Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=2011889

Impression management and Non-GAAP reporting in earnings announcements

Encarna Guillamon-Saorin

Universidad Carlos III de Madrid

Helena Isidro

Instituto Universitário de Lisboa (ISCTE-IUL), BRU UNIDE, Lisboa, Portugal

Ana Marques1

NOVA School of Business and Economics – Universidade Nova de Lisboa

January 2012

The authors appreciate the valuable comments received from the workshop participants at NOVA School of Business and Economics and at the Grenoble Ecole de Management. This study was supported by the Foundation for Science and Technology in Portugal (grant PTDC/EGE-GES/103770/2008). Encarna Guillamon-Saorin acknowledges financial contribution from the Spanish Ministry of Science and Innovation (SEJ2007-67582-C02-02/ECON, ECO2010-19314) and Comunidad Autonoma de Madrid (SEJ2008-00059-003). Ana Marques also acknowledges financial support received from Nova Forum. We are grateful for the excellent research assistance of Arash Aloosh and Luís Araújo.

1Corresponding author: NOVA School of Business and Economics, Campus de Campolide

1099-032 Lisboa, Portugal. Tel: +351.918080250. Fax: +351.21387933. Email: [email protected]

Electronic copy available at: http://ssrn.com/abstract=2011889

1

Impression management and Non-GAAP reporting in earnings announcements

Abstract

This paper analyzes whether managers combine two mechanisms capable of influencing

investors’ judgments in earnings announcements. Specifically, we study whether managers use

impression management techniques to emphasize non-GAAP earnings measures when announcing

annual results. The study is carried out on an international sample of European countries, during 2003-

2005. The method used is manual content analysis. We find evidence that managers use impression

management techniques as a complement to the disclosure of non-GAAP earnings measures.

Furthermore, our analysis of market reactions indicates that although investors recognize that non-

GAAP earnings measures have information content they penalize firms that present these figures in

combination with impression management techniques. Thus, investors seem to perceive the use of

impression management to enhance non-GAAP figures as an opportunistic strategy and consequently

inflict a penalty for this self-serving behavior.

Keywords: Non-GAAP earnings, impression management, pro forma, press releases.

JEL classification: M41

2

1. Introduction

Managers use earnings announcements to convey private information about firm’s performance

to capital market participants. When selecting information to disclose in public announcements

managers benefit from a considerable degree of discretion. In this paper, we study the link between two

discretionary mechanisms: the disclosure of non-GAAP earnings measures and the use of impression

management techniques in earnings announcements’ press releases. First, we investigate whether non-

GAAP disclosure and impression management are complementary or substitute mechanisms in

voluntarily corporate communications. Second, we assess whether short-term market reaction to the

disclosure of non-GAAP earnings measures changes when it is accompanied by impression

management techniques.

Managers frequently include in earnings announcements self-constructed earnings figures that

deviate from reported GAAP earnings (i.e. non-GAAP figures). These non-GAAP numbers often

portray a better image of firm performance than the GAAP numbers provided by audited financial

reports. Critics of this practice claim these figures aim at misleading investors. Managers, on the other

hand, claim that the self-constructed numbers represent better permanent earnings and are designed to

aid investors’ interpretation of financial results. Whatever the motivation driving the disclosure, the

manager-adjusted earnings numbers have the potential to influence investors’ decisions (Andersson and

Hellman, 2007; Bhattacharya et al., 2007).

Managers can also influence investors’ perceptions via the use of impression management

techniques (Adelberg, 1979). For example, managers can pass a positive impression of firm

performance by emphasizing the figures that portray a better image, and select only the “best” numbers

3

from the financial statements. Impression management can be operationalized in different forms

(thematic manipulation, emphasis, performance comparisons, selectivity, forward-looking disclosures

etc.) with the aim of presenting a self-serving view of corporate and management performance. Recent

studies suggest that impression management techniques are used in annual earnings’ announcement

press releases to influence investors’ judgments (Garcia Osma and Guillamon-Saorin, 2011), and to

support manipulated earnings numbers (Aerts and Cheng, 2011; Guillamon-Saorin and Garcia Osma,

2010).

An important aspect of management’s opportunistic disclosures is credibility. Prior findings

indicate that managers are successful in affecting the perception of investors and analysts using

opportunistic disclosures. For example, the increase in optimistic disclosures detected by Lang and

Lundholm (2000) is associated with increased stock prices leading up to equity offerings. Also, the level

of optimism in an earnings announcement is positively associated with the market’s short-term response

to the announcement (Davis et al., 2011; Henry, 2008). It is possible that managers attempt to enhance

credibility by combining different disclosure practices to make the content of corporate reports more

consistent and convincing.

Prior literature provides evidence of the use of causal disclosures in combination with earnings

management in the prospectus of IPOs firms (Aerts and Cheng, 2010). This behavior is seen as an

opportunistic attempt to rationalize and legitimize the corporate earnings outcomes. Similarly, Godfrey

et al. (2003) shows a positive association between manipulated earnings and the use of graphical

impression management. Thus, it is possible that managers combine the use of non-GAAP earnings

disclosures and impression management practices. If managers do so, the question arises whether users

of information are fooled by this combination or, instead, penalize it. If impression management is

successful and convinces investors that the non-GAAP measures reflect performance, the market

4

reaction to non-GAAP information will be stronger. However, if market participants perceive the

impression management surrounding non-GAAP measures as a signal that managers want to

misrepresent the firms’ performance the market reaction will be negative or non-existent.

Prior research investigating corporate opportunistic disclosures analyze formal text included in

sections of the annual reports, like chairman statements and MD&A (e.g. Abrahamson and Park, 1994;

Aerts, 2005; Schleicher and Walker, 2010; Subramanian et al., 1993; Yuthas et al., 2002) but also

earnings announcements press releases (Bowen et al., 2005; Davis et al., 2011; Demers and Vega, 2008;

Garcia Osma and Guillamon-Saorin, 2011; Henry, 2008; Henry and Leone, 2009). Press releases

announcing annual results serve other communication strategies than annual reports. They include more

expressive language and can be used as management self-serving tools (Aerts and Cormier, 2009).

Rogers et al. (2011) find evidence consistent with earnings announcements containing information that

derived into lawsuits against companies. This evidence suggests that information included in earnings

announcements press releases is, in general, relevant to investors. Investors, particularly less

sophisticated ones who rely more on public sources of information, are more likely to be misled by

opportunistic disclosures in press releases such as non-GAAP earnings (Bhattacharya et al., 2007) and

high impression management.

In our empirical tests we include hand-collected information regarding: (i) the level of

impression management used in the earnings announcement press releases as measured by a score

derived from the content analysis, and (ii) the voluntary disclosure of non-GAAP earnings measures.

Our sample consists of the largest firms in Europe and the time period analyzed includes years 2003,

2004 and 2005. The low litigation environment and absence of regulation on non-GAAP disclosure that

characterizes many European markets facilitate the use of discretionary information in earnings

5

announcements.1 Capital markets are also relatively less developed in Europe than in other countries

(such as the US), which implies that the potential markets effects of misleading disclosures to less

sophisticated investors can be high. Thus, this is an interesting setting for the analysis of the link

between impression management and non-GAAP disclosure, and the consequent market implications.

In our analysis of the relationship between the two mechanisms we find a positive association

between the use of impression management techniques and the decision to disclose non-GAAP figures

in the press releases. This indicates a complementary relation between the two disclosure practices.

Moreover, companies with a higher level of adjustments to non-GAAP measures (i.e. where non-GAAP

earnings deviates more from GAAP earnings) show higher levels of impression management techniques

in earnings announcements. This evidence suggests that managers use both disclosure strategies to

create a positive impression on readers, which is consistent with an opportunistic rather than informative

intention.

Furthermore, our market reaction tests reveal a negative market reaction to the combination of

non-GAAP disclosures and the use of impression management. This suggests that investors perceive the

use of impression management to emphasize non-GAAP numbers to be misleading and consequently

punish this practice. Although not fully comparable, our results complement those which report positive

market´ short-term responses to positive and optimistic tone in corporate reports (Davis et al., 2011;

Henry, 2008).

Capital markets, however, recognize that non-GAAP disclosures can be used by managers to

mitigate information asymmetry. Our analysis of cumulative abnormal returns for a three-day window

1 The only institutional pronouncement about this topic in Europe is the recommendation the CESR - Committee of European Securities Regulators, issued in October 2005. The objective of this recommendation is to encourage European-listed firms which chose to disclose non-GAAP financial measures to do it “in a way that is appropriate and useful for investor’s decision making”.

6

around the earnings announcement day reveals that the market reacts positively to the adjustments made

to GAAP figures, which is similar to the market reaction to an earnings surprise. Thus, the disclosure of

these alternative performance figures is only penalized when combined with the use of impression

management techniques.

This study contributes to the voluntary disclosure literature in two ways. First, it shows that non-

GAAP disclosures and impression management are used together to create an overall positive

impression of firm performance. This combination can have a substantial impact on investors’

perceptions about firm’s performance, particularly on less sophisticated investors who rely more on

earnings information conveyed through corporate communications such as press releases. Second, this

research provides evidence that the two potentially misleading voluntary disclosure mechanisms affect

capital markets. We find that investors perceive the combined use of impression management techniques

and non-GAAP disclosure as a sign of opportunistic intentions. Moreover, to the best of our knowledge,

this is the first study which documents the usage of impression management techniques in narratives in

an international context, as prior studies investigating impression management internationally focus on

the manipulation of graphs in annual reports (Beattie and Jones, 1997; 2001). Detecting potentially

misleading management disclosure practices can be important for analysts, regulators and the various

entities that interact with firms. For example, insights from this work provide valuable information to

guide standard setters when issuing recommendations or regulations related to voluntary disclosures,

particularly non-GAAP information.

The remaining of the paper is organized as follows. The next section describes previous findings

and develops our hypotheses. Section 3 discusses the sample selection and the hand-collection and

coding of the data. Section 4 explains the research design. Section 5 presents the empirical results.

7

Section 6 concludes.

2. Literature review and hypotheses development

Voluntary disclosures can be used to provide investors with valuable incremental information or

to attempt to mislead them (Core, 2001; Verrecchia, 2001). Management attempts to mislead outsiders

and influence shares prices suggests that managers believe investors are not able to see through biased

disclosures (Adelberg, 1979; Courtis, 2004). If, on the contrary, managers believe in financial markets’

efficiency and in the ability of investors to recognize misleading voluntary disclosures, they have no

economic incentives to attempt to mislead investors, as doing so can increase cost of capital and affect

their reputation (Baginski et al., 2000).

The disclosure of non-GAAP earnings metrics in earnings announcements has created

controversy because while managers argue that they provide stakeholders with a more accurate

assessment of corporate performance (Bray, 2001), policymakers and regulators alert for the potential

misleading intention behind these incomplete or even inaccurate numbers (Derby, 2001). Early studies

established that non-GAAP earnings are more highly correlated with returns than GAAP earnings

(Bhattacharya et al., 2003; Bradshaw and Sloan, 2002). This seems to indicate that these figures are

disclosed by managers to provide markets with a more useful earnings’ metric than the number obtained

following accounting standards. Another case where the managers’ intention seems to be to provide

valuable information to users of financial information is when firms report non-GAAP earnings

numbers which are lower than GAAP figures (Curtis et al., 2011). However, managers are motivated to

disclose and emphasize the measures that portray the firm in the best performance possible in an attempt

to influence stakeholders’ perceptions (Bowen et al., 2005). Consistent with this idea previous research

8

indicates that firms often disclose non-GAAP earnings figures which meet or beat earnings benchmarks

when GAAP figures fall short of the benchmark (Bhattacharya et al., 2004).

Impression management is justified by the human need to present themselves in the most

positive light (Hooghiemstra, 2000; Schlenker, 1980; 2003). In a corporate reporting setting, impression

management intends to manipulate the impression conveyed to users of accounting information

(Clatworthy and Jones, 2001). Most studies investigating the competing theories of impression

management and incremental information for voluntary disclosures find support for the impression

management interpretation. For example, Lang and Lundholm (2000), using a matched-pair design,

analyze the disclosure practices around new stock offerings and find that optimistic disclosures

increased before the equity public offerings while the pessimistic decreased around the same period.

Matsumoto et al. (2006) investigate impression management and incremental information in relation to

managerial optimism. Their results confirm that managerial optimism is neither confirmed by analysts’

opinion nor related to future financial performance suggesting manager’s engagement in self-serving

disclosures.

Managers have incentives to engage in several self-serving practices simultaneously, in order to

increase the effect of disclosures on users’ perceptions of firm performance. Evidence of this strategy

has been found in prior literature. For example, Aerts and Cheng (2011) find an association between

earnings management and impression management, using causal explanations in the prospectus of

Chinese IPO firms. Similarly, Guillamon-Saorin et al. (2011) show that impression management is used

together with real earnings management practices, and Godfrey et al. (2003) show that firms exhibiting

graphical impression management in their annual reports also engage in earnings management. These

results constitute evidence of the strong tendency to acclaim positive earnings-related outcomes and to

combine disclosure mechanisms that help to pass to outsiders the desired corporate message. Following

9

this line of research, we propose that managers may use a combined disclosure strategy where they

apply several impression management techniques and disclose non-GAAP earnings figures in earnings

announcements press releases. Therefore, we state our first hypothesis as follows:

H1: There is a positive association between the disclosure of non-GAAP earnings figures and

the use of impression management techniques.

The disclosure of manager-adjusted numbers in earnings announcement has informational effects

on capital markets (Bhattacharya et al., 2003; Bradshaw and Sloan, 2002), and influences the judgments

of both less-sophisticated investors and financial analysts (Andersson and Hellman, 2007). The use of

impression management in corporate communications has also implications for capital markets

participants. Krische (2005) uses an experimental setting to investigate the effect of strategic

inclusion/exclusion of transitory prior-period gains or losses to influence investors evaluation of current

year results. The effect found is interpreted as unintentional and due to the reader cognitive effects.

Moreover, Davis et al. (2011) find that there is a market reaction to the unexpected level of optimistic

words, using a computerized textual-analysis software to read press releases (Diction).

If managers combine the use of impression management and non-GAAP disclosures the question

arises whether and how the market participants react to this combination. If investors are positively

influenced by the use of impression management techniques and believe the information disclosed in the

press release (including the non-GAAP earnings figures) to be relevant we should observe a positive

incremental reaction to the combined use of non-GAAP measures and impression management. On the

other hand, if investors interpret the presence of impression management as an attempt to inflate firm

performance they should react negatively, punishing managers for their endeavor. This would be similar

10

to the effect found by Barton and Mercer (2005) where managers are punished for trying to justify their

bad results with external events not related to their performance. It would also be consistent with the

negative market reaction to indicator variables representing the disclosure of non-GAAP measures in the

US before Regulation G (a period when markets believe these were used for manipulating earnings

perceptions), identified in Marques (2006).2 Given the two possible scenarios, we state our second

hypothesis in the null form:

H2: Market participants’ reaction to non-GAAP earnings is not affected when impression

management is used in the same earnings announcement.

3. Sample selection procedure and hand-collection of data

We begin our sample selection process by considering all firms included in the Financial Times

2006 classification of the 500 largest European companies. This allows us to study a group of firms

which represent a significant portion of European capital markets, where the potential effects for

managers’ misleading practices is significant. Financial institutions and utilities firms, which follow

specific regulations that can affect voluntary disclosure, are excluded from the sample. Data on financial

items and market returns is obtained from Worldscope/Datastream. Data on analysts’ consensus is

obtained from I/B/E/S. After eliminating observations with missing financial information and press

releases, the final sample consists of 717 firm-year observations, for 267 firms covering fiscal years

2003, 2004 and 2005 (Table 1 provides the details).

2 This negative market reaction is present in both the short and long-term windows of tables 6 and 7. However, they are only significant in the long windows (of 63 days), which analyze the quarterly market reaction.

11

Earnings announcements’ press releases are gathered from the companies’ websites and Factiva.

We perform a manual content analysis to quantify the level of impression management in the press

release. This method is comparable to that used in prior research (Aerts, 2005; Schleicher and Walker,

2010). Most prior work analyzing disclosures tone relies on pre-specified wordlists (Davis et al., 2011;

Henry, 2008; Loughran and McDonald, 2011; Rogers et al., 2011). These studies state that this

methodology allows them to perform a systematic and objective content analysis. However, software

with integrated wordlists give rise to problems including the omission or miscoding of keywords (Henry

and Leone, 2009; Larcker and Zakolyukina, 2010). Our method, although more subjective, allows the

analysis of a diverse range of practices which cannot be coded using computer-aid techniques. Most of

the practices analysed in this study (i.e. emphasis, repetition, selectivity, performance comparisons)

cannot be analysed and coded using computer-aid methods. Manual content analysis has also been

widely used and enhanced in prior literature for allowing greater flexibility and more detailed analysis

(Conway, 2007; Linderman, 2001). Next we describe our measures of impression management and non-

GAAP information.

3.1. Measure of impression management

The level of impression management in each earnings announcement is analyzed following a

schema developed in prior work (Brennan et al., 2009; Hussainey et al., 2003). Appendix 1 shows the

method followed to examine the following five impression management disclosure techniques:

disclosure tone, adding emphasis, performance comparisons, forward-looking disclosures, and

selectivity to create an overall positive connotation in the press release. The appendix also illustrates

these practices using one of the companies included in the analysis: Ahold. The five techniques are

12

described below.

(1) Disclosure tone. This technique consists of using positive language, keyword, statements or amounts

to create a positive image of corporate results that would not be achieved using more neutral

statements. We analyze disclosure tone by coding positive and negative amounts as in prior research

(Brennan et al., 2009)3. The amounts are classified as positive (negative) if current year amount is

higher (lower) than prior year. For example, “Schering AG Group reported an organic growth in net

sales of 5% in 2004” (taken from Schering AG Group press release for 2004). This explicit

statement of increase in sales is coded as a positive tone.

(2) Emphasis. This consists of making a particular piece of information more obvious to the reader by

using two strategies: (a) placing the information strategically in the press release (emphasis by

location) and (b) repeating the same piece of information in the press release (emphasis by

repetition).4 For example, SGS company includes the same information related to revenues in the

headline “With top line growth of 17.6% to CHF 2,885 million, SGS achieved a 30.3% improvement

in operating income to CHF 391 million” as well as in the first paragraph of the press release “In an

improved trading environment, revenues for the Group increased to CHF 2,885 million, up CHF 467

3 Except for Brennan et al. (2009), Garcia Osma and Guillamon-Saorin (2011) and Guillamon-Saorin et al. (2011), no other prior work has investigated disclosure tone using quantitative information. Most of the work analysing tone of disclosures use computer developed software or algorithms that limit the analysis to the coding of keywords (e.g. Henry, 2006; 2008; Rogers et al. 2011) or basic analysis of textual complexity (e.g. Li, 2008). 4 Three sections are defined to identify emphasis by location: most-, and next most- and least emphasised. For the purpose of this study we focus on the analysis of the two first sections of the press release. The most emphasised section could be the headline (if present), subheadings (if headline not present) or first and second paragraph (if headline and subheadings not present). The next most emphasised section could be the subheadings (if present) or the second and third paragraphs (if subheadings not present).

13

million over last year in local currency terms (CHF 431 million on a reported basis).” (taken from

SGS press release for 2004).5

(3) Performance comparisons. The use of performance benchmarks as a potential misleading disclosure

practice is derived from prior literature (Lewellen et al., 1996; Schrand and Walther, 2000).

Managers may decide to include or not a benchmark to compare with current year figures depending

of the firm performance or may choose a benchmark strategically to show positive rather than

negative changes (i.e. instead of comparing this year’s decrease in earnings relatively to last year’s

earnings, the manager may compare this year´s earnings with average growth in the industry to show

a positive change). In the statement “Anglo American announces record earnings of $3.7 billion, up

39%” (taken from Anglo American press release for 2005) the percentage “39%” is emphasizing the

increase in profits in relation to prior year.

(4) Tone of forward-looking disclosures. Forward-looking is based on current expectations and beliefs

and involves anticipating future events. We use a list of forward-looking keywords developed in

prior work (Hussainey et al., 2003; Matsumoto et al., 2006) and add those words with prospective

connotation found in the press release during the coding. We code forward-looking statements as

positive or negative based on the inclusion of the keywords from the list, together with numerical

information.6 For example consider the statement “The Board of directors will propose a dividend of

CHF 9.00 per share, 50% higher than the regular 2002 dividend. The group confirms its targets for

2005 at CHF 45 earnings per share” (taken from SGS press release for 2003). The first statement

5 Although it is common that information included in the headline is also included in the main body of the press release, we consider this practice emphasis by repetition because it is up to the discretion of the manager to (1) provide the press release with a headline (2) to include the same piece of information in the headline and in the main body of the press release (Garcia Osma and Guillamon-Saorin, 2011). 6 The list of forward-looking keywords is based in prior literature (Hussainey et al., 2003; Matsumoto et al., 2006) and it is available from the authors upon request.

14

includes the forward-looking keyword “will” and the positive keyword “higher” together with

quantitative information “CHF 9.00”. Therefore, this is classified as a positive forward-looking

statement. The second statement includes the forward-looking keyword “2005” and quantitative

information “CHF 45”. This statement is considered a neutral forward-looking statement because it

does not include any positive or negative explicit connotation. 7

(5) Selectivity: The selection of figures to be included in the press release is made by managers, which

can choose the most favorable item from all the information available. Selectivity implies first, (a)

choosing a figure from the face of the profit and loss account and (b) deciding which figure to

include in the press release among those available in the profit and loss account. Depending on the

figure chosen we assign a level of selectivity to that figure (high, medium or low). This method is

developed by Brennan et al. (2009).

Figure 4 in Appendix 1 shows the weighting system followed to build our score of impression

management (IMS) using the example of Ahold company. For example, a positive/negative amount is

given a +1/-1 point. Repetition and reinforcement are awarded +0.5/-0.5 points. When the amount is

located in the most emphasized section of the press release they receive an extra +1/-1 point while if the

location is in the next most emphasized it gets +0.5/-0.5 points. Positive/negative quantitative forward-

looking disclosures get +1/-1 point. Finally, figures selected from the profit and loss account get

+1/0.5/0.0 depending on whether they are the highest/medium/lowest possible figure from the range

available on the profit and loss account. The score is based on the coding of positive and negative

amounts, repetition of amounts, performance comparisons and location of figures in the press release.

Forward-looking disclosures are also coded separately and provide a measure of optimism. Selectivity is

7 In this case the forward-looking keyword is a year “2005”. This refers to future years and it is accounted for in our list of forward-looking keywords.

15

coded by comparing the figures included in the press release with the range of figures included on the

face of the profit and loss account. The final measure is calculated as the total composite score for all

positive amounts minus the total composite score for all negative amounts, divided by the total number

of words as in prior literature (Gordon et al., 2010).8 A measure scaled by total number of words allows

comparisons between press releases sections of different lengths (Rogers et al., 2011).

3.2. Information about the disclosure of non-GAAP earnings measures

We also hand-collect and code information about the non-GAAP earnings measures disclosed

from the earnings announcement press releases. Specifically, we code the type of non-GAAP measures

and their values. We use this data to calculate the value of the adjustments made by managers i.e., how

different the non-GAAP values are from the GAAP earnings numbers. Based on the type of categories

reported for non-GAAP measures in previous papers (e.g. Marques, 2006) we identify and code the

following non-GAAP figures: (i) non-GAAP earnings per share, (ii) Non-GAAP from continuing

operations, per share, (iii) other non-GAAP per share measures, (iv) non-GAAP net income, (v) non-

GAAP income from continuing operations and (vi) other non-GAAP aggregate measures. In the

8 For the purpose of the analysis of impression management we focus on the most prominent location of the press releases. The importance of location of information has been demonstrated in prior literature (Files et al., 2009; Price et al., 1997; Zillmann et al., 2004). Information included in a prominent location of a document attracts more attention and creates a lasting first impression (Anderson, 1965; Anderson and Hubert, 1963; Bernstein and Garst, 1982). Furthermore, a recent studies report evidence of the use of misleading practices in press releases headlines (Guillamon-Saorin et al., 2011) and the first five minutes of conference calls (Hobson et al., 2011). The five disclosure practices analysed in this study and used to calculate the impression management measures are coded on the first and second sections of the press release.

16

empirical analysis we focus only on categories one, two, four and five9. Furthermore, in order to be

conservative, we exclude from our study non-GAAP financial measures with ambiguous labels.

4. Research design

Our first hypothesis is based on the proposition that managers may use a combined disclosure

strategy, associating impression management practices with the voluntary disclosure of non-GAAP

earnings measures. To test this we estimate two versions of the following model:

IMSi,t = α0 + α1NGi,t + α2LEV i,t + α3LOSSi,t + α4Change_ROAi,t + α5SIZEi,t +

ΣαkDV_Years + ΣαjDV_INDs + µi,t (1)

The dependent variable is the impression management score (IMS), defined as detailed in

Appendix 1. In the first version of equation (1) NG is NG_reporting, an indicator variable coded as one

when companies report non-GAAP figures in their press release, and zero otherwise. In the second

version of equation (1) NG is NG_Adjustment, which represents the adjustments made by managers to

the GAAP earnings measures in their definition of the non-GAAP figures. NG_Adjustment is calculated

as the difference between non-GAAP earnings and GAAP earnings, scaled by market value of equity at

the end of the previous year. A positive estimated coefficient (α1) in the first version of the equation

indicates that the decision to disclose non-GAAP measures is associated with more impression

management. A positive estimated coefficient (α1) in the second version of the equation indicates that

9 We only collect non-GAAP measures that portray a firm’s results (i.e. some type of earnings figure) and we ignore measures related with other aspects of a firm’s performance (e.g. sales, cash measures and financial ratios).

17

higher levels of exclusion of expenses (leading to non-GAAP values superior to GAAP EPS) are

associated with higher usage of impression management techniques. Both positive coefficients would

suggest that the two practices are complementary disclosure mechanisms. Alternatively, a negative

estimated coefficient would indicate a substitution role.

We consider various control variables that have been found to affect disclosure in general and

impression management in particular (Guillamon-Saorin et al., 2011). LEV is calculated as the ratio of

total debt to total assets and has been found to be positively associated with impression management

(Aerts, 2005). Thus, we expect to find a positive coefficient for this variable. LOSS is included because

firms with poor performance are more likely to have poorer reporting quality (Francis et al., 2008).

LOSS is an indicator variable coded as one when the company reports losses, and zero otherwise.

Change_ROA controls for the possible association between investors’ perception of lower quality

earnings and earnings which exhibit a high degree of variability, as discussed in Lougee and Marquadt

(2004). ROA stands for return on assets and is calculated as earnings before extraordinary items scaled

by beginning of the year total assets. We expect a positive coefficient for the variable. Firm size is a

proxy for quality of disclosure, as large firms can afford the information production costs and have less

competitive advantage costs (Lang and Lundholm, 1993). SIZE is calculated as the log of the market

capitalization of the firm, in the beginning of the year. A negative coefficient is expected for this

variable, as this would indicate that impression management is misleading and thus negatively

associated with disclosure quality. Finally, we include indicator variables to account for the fact that we

pool observations across three years, as well as across different industry sectors (which we identify via

1-digit SIC codes). All variables are for firm i and year t.

Our second hypothesis assesses whether the association of the two potentially misleading

disclosure practices (non-GAAP reporting and impression management) have a combined effect on

18

market reactions in an earnings announcement press release. We make no directional prediction for this

effect on market reactions, which we test with the following model:

CAR = β0 + β1GAAP_Surprisei,t + β2NG_Adjustmenti,t + β3IMSi,t +

β4IMS*NG_Adjustmenti,t + β5SIZEi,t + β6LEV i,t + β7Change_ROAi,t +

β8BM i,t + β9LOSSi,t + Σ βkDV_Years + ΣβjDV_INDs + εi,t (2)

We measure the market reaction as the three-day cumulative abnormal market adjusted return

(CAR), centered on the date of the earnings announcement press release. We compute its values as

follows: CAR = Πk=-1,+1(1+ARk)-1, where AR is the abnormal return based on the one-factor market

model residuals estimated over the previous 365 days ending in day k-2. Given the international nature

of the sample we use a country-specific value-weighted market index. Following the methodology in

Marques (2006), we split the total earnings surprise to non-GAAP earnings measures (i.e., the difference

between the non-GAAP figures and analysts’ consensus), into two components: GAAP_Surprise and

NG_Adjustment. GAAP_Surprise is the GAAP earnings surprise calculated as the difference between

GAAP earnings per share (before extraordinary items, on a diluted basis) and the analysts’ consensus

forecast of earnings, scaled by share price at the end of the previous year.10 The second component

represents the adjustments made by managers to the GAAP earnings measures in their calculation of the

non-GAAP figures. Thus, NG_Adjustment is calculated as the difference between non-GAAP earnings

and GAAP earnings, scaled by share price at the end of the previous year. Studies based on US data find

10 Analysts’ consensus is defined as I/B/E/S median forecast of earnings per share.

19

that non-GAAP earnings are more valuable to financial markets than GAAP earnings. If this evidence

holds for European companies the estimated coefficient (β2) should be positive.

Our focus is the coefficient of the interaction of NG_Adjustment and IMS (β4). We do not make

a directional prediction, as we establish two possible scenarios. In the first, investors continue to believe

that non-GAAP earnings contain more information that GAAP earnings and the presence of impression

management has a positive effect, increasing the market reaction to the adjustments made to GAAP

figures. This leads to a positive estimated coefficient for the interaction variable. In the second scenario,

the presence of impression management is interpreted as an attempt to mislead market participants and

leads to a negative reaction, punishing managers’ behavior.

We also include several control variables expected to affect market returns. SIZE controls for

size effects as, for a given level of “unexpected” earnings, the cumulative abnormal returns of small

firms exceed those of large firms (Freeman, 1987). Thus, we expect to find a negative coefficient for

SIZE. Based on the results of Dhaliwal et al. (1991), who find that the earnings response coefficients are

larger for all-equity and low-leverage firms we include LEV and expect to estimate a negative

coefficient for it. Change_ROA controls for firms’ financial performance. To control for risk we use

BM, the ratio of book value of equity to market value of equity (Fama and French, 1993). We include

LOSS following Hayn´s (1995) results documenting the impact of a loss report on share valuation

Finally, we include indicator variables for years and industry sectors.

5. Results

5.1. Descriptive statistics and univariate tests

Table 2 presents the descriptive statistics by country for the two voluntary disclosure practices

20

analyzed in this study, non-GAAP earnings disclosure and the use of impression management

techniques. The percentage of firms disclosing non-GAAP earnings by country ranges from 0%, in

Austria, Hungary and Portugal, to 83%, in Greece. Considering the entire sample, we find that almost

50% of the earnings announcement press releases include non-GAAP earnings measures. There is also a

great deal of variance in the impression management scores (IMS) among countries. The country with

the highest value for IMS is Turkey (0.145) and the one with the lowest is Luxembourg (0.024). The

mean score is positive which indicates an overall positive connotation of the information included in

press releases. A score of 0.145 means that in every 100 words analyzed there are 14.5 points more of

positive content than negative content. On the other hand, a score of 0.024 indicates that the positive and

negative contents are almost balanced. The table also reports the number of press releases analyzed per

country.

Table 3 presents the results of univariate tests on the means of impression management score.

The first test aims to understand whether non-GAAP disclosures and the use of impression management

techniques are complementary or substitute corporate reporting mechanisms. The mean impression

management score is 0.079 for firms that do not report non-GAAP earnings measures whilst it is 0.088

for firms reporting non-GAAP earnings measures in press releases. The difference in means is

statistically significant (p-value=0.015). This descriptive evidence suggests that the two mechanisms are

complementary, not substitutes.

The second test reported in Table 3 assesses whether the level of impression management

changes when non-GAAP earnings are lower or higher than GAAP earnings figures. As explained

earlier, managers can disclose non-GAAP figures either to inform or to mislead investors. Curtis et al.

(2011) suggest that firms making adjustments to GAAP numbers in such a way that the resulting figure

is lower than GAAP earnings per share indicate management informative intentions. Thus, this test

21

allows us to assess if there is an association between the motive of the non-GAAP disclosure and the

level of impression management used by manager. The test shows that the two means are very similar

(0.085 and 0.090) and the difference is not statistically significant (p-value=0.632) suggesting that the

use of impression management techniques does not depend on the informativeness of non-GAAP

disclosures.

Finally, we also assess whether impression management is firm specific (i.e. we look for a ‘firm

style’ in the preparation of earnings announcements press releases). To this end, we assign each firm in

every year to five, ten and 20 quantiles of impression management. Untabulated results show that only

14% of the firms belong to the same or adjacent IMS quantile in the period analyzed. Thus, we find no

evidence of the existence of a ‘firm style’.

Panel A of Table 4 presents descriptive statistics on the continuous variables included in our

models. The mean NG_adjustment is 0.023, indicating that, on average, the values of the non-GAAP

earnings disclosed are higher than the GAAP earnings figures. This is consistent with previous findings,

both in the US and in Europe, and it is the mechanical result of managers mostly excluding expenses

(Hitz, 2010). The mean GAAP_surprise is 0.005, revealing that GAAP earnings are on average, higher

than the analysts’ consensus forecasts. The mean value of IMS is 0.086 indicating that, on average,

managers present their firm achievements in a positive light. Sample firms have a median leverage ratio

of 25% and a median Change_ROA of 1.2%.

Panel B of Table 4 reports the Pearson correlations. Overall, correlations among the variables are

not statistically significant. In fact, only two correlations (between SIZE and CAR, and SIZE and

GAAP_Suprise) are statistically significant, at a 5% level of confidence. These results indicate that our

variables capture different aspects of firm characteristics and there should not be multicollinearity

22

problems.

Panel C of Table 4 presents the means of variables by IMS groups. The three IMS groups result

from splitting the sample into three terciles and represent high, medium and low level of the IMS. The

mean of non-GAAP adjustments increases as the level of IMS gets higher. In particular, the mean value

of NG_Adjustmentis increases from 0.015 for the low IMS group to 0.034 for the high IMS group (the

increment is statistically significant: p-value = 0.045). This result indicates that managers use more

impression management techniques when they make more adjustments to GAAP earnings to calculate

non-GAAP figures. This evidence reinforces our previous findings that the two mechanisms are

complementary.

5.2. Regression results

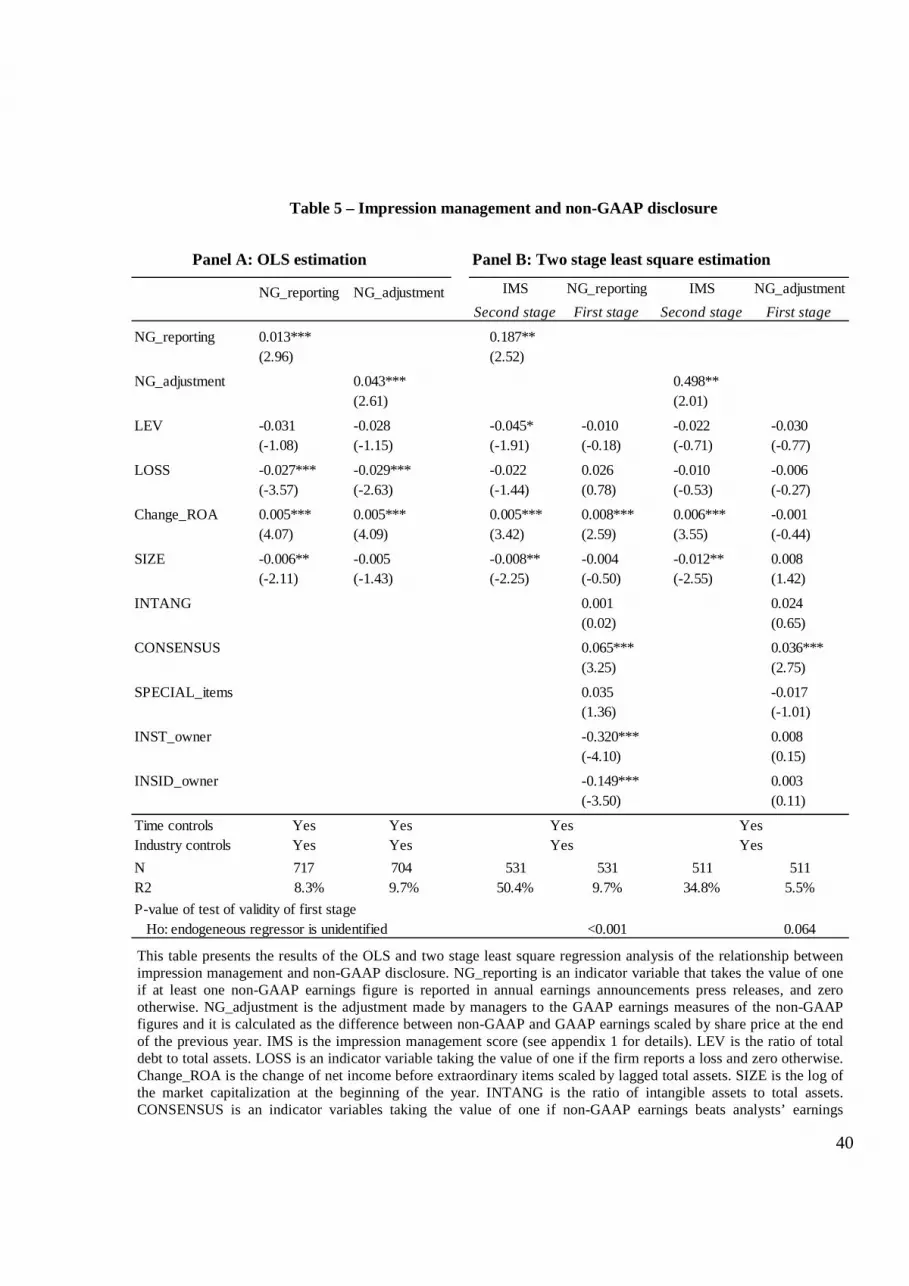

Table 5 presents the results of the two alternative estimations of equation (1), which is used to

test our hypothesis one of whether firms that report non-GAAP figures (and make more adjustments) are

also more likely to engage in impression management. In Panel A we apply an OLS estimation model.

In Panel B we use a two-stage model which assumes the existence of self-selection in non-GAAP

reporting decisions. Prior literature has identified a number of firm conditions affecting managers’

decision to disclose non-GAAP measures (e.g. Heflin and Hsu, 2008). We use these determinants in the

first-stage equation.

Both sets of estimations presented in Table 5 reveal that impression management is positively

and significantly associated with the non-GAAP reporting decision (t-statistic is 2.96 in the OLS

estimation and 2.52 in the two-stage estimation). Moreover, the coefficient estimated for

NG_Adjustment is also positive and statistically significant in both estimations (t-statistics is 2.61 in

23

the OLS estimation and 2.01 in the two-stage estimation). These findings confirm our first hypothesis

and indicate that (i) firms tend to combine the use of impression management techniques with the

disclosure of non-GAAP earnings metrics, and (ii) the level of impression management applied

increases with the level of adjustments made by managers to compute non-GAAP earnings figures.

Given the way we calculate NG_Adjustment, higher values of this association indicate that as firms

exclude more expenses they also increase the level of impression management, suggesting a combined

approach to manipulate investors’ perceptions. Only two control variables are consistently significant

(Change_ROA and SIZE) and their signs are as expected.

An alternative explanation for the association between the level of non-GAAP adjustments and

IMS would be that as firms make more adjustments when calculating their non-GAAP earnings figures

they include more positive references and explanations of them. This would create a mechanical

relationship between non-GAAP and IMS. As a robustness check, we create an alternative IMS from

which we remove disclosure tone. By eliminating “disclosure tone” from the score we remove most of

the increasing effect produced by the additional explanations related to the inclusion of larger

adjustments to non-GAAP figures. Our results, using this alternative IMS are consistent with findings in

Table 5.

Our findings also reveal that Change_ROA, CONSENSUS, INST_owner and INSIDER_owner

are statistically significant determinants of the decision to disclose non-GAAP earnings figures in the

press releases we analyze. The first two variables have a positive impact on this decision, which is

consistent with the results found for US firms by Marques (2006). On the other hand, INST_owner and

INSIDER_owner have a negative impact of the decision to disclose non-GAAP earnings, as these are

monitoring entities. This is consistent with the results found for US firms by Jennings and Marques

(2009). In order to assess the validity of our first stage we test the null hypothesis that the endogenous

24

regressor is unidentified. Results (in the last line of Table 4) indicate that our model does include

variables which are determinants of NG_reporting (p-value<0.001) and NG_adjustments (p-

value=0.038).

Before testing our second hypothesis we analyze, as a stepping stone, whether the European

markets believe that the alternative earnings measures voluntary disclosed by managers are a more

appropriate measure of earnings than GAAP figures. This has been established in the US markets, but

has never been tested for European markets. To do this, we run two regressions, whose results are

reported in columns (1) and (2) of Table 6. As expected, the first regression shows a positive and

statistically significant reaction to GAAP_surprise. The second regression reveals a positive and

statistically significant market reaction to the manager adjustments to GAAP earnings. In line with the

US findings, adjustments seem to have information content which is valued by investors. A test of

difference of coefficients reveals that the estimated coefficient of GAAP_surprise is significantly higher

than the coefficient of NG_adjustment (p-value=0.004). This evidence suggests that either (a) not all of

the adjustments made by managers are considered appropriate by investors (i.e., investors believe some

of the items managers made adjustments for to be recurring), or (b) there are situations where non-

GAAP figures are not seen as informative.

Next, we test our second hypothesis, which states (in the null form) that market participants’

reaction to non-GAAP earnings is not affected when impression management is used in the same

earnings announcement. We start by investigating the market response to impression management in

isolation and find no significant effect - column (3) of Table 6.11 The results of estimating equation (2)

11 We acknowledge that Davis et al. (2011) find a significant market reaction to positive tone in press releases. However, our results cannot be compared directly to those in Davis et al. (2011) for a number of reasons: (i) we consider several impression management techniques while they only measure disclosure tone, (ii) we use the absolute value of our impression

25

are present in column (4) of Table 6. We are especially interested in the coefficient of

IMS*NG_adjustment, as this reflects the market reaction to the combined presence of non-GAAP

disclosures and impression management. The coefficient is negative and statistically significant (t-

statistic = -2.16), which is consistent with the idea that managers combine the two disclosure practices

with the intention of misleading market participants.12 As a response, markets react negatively. It is

important to note that the estimated coefficient of NG_adjustment is still positive and statistically

significant (t-statistic = 2.43). Thus, when no impression management is present (i.e., when the positive

and negative aspects presented by managers in the press releases balance out) the overall market

reaction to the adjustments is still positive. To assess the economic significance of the results we

analyze the sensitivity of the firm’s market returns to the NG adjustments for different levels of

impression management. This sensitivity is given by ∂CAR / ∂NG_adjustment = β2 + β4IMS. For the

bottom 25% IMS (which is 0.032 as shown in Table 4) the sensitivity of the firm’s abnormal returns to

non-GAAP adjustments is 0.077 (0.095 – 0.553 x 0.032). Consequently, a one standard deviation

increase in the non-GAAP adjustments made by managers (which is 0.105 as shown in Table 4) results

in an increase in market returns of 0.008 (0.105 x 0.077). For the top 75% IMS (0.127) the sensitivity of

the firm’s abnormal returns to non-GAAP adjustments is 0.025 (0.095 – 0.553 x 0.127). An increase of

one standard deviation in non-GAAP adjustments leads to positive market reaction of only 0.003 (0.105

x 0.025) which is approximately 67% less than the reaction for the bottom 25% IMS. In summary, the

investor reaction to non-GAAP information included in earnings announcements varies with the level of

management score, while they use an unexpected value of positivism and (iii) our sample consists of European firms while they analyze press releases of US firms. 12 The models include time fixed effects, but to ensure that the negative market reaction is not concentrated on a specific year we instead include three-way interaction variables between IMS, NG_adjustment, and year indicators. The year interactions are not statistically significant in most cases and the empirical results do not change.

26

impression management used by managers in the same announcement. The market reaction to non-

GAAP adjustments is inversely affected by the level of impression management.

Finally, we test whether there is a market effect in the GAAP_suprise when impression

management is present. Results in column (5) of Table 6, indicate that the coefficient of the interaction

between IMS and GAAP_surprise, although positive, is not statistically significant. Thus, there is an

absence of an incremental market reaction to the GAAP earnings surprise when presented together with

impression management practices. For completeness, we estimate a comprehensive model including

both the GAAP and non-GAAP surprise and the two interactions effects. Results reported in the last

column of Table 6 are consistent with the findings discussed above.

6. Sensitivity analyses

Given the potential subjectivity of manually-constructed scores, we test the sensitivity of our

findings to alternative impression management measurements. We first create a more comprehensive

score adding qualitative aspects of the press releases to the score. This alternative measure, which

combines quantitative and qualitative information, is calculated in a similar way to that described in the

Appendix (Figure 3 and 4). The disclosure practices analyzed for qualitative information are: (1)

disclosure tone, (2) emphasis by a) location, b) repetition, c) reinforcement and (3) forward-looking

disclosure tone. These practices are similar to those included in our main score but focusing on

quantitative information. Untabulated results, which use this alternative score, are consistent with the

ones discussed above. In fact, the magnitude, sign and level of significance remain similar.

Second, we substitute the score by a dichotomous variable coded as one when the level

impression management is high. We perform two alternative divisions, as we split the sample into three

27

or five impression management groups before eliminating the middle group to better separate the high

and low firms. This procedure results in fewer observation to run the empirical tests but the empirical

results remain unchanged.

Third, we construct an abnormal measure of impression management in the spirit Davis et al.

(2011). We use the annual change in IMS to build a firm-adjusted score, and the change between the

firm’s IMS and the industry median IMS to obtain an industry-adjusted score. For the firm-adjusted

score the results are statistically weaker but still in line with our conclusion. In the case of industry-

adjusted score the results are robust.

7. Summary and conclusions

In this study we examine the links between managers’ use of non-GAAP disclosures and

impression management techniques in earnings announcements press releases. We first investigate

whether non-GAAP disclosure and impression management are complementary mechanisms in

voluntarily corporate communications, or instead if they substitute each other. We next assess the capital

market reaction to the disclosure of non-GAAP information that is supplemented with impression

management techniques.

Our sample consists of the largest European firms. Given that there is no regulation on non-

GAAP earnings disclosures in Europe, the potential for misleading investors in higher in Europe than in

the US (where the Securities and Exchange Commission issued Regulation G in 2003). Thus, it is

important to understand market reactions to these disclosures in a market where several institutional

differences still prevail.

Our results indicate that (1) managers combine the two disclosure mechanisms when reporting

28

earnings figures in a way consistent with opportunistic disclosure, and (2) market participants

successfully identify and associate the management disclosure strategy with self-serving behavior and

penalize these practices. Additionally, we identify a positive market reaction to the adjustments made by

managers when calculating their non-GAAP earnings measures, in Europe. This indicates that European

investors see the usefulness of these measures, something that had been shown in the US.

The findings of this study should be of interest to market participants in their assessment of the

informational value of managers’ disclosures. Our evidence is also important for regulatory bodies. As

investors seem to identify potentially misleading disclosure practices investigated in this study when

facing investment decisions, our research raises the question whether regulators need to discipline the

use of impression management and non-GAAP information in corporate communications.

29

Appendix 1: Measuring Impression Management

We illustrate these practices using a particular case of a company included in our sample. We perform manual content analysis which allows a detailed scrutiny of the press release in search of potentially misleading disclosure practices. Our analysis involves the study of three consecutive years (2003 to 2005). To illustrate the practices analyzed in this study we have selected one of the companies: Ahold company. The illustration focuses on the press release for 2003. We code manually the five potentially misleading disclosure practices investigated in the current study. Each press release is assigned two levels of emphasis (Most- and Next-most emphasized sections) and the quantitative information is coded for each section separately. For the purposes of this study we focus on the first two sections of the press release (most and next most-emphasized sections).

Ahold Reports Improved Results for 2003

Most emphasized

section 11629 words

19 April 2004

08:38

Business Wire

English

(c) 2004 Business Wire. All Rights Reserved.

ZAANDAM, The Netherlands - (BUSINESS WIRE) - April 19, 2004 -

Highlights of 2003

-- Net loss Euro 1 millionNUM+ IS

(2002: net loss of Euro 1.2 billionBench+

)

-- Operating income Euro 718 millionNUM+ IS

(2002: operating income Euro 239 millionBench+

)

-- Net sales Euro 56.1 billionNUM-

, a decrease of 10.6%Bench-

compared to 2002, but an increase of

2.7%Bench+

excluding foreign currency translation impact

-- Net loss under US GAAP Euro 747 millionNUM+

(2002: net loss Euro 4.3 billionBench+

)

-- Improved balance sheet: equity increased to Euro 4.9 billionNUM+

(2002: Euro 2.6 billionBench+

).

Net debt reduced to Euro 7.5 billionNUM+

(2002: Euro 12.3 billionBench+

)

-- Net cash before financing activities generated Euro 1.5 billionNUM+

(2002: net cash outflow

Euro 107 millionBench+

)

Next most emphasised

section

Ahold today published its 2003 results. "We are pleased to announce that we have clearly

improved results in 2003, an extremely challenging year," said Hannu Ryopponen, Chief

Financial Officer, commenting on the results. "A very turbulent period for the company was

marked by the events announced in February 2003, as well as a tough trading environment in

our key markets." Anders Moberg, CEO commented: "Months of ongoing effort resulted in a

number of achievements, specifically defining a new strategy and creating the financial platform

to move forward. At the end of last year we indicated that 2003 in many respects had been a

lost year, but today's announcement also shows that Ahold is on track with its 'Road to

Recovery' program."

...........

Least emphasised section

Key: NUM+/-=positive/negative amount, Bench+/-= positive/negative performance

comparisons, IS= figure included in the Income Statement.

30

Among the figures identified in the press release of Ahold two of them are selected from the profit and loss account. We calculate the selectivity level for these two amounts (Operating income and net income) marked with an arrow in the income statement (see Figure 1). First, figures are ranked from higher (1) to lower (6) in absolute value. Then, following the schema in Figure 2, the two figures are categorised as high selectivity (operating profit) and medium selectivity (net income).

Figure 1: Income statement 2003Ahold company

UAH 2010

(1)

(2)

(6)

(5)

(4)

(3)

Figure 2: Measuring selectivity: Assigning categories

No. amounts Ranking

1

2 }

High selectivity

3

4 }

Medium selectivity

5

6 }

Low selectivity

The impression management score is calculated following the method to measure and the method to calculate the score included in Figures 3 and 4.

31

Disclosure tone: This is operationalized by coding positive and negative amounts. Amounts are categorized into positive or negative by reference to prior year results (as reported in the actual press release). Emphasis by location: Emphasis by Repetition: Repetition occurs when the same amount is mentioned more than once in the press release. (repeated amounts are not included/counted in the positive amounts). Performance comparison: When the current year amount is accompanied by a benchmark/prior year amount showing increase/decrease in the current year amount. FL disclosure tone: based on current expectations and beliefs. It involves anticipating a future event. Selectivity: Refers to figures selected from the profit and loss account to be included in the press release. The level of selectivity is coded as high, medium or low depending on whether the figure included is the highest, medium or lowest possible (See figure 2).

Figure 3. Method to measure impression management (management positiveness and optimism) Technique Object of technique Measure (1) Disclosure tone Quantitative amounts Number of quantitative positive and negative amounts (2) Emphasis (a)Location/positioning/presentation of

amounts Most-, Next-most emphasized section

(b) Repetition of Quantitative amounts Number of positive and negative repetitions of amounts

(3) Performance comparisons

Quantitative amounts Benchmark, Prior year amount, Both

(4) FL disclosures tone Quantitative amounts Number of positive and negative FL amounts (5) Selectivity Quantitative amounts High, Medium and Low level of selectivity

Figure 4: Calculating impression management score (IMS)

Measure

Positive amount

Negative amounts

� Number of quantitative disclosures 6 1

� Impression management score (IMS) Positive

score Negative

score

(1) Disclosure of quantitative performance monetary and non-monetary amounts 6x1.0 1x1.0 (2)(a) Emphasis – Location: - Most 0.0 0.0 - Next-most 6 x 0.5 1x0.5 (2)(b) Emphasis – Repetition 0.0 0.0 (3) Performance comparisons 7x0.5 1x0.5 (4) FL disclosure tone 0.00 0.00 (5) Selectivity - highest/medium/lowest category of amounts from which selection can be made 1x1.0 1x0.5 Total impression management score 13.5 2.5 �IMS calculation 13.5Positive score –2.5 Negative score = 12Net positive score/141 Total number of words in sections coded = + 0.085

Although in this illustration we focus on the press release of Ahold for 2003 our analysis involves the study of three consecutive years (2003 to 2005). Ahold has a net loss of 1 million euro in 2003 (2002: net loss of 1.2 billion euro). In 2004 the company increases losses to 436 million euro and in 2005 goes down to 20 million euro losses. Despite this overall bad performance, the press releases for 2003, 2004 and 2005 for Ahold has a positive impression management score (IMS) as measured in this study. This reflects an overall positive tone of the quantitative information included in its press release. The IMS for Ahold is 0.08 for 2003, 0.00 for 2004 and 0.05 for 2005. This means that the IMS for Ahold press release is high in 2003 (IMS median=0.07), neutral in 2004 and medium in 2005.

32

References

Abrahamson, E., Park, C. 1994. 'Concealment of negative organizational outcomes: an Agency Theory perspective'. Academy of Management Journal, 37(5): 1302-1334.

Adelberg, A. H. 1979. 'Narrative disclosures contained in financial reports: means of communication or manipulation?'. Accounting and Business Research, 9(35): 179-189.

Aerts, W. 2005. 'Picking up the pieces: impression management in the retrospective attributional framing of accounting outcomes'. Accounting, Organizations and Society, 30(6): 493-517.

Aerts, W., Cormier, D. 2009. 'Media legitimacy and corporate environmental communication'. Accounting, Organizations and Society, 34(1): 1-27.

Aerts, W., Cheng, P. 2010. 'Causal disclosures on earnings and earnings management in an IPO setting'. Journal of Accounting and Public Policy. Forthcoming.

Aerts, W., Cheng, P. 2011. 'Causal disclosures on earnings and earnings management in an IPO setting'. Journal of Accounting and Public Policy, 30: 431-459.

Anderson, N. H., Hubert, S. 1963. 'Effects of concomitant verbal recall on order effects in personality impression formation'. Journal of Verbal Learning and Verbal Behavior, 2: 379-391.

Anderson, N. H. 1965. 'Primacy effects in personality impression formation using a generalized order effect paradigm'. Journal of Personality and Social Psychology, 2(1): 1-9.

Andersson, P., Hellman, N. 2007. 'Does Pro Forma reporting bias analyst forecasts?'. European Accounting Review, 16(2): 277-298.

Baginski, S. P., Hassell, J. M., Hillison, W. A. 2000. 'Voluntary causal disclosures: Tendencies and capital market reaction'. Review of Quantitative Accounting and Finance, 15(4): 371-389.

Barton, J., Mercer, M. 2005. 'To blame or not to blame: Analysts reactions to explanations of poor management performance'. Journal of Accounting and Economics, 39(3): 509-533.

Beattie, V. A., Jones, M. J. 1997. 'A comparative study of the use of financial graphs in the corporate annual reports of major U.S. and U.K. companies'. Journal of International Financial Management and Accounting, 8(1): 33-68.

Beattie, V. A., Jones, M. J. 2001. 'A six-country comparison of the use of graphs in annual reports'. The International Journal of Accounting, 36: 159-222.

Bernstein, M., Garst, R. E. 1982. Headlines are Deadlines: Columbia University Press, New York.

Bhattacharya, N., Black, E. L., Christensen, T. E., Larson, C. R. 2003. 'Assessing the relative informativeness and permanence of pro forma earnings and GAAP operating earnings'. Journal of Accounting and Economics, 36(1-3): 285-319.

Bhattacharya, N., Black, E., Christensen, T., Mergenthaler, R. 2004. ' Empirical evidence on recent trends in pro forma reporting. '. Accounting Horizons, 18: 27-43.

Bhattacharya, N., Black, E. L., Christensen, T., Mergenthaler, R. D. 2007. 'Who trades on pro forma earnings information?'. The Accounting Review, 82(3): 581-619.

Bowen, R. M., Davis, A. K., Matsumoto, D. A. 2005. 'Emphasis on pro forma versus GAAP earnings in quarterly press releases: determinants, SEC intervention and market reactions'. The Accounting Review, 80(4): 1011-1038.

Bradshaw, M. T., Sloan, R. G. 2002. 'GAAP versus the street: an empirical assessment of two alternative definitions of earnings'. Journal of Accounting Research, 40(1): 41-66.

Bray, C. 2001. 'SEC looking at pro forma earnings with "purpose in mind"'. Dow Jones Newswires (June18).

Brennan, N. M., Guillamon-Saorin, E., Pierce, A. 2009. 'Impression management: Developing and illustrating a scheme of analysis for narrative disclosures - A methodological note'. Accounting, Auditing & Accountability Journal, 22(5): 789-832.

Clatworthy, M., Jones, M. J. 2001. 'The effect of thematic structure on the variability of annual report readability'. Accounting, Auditing & Accountability Journal, 14(3): 311-326.

Clatworthy, M., Jones, M. J. 2003. 'Financial reporting of good news and bad news: evidence from accounting narratives'.

33

Accounting and Business Research, 33(3): 171-185.

Conway, M. 2007. 'The subjective precision of computers: a methodological comparison with human coding in content analysis'. Journalism and Mass Communication Quarterly, 83(1): 186-200.

Core, J. E. 2001. 'A review of the empirical disclosure literature: discussion'. Journal of Accounting and Economics, 31: 441-456.

Courtis, J. K. 2004. 'Corporate report obfuscation: Artefact or phenomenon?'. British Accounting Review, 36(3): 291-312.

Curtis, A., McVay, S., Whipple, B. 2011. The use of non-GAAP earnings information in the presence of transitory gains. Working paper.

Davis, A. K., Piger, J. M., Sedor, L. M. 2011. 'Beyond the numbers: Measuring the information content of earnings press release language'. Contemporary Accounting Research. Forthcoming.

Demers, E., Vega, C. 2008. Soft Information in Earnings Announcements: News or Noise?. Working paper.

Derby, M. S. 2001. 'Investors getting more data, but is it the right data?'. Dow Jones Newswires (September 3).

Dhaliwal, D., Lee, K., Fargher, N. 1991. 'The association between unexpected earnings and abnormal security returns in the presence of financial leverage'. Contemporary Accounting Research, 8: 20-41.

Fama, E. F., French, K. R. 1993. 'Common riskfFactors in the returns on stocks and bonds'. Journal of Financial Economics 33(1): 3-56.

Files, R., Swanson, E. P., Tse, S. 2009. 'Stealth disclosure of accounting restatements'. The Accounting Review, 84(5): 1495-1520.

Francis, J., Nanda, D., Olsson, P. 2008. 'Voluntary disclosure, earnings quality and cost of capital'. Journal of Accounting Research, 46(1): 53-99.

Freeman, R. N. 1987. 'The association between accounting earnings and security returns for large and small firms'. Journal of Accounting and Economics, 9: 195-228.

Garcia Osma, B., Guillamon-Saorin, E. 2011. 'Corporate governance and impression management in annual press releases'. Accounting Organizations and Society, 36(4/5): 187-208.

Godfrey, J., Mather, P., Ramsay, A. 2003. 'Earnings and impression management in financial reports: the case of CEO changes.'. Abacus, 39(1): 95-123.

Gordon, E. A., Henry, E., Peytcheva, M., Sun, L. 2010. Discretionary disclosure and market reaction to restatements: Available at http://ssrn.com/abstract=930540.

Guillamon-Saorin, E., Garcia Osma, B. 2010. Self-serving financial reporting communication: A study of the association between earnings management and impression management. Working paper: Universidad Carlos III de Madrid & Universidad Autonoma.

Guillamon-Saorin, E., Garcia Osma, B., Aerts, W. 2011. Self-serving financial reporting communication: A study of the association between earnings management and impression management. Working paper: Universidad Carlos III de Madrid & Universidad Autonoma.

Guillamon-Saorin, E., Garcia Osma, B., Jones, M. J. 2011. 'Opportunistic disclosure in press release headlines'. Accounting and Business Research forthcoming.

Hayn, C. 1995. 'The information content of losses'. Journal of Accounting and Economics, 20(2): 125-153.

Heflin, F., Hsu, C. 2008. 'The impact of the SEC’s regulation of non-GAAP disclosures'. Journal of Accounting and Economics, 46(2-3): 349-365.

Henry, E. 2008. 'Are investors influenced by how earnings press releases are written?'. Journal of Business Communication, 45(4): 363-407.

Henry, E., Leone, A. J. 2009. Measuring qualitative information in capital markets research, Working paper: University of Miami.

Hitz, J.-M. 2010. 'Press Release Disclosure of ‘Pro Forma’ Earnings Metrics by Large German Corporations – Empirical

34

Evidence and Regulatory Recommendations'. Accounting in Europe, 7(1).

Hobson, J. L., Mayew, W. J., Venkatachalam, M. 2011. 'Analyzing speech to detect financial misreporting'. Journal of Accounting Research forthcoming.

Hooghiemstra, R. 2000. 'Corporate communication and impression management'. Journal of Business Ethics, 27(1/2): 55-68.

Hussainey, K., Schleicher, T., Walker, M. 2003. 'Undertaking large-scale disclosure studies when AIMR-FAF ratings are not available: the case of prices leading earnings'. Accounting and Business Research, 33(4): 275-294.

Jennings, R., Marques, A. 2009. 'The Joint Effects of Corporate Governance and Regulation on the Disclosure of Manager-Adjusted Non-GAAP Earnings in the US'. Journal of Business Finance and Accounting, 38(3-4): 364-394.

Krische, S. D. 2005. 'Investors' evaluations of strategic prior-period benchmark disclosures in earnings announcements'. The Accounting Review, 80(1): 243-268.

Lang, M., Lundholm, R. 1993. 'Cross-sectional determinants of analyst ratings of corporate disclosures'. Journal of Accounting Research, 31(2): 246-271.

Lang, M., Lundholm, R. 2000. 'Voluntary disclosure and equity offerings: reducing information asymmetry or hyping the stock?'. Contemporary Accounting Research, 17(4): 623-662.

Larcker, D., Zakolyukina, A. 2010. Detecting deceptive discussions in conference calls. Working paper. Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1572705.

Lewellen, W. G., Park, T., Ro, B. T. 1996. 'Self-serving behavior in managers' discretionary information disclosure decisions'. Journal of Accounting and Economics, 21(2): 227-251.

Li, F. 2008. 'Annual report readability, current earnings, and earnings persistence'. Journal of Accounting and Economics, 45(2-3): 221-247.

Linderman, A. 2001. Computer content analysis and manual coding techniques: a comparative analysis, Theory, Method and Practice in Computer Content Analysis: 97-109: West, M.D. (editors), Ablex, Westport CT.

Lougee, B. A., Marquardt, C. A. 2004. 'Earnings informativeness and strategic disclosure: an empirical examination of 'pro forma' net income'. The Accounting Review, 79(3): 769-795.

Loughran, T., McDonald, B. 2011. 'When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks'. Journal of Finance, 66(1): 35-65.

Marques, A. 2006. 'SEC interventions and the frequency and usefulness of non-GAAP financial measures'. Review of Accounting Studies, 11: 549-574.

Matsumoto, D., Pronk, M., Roelofsen, E. 2006. Do analysts mitigate optimism by management? Working paper. University of Washington, Tilburg University and RSM/Erasmus University.

Price, V., Tewksbury, D., Powers, E. 1997. 'Switching trains of thought: The impact of news frames on readers' cognitive responses'. Communication Research, 24(5): 481-506.

Rogers, J. L., Van Buskirk, A., Zechman, S. L. C. 2011. 'Disclosure Tone and Shareholder Litigation'. The Accounting Review, 86(6).

Schleicher, T., Walker, M. 2010. 'Bias in the tone of forward-looking narratives'. Accounting and Business Research, 40(4): 1-20.

Schlenker, B. R. 1980. Impression Management: The Self-concept, Social Identity, and Interpersonal Relations. Monterrey, CA: Brooks-Cole, 1980.

Schlenker, B. R. 2003. Self-presentation. In M. Leary& J. Tangeney (Eds.), Handbook of self and identity: 492-518. New York: Guilford Press.

Schrand, C., Walther, B. R. 2000. 'Strategic benchmarks in earnings announcements: The selective disclosure of prior-period earnings components'. The Accounting Review, 75(2): 151-177.

Subramanian, R., Insley, R. G., Blackwell, R. D. 1993. 'Performance and readability: a comparison of annual reports of profitable and unprofitable corporations'. The Journal of Business Communication, 30(1): 49-61.

35

Verrecchia, R. E. 2001. 'Essays on disclosure'. Journal of Accounting and Economics, 32: 97-180.

Yuthas, K., Rogers, R., Dillard, J. F. 2002. 'Communicative action and corporate annual reports'. Journal of Business Ethics, 41(1/2): 141-157.

Zillmann, D., Chen, L., Knobloch, S., Callison, C. 2004. 'Effects of lead framing on selective exposure to internet news reports'. Communications Research, 31(1): 58-81.

36

Table 1 – Sample selection

Firm years

Financial Times 500 largest European firms, 2003-2005 1500

Financial and utility firms (552)

948

Unavailable press releases (144)

804

Missing financial and forecast data (87) Final sample

717 representing 267 firms

This table shows the sample selection details between 2003 and 2005. Numbers in parentheses are observations that are dropped.

37

Table 2 – Descriptive evidence on disclosure practices

Country N % firms disclosing non-GAAP earnings

IM mean score