Embed Size (px)

Citation preview

INSURANCE BROKER LIABILITY

Robert D. Chesler, Esq. Anderson Kill, PC (Newark) Adam Cantor, Esq. Senior Vice President- Northeast Region Willis Towers Watson

Willis Americas Administration (Short Hills)

Thomas F. Quinn, Esq. Wilson Elser Moskowitz Edelman & Dicker, LLP (Newark)

W381000W6

© 2016 New Jersey State Bar Association. All rights reserved. Any copying of material herein, in whole or in part, and by any means without written permission is prohibited. Requests for such permission should be sent to NJICLE, a Division of the New Jersey State Bar Association, New Jersey Law Center, One Constitution Square, New Brunswick, New Jersey 08901-1520.

Thank you for logging in – the webinar will begin shortly.

1. All Attendee phone lines are muted. 2. Questions may be submitted

Via Chat on the right hand side of your screen. Questions will be answered periodically during the

presentation

Note: Attendees with dial up connections will see a slower response.

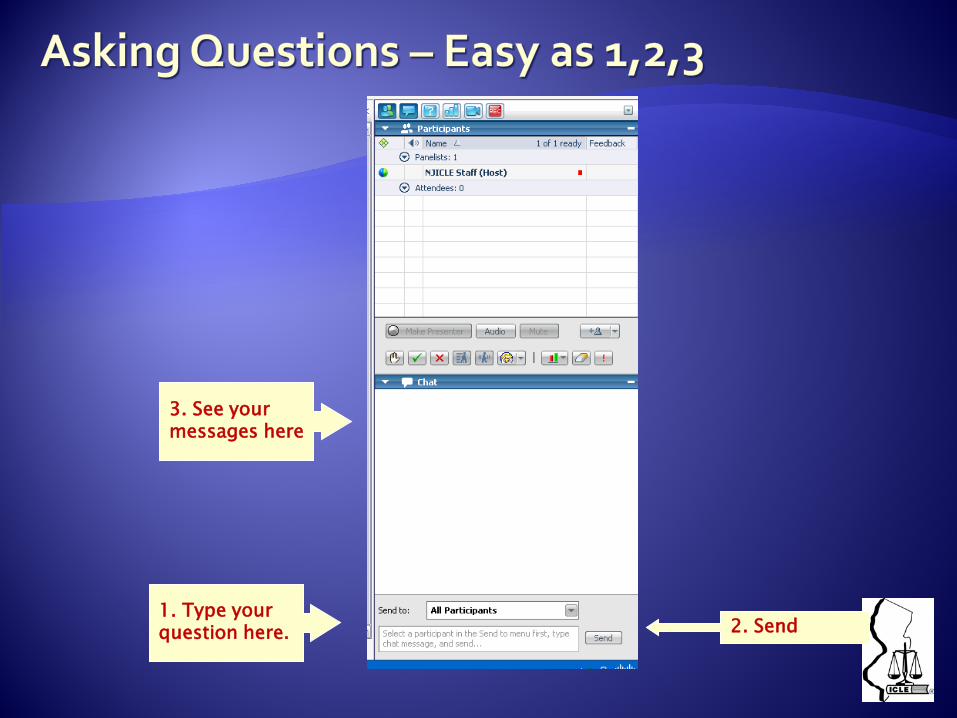

1. Type your question here.

3. See your messages here

2. Send

PLEASE FAX OR E-MAIL YOUR ATTENDANCE VERIFICATION FORM TO NJ ICLE

FAX: 732-249-1428

E-MAIL: [email protected]

TO ACCESS SEMINAR MATERIALS, ATTENDANCE VERIFICATION AND CLE FORMS

PLEASE GO TO:

http://tcms.njsba.com/personifyebusiness/njicle/WebinarInformation.aspx

NJICLE WEBINAR

February 25,2016 12 pm – 1:40 pm

Presenter: Robert D. Chesler, Esq. (973) 642-5864 [email protected]

Insurance Broker Liability

7 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

DISCLAIMER The views expressed by the participants in this program are not those of the participants’ employers, their clients, or any other organization. The opinions expressed do not constitute legal advice, or risk management advice. The views discussed are for educational purposes only, and provided only for use during this session.

8 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

OVERVIEW 1. The inherent Tensions in the Relationship Between

the Broker, the Insured, the Insurance Coverage Lawyer and the Insurance Claims Handler.

9 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

OVERVIEW 2. Circumstances Creating Perils for Brokers in the

Context of Coverage Disputes

10 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

OVERVIEW 3. Issues that are Emerging in Regards to the Role of the

Broker in Coverage Disputes.

11 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

OVERVIEW 4. How Brokers, Insureds and Insurers Should React to

Today's Realities.

12 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

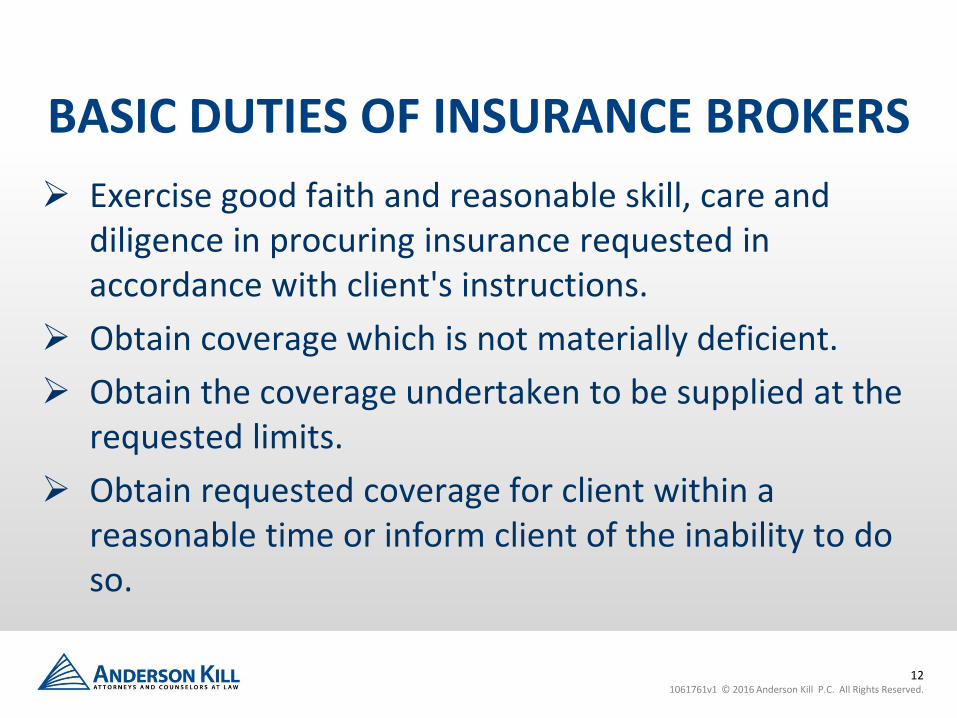

BASIC DUTIES OF INSURANCE BROKERS Exercise good faith and reasonable skill, care and

diligence in procuring insurance requested in accordance with client's instructions.

Obtain coverage which is not materially deficient. Obtain the coverage undertaken to be supplied at the

requested limits. Obtain requested coverage for client within a

reasonable time or inform client of the inability to do so.

13 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

CLAIMS BY POLICYHOLDERS AGAINST INSURANCE BROKERS

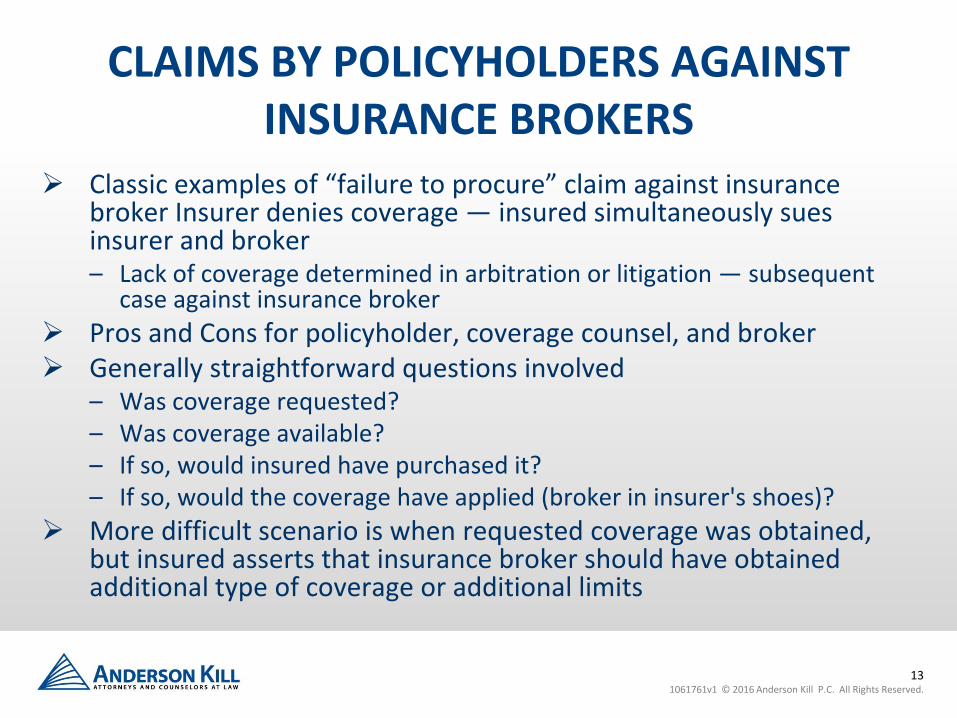

Classic examples of “failure to procure” claim against insurance broker Insurer denies coverage — insured simultaneously sues insurer and broker – Lack of coverage determined in arbitration or litigation — subsequent

case against insurance broker Pros and Cons for policyholder, coverage counsel, and broker Generally straightforward questions involved

– Was coverage requested? – Was coverage available? – If so, would insured have purchased it? – If so, would the coverage have applied (broker in insurer's shoes)?

More difficult scenario is when requested coverage was obtained, but insured asserts that insurance broker should have obtained additional type of coverage or additional limits

14 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

GENERAL DUTIES IMPOSED ON BROKERS ARE LIMITED

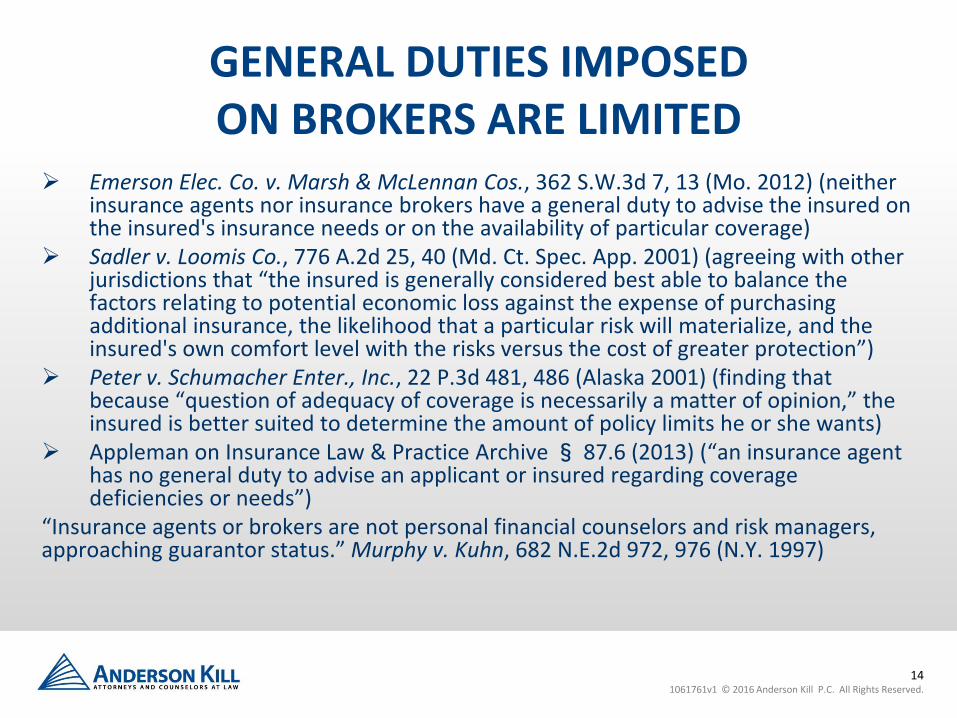

Emerson Elec. Co. v. Marsh & McLennan Cos., 362 S.W.3d 7, 13 (Mo. 2012) (neither insurance agents nor insurance brokers have a general duty to advise the insured on the insured's insurance needs or on the availability of particular coverage)

Sadler v. Loomis Co., 776 A.2d 25, 40 (Md. Ct. Spec. App. 2001) (agreeing with other jurisdictions that “the insured is generally considered best able to balance the factors relating to potential economic loss against the expense of purchasing additional insurance, the likelihood that a particular risk will materialize, and the insured's own comfort level with the risks versus the cost of greater protection”)

Peter v. Schumacher Enter., Inc., 22 P.3d 481, 486 (Alaska 2001) (finding that because “question of adequacy of coverage is necessarily a matter of opinion,” the insured is better suited to determine the amount of policy limits he or she wants)

Appleman on Insurance Law & Practice Archive § 87.6 (2013) (“an insurance agent has no general duty to advise an applicant or insured regarding coverage deficiencies or needs”)

“Insurance agents or brokers are not personal financial counselors and risk managers, approaching guarantor status.” Murphy v. Kuhn, 682 N.E.2d 972, 976 (N.Y. 1997)

15 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

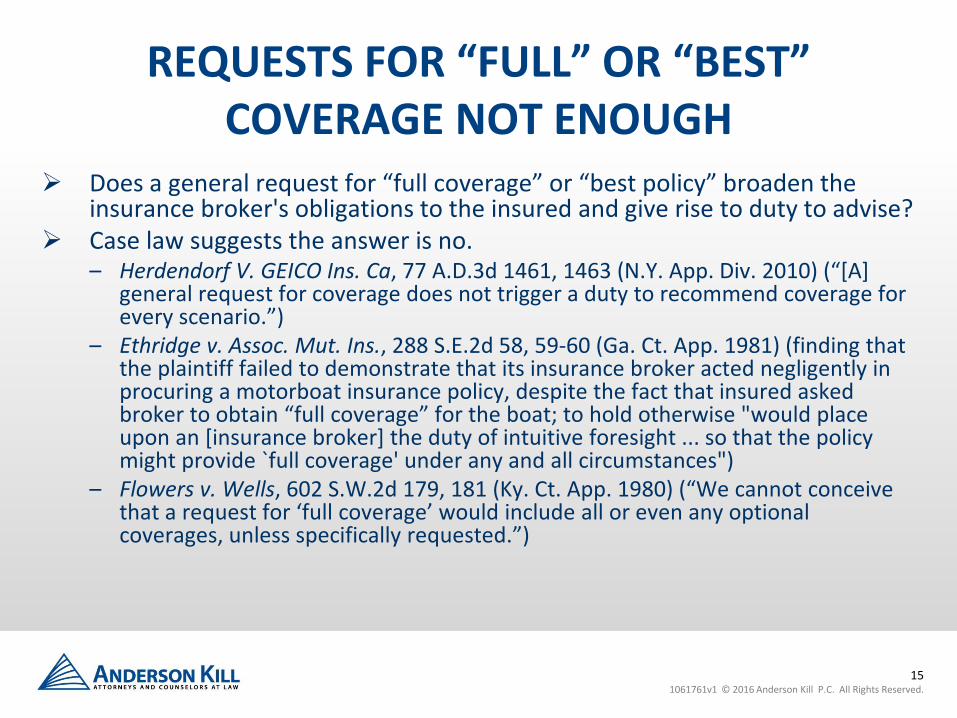

REQUESTS FOR “FULL” OR “BEST” COVERAGE NOT ENOUGH

Does a general request for “full coverage” or “best policy” broaden the insurance broker's obligations to the insured and give rise to duty to advise?

Case law suggests the answer is no. – Herdendorf V. GEICO Ins. Ca, 77 A.D.3d 1461, 1463 (N.Y. App. Div. 2010) (“[A]

general request for coverage does not trigger a duty to recommend coverage for every scenario.”)

– Ethridge v. Assoc. Mut. Ins., 288 S.E.2d 58, 59-60 (Ga. Ct. App. 1981) (finding that the plaintiff failed to demonstrate that its insurance broker acted negligently in procuring a motorboat insurance policy, despite the fact that insured asked broker to obtain “full coverage” for the boat; to hold otherwise "would place upon an [insurance broker] the duty of intuitive foresight ... so that the policy might provide `full coverage' under any and all circumstances")

– Flowers v. Wells, 602 S.W.2d 179, 181 (Ky. Ct. App. 1980) (“We cannot conceive that a request for ‘full coverage’ would include all or even any optional coverages, unless specifically requested.”)

16 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

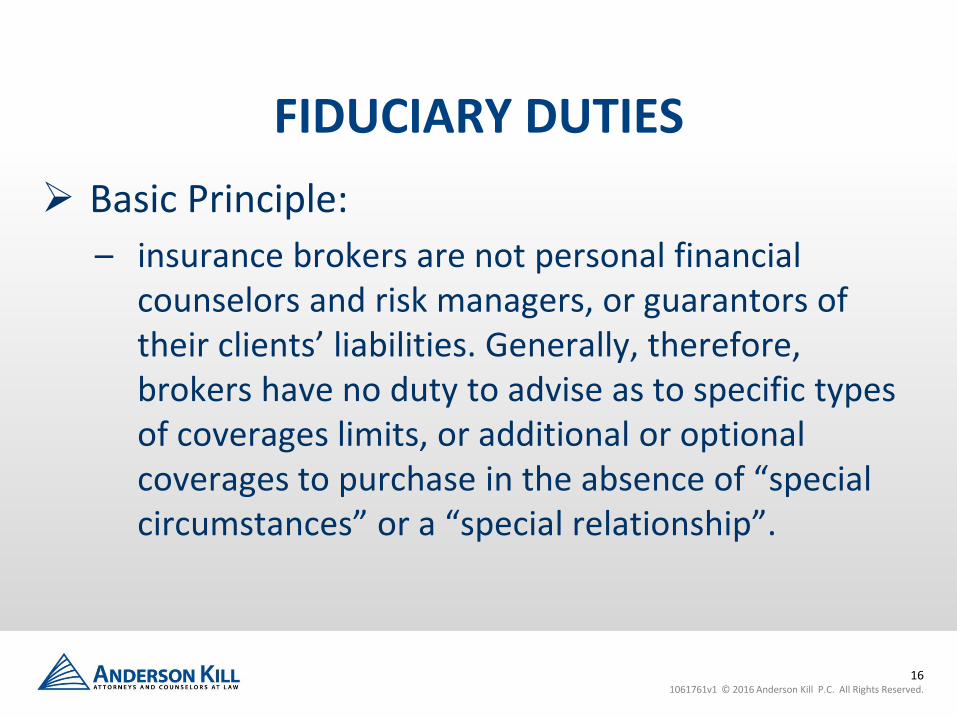

FIDUCIARY DUTIES Basic Principle:

– insurance brokers are not personal financial counselors and risk managers, or guarantors of their clients’ liabilities. Generally, therefore, brokers have no duty to advise as to specific types of coverages limits, or additional or optional coverages to purchase in the absence of “special circumstances” or a “special relationship”.

17 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

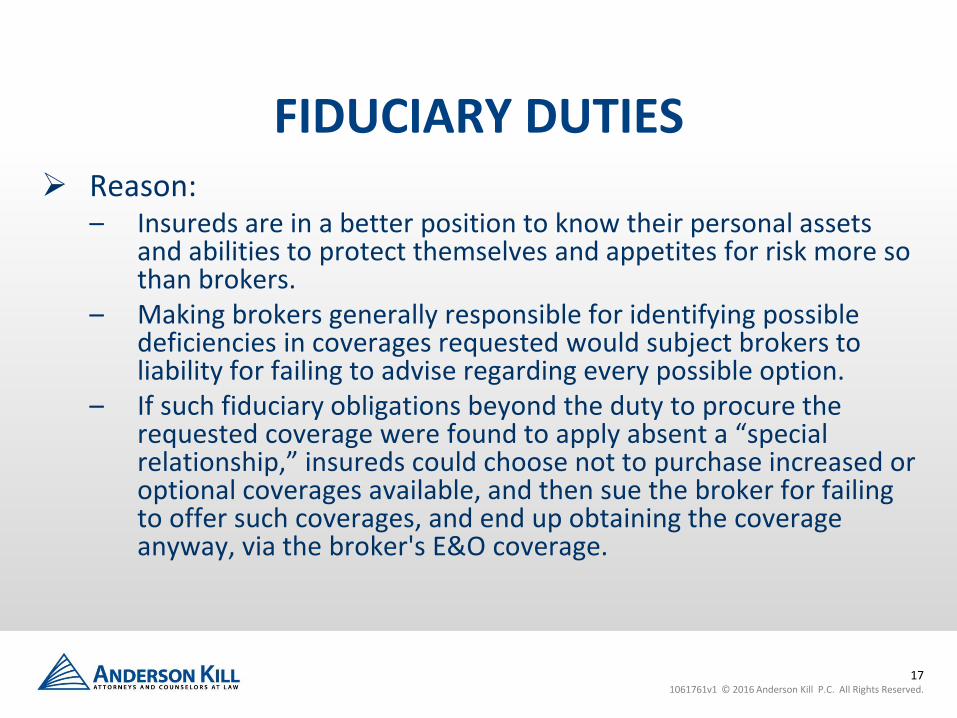

FIDUCIARY DUTIES Reason:

– Insureds are in a better position to know their personal assets and abilities to protect themselves and appetites for risk more so than brokers.

– Making brokers generally responsible for identifying possible deficiencies in coverages requested would subject brokers to liability for failing to advise regarding every possible option.

– If such fiduciary obligations beyond the duty to procure the requested coverage were found to apply absent a “special relationship,” insureds could choose not to purchase increased or optional coverages available, and then sue the broker for failing to offer such coverages, and end up obtaining the coverage anyway, via the broker's E&O coverage.

18 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

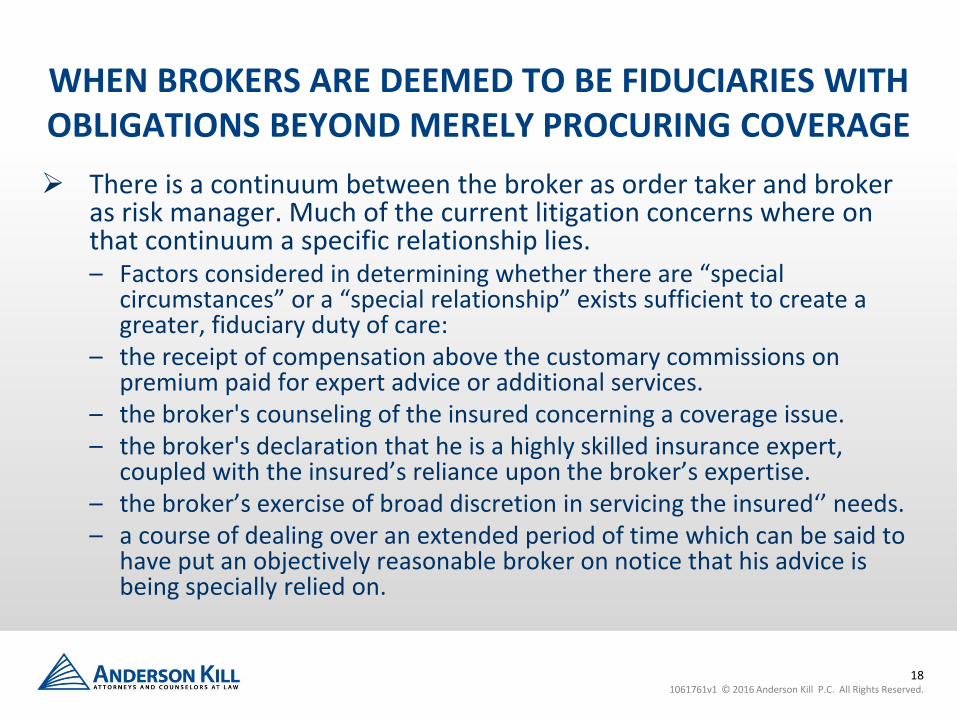

WHEN BROKERS ARE DEEMED TO BE FIDUCIARIES WITH OBLIGATIONS BEYOND MERELY PROCURING COVERAGE There is a continuum between the broker as order taker and broker

as risk manager. Much of the current litigation concerns where on that continuum a specific relationship lies. – Factors considered in determining whether there are “special

circumstances” or a “special relationship” exists sufficient to create a greater, fiduciary duty of care:

– the receipt of compensation above the customary commissions on premium paid for expert advice or additional services.

– the broker's counseling of the insured concerning a coverage issue. – the broker's declaration that he is a highly skilled insurance expert,

coupled with the insured’s reliance upon the broker’s expertise. – the broker’s exercise of broad discretion in servicing the insured‘’ needs. – a course of dealing over an extended period of time which can be said to

have put an objectively reasonable broker on notice that his advice is being specially relied on.

19 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

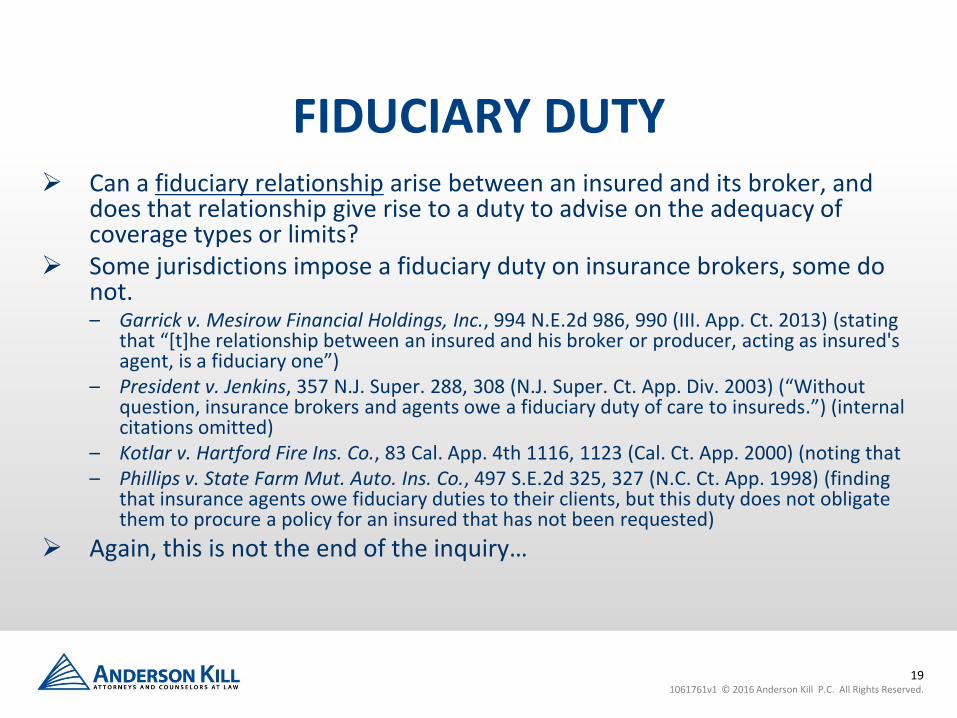

FIDUCIARY DUTY Can a fiduciary relationship arise between an insured and its broker, and

does that relationship give rise to a duty to advise on the adequacy of coverage types or limits?

Some jurisdictions impose a fiduciary duty on insurance brokers, some do not. – Garrick v. Mesirow Financial Holdings, Inc., 994 N.E.2d 986, 990 (III. App. Ct. 2013) (stating

that “[t]he relationship between an insured and his broker or producer, acting as insured's agent, is a fiduciary one”)

– President v. Jenkins, 357 N.J. Super. 288, 308 (N.J. Super. Ct. App. Div. 2003) (“Without question, insurance brokers and agents owe a fiduciary duty of care to insureds.”) (internal citations omitted)

– Kotlar v. Hartford Fire Ins. Co., 83 Cal. App. 4th 1116, 1123 (Cal. Ct. App. 2000) (noting that – Phillips v. State Farm Mut. Auto. Ins. Co., 497 S.E.2d 325, 327 (N.C. Ct. App. 1998) (finding

that insurance agents owe fiduciary duties to their clients, but this duty does not obligate them to procure a policy for an insured that has not been requested)

Again, this is not the end of the inquiry…

20 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

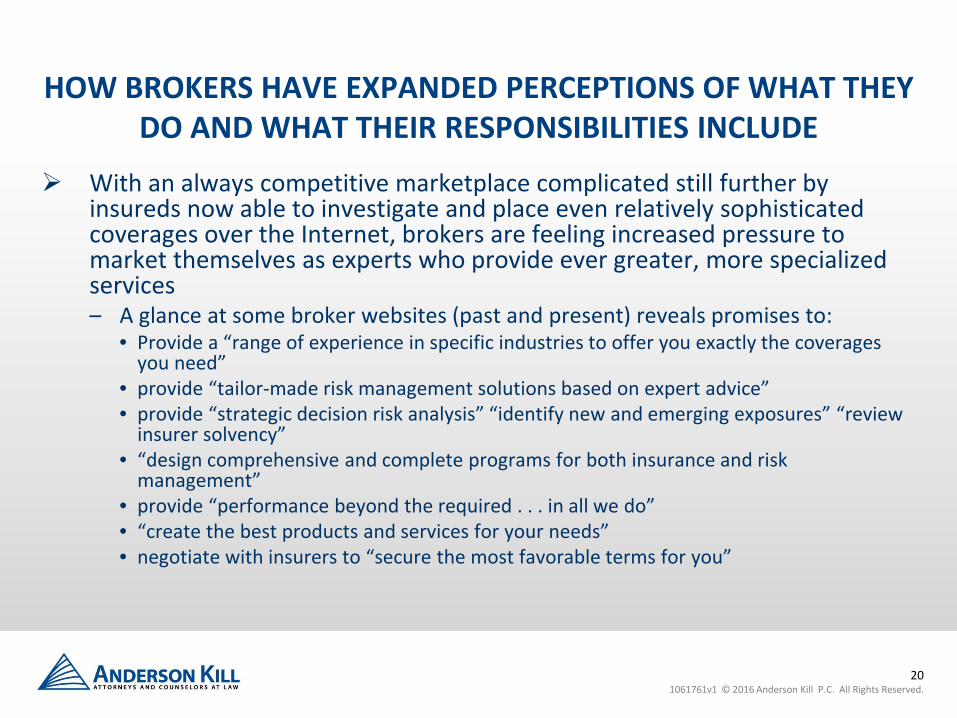

HOW BROKERS HAVE EXPANDED PERCEPTIONS OF WHAT THEY DO AND WHAT THEIR RESPONSIBILITIES INCLUDE

With an always competitive marketplace complicated still further by insureds now able to investigate and place even relatively sophisticated coverages over the Internet, brokers are feeling increased pressure to market themselves as experts who provide ever greater, more specialized services – A glance at some broker websites (past and present) reveals promises to:

• Provide a “range of experience in specific industries to offer you exactly the coverages you need”

• provide “tailor-made risk management solutions based on expert advice” • provide “strategic decision risk analysis” “identify new and emerging exposures” “review

insurer solvency” • “design comprehensive and complete programs for both insurance and risk

management” • provide “performance beyond the required . . . in all we do” • “create the best products and services for your needs” • negotiate with insurers to “secure the most favorable terms for you”

21 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

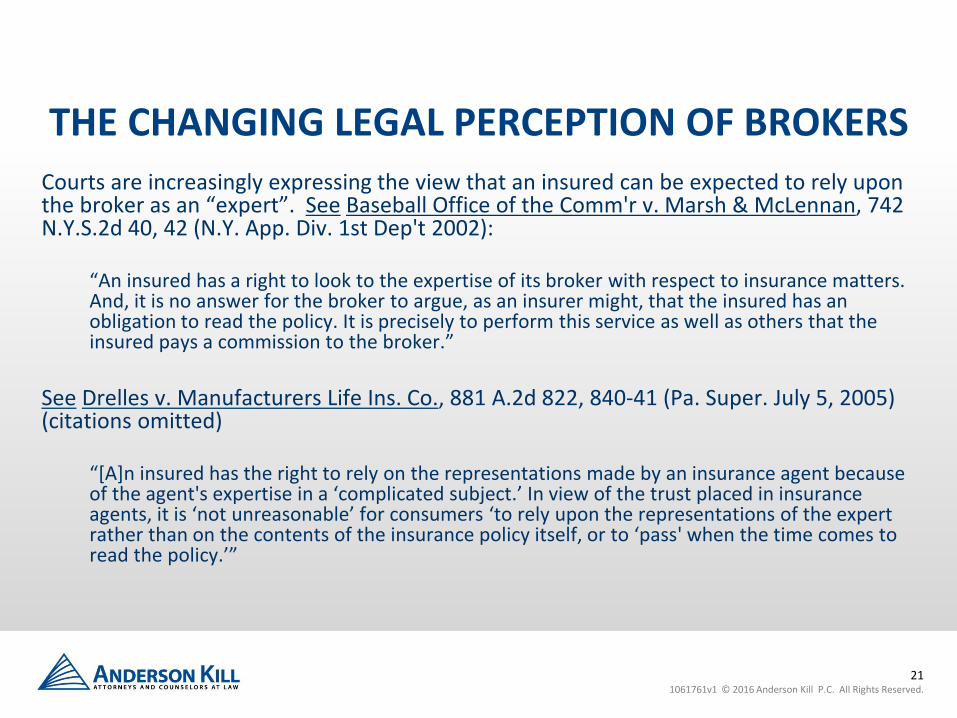

THE CHANGING LEGAL PERCEPTION OF BROKERS Courts are increasingly expressing the view that an insured can be expected to rely upon the broker as an “expert”. See Baseball Office of the Comm'r v. Marsh & McLennan, 742 N.Y.S.2d 40, 42 (N.Y. App. Div. 1st Dep't 2002):

“An insured has a right to look to the expertise of its broker with respect to insurance matters. And, it is no answer for the broker to argue, as an insurer might, that the insured has an obligation to read the policy. It is precisely to perform this service as well as others that the insured pays a commission to the broker.”

See Drelles v. Manufacturers Life Ins. Co., 881 A.2d 822, 840-41 (Pa. Super. July 5, 2005) (citations omitted)

“[A]n insured has the right to rely on the representations made by an insurance agent because of the agent's expertise in a ‘complicated subject.’ In view of the trust placed in insurance agents, it is ‘not unreasonable’ for consumers ‘to rely upon the representations of the expert rather than on the contents of the insurance policy itself, or to ‘pass' when the time comes to read the policy.’”

22 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

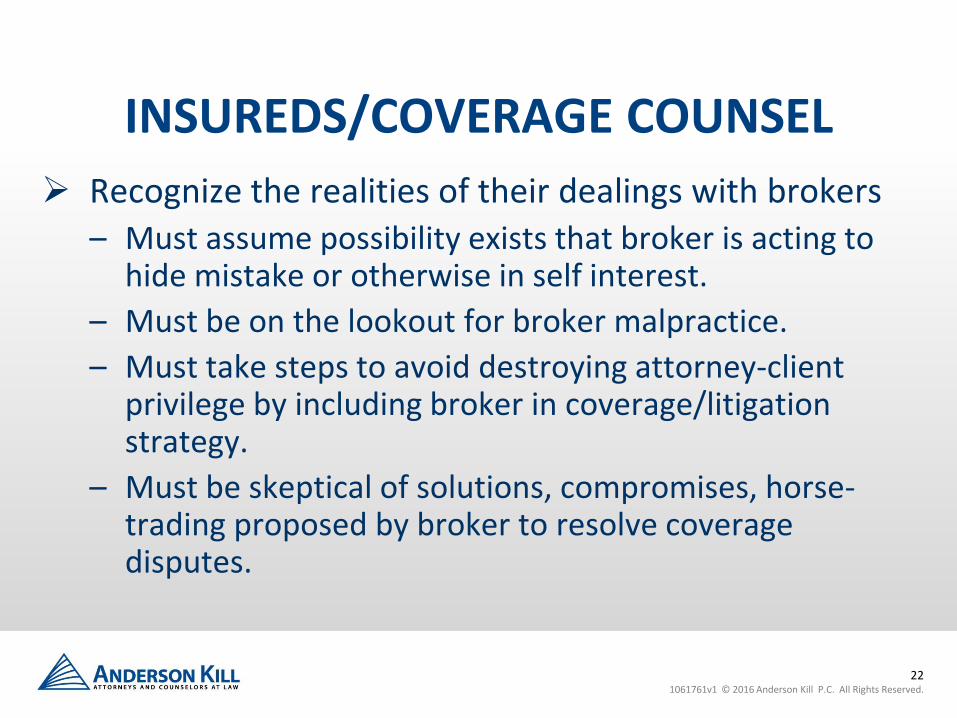

INSUREDS/COVERAGE COUNSEL Recognize the realities of their dealings with brokers

– Must assume possibility exists that broker is acting to hide mistake or otherwise in self interest.

– Must be on the lookout for broker malpractice. – Must take steps to avoid destroying attorney-client

privilege by including broker in coverage/litigation strategy.

– Must be skeptical of solutions, compromises, horse-trading proposed by broker to resolve coverage disputes.

23 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

BROKER AS RISK MANAGER In drafting policy – operating like a risk manager; recommending policy limits

24 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

BROKER AS LAWYER In claims-handling – acting like a lawyer Broker wants to provide broad services Claim advocates

25 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

NOTICE Notice – what is a ‘claim’ Is there prejudice Claims-made

26 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Aden v. Fortsh, 169 N.J. 64 (2001) The New Jersey Supreme Court has been quite vocal regarding the substantial duties owed by brokers to their insureds. In Aden v. Fortsh, the court held that a comparative negligence defense is unavailable to a professional insurance broker who asserted that the client failed to read a policy and failed to detect the broker’s own negligence. The court found that the broker is the expert, not the insured, and that the insured client is entitled to rely on its broker’s professional expertise in properly performing the job the broker was hired to do.

27 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

ADEN The court noted that there is a heightened expectation of professional services in New Jersey and that brokers owed a fiduciary duty to clients “because of the increasing complexity intricacies.”

28 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

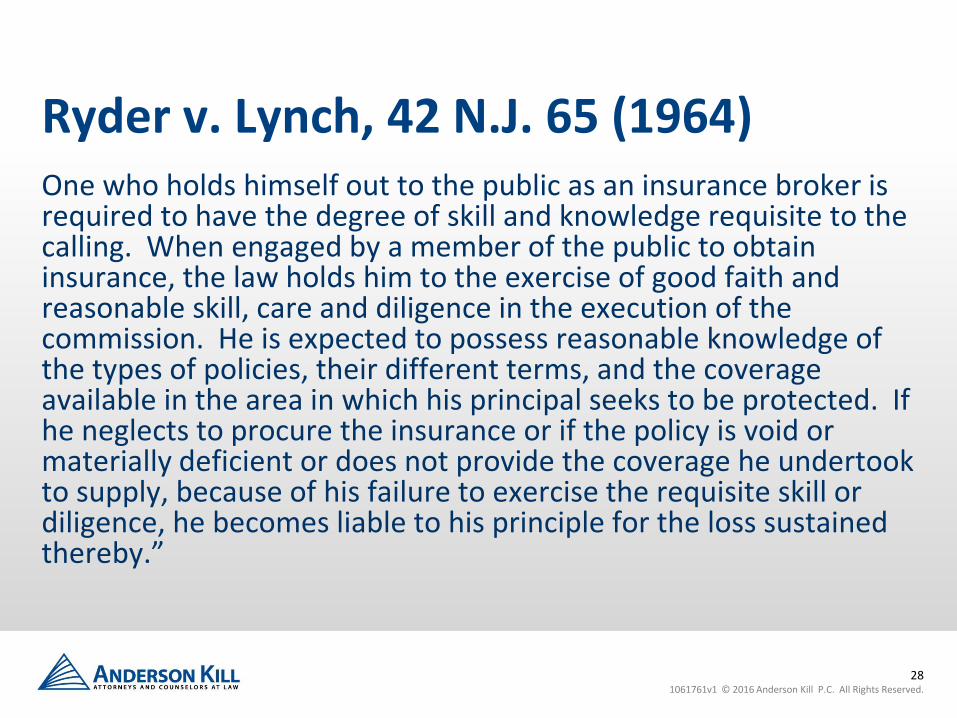

Ryder v. Lynch, 42 N.J. 65 (1964) One who holds himself out to the public as an insurance broker is required to have the degree of skill and knowledge requisite to the calling. When engaged by a member of the public to obtain insurance, the law holds him to the exercise of good faith and reasonable skill, care and diligence in the execution of the commission. He is expected to possess reasonable knowledge of the types of policies, their different terms, and the coverage available in the area in which his principal seeks to be protected. If he neglects to procure the insurance or if the policy is void or materially deficient or does not provide the coverage he undertook to supply, because of his failure to exercise the requisite skill or diligence, he becomes liable to his principle for the loss sustained thereby.”

29 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

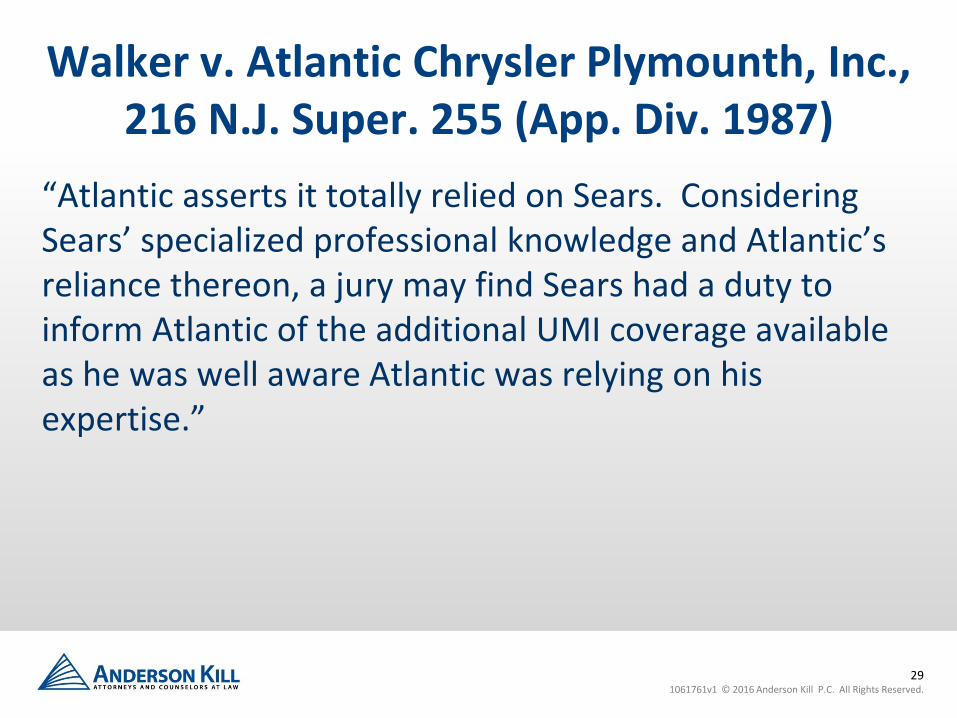

Walker v. Atlantic Chrysler Plymounth, Inc., 216 N.J. Super. 255 (App. Div. 1987)

“Atlantic asserts it totally relied on Sears. Considering Sears’ specialized professional knowledge and Atlantic’s reliance thereon, a jury may find Sears had a duty to inform Atlantic of the additional UMI coverage available as he was well aware Atlantic was relying on his expertise.”

30 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

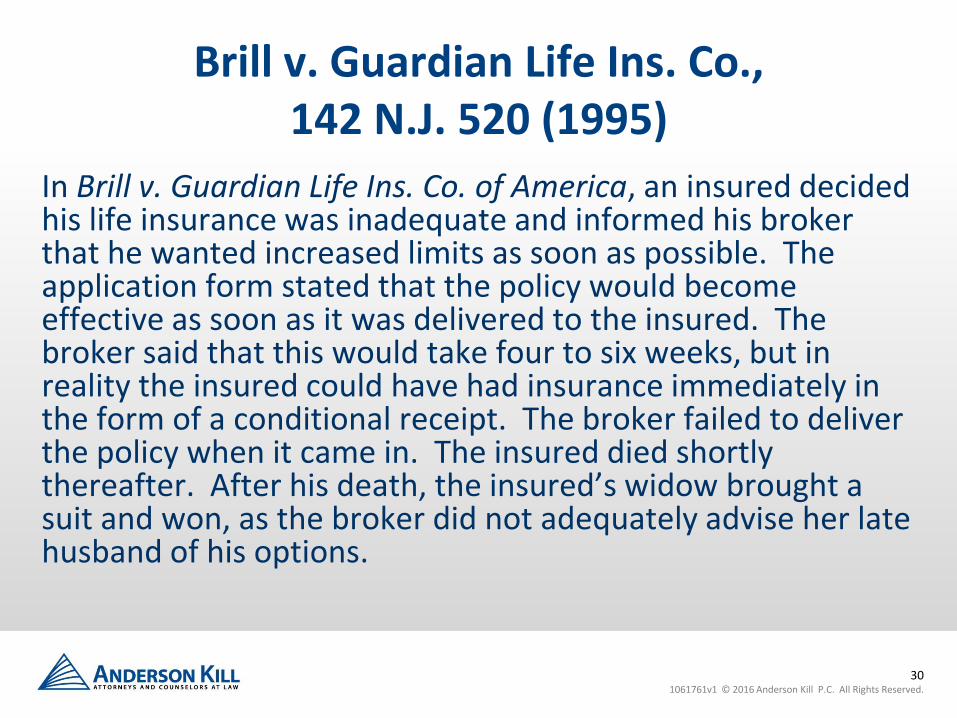

Brill v. Guardian Life Ins. Co., 142 N.J. 520 (1995)

In Brill v. Guardian Life Ins. Co. of America, an insured decided his life insurance was inadequate and informed his broker that he wanted increased limits as soon as possible. The application form stated that the policy would become effective as soon as it was delivered to the insured. The broker said that this would take four to six weeks, but in reality the insured could have had insurance immediately in the form of a conditional receipt. The broker failed to deliver the policy when it came in. The insured died shortly thereafter. After his death, the insured’s widow brought a suit and won, as the broker did not adequately advise her late husband of his options.

31 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

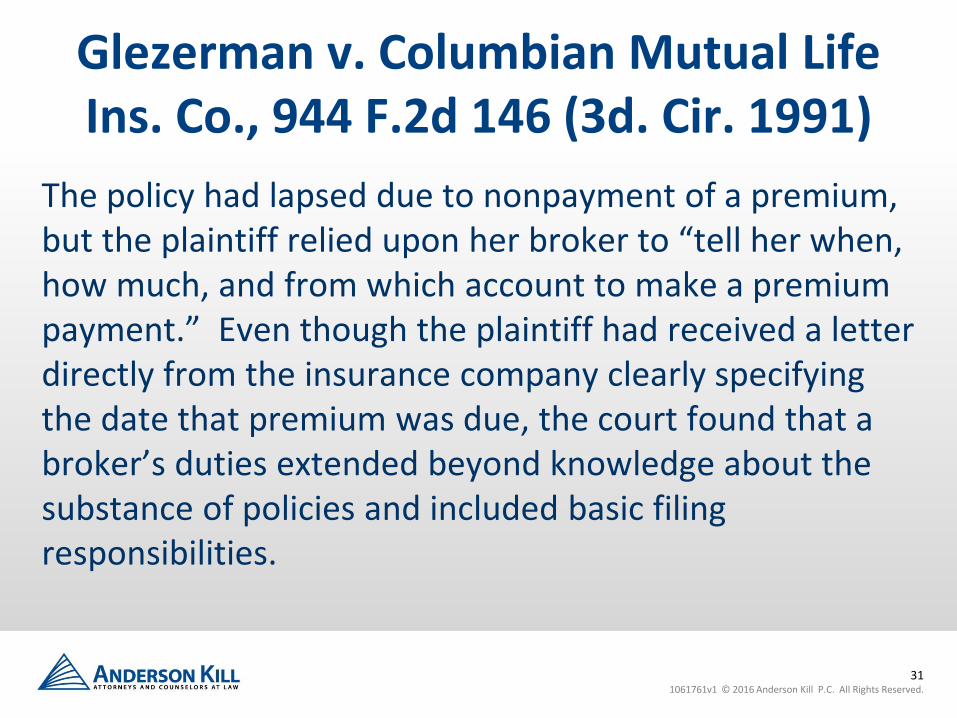

Glezerman v. Columbian Mutual Life Ins. Co., 944 F.2d 146 (3d. Cir. 1991)

The policy had lapsed due to nonpayment of a premium, but the plaintiff relied upon her broker to “tell her when, how much, and from which account to make a premium payment.” Even though the plaintiff had received a letter directly from the insurance company clearly specifying the date that premium was due, the court found that a broker’s duties extended beyond knowledge about the substance of policies and included basic filing responsibilities.

32 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Carter Lincoln Mercury v. Emar Group, 135 N.J. 182 (1994)

Brokers owe duties even to parties that are not their clients. Brokers have a duty to any foreseeable parties injured by the broker’s or agent’s negligence. As an example, the broker’s duty to evaluate the financial stability of an insurer with whom it wished to place insurance extended to other claimants beyond its client if it was reasonable to foresee that the insurance was to be procured for those claimants’ protection.

33 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Warren County Vocational Technical School v. Brown & Brown (App.Div. 2007)

Broker was also consultant Court found that Broker mistakenly believed that worker’s compensation insurance covered back pay and front pay in the context of LAD. Insured was ‘completely uninsured against claims for compensation due to purely emotional injuries. Battle of expert witnesses – broker apparently did not question standard.

34 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Huggins v. Liberty Mutual Ins. Co., 2014 N.J. Super. Unpub., LEXIS 1102 (App. Div. 2014)

Client asked for most inclusive coverage available – all beneficial coverage options. She didn’t get sump pump coverage – whose fault? No dispute that it was broker’s responsibility.

35 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Murphy v. Kuhn Murphy v. Kuhn, 682 N.E.2d 972, 974 (N.Y. 1997) (finding that

brokers “have a common-law duty to obtain requested coverage for their clients within a reasonable time or inform the client of the inability to do so”)

Murphy v. Kuhn, 682 N.E.2d 972, 975 (N.Y. 1997) (“the record in [this] case presents only the standard consumer-agent insurance placement relationship”)

Appleman on Insurance Law & Practice Archive § 87.6 (2013) (“an insurance agent has no general duty to advise an applicant or insured regarding coverage deficiencies or needs”)

“Insurance agents or brokers are not personal financial counselors and risk managers, approaching guarantor status.” Murphy v. Kuhn, 682 N.E.2d 972, 976 (N.Y. 1997)

36 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

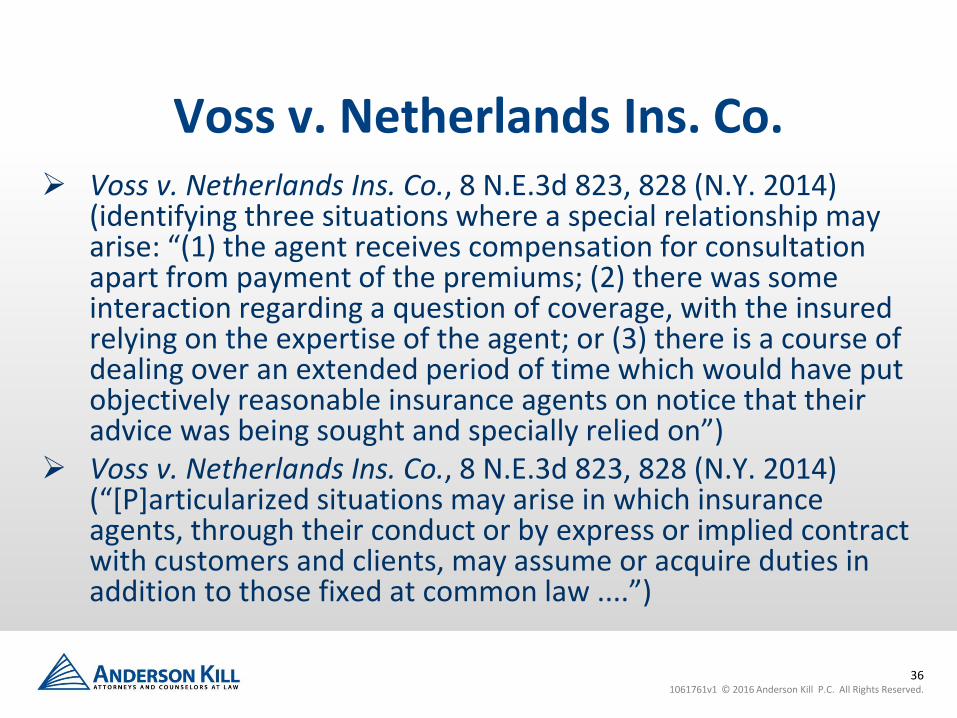

Voss v. Netherlands Ins. Co. Voss v. Netherlands Ins. Co., 8 N.E.3d 823, 828 (N.Y. 2014)

(identifying three situations where a special relationship may arise: “(1) the agent receives compensation for consultation apart from payment of the premiums; (2) there was some interaction regarding a question of coverage, with the insured relying on the expertise of the agent; or (3) there is a course of dealing over an extended period of time which would have put objectively reasonable insurance agents on notice that their advice was being sought and specially relied on”)

Voss v. Netherlands Ins. Co., 8 N.E.3d 823, 828 (N.Y. 2014) (“[P]articularized situations may arise in which insurance agents, through their conduct or by express or implied contract with customers and clients, may assume or acquire duties in addition to those fixed at common law ....”)

37 1061761v1 © 2016 Anderson Kill P.C. All Rights Reserved.

Thank You

Robert D. Chesler, Esq. (973) 642-5864

The FINEX Claims Process: 12 Step Approach to Effective Claims Management

© 2016 Willis Towers Watson. All rights reserved.

Adam Cantor Senior Vice President, Regional Leader – FINEX Claims Willis Towers Watson

STEP ONE

40

Tailor the Policy to Meet Insured’s Needs

Definition of claim

Timing of notice

Selection of counsel

Settlement and cooperation issues

Allocation, exclusions, etc.

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

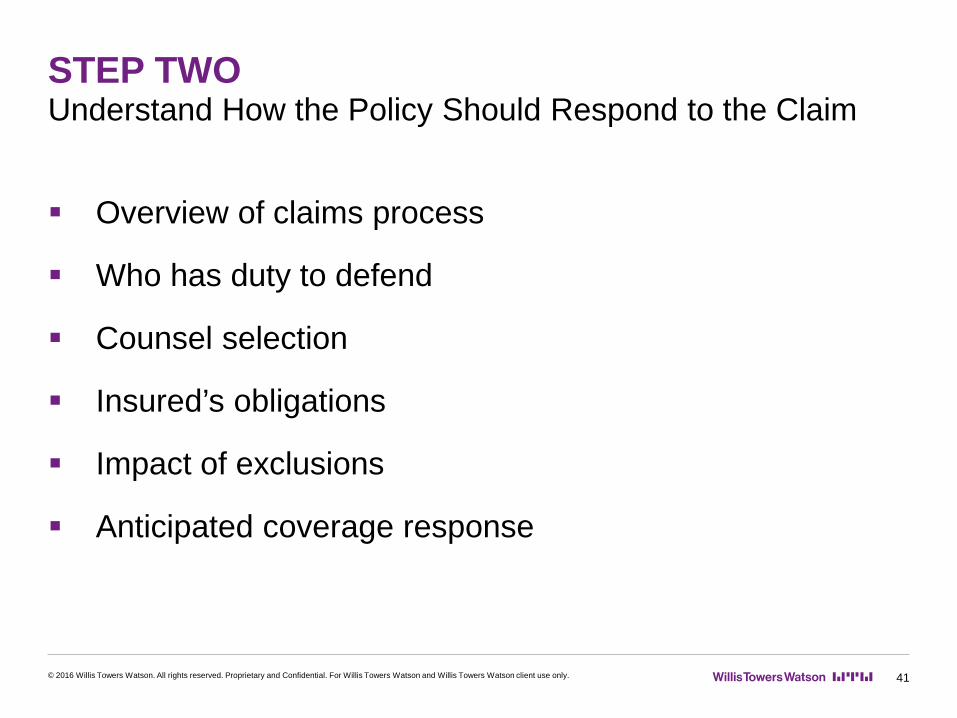

STEP TWO

41

Understand How the Policy Should Respond to the Claim

Overview of claims process

Who has duty to defend

Counsel selection

Insured’s obligations

Impact of exclusions

Anticipated coverage response

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

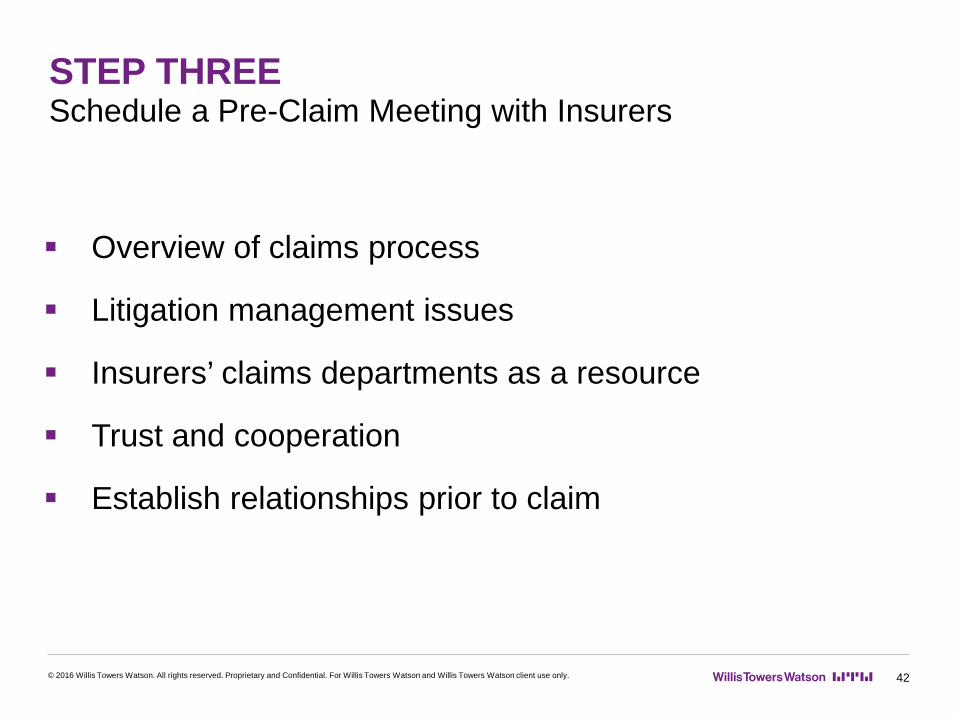

STEP THREE

42

Schedule a Pre-Claim Meeting with Insurers

Overview of claims process

Litigation management issues

Insurers’ claims departments as a resource

Trust and cooperation

Establish relationships prior to claim

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

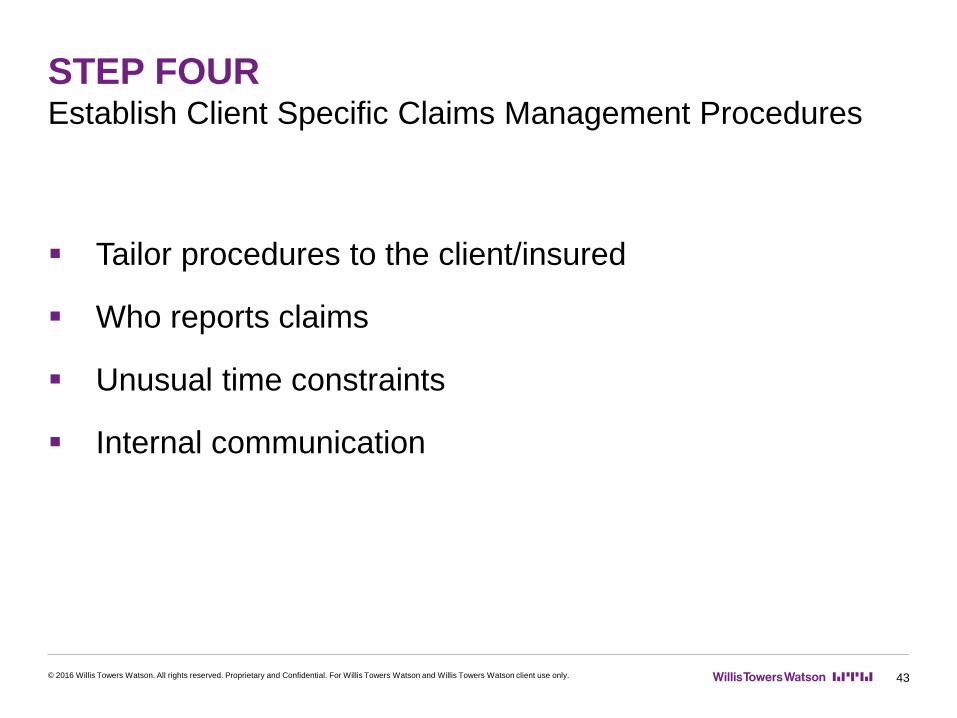

STEP FOUR

43

Establish Client Specific Claims Management Procedures

Tailor procedures to the client/insured

Who reports claims

Unusual time constraints

Internal communication

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

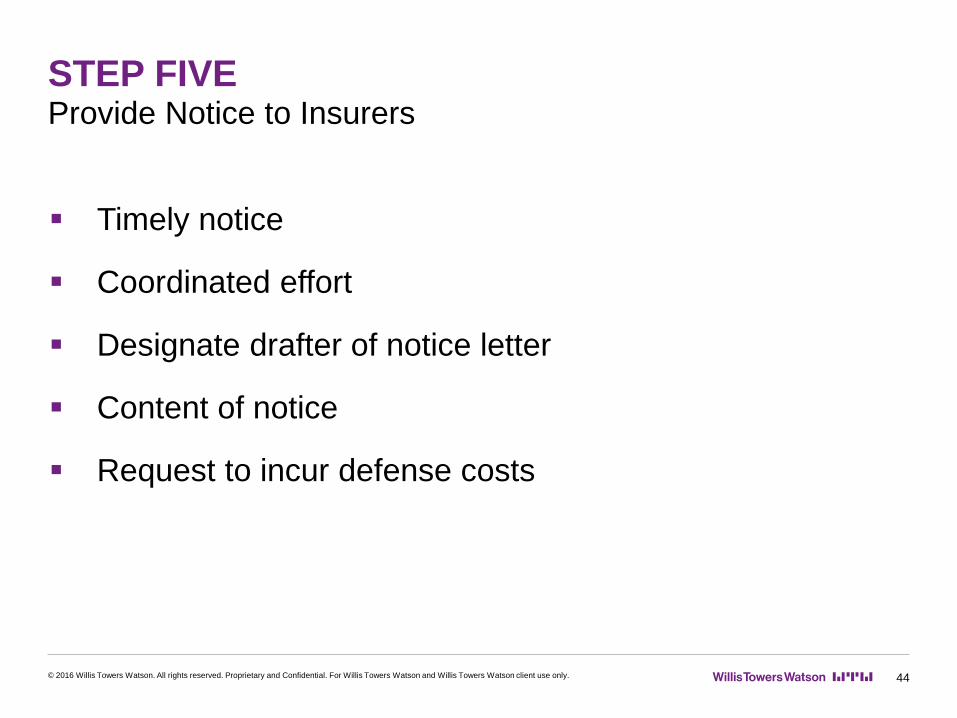

STEP FIVE

44

Provide Notice to Insurers

Timely notice

Coordinated effort

Designate drafter of notice letter

Content of notice

Request to incur defense costs

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

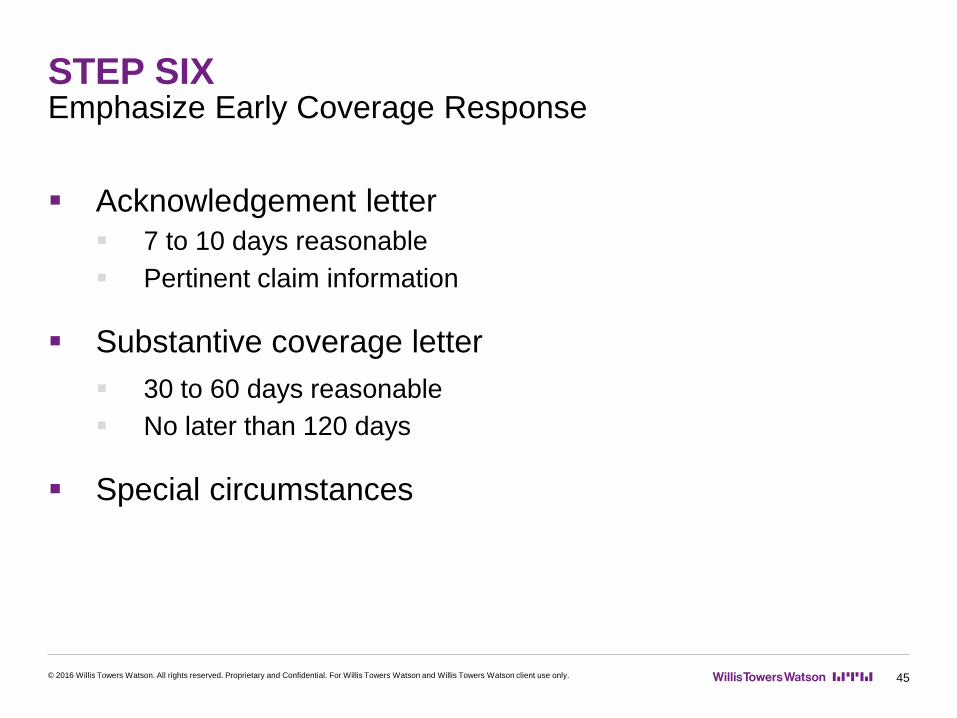

STEP SIX

45

Emphasize Early Coverage Response

Acknowledgement letter 7 to 10 days reasonable Pertinent claim information

Substantive coverage letter 30 to 60 days reasonable No later than 120 days

Special circumstances

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

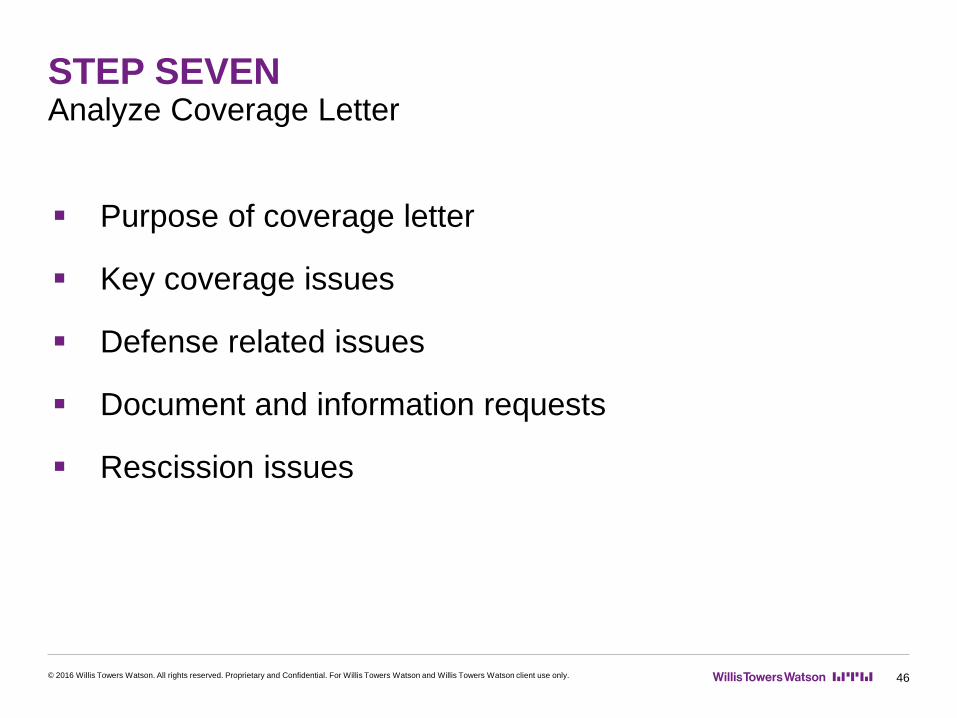

STEP SEVEN

46

Analyze Coverage Letter

Purpose of coverage letter

Key coverage issues

Defense related issues

Document and information requests

Rescission issues

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

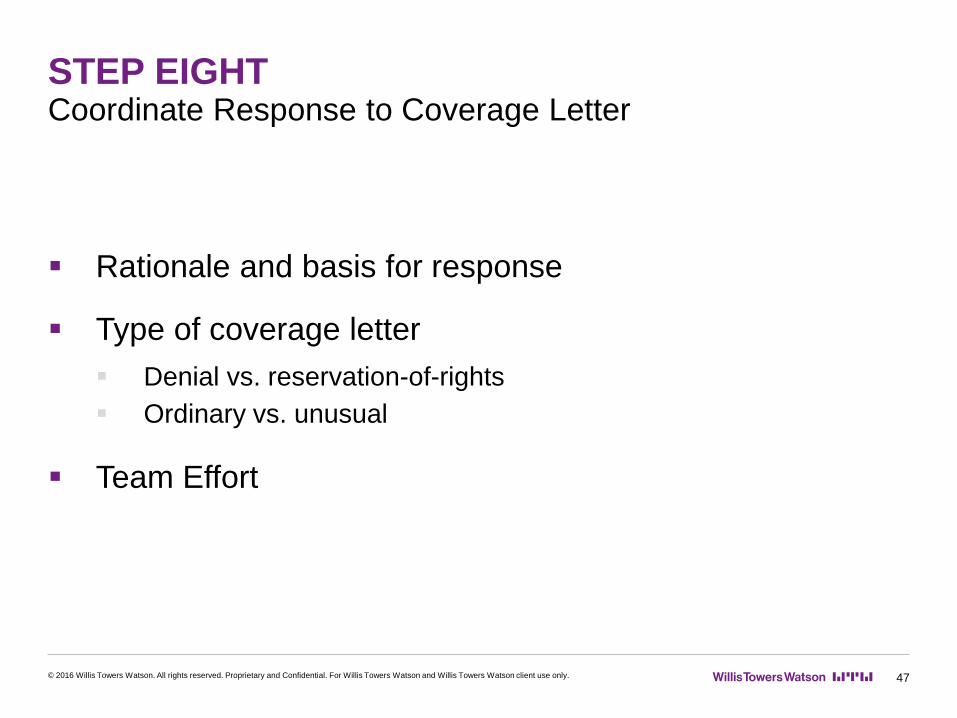

STEP EIGHT

47

Coordinate Response to Coverage Letter

Rationale and basis for response

Type of coverage letter Denial vs. reservation-of-rights Ordinary vs. unusual

Team Effort

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

STEP NINE

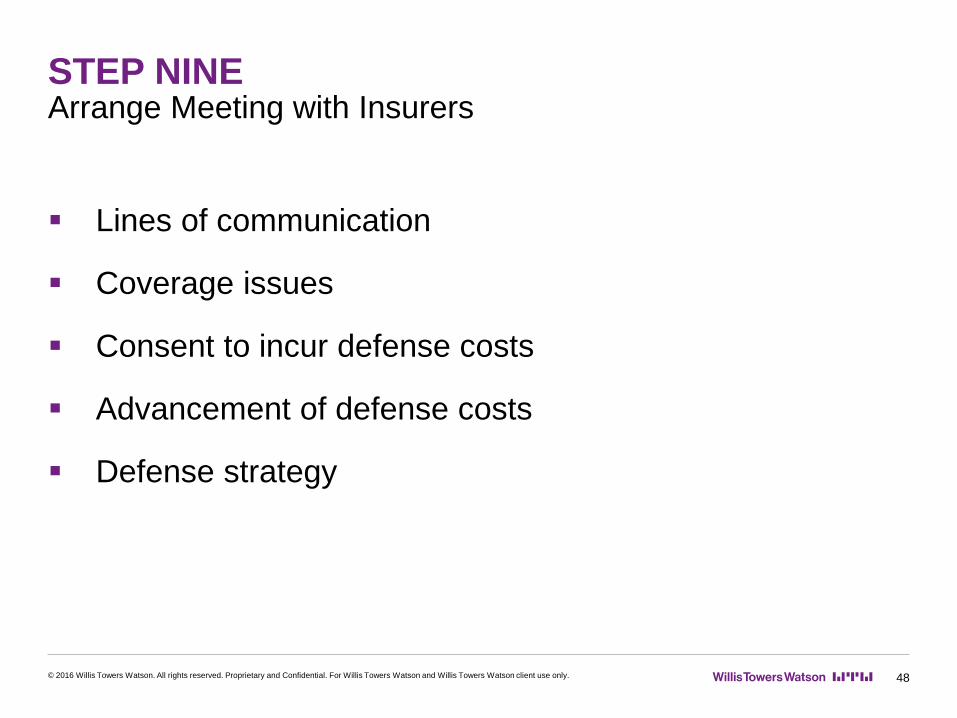

48

Arrange Meeting with Insurers

Lines of communication

Coverage issues

Consent to incur defense costs

Advancement of defense costs

Defense strategy

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

STEP TEN

49

Keep Carriers Informed

Defense bills

Significant litigation documents

Periodic status reports

Details of settlement negotiations

Confidentiality and attorney client issues

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

STEP ELEVEN

50

Request Consent to Settle

Consent to settle

Reasonableness of settlement amount

Understand settlement parameters

Participation from carriers

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

STEP TWELVE

51

Negotiate Favorable Claim Resolution

Client expectations

Coverage stance

Business interests

Innovative claim resolution strategies

Claim release/policy release

Written agreement to pay

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Top 10 Lessons Learned

52

Address claims issues upfront

Know key decision makers on claims side

Provide timely notice of claim

Effectively manage counsel issues

Challenge carriers’ coverage position

Utilize team approach in claims process

Adopt realistic expectation of claim

Satisfy cooperation/settlement obligations

Understand consequences of release

Consider global resolution of claim

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

QUESTIONS?

53

Adam Cantor Willis Towers Watson / FINEX Practice, Claims & Legal Group

(973) 829-2929 E-mail: [email protected]

© 2016 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

The webinar has ended.

The program handbook, relevant CLE forms and additional materials for this program can be accessed at:

http://tcms.njsba.com/personifyebusiness/njicle/WebinarInformation.aspx

Please hang up your telephone now.

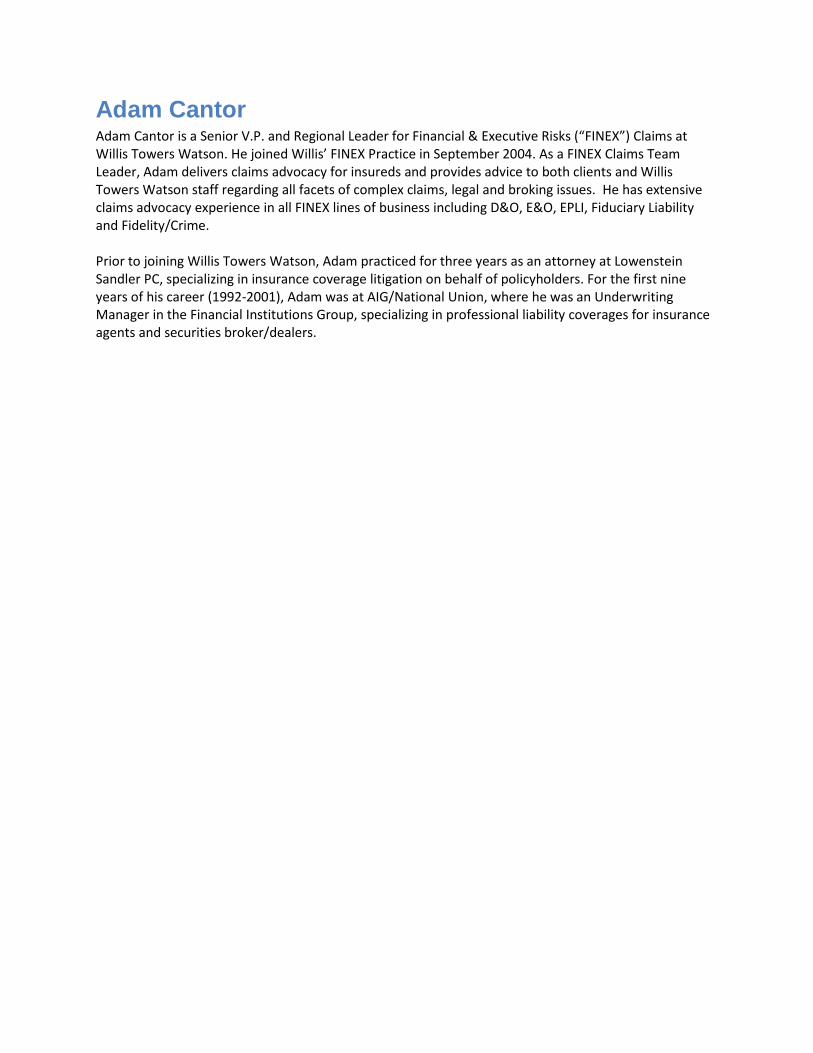

Adam Cantor Adam Cantor is a Senior V.P. and Regional Leader for Financial & Executive Risks (“FINEX”) Claims at Willis Towers Watson. He joined Willis’ FINEX Practice in September 2004. As a FINEX Claims Team Leader, Adam delivers claims advocacy for insureds and provides advice to both clients and Willis Towers Watson staff regarding all facets of complex claims, legal and broking issues. He has extensive claims advocacy experience in all FINEX lines of business including D&O, E&O, EPLI, Fiduciary Liability and Fidelity/Crime. Prior to joining Willis Towers Watson, Adam practiced for three years as an attorney at Lowenstein Sandler PC, specializing in insurance coverage litigation on behalf of policyholders. For the first nine years of his career (1992-2001), Adam was at AIG/National Union, where he was an Underwriting Manager in the Financial Institutions Group, specializing in professional liability coverages for insurance agents and securities broker/dealers.

Robert D. [email protected]

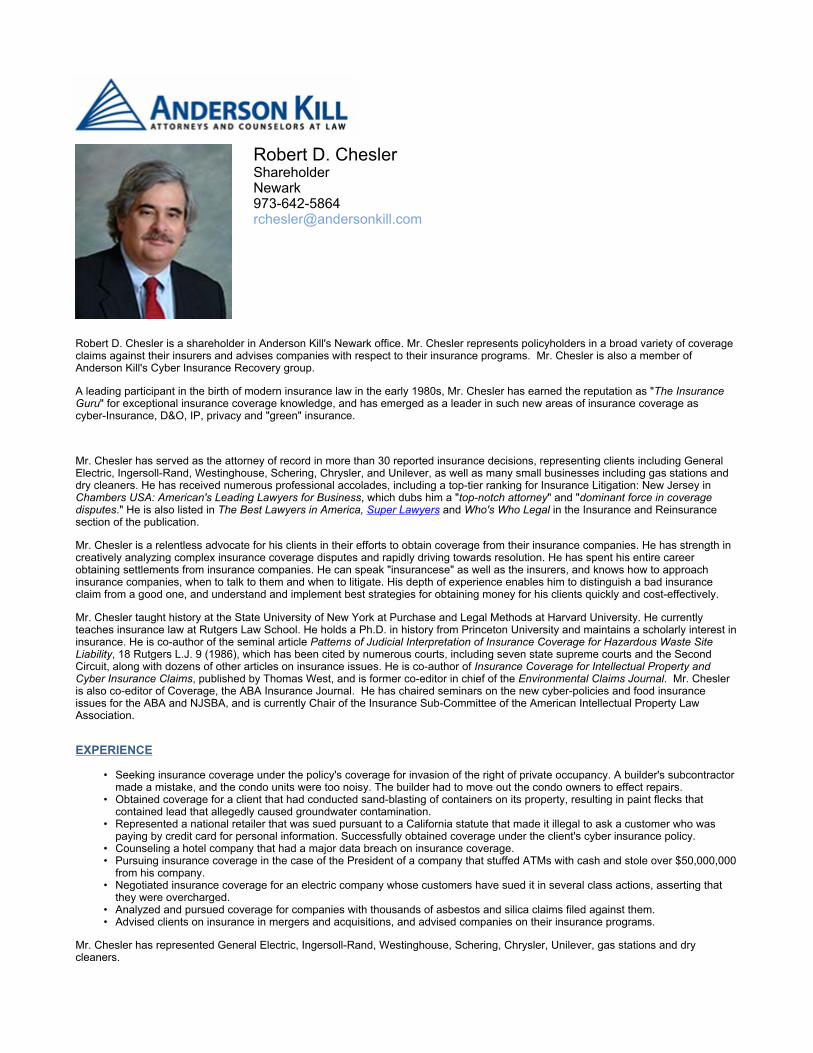

Robert D. Chesler is a shareholder in Anderson Kill's Newark office. Mr. Chesler represents policyholders in a broad variety of coverageclaims against their insurers and advises companies with respect to their insurance programs. Mr. Chesler is also a member ofAnderson Kill's Cyber Insurance Recovery group.

A leading participant in the birth of modern insurance law in the early 1980s, Mr. Chesler has earned the reputation as "The InsuranceGuru" for exceptional insurance coverage knowledge, and has emerged as a leader in such new areas of insurance coverage ascyber-Insurance, D&O, IP, privacy and "green" insurance.

Mr. Chesler has served as the attorney of record in more than 30 reported insurance decisions, representing clients including GeneralElectric, Ingersoll-Rand, Westinghouse, Schering, Chrysler, and Unilever, as well as many small businesses including gas stations anddry cleaners. He has received numerous professional accolades, including a top-tier ranking for Insurance Litigation: New Jersey inChambers USA: American's Leading Lawyers for Business, which dubs him a "top-notch attorney" and "dominant force in coveragedisputes." He is also listed in The Best Lawyers in America, Super Lawyers and Who's Who Legal in the Insurance and Reinsurancesection of the publication.

Mr. Chesler is a relentless advocate for his clients in their efforts to obtain coverage from their insurance companies. He has strength increatively analyzing complex insurance coverage disputes and rapidly driving towards resolution. He has spent his entire careerobtaining settlements from insurance companies. He can speak "insurancese" as well as the insurers, and knows how to approachinsurance companies, when to talk to them and when to litigate. His depth of experience enables him to distinguish a bad insuranceclaim from a good one, and understand and implement best strategies for obtaining money for his clients quickly and cost-effectively.

Mr. Chesler taught history at the State University of New York at Purchase and Legal Methods at Harvard University. He currentlyteaches insurance law at Rutgers Law School. He holds a Ph.D. in history from Princeton University and maintains a scholarly interest ininsurance. He is co-author of the seminal article Patterns of Judicial Interpretation of Insurance Coverage for Hazardous Waste SiteLiability, 18 Rutgers L.J. 9 (1986), which has been cited by numerous courts, including seven state supreme courts and the SecondCircuit, along with dozens of other articles on insurance issues. He is co-author of Insurance Coverage for Intellectual Property andCyber Insurance Claims, published by Thomas West, and is former co-editor in chief of the Environmental Claims Journal. Mr. Chesleris also co-editor of Coverage, the ABA Insurance Journal. He has chaired seminars on the new cyber-policies and food insuranceissues for the ABA and NJSBA, and is currently Chair of the Insurance Sub-Committee of the American Intellectual Property LawAssociation.

EXPERIENCE

• Seeking insurance coverage under the policy's coverage for invasion of the right of private occupancy. A builder's subcontractormade a mistake, and the condo units were too noisy. The builder had to move out the condo owners to effect repairs.

• Obtained coverage for a client that had conducted sand-blasting of containers on its property, resulting in paint flecks thatcontained lead that allegedly caused groundwater contamination.

• Represented a national retailer that was sued pursuant to a California statute that made it illegal to ask a customer who waspaying by credit card for personal information. Successfully obtained coverage under the client's cyber insurance policy.

• Counseling a hotel company that had a major data breach on insurance coverage.• Pursuing insurance coverage in the case of the President of a company that stuffed ATMs with cash and stole over $50,000,000

from his company.• Negotiated insurance coverage for an electric company whose customers have sued it in several class actions, asserting that

they were overcharged.• Analyzed and pursued coverage for companies with thousands of asbestos and silica claims filed against them.• Advised clients on insurance in mergers and acquisitions, and advised companies on their insurance programs.

Mr. Chesler has represented General Electric, Ingersoll-Rand, Westinghouse, Schering, Chrysler, Unilever, gas stations and drycleaners.

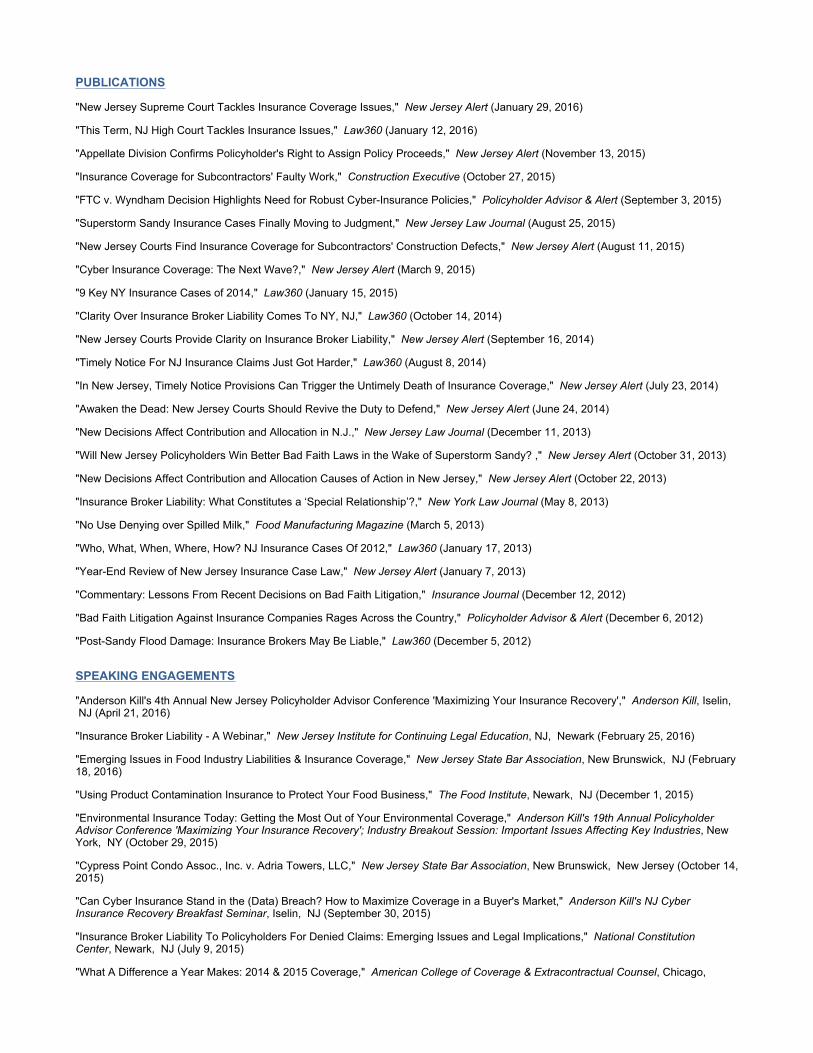

PUBLICATIONS

"New Jersey Supreme Court Tackles Insurance Coverage Issues," New Jersey Alert (January 29, 2016)

"This Term, NJ High Court Tackles Insurance Issues," Law360 (January 12, 2016)

"Appellate Division Confirms Policyholder's Right to Assign Policy Proceeds," New Jersey Alert (November 13, 2015)

"Insurance Coverage for Subcontractors' Faulty Work," Construction Executive (October 27, 2015)

"FTC v. Wyndham Decision Highlights Need for Robust Cyber-Insurance Policies," Policyholder Advisor & Alert (September 3, 2015)

"Superstorm Sandy Insurance Cases Finally Moving to Judgment," New Jersey Law Journal (August 25, 2015)

"New Jersey Courts Find Insurance Coverage for Subcontractors' Construction Defects," New Jersey Alert (August 11, 2015)

"Cyber Insurance Coverage: The Next Wave?," New Jersey Alert (March 9, 2015)

"9 Key NY Insurance Cases of 2014," Law360 (January 15, 2015)

"Clarity Over Insurance Broker Liability Comes To NY, NJ," Law360 (October 14, 2014)

"New Jersey Courts Provide Clarity on Insurance Broker Liability," New Jersey Alert (September 16, 2014)

"Timely Notice For NJ Insurance Claims Just Got Harder," Law360 (August 8, 2014)

"In New Jersey, Timely Notice Provisions Can Trigger the Untimely Death of Insurance Coverage," New Jersey Alert (July 23, 2014)

"Awaken the Dead: New Jersey Courts Should Revive the Duty to Defend," New Jersey Alert (June 24, 2014)

"New Decisions Affect Contribution and Allocation in N.J.," New Jersey Law Journal (December 11, 2013)

"Will New Jersey Policyholders Win Better Bad Faith Laws in the Wake of Superstorm Sandy? ," New Jersey Alert (October 31, 2013)

"New Decisions Affect Contribution and Allocation Causes of Action in New Jersey," New Jersey Alert (October 22, 2013)

"Insurance Broker Liability: What Constitutes a ‘Special Relationship’?," New York Law Journal (May 8, 2013)

"No Use Denying over Spilled Milk," Food Manufacturing Magazine (March 5, 2013)

"Who, What, When, Where, How? NJ Insurance Cases Of 2012," Law360 (January 17, 2013)

"Year-End Review of New Jersey Insurance Case Law," New Jersey Alert (January 7, 2013)

"Commentary: Lessons From Recent Decisions on Bad Faith Litigation," Insurance Journal (December 12, 2012)

"Bad Faith Litigation Against Insurance Companies Rages Across the Country," Policyholder Advisor & Alert (December 6, 2012)

"Post-Sandy Flood Damage: Insurance Brokers May Be Liable," Law360 (December 5, 2012)

SPEAKING ENGAGEMENTS

"Anderson Kill's 4th Annual New Jersey Policyholder Advisor Conference 'Maximizing Your Insurance Recovery'," Anderson Kill, Iselin, NJ (April 21, 2016)

"Insurance Broker Liability - A Webinar," New Jersey Institute for Continuing Legal Education, NJ, Newark (February 25, 2016)

"Emerging Issues in Food Industry Liabilities & Insurance Coverage," New Jersey State Bar Association, New Brunswick, NJ (February18, 2016)

"Using Product Contamination Insurance to Protect Your Food Business," The Food Institute, Newark, NJ (December 1, 2015)

"Environmental Insurance Today: Getting the Most Out of Your Environmental Coverage," Anderson Kill's 19th Annual PolicyholderAdvisor Conference 'Maximizing Your Insurance Recovery'; Industry Breakout Session: Important Issues Affecting Key Industries, NewYork, NY (October 29, 2015)

"Cypress Point Condo Assoc., Inc. v. Adria Towers, LLC," New Jersey State Bar Association, New Brunswick, New Jersey (October 14,2015)

"Can Cyber Insurance Stand in the (Data) Breach? How to Maximize Coverage in a Buyer's Market," Anderson Kill's NJ CyberInsurance Recovery Breakfast Seminar, Iselin, NJ (September 30, 2015)

"Insurance Broker Liability To Policyholders For Denied Claims: Emerging Issues and Legal Implications," National ConstitutionCenter, Newark, NJ (July 9, 2015)

"What A Difference a Year Makes: 2014 & 2015 Coverage," American College of Coverage & Extracontractual Counsel, Chicago,

IL (May 21, 2015)

"Insurance Broker Liability to Policyholders for Denied Claims: Latest Case Law Developments," Strafford Publications, N/A, N/A (May13, 2015)

"Maximizing Your Insurance Recovery," Anderson Kill's 3rd Annual New Jersey Policyholder Advisor Conference, Iselin, NJ (April 23,2015)

"Cyber Security Development You Need to Know," New Jersey Institute for Continuing Legal Education, Newark, NJ (January 28,2015)

"The Top 10 Case Law Developments Every Insurance Law Practitioner Should Know: 2014 Update - A Webinar," New Jersey Institutefor Continuing Legal Education , Newark, NJ (November 13, 2014)

"Broker Liability," HarrisMartin Superstorm Sandy Insurance Litigation Conference, New York, NY (May 9, 2014)

"Maximizing Your Insurance Recovery," Anderson Kill 2nd Annual New Jersey Policyholder Advisor Conference, Iselin, NJ (April 24,2014)

"Navigating Insurer Affirmative Defenses Against Policyholders in Bad Faith Litigation," Strafford Publications Insurer Bad Faith Set-UpDefense and "Reversal Bad Faith" Claims: Insurer vs. Policyholder Perspectives Webinar, Newark, NJ (January 29, 2014)

"Emerging Issues In Food Industry Liabilities & Insurance Coverage," NJICLE Seminar, New Brunswick, NJ (December 4, 2013)

"Insurance Implications of Data Security," Anderson Kill's 17th Annual Policyholder Advisor Conference, New York, NY (October 17,2013)

"Emerging Issues: Cyber Risk/Computer Related Losses," American Bar Association Property and Insurance Law Committee AnnualSpring Meeting - Exclusions and Extensions of Coverage Under the All-Risk Property Policy, Palm Beach Gardens , FL (May 17, 2013)

"What Every In-House Counsel Needs to Know About Data Security," Delaware Valley Association of Corporate CounselSeminar, Philadelphia, PA (April 23, 2013)

"Maximizing Your Insurance Recovery," AKO's New Jersey Policyholder Advisor Conference, Iselin, NJ (April 18, 2013)

"Defining and Delivering Greater Value to Corporate Clients," Association of Corporate Counsel Value Challenge Program, Seattle, WA (March 21, 2013)

"Mastering Data Breach, ID Theft & Privacy Laws," New Jersey State Bar Association CLE Seminar, New Brunswick, NJ (March 7,2013)

"New York/New Jersey Floods/Storm Protection Project," New Jersey Institute of Technology Seminar in Environmental ProblemSolving, Newark, NJ (March 5, 2013)

"Emerging Environmental Insurance Products and Issues as Well as Methods to Avoid Expensive Litigation," Pace University School ofLaw, Center for Continuing Legal Education, White Plains, NY (February 22, 2013)

"Rebuilding New Jersey: Insurance Issues and Superstorm Sandy," NJICLE Seminar, New Brunswick, NJ (February 21, 2013)

"An Overview of Insurance Considerations Created by Hurricane Sandy: Important Information for Lawyers and Their Clients," EssexCounty Bar Foundation, West Orange , NJ (December 17, 2012)

"Food Adulteration: Is It Preventable?," FX Conference Live Event, Newark, NJ (November 29, 2012)

"Important Issues Affecting Environmental Insurance Today," Anderson Kill's 16th Annual Policyholder Advisor Conference, New York, NY (October 25, 2012)

PRESS

"NJ Justices Send "Warning Call" To Insureds On Late Notice," Law360 (February 11, 2016)

"Hanover's 3rd Circ. Win Exposes Policyholders To Vague Suits," (October 28, 2015)

"Thirteen Anderson Kill Attorneys Selected as 2015 Super Lawyers, Seven Rising Stars," (October 1, 2015)

"Anderson Kill Attorneys Recognized in 2016 Best Lawyers in America," (August 26, 2015)

"Storm Clouds Still Ahead As NJ Winds Down Sandy Suits," Law360 (August 21, 2015)

"4 Insurance Battlegrounds To Watch In New Jersey," Law360 (June 10, 2015)

"Chambers USA Recognizes Anderson Kill's Insurance Recovery Group for Ninth Year Running," (June 4, 2015)

"NJ Ruling Could Deter Insurers From Trying To Buck Defense," Law360 (May 7, 2015)

"Ammonia Spill Constitutes "Direct Physical Loss or Damage" Under Property Insurance Policy, US District Court in NJ Finds ,"

(December 2, 2014)

"Anderson Kill Forms Cyber Insurance Recovery Group ," (September 3, 2014)

"NY High Court Chips Away At Broker Liability Shield," Law360 (March 3, 2014)

"Calif. Reinforces Broker Shield Against Policyholder Suits," Law360 (November 20, 2013)

"Fate Of Significant Sandy-Inspired Bills Still Uncertain," Law360 (October 29, 2013)

"NJ Ruling Protects Insureds From Insolvent Carrier Gaps," Law360 (October 10, 2013)

"Brokers Catching Heat For Sandy Coverage Headaches In NJ," Law360 (July 3, 2013)

"Brokers Facing Sandy Lawsuits," Risk & Insurance (June 10, 2013)

"New Jersey Cases To Watch In 2013," Law360 (January 1, 2013)

"Guiding clients after the storm, insurance agencies brace for life after Sandy," The Star-Ledger (November 25, 2012)

"As Demand For Recall Policies Surges, Coverage Obstacles Lurk," Law360 (October 25, 2012)

"Anderson Kill Adds Policyholder Pro From Lowenstein," Law360 (September 4, 2012)

"Robert D. Chesler Joins Anderson Kill as a Shareholder in Insurance Recovery Group in Newark, NJ ," (September 4, 2012)

"Michaels Has Edge In Data Theft Coverage Suit, Attys Say," Law360 (June 11, 2012)

"Cos. Eye Data Breach Policies As CGL Exclusions Multiply," Law360 (March 13, 2012)

"Insurance policy options for food and beverage manufacturers who may require more protection under the U.S. Food SafetyModernization Act," Controlling Engineering (February 15, 2012)

"How the new Food Safety and Modernization Act will increase the demand and cost for product recall insurance," Risk & Insurance (January 10, 2012)

"Changes in general liability insurance policies brought on by increased risks in the age of social media," Risk & Insurance (June 1,2011)

"Lawyers' and law firms' need for cyber insurance policies, which provides coverage for intangibles such as identity theft and IPinfringement--claims that general policies do not cover," Lawyers USA (July 21, 2010)

"Does a Subpoena Constitute a Claim for Purposes of D&O Insurance Coverage," The D&O Diary (January 21, 2009)

"The growth of cyber insurance, a new form of coverage for intangible Internet-based property loss," Lawyers USA (April 21, 2008)

"The Chubb Federal Insurance case against Skyy Spirits and its effect on business owners' perception on the value of liabilitycoverage," NJBiz (June 27, 2005)

HONORS & AWARDS

Robert D. Chesler

MEMBERSHIPS

Professional Memberships

Chair, Intellectual Property Insurance Sub-Committee of the American Intellectual Property Law Association; American Bar Association;Insurance Subcommittee of Litigation Section; TIPS; Essex County Bar Association: Insurance Committee; and the New Jersey StateBar Association; Insurance Section; Co-Chair, Food & Beverage Subcommittee of the ABA Section of Litigation Insurance CoverageLitigation Committee; Society of Environmental Insurance Professionals.

Association Memberships

Founding Member, American College of Coverage and Extra-Contractual Counsel

BAR ADMISSIONS

New Jersey

EDUCATION

Harvard Law School, J.D. (cum laude)

Princeton University, Ph.D.

Princeton University, M.A.

Rutgers - The State University of New Jersey, B.A. (summa cum laude)

Attorney Advertising. Prior results do not guarantee a similar outcome.

New Jersey

Services

Admissions

Memberships & Affiliations

Awards & Distinctions

Thomas F.QuinnPartner

Contact

p. 973.735.6036f. [email protected]

Accountants

e-Discovery

Insurance & Reinsurance Coverage

Lawyers

Professional Liability & Services

United Kingdom

Pro Bono

Toxic Tort

BarNew Jersey

CourtsU.S. District Court, District of NewJerseyU.S. Court of Appeals, Third CircuitU.S. Supreme Court

American Bar Foundation, FellowLitigation Counsel of America, FellowAmerican Bar Association: Tort andInsurance Practice Section; LitigationSection New Jersey Bar Association: InsuranceCoverage Committee; EnvironmentalLaw Committee Essex County BarAssociation: President (2013-2014); pastchair, Insurance Coverage Committee Trial Lawyers Association of New JerseyProfessional Liability UnderwritingSociety (PLUS)Council of Litigation Management (CLM)

Ranked by Chambers USA as a

Tom Quinn’s commercial civil litigation practice spans 30 years and focuses onprofessional liability defense and insurance coverage. He represents lawyers,accountants, insurance brokers and other miscellaneous professionals inmalpractice actions, and represents insurance companies in coverage disputes andrendering coverage opinions. He also has a general commercial litigation practicehandling ERISA and environmental matters, including class actions. In addition,Tom is well versed in the substance and subtleties of the London insurance market, leveragingthe firm’s London office to provide ready access to our network of attorneys for London-basedinsurers.

Tom’s trial practice focuses on New Jersey state and federal courts, and he is a New JerseyCertified Civil Trial Attorney. Tom is well known to New Jersey judges and has lectured on bothprofessional liability and insurance coverage issues at their annual Judicial College. He isthe immediate past president of the Essex County Bar Association, New Jersey’s second-largestbar organization. Tom is credited with more than 15 reported cases, and more than 20 unreportedcases, primarily in the coverage and professional malpractice areas, some of which are landmarkNew Jersey decisions. In addition to litigation, Tom counsels professionals on risk managementtechniques and represents them before ethics boards.

Whether defending a lawyer or advising an insurer, Tom has the ability to quickly grasp thesubject matter of a case and focus precisely on the core issues to formulate a practical strategy forresolving the case. Tom is cognizant that the best outcome of litigation generally is a resolvedcase, and he has the requisite experience to determine whether case resolution should beaccomplished through motion practice, litigation, settlement or trial.

Areas of FocusProfessional Liability In the representation of lawyers, Tom has defended both large law firms and solo practitioners in avariety of disputes involving real estate, civil litigation, family law, class actions, corporate issuesand bankruptcy matters. He also represents lawyers in ethics proceedings and proposed classaction lawsuits. Tom has achieved trial victories in his defense of a lawyer in a real estate/conflictof interest matter, a lawyer in a real estate family dispute, a lawyer who counseled a client oncorporate debt issues, and a lawyer who had erroneously failed to advise a client about a filingdeadline. He also has defended lawyers in ethics trials before special masters.

In the accountants’ liability area, Tom has experience defending malpractice cases involvingalleged faulty audits and other attestation work, improper valuations, tax-related errors, and claimsof lack of independence. He has counseled accountants on how to respond to third-party andgrand jury subpoenas, and has defended and counseled accountants in ethics proceedings.

Education

Certifications/Licenses

Ranked by Chambers USA as aleading lawyer in the Litigation:Insurance category, 2009-2015 AV® Preeminent™ Rated byMartindale Hubbell Selected for inclusion in NewJersey Super Lawyers, 2005-2015(top 100in N.J. 2010-2012)Selected as one of The BestLawyers in America in theInsurance Law area (2006-2016)and Legal Malpractice 2016Best Lawyers – Insurance Law,Attorney of the Year, Newark, 2012

Seton Hall University School of Law,J.D., 1981, cum laude; Seton Hall LawReview

Georgetown University, B.A., 1978

New Jersey Certified Civil Trial Attorney

grand jury subpoenas, and has defended and counseled accountants in ethics proceedings.

Tom also has been lead trial attorney representing insurance professionals in cases involvingclaims ranging from failure to obtain requisite coverage and/or insufficient limits of coverage, toallegations that captive managers failed to develop adequate coverage programs and left theirclients financially exposed.

In addition, Tom has represented title agents, appraisers, home inspectors, computer consultantsand many other professionals in litigated matters.

Insurance Coverage Tom is a well-known New Jersey coverage lawyer with extensive experience representingdomestic and foreign insurers in coverage disputes involving environmental, product liability,professional liability, advertising injury, commercial general liability (CGL) and first-party propertydamage claims.

Among his reported cases, Tom was counsel of record on the leading case in New Jerseyregarding asbestos insurance coverage and allocation issues, as well as other significant caseson the duty to defend. He also successfully defended at trial an excess insurer in an Agent Orangeand environmental coverage case and has been lead counsel to insurers regarding an underlyingunfair competition lawsuit and underlying pharmaceutical class action cases. He has representedfidelity insurers in substantial litigation with regulatory authorities. He also has defended classaction lawsuits against health insurers on issues related to payment of benefits. He also counselsand represents London-and-Bermuda based Insurers in a variety of matters, including SuperstormSandy claims.

Tom’s insurance coverage experience also encompasses more common coverage issues as wellsuch as automobile coverage, additional insured issues under GL and contractor policies,coverage for employment litigation, and coverage of claims made under professional liabilitypolicies. Tom was recently asked by the New Jersey State Bar Association to update theinsurance coverage chapter of its Employment Law treatise.

Tom has lectured nationwide on coverage issues and has published on the subject. He is the pastchair of the Insurance Coverage Committee of the Essex County Bar Association.