Embed Size (px)

Citation preview

Integrating small farmers into GVCs:

Confronting concentration in the cocoa sector

Yanchun Zhang

Chief, CPIOSSpecial Unit on Commodities

UNCTAD

Trade and Development Board, sixty-third session

5 December 2016

• Gayi S and Tsowou K (2016). Cocoa industry:

Integrating small farmers into the global value

chain. UNCTAD/SUC/2015/4, New York and

Geneva.

• UNCTAD (2016). Agricultural commodity value

chains: The effects of market concentration on

farmers and producing countries – the case of

cocoa. TD/B/63/2.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

This presentation draws from two recentUNCTAD papers on this topic:

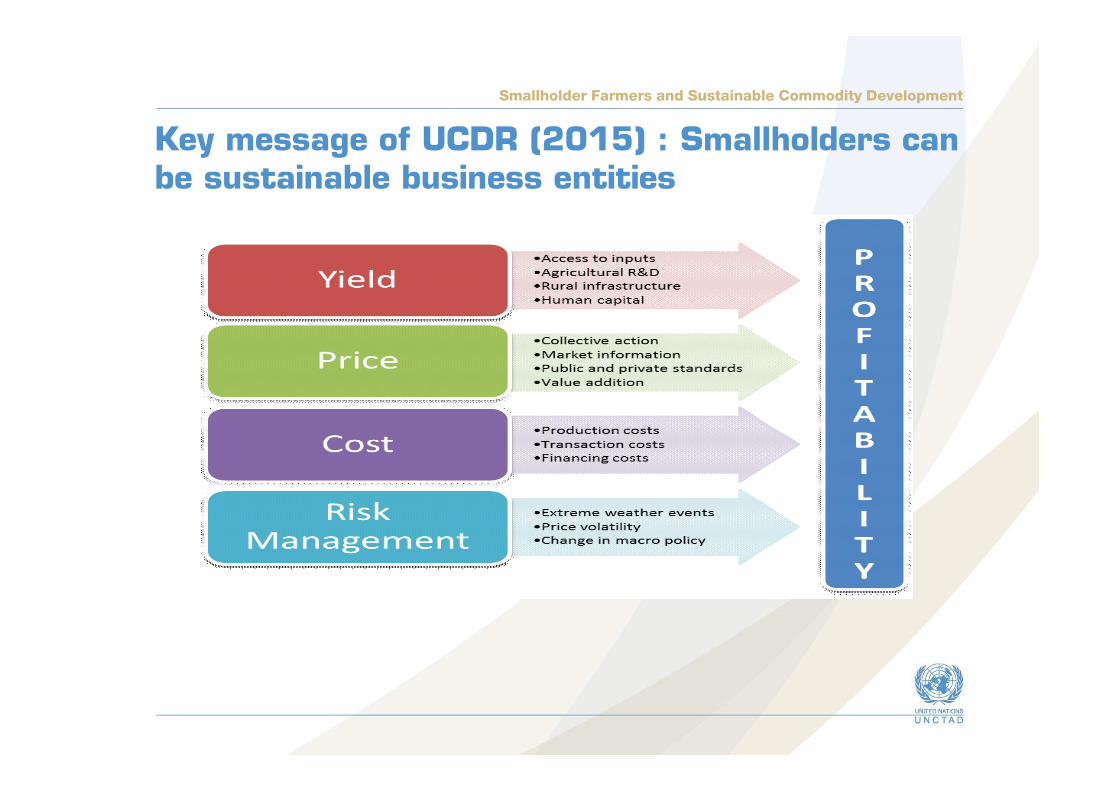

Smallholder Farmers and Sustainable Commodity Development

Key message of UCDR (2015) : Smallholders can be sustainable business entities

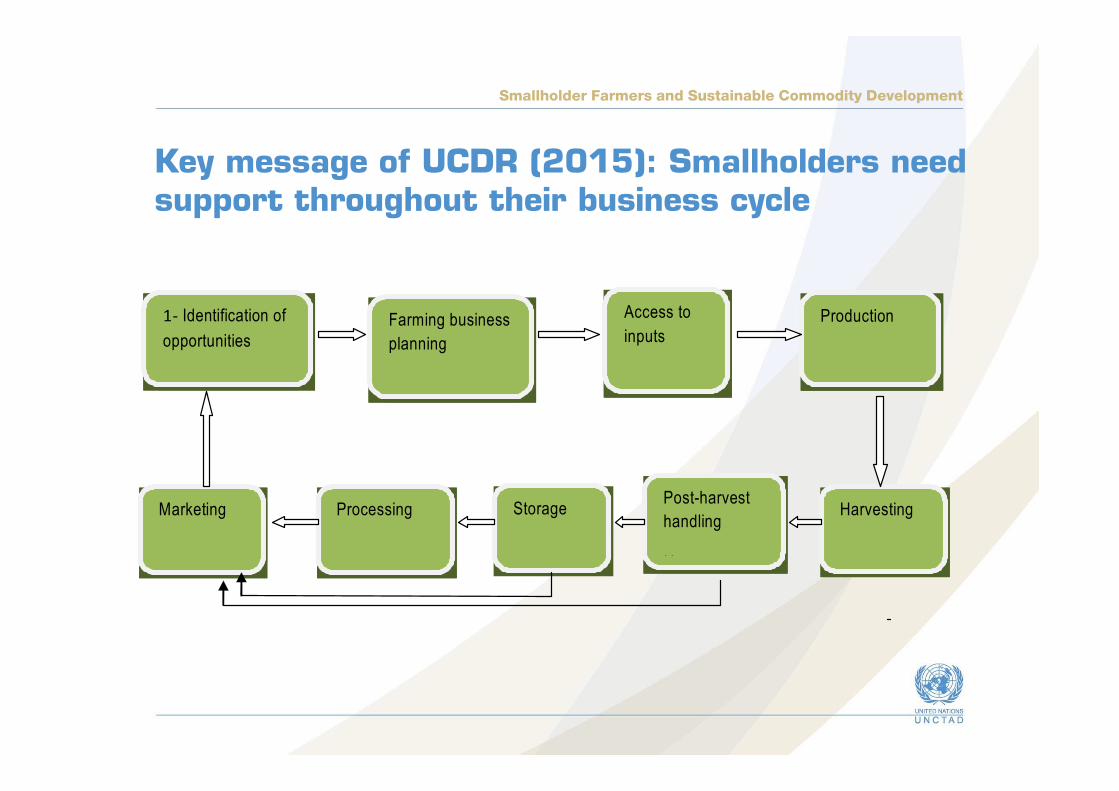

Smallholder Farmers and Sustainable Commodity Development

Key message of UCDR (2015): Smallholders need support throughout their business cycle

1- Identification of

opportunities

Access to

inputs Production

Harvesting Storage Marketing Processing

Farming business

planning

Post-harvest

handling

Harvest

• The concentration of the cocoa sector

• Sector-level consequences of concentration

• Impacts on farmers

• Policy recommendations

Outline of presentation

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

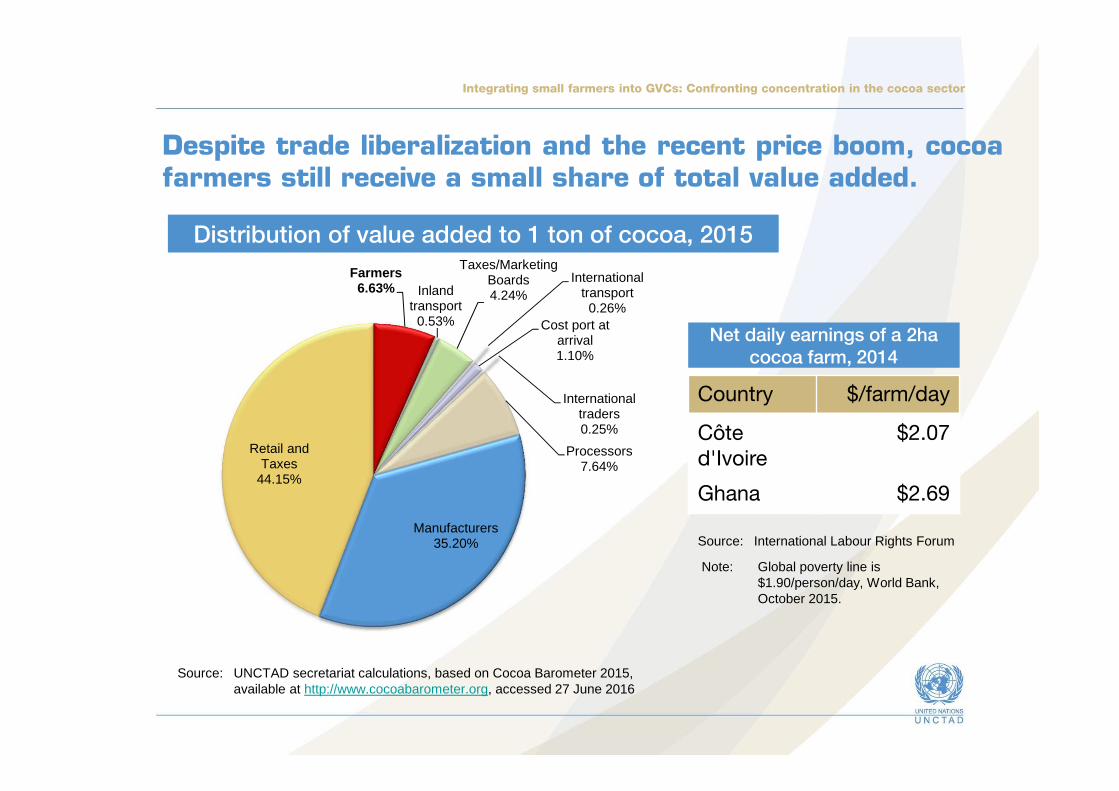

Despite trade liberalization and the recent price boom, cocoafarmers still receive a small share of total value added.

Farmers6.63% Inland

transport0.53%

Taxes/Marketing Boards4.24%

International transport0.26%

Cost port at arrival1.10%

International traders0.25%

Processors7.64%

Manufacturers35.20%

Retail and Taxes

44.15%

Distribution of value added to 1 ton of cocoa, 2015

Source: UNCTAD secretariat calculations, based on Cocoa Barometer 2015, available at http://www.cocoabarometer.org, accessed 27 June 2016

Country $/farm/day

Côte d'Ivoire

$2.07

Ghana $2.69

Net daily earnings of a 2ha

cocoa farm, 2014

Source: International Labour Rights Forum

Note: Global poverty line is $1.90/person/day, World Bank, October 2015.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

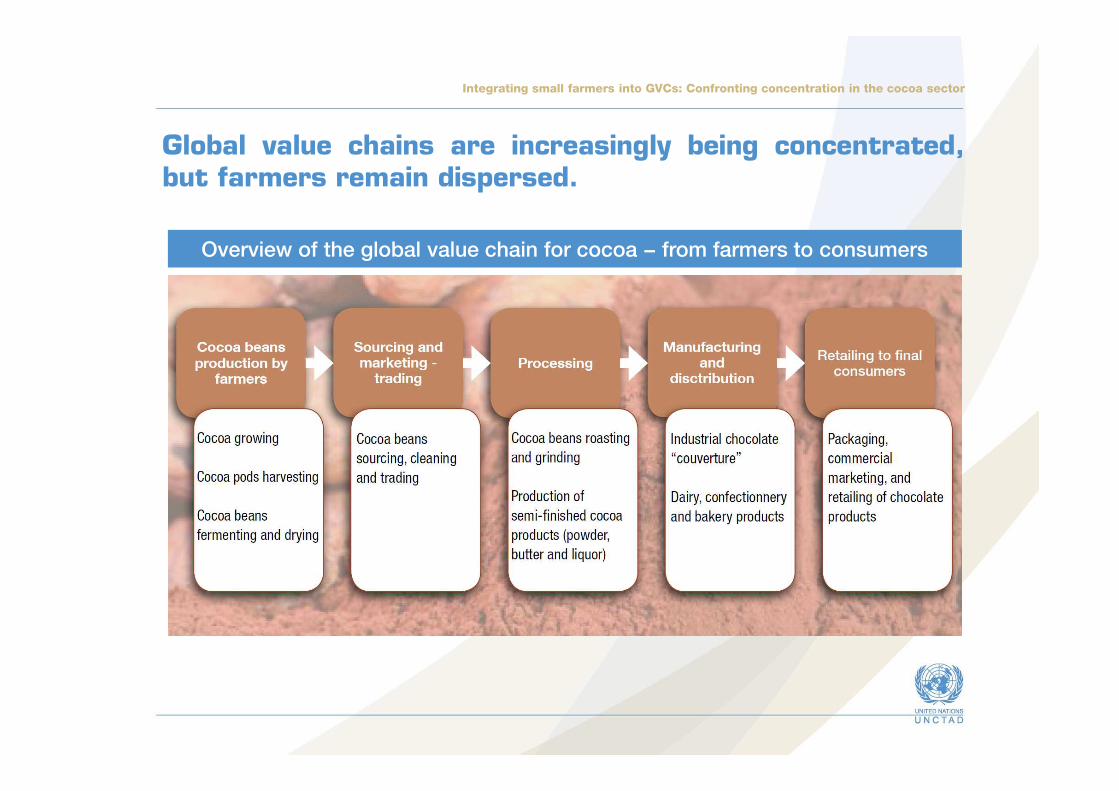

Global value chains are increasingly being concentrated,but farmers remain dispersed.

Overview of the global value chain for cocoa − from farmers to consumers

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

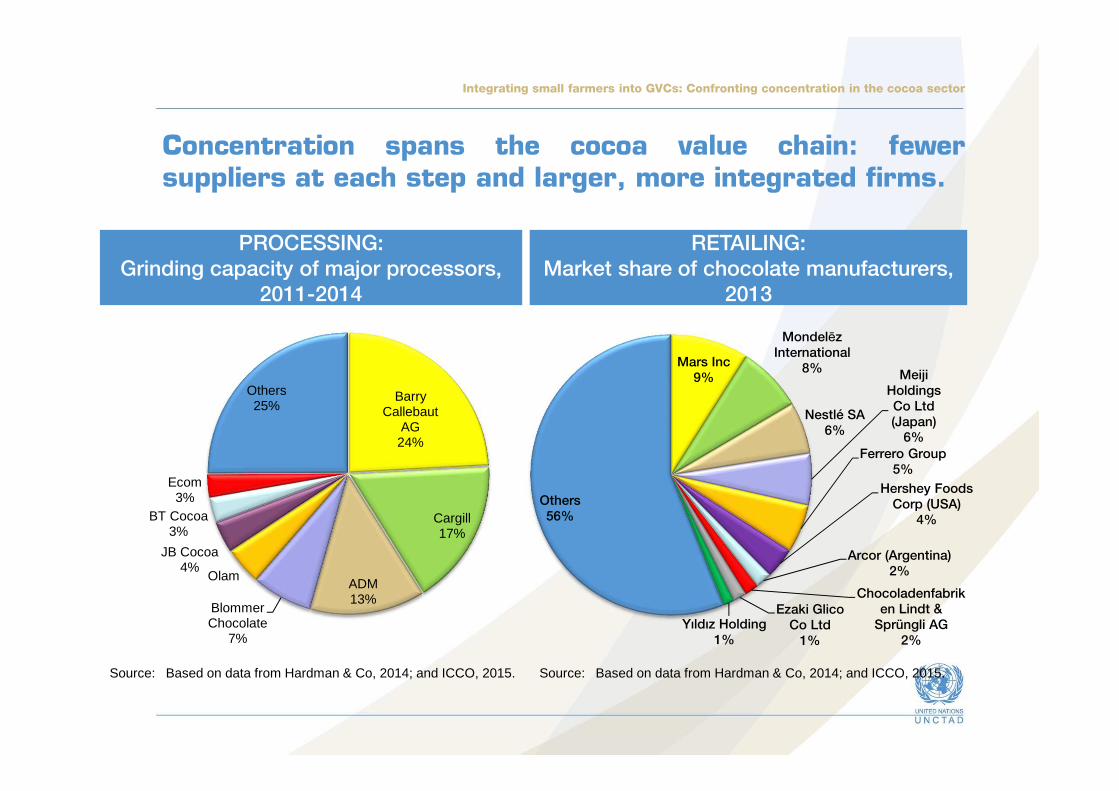

Concentration spans the cocoa value chain: fewersuppliers at each step and larger, more integrated firms.

Barry Callebaut

AG24%

Cargill17%

ADM13%

BlommerChocolate

7%

Olam

JB Cocoa4%

BT Cocoa3%

Ecom3%

Others25%

PROCESSING:

Grinding capacity of major processors,

2011-2014

Source: Based on data from Hardman & Co, 2014; and ICCO, 2015.

Mars Inc

9%

Mondelēz

International

8%

Nestlé SA

6%

Meiji

Holdings

Co Ltd

(Japan)6%

Ferrero Group

5%

Hershey Foods

Corp (USA)

4%

Arcor (Argentina)

2%

Chocoladenfabrik

en Lindt &

Sprüngli AG

2%

Ezaki Glico

Co Ltd

1%

Yıldız Holding

1%

Others

56%

RETAILING:

Market share of chocolate manufacturers,

2013

Source: Based on data from Hardman & Co, 2014; and ICCO, 2015.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

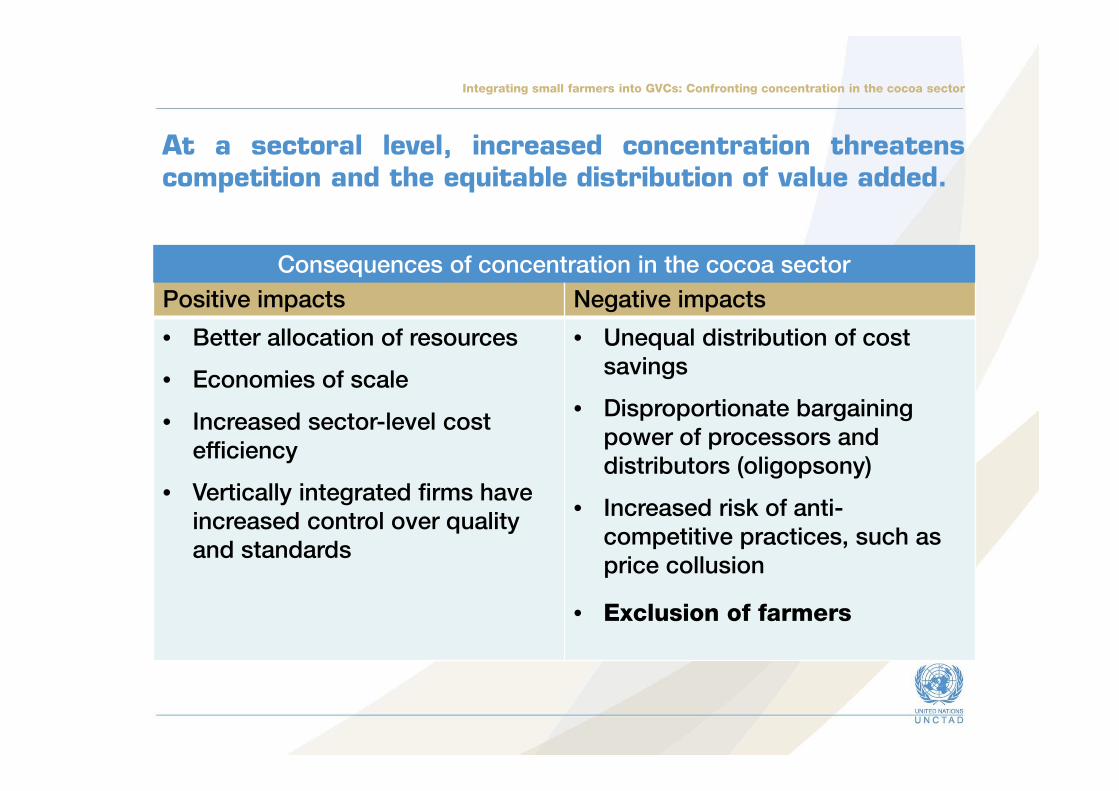

At a sectoral level, increased concentration threatenscompetition and the equitable distribution of value added.

Positive impacts Negative impacts

• Better allocation of resources

• Economies of scale

• Increased sector-level cost

efficiency

• Vertically integrated firms have

increased control over quality

and standards

• Unequal distribution of cost

savings

• Disproportionate bargaining

power of processors and

distributors (oligopsony)

• Increased risk of anti-

competitive practices, such as

price collusion

• Exclusion of farmers

Consequences of concentration in the cocoa sector

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

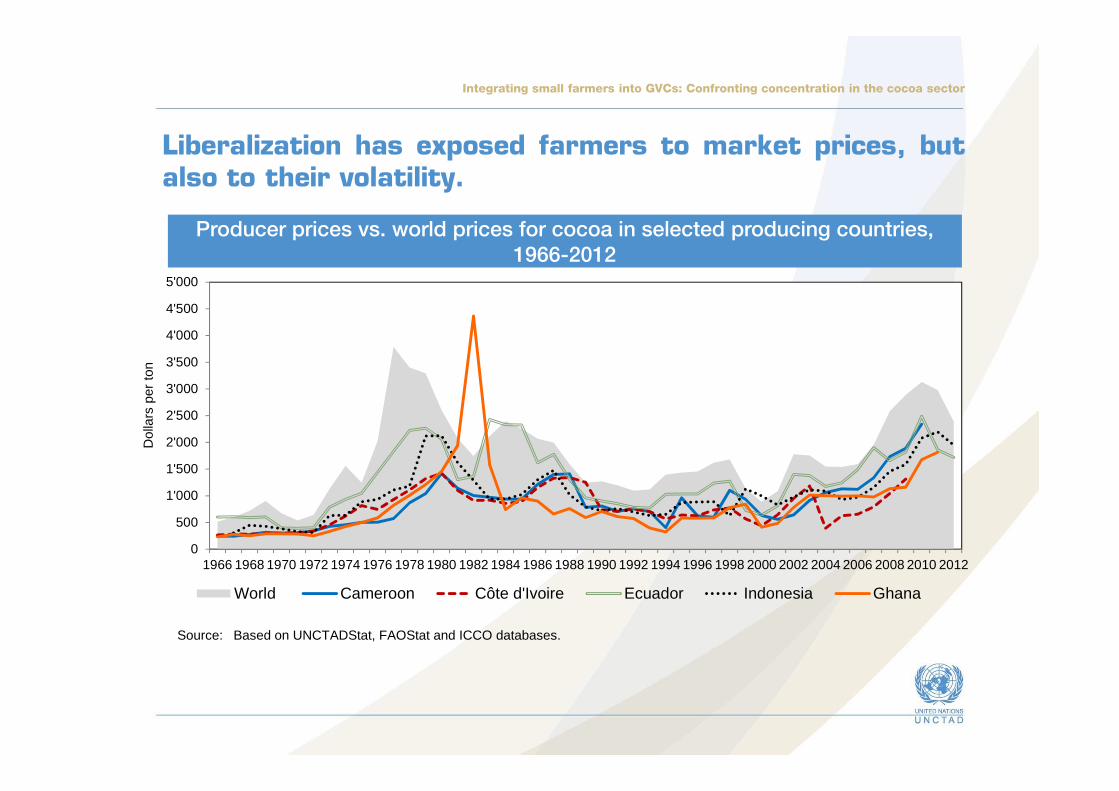

Liberalization has exposed farmers to market prices, butalso to their volatility.

0

500

1'000

1'500

2'000

2'500

3'000

3'500

4'000

4'500

5'000

1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Dol

lars

per

ton

World Cameroon Côte d'Ivoire Ecuador Indonesia Ghana

Producer prices vs. world prices for cocoa in selected producing countries,

1966-2012

Source: Based on UNCTADStat, FAOStat and ICCO databases.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

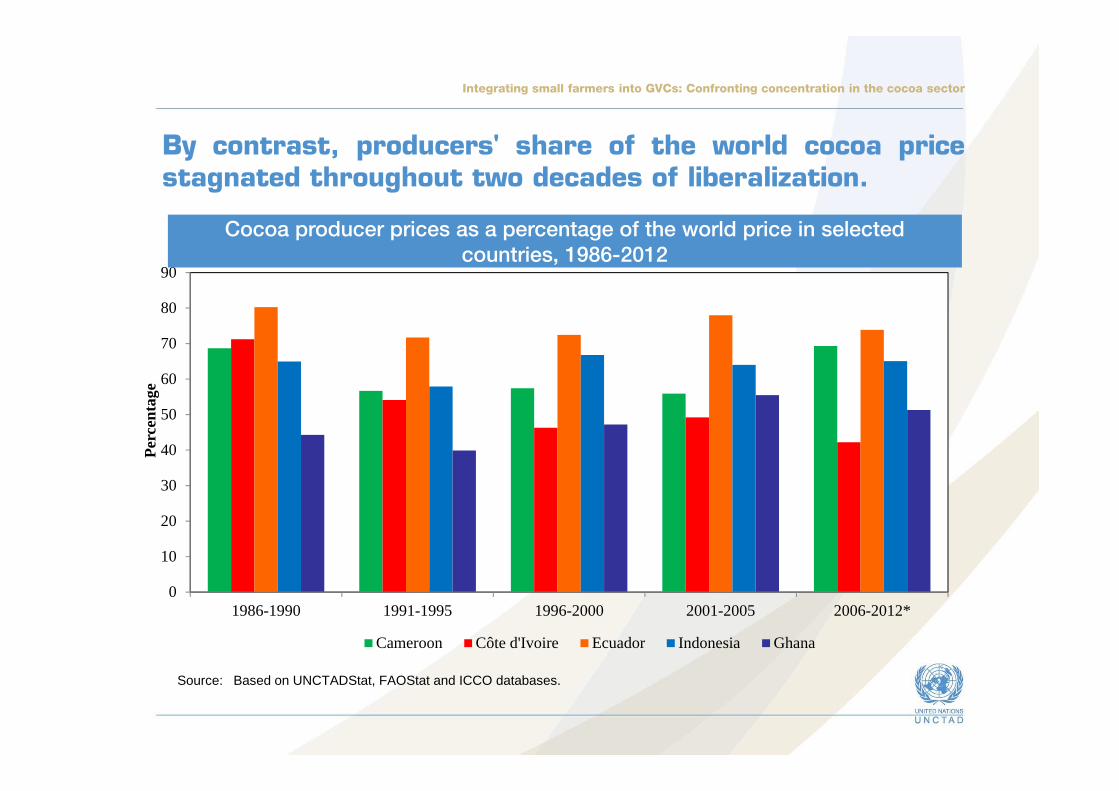

By contrast, producers' share of the world cocoa pricestagnated throughout two decades of liberalization.

0

10

20

30

40

50

60

70

80

90

1986-1990 1991-1995 1996-2000 2001-2005 2006-2012*

Per

cent

age

Cameroon Côte d'Ivoire Ecuador Indonesia Ghana

Cocoa producer prices as a percentage of the world price in selected

countries, 1986-2012

Source: Based on UNCTADStat, FAOStat and ICCO databases.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

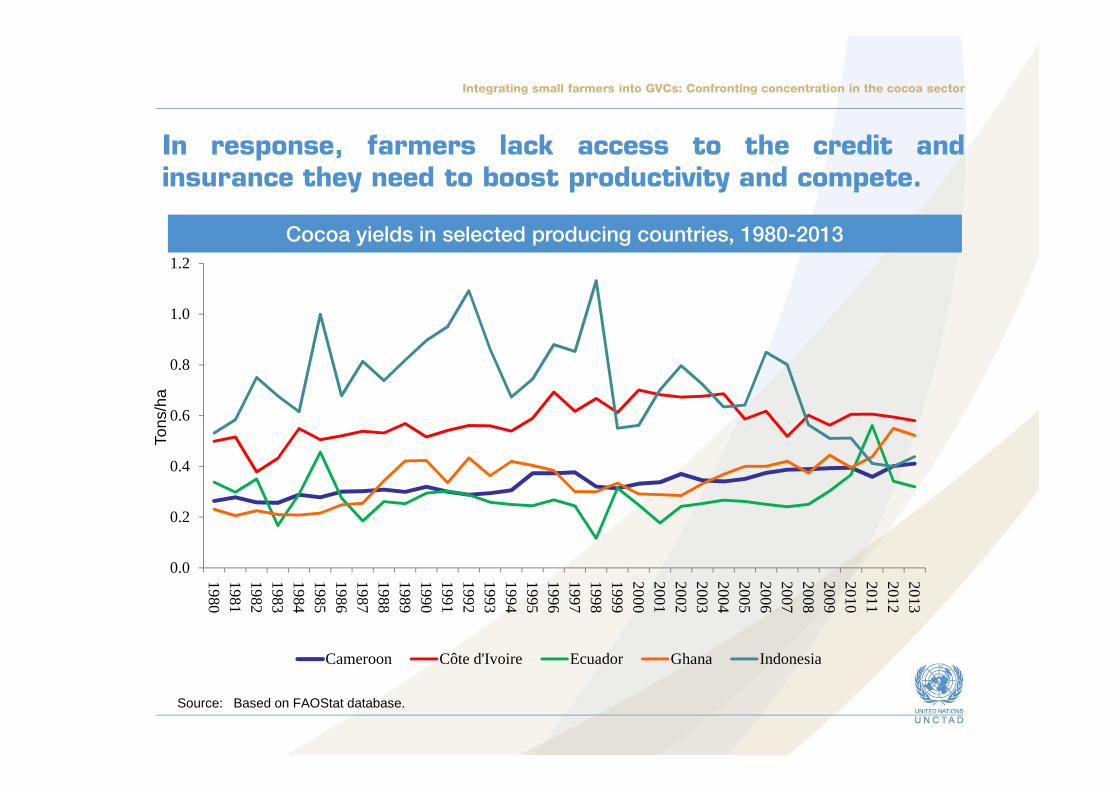

In response, farmers lack access to the credit andinsurance they need to boost productivity and compete.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Cameroon Côte d'Ivoire Ecuador Ghana Indonesia

Tons

/ha

Cocoa yields in selected producing countries, 1980-2013

Source: Based on FAOStat database.

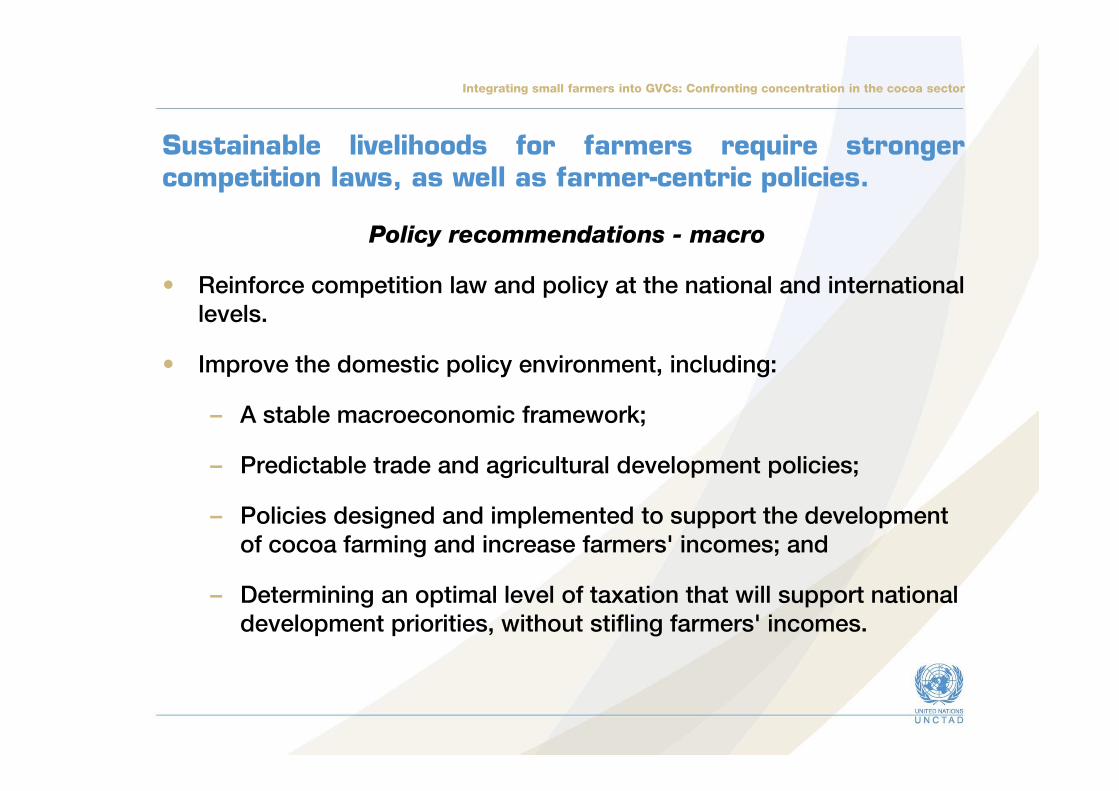

Policy recommendations - macro

• Reinforce competition law and policy at the national and international

levels.

• Improve the domestic policy environment, including:

– A stable macroeconomic framework;

– Predictable trade and agricultural development policies;

– Policies designed and implemented to support the development

of cocoa farming and increase farmers' incomes; and

– Determining an optimal level of taxation that will support national

development priorities, without stifling farmers' incomes.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

Sustainable livelihoods for farmers require strongercompetition laws, as well as farmer-centric policies.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

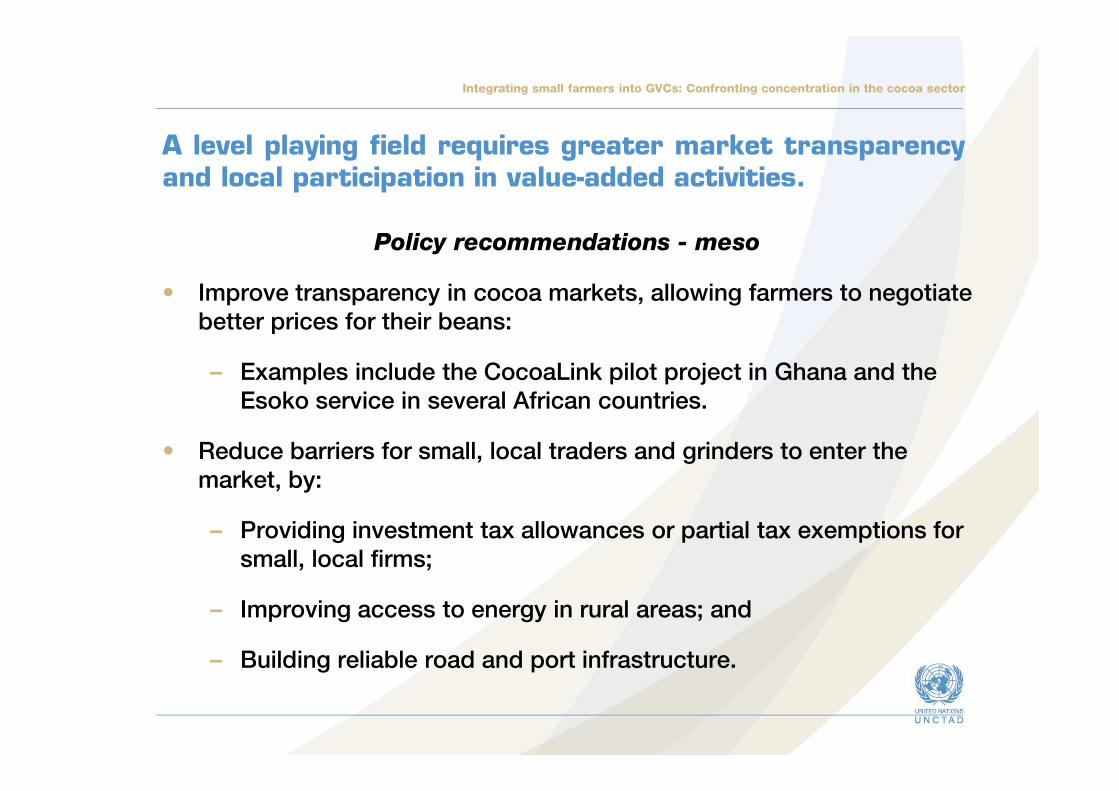

A level playing field requires greater market transparencyand local participation in value-added activities.

Policy recommendations - meso

• Improve transparency in cocoa markets, allowing farmers to negotiate

better prices for their beans:

– Examples include the CocoaLink pilot project in Ghana and the

Esoko service in several African countries.

• Reduce barriers for small, local traders and grinders to enter the

market, by:

– Providing investment tax allowances or partial tax exemptions for

small, local firms;

– Improving access to energy in rural areas; and

– Building reliable road and port infrastructure.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

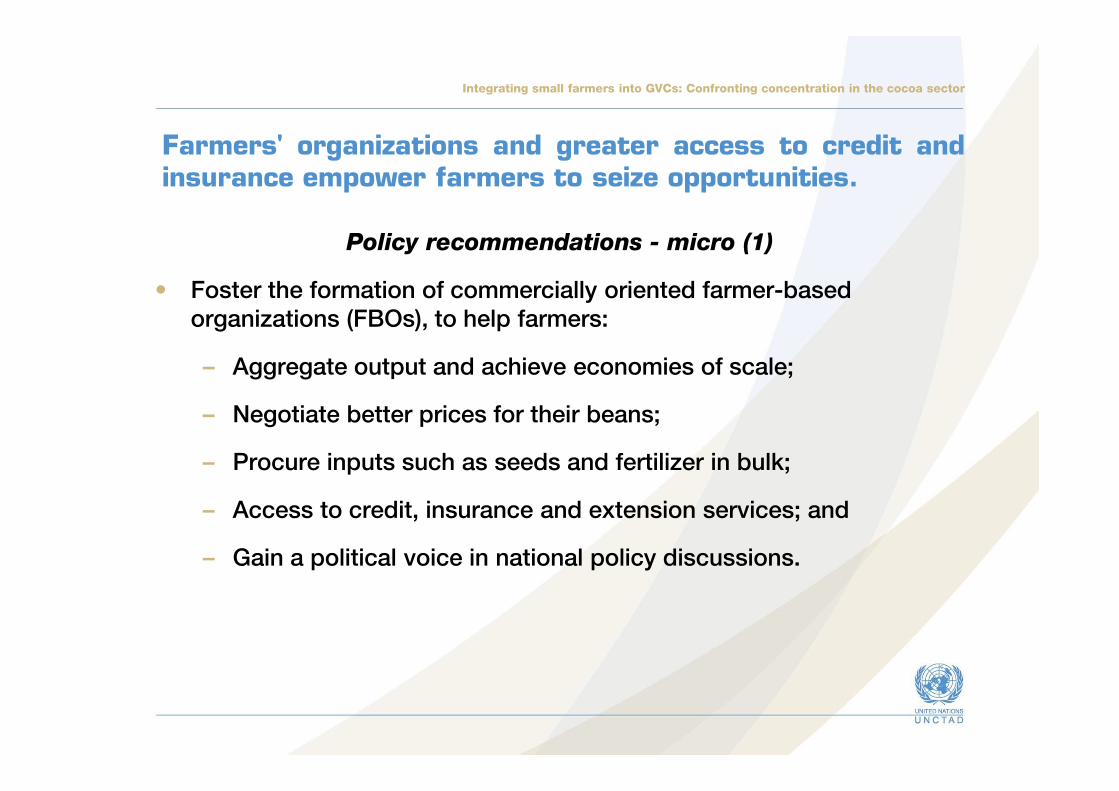

Farmers' organizations and greater access to credit andinsurance empower farmers to seize opportunities.

Policy recommendations - micro (1)

• Foster the formation of commercially oriented farmer-based

organizations (FBOs), to help farmers:

– Aggregate output and achieve economies of scale;

– Negotiate better prices for their beans;

– Procure inputs such as seeds and fertilizer in bulk;

– Access to credit, insurance and extension services; and

– Gain a political voice in national policy discussions.

Integrating small farmers into GVCs: Confronting concentration in the cocoa sector

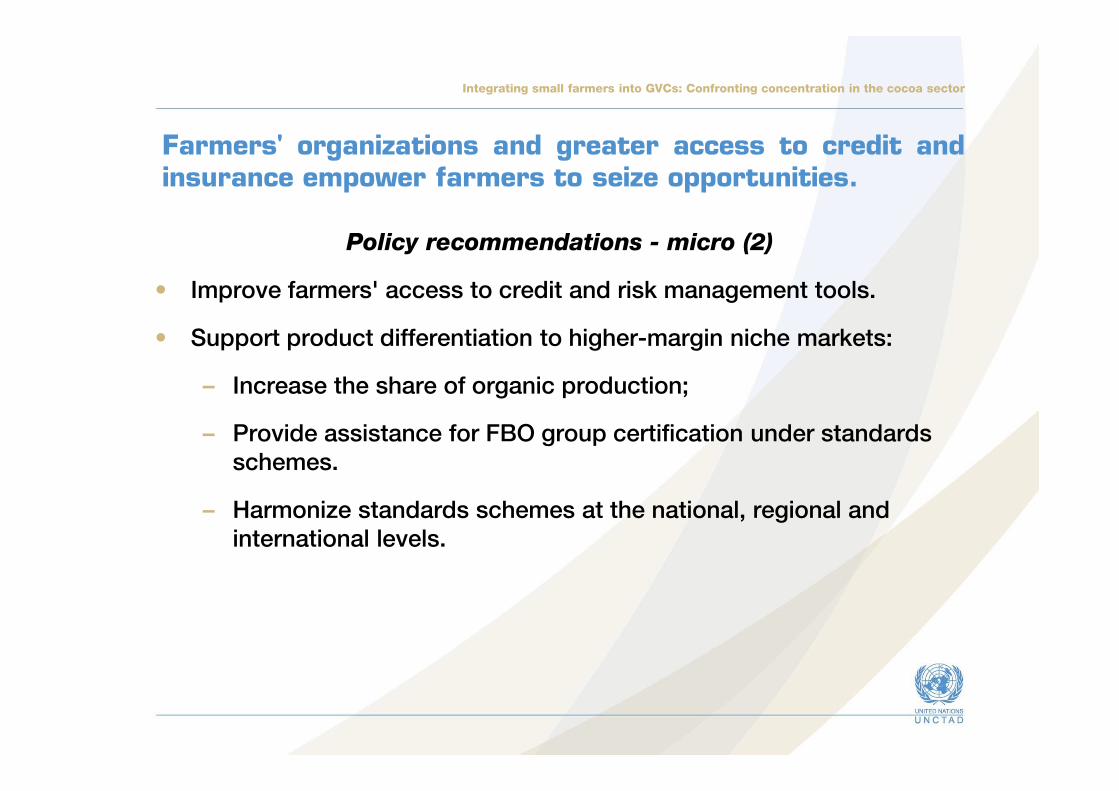

Farmers' organizations and greater access to credit andinsurance empower farmers to seize opportunities.

Policy recommendations - micro (2)

• Improve farmers' access to credit and risk management tools.

• Support product differentiation to higher-margin niche markets:

– Increase the share of organic production;

– Provide assistance for FBO group certification under standards

schemes.

– Harmonize standards schemes at the national, regional and

international levels.