Embed Size (px)

Citation preview

MaximizingTheEmployeeRetentionCredit

Presented By:JeremyMorris,CPA&MarkGingrich,CPA,JD

Housekeeping Items:• Wehavemutedallparticipantstoeliminatebackgroundnoise.PleaseusetheQ&Afeaturetosubmitanyquestions/comments.

• Thewebinarisbeingrecordedandboththerecordingandtheslideswillbeavailablelatertodayhere:https://williamskeepers.com/recap-of-boss-seminars/

Howdidwegethere?

© 2021 Williams-Keepers, LLC

• Nearlyoneyearagototheday(March27,2020),theCoronavirusAid, Relief,andEconomicSecurity(CARES) Actwassignedintolawto provideeconomicstimulusinresponsetotheCOVID-19pandemic.

• Amongthevariousprovisionsofthis247-page,$1.8trillionbillwas thecreationofanEmployeeRetentionTaxCredit(ERC),designedto benefitbusinessesthatsufferedsignificantreductionsinrevenue and/orfullorpartialsuspensionofoperationsduetoCOVID-related governmentmandatesbutwhoneverthelessmaintainedpayroll.

Howdidwegethere?

© 2021 Williams-Keepers, LLC

• For2020,theERCmaxesoutat$5,000peremployeeannually.Thus, aneligible50-employeebusinesscouldpossiblyreceive$250,000in taxcredits!

• Andyet,theresponsefrommostbusinessesandadvisorswasa collective“Meh.”

• Thereason?

© 2021 Williams-Keepers, LLC

PPP

Howdidwegethere?

© 2021 Williams-Keepers, LLC

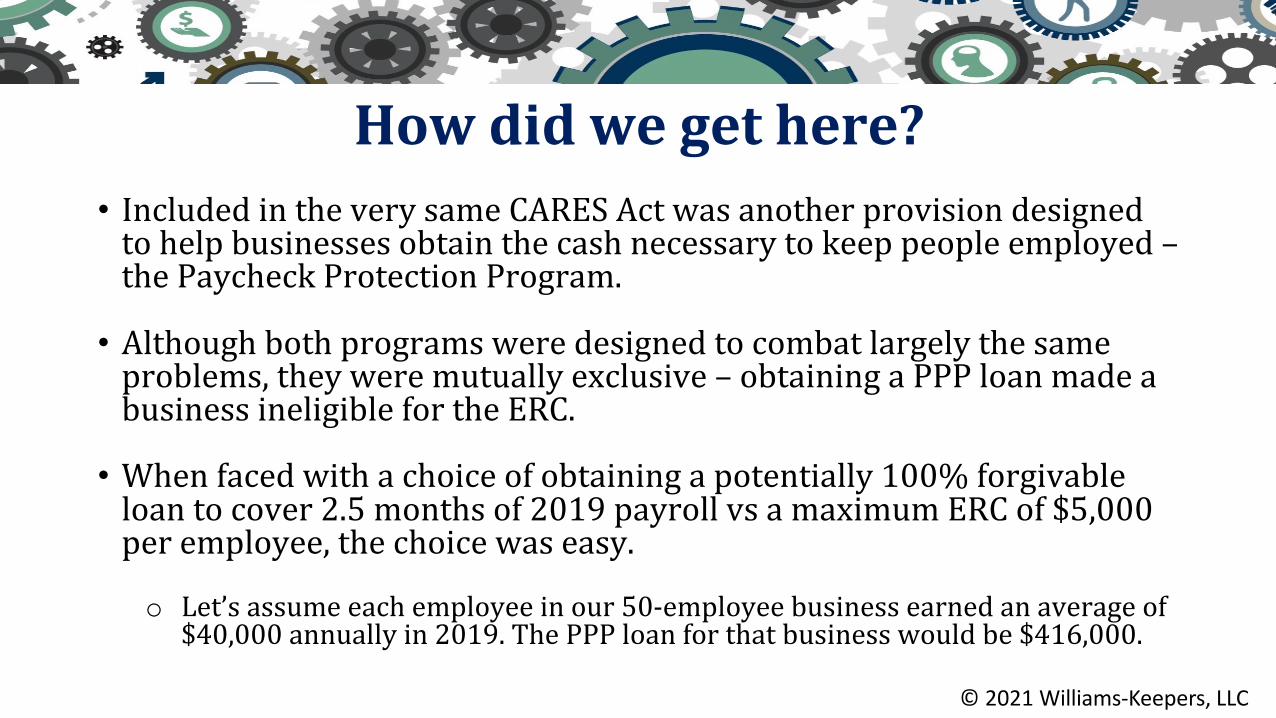

• IncludedintheverysameCARESActwasanotherprovisiondesignedtohelpbusinessesobtainthecashnecessarytokeeppeopleemployed–thePaycheckProtectionProgram.

• Althoughbothprogramsweredesignedtocombatlargelythesameproblems,theyweremutuallyexclusive– obtainingaPPPloanmadeabusinessineligiblefortheERC.

• Whenfacedwithachoiceofobtainingapotentially100%forgivableloantocover2.5monthsof2019payrollvsamaximumERCof$5,000peremployee,thechoicewaseasy.

o Let’sassumeeachemployeeinour50-employeebusinessearnedanaverageof$40,000annuallyin2019.ThePPPloanforthatbusinesswouldbe$416,000.

Howdidwegethere?

© 2021 Williams-Keepers, LLC

Sowhyarewetalkingaboutthisnow?• OnDecember27,then-PresidentTrumpsignedintolawtheConsolidated AppropriationsAct(CAA),which,amongotherthings,removedtherestriction onERCeligibilityassociatedwithtakingaPPPloan.

• Inaddition,theprogramwasextendedthroughQ22021,withlessstringent qualificationsandalargermaximumcreditperemployee.

• OnMarch11,2021,PresidentBidensignedintolawtheAmericanRescue PlanAct(ARPA),whichfurtherextendstheERCthroughQ42021.

© 2021 Williams-Keepers, LLC

BreakingdowntheERCfor 2020and2021

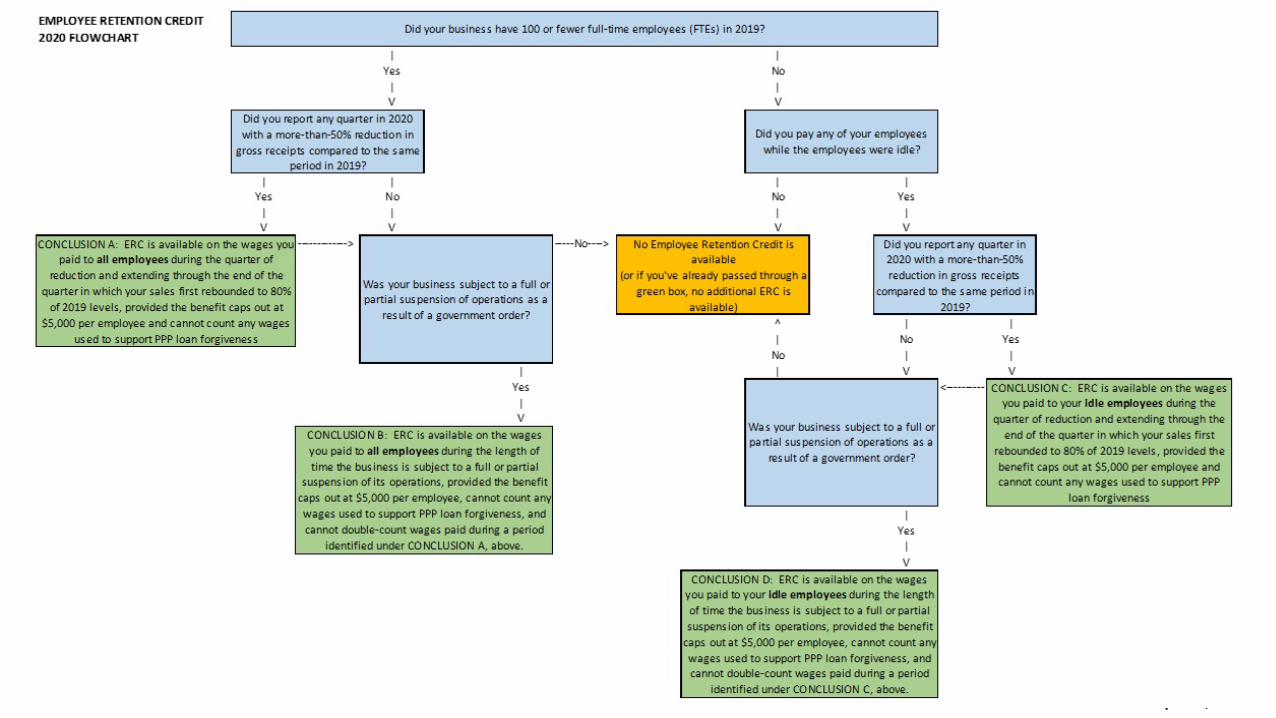

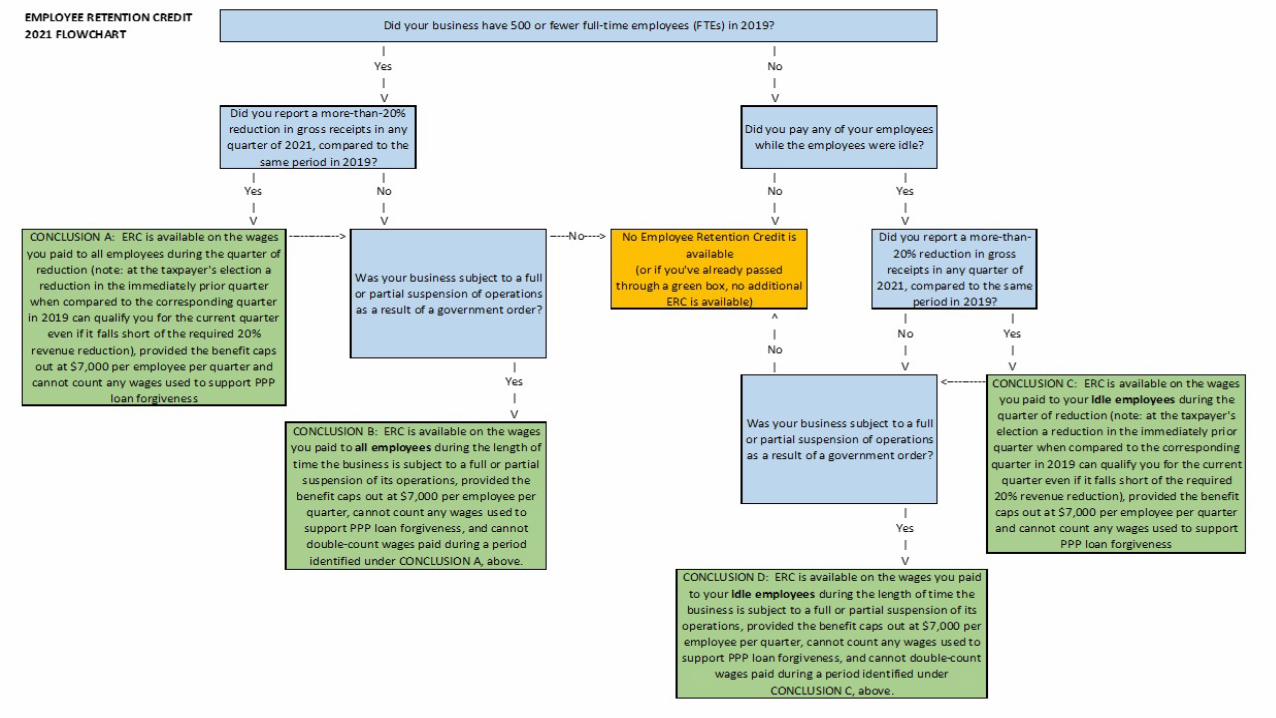

Which"employers"aregenerallyeligible?

© 2021 Williams-Keepers, LLC

• All employers areeligibleforthe ERC,includingtax-exempt organizations(butnotmostgovernmentalemployers)o Employer=payswagestoemployeesasthecommon-lawemployer

• Thereisnosizelimitationorthreshold.o BUT...businesssizedoesimpactwhichwagescount,and"large"businesses couldhavelittletonoeligiblewages,functionallyexcludingthemfromthe program. Moreonthislater.

• Stateandlocalgovernmentsandtheirinstrumentalities arenot eligible.

© 2021 Williams-Keepers, LLC

2019EmployeeCountMatters

© 2021 Williams-Keepers, LLC

• Whilesizedoes not affect eligibility, perse,itsignificantly impactstheERCmath.

• Why?Because large employersonlygettocountwagespaid toemployeeswhowereidle(i.e.,notworking).

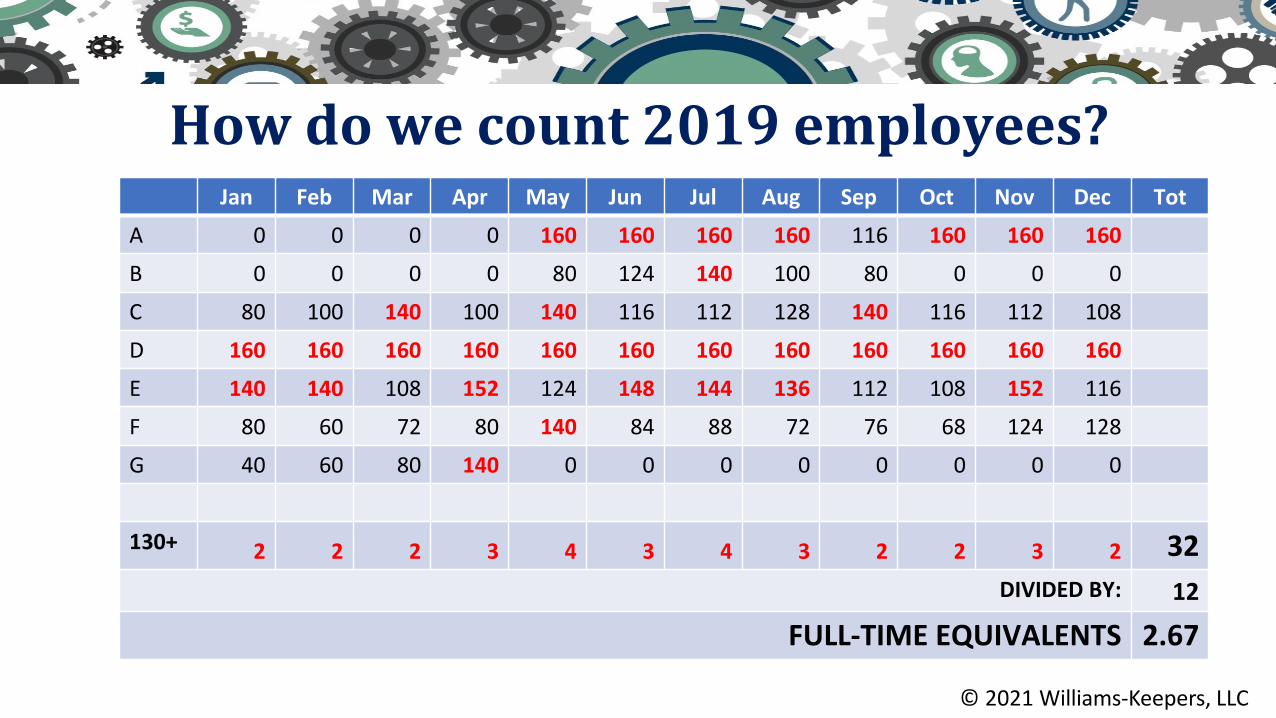

Howdowecount2019employees?

© 2021 Williams-Keepers, LLC

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Tot

A 0 0 0 0 160 160 160 160 116 160 160 160

B 0 0 0 0 80 124 140 100 80 0 0 0

C 80 100 140 100 140 116 112 128 140 116 112 108

D 160 160 160 160 160 160 160 160 160 160 160 160

E 140 140 108 152 124 148 144 136 112 108 152 116

F 80 60 72 80 140 84 88 72 76 68 124 128

G 40 60 80 140 0 0 0 0 0 0 0 0

130+ 2 2 2 3 4 3 4 3 2 2 3 2 32DIVIDED BY: 12

FULL-TIME EQUIVALENTS 2.67

© 2021 Williams-Keepers, LLC

TheGrossReceiptsTest

OpportunitiesforPlanning?

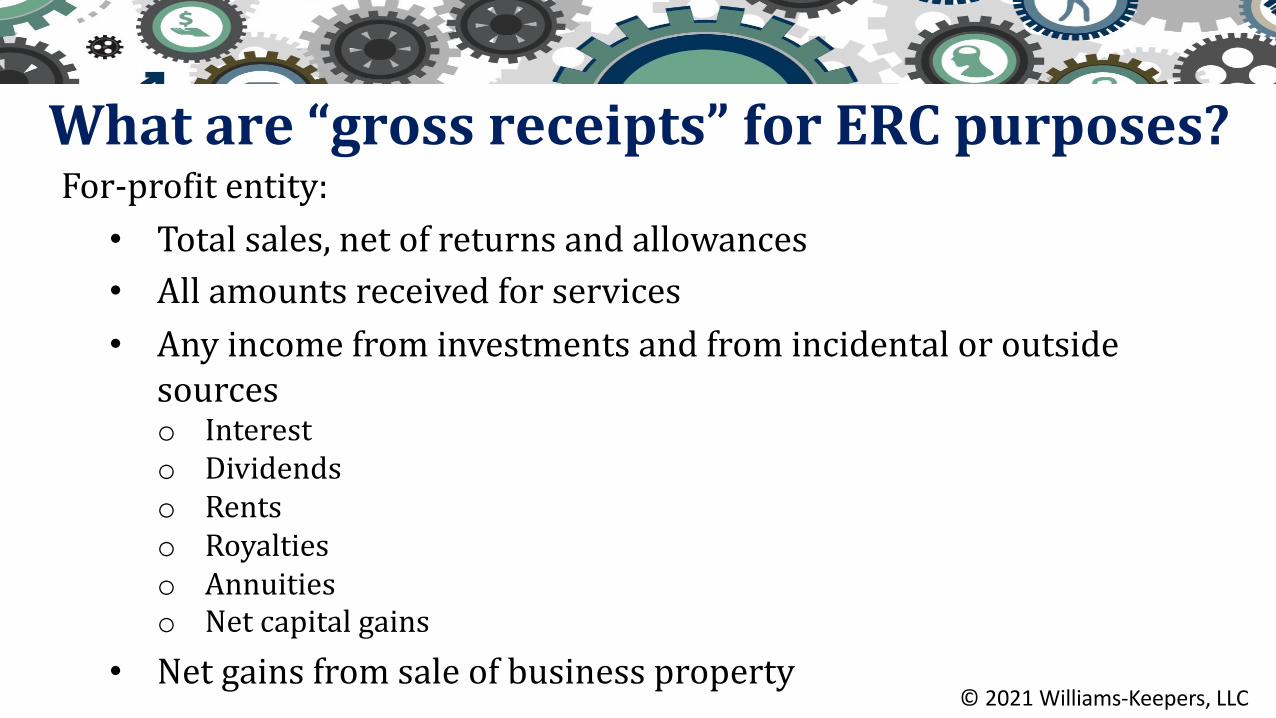

Whatare“grossreceipts”forERCpurposes?For-profitentity:• Totalsales,netofreturnsandallowances• Allamountsreceivedforservices• Anyincomefrominvestmentsandfromincidentaloroutsidesourceso Interesto Dividendso Rentso Royaltieso Annuitieso Netcapitalgains

• Netgainsfromsaleofbusinessproperty© 2021 Williams-Keepers, LLC

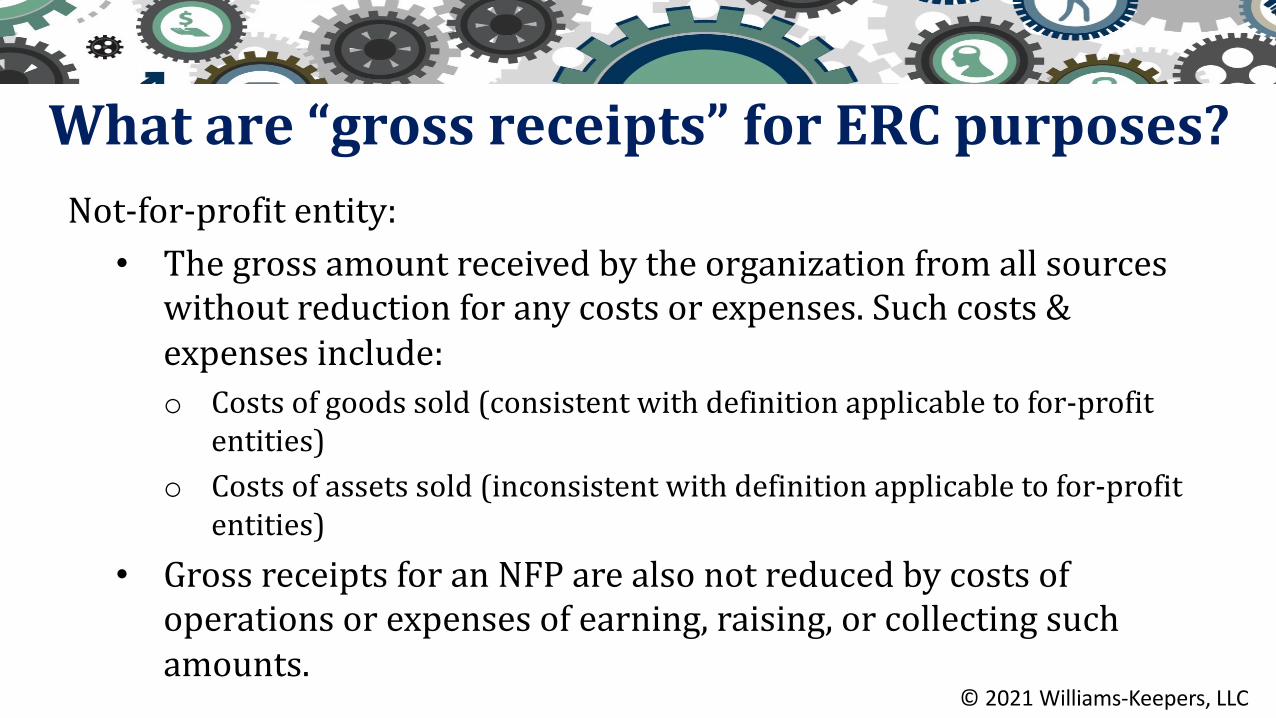

Whatare“grossreceipts”forERCpurposes?Not-for-profitentity:• Thegrossamountreceivedbytheorganizationfromallsourceswithout reductionforanycostsorexpenses.Suchcosts&expensesinclude:o Costsofgoodssold(consistentwithdefinitionapplicabletofor-profit

entities)o Costsofassetssold(inconsistentwithdefinitionapplicabletofor-profit

entities)• GrossreceiptsforanNFParealsonotreducedbycostsofoperationsor expensesofearning,raising,orcollectingsuchamounts.

© 2021 Williams-Keepers, LLC

Whatare“grossreceipts”forERCpurposes?Not-for-profitentity(continued):

• Contributions• Gifts• Grants• Duesorassessmentsfrommembersoraffiliatedorganizations• Grosssalesorreceiptsfrombusinessactivities(includingbusinessactivities unrelatedtothepurposesforwhichtheorganizationqualifiesforexemption)

• Grossamountreceivedfromthesaleofassetswithoutreductionforcostor otherbasisandexpensesofsale

• Investmentincomeo Interesto Dividendso Rentso Royalties

© 2021 Williams-Keepers, LLC

Whatare“grossreceipts”forERCpurposes?• Inbothinstances,thedefinitionsarederivedfromtheInternalRevenueCodeandRegulationsandrequiregrossreceiptsbe determinedunderthetaxpayer’sfederal-income-taxaccounting method.

• Thus,abusinesscannotpickandchooseadifferentmethodthat wouldprovideamorefavorableoutcome.

• However,theERCdoesnotrequirethatthereductioningross receiptsbelinkedinanywaytoCOVID-19.

• Thishassignificantplanningimplicationsforcash-basistaxpayers.

© 2021 Williams-Keepers, LLC

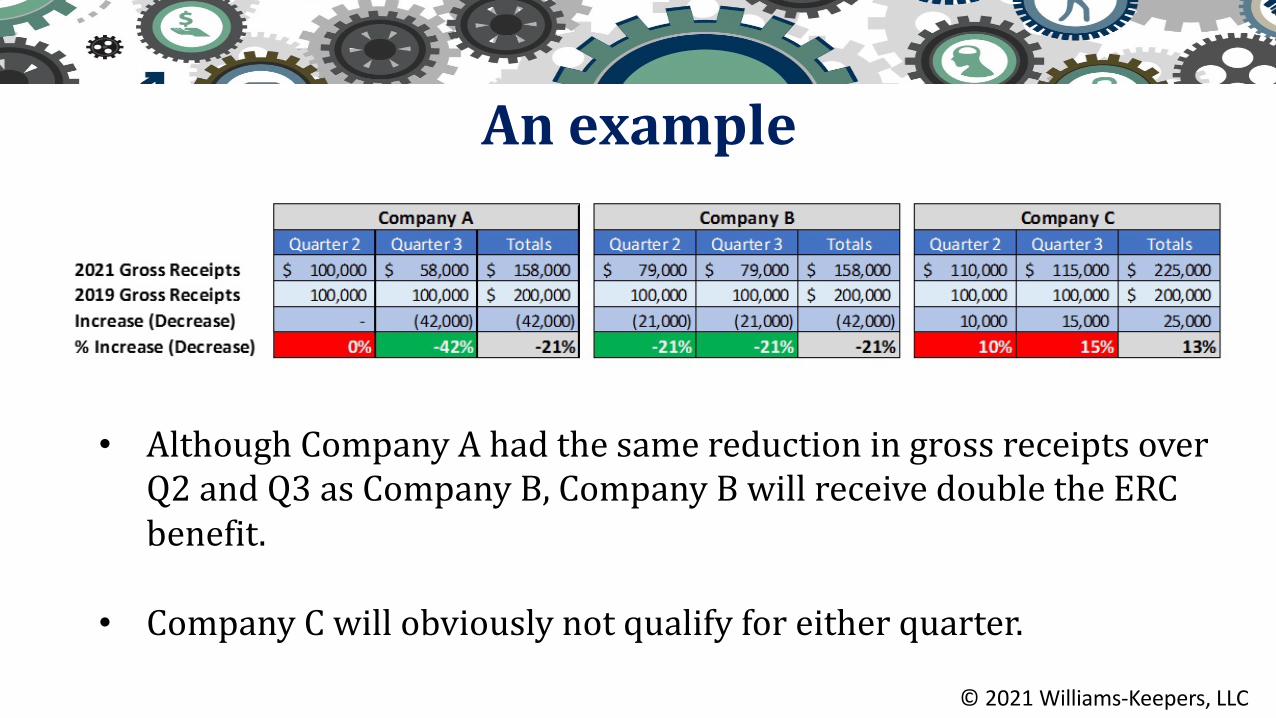

• AlthoughCompanyAhadthesamereductioningrossreceiptsoverQ2andQ3as CompanyB,CompanyBwillreceivedoubletheERCbenefit.

• CompanyCwillobviouslynotqualifyforeitherquarter.

Anexample

© 2021 Williams-Keepers, LLC

Butwhatif…

© 2021 Williams-Keepers, LLC

• Let’sassumethefollowing:o CompaniesA&Carecash-basistaxpayerso CompaniesA&Cgenerallycollectfromcustomerswithin30days

• WhatifCompanyAheldback$21,000ofitsJune2021invoicesuntil July?

• WhatifCompanyCheldback$35,000ofitsJune2021invoicesuntil July?

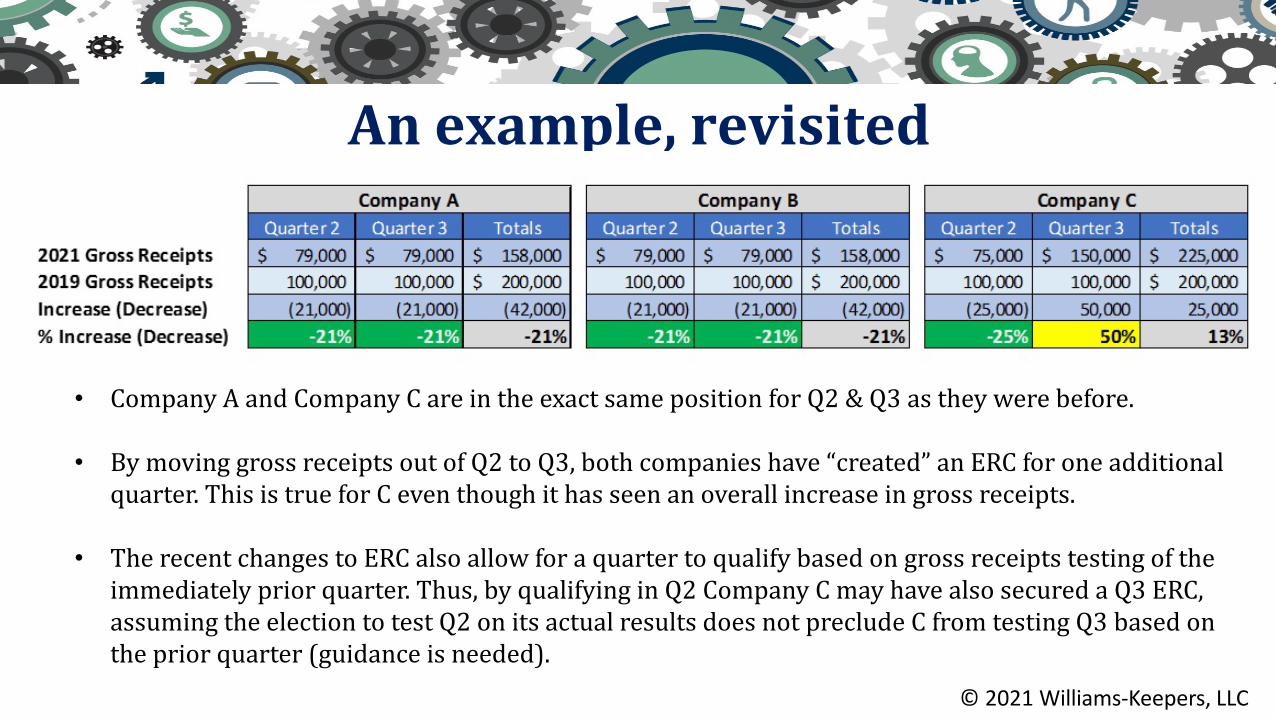

Anexample,revisited

• CompanyAandCompany Care intheexactsamepositionforQ2&Q3astheywerebefore.

• BymovinggrossreceiptsoutofQ2toQ3,bothcompanieshave“created”anERCforone additionalquarter.ThisistrueforCeventhoughithasseenanoverallincreaseingrossreceipts.

• TherecentchangestoERCalsoallowforaquartertoqualifybasedongrossreceiptstestingof theimmediatelypriorquarter.Thus,byqualifyinginQ2CompanyCmayhavealsosecuredaQ3 ERC,assumingtheelectiontotestQ2onitsactualresultsdoesnotprecludeCfromtestingQ3 basedonthepriorquarter(guidanceisneeded).

© 2021 Williams-Keepers, LLC

Keytakeaways• Thegrossreceiptstestisasa“cliff,”sobusinessesthatareclosetothe thresholdsmaybemadeworseoffbysellingmoreinsituationswherethat willdisqualifythemfromthissignificantsubsidy.

• Businessesusingcash-basisaccountingforincometaxpurposesmaybe abletoqualifyforERCin2021withplanning.

• Thecash-basisstrategiesmightallowabusinesstoshiftincomebetween periodstoallowthebusinesstodemonstratetherequisitegrossreceipts reduction. Thecrazythingisthisispossibleevenifthebusinessisdoing wellfortheyear.

© 2021 Williams-Keepers, LLC

© 2021 Williams-Keepers, LLC

TheSuspensionofOperationsTest

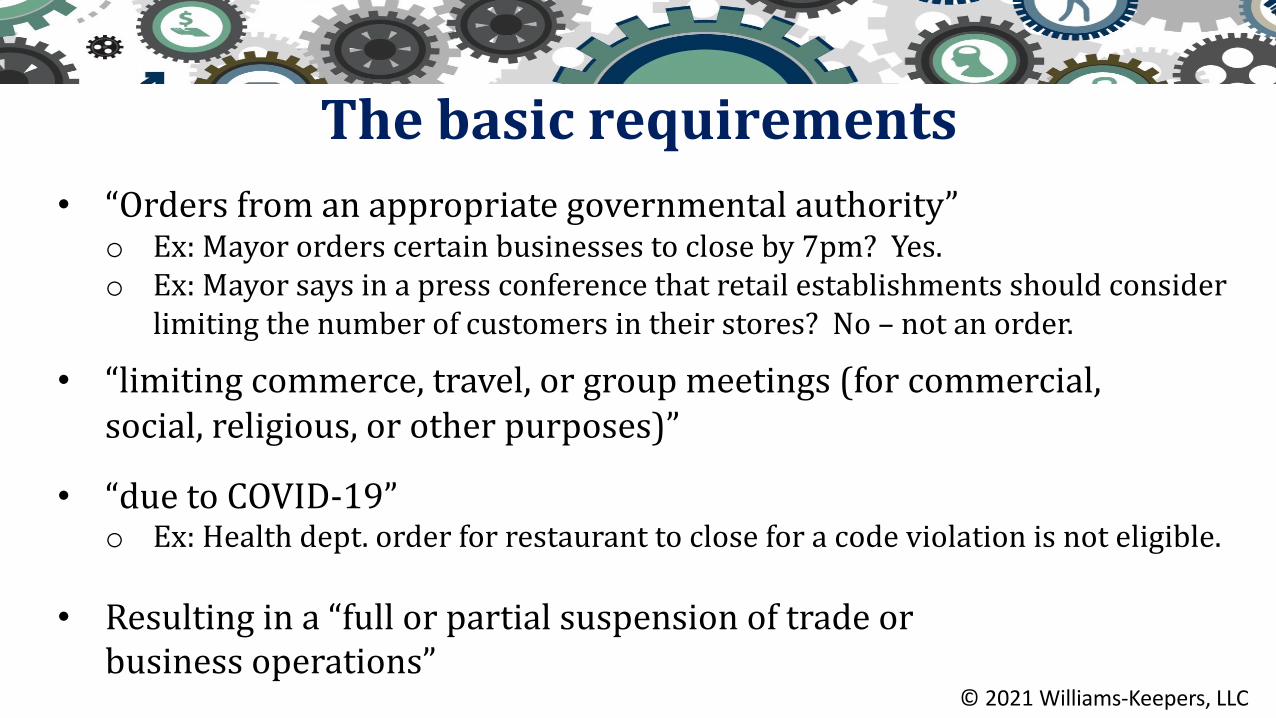

Thebasicrequirements• “Orders fromanappropriategovernmentalauthority”

o Ex:Mayororderscertainbusinessestocloseby7pm? Yes.o Ex:Mayorsaysinapressconferencethatretailestablishmentsshould consider

limitingthenumberofcustomersintheirstores? No– notanorder.

• “limiting commerce,travel,orgroupmeetings(forcommercial,social, religious,orotherpurposes)”

• “due toCOVID-19”o Ex:Healthdept.orderforrestauranttocloseforacodeviolationisnot eligible.

• Resulting ina“fullorpartialsuspensionoftradeorbusiness operations”

© 2021 Williams-Keepers, LLC

Thingsgetweirdwhenstate&localpolicies drivefederaltaxconsequences

• Twobusinesses:o BusinessAoperatesinJurisdictionX,whichprohibitedindoordiningfromMar23, 2020throughDec31,2020.

o BusinessBoperatesinJurisdictionY,whichhadasimilarrulefromMar23,2020until June30,2020butthenfullyreopenedJuly1withnorestrictions.

o Neithersufferedasignificantreductioningrossreceipts.• Results

o BusinessAiseligiblefortheERCforwagespaidfromMar23throughDec31.o BusinessBiseligiblefortheERConlyforwagespaidfromMar23throughJun30.

• WhatifBusinessA actuallymade moremoneyin2020thanin2019?o It doesn’t matter. Iftheywereorderedshutdown, theyare ERCeligibleforthe periodofthe shutdown.

© 2021 Williams-Keepers, LLC

Suspensionofessentialbusinessoperations• Fullsuspensioniseasy

o Isthebusinessanessentialbusinessthat wasallowedto keepalloperations open? Ifyes,itdoesn’tqualifyfortheERCunlessitsufferedasubstantial reduction.

• Partialsuspension– thingsgetmessyo Thetest:Anemployerthatoperatesanessentialbusinesssuffersa

partial suspensionifunderthefactsandcircumstancesmorethananominalportion ofitsbusinessoperationsaresuspendedbyagovernmentorder.

© 2021 Williams-Keepers, LLC

Partialsuspensions• Morethannominal?SafeharborsfromtheIRS:

o Morethan10%ofgrossreceipts≠nominalo Morethan10%ofemployeehours≠nominal

• Examples:o Employer’ssuppliersmustsuspendoperationsundergovernmentorder,whichhas rippleeffectand

causesclosure? YESo Employer’scustomerssubjectto stay-at-home order,sodemanddropstothepoint thestoremust

closetemporarily? NOo Employernotorderedtoclosebutdecidesreducinghoursistherightthingto do? NOo Employerorderedtoclosework site, butemployeeswereabletoteleworkbefore COVIDandmigrate

toaremoteworkenvironment? NOo Employerorderedtocloseworksiteandcanoffersomeservicestoitscustomers remotelybutis

unabletoprovideotherswhichrequirespecializedequipment locatedonsite? YES

© 2021 Williams-Keepers, LLC

Partialsuspensions• Examples:(continued)

o Employerorderedtocloseworksiteandcanoffersomeservicestoits customersremotelybutisunabletoprovideotherservicesremotely? YES§ Remoteworkfactors:Pre-COVIDteleworkcapabilities;Portabilityofwork;

Needfor presenceinemployee’sphysical workspace;Significant(morethan2weeks)migration periodrequired

o Employerorderedtoclosesomeoperationsbutnotallandportionclosedis notnominal? YES

© 2021 Williams-Keepers, LLC

Partialclosureinspecificindustries• Restaurants: Indoordiningclosed? YES. Spacinglimitationswithamorethan nominalimpact? YES. Hours limitation? YES. Drivethruonly? YES.

• Retail:Storefrontclosed? YES. Socialdistancingrestrictionspermitinstore shoppingbutresultingcapacitylimitationrequiressomecustomerstoqueue forashorttimeoutside? NO.

• Medical:Non-urgentmedicalproceduresprohibited? YES.

• Grocerystore: Nominalactivity(e.g.,saladbar)orderedclosed? NO.© 2021 Williams-Keepers, LLC

Whenmodificationsofservicedeliveryarepartialclosures

• Factorso Limitedoccupancytoallowforsocialdistancingo Serviceonlyonanappointmentbasisforbusinessespreviouslyoffering

walk-upserviceo Changingformatofservice(e.g.,restrictionsonbuffetorself-serve)

• BUT…onlyifthemodificationhasamorethannominaleffectonthe businessoperationsbasedonthefactsand circumstances.

• AND…modificationsaffectingcustomerbehavior(e.g.,“I don’t want towearamask”) donot count.

© 2021 Williams-Keepers, LLC

Multiplelocations• Businessesoperatingindifferentjurisdictionsfaceddifferentrules.

• Generally,a shutdown anywhereisa shutdown everywhere.

• Notonlythat,butdifferentbusinessesinthesamecontrolgroupare treatedasone,soapartial shutdown atanaffiliatedbusinessmay causewagespaidtoessentialemployeestoqualify.

© 2021 Williams-Keepers, LLC

Reallifeismessy• InMissouri,forpartofMarch,allofApril,andmostofMay,public-facing retailbusinessesweregenerallysubjecttoarestrictionthatitsoccupancy waslimitedto25%ofthefirecodecapacityofthebuilding.

• Example:o Ioperateapetgroomingbusinessthatusedtoallowwalk-inappointmentsandhasa retailshopwithpetfoodandaccessoriesatthefrontofthestore.

o Thefirecodecapacityofmybuildingis20people,andInormallyhave5employees workingatanytime.

o AsaresultofCOVID,mybusinesscanceledwalk-inappointmentsandimplementeda “driveup”check-insystemandrequirecustomerstocallwhentheyarrive. Veryfew productsweresold,butgroomingrevenueswereroughlystable.

• Whatdoyouthink?

© 2021 Williams-Keepers, LLC

© 2021 Williams-Keepers, LLC

InteractionsBetweentheERCandPPP

InteractionbetweenERCandPPP• TheremovaloftheprohibitionagainstPPPborrowersobtainingthe ERCfinallymadetheERCavaluable,broad-scaleaidprogram.

• SincemostbusinessesnoweligibleforanERCalsoobtainedaPPP loan,thereisstillworktobedoneinmostcircumstancestomake surethebenefitsofbothprogramsarebeingmaximized.

• Remember:abusinesscanobtainbothaPPPloanandobtainanERC, evenduringthesame periodoftime,butwagescannotbeusedto supportbothPPPforgivenessandtheERC.

© 2021 Williams-Keepers, LLC

WhatifIhaveobtainedPPPforgiveness?• Formanybusinesses,thecoveredperiodoftheirFirstDrawPPPloan hasalreadyexpired.

• Manyofthesebusinesseshavealreadyrequestedforgivenessand,for alltherightreasonsatthetime,utilized only payrollcoststosupport forgiveness.

• ForbusinessesthatwanttoretroactivelyclaimtheERCin2020,there hasbeenmuchconfusiononhowapreviously-filedPPPforgiveness applicationimpactstheabilitytoclaimtheERC.

© 2021 Williams-Keepers, LLC

WhatifIhaveobtainedPPPforgiveness?Notice2021-20

Theamountofthepayrollcostsforwhichthetaxpayerisdeemedto havemadeanelectiontobetreatedasPPPpayrollcostsisthe amount ofqualifiedwagesincludedaspayrollcostsonthePPPLoan ForgivenessApplicationupto(butnotexceeding)theminimum amountofpayrollcosts,togetherwithanyothereligibleexpenses reportedonthePPPLoanForgivenessApplication,sufficienttosupport theamountofthePPPloanthatisforgiven.

© 2021 Williams-Keepers, LLC

WhatifIhaveobtainedPPPforgiveness?• Inmoresimpleterms:Ataxpayerisdeemedtohaveusedthe minimumamountofpayrollcostsreportedonitsPPPLoan ForgivenessApplicationthatisnecessarytosupporttheforgiveness amountrequested.Any“excess”payrollcostsareeligibleforERC.

• TheNotice doesnot,however,allowabusinesstoadjustthefiled ForgivenessApplicationtoclaimmorenon-payrollcosts,evenifthebusiness incurredmorenon-payrollcoststhanreportedontheForgiveness ApplicationandevenifthePPPborrower hadnot yetexceededthe 60%payrollrequirementontheForgivenessApplication.

• Ifthecost wasn’t includedontheForgivenessApplication,it doesn’t count.

© 2021 Williams-Keepers, LLC

© 2021 Williams-Keepers, LLC

Keytakeaways• IfyouhavenotyetfiledforPPPforgivenessandareeligiblefora retroactiveERC,considerholdingthePPPForgivenessApplicationso thatyoucancoordinateitwiththeERC.

• Ifyouhavealreadyfiledforforgivenessandareeligiblefora retroactiveERC,itisstillpossibletooptimize,butyouareconstrained bywhatisreportedonthePPPLoanForgivenessApplication.

• Ifyoudonothaveenoughcoststosupportboth,prioritizePPP(100% ofwage)overERC(50%ofwage).

© 2021 Williams-Keepers, LLC

InSummary• TheremovaloftheprohibitionagainstPPPborrowersclaiminganERC nowmakestheERCaviableaidprogramformanybusinesses.

• Thesizeofyourbusinessmatters– morethan100full-time employeesin2019willallbuteliminate2020creditbenefitandmore than500full-timeemployeesin2019willallbuteliminate2021 benefit.

• Abusinesscanqualifybaseduponasignificantreductioninquarterly grossreceiptscomparedto2019(greaterthan50%for2020and greaterthan20%for2021).

© 2021 Williams-Keepers, LLC

Insummary• Cash-basistaxpayershavesomecontrolover2021revenue recognitionandcaninfluencethequalificationcalculation.

• Abusinesscanalsoqualifyduetoafullorpartialsuspensionof businessactivities.Therulesaresituation-specificandare complicated. Don’t immediatelyassumeyoudoor don’t qualify;more reviewislikelyneeded.

• ThelasthurdleiscoordinatingtheERCbenefitwithPPPbenefits.If youare eligiblefora2020ERCand havenot yetfiledforPPPloan forgiveness,considerwaitingtofileforforgivenessuntiltheERC calculationiscomplete.

© 2021 Williams-Keepers, LLC

Questions?

JeremyMorris, CPAWKMember

Phone:(573)632-0932Email:[email protected]

JeremybeganhiscareerinpublicaccountingatWKin2005andjoinedthemembergroupin2016.Heprovidestaxandconsultingservicesforthefirm’sindividualandbusinessclientsandmakespresentationstolocalgroupsonvarioustax topics.

• Jeremyworkswithinsurancecompanies,closelyheldbusinesses,constructioncompanies,andestatesand trusts.

• Jeremyearnedhisbachelor’sandmaster’sdegreesinaccountingfromtheUniversityofMissouriin2002andearnedamasterofsciencedegreeinbusinessadministrationfromPennStateUniversityin 2005.

• JeremycurrentlyservesasChairElectfortheJeffersonCityYMCABoardofDirectorsandasTreasurerfortheCatholicCharitiesofCentralandNorthernMissouriBoardofDirectors.HeisapastTreasureroftheJeffersonCityYMCAandtheJeffersonCityConcertAssociation.JeremyisamemberoftheAdvisoryCommitteeforBigBrothersBigSistersofJeffersonCity,theMizzouAlumniAssociationleadershipboardforColeCounty,andfinancecommitteesfortheJeffersonCityYMCAandSt.Joseph’sCathedralParish.HeisamemberoftheAmericanInstituteofCertifiedPublicAccountantsandtheMissouriSocietyofCertifiedPublic Accountants.

MarkGingrich,CPA,JDWKMember

Phone:(573) 499-6879Email:[email protected]

Markleverageshistrainingintaxresearchtoofferplanningandconsultingsolutionsrelatedtoestateplanning,trustandestatematters,businessstructuring,andsuccessionplanning.HejoinedtheWKownershipgroupin2014.

• AnativeofColumbia,MarkjoinedWKin2009aftercompletinghislawdegreewithhighhonorsattheUniversityofIowainIowaCity.HeisagraduateoftheUniversityofMissouri,whereheearnedundergraduatedegreesinaccountingandbusinessadministrationwithemphasisineconomicsandamaster’sdegreein accounting.

• MarkisamemberoftheAmericanInstituteofCertifiedPublicAccountantsandtheMissouriSocietyofCertifiedPublicAccountants.Heisalsoamemberofthenational,stateandlocalbarassociationsandtheOrderoftheCoif.MarkisapastpresidentoftheMid-MissouriEstatePlanningCouncil,servesastheboardtreasureroftheMissouriInnovationCenter,andhasvolunteeredwithJuniorAchievementofCentralMissouri,theBooneCountyBarAssociation’sYoungLawyersCommittee,andtheBoyScoutsofAmerica,amongotherlocal organizations.