Embed Size (px)

Citation preview

ISO-9000 Certification and OwnershipStructure: Effects upon Firm Performance

Esteban Lafuente, Alberto Bayo-Moriones1 andMiguel Garcıa-Cestona

Departament d’Economia de l’Empresa, Universitat Autonoma de Barcelona, Edifici B. Campus UAB, 08193Bellaterra (Barcelona), Spain, and 1Departamento de Gestion de Empresas, Universidad Publica de Navarra,

Campus de Arrosadia, 31006 Pamplona, SpainCorresponding author email: [email protected]

ISO certification has become a pervasive mechanism adopted by firms to improve their

operational performance. In this paper, we examine the operational and organizational

factors that increase the likelihood of adopting ISO certification and the impact thatISO certification and ownership structure have upon firm performance. Using a sample

of 163 Spanish manufacturing firms for the period 1996–2000 we perform a rare events

logit model and a regression analysis. Our findings show that firms producingintermediate goods that have implemented just-in-time practices are more likely to

adopt ISO certification. Furthermore, we report a strong influence of the ownership

structure upon ISO adoption policy, especially when a multinational firm is the largest

shareholder. Empirical evidence supports that ISO certification and ownership structurepositively impact firm performance. However, our results indicate that the positive

impact of ISO certification on performance diminishes in firms where ownership is

highly concentrated.

Introduction

ISO certification has emerged as a managerialtool that aims to achieve a better performance atboth the firm and the plant level throughcontinuous improvements of processes and tech-niques. The academic literature offers two ap-proaches to explain how quality managementpractices could have an effect on businessperformance. First, the operational view high-lights that firms adopting quality managementschemes (such as ISO-9000) improve their per-formance as a result of the prevention ofproduction process failures (reducing internalprocess variability), the empowerment of workersto identify potential sources of quality gains, and

a commitment to customer satisfaction (Garvin,1984). Second, the strategic approach to adop-tion emphasizes that the costs linked to qualityimprovements must be seen as investments, andthe benefits from those investments are reflectedin firm performance measures (Rust, Zahorik andKeiningham, 1995). As a result, it can beexpected that quality management enhancesproduct quality (design, conformance and dur-ability, amongst others), leading to the achieve-ment of important financial and organizationalgains derived from technological innovations andquality improvements (Dean and Bowen, 1994).Despite these arguments, empirical research

examining the consequences of the adoption ofISO certification is not conclusive. On the onehand, some papers show a strong effect of ISOcertification on business performance (Corbett,Montes-Sancho and Kirsch, 2005; Gonzalez-Benito and Gonzalez-Benito, 2005; Terziovski,Power and Sohal, 2003). On the other hand, the

This research was funded by grants from the SpanishMinistry of Education and Science (SEJ2004-07530-CO4-02/ECON, SEJ2007-67895-CO4-02/ECON andSEJ2007-66511/ECON).

British Journal of Management, Vol. 21, 649–665 (2009)DOI: 10.1111/j.1467-8551.2009.00660.x

r 2009 British Academy of Management. Published by Blackwell Publishing Ltd, 9600 Garsington Road, OxfordOX4 2DQ, UK and 350 Main Street, Malden, MA, 02148, USA.

positive relationship between ISO certificationand business performance appears as weak andnot always significant in empirical research(Tsekouras, Dimara and Skuras, 2002). More-over, operational and strategic-oriented literatureoffers two main explanations for the feebleimpact of ISO certification on firm performance.First, the lack of commitment from firms’personnel and management team regarding ISOimplementation, along with the fact that ISOresults are not observable in the short term, maylead to system failure (Samson and Terziovski,1999). Second, quality management practices,such as ISO certification, might be context-relianton other factors such as market environment andthe intensity of competition (Karmarkar andPitbladdo, 1997; Powell, 1995).Alternative to this approach, other authors

adopt an ex ante view of the problem, aiming tounderstand the underlying reasons for adoptingISO certification and quality management prac-tices (Adams, 1999; Anderson, Daly and John-son, 1999; Tsekouras, Dimara and Skuras, 2002).These authors study those characteristics thatmake firms more likely to adopt ISO certification.Nevertheless, they only consider operationalvariables when examining the adoption of ISOcertification and for them the implementation ofthe scheme is assumed to depend on the firm’sobjectives and the specific production and serviceprocesses (Terziovski, Power and Sohal, 2003;Tsekouras, Dimara and Skuras, 2002). In addi-tion, the adoption of quality management prac-tices may help differentiate more innovative firmsfrom less innovative ones on the basis ofperformance indicators (Baldwin and Johnson,1996; Young, Charns and Shortell, 2001). Con-sequently, ISO certification can be identified as asource of competitive advantage that couldexplain its wide implementation, especially inmanufacturing firms. Despite the strategic rele-vance of ISO certification, the body of literaturethat deals with this issue is still scarce, and it hasbeen mainly focused on internal and productionvariables, where relevant organizational factorsthat may influence the decision to adopt ISOcertification are not taken into account.Out of these arguments comes our research

objective guiding this paper which is to examineboth the production-related and organizationalfactors that make firms more likely to adopt ISOcertification. In consonance with the importance

given to organizational factors in our framework,we assume that firm managers can be encouragedto adopt ISO certification by different groupsrelated to the firm, such as large shareholders orinternational corporations with an interest in thecompany.The main contribution of this paper is twofold.

First, our findings indicate that organizationalvariables such as ownership structure becomeimportant when examining the adoption of ISOcertification. Second, from a longitudinal analysisthat relates ISO certification, ownership structureand their impact on firm performance, we find astatistically significant positive relationship be-tween ISO certification and firm performance. Inaddition, ownership structure also becomes animportant determinant of firm performance.More specifically, and according to agencytheory, those firms with either higher levels ofownership concentration or a large corporateshareholder benefit from better monitoring. Inturn, this leads to better financial results,compared to those firms with a more dispersedownership structure.The paper is organized as follows. The next

section presents the theoretical framework re-lated to the adoption of ISO certification, theimpact of ISO certification upon firm perfor-mance, and the role of ownership structure onadoption and performance. Data and methodol-ogy are described next, while the discussion of theresults is offered in the penultimate section. Finalconclusions are displayed in the last section.

Theoretical framework

Who adopts the ISO-9000 certification?

The drivers behind the adoption of ISO comefrom the supply and demand side. A source ofpotential benefits of ISO adoption comes fromprocess improvement in terms of productivitygains, cost and waste reduction, the eliminationof procedural problems, better managementcontrol, quality enhancement and efficiency im-provement (Bhuiyan and Alam, 2005; Casadesusand Karapetrovic, 2005). Tzelepis et al. (2006)argue that the adoption of ISO reduces manage-rial inefficiency, rather than being a new produc-tion factor. Other possible mechanisms thatinfluence firm performance have to do withmarketing reasons. Acquisition and retention of

650 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

customers, entry into new markets and fewerdissatisfied customers have been cited as market-ing advantages of certification (Buttle, 1997). Infact, it has been suggested that management maybe tempted to use ISO as a commercial toolminimizing its impact at the internal level (Boiraland Roy, 2007).From these two approaches it can be noticed

that the underlying assumption for adopting ISOcertification relies on increased agents’ disciplinebecause firms operate in competitive markets. Tocapture this, our framework considers a set ofvariables related to product, production process,and technology implementation that are expectedto favour the adoption of ISO certification. Weproceed now to analyse the different factorsinvolved.First, we consider firm size. Size affects the

decision to adopt ISO certification or, in fact, anyother quality management scheme, because itaffects the registration costs, the initial costsassociated with the creation of the implicit workteam and the efficient resource allocation policies(Adams, 1999). However, the adoption of ISO-9000 is also conditioned by the training costsassociated with its implementation. Hence, it isimportant to control for the employment com-position and its intensity within a firm’s produc-tion structure. Firms with lower rates of full-time(permanent) employees may face higher trainingcosts due to a more frequent incorporation ofnew employees into the firm, which deters themanager from the adoption of ISO-9000. Inaddition, firms where labour costs are animportant component of total manufacturingcosts might be less likely to adopt this practice,since these firms exert a more active monitoringtask over labour force performance, whereasmonitoring could be more efficient in those firmswith a higher level of automation. From thisargument comes our first hypothesis.

H1a: Firms with higher rates of permanentemployees are more likely to adopt ISO-9000certification.

H1b: Less labour-intense firms are more likelyto adopt ISO-9000 certification.

Second, ISO certification can act as a regula-tory constraint when either the government orthe market fails in monitoring quality systems.Therefore, the presence in international markets

can act as a stimulus to adopt ISO-9000.Certification costs are considerable and differacross firms; therefore, these quality schemes canalso act as a barrier to entry in regulated markets.In this sense, to sustain a market share and togain access to international markets, firms mayneed to meet governmental quality requirements.Anderson, Daly and Johnson (1999) find that USfirms with higher exports to Europe are morelikely to adopt ISO certification. Thus, ISOcertification can be seen as a signal mechanismfor quality performance. This leads to our secondhypothesis.

H2: Firms participating in foreign markets aremore likely to adopt ISO-9000 certification.

The third factor is product type. Like Tse-kouras, Dimara and Skuras (2002), we expectthat firms producing intermediate goods are morelikely to adopt ISO certification. Firms that selltheir production to other enterprises will be morerigorously monitored by the buyer, and thisencourages the producer to control qualitystandards at plant level, in order to keep businesscontracts. In the case of consumer goods, theproducer may relax product quality controlmechanisms because observability costs are highfor a single consumer, which opens the door toconsumer organizations. Thus, our third hypoth-esis emerges.

H3: Firms producing intermediate goods aremore likely to adopt ISO-9000 certification.

Two important factors related to productionmanagement are the production process and just-in-time (JIT) practices. In particular, we assumethat firms with more standardized (repetitive)production processes are more likely to adoptISO certification. This is because control tasksover production are easier to establish whenproduction stages are observable and easier tomonitor. Also, those firms with a continuousproduction process benefit from a more reliableproduction control system, and so the adoptionof the ISO certification is expected to lead tolower failure rates and a lower cost of defects.The concept of JIT is related to the production ofa required volume of items at a specific point intime (Takahashi, Morikawa and Nakamura,2004). Its main objective is to improve thequality, flexibility and levels of service fromsuppliers by developing a buyer–supplier long-

ISO-9000 Certification and Ownership Structure 651

r 2009 British Academy of Management.

term relation based on trust (White, Pearson andWilson, 1999). As such, JIT may be seen as astrategic tool, since its effective implementationmay achieve important improvements in produc-tion processes. Thus, it is assumed that JIT is animportant dimension of quality management thatfavours ISO adoption policies (Withers, Ebra-himpour and Hikmet, 1997). This leads to ourfourth hypothesis.

H4a: Firms with a more standardized produc-tion process are more likely to adopt ISO-9000certification.

H4b: Firms that have incorporated JIT prac-tices are more likely to adopt ISO-9000certification.

Finally, we introduce leverage and industrysector as control variables. Since ISO certificationcan be seen as a long-term investment that mayhelp improve a firm’s performance, the decisionto adopt ISO certification is conditioned by thecapital structure of the firm. A rise in liabilitiesincreases the firm’s risk of capital, affecting thevalue of the firm and those decisions concerningnew investment projects. Thus, we expect that afirm’s leverage negatively affects the decision toadopt ISO certification. We also consider thesector to control for potential industry differencesin the implementation of ISO-9000. In this case,our industry categorization follows the OECDclassification of technological implementation.

ISO certification and firm performance: anunsettled issue

We have mentioned earlier that ISO certificationmight be seen as a strategic tool that couldfacilitate the creation of a competitive advantage,and that managers could perceive this investmentas a cost-control tool. Hence, ISO certification isadopted to enhance firm performance, and wewill consider the following financial measures ofperformance: the ratio of operational revenue tototal assets (ROA), the ratio of net profit toequity (ROE) and labour productivity (ratio ofnet sales relative to number of employees). Weare aware that financial performance is just onedimension of the multidimensional construct ofbusiness performance. For instance, Calisir,Bayraktar and Beskesh (2001) and Beattie andSohal (1999) remark that there are also non-

financial goals derived from the adoption of ISO,such as improvements in production process andthe quality perception of the product. Unfortu-nately, we lack information about these issues inour data.In general, we would expect a significant increase

in firm performance after the introduction ofISO-9000 certification (see Figure 1). Nevertheless,empirical evidence relating ISO certification andbusiness performance provides inconclusive results.On the one hand, we find some evidence support-ing the positive relation between ISO certificationand firm performance (market value as well asaccounting performance measures) in Corbett,Montes-Sancho and Kirsch (2005), Hendricksand Singhal (1996) and Terziovski, Power andSohal (2003). For Spain, Casadesus, Jimenez andHeras (2001) find that Spanish firms significantlyimproved their operational and financial perfor-mance after the adoption of ISO certification, andNicolau and Sellers (2002) also report a positivereaction of the Spanish stock markets to theadoption of ISO certification. On the other hand,Tsekouras, Dimara and Skuras (2002) report norelation between the adoption of ISO certificationand firm performance, whereas Easton and Jarrell(1998) also find that the adoption of qualitysystems at the production level does not increasefirm performance.After this, we consider that the link between

ISO certification and performance is double-sided: whereas poor performers are more likelyto adopt this practice aiming to foster futureperformance, firms that have implemented it aremore likely to exhibit higher performance com-pared to their non-adopter counterparts. We willtherefore test the following.

Cha

nges

in F

irm

Perf

orm

ance

Time

ISO Firms

Non - ISO Firms

Impulse Effect

t-1

PerformanceDifference

t+nt t+1

Source: Self-devisedSource: Self-devised.

Figure 1. Timing: adoption of ISO-9000 certification and firm

performance

652 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

H5a: Poor performance increases the prob-ability of adopting ISO-9000 certification.

H5b: The adoption of ISO-9000 certificationpositively impacts firm performance.

Ownership structure and firm performance

To a large extent, the adoption of ISO certifica-tion entails great commitment from employeesand managers. Concerning firm managers,Grossman and Hart (1986), Hart and Moore(1990) and Shleifer (1998), among others, remarkthat private firms benefit from market monitoringand control mechanisms. Here agents have boththe decision-making power and the incentives tobehave efficiently and to avoid managerial con-trol losses inside the firm as a result of negativereactions from the shareholders. Consequently,we think that it is important to consider theorganizational influence when examining firms’behaviour and their decision to adopt (or not)ISO certification. In this paper, we assume thatagents (managers) and principals (shareholders)behave according to firm performance, and thisalignment of objectives affects future managerialbehaviour and consequently the decisions relatedto the adoption of ISO certification. In particular,we assume that firms will adopt ISO certificationduring the period that immediately follows apoor performing one. Doing so, managers willcorrect poor firm performance through the imple-mentation of production quality systems, i.e.adopting ISO certification. Therefore, we proposethat there is a managerial effect upon the decisionto adopt ISO certification derived from thecontrol rights exerted by different stakeholderson the managerial decision-making process.We also consider the effects of ownership

concentration and the presence of multinationalenterprises within the ownership structure of thefirm. There is no empirical evidence that relatesthe presence of multinational firms as largeshareholders and the adoption of ISO certifica-tion. However, Merino (2003) and Gonzalez-Benito and Gonzalez-Benito (2005) examine thedependence of multinational firms and theirimpact upon the decision to adopt qualitymanagement practices. Only Merino (2003)reports a significant positive relationship. Thus,our sixth hypothesis emerges.

H6: Firms controlled by multinational firms aremore likely to adopt ISO-9000 certification.

Concerning the impact that ownership structurehas over firm performance, empirical evidencepresents mixed results. Whereas Demsetz and Lehn(1985), McConnell and Servaes (1990) and Demsetzand Villalonga (2001) find no significant effect ofownership concentration upon firm performance,Morck, Shleifer and Vishny (1988), Wruck (1989),Zwiebel (1995) and Earle, Kucsera and Telegdy(2005) report a positive relationship between own-ership concentration and firm performance. How-ever, it is important to remark that in the last twostudies the reported ownership–performance rela-tionship is inverse U-shaped. A possible explana-tion emerges when considering the fact thatconcentration creates costs within the firm thatoutweigh its benefits over some intervals of thedistribution. Also, Zwiebel (1995) remarks thatownership concentration works differently in ac-cordance with the largest shareholder characteris-tics. Thus, our last hypothesis will read like this.

H7a: Ownership concentration positively im-pacts firm performance.

H7b: The relationship between ownershipconcentration and performance is stronger forthose firms where the main shareholder is amultinational firm.

Data and method

Data

The information used to carry out this researchcomes from two sources. First, we used the dataavailable from the BBVA Foundation Survey onTechnological and Organizational Innovation inManufacturing. The information collected in thissurvey refers to Spanish firms and it wasconducted through a face-to-face interview witha manager of the plant in 1996. It is important toremark that after 1996 no further surveys havebeen conducted on this sample of firms. Themanufacturing establishments included in oursample employ at least 50 workers. This lowerbound has been used in other studies in the areaof organizational innovation (Osterman, 1994).In over 80% of cases the person interviewed

was the senior manager, the operations manageror the personnel manager of the plant. Responses

ISO-9000 Certification and Ownership Structure 653

r 2009 British Academy of Management.

were collected at the plant level, since it is therewhere management practices are implemented andwhere the knowledge of the issues considered in thestudy are best known. The response rate was29.72%. The survey instrument includes informa-tion about the incidence of new managementpractices in the areas of quality, human resources,technology and operations management. Further-more, one of the goals of the research was to assessthe effect that these practices have upon businessperformance. The questions concerning humanresource management refer to blue-collar workers,the core and largest group of employees inmanufacturing. The questionnaire was also subjectto a pre-test in order to ensure that the questionswere clearly worded and understood. The samplewas size- and sector-stratified to be representativeof the population of manufacturing establish-ments. Three strata for size and 12 for manufac-turing sector were considered. The sampleallocated to the strata was distributed proportion-ally, and in all the strata the plants finallyinterviewed were randomly selected.Second, information concerning the ownership

structure and accounting data was obtained fromthe Spanish database SABI (Sistema de Analisisde Balances Ibericos) provided by the BureauVan Dijk. The two databases were merged tohave access to accounting, organizational andmanagerial information. The number of firmsincluded in both information sources is 194.However, only companies for which a completedata set of the dependent and independentvariables can be constructed were finally in-cluded. Thus, data availability limited the sampleto 163 observations.

The adoption of ISO-9000 certification

ISO certification covers several fields related toproduction and service processes within the firm.Thus, to identify a firm that has incorporated ISOcertification we propose a dummy dependentvariable that takes the value of one if the firm hasadopted ISO-9000 certification in the year 1996,and zero otherwise. At this point, it is important toremark that from our data is not possible toidentify whether the firm has adopted a partial ISOcertification, which constitutes a limitation of thepaper. From the descriptive statistics it can be seenthat 97 companies reported the implementation ofISO certification in 1996 (see Table 1).

The rationale for the selection of the indepen-dent variables set follows. We define size as thenatural log of the total assets, which is introducedas a lagged term. Concerning the product type,we use a dummy variable taking the value of oneif the firm operates in a downstream market (i.e.the firm produces an intermediate good) and zerootherwise (it produces a consumer good). In oursample, 51.53% of the firms produce intermedi-ate goods. For firms with ISO-9000 certification,the relation increases to 59.79%.

Table 1. Descriptive statistics: adoption of ISO certification in

the year 1996

Variables ISO firms Non-ISO

firms

Total

sample

Adoption of ISO

certification

1 0 0.5951

(0.4924)

Size (ln assets)t–1 9.8193*** 9.1458 9.5466

(1.4681) (1.1964) (1.4005)

Rate of temporary

employees

0.1404 0.1661 0.1508

(0.1585) (0.1744) (0.1651)

Product type 0.5979*** 0.3939 0.5153

(0.4929) (0.4924) (0.5013)

Export capacity 0.4202*** 0.2980 0.3707

(0.2582) (0.2440) (0.2589)

JIT implementation 0.6083*** 0.2879 0.4785

(0.4907) (0.4562) (0.5011)

Small orders 0.5464 0.6667 0.5951

(0.5004) (0.4750) (0.4924)

Line production 0.2784 0.2273 0.2577

(0.4505) (0.4223) (0.4387)

Straight line production 0.1753 0.1061 0.1472

(0.3822) (0.3103) (0.3554)

Labour intensity 0.2393** 0.2848 0.2577

(0.1125) (0.1165) (0.1160)

Leverage ratiot–1 3.6964 2.93027 3.3861

(6.2795) (3.0716) (5.2244)

ROAt–1 0.0624 0.0768 0.0682

(0.0746) (0.1038) (0.0876)

ROEt–1 0.0002 0.2154 0.0874

(0.7024) (1.3216) (1.0022)

Labour productivityt� 1 4.9465 4.6927 4.8438

(1.2630) (0.8137) (1.1075)

Multinational firm influence 0.4742*** 0.2576 0.3865

(0.5019) (0.4407) (0.4885)

Stake held by the main

shareholder (C1)

0.7317*** 0.5939 0.6759

(0.3065) (0.2917) (0.3073)

Low technological sectors 0.2577*** 0.4697 0.3436

(0.4397) (0.5029) (0.4764)

Medium technological

sectors

0.2887 0.3182 0.3006

(0.4555) (0.4693) (0.4599)

High technological sectors 0.4536*** 0.2121 0.3558

(0.5004) (0.4119) (0.4802)

Number of observations 97 66 163

Values in parentheses represent standard deviation.*,**,*** indicates significance at the 0.10, 0.05 and 0.01 level,respectively.

654 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

The importance of the positive externalitiesthat ISO certification may create, as a result ofthe signals associated with quality improvements,is proxied by the relevance of market preferences.Like Anderson, Daly and Johnson (1999), we usethe firm’s export capacity, measured as the ratioof foreign sales (in either the EU or othermarkets) to total sales. From our descriptivestatistics (Table 1) we observe that firms thatadopted ISO-9000 certification have statisticallysignificant higher levels of sales located ininternational markets (42%) compared withthose that did not adopt it (nearly 30%).Data availability also allows us to identify three

different kinds of production processes: small ordersof several products, line production and straight-line production. Thus, we include in the analysisdummy variables identifying the kind of productionprocess carried out at the plant level. We are awarethat manufacturing firms can also implement amixture of these production processes; however, ourdata do not allow us to differentiate whether firmsmake use of one or several production processes.Concerning JIT practice, we include in the analysisa dummy variable that takes the value of one if thefirm has implemented JIT in their productionprocess, and zero otherwise. In the final sample47.85% of the firms have adopted JIT in theirproduction process, and 60.83% of firms thatadopted ISO had implemented JIT.We consider two variables related to labour

force: the rate of temporary employees and theratio of labour costs to total manufacturing costsin 1996, as a measure for labour intensity. Toavoid potential biases, depreciation was excludedfrom manufacturing costs. In our sample, firmsthat adopted ISO certification have statisticallysignificant lower levels of labour intensity(23.93%), compared to their non-ISO counter-parts (28.48%).Also, we introduce a variable that reflects the

firm’s capital structure (leverage), measured asthe ratio of debt to equity in the year prior to theadoption of ISO certification. Furthermore, weconsider three variables that represent firmperformance: ROA, calculated as the ratio ofoperating profit to total assets (book value);ROE; and a labour productivity ratio, calculatedas the natural log of sales relative to the numberof employees. These variables are introduced aslagged terms to check whether poor performancemay lead managers to implement ISO-9000 as a

tool for improving operational and financialperformance.Concerning the organizational variables, we

include a dummy variable taking the value of oneif there is a partial or total dependence of amultinational firm, and zero otherwise. Ownershipconcentration is measured as the stake held by thelargest shareholder (C1) in the year 1996. Inaddition, we introduce an interactive term thatconsiders the effect of the largest shareholder’smonitoring, when this major shareholder is amultinational firm. In our sample, firms are ratherlarge, and dominating multinational corporationsare present in 71 firms, of which 52 report theimplementation of ISO-9000 certification.To identify those characteristics that make

firms more likely to adopt ISO certification, onecan perform a logit regression model estimatedby maximum likelihood. However, as shown inTable 1, our sample is rather small since itcomprises 163 firms. Also, nearly 60% of firmsreport the adoption of ISO-9000 certification.Consequently, the application of traditional logitmodels with this sample may lead to biasedresults due to overestimation of the parameterestimates. Recently, King and Zeng (2001a,2001b) developed a method for computingestimates in logit models that correct for thepresence of rare events and small samples. Thisprocedure, labelled the rare events logit model, isbased on the standard logit model but uses anestimator that generates a lower root meansquare error for coefficients. This enables us tocarry out our analysis with the appropriatestatistical corrections.Given the characteristics shown by our sample

and by the dependent variable, in this study wemake use of the rare events logit model withclustered observations for estimating the para-meter estimates. To test our hypotheses we carryout the following model:

Adoption of ISO-9000i

¼ b0 þ b1Sizei;t�1 þ b2Temporary employeesi

þ b3Labour intensityi þ b4Exportiþ b5Type of producti þ b6Production processiþ b7JITiþb8Leveragei;t�1þb9Performancei;t�1

þ b10C1i þ b11Multinationali

þ b12C1i �Multinationali þ b13Industryi þ ei

ð1Þ

ISO-9000 Certification and Ownership Structure 655

r 2009 British Academy of Management.

Parameter estimates from the rare events logitmodel only indicate the direction of the effect ofeach explanatory variable on the response prob-ability. To obtain a better understanding of ourresults, we also calculate the first difference,which is the change in the probability as afunction of a specific change in a variable holdingthe rest of the variables constant at their means.First differences for the set of independentvariables are estimated as tx 5Pr(Y5 1|X5 1) –Pr(Y5 1|X5 0). As additional measures of good-ness of fit, we present the results for thelikelihood ratio test (inclusion of variables) andthe proportion of correctly classified observa-tions. This is done for the full sample, as well asfor those observations that have adopted ISO-9000 certification and those that have not.

ISO-9000 certification, ownership structure andfirm performance

Next, we present the framework to evaluate theimpact that ISO certification and ownershipstructure have on firm performance for the period1997–2000. As a measure of firm performance,our dependent variable, we use the variablesincluded in the ISO adoption model: ROA, ROEand the labour productivity ratio. As shown inTable 2, for the period 1997–2000, those firmsthat adopted ISO certification exhibit statisticallysignificant higher levels of ROE and labourproductivity. The analysis is conducted in twostages. First, we evaluate the impulse effect thatISO-9000 certification has on firm performance.In a second stage we consider the impact that ISOand ownership structure has upon firm perfor-mance. Descriptive statistics for the full set ofvariables included are presented in Table 2.In the first stage, we attempt to test whether the

shift to quality expressed by the adoption of ISOcertification has an impulse effect that explainsthe differences shown in our performance mea-sures represented by a change in the performanceslope. Since we expect that previous poorperformance increases the likelihood for adopt-ing ISO certification, we also expect that theadoption of ISO certification helps explain theobserved performance differences in the shortrun. As a result, we propose to explain changes inperformance using as key explanatory variablesthe presence of the impulse effect linked to theadoption of ISO certification and the changes in

the shares held by the main shareholder. Toattain this goal we estimate the following model:

DPerformancei;t ¼ d0 þ d1DSizei;t�1þ d2DISOi;t þ d3DOwnershipi;t

þ d4DTimei;t

þ d5DTimei;t � Sectori;t þ ei;t

ð2ÞEquation (2) uses as dependent variable the

observed changes in our three performancemeasures (DROA, DROE and DLabour produc-tivity). As independent variables we introduce thechanges in firm size, considered as a lagged termand measured as the natural logarithm of totalassets (DSize). We include a dummy variable thattakes the value of one for the first sub-periodunder analysis (1996–1997) if the change linkedto the adoption of ISO certification (DISO) tookplace, and zero for the rest of the sub-periodsconsidered. We expect that d240, to corroboratethat the presence of an impulse effect in the

Table 2. Descriptive statistics: impact of ISO certification and

ownership structure upon firm performance (period 1997–2000)

Variables ISO firms Non-ISO

firms

Total

sample

ROA 0.0829 0.0714 0.0782

(0.0785) (0.1013) (0.0886)

ROE 0.1291* 0.0627 0.0874

(0.5912) (0.9202) (0.7437)

Labour productivity 5.0747*** 4.7913 4.9599

(0.6940) (0.6038) (0.6730)

Variation in ROA 0.9570 0.0805 0.6021

(12.5548) (2.5622) (9.8254)

Variation in ROE 0.1359 0.3132 0.2077

(5.1601) (7.6450) (6.2808)

Variation in labour

productivity

0.0591 0.0573 0.0583

(0.2973) (0.1796) (0.2492)

Size (ln assets)t–1 10.0398*** 9.3570 9.7633

(1.4544) (1.2200) (1.4040)

Stake held by the main

shareholder (C1)

0.7484*** 0.6589 0.7122

(0.3090) (0.2947) (0.3062)

Multinational firm influence 0.4742*** 0.2576 0.3865

(0.4999) (0.4381) (0.4873)

Low technological sector 0.2577*** 0.4697 0.3436

(0.4380) (0.5000) (0.4753)

Medium technological sector 0.2887 0.3182 0.3006

(0.4537) (0.4667) (0.4589)

High technological sector 0.4536*** 0.2121 0.3558

(0.4985) (0.4096) (0.4791)

Number of observations 388 264 652

Values in parentheses represent standard deviation.*,**,*** indicates significance at the 0.10, 0.05 and 0.01 level,respectively.

656 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

adoption of ISO certification helps in explainingperformance differences. For ownership struc-ture, we introduce a variable that captures thechanges in ownership as the variation in thepercentage of shares held by the largest share-holder (DOwnership). Time dummy variablesaccount for the differential impact of time trendsand technical change on the dependent variablewith respect to the omitted year dummy (DTime).Finally, interaction terms between time and thesector dummy variables considering the OECDtechnological classification are also introduced.These variables account for the differentialimpact of competition on the different industrialsectors.In a second stage, we evaluate the longitudinal

impact that ISO certification has on performance.Different from the previous stage, at this point wetest whether those firms that adopted ISOcertification show higher performance levelscompared with their non-adopter counterparts.The model to be estimated is as follows.

Performancei;t ¼ g0 þ g1Sizei;t�1 þ g2Size2i;t�1

þ g3ISOi;t þ g4Ownershipi;t

þ g5ISOi;t �Ownershipi;t

þ g6Timei;t þ g7Sectori;t þ ei;t

ð3Þ

In this case, the dependent variable is the valueof the corresponding performance measure(ROA, ROE and labour productivity) for theith firm at time t. We include firm size asindependent variable, as a lagged term. Thisvariable accounts for the potential economies ofscale and scope experienced by firms. Addition-ally, we also include a quadratic term for size totest for the presence of a non-linear relationshipbetween size and performance. In equation (3) weintroduce a dummy variable related to ISOcertification that takes the value of one if ISOcertification was implemented and zero otherwise.Sector dummy variables considering the OECDtechnological classification are introduced.According to our hypotheses, and following

equation (3), we expect a coefficient g340. Also,we expect a g440, meaning that ownershipconcentration, understood as the largest stakeheld by the main shareholder or the dependenceof a multinational firm, positively impacts firmperformance.

Concerning the econometric approach, paneldata analysis is the most efficient tool when thesample is a mixture of time series and cross-sectional data. At this point, an importantqualification is also in order. Our variables ofinterest in equations (2) and (3) have dissimilarfeatures which affect the selection of the multi-variate analysis. Whereas in equation (2) thevariable linked to the adoption of ISO-9000 (d2)is time-varying, the dummy variable accountingfor the adoption of ISO-9000 in equation (3) isnot (g3). In the case of equation (2), and forgreater robustness in our estimation, we test theconsistency in the parameter estimates. Resultsfor the Hausman test do not reject random effectsfor the three dependent variables. Concerning theestimation of equation (3), we first tested for thepresence of group-wise heteroskedasticity andautocorrelation in all the models using the threemeasures of firm performance. The results emer-ging from the Breusch–Pagan test (1979) lead usto reject the null hypothesis of constant varianceacross firms. Moreover, the result of the Wool-dridge (2000) test for autocorrelation in paneldata models leads us to reject the null hypothesisof no first-order autocorrelation. Given thestructure of the covariance matrix and the errorterm, as well as the characteristics of the variableaccounting for the adoption of ISO-9000, weconsider that a random effects model estimatedthrough feasible generalized least squares is anappropriate estimation method for equation (3).

Empirical findings

Who adopts ISO certification?

Table 3 presents the results for the rare eventslogit models estimated for the adoption of ISO-9000 certification. Table 4 reports the predictedchange in the probability of adopting ISOcertification. In addition, we explore differencesin the probability of adopting ISO-9000 dueto variations in the selected continuous variables.Thus, we also estimated discrete changesat different points of the distribution of theindependent variables such as tx 5Pr(Y5 1|X5Q(q2)) – Pr(Y5 1|X5Q(q1)), where q1 and q2represent quantile points of the distribution ofthe independent variable under analysis.Our results show that the parameter estimates

for firm size are not statistically significant, and

ISO-9000 Certification and Ownership Structure 657

r 2009 British Academy of Management.

this could indicate that the costs linked to theadoption of ISO certification are affordable forany firm, irrespective of its size. Likewise, whenexamining the results for the characteristics of thelabour force, our findings show that the relation-ship between temporary employment and theadoption of ISO-9000 is not statistically signifi-

cant. Hence, we reject our Hypothesis 1a. To thecontrary, the included variable for labour in-tensity exerts a negative effect on the adoption ofISO certification. According to our framework,the estimated probability changes are negativeand statistically significant for highly labour-intense firms. From Table 4 we observe that theprobability of adopting ISO-9000 significantlydecreases by 4.84% as a consequence of anincrease in the firm’s labour intensity ratio fromits median value (24.83%) to the upper quartile(31.74%). Therefore, we confirm our Hypothesis1b. Sales in international markets have a positiveimpact on ISO certification adoption in all themodels we carried out. However, and unlikeAnderson, Daly and Johnson (1999), the lack ofsignificance in our results does not allow us tomake any conclusive comments, and this leads usto reject our second hypothesis (Hypothesis 2).As for the findings for product type, and

similar to Tsekouras, Dimara and Skuras (2002),our results strongly support that firms manufac-turing intermediate goods are more likely toadopt ISO-9000 certification. More specifically,our findings indicate that the adoption of ISO-9000 in firms producing intermediate goodsincreases by 27.12% relative to that for firmswhich produce a consumer good (Table 4). Thisresult is in accordance with our third hypothesis(Hypothesis 3), and it suggests that these types offirms operate in more competitive environmentsdue to the monitoring task developed by pur-chasers. Consequently, we might interpret thatthe adoption of ISO-9000 certification acts moreas a tool for attaining a competitive advantagethan for purposes of compliance with customers.Parameter estimates for the production process

variables are negative but not significant. Thus,we reject our Hypothesis 4a; however, thenegative sign in the coefficients suggest that ISOcertification is more linked to higher levels ofautomation. Our empirical findings supportthe view that those firms that have implementedthe JIT practice in their production process aremore likely to adopt ISO certification. This isconsistent with our Hypothesis 4b, indicatingthat the decision for adopting ISO in firms thathave implemented JIT rises 26.75% relative tothe implementation level in firms without JIT(Table 4).Our results for the performance variable

(ROA) are similar to those found in Tsekouras,

Table 3. Rare events logit results: adoption of ISO certification

Independent variables (1) (2) (3)

Size (ln assets)t–1 0.1376 0.1618 0.1503

(0.1166) (0.1174) (0.1191)

Rate of non-permanent

employees

–0.5634 –0.6656 –0.3873

(1.1156) (1.1758) (1.1520)

Product type 1.0660*** 1.1543*** 1.1746***

(0.3875) (0.4120) (0.4255)

Export capacity 0.8538 0.7368 0.4367

(0.7473) (0.7764) (0.7860)

Small orders –0.9023* � 0.8347 –0.7305

(0.5500) (0.5538) (0.5403)

Line production –0.3533 –0.2256 –0.0109

(0.6194) (0.6338) (0.6306)

JIT 1.2923*** 1.2561*** 1.1730***

(0.3685) (0.3738) (0.3805)

Labour intensity –3.6332** –3.3392** –3.0087*

(1.4573) (1.4639) (1.5698)

Leverage ratiot–1 –0.0263 –0.0197 –0.0240

(0.0283) (0.0309) (0.0313)

ROAt–1 –2.2383 –2.4515 –2.2762

(1.9978) (2.1374) (2.0538)

Multinational firm

influence

0.4530 –1.8346

(0.4182) (1.1991)

Stake held by the main

shareholder (C1)

0.9917 0.0866

(0.6667) (0.7796)

Multinational firm

influence � C1

3.2215**

(1.4824)

Low technological

sector

–0.8114* –0.5858 –0.6109

(0.4618) (0.4630) (0.4857)

Medium technological

sectors

–0.5545 –0.2971 –0.3074

(0.4408) (0.4671) (0.4660)

Intercept –0.0117 –1.3581 –0.8283

(1.4049) (1.5420) (1.5411)

Log likelihood value –86.3438 –83.4412 –80.5778

Pseudo R2 0.2152 0.2416 0.2676

LR w2 31.50*** 35.99*** 43.68***

LR test 5.82** 5.73**

Correctly classified (ISO

adopters)

0.7835 0.8041 0.7732

Correctly classified

(non-ISO adopters)

0.7273 0.7424 0.7424

Correctly classified

(total sample)

0.7607 0.7791 0.7607

Number of observations 163 163 163

Standard errors are presented in parentheses. Total sample size

163.*,**,*** indicates significance at the 0.10, 0.05 and 0.01 level,respectively.

658 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

Dimara and Skuras (2002): firms with poorfinancial performance in the year prior to theadoption of ISO certification are more likely toadopt ISO certification. Despite this, we reject ourfifth hypothesis (Hypothesis 5) due to the lack ofsignificance in the parameter estimates at differentquartiles of the distribution of the ROA ratio.However, this might reinforce that ISO certificationis also understood as a strategic tool, responding tothe need for improving business performance. It isimportant to remark that we have also estimatedalternative specifications to test whether ROE andlabour productivity have an impact upon theadoption of ISO certification. Results remainunchanged. They are not shown due to lack ofspace, but they are available on request.As for the organizational variables, our find-

ings reported in Table 3 show that the influenceexerted by a multinational firm is statisticallysignificant only when such a firm is the mainshareholder. Consequently, Hypothesis 6 is par-tially confirmed. From Table 4 we observe thatthe decision to adopt ISO-9000 rises 3.38% infirms totally controlled by a multinational,relative to that shown by firms where a multi-national holds 84% of the control rights (topquartile). This result is especially relevant, sincewe can conclude that multinational firms play an

important role in what concerns a firm’s perfor-mance improvements and its strategic design. Asindicated by Andersson, Forsgren and Holm(2002), the strong presence (influence) of multi-national firms within an organization may lead toincreasing adoption of new control tools, eitherto seek a source of competitive advantage or toestablish efficient controls over production, whichmay help ensure the quality of products.

The impulse effect of ISO certification upon firmperformance

Table 5 presents the results for the differentmodels that evaluate the presence of an impulseeffect of ISO certification upon firm performance(equation (2)). When the dependent variable isthe variation in ROA and the changes in labourproductivity, our findings indicate that d2 isgreater than zero and statistically significant.This confirms that the productive shift followingthe adoption of ISO-9000 certification (DISO)exerts an impulse effect that helps explainperformance differences (Table 5). However,when the dependent variable is the change inROE, we find no statistically significant change inthe DROE slope for those firms that adopted ISO-9000. This can be attributed to the fact that this

Table 4. Rare events logit model: sensitivity to the implementation of the ISO-9000 certification (from specification (3) in Table 3)

Independent variables Discrete change for

dummy variables

Discrete changes at different percentiles

of the distribution of the corresponding

independent variables

0.10–0.25 0.25–0.50 0.50–0.75 0.75–0.90

Product type 0.27116w

Small orders –0.16255

Line production –0.00224

JIT 0.26752w

Multinational firm influence –0.40107

Low technological sector –0.15054

Medium technological sectors –0.06983

Size lagged (ln assets) 0.02465 0.01995 0.03799 0.02998

Rate of non-full time employees –0.00151 –0.00658 –0.01572 –0.00893

Export capacity 0.01361 0.02394 0.01400 0.01417

Labour intensity –0.04837 –0.03924 –0.04836w –0.06848w

Leverage ratio in 1995 –0.00239 –0.00662 –0.00581 –0.01724

Return on assets in 1995 –0.03036 –0.02508 –0.02372 –0.03446

Stake held by the main shareholder (C1) 0.00418 0.00361 0.00493 0.00000

Multinational firm influence � C1 0.00000 0.00000 0.52029w 0.03379w

The first difference represents the change in the probability as a result of a discrete change from zero to one in the independent

variable, i.e. tx 5Pr(Y5 1|X5 1) – Pr(Y5 1|X5 0). In the case of continuous variables the first difference refers to discrete changes

in the variable of interest at different percentiles. Total sample size 163.windicates that the change in the discrete and continuous variables at their corresponding percentiles is significant at the 0.05 level.

ISO-9000 Certification and Ownership Structure 659

r 2009 British Academy of Management.

ratio is a shareholder-oriented variable, and itscomponents are affected by extraordinary opera-tions different from the firm’s core activity.Furthermore, these results give support to theargument that the implementation of ISO-9000certification affects to a greater extent the opera-tional performance of the business, which is moreobservable in performance measures more relatedto operational and productive performance, suchas ROA and labour productivity.Concerning changes in ownership structure,

our results indicate that changes in the sharesheld by the largest shareholder (DC1) exert astatistically significant negative effect on changesin ROE, whereas changes in this stake when amultinational firm is the main shareholder arenegatively correlated to both ROA and ROE

(Table 5). Nevertheless, when the dependentvariable is the change in the labour productivityratio, we observe that changes in the stake heldby the largest shareholder are not correlated tochanges in performance in a significant way, nomatter the type of shareholder. These findingsseem to confirm those reported by Zwiebel (1995),who finds that ownership concentration impactsperformance differently, in accordance with thelargest shareholder characteristics and interests.

Impact of ISO certification and ownershipstructure upon firm performance

Table 6 presents the results of the models thatconsider ISO certification and ownership struc-ture as determinants of firm performance (equa-

Table 5. Regression results: impact of the impulse effect of ISO certification and shifts in ownership structure upon firm performance

Independent variables DROA DROE DLabour productivity

(1) (2) (3) (1) (2) (3) (1) (2) (3)

DSize (ln assets)t–1 2.0546 1.9445 2.0399 2.8884** 2.5656** 2.8714** 0.3370*** 0.3392*** 0.3371***

(2.2874) (2.2907) (2.2851) (1.4688) (1.4509) (1.4614) (0.0563) (0.0564) (0.0564)

DAdopt ISO certification 2.8386* 2.8353* 2.8382* –0.4334 –0.4431 –0.4339 0.0582* 0.0583* 0.0582*

(1.6177) (1.6178) (1.6161) (1.0384) (1.0247) (1.0335) (0.0298) (0.0298) (0.0297)

DStake held by the main

shareholder (C1)

–3.2927 –9.6595*** 0.0669

(3.5293) (2.2354) (0.0869)

DMultinational firm as C1 –7.2188* –8.3612*** 0.0285

(4.2596) (3.0438) (0.1174)

Year 1997 (dummy) –1.9850 –1.9854 –1.9754 1.5797 1.5788 1.5909 0.0406 0.0406 0.0406

(1.9313) (1.9315) (1.9293) (1.2401) (1.2233) (1.2338) (0.0476) (0.0476) (0.0476)

Year 1998 (dummy) 1.6581 1.7885 1.9442 2.0832*** 2.4657*** 2.4145** 0.0282 0.0255 0.0270

(1.4928) (1.4994) (1.5031) (0.9585) (0.9497) (0.9613) (0.0368) (0.0369) (0.0371)

Year 1999 (dummy) 0.1081 0.1058 0.1175 1.3408 1.3340 1.3517 –0.0253 –0.0253 –0.0254

(1.4926) (1.4928) (1.4911) (0.9584) (0.9455) (0.9536) (0.0367) (0.0368) (0.0368)

Year 1997 � Low

technological sector

0.8581 0.8583 0.8581 0.9340 0.9347 0.9340 –0.0641 –0.0641 –0.0641

(1.8967) (1.8969) (1.8948) (1.2179) (1.2015) (1.2117) (0.0467) (0.0467) (0.0467)

Year 1998 � Low

technological sector

–1.4894 –1.4132 –1.5072 –1.1022 –0.8787 –1.1229 –0.0106 –0.0122 –0.0106

(1.8303) (1.8323) (1.8285) (1.1753) (1.1605) (1.1693) (0.0451) (0.0451) (0.0451)

Year 1999 � Low

technological sector

0.5594 0.5560 0.5590 0.3612 0.3510 0.3607 0.0481 0.0482 0.0481

(1.8298) (1.8300) (1.8279) (1.1750) (1.1591) (1.1690) (0.0451) (0.0451) (0.0451)

Year 1997 � Medium

technological sector

6.2091*** 6.2092*** 6.2091*** 0.2320 0.2324 0.2320 0.0676 0.0676 0.0676

(1.9777) (1.9179) (1.9157) (1.2314) (1.2147) (1.2251) (0.0472) (0.0472) (0.0472)

Year 1998 � Medium

technological sector

–1.5682 –1.5731 –1.6017 –0.7585 –0.7731 –0.7974 –0.0129 –0.0128 –0.0127

(1.8937) (1.8939) (1.8919) (1.2160) (1.1995) (1.2099) (0.0466) (0.0466) (0.0467)

Year 1999 � Medium

technological sector

0.0415 0.0420 0.0416 0.5969 0.5983 0.5970 –0.0175 –0.0175 –0.0175

(1.8937) (1.8939) (1.8918) (1.2160) (1.1995) (1.2098) (0.0466) (0.0466) (0.0467)

Intercept –0.2923 –0.2801 –0.3003 –1.2551** –1.2194** –1.2644** 0.0086 0.0084 0.0087

(0.8021) (0.8023) (0.8013) (0.5150) (0.5081) (0.5124) (0.0197) (0.0198) (0.0198)

Wald test (w2) 19.85** 21.72** 22.19** 13.93 32.99*** 21.62** 60.39*** 60.95*** 60.36***

R2 (overall) 0.0301 0.0314 0.0336 0.0213 0.0491 0.0327 0.0862 0.0871 0.0863

Hausman test (w2) 1.30 1.26 1.17 2.19 2.29 1.99 4.08 3.99 4.07

Number of observations 652 652 652 652 652 652 652 652 652

Standard errors are presented in parentheses. Total sample size 652 (163 firms yearly).*,**,*** indicates significance at the 0.10, 0.05 and 0.01 level, respectively.

660 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

tion (3)). As can be seen, our main result indicatesthat there is a positive and statistically significanteffect between the adoption of ISO certificationand firm performance (g340). This result isrobust to different model specifications. So, thisfinding is in accordance with our Hypothesis 5b.Our results also show that the relationship

between ISO-9000 and ownership is conditionedby the characteristics of the main shareholder. Onthe one hand, the coefficient for the variable C1� ISO is not consistently significant, indicatingthat, for those firms that adopted the ISO-9000,performance is not linked to the presence of a

more concentrated ownership structure (Table 6).This leads us to reject our Hypothesis 7a. On theother hand, when the main shareholder is amultinational firm we observe that g440 andg5o0 in specifications (2) and (3) for everydependent variable. These findings support ourHypothesis 7b, and could indicate that thecontrol rights exerted by multinational firms areimportant to promote innovative propositions(such as the adoption of ISO certificates) as wellas to improve monitoring tasks within the firm,leading to better performance results (g440).These results hold for all the specifications

Table 6. Regression results: impact of ISO certification and ownership structure upon firm performance

Independent

variables

ROA ROE Labour productivity

(1) (2) (3) (1) (2) (3) (1) (2) (3)

Size (ln assets)t–1 0.0731*** 0.0614*** 0.0646*** –0.0110 –0.0363 –0.0305 0.5855*** 0.6540*** 0.6580***

(0.0158) (0.0159) (0.0158) (0.0359) (0.0345) (0.0342) (0.0765) (0.0698) (0.0707)

Size squared (ln

assets)t–1

–0.0032*** –0.0027*** –0.0029*** 0.0008 0.0018 0.0015 –0.0181*** –0.0216*** –0.0219***

(0.0007) (0.0008) (0.0008) (0.0017) (0.0016) (0.0016) (0.0036) (0.0033) (0.0034)

Adopt ISO

certification

0.0236*** 0.0256*** 0.0201*** 0.0753*** 0.0780*** 0.0734*** 0.1456*** 0.1458*** 0.1196***

(0.0078) (0.0041) (0.0038) (0.0274) (0.0144) (0.0140) (0.0525) (0.0354) (0.0325)

Stake held by the

main shareholder

(C1)

0.0165* 0.0532** 0.0767*

(0.0091) (0.0265) (0.0423)

C1 � ISO –0.0143 –0.0334 –0.1093*

(0.0103) (0.0371) (0.0612)

Multinational

firm

0.0609*** 0.0732*** 0.1686***

(0.0098) (0.0199) (0.0482)

Multinational

firm � ISO

–0.0573*** –0.0662*** –0.1762***

(0.0109) (0.0232) (0.0576)

Multinational

firm as C1

0.0372*** 0.0763*** 0.1676***

(0.0104) (0.0244) (0.0357)

Multinational

firm as C1 � ISO

–0.0313*** –0.0646** –0.1520***

(0.0113) (0.0272) (0.0485)

Low

technological

sector

0.0224*** 0.0225*** 0.0229*** 0.0266** 0.0346** 0.0345** –0.1356*** –0.1061*** –0.1124***

(0.0042) (0.0041) (0.0040) (0.0135) (0.0135) (0.0135) (0.0377) (0.0357) (0.0323)

Medium

technological

sectors

0.0245*** 0.0216*** 0.0237*** 0.0326** 0.0336** 0.0334** –0.1363*** –0.1114*** –0.1140***

(0.0044) (0.0043) (0.0044) (0.0139) (0.0135) (0.0134) (0.0428) (0.0396) (0.0379)

Time dummies YES YES YES YES YES YES YES YES YES

Intercept � 0.3787*** –0.3056*** –0.3200*** 0.0466 0.1931 0.1671 1.0455** 0.6856* 0.6905*

(0.0833) (0.0818) (0.0818) (0.1885) (0.1791) (0.1781) (0.4114) (0.3718) (0.3772)

Wald test (w2) 445.21*** 513.33*** 426.39*** 39.78*** 51.96*** 49.57*** 808.54*** 981.17*** 1184.15***

Adjusted R2

(unweighted)a0.0273 0.0579 0.0444 0.0100 0.0107 0.0100 0.3241 0.3294 0.3277

Number of

observations

652 652 652 652 652 652 652 652 652

Standard errors adjusted for heteroskedasticity are presented in parentheses. Estimation method: feasible generalized least squares.

Total sample size 652 (163 firms yearly).aUnweighted R2 is reported because the generalized least squares (GLS) transformation inflates the statistic from the regression(Greene, 2003). We obtain the unweighted R2 regressing the untransformed dependent variable on the predicted values using thecoefficients from the weighted (GLS) regression.*,**,*** indicates significance at the 0.10, 0.05 and 0.01 level, respectively.

ISO-9000 Certification and Ownership Structure 661

r 2009 British Academy of Management.

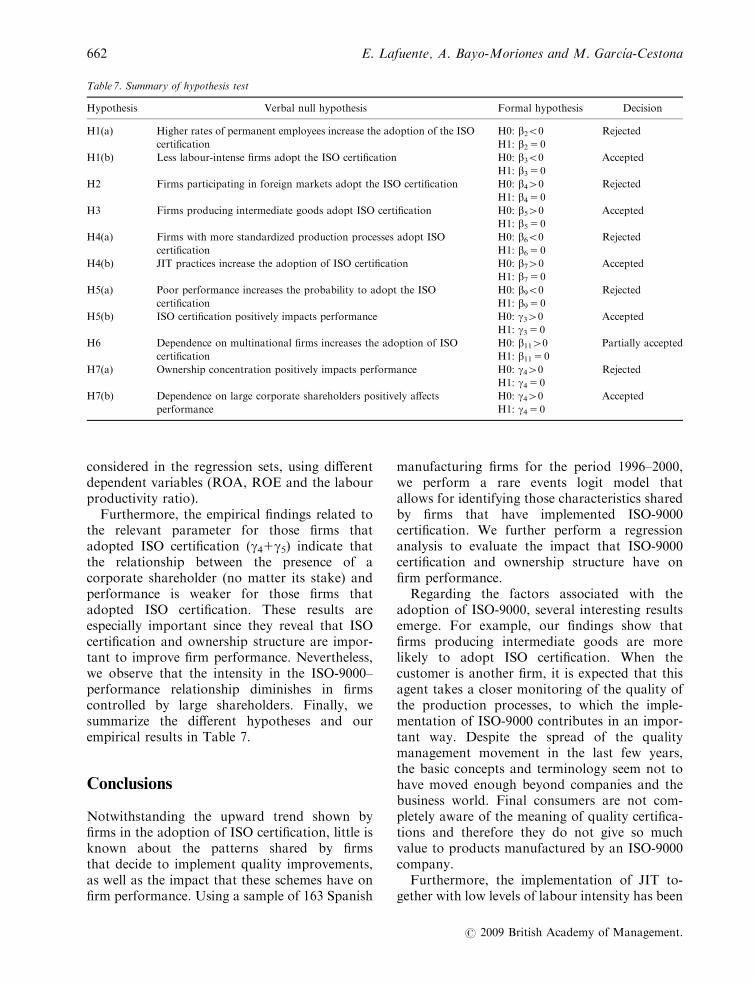

considered in the regression sets, using differentdependent variables (ROA, ROE and the labourproductivity ratio).Furthermore, the empirical findings related to

the relevant parameter for those firms thatadopted ISO certification (g41g5) indicate thatthe relationship between the presence of acorporate shareholder (no matter its stake) andperformance is weaker for those firms thatadopted ISO certification. These results areespecially important since they reveal that ISOcertification and ownership structure are impor-tant to improve firm performance. Nevertheless,we observe that the intensity in the ISO-9000–performance relationship diminishes in firmscontrolled by large shareholders. Finally, wesummarize the different hypotheses and ourempirical results in Table 7.

Conclusions

Notwithstanding the upward trend shown byfirms in the adoption of ISO certification, little isknown about the patterns shared by firmsthat decide to implement quality improvements,as well as the impact that these schemes have onfirm performance. Using a sample of 163 Spanish

manufacturing firms for the period 1996–2000,we perform a rare events logit model thatallows for identifying those characteristics sharedby firms that have implemented ISO-9000certification. We further perform a regressionanalysis to evaluate the impact that ISO-9000certification and ownership structure have onfirm performance.Regarding the factors associated with the

adoption of ISO-9000, several interesting resultsemerge. For example, our findings show thatfirms producing intermediate goods are morelikely to adopt ISO certification. When thecustomer is another firm, it is expected that thisagent takes a closer monitoring of the quality ofthe production processes, to which the imple-mentation of ISO-9000 contributes in an impor-tant way. Despite the spread of the qualitymanagement movement in the last few years,the basic concepts and terminology seem not tohave moved enough beyond companies and thebusiness world. Final consumers are not com-pletely aware of the meaning of quality certifica-tions and therefore they do not give so muchvalue to products manufactured by an ISO-9000company.Furthermore, the implementation of JIT to-

gether with low levels of labour intensity has been

Table 7. Summary of hypothesis test

Hypothesis Verbal null hypothesis Formal hypothesis Decision

H1(a) Higher rates of permanent employees increase the adoption of the ISO

certification

H0: b2o0

H1: b2 5 0

Rejected

H1(b) Less labour-intense firms adopt the ISO certification H0: b3o0

H1: b3 5 0

Accepted

H2 Firms participating in foreign markets adopt the ISO certification H0: b440

H1: b4 5 0

Rejected

H3 Firms producing intermediate goods adopt ISO certification H0: b540

H1: b5 5 0

Accepted

H4(a) Firms with more standardized production processes adopt ISO

certification

H0: b6o0

H1: b6 5 0

Rejected

H4(b) JIT practices increase the adoption of ISO certification H0: b740

H1: b7 5 0

Accepted

H5(a) Poor performance increases the probability to adopt the ISO

certification

H0: b9o0

H1: b9 5 0

Rejected

H5(b) ISO certification positively impacts performance H0: g340

H1: g3 5 0

Accepted

H6 Dependence on multinational firms increases the adoption of ISO

certification

H0: b1140

H1: b11 5 0

Partially accepted

H7(a) Ownership concentration positively impacts performance H0: g440

H1: g4 5 0

Rejected

H7(b) Dependence on large corporate shareholders positively affects

performance

H0: g440

H1: g4 5 0

Accepted

662 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

found to be positively linked to the decision toadopt ISO certification. Our results highlight thekey role of technology and production organiza-tion in the diffusion of ISO-9000, suggesting theexistence of complementarities between them. Inthe case of JIT, the need to produce goods in theright amount at the right moment and theabsence of inventories require a good workingof manufacturing processes. It would be difficultto put ISO-9000 into practice when stockmanagement fails and defective parts are found,so JIT can support the successful introduction ofISO-9000 by improving the reliability of suppliesand in-progress products. Similar argumentscould apply to labour-intense companies, wheredisruptions due to low reliability of productionprocesses may imply higher quality costs.As far as the impact of ISO-9000 certification is

concerned, our findings report a positive effect interms of higher ROA and labour productivity.This result is of great relevance within the ISO-9000 literature. One of the main issues of debatearound ISO-9000 is whether this standard is stillan order winner or has become an order qualifier(Rahman and Sohal, 2002). Hill (1987) definesorder qualifiers as those criteria that a companymust meet in order to be considered in themarketplace, whereas order winners are thosecriteria that actually win orders or generate sales.According to our results, it seems that in theanalysed period ISO-9000 was an order winner,since it had a positive impact on performance andmany companies remained in the marketplacewithout the certification. We are also aware thatthis argument should be corroborated in futureresearch using more recent data, because ISO-9000 has reached such a level of diffusion that itcould be reasonable to think that it can no longerbe used as a leading competitive weapon in themarket.Concerning the relevance of ownership struc-

ture, we find that the owner type becomes a morerelevant variable than the degree of concentra-tion. This result reinforces the need for better andmore detailed information concerning ownership.In particular, when a multinational firm is themain shareholder, we obtain some significantresults both in terms of the adoption of ISO-9000and in terms of changes in performance. The factthat the effect of ownership concentration doesnot appear in non-multinational firms couldsuggest that these firms use alternative super-

vision mechanisms. On the other hand, a moreconcentrated ownership structure, per se, doesnot lead to a higher probability of adoption.Somehow the current owners already control thefirm and further measures may not be necessary.As for the impact of ownership on firm perfor-mance, our results indicate that membership to amultinational firm improves performance. Thisresult can be explained by the better access toresources and good management practices thatthese companies have. More interestingly, ourempirical findings show that ISO certification andmultinational ownership behave as substitutemechanisms for improving firm performance. Apossible explanation has to do with the lowerpossibility of improvement in multinationalcompanies. Since they start at a higher perfor-mance level, as reported before, the introductionof new techniques is supposed to have smallereffects since performance is already good, makingit more difficult to achieve further improvements.We believe that these results have important

implications for both scholars and practitionersas they reveal that the adoption of ISO certifica-tion is related to strategic decision-makingprocesses. Furthermore, empirical evidence givessupport to the fact that ISO certification andownership structure are important mechanismsthat help firms to improve operational andfinancial performance. Consequently, companiesshould be encouraged to adopt ISO certificationin order to foster their competitiveness. Ourfindings show that variables related to theavailability of financial resources such as size,past profitability or leverage have no impact onthe probability of introducing the ISO-9000standard. This suggests that the costs thatcompanies must come up with in the certificationprocess are low and quite affordable by any kindof firm. Therefore, access to financial resourcesdoes not seem to be an important barrier whendeciding to start the certification process.From a theoretical point of view, we emphasize

the interrelationships between ISO-9000, owner-ship characteristics and performance. Whereasalternative approaches have underlined the linksbetween ISO-9000 and operations and technol-ogy management, this paper has paid specialattention to the role played by this standard inthe surveillance of firm activities, and conse-quently we verify to what extent business goalsare aligned with owners’ interests. Our results

ISO-9000 Certification and Ownership Structure 663

r 2009 British Academy of Management.

could be applicable not only to ISO certificationbut also to other certifications that can provideowners with information about the correctnessand suitability of the decisions and actions takenby firm managers.As with any cross-sectional study, the main

limitation of this paper lies in the absence of alongitudinal analysis that could have given agreater perspective to our approach to theadoption of ISO-9000. As a consequence, thetypical cautions in these situations should applyin the interpretation of our findings.

References

Adams, M. (1999). ‘Determinants of ISO accreditation in the

New Zealand manufacturing sector’, Omega, 27, pp. 285–292.

Anderson, S., D. Daly and M. Johnson (1999). ‘Why firms seek

ISO certification: regulatory compliance of competitive

advantage?’, Production and Operations Management, 8, pp.

28–43.

Andersson, U., M. Forsgren and U. Holm (2002). ‘The strategic

impact of external networks: subsidiary performance and

competence development in the multinational corporation’,

Strategic Management Journal, 23, pp. 979–996.

Baldwin, J. and J. Johnson (1996). ‘Business strategies in more

and less innovative firms in Canada’, Research Policy, 25, pp.

785–804.

Beattie, K. and A. Sohal (1999). ‘Implementing ISO 9000: a

study of its benefits among Australian organizations’, Total

Quality Management, 10, pp. 95–106.

Bhuiyan, N. and N. Alam (2005). ‘An investigation into issues

related to the latest version of ISO 9000’, Total Quality

Management, 16, pp. 199–213.

Boiral, O. and M. Roy (2007). ‘ISO 9000: integration rationales

and organizational impacts’, International Journal of Opera-

tions and Production Management, 27, pp. 226–247.

Breusch, T. and A. Pagan (1979). ‘A simple test for hetero-

scedasticity and random coefficient variation’, Econometrica,

47, pp. 1287–1294.

Buttle, F. (1997). ‘ISO 9000: marketing motivations and

benefits’, International Journal of Quality and Reliability

Management, 14, pp. 936–947.

Calisir, F., C. Bayraktar and B. Beskesh (2001). ‘Implementing

the ISO 9000 standards in Turkey: a study of large

companies’ satisfaction with ISO 9000’, Total Quality

Management, 12, pp. 429–438.

Casadesus, M. and S. Karapetrovic (2005). ‘Has ISO-9000 lost

some of its lustre? A longitudinal impact study’, International

Journal of Operations and Production Management, 25, pp.

580–596.

Casadesus, M., G. Jimenez and I. Heras (2001). ‘Benefits of ISO

9000 implementation in Spanish industry’, European Business

Review, 3, pp. 327–335.

Corbett, C., M. Montes-Sancho and D. Kirsch (2005). ‘The

financial impact of ISO 9000 certification in the United

States: an empirical analysis’, Management Science, 51, pp.

1046–1059.

Dean, J. and D. Bowen (1994). ‘Managing theory and total quality:

improving research and practice through theory develop-

ment’, Academy of Management Review, 19, pp. 392–418.

Demsetz, H. and K. Lehn (1985). ‘The structure of corporate

ownership: causes and consequences’, Journal of Political

Economy, 93, pp. 1155–1177.

Demsetz, H. and B. Villalonga (2001). ‘Ownership structure

and corporate performance’, Journal of Corporate Finance, 7,

pp. 209–233.

Earle, J., C. Kucsera and A. Telegdy (2005). ‘Ownership

concentration and corporate performance on the Budapest

Stock Exchange: do too many cooks spoil the goulash?’,

Corporate Governance, 13, pp. 254–264.

Easton, G. and S. Jarrell (1998). ‘The effects of total quality

management on corporate performance’, Journal of Business,

71, pp. 253–307.

Garvin, D. (1984). ‘What does product quality really mean?’,

Sloan Management Review, 26, pp. 25–43.

Gonzalez-Benito, J. and O. Gonzalez-Benito (2005). ‘An

analysis of the relationship between environmental motiva-

tions and ISO 14001 certification’, British Journal of

Management, 16, pp. 133–148.

Greene, W. (2003). Econometric Analysis, 5th edn. Upper

Saddle River, NJ: Prentice Hall.

Grossman, S. and O. Hart (1986). ‘The costs and benefits of

ownership: a theory of vertical and horizontal integration’,

Journal of Political Economy, 94, pp. 691–719.

Hart, O. and J. Moore (1990). ‘Property rights and the nature

of the firm’, Journal of Political Economy, 98, pp. 1119–1158.

Hendricks, K. and V. Singhal (1996). ‘Quality awards and the

market value of the firm: an empirical investigation’,

Management Science, 42, pp. 415–436.

Hill, T. J. (1987). ‘Teaching manufacturing strategy’, Interna-

tional Journal of Operations and Production Management, 6,

pp. 10–20.

Karmarkar, U. and R. Pitbladdo (1997). ‘Quality, class, and

competition’, Management Science, 43, pp. 27–39.

King, G. and L. Zeng (2001a). ‘Logistic regression in rare

events data’, Political Analysis, 9, pp. 137–163.

King, G. and L. Zeng (2001b). ‘Explaining rare events in

international relations’, International Organization, 55, pp.

693–715.

McConnell, J. and H. Servaes (1990). ‘Additional evidence on

equity ownership and corporate value’, Journal of Financial

Economics, 27, pp. 595–612.

Merino, J. (2003). ‘Factors relating to the adoption of quality

management practices: an analysis for Spanish manufactur-

ing firms’, Total Quality Management, 14, pp. 25–44.

Morck, R., A. Shleifer and R. Vishny (1988). ‘Management

ownership and market valuation: an empirical analysis’,

Journal of Financial Economics, 20, pp. 293–315.

Nicolau, J. and R. Sellers (2002). ‘The stock market’s reaction

to quality certification: empirical evidence from Spain’,

European Journal of Operational Research, 142, pp. 632–641.

Osterman, P. (1994). ‘How common is workplace transforma-

tion and who adopts it?’, Industrial and Labor Relations

Review, 47, pp. 173–188.

Powell, T. (1995). ‘TQM as competitive advantage: a review

and empirical study’, Strategic Management Journal, 16, pp.

15–37.

Rahman, S. and A. Sohal (2002). ‘A review and classification of

total quality management research in Australia and an

664 E. Lafuente, A. Bayo-Moriones and M. Garcıa-Cestona

r 2009 British Academy of Management.

agenda for future research’, International Journal of Quality

and Reliability Management, 19, pp. 46–66.

Rust, R., A. Zahorik and T. Keiningham (1995). ‘Return on

quality (ROQ): making service quality financially accountable’,

Journal of Marketing, 59, pp. 58–70.

Samson, D. and M. Terziovski (1999). ‘The relationship

between total quality management practices and operational

performance’, Journal of Operations Management, 17, pp.

393–409.

Shleifer, A. (1998). ‘State versus private ownership’, Journal of

Economic Perspectives, 12, pp. 133–150.

Takahashi, K., K. Morikawa and N. Nakamura (2004).

‘Reactive JIT ordering system for changes in the mean and

variance of demand’, International Journal of Production

Economics, 92, pp. 181–196.

Terziovski, M., D. Power and A. Sohal (2003). ‘The long-

itudinal effects of the ISO 9000 certification process on

business performance’, European Journal of Operational

Research, 146, pp. 580–595.

Tsekouras, K., E. Dimara and D. Skuras (2002). ‘Adoption of a

quality assurance scheme and its effect on firm performance:

a study of Greek firms implementing ISO 9000’, Total

Quality Management, 13, pp. 827–841.

Tzelepis, D., K. Tsekouras, D. Skuras and E. Dimara (2006).

‘The effects of ISO 9001 on firms’ productive efficiency’,

International Journal of Operations and Production Manage-

ment, 26, pp. 1146–1163.

White, R., J. Pearson and J. Wilson (1999). ‘JIT manufacturing:

a survey of implementation in small and large US manu-

facturers’, Management Science, 45, pp. 1–15.

Withers, B., M. Ebrahimpour and N. Hikmet (1997). ‘An

exploration of the impact of TQM and JIT on ISO 9000

registered companies’, International Journal of Production

Economics, 53, pp. 209–216.

Wooldridge, J. (2000). Introductory Econometrics: A Modern

Approach. New York: Southwestern Publishers.

Wruck, K. (1989). ‘Equity ownership concentration and firm

value: evidence from private equity financings’, Journal of

Financial Economics, 23, pp. 3–28.

Young, G., M. Charns and S. Shortell (2001). ‘Top manager

and network effects on the adoption of innovative manage-

ment practices: a study of TQM in a public hospital system’,

Strategic Management Journal, 22, pp. 935–951.

Zwiebel, J. (1995). ‘Block investment and partial benefits

of corporate control’, Review of Economic Studies, 62, pp.

161–185.

Esteban Lafuente lectures at the Universitat Autonoma of Barcelona. His research interests includecorporate governance and efficiency analysis, and he has published in Regional Studies andEntrepreneurship and Regional Development.

Alberto Bayo-Moriones is Senior Lecturer in human resource management at the Public Universityof Navarra, where he earned his PhD. His main research interests are organizational innovation andcompensation management. His research has been published in journals such as the British Journalof Industrial Relations, Industrial and Labor Relations Review and International Journal of Operationsand Production Management.

Miguel Garcıa-Cestona is associate professor of managerial economics at the Universitat Autonomaof Barcelona and has also served as coordinator of a joint doctoral programme in economics,management and organizations. He holds an MA in economics and a PhD in businessadministration from Stanford University. His research interests lie in the fields of corporategovernance and comparative institutional analysis; he has co-authored a book chapter and haspublished in, amongst others, the Journal of Banking and Finance and the European Journal ofOperational Research.

ISO-9000 Certification and Ownership Structure 665

r 2009 British Academy of Management.