Embed Size (px)

Citation preview

Assignment on

Monetary Policy ofBangladesh

Course Code: MBM 506Section: 01

Submitted ToProfessor Abdul Bayes

Submitted By

Md. Asaduzzaman Rana

Date of submission: 13-08-2014

Introduction:

The Central Bank is the highest authority employed by thegovernment for formulation of monetary policy to guide theeconomy in a certain country. Monetary policy is defined asthe regulation of the money supply and interest rates by acentral bank. Monetary policy also refers to how the centralbank uses interest rates and the money supply to guideeconomic growth by controlling inflation and stabilizingcurrency. Like any other central bank, Bangladesh Bank isperforming the role to formulate monetary policy inBangladesh.

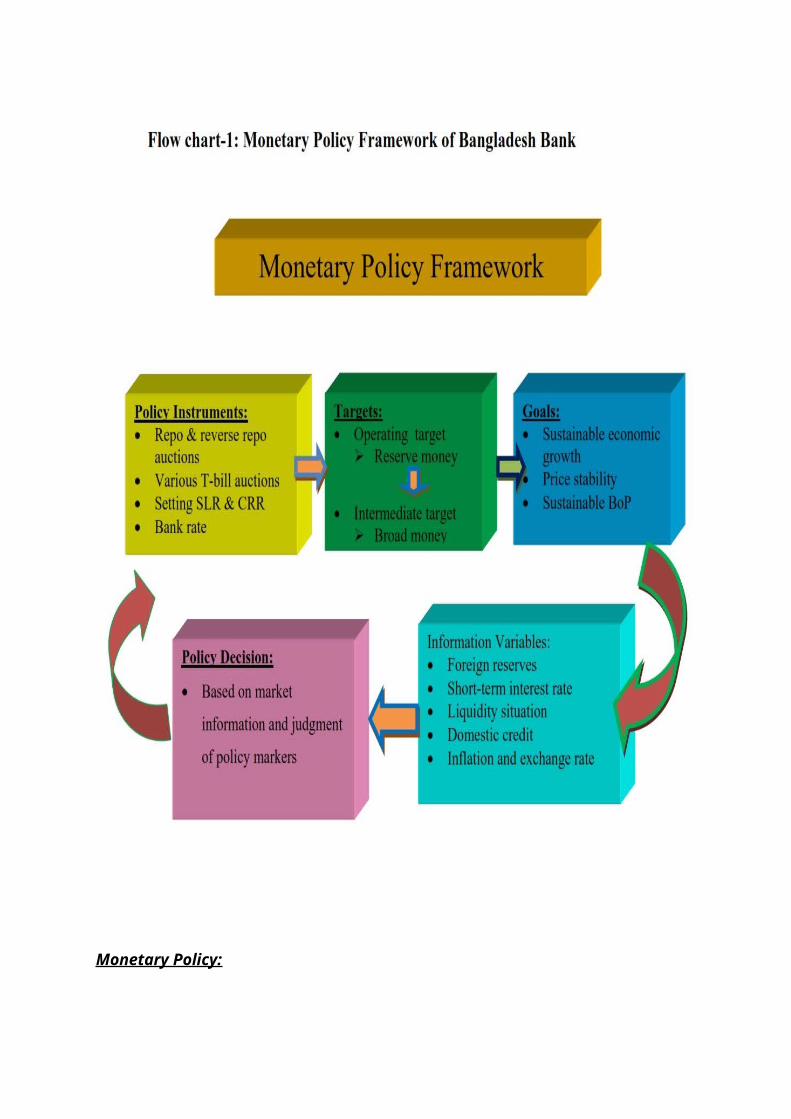

The monetary policy framework of Bangladesh Bank identifies alogical sequential set of actions for designing and conductingthe monetary policy. The framework is based on credibleinformation on the stability of the money demand function, themoney supply process, and the monetary transmission mechanism.Monetary policy in Bangladesh is framed using projected realGDP growth rate. The targeted rate of inflation adopts ReserveMoney (RM) and Broad Money (M2) as operating and intermediatetargets respectively connecting between different policiesinstruments like repo, reverse repo rates, bank rate, CashReserve Requirement (CRR) and Statutory Liquidity Requirement(SLR).

The control of money supply is an important policy tool inconducting monetary policy. The success of monetary policydepends on the degree of predictability, measurability andcontrollability that the monetary authority has over moneysupply.

Within the framework, the monetary policy aims at supportinghighest sustainable output growth along with reasonable pricestability and smooth adjustment to internal and externalshocks faced by the economy. The process uses repo, reverserepo, and Bangladesh Bank bill rates as policy instruments forinfluencing financial and real sector prices toward thetargeted path of inflation. The underlying assumption is thatgrowth of monetary aggregates (such as RM and M2) has apredictable relationship with the domestic price level.Therefore, by controlling the growth of monetary aggregates,Bangladesh Bank aims at achieving price stability. Inpractice, Bangladesh Bank sets a growth rate of RM that isdeemed to be consistent with targeted inflation and outputgrowth, with the idea that the RM growth will in turn lead,through money multiplier, to a given growth rate of M2 in theeconomy.

Monetary policy consists of a set of rules that aim atregulating the supply of money in accordance withpredetermined goals. Monetary policy is important because itcan influence economic growth, inflation, and the balance ofpayments (BOP). The central bank conducts monetary policy byusing instruments that influence the supply of money andinterest rates in the economy. The fundamental objective ofpursuing monetary policy by the central bank is to ensure thatthe expansion in the money supply is consistent with theobjectives of the government policies for economic growth,inflation, and the BOP. In conducting monetary policy, thecentral bank tries to ensure that the supply of money is inline with the amount of money demanded by the economic agents:households and firms. The main policy goals of monetary policyof Bangladesh Bank are:

To achieve sustainable economic growth To maintain price stability To attain sustainable BoP.

Monetary Policy:

Monetary policy is the term used by economists to describeways of managing the supply of money in an economy. MonetaryPolicy is the management of money supply and interest rates bycentral bank to influence prices and employment for achievingthe objectives of general economic policy. Monetary policyworks through expansion or contraction of investment andconsumption expenditure.

According to Paul Einzig

“Monetary policy includes all monetary decisions and measuresirrespective of whether their aims are monetary and non-monetary, and all non-monetary decisions and measures that aimit affecting the monetary system.”

According to Harry G. Johnson

“Monetary policy employing the central band’s control ofsupply of money as an instrument for achieving the objectivesof general economic policy.”

According to G.K. Shaw

“By monetary policy we mean any conscious action undertaken bythe monetary authorities, to exchange the quantity, or cost(interest rate) of money.”

From the above discussion, monetary policy may be defined asthe central bank’s policy pertaining to the control of theavailability, cost and use of money and credit with the helpof monetary measures in order to achieve specific goals.

Objectives of Monetary Policy:

Monetary policy aims and methods have changed over time. Bothin developed and developing economies, monetary policies seekto maintain price stability by sustained stable output growthin the face of internal and external shocks that are facedfrom time to time.

In developed economies with production factors at or close tofull employment, monetary policies are formulated typicallywith the output gap (difference between the actual and thelonger run potential output) in view; the policy stance iseased to provide stimulus at times of slowdown when actualoutput lags the longer run potential, and the stance istightened to slow things down when the economy overheats withactual output running ahead of the sustainable longer runpotential.

Diagnosing and treating asset price bubbles symptomatic ofoverheating are major issues of current debate in monetarypolicy.

For developing economies like Bangladesh with significantunderemployment/ under exploitation of production factors,stimulating higher growth is imperative for rapid reductionand eventual elimination of endemic poverty, and is thereforean overriding priority. The stimulus provided by monetarypolicies in accommodating the growth aspirations must nothowever over step towards macroeconomic imbalancedestabilizing and jeopardizing future growth; and the pursuitof monetary policies comprise the continual balancing act ofsupporting the highest sustainable output growth whileadjusting smoothly to internal and external shocks that theeconomy encounter from time to time.

The primary objective of the Monetary Policy of Bangladesh isto outline the formulation and implementation of monetarypolicy of the Bangladesh Bank (BB), and to convey itsassessment of the recent and the expected monetary andinflation developments to the stakeholders and the public atlarge.

The Bangladesh Bank Order of 1972 outlines the main objectivesof monetary policy in Bangladesh, which comprises—

To achieve the price stability To regulate currency and reserves

To promote and maintain a high level of production,employment and real income, and economic growth, sinceindependence BB operated under a variety of peggedexchange rate systems amid capital controls

To manage the monetary and credit system To maintain the par value of domestic currency To promote growth and development of the country's

productive resources in the best national interest

Although the long-term focus of monetary policy in Bangladeshis on growth with stability, the short-term objectives aredetermined after a careful and realistic appraisal of thecurrent economic situation of the country.

In effect, the exchange rate served as a nominal anchor, withthe ultimate goal of maintaining price stability. However,prices of non-tradable goods, given the latter’s high share innational expenditure, dominated the inflation behavior. Indeedthe prevailing exchanges rate during the 1970s and 80sremained mostly overvalued, which was also accompanied by high(typically double-digit) inflation.

Strategy of Monetary Policy:

The MPS (Monetary Policy Statement) starts with expression ofthe monetary policy frameworks in terms of the goals,instruments, and the channels of transmission. Maintainingprice stability while supporting the highest sustainableoutput growth is the stated objective of monetary policiespursued by the Bangladesh Bank.

Instruments of Monetary Policy:

In 1989, the government adopted a comprehensive FinancialSector Reform Programme (FSRP), following which the country'smonetary policy assumed a new orientation towards promotion ofmarket economy in a competitive environment. Bangladesh Bankstarted moving away from direct quantitative monetary controlto indirect methods of monetary management since the beginning

of 1990. Although, the fixation of target continued to remainas the central piece of exercise, the way to achieve it hadbeen changed. Credit ceilings on individual banks and directcontrols of interest rates were withdrawn. At present, themoney supply is regulated through indirect manipulation ofreserve money instead of credit ceiling. Major instruments ofmonetary control available with Bangladesh Bank are the bankrate, open market operations, rediscount policy, and statutoryreserve requirement.

The methods of credit control can be classified as follows:

a. Quantitative/ General Methods:

01. Bank rate policy

02. Open market policy

03. Variation of reserve ratio

b. Qualitative/ General Methods:

01. Rationing of credit

02. Direct action

03. Regulation of consumers’ credit

04. Moral persuasion

05. Publicity

Major Instruments Use by Bangladesh Bank:

Major instruments of monetary control available withBangladesh Bank are the bank rate, open market operations,rediscount policy, and statutory reserve requirement.

►Bank rate

Until 1990, the use of this instrument as the lending rate ofthe central bank for borrowings of the commercial banks to

meet their temporary needs was virtually non-existent inBangladesh. The rate was changed in a few occasions only toalign it with the re fixation of the rates of deposits andadvances. Moreover, the existence of refinance facilities atrates lower than the bank rate substantially eroded itssignificance. However, since 1990, the instrument has been putin use to change the cost of borrowings for banks and therebyto affect the market rate of interest. Bank rate was graduallylowered from 9.75% in January 1990 to 5% in March 1994. It wasraised to 5.75% from 10 September 1995 and further, to 7.5%and 8% from 19 May 1997 and 20 November 1997 respectively. Therate was lowered to 7% from 29 August 1999.

► Open market operations (OMO)

These involve the sale or purchase of securities by thecentral bank to withdraw liquid funds from the banking systemor inject the same into that system. OMO allows flexibility interms of both the amount and timing of intervention, which didnot exist in Bangladesh before 1990. Bangladesh Bankintroduced a 91-day Bangladesh Bank Bill, a market-based toolfor monetary intervention, in December 1990. The bank bill wassubsequently withdrawn from the market. At present, OMOoperations are conducted through participation of banks inmonthly or fortnightly/weekly auctions of treasury bills.

► Rediscount policy

After the introduction of FSRP, the refinance facility wasreplaced by rediscount facility at bank rate to eliminatediscrimination in access to central bank funds. Refinancefacility is now available for agricultural credit provided byBangladesh krishi bank and for projects of Bangladesh RuralDevelopment Board financed by sonali bank. Banks are advisedto extend credit considering banker-customer relationship.

► Statutory reserve requirement

Cash reserve requirement (CRR) of the deposit money banks hasa significant potential to regulate money supply throughaffecting money multiplier, while statutory liquidityrequirement (SLR) is generally used to affect the lendingcapability of the bank. Bangladesh Bank used these twoinstruments very infrequently before 1990 and very often after1990. The CRR and SLR were 8% and 23% respectively on 25 April1991 and were reduced to 7% and 22% respectively on 5 December1991. Later, these rates were changed twice and set at 5% and20% respectively on 24 May 1992. The CRR was further loweredto 4% from 4 October 1999. The downward revision in CRR andSLR were made to enable the banks to increase their lendingcapacity.

Frameworks of Bangladesh’s Monetary Policy:

The Policy Target(s)

In this backdrop, it is necessary that the monetary policyframework (in terms of the goals, the instruments, and theanalytic channels of transmission) be articulated for greaterclarity and transparency benefiting both the policy makers aswell as the stakeholders. A policy system, where the goals aretransparent and their achievement verifiable, directly adds tothe credibility of the central bank, a major objective of thisdocument is to define such a framework. Most industrialeconomy monetary policy is run with the task of keeping watchon both the output gap (i.e., the deviation of actual outputfrom its long-run equilibrium level) and the inflation gap,which is similarly defined. In contrast, however, thechallenge in the developing world is how to augment thecapacity output through both productivity growths as well asvia the installation of additional capacity. Faster growth inmost developing contexts is necessary to reduce (andeventually eliminate) common poverty. Hence, the appropriatemonetary policy strategy in the Bangladesh context would be toachieve the goal of price stability with the highestsustainable output growth. Any monetary stimulus to promote

growth must keep in perspective the broader goal ofmacroeconomic stability, which is a prerequisite for futuregrowth. Price stability would also include the stability ofthe currency regime. While fiscal policy too is relevant inaddressing these goals and thus there is a need for policycoordination, monetary policy must play its due role. Whileleading central banks in the industrial world haveincreasingly adopted the unitary goal of fighting inflation,interestingly directive by enumerating

(a) The promotion of price stability,

(b) Ensuring full employment,

(c) Supporting global economic and financial stability(so long as the latter may be targeted withoutprejudicing the first two goals) as the chief monetarypolicy goals.

In broad terms, therefore the latter view is consistent withthe BB vision as enunciated above, although anchored alongdifferent perspectives.

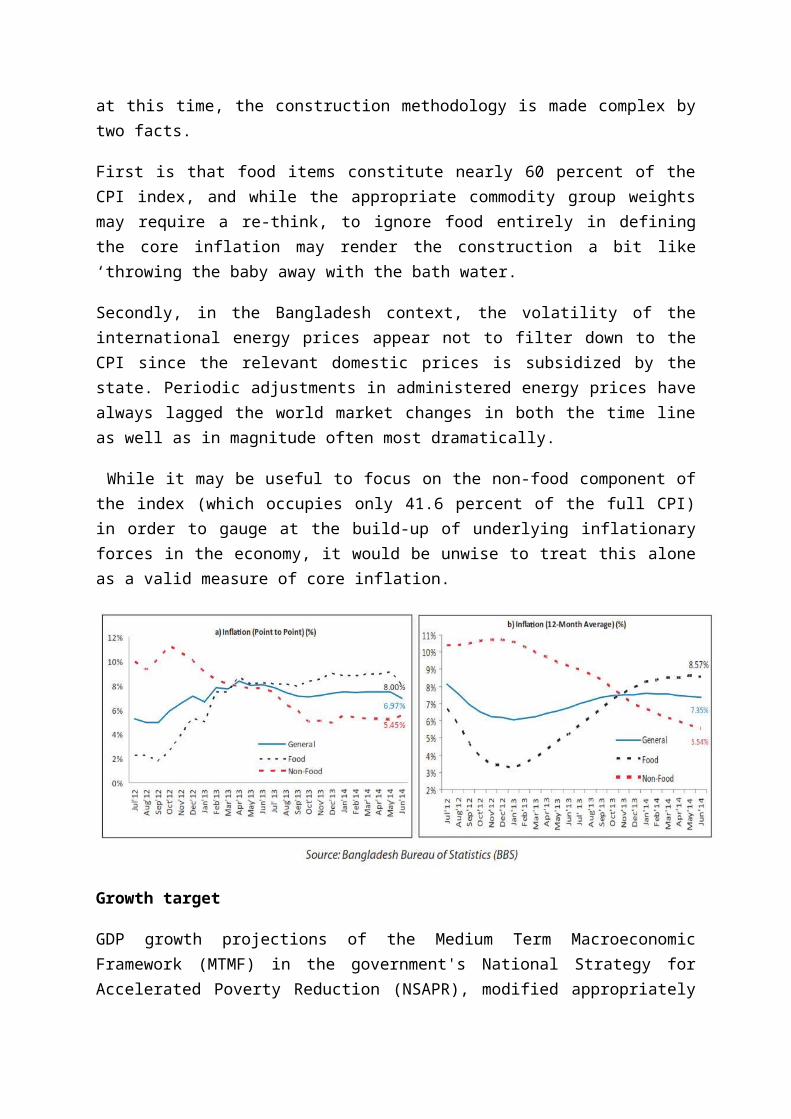

Inflation Target

It is the general wisdom that monetary policy tools are ofimmediate influence in controlling inflation. However,contemporary evidence amply illustrates that monetary policycannot deal well with the inflationary impact of externalshocks such as the recent international price of oil andrelated energy products. Many central banks therefore focus onthe core inflation, which is typically constructed bysubtracting the most volatile components (e.g., food andenergy prices, indirect taxes etc.) from the consumer priceindex (CPI). The Bank of Canada argues that it is the coreconcept that better predicts the underlying price stability inthe economy. Hence as a policy goal, core inflation may be amore credible target than CPI inflation. While there is nostandard measure of core inflation in the Bangladesh context

at this time, the construction methodology is made complex bytwo facts.

First is that food items constitute nearly 60 percent of theCPI index, and while the appropriate commodity group weightsmay require a re-think, to ignore food entirely in definingthe core inflation may render the construction a bit like‘throwing the baby away with the bath water.

Secondly, in the Bangladesh context, the volatility of theinternational energy prices appear not to filter down to theCPI since the relevant domestic prices is subsidized by thestate. Periodic adjustments in administered energy prices havealways lagged the world market changes in both the time lineas well as in magnitude often most dramatically.

While it may be useful to focus on the non-food component ofthe index (which occupies only 41.6 percent of the full CPI)in order to gauge at the build-up of underlying inflationaryforces in the economy, it would be unwise to treat this aloneas a valid measure of core inflation.

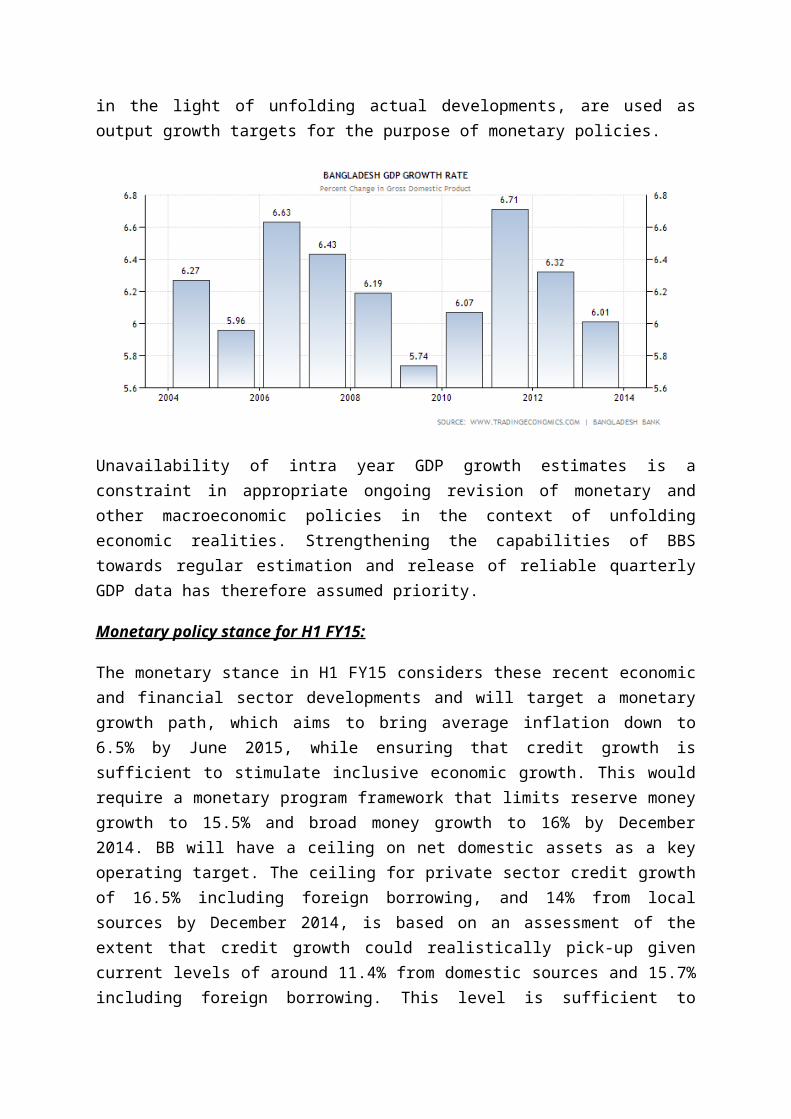

Growth target

GDP growth projections of the Medium Term MacroeconomicFramework (MTMF) in the government's National Strategy forAccelerated Poverty Reduction (NSAPR), modified appropriately

in the light of unfolding actual developments, are used asoutput growth targets for the purpose of monetary policies.

Unavailability of intra year GDP growth estimates is aconstraint in appropriate ongoing revision of monetary andother macroeconomic policies in the context of unfoldingeconomic realities. Strengthening the capabilities of BBStowards regular estimation and release of reliable quarterlyGDP data has therefore assumed priority.

Monetary policy stance for H1 FY15:

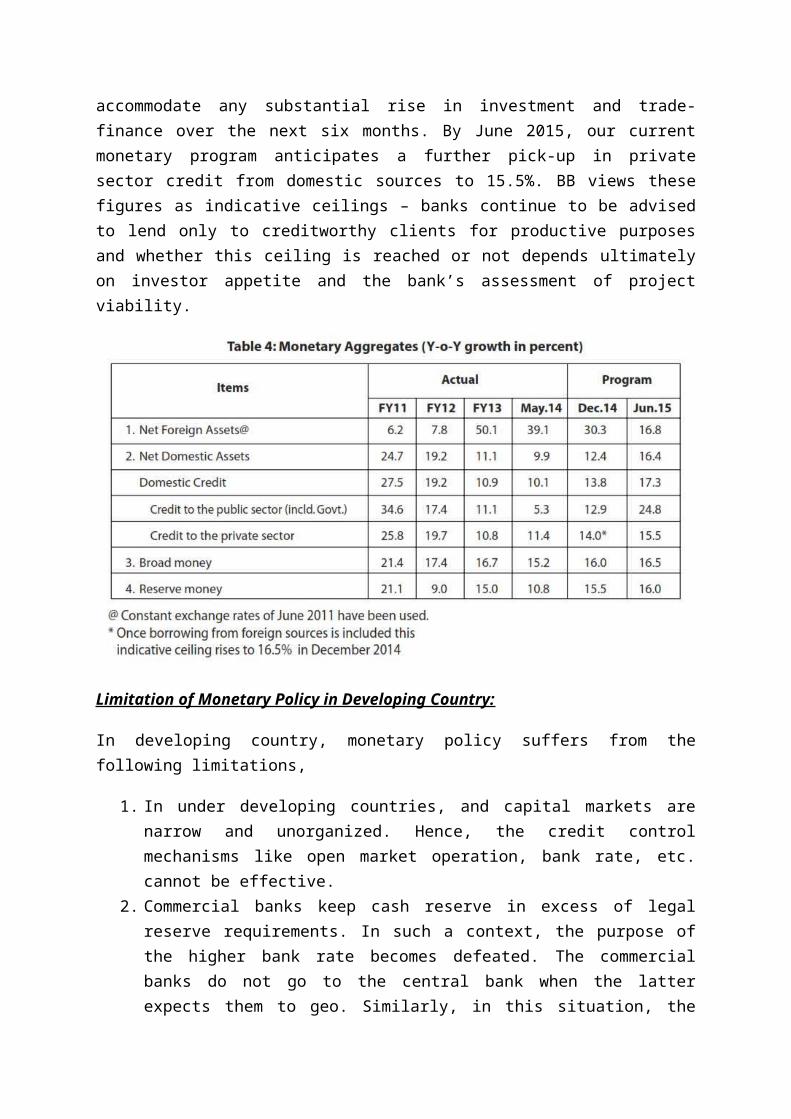

The monetary stance in H1 FY15 considers these recent economicand financial sector developments and will target a monetarygrowth path, which aims to bring average inflation down to6.5% by June 2015, while ensuring that credit growth issufficient to stimulate inclusive economic growth. This wouldrequire a monetary program framework that limits reserve moneygrowth to 15.5% and broad money growth to 16% by December2014. BB will have a ceiling on net domestic assets as a keyoperating target. The ceiling for private sector credit growthof 16.5% including foreign borrowing, and 14% from localsources by December 2014, is based on an assessment of theextent that credit growth could realistically pick-up givencurrent levels of around 11.4% from domestic sources and 15.7%including foreign borrowing. This level is sufficient to

accommodate any substantial rise in investment and trade-finance over the next six months. By June 2015, our currentmonetary program anticipates a further pick-up in privatesector credit from domestic sources to 15.5%. BB views thesefigures as indicative ceilings – banks continue to be advisedto lend only to creditworthy clients for productive purposesand whether this ceiling is reached or not depends ultimatelyon investor appetite and the bank’s assessment of projectviability.

Limitation of Monetary Policy in Developing Country:

In developing country, monetary policy suffers from thefollowing limitations,

1. In under developing countries, and capital markets arenarrow and unorganized. Hence, the credit controlmechanisms like open market operation, bank rate, etc.cannot be effective.

2. Commercial banks keep cash reserve in excess of legalreserve requirements. In such a context, the purpose ofthe higher bank rate becomes defeated. The commercialbanks do not go to the central bank when the latterexpects them to geo. Similarly, in this situation, the

instrument of reserve requirement does not functionproperly.

3. A narrow bill market makes the discount rate ineffective.4. The existence of non-bank financial intermediaries also

makes the credit control measures of the central bankineffective, because, such intermediaries like sahukar,village moneylender, etc. cannot be brought under thecontrol and regulation of the banking system.

5. For all these reasons, monetary policy for controllinginflation in backward countries has not been veryeffective.

6. In order developed countries, banking habits are alsounderdeveloped which hampers the effectiveness ofmonetary policy seriously.

7. In backward countries, monetary expansion generally leadsto increase imports, unfavorable balance of payments andloss of gold reserve, etc.

8. By its nature, monetary policy is not effective in theshort run.

9. The role of monetary policy is not compulsive butpermissive. This seriously limits the efficiency ofmonetary policy in backward countries.

10. In under developed society where liquidity trap isin existence monetary policy cannot work efficiently.

11. Administrative honesty and firmness are not veryrigorous in less developed countries, which reduce theefficiency of monetary policy a policy a lot.

12. Lastly, the lag between the decision about aparticular policy and its implementation also hinders themonetary policy in its success.

Here we found that monetary policy suffers from variouslimitations in the developing country. So, it should besupplemented by fiscal policy to make it effective. Despitethis information, monetary policy sets the tone of economicdevelopment in recent years.

Conclusion:

The Monetary Policy Statement (MPS) is intended to outline theobjective and the modalities of formulation and conducting ofmonetary policies by the Bangladesh Bank, its assessment ofthe recent and the expected monetary and price developments,and the stance of monetary policies that will be pursued overthe near term .Objectives of the monetary policies of theBangladesh Bank as outlined in the Bangladesh Bank Order, 1972comprise attaining and maintaining of price stability, highlevels of production, employment and economic growth. In sucha directed regime with little or no role of financial pricesin influencing the magnitudes or directions of credit thepresent MPS (Monetary Policy Statement) provides the monetarypolicy stance that BB (Bangladesh Bank) intends to followduring the second half: July-December 2014: H1FY15. The primeobjective of the policy stance is to ensure the use of thefinancial instruments towards promoting real sector growth atits targeted level along with ensuring reasonable pricestability.