Embed Size (px)

Citation preview

“Credit Risk Management at Standard

Chartered Vietnam”

Master Thesis

submitted to

IMC University of Applied Sciences Krems

and

Vietnam University of Commerce

Master Program

Vietnamese Austrian Business Administration

by

HOANG VIET THANH

For the award of the title

Master of Arts in Business (MA)

Thesis Supervisor: PRO. NGUYEN HOANG

Submitted on: 9th September 213

Eidesstattliche Erklärung

„Ich erkläre an Eides statt, dass ich die vorliegende Masterarbeit (Diplomarbeit) selbstständig verfasst, und in der Bearbeitung und Abfassung keine anderen als die angegebenen Quellen oder Hilfsmittel benutzt, sowie wörtliche und sinngemäße Zitate als solche gekennzeichnet habe. Die vorliegende Masterarbeit wurde noch nicht anderweitig für Prüfungszwecke vorgelegt.“

Datum: 9. August 2013 Unterschrift

HOANG VIET THANH

Statutory declaration

“I declare in lieu of an oath that I have written this master thesis myself and that I have not used any sources or resources other than stated for its preparation. I further declare that I have clearly indicated all direct and indirect quotations. This master thesis has not been submitted elsewhere for examination purposes.”

Date: 09th August 2013 Signature

HOANG VIET THANH

Acknowledgement

I take immense pleasure in thanking Rector of Vietnam

Commercial University, and Prof. NGUYEN Hoang, Chief of

International Training Department, Rector of the Applied

Sciences IMC Krems University, for having permitted me to

have a chance to complete this dissertation.

I wish to express my deep sense of gratitude to my Internal

Guide, Prof. NGUYEN Hoang, chief of International Training

Department, Vietnam Commercial University; for his able

guidance and useful suggestions, which helped me in

completing the work, in time. Needless to mention that all

SCB staff who had been a source of inspiration, for all

their valuable assistance in the project work and for their

timely guidance in the conduct of my thesis.

Finally, yet importantly, I would like to express my

heartfelt thanks to my parents for their blessings, my

friends/classmates for their help and wishes for the

successful completion of my dissertation.

Master of Art in Business Applicant

HOANG VIET THANH

FORWORD

n the situation of crisis economy, financial

market of each country has been faced with

fluctuation and risk hidden. As the results,

financial quantitative factors for credit risk management

are the top hottest factors. The world crisis consequences

appear all over the world, thus, credit risk measurements

are needed for every country to identify, evaluate,

foresee the financial situation of each enterprise. Thus,

this is the reason why, author chose the title of Credit

Risk Management of SCB.

I

In the size of thesis for Master of Art in Business,

author would like to indicate his little experience in

this sector along with combining with credit risk

management knowledge over the world. Besides he also would

love to draw quickly the overview of credit in Vietnam,

then, scoped into special application for SCB. Finally,

the dissertation will include the conclusion and short

recommendation for improving credit risk quality at SCB.

LIST OF CONTENTS

Statutory Declaration Acknowledgement ForewordTable of ContentsList of figuresChapter 1: Introduction 11. Background 12. Objectives 13. Structure 2Chapter 2: Literature Review 52.1. Credit risk definition 82.2. The components of credit risk 92.3. Credit risk management 112.4. Risk causes 162.5. Credit measurement 182.6. Basel Committee recommendation in Credit Risk Management

19

Chapter 3: Overview of Credit Risk Management in Viet Nam Banks

21

1. The organization of banks in Vietnam 212. The growth in total assets of banks in Vietnam though period

22

3. Operating Environment in Vietnam’s banking domain 234. Credit Risk Ratio 24

5. Bad Debt 256. The Vietnamese bank ratio of profit/ total revenues 31Chapter 4: Methodology 324.1. Research purpose and target 324.2. Data 334.3. Information gathering method 344.4. Procedures 364.5. Limitation 38Chapter 5: Credit Risk Management at Standard CharteredBank Vietnam (Ltd)

40

5.1. Introduction 405.2. Credit Risk at Standard Chartered Vietnam 415.3. Credit Risk Management at Standard Chartered Bank Vietnam (Ltd).

42

5.4. Financial Analysis 53

5.5. Questionnaire result analysis 615.6. Credit Risk Management Summation 745.7. Recommendation 765.8. Conclusion 82References 83Annex 1 85

TABLE OF FIGURES

Figure 1: Credit Analysis Process Flow (John

B.Caouette, Edward I. Altman, Managing Credit

Risk, 1998)11

Figure 2: Credit Organization in a large bank

Joetta Colquitt (2007) 13

Figure 3: Functional Approach to the Credit

Process (Joetta Colquitt (2007) 14

Figure 4: Credit Rating System of Fitch, S&P and

Moody’s 18

Figure 5: The increase of total assets at

Vietnamese Banks from 2009 to 2012 (Extracted from

SBV annual report)21

Figure 6: Credit Risk Ratios at Vietnamese Banks

(Extracted from Vietinbank, Vietcombank, BIDV,

ACB, Eximbank annual report).22

Figure 7: Classification of Loans in Vietnam 24Figure 8: Bad debt rate of Vietnamese banks as at

31th December 2012 (Financial Report of Commercial

Banks)25

Figure 9: The possible loss loans (Group 5)

against total liabilities of Vietnamese banks

(Financial Report of Commercial Banks)26

Figure 10: Vietnam Asset Management Company in

settling the bad debt 27

Figure 11: Extracted from banks financial annual

report. 29

Figure 12: List of SCB staff joined in

questionnaire32

Figure 13: Table of Standard Chartered Vietnam Limited Products 35

Figure 14: The lending procedures of Standard

Chartered Bank Vietnam (Ltd). (Internal Process

37

Document)Figure 15: Documents for Loan Applicants (SCB

Products Internal Document) 38

Figure 16: Credit Grading of SCB (Internal

Document). 39

Figure 17: Table of collateral evaluation at SCB

(Internal Document) 40

Figure 18: Table of maximum percentage for lending

at SCB (Internal Document) 41

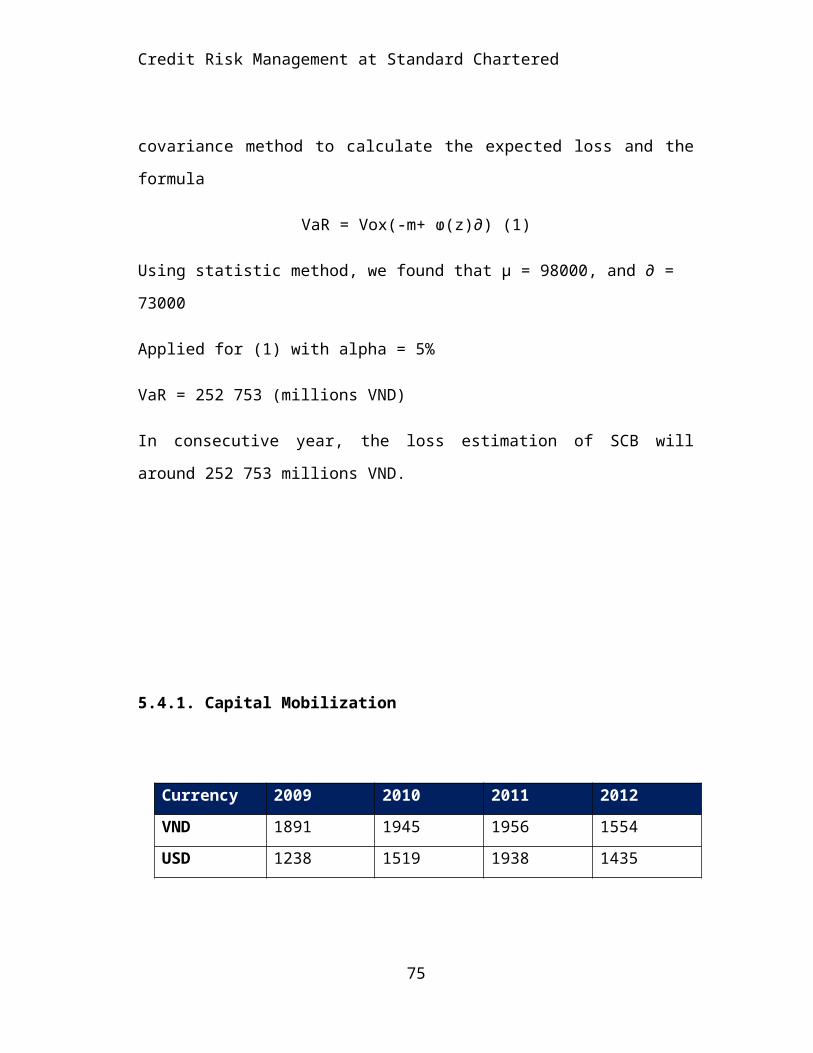

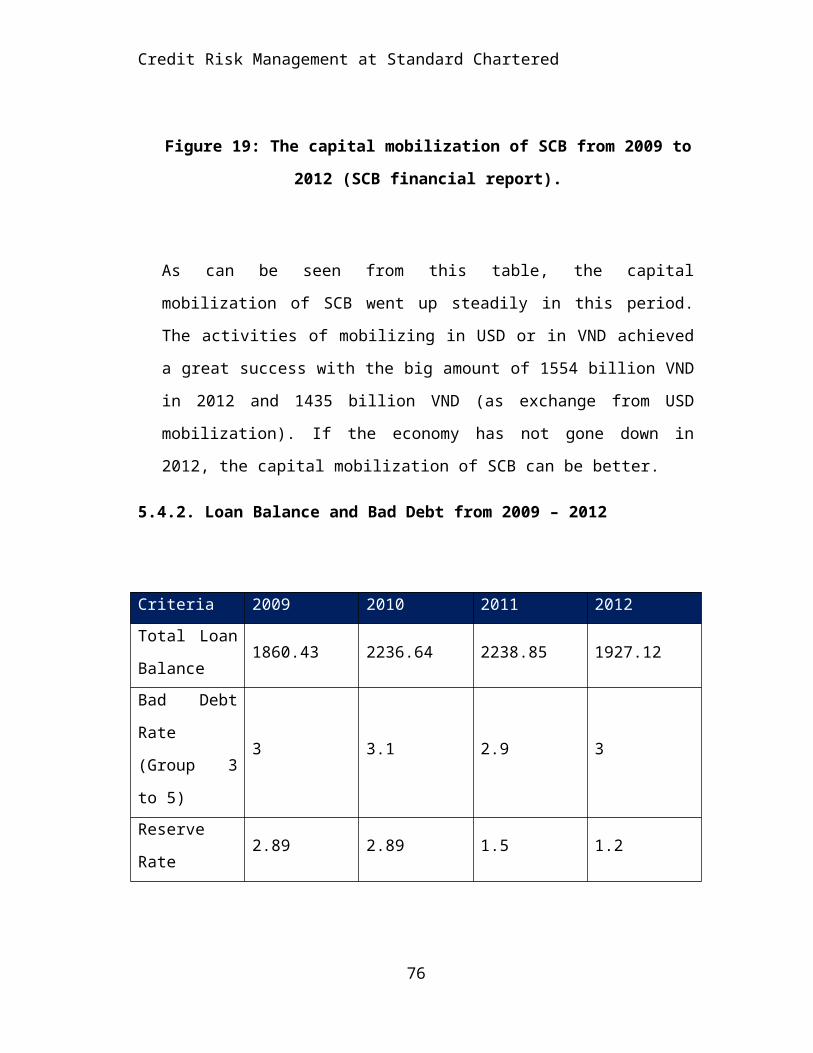

Figure 19: The capital mobilization of SCB from

2009 to 2012 (SCB financial report). 48

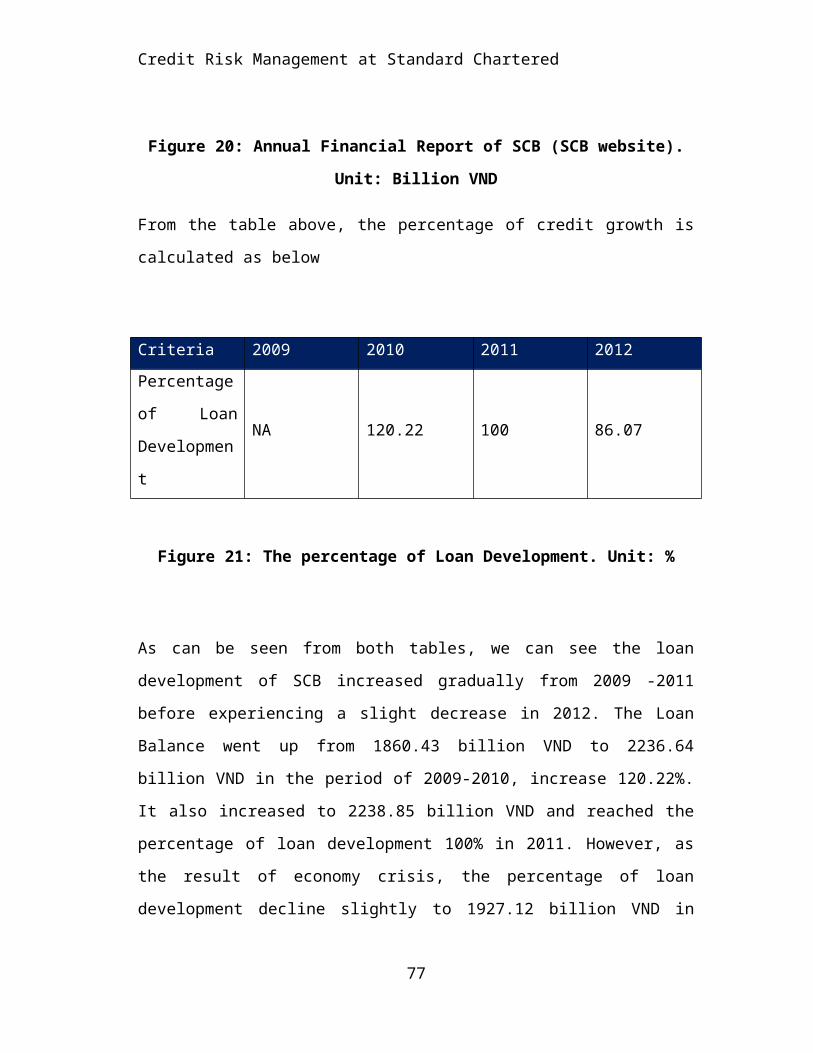

Figure 20: Annual Financial Report of SCB (SCB

website). Unit: Billion VND 48

Figure 21: The percentage of Loan Development.

Unit: % 48

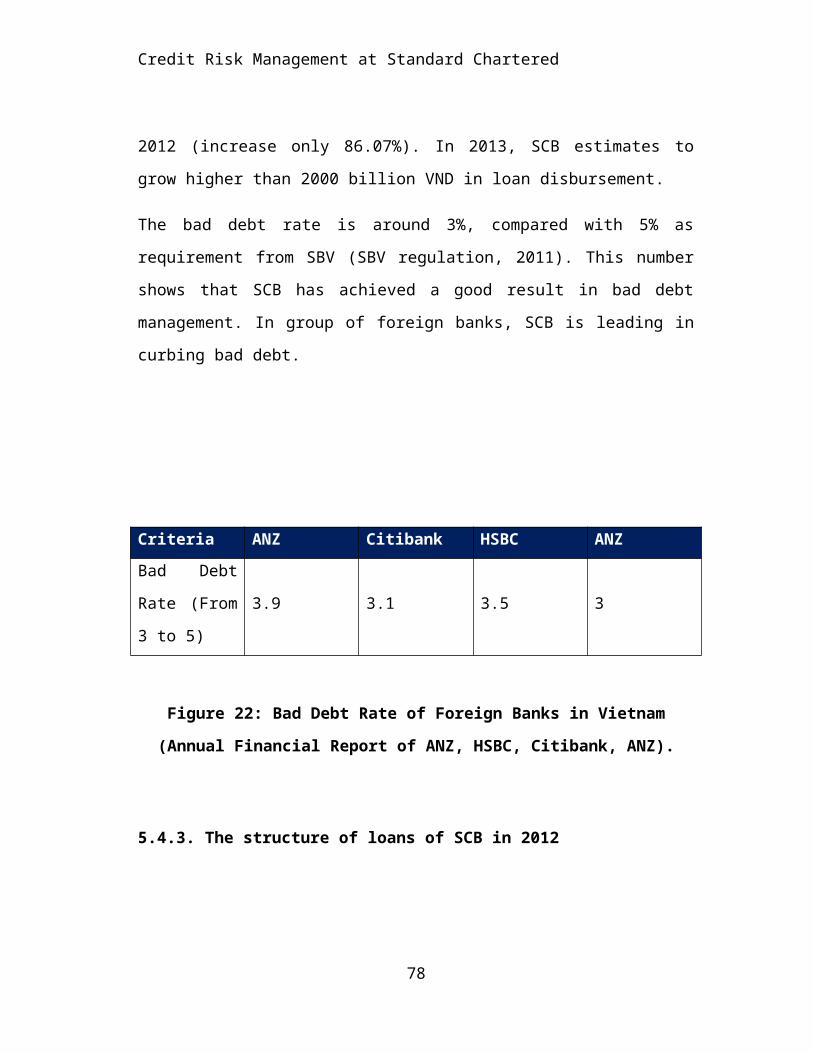

Figure 22: Bad Debt Rate of Foreign Banks in

Vietnam (Annual Financial Report of ANZ, HSBC,

Citibank, ANZ).49

Figure 23: The liquidity of SCB from 2009 -2012

(Internal Document) 51

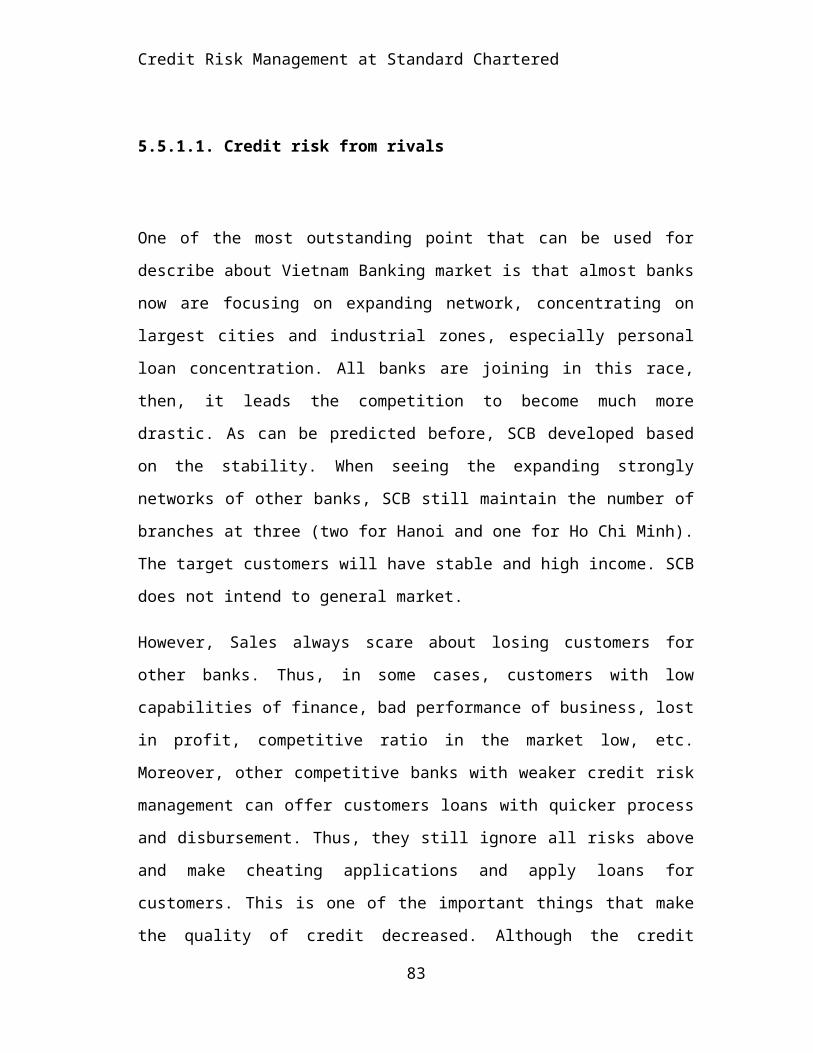

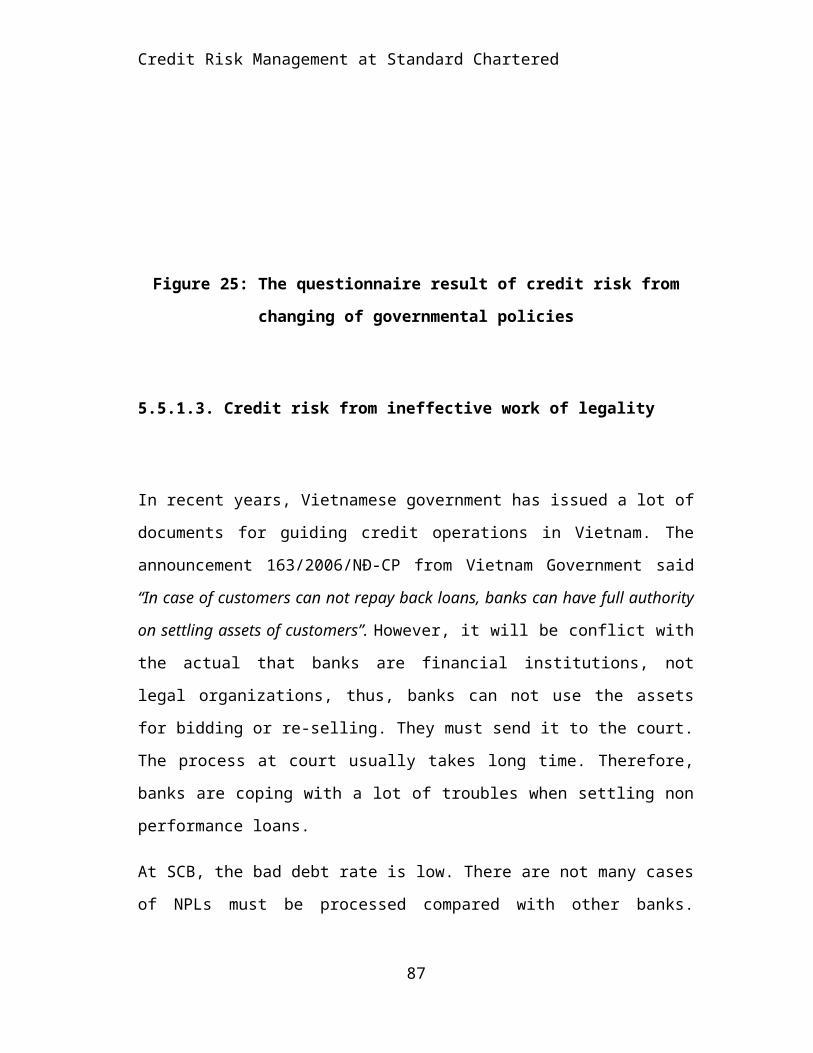

Figure 24: The questionnaire result of credit risk

from rivals 53

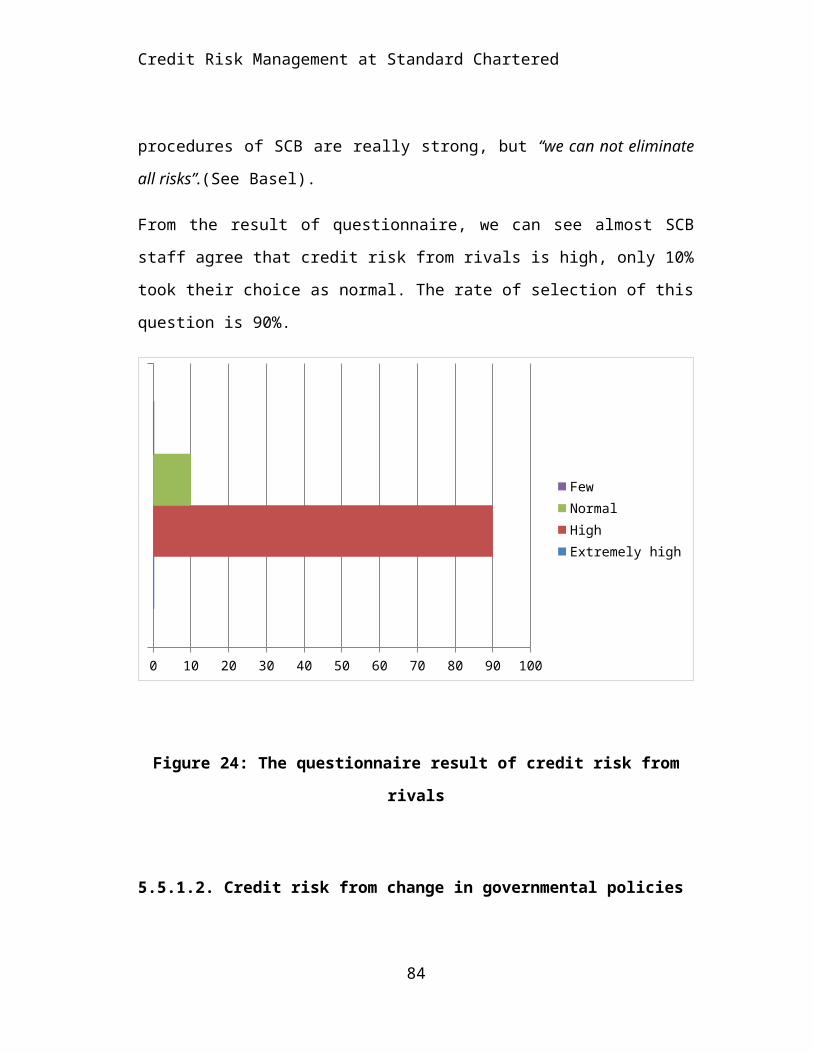

Figure 25: The questionnaire result of credit risk

from changing of governmental policies 55

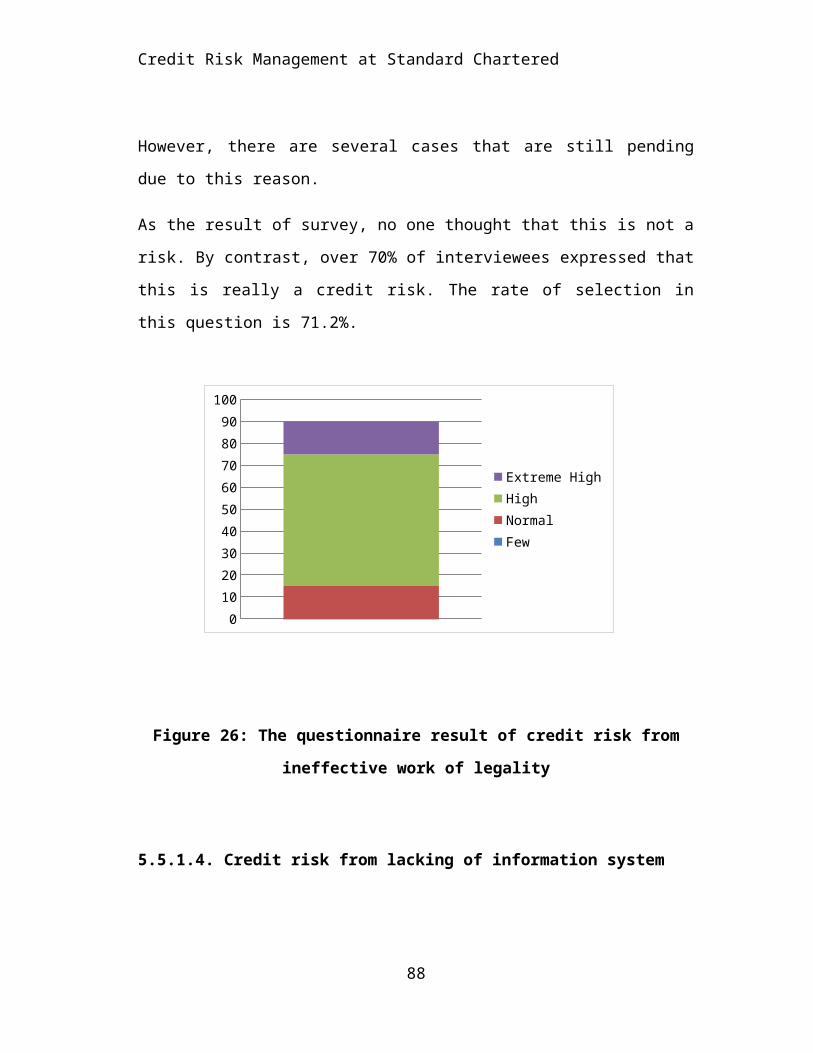

Figure 26: The questionnaire result of credit risk

from ineffective work of legality 56

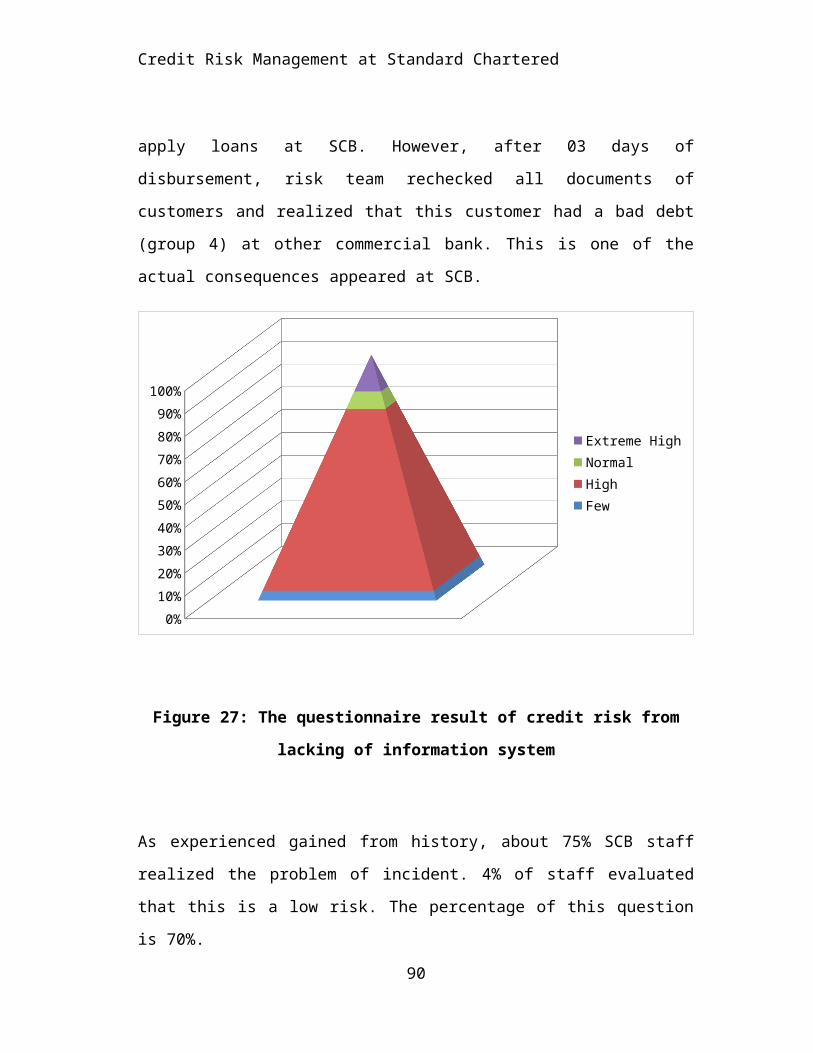

Figure 27: The questionnaire result of credit risk 57

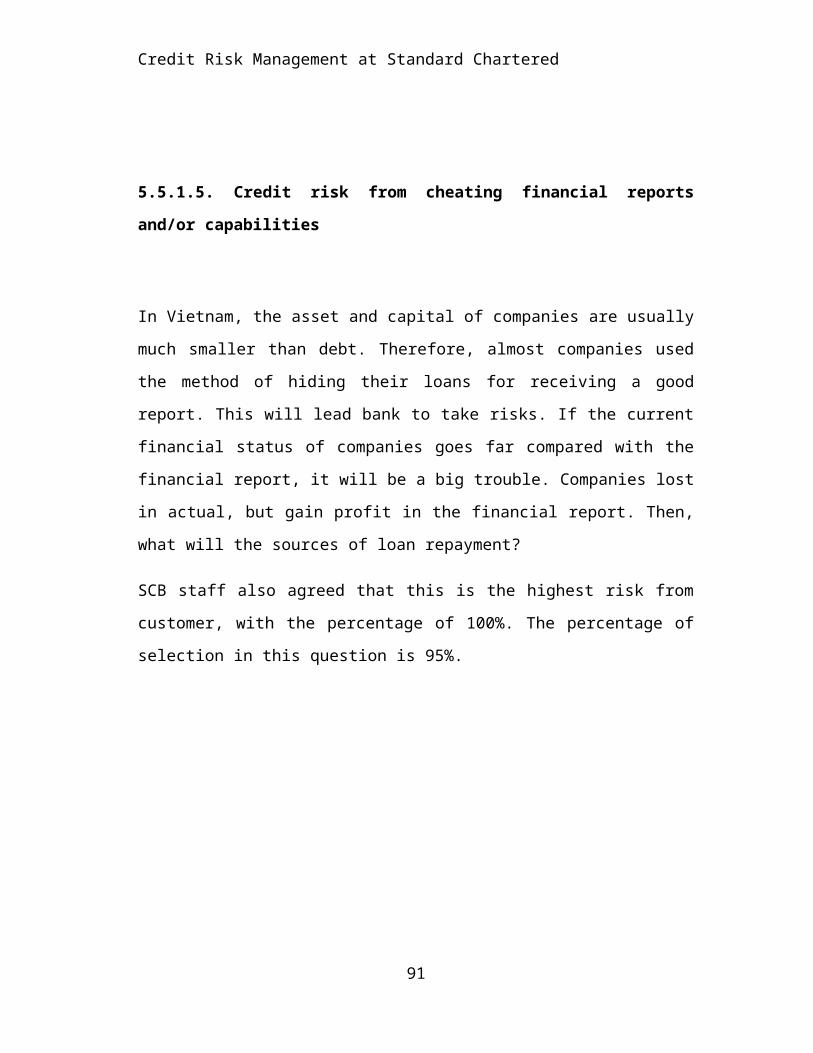

from lacking of information systemFigure 28: Credit risk from cheating financial

reports and/or capabilities 58

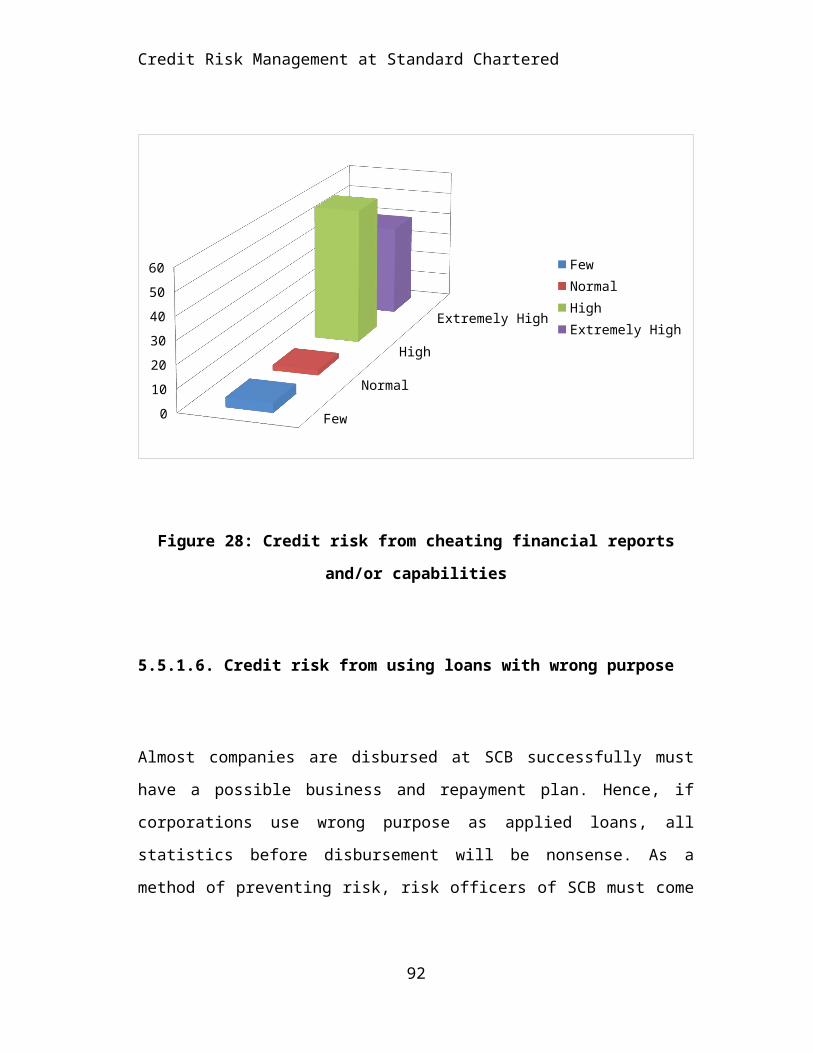

Figure 29: Credit risk from using loans with wrong

purpose 59

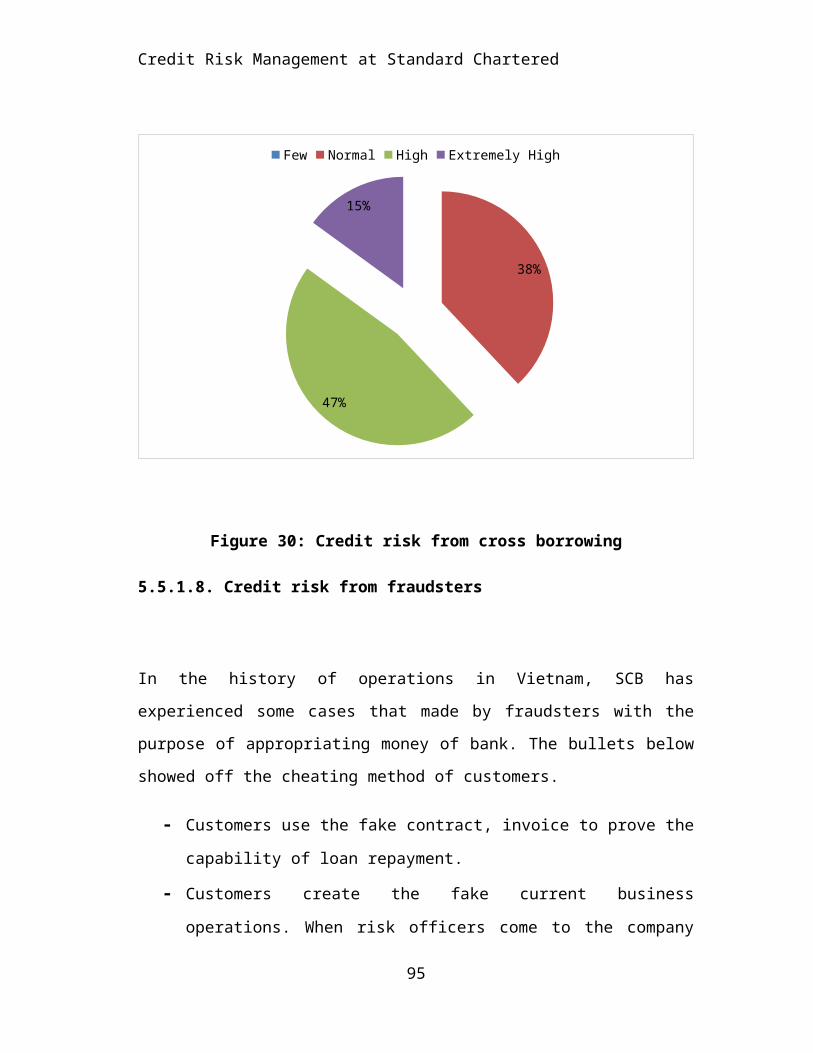

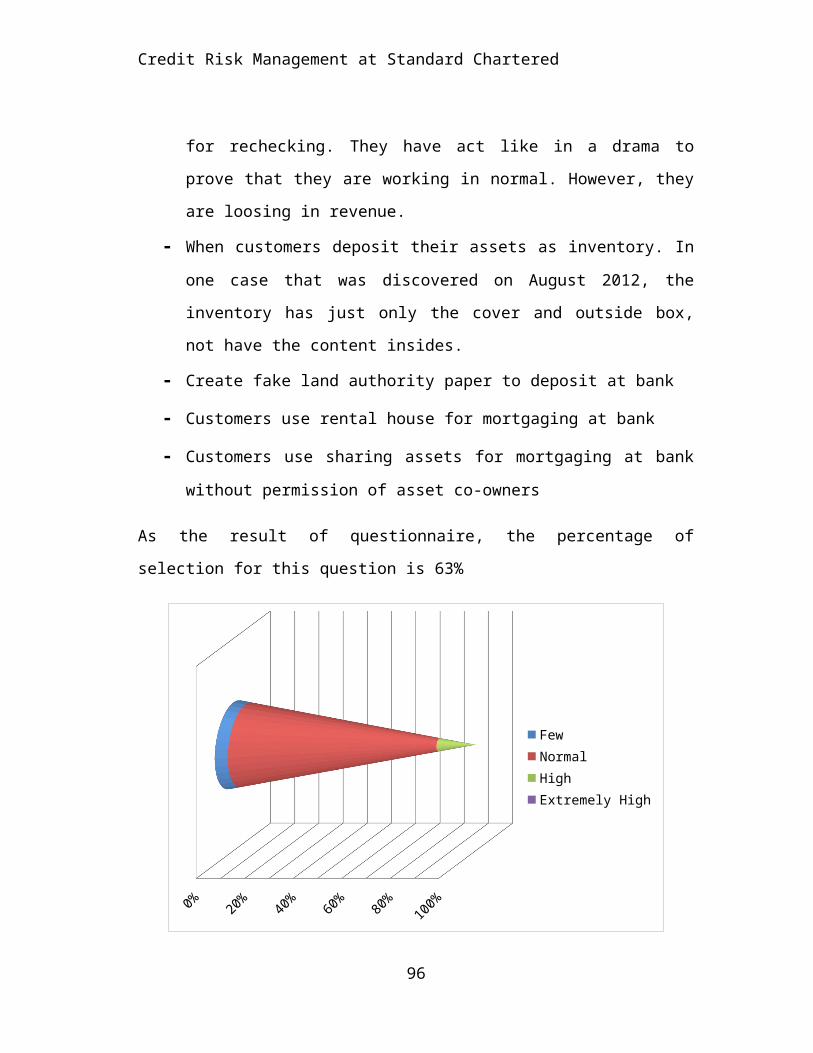

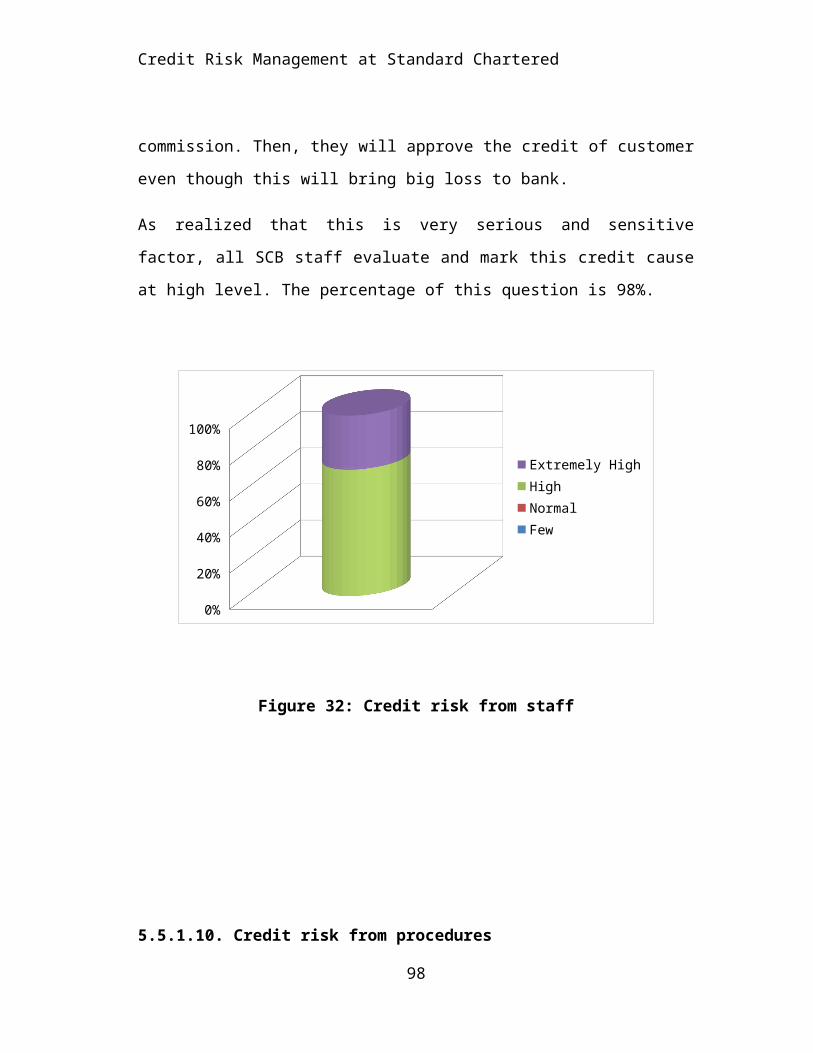

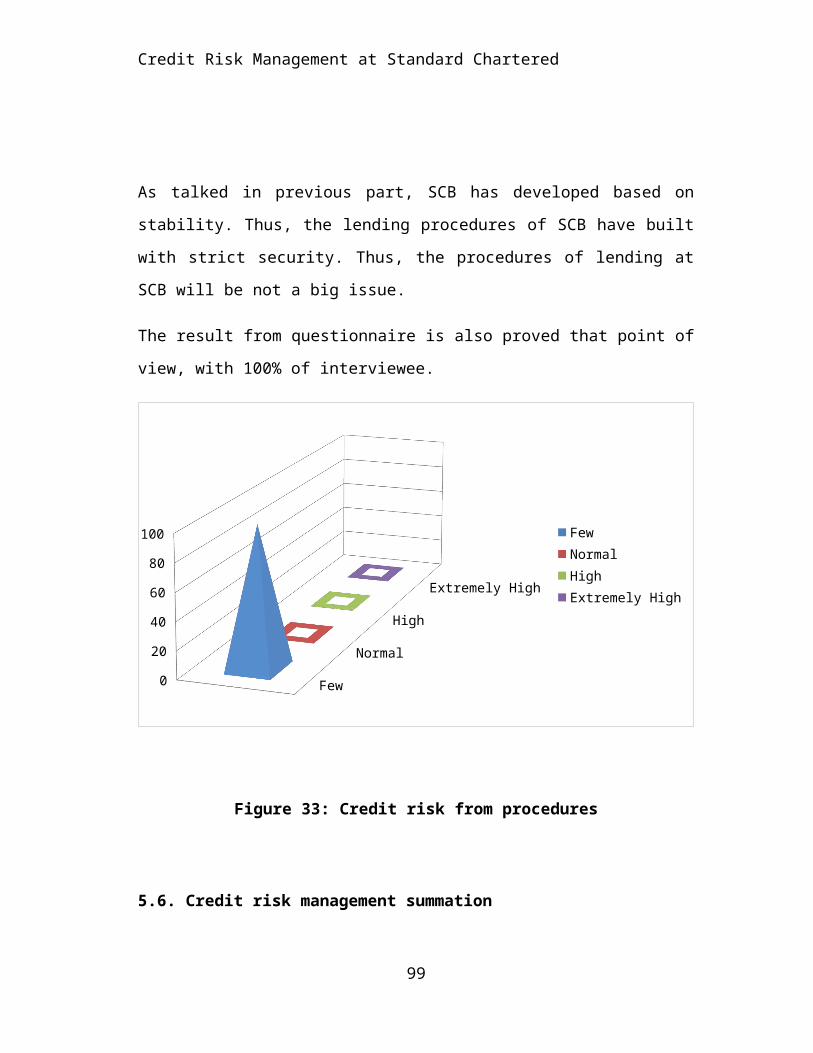

Figure 30: Credit risk from cross borrowing 60Figure 31: Credit risk from fraudsters 61Figure 32: Credit risk from staff 62Figure 33: Credit risk from procedures 63

Credit Risk Management at Standard Chartered

Chapter 1: Introduction

1. Background

Vietnam is growing with the fast speed in economy.

Vietnam’s GDP was 136 bil USD, the GDP increased 5.6 %,

the revenue per person is 1540 USD/ year, the inflation

rate is roughly 8% (2012, VBF). Besides, in financial

institutes, banks have achieved some remarkable success,

the CAR (Capital Adequacy Ratio) is 13,7% (higher than 9%

required by SBV), the lending amount against Vietnam Dong

capitalized is 95%, LDR is 91.13% (compared with 103.23%

in 2011), the liquidity was improved in crisis economy.

There outstanding number has been attracted a lot

attention from foreign investments and economy specialist.

Though keeping in safe healthy during this year, Vietnam’s

bank field was faced with a lot of problems. The bad debt

ratio was 4.9% in 2012, increased dramatically with 3.1%

in 2011; (-2.4%) is the decrease of total assets of all

bank system (2012 SBV report). Therefore, credit risk

management is really necessary for Vietnam’s economy at

that moment. If a bank collapsed, that is not problem for

1

Credit Risk Management at Standard Chartered

one enterprises, this will lead to a bad situation of

economy.

2. Objectives

Credit is a sector that brings a lot of benefits to banks

in Vietnam, but this is one of the most risky sectors

(make up 70% banking risk). Once it happens, it can lead

banks to many serious scenarios, even bankruptcy. In the

world, there are numerous studies that have been made

already for the whole credit risk management in banks.

Then, all studies has been showed off the disadvantages

and advantages of credit risk system in each country like

Takeshi Jingu (2013) for off balance sheet lending risk in

China, Yogieta S.Mehra (2010) for operational risk

management in India. However, almost researches have made

for this sector focusing on some surface elements of

credit risk such as provisioning, processing, etc, not

draw a full picture with whole scenarios can be appeared

when credit risk comes especially in Vietnam where banks

are different from western system. Therefore this study

has been made with the purpose of concentration on credit

risk management (banking) in Vietnam and help reader to

2

Credit Risk Management at Standard Chartered

possess the knowledge of risk management, especially in

credit of banking sector.

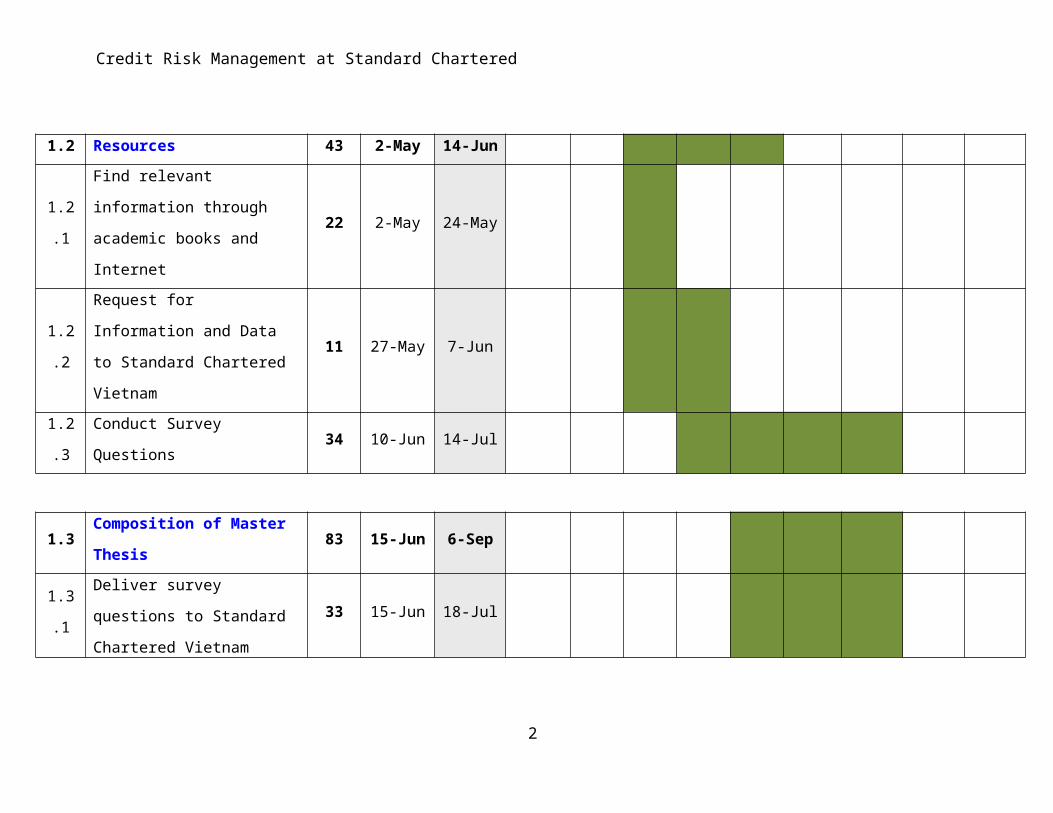

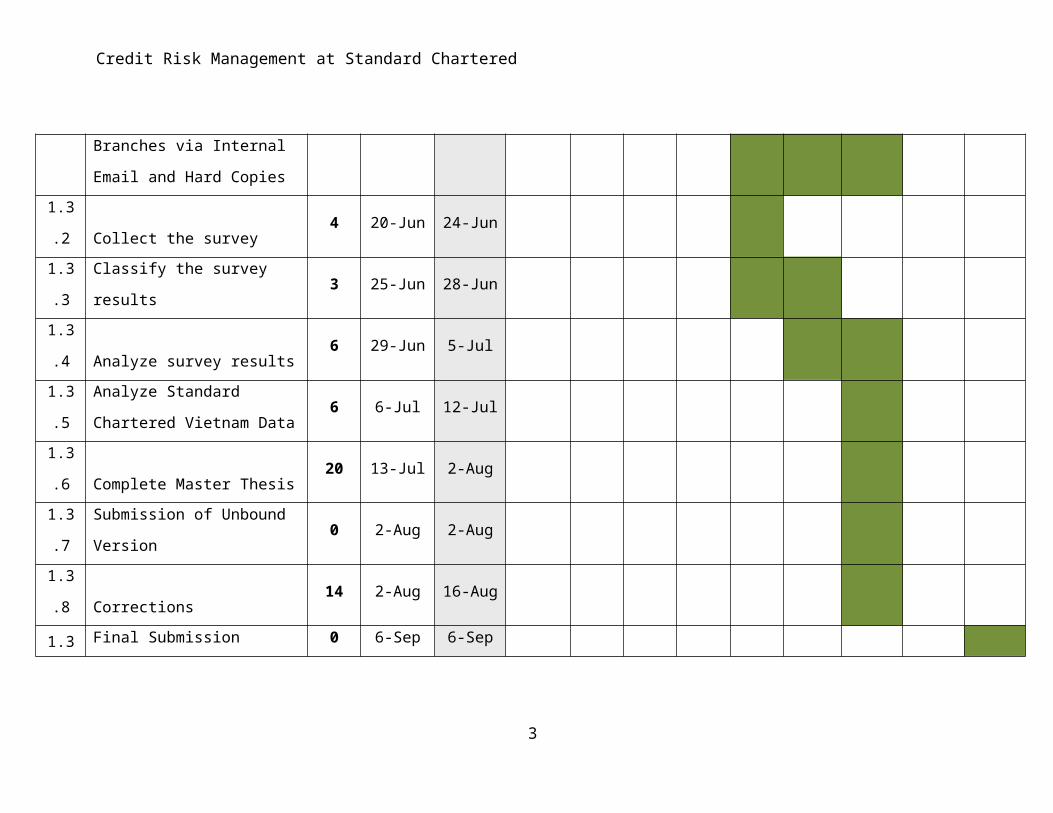

3. Structure

It is very important to build up a well framework to

follow up before go into the detail. The thesis work flow

can be summarized as diagram below

3

Credit Risk Management at Standard Chartered

In chapter 2, the literature review will be made. The

function of this chapter is to bring out the background,

knowledge and information to understand “what is the credit risk?,

how does it works ?, how can we measure it?, etc”.

The review of banking firms in Vietnam will be reflected

in the chapter 3. The reason why this chapter given in the

thesis is that we can have the full review and see the

growth of banking area in Vietnam passed through each

period. Moreover, we can look again the dramatic change of

financial institutes in Vietnam.

In chapter 4, the methodologies of research will be

indicated in this chapter. The methodologies of research

will focus on data aim, objectives of research; data

source and analyzing methods.

For the chapter 5, The credit risk management practices of

SCB will be reflected in this chapter. Besides, the4

Credit Risk Management at Standard Chartered

comparison against Basel requirement will be implemented.

On the other hand, the research is completed by a small

research.

Eventually, a conclusion and recommendations will be

listed for ending the thesis.

5

Credit Risk Management at Standard Chartered

Chapter 2: Literature review

Researches of Credit Risk Management in the world

Credit Risk Management is a very important sector for each

country. Financial institutions have right to gain money

by lending, then, they can get back the original and

interest. That is profits of all banks. However, credit

always contains a lot of risk and can not be eliminated

fully. We can just minimize risk and its bad effect to

banks, even to the whole economy.

In the world, there are many researches related to this

incident. From America to Asia, this incident is always

put in the top urgent. In the size of master thesis,

author would like to choose the most three outstanding6

Credit Risk Management at Standard Chartered

researches in the world about this domain and one of three

will be chose for master thesis flow.

Firstly, that is the research of Dr. Yuan Mu – China. The

research that he did is applied for Doctor title at

University of Sterling, UK is about China’s Banks Credit

Risk Assessment. At the beginning of the research, he

talked about the methodologies used in the research. The

methods are Soft Budget Constraint and the uncertain of

Keynesian approach. In the Keynesian, they introduce the

prefecture of quantity model in credit assessment and this

is the debate of Mr Yuan. He thought that we are living in

not perfect world, thus, generally we can not obtain the

full information. Moreover, two models above come from

western, so it is not suitable in China where is different

from politic, behavior, demographic, etc.

In the next step, he made an overview about roles of banks

and money for the economy, especially, he mentioned credit

as a factor that is not able to unloose in the economy.

After listing some knowledge about credit risk, he, then,

gave the history scales of Chinese banking history. In

this part, the viewer can see clearly the unbelievable

change of China for each period. He also mentioned the

roles of money and bank in China.

7

Credit Risk Management at Standard Chartered

Next, he drew a general view of economy of China now with

the statistic. The financial ratios related to credit area

were also dealt with. The final chapters in his research,

he used for his case studies. He did two case studies, one

focused on the credit risk management system of ICBC, the

remaining was utilized for whole banking system in a

province of China.

Nevertheless, he concluded his research by his

recommendation based on the result of interview and his

literature review.

Secondly, that is the research of Dr Edward I.Altman – USA.

In his research, he dealt with the literature review of

credit sector first. Edward has wide knowledge and

experience in banking sector because he is not only a

lecturer of New York University, but also he is the

director of credit risk centre of BNY Mellon (top 50

largest bank in USA).

The literature review of him concentrated on the effect of

change in regulatory to credit risk. Then, he mentioned

the important of credit measurement in credit risk

management. He said that “If we do not have a clearly way of Credit

Measurement, it will be a blind alley for credit risk management”. The

credit risk measurement used is the scales of risk

evaluation made by Moody’s and S&P. On the other hand, the

8

Credit Risk Management at Standard Chartered

rules of Basel were mentioned as highly importance by

Edward.

The size of Edward Research is much bigger than Dr. Yuan

because if Mr Yuan focused strongly in China, Edward used

his research to compare the credit risk management in the

United States of America and the Europe by financial

ratios like capital position, Capital/ Assets Ratio, etc.

In his research, he did not use any interview or

questionnaire. He analyzed based on actual data of banks

in the US and previous research paper.

The third research that I mentioned before is the research

of JPMorgan Chase. His research applied for banks in the

UK. JP Morgan Chase’s research has appeared in the Journal

of Credit Risk in 2013.

As other research, he also started with the literature

review. However, there are some different between 02

researches below. As normal, he went down from the basic

definition, the principle of credit risk management,

measurement, problem in credit management, but the special

thing is that he mentions 04 credit models: Merton, Rating

Actuary and Macroeconomic. Four of credit models above

will support the credit risk management in banks to be

9

Credit Risk Management at Standard Chartered

much more clearly from security in credit to protect bank

from the change.

Continuously, he said about the methodologies of his

research (aim, method and limitation). He did compare each

other between banks in the UK to find out which bank is

the best in credit risk management. The actual data and

the statistic are obviously mentioned strongly.

In summary, in the size of Master thesis for the title of

“Master of Art in Business Administration”, the author

will based on the flow of 03 researches above to find out

the problem in credit risk management of Vietnam in

general, at Standard Chartered Vietnam in special way.

Each research has advantage that we can not refuse and the

disadvantage needed to realize. The research will prefer

the way of Mr Yuan model to remaining 02 researches. The

reason is that the model of Mr Yuan applied for China

where has not totally but almost similar demographic,

politic, behavior, etc. However, the remaining researches

will support to find out the best recommendation for a

good credit risk management. Because researches applied

for UK, US, where have powerful competence in credit risk

management.

2.1. Credit risk definition

10

Credit Risk Management at Standard Chartered

In the economy, credit provider is a basic function of

banks. For almost bank in Vietnam, credit activities make

up ½ total assets and profit from lending is 2/3 against

the total profits of whole banks. However, banking risks

focus on mostly in credit activities. According to Joel

Bessis (2010), “Credit risk is the first of all risk in term of importance”.

Regarding GARP. 2012.”Credit risk is the potential loss due to the

nonperformance of a financial contract, or financial aspects of

nonperformance in any contract”.

State Bank of Vietnam (SBV) - Decision 493/2005/QĐ-NHNN,

22/04/2005. “Credit risk is the loss of payback or late payment”

Generally speaking, “Credit risk is the potential loss that is created

when banks offer credit contracts to customers. Customers do not (or can not)

take the responsibility for their loans and guarantee financial aspects”.

However, we need to understand that credit risk potential

will be kept in every loan. Although a bank has low bad

debt ration, they still face with high credit risk when

they concentrate on only type of individual customers.

Quantitative Concept: Credit Risk is reflected by the bad debt

ratio of bank

Qualitative Concept: Credit Risk is along with the quality of

credit. Means, the quality good will maintain the credit

risk low, and vice versa.11

Credit Risk Management at Standard Chartered

2.2. The components of credit risk

There is necessary to know the categories of credit risk

for having the deep understanding the environment of

credit risk. Concerning about this element, each research

have different expressions. Due to UniCredit Group, they

classified credit risk into three types: Credit Default

Risk, Concentration Risk and Country Risk. Karen A.

Horcher (2005) expressed her ideas a little bit with

author above in her book “Essentials of Financial Risk

Management”. She though that there is essential to divide

credit risk into six separate types including default

risk, counterparty pre settlement risk, counterparty

settlement risk, legal risk, country or sovereign risk and

concentration risk. However, due to GARP (2007), this

organization listed legal risk as an operational risk and

the concentration risk, is a mistake in managing credit

rather than relating as a type of credit risk. Thus, the

thesis will concentrate on the four remaining types of

credit risk classified by Karen A. Horcher (2005).

2.2.1. The default risk

12

Credit Risk Management at Standard Chartered

The definition is given by UniCredit Group is the

probability of borrower’s default. The risk appears when

customers have late payback on loan (or) can not

responsible for their obligations.“Default risk may impact all

credit-sensitive transactions, including loans, securities and derivatives” (see

UniCredit Group).

To avoid such risk, Pavla Vodová (2006) considers that

banks should separate bad customer by defining the

procedures of evaluating credit applicants and set a

maximum credit amount provided to one borrower.

2.2.2. Counterparty Risk

Firstly, according to Julius Tandler (2007), Counterpartyrisk is defined as “Risk of non-performance of counterparts onrepaying any amount of money owed to our bank”.

For evaluating the counterparty risk, the credit scoring

should be used. For example, the party who hold the credit

scoring A will have the lower counterparty risk compared

with credit scoring B.

Counterparty Risk encloses Pre-Settlement Risk and Settlement

Risk. 13

Credit Risk Management at Standard Chartered

Regarding the Pre-Settlement Risk, the Pre-Settlement Risk

arises when the party defaults before the settlement date

and can not meet the provisions of contract, e.g. A

company has a credit contract with the settlement date is

the beginning of Y+3 with the currency USD, but in the end

of Y+2, with the situation of profitable exchange rate

between VND and USD, they exchange their USD to VND in

black market to make profit. Unfortunately, after one week

the buying rate of USD rockets the market. They can not

have fulfilling USD amount as contract required at the

settlement date.

Pre-Settlement Risk includes two components, there are

current exposure and potential exposure (Julius Tandler

2007).

Settlement risk is a baking term used when the

counterparty fail to delivery their assets, money or the

term of contract at the settlement date. Investopedia

explains that “Settlement risk was a problem in the forex market up until

the creation of continuously linked settlement (CLS), which is facilitated by CLS

Bank International, which eliminates time differences in settlement, providing

a safer forex market”.

The cases of German bank Herstatt on 26 June 1974 is a

clearly example about this incident. This bank received

the foreign exchange from their counterparty in Europe,

14

Credit Risk Management at Standard Chartered

but had not made any payment to the financial institution

counterparty at the settlement date. Then, this bank was

bankrupted, leaving the international banking sector a

loss of $620 million (see Remolona 1990).

2.2.3. Country Risk (Sovereign Risk)

As collected from Wikipedia, “Country risk refers to the risk ofinvesting in a country, dependent on changes in the business environmentthat may adversely affect operating profits or the value of assets in a specificcountry”.

Ms Cristina Alina Naftanalia (2012) guessed that “Countryrisk is a materialization risk of the losses caused by the situation and evolutionof the political and macroeconomic developments from the partner country”;while the Sovereign Risk was considered by her that thegovernment uses their authority to guarantee thetransactions.

2.3. Credit Risk Management

2.3.1. What is the credit risk management?

15

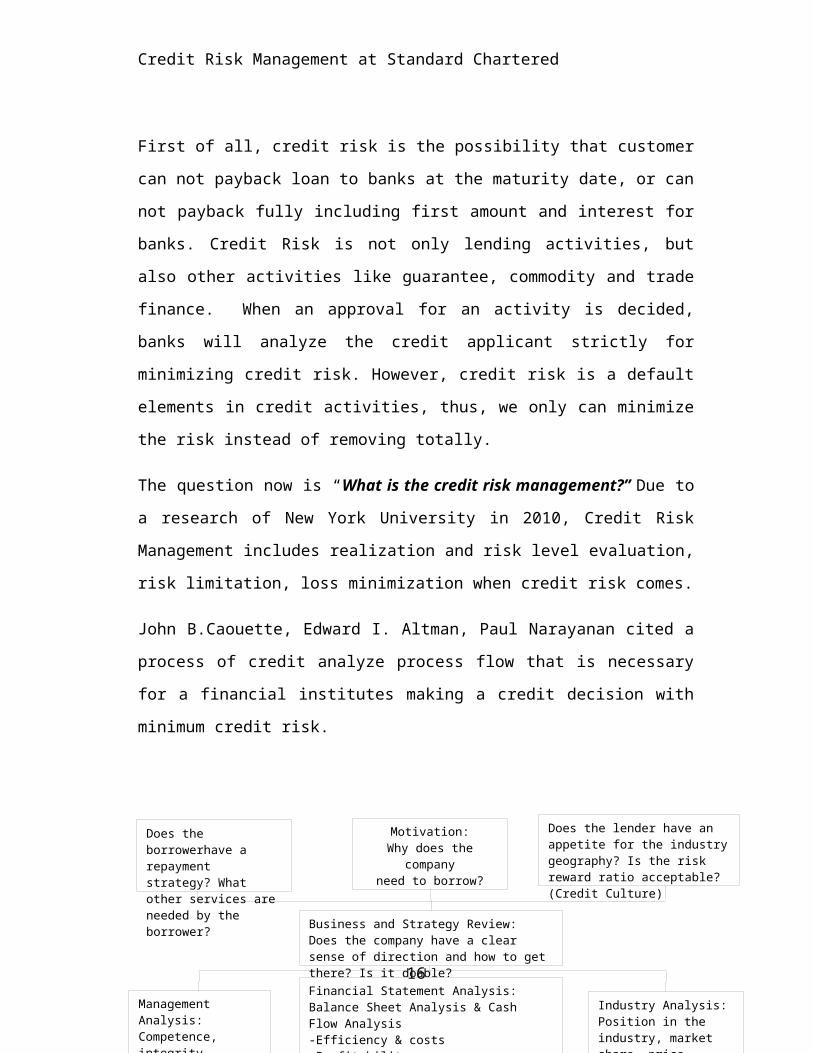

Does the borrowerhave a repayment strategy? What other services are needed by the borrower?

Motivation:Why does the

companyneed to borrow?

Does the lender have an appetite for the industry geography? Is the risk reward ratio acceptable? (Credit Culture)

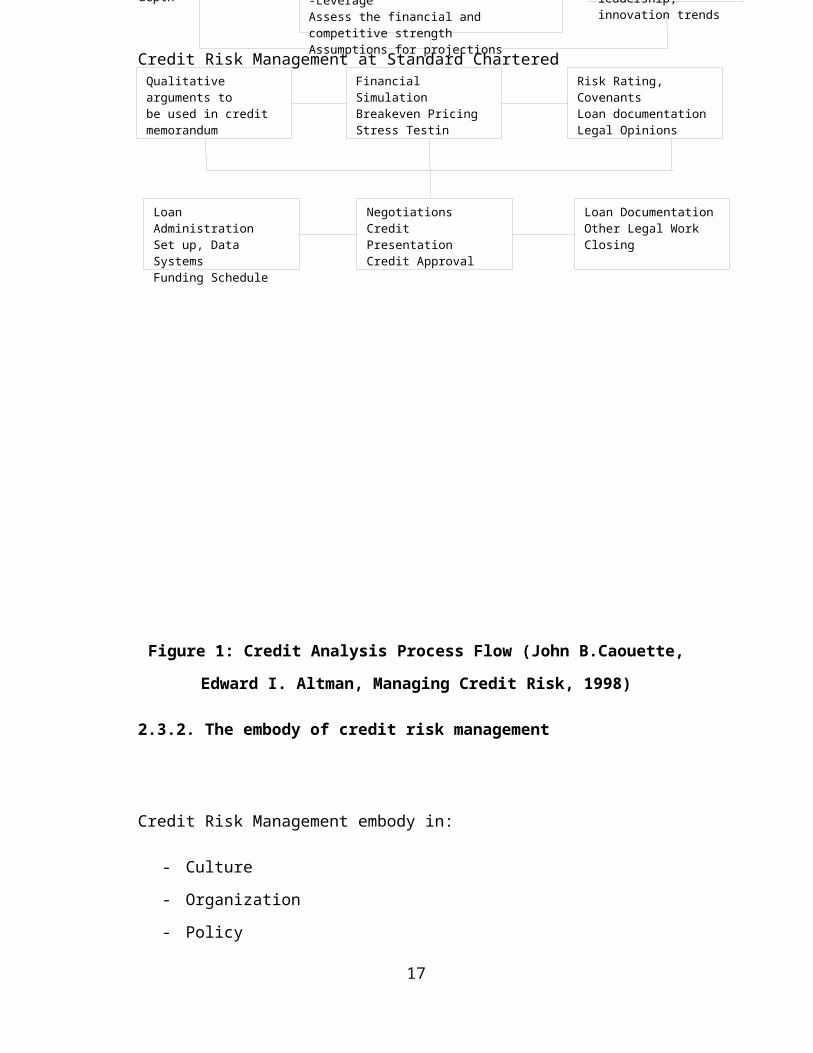

Business and Strategy Review: Does the company have a clear sense of direction and how to get there? Is it doable?Financial Statement Analysis: Balance Sheet Analysis & Cash Flow Analysis-Efficiency & costs-Profitability-LeverageAssess the financial and competitive strengthAssumptions for projections

Management Analysis: Competence, integrity, depth

Industry Analysis: Position in the industry, market share, price leadership, innovation trends

Credit Risk Management at Standard Chartered

First of all, credit risk is the possibility that customer

can not payback loan to banks at the maturity date, or can

not payback fully including first amount and interest for

banks. Credit Risk is not only lending activities, but

also other activities like guarantee, commodity and trade

finance. When an approval for an activity is decided,

banks will analyze the credit applicant strictly for

minimizing credit risk. However, credit risk is a default

elements in credit activities, thus, we only can minimize

the risk instead of removing totally.

The question now is “What is the credit risk management?” Due to

a research of New York University in 2010, Credit Risk

Management includes realization and risk level evaluation,

risk limitation, loss minimization when credit risk comes.

John B.Caouette, Edward I. Altman, Paul Narayanan cited a

process of credit analyze process flow that is necessary

for a financial institutes making a credit decision with

minimum credit risk.

16

Financial Statement Analysis: Balance Sheet Analysis & Cash Flow Analysis-Efficiency & costs-Profitability-LeverageAssess the financial and competitive strengthAssumptions for projections

Management Analysis: Competence, integrity, depth

Industry Analysis: Position in the industry, market share, price leadership, innovation trends

Qualitative arguments to be used in credit memorandum

Financial SimulationBreakeven PricingStress Testin

Risk Rating, CovenantsLoan documentationLegal Opinions

Loan AdministrationSet up, Data SystemsFunding Schedule

Loan DocumentationOther Legal WorkClosing

NegotiationsCredit PresentationCredit Approval

Credit Risk Management at Standard Chartered

Figure 1: Credit Analysis Process Flow (John B.Caouette,

Edward I. Altman, Managing Credit Risk, 1998)

2.3.2. The embody of credit risk management

Credit Risk Management embody in:

- Culture

- Organization

- Policy

17

Credit Risk Management at Standard Chartered

(See Heinz-Peter Berg, 2010)

2.3.2.1. Culture

According to Federal Reserve Bank of Philadelphia, “Credit

culture more narrowly as the sum of all the characteristics of an

organization's unique behavior in its extension of credit.It not only

encompasses the tangible written policies and procedures, but also intangible,

such as ideas, traditions, skills, attitudes, philosophies, and standards.”

In the book “Credit Risk Management” of Joetta Colquitt

(24 May 2007), he thought that a great credit culture

should have

- Highest annual growth rates of loan

- Weighted credit quality goals for bonds

- Targeted returns to be measured against inclusive of

any asset price changes and interest spread income

- Acceptable exposure levels should be quantified for

the loan mix of the portfolio according to the

liquidity and term structures of the different debt

types.

18

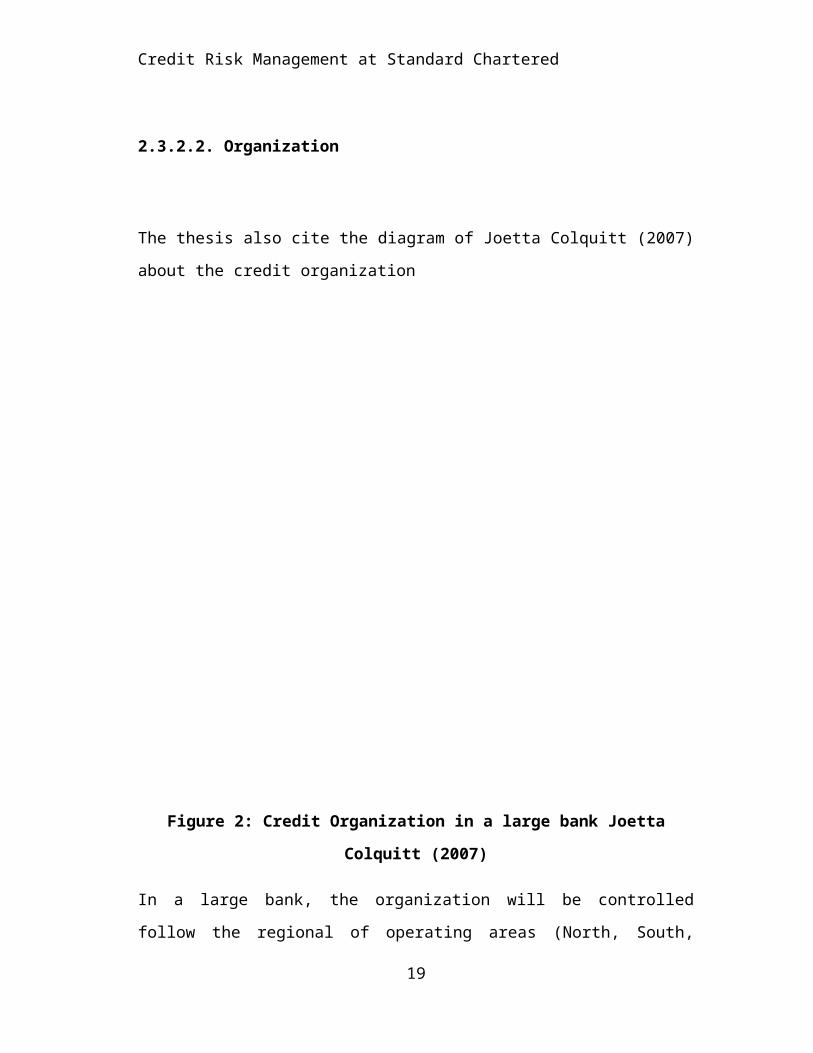

CEOCredit OfficerCredit AdminCredit ManagerCredit Risk Management at Standard Chartered2.3.2.2. Organization

The thesis also cite the diagram of Joetta Colquitt (2007)

about the credit organization

Figure 2: Credit Organization in a large bank Joetta

Colquitt (2007)

In a large bank, the organization will be controlled

follow the regional of operating areas (North, South,

19

Credit Risk Management at Standard Chartered

West, East), and the sales field will be separated with

the credit risk management (as figure above). The

separation will help the credit go under the transparent

and minimizing the loss of credit.

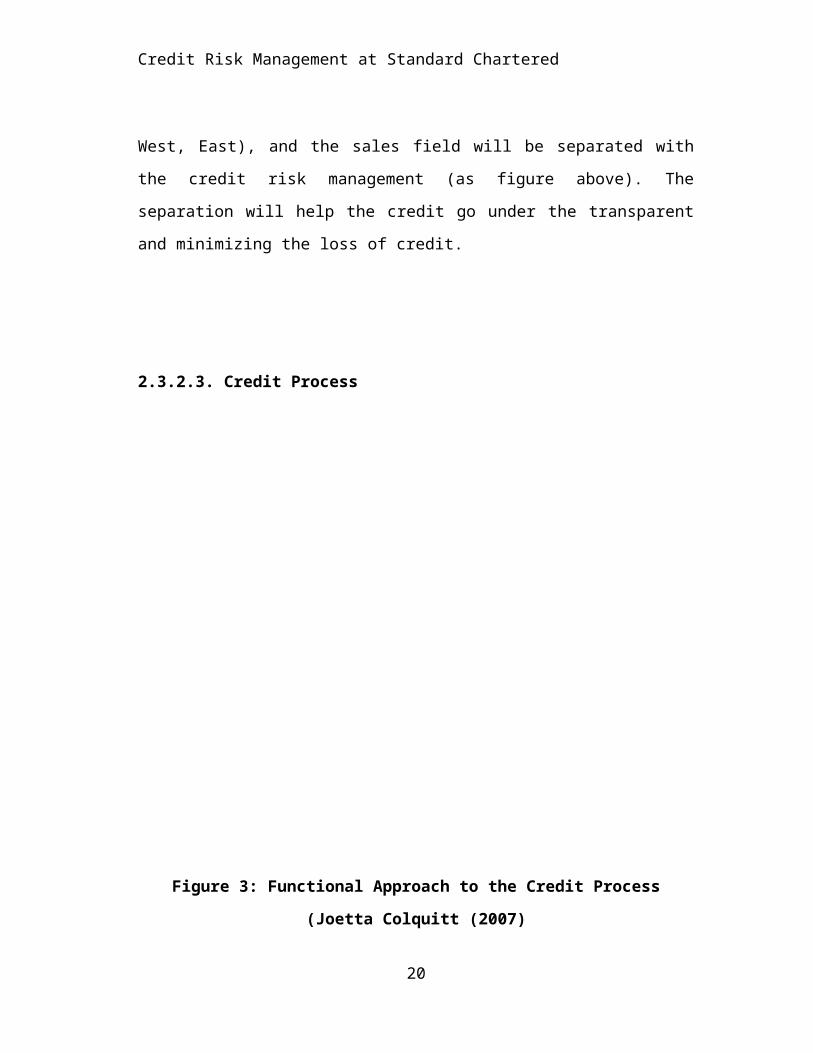

2.3.2.3. Credit Process

Figure 3: Functional Approach to the Credit Process

(Joetta Colquitt (2007)

20

Credit Risk Management at Standard Chartered

When a customer comes to bank for a loan request, the

first staff they met is Relationship Manager who can

advise which loan package that is suitable for customer,

and collect the credit application of customer. Then,

he/she will propose the documentation of customer to get

the approval for disbursement after assessing

documentation. RM must follow the loan from the opening

case to ending case. If there is any problem with loans

(customers can not payback loan), RM must send the request

to investigate and further action to the work out and

recovery department.

2.4. Risk Causes

The risk causes of credit can be divided in to Objective

Causes and Subjective Causes. (Kenneth J. Singleton, 2003).

2.4.1. Subjective Causes

Human Resources and Work forces

21

Credit Risk Management at Standard Chartered

- The limitation of creditor competence is the big reason

for Credit Risk happen. They evaluate and finalize wrongly

credit decision to non-profit investment, non-effect

business plan, etc. On the other hand, the unstable

financial analyze skill of creditor takes them into fail

in large project consider and decide step with long

investment tenor, project feasibility and capability.

- The morality of creditor is very important in right

credit decision with high influence. Indeed, if creditor

receives corrupt money from project owners or individual

customers for make an artificial report or financial

statements, it can take them to wrong credit decision,

then, make loss to banks.

Operations and Technology

- The credit operates base on the internal rules, DOI

(Digital Object Identifier), Process. However, in credit

risk management, all elements above sometimes are not

complied, not follow the loan distinction, reserves, then,

it weakens the credit risk management of bank. On the

other hand, the technology is one of the reasons that

raise the banking credit risk.

22

Credit Risk Management at Standard Chartered

- Credit risk may come from verifier board, checker teams.

If they do not follow strictly the process, bank rules,

the risk can be happened.

- The next reason is the policy. Every bank has particular

policy combine with their business strategy. Yet, they

will make a big mistake when create regulation with the

purpose of rocketing business. At that moment, the policy

will be changed into focusing on one kind of economic

element, expanding long term loans while lack of long term

capital, concentrating on profits and bypass the credit

risk compliance.

2.4.2. Objective Causes

Market and Client

- Price fluctuation on the market can make the input

prices (iron, steel, etc.) be high. From this, the

activities of enterprises are not smooth as normal. Thus,

the credit actives will be also influenced. On the other

hand, the compound market of exporting and importing

market can effect direct to banking credit operations.

23

Credit Risk Management at Standard Chartered

- The cause also comes from customers. They use lending

with other purpose, not focus on business, this have led

the liabilities to increase higher and higher including

banking loans. Secondly, lack of enterprise management can

engender bad result for company even collapsed. Bank can

not collect totally asset from bankruptcy company and get

lost. Thirdly, this is lack of attitude. They did not have

the manner to pay back money while they have the capacity.

Politics and Economy

- The change of mobilization interest ceiling rate from

SBV can lead the lending interest went up. As the result,

many enterprises can not pay back the loan with high

interest and put the burden on the bank.

- The depression of global economy brings the negative

effects to companies. Surplus supply while lack of demand.

They can not sell their goods, products, then, the profits

go down.

- The fluctuation of foreign exchange, gold rate, etc

influences also the enterprise activities.

24

Credit Risk Management at Standard Chartered

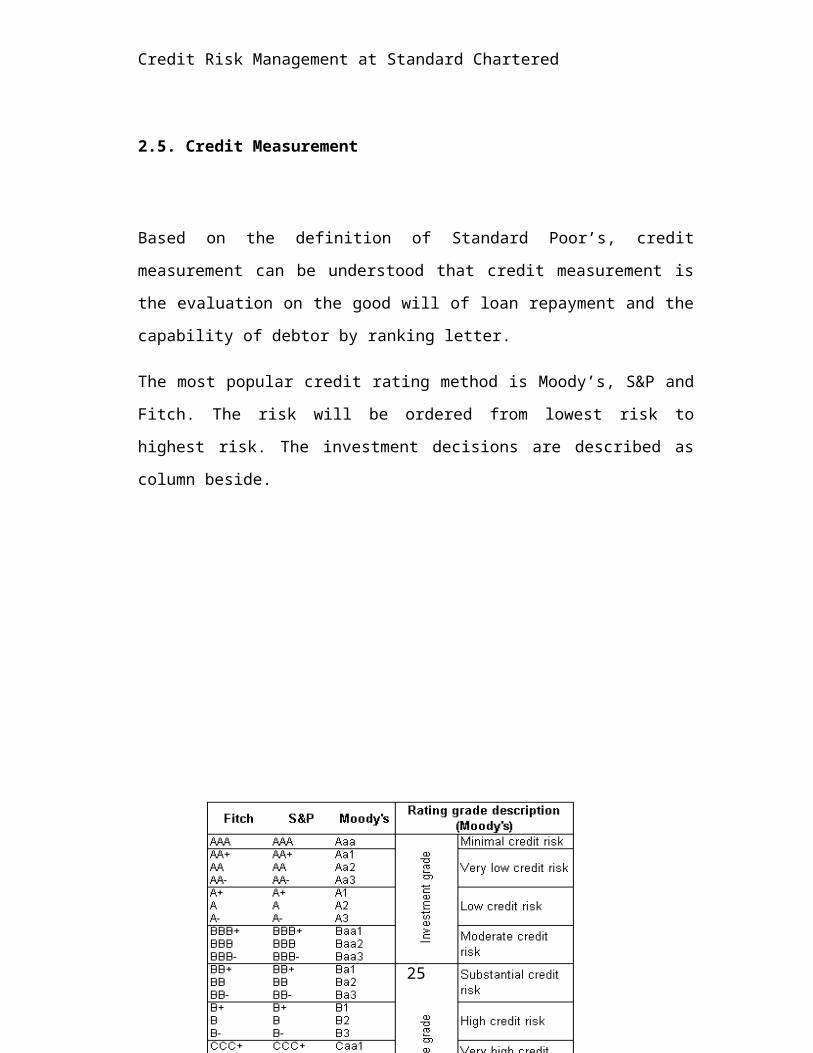

2.5. Credit Measurement

Based on the definition of Standard Poor’s, credit

measurement can be understood that credit measurement is

the evaluation on the good will of loan repayment and the

capability of debtor by ranking letter.

The most popular credit rating method is Moody’s, S&P and

Fitch. The risk will be ordered from lowest risk to

highest risk. The investment decisions are described as

column beside.

25

Credit Risk Management at Standard Chartered

Figure 4: Credit Rating System of Fitch, S&P and Moody’s

2.6. Basel Committee recommendation in Credit Risk

Management

Basel Committee was established by President of Central

Bank G10 in 1975 (See Wikipedia). This committee has

executive representative of national banking observation

unit of Belgium, Canada, France, Germany, Italy, Japan,

Holland, The United Kingdom, The United States of America.

Basel Committee has annual meeting at International

Payment Bank in Washington, US or Basel City of

Switzerland. The rules of Basel Committee in credit risk

management focus on (See Studies on Credit Concentration,

Basel Committee on Banking Supervision 2005)

26

Credit Risk Management at Standard Chartered

Rules 1: BOM is responsible for approval and re-evaluate

frequently the credit risk management policy and strategy.

Credit Risk Strategy reflects the level of risk acceptance

with demand profit of bank. Besides, Credit Risk Strategy

also identify the target market and general features in

Credit Portfolio.

Rules 2: BOED must accept to operate credit activities

under bad debt rate required by BOM. They also must

develop policies to foresee credit risks in whole

portfolio.

Rules 3: All banks must identify clearly and manage

strictly in all products and services. For new product

ranges, it need to be verified, tested, risk controlled

before lunching or sent to market with the approval from

BOM.

Rules 4: All banks must set up credit limit for whole

credit portfolio

Rules 5: All banks must work within the required credit

limit

Rules 6: All banks must have a clear process and policies

Rules 7: Lending Operations will be made based on fairly

treating between two partners

27

Credit Risk Management at Standard Chartered

Rules 8: All banks must update frequently the status of

loans for loans that have signal of bad debt or credit

risk.

Rules 9: All banks must build the system to monitor every

loans to ensure that the reserve is whether enough or not.

Chapter 3: Overview of Credit Risk Management in

Viet Nam Banks

Vietnam is a developing country with fast growth speed

compared with some countries in Asia and over the world.

The banking industry of Vietnam has developed since 1951

after the events of State Bank of Vietnam establishment.

Although banking field in Vietnam has experienced over 60

years – a very modest number with other developed country

like Japan, China, the US or the UK. However, Banks in

Vietnam has achieved a lot of success and has contributed

greatly to the Vietnam’s economy.

28

Credit Risk Management at Standard Chartered

1. The organization of banks in Vietnam

As the decision of Vietnamese government – 163 CP, Vietnam

has only one State Bank that has the unique function of

printing notes and managing the cash flow. SBV will be at

the centre and manage all banks in Vietnam.

Vietnam has approximately 70 working financial

institutions including Policy Banks, Governmental Credit

Foundation, Commercial Banks, Wholly-owned Foreign Banks,

Branches and representative of foreign banks, Join Venture

Banks.

2. The growth in total assets of banks in Vietnam though

period

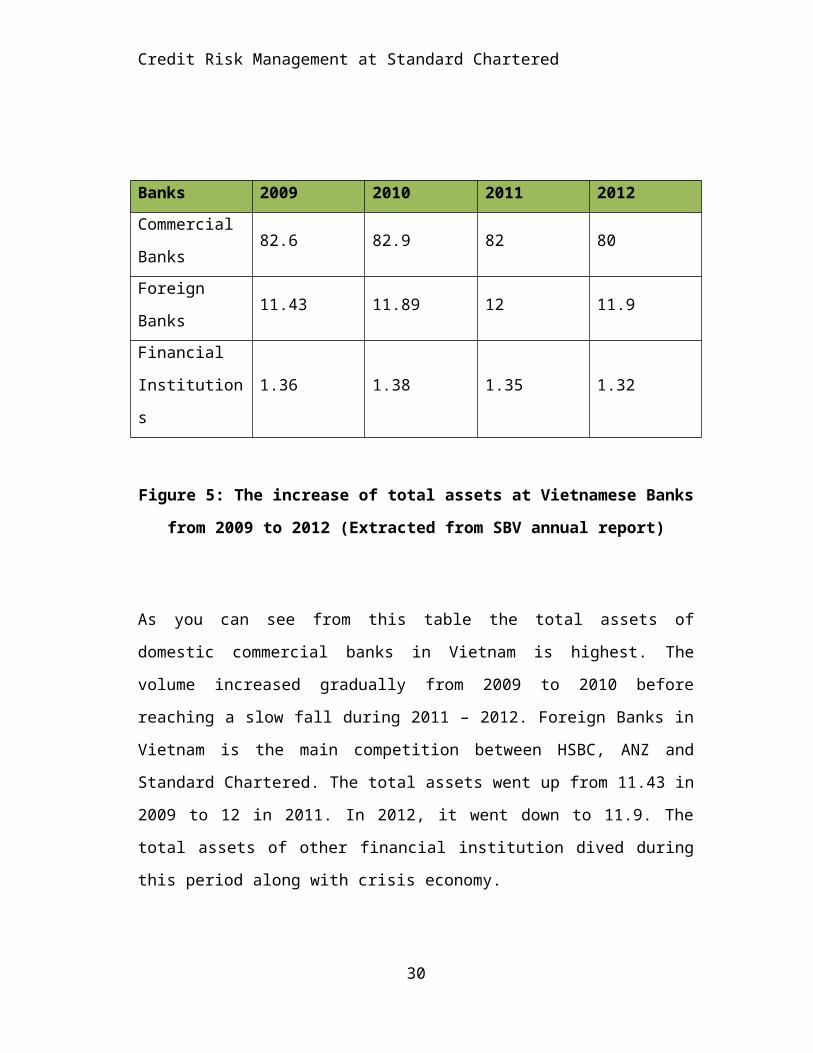

Unit: thousand billions vietnam dong

29

Credit Risk Management at Standard Chartered

Banks 2009 2010 2011 2012Commercial

Banks82.6 82.9 82 80

Foreign

Banks11.43 11.89 12 11.9

Financial

Institution

s

1.36 1.38 1.35 1.32

Figure 5: The increase of total assets at Vietnamese Banks

from 2009 to 2012 (Extracted from SBV annual report)

As you can see from this table the total assets of

domestic commercial banks in Vietnam is highest. The

volume increased gradually from 2009 to 2010 before

reaching a slow fall during 2011 – 2012. Foreign Banks in

Vietnam is the main competition between HSBC, ANZ and

Standard Chartered. The total assets went up from 11.43 in

2009 to 12 in 2011. In 2012, it went down to 11.9. The

total assets of other financial institution dived during

this period along with crisis economy.

30

Credit Risk Management at Standard Chartered

3. Operating Environment in Vietnam’s banking domain

Vietnam’s banks operations have been effected negatively

from macro economy in recent years. The world economic

crisis impacts greatly to operations of banks. Besides

that Vietnam suffers the highest inflation rate in history

with the largest number around 18% in the period from 2009

to 2012. Thus, SBV issued the tightened policies for

curbing inflation. The capitalization interest went down,

and lending interest rocketed market, the liquidity has

been in dilemma.

At the end of 2010 and beginning of 2011, the tightened

policies of SBV showed clearly in increase the interest of

reimbursement and decrease credit growth limit. Therefore,

commercial banks Vietnam coped with the difficulties in

reaching projected revenues.

The element of gain/loss FX in recent years also is the

important factor that impacted directly to operations of

banks. In 2011, the exchange rate between VND and USD for

31

Credit Risk Management at Standard Chartered

interbank increased by roughly 9%. After adjustment of

exchange rate with the high inflation rate, the forex

market is in stressed.

Other factor is the gold trade. Gold trade in recent times

has been managed strictly from SBV. From 01st Jan 2013,

all commercial banks do not have the authority for trading

gold. This decision from SBV leads many banks to loss

heavily in profits and capital.

After reviewing the operating environment of Vietnamese

banks, we can realized that SBV has been careful in

managing banks in Vietnam during difficulties economy over

the world with the purpose of avoiding to be in case like

the corruption of giant financial bodies in USA.

4. Credit Risk Ratio

Credit Risk Ratio is calculated as

Credit Ratio = CurrentLiabilitiesCurrentAssets

(See Basel II)

32

Credit Risk Management at Standard Chartered

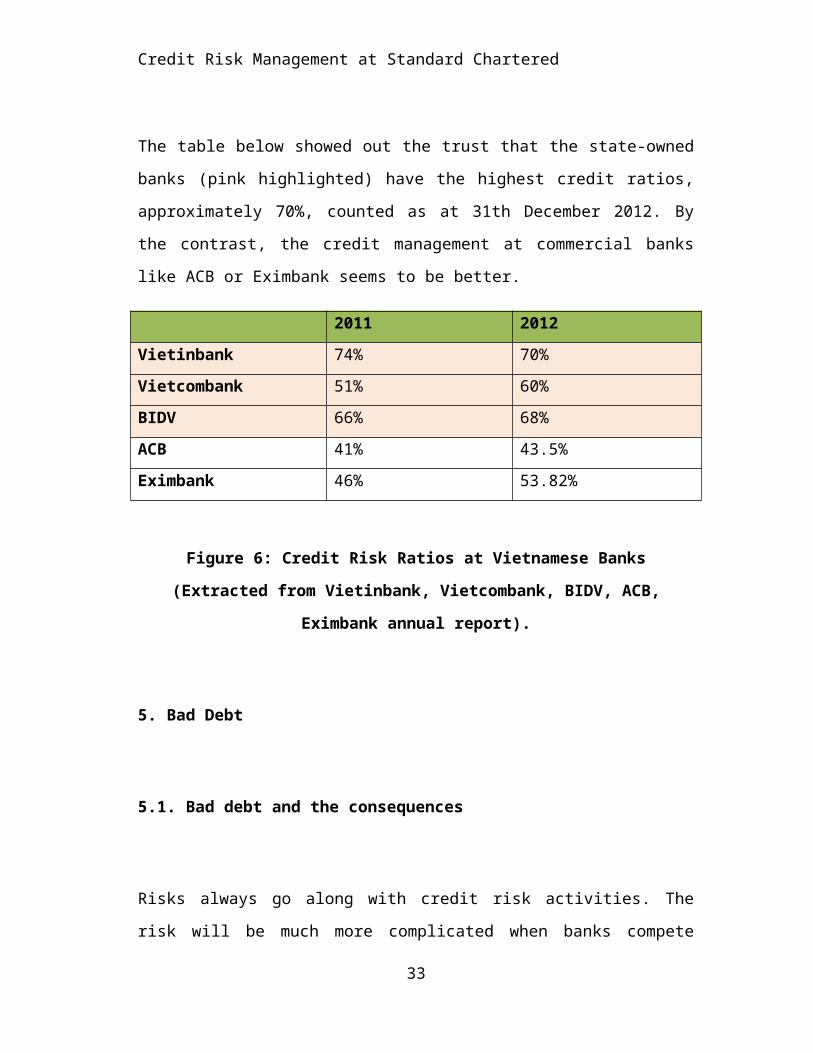

The table below showed out the trust that the state-owned

banks (pink highlighted) have the highest credit ratios,

approximately 70%, counted as at 31th December 2012. By

the contrast, the credit management at commercial banks

like ACB or Eximbank seems to be better.

2011 2012Vietinbank 74% 70%Vietcombank 51% 60%BIDV 66% 68%ACB 41% 43.5%Eximbank 46% 53.82%

Figure 6: Credit Risk Ratios at Vietnamese Banks

(Extracted from Vietinbank, Vietcombank, BIDV, ACB,

Eximbank annual report).

5. Bad Debt

5.1. Bad debt and the consequences

Risks always go along with credit risk activities. The

risk will be much more complicated when banks compete

33

Credit Risk Management at Standard Chartered

together to have many more customers on their hands.

Stages of credit evaluation can be ignored. They prefer

the amount of disbursement to the credit risk management.

From this, it will bring big risk with huge losses to

banks in Vietnam. “Bad debt in the banking sector is a

major concern”, Mr. Le Xuan Nghia, the deputy head of the

National Financial Supervisory Committee.

Bad debt will be a true disaster if it comes true for

banks. The first consequence can be listed out is that bad

debt may lead to decrease the cash flow. When the cash

flow is affected, there is a problem in credit activity of

this bank. They can not have enough money for credit

sector as usual while this is the main sector of banks

with highest revenue. On the other hand, individual

customers, SMEs, corporations are hard to approach the

capital of banks.

Secondly, bad debt is the burden of economy. Bad debt will

not only effect to banks, but also the whole economy. Bad

debt and low interest rate will calm the development of

economy.

Thirdly, if banks have bad debt, they will have plans to

settle the property of customers. However, with the

downturn of economy, this work is not simple, especially

in Vietnam. There are some conflicts between legal

34

Loans in tenorLoans overdue under 10 days Qualified - Group 1Loans overdue from 10 to under 30 daysNotice - Group 2Loans overdue from 30 days to under 90 daysUnder - Qualified - Group 3Loans overude from 90 days to under 180 daysDoubful - Group 4Loans overdue over 180 days Possible loss - Group 5Credit Risk Management at Standard Chartereddocuments. Due to 03/2001/TTLT-NHNN of SBV, banks can not

sell the asset of loans to collect debt. However, the

announcement number 195 of SBV said that banks can sell

the asset of loans directly to collect debt without

permission of debtors. Furthermore, the process of selling

the assets and suing has been taken a lot of time. The

capital will be kept under the mortgage for a long time

and can not be used.

5.2. Bad debt number in Vietnam

Bad debt in Vietnam will be divided into five groups as

the official decision of SBV (15/2010/TT-NHNN, 2010)

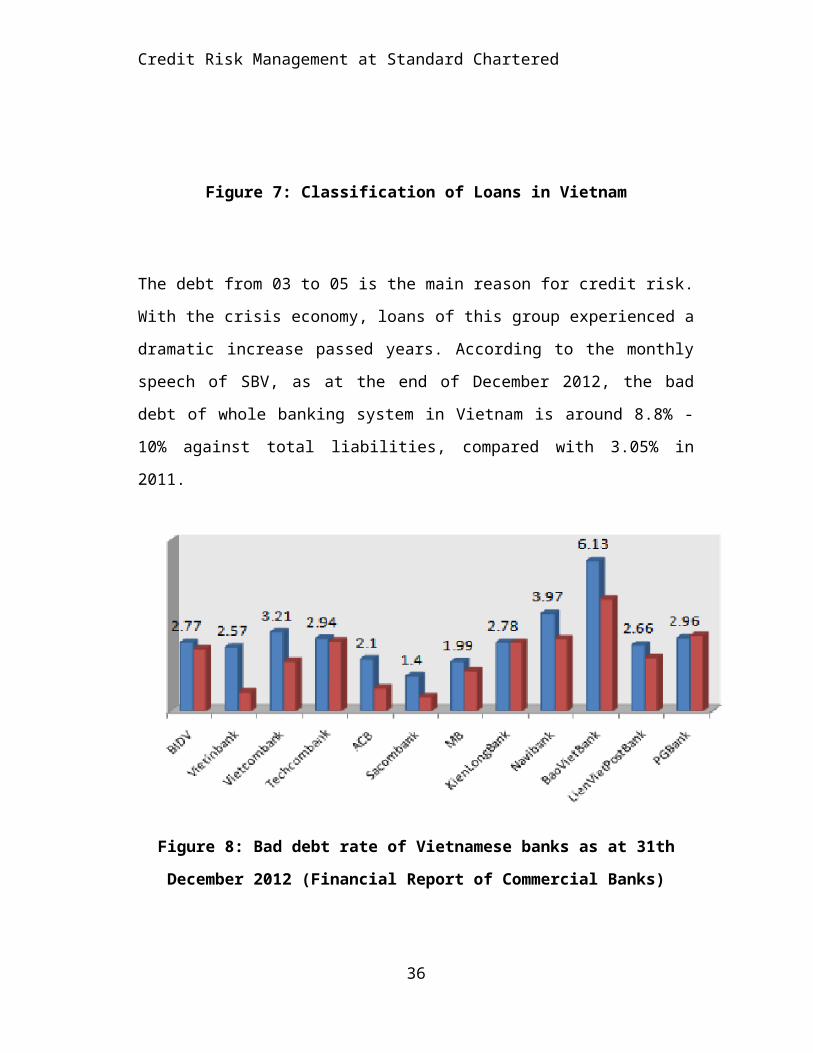

35

Credit Risk Management at Standard Chartered

Figure 7: Classification of Loans in Vietnam

The debt from 03 to 05 is the main reason for credit risk.

With the crisis economy, loans of this group experienced a

dramatic increase passed years. According to the monthly

speech of SBV, as at the end of December 2012, the bad

debt of whole banking system in Vietnam is around 8.8% -

10% against total liabilities, compared with 3.05% in

2011.

Figure 8: Bad debt rate of Vietnamese banks as at 31th

December 2012 (Financial Report of Commercial Banks)

36

Credit Risk Management at Standard Chartered

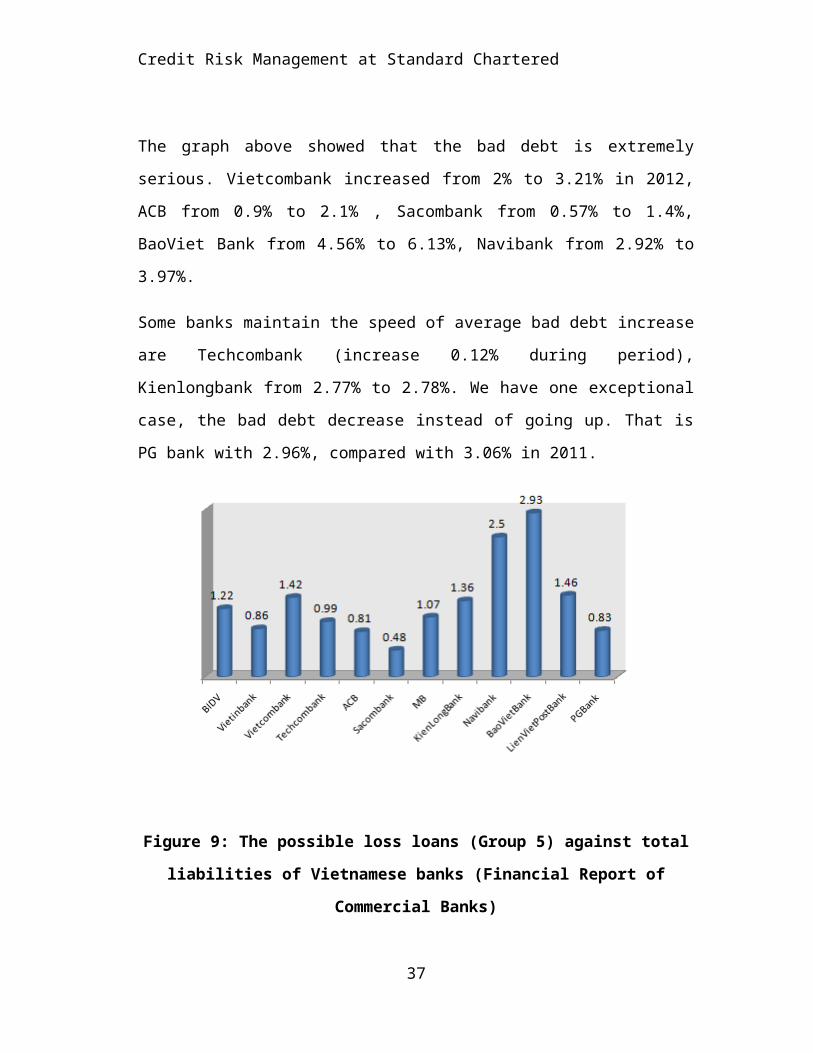

The graph above showed that the bad debt is extremely

serious. Vietcombank increased from 2% to 3.21% in 2012,

ACB from 0.9% to 2.1% , Sacombank from 0.57% to 1.4%,

BaoViet Bank from 4.56% to 6.13%, Navibank from 2.92% to

3.97%.

Some banks maintain the speed of average bad debt increase

are Techcombank (increase 0.12% during period),

Kienlongbank from 2.77% to 2.78%. We have one exceptional

case, the bad debt decrease instead of going up. That is

PG bank with 2.96%, compared with 3.06% in 2011.

Figure 9: The possible loss loans (Group 5) against total

liabilities of Vietnamese banks (Financial Report of

Commercial Banks)

37

Credit Risk Management at Standard Chartered

Overall, almost bank have twice increase of this group as

at 31th December 2012. As the requirement of 15/2010/TT-

NHNN, 2010, for loans in group 5, all banks must keep the

reserve at 100%.

As can be seen from this chart, the highest number is

belonged to BaoViet Bank, i.e. 2.93%. The second place is

Navibank with the number of 2.5%. The remaining positions

are LienVietPostBank, Vietcombank, Kienlongbank with the

number of 1.46%, 1.42%, 1.36% respectively.

Other banks have the loans in this group at roughly 1% are

Vietinbank (0.86%), Techcombank (0.99%), ACB (0.81%), PG

Bank (0.83%).

In general, the highest loans of group 5 are focus on

small banks with low credit management system. “State-

owned economic groups are performing very inefficiently.

They have used a large part of the national capital and

are accumulating bad debts for banks" Mr Nghia, a former

central bank official said. The speech of him is the most

suitable answer for the case of Vietcombank.

5.3. Bad Debt Controlling in Vietnam

38

VAMC InvestorsBanks

Government

Credit Risk Management at Standard Chartered

World Economy has been experienced a deep fall. The

consequence is that enterprises can not sell their good,

high inventory. Then, they are not able to pay back loans

to banks and lead to create bad debs. In Vietnam, after a

slow decrease of bad debt, it went up over the two passed

quarter in 2013 (from 4.14% in 2012 to 4.65% in 2013 –

VnEconomy). As forecasted and experienced the deep

consequences, Vietnam Government has decided to create

Vietnam Asset Management Company – VAMC on June 2013.

VAMC was established based on the decision number 53 of

SBV. Follow this decision, if financial institutions have

bad debt rate over 3%, they will be required to sell for

VAMC.

39

Credit Risk Management at Standard Chartered

Figure 10: Vietnam Asset Management Company in settling

the bad debt

VAMC uses the capital of government for purchasing the bad

debt of banks. The bad debts include the assets of debtors

when applying a loan, bonds, etc. Then, company will re-

sell those assets to investors. In 2013, Vietnamese

Government estimates to settle around 80 -100 thousand

billions VietnamDong of bad deb (VnEconomy).

For dealing with bad debt, banks have been required

compulsory reserves by SBV (TT02-2013-NHNN,2013). The

required rate is:

- Group 1: 0%

- Group 2: 5%

- Group 3: 20%

- Group 4: 50%

- Group 5: 100%

The required reserves can help banks to avoid bankruptcy

in case of too much bad debts. The required reserves must

be calculated as formula below

R = Max (0, A-C) x r

While: R Compulsory Reserve Amount40

Credit Risk Management at Standard Chartered

A Loan Amount

C Collateral Valuation

r Reserves Rate Required

(See SBV regulation, 493/2005/Q.-NHNN, 2005)

Finally, the SBV’s decision number 780 has cited about the

debt restructuring. If loans are in group 1, but customers

are in dilemma and facing with difficulties in paying

back, financial institution can consider the debt

restructuring (including adjust tenor and debt

rescheduling) after strictly evaluation. This action can

support enterprise to have more time to payback loans.

During this time, they will have plan and strategy to push

up the operations of company and pay back money to banks.

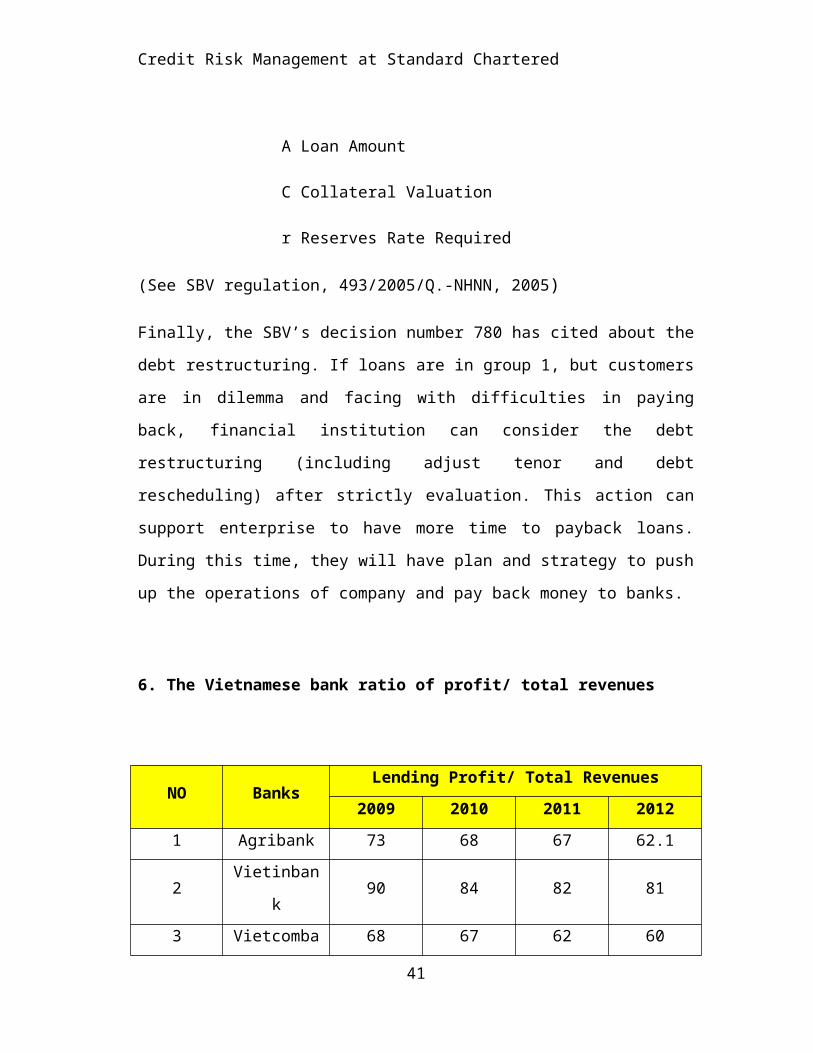

6. The Vietnamese bank ratio of profit/ total revenues

NO BanksLending Profit/ Total Revenues

2009 2010 2011 20121 Agribank 73 68 67 62.1

2Vietinban

k90 84 82 81

3 Vietcomba 68 67 62 60

41

Credit Risk Management at Standard Chartered

nk4 BIDV 70 72 71 715 ACB 63 63 61 59

6Standard

Chartered58 58 57.5 58

Figure 11: Extracted from banks financial annual report.

This table showed that, with the lending profit/ total

revenues over 50%, this is also means that the lending

operation is the main area of all banks in Vietnam.

Therefore, if banks do not have the credit risk management

strong enough, banks will face with a lot of troubles come

from the market, this is also effected to whole Vietnamese

economy.

Chapter 4: Research methodology

4.1. Research purpose and target42

Credit Risk Management at Standard Chartered

In the basic way, the purpose and target of the research

is to show the practices of SCB in credit risk management

by analyzing current financial ratios of SCB, describing

the credit management of SCB. On the other hand, author

would like to provide the overview of credit market in

Vietnam with scope of Vietnam Economy, bad debt statistic,

etc. Finally, the research includes a small survey used

for SCB staff with the purpose of investigating the root

causes of credit risk of SCB. Then, author would indicate

some recommendations for credit risk improvement at SCB.

Generally, the research will answer respectively those

answers below:

- Which credit risk is SCB coping?

- How can describe the credit management system of SCB?

(lending procedures, credit management organization,

credit policies, credit measurement)

- How is safety of SCB financial ratios?

- Does SCB credit risk management satisfy with the

requirement of Basel?

- After doing the survey, what do the causes of SCB

credit risk come from?

- What are the suggestions for enhancing the credit

risk management at SCB?

43

Credit Risk Management at Standard Chartered

4.2. Data

For all researches in the world, we need support

information. The support information is divided into 2

types: primary and secondary. In this thesis, the primary

and secondary information are used.

4.2.1. Secondary information

As business dictionary, “Secondary data is collected by someone

other than the user”. E.g. a student does a research in asset

and liability management in bank can use paragraph that

describes the general asset management of country from

ministry of finance.

Secondary information is the basis for everyone who has

started a research. The second chapter – literature review

is an example of secondary information collection.

Secondary information may be found from a lot of

references. It can be from books, magazines, newspapers;

or from Internet; even from others experiences.44

Credit Risk Management at Standard Chartered

All secondary data that was collected during master work

is really necessary for the author and help author to

solve with problems in credit risk management of banks in

Vietnam. The information, data of banks in Vietnam is

always kept in secret. The approach with this kind of

information is really hard, but, with the support of

Standard Chartered Vietnam and other banks colleagues,

author has obtained a lot of precious secondary data which

is really useful for the dissertation.

4.2.2. Primary information

If secondary data is collected from others and it will be

summarized and categorized by author, primary data will be

processed by the author. “Data observed or collected directly from

first-hand experience”, quoted from Business Dictionary.

In a dissertation, primary information is one of the best

ways that help students to apply the theoretical knowledge

that is received from academic environment into reality.

It will bring an effective view of thesis about problem,

with the comparison between the practices and literature.

Then, the productivity of article will be higher.45

Credit Risk Management at Standard Chartered

During the size of master dissertation, primary data will

be also utilized by author. The purpose of using this

method is that primary data will support author to find

out the true causes of credit risk to Standard Chartered

Vietnam, then, author can propose right and suitable

solutions for credit risk improvement at SCB. The method

of primary information is to use questionnaire. The

participant for questionnaire is SCB staff.

4.3. Information gathering method

With the purpose of research, there are really necessary

to combine the methodology of qualitative and quantitative

methods for the highest and the most effective

productivity. The usage of both is called mixed method.

Based on the definition of Dr. Johnson, “Mix research - research

that involves the mixing of quantitative and qualitative methods or paradigm

characteristics”.

4.3.1. Quantitative method

46

Credit Risk Management at Standard Chartered

As defined by Paranomality website, “Quantitative method is a

research method that relies less on interviews, observations, small numbers of

questionnaires, focus groups, subjective reports and case studies but is much

more focused on the collection and analysis of numerical data and statistics.”

Additionally, the definition of Creswell (1994) stated

that the quantitative research is explaining phenomena by

collecting numerical data that are analyzed using

mathematically based methods.

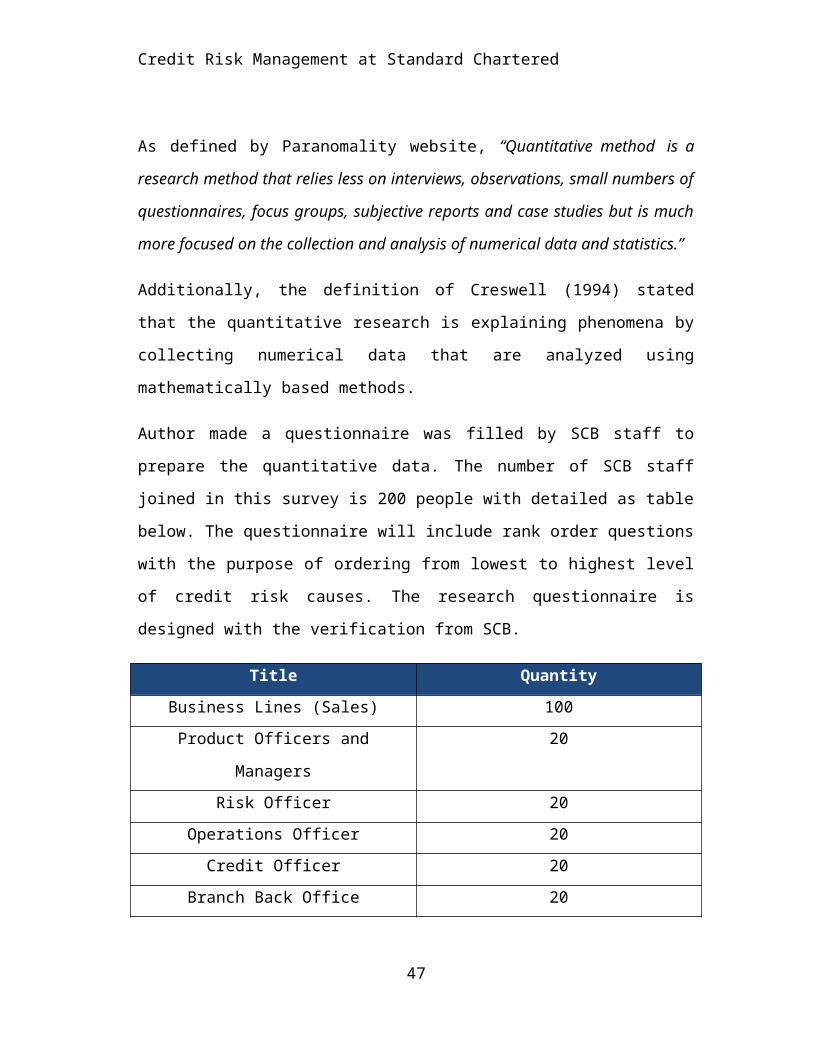

Author made a questionnaire was filled by SCB staff to

prepare the quantitative data. The number of SCB staff

joined in this survey is 200 people with detailed as table

below. The questionnaire will include rank order questions

with the purpose of ordering from lowest to highest level

of credit risk causes. The research questionnaire is

designed with the verification from SCB.

Title QuantityBusiness Lines (Sales) 100Product Officers and

Managers

20

Risk Officer 20Operations Officer 20Credit Officer 20

Branch Back Office 20

47

Credit Risk Management at Standard Chartered

Figure 12: List of SCB staff joined in questionnaire

The target of questionnaire is to statistic the causes of

risk in the opinion of SCB staff. The research response

result input to SPSS and Excel for analyzing data.

4.3.2. Qualitative method

The definition of qualitative method is given by Wikipedia

is “Qualitative researchers aim to gather an in-depth understanding of

human behavior and the reasons that govern such behavior”.

On the Business Dictionary, they define the qualitative

method that the qualitative method includes the interview

conducted to gather the needs, reaction and point of view

to a problem.

The qualitative method was processed under face to face

interviews and voice conferences. The steps of qualitative

will be discussed in the next part.

4.4. Procedures

48

Credit Risk Management at Standard Chartered

After showing out the literature review, the financial

analysis for credit risk management in Vietnam, especially

at Standard Chartered Vietnam will be processed. The

analysis will be focus on two categories below.

Short-term liquidity risk, this ratios help to know the

current operations of enterprise and the ability of pay

back liabilities in short term.

Long-term risk shows the possibility of paying back

liabilities in the long term.

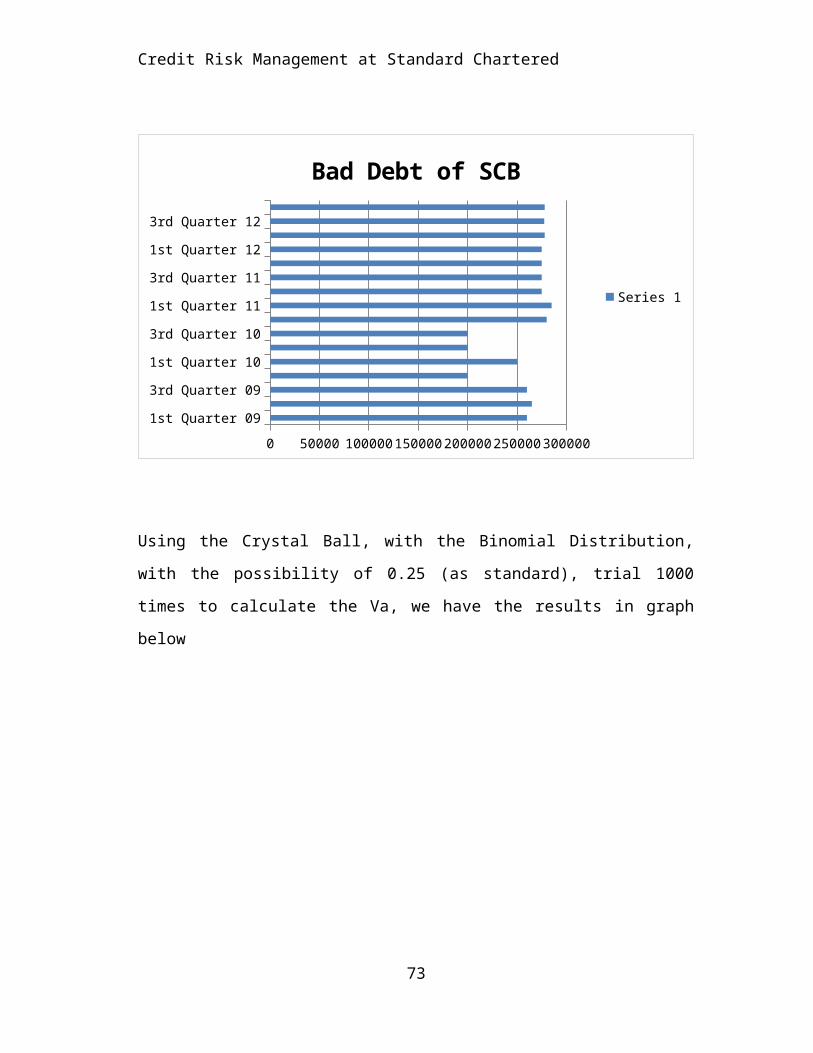

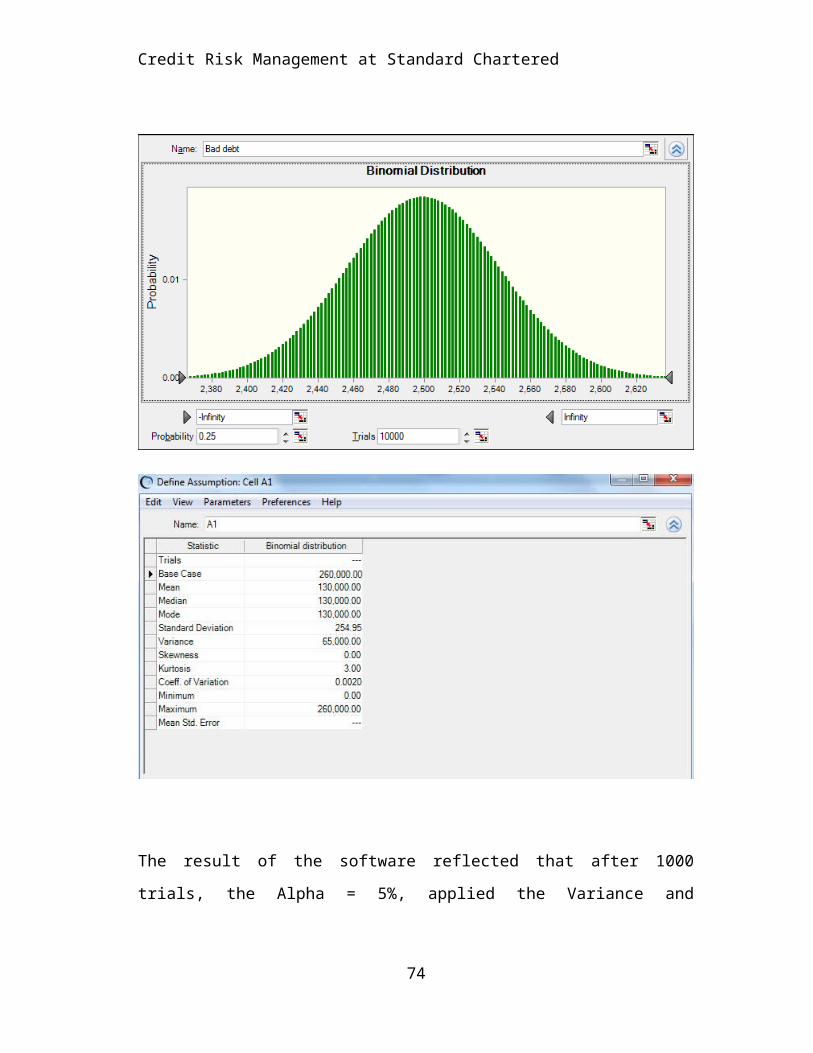

Along with analysis financial ratios, author used crystal

ball for calculating the expected loss of SCB based on the

data of bad debt at SCB through the period from 2009 –

2012. The analysis will operated under Variance and

covariance method.

The survey was conducted under the permission of SCB

Vietnam. At the beginning, author sent introduction email

by internal system to whole SCB Vietnam and get the

response for accepting to join the survey or not. The

response from email was tracked. After having enough

people as listed in previous page, author sent electric

questionnaires to all interviewees via email. Kindly be

noted at this point, the questionnaire was made by Google,

and the data return was recorded under XLSX file. Then,

the data was imported directly to SPSS for analyzing.49

Credit Risk Management at Standard Chartered

The interviewer was joined by 250 SCB Staff. The reason

for needing much more 50 participants than official

portfolio is that some staff could give up during the

interview session; the connection between Google server

and SCB net could be broken, then, the records of

interviewees were not validated on the system, etc. Many

reasons could be appeared during session, then, we need to

have supplementary questionnaire to avoid risk of

insufficient data. The result of the survey is that author

collected 210 result samples from colleagues. However, as

mentioned before, author chose only random 200 samples for

statistic in the master dissertation.

Besides, the direct interview with SCB managers will be

held. Why does the author need to question them directly

instead of emailing for them as other staff? We can answer

this question in simple way. They are all managers of SCB.

They are really busy for dealing with bank operations. On

the other hands, they have a lot of emails per day and if

author sent email to them, they can miss this email

because it is marked not importance, secondly, they think

that they do not need to response this kind of email.

Thus, author did call to them and arrange the small voice

conference with 10 managers in the south. Each

conversation has the duration of 5 minutes. For the rest

managers, the author tried to appoint with them for having50

Credit Risk Management at Standard Chartered

lunch together, in this appointment, the questionnaire was

implemented. Fortunately, the voice conferences and

appointments with managers were successfully, author got

all their information, comments about this problem at SCB.

Their points of view are really precious for not only

statistic of the survey, but also for the current status

of credit risk at SCB.

4.5. Limitation

4.5.1. Difficulty in the ratios list

There is a lot of limitation in selecting the financial

ratios. It is really hard for analyzing all ratios. Author

must select the most important and outstanding factors to

list in the dissertation.

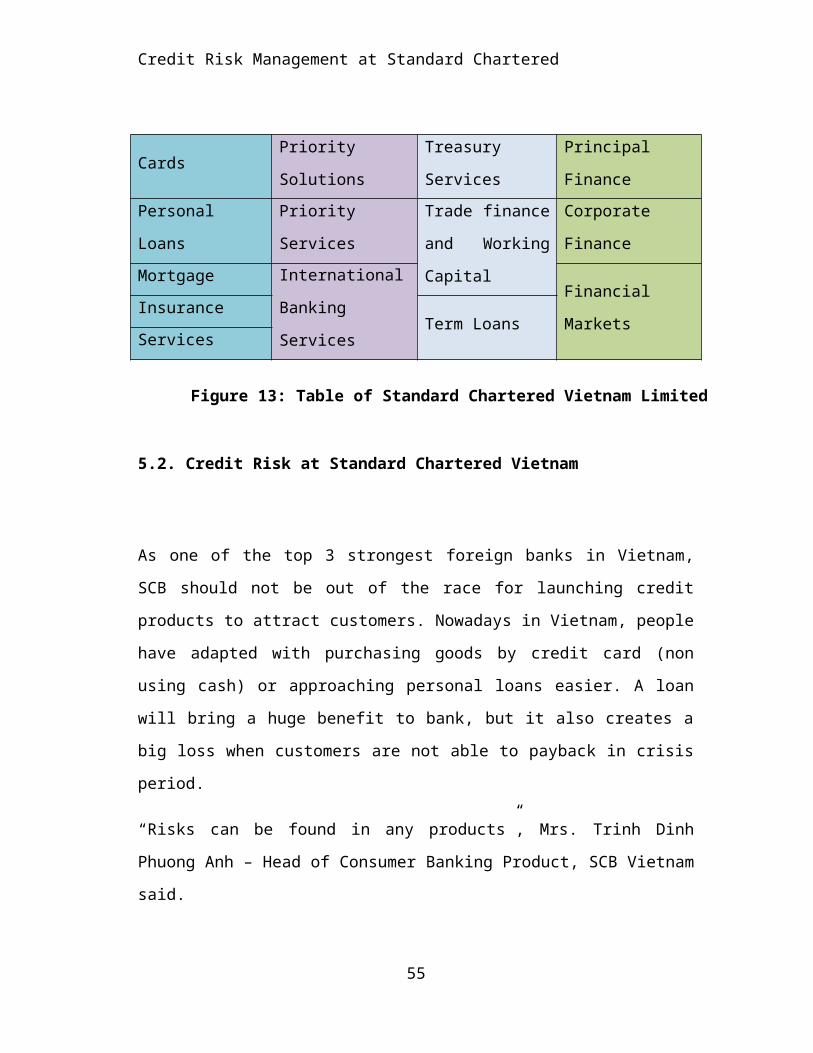

4.5.2. Difficulty in private data approach

Almost documents in banks are confidential. Although

author is currently an officer of SCB, the data copy must

51

Credit Risk Management at Standard Chartered

be authorized by compliance department. However, author

can see a part of needed information because the remaining

documents are ranked as highly confidential. Thus, author

does not have the authorization to access.

4.5.3. Limitation of getting co-operation from SCB staff

SCB staff have high workload. Thus, author found hard to

getting the co-operation from filling in the survey. The

only method in this situation is to persuade as many as

staff for reaching the number of estimation, design an e-

survey and send link through internal email.

52

Credit Risk Management at Standard Chartered

Chapter 5: Credit Risk Management at Standard

Chartered Bank Vietnam (Ltd)

5.1. Introduction

Standard Chartered is a successful M&A between Standard

Bank and Chartered Bank in London (UK) in 1969. As the

information from Wikipedia, “It operates a network of over 1,700

branches and outlets (including subsidiaries, associates and joint ventures)

across more than 70 countries and employs around 87,000 people. It is a

universal bank with operations in consumer, corporate and institutional

banking, and treasury services. Despite its UK base, around 90% of its profits

53

Credit Risk Management at Standard Chartered

come from Africa, Asia and the Middle East.”. With the revenue of $

18258 billion and Operating Income of 19071 billion in

2012 (See FTSE 2012), Standard Chartered is one of the

biggest international banks over the world.

In Vietnam, Standard Chartered opened a representative in

1904 in Saigon, Vietnam (now Ho Chi Minh city). Then, It

came out of Vietnam due to the war and returned in 1993.

In 2009, Standard Chartered commenced operations in its

locally incorporated entity – Standard Chartered Vietnam

(Limited).

After long time operation in Vietnam, Standard Chartered

Vietnam has been a bank in top 3 of strongest foreign

banks in Vietnam along with ANZ and HSBC. It provides

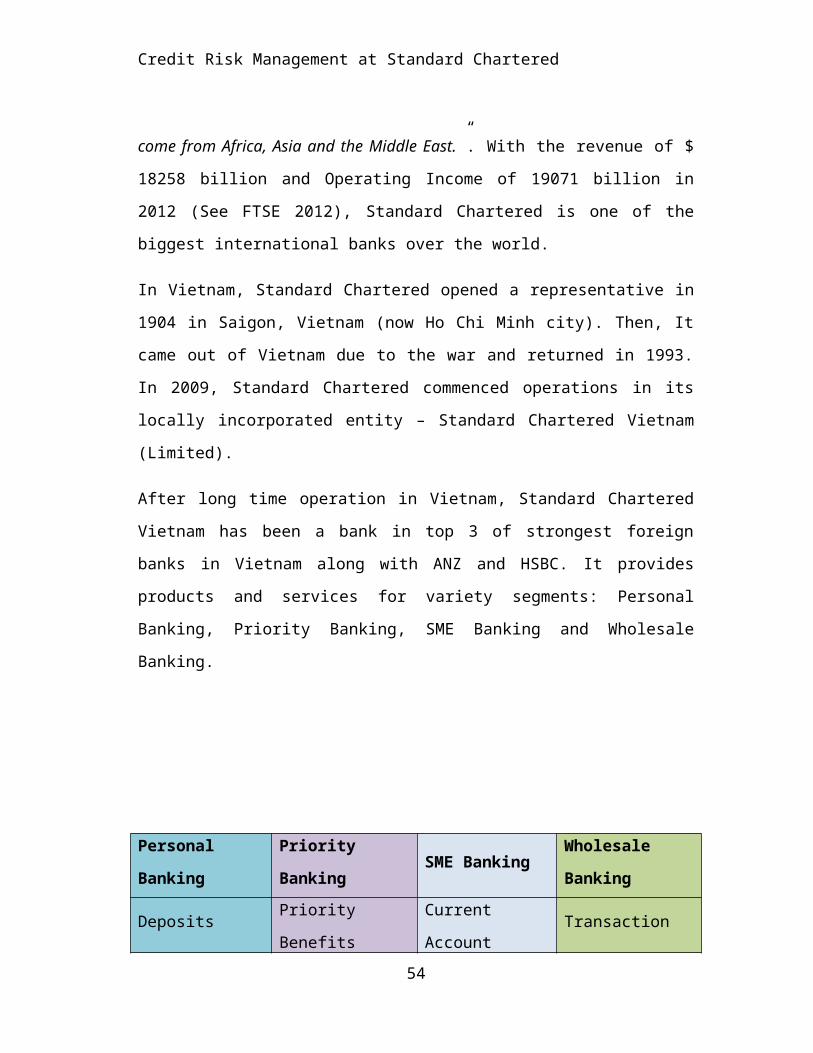

products and services for variety segments: Personal

Banking, Priority Banking, SME Banking and Wholesale

Banking.

Personal

Banking

Priority

BankingSME Banking

Wholesale

Banking

Deposits Priority

Benefits

Current

AccountTransaction

54

Credit Risk Management at Standard Chartered

CardsPriority

Solutions

Treasury

Services

Principal

FinancePersonal

Loans

Priority

Services

Trade finance

and Working

Capital

Corporate

FinanceMortgage International

Banking

Services

Financial

MarketsInsurance

Term LoansServices

5.2. Credit Risk at Standard Chartered Vietnam

As one of the top 3 strongest foreign banks in Vietnam,

SCB should not be out of the race for launching credit

products to attract customers. Nowadays in Vietnam, people

have adapted with purchasing goods by credit card (non

using cash) or approaching personal loans easier. A loan

will bring a huge benefit to bank, but it also creates a

big loss when customers are not able to payback in crisis

period.

“Risks can be found in any products”, Mrs. Trinh Dinh

Phuong Anh – Head of Consumer Banking Product, SCB Vietnam

said.

55

Figure 13: Table of Standard Chartered Vietnam LimitedProducts

Credit Risk Management at Standard Chartered

In Vietnam, Vietnamese have approached the credit cards

since 2008, so credit cards are just familiar with a part

of people in Vietnam. Many people do not have the

awareness the importance of paying back money after buying

goods. Like personal loans, when customers apply to a

credit card or loan, they do not need to have a clearly

financial plan for repayment. The application just

includes the job certification and salary statement. This

will create a big split for bad debt if banks do not have

a strong credit risk management.

More secured than credit card and personal loans, mortgage

loans require customers to deposit their asset for

guarantee. In case of bad debt, banks can settle the asset

for money collection. However, as talked in the previous

chapter, there is still some mismatch of the legal

documents in Vietnam. It will take long times for asset

settlement. On the other hand, the property fluctuates

daily. At the moment of credit decision, the asset (or

property) is in good price and can be guarantee for loans.

However, after few months, the price of asset can be

declined. In this case banks will be lost, the

consequences are really incredible.

SCB is a foreign bank, thus, the process of credit risk

management in each country will be synced with SCB group.

56

Credit Risk Management at Standard Chartered

Indeed, with the credit risk management system, SCB

Vietnam have stable in credit development. Although the

profit can be low compared with other banks, but SCB has

the lowest bad debt rate in Vietnam. “Slowly but surely”,

Louis Taylor – CEO SCB Vietnam said. The credit risk

management of SCB will be explained deeply in the next

part.

5.3. Credit Risk Management at Standard Chartered Bank

Vietnam (Ltd).

Credit Risk Management system is an important tool for all

banks. In Vietnam, as a foreign bank, SCB must have strict

regulation on credit management. If they do not protect

their credit risk management, they must to face with a lot

of troubles when credit risks happen. The worst result is

that they must re-sell bank to other financial institution

like SCB Canada (Wikipedia) and go out of Vietnam. Thus,

Credit Risk Management is one of the actions that is put

in priority.

5.3.1. Lending Procedures

57

Credit Risk Management at Standard Chartered

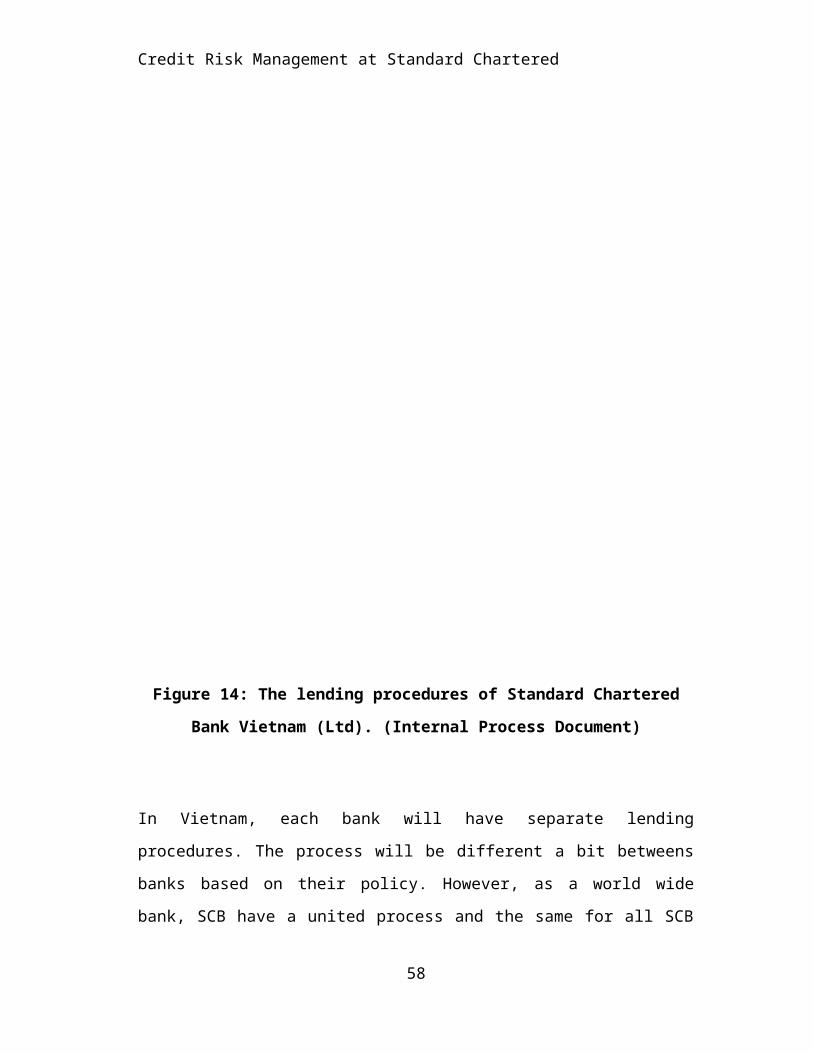

Figure 14: The lending procedures of Standard Chartered

Bank Vietnam (Ltd). (Internal Process Document)

In Vietnam, each bank will have separate lending

procedures. The process will be different a bit betweens

banks based on their policy. However, as a world wide

bank, SCB have a united process and the same for all SCB

58

Credit Risk Management at Standard Chartered

in over the world. Therefore the procedures of SCB will

have some changes, compared with other local banks.

As can be seen from the figure above, first step is

“document collection”. This step will be processed by

sales officers (PFC-*, DS*, R*). After agreeing to apply

for loan, customers will be requested for document

preparation. The needed documents for two kind of loans

are listed on two table below.

59

Credit Risk Management at Standard Chartered

Figure 15: Documents for Loan Applicants (SCB Products

Internal Document)

Sales Officers will make a seal “Original Seen and

Verified” on all received documents from customers to

announce the responsibility of documents. Then, they will

transfer all documents to Sales Coordinators.

The next stage is basic assessment. After receiving

documents from Sales, Sales Coordinator will have a check

as if fulfilling documents, verify signature of customer.

Sales Coordinator will book loan on “Lending Tracking

System” to announce for credit. Then, they will scan all

documents to a system that is called eOPS and book CIC. In

Vietnam, the credit history of all customers will be

stored in CIC (a property of SBV). Sales Coordinator must

attach the result of CIC with the document before transfer

to other department before processing.

Credit Officers and Operations Officer will do the

remaining steps. Credit Officer will check again the

submitted documents by Sales Coordinator. If there is any

enquires, they will reject to Sales Coordinator and note

the rejection reason on comment of EOPS. From this, Sales

Coordinator will request Sales Officer to explain. After

having acceptable reason, Credit Officer will do the next60

Credit Risk Management at Standard Chartered

action.Credit Officer will call to customers for KYC,

verify against the document of customer. Credit officer

will also check the CIC result from Sales Coordinator. If

customer has not bad debt or bad lending history, credit

officer make a loan proposal, then submit to authorization

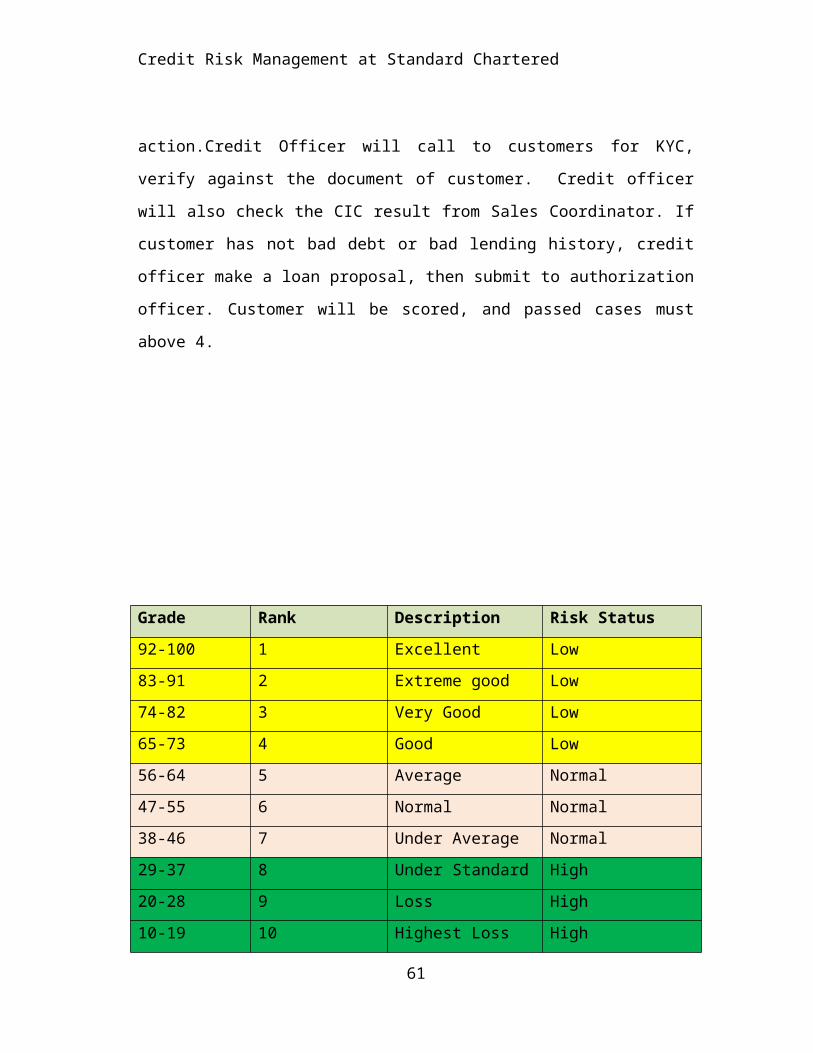

officer. Customer will be scored, and passed cases must

above 4.

Grade Rank Description Risk Status92-100 1 Excellent Low83-91 2 Extreme good Low74-82 3 Very Good Low65-73 4 Good Low56-64 5 Average Normal47-55 6 Normal Normal38-46 7 Under Average Normal29-37 8 Under Standard High20-28 9 Loss High10-19 10 Highest Loss High

61

Credit Risk Management at Standard Chartered

Figure 16: Credit Grading of SCB (Internal Document).

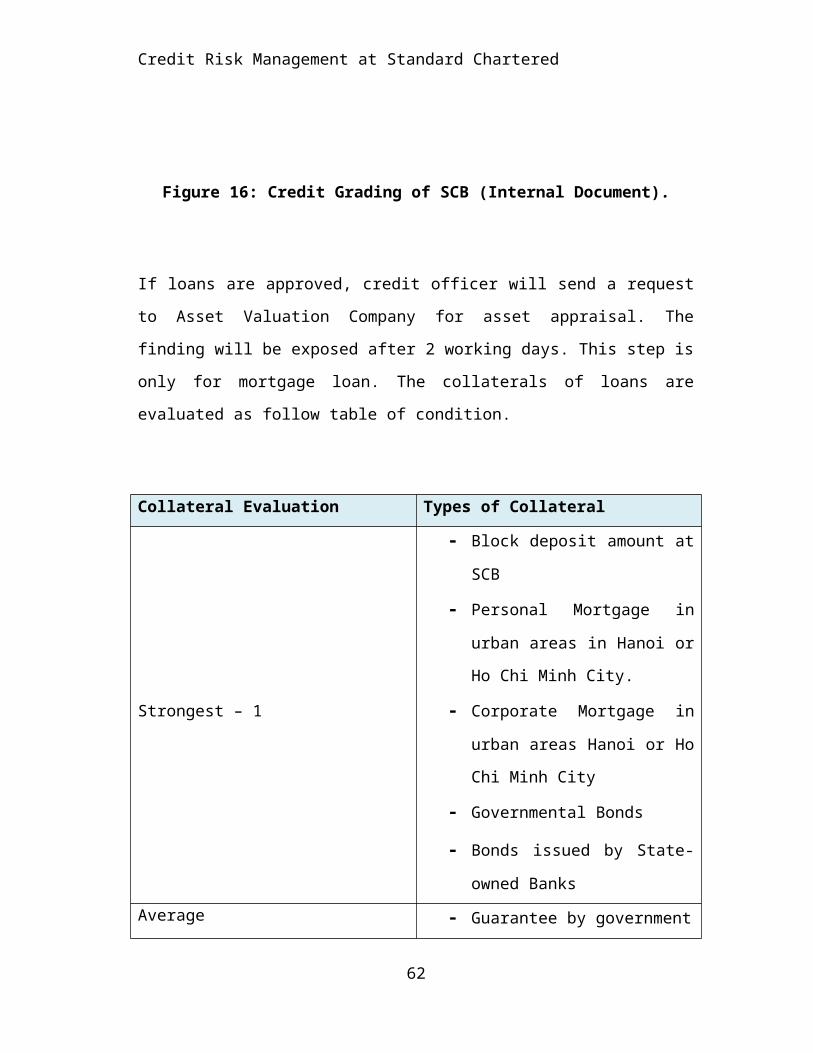

If loans are approved, credit officer will send a request

to Asset Valuation Company for asset appraisal. The

finding will be exposed after 2 working days. This step is

only for mortgage loan. The collaterals of loans are

evaluated as follow table of condition.

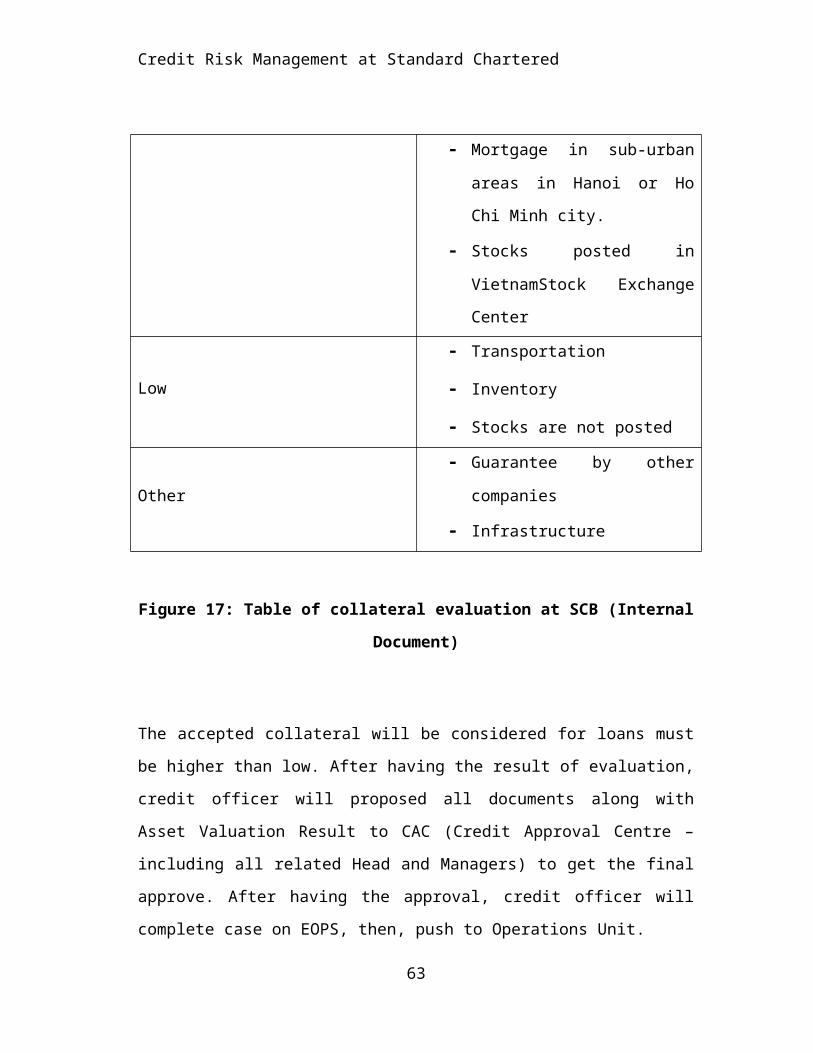

Collateral Evaluation Types of Collateral

Strongest – 1

- Block deposit amount at

SCB

- Personal Mortgage in

urban areas in Hanoi or

Ho Chi Minh City.

- Corporate Mortgage in

urban areas Hanoi or Ho

Chi Minh City

- Governmental Bonds

- Bonds issued by State-

owned BanksAverage - Guarantee by government

62

Credit Risk Management at Standard Chartered

- Mortgage in sub-urban

areas in Hanoi or Ho

Chi Minh city.

- Stocks posted in

VietnamStock Exchange

Center

Low

- Transportation

- Inventory

- Stocks are not posted

Other

- Guarantee by other

companies

- Infrastructure

Figure 17: Table of collateral evaluation at SCB (Internal

Document)

The accepted collateral will be considered for loans must

be higher than low. After having the result of evaluation,

credit officer will proposed all documents along with

Asset Valuation Result to CAC (Credit Approval Centre –

including all related Head and Managers) to get the final

approve. After having the approval, credit officer will

complete case on EOPS, then, push to Operations Unit.

63

Credit Risk Management at Standard Chartered

Operations Officers will include ATM& Card Operations

Officer, Lending Operations Officer, Account Services

Officer. Lending Operations will take the responsibility

for disbursing money to customer account when Account

Services team open successfully. The request will also

send to ATM& Cards team for issuing cards for customer if

demand.

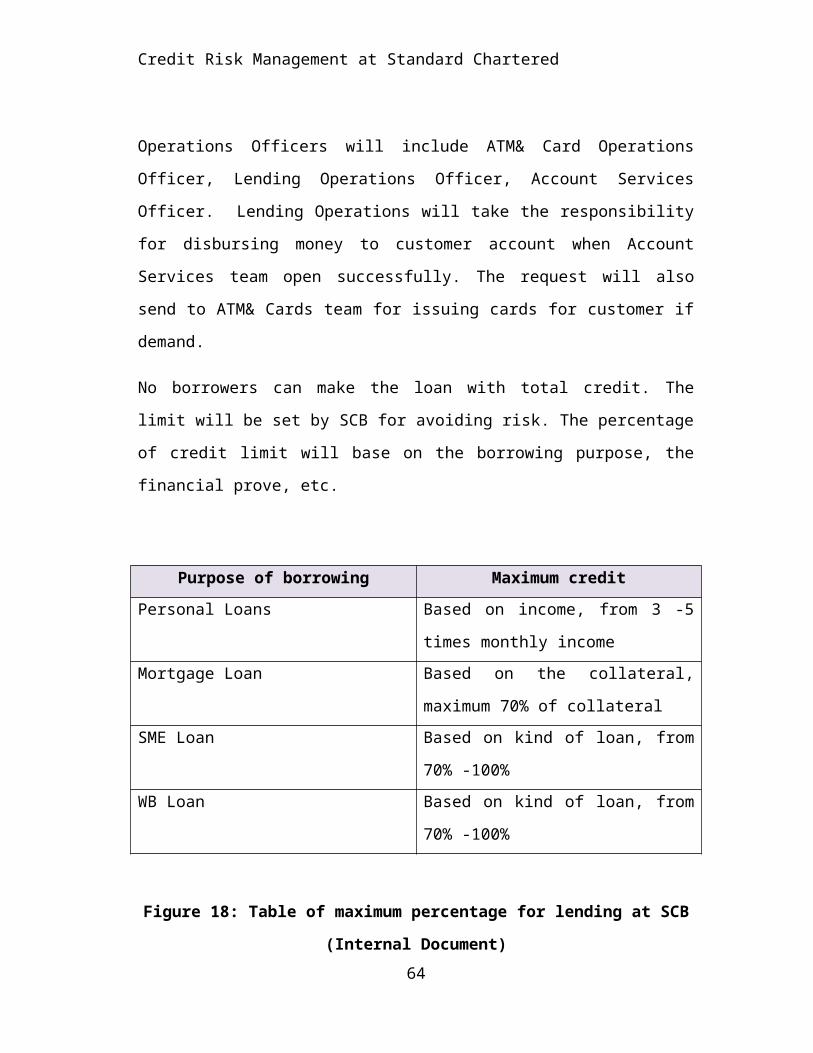

No borrowers can make the loan with total credit. The

limit will be set by SCB for avoiding risk. The percentage

of credit limit will base on the borrowing purpose, the

financial prove, etc.

Purpose of borrowing Maximum creditPersonal Loans Based on income, from 3 -5

times monthly incomeMortgage Loan Based on the collateral,

maximum 70% of collateralSME Loan Based on kind of loan, from

70% -100% WB Loan Based on kind of loan, from

70% -100%

Figure 18: Table of maximum percentage for lending at SCB

(Internal Document)64

Credit Risk Management at Standard Chartered

As the requirement from Basel (2000), Credit organization

must have clearly credit granting. That’s means the

lending procedure must be divided carefully, separate the

business unit and credit department where credit

processing and deciding. On the other hand, the limit for

borrower must be set based on bank’s policy. Compared with

those rules of Basel, SCB has worked well in this field.

5.3.2. Credit Organizational Structure

SCB has indentified the roles and responsibility of BOM

and all staff in credit operation and management to ensure

that:

- All important credit strategy and grading should be

considered carefully by individual and team with wide

knowledge and experience in credit risk management.

- All departments related to credit activities will be

separated to guarantee credit quality. For example,

credit analyzing department, business line, credit65

Credit Risk Management at Standard Chartered

management are three departments which work

individually for minimizing the unclear in lending

process.

Here are all units at SCB involving the credit risk

management

- Board of Management (BOM)

- Board of Executive Directory (BOED)

- Credit Risk Management Union (CRMU)

- Credit Centre (CC)

- Board of Branch Managers (BOBM)

- Collection Department (CD)

- Group Audit (GA)

Board of Management (BOM)

BOM is responsible for final accurate of credit activities

in banks including strategy propose, target and action

plan of BOM. The credit responsibilities are:

- Approve and re-evaluate frequently credit strategy as

a party of strategy and business target of bank.

- Approve credit policy with safety in lending

guideline.66

Credit Risk Management at Standard Chartered

- Approve organization structure of credit sector in

bank including delegation

- Approve types and products of lending.

- Ensure recruiting a qualified management team enough

for credit management.

- Forecast the scenario of credit risk now or in the

future

- Read carefully the annual financial report of bank,

BOED, internal audit, etc to monitor the quality of

credit process compliance.

-

Board of Executive Directors (BOED)

BOED is responsible for complying with the credit strategy

published by BOM

- Guarantee the credit activities followed indentified

strategy.

- Observe the capabilities of loan repayment and

suggest the level of reserve.

- Ensure the Human Resources and Training Development

if any.

67

Credit Risk Management at Standard Chartered

- Report the credit risk management to BOM at least

twice a year.

Credit Risk Management Union (CRMU)

- CRMU is including senior managers in credit sector.

CRMU is under the responsibility of following credit

risk codes of bank

- Build and propose credit policies and procedures,

then, submit to BOED.

- Set the credit limit for lending portfoliobased on

credit risk management strategy.

- Evaluate the quality of lending portfolio and

portfolio materials.

- Maintain and evaluate the credit scorecard

Credit Centre (CC)

CC is the unit where approve all loan applications.

68

Credit Risk Management at Standard Chartered

- Approve all loans under 120 billions VietnamDong, if

excess the above amount needed to have approval from

BOED.

- Report credit activity directly to CRMU and support

for Audit Company, Group Audit.

- Comply strictly to lending policies and procedures.

Board of Branch Managers (BOBM)

BOBM must warrantee the operations of branch. BOBM do not

have the right to approve loan application, but the

related credit responsibilities are

- Manage all process and policy compliance at branches.

- Promote and training the lending products, policies,

and system to staff.

- Report the credit operations to CRMU

- Guarantee the competence of staff at branches in

credit area.

Collection Department (CD)

69

Credit Risk Management at Standard Chartered

An effective department of collection in bank is highly

important. When experience staff in credit collection work

in a unit, they can suggest the methods that are suitable

for situation, use deeply knowledge of law, negotiate and

other skills that gained previous cases. Moreover, the

alerts of collection officers are necessary for minimizing

bad debt. They can base on some criteria like overdue,

loans in difficulty trading areas, etc. to notify to

credit officer.

When they foresee the signals of bad debt, collection must

follow the collection solutions that are built by CRMU.

- Negotiate with customer for restructuring loans by

changing terms, interests or collateral.

- Request to repay back loans.

- Settle the collateral or sue for non – performing

loan at the court.

- Transfer loans to shares.

Group Audit (GA)

Target

70

Credit Risk Management at Standard Chartered

GA will directly report to BOM. They have an important

role in identify whether all units comply strictly with

the policies whether or not. GA will an individual unit,

they just need to report to BOM about the activities of

credit. BOM can not control the operations of GA. GA is

under the control of Regional Audit including Singapore,

Thailand, Malaysia, Vietnam, Indonesia, Philippines.

Responsibility

GA must follow

- Evaluate the suitability, full and effective of

internal process and policy.

- Checking the transparent of financial ratios.

- Consider any official decisions from CEO to bank’s

operations.

- Discover fraud in credit sector.

- Checking the authority on the system for each unit.

- Unusual audit for minimizing frauds.

GA will have unlimited right to assess to the system,

bank’s operations and must receive the support in

reporting of related units.

The organization of SCB was showed above. The organization

of SCB credit management was designed in united concept

71

Credit Risk Management at Standard Chartered

over the world. Therefore, the verification of SCB

(internal audit) always operates individually. CEO only