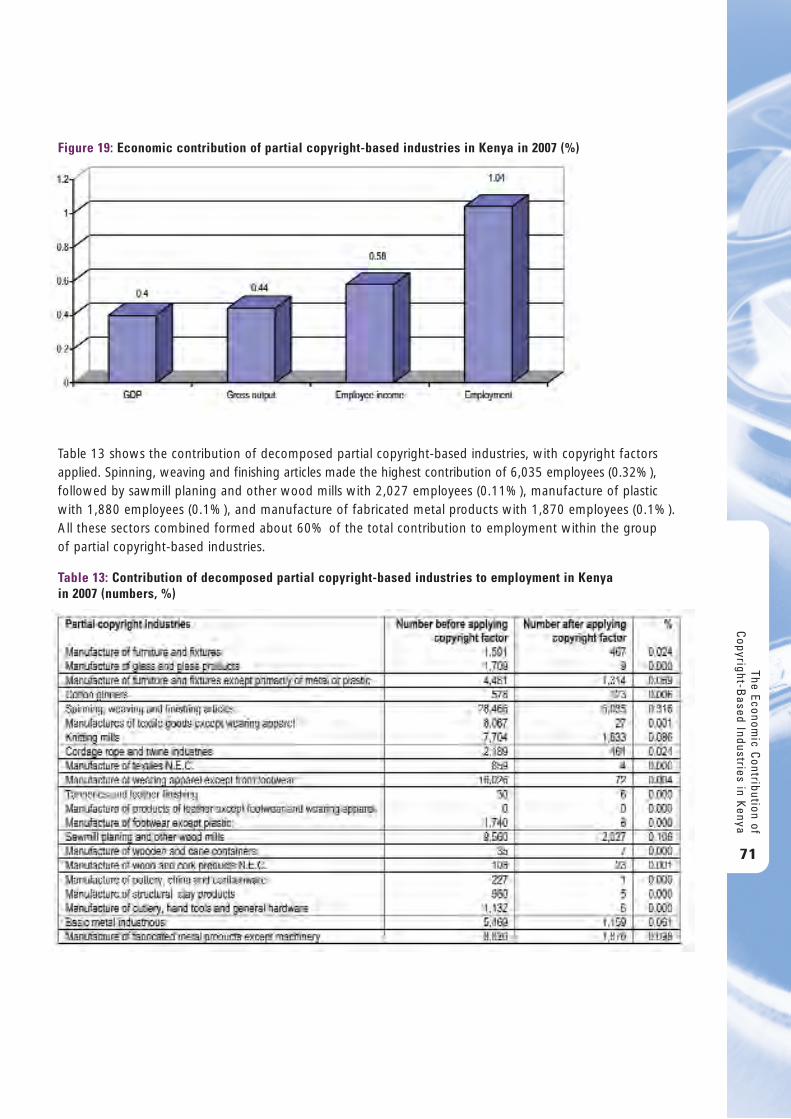

Figure 19: Economic contribution of partial copyright-based industries in Kenya in 2007 (%) 71

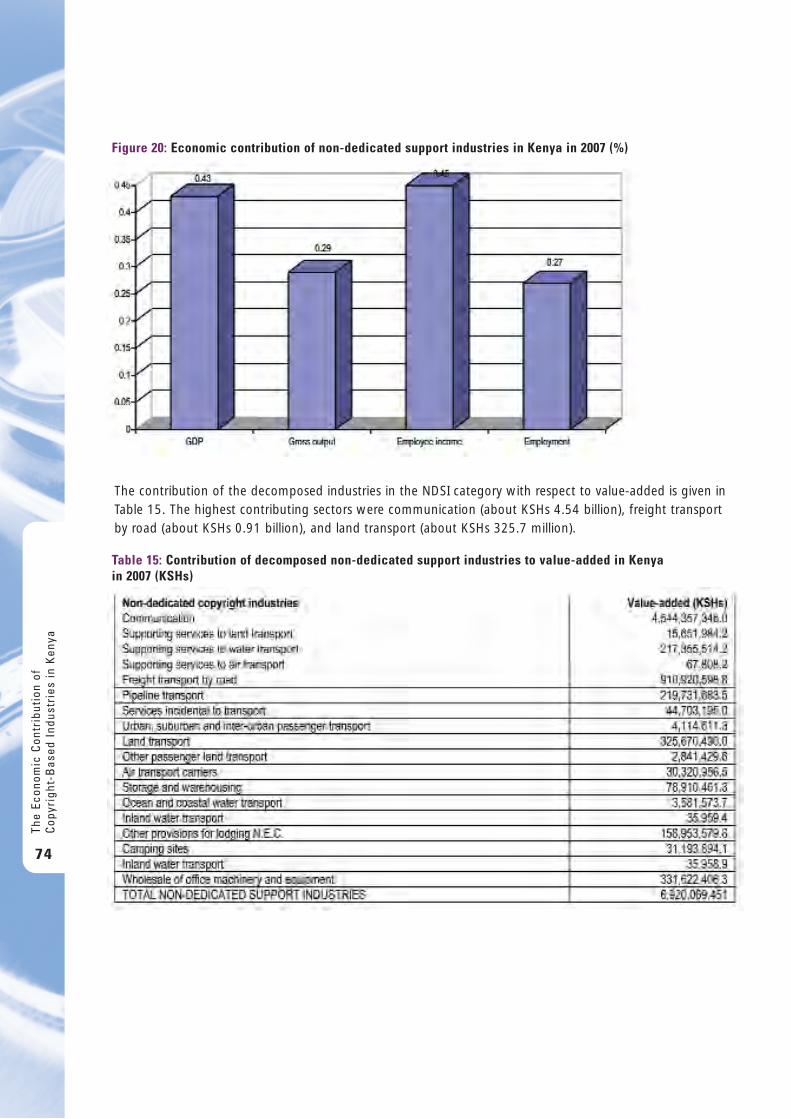

Figure 20: Economic contribution of non-dedicated support industries in Kenya in 2007 (%) 74

Figure 21: Contribution of copyright-based industries to exports and imports in relationto the total national economy in Kenya in 2007 (%) 76

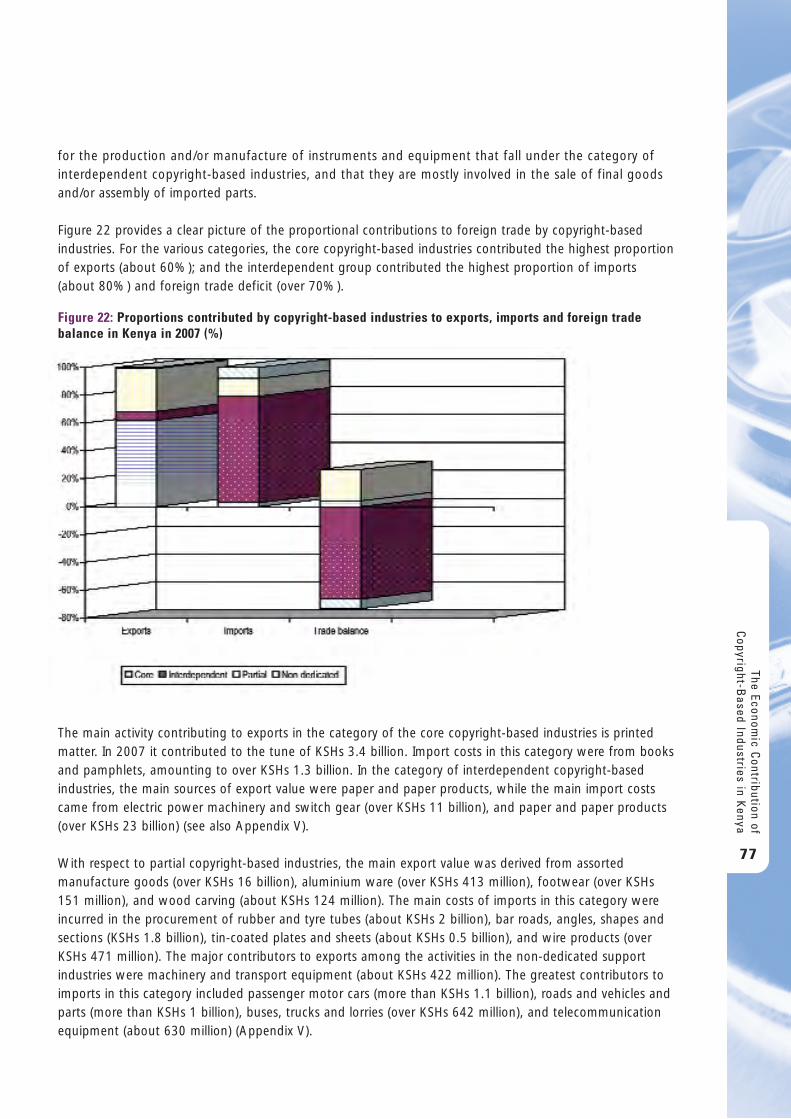

Figure 22: Proportions contributed by copyright-based industries to exports,imports and foreign-trade balance in Kenya in 2007 (%) 77

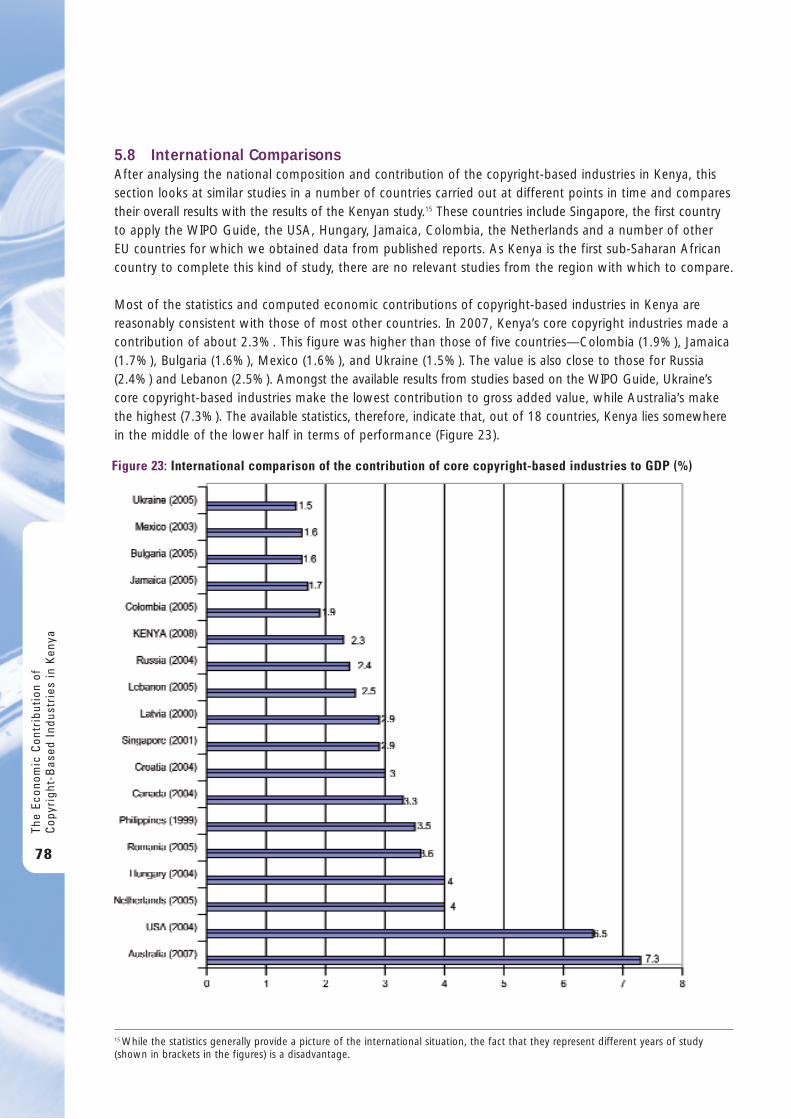

Figure 23: International comparison of the contribution of core copyright-based industries to GDP (%) 78

Figure 24: International comparison of the contribution of core copyright-based industriesto employment (%) 79

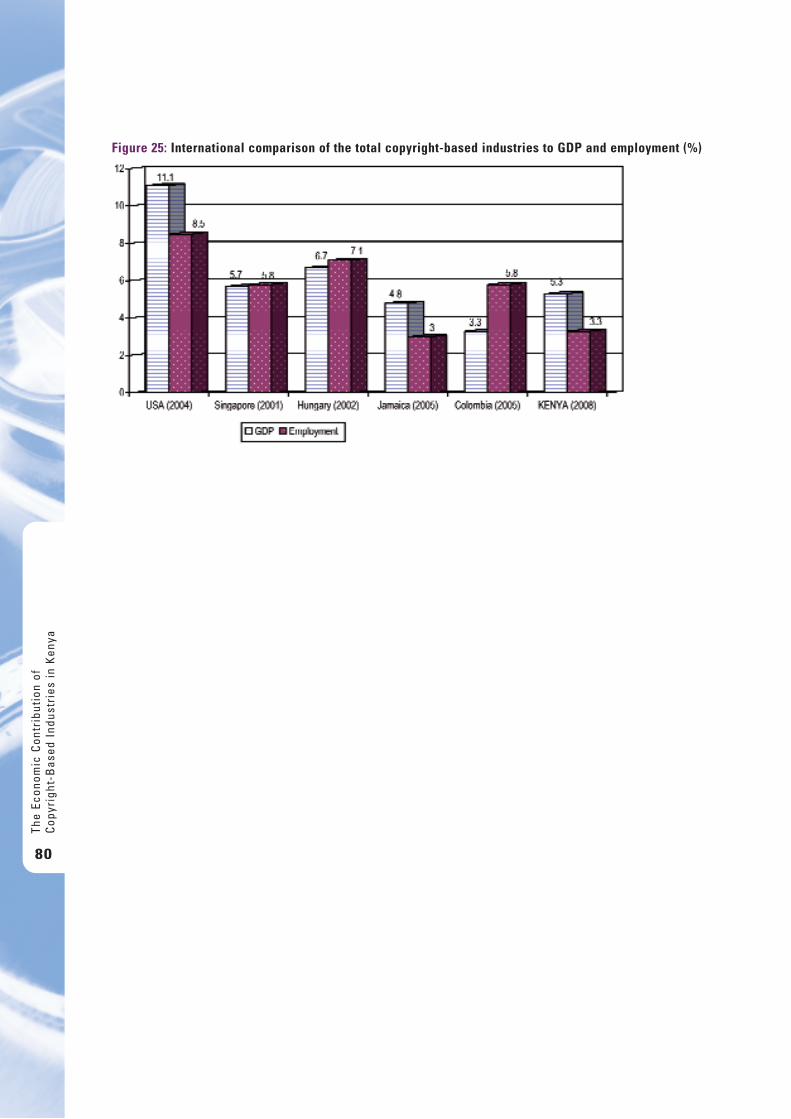

Figure 25: International comparison of the total copyright-based industries to GDP and employment (%) 80

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

30

A c k n o w l e d g e m e n t s

I acknowledge with thanks the assistance given by many organizations, individuals and government officialsin the course of this study. Special thanks go to Marisella Ouma, Acting Executive Director of Kenya CopyrightBoard (KCB), for granting us her time to answer many queries and for availing useful information oncopyright-based industries in Kenya. In particular, I am immensely appreciative of her effort in spending longhours drafting and signing many introductory letters to potential providers of data, and in being readilyavailable for consultations.

This report may not have been possible without the support of the Kenya Revenue Authority (KRA). TheAuthority provided information on the Kenyan classification of copyright-based industries and data onValue-Added Tax (VAT) and sales, which made it possible to compute value-added and gross output. I amespecially grateful to Jonah Ogaro and his team for working tirelessly on the long list of activities, amidsttheir tight official schedules. I must also acknowledge my former University of Nairobi students, who Iengaged as Research Assistants, for data collection. These were Eunice Nginya, Michael Katete, JosephineWere and Juliana Wanyama. They did not only do an excellent job in collecting data and information inthe face of difficulties but also participated in numerous discussion meetings, and often had the graceand patience to bear with me even when I had shown obvious frustrations. Many thanks too go to allgovernment officials and individuals in the private sector whose names I am not able to mention forfinding time to assist us in obtaining data and information for this study.

The UN World Intellectual Property Organization (WIPO) Office in Geneva facilitated this study in anumber of ways. I greatly appreciate the information provided through publications, reports anddiscussions, and the comments received from the team associated with this study, particularly DimiterGantchev and Christopher Kalanje. Dimiter Gantchev (the current Acting Director, Creative IndustriesDivision) deserves special mention. In addition to his expert contributions, I am deeply obliged to him for his patience and understanding; he encouraged me to soldier on even when the exercise appearedimpossible. I am particularly thankful to him for enabling me to attend the October 2008 Expert Meetingin Singapore. The meeting made many issues clear and demystified apparent obstacles in the study thathitherto seemed insurmountable. I further recognize Stephen Siwek (WIPO’s International Consultant) forhis special role. He went through our drafts with a keen eye for detail, offering worthy criticism andguiding comments, and pointing out errors that would not otherwise have been noticed. The quality ofthis publication owes a lot to him.

This study was conducted with funding from WIPO. We therefore express our gratitude at the challengingbut important opportunity the organization provided us to undertake this study. However, the viewsexpressed in this study are those of the authors and not necessarily those of the WIPO Secretariat or of the Member States of WIPO.

Dickson Nyariki

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

31

S u m m a r y

Copyright-based industries form part of creative industries, which are economic activities based on thecreation, management, use and trade in original creations expressed in tangible form. Creative industries arereferred to as copyright-based industries and products there-from as copyright-based goods when they areprotected under intellectual property rights. There is a growing interest in the copyright-based industriestoday due to the recognition that creativity is the very basis for social, economic and cultural developmentof nations. Based on the World Intellectual Property Organization (WIPO) Guide (2003), studies have beenconducted to quantify the contributions of copyright-based industries in several European, Latin Americanand Asian countries. Currently, there are a number of similar studies going on in Africa.

The overall objective of the Kenyan study was to quantify the economic contribution of copyright andrelated rights-based industries in the country by estimating their value-added to GDP, share of nationalemployment, and revenue generated from foreign trade. The findings of this study are expected to informpolicy formulation processes towards an improved policy framework for the operation of the creative sectorin the country. In accordance with the WIPO Guide, this study categorized the copyright and related rights-based industries into core, interdependent, partial, and non-dedicated support industries.

This study relied mainly on secondary data for 2007 obtained from various government departments andother relevant institutions. The main sources of data included the Kenya Revenue Authority (KRA); KenyaNational Bureau of Statistics (KNBS); Attorney General Chambers; Kenya Institute for Public Policy Researchand Analysis (KIPPRA); Institute of Policy Analysis and Research (IPAR); Kenya Association of Manufacturers(KAM); and the Music Copyright Society of Kenya (MCSK). Other secondary sources of data were past andcurrent research and government reports. In addition, internet searches were employed to access availableinformation on the contribution of creative industries to the national economy.

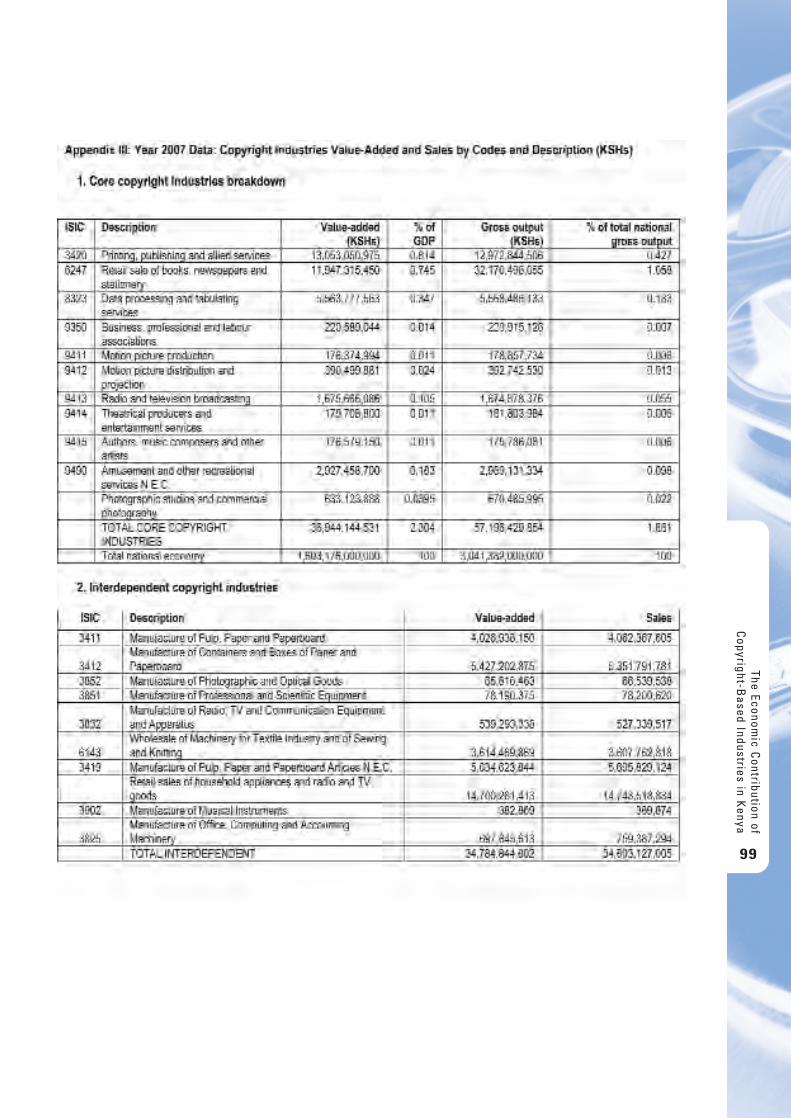

The results show that the total value-added of copyright-based industries in 2007 amounted to about KSHs85.21 billion, which represented 5.32% of Kenya’s GDP. The contribution to the country’s total value-addedby the core industries was KSHs 36.94 billion (2.3%), by the interdependent industries KSHs 34.78billion (2.17%), the partial industries KSHs 6.56 billion (0.41%), and the non-dedicated supportindustries KSHs 6.92 billion (0.43%). The entire copyright-based industries contributed KSHs 114.23billion out of the national gross output of KSHs 3,041.38 billion, which represented 3.76% of the grossoutput. Out of this total, the core copyright-based industries made a contribution of KSHs 57.2 billion,which formed 1.88%. With respect to the income for employees, the copyright-based industries made atotal of KSHs 19.12 billion, making a proportion of about 1.97% compared to the total national economicvalue of KSHs 749.82 billion. The total employee income for core industries was KSHs 7.61 billion, whichwas 1.02% of the national employee income. Generally, those employed in the non-dedicated supportindustries were the highest paid workers in the copyright-based industries in Kenya.

Copyright-based industries employed 62,131 people. These comprised 3.26% of the total nationalworkforce. Within this number, employee numbers in the core copyright industries were 22,799,constituting 1.2% of the total national workforce.

The core copyright-based industries outperformed the other three categories of copyright-based industries in all the main economic contributions considered in this study—GDP, gross output, employment andemployee incomes. The interdependent copyright-based industries did better than the partial copyright-based and non-dedicated support industries in the contribution to GDP and gross output. The partial

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

32

copyright-based industries exceeded the interdependent copyright-based and non-dedicated supportindustries in the contribution to employment and employee incomes.

Within the copyright-based industries, the core copyright-based industries made the highest contribution of43% to the total copyright-based GDP, followed by the interdependent copyright-based industries, whichcontributed 41%. With respect to gross output, the core copyright-based industries contributed an evenhigher share of 49% compared to the contribution of interdependent industries of 31% of the totalcopyright-based gross output. The partial copyright-based and non-dedicated support industries madecontributions of 12% and 8% respectively.

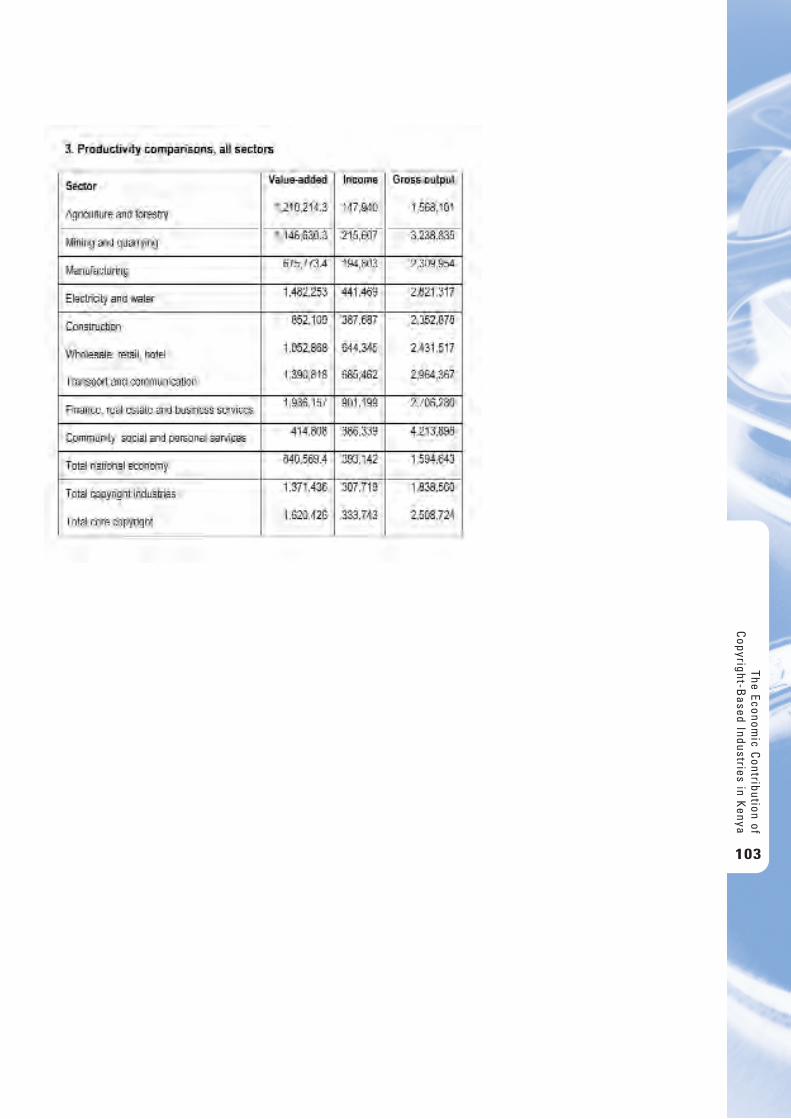

Of the copyright-based industries, the most productive, in terms of the total added value per employee, wasthe interdependent industries with a contribution of KSHs 2,446,188, followed by the core copyright-basedindustries with a contribution of KSHs 1,620,426, all the copyright-based industries combined with acontribution of KSHs 1,371,436, and the total national economy with a contribution of KSHs 840,569 peremployee. This shows that the productivity of all the copyright-based industries was more than one-and-a-half times that of the national productivity, while the productivity of the core copyright-based industries andthe interdependent copyright-based industries was twice and three times that of the national productivityrespectively. Also, compared to the other major sectors of the economy, copyright-based industriesperformed impressively in terms of productivity. The core copyright-based industries were second best with a productivity value of KSHs 1.62 million per employee, compared to the best-performing sector—finance,real estate and business services—with a productivity value of KSHs 1.94 million per employee.

The contribution of the copyright-based industries to the national economy on the basis of GDP was higherthan that of the agricultural sector (2.3%), education (2.5%), and healthcare (3.9%), and comparedfavourably with the contributions of the other main sectors of the Kenyan economy, such as fisheries (5.4%)and manufacturing (6.2%). The contribution of copyright-based industries of 62,131 people to the nationalemployment was also higher than that of the electrical-and-water sector (19,000 employees) and themining-and-quarrying sector (6,300 employees). Furthermore, the contribution of copyright-based industriesto the national employee income (KSHs 19.12 billion) was more than that from the mining-and-quarrying(KSHs 1.35 billion) and electrical-and-water (KSHs 8.37 billion) sectors, individually as well as combined.

The core and partial copyright-based industries contributed proportionally more value of exports thanimports compared to the total national exports and imports, which were 1.30% and 0.22% for the coreand 6.54% and 0.99% for the partial, respectively. Similarly, all copyright-based industries combinedproportionally produced higher export value relative to the total national export value (9.35%) than importvalue relative to the total national import value (7.86%). The national economy exhibited a huge foreigntrade deficit compared to the copyright-based industries, implying that the copyright-based industries aredoing better than the overall national economy. However, the copyright-based industries have a relativelyhigh import component, particularly within the interdependent category, that reduces its value-added andgross output.

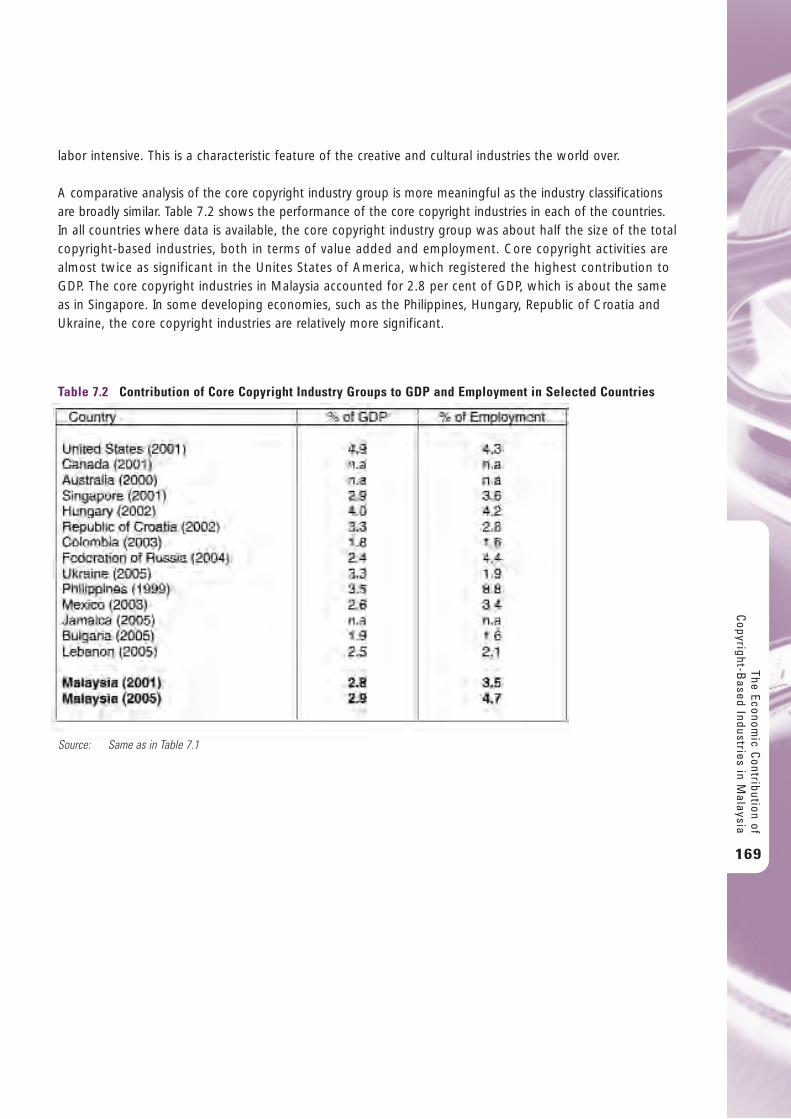

Most of the statistics and computed economic contributions of copyright-based industries in Kenyacompared reasonably well with those of other countries. In 2007, Kenya’s core copyright-based industriesmade a contribution of over 2.3% to GDP. Compared with the results of similar studies conducted earlier inother countries, this figure was larger than those for Colombia (1.9%), Jamaica (1.7%), Bulgaria (1.6%),Mexico (1.6%) and Ukraine (1.5%). According to the studies so far carried out based on the WIPO Guide,Ukraine core copyright-based industries make the lowest contribution (1.5%) to GDP, while Australia makethe highest (7.3%), followed by the USA (6.5%). These statistics, therefore, indicate that Kenya lies

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

33

somewhere in the middle of the lower half in terms of performance. With respect to employment contributionby the core copyright-based industries, Kenya did not do as well as with GDP contribution. Kenya’scontribution of 1.2% of employees, compared to the national employment, was only better than Ukraine’s(1.16%). However, the core and interdependent copyright-based industries combined accounted for 4.5%of Kenya’s GDP, well above many countries in comparison. A comparison of the contribution of the totalcopyright-based industries to GDP and employment between Kenya and the USA, Singapore, Hungary,Jamaica, and Colombia reveals that Kenya performed favourably. It did better than Jamaica, comparedclosely with Colombia, and did not rank far behind Singapore and Hungary.

In summary, therefore, the contribution of copyright-based industries in Kenya in 2007 was as follows:On the basis of GDP, their contribution within the country was higher than that of the agricultural sector,education, and healthcare, and compared favourably with the fisheries and manufacturing sectors. Withrespect to employment, the industries engaged a higher number of people than the electrical-and-waterand mining-and-quarrying sectors.As far as productivity is concerned, in terms of GDP per employee, theindustries performed one-and-a-half times better than the national economy. Internationally, the industriesperformed averagely in terms of GDP, but did better than a number of countries in Europe, South America,Asia, and the Caribbean.

A few discrepancies were noted in the data used in this study, mainly as a result of databases in Kenyabeing piecemeal and scattered in different government agencies. This presented difficulties in estimating thefull contribution of the copyright-based industries to GDP. The contribution of these industries to the totalvalue-added, therefore, is likely higher than what was shown.

Despite some inadequacies in the policies governing the operations of copyright-based industries in Kenya,their economic contribution is reasonably significant. The economic contribution of copyright-basedindustries in Kenya is higher than a number of important sectors in the country and compares well withthose of several countries in Europe, Asia and the Americas for which similar studies have been conducted.In order to promote the growth and development of already vibrant copyright-based sectors in Kenya,appropriate and operational policy frameworks are imperative.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

34

1 . I n t r o d u c t i o n

1.1 Background and ContextCopyright industries form part of creative industries, which are economic activities based on the creation,management, use and trade in original creations expressed in tangible form. When the producedexpressions are protected under intellectual property (IP) rights, then such industries are referred to ascopyright industries and the products there-from as copyright goods. Copyright is a legal term describingrights given to creators for their literary and artistic works. It is a type of property that is founded on aperson’s creative skill and labour. It is designed to prevent the unauthorized use by others of a work, that is,the original form in which an idea or information has been expressed by the creator. According to the WIPOGuide (2003), copyright is not a tangible thing. It is made up of a bundle of exclusive economic rights to docertain acts with an original work or other copyright subject-matter. These rights include the right to copy,publish, communicate (e.g., broadcast, make available online) and publicly perform the copyright material.The copyright creators also have a number of non-economic rights.

The kinds of works covered by copyright include: literary works such as novels, poems and plays; referenceworks; newspapers; computer programs and databases; films, musical compositions and choreography;artistic works such as paintings, drawings, photographs and sculptures; advertisements; architecture; andmaps and technical drawings. Creative industries—most of which are based on copyright and relatedrights—are said to have considerable impact on national economies. National studies in many countrieshave revealed that these industries are major contributors in terms of their relative aggregate value-added to a country’s Gross Domestic Product (GDP) as well as their contribution to employment and foreign trade. For example, as shown in a report by Siwek (2004), one of the highest contributions of the core copyright-based industries to the national economy in terms of gross added value has been in the UK (7.1%). Anotherhas been the USA with a contribution of about 6% in 2002. The contribution of total copyright-basedindustries in the USA in terms of GDP in the same year was an impressive 12%.2

Thus, copyright today is seen as more than a legal system providing a secure and stable environment forcreative activity in different markets. The growing interest is largely due to a number of factors, namely a)the increased recognition of the role of IP in post-industrial society, where more attention is being paid tonon-material production factors; b) the expansion of the scope of copyright protection as a result of digitaltechnology, which has seen the economic gains from different technology-based products rise to verysignificant levels; c) the recognition of copyright-protected material as one of the main components inelectronic commerce and digital transactions courtesy of the digital revolution; and d) the recognition of the fact that creativity is the very basis for the social, economic and cultural development of nations.

The nature of copyright and the scope of its protection, enforcement and infringement have been thesubject of extensive research. Recently, however, the focus has shifted towards the economic characteristicsof copyright. The first studies to quantify the economic contribution and significance of copyright-basedindustries were published in Canada and Sweden in the 1970s. These were followed by further works fromthe USA, New Zealand, the United Kingdom, Holland, Germany and Austria in the 1980s. More studiesbased on an integrated, standardized methodology have since been conducted in the 1990s in Finland,Japan, Argentina, Brazil, Paraguay, Uruguay, and Chile.3 The analysis of the contribution of copyright

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

35

2 Information based on Siwek, S.E. (2004): Report on “The Economic Contribution of Copyright-Based Industries in the US.” Preparedfor the International Intellectual Property Alliance. 3 Penyigey, K. and Munkácsi, P. (2005). “The Economic Contribution of Copyright-Based Industries in Hungary.” In: National Studies onAssessing the Economic Contribution. WIPO, page 287.

industries to national economies in EU countries was published in 2003.4 In 2003, WIPO issued amethodological guide with a view to revealing the economic contribution of copyright-based industriesunder the title: “Guide on Surveying the Economic Contribution of Copyright-Based Industries”.5 TheSingapore, Canada, and USA reports, which were also based on the Guide, were published in 2004,followed by the Latvian report in early 2005.

The motivation behind research on the economic roles of copyright-based industries is to makeeconomic policymakers aware of the economic importance of these industries. This is expected toencourage mainstreaming of copyright-based industries in the development policies of a given country.It is against this background that WIPO and the Government of Kenya commissioned the current studyin light of the increasing importance of copyright-based goods and services to the economy, and as anelement towards introducing an improved policy framework for the operation of the creative sector inthe country. It is expected that the results of this study will serve as an important input in promoting the growth and development of the copyright-based sectors in the country. The Kenyan study is basedon the WIPO Guide (2003).

In this study, copyright covers creative work such as a writer putting words down on paper, a photographertaking a photograph, or a software designer creating a code. Related rights include rights of performingartists, rights of television and radio broadcasters, rights of producers of phonograms, and rights of producers ofmotion pictures. The term ‘copyright’ is used in most cases to cover both copyright and related rights.

1.2 Objectives and Structure of the StudyThe key objectives of this study were to:

a. Quantify the economic contribution of copyright and related rights-based industries in the country by estimating their value-added to GDP, share of national employment, and revenue generated fromforeign trade.

b. Analyze and elaborate on selected copyright and related rights-based industries of importance toKenya, their national market structure, value chain, demand and supply patterns, labour market, policy framework, support from public and civil sectors including the role of collective managementorganizations and other copyright-related organizations, financing mechanisms, and implications of the digital environment, among others.

c. Propose policy, strategy and institutional interventions to encourage the growth and development of copyright-based industries in the country.

The structure of the study is in seven parts:

a. The first part consists of an introduction and a presentation of the objectives and structure of thestudy.

b. The second part presents an overview of the copyright policy and law in Kenya.c. The third part describes the copyright and related rights-based industries in Kenya, presents the

copyright factors used, and provides a comparison of Kenya’s industry coding system and that of theWIPO Guide (2003).

d. Part four provides details of data collection and methods of analysis.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

36

4 Picard, R.G., Toivonen, T.E. and Grönlund, M. (2003). “The Contribution of Copyright and Related Rights to the European Economy.”European Commission, Directorate General (Internal Market).5 World Intellectual Property Organization (WIPO) (2003). “Guide on Surveying the Economic Contribution of the Copyright-BasedIndustries.” WIPO, Geneva.

e. The fifth part discusses the results of analysis on the economic contribution of copyright and relatedrights-based industries in Kenya, adapting the general guidelines presented in the Guide to the Kenyansituation, in terms of value-added generated by copyright and related rights-based industries, theircontribution to employment generation, productivity of the various copyright-based sub-sectors, theforeign trade of copyright and related rights-based industries, and a brief comparison of the Kenyanand international studies carried out on the basis of the WIPO Guide.

f. Part six provides a description of the development of some core copyright-based industries in Kenya.g. The final part presents the conclusions of the study and policy recommendations.

1.3 Scope of StudyThe current study attempted to quantify as extensively as possible the economic contribution of copyright-protected goods and services in Kenya in 2007. The study included the following steps:

a. The first step included the identification of the copyright and related rights-based industries to bestudied using as reference Annex I of the WIPO Guide as well as the selected copyright and relatedrights-based industries which were given more detailed analysis. The categorization of the copyrightand related rights-based industries followed the categories presented in the Guide—core,interdependent, partial and non-dedicated copyright industries.

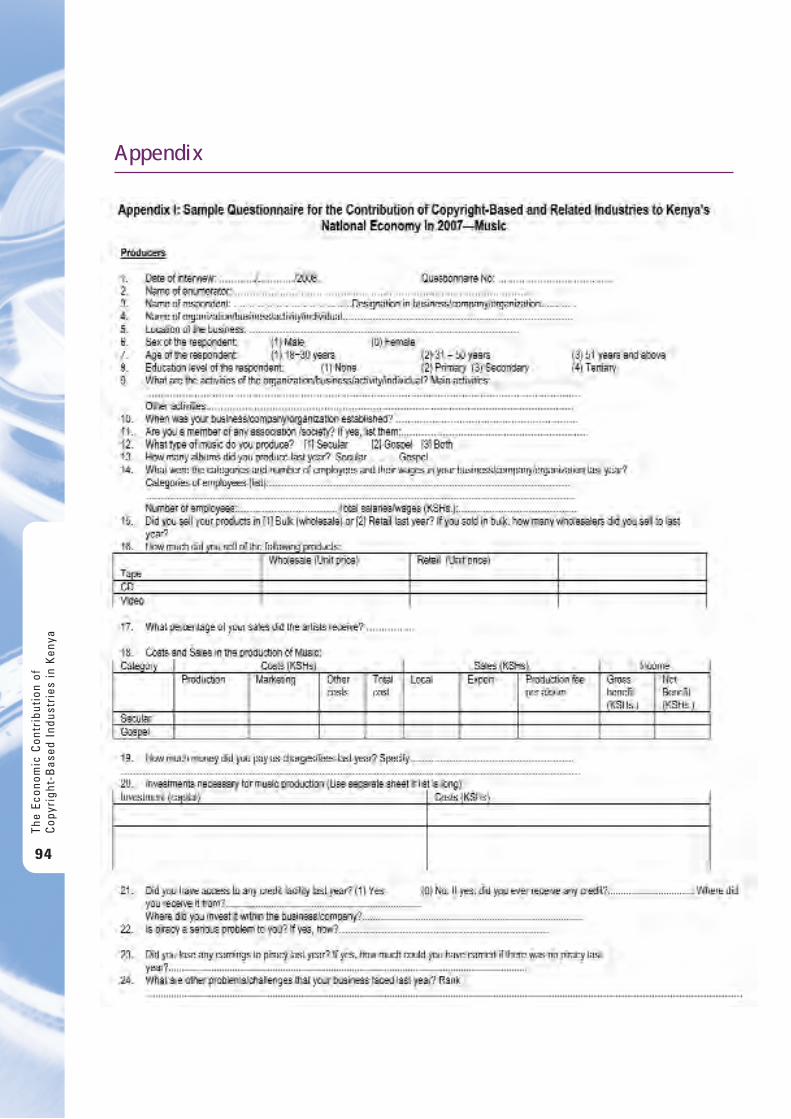

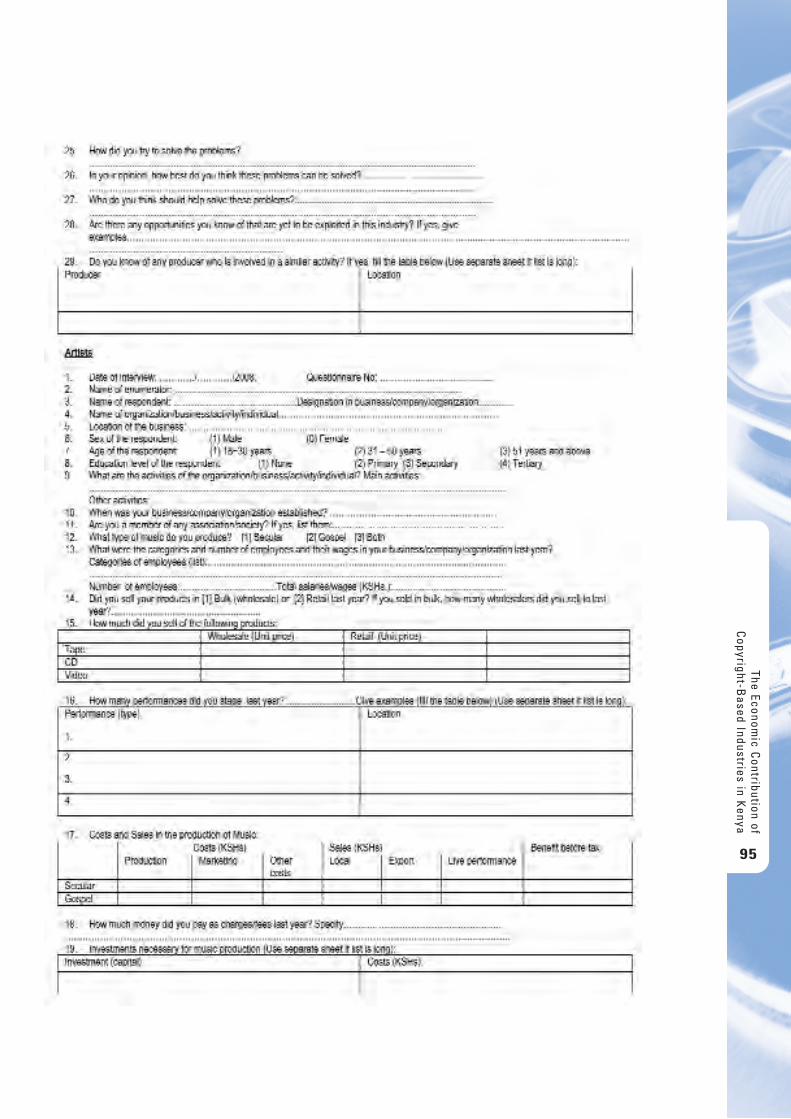

b. Based on the decision on item (a) above, data collection was undertaken. This involved compilingstatistical data by industry classes and collecting additional statistics by preparation and use ofappropriate questionnaires (see Appendix I for a sample questionnaire). The data were then disaggregatedto the required level of detail. Interviews and questionnaires were used to address specific areas.Consultations with the relevant industry sectors, through industry associations, and the relevant public-sector institutions and/or ministries were part of the process.

c. The third step was measurement and calculation of the contribution of the copyright and relatedrights-based industries studied to the national total added value, gross output, employment,employee income and foreign trade, using a selected approach under the WIPO Guide. Theestimation of the relative size of copyright and related rights-based industries covered the size ofthe copyright and related rights-based industries against macro-economic variables such as GDP,gross output and employment.

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

37

2 . C o p y r i g h t Po l i c y a n d L a w i n K e n ya

2.1 Policies Related to Creative and Copyright IndustriesEven though there have been concerted efforts recently by the Government of Kenya to develop policyfocused on creative and copyright-based industries, there has been no national policy on these industries inthe past. The absence of a National IP Policy has meant that Intellectual Property is not well mainstreamedinto the National Development policies and programmes. Its value is thus not adequately recognized bypolicymakers as an important tool for national development that needs to be promoted and protected.Because of inadequacies in the existing policies, most of the creative industries may not be operatingoptimally and therefore a lot of the contribution of these industries is treated as informal and may not becaptured by the government through taxes.

It has been shown through research that strengthening IP protection can stimulate direct foreign investments(DFI), technology transfer and increased funding for research and development. Thus, a number of recentefforts have been made by the Kenya Government that recognize the role creative and/or copyright-basedindustries play in the creation of wealth and therefore reduction of poverty. The government has proposedpolicies that favour the poor and has suggested that poverty alleviation can be achieved by strengtheningthe IP system. The government has therefore established three institutions that administer and promoteintellectual property rights (IPRs). These are the Kenya Industrial Property Institute (KIPI), which administersand promotes industrial property rights that include trademarks and patents; the Kenya Copyright Board(KCB), which is responsible for the administration of copyrights and related rights; and the Kenya PlantHealth Inspectorate Service (KEPHIS), which is responsible for the protection of new plant varieties.

The enactment of the Copyright Act 2001 by the Kenya Government is said to have contributed to arapid growth in the local music industry, and has increased income and employment opportunities. Thestrengthening of registration of industrial designs is also deemed to have had a positive role in increasingconfidence in ownership of products produced by local small and medium enterprises has both strengthenedits IP system and provided opportunities for reducing poverty.6

2.2 Copyright Law

2.2.1 The Subject Matter and Beneficiaries of Copyright LawThe copyright law is based on certain fundamental ideas about creativity and possession. It arises from thenotion that anything we create is an extension of “self” and should be protected from unauthorized use.Copyright law, however, protects only the form of expression of the ideas but not the ideas themselves.It protects the owners of the rights against those who “copy”, or those who take and use the form inwhich the original work has been expressed by the author. It therefore deals with the intellectualcreators in their creation.

Copyright protection includes every production in the literary, scientific and artistic domain whatever themode of expression. For a work to enjoy copyright protection it must be an original creation. This means

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

38

6 Otieno-Odek, J. (2007). IPRs and Poverty Alleviation. Paper Presented at a Breakfast Meeting on IPRs and Poverty Alleviation, 24 April2007, Norfolk Hotel, Nairobi.

that the work must originate from the author—it must have its origin in the labour of the author. The ideasin the work do not have to be new but the form of expression, be it literary or artistic, must be an originalcreation of the author.

2.2.2 Overview of the Kenyan Copyright LawIn Kenya, the law governing copyright is the Copyright Act 2001 (Act No. 12 of 2001) and the CopyrightRegulations of 2004, published on 18th February 2005. Kenya’s copyright law forms part of civil law, whichis designed to settle property-related and personal matters. Copyright protection law is absolute in itsstructure, establishing a negative obligation which is very similar to an ownership title in character. Thebeneficiaries of copyright protection, as in most countries, are the authors—the creators of individual,original works in literature, science and art—who are entitled to moral and economic rights.

The Copyright Act of 2001 replaced the Copyright Act Cap. 130 of Kenya, which was in force between 1st

April 1966 and 31st January 2003. As in countries like Hungary, the copyright law in Kenya has evolved over the decades in response to new challenges, some of them arising from changes in technology. TheCopyright Act Cap. 130 underwent amendments in 1975, 1982, 1989 and 1995. The Act was amended in order to update it and enhance penalties for infringement of copyright and related rights, and also toexpand the scope of protection. For instance, in 1995, the amendment extended copyright protection tocomputer programs. However, in 2001, it was repealed by Section 52 of the Copyright Act of 2001. Theprovisions of Section 51 of the Act state that “No copyright or right in the nature of copyright shall subsistotherwise than by virtue of this Act or some other enactment in that behalf”. This section expressly providesfor abrogation of common-law rights relating to copyright. The Copyright Act 2001 greatly enhancedpenalties for infringement of copyright and is now in conformity with the Trade-Related Aspects of IntellectualProperty Rights (TRIPs) Agreement, the WIPO Copyright Treaty (WCT) (1996) on the protection of the rightsof authors in literary and artistic works, and the WIPO Performance and Phonograms Treaty (WPPT) (1996).

The Copyright Act 2001 introduced several provisions aimed at making it easier to enforce. Some of theprovisions include:

1) The establishment of the Kenya Copyright Board (KCB). Having recognized the negative impacts ofpiracy in the copyright industry on the economy and on the creativity of the authors, the KCB wascreated as a corporate and autonomous body for administration and enforcement of copyright andrelated rights.

2) The appointment of copyright inspectors and prosecutors trained to enforce the Act under the KCB.3) The establishment of a databank of authors and their works to provide a point of reference for the

public and potential users of copyright works as a way of reducing piracy.4) The enhancement of penalties with imprisonment of up to 10 years and fines up to KSHs 800,000

in order to deter piracy.5) The introduction of authentication devices to distinguish genuine from pirated works.6) Registration and supervision of collective management societies to strengthen the rights holders by

bringing them together.7) The establishment of a competent authority headed by qualified personnel to adjudicate on arising issues.8) Jurisdiction to hear copyright cases, where only experienced magistrates hear and determine court cases.

The Copyright Act 2001 received the Presidential assent on 31st December 2001 and was brought intoforce without the requisite implementing regulations on 1st February 2003. Therefore, as in most

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

39

developing countries, the Kenyan Copyright Act has experienced a number of difficulties related to itsenforcement. Notable obstacles include:

1) Lack of public awareness, which has led to a thriving business in pirated works (thereby reducing legalemployment opportunities), loss of revenue to the government, and death of talent in the copyrightindustry.

2) Lack of training and awareness on the part of most rights holders. Most of the agreements assignedeither for licensing or assignment of copyright do not satisfy the legal requirements to be admissible in court.

3) Lack of training on the part of enforcement officers on copyright laws, implying lack of knowledge on how to gather relevant evidence and lack of awareness of seriousness of copyright infringement.

4) Evidentiary rules requiring detailed and complicated proof of copyright and copyright ownership forcreative works cause unwarranted loss of time, effort and money by the rights holder.

5) Lack of intellectual property expertise is another difficulty faced in enforcing copyright infringements. 6) Lack of intellectual property policy has meant that intellectual property is not mainstreamed into

national development.7) Weak coordination among enforcement agencies.8) It is often difficult to prove the amount of actual damage suffered by the rights holder. 9) High cost of litigation renders rights holders unable to instruct advocates to represent them in court

in case of infringement of their rights.8) Legal procedures to obtain information from or about infringers are missing. The ability to obtain

information necessary to detect and detain all actors in the distribution chain and to identify thesources of supply of illegal goods is important if piracy is to be fought effectively.

9) There are emerging issues in enforcement with the advancement of technology. For example, piracyhas taken a new dimension and has become more sophisticated and lucrative. This has led to the tradein pirated materials becoming a very attractive business.

2.2.3 Economic Considerations of the Kenyan Copyright LawCopyright constitutes an essential element in the economic development process of Kenya. As is always thecase with other countries, some people in Kenya possess the natural gift of intellectual creation more thanothers. Protection under the Kenyan copyright law encourages them to create further works, thus enrichingKenya’s store of literature, music and art, as well as promoting economic development. Certainly, theoverwhelming numbers of authors of creative works are interested in having some control over how theircreations are used and in reaping some economic benefits from that use. This aspect of the Kenyancopyright law as a stimulus for intellectual creativity is of fundamental importance.

In addition, the considerable investments which are sometimes necessary for the creation anddissemination of works of the mind will be more easily obtainable if effective protection exists under the law. In some sectors, for instance book-printing, film-making and record manufacturing, such legalprotection is in fact indispensable—it is simply not possible to engage in these expensive activities if nosatisfactory legal protection exists which gives the possibility to take action against those who use theproducts without permission.

Furthermore, if the copyright protection exists in a work, the author is encouraged not only to create thework but also to make it public and disseminate it widely, because he knows that he will not lose controlover it simply because it is made known to others. Such a wide dissemination of works is generally of greatbenefit for the society as a whole.

An author’s work is generally the personal expression of his thoughts and of his personality and he shouldtherefore be able to claim respect for it—that is, to decide whether, when and how his work may be

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

40

reproduced and performed in public and also to object to any distortion or mutilation of the work when it is used. Such protection is granted under the law on copyright (moral rights).

Finally, the works of the authors of a country enable the country’s manners, customs and cultural heritageto become better known both inside and outside the country. Consequently, any country wishing tostimulate and inspire its own authors in their creativity must necessarily provide for copyright protection.(For more on Kenya’s copyright law, see Appendix II.)

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

41

3 . C o p y r i g h t - b a s e d I n d u s t r i e s i n K e n ya

3.1 Composition of Copyright-Based IndustriesAs alluded to earlier, copyright-based industries include all the activities and industries that produce works(creations) protected by the copyright law and the industries that consume or utilize such products. Thecopyright law ensures that the rights of those engaged in creations in copyright and related industries areprotected and that the creator of such works benefits both morally and financially from the consumption ofworks they have created.

The creation of works under the protection of copyright law presents a starting point in terms of economicweight and effect of copyright. The creation of copyright-protected works is essentially associated with otheractivities that increase added value. The consumption of literary and artistic creations and works cannot bepossible without interposing certain associated activities (e.g. wrapping, copying, distribution, etc.).

The law covers creative works such as the activities of writers, authors, software designers, etc. Theseactivities are important factors in the economic development of nations worldwide, Kenya included. Apartfrom meeting social and cultural functions, the production of these works is key to enhancing economicvalue through generating added value.

3.2 Types of Copyright-Based IndustriesThe methodological guide published by WIPO (2003) distinguishes four main categories of copyright-basedindustries depending on the type of association to copyright. They are:

I Core copyright-based industries.II Interdependent copyright-based industries.III Partial copyright-based industries.IV Non-dedicated support industries.

Creations and works protected by the copyright law do not carry equal weight in different sectors of theeconomy. There are those that are totally based on copyright-protected creative works. These include,according to the WIPO Guide, core copyright-based industries and interdependent copyright-basedindustries. In other sectors, copyrighted creations are only partly represented or have no role to play at all.These include partial and non-dedicated copyright-based industries.

3.2.1 Core Copyright-Based IndustriesCore copyright-based industries are industries fully engaged in the creation, manufacturing and production,performance, broadcasting and communication, and exhibition or distribution and sale of works and othercreations under the scope of copyright. They are areas in the economy whose activities are based on worksprotected by copyright and related rights. They form the core of copyright-based industries and activities inthem are almost exclusively associated with creations protected by copyright, hence their full activities andperformance are taken into consideration when establishing the economic contribution of copyright-basedindustries. The following industries fall into this category according to the WIPO Guide:

i. Press and literature.ii. Music, theatrical productions and opera.

The

Econ

omic

Con

trib

utio

n of

Cop

yrig

ht-B

ased

Ind

ustr

ies

in K

enya

42

iii. Motion pictures and video.iv. Radio and television.v. Photography.vi. Software and databases.vii. Visual and graphic arts.viii. Advertising.ix. Copyright collecting societies.

3.2.2 Interdependent Copyright-Based IndustriesThe interdependent copyright-based industries are defined by the WIPO Guide (2003) as “industries that are engaged in production, manufacture and sale of equipment whose function is wholly or primarily tofacilitate the creation, production or use of works and other protected subject matter.” These industrieswholly depend on core copyright industries for existence.

This category of industries includes:

i. Manufacture, wholesale and retail of TV sets, radios, VCRs, CD players, DVD players, electronic game equipment and other similar equipment.

ii. Manufacture, wholesale and retail (sales and rental) of computers and equipment.iii. Manufacture, wholesale and retail (sales and rental) of musical instruments.iv. Manufacture, wholesale and retail (sales and rental) of photographic

and cinematographic instruments.v. Manufacture, wholesale and retail (sales and rental) of photocopiers.vi. Manufacture, wholesale and retail of blank recording materials.vii. Manufacture, wholesale and retail of paper.

3.2.3 Partial Copyright-Based IndustriesIndustries in which only a specific proportion of their production is associated with products protected bycopyright and related rights are referred to as partial copyright-based industries. The ratio is indicated by a copyright factor which shows what percentage of the product is under protection of copyright. Thefollowing industries fall under this category, according to the WIPO Guide (2003):

i. Apparel, textiles and footwear.ii. Jewellery and coins.iii. Other crafts.iv. Furniture.v. Household goods, china and glass.vi. Wall coverings and carpets.vii. Toys and games.viii. Architecture, engineering, surveying.ix. Interior design.x. Museums.

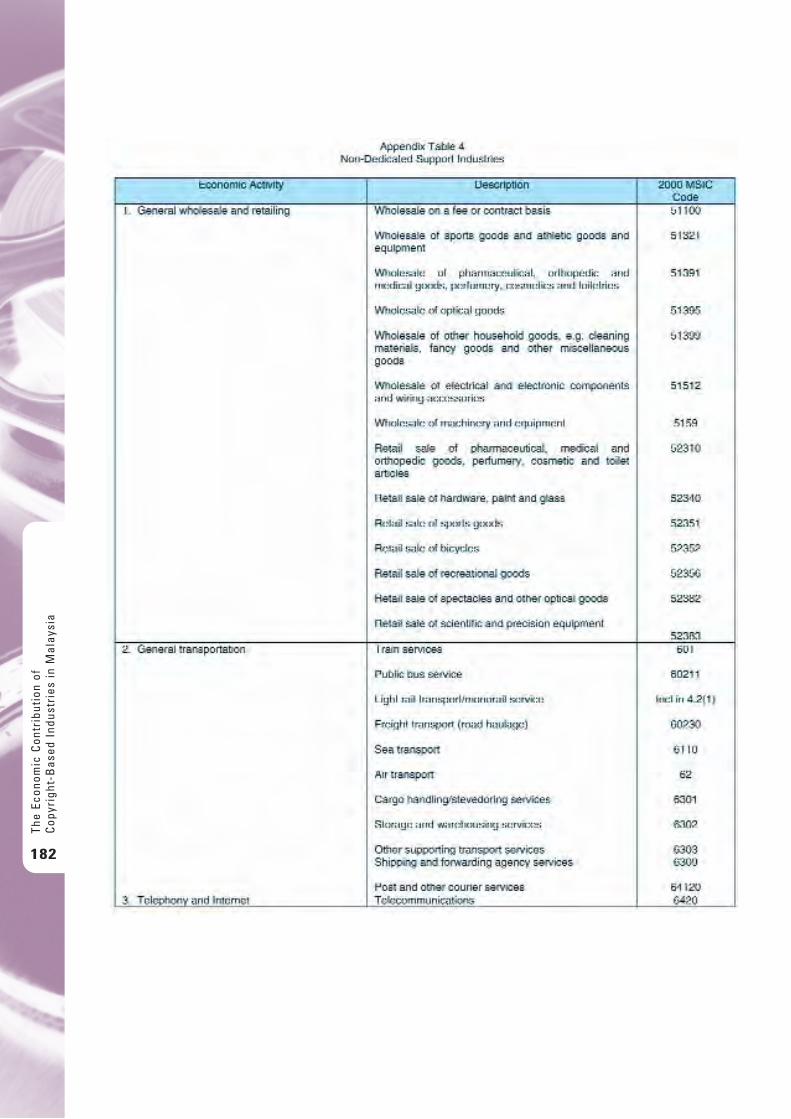

3.2.4 Non-Dedicated Support IndustriesThe non-dedicated support industries are those in which a portion of their activities is related to facilitatingbroadcast, communication, distribution and sale of products and works and other protected subject matter.The following industries fall under this category according to the WIPO Guide (2003):

The Economic C

ontribution ofC

opyright-Based Industries in K

enya

43

i. General wholesale and retailing.ii. General transportation.iii. Telephony and internet.

3.3 Comparison of Industry Classification for Kenya with the WIPO GuideTable 1 summarizes all the copyright-based industries included in the Kenyan survey. The industries weredetermined according to the WIPO Guide but taking into account the specific characteristics of the Kenyanstatistical system.