Embed Size (px)

Citation preview

LIST OFTABLES

TABLENO

TITLE PAGENO

4.1 Net working capital of Travancore sugars and chemicals from 2006-2007 to 2010-2011

4.2 Current ratio of Travancore sugarsand chemicals

4.3 Quick ratio of Travancore sugars and chemicals

4.4 Absolute liquidity ratio of Travancore sugars and chemicals

4.5 Working capital turnover ratio of Travancore sugars and chemicals

4.6 Debtors turnover ratio of Travancore sugars and chemicals

4.7 Debtors collection period of Travancore sugars and chemicals

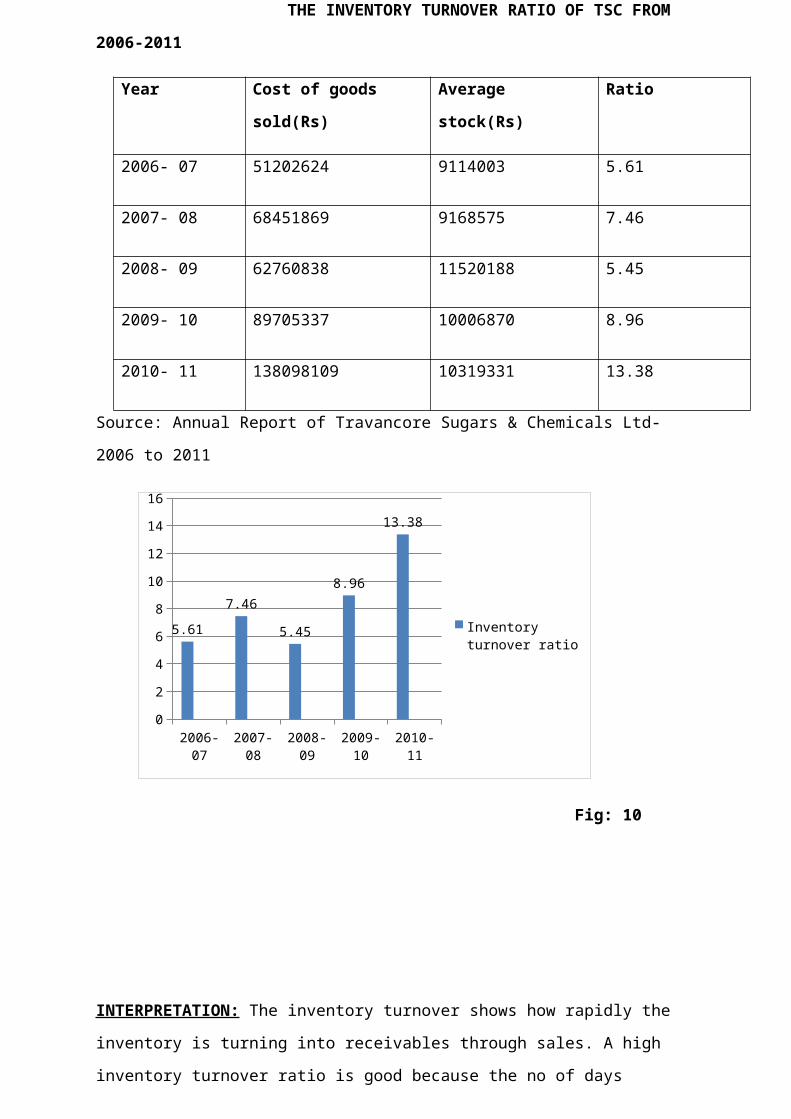

4.8 Inventory turnover ratio of Travancore sugars and chemicals

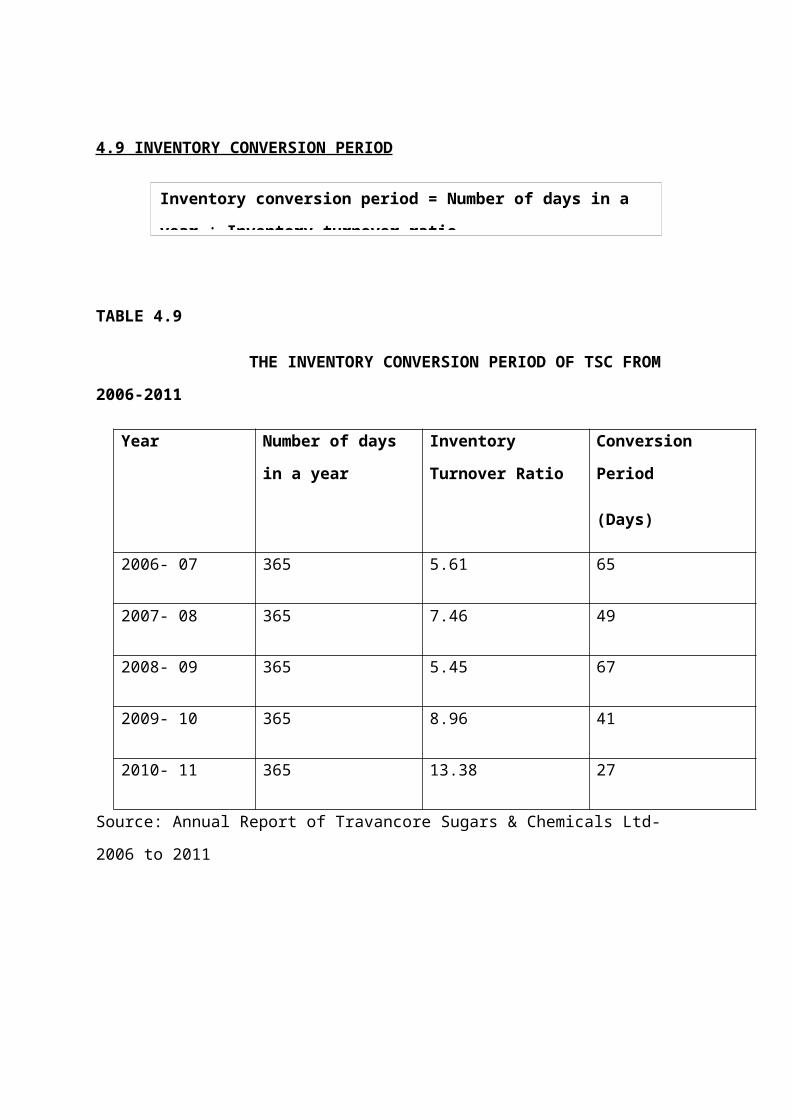

4.9 Inventory conversion period of Travancore sugars and chemicals

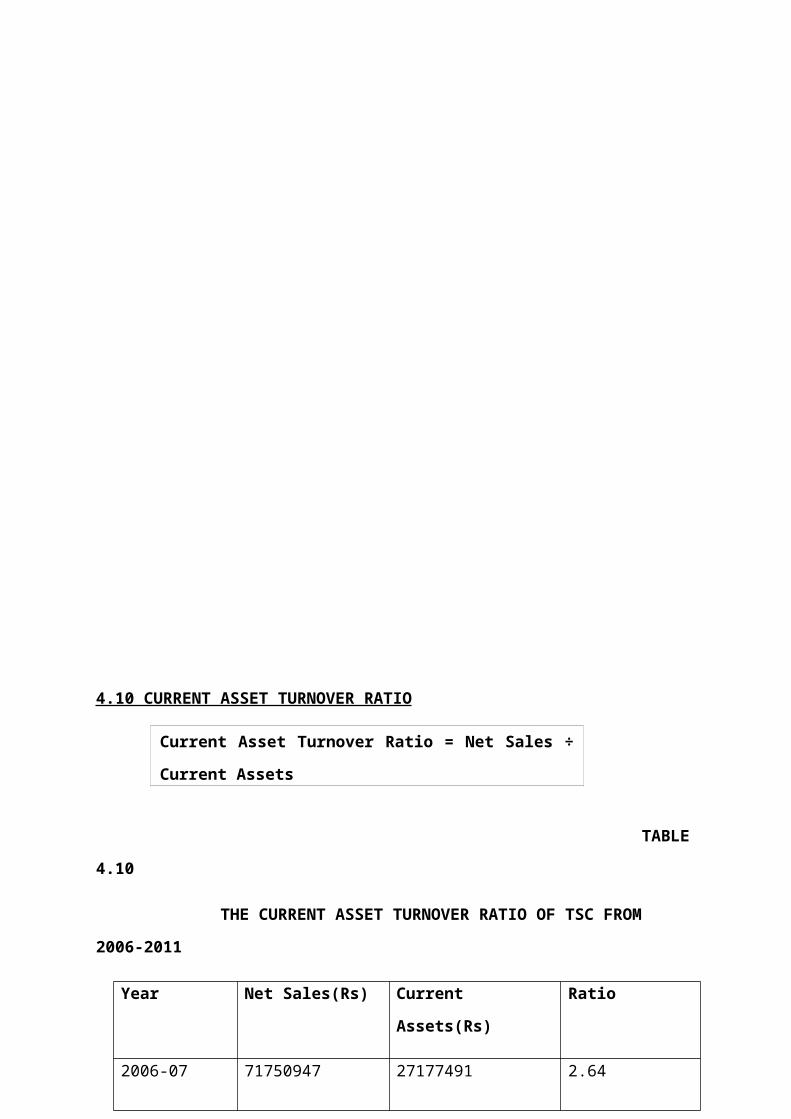

4.10 Current asset turnover ratio of Travancore sugars and chemicals

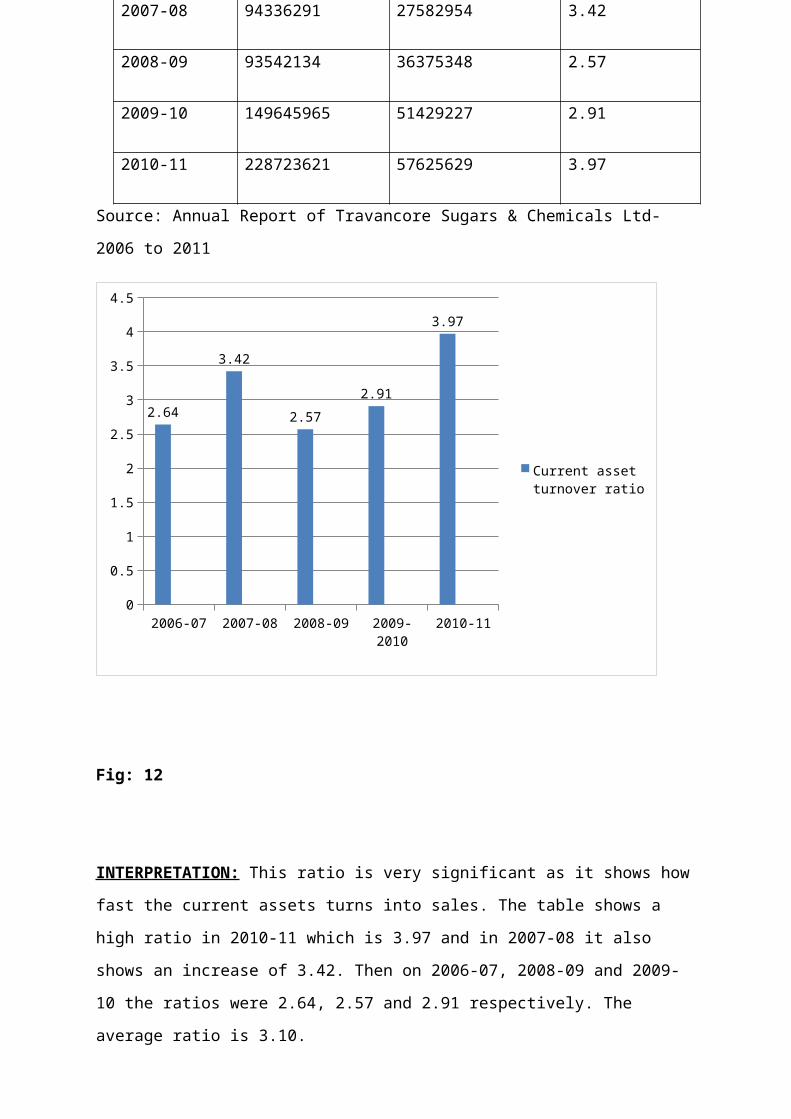

4.11 Creditors turnover ratio of Travancore sugars and chemicals

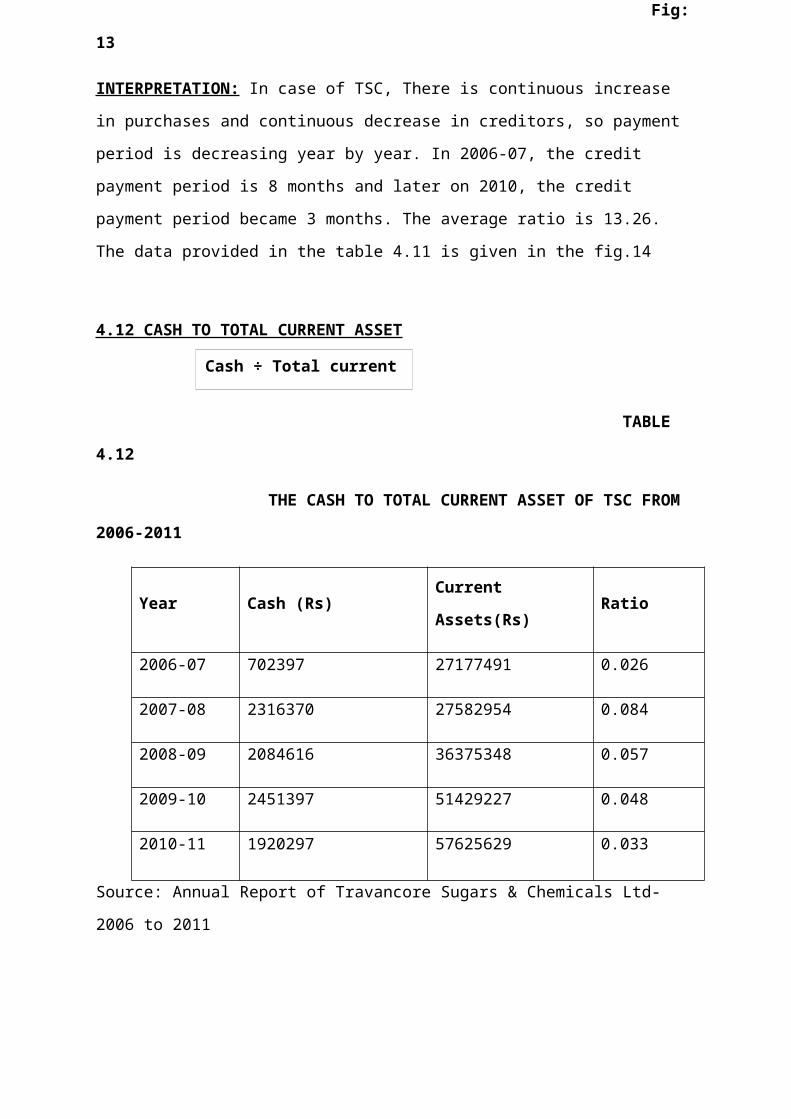

4.12 Cash to total current asset of Travancore sugars and chemicals

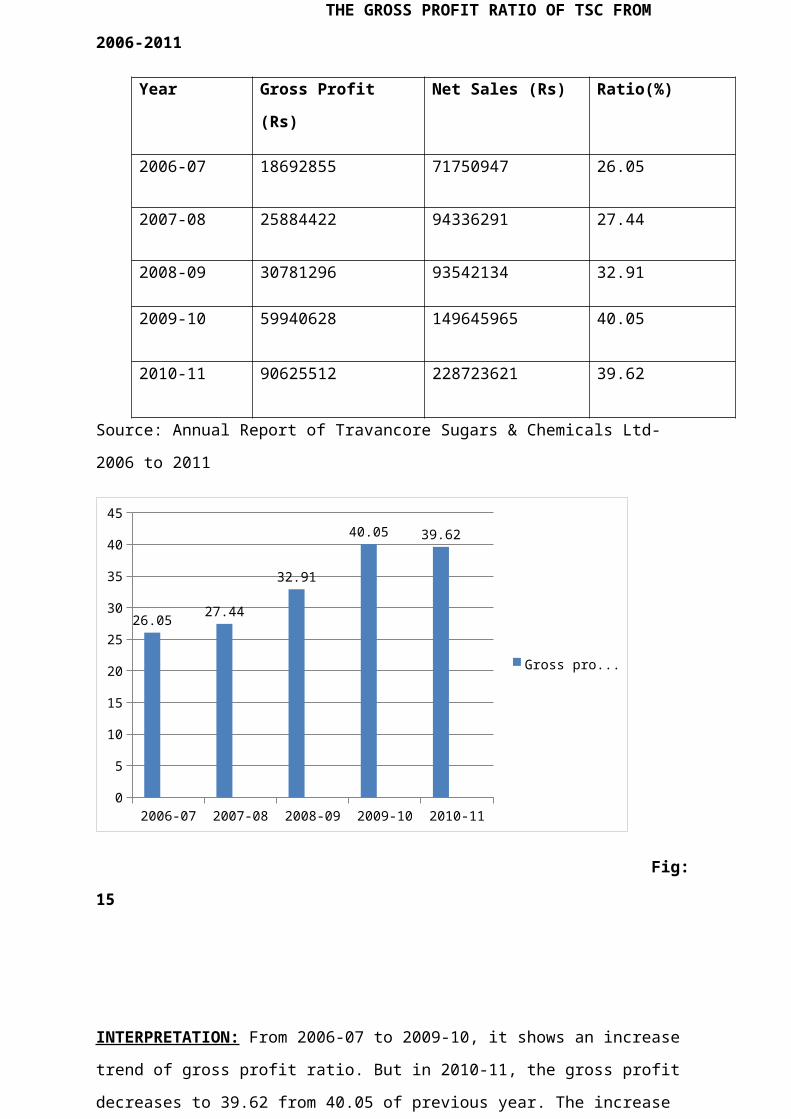

4.13 Gross profit ratio of Travancore sugars and chemicals

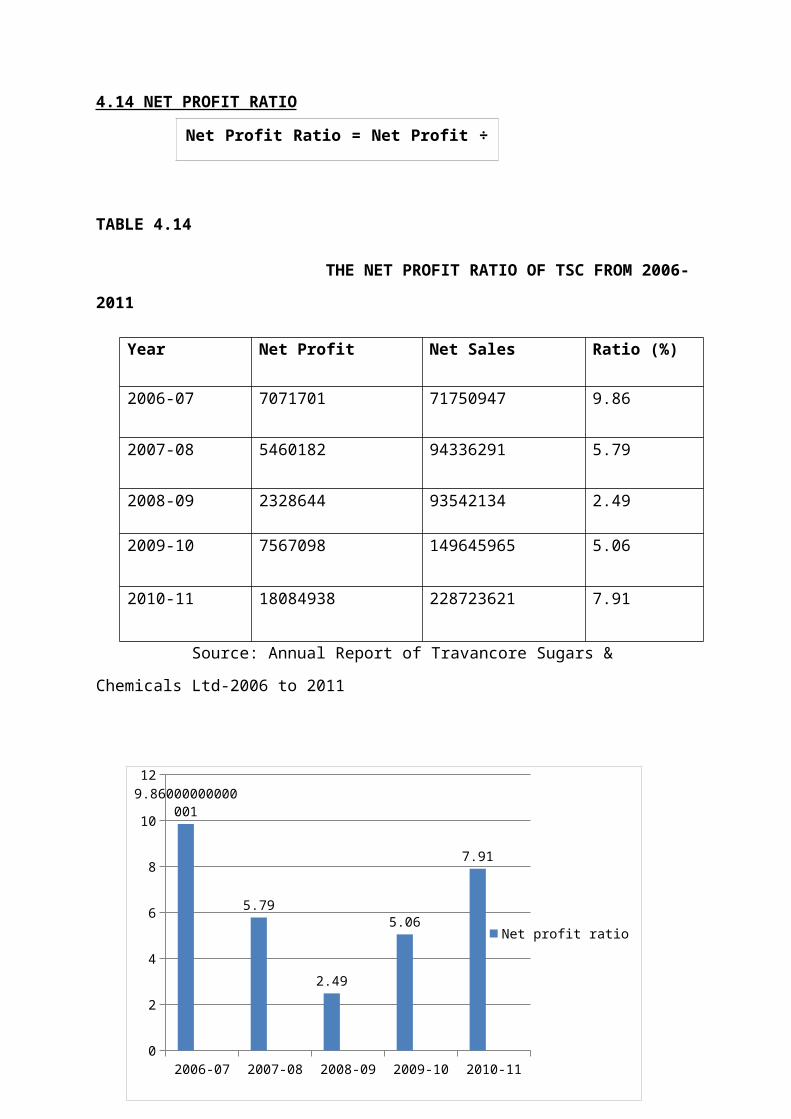

4.14 Net profit ratio of Travancore sugars and chemicals

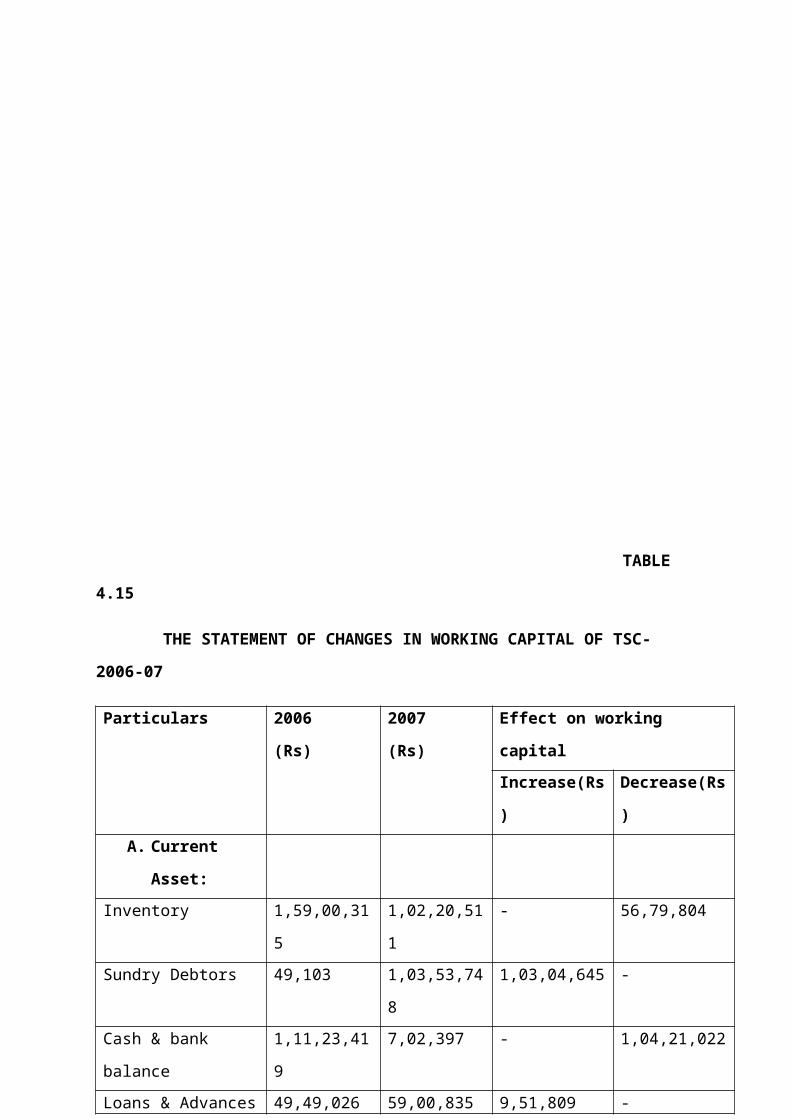

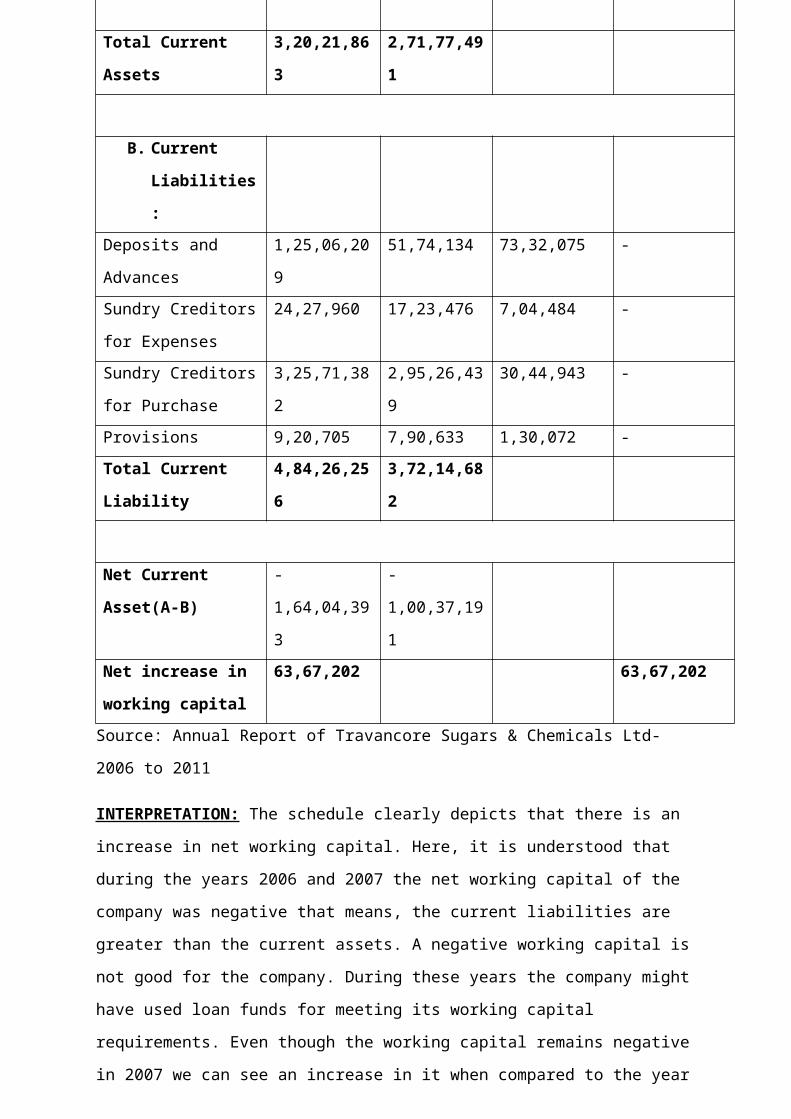

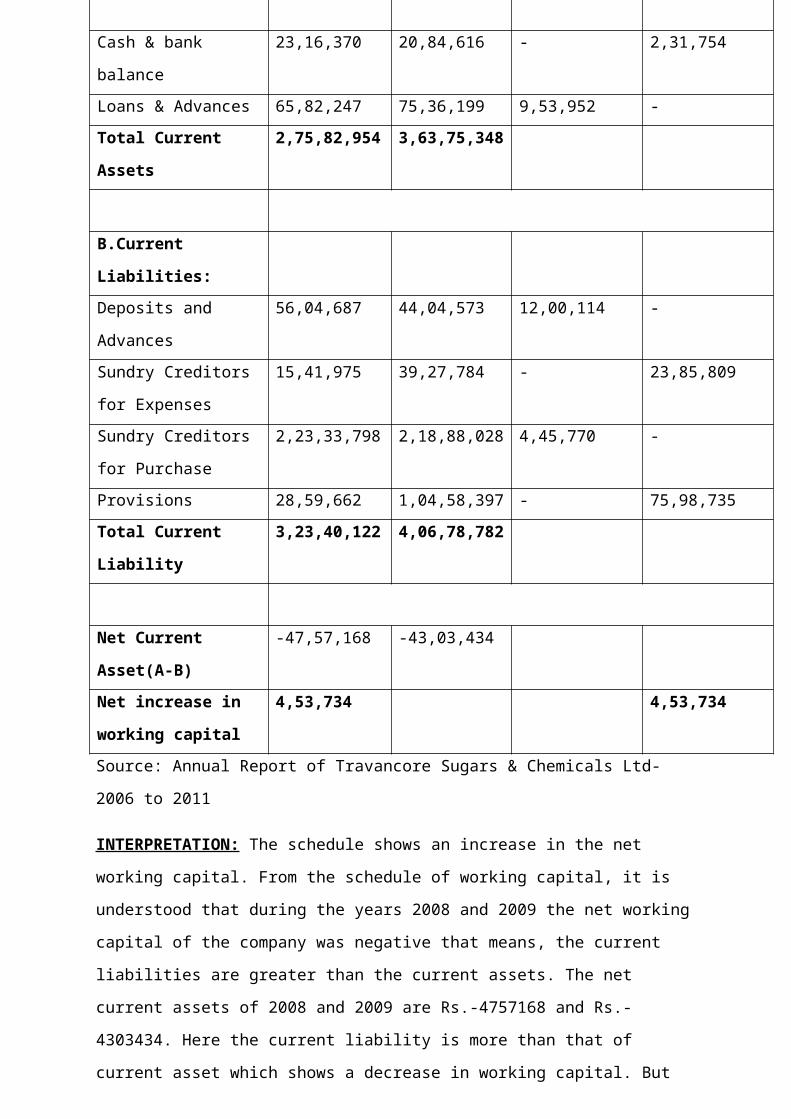

4.15 Statement of change in working capital for the year 2006-2007

4.16

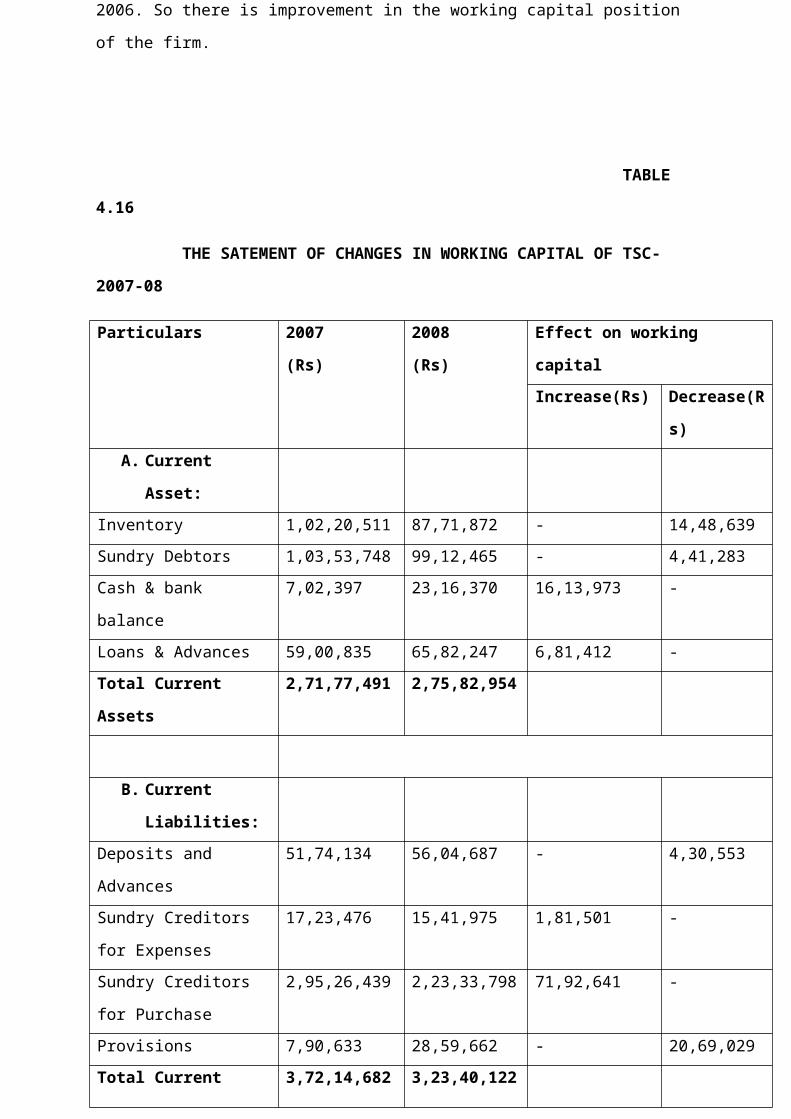

Statement of change in working capital for the year 2007-2008

4.17

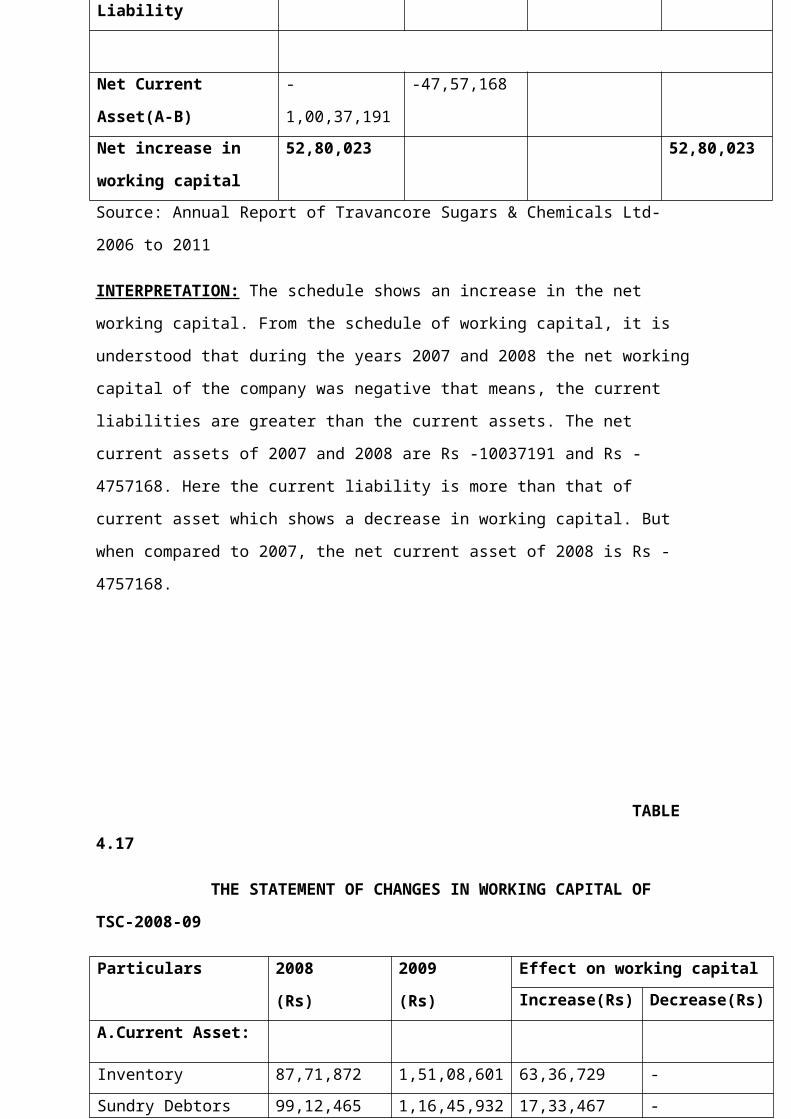

Statement of change in working capital for the year 2008-2009

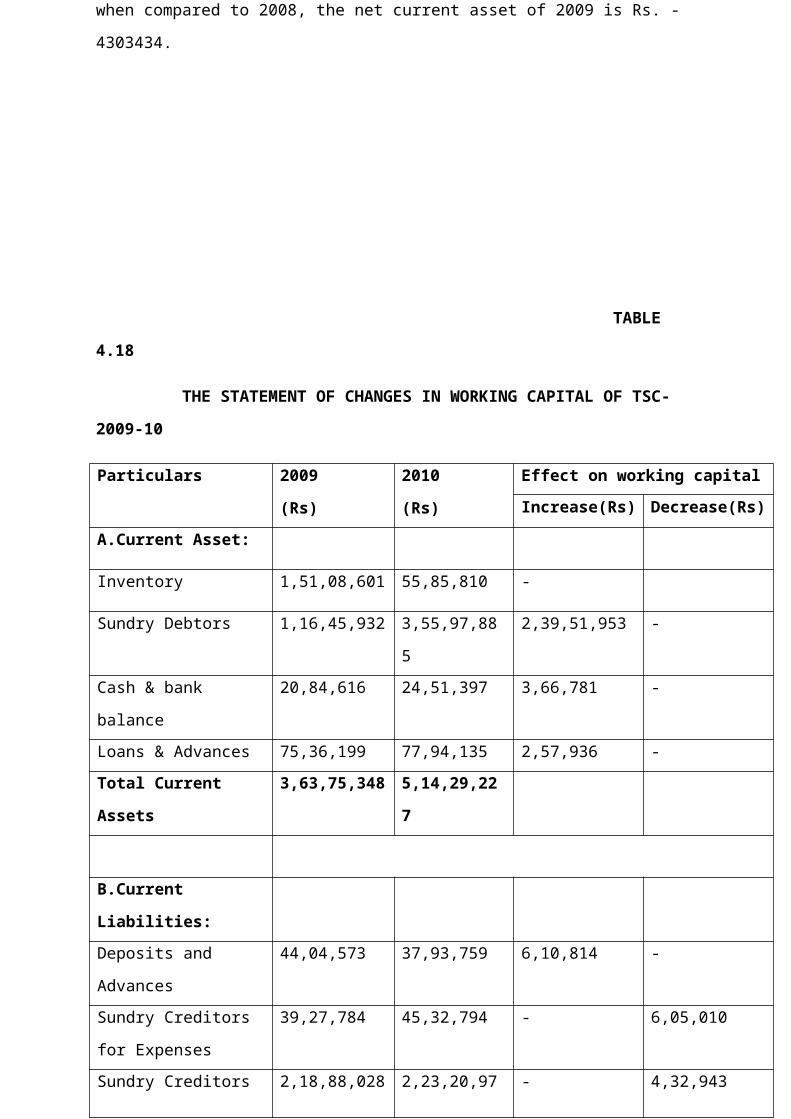

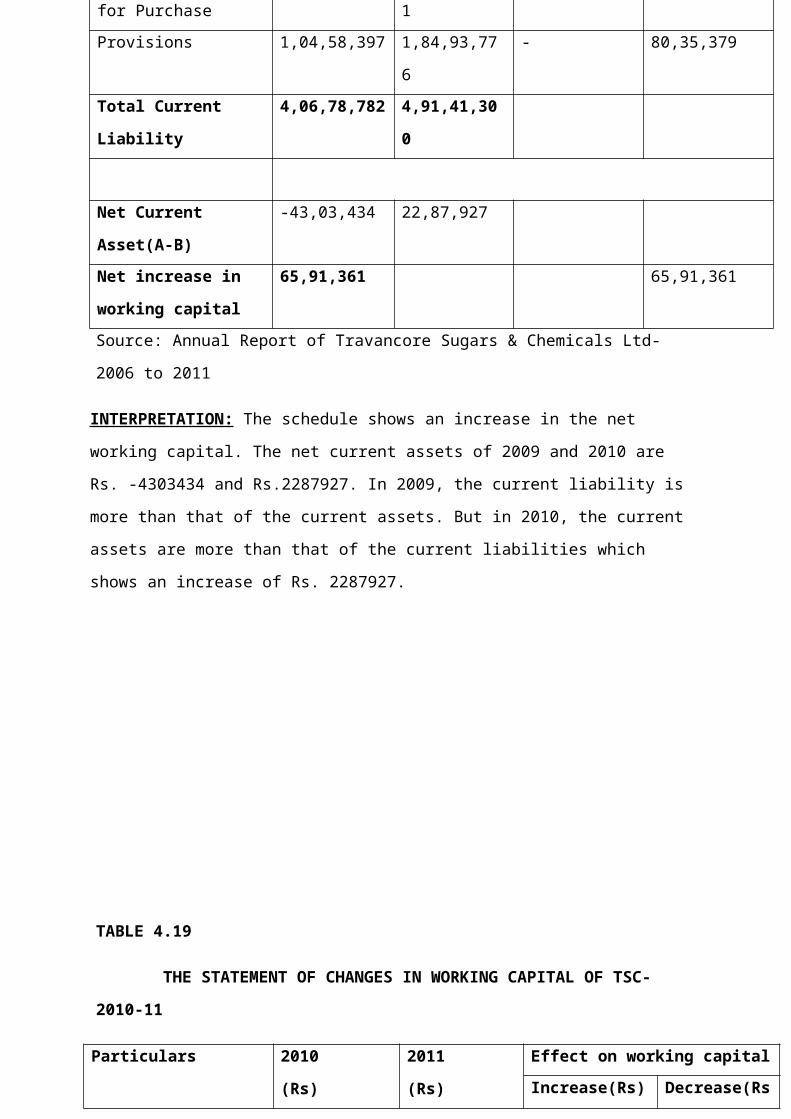

4.18

Statement of change in working capital for the year 2009-2010

4.19

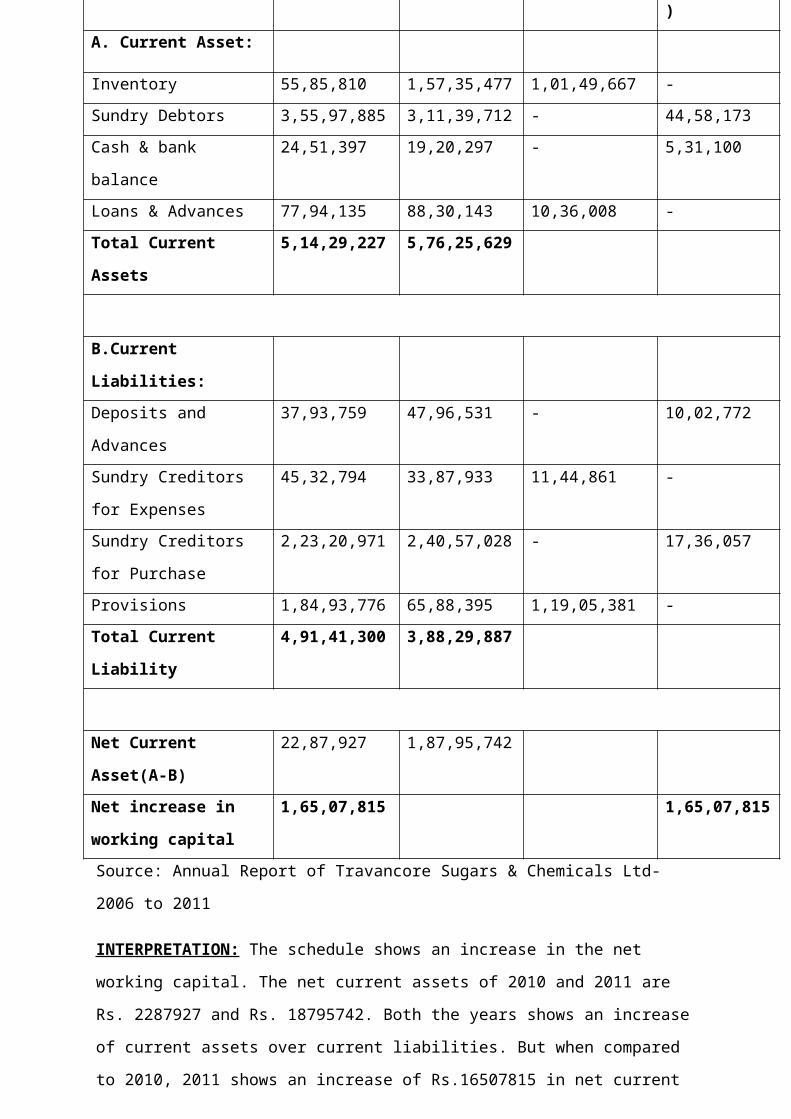

Statement of change in working capital for the year 2010-2011

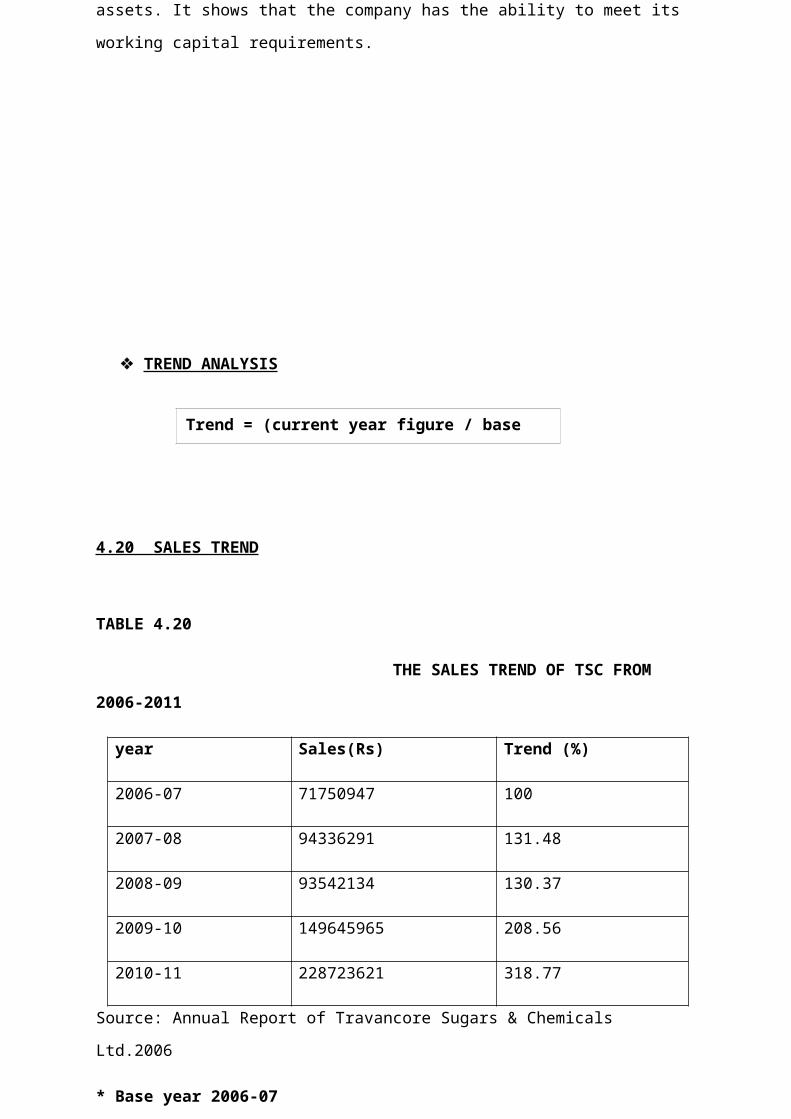

4.20

Sales Trend of Travancore sugars and chemicals

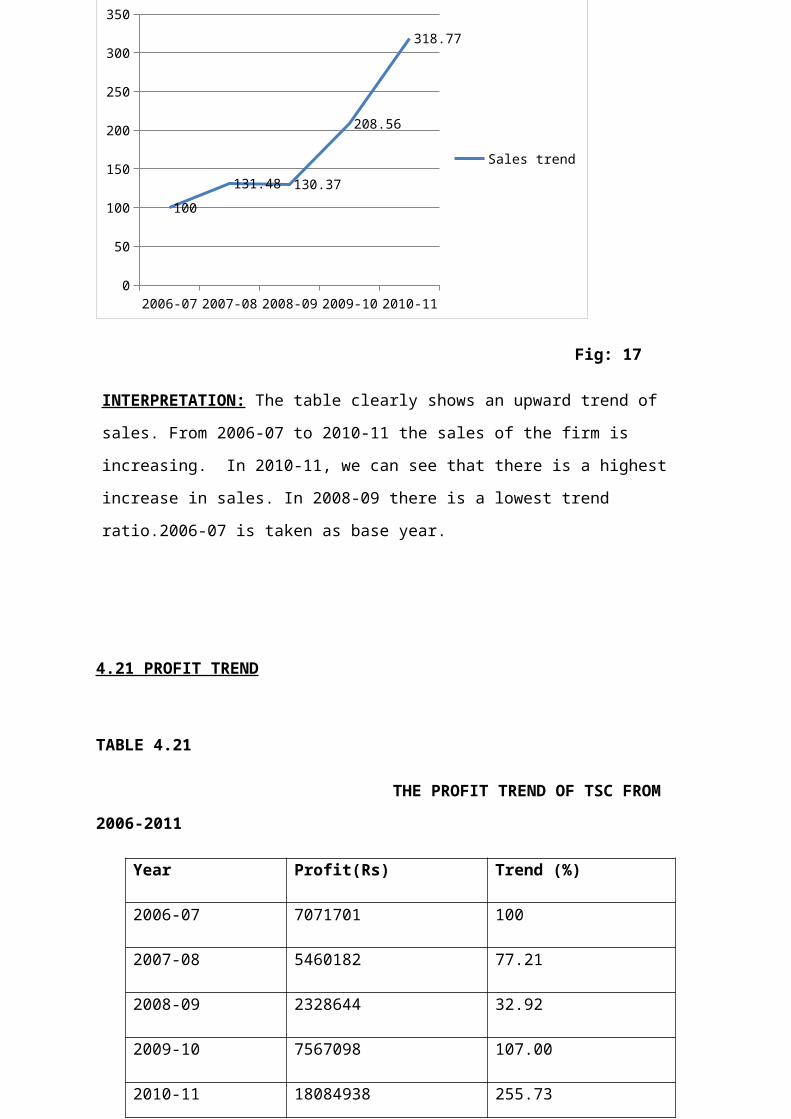

4.21

Profit Trend of Travancore sugars and chemicals

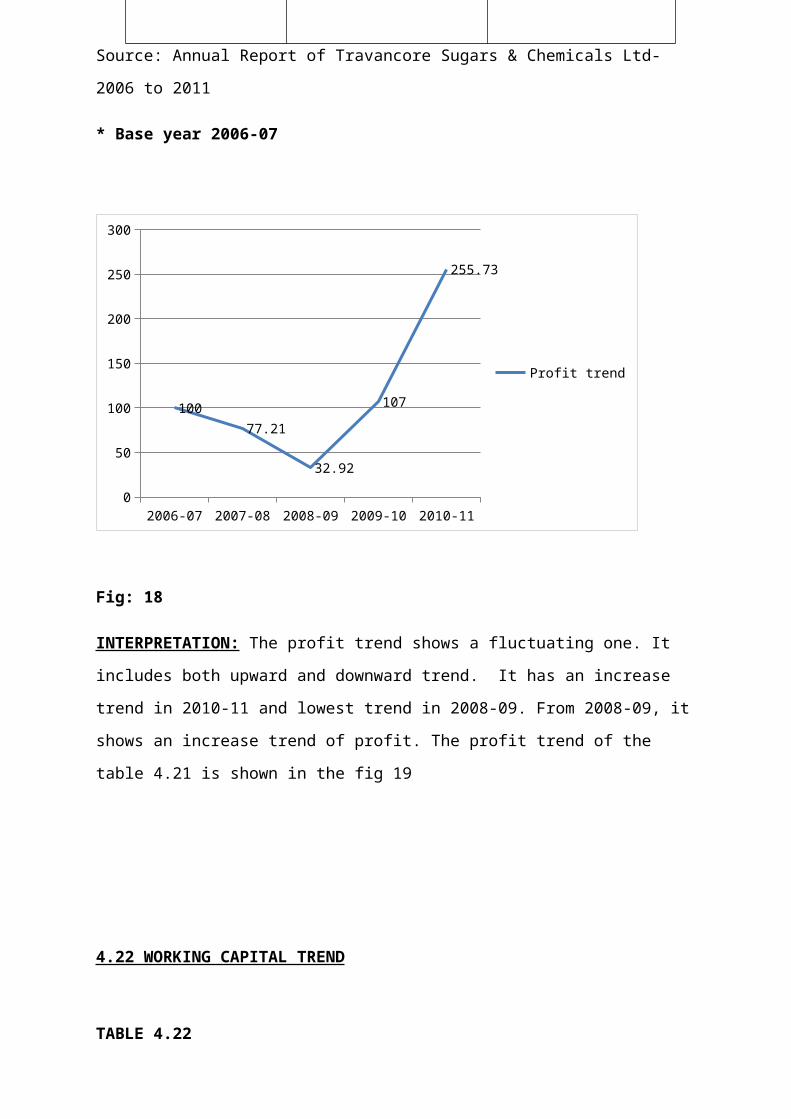

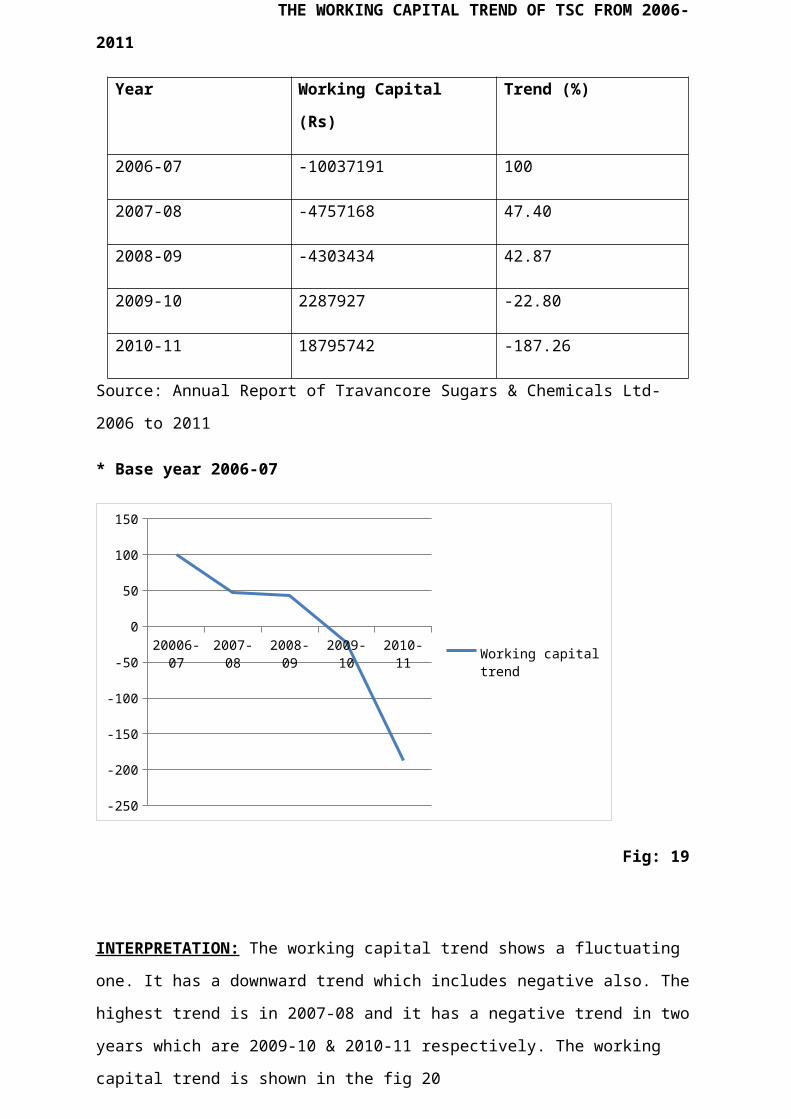

4.22

Working Capital Trend of Travancore sugars and chemicals

4.23

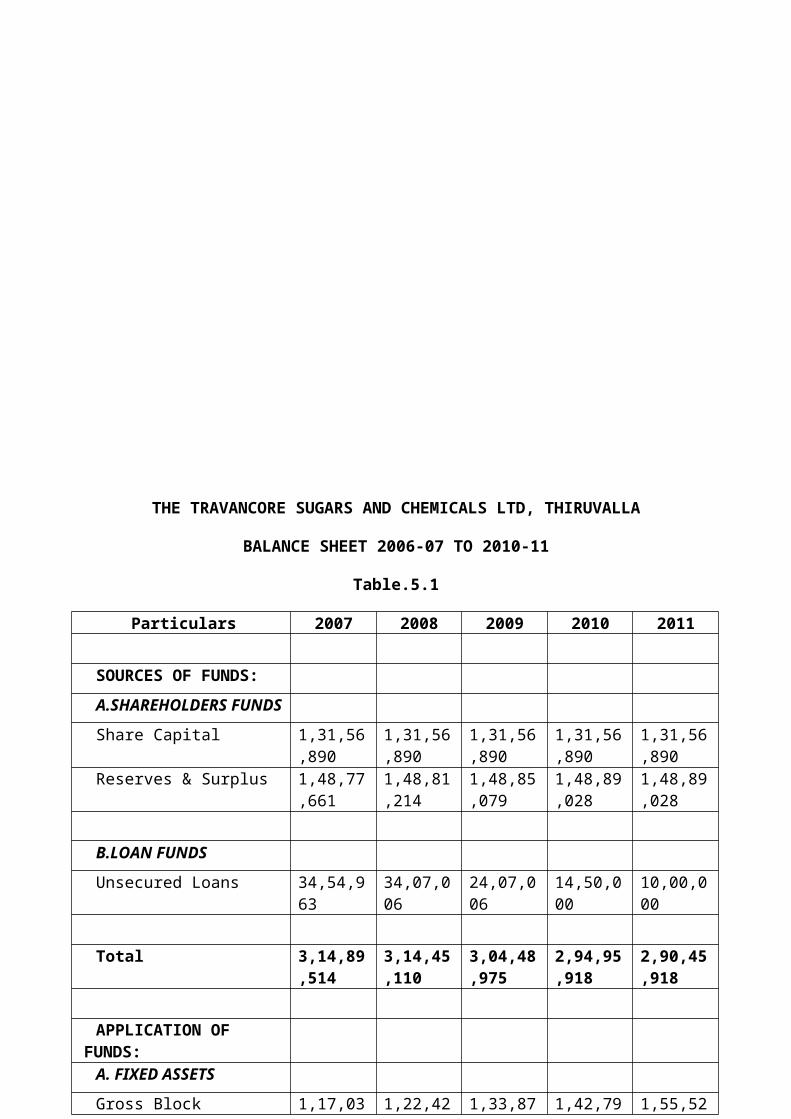

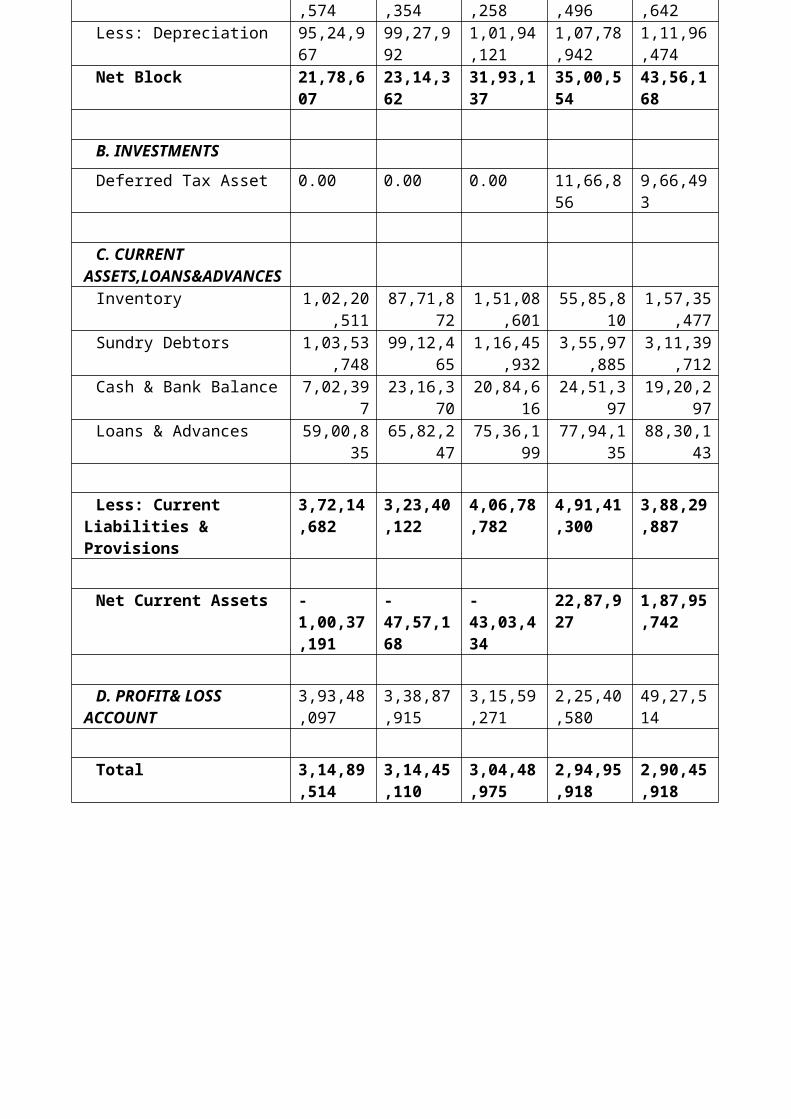

Balance sheet of the year 2006-2007 to 2010-2011

4.24

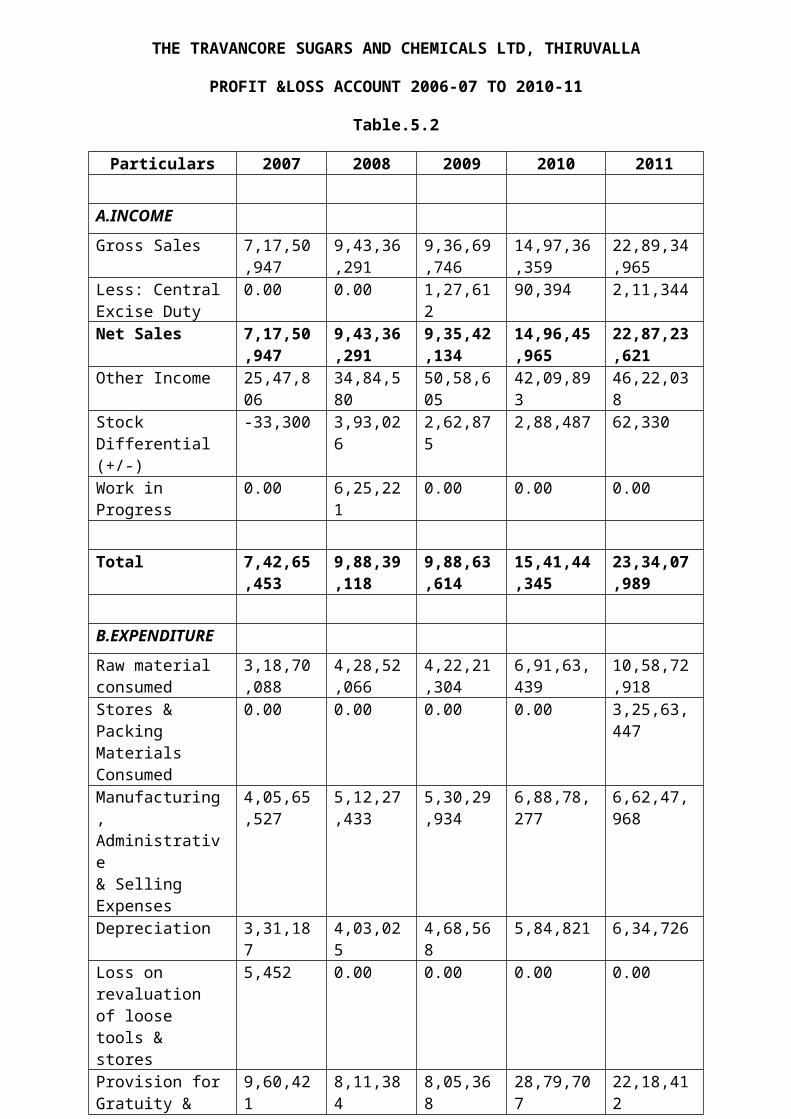

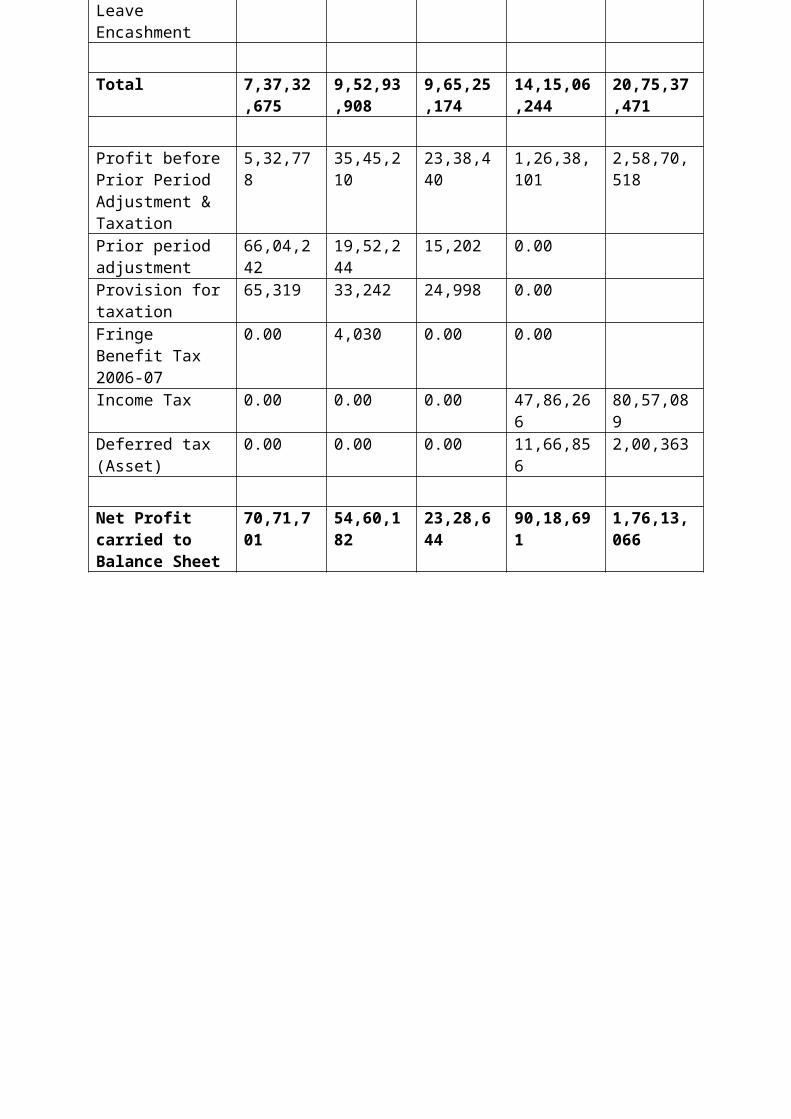

Profit and loss account of year 2006–2007 to 2010-2011

LIST OF FIGURES

FIGURENO

TITLE PAGENO

1 Organizational Chart Of Travancore Sugars And Chemicals

2 Structure Of Finance Department Of Travancore Sugars And Chemicals

3 Graph Showing Net Working Capital

4 Graph Showing Current Ratio

5 Graph Showing Quick Ratio

6 Graph Showing Absolute Liquidity Ratio

7 Graph Showing Working Capital Turnover Ratio

8 Graph Showing Debtors Turnover Ratio

9 Graph Showing Debts Collection Period

10 Graph Showing Inventory Turnover Ratio

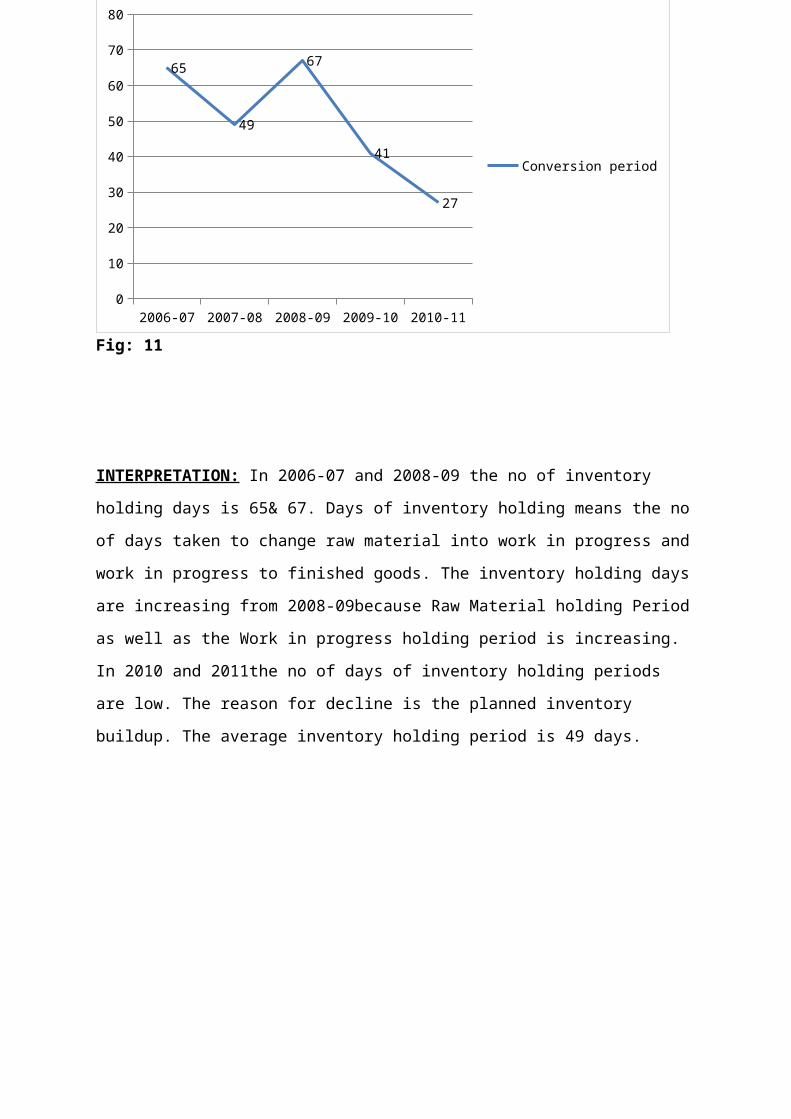

11 Graph Showing Inventory Conversion Period

12 Graph Showing Current Asset Turnover Ratio

13 Graph Showing Creditors Turnover Ratio

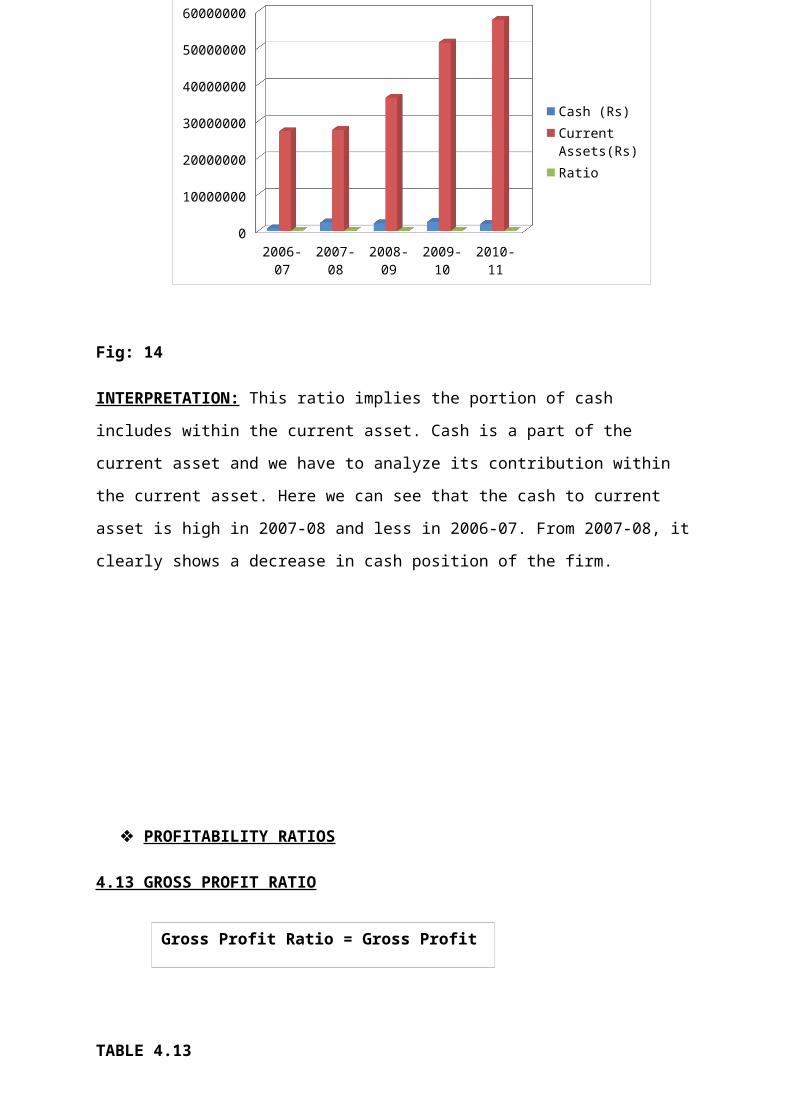

14 Graph Showing Cash To Total Current Asset

15 Graph Showing Gross Profit Ratio

16 Graph Showing Net Profit Ratio

17 Graph Showing Sales Trend

18 Graph Showing Profit Trend

19 Graph Showing Working Capital Trend

ABBREVIATIONS

1. IMFL: INDIAN MADE FINE LIQUOR .2. KSBC :KERALA STATE BEVERAGE CORPORATION LTD.

3. NWC :NET WORKING CAPITAL

4. WC : WORKING CAPITAL

5. RMCP : RAW MATERIAL CONVERSION PERIOD

6. WIPCP : WORK IN PROGRESS CONVERSION PERIOD

7. FGCP : FINISHED GOODS CONVERSION PERIOD

8. ICP : INVENTORY CONVERSION PERIOD

9. RCP : RECEIVABLES CONVERSION PERIOD

10.PAYABLES (PDP) : PAYABLES DEFERRAL PERIOD

11.NOC : NET OPERATING CYCLE

12.GOC : GROSS OPERATING CYCLE

13.K.R.S : KERALA ROADWAYS TRANSPORT LTD

14.TSC :TRAVANCORE SUGARS AND CHEMICALS

CHAPTER 1

INTRODUCTION TO THE STUDY

CHAPTER 1

INTRODUCTION

1.1 INTRODUCTION

A business undertaking requires funds for two

purposes: -

To create productive capacities through purchase of fixed

assets, etc.

To finance current assets required for day to day running

of the business.

Working capital refers to the funds invested in current

assets i.e., investment in stock, sundry debtors, cash

and current assets. Current assets are essential to use

fixed assets profitably. For example a machine cannot be

used without providing necessary raw materials. It is

obvious that a certain amount of funds is always tied up

in raw material inventories working progress, finished

goods, consumable stores, sundry debtors and day-to-day

cash requirements. However, the business also enjoys

credit facilities from his suppliers who may give the raw

materials on credit. Similarly a businessman may not pay

immediately for various expenses. But labours are paid

periodically. Therefore certain amount of funds is

automatically available to finance the current assets

requirements. However, the requirements for current

assets are usually greater than the amount of funds

available through current liabilities. In other words,

the current assets are to be kept at higher level than

the current liabilities. This difference is known as

working capital.

Working Capital Management is significant in financial

management due to the fact that it plays a vital role in

keeping the wheel of the business running. Every business

requires capital, without which it cannot be promoted. It

holds exceptional importance in the case of a

manufacturing company. It also covers various concepts

like inventory management, cash management, credit policy

etc. Working capital is the heart of the business. If it

is weak, business cannot prosper and survive. It is

therefore said the fate of large scale investment in

fixed assets is often determined by a relatively small

amount of current assets. As the working capital is

important to the company is important to keep adequate

working capital with the company. Cash is the lifeline of

company. If this lifeline deteriorates so the company’s

ability to fund operation, reinvest do meet capital

requirements and payment. Understanding company’s cash

flow prospects is to look at its working capital

management. This study is undertaken to find out

efficiency of working capital management of Travancore

Sugars And Chemicals Ltd., Valanjavattom.

1.2 OBJECTIVES OF THE STUDY

To identify the financial strength and weakness of

Travancore Sugars And Chemicals Ltd.

To study the performance of beverage industry in general and

Travancore Sugars And Chemicals Ltd. in particular

To study the liquidity and solvency position of Travancore

Sugars And Chemicals Ltd.

To study the cash management practices of Travancore Sugars

And Chemicals Ltd.

To study the receivable management practices of Travancore

Sugars And Chemicals Ltd.

To examine the inventory management of Travancore Sugars And

Chemicals Ltd.

1.3 SCOPE OF THE STUDY

The study of working capital is of major

importance to the internal and external analysis because of

its close relationship with the current day to day operations

of a business. To meet the current requirements of a business

enterprise such as the purchases of services, raw materials

etc. working capital is essential. It is also pointed out that

working capital is nothing but one segment of the capital

structure of a business.

In this study, the working capital management of

the company is analyzed and conclusions and suggestions are

drawn from it in order for the betterment of the company.

1.4 RESEARCH METHODOLOGY

Research methodology is a way to

systematically solve the research problem. It may be

understood as a science of studying how research is done

scientifically. In it we study the various steps that are

generally adopted by a researcher in studying his research

problem along with the logic behind them. It is necessary for

the researcher to know not only the research

methods/techniques but also the methodology. Researchers not

only need to know how to develop certain indices or tests, how

to calculate the mean, the mode, the median or the standard

deviation or chi-square, how to apply particular research

techniques, but they also need to know which of these methods

or techniques, are relevant and which are not, and what would

they mean and indicate and why. Researchers also need to

understand the assumptions underlying various techniques and

they need to know the criteria by which they can decide that

certain techniques and procedures will be applicable to

certain problems and others will not. All this means that it

is necessary for the researcher to design his methodology for

his problem as the same may differ from problem to problem.

1.4.1 METHODS FOR DATA COLLECTION

The collection is the process of enumeration together with the proper recording of results. The

success of an enquiry is based up on the proper collection of

data. The data may be classified as primary and secondary.

PRIMARY DATA

Primary data are those data, which are

collected at the first time, and they are original in

character. This study covers the enquiry regarding the

inventory data. Under this research the data collected

personally.

SECONDARY DATA

Secondary data are those data

that are already collected by someone for some purposes

and are available for the present study. Various sources of

secondary data including Annual reports, Official website of

Travancore Sugars And Chemicals Ltd., research abstracts

published in various books and research articles published in

business journals.

1.4.2 PERIOD OF THE STUDY

The study covers a period of fiveyears performance of Travancore Sugars And Chemicals Ltd. The

years taken for the study are from 2006-11.

1.4.3 AREA OF THE STUDY

The area selected for the study isTravancore Sugars And Chemicals Ltd. Valanjavattom.

1.4.4 TOOLS FOR DATA ANALYSIS

The data collected where grouped and

analyzed by using appropriate accounting ratios. The trend

analysis where also used for this study. Statement of change

in working capital is also prepared with a way to ascertain

the effect of changes of various components in the working

capital of company.

1.5 LIMITATIONS OF THE STUDY

Some of the data was not given by the company due to

the maintenance of financial secrecy. So the study

cannot be covered to all the areas of working

capital.

The qualitative aspects where also used only in a

limited contexts.

The limitation in the compilation of secondary data

might have affected the findings of the study.

1.6 CHAPTERISATION

This study report contains five chapters.

Chapter 1- This chapter contains the Introduction,

Objectives of the study, Scope of the study, Research

Methodology, Period of the study, Tools for data analysis,

and Limitations of the study.

Chapter 2- deals with profiles of the study.

Chapter 3- gives a theoretical framework for undertaking the

study and deals with growth and development of beverage

industry and the performance of Travancore Sugars And

Chemicals Ltd.

Chapter 4- explains the results of analysis of working

capital management of Travancore Sugars And Chemicals Ltd.

Chapter 5- consists of findings, suggestions and conclusion.

CHAPTER 2

PROFILES

2.1 INDUSTRY PROFILE

I n d i a h a s a p o p u l a t i o n o f m o r e

t h a n 1 . 1 5 0 B i l l i o n s w h i c h i s j u s t b e h i n d C h i n a .

According to the national sample survey; by 2030 India

population will be around 1.450 Billion and will surpass

China to become the World largest in terms of

population. Beverage Industry which is directly

related to the population is expected to maintain a

robust growth rate. The price stability throughout the year

has contributed to the increase in domestic liquor sales. The

Indian beverage market offers hot options. In India, various

positive factors drive the beverage markets. One is the

rising number of people in the middle class with extra money

to spend on new beverages like wine new brands of imported

whiskey, or the fancy energy drinks, some of which are really

good to enable people to work longer, to listen longer

during conferences, and even to party longer and have

fun.

MAJOR MARKET UNDER INDIAN BEVERAGE INDUSTRY

1. Indian Non-Alcoholic Beverage Market

2. Indian Soft Drink Market

3. Indian Tea Market

4. Indian Alcoholic Beverage Market

5. Indian Beer Market

6. Indian Wine Market

Liquor production is one of the

profitable businesses in today’s world. In India several

private, public and government companies are producing liquor

and making huge profits. But this liquor consumption is

injurious to human body. It will spoil the life of young

generations of a country. The government cannot stop the

production and distribution of liquor because it accelerates

the revenue in the form tax. The turnover tax of liquor

(IMFL) sales is 96%.

KSBC (Kerala State Beverages

Corporation) has the monopoly right to distribute the liquor

throughout the state and any other selling activities within

the state are illegal and are subject to serve punishment

including imprisonment.

The Kerala State Beverages (M&M)

Corporation handles potable liquor made out of Extra Neutral

Alcohol. Potable liquor is a consumable item containing

potable Alcohol and other chemicals. The role the KSBC is

channelizing all kinds of liquor/beer/wine from manufactures

throughout the country for the consumers in Kerala. As such

KSBC is not restricting purchase of liquor from any

manufacturer who is prepared to enter into a valid contract.

KSBC performs the role of procuring liquor and take adequate

steps to ensure the quality standards of liquor and place them

to the consumer through the various channels of distribution

enabling the consumer to take his preference. The liquor

brought through KSBC contains the holographic stickers pasted

on the bottle caps. The

activity of KSBC confines to contracts for procurement and

distribution. Consumer has to know hid health condition while

deciding to drink. Alcohol is not a freely marketable item

like any other consumable but can be sold only through

license. In this point of view there is a message that

consumer has to check his health while consuming liquor.

The judicial commission of inquiry appointed by the Government

to streamline the liquor trade in the state recommended-

To provide genuine liquor at reasonable price, through

Government agencies

Exploitation through increased taxation and

exploitation by middleman should be stopped and

consumer protection must be the guiding policy.

For achieving the above, nationalization of entire liquor

trade was suggested.

In line with the suggestion the

Government decided to set up a Public Sector Corporation to

procure spirit and arrange blending, bottling, sealing and

distribution of arrack and also for dealing with the sale of

IMFL. An amendment was made in the Abkari Act in 1984 to give

effect to the same.

KSBC was formed on 23.2.1984 to take over the wholesale

distribution of liquor in a phased manner and to eventually

set up distilleries and blending units to produce spirit,

arrack and IMFL. Since then the distribution of liquor has

been brought under the control of the Corporation. By a

decision in 2001 the majority of the retail outlets also have

been entrusted to the Corporation. As at present the whole

activity of IMFL from procurement to distribution and sale to

the consumer is controlled by the Corporation except for loose

vending of liquor by Bars/Clubs and a small portion of the

retails by Consumer Federation.

Objectives

1. To provide genuine quality liquor to consumers at

reasonable prices

2. To make available supplies of liquor commensurate to demand

3. To evolve a proper system to prevent misuse, distribution

of spurious liquor through unauthorized sources and evasion of

duties and taxes by middlemen

4. Consumer protection and satisfaction

Corporate Objectives of the Company

To build lasting relationships with customers based on

trust and mutual benefit

To uphold highest ethical standards in conduct of our

business

To create and nurture a culture that supports flexibility,

learning and is proactive to change

To chart a challenging career for employees with

opportunities for advancement and rewards

To value the opportunity and responsibility to make a

meaningful difference in people’s lives

To maintain the Quality of the product

2.2 COMPANY PROFILE

A PROFILE OF TRAVANCORE SUGARS AND CHEMICALS LTD.

COMPANY NAME: Travancore Sugars & Chemicals Ltd.

OWNER: Government of Kerala

LOCATION: Valanjavattom

FULL ADDRESS: Travancore Sugars & Chemicals Ltd.

Valanjavattom,

Thiruvalla -689 104

Tel: 0471-2332632

E-

mail: [email protected]

The Travancore Sugars and Chemicals Ltd (TSC Ltd) was

incorporated in June 1937 with an authorized share capital of

Rs.60, 00,000 with an objective to acquire carryon and

transact the traders and business of planets, general

merchants and importers, manufactures of dealers in sugar,

wine and spirits. Now the Company is concentrating on Indian

made fine liquor (IMFL) production. There is no marketing

department in the company because the sales of IMFL products

are only done through the Kerala State Beverage Corporation

(KSBC) Ltd. This government company registered under the joint

stock Companies Act 1956 and its share capital as at 2008 is

Rs.1, 31, 56,890

Manpower of the Company is 218 employees at present and

turnover approximately for the year ended 2007-2008 is 83

lakhs. The operations of the company are highly sophisticated

over the years and the company has developed very high

reputation for the quality of its products. The products are

resilient, inexpensive and hygienic. The Company follows

strict quality control measures.

LOCATION

Selection of proper location for a new plant is

essential for the smooth functioning of the company.

Travancore sugars and chemicals Ltd is situated at the place

called Valanjavattom near Thiruvalla.

Major reason for the selection of this location is

availability of transportation facilities, banking facilities

and well skilled labour forces etc.

LOGISTICS:

Internal Movement

Trolley and vehicles are used to move semi-finished goods from

one process station to another process station.

External Environment

In the case of road Transport TSC has made contract with

various transport companies like K.R.S (Kerala Roadways

Transport Ltd ) and A.C cargo management. Other mode of

transportation is rail.

Mission of the Company

“To provide full employment to its employees & to keep financial stability of the

concern”

Vision of the Company

“To increase its production as double and to attract more customers”

BOARD OF DIRECTORS

CHAIRMAN:

Mr. C.K. VISWANATHAN IAS.

DIRECTORS:

Mr. T.K. MANOJ KUMAR

Mr. N.SHANKAR REDDY IPS

Mr. MANAPANDIYAN IAS

MANAGING DIRECTOR: Mr.

N VIJYAANAND

SENIOR MANAGER (FINANCE) & SECRETORY IN CHARGE:

Mr. ALEX P. ABRAHAM, FCA.

AUDITORS:

M/S SRIDHAR & Co.

Chartered Accounts,

Thiruvananthapuram.

BANKERS:

State Bank of Travancore

State Bank of India

Indian Overseas Bank

Government Treasury

Pathanamthitta District

Co-operative Bank

LEGAL ADVISERS:

M/S MENON AND PAI

Ernakulum

2.3 PRODUCT PROFILE

Travancore Sugars Chemicals Ltd produces variety of products

which are given below.

INDIAN MADE FINE LIQUOR (IMFL)

During the financial year 2008-2009 the company sold 2774528

bulk litres of IMFL valued Rs.87031902 but during the

financial year 2007-2008 the company sold 2782000 bulk litres

of IMFL valued Rs.858814668. So we can find out that there is

a minute change in sales of IMFL. But even if there is change

in sales the value rate is increased now the company produces

so many brands of liquor which are given below.

(a) MAJOR PREMIUM BRAND

This brand is specially produced for high class segment.

Normally this brand is costlier than other products. It is

one of the brands which has a great move in the market. This

product is an advancement of its earliest product named

Commander VSOP Brandy.

(b) FESTIVAL XXX RUM

Festival xxx rum is a leading brand in middle class segment.

During the year 2007-2008 as per sales report this brand makes

good sales.

(c) JAWAN XXX RUM

During the year 2007-2008 as per the sales report this is the

most profit making brand of the company. These brand targets

mainly on middle class segment. Price of this product is

around 180rs for 750 ml bottle. The main ingredients are

caromic colour, essence and extra 96% neutral alcohol and food

flavor.

(d) CHEERS XXX RUM

This is a special brand for low class segment, these brands

also keep god sales report, but low compared to others.

DENATURED AND METYLATED SPIRIT

During the year 2007-2008 the company sold 17944 bulk liters

of methylated spirit valuated 792775 Rs. and 3259 liters of

Denatured spirit costing Rs.143746. The earnings from these

were much high compared to its earning in previous years. In

the year 2006-2007 total earnings from both was around 6.5

lakh only.

RECTIFIED SPIRIT

During the year 2008-2009 the company sold 149462 liters of

rectified spirit valued at Rs.5380643. When compared to the

previous year there is much more decrease in the sales of

rectified spirit. It contains 94% alcohol.

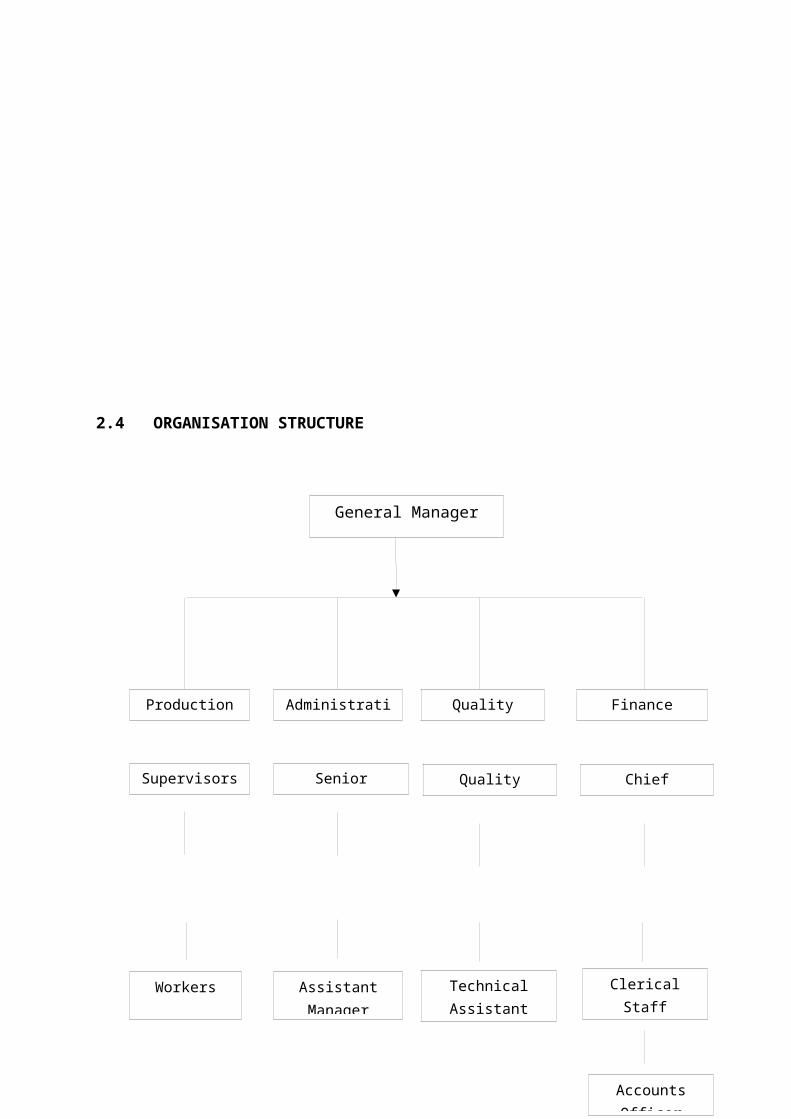

2.4 ORGANISATION STRUCTURE

General Manager

Finance

ChiefAccountant

QualityManager

Supervisors SeniorManager

QualityControl

Administration

Production

ClericalStaff

Workers AssistantManager

TechnicalAssistant

AccountsOfficer

Fig: 1

FUNCTIONAL DEPARTMENTS OF TSC

In TSC the work activities that are similar and logically

connected are grouped to form departments. At present there

are seven departments in the organization. They are as

follows.

1. Production Department

2. Quality Control Department

3. Production Planning Department

4. Material Department

5. Finance Department

6. Human Resource Management

7. Personnel and Administrative Department

FINANCE AND ACCOUNTS DEPARTMENT :

This department is headed by an eminent Finance Manager, who

can make the finance details of the organization up to date.

Every year an audit will be conducted for checking the

financial position of the organization and to check the

correctness of the accounts.

FINANCIAL MANAGEMENT IN TSC LTD.

Senior finance Manager manages the finance department and he

reports to the M.D directly, about the functions of the

department.

BASIC FUNCTIONS OF ACCOUNTS DEPARTMENT

1. Planning and allocating works to accounts staff.

2. Salary and wage administration.

3. Incentives and overtime payment etc.

4. Retirement, gratuity and other personal matters.

5. Verifying cash books.

6. Verifying debtor’s statement.

7. Verifying stock statement.

8. Attending legal and departmental proceedings.

9. Verifying bank reconciliation statement.

10. Scrutinizing of purchase bill, expense bill etc.

11. Submitting periodicals to PF, ESI sales Tax.

12. Legal Security.

13. Monthly closing accounts.

14. Debit and credit note preparation.

15. Renewal of various licenses.

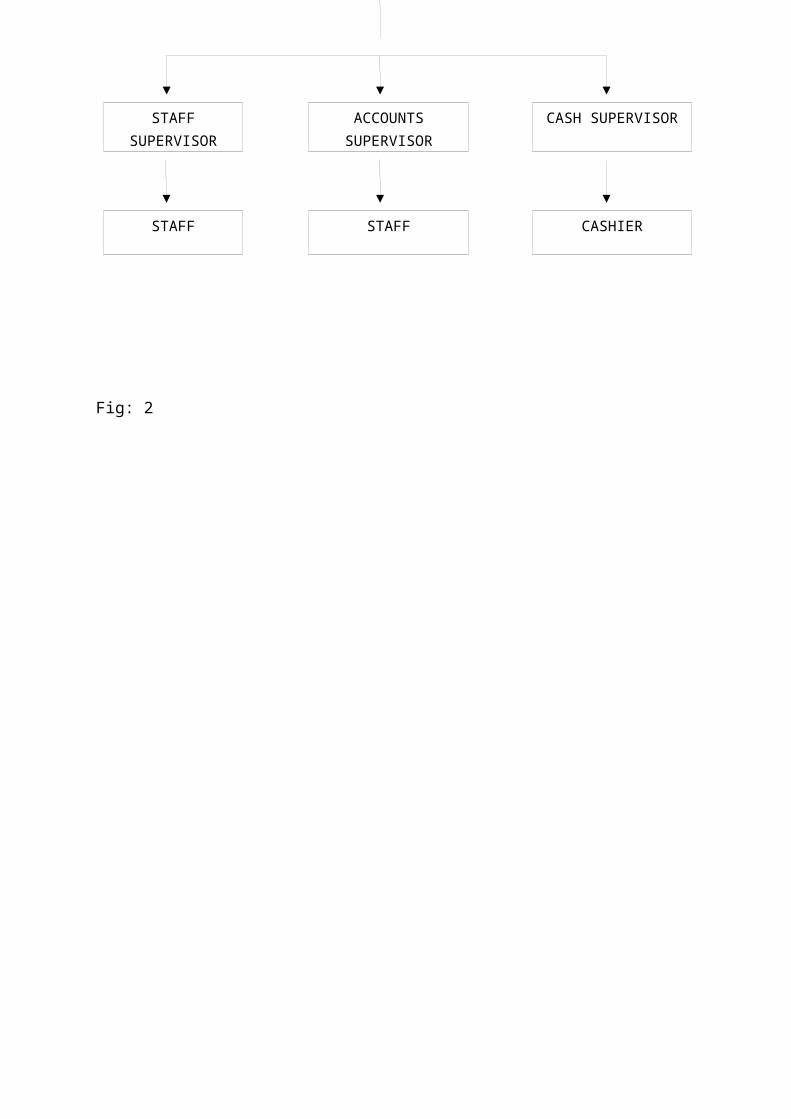

2.5 FINANCE DEPARTMENT STRUCTURE

FINANCE MANAGER

Fig: 2

STAFFSUPERVISOR

ACCOUNTSSUPERVISOR

CASH SUPERVISOR

STAFF STAFF CASHIER

CHAPTER 3

THEORETICAL FRAMEWORK

3.1 INTRODUCTION

Financial management decisions are divided into the management

of assets (investments) and liabilities (sources of

financing), in the long-term and the short-term. It is common

knowledge that a firm’s value cannot be maximized in the long

run unless it survives the short run. Firms fail most often

because they are unable to meet their working capital needs;

consequently, sound working capital management is a requisite

for firm survival.

About 60 percent of a financial manager’s time is devoted to

working capital management, and many of the potential

employees in finance-related fields will find out that their

first assignment on the job will involve working capital. For

these reasons, working capital policy and management is an

essential topic of study. In many text books working capital

refers to current assets, and net working capital is defined

as current assets minus current liabilities. Working capital

policy refers to decisions relating to the level of current

assets and the way they are financed, while working capital

management refers to all those decisions and activities a firm

undertakes in order to manage efficiently the elements of

current assets.

The term working capital originated with the old Yankee

peddler, who would load up his wagon with goods and then go

off on his route to peddle his wares. The merchandise was

called working capital because it was what he actually sold,

or “turned over”, to produce his profits. The wagon and horse

were his fixed assets. He generally owned the horse and wagon,

so they were financed with “equity” capital, but he borrowed

the funds to buy the merchandise. These borrowings were called

working capital loans, and they had to be repaid after each

trip to demonstrate to the bank that the credit was sound. If

the peddler was able to repay the loan, then the bank would

issue another loan, and these were sound banking practices.

The days of the Yankee peddler have long since pasted, but the

importance of working capital remains. Current asset

management and short-term financing are still the two basic

elements of working capital and a daily headache for the

financial managers.

3.2 MEANING OF WORKING CAPITAL

A firm may exist without making profits but cannot survive

without liquidity. The function of working capital

management organization is similar that of heart in a human

body. Also it is an important function of financial

management. The financial manager must determine the

satisfactory level of working capital funds and also the

optimum mix of current assets and current liabilities. He

must ensure that the appropriate sources of funds are used

to finance working capital and should also see that short

term obligation of the business are met well in time.

Working Capital consists of that portion of the assets of a

business, which are used, in current operations. It includes

receivables, inventories or raw materials, stores, work-in-

progress and finished goods, merchandise, bill receivable

and cash. These types of assets are normally temporary in

nature. In accounting concept of working capital it is the

difference between inflow and outflow of funds i.e. sources

and uses of funds, (i.e. net cash inflow). In other words,

working capital is the excess of current assets over current

liabilities. Working capital management is concerned with

problem that arises in attempting to manage the current

liabilities and the interrelationship exists between them.

Management of short-term asset and short term financing is

referring to working capital management and current asset

management. The goal of working capital management is to

manage a current asset in such a manner so that the

satisfactory level should be maintained.

Working capital as represented by excess of current assets

over current liabilities and identifying the relatively

liquid portion of the total enterprise capital which

constitutes a margin for meeting obligation within the

ordinary operating cycle of the business.

"The sum of the current asset is the working capital." J.S

Mill defines the gross concept. "Whenever working capital is

mentioned it brings to mind current assets and current

liabilities with general understanding that working capital

is the difference between the two."

CONCEPTS OF WORKING CAPITAL

There are two concepts of working capital, Gross concept

(GWC) and Net Concept (NWC).

Gross working capital refers to a firm's investment in

current assets. Current assets are the assets, which can be

converted into cash within an accounting year and includes

cash, short-term securities, debtor, bills receivables and

inventories. In other way, it defines as "total of current

assets i.e. circulating capital." This concept is also known

as quantitative concept.

The net concept i.e. net working capital concept refers to

the difference between current assets and current

liabilities. Current liabilities are those claims of

outsiders, which are expected to mature for payment within

an accounting year and include creditors, bills payable,

bank overdraft and outstanding expenses. This concept gives

idea regarding sources of financing capital i.e. amount of

current assets which would remain surplus if all current

liabilities are paid. It can be positive or negative

(positive is net working capital and negative is deficit

working capital)

3.3 TYPES OF WORKING CAPITAL

Classification on the basis of concept:

Gross working capital: This concept is also known as

quantitative concept It takes current assets i.e. cash,

accounts receivables, merchandize, debtors etc. into

account When die organization considers long-term

funds, this concept is significant.

Net working capital: This concept is also known as

qualitative concept. According to this concept, working

capital is the excess of current assets over current

liabilities. This concept shows how much amount is left

for operating activities. For determining the financial

position (i.e. liquidity) this concept is significant

Deficit Working Capital: Excess of current liabilities

over current assets is deficit working capital. Such a

situation is not absolutely theoretical and occurs when

a firm is nearly a crisis of some magnitude.

Classification on the basis of financial statement:

This classification has been done on the basis of financial

statement because the information regarding the working

capital is collected from the profit and loss account or

balance sheet.

(I) Balance sheet:

When the information regarding the working capital is

collected from the balance sheet (i.e. the items appearing in

balance sheet), then this type of working capital is known as

balance sheet working capital.

The basis can now again classified as;

• Gross Working Capital

• Net Working Capital

• Deficit Working Capital

(II) Profit & Loss Account:

Cash working capital: Cash working capital arises when the

items regarding the working capital is collected from the

profit and loss account i.e. the items appearing in P&L A/c.

It shows the real flow of money and values at a particular

time and is considered to be then more realistic approach

and having great significance to working capital management

in recent years as it shows the adequacy of cash flow in

business. It is based on operating cycle concept.

The duration of time required to complete the different

events like conversion of cash into raw materials, raw

material into work-in-progress, work-in-progress into

finished goods, finished goods to debtors and bill receivable

through sales and conversion of bill receivable to cash etc.

in case of manufacturing firm.

Classification on the basis of variability:

Permanent working capital:

The working capital which is permanent in nature is

permanent working capital. They cannot be varied due to

variation in sales. It is the minimum level of current

assets kept by the organization required always for business

operation even if there is fluctuation in sales. Normally it

consists of low level of inventory cash, bill receivable,

and material in process, finished goods. These can be

obtained any day of the year because it is permanent in

nature. Amount of such investment is called as Permanent

Working Capital. Permanent Working Capital is also known as

fixed or regulating Working Capital. This amount varies

year-to-year depending upon the growth and stage of business

cycle in which it operates.

Variable working capital:

It is required during the most active seasons of the year.

It is most suited to the business, which is seasonal and

cyclical in nature. It represents as additional asset

required for normal functioning of business in favorable

seasons. It changes according to variation in sales.

Temporary Working Capital:

Total Current Assets - Permanent Current Assets. It changes

according to change in operational activity. This is also

known as Temporary, Seasonal or Special Working Capital. The

Permanent is constant and temporary is fluctuating according

to seasonal demand.

3.4 FACTORS AFFECTING WORKING CAPITAL REQUIREMENTS

A firm should plan its operations in such a way that it

should have neither the lack of working capital nor it

should have excess of working capital. There is no set of

rules or formula to determine the working capital

requirement but there are so many factors that affect in

determining the requirement of working capital. The factors

mainly affect the size and nature of industry and firm.

These factors are also changing from time to time. In

general, following factors are affecting the requirement of

working capital.

1. Nature of Industry: The main factor which affects the

requirement is the nature of the industry i.e. if the

industry is of small type there may be less need of cash,

investment. On the other hand, if the industry is of large

type, the block cash etc. are kept on large basis. Even

the goods and raw materials are purchased and supplied on

credit basis.

Investing huge amount in fixed assets, have the lowest

needs for current assets, partly because of the cash

nature of their business and partly because of selling

services instead of products. Thus, no funds will be tied

up in accounts receivables and inventories. On the other

hand, trading and financial firms have a very low

investment in fixed assets but huge amount to be invested

in working capital.

2. Demand of creditors: Creditors are the liability of any

organization. They have interested in the assets of a

company and security of loans. They want their advances

should be sufficiently covered. This can only be possible

when the assets are greater than its liabilities so that

they may easily get money as and when needed and at the

time of maturity.

3. Cash Requirements: Cash is a part of current assets. The

company should maintain the minimum cash level. It helps

in the smoother functioning of business operation. It

should be adequate and properly utilized. It is both the

means and end of enterprise. Just as blood, gives life to

the human body, in the same way cash gives profit and

solvency to the working capital structure of an

enterprise.

4. General nature of business: The general nature of business

is also as important determinant of working capital.

Working capital requirements are depend upon general

nature and its activity to work. In public utility

services, the working capital requirement is relatively

slow as the inventories and goods rapidly change into

cash. The large concerns that are engaged in production

maintenance, a big part of investment consists of working

capital. They have to maintain cash, inventory at very

large level. Manufacturing organization, however face

problems of slow turnover of inventories and receivable

and invest large amount in working capital. The industrial

concern should have a fairly large amount of working

capital though it varies from industry to industry

depending on their assets structure.

5. Time: This is also an important factor that affects the

requirement of working capital. If the time required in

manufacturing goods is more (large), the investment in

working capital is also greater and if the time is less

than the amount invested in working capital is also less.

Moreover, the amount of working capital depends upon

inventory turnover and the unit cost of goods that are

sold. The greater the cost the larger is amount of working

capital.

6. Volume of sales: This is the most important factor

affecting the requirement of working capital. A firm

maintains current assets because they are needed to

support the operational activation, which result in sales.

The volume of sale and the size of the working capital are

directly related to each other. As the volume of sale

increases the working capital investment increases and

vices versa.

7. Terms of purchase and sale: If the credit terms of

purchases are more favorable and those of sales less

liberal, less cash is invested in inventory. With more

favorable credit terms, working capital requirements can

be reduced as the firms do get more time for payment to

creditors or suppliers. The credit granting policy of a

firm affects the working capital requirement by

influencing the size of account receivables.

8. Inventory Turnover: If it is high, the working capital

requirement will be low. If it is low, working capital

requirement reduces. Managing working capital is

synonymous with controlling inventories. Good inventory

management is helpful for the structure of working

capital.

9. Receivable Turnover: It is necessary to have an effective

control over receivables. Prompt collection of receivables

and good facilities for setting payables result into low

working capital requirements obtain maximum sales; keep

bad debt losses to minimum. Minimize the cost of

investment etc. are the objectives of receivables

management.

10.Business cycle: More working capital is required in the

prosperity of business expansion and less working capital

required at the time of depression. In the period of

prosperity, additional funds are required to invest in

plant and machinery to meet the increased demand. The

depression phase lead to fall in the level of inventories

and book debts and so less working capital is required.

Business fluctuation influences the size of working

capital mainly through the effect of inventories.

11.Variation in Sales: A seasonal business requires the

maximum amount of working capital for a relatively short

period of time.

12.Production Cycle: The time to convert raw material into

finished goods is referred to as the production cycle or

operating cycle. The longer the duration, more working

capital is required and lesser the duration less working

capital is required. So it is an important factor, which

affects the working capital requirement more working

capital is required to finance the production cycle.

13.Liquidity and Profitability: If firm is interested in

maintaining the liquidity and wants to improve the

liquidity, more working capital is required. If a firm

desires to take a greater risk for bigger gains and

losses, it reduces the size of its working capital in

relation to its sales. A firm therefore should choose

between liquidity and profitability and decides about its

working capital requirement accordingly.

14.Profit planning and control: Adequate profit assists in

generation of cash. It makes it possible for management

to plough back a part of earning into the business and

substantially build up internal financial resources.

15.Activities of the firms: A firm' policy regarding the

sale also depends upon the requirement of working

capital. If a firm's sells its goods to customer on

credit basis, it requires more working capital as

compared to cash sales.

16.Production Policy: There are two options open to the

enterprise, either they confine their production only to

periods when goods are purchased or they follow a steady

production policy throughout the year. In former case,

there will be serious production problems. During the

slack season, the firm will have to maintain the working

force and physical facilities without adequate production

or sale. The programmed accumulation of stock will

naturally require an increasing amount of working

capital, which will remain tied up for some months.

17.Turnover of circulating capital: Conversion of cash to

inventory, inventory to finished goods, finished good to

book debts of account receivables, book debt to cash

account play an important role in judging the working

capital requirement.

18.Inherent hazards and contingencies: An enterprise

operating an industry subject to wide fluctuation in

demand and prices for its products, periodic operating

losses or rapidly changing technology, requires

additional working capital.

19.Repayment ability: Enterprise repayment ability

determines the level of its working capital.

20.Availability of credit: An enterprise which can get

credit from bank and suppliers easily on favorable

conditions will operate with less working capital than an

enterprise with such a facility.

21.Operational and Financial efficiency: Working capital

turnover can only be improved with a better operational

and financial efficiency of a firm.

22.Dividend Policy: A shortage of working capital often acts

as powerful reason for reducing or shipping a cash

dividend.

23.Value of current assets: A decrease in the real value of

current assets compared to their book value reduces the

size of the working capital. If real value of current

assets increases, there will be an increase in working

capital.

24.Price level changes: The rise price level will require an

enterprise to maintain a higher amount of working capital.

The companies, which can immediately reverse their product

prices with rising price level, will not face a severe

working capital problem.

25.Gestation Period: Certain industries have a long

gestation period with a result that a considerable number

of years must elapse before production; operation can be

carried on profitably. During this period income is

insufficient and working capital is greater.

3.5 FINANCING OF WORKING CAPITAL

The working capital requirements of a concern can be

classified as:

a) Permanent or fixed working capital requirements.

b) Temporary or variable working capital requirements.

In any concern, a part of the working capital investments are

as permanent investments in fixed assets. This is so because

there is always a minimum level of current assets which are

continuously required by the enterprise to carry out its day

to day business operations and this minimum cannot be expected

to reduce at any time. This minimum level of current assets

gives rise to permanent working capital.

Similarly, some amount of working capital may be required to

meet the seasonal demands and some special exigencies such as

rise in prices, strikes etc. This proportion of working

capital gives rise to temporary or variable working capital

which cannot be permanently employed gainfully in business.

FINANCING OF PERMANENT WORKING CAPITAL

Permanent working capital should be financed in such a manner

that the enterprise may have its uninterrupted use for a

sufficiently long period. There are five important sources of

permanent working capital. They are;

1) Shares: Issue of shares is the most important source for

raising the permanent capital. A company can issue various

types of shares as equity shares, preference shares and

deferred shares.

2) Debentures: A debenture is an instrument issued by the

company acknowledging its debt to its holder. It is also an

important method of raising long term capital. The

debenture holders are the creditors of the company. A fixed

rate of interest is paid on debentures. The interest on

debentures is a charge against profit and loss account. The

firm issuing debentures also enjoys a number of benefits

such as trading on equity, retention of control, tax

benefits, etc.

3) Public Deposits: Public deposits are the fixed deposits

accepted by a business enterprise directly from the public.

This source of raising short term and medium term finance

was very popular in the absence of banking facilities.

Public deposits as a source of finance have a large number

of advantages such as simple and convenient source of

finance, taxation benefits, trading on equity, etc.

4) Ploughing back of profits: It means the reinvestments by

concern of its surplus earnings in its business. It is an

internal source of finance and is not suitable for

established firm for its expansion, modernization and

replacement etc. this method of finance has a number of

advantages as it is the cheapest rather cost free source of

finance; there is no need to keep securities; there is no

dilution of control; it ensures stable dividend policy and

gains confidence of public.

5) Loans from financial institutions: Financial institutions

such as Commercial Banks, Life Insurance Corporation,

Industrial Finance Corporation of India etc. also provide

short term, medium term and long term loans. This source of

finance is more suitable to meet the medium term demands of

working capital.

FINANCING OF TEMPORARY WORKING CAPITAL

The main sources of short term working capital are as

follows:

1) Indigenous bankers: Private money-lenders and other

country bankers used to be the only source of finance

prior to the establishment of commercial banks. They used

to charge very high rates of interest and exploited the

customers to the largest extent possible. Now-a-days with

the development of commercial banks they have lost their

monopoly. But even today some business houses have to

depend upon indigenous bankers for obtaining loans to meet

their working capital requirements.

2) Trade credit: Trade credit refers to the credit extended

by the suppliers of goods in the normal course of

business. As present day commerce is built upon credit,

the trade credit arrangement of a firm with its suppliers

is an important source of short term finance. The credit-

worthiness of a firm and the confidence of its suppliers

are the main basis of securing trade credit. It is mostly

granted on an open account basis whereby supplier sends

goods to the buyer for the payment to be received in

future as per terms of the sales invoice. It may also take

the form of bills payable whereby the buyer signs a bill

of exchange payable on a specified future date.

3) Installment credit: This is another method by which the

assets are purchased and the possession of goods is taken

immediately but the payment is made in installments over a

pre-determined period of time. Generally, interest is

charged on the unpaid price or it may be adjusted in the

price. But in any case, it provides funds for some time

and is used as a source of short term working capital by

many business houses which have difficult fund position.

4) Advances: Some business houses get advances from their

customers and agents against orders and this source is a

short term source of finance for them. It is a cheap

source of finance and in order to minimize their

investment in working capital, some firms having long

production cycle, especially the firms manufacturing

industrial products prefer to take advances from their

customers.

5) Factoring: Another method of raising short term finance is

through accounts receivable credit offered by commercial

banks and factors. A commercial bank may provide finance

by discounting the bills or invoices of its customers.

Thus, a firm gets immediate payment for sales made on

credit. A factor is a financial institution which offers

services relating to management and financing of debts

arising out of credit sales. Factors render services

varying from bill discounting facilities offered by

commercial banks to a total takeover of administration of

credit sales including maintenance of sales ledger,

collection of accounts receivables, credit control and

protection from bad debts, provision of finance and

rendering advisory services to their clients.

6) Accrued expenses: Accrued expenses are the expenses which

have been incurred but not yet due and hence not yet paid

also. These simply represent a liability that a firm has

to pay for the services already received by it. The most

important items of accruals are wages and salaries,

interest, and taxes. The amount of accruals varies with

the change in the level of activity of a firm. When the

activity level expands, accruals also increase and hence

they provide spontaneous source finance. Further as no

interest is payable on accrued expenses, they represent a

free source of finance.

7) Deferred incomes: They are incomes received in advance

before supplying goods or services. They represent funds

received by a firm for which it has to supply goods or

services in future. These funds increase the liquidity of

a firm and constitute an important source of short term

finance. However, firms having great demand for its

products and services, and those having good reputation in

the market can demand deferred incomes.

8) Commercial paper: It represents unsecured promissory

notes issued by firms to raise short term funds. It is an

important money market instrument. Only a company which is

listed on the stock exchange has a net worth of at least

Rs. 10 crores and a maximum permissible bank finance of

Rs. 25 crores can issue commercial paper not exceeding 30

per cent of its working capital. The maturity period of

commercial paper, in India, mostly ranges from 91 to 180

days. Commercial paper is a cheaper source of raising

short term finance as compared to the bank credit and

proves to be effective even during period of tight bank

credit.

9) Working capital finance by commercial banks: Commercial

banks are the most important source of short term capital.

The major portion of working capital loans are provided by

commercial banks. They provide a wide variety of loans

tailored to meet the specific requirements of a concern.

The different forms in which the banks normally provide

loans and advances are loans, cash credits, overdrafts,

purchasing and discounting of bills.

3.6 TECHNIQUES FOR ANALYSING WORKING CAPITAL

There are four important techniques for analyzing the

working capital position of an enterprise.

Ratio Analysis

Fund Flow Analysis

Cash Flow Analysis

Trend Analysis

Ratio Analysis: It is commonly used technique for

analyzing working capital management. Management can use

ratio analysis of working capital as a means of checking

upon the efficiency with which working capital is being

used in a concern. It can be used with profit to measure

the pulse of the working capital. It can help us to

diagnose the working capital position of the

enterprise.This technique is most commonly used because

it practically deals with each and every aspect of

working capital analysis. In this technique for each

aspect of analysis, certain ratios are computed and then

results are drawn based on trends shown by then against

those fixed as guideposts. Various ratios are used in

analyzing the various aspects of the working capital

position of an enterprise. Ratio analysis is not only a

technique to find out or point out the relationship

between two figures but also points out the devices to

measure the fundamental strengths or weakness of a

concern.

Following are some of the important ratios used to analyze

the liquidity, efficiency and profitability position of the

firm.

LIQUIDITY RATIOS

Liquidity is the ability of the firm to meet its current

liability as they fall due. Since liquidity is basic to

continuous operations of the firm it is necessary to

determining the degree of liquidity of the firm. It is also

known as working capital ratio. The most important liquidity

ratios are;

CURRENT RATIO

Current Ratio is the most commonly used ratio to measure

liquidity of a concern. It represents the ratio of current

assets to current liabilities. In a sound business a Current

Ratio of 2:1 is considered as an ideal one.

QUICK RATIO

This ratio is also known as “Acid Test Ratio”. It is the

relation between quick assets to current liabilities. It is

determined by dividing “quick assets” by current

liabilities. An Acid Test Ratio of 1:1 is considered

satisfactory as a firm can easily meet all its current

liabilities.

ABSOLUTE LIQUIDITY RATIO

This ratio is obtained by dividing cash (of course cash in

hand and cash at bank) and marketable securities by current

liabilities. It is also known as Cash Position Ratio. A

ratio of 0.5:1 is recommended to ensure liquidity. This test

is more vigorous measure of a firm’s liquidity position.

TURNOVER RATIO OR EFFICENCY RATIO

The ratios computed under this group indicate the efficiency

of the organization to use various kinds of assets by

converting them in the form of sale. These ratios are also

called activity ratios or asset management ratios. The asset

basically categorized as fixed assets and current assets and

the current assets further classified according to individual

components of current assets viz. investment and receivables

or debtors or as net current asset. The important efficiency

ratios are the following.

WORKING CAPITAL TURNOVER RATIO

This ratio reflects the turnover of the firm’s net working

capital in the course of the year. It is a good measure of

over- trading and under- trading. It helps in simple

assessment of liquidity, profitability, solvency and

efficiency of the firm.

DEBTORS TURNOVER RATIO

The purpose of this ratio is to know the credit collection

power and policy of the firm. For this a relationship is

established between accounts receivables and net credit

sales of the period. A shorter collection period implies

prompt payment by debtors.

AVERAGE DEBT COLLECTION PERIOD:

The average collection period measures the quality of

debtors since it indicate the speed of their collection. The

shorter the average collection period, the better the

quality of the debtors since a short collection period

implies the prompt payment by debtors. The average

collection period should be compared against the firm’s

credit terms and policy judges its credit and collection

efficiency.

INVENTORY TURNOVER RATIO

This ratio indicates whether investment is efficiently used

or not. It, therefore, explains whether investment in

inventories is within proper limits or not. It also measures

the effectives of the firm’s sales efforts.

INVENTORY CONVERSION PERIOD

This indicates how quickly a company is turning over its

inventory. When deciding the appropriate level of inventory, a

company should strike a balance between the cost of tying up

capital and the demands from the customer. Generally, a high

inventory turnover (short inventory holding period) is

Preferred. An unreasonably long inventory holding period may

indicate an economic recession, obsolete inventory, poor sales

and marketing, a change of customer taste or bad inventory

management.

CURRENT ASSET TURNOVER RATIO

Current assets turnover ratio is calculate to know the firms

efficiency of utilizing the current assets .current assets

includes the assets like inventories, sundry debtors, bills

receivable, cash in hand or bank, marketable securities,

prepaid expenses and short term loans and advances. This ratio

includes the efficiency with which current assets turn into

sales. A higher ratio implies a more efficient use of funds

thus high turnover ratio indicate to reduced the lock up of

funds in current assets. An analysis of this ratio over a

period of time reflects working capital management of a firm.

CREDITORS TURNOVER RATIO

It indicates the number of times the accounts payable rotate

in a year. It signifies the credit period enjoyed by the firm

in paying its creditors. This ratio shows the relationship

between net credit purchases for the whole year and average

creditors. The ratio signifies that the creditors are being

paid promptly, thus enhancing the credit worthiness of the

company.

PROFITABILITY RATIOS

GROSS PROFIT RATIO

This ratio expresses the relationship between gross

profit and sales. This ratio helps in ascertaining

whether the average percentage of mark up on the goods

in maintained or not. It also indicates the degree to

which selling price per unit may decline without

resulting in losses from operations to the firm.

NET PROFIT RATIO

This ratio is also called as the net profit to sales or

net profit margin ratio. It is determined by dividing

the net income after tax to the net sales for the period

and the measures the profit per rupee of sales.

Fund Flow Analysis: Fund flow analysis shows how funds

have been procured for a business and how they have been

employed. This technique helps to analyze changes in

working capital components between two dates. The

comparison of current assets and current liabilities as

shown in the balance sheet at beginning and at the end

of a specific period, shows changes in such types of

current assets as well as the sources from which working

capital has been obtained. It shows how funds have been

procured for a business and how they have been employed.

It is a useful tool for internal management in its

control of working capital.

"The statement of sources and applications of funds gives a

clear answer to the questions of what has become of the net

profit in such situations. And also what has become of the

funds obtained from all other sources”. However, with the

help of this technique we cannot know whether the working

capital is being used most efficiently. It does not throw

light on the significance of movements in the working

capital structure.

One objective of efficient working capital management is to

minimize the amount of cash in hand. Minimizing the funds

required means knowing when funds will be available and when

funds will be needed. The funds flow can be managed so that

the inflows and outflows nearly match. It is not sufficient

that the final accounts shows a profit and the balance sheet

points a rosy picture of financial health of an enterprises.

All mis will look meaningless unless the funds inflows and

outflows are so regulated that at all times there is enough

cash available to meet obligation as and when they mature.

Cash Flow Analysis: It is an important component of

working capital because it is a form of liquid capital.

It is very necessary for day-to-day operation. It is the

important current asset, which affects business

activities. Cash flow analysis is an important tool for

cash flow planning. Cash is the focal point of working

capital flows.

A statement showing the variation in cash has to be

prepared and is known as cash flow statement. It highlights

the causes, which changes the cash position between two

balance sheet dates. It depicts a penetrating review of cash

movement and an operating cycle. It shows the flow of cash for

a period. Hence, an analysis dealing with inflow and outflow

of cash referred to as cash flow analysis. It shows the

movement of cash in and out of the business by listing the

source of cash receipts and the uses of cash. Sound working

capital management requires maintenance of an adequate amount

of cash. Controlling the investment in working capital begins

with cash management.

Trend Analysis: Working capital trend analysis in an

important technique of working capital management. Trend

percentage constitutes an important tool of

interpretative analysis of financial position of a

company.

It indicates die changes, which have been taking, place from

time to time in individual items of current assets, current

liabilities and net working based on some standard year and

its effect on working capital position. It enables us to

evaluate the upward and downward trend of current asset and

current liabilities. These are usually measured from review of

comparative balance sheets of a concern at the end of two

accounting years and results are drawn based on trend shown by

them. Trend analysis involves the calculation of percentage

relationship that each statement item bears to the same items

in the base year. Trend percentage discloses change in the

financial and operating data between specific periods and

makes it possible for the analyst to form an opinion as to

whether favorable or unfavorable tendencies are reflected by

data.

The goal of working capital management is to manage the firm's

current assets and current liabilities is such a way that a

satisfactory level of working capital is maintained. This is

so because if the firm cannot maintain a satisfactory level of

working capital, it is likely to become insolvent and may even

be forced into bankruptcy. The current assets should be large

enough to cover its current liabilities in order to ensure a

reasonable margin of safety. Each of current assets must be

managed efficiently in order to maintain the liquidity of the

firm while not keeping too high level of any one of them.

3.7 INADEQUATE WORKING CAPITAL

Every business concern must have adequate working capital to

run its business operations. It should have neither redundant

or excess working capital nor inadequate nor shortage of

working capital. Both excess and short working capital

positions are bad for any business. Out of the two, inadequacy

of working capital is more dangerous from the point of view of

the firm.

DISADVANTAGES OF INADEQUATE WORKING CAPITAL

1. A concern with inadequate working capital cannot pay its

short-term liabilities in time. Thus, it will lose its

reputation and shall not be able to get good credit

facilities.

2. It cannot buy its requirements in bulk and avail

discounts etc.

3. It becomes difficult for the firms to exploit favorable

market conditions and undertake profitable projects due

to lack of working capital.

4. The firm cannot pay its day-to-day expenses of its

operations and creates inefficiency, increases costs and

reduces the profits of the business.

5. It becomes impossible to utilize efficiently the fixed

assets due to non availability of liquid funds.

6. The rate of return on investments also falls with the

shortage of working capital.

3.8 COMPONENTS OF WORKING CAPITAL

The three major component of working capital management

include:

Inventory management

Receivables management

Cash management

A detailed discussion of these components is given below:

INVENTORY MANAGEMENT:

Inventory is defined as the sum of the

value of raw material and supplies, including spares, semi-

processed material or work in progress and finished goods. The

nature of inventory is largely depending upon the type of

operation carried on. It is possible to reduce the inventory

to a certain level without affecting production and sales, by

using simple inventory planning and controlling technique. The

reduction in “excessive” inventories carries a favorable

impact on the company’s profitability.

Maintaining inventories involves tying up

of the company’s funds and incurrence of storage and handling

cost. There are three components: Raw material, Work in

progress; and finished goods involved in inventory management.

RECEIVABLES MANAGEMENT:

Receivables or debtors are the one

of the most important parts of the current assets which is

created if the company sells the finished goods to the

customer but not receive the cash for the same immediately.

Trade credit arises when firm sells its products and services

on credit and does not receive cash immediately. It is

essential marketing tool, acting as bridge for the movement of

goods through production and distribution stages to customers.

The receivables include three characteristics:

1) It involve element of risk which should be carefully

analysis.

2) It is based on economic value.

3) It implies futurity. The cash payment for goods or serves

received by the buyer will be made by him in a future period.

CASH MANAGEMENT:

Cash is common purchasing power or medium of exchange. As

such, it forms the most important component of working

capital. The term cash with reference to cash management is

used in two senses, in narrow sense it is used broadly to

cover cash and generally accepted equivalent of cash such as

cheques, draft and demand deposits in banks. The broader view

of cash includes near cash items, such as marketable

securities or bank time deposits. The basic characteristic of

near-cash assets is that they can readily be converted into

cash. They also provide short term investment outlet for

excess and are also useful for meeting planned outflow of

funds.

Cash management is concerned with the managing of:

(i)Cash flows into and out of the firm

(ii)Cash flows within the firm and

(iii)Cash balances held by the firm at a point of the time by

financing deficit or investing surplus cash.

OBJECTIVES OF CASH MANAGEMENT

There are two basic objectives of cash management:

To meet the cash disbursement needs as per the payment

schedule;

To minimize the amount locked up as cash balances.

CHAPTER 4

DATA ANALYSIS

AND

INTERPRETATION

WORKING CAPITAL MANAGEMENT OF TRAVANCORE SUGARS & CHEMICALS

LTD: AN ANALYSIS

The present chapter is an attempt to evaluate the working

capital management of TSC. For the purpose of analysis data

were collected from financial statements of TSC for the period

from 2006 – 07 to 2010 – 11. Appropriate accounting ratios,

schedule of working capital and trend analysis were used.

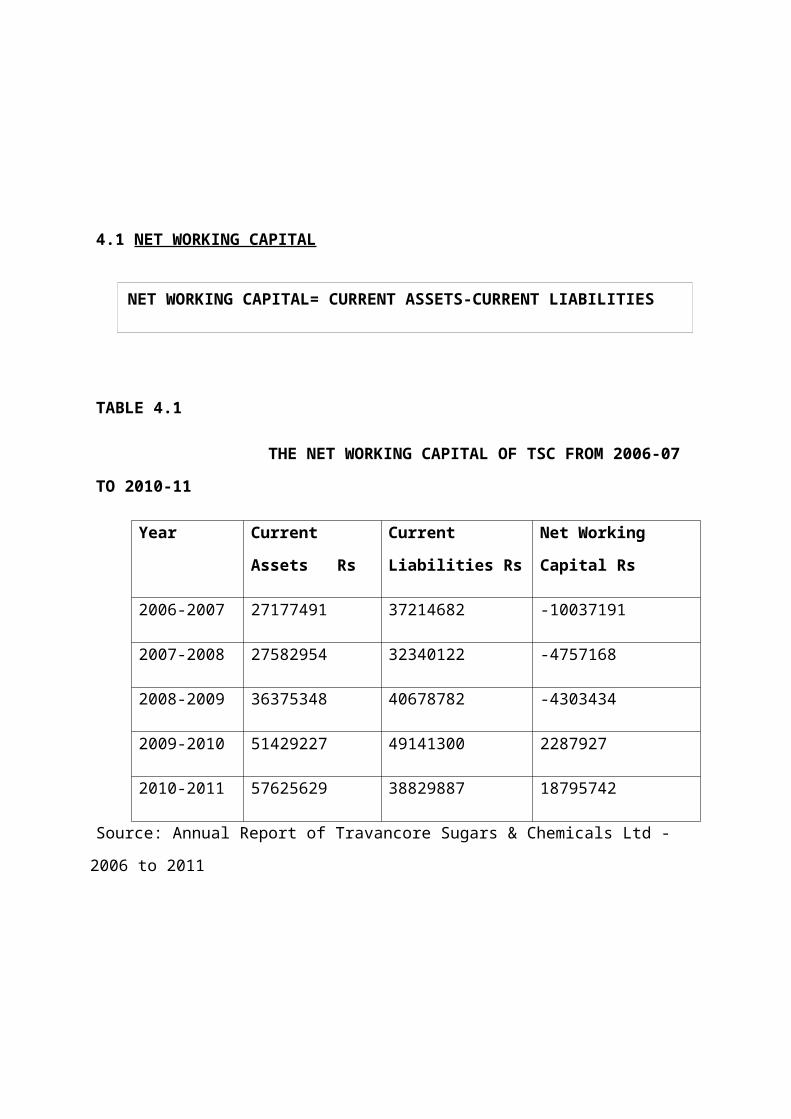

4.1 NET WORKING CAPITAL

TABLE 4.1

THE NET WORKING CAPITAL OF TSC FROM 2006-07

TO 2010-11

Year Current

Assets Rs

Current

Liabilities Rs

Net Working

Capital Rs

2006-2007 27177491 37214682 -10037191

2007-2008 27582954 32340122 -4757168

2008-2009 36375348 40678782 -4303434

2009-2010 51429227 49141300 2287927

2010-2011 57625629 38829887 18795742

Source: Annual Report of Travancore Sugars & Chemicals Ltd -

2006 to 2011

NET WORKING CAPITAL= CURRENT ASSETS-CURRENT LIABILITIES

2006-2007

2007-2008

2008-2009

2009-2010

2010-2011

-20000000

-10000000

0

10000000

20000000

30000000

40000000

50000000

60000000

70000000

Current Assets RsCurrent Liabilities RsNet Working Capital Rs

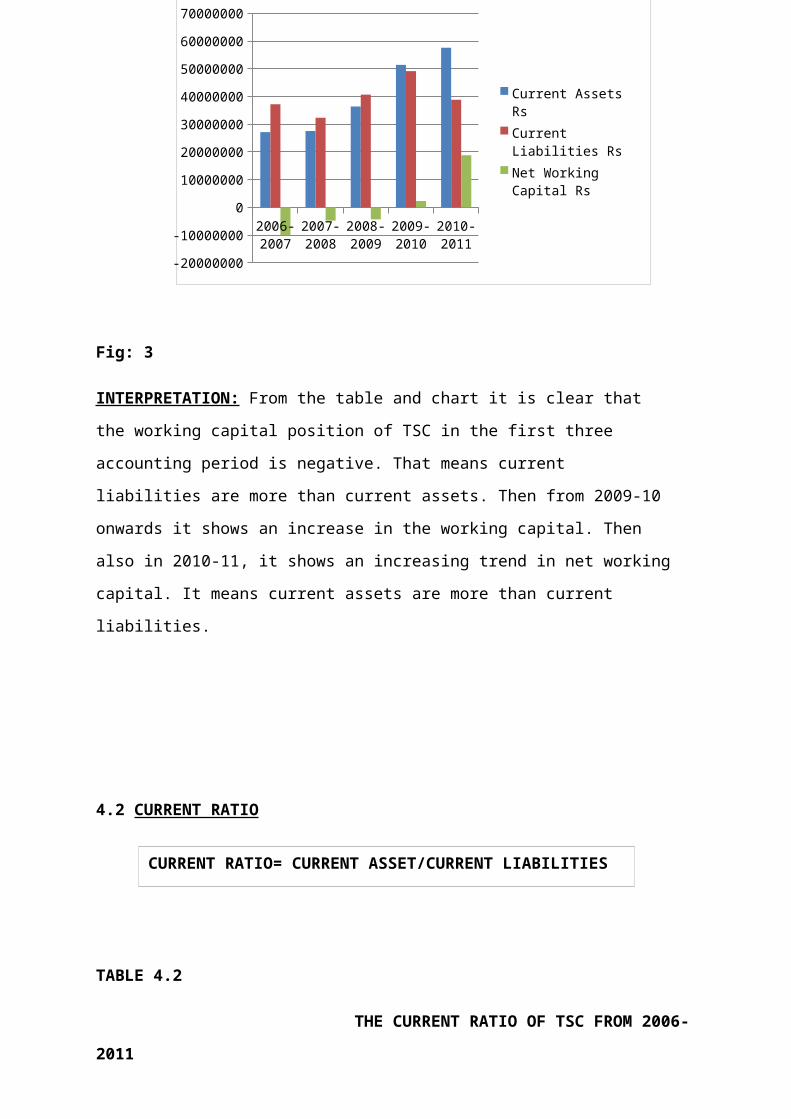

Fig: 3

INTERPRETATION: From the table and chart it is clear that

the working capital position of TSC in the first three

accounting period is negative. That means current

liabilities are more than current assets. Then from 2009-10

onwards it shows an increase in the working capital. Then

also in 2010-11, it shows an increasing trend in net working

capital. It means current assets are more than current

liabilities.

4.2 CURRENT RATIO

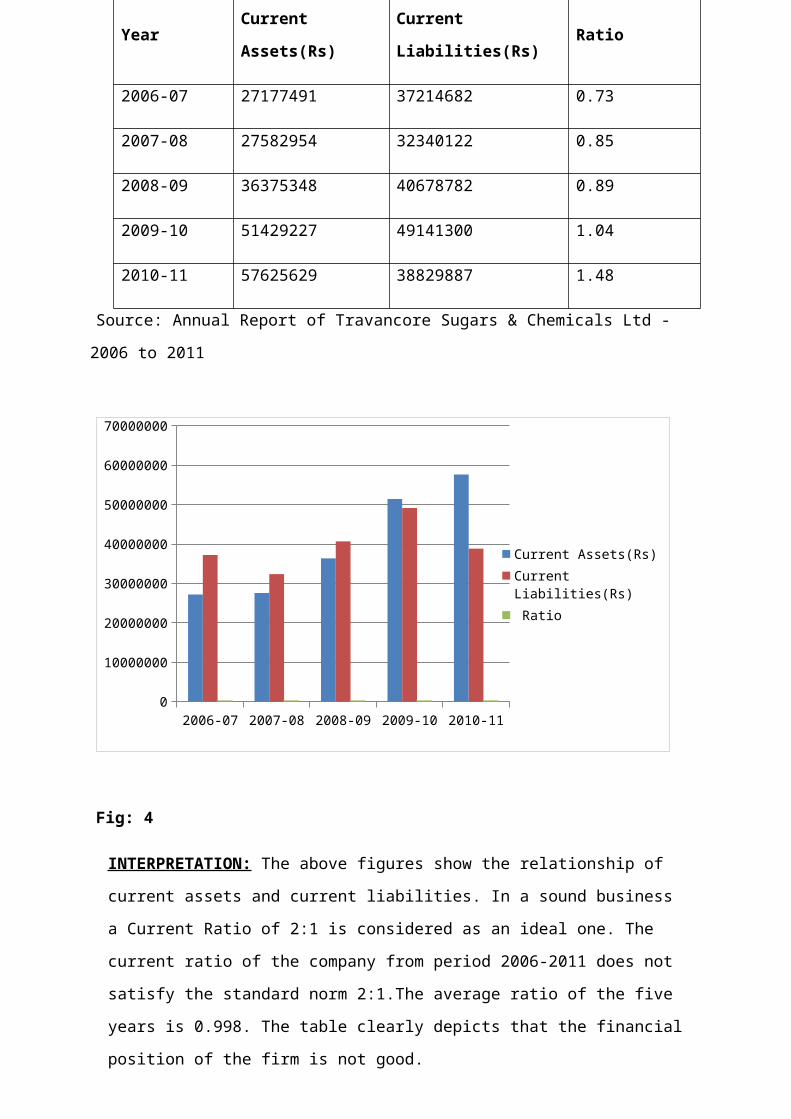

TABLE 4.2

THE CURRENT RATIO OF TSC FROM 2006-

2011

CURRENT RATIO= CURRENT ASSET/CURRENT LIABILITIES

YearCurrent

Assets(Rs)

Current

Liabilities(Rs)Ratio

2006-07 27177491 37214682 0.73

2007-08 27582954 32340122 0.85

2008-09 36375348 40678782 0.89

2009-10 51429227 49141300 1.04

2010-11 57625629 38829887 1.48

Source: Annual Report of Travancore Sugars & Chemicals Ltd -

2006 to 2011

2006-07 2007-08 2008-09 2009-10 2010-110

10000000

20000000

30000000

40000000

50000000

60000000

70000000

Current Assets(Rs)Current Liabilities(Rs) Ratio

Fig: 4

INTERPRETATION: The above figures show the relationship of

current assets and current liabilities. In a sound business

a Current Ratio of 2:1 is considered as an ideal one. The

current ratio of the company from period 2006-2011 does not

satisfy the standard norm 2:1.The average ratio of the five

years is 0.998. The table clearly depicts that the financial

position of the firm is not good.

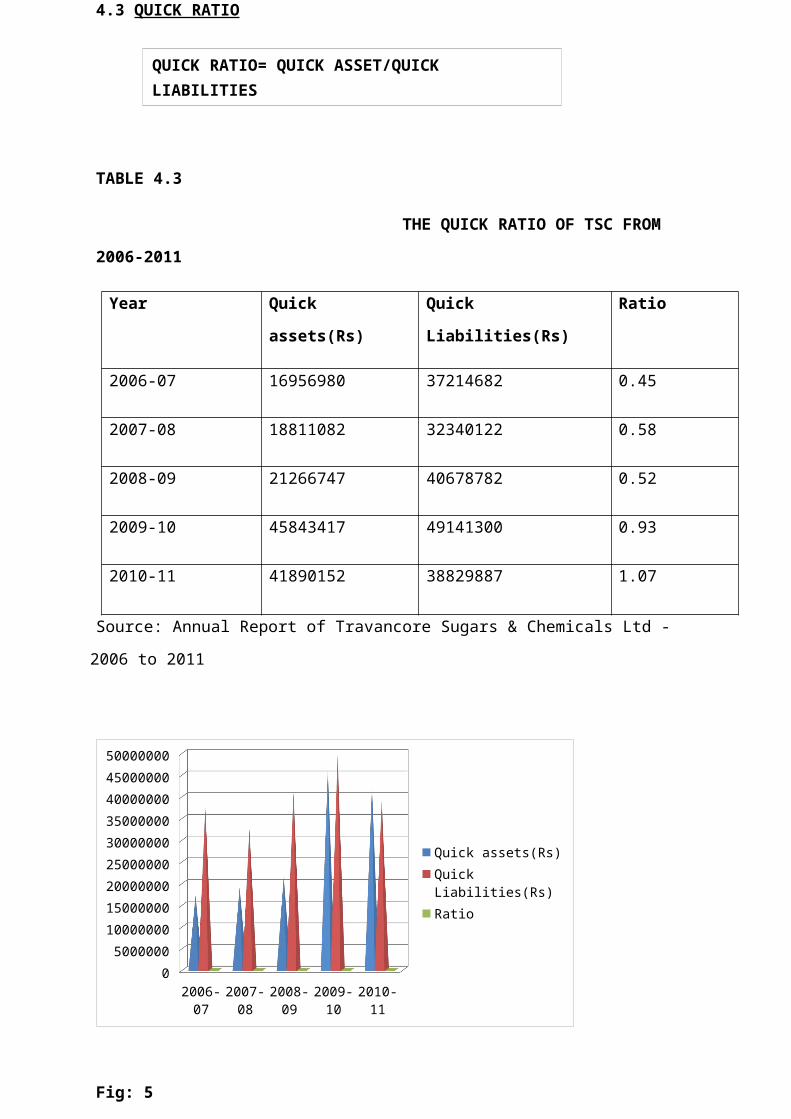

4.3 QUICK RATIO

TABLE 4.3

THE QUICK RATIO OF TSC FROM

2006-2011

Year Quick

assets(Rs)

Quick

Liabilities(Rs)

Ratio

2006-07 16956980 37214682 0.45

2007-08 18811082 32340122 0.58

2008-09 21266747 40678782 0.52

2009-10 45843417 49141300 0.93

2010-11 41890152 38829887 1.07

Source: Annual Report of Travancore Sugars & Chemicals Ltd -

2006 to 2011

2006-07

2007-08

2008-09

2009-10

2010-11

05000000100000001500000020000000250000003000000035000000400000004500000050000000

Quick assets(Rs)Quick Liabilities(Rs)Ratio

Fig: 5

QUICK RATIO= QUICK ASSET/QUICK LIABILITIES

INTERPRETATION: The above table shows the relationship between

quick assets and current liabilities. The standard norm for

quick ratio is 1:1. An examination of the above table shows

that the quick ratio of the company for the period 2010-11 is

only satisfactory and the other period’s does not satisfies

the standard norm 1:1. The average ratio of the five years is

0.71. The table clearly depicts that the financial position of

the firm is not good.

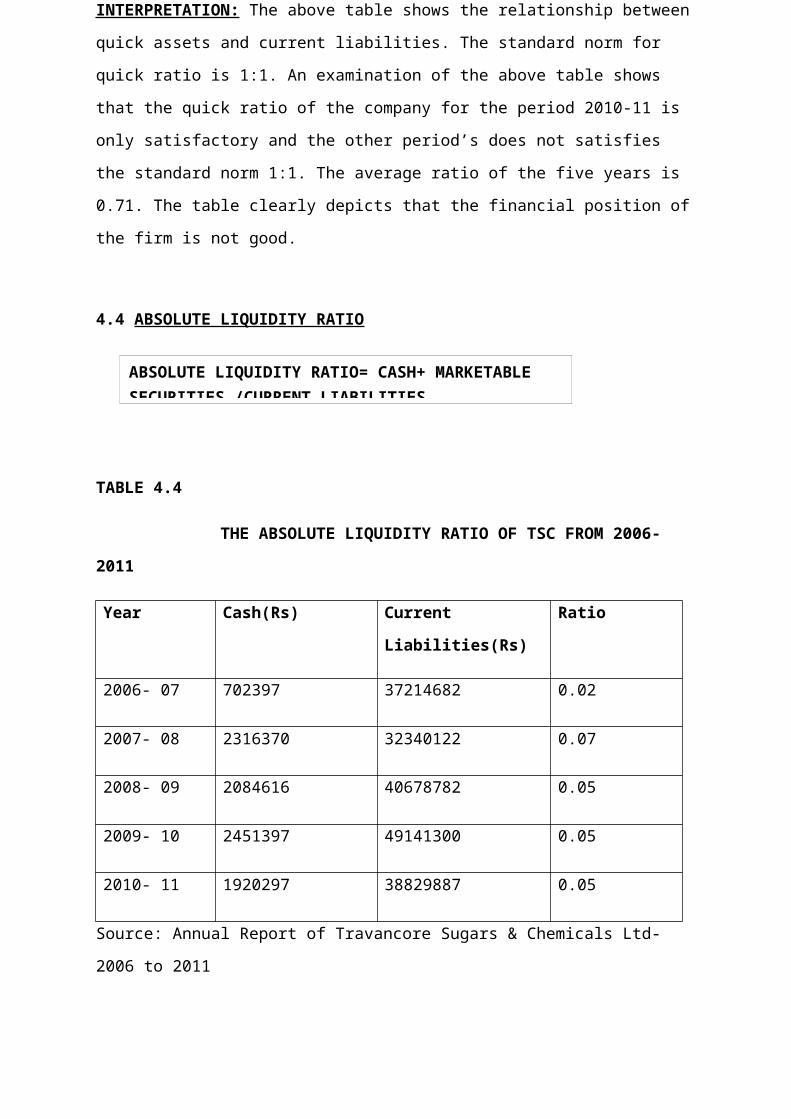

4.4 ABSOLUTE LIQUIDITY RATIO

TABLE 4.4

THE ABSOLUTE LIQUIDITY RATIO OF TSC FROM 2006-

2011

Year Cash(Rs) Current

Liabilities(Rs)

Ratio

2006- 07 702397 37214682 0.02

2007- 08 2316370 32340122 0.07

2008- 09 2084616 40678782 0.05

2009- 10 2451397 49141300 0.05

2010- 11 1920297 38829887 0.05

Source: Annual Report of Travancore Sugars & Chemicals Ltd-

2006 to 2011

ABSOLUTE LIQUIDITY RATIO= CASH+ MARKETABLE SECURITIES /CURRENT LIABILITIES

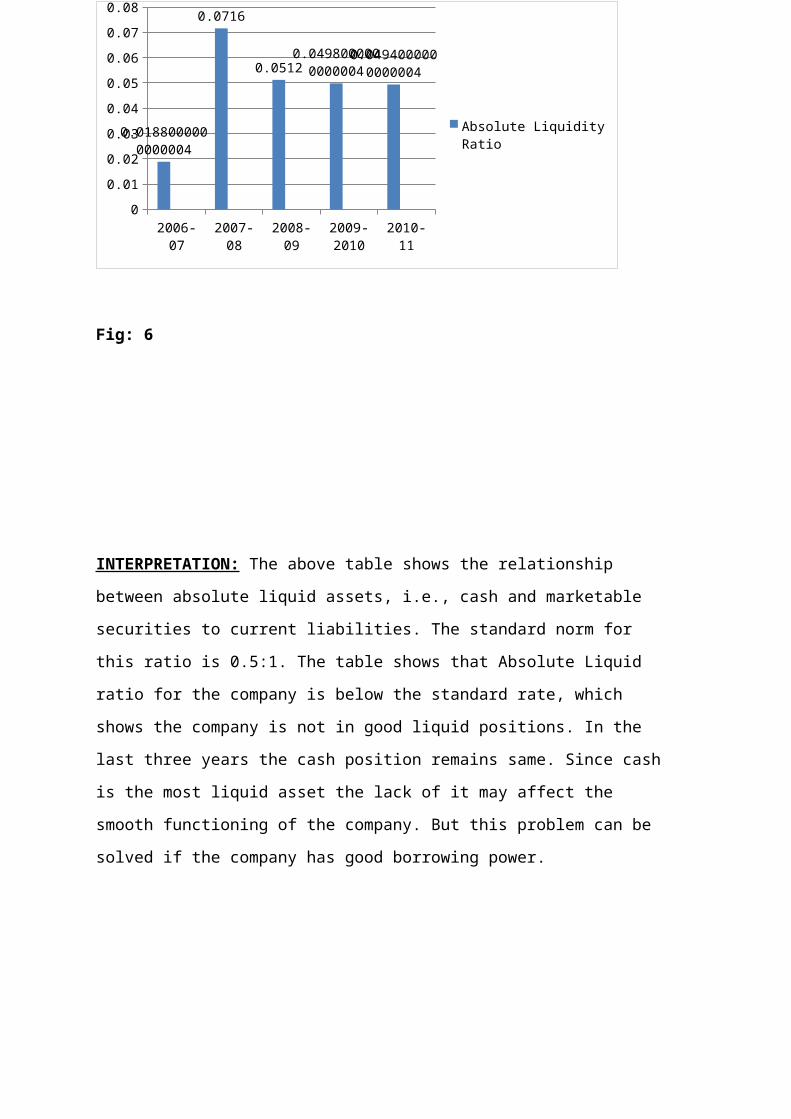

2006-07

2007-08

2008-09

2009-2010

2010-11

00.010.020.030.040.050.060.070.08

0.0188000000000004

0.0716

0.05120.0498000000000004

0.0494000000000004

Absolute Liquidity Ratio

Fig: 6

INTERPRETATION: The above table shows the relationship

between absolute liquid assets, i.e., cash and marketable

securities to current liabilities. The standard norm for

this ratio is 0.5:1. The table shows that Absolute Liquid

ratio for the company is below the standard rate, which

shows the company is not in good liquid positions. In the

last three years the cash position remains same. Since cash

is the most liquid asset the lack of it may affect the

smooth functioning of the company. But this problem can be

solved if the company has good borrowing power.

TURNOVER RATIO OR EFFICENCY RATIO

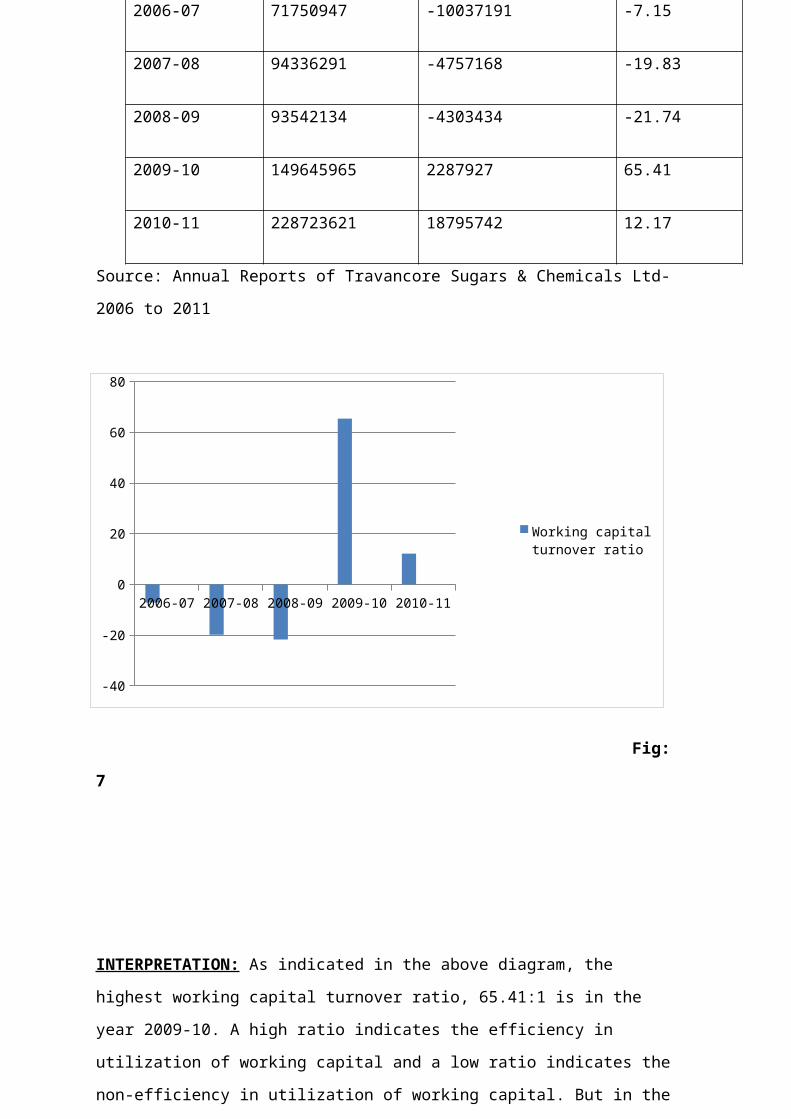

4.5 WORKING CAPITAL TURNOVER RATIO

TABLE

4.5

THE WORKING CAPITAL TURNOVER RATIO OF TSC FROM 2006-2011

Year Net Sales(Rs) Net working

capital(Rs)

Ratio (%)

Working Capital Turnover Ratio = Net Sales ÷ Net

Working Capital

2006-07 71750947 -10037191 -7.15

2007-08 94336291 -4757168 -19.83

2008-09 93542134 -4303434 -21.74

2009-10 149645965 2287927 65.41

2010-11 228723621 18795742 12.17

Source: Annual Reports of Travancore Sugars & Chemicals Ltd-

2006 to 2011

2006-07 2007-08 2008-09 2009-10 2010-11

-40

-20

0

20

40

60

80

Working capital turnover ratio

Fig:

7

INTERPRETATION: As indicated in the above diagram, the

highest working capital turnover ratio, 65.41:1 is in the

year 2009-10. A high ratio indicates the efficiency in

utilization of working capital and a low ratio indicates the

non-efficiency in utilization of working capital. But in the

first three years the ratio is negative which means the

firm’s working capital is not good.

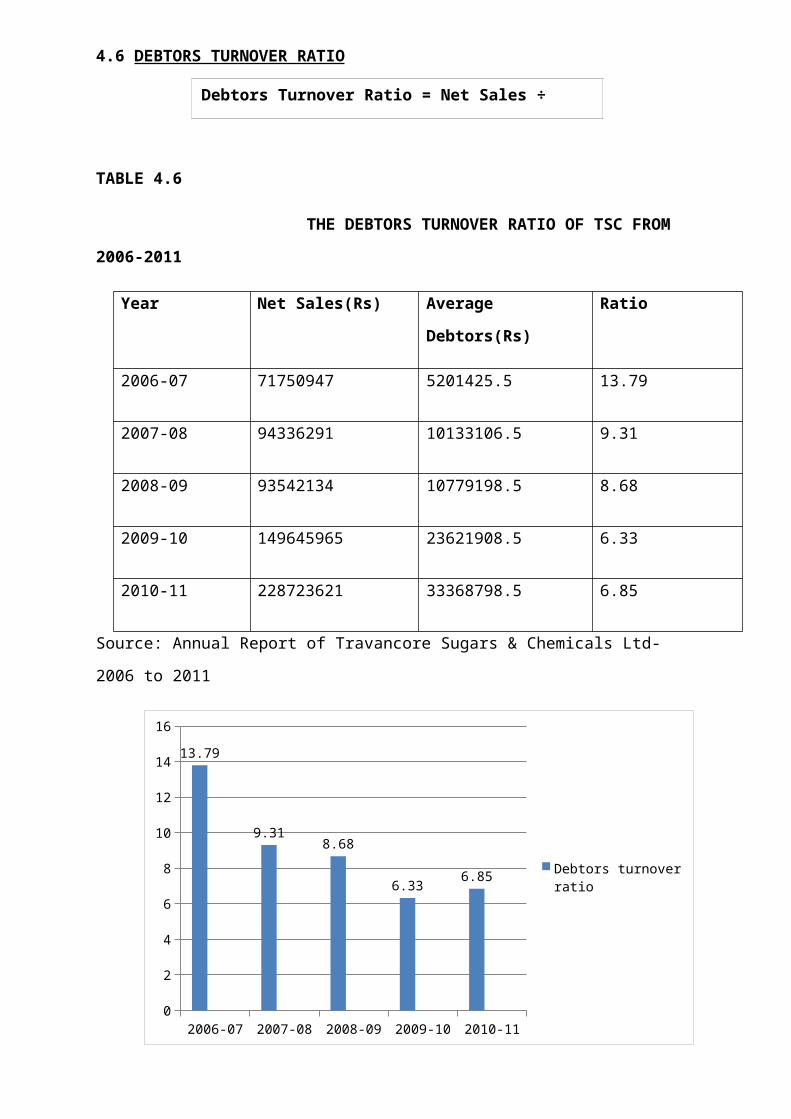

4.6 DEBTORS TURNOVER RATIO

TABLE 4.6

THE DEBTORS TURNOVER RATIO OF TSC FROM

2006-2011

Year Net Sales(Rs) Average

Debtors(Rs)

Ratio

2006-07 71750947 5201425.5 13.79

2007-08 94336291 10133106.5 9.31

2008-09 93542134 10779198.5 8.68

2009-10 149645965 23621908.5 6.33

2010-11 228723621 33368798.5 6.85

Source: Annual Report of Travancore Sugars & Chemicals Ltd-

2006 to 2011

2006-07 2007-08 2008-09 2009-10 2010-110

2

4

6

8

10

12

14

1613.79

9.318.68

6.33 6.85 Debtors turnover ratio

Debtors Turnover Ratio = Net Sales ÷ Average Debtors

Fig:

8

INTERPRETATION: Debtors Turnover ratio indicates the no of

times debtors turnover each year. Higher the value of debtors

turnover, the more efficient is the management of credit

because the collection period of the debtors will low. highest

debtors turnover ratio is recorded in 2006-07 with 13.57. .

Then it decreases from 2006-07 to 2009-10. Then in 2010-11,

there is a little increase in the ratio. The increased Debtors

Turnover Ratio shows the better management in debtors

collection.

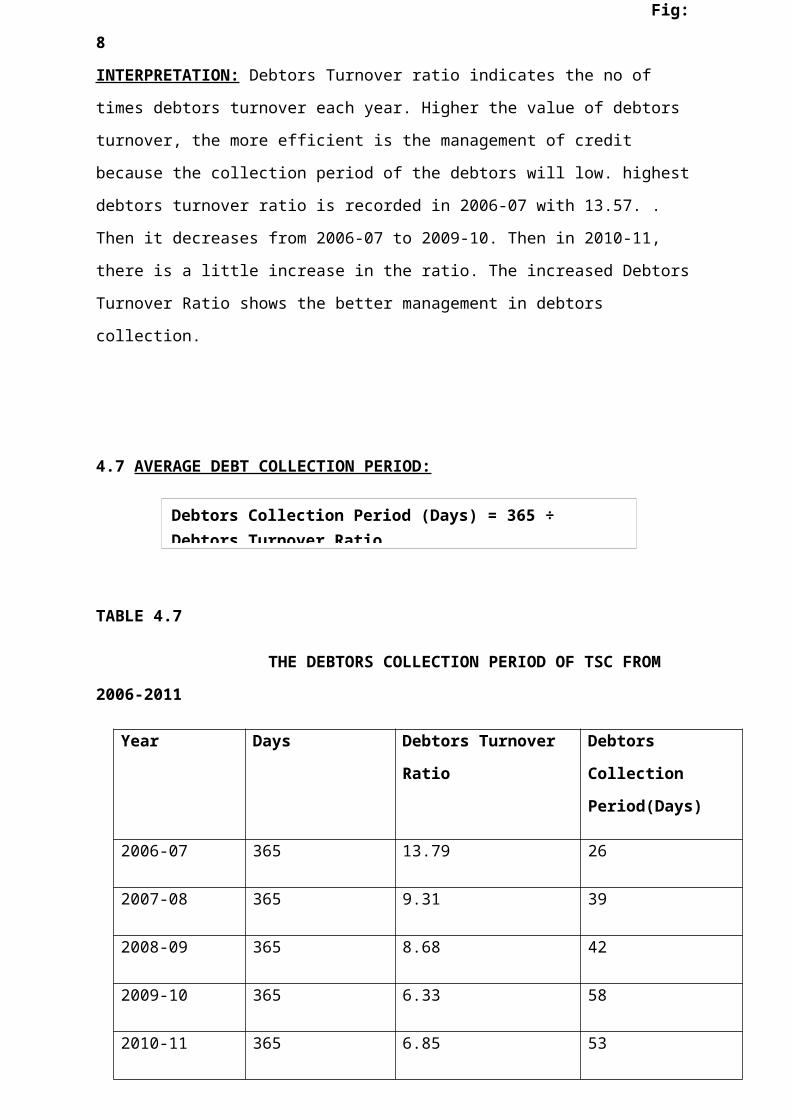

4.7 AVERAGE DEBT COLLECTION PERIOD:

TABLE 4.7

THE DEBTORS COLLECTION PERIOD OF TSC FROM

2006-2011

Year Days Debtors Turnover

Ratio

Debtors

Collection

Period(Days)

2006-07 365 13.79 26

2007-08 365 9.31 39

2008-09 365 8.68 42

2009-10 365 6.33 58

2010-11 365 6.85 53

Debtors Collection Period (Days) = 365 ÷ Debtors Turnover Ratio

Source: Annual Report of Travancore Sugars & Chemicals Ltd-

2006 to 2011

2006-07

2007-08

2008-09

2009-10

2010-11

050

100150200250300350400

DaysDebtors Turnover RatioDebtors Collection Period(Days)

Fig: 9

INTERPRETATION: The average collection period increased from

2006-07 to 2009-10 and then it decreases on 2010-11. The

increasing average collection period shows the inefficiency of