Embed Size (px)

Citation preview

Table of Contents1.0 Introduction........................................21.1 Constructing An Investment Policy Statement.........21.2 Investment Objectives...............................31.3 Target Return For The Portfolio.....................41.4 Level of the Risk...................................51.4 Constraints.........................................61.6 Investment Guidelines...............................72.0 Construction Portfolio..............................92.1 Economic Outlook of Malaysia and its Financial Condition..............................................102.2 Describing The Allocated Funds (across countries, asset classes and securities)..........................152.3 How Select the assets?.............................172.4 Why We Selected the Assets?........................182.5 Proportion of the Investment and The Reason?.......18Reference:.............................................20

1.0 Introduction

This investment policy statement’s objective is to

provide the primary goals and guidelines for our client

on the portfolio management process and describes the

main strategies to endorse the construction on our

investment policy statement. However, we will develop and

divulge the whole information based on our client’s age,

financial ability, asset allocation, risk tolerance and

time horizon that will be included into her investment

objectives. Throughout this work, we will extend and give

our preliminary suggestions to construct the Investment

Policy Statement (IPS) based on the followings. In

addition to this, we will give a quick introductory

explanation what is an investment policy statement, its

purpose, outline expectations and responsibilities both

managers and clients.

BWFNN3033 Portfolio Management

2

Procedure manuals that no one can scrutinise serve little

purpose. The same is true with a statement of investment

policy. If investors are going to have one, the policy

without doubt should influence the investment process.

However, the most important and worthwhile part of the

investment policy statement will do four things that

ultimately affect the investment performance

successfully. Firstly, it will outline expectations and

responsibilities of the parties involved. Secondly, it

will determine the investment objectives and relevant

constraints. Thirdly, it will address the choice of

assets for the portfolio. Lastly, it will provide a

mechanism for evaluation.

1.1 Constructing An Investment Policy Statement

This investment policy statement should be suited for the

specific conditions the portfolio faces and there are

some elements of a useful investment policy that will

help the client to maintain the gainful portfolio

holdings over the long-term. Before carrying out this, we

BWFNN3033 Portfolio Management

3

will introduce and extend the each element by giving the

abstract points based on the example we have chosen.

1.2 Investment Objectives

Our client is Mrs. Clara who is married, has

children and primarily focused on accelerating her wealth

building efforts for her children’s college education and

for her own retirement. As an investment manager, we need

to build up well appropriate asset allocation and

investment strategy because our client is at the mid-life

accumulators who will be caring about her further

financial affairs that can help her over the long-term

way if it is undertaken. Her financial objectives over

the long-term are as below:

The likely income level of the family

Advancing in professions and careers

Building wealth for retirement

Wealth to fund children’s college tuition

Saving for retirement

Takes one or more vacations per year

Buying or leasing a car for her children

BWFNN3033 Portfolio Management

4

Buying vacation home

Other related expenses that will incur her in the

future. All these reasonable objectives must have been

imparted to the client in order to get the precise

knowledge and insights because sometimes the client’s

stated objectives are unrealistic or out of reach so

that as investment manager, we ought to educate our

client on her financial objectives that will be

attaining.

1.3 Target Return For The Portfolio

Specifically the investment policy statement must have

said the target return. This is the level of performance

that the fund seeks to attain. However, the target return

tells us about the standard market which we will be

referring as a main source to gauge the standardised

market return and it can also measure the overall

performance of the market. By indicating this, we are

merely going to refer FBMKLCI Index. This is an important

stage to measure the healthiness of the marketplace over

BWFNN3033 Portfolio Management

5

the

long-term investment. By keeping pace with standardised

index fund, we can know our client’s investment whether

it is going to plummet or skyrocket so that choosing a

right benchmark target return is crucial. In addition,

the chosen target must be reasonable and consistent with

the reality of the life of marketplace. As a fact of this

matter, the target return has some reasonable and

unreasonable objectives. Our client’s target return has

been considered meticulously to keep her investment well

in the long run.

Average rate of return of 8 percent

KLCI Index attainable return should be between 25 –

40 percent or no less than 25 percent.

FTSE Bursa Malaysia EMAS Index over the long term

possibly 10 years investment we expect to gain an

average rate of return 20 percent.

Basically, the index fund helps us to get the clear

picture of our selected stocks. Let us say if the average

market does well, our investment presumably will do best.

In short, the average market return tells us the

BWFNN3033 Portfolio Management

6

performance of the overall stocks. Therefore, we have

selected two local indices to get our benchmark return

over the long-term investment as it is mentioned above 10

years and it is a maximum term for our client’s

investment.

1.4 Level of the Risk

We, as an investment group have dedicated much of our

time for the complex topic and it is a critical stage to

assess. In this part, we introduce briefly about the risk

in the portfolio. Risk management insights should be

taught to our client in order to ensure that our client

sufficiently fathom the fundamental nature of risk and

how it can influence the client’s expectations and its

investment performance. As beginner managers, we should

understand that the existence of risk is certain over the

investment life and it is inevitable. However, the risk

can be managed through the investment period. We can

assure our client that the risk decision sometimes lead

to down to the specific downturn conditions. Therefore,

as investment managers, we have considered all the

BWFNN3033 Portfolio Management

7

necessary actions in order to protect our client’s

investment and manage it through that period. There are

however three type of risks that portfolio can take.

These are the risks that require us to measure by either

beta or return variance. The following risks that

portfolio can take into considerations are less, more

than average or the norm condition of market.

As a manager, we advise our client to take a long-term or

above-average risk because it helps our investor or

client to attain much profitable return due to more risk,

our client can probably expect the higher or better

return. Our suggestion based on the long-term equity

securities, government bonds, corporate bonds, and other

fixed income securities. Long-term investment requires

our investor to take higher risk, so as a matter of that

risk, our client can get much lucrative return in the

long run to subsidise the family needs. One of the most

investable stocks is blue chip stock because of its

reputable market capitalisation; it can generate higher

return over the long-term investment

BWFNN3033 Portfolio Management

8

Thus, level of risk in the portfolio is above average,

our priority is to maximise possibility of potential

gains. Therefore, at our client’s age, she should invest

her investment such as secured sovereign bonds, real

estate investment trust and so on. She can gain good

return from the real estate investment by the increasing

the value of her property.

1.4 ConstraintsThere are a few considerations in order to identify those

constraints’ condition we have to take a look carefully

on each criterion that could affect or she must operate.

This is fourth stage that will be elaborating the

constrains based on our client’s will which she will be

allocating the security assets in a way that she can

benefit most.

i. Time Horizon

ii. Exclusions Investment

iii. Liquidity

Time Horizon - our client is at the medium accumulators

which means that her time horizon defines the she will

BWFNN3033 Portfolio Management

9

not

take too much risks in the equity market. We advise her

to invest her money in medium risk assets. In fact,

medium risk assets are the investment vehicles that have

a feasible chance that the assets will appreciate in

value and able to bear a certain degree of risk.

Investors who follow the medium assets risk tend to have

an average risk tolerance. Medium assets such as

mentioned above government bonds, real estate, exempt tax

municipal bonds, zero coupon bonds, foreign common stocks

(blue chips). Actually, investing globally in foreign

stocks or sovereign bonds is much diversifiable for the

client’s portfolio because it has low correlation in

contrast to local government. There are many blue chip

stocks, which are the companies with market

capitalisation of 4billion dollars and above and it is

often called as large cap such companies are Apple,

Amazon, EBay, Boeing, Coca-Cola and so on during this

policy statement, we will elaborate the different type of

asset classes according to its industry.

BWFNN3033 Portfolio Management

10

Exclusion Investments – is another type of investment

constraint that refers to the unwillingness of investing

the money that can often harm society ethically or

morally. Our client’s one of her portfolio constraints is

not to invest the fund in tobacco companies, alcoholic

companies, other prohibited beverages because Mrs. Clara

is Moslem and according to her willing, she is not going

to invest the fund in prohibited things that the religion

does not allow.

Liquidity – Our client should carry forward adequate

liquidity – through the choice of investment vehicles and

proper allocation of the assets such as investing in

foreign exchange market, money market instruments and

Malaysian government bonds. However, the foreign exchange

market is thought that it is the most liquid market

because trillion dollars will be exchanging each day.

1.6 Investment Guidelines This part provides our client with solid and robust

investment guidelines in order to ensure that our client

is on the right way. This is the last part of our

BWFNN3033 Portfolio Management

11

Investment Policy Statement and it is crucial to define

the appropriate guideline for the asset allocation

process that we will be discussing in the next part of

construction portfolio. However, this is essential to

make sure as investment manager, we provide our client

with significant and advantageous value of her

investment. Our investment guideline comprises of several

asset class, such short-term securities, long-term asset

and other liquid and illiquid financial securities. The

selected assets classes are as below:

Stocks

Bonds

Real Estate

Foreign Stock

Foreign Bonds

These are the financial securities that we are going to

imply and create the allocation of the assets. Moreover,

asset allocation gives us the maximum rate of return. It

will provide a stream of income that holds with

inflation.

BWFNN3033 Portfolio Management

12

Diversification is another sub-topic of our investment

guideline. The fund that will be investing across the

different asset classes is pivotal and it helps us to

diversify our possibility of risk.

Using a pooled fund – obviously, investing in mutual

funds, unit trust funds are profitable for the middle

accumulators because of its functions, management, as

well as its long –term returns. In addition, this can

give us a higher return over the long-term and there are

less chance to lose the money so that it is important to

ponder that investing in pooled funds can benefit our

client.

Rebalancing stage – tells our client that she will have

to update the assets classes at least annually. The aim

of this rebalancing is to protect from the exposure and

continue the asset allocation with stipulated ranges.

Evaluation – more importantly, to ensure the assets are

doing well or not, we refer to our identified benchmark.

Through benchmark, we can evaluate the each asset class’s

performance that will be included in our client’s

BWFNN3033 Portfolio Management

13

portfolio. Benchmark can truly reflect the all assets

that will be chosen in the portfolio.

2.0 Construction Portfolio Generally speaking, an asset class is classification of

financial assets that deal with same characteristics that

can be tradable. If we look at traditionally, there are

the main asset classes, which comprise of equities,

bonds, cash, and real estate. In modern and globalised

world, those assets can be divided up internationally as

well.

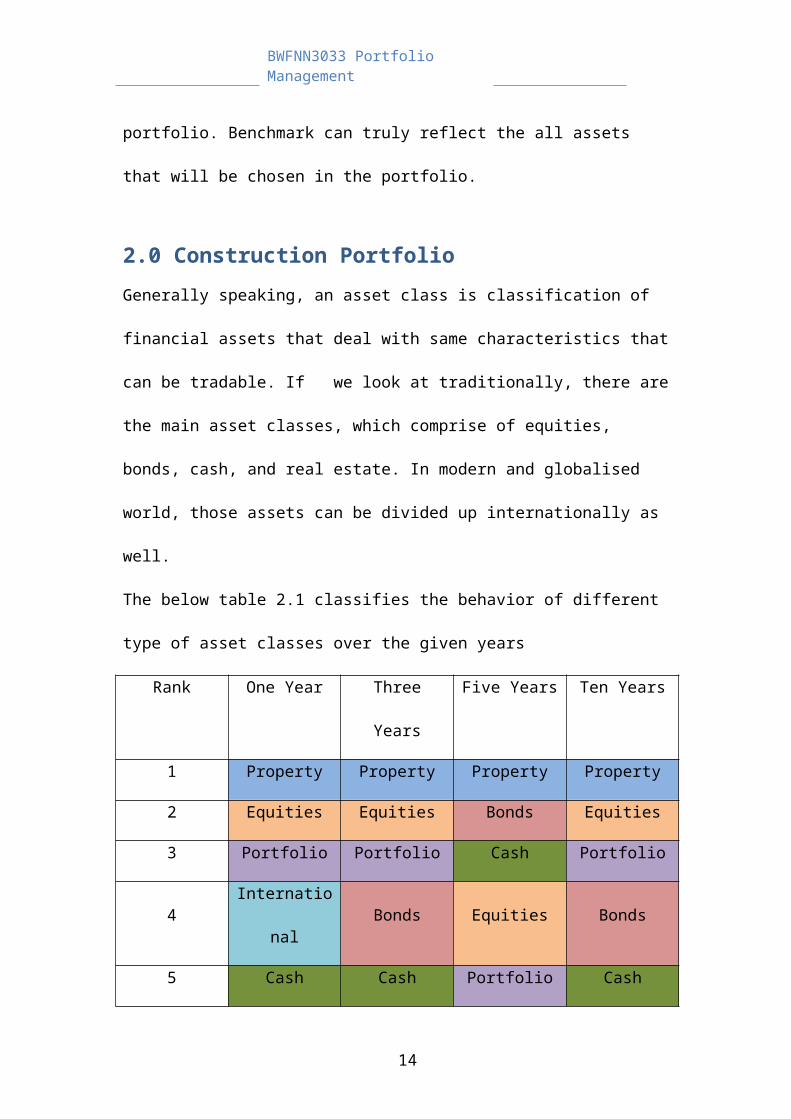

The below table 2.1 classifies the behavior of different

type of asset classes over the given years

Rank One Year Three

Years

Five Years Ten Years

1 Property Property Property Property

2 Equities Equities Bonds Equities

3 Portfolio Portfolio Cash Portfolio

4Internatio

nalBonds Equities Bonds

5 Cash Cash Portfolio Cash

BWFNN3033 Portfolio Management

14

6 InflationInternatio

nalInflation Inflation

7 Bonds InflationInternatio

nal

Internatio

nal

Four key lessons should be taught to our client from the

above given table:

However each classified asset react in a different way to

the fundamental economic conditions and of course it is

performance will not be identical at a given point time.

Portfolio which consists of variety asset classes, can

give our client more steady condition over the ten years.

Our client should beat the inflation over the investment

period. The selected and best-chosen assets that perform

better inflation are real estate or equity.

Diversifying internationally can help our client to avoid

from the disadvantageous of asset classifications.

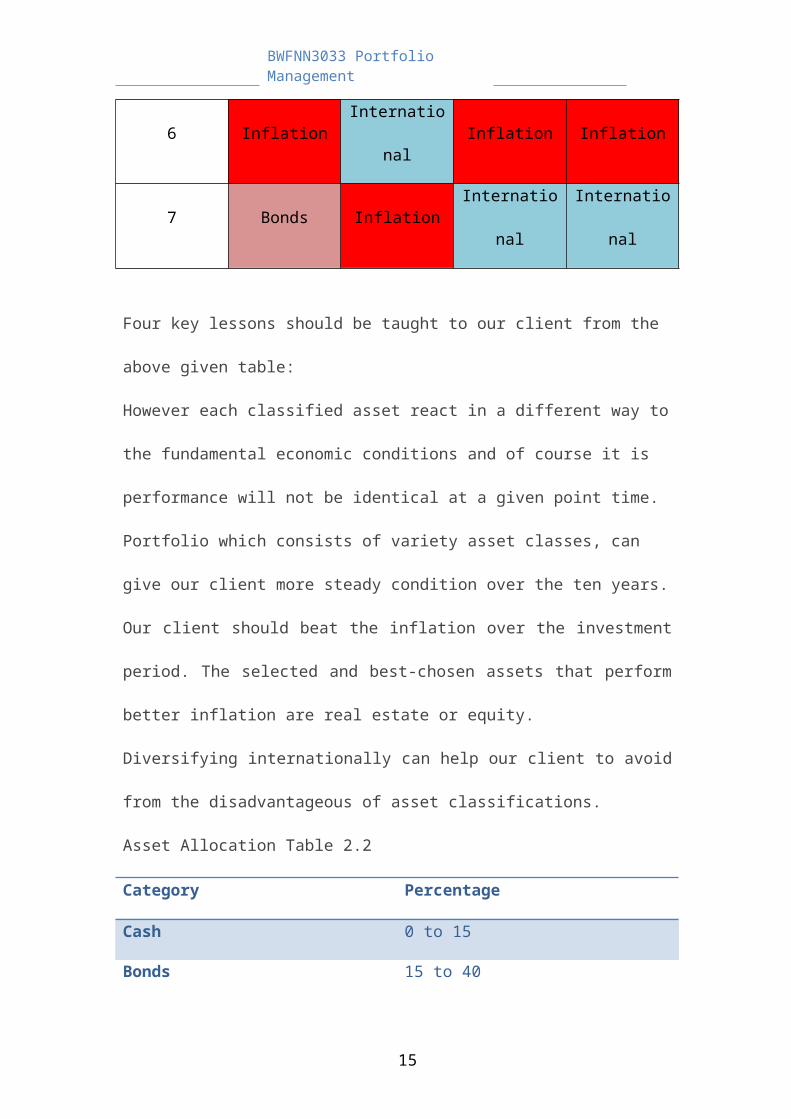

Asset Allocation Table 2.2

Category Percentage

Cash 0 to 15

Bonds 15 to 40

BWFNN3033 Portfolio Management

15

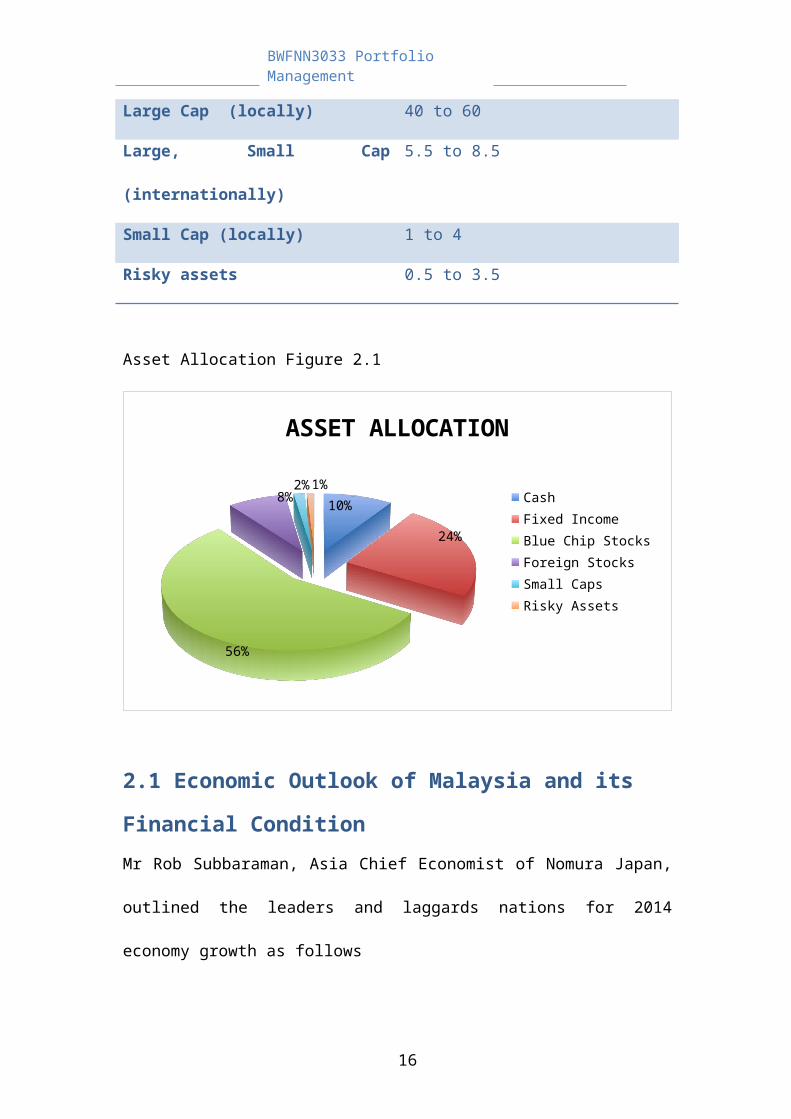

Large Cap (locally) 40 to 60

Large, Small Cap

(internationally)

5.5 to 8.5

Small Cap (locally) 1 to 4

Risky assets 0.5 to 3.5

Asset Allocation Figure 2.1

10%

24%

56%

8%2%1%

ASSET ALLOCATION

CashFixed IncomeBlue Chip Stocks Foreign StocksSmall CapsRisky Assets

2.1 Economic Outlook of Malaysia and its

Financial ConditionMr Rob Subbaraman, Asia Chief Economist of Nomura Japan,

outlined the leaders and laggards nations for 2014

economy growth as follows

BWFNN3033 Portfolio Management

16

The leaders

Korea 4.1%Philippines 7.1% Malaysia 4.5%

The laggards:

China India Indonesia Thailand

GDP expected to grow by 5.1% fro 2014, driven by higher

consumer and business spending.

The sustainability of Malaysia’s favourable near-term

outlook into 2015 and beyond hinges on the implementation

of structural reforms.

Malaysia is one of a few developing countries that

successfully converted an abundance of natural resources

into long-term sustainable growth.

The MH370 tragedy unexpectedly provides an avenue for

Malaysians to strengthen increasingly fragmented social

capital in the country. Societal risks, such as radical

religion and interfaith disharmony, which seemed to be on

the rise before the tragedy become almost subdued and

BWFNN3033 Portfolio Management

17

muted, as if it was a warning from the Almighty. The

tragedy force us to pray together, regardless of

religions of the victims and of greater significance,

mobilizing productive military and commercial assets from

many countries, reflecting a truly global operation. But,

more importantly, we are now valuing so preciously the

lives of those onboard and praying for their souls in

heaven, again without questioning their citizenship and

religious beliefs. In fact, this rare tragedy proved to

be a rallying point for Malaysians moving forward. On the

international front, there is joint search and rescue

(SAR) operations and of most importance military

cooperation, involving superpowers and friendly nations.

These positive externalities augur well for the ASEAN

economic community (AEC) and Asian century as a whole.

There are clearly many lessons that can be learned,

looking from economic and public policy perspectives. We

need to put in place or beef up an early detection system

with adequate warning signals, conduct stress tests and

implement pre-emptive measures. Apart from having good

supervisory oversight, we have to strictly enforce rules

BWFNN3033 Portfolio Management

18

and

regulations and follow standard procedures, as stipulated

by the Government and relevant international agencies and

organizations. These lessons seem almost parallel to an

early warning signals, macro-prudential measures, stress

tests and supervisory oversight that need to be put in

place and implemented to avoid economic and financial

crisis, without which social costs would be far higher,

affecting welfare and wellbeing of millions of households

and consumers.

Growth in real GDP for 2014 is projected to be at 5.5%,

on account of expected fiscal consolidation measures to

rein in budget deficit, generally tight monetary

conditions and enhanced downside risks, especially on

domestic front. External demand, however, is expected to

provide strong support for growth, especially with

accelerating expansion in the world economy, although

global risks remain on the horizon. These include risks

arising from volatility of capital flows and deflation in

key advanced economies, especially with inflation running

below many central banks' targets. As for the year 2015,

BWFNN3033 Portfolio Management

19

real GDP growth is projected to move back nicely along

the potential output growth path of between 5.5 to 6.0%

in 2015, driven by economic efficiency and innovation,

especially with expected enhanced competition in both

product and services markets, less market distortions and

imperfections, greater labour market flexibility and more

importantly productivity gains as well as more efficient

allocation of scarce resources. This projection takes

into account the likely positive impacts as described

above, under the so-called "transformation or reform

scenario". Nonetheless, the achievements under this

scenario require strong "political will" on the part of

the Government, solving not only tough "politico-

economic" issues, but also mending Malaysia's emotionally

charged matters, such as "religious and ethnic"

relations, perception of corruption and mismanagement,

among other things. As a whole, political struggles in

solving current fiscal issues must be won with strong

commitment, intelligent communications, and rock solid

credibility. These "Three C's" can only be delivered by

the establishment of "National Fiscal Council", an

BWFNN3033 Portfolio Management

20

independent body free from day-to-day politics,

established with an overarching goal of achieving fiscal

sustainability and prudence management of public

finances. The ultimate goal is achieve sustainable

economic and social development. Budget deficit reduction

is a necessity and leisurely approach as practiced in the

past is not the best option for this blessed country,

going forward.

Malaysia’s financial system has weathered the recent

global financial crisis well, helped by limited reliance

of financial intermediaries on cross border funding, a

well-developed supervisory and regulatory regime, and a

well capitalised banking system.

Stress test suggests that banks are resilient to a range

of economic and market shocks; though the high level of

reliance on demand deposits is a potential vulnerability.

Other risks faced by the financial system include those

related to rapid loan growth, rising house prices, and

high household leverage, which call for enhanced

monitoring of household leverage and a review of the

effectiveness of the macro prudential measures.

BWFNN3033 Portfolio Management

21

The

regulatory and supervisory regime for banks, insurance

firms, securities markets, and market infrastructure

exhibits a high degree of compliance with international

standards. Areas for improvement include enhancing the

framework of consolidated supervision and addressing

legal provisions that could potentially compromise

independence. The authorities have initiated action to

address most remaining shortcomings, with a draft law set

to eliminate the key gaps in the framework for banking

and insurance supervision. Banking supervision is

comprehensive and intensive, and gaps mainly relate to

formal powers to include financial holding companies in

the consolidated supervision framework, to certain legal

provisions that could potentially compromise

independence.

Malaysia’s financial sector is well diversified. It

comprises banking intermediaries, insurance companies and

capital market intermediaries with total assets of close

to 400percent of GDP as end of 2011

BWFNN3033 Portfolio Management

22

Monetary Conditions – outstanding household loan growth

was stable during the March 2014. Overall loan demand

increased with higher loan applications from both the

business and household sectors.

Banking System – Banking system capitalisation remained

strong with the common equity tier 1 Capital Ratio, tier

1 Capital Ratio and Total Capital Ratio at 12%, 12.8% and

respectively 14.4%. Net impaired loans remained at 1.3%

of net loans while the loan coverage ratio was above100%.

Exchange Rate and International Reserves - In March, the

ringgit appreciated against the US dollar and recorded a

mixed performance against the currencies of Malaysia’s

other major trade partners. International reserves of

Bank Negara Malaysia amounted to RM 427.4 billion

(equivalent to USD131.1 billion) as at 15 April 2014,

sufficient to finance 9.4 months of retained imports are

3.3 times the short-term external debt.

For Malaysia to become a high-income economy, the World

Bank’s recommendations were that the Malaysian economy

specialise further, improve workforce skills, make growth

more inclusive, and bolster public finance. This

BWFNN3033 Portfolio Management

23

obviously requires that “national interest” be defined

broadly – to include all Malaysians and reverse policies

that benefit a select few.

2.2 Describing The Allocated Funds (across countries, asset classes and securities) Allocating your investments among different asset classes

is a point to help reduce risk and potentially raise

gains. Apprise it the opposite of "putting all your eggs

in one basket." The first way to understanding

optimal asset allocation is know its meaning and purpose,

then taking a closer look at how allocation can benefit

you, and the right asset mix to get and maintain it.

Allocated funds is a mutual fund that provides investors

with a portfolio of a fixed or variable mix of the three

main asset classes which are stocks, bonds and cash

equivalents, in a variety of securities. Some asset

allocation funds maintain a specific proportion of asset

classes over time, while others vary the proportional

composition in response to changes in the economy and

investment markets.

BWFNN3033 Portfolio Management

24

Asset allocation mutual funds come in several varieties.

Generally, a "balanced fund" implies a fixed mixed of

stocks and bonds, such as 60% stocks and 40% bonds.

"Life-cycle" or "target-date" funds, which are often used

in retirement plans, usually have a mix of stocks; bonds

and cash equivalent securities that starts out with a

higher risk-return position and gradually become less

risky as the investor ages and/or nears retirement. So-

called "life-style," or actively managed asset-allocation

funds provide the active management of a fund's asset

classes in response to market conditions.

Large-cap stock - These are shares issued by large

companies with a market capitalization generally greater

than $10 billion.

Mid-cap stock - These are issued by mid-sized companies

with a market cap generally between $2 billion and $10

billion.

Small-cap stocks – this type of asset are show small size

of firm with a market cap that is less than $2 billion.

It has the highest risk due to lower liquidity.

BWFNN3033 Portfolio Management

25

Fixed-income securities – the fixed-income asset class consist

of debt securities, which have to pay the owner or

holder, some amount of fee at a maturity. When the

security matures, the income should be as well as the

return of principal.

International securities - These types of assets are issued by

foreign companies and listed on a foreign exchange.

International securities allow an investor to diversify

outside of his or her country, but they also have

exposure the foreign related risk. The risk that a

country will not be able to honor its financial

commitments.

BWFNN3033 Portfolio Management

26

2.3 How Select the assets?First of all, I see the needs of my client, Mrs . Clara

Based on her occupation, I can see that she must be

considering about target risk and target date strategies.

This is because she is going to retire in a few years.

So, she has to be well prepared about when the return

that she will get.

Target risk strategies

The fund that she invests may not be return as she wants.

Might be she loses the money or gain extra money. Stock

markets and investments are keep on changing and can

decline significantly due to issuer, market, economic,

political, regulatory, geopolitical and other conditions.

For example, Mrs Clara selected to invest in small-cap

company is because it is more volatile than investments

in larger companies. So that the possibility she can gain

more interest is higher. The second investment that she

did for example is investment in foreign markets that

involve greater risk and volatile than investments in

larger companies.

BWFNN3033 Portfolio Management

27

Target date strategies

This strategy is for Mrs Clara to choose the time horizon

that works best for her specific financial goals

consistent with the approximate retirement year. As she

wants to have a good return in the year she retired, she

chose the asset allocation of cash, fixed income, blue

chip stocks, foreign stocks, small caps and risky assets

that have a specific date on when she will gain earnings

from her investments.

2.4 Why We Selected the Assets?We have picked out the assets based on our diligent

research. We as an investment manager pondered that there

are so many different or identical factual evidences.

However, we selected the assets based on the factors that

our client can able to meet. The factors are such as risk

BWFNN3033 Portfolio Management

28

tolerance; time horizon and et cetera. Several numbers

of assets that Mrs Clara has allocated are for reducing

the portfolio risk since different investments can be

affected by the economic events and market factors. By

owning different types of investments help to reduce the

possibility of exposure that a particular risk type will

adversely affect her portfolio.

2.5 Proportion of the Investment and The

Reason?Since our client is in the mid-life accumulators, she has

a desire to begin a plan for a comfortable retirement. At

this life cycle stage, our client tend to realize that

her productive years are about half over and needs a good

proportion of asset allocation to get high return on

investment which give a significant impact on wealth. We

recommend the appropriate proportion for asset classes

for client to achieve the main goals which is to maximize

return and minimize risk and obtain a long-term growth

capital.

BWFNN3033 Portfolio Management

29

To achieve high level of return, we suggest that our

clients need to invest 64% in equities, which are

Blue chip stocks for 56% and foreign stocks for 8%.

This is because equities have the highest potential

of return but also have high risk. The positive side

of stocks is that the stocks keep pace with

inflation and hold or increase their value over

time. The possibility of losses can happen but on

this situation, our investor can recover the losses

due to her longer time horizon before retire.

The proportion for fixed income is 24% which the

investor will receive steady income that provided.

The fixed income assets tend to have lower return

than equities because it has low risk. This low risk

securities include corporate and government bonds.

In the financial assets at least need a small

proportion of cash which is 9% for investment

opportunities that our client should have. Cash pay

little or no interest but it is for shelter from

BWFNN3033 Portfolio Management

30

other asset classes that have high short term risk

of loss.

Our clients also should take a very small proportion

for high risk asset which are 2% for small cap and

1% for risky assets. This in return can contribute

to the income from the investment. We want to take a

precaution action since the investor is not a risk

averse. This is the right proportion to invest in

risky assets.

BWFNN3033 Portfolio Management

31

Reference:

Akhbar, Siaran.(2014, April 10). Monetary and Financial

Developments. Retrieved from:

http://www.bnm.gov.my/files/publication/msb/2014/3/i_en.p

df

Malaysia Business Advisory. (2014). Malaysia Economy 2014.

Retrieved from: http://malaysiabizadvisory.com/malaysia-

economy-2014/

Suzy. (2014, January 28). Malaysian Economic Outlook. Retrieved

from: http://www.mier.org.my/outlook/

Vinals, Jose., Singh, Anoop.(2013, January 28). Financial

System Stability Assessment. Retrieved from

https://www.imf.org/external/pubs/ft/scr/2013/cr1352.pdf

BWFNN3033 Portfolio Management

32